Pwc Current Issues in Income Tax Accounting Us Gaap and Ifrs Pt 1

85

Current issues in income tax accounting (US GAAP & IFRS) www.pwc.com May 16, 2012 May 16, 2012

description

Current issues in incometax accounting(US GAAP & IFRS)

Transcript of Pwc Current Issues in Income Tax Accounting Us Gaap and Ifrs Pt 1

Current issues in incometax accounting(US GAAP & IFRS)

www.pwc.com

May 16, 2012May 16, 2012

Agenda

Introductions

Basic overview of the model

Uncertain tax positions

PwC

Unremitted foreign earnings

Special topics (Intraperiod Allocations, Non-controlling interest, Passthrough Accounting)

Interim accounting

Q&A

Current issues in income tax accounting (US GAAP & IFRS)

Basic model

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

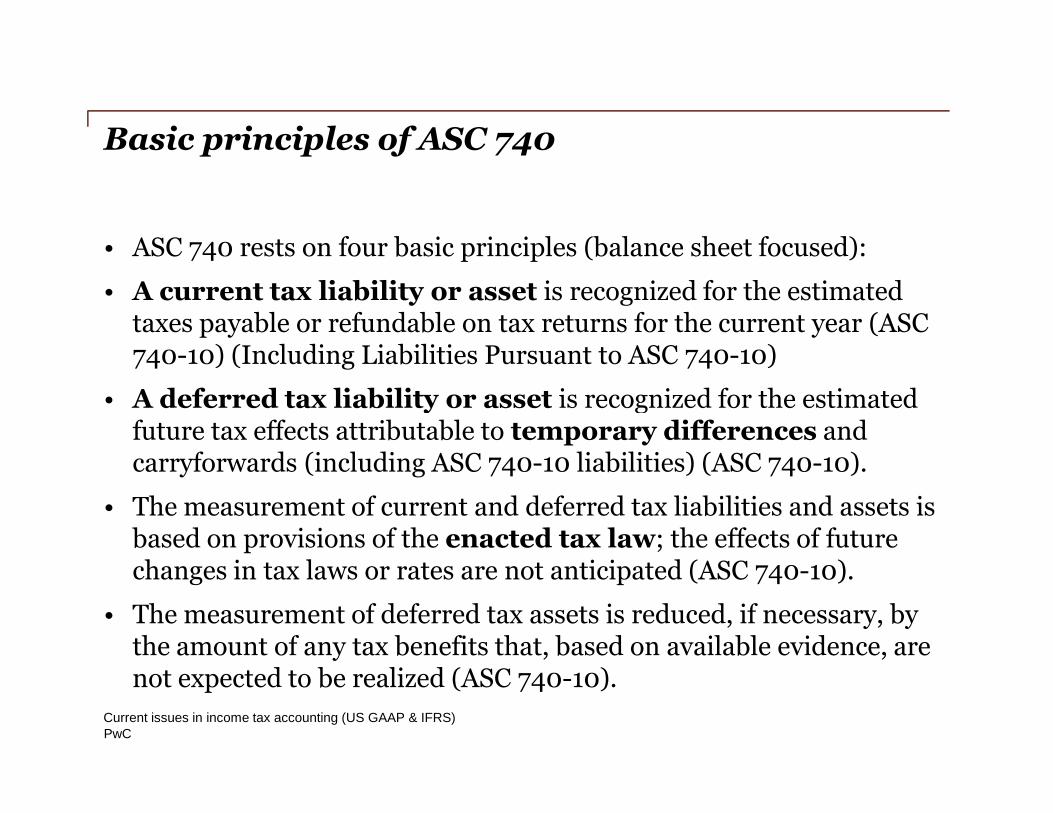

Basic principles of ASC 740

• ASC 740 rests on four basic principles (balance sheet focused):

• A current tax liability or asset is recognized for the estimatedtaxes payable or refundable on tax returns for the current year (ASC740-10) (Including Liabilities Pursuant to ASC 740-10)

• A deferred tax liability or asset is recognized for the estimated

PwC

• A deferred tax liability or asset is recognized for the estimatedfuture tax effects attributable to temporary differences andcarryforwards (including ASC 740-10 liabilities) (ASC 740-10).

• The measurement of current and deferred tax liabilities and assets isbased on provisions of the enacted tax law; the effects of futurechanges in tax laws or rates are not anticipated (ASC 740-10).

• The measurement of deferred tax assets is reduced, if necessary, bythe amount of any tax benefits that, based on available evidence, arenot expected to be realized (ASC 740-10).

Current issues in income tax accounting (US GAAP & IFRS)

Income tax components

• Current tax provision is an estimate of taxes payable orrefundable on tax returns for the current year (ASC 740-10).(Includes liabilities for unrecognized tax benefits)

• Deferred tax provision is the change in the estimated future taxeffects attributable to temporary differences and carryforwards (ASC740-10).

PwC

740-10).

• Total income tax provision is the combination of the both thecurrent and deferred components of the provision.

Current issues in income tax accounting (US GAAP & IFRS)

Tax provision process

1. Adjust pretax income for permanent differences.

2. Identify all temporary differences and carryforwards.

3. Calculate the current income tax expense or benefit.

4. Recognize deferred tax assets and liabilities.

PwC

5. Evaluate the need for a valuation allowance for gross deferred taxassets.

6. Calculate the deferred income tax expense or benefit.

Current issues in income tax accounting (US GAAP & IFRS)

Permanent differences(Step 1) – Adjust Pre-tax income for permanent differences

• Permanent Differences…

- These are book versus tax items or book/tax differences that willnot reverse in future periods.

• Permanent Differences Do…

- Impact the total tax provision. That is, an increase in current tax

PwC

- Impact the total tax provision. That is, an increase in current taxexpense (I/S debit) is not offset by any deferred tax benefit (I/Scredit) of equal amount or vice versa.

• Impact the overall effective rate on the total tax provision.

