Pushing the Innovation Envelope: Strategies for Boosting Productivity and ROI - Kenneth Kaitin,...

40

Pushing the Innovation Envelope Kenneth I Kaitin, PhD Professor and Director Tufts Center for the Study of Drug Development Evolution Summit 2015 Las Vegas, NV, September 20, 2015 Strategies for Boosting Productivity and ROI

-

Upload

marcus-evans -

Category

Business

-

view

1.051 -

download

0

Transcript of Pushing the Innovation Envelope: Strategies for Boosting Productivity and ROI - Kenneth Kaitin,...

Pushing the Innovation Envelope

Kenneth I Kaitin, PhD Professor and Director

Tufts Center for the Study of Drug Development

Evolution Summit 2015 Las Vegas, NV, September 20, 2015

Strategies for Boosting Productivity and ROI

Agenda

• Environment for pharmaceu1cal R&D

• CSDD’s current drug development metrics

• New models of bioinnova1on

The Current Landscape for Pharma Innova6on

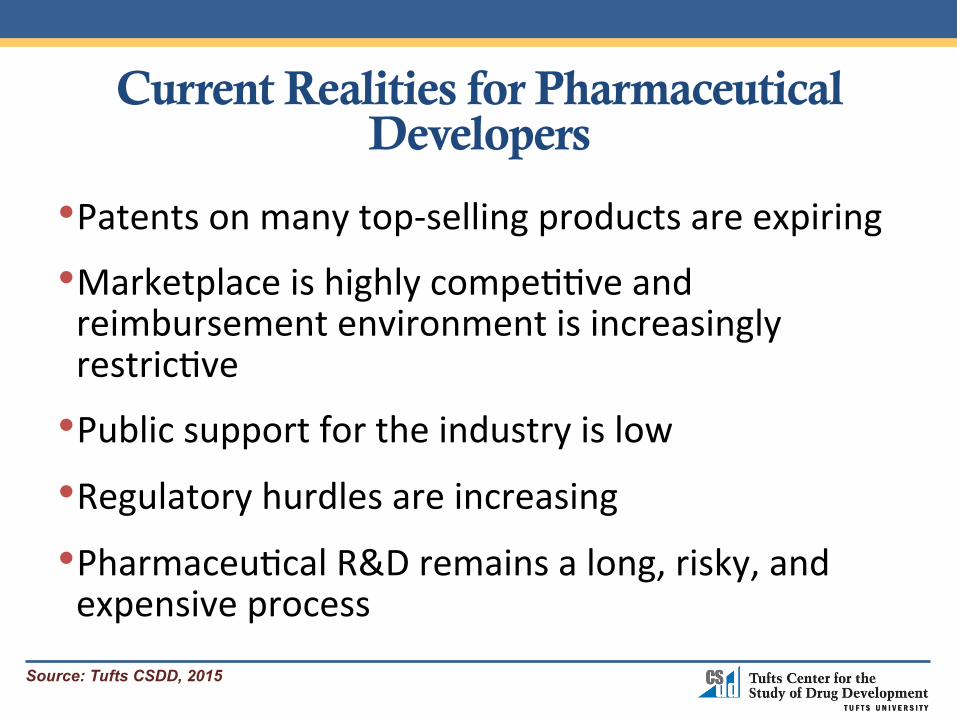

Current Realities for Pharmaceutical Developers

• Patents on many top-‐selling products are expiring

• Marketplace is highly compe11ve and reimbursement environment is increasingly restric1ve

• Public support for the industry is low • Regulatory hurdles are increasing • Pharmaceu1cal R&D remains a long, risky, and expensive process

Source: Tufts CSDD, 2015

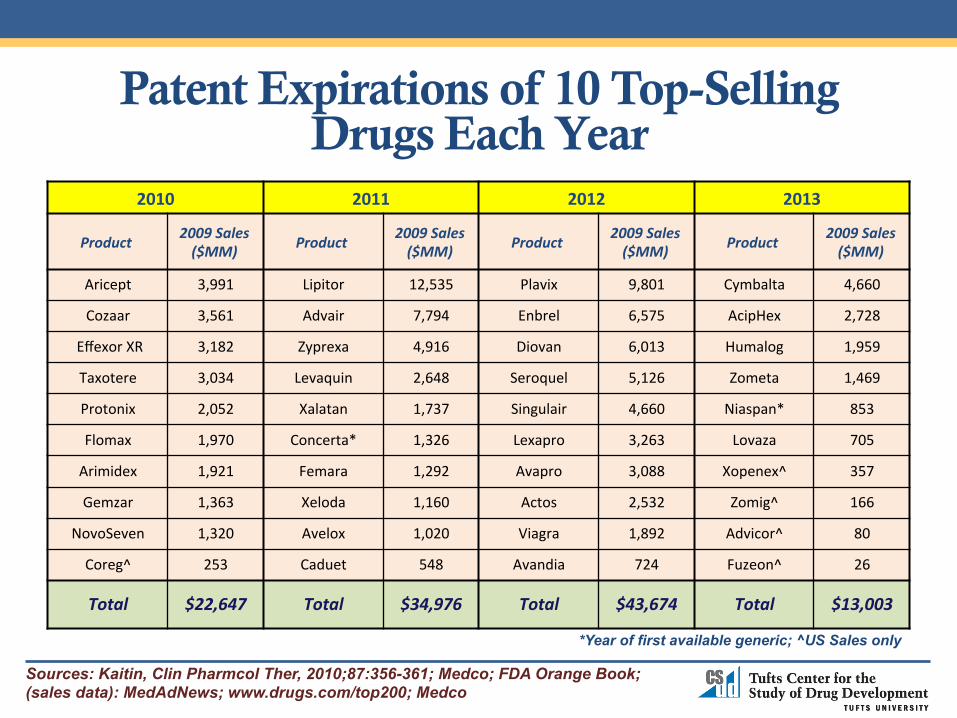

Patent Expirations of 10 Top-Selling Drugs Each Year

2010 2011 2012 2013

Product 2009 Sales ($MM) Product 2009 Sales

($MM) Product 2009 Sales ($MM) Product 2009 Sales

($MM)

