Purchasing and Supply Chain Management by W.C....

56

Purchasing and Supply Chain Management by W.C. Benton Chapter Sixteen Equipment Acquisition and Disposal McGraw-Hill/Irwin Copyright © 2010 The McGraw-Hill Companies. All Rights Reserved.

Transcript of Purchasing and Supply Chain Management by W.C....

Purchasing and Supply Chain Managementby W.C. Benton

Chapter SixteenEquipment Acquisition and

Disposal

McGraw-Hill/Irwin Copyright © 2010 The McGraw-Hill Companies. All Rights Reserved.

Learning Objectives

1. To identify the issues in the capital equipment acquisition process.

2. To identify the various steps in the capital equipment acquisition process.

3. To learn the three criteria applied to a cash flow analysis for equipment acquisition.

4. To learn how an economic evaluation is accomplished.

16-2

Learning Objectives

5. To discuss the role purchasing plays in capital equipment acquisitions.

6. To explain the evaluation criteria for selection.

7. To learn about life cycle costing.

8. To learn how to evaluate lease-versus-buy decisions.

16-3

Acquisition of Capital Equipment and Assets

• The acquisition of capital equipment is a major decision in most firms.

• ______________________________________ ______________________________________.

• The tax planning process is also a significant component of this decision.

• ______________________________________ ______________________________________ ______________________________________.

16-4

Equipment Buying

• ______________________________________ ______________________________________ ______________________________________.

• Most of the equipment costs are pegged to industry norms.– Sometimes it is more cost-effective to buy the

equipment at an auction than some of the more traditional sources.

• ______________________________________ ______________________________________ ______________________________________.

16-5

Acquisition of Capital Equipment

• The acquisition of capital equipment involves the allocation and commitment of funds. – ______________________________________

______________________________________ ______________________________________.

• The timing of these capital acquisition decisions is critical to the financial health of a firm. – ______________________________________