• Common Permanent Differences

- Percentage Depletion in excess of Tax Basis

- Section 199 Deduction

- State TaxesCurrent issues in income tax accounting (US GAAP & IFRS)

Temporary differences(Step 2) – Identify all temporary differences & carryforwards

• The objective of deferred tax accounting is to:

- Recognize a liability or asset related to temporary differences

• The objective is accomplished by:

- Comparing the aggregate GAAP amount of any one item to thatitem’s aggregate tax basis (book basis balance sheet versus tax

PwC

item’s aggregate tax basis (book basis balance sheet versus taxbasis balance sheet)

- Recognizing deferred taxes for those items that will producetaxable or deductable differences when the GAAP balance amountis recovered or settled

And

- Recording deferred taxes for items without related balance sheetcaptions (i.e. tax credits and carryforwards)

Current issues in income tax accounting (US GAAP & IFRS)

Deferred tax terminology(Step 2) – Identify all temporary differences & carryforwards

Current Provision

• Focuses on the change in gross temporary differences

Deferred Tax Assets / Liabilities

• Is the tax effect of the cumulative temporary differences pluscarryforward attributes

PwC

carryforward attributes

Valuation Allowance

• Reduces the Deferred Tax Asset to a Realizable Amount

Current issues in income tax accounting (US GAAP & IFRS)

Examples of deferred tax assets(Step 2) – Identify all temporary differences & carryforwards

• Temporary Depletion (Cost or Percentage)

• Depreciation

• Development Costs

• Deferred Stripping

• Reclamation

PwC

• Reclamation

• Compensation accruals (vacation, bonus, commission)

• Contingency accruals (legal, environmental)

• Tax carryforward items, for example:

• Foreign tax credits in worldwide taxation regimes that allow creditsfor foreign taxes paid

• Net operating losses

• AMT Credits

Current issues in income tax accounting (US GAAP & IFRS)

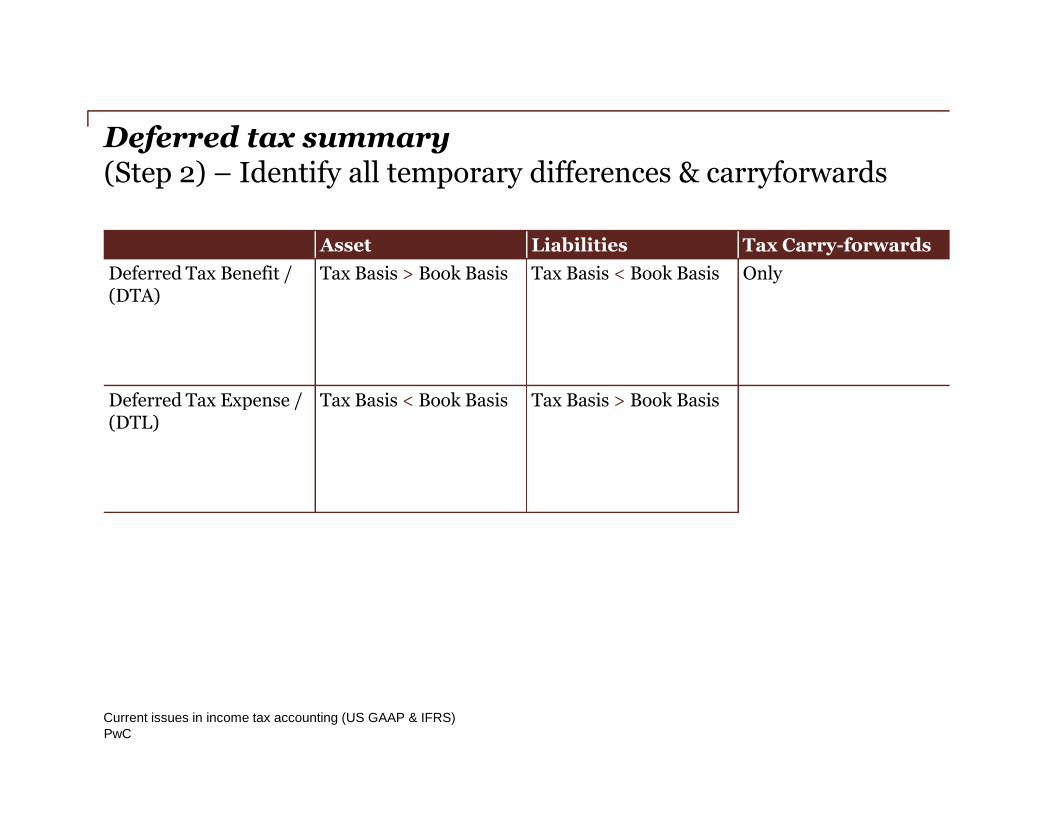

Deferred tax summary(Step 2) – Identify all temporary differences & carryforwards

Asset Liabilities Tax Carry-forwards

Deferred Tax Benefit /(DTA)

Tax Basis > Book Basis Tax Basis < Book Basis Only

Deferred Tax Expense / Tax Basis < Book Basis Tax Basis > Book Basis

PwC

Deferred Tax Expense /(DTL)

Tax Basis < Book Basis Tax Basis > Book Basis

Current issues in income tax accounting (US GAAP & IFRS)

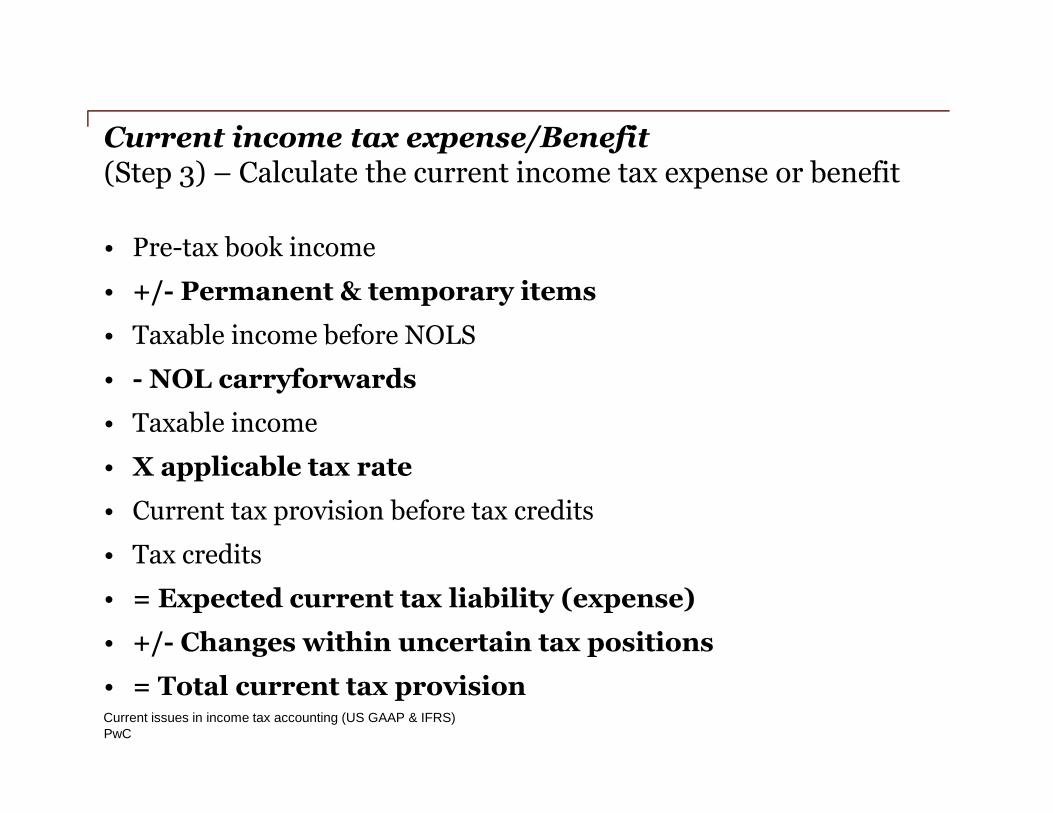

Current income tax expense/Benefit(Step 3) – Calculate the current income tax expense or benefit

