PwC’s Insurance Insights - PwC India · PwC’s Insurance Insights Analysis of regulatory changes...

17

PwC’s Insurance Insights Analysis of regulatory changes and impact assessment, July 2018

Transcript of PwC’s Insurance Insights - PwC India · PwC’s Insurance Insights Analysis of regulatory changes...

PwC’s Insurance InsightsAnalysis of regulatory changes and impact assessment, July 2018

2 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

This edition highlights the importance and emergence of group insurance policies over the last few years. The group insurance market has an approximate value of around 65 billion US$. Although there has been consistent growth of around 3.5-4% over the last few years, the changing dynamics of employer-employee relationship and the need to reform group benefit needs has led to this market becoming an attractive area of investment.

Drivers in the change in employee-employer dynamicOne of the key issues affecting the growth of group insurance has been the change in the relationship between employers and their employees. With the workforce having a more modern

outlook, employers are now having to offer relevant solutions to meet their expectations. Another driver affecting the relationship between two parties is that employers are now looking for ways to enhance experiences of employees outside of the workplace. This includes activities such as flexible working hours and rewards based on the well-being of the employee. Recently, employers have had to look for ways to provide self-directed tools and advice that allows employees to manage their overall well-being and enhance their productivity at work. These trends have continued to shape the group insurance market and made group insurers reposition their business and operating models. Understanding these trends has helped group insurers to deliver high

quality products with more focus on improved customer experience.

Global regulations Regulation in insurance has become a very important issue over the last few years. Insurance plays many different roles in different countries. However, in order to ensure that people that are being insured are being fairly treated, it is important that regulations are in place. In case of group policies in the UK, the Financial Conduct Authority ( FCA) requires that a firm should provide information to its customers to pass on to other policyholders and also that the customer should be told that to provide information to each of the policyholders.

Importance and emergence of group insurance globally1

2 https://www.pwc.com/us/en/insurance/assets/pwc-insurance-top-issues-2018-compilation-report.pdf

3 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Group insurance in IndiaIn India, group insurance guidelines were introduced by the IRDA in 2005. These guidelines stated the applicability, the administration and the marketing of group insurance policies. In 2011, IRDA had issued a clarification regarding implementing a service charge, and that this should be disclosed as an additional cost and not as part of the premium from members of the policy. In the life insurance market, we see that there are more lives that are being covered under group schemes, which matches the trend that is seen globally. However, what is interesting to note is that over the last one year particularly, there is more premium that is generated from private life insurers as compared to public sector life insurance companies. In the case of LIC, there has been a fall in premium generation from group schemes of more than 48%. Especially in group insurance, private life insurers enjoy more than 90% of the market share.

Number of lives covered under group schemes

Type of Insurer Up to 30 June 2017 Up to 30 June 2018 Growth in %

Private Life 28395353 36199531 27.48

LIC 6368953 3308615 -45.08

Grand Total 34764306 39508146 -

Our point of viewGroup insurance is increasingly becoming important as a business platform to meet the needs of employees including employee’s health, wealth management and long-term career needs. It is also helping employers offer different solutions to their employees to maintain employee satisfaction levels and therefore, continue to increase worker productivity. The existing players in this market will not be able to stay stagnant due to different ideas and business models that are arising and are changing the dynamics of the group insurance market. The focus for new players in the market should be on creating customer-centric operating models that use new business and technologies to enhance the business to customer relationship.