Aricept 3,991 Lipitor 12,535 Plavix 9,801 Cymbalta 4,660

Cozaar 3,561 Advair 7,794 Enbrel 6,575 AcipHex 2,728

Effexor XR 3,182 Zyprexa 4,916 Diovan 6,013 Humalog 1,959

Taxotere 3,034 Levaquin 2,648 Seroquel 5,126 Zometa 1,469

Protonix 2,052 Xalatan 1,737 Singulair 4,660 Niaspan* 853

Flomax 1,970 Concerta* 1,326 Lexapro 3,263 Lovaza 705

Arimidex 1,921 Femara 1,292 Avapro 3,088 Xopenex^ 357

Gemzar 1,363 Xeloda 1,160 Actos 2,532 Zomig^ 166

NovoSeven 1,320 Avelox 1,020 Viagra 1,892 Advicor^ 80

Coreg^ 253 Caduet 548 Avandia 724 Fuzeon^ 26

Total $22,647 Total $34,976 Total $43,674 Total $13,003

Sources: Kaitin, Clin Pharmcol Ther, 2010;87:356-361; Medco; FDA Orange Book; (sales data): MedAdNews; www.drugs.com/top200; Medco

*Year of first available generic; ^US Sales only

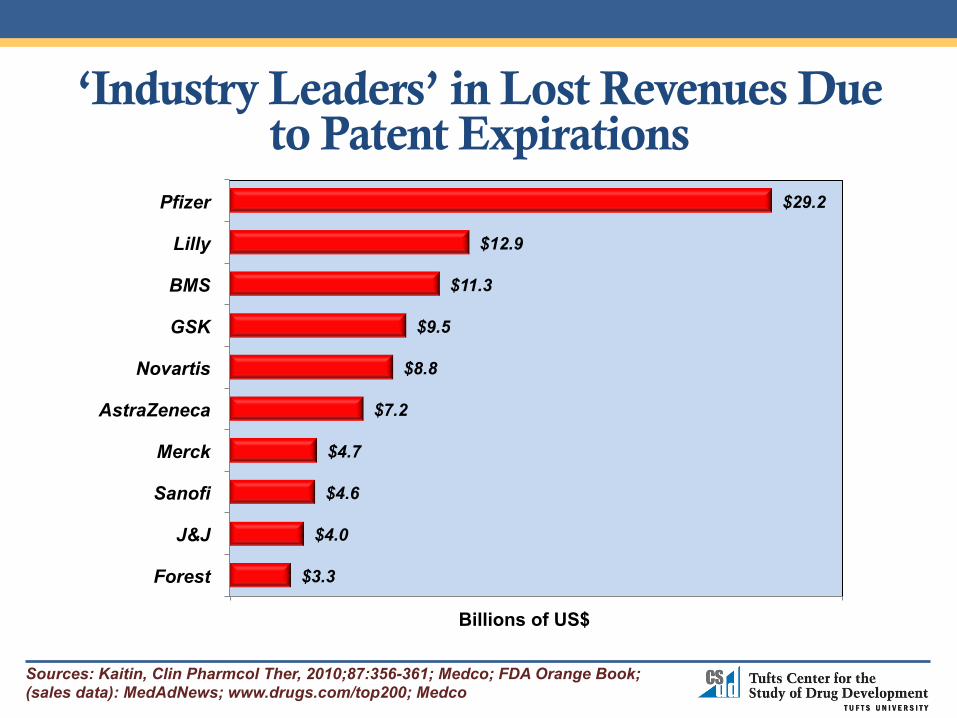

‘Industry Leaders’ in Lost Revenues Due to Patent Expirations

$3.3

$4.0

$4.6

$4.7

$7.2

$8.8

$9.5

$11.3

$12.9

$29.2

Forest

J&J

Sanofi

Merck

AstraZeneca

Novartis

GSK

BMS

Lilly

Pfizer

Billions of US$

Sources: Kaitin, Clin Pharmcol Ther, 2010;87:356-361; Medco; FDA Orange Book; (sales data): MedAdNews; www.drugs.com/top200; Medco

Blockbuster Patent Expirations, 2014-16 Year Brand Generic Company Indication Sales