• Pre-tax book income

• +/- Permanent & temporary items

• Taxable income before NOLS

• - NOL carryforwards

PwC

• Taxable income

• X applicable tax rate

• Current tax provision before tax credits

• Tax credits

• = Expected current tax liability (expense)

• +/- Changes within uncertain tax positions

• = Total current tax provisionCurrent issues in income tax accounting (US GAAP & IFRS)

Deferred tax terminology(Step 3) – Calculate the current income tax expense or benefit

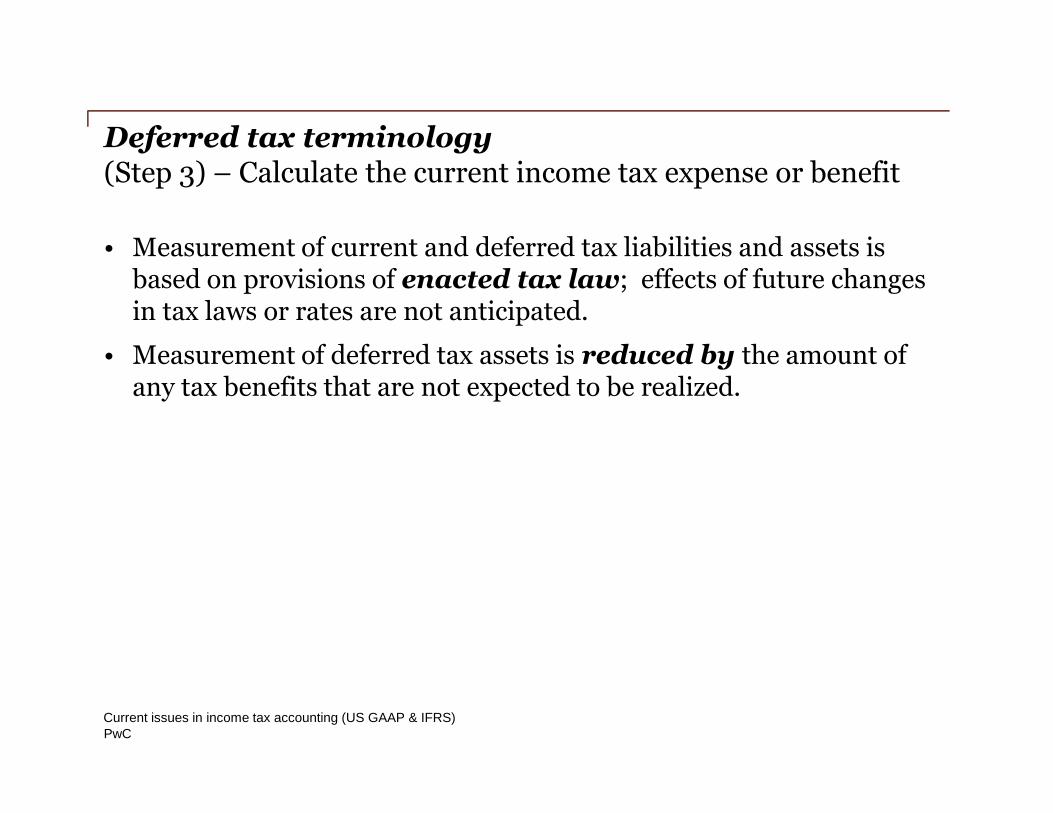

• Measurement of current and deferred tax liabilities and assets isbased on provisions of enacted tax law; effects of future changesin tax laws or rates are not anticipated.

• Measurement of deferred tax assets is reduced by the amount ofany tax benefits that are not expected to be realized.

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Recognize deferred tax assets and liabilities(Step 4) – Recognize deferred tax assets and liabilities

• The deferred tax expense or benefit for the current year iscomputed as the change during the year in an enterprise’s deferredtax liabilities and assets.