4 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

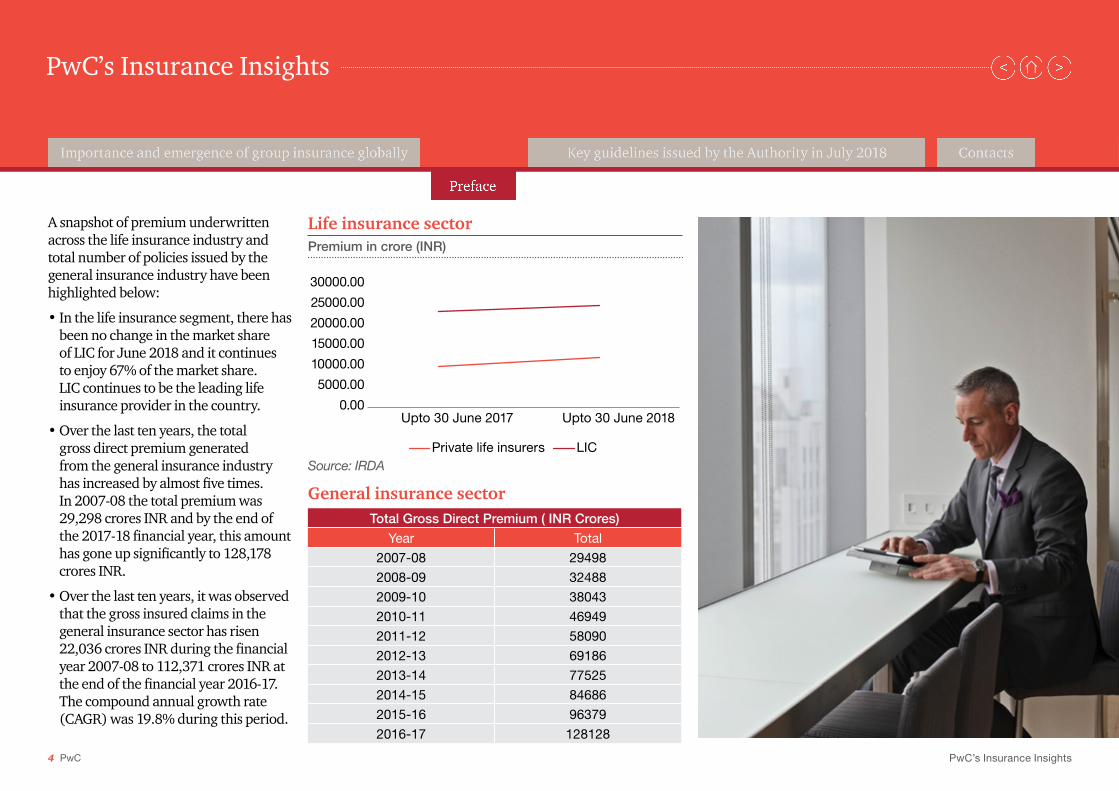

A snapshot of premium underwritten across the life insurance industry and total number of policies issued by the general insurance industry have been highlighted below:

• In the life insurance segment, there has been no change in the market share of LIC for June 2018 and it continues to enjoy 67% of the market share. LIC continues to be the leading life insurance provider in the country.

• Over the last ten years, the total gross direct premium generated from the general insurance industry has increased by almost five times. In 2007-08 the total premium was 29,298 crores INR and by the end of the 2017-18 financial year, this amount has gone up significantly to 128,178 crores INR.