______________________________________ ______________________________________.

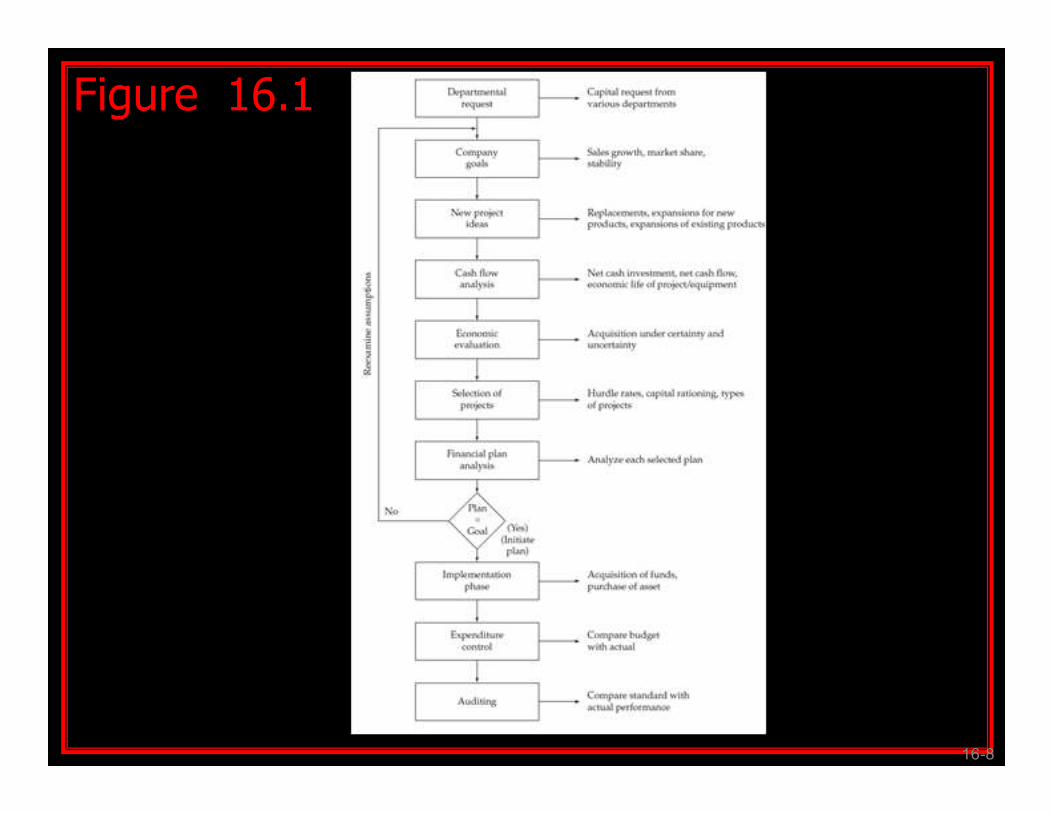

• In Figure 16.1, a generic capital equipment acquisition process is presented. __________________________ ______________________________________.

16-6

Acquisition of Capital Equipment

• Long-term investment decisions are usually driven by the tax effect of acquiring equipment now rather than later. ______________________________________.

• Each cross-functional step is a subsystem of the entire process, which is closely related to a variety of other subsystems.– A Department of Defense information technology

example is given in Appendix 16.A.

16-7

16-8

Figure 16.1

Departmental Requisition• The capital acquisition process is initiated with a department requesting equipment replacements and expansions.– ______________________________________

______________________________________.

• The requisition process is sometimes initiated by a “wish list,” low-cost projection, or special appropriation for major acquisitions. – ______________________________________

______________________________________.

• As an example, IBM places a limit of $25,000 for general acquisitions. – ______________________________________

______________________________________. 16-9

Typical Policies

• Typical policies might allow a department to purchase computer equipment or a compressor in the regular course of business whereas a request for an automobile or tractor would have to first be recommended by the plant manager or superintendent.

• ______________________________________.

16-10

16-11

Company Goals and Objectives

• The next step in the process is to compare the acquisition request with the overall long-run objectives of the firm.

• ______________________________________.

• The objectives of the company are important because the purchase of any major equipment will probably affect the capacity and the methods of the company for many years in the future.

• Company goals _______________________________ ______________________________________ ______________________________________.

16-12

New Project Ideas

• The classification of the various capital equipment requests must be based on certain common characteristics.

• Although equipment classification varies from company to company, capital projects are frequently grouped according to the following categories:– ______________________________________– ______________________________________– ______________________________________– ______________________________________– ______________________________________– ______________________________________

16-13

Replacements and Expansion

• The replacement of old equipment ________________ ______________________________________ ______________________________________. – The company can easily do an in-depth cost savings and

efficiency study.

• Companies on a growth pattern fueled by technologyacquire new equipment to expand into a newly introduced product line. Investment in capital equipment for expansion purposes should increase incremental revenue.

– ______________________________________ ______________________________________.

• Expanding existing equipment is also a way to increase output. The other categories of capital investment revolve around the plant, facilities, and construction.

16-14

New Construction

• As an example, the capital acquisition process for construction projects must follow a well designed process of specification, construction bid process, contractor selection, and the actual construction phase.

• ______________________________________ ______________________________________.

• The construction acquisition ____________________ ______________________________________ ______________________________________.

• ______________________________________ ______________________________________.

16-15

Cash-Flow Analysis

• If a capital equipment request survives the new project ideas step, cash-flow estimates must be considered for each capital investment idea.

• ______________________________________ ______________________________________ ______________________________________.

Three criteria should apply to the cash-flow analysis:– ______________________________________.– ______________________________________.– ______________________________________.

16-16

Net Cash Flow

• Net cash flows are _______________________ ______________________________________.

• ______________________________________ ______________________________________.

• The economic life of the project versus the physical life of the project also must also be considered.

16-17

Life Cycle Costing

• The U.S. Department of Defense uses a concept called “life cycle costing.” Life cycle costing is an evaluation method used to evaluate alternative capital acquisition based on the total cost of the equipment over the expected life of the product.

• The total cost components are given below:1. ______________________________________2. ______________________________________3. ______________________________________ 4. ______________________________________5. ______________________________________

16-18

Life Cycle Costing

• There are numerous testimonials _________________ ______________________________________.

• Consider a trucking firm that currently spends an average of $363 per month to maintain each vehicle. Recently the firm purchased 10 trucks by competitive bidding using the life cycle costing concept. The average monthly maintenance cost for the new trucks is $195 per unit for the life of the vehicles.