($BB)*

2014 Nexium Esomeprazole Astra Zeneca GERD 4.5

Cymbalta Duloxitine Eli Lilly Depression, anxiety, nerve pain 4.2

Symbicort Budesonide/Formoterol Astra Zeneca Asthma, COPD 3.1

Celebrex Celecoxib Pfizer Arthritis, acute pain 2.5

Evista Raloxifine Eli Lilly Osteoporosis 1.4

Sandostatin Octreotide Novartis Acromegaly syndrome 1.4

Actonel Risedronate Warner Chilcott Osteoporosis 1.1

2015 Abilify Aripiprazole Otsuka Schizophrenia, bipolar disorder 5.2

Gleevec Imatinib mesylate Novartis Chronic myeloid leukemia (CML) 4.7

Copaxone Glatiramer Teva Multiple sclerosis 3.6

Namenda Memantine Forest Alzheimer's disease 1.4

Zyvox Linezolid Pfizer Antiviral 1.3

Prezista Darunavir Janssen HIV 1.3

Provigil Modofinil Teva Excessive sleepiness 1.2

Avodart Dutasteride GlaxoSmithkline Benign prostatic hyperplasia (BPH) 1.2

Combivent Albuterol/Ipratropium Boehringer Ingelheim COPD 1.1

2016 Crestor Rosuvastatin calcium Astra Zeneca Hypercholesterolemia 7.1

Benicar Olmesartan medoxomil Daiichi Sankyo Hypertension 2.6

Source: EvaluateGroup.com, 2014 * 2011 Global Sales

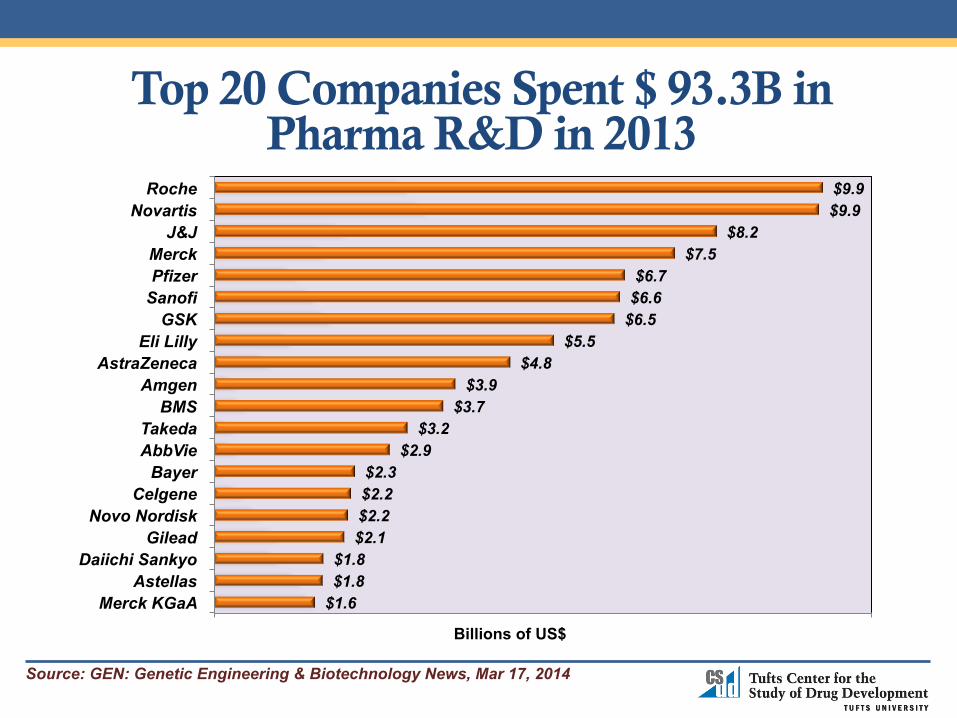

Top 20 Companies Spent $ 93.3B in Pharma R&D in 2013

$1.6 $1.8 $1.8

$2.1 $2.2 $2.2 $2.3

$2.9 $3.2

$3.7 $3.9

$4.8 $5.5

$6.5 $6.6 $6.7

$7.5 $8.2

$9.9 $9.9

Merck KGaA Astellas

Daiichi Sankyo Gilead

Novo Nordisk Celgene

Bayer AbbVie Takeda

BMS Amgen

AstraZeneca Eli Lilly

GSK Sanofi Pfizer Merck

J&J Novartis

Roche

Billions of US$

Source: GEN: Genetic Engineering & Biotechnology News, Mar 17, 2014

Source: Tufts CSDD, 2015; R&D expenditures from PhRMA

New Drug and Biologic Approvals Are Not Keeping Pace with Rising R&D Costs

0

14

28

42

56

0

14

28

42

56

1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

R&

D Expenditures

(Billions of 2013$)