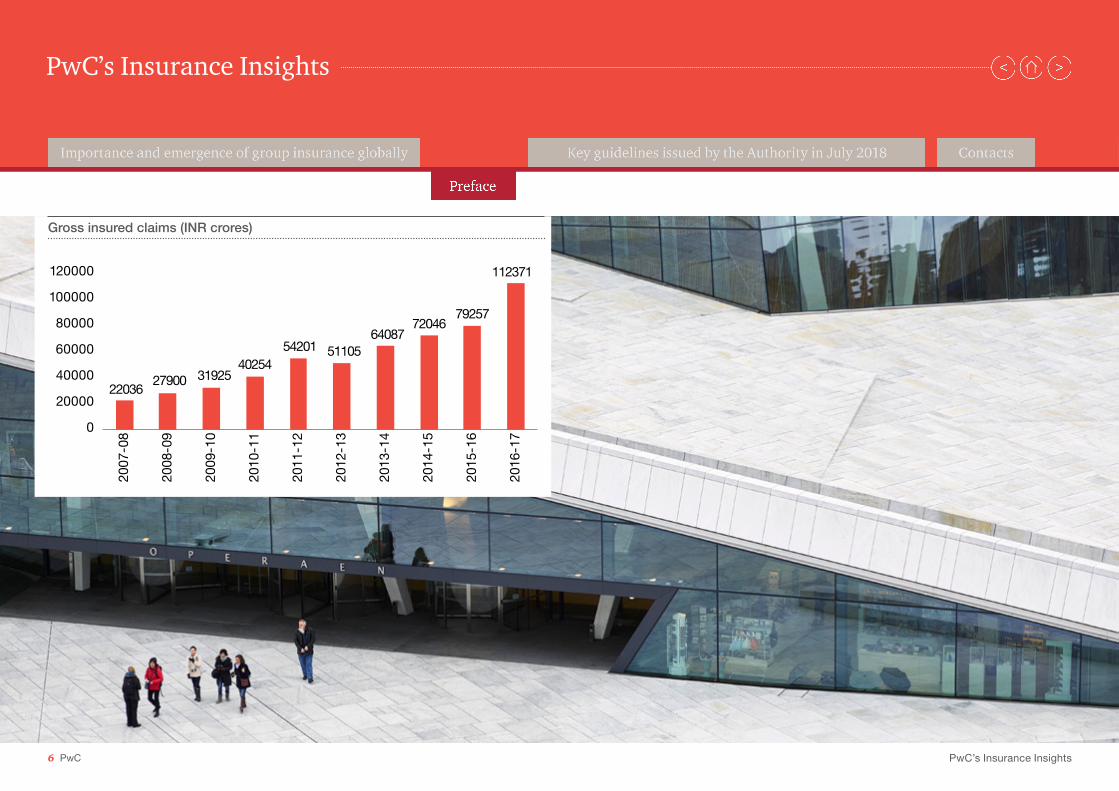

• Over the last ten years, it was observed that the gross insured claims in the general insurance sector has risen 22,036 crores INR during the financial year 2007-08 to 112,371 crores INR at the end of the financial year 2016-17. The compound annual growth rate (CAGR) was 19.8% during this period.

Premium in crore (INR)

0.00

5000.00

10000.00

15000.00

20000.00

25000.00

30000.00

Upto 30 June 2017 Upto 30 June 2018

Private life insurers LICSource: IRDA

General insurance sectorTotal Gross Direct Premium ( INR Crores)

Year Total

2007-08 29498

2008-09 32488

2009-10 38043

2010-11 46949

2011-12 58090

2012-13 69186

2013-14 77525

2014-15 84686

2015-16 96379

2016-17 128128

Life insurance sector

5 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

0

20000

40000

60000

80000

100000

120000

140000

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

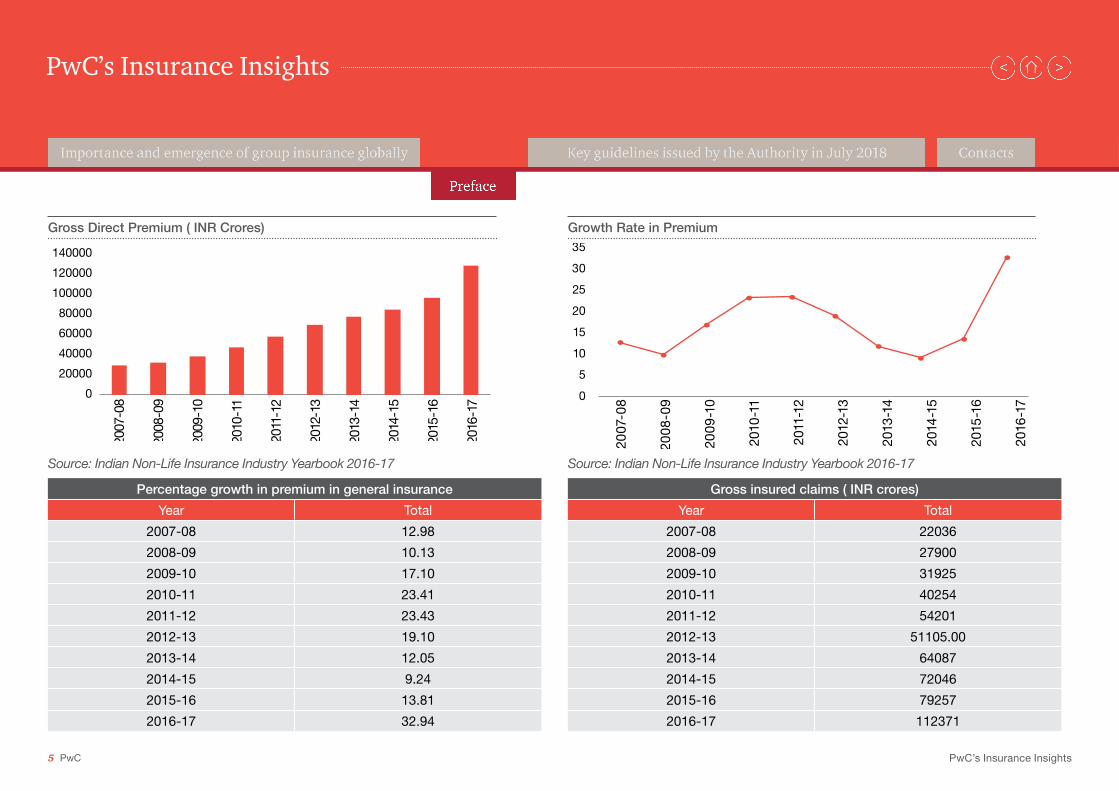

Gross Direct Premium ( INR Crores) Growth Rate in Premium

Source: Indian Non-Life Insurance Industry Yearbook 2016-17 Source: Indian Non-Life Insurance Industry Yearbook 2016-17