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

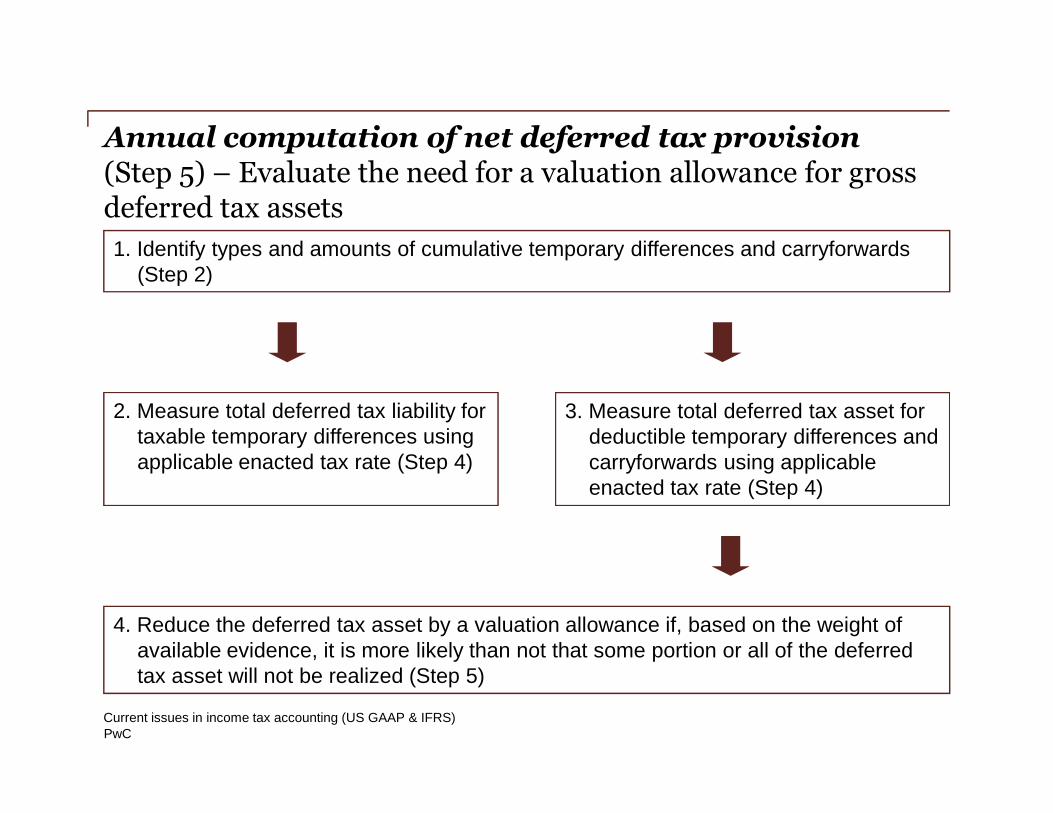

Annual computation of net deferred tax provision(Step 5) – Evaluate the need for a valuation allowance for grossdeferred tax assets

1. Identify types and amounts of cumulative temporary differences and carryforwards(Step 2)

2. Measure total deferred tax liability for 3. Measure total deferred tax asset for

PwC

4. Reduce the deferred tax asset by a valuation allowance if, based on the weight ofavailable evidence, it is more likely than not that some portion or all of the deferredtax asset will not be realized (Step 5)

2. Measure total deferred tax liability fortaxable temporary differences usingapplicable enacted tax rate (Step 4)

3. Measure total deferred tax asset fordeductible temporary differences andcarryforwards using applicableenacted tax rate (Step 4)

Current issues in income tax accounting (US GAAP & IFRS)

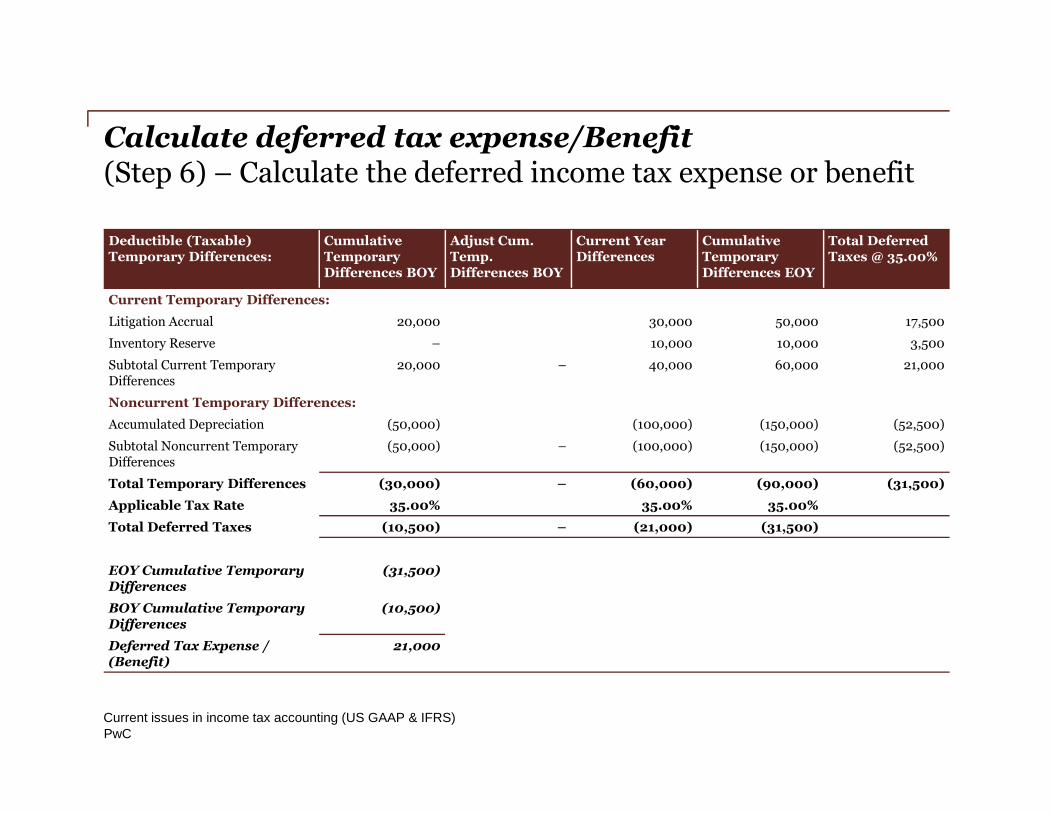

Calculate deferred tax expense/Benefit(Step 6) – Calculate the deferred income tax expense or benefit

Deductible (Taxable)Temporary Differences:

CumulativeTemporaryDifferences BOY

Adjust Cum.Temp.Differences BOY

Current YearDifferences

CumulativeTemporaryDifferences EOY

Total DeferredTaxes @ 35.00%

Current Temporary Differences:

Litigation Accrual 20,000 30,000 50,000 17,500

Inventory Reserve – 10,000 10,000 3,500

Subtotal Current TemporaryDifferences

20,000 – 40,000 60,000 21,000

Noncurrent Temporary Differences:

PwC

Noncurrent Temporary Differences:

Accumulated Depreciation (50,000) (100,000) (150,000) (52,500)

Subtotal Noncurrent TemporaryDifferences

(50,000) – (100,000) (150,000) (52,500)

Total Temporary Differences (30,000) – (60,000) (90,000) (31,500)

Applicable Tax Rate 35.00% 35.00% 35.00%

Total Deferred Taxes (10,500) – (21,000) (31,500)

EOY Cumulative TemporaryDifferences

(31,500)

BOY Cumulative TemporaryDifferences

(10,500)

Deferred Tax Expense /(Benefit)

21,000

Current issues in income tax accounting (US GAAP & IFRS)

Uncertain tax positions

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Key definitions and concepts

1. Tax Position – Position in a previously filed tax return or expected tobe taken in a future tax return (ASC 740-10-20 Glossary)

2. Unit of Account – That which is being measured by reference to thelevel at which an asset or liability is aggregated or disaggregated (ASCMaster Glossary)

PwC

3. Recognition – A tax benefit from a UTP may only be recognized if itis “more-likely-than-not” that the position is sustainable based solelyon technical merits and any relevant administrative practices (ASC740-10-55-3)

4. Measurement – Greatest amount of benefit cumulatively >50% likelyof being realized (ASC 740-10-30)

Current issues in income tax accounting (US GAAP & IFRS)

Key definitions and concepts (cont)

5. Subsequent recognition and measurement – Recognition andmeasurement subject to change based on new information (ASC 740-10-35)