• The ease and cost of operating costs also will have a significant effect on the capital acquisition. ______________________________________ ______________________________________.

16-19

Economic Evaluation

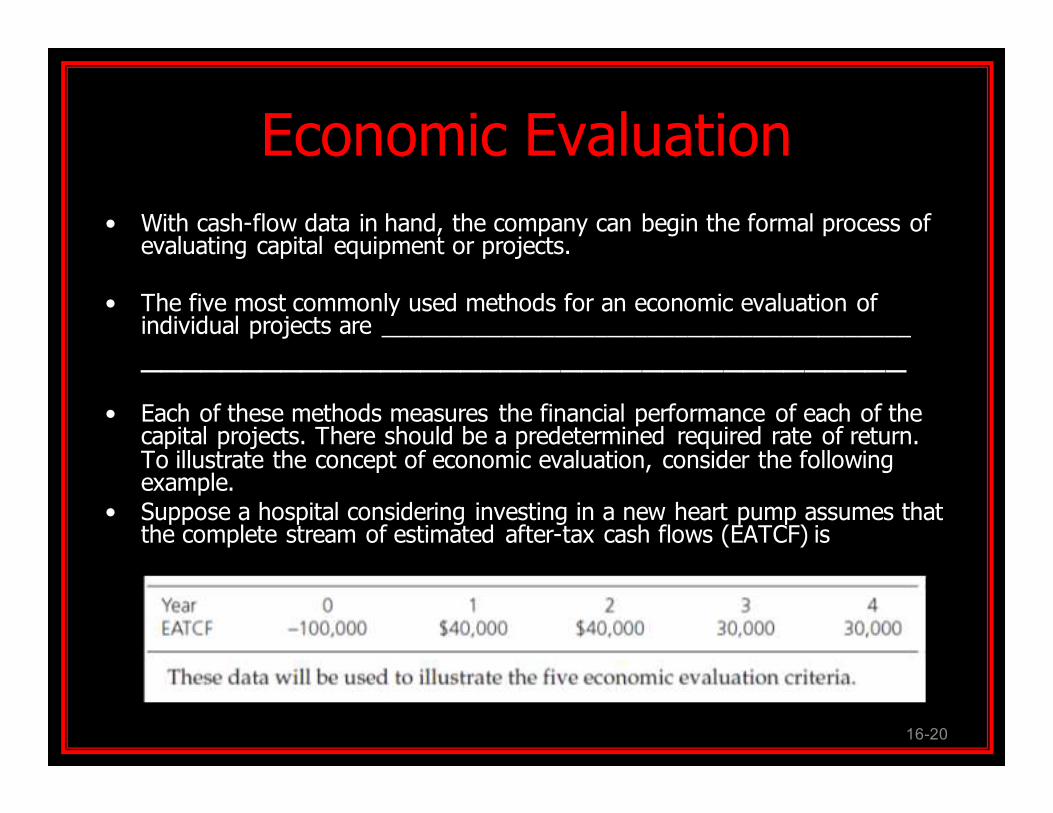

• With cash-flow data in hand, the company can begin the formal process of evaluating capital equipment or projects.

• The five most commonly used methods for an economic evaluation of individual projects are ________________________________________

______________________________________

• Each of these methods measures the financial performance of each of the capital projects. There should be a predetermined required rate of return. To illustrate the concept of economic evaluation, consider the following example.

• Suppose a hospital considering investing in a new heart pump assumes that the complete stream of estimated after-tax cash flows (EATCF) is