Percentage growth in premium in general insurance

Year Total

2007-08 12.98

2008-09 10.13

2009-10 17.10

2010-11 23.41

2011-12 23.43

2012-13 19.10

2013-14 12.05

2014-15 9.24

2015-16 13.81

2016-17 32.94

Gross insured claims ( INR crores)

Year Total

2007-08 22036

2008-09 27900

2009-10 31925

2010-11 40254

2011-12 54201

2012-13 51105.00

2013-14 64087

2014-15 72046

2015-16 79257

2016-17 112371

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-170

5

10

15

20

25

30

35

6 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Gross insured claims (INR crores)

2203627900 31925

4025454201 51105

6408772046

79257

112371

0

20000

40000

60000

80000

100000

120000

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

7 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

PUC Certificate at the time of renewal of insurance of vehicle-directions2

IntroductionWith reference to the order dated 10 August 2017, passed by the Honourable Supreme Court of India in Writ Petition (Civil) No. 13029 of 1985 in M.C. Mehta v. Union of India and Others, the honourable court has directed insurance companies to insure vehicles only if it has a valid pollution under control (PUC) certificate on the date of renewal of the insurance policy.

Implications for insurers• At the time of renewal of motor

insurance, insurance companies will now be required to obtain PUC certificates from clients whereas previously no additional documents were required for renewal of third-party motor insurance.

• The linking of vehicle insurance with the PUC certificate is expected to have a strong and positive impact in the levels of compliance of vehicle drivers.

Our point of view• As PUCs are now mandatory

for clients to renew their motor insurance, the regulator has ensured that there are social benefits arising from this. This will require vehicle drivers to maintain their motor vehicles properly, hence benefiting the environment also. This will ensure increased levels of compliance from vehicle drivers.

Ref: IRDA/NL/CIR/MISC/104/07/2018 Date of issue: 6 July 2018 Applicability: All CEOs and CMDs of general insurance companies