NM

E/N

BE

App

rova

ls

* Trend line is 3-year moving average; R&D expenditure adjusted for inflation

R&D Expenditures

New Approvals

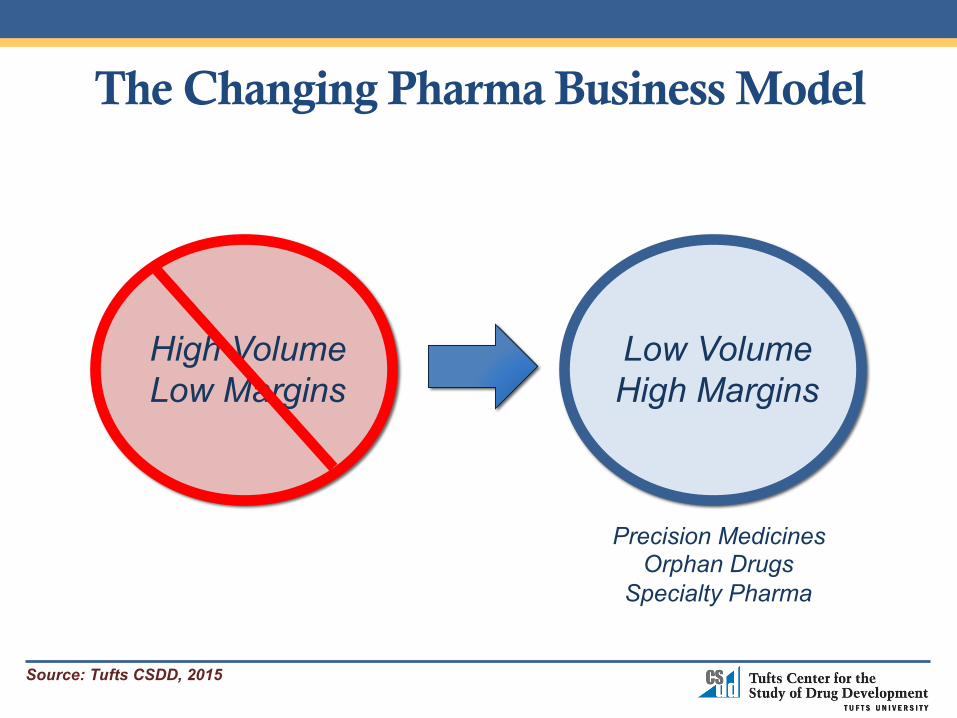

The Changing Pharma Business Model

Source: Tufts CSDD, 2015

High Volume Low Margins

Low Volume High Margins

Precision Medicines Orphan Drugs

Specialty Pharma

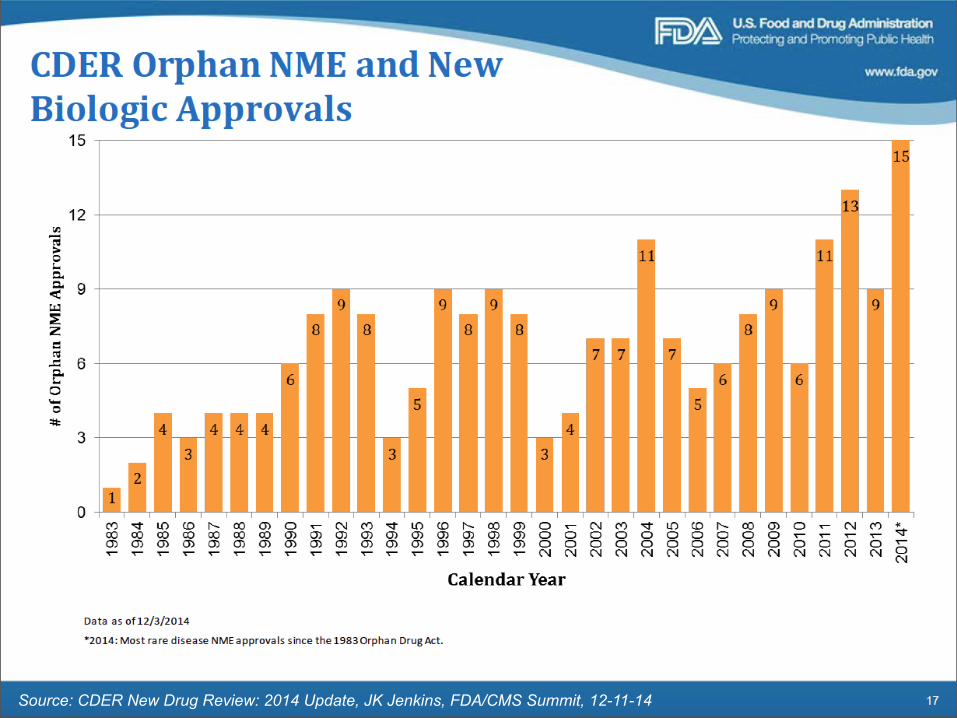

Source: CDER New Drug Review: 2014 Update, JK Jenkins, FDA/CMS Summit, 12-11-14

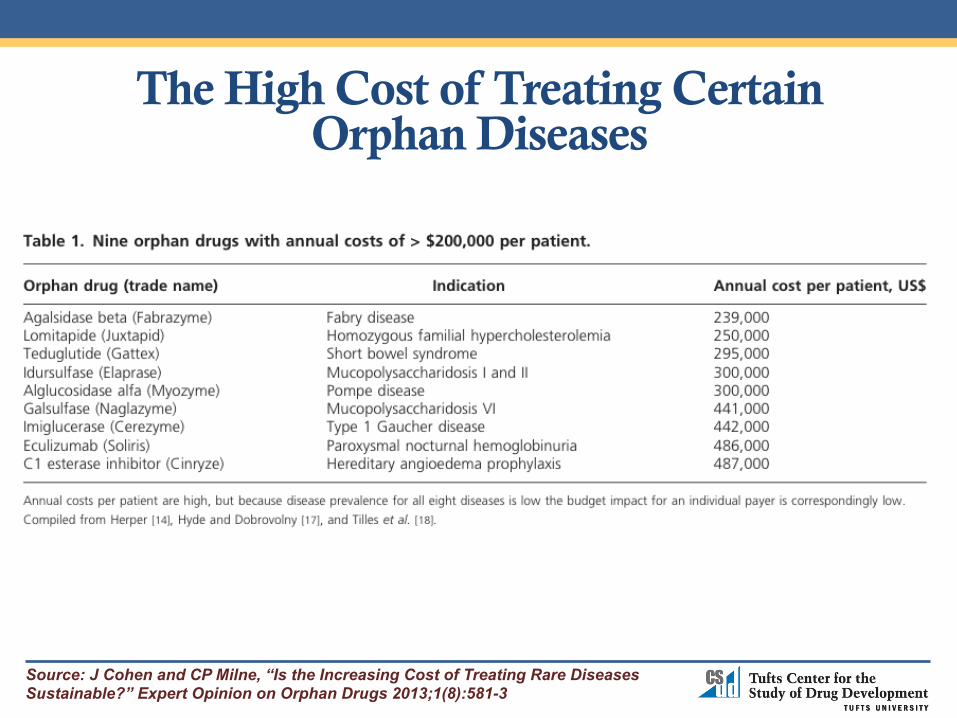

The High Cost of Treating Certain Orphan Diseases

Source: J Cohen and CP Milne, “Is the Increasing Cost of Treating Rare Diseases Sustainable?” Expert Opinion on Orphan Drugs 2013;1(8):581-3