16-20

Payback Method

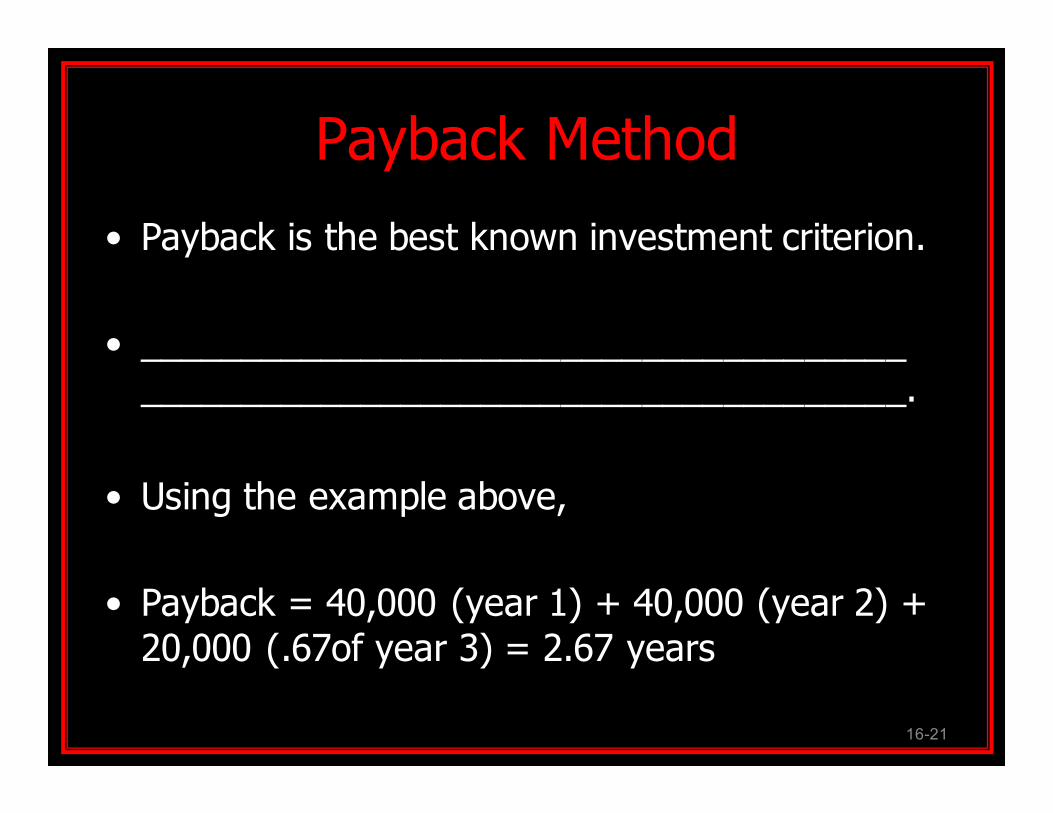

• Payback is the best known investment criterion.

• ______________________________________ ______________________________________.

• Using the example above,

• Payback = 40,000 (year 1) + 40,000 (year 2) + 20,000 (.67of year 3) = 2.67 years

16-21

Average Rate of Return

• ____________________________________________________________________________ :

Average rate of return =ARR = (∑EATCF/Economic life)/Initial investment

ARR = [(40,000 + 40,000 + 30,000 + 30,000)/4]/100,000= 35 percent

• If ARR > the required ARR, accept project.• If ARR < the required ARR, reject project.

• This method ignores timing of the cash flows: What if most of the $140,000 in the example problem was all lumped into one year? The ARR would still be 35 percent.