6. Effective settlement – The point at which an Uncertain Tax Positionbecomes certain. (ASC 740-10-25-10)

PwC

7. Interest/Penalties

- Required accrual of interest and penalties (ASC 740-10-25-56)

- Classification is an accounting policy election (ASC 740-10-25-57)

8. Balance sheet classification – Non-current treatment for “liability forunrecognized tax benefit” unless cash payment is expected within 12months

Current issues in income tax accounting (US GAAP & IFRS)

Key definitions and concepts (cont)

9. Disclosures (ASC 740-10-50-15)

- Tabular roll-forward of aggregated unrecognized tax benefits(UTBs)

- The total amount of UTBs that, if recognized, would affect theeffective tax rate

PwC

effective tax rate

- The total amount of interest and penalties recognized in theincome statement and accrued on the balance sheet

- Discussion of reasonably possible changes in the UTBs in the next12 months

- Description of open tax years by major jurisdictions

Current issues in income tax accounting (US GAAP & IFRS)

Recognition

• Two-step model (recognition then measurement) beginning withwhether the tax position should be recognized (i.e. whether anybenefit should be recorded)

• Recognition is based on the following criteria:

- More-likely-than-not (>50%) that the position will be sustained

PwC

- More-likely-than-not (>50%) that the position will be sustainedupon examination by taxing authority (including any appeal orlitigation process)

- Technical merits of the position

- No consideration of detection risk

- Past administrative practices accommodation

Current issues in income tax accounting (US GAAP & IFRS)

Recognition

• Temporary differences are considered to have met therecognition threshold

• Positions do not generally affect the aggregate amount of taxespayable over time, they can generate an economic benefit by delayingthe tax payment

PwC

• Historically, may have only accrued for interest

• ASC 740 requires separation into two parts

- Sustainable book/tax difference pursuant to ASC 740's recognitioncriteria

- A liability for any "unrecognized" benefit.

Current issues in income tax accounting (US GAAP & IFRS)

Measurement

• Assuming the recognition threshold has been met, the company thenneeds to measure the benefit to be sustained:

• Tax positions should be measured at the largest amount that has acumulative probability >50% of being the ultimate outcome

• Consider the amounts and probabilities of various outcomes

PwC

• Consider the amounts and probabilities of various outcomes

Current issues in income tax accounting (US GAAP & IFRS)

Measurement

• Example

Enterprise takes a deduction in a tax return that results in a tax benefitof $100. This position meets the recognition threshold (i.e., MLTN).Distribution of potential outcomes:

Potential benefit Individual probability Cumulative probability

PwC

Potential benefit Individual probability Cumulative probability

$100 15% 15%

$80 20% 35%

$60 20% 55%

$40 30% 85%

$20 15% 100%

Recognition of the largest amount that has a cumulative probability of>50% of being ultimately realized is $60

Current issues in income tax accounting (US GAAP & IFRS)

Subsequent recognition and measurement

• Key areas of judgement and challenges

- Evaluating “new information” that leads to changes in recognitionand measurement

- Tracking reversals of temporary differences

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Subsequent recognition and measurement

• Recognition and measurement should be reassessed (using ASC 740-10 model) at each reporting date.

- ASC 740-10 assessment (recognition and measurement) subject tochange based on new information

◦ Changes to prior year tax positions would be treated as discrete

PwC

◦ Changes to prior year tax positions would be treated as discreteitems in the period the change occurs

◦ Changes to current year tax positions would be accounted for under ASC 270-10-45-12

- May occur prior to final to resolution of matter

- “Subsequent event” disclosure considerations

Current issues in income tax accounting (US GAAP & IFRS)

Subsequent recognition and measurement

• Developments in the audit

• Audit plans

• Oral statements by tax authority

• Pre-filing agreements

• Developments in the law

• Public statements by taxauthority

• Audit guidelines

• Potential Sources of “New Information”

PwC

• Pre-filing agreements

• “LIFE” audits

• Experience in prior audits

• Taxing authority programchanges

• APA, competent authority

• Notice of ProposedAdjustment

• Revenue Agent’s Report

• Designation for litigation

• Listing of transactions

Current issues in income tax accounting (US GAAP & IFRS)

Settlement

• In order to apply ASC 740 model for tax uncertainties, Companiesmust

- Maintain an inventory of Unsettled UTPs

- Monitor and track settlement of UTPs

Key Question – When is an Uncertain Tax Position settled ?

PwC

Key Question – When is an Uncertain Tax Position settled ?

Current issues in income tax accounting (US GAAP & IFRS)

Effective settlement

• What does Effective Settlement mean?

• Three considerations on “Effective Settlement”

- Whether a tax position has been specifically examined

- Whether the examination has been completed.

PwC

- Whether there is only a remote likelihood of re-examination

Current issues in income tax accounting (US GAAP & IFRS)

Effective settlement

• Taxing authority has completed examination procedures includingappeals and administrative reviews required

• Taxpayer does not intend to appeal or litigate any aspect of taxposition included in completed examination

• It is remote that the taxing authority would examine or reexamine

PwC

• It is remote that the taxing authority would examine or reexamineany aspect of the tax position

Current issues in income tax accounting (US GAAP & IFRS)

Unremitted foreign earnings

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Unremitted foreign earnings

• Calculation of US DTL on Unremitted Foreign Earnings

• Effective Tax Rate implications

• Unborn Foreign Tax Credits

• Withholding Taxes

PwC

• Classification of US DTL

Current issues in income tax accounting (US GAAP & IFRS)

Unremitted foreign earnings

• Permanent Reinvestment Assertion

• Support Required to Substantiate the Assertion

• Effect of assertion on current year earnings and EAETR

• Distributions

PwC

• Frequency of updating the assertion

• Partial reinvestment assertion

• Effect of a change in assertion

Current issues in income tax accounting (US GAAP & IFRS)

Special topics

Intraperiod allocation, non-controllinginterest, & Passthrough

PwCMay 2012AFIT - Intraperiod Allocation, Interim Reporting and Intercompany Transactions

Intraperiod tax allocation

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

What does “Intraperiod Tax Allocation” mean

• Income tax expense (benefit) can be reflected in:

- Continuing operations

- Discontinued operations

- Extraordinary Items

PwC

- Cumulative effect of accounting change

- Other comprehensive income (OCI)

- APIC

- Goodwill (or other intangible assets)

Current issues in income tax accounting (US GAAP & IFRS)

Intraperiod tax allocation

• ASC 740-20-45-2 states that income tax expense or benefit for theyear shall be allocated among continuing operations, discontinuedoperations, extraordinary items, other comprehensive income, anditems charged or credited directly to shareholders’ equity.