Bringing a New Drug to Market: Current TuNs CSDD Drug Development Metrics

Source: Tufts CSDD, 2015

0 10

AIDS Antiviral

Anti-infective*

Immunologic

Cardiovascular

Antineoplastic

Gastrointestinal

Endocrine

Respiratory

CNS

5.9

6.0

7.4

7.4

7.5

7.7

7.8

8.3

8.7

0.9

0.8

1.2

1.6

0.6

0.9

1.0

1.6

1.0

Years

Clinical Phase Approval Phase

Clinical and Approval Times Vary Across Therapeutic Classes, 2010-14

* Anti-infective excludes AIDS antivirals

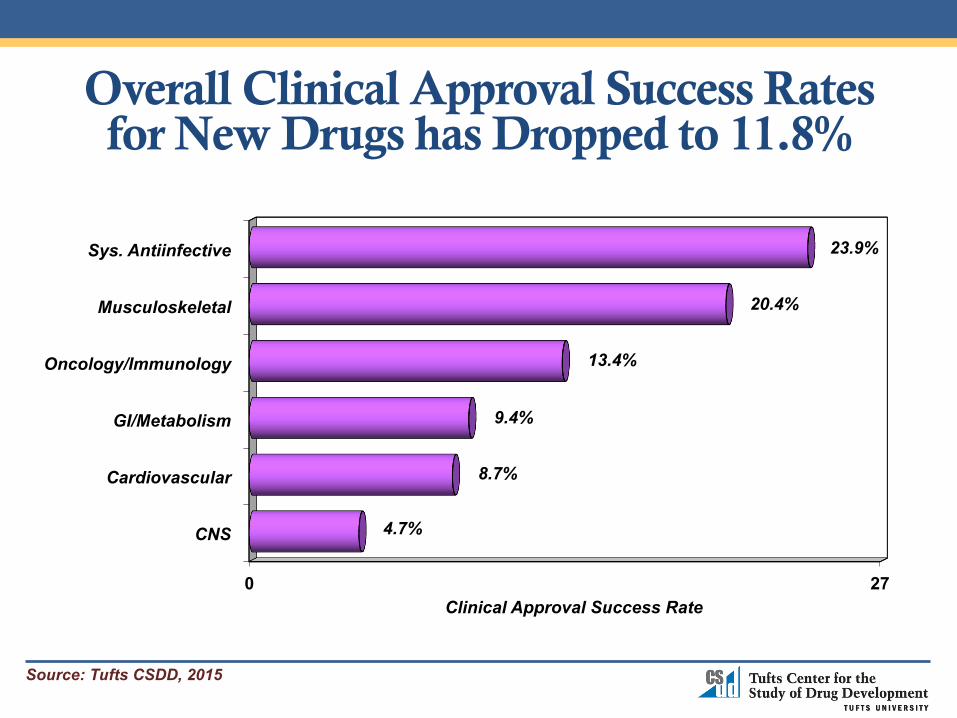

Overall Clinical Approval Success Rates for New Drugs has Dropped to 11.8%

0 27

CNS

Cardiovascular

GI/Metabolism

Oncology/Immunology

Musculoskeletal

Sys. Antiinfective

4.7%

8.7%

9.4%

13.4%

20.4%

23.9%

Clinical Approval Success Rate

Source: Tufts CSDD, 2015

72%

35%

80%

71%

49%

55%

68%

35%

50%

63%

32%

64% 60%

33%

46%

58% 52%

79%

0

100

Phase 1-2 Phase 2-3 Phase 3-Subm

Tran

sitio

n Pr

obab

ility

Musculoskeletal Onc/Immunologic GI/Metabolic Cardiovascular CNS Syst Antiinfective