2 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3497&flag=1

8 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

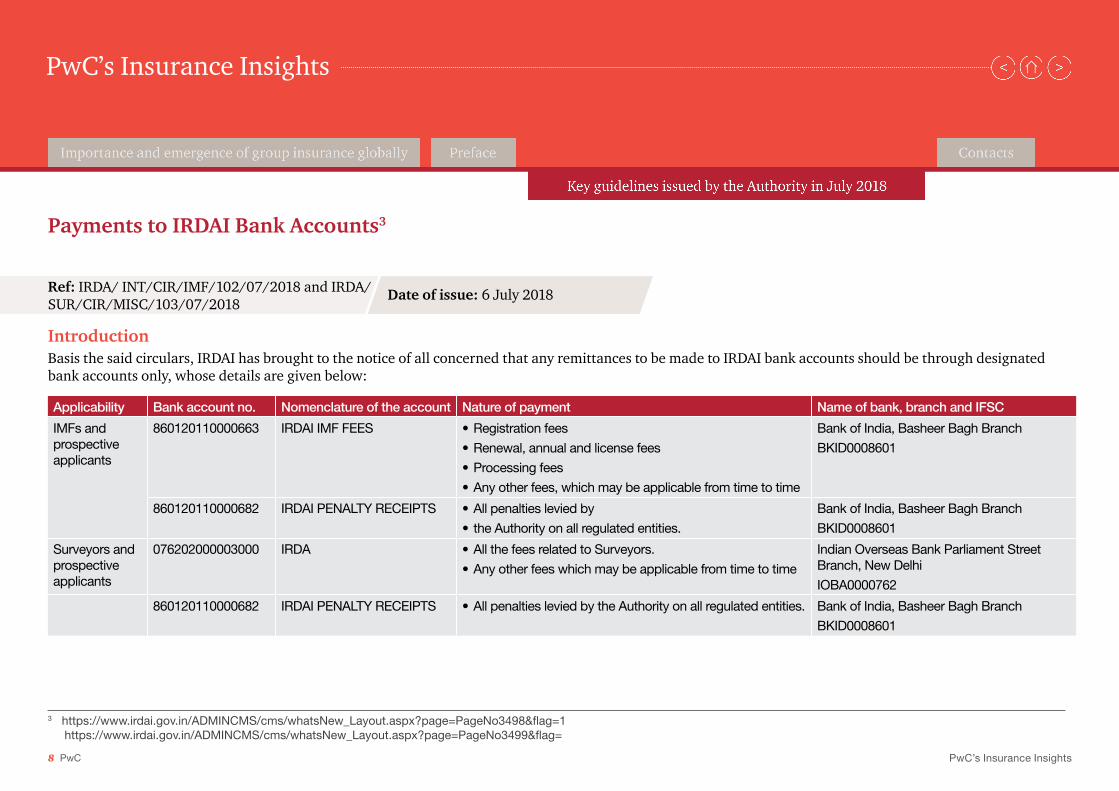

Payments to IRDAI Bank Accounts3

Ref: IRDA/ INT/CIR/IMF/102/07/2018 and IRDA/SUR/CIR/MISC/103/07/2018

Date of issue: 6 July 2018

IntroductionBasis the said circulars, IRDAI has brought to the notice of all concerned that any remittances to be made to IRDAI bank accounts should be through designated bank accounts only, whose details are given below:

Applicability Bank account no. Nomenclature of the account Nature of payment Name of bank, branch and IFSC

IMFs and prospective applicants

860120110000663 IRDAI IMF FEES • Registration fees

• Renewal, annual and license fees

• Processing fees

• Any other fees, which may be applicable from time to time

Bank of India, Basheer Bagh Branch

BKID0008601

860120110000682 IRDAI PENALTY RECEIPTS • All penalties levied by

• the Authority on all regulated entities.

Bank of India, Basheer Bagh Branch

BKID0008601

Surveyors and prospective applicants

076202000003000 IRDA • All the fees related to Surveyors.

• Any other fees which may be applicable from time to time

Indian Overseas Bank Parliament Street Branch, New Delhi

IOBA0000762

860120110000682 IRDAI PENALTY RECEIPTS • All penalties levied by the Authority on all regulated entities. Bank of India, Basheer Bagh Branch

BKID0008601

3 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3498&flag=1 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3499&flag=

9 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

In addition to the above, it is necessary for the applicants to inform the Accounts Department of IRDAI that the remittance made in the bank accounts mentioned above should be in the prescribed format according to Annexure I. The same should be mailed to accounts [at] irda [dot] gov [dot] in with a copy marked to imf [at] irda [dot] gov [dot] in, in case of IMFs and prospective applicants. It should be mailed to accounts [at] irda [dot] gov [dot] in with a copy marked to surveyors [at] irda [dot] gov [dot] in, in case of Surveyors and prospective applicants, on the day of making the remittance.

ImplicationsIn case any remittance is made to the above mentioned bank accounts violating the prescribed format and done without sending the above mentioned confirmation mail will not be taken into account by IRDAI.

10 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Unclaimed amount of policyholders4

IntroductionReference is drawn to Para 6(10) of the issued vide Circular Ref: Master Circular IRDA/F&A/CIR/Misc/173/07/2017 dated 25 July 2017, insurers need to disclose amounts remitted to the Senior Citizens’ Welfare Fund (SCWF) as contingent liability as part of their financial statements. Currently, this rule stands withdrawn and they do not need to disclose the amount that has been remitted to SCWF effective from FY 2018-19.

Our point of viewThis is a good drive initiated by the regulator as it allows for the benefits of senior citizens to be looked after. After a tenure of 10 years, if there is any unclaimed amount from policyholders, it will be transferred to the SCWF, which will help manage senior citizens funds, thereby providing a benefit to the entire social sector.

4 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3502&flag=1

Ref: Master Circular IRDA/F&A/CIR/Misc/173/07/2017 dated 25 July 2017

Date of issue: 11 July 2018 Applicability: To, CMDs/CEOs all Life/General/Health Insurers

11 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

IntroductionWith reference to the order dated 12 January 2017 for reviewing IRDA (Linked Insurance Products) Regulations 2013 and IRDA (Non-Linked Products) Regulations 2013, a committee was constituted by the Authority. A report dated 7 December 2017 was submitted by the Committee, with their recommendations on the above mentioned regulations.