• Rule of Thumb - the tax follows the items of income, gain, expense orloss

PwC

loss

Current issues in income tax accounting (US GAAP & IFRS)

Authoritative guidance

ASC 740-20-45-7 states that

The tax effect of pretax income or loss from continuing operationsgenerally should be determined by a computation that does notconsider the tax effects of items that are not included in continuingoperations (an “incremental approach”)

PwC

PwC Guidance in Guide to Accounting for Income Taxes

Chapter 12.

Current issues in income tax accounting (US GAAP & IFRS)

Intraperiod allocation issues

Intraperiod allocation is a mechanical process:

Calculate the total tax expense from all sources

Calculate the tax expense from continuing operations without regardto other categories

If there is only one category other than continuing operations, allocate

PwC

If there is only one category other than continuing operations, allocatethe entire difference between (1) and (2) to that category

If there is more than one category other than continuing operations,allocate the difference among the other items in proportion to theirindividual effects on total tax expense (ASC 740-20-45-14)

Current issues in income tax accounting (US GAAP & IFRS)

Tax effects specifically allocated to continuingoperations

• Changes in tax laws or rates (ASC 740-20-45-8(b); see also ASC 740-10-25-47 & 48)

• Change in tax status (ASC 740-20-45-8(c); see alsoASC 740-10-25-32)

• Changes in the assessment about the realizability of deferred tax

PwC

• Changes in the assessment about the realizability of deferred taxassets that existed at the beginning of the year because of a change inthe expectation of taxable income available in future years that arenot related to “source-of-loss” items (ASC 740-20-45-8(a); see alsoASC 740-10-45-20)

Current issues in income tax accounting (US GAAP & IFRS)

Tax effects specifically allocated to continuingoperations

• Tax deductible dividends paid to shareholders (ASC 740-20-45-8(d))

• Tax effect of changes in assertion on plans for repatriation of prioryears’ unremitted earnings of foreign subsidiaries(ASC 740-30-25-19)

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Tax effects allocated to specific components otherthan continuing operations (ASC 740-20-45-11)

• Other comprehensive income

- Cumulative translation adjustments (ASC 830)

- Gains and losses on cash flow hedges - hedging derivatives (ASC815)

- Unrealized gains and losses of “available-for-sale” debt and equity

PwC

- Unrealized gains and losses of “available-for-sale” debt and equitysecurities (ASC 320)

- Net unrecognized gains and losses and unrecognized prior servicecost related to pension and other OPEB (ASC 715)

Current issues in income tax accounting (US GAAP & IFRS)

Tax effects allocated to specific components otherthan continuing operations (ASC 740-20-45-11)

• Adjustments of the opening balance of retained earnings for certainchanges in accounting principles or a correction of an error

• Gains and losses included in comprehensive income but excludedfrom net income (i.e., translation, changes in carrying value of netmarketable securities)

PwC

• An increase or decrease in contributed capital (for exampledeductible expenditures recorded as a reduction in the proceeds fromissuing capital stock)

• An increase in the tax basis of assets acquired in a taxable businesscombination accounted for as a pooling of interests and for which atax benefit is recognized at the date of the business combination

Current issues in income tax accounting (US GAAP & IFRS)

Tax effects allocated to specific components otherthan continuing operations (ASC 740-20-45-11)

• Expenses for employee stock options recognized differently forfinancial reporting and tax purposes (see ASC 718-740)

• Dividends that are paid on unallocated shares held by an ESOP andthat are charged to retained earnings

• Deductible temporary differences and carryforwards that existed at

PwC

• Deductible temporary differences and carryforwards that existed atthe date of a quasi-reorganization (except as set forth in (ASC 852-740-55)

Current issues in income tax accounting (US GAAP & IFRS)

Intraperiod allocations issues-valuationallowances

• In the case of a change in the valuation allowance applicable tobeginning-of-year deferred tax assets that results from changes incircumstances that cause the assessment of the likelihood ofrealization of these assets by income in future years to change, theeffect is reflected in continuing operations. (ASC 740-10-45-20)

• When income in the current year allows for the release of a

PwC

• When income in the current year allows for the release of avaluation allowance, the benefit from the release of the valuationallowance is allocated to the current year component of income thatallows for its recognition.

Current issues in income tax accounting (US GAAP & IFRS)

Intraperiod allocations issues-valuationallowances

• However, there is an exception to the extent that the valuationallowance relates to source-of-loss items.

• For the initial recognition of “source-of-loss” items the benefits areallocated back to the prior-year source that generated the loss.

• Source-of-loss items

PwC

• Source-of-loss items

- Tax benefits relating to certain equity items.

Current issues in income tax accounting (US GAAP & IFRS)

Non-controlling interest

• The financial statement amounts reported for income tax expenseand net income attributable to non-controlling interest differ basedon whether the subsidiary is a C-corporation or a partnership. Thetax status of each type of entity causes differences in the amounts aparent company would report in its consolidated income taxprovision and net income attributable to non-controlling interest.

PwC

provision and net income attributable to non-controlling interest.

Current issues in income tax accounting (US GAAP & IFRS)

Non-controlling interest

• A C-Corporation is generally a taxable entity and is responsible forthe tax consequences of transactions by the corporation. Therefore, aparent that consolidates a C-corporation would include the incometaxes of the C-corporation, including the income taxes attributable tothe non-controlling interest, in the consolidated income taxprovision. Net income attributable to the non-controlling interest

PwC

provision. Net income attributable to the non-controlling interestwould be calculated as the non-controlling interest’s share of the C-corporation’s net income, which would include a provision forincome taxes.

Current issues in income tax accounting (US GAAP & IFRS)

Non-controlling interest

• The legal liability for income taxes of a partnership generally donesnot accrue to the partnership itself. Instead, the investors areresponsible for income taxes on their share of the partnership’sincome. Therefore, a parent that consolidates a partnership wouldonly reort income taxes on its share of the partner’s income in theconsolidated income tax provision. This would result in a reconciling

PwC

consolidated income tax provision. This would result in a reconcilingitem in the parent’s effective tax rate reconciliation that should bedisclosed, if material.

Current issues in income tax accounting (US GAAP & IFRS)

Partnerships and other flow-through entities

• Generally, deferred taxes related to investment in a foreign ordomestic partnership (and other flow-through entities that are taxesas partnerships, such as multi-member LLCs) should be measuredbased on the differences between the financial statement investmentand its tax basis (i.e. outside basis differences).

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Partnerships and other flow-through entities

• Exceptions to the general guidance have been made in practice.Specifically, different views exist regarding if and when deferredtaxes should be provided on the portion of an outside basis differenceattributable to nondeductible goodwill.