• ______________________________________.16-22

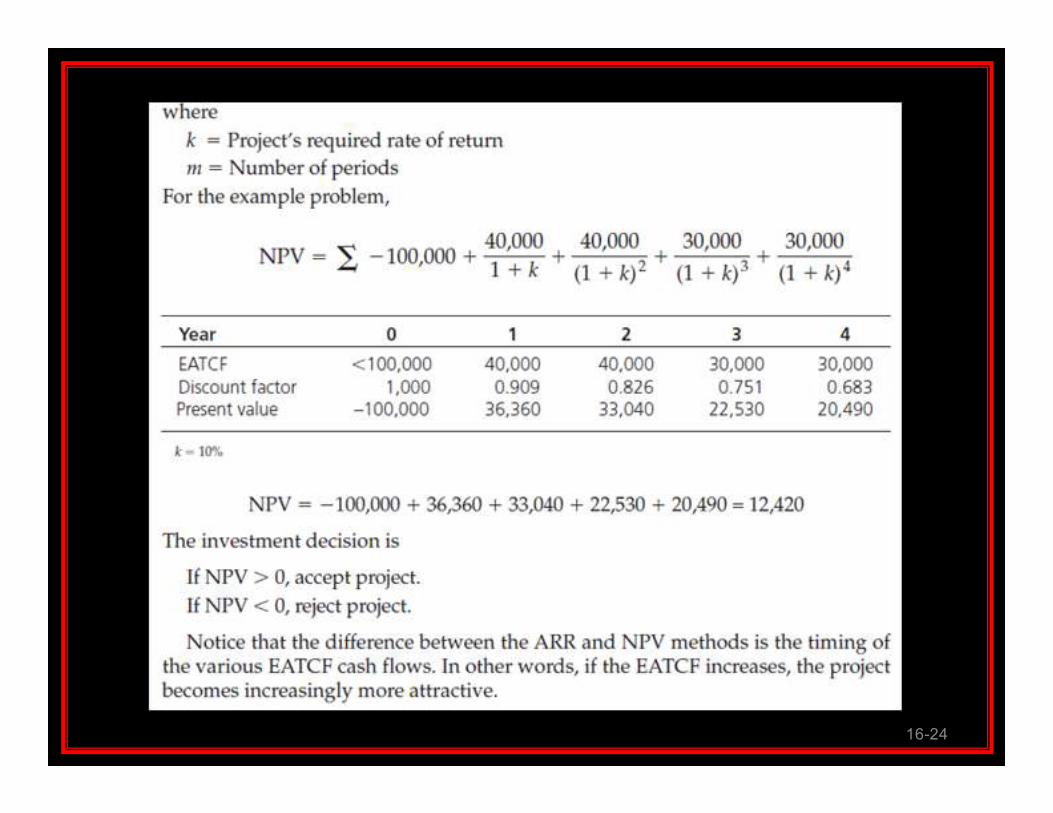

Net Present Value

• ______________________________________ ______________________________________ ______________________________________ ______________________________________.

• Net present value is concerned with netting the initial investment, which is negative, and the present value of the subsequent EATCF, most of which are usually positive.

NPV =

• Where k = Project’s required rate of return

• For the example problem, m=number of periods

16-23

∑=

+

m

t

tk

0)(1

EATCF

16-24

Internal Rate of Return (IRR)

• ______________________________________ ______________________________________ ______________________________________.

• On the other hand if the cost of capital is greater than the IRR, the project has a negative NPV.

• The IRR will give the same answer as the NPV. The IRR is defined as the discount rate that will make the NPV of the project equal zero.