Phase Transition Probabilities by Therapeutic Class

Source: DiMasi et al, Clin Pharmacol Ther, 2010;87:272-277

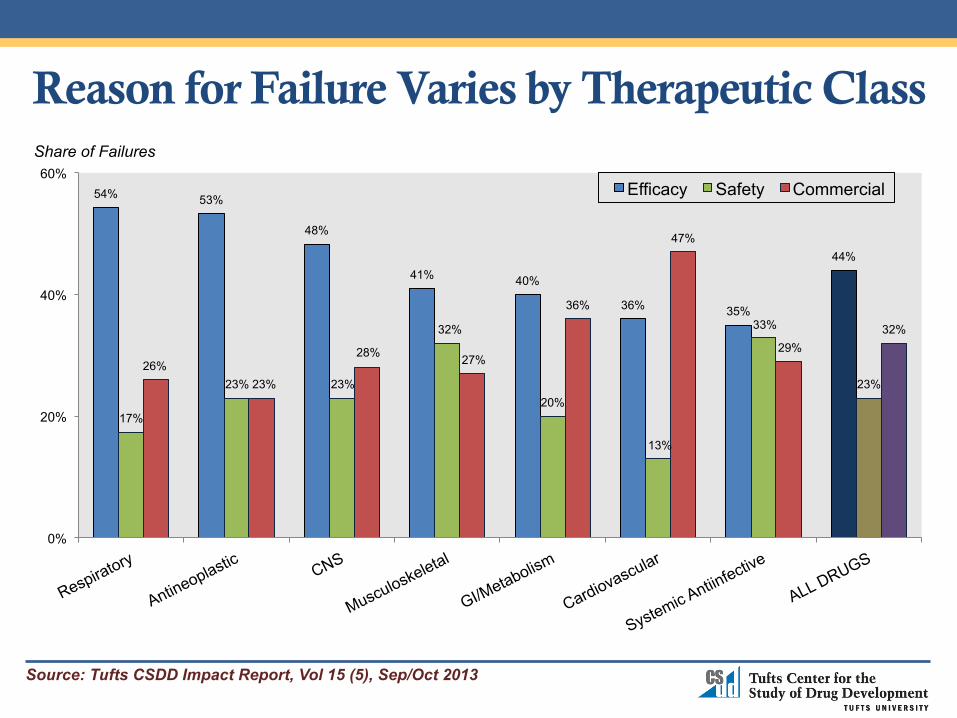

54% 53%

48%

41% 40%

36% 35%

44%

17%

23% 23%

32%

20%

13%

33%

23% 26%

23%

28% 27%

36%

47%

29% 32%

0%

20%

40%

60% Efficacy Safety Commercial

Share of Failures

Source: Tufts CSDD Impact Report, Vol 15 (5), Sep/Oct 2013

Reason for Failure Varies by Therapeutic Class

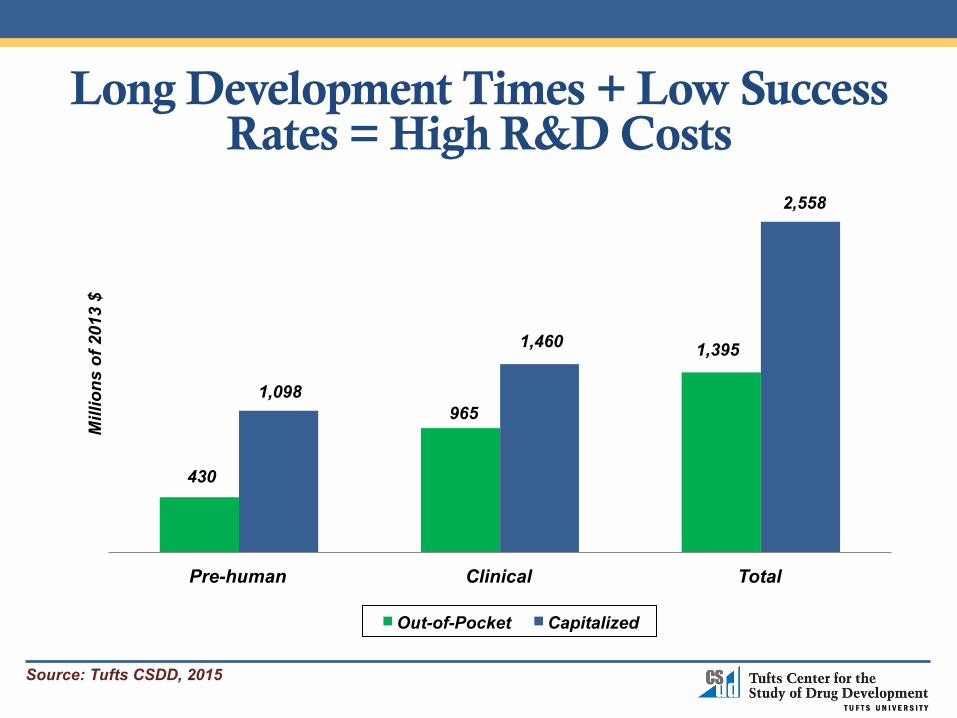

Long Development Times + Low Success Rates = High R&D Costs

Source: Tufts CSDD, 2015

430

965

1,395

1,098

1,460

2,558

Pre-human Clinical Total

Mill

ions

of 2

013

$

Out-of-Pocket Capitalized

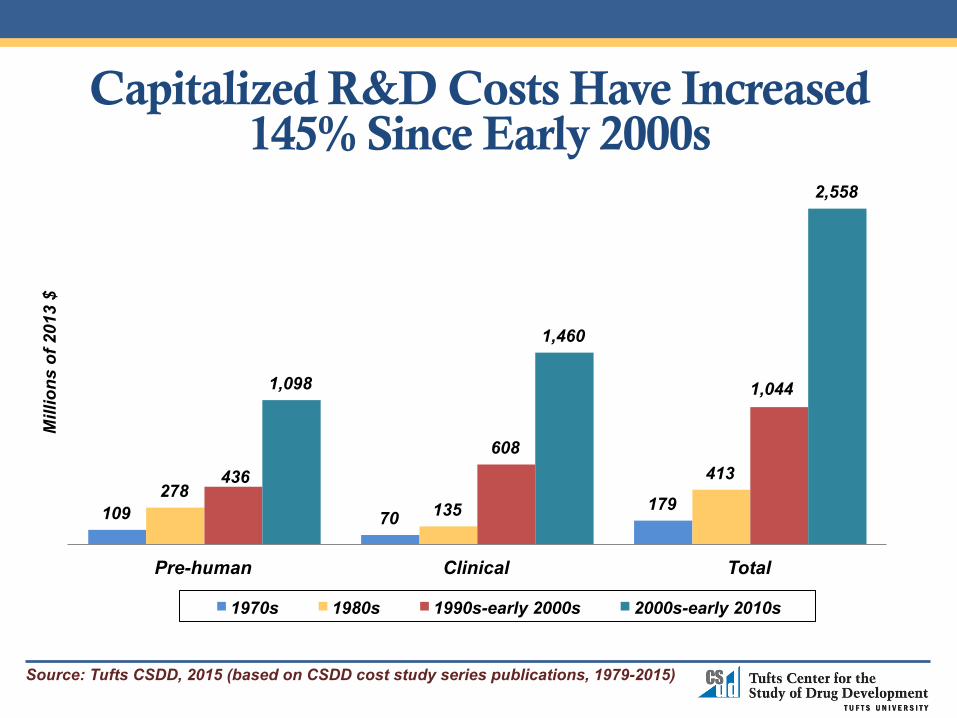

Capitalized R&D Costs Have Increased 145% Since Early 2000s

Source: Tufts CSDD, 2015 (based on CSDD cost study series publications, 1979-2015)

109 70 179

278 135

413 436 608

1,044 1,098

1,460

2,558

Pre-human Clinical Total

Mill

ions

of 2

013

$

1970s 1980s 1990s-early 2000s 2000s-early 2010s

Source: Tufts CSDD, 2015

Drivers of High Development Costs

• Poor preclinical screens and predic1ve models • Chronic and complex indica1ons • Clinical trial size • Pa1ent recruitment/reten1on • Increased protocol complexity • Regulatory demands • Commercial demands

Source: Tufts CSDD, 2015

Typical Phase III Protocol 2002 2012

Scientific Total Number of Endpoints 7 13

Total Number of Procedures 106 167

Total Number of Eligibility Criteria 31 50

Average Number of Major Amendments 2.3 3.6

Proportion of ‘Non-Core’ Procedures 18% 31%

Operating Total Number of Countries 11 34

Total Number of Investigative Sites 124 196

Total Number of Patients Randomized 729 597

Total Number of Data Points Collected 494,236 929,203

Increase over Plan Timeline to Reach LPLV 28% 73%

Protocol Complexity is Increasing

Source: Tufts CSDD, 2015; *Medidata Solutions

Source: Tufts CSDD, 2015

Portfolio Decision-Making Grid

Oncology

CNS

Cardiovascular

Infectious Disease

Medical Need

Competitive Landscape

Technical Challenge

Exploitable Science

Compounds in Development by Therapeutic Area: Oncology Leads

Source: EvaluatePharma® (3 May 2012)