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Partnerships and other flow-through entities

• We believe that an entity must adopt a consistent policy to

(1) look through the outside basis of the partnership and exclude itfrom the computation of deferred taxes on all underlying items forwhich ASC 740 provides an exception to its comprehensive model ofrecognition

PwC

-or-

(2) not look through the outside basis of the partnership and recorddeferred taxes based on the entire difference between the book andtax bases of its investment.

Current issues in income tax accounting (US GAAP & IFRS)

Interim period reporting

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• ASC 70-270-30-6 (Interim Reporting) states that

At the end of each interim period the company should make its bestestimate of the effective tax rate expected to be applicable for the fullfiscal year. In some cases, the estimated annual effective tax ratewill be the statutory rate modified as may be appropriate inparticular circumstances. In other cases, the rate will be the entity's

PwC

particular circumstances. In other cases, the rate will be the entity'sestimate of the tax (or benefit) that will be provided for the fiscalyear, stated as a percentage of its estimated ordinary income (orloss) for the fiscal year (see paragraphs 740-270-30-30 through 30-34 if an ordinary loss is anticipated for the fiscal year).

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• ASC 70-270-30-8 (Interim Reporting) further states that

The estimated effective tax rate shall also reflect anticipatedinvestment tax credits, foreign tax rates, percentage depletion,capital gains rates, and other available tax planning alternatives.However, in arriving at this estimated effective tax rate, no effectshall be included for the tax related to significant unusual or

PwC

shall be included for the tax related to significant unusual orextraordinary items that will be separately reported or reported netof their related tax effect in reports for the interim period or for thefiscal year. The rate so determined shall be used inproviding for income taxes on a current year-to-datebasis.

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

PwC Guidance at Guide to Accounting for Income Taxes

Chapter 17.

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Basic rules

• Calculate the tax effects of current-year ordinary income or loss usingan estimated full year effective tax rate.

• All other items are recorded discretely, which includes:

- Significant, unusual or infrequent items

- Extraordinary items

PwC

- Extraordinary items

- Discontinued operations

- Cumulative effects of changes in accounting principles

• Concept is that each interim period is primarily an integral part ofthe annual period.

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• ASC 740-270-25-9 states that

The tax effects of losses that arise in the early portion of a fiscal yearshall be recognized only when the tax benefits are expected to beeither:

a. Realized during the year

PwC

a. Realized during the year

b. Recognizable as a deferred tax asset at the end of the year inaccordance with the provisions of Subtopic 740-10.

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• ASC 740-270-25-5 states that

The effects of new tax legislation shall not be recognized prior toenactment. The tax effect of a change in tax laws or rates on taxescurrently payable or refundable for the current year shall berecorded after the effective dates prescribed in the statutes andreflected in the computation of the annual effective tax rate

PwC

reflected in the computation of the annual effective tax ratebeginning no earlier than the first interim period that includes theenactment date of the new legislation. The effect of a change in taxlaws or rates on a deferred tax liability or asset shall not beapportioned among interim periods through an adjustment of theannual effective tax rate.

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• ASC 740-270-25-6 adds that

The tax effect of a change in tax laws or rates on taxes payable orrefundable for a prior year shall be recognized as of the enactmentdate of the change as tax expense (benefit) for the current year. SeeExample 6 (paragraph 740-270-55-44) for illustrations ofaccounting for changes caused by new tax legislation.

PwC

accounting for changes caused by new tax legislation.

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• ASC 740-270-25-2 states the general rules that

• The tax (or benefit) related to ordinary income (or loss) shall becomputed at an estimated annual effective tax rate and the tax (orbenefit) related to all other items shall be individually computed andrecognized when the items occur.

PwC

• “Other items” often are referred to as “discrete items.”

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• Key questions:

- What is the definition of “the tax (or benefit)”?

- What is the definition of “ordinary income”?

- What are “other (discrete) items”?

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Interim reporting – Definitions

• Tax (or benefit) is the total income tax expense (or benefit),including the provision (or benefit) for income taxes both currentlypayable and deferred. (ASC 740-270-20 Glossary)

• Ordinary income (or loss) refers to income (or loss) fromcontinuing operations before income taxes (or benefits) excludingsignificant unusual or infrequently occurring items. Extraordinary

PwC

significant unusual or infrequently occurring items. Extraordinaryitems, discontinued operations, and cumulative effects of changes inaccounting principles are also excluded from this term. The term isnot used in the income tax context of ordinary income versus capitalgain. The meaning of unusual or infrequently occurring items isconsistent with their use in the definition of the term extraordinaryitem. (ASC 740-270-20 Glossary)

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting – Definitions

Extraordinary items are events and transactions that aredistinguished by their unusual nature and by the infrequency of theiroccurrence. Thus, both of the following criteria should be met toclassify an event or transaction as an extraordinary item:

a.Unusual nature. The underlying event or transaction shouldpossess a high degree of abnormality and be of a type clearly

PwC

possess a high degree of abnormality and be of a type clearlyunrelated to, or only incidentally related to, the ordinary andtypical activities of the entity, taking into account the environmentin which the entity operates (see paragraph 225-20-60-3).

b.Infrequency of occurrence. The underlying event or transactionshould be of a type that would not reasonably be expected to recurin the foreseeable future, taking into account the environment inwhich the entity operates (see paragraph 225-20-60-3). (ASC 740-270-20 Glossary)

Current issues in income tax accounting (US GAAP & IFRS)

Interim period tax provisions

• Discrete items are excluded from the annual effective tax ratecomputation and are separately reported in interim reports orreported net of tax effects in interim reports.(ASC 740-270-30-11 through 13).

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Potential discrete tax items

• Tax true-ups

• Resolution of tax audits

• Statute of limitation expiration

• Changes in prior years’ unrecognized tax benefits

PwC

• Certain changes in valuation allowances

• Changes in tax laws or rates

• Changes in judgment about unremitted earnings

Current issues in income tax accounting (US GAAP & IFRS)

ASC 740-270 interim reporting

• The annual ETR also includes the effect of valuation allowances on:

- Temporary differences arising in the current year

- Beginning-of-the-year DTAs if attributable to changes in estimatesof the current year’s income (ASC 740-270-30-7)

• The ETR estimate applies to year-to-date ordinary income.

PwC

• The ETR estimate applies to year-to-date ordinary income.

• The ETR estimate excludes

- Jurisdictions with losses and no tax benefit

- Jurisdictions with no reliable estimate

Current issues in income tax accounting (US GAAP & IFRS)

ASC 740-270 interim reporting

• The ETR represents the best estimate of the composite tax provisionin relation to the best estimate of worldwide pretax book ordinaryincome.