= 0

16-25

∑=

+

m

t

t

0)IRR(1

EATCF

16-26

16-27

Profitability Index

Selection

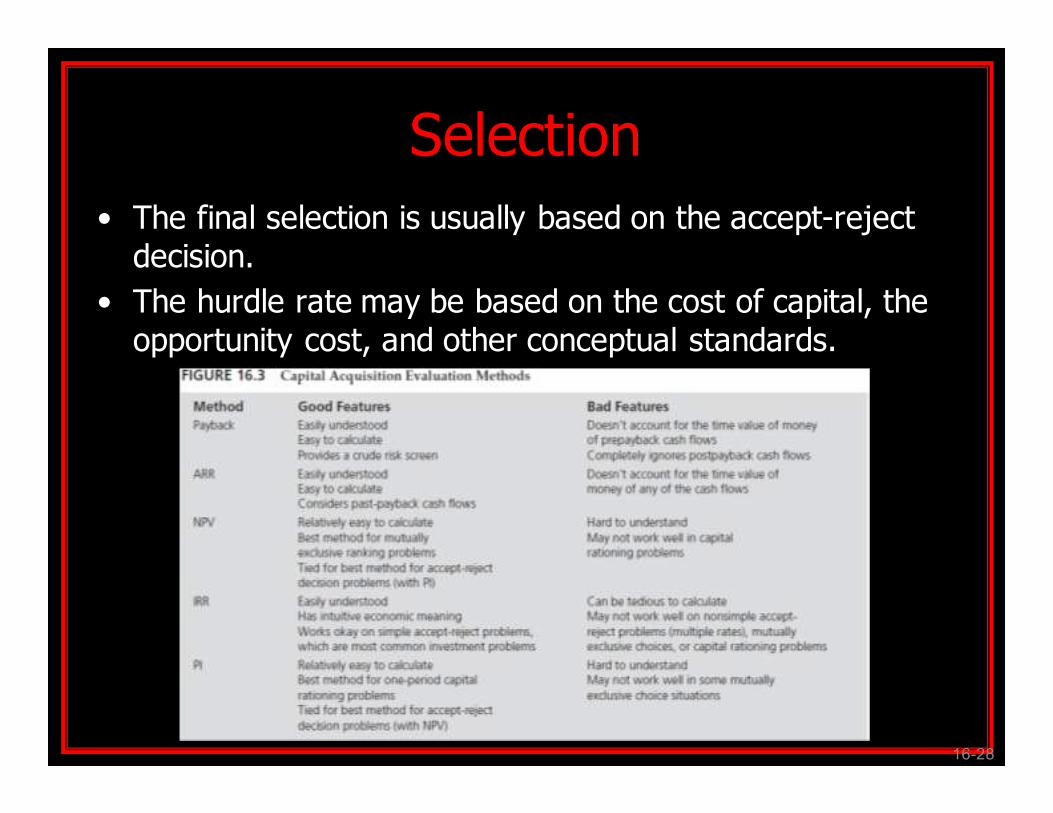

• The final selection is usually based on the accept-reject decision.

• The hurdle rate may be based on the cost of capital, the opportunity cost, and other conceptual standards.

16-28

Financial Plan Analysis• At this stage, a comprehensive comparison of the

selected alternatives is performed. ______________________________________ ______________________________________ ______________________________________.

• For the purpose of the purchasing professional, two methods will be considered:______________________ ______________________________________. The leasing method has been become very popular in the last 20 years and can be used to finance nearly any kind of fixed asset. ________________________________ ____________________________________________________________________________ :

16-29

Leasing vs. Buying

Effects on future financing. __________________ ______________________________________ ______________________________________.

• There is also a positive balance sheet effect of leasing simply because the lease is not considered a debt or an asset.

• A leasing arrangement can actually increase a firm’s borrowing capacity.

• ______________________________________ ______________________________________ ______________________________________.

16-30

The Tax Effect

• Tax effect. ______________________________ ______________________________________ ______________________________________.

• ______________________________________ ______________________________________.

• When a firm leases land for its operations, it can easily deduct the lease expense for the income burden. __________________________________ ______________________________________ ______________________________________.

16-31

Risk of Obsolescence

• Risk of obsolescence. In the case of fast-moving technology, it is possible for the lessee to shift the risk level to the lessor. ______________________________________ ______________________________________ ______________________________________.

16-32

Salvage Value

• Salvage value. _________________________ ______________________________________.

• If expected salvage value is high for leased equipment, the cost of ownership to the lessee may be lower. ______________________________________ ______________________________________ ______________________________________ ______________________________________.

16-33

Maintenance

• Maintenance. _________________________ ______________________________________ ______________________________________.

• If the lessor assumes the costs of maintenance, insurance, and taxes, it will usually pass the expense to the lessee in the form of increased lease payments.

16-34

Discount Rate

• Discount rate. _________________________ ______________________________________.

• Both leasing and buying involve cash outflow over an extended period.

• Since the lease payment is fixed and other costs associated with the lease ______________________________________ ______________________________________ ______________________________________ ______________________________________.

16-35

Types of Leases

There are three types of leases:

1. Sales and leaseback arrangements. The buyer-lessee obtains the title to the property and pays rent. _____________________

______________________________________.

2. Operating lease. The operating lease makes it possible for a company to use assets such as computers, trucks, automobiles, and furniture. In this type of agreement, the lessor maintains and services the equipment. _________________________________

______________________________________ ______________________________________.

3. Capital lease. ________________________________________

______________________________________ ______________________________________.

16-36

Lease versus Borrow and Purchase

• ______________________________________ ______________________________________.

• There is a tax advantage if the leasing company has a high tax liability; thus, buying equipment and leasing it to contractors is a profitable business.

• ______________________________________ ______________________________________ ______________________________________.

16-37

• ____________________________________________________________________________.

• The approval process usually ends with the board of trustees. This stage in the process is basically a rubber stamp.

• The time between approval of the capital and completion of the acquisition is the critical scheduling stage.

• ______________________________________ _____________________________________.

16-38

EXPENDITURE CONTROLIMPLEMENTATION

Audits

• ______________________________________ ______________________________________.

• The entire project should be audited to analyze the differences.

• ______________________________________ ______________________________________.