Oncology 31%

Systemic Intiinfectives 15%

Central Nervous System 14%

Cardiovascular 7%

Musculoskeletal 5%

Endocrine 5%

Gastrointestinal 4%

Respiratory 4%

Dermatology 3%

Sensory Organs 3%

Genito-Urinary 3% Blood 3%

Other 4%

Trends in New Drug and Biologics Approvals Within Four Largest Therapeutic Class

Source: Tufts CSDD, 2015

0% 10% 20% 30% 40% 50% 60% 70%

2010-13

2000-09

1990-99

1980-89

Share of US New Drug Approvals

Anti-infective* Antineoplastic Cardiovascular CNS

* Anti-infective excludes AIDS antivirals

Source: Tufts CSDD, 2015

How to Stimulate Innovation in Areas with High Medical Need but Low Investment

Appeal and/or High Technical Risk

• Legisla1ve and regulatory push/pull ini1a1ves, such as BTD, priority vouchers and market exclusivity

• Establish public support by making disease area a na1onal priority: e.g., “War on Cancer”, AIDS, Ebola, White House BRAIN Ini1a1ve

• Invest in basic research • Foster strategic partnerships and integrated alliances

The Bioinnova6on Landscape is Changing

Strategies Driving Development Performance

1990-1999 2000-2009 2010-present

Operating Changes

• Project Management

• Procurement/Cost-containment

• Globalization • Downsizing/

Consolidation

• Downsizing and Consolidation

• Flexible and virtual workplaces

Alliances • M&As • Public-private

partnerships • Transactional

Outsourcing

• M&As • In-Licensing and

Joint Ventures • Functional

service outsourcing

• M&As • In-Licensing, JVs • Public-private

partnerships • Precompetitive

alliances • Integrated outsourcing

Technologies • Rapid screening • Combinatorial

chemistry • EDC and IVRS

• -Omics • eClinical Trial

Solutions (e.g., CTMS)

• Platform technologies • Companion

diagnostics • Integrated Big Data • Social media • Mobile health

Source: Tufts CSDD, 2015

Transforming R&D Strategy: Innovation Partnerships

u Academic-Industry: (‘upstream/TR focus’) e.g., PFEs-CTIs; J&J Innovation Centers, LLY-Lilly Innovation Fellowship Awards; ADDCs

u Multi-Stakeholder Consortia and PPPs: e.g., ADNI (26 partners); Enlight Biosciences (8 cos); TransCelerate BioPharma (18); IMI; MS Outcome Assessments Consortium; Coalition Against Major Diseases (CAMD)

u Outsourcing providers: (virtual) LLY-Chorus; (functional) LLY-Covance/Advion; BMS-Accenture; AZN-(API)

u Patient groups: e.g., VRTX-CFF; Breast Cancer Alliance; Lupus Foundation; Michael J. Fox Foundation

u Payer-Industry

u VC partnerships

u Open innovation and Crowdsourcing: e.g., LLY-Open Innovation Drug Discovery; Transparency Life Sciences