The Authority further constituted a working group, whose responsibilities are as follows:

• Review recommendations of the ‘Committee on Review of Product Regulations – Life’.

• Examine the feedback received from various stakeholders on the above mentioned Committee report.

• Prepare the draft product regulations considering the above report and feedback as reference points.

Furthermore, the working group should meet once a month from the date of constitution of the working group for submitting their recommendations to the Member (Actuary).

Our point of viewWith the focus of the committee being on reviewing linked insurance products and non-linked products,

the regulator aims to have products that are customer-centric in nature, which in turn, will provide benefits to policyholders. With this committee in place, the regulator will be able to review the product regulations, and thereby receive feedback on the various products currently being offered in the insurance market.

5 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3507&flag=1

Ref: IRDAI/ACT/REG/ PRO/ 111/07/2018 Date of issue: 17 July 2018 Applicability: To all

Constitution of working group on life insurance product regulations5

12 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

IntroductionBased on the circular, IRDAI has decided to constitute a committee for the purpose of examining matters pertaining to Motor Third Party pricing as well as to provide recommendations on pricing for the year 2019-20. The tenure of the Committee will be up to 31.12.2018.

The functions of the Committee are as follows:

• Examine motor third party insurance pricing aspects, which mainly includes data related, and recommend prices for 2019-20.

• Revisit the classification of vehicles keeping in view latest developments in the industry.

• Any other matter relevant to motor third party pricing.

Our point of view• With the formation of the committee,

the regulator is focusing on the importance of third party motor insurance. This is a good drive initiated by the regulator wherein with the growing complexity of automation and Insurtech, steps are being taken to set realistic premiums with respect to the Motor Third Party Insurance, which will in turn, benefit the policyholders in the long run.

6 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3509&flag=1

Ref: IRDA/NL/ORD/MOTP/112/07/2018 Date of issue: 20 July 2018 Applicability: To all

Constitution of committee for motor third party pricing for 2019-206

13 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Constitution of working group for standardisation of exclusions in Health Insurance Contracts7

Introduction With the growing importance given to standardisation in the health insurance industry and to enhance transparency and uniformity, the said circular mentions guidelines issued by the Authority such as standardisation of terminology, which is to be used in Health Insurance Policies and Standard Nomenclature and Procedure for Critical Illnesses. Furthermore it is stated in the circular that it is desirable for the industry to adopt a uniform approach while incorporating the ‘exclusions’ as part of product design as well as for the wording of the ‘exclusions’.

For the purpose of scrutinising the above mentioned issue and submitting

appropriate recommendations, a working group was formed with the following functions:

• Examine exclusions that are prevalent in health insurance policies

• Rationalise exclusions by minimising the number, to enhance the scope of health insurance coverage granted

• Rationalise the exclusions that disallow coverage with respect to new modalities of treatments and technologically advanced medical treatments

• Identify the type of exclusions which should not be allowed

• Study wordings or language of exclusions and standardise the

wordings of exclusions in a simple and easily understandable language

• Study the scope for allowing individual specific and/or ailment or disease specific permanent exclusions at the time of underwriting so that policyholders are not denied health insurance claims unrelated to exclusions

• Any other matter relevant to the subject of exclusions

Furthermore, it is advisable that the working group should hold meetings as and when required, and is mandated to submit a report along with the recommendations within eight weeks from the date of this order.

Our point of viewWith the panel examining exclusions that are predominant in the health insurance industry, the view of the regulator is to enhance the scope of the insurance coverage in terms of critical illnesses covered. In a significantly consumer-centric step, the regulator has focused on minimising the number of illnesses or diseases that are not covered under various existing health insurance policies.

Ref: IRDAI/HLT/ORD/Misc/113/07/2018 Date of issue: 24 July 2018 Applicability: To all

7 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3513&flag=1

14 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Modified guidelines on standards and benchmarks for hospitals in the provider network8

Introduction Reference is drawn to Clause (a) and Clause (b) of Chapter IV of Guidelines on Standardization in Health Insurance issued vide Circular Ref: IRDA/HLT/REG/CIR/146/07/2016 dated 29 July 2016, on examining the standards and benchmarks specified in the same.