• The composite tax provision should include federal, foreign and stateincome taxes, and should reflect anticipated investment tax credits,foreign tax rates, percentage depletion, capital gains rates, and other

PwC

foreign tax rates, percentage depletion, capital gains rates, and otheravailable tax planning alternatives. (ASC 740-270-30-8)

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting – Computation

• Steps to compute the interim tax provision using the annual effectivetax rate

- Determine projected annual taxable income using projected pretaxincome, permanent and temporary differences, credits andcarryforwards for the entire year for each tax component of eachjurisdiction

PwC

jurisdiction

- Compute the tax for the year for each component

- Aggregate the pretax book income and tax expense for the year

- Compute the estimated effective tax rate for the year

- Apply this rate to year-to-date consolidated book ordinaryincome/(loss)

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting – Computation (cont)

• Steps to compute the interim tax provision using the annual effectivetax rate

- Determine the tax impacts of discrete items occurring during theyear-to-date interim period

- Sum the two computed tax amounts to derive income tax for the

PwC

- Sum the two computed tax amounts to derive income tax for theyear-to-date interim period

- Current quarter’s provision = the difference between the year-to-date provision for the current quarter and the previous quarter’syear-to-date provision

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• Exclude from the consolidated annual estimated tax ratecomputation loss jurisdictions for which no benefit can be recognizedon those losses (ASC 740-270-30-36)

• Compute a separate annual estimated rate for each such lossjurisdiction

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Interim reporting

Exercise 2-1

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Changes in valuation allowances

• If realization of deferred tax asset is driven by “future” years’ incomeprojections – the change in valuation allowance is considered a“discrete event” in the quarter as of the date the change incircumstances occurs.

• If realization of deferred tax asset is driven by “current” year’sincome projections – the change in valuation allowance is part of the

PwC

income projections – the change in valuation allowance is part of theannualized effective tax rate computation.

• To apply these rules the deferred tax assets must be divided betweenthose expected to be realized in the current year and those expectedto be realized in future years.

Current issues in income tax accounting (US GAAP & IFRS)

Change in valuation allowance during an interimperiod(FAS 109, ¶193 and ¶194, uncodified)

• Need to segregate the effect of the change into two portions:

1. The amount of the change that relates to the current year

2. The amount of the change that relates to future years

• The first portion is reflected as an element of the effective annual taxrate

PwC

rate

• The second portion is recognized on a discrete basis

Current issues in income tax accounting (US GAAP & IFRS)

Valuation allowances – Release in interim period

Facts: Assume that an enterprise has $3,000,000 of net operating losscarryforwards available at the beginning of year 20X7. At that date, theenacted tax rate was 35%. Because of uncertainty related torealizability, management established a valuation allowance of$1,000,000 at the end of 20X6.

Although the company broke even for the first six months of 20X7, due

PwC

Although the company broke even for the first six months of 20X7, dueto a recent increase in sales orders and firm contracts, the companynow estimates it will have income of $200,000 for the current year, andincome in future years is expected to be sufficient to allow recognitionof the entire deferred tax asset. This will permit a full reversal of thevaluation allowance for NOL carryforwards that existed at thebeginning of the year

Question: How should the reversal be accounted for in Q2 of 20X7?

Current issues in income tax accounting (US GAAP & IFRS)

Changes in tax laws or rates

• Changes impacting deferred taxes - discrete event in the quarter thedate of enactment occurs

• Changes impacting current year taxes payable or receivable –annualized effective tax rate item beginning the first interimreporting period as of the date of new legislation

PwC

• Changes impacting prior year taxes payable or receivable - discreteevent in the quarter in which the date of enactment occurs

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• Reliability of estimates

- When a company operates in a jurisdiction where a "reliableestimate" of the translated effective tax rate cannot be made, ASC740-270-30-36(b) requires the company to exclude the "ordinary"income (or loss) in that jurisdiction and the related tax (or benefit)attributable to “ordinary” income in that jurisdiction from the

PwC

attributable to “ordinary” income in that jurisdiction from theoverall estimate of the ETR and interim period tax (or benefit)

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• ASC 740-270-30-17 states

• Paragraph 740-270-25-3 requires that if an entity is unable toestimate a part of its ordinary income (or loss) or the related tax (orbenefit) but is otherwise able to make a reliable estimate, the tax (orbenefit) applicable to the item that cannot be estimated be reportedin the interim period in which the item is reported.

PwC

in the interim period in which the item is reported.

• ASC 740-270-30-18 further states that if a "reliable estimate" ofthe ETR cannot be made, the actual tax rate for the year-to-date mayrepresent the most appropriate estimate of the annual effective taxrate.

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• These paragraphs make it clear that the effective tax rate approachmust be used to the extent that, but only to the extent that, a reliableestimate can be made.

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• Disclosure considerations:

- The tax effects of significant unusual or infrequent items that arerecorded separately or reported net of their related tax effect (ASC740-270-30-8)

- Significant changes in estimates or provisions for income taxes

PwC

- Significant changes in estimates or provisions for income taxes(ASC 270-10-50-1(d)), e.g., changes during the period in theassessment of the need for a valuation allowance

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting – Disclosure

• ASC 740-270-50-1 states that

Application of the requirements for accounting for income taxes ininterim periods may result in a significant variation in thecustomary relationship between income tax expense and pretaxaccounting income. The reasons for significant variations in thecustomary relationship between income tax expense and pretax

PwC

customary relationship between income tax expense and pretaxaccounting income shall be disclosed in the interim period financialstatements if they are not otherwise apparent from the financialstatements or from the nature of the entity's business.

Current issues in income tax accounting (US GAAP & IFRS)

Interim reporting

• Disclosure considerations

- SAB 74

- Material changes to uncertain tax positions, amounts of uncertaintax benefits that, finalized would affect the effective tax rate, totalamounts of interest and penalties and positions that are expected

PwC

amounts of interest and penalties and positions that are expectedto change within the next 12 months and open tax years.

Current issues in income tax accounting (US GAAP & IFRS)

Questions & Answers

PwCCurrent issues in income tax accounting (US GAAP & IFRS)

Thank you

Sharon Powers

Carolyn Iacobelli

PwC

James Terry

Current issues in income tax accounting (US GAAP & IFRS)

© 2012 PricewaterhouseCoopers LLP. All rights reserved. PwC refers to the United Statesmember firm, and may sometimes refer to the PwC network. Each member firm is a separatelegal entity. Please see www.pwc.com/structure for further details.