Source: Tufts CSDD, 2015

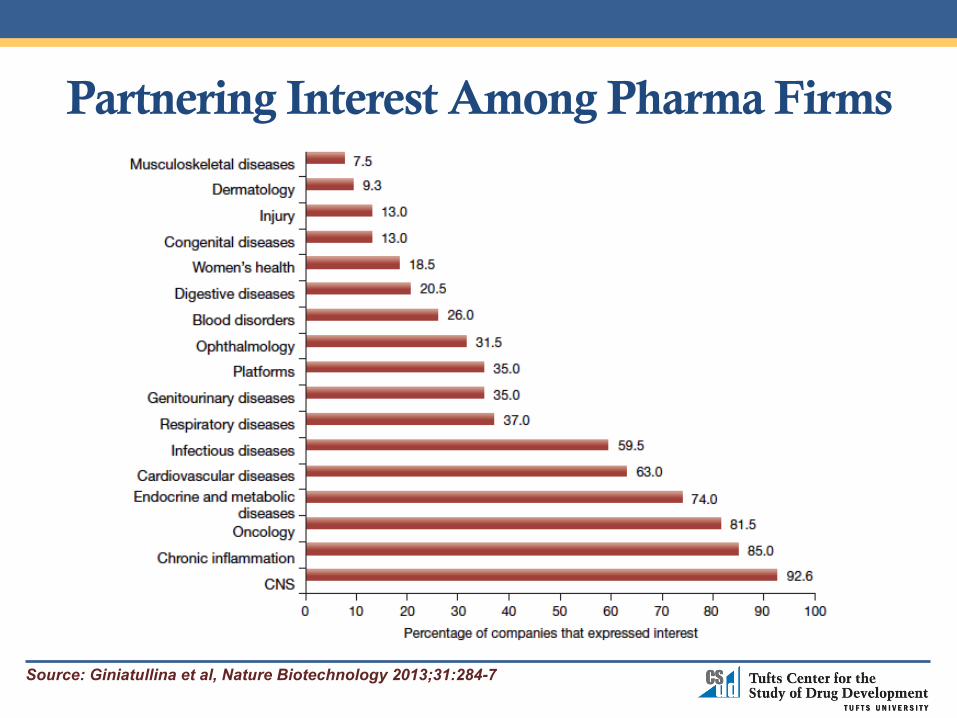

Source: Giniatullina et al, Nature Biotechnology 2013;31:284-7

Partnering Interest Among Pharma Firms

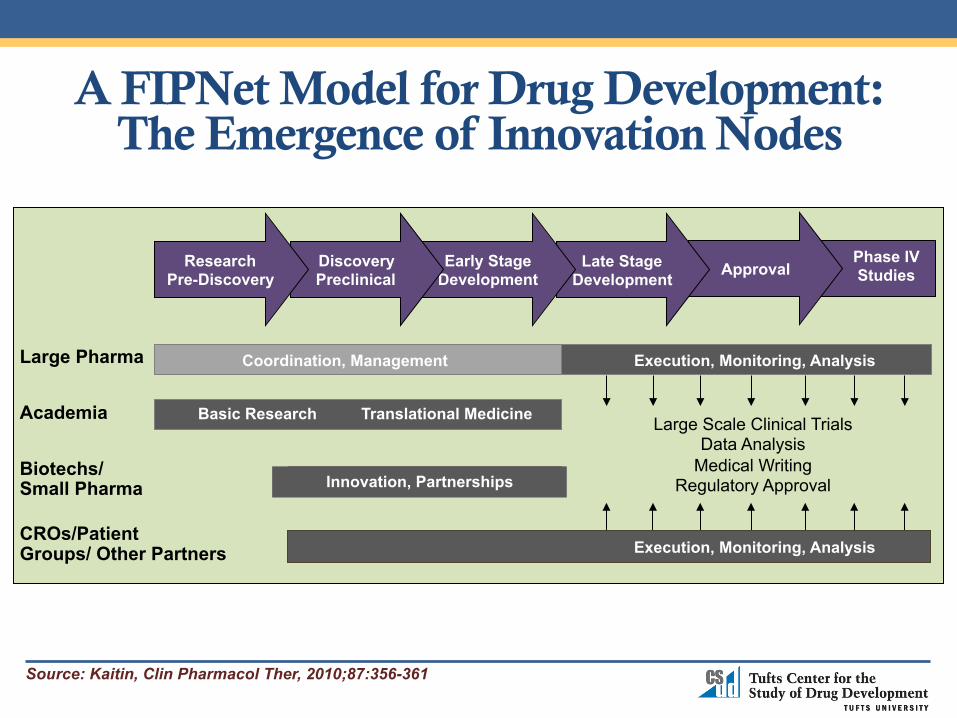

A FIPNet Model for Drug Development: The Emergence of Innovation Nodes

Phase IV Studies Approval Late Stage

Development Early Stage

Development Discovery Preclinical

Research Pre-Discovery

Large Pharma Academia

Biotechs/ Small Pharma CROs/Patient Groups/ Other Partners

Basic Research Translational Medicine

Execution, Monitoring, Analysis

Innovation, Partnerships

Coordination, Management Execution, Monitoring, Analysis

Large Scale Clinical Trials Data Analysis

Medical Writing Regulatory Approval

Source: Kaitin, Clin Pharmacol Ther, 2010;87:356-361

Source: Tufts CSDD, 2015

Lupus

Innovation Nodes: 21st Century Bioinnovation

Type 2 Diabetes

Alzheimer’s Disease Accelerating Medicines

Partnerships

Government • NIH • FDA

Founda6ons • American Diabetes Assoc • Alzheimers Assoc • Founda1on of NIH • Geoffrey Bean Founda1on • Lupus Founda1on of America

• Rheumatology Research Founda1on

• USAgainstAlzheimers

Companies • Abbvie • BiogenIdec • BMS • GSK • J&J

• Eli Lilly • Merck • Pfizer • Sanofi • Takeda

Rheumatoid Arthritis

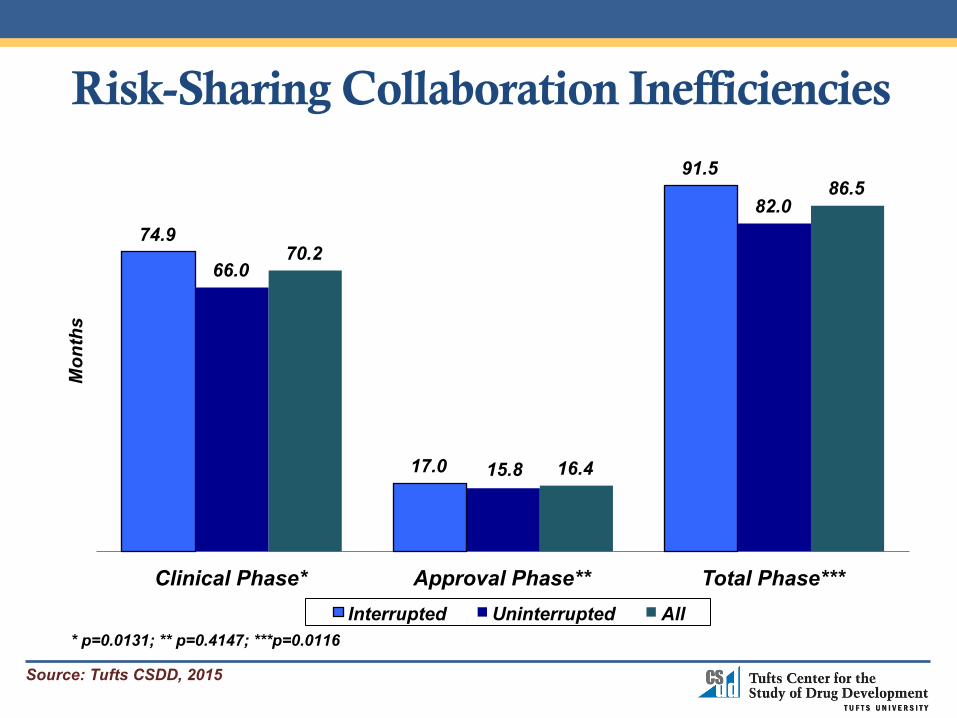

Risk-Sharing Collaboration Inefficiencies

Source: Tufts CSDD, 2015

74.9

17.0

91.5

66.0

15.8

82.0

70.2

16.4

86.5

Clinical Phase* Approval Phase** Total Phase***

Mon

ths

Interrupted Uninterrupted All * p=0.0131; ** p=0.4147; ***p=0.0116

Characteristics of Top-Performing Strategic Partnerships

Source: Tufts CSDD, 2015

• High level of partner specializa1on • Shared governance and opera1ng risk • Integrated systems, SOPs, processes

• Sophis1cated planning and coordina1on • More efficient interac1ons

• Faster engagement

• Innova1ve ideas

Bottom Line: Integrated strategic partnerships allow stakeholders to spread risk and leverage knowledge and resources, offering the best hope of finding new treatments for many unmet medical needs.

Source: Tufts CSDD, 2015

Tufts Center for the Study of Drug Development Tufts University, Boston, Massachusetts, USA

Email [email protected]

Website http://csdd.tufts.edu

Kenneth I Kaitin, PhD Professor and Director Tufts University School of Medicine

For more information about theFor more information about the marcus evans Pharma

S it iSummits series: [email protected]