The modified clauses (a) and (b) are issued stating the following:

• It is mandated by the authority that all the existing network providers, within twelve months from the date of notification of modified guidelines, should comply with the following:

1. Register with Registry of Hospitals in the Network of Insurers (ROHINI) maintained by Insurance Information Bureau (IIB). [https://rohini.iib.gov.in/].

2. Obtain either Pre-entry level Certificate (or higher level of certificate) issued by National Accreditation Board for Hospitals and Healthcare Providers (NABH) or State Level Certificate (or higher level of certificate) under National Quality Assurance Standards (NQAS), issued by National Health Systems Resources Centre (NHSRC).

From the date of notification of these modified Guidelines, the network

providers should comply with the requirements stipulated in Clause (a) (i) as mentioned above. On the other hand, these network providers are required to comply with the requirements specified in Clause (a) (ii) as mentioned within one year from the date of enlisting as a Network Provider and this should be one of the conditions of Health Services Agreement.

• Insurers and TPAs may also strive to get hospitals involved in reimbursement claims to meet the requirements specified in Clause (a) (i) and (a) (ii) as mentioned above.

These modified guidelines are applicable with immediate effect.

Ref: IRDAI/HLT/GDL/CIR/114/07/2018 Date of issue: 27 July 2018 Applicability: To all insurance companies and third party administrators (TPAs)

8 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3517&flag=1

15 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Modified guidelines on standards and benchmarks for hospitals in the provider network8

Introduction According to the Guidelines on Product Filing Procedures, general insurance products are required to use the ‘use and file’ procedure. In terms of managing the diligence of the procedure, the product management committee and the senior management of the insurance company are responsible for making sure that products are designed appropriately and are within the interests of the policyholder. According to the policy, the authority will be allocating Unique Identification Numbers (UIN) to these products. From 1 August 2018, the Business Analytics Project (BAP) tool will allow general insurance

companies to generate UIN for their products. The generation of this number is subject to the products meeting interests of policyholders and also meeting respective regulatory guidelines.

Our point of viewThe UIN allows for greater monitoring of products by the regulator. The IRDA can further scrutinise whether products are meeting minimum specifications. By having a centralised system, the regulator can further assess the impact these products are having on policyholders, whether these products are beneficial to the policyholder.

Ref: IRDA/NL/GDL/F&U/115/07/2018 Date of issue: 31 July 2018 Applicability: The Chairman- Cum- Managing Directors/ Chief Executive Officers of General Insurance Companies

9 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3518&flag=1

16 PwC PwC’s Insurance Insights

PwC’s Insurance Insights

Vivek Iyer Partner [email protected] Mobile: +91 9167745318

Dnyanesh Pandit Director [email protected] Mobile: +91 9819446928

Joydeep K Roy Partner [email protected] Mobile: +91 9821611173

Saigeeta Bhargava Associate Director [email protected] Mobile: +91-9560518833

Yugal Mehta Manager [email protected] Mobile: +91 9970163293

Varsha Mehrotra Consultant [email protected] Mobile: +91 83890640211

Prateek Kannan Consultant [email protected] Mobile: +91 9840753109

At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 158 countries with more than 2,36,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com

In India, PwC has offices in these cities: Ahmedabad, Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata, Mumbai and Pune. For more information about PwC India’s service offerings, visit www.pwc.com/in

PwC refers to the PwC International network and/or one or more of its member firms, each of which is a separate, independent and distinct legal entity. Please see www.pwc.com/structure for further details.

© 2018 PwC. All rights reserved

About PwC

pwc.inData Classification: DC0

This document does not constitute professional advice. The information in this document has been obtained or derived from sources believed by PricewaterhouseCoopers Private Limited (PwCPL) to be reliable but PwCPL does not represent that this information is accurate or complete. Any opinions or estimates contained in this document represent the judgment of PwCPL at this time and are subject to change without notice. Readers of this publication are advised to seek their own professional advice before taking any course of action or decision, for which they are entirely responsible, based on the contents of this publication. PwCPL neither accepts or assumes any responsibility or liability to any reader of this publication in respect of the information contained within it or for any decisions readers may take or decide not to or fail to take.

© 2018 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Private Limited (a limited liability company in India having Corporate Identity Number or CIN : U74140WB1983PTC036093), which is a member firm of PricewaterhouseCoopers International Limited (PwCIL), each member firm of which is a separate legal entity.

PD/September 2018-14335