• ______________________________________ ______________________________________.

16-39

Disposal of Capital Equipment

• The disposal of capital equipment is becoming more complicated. _______________________ ______________________________________ ______________________________________.

• The purchasing function is usually charged with the task of scrapping or selling retired equipment.

• In some cases, _________________________ ______________________________________ ______________________________________.

16-40

Purchasing New Versus Used Capital Equipment

• Despite today’s competitive markets, it may not be cost-effective to procure new equipment.

• ______________________________________ ______________________________________ ______________________________________.

• In this section, the guidelines for purchasing new versus used equipment will be established.

16-41

New Equipment Purchases

• ______________________________________ ______________________________________.

• The buying firm must first determine the number of hours per year the equipment will be employed.

• The buyer must be careful to pay close attention to the theoretical usage levels of certain equipment.

• ______________________________________ ______________________________________ ______________________________________. – Most construction equipment is usually purchased new.

16-42

New Equipment Purchases

• ______________________________________ ______________________________________ ______________________________________.

• ______________________________________ ______________________________________ ______________________________________.

• In the case of computers, copiers, and other high-tech products, it may be more cost-effective to purchase new equipment.– However, if an older model is adequate for the

expected use, significant savings could occur.

16-43

Used Equipment Purchases• Low cost is usually the only reason to buy used

equipment.

• ______________________________________ ______________________________________.

• ______________________________________.

• In some cases, used equipment may provide a good short-term solution to a company’s production problems.

• ______________________________________ ______________________________________.

16-44

Used Equipment Purchases

• ______________________________________.

• ______________________________________.

• As we all know, used car dealers are experts when it comes to cleaning and painting severely damaged vehicles. _______________________ ______________________________________.

– The selling terms are usually “as is” and net cash with no warranty.

16-45

Lease versus Borrow and Purchase Example

• When does it make more sense to buy equipment? When does it make more sense to lease?

• ______________________________________ ______________________________________.

• ______________________________________ ______________________________________.

• There is a tax advantage if the leasing company has a high tax liability; thus, buying equipment and leasing it to contractors is a profitable business.– Since the equipment still must be used in the construction

industry, the company leases the equipment it owns to contractors.

16-46

Lease versus Borrow and Purchase Example

• On the other hand, many contractors have higher after-tax costs for buying capital equipment than those faced by the leasing company, allowing the leasing company to pass some of its savings on to contractors and still make a profit.

• ______________________________________ _____________________________________.

• The following lease-versus-buy method can be used to compare

1. ______________________________________, 2. ______________________________________

3. ______________________________________.16-47

Lease versus Borrow and Purchase

The following example shows how to use these steps. A trucking contractor has two choices:

(1) buy a new tri-axle dump truck or

(2) lease it for three years. The dump truck has a useful life of five years and costs $100,000. The Helpful Bank is willing to loan the contractor $88,000 at 7 percent interest and requires a down payment of $12,000 and annual payments of $20,891, which are due at the end of each of the next five years.

16-48

Additional Data for the Example

• Since the contractor does not have the proper facilities, the bank will require the contractor to sign a maintenance contract with ACME Mack Trucks.

• The contract, good for five years of maintenance, requires annual payments of $5,000. ACME made the contractor a proposal that competes with the bank’s offer.

• ACME is willing to lease the contractor the same dump truck for three years. Since the contractor’s cash situation is very tight, ACME structured the lease with the $30,917 payment due at the end of each year.

16-49

Step 1: Comparing Purchase Price and Lease Payments

• _________________________________________________________

________________________________________________________.

16-50

Step 2: Comparing Income Tax Effect

• ______________________________________ ______________________________________.

• Since the value of these tax benefits varies greatly among individuals and corporations, it is important to calculate potential tax benefits on an individual basis.

• ______________________________________ ______________________________________.

• Using this rule, a $10,000 tax deduction is worth nothing if the tax rate is 0 percent, $1,500 at 16 percent, and $2,800 at 28 percent.

• The situation is relatively simple with leases. Each lease payment is a tax deduction for the company leasing the equipment. ______________________________________ ______________________________________.

16-51

Step 2: Comparing Income Tax Effect• If the buy option is chosen, depreciation on a tractor must be taken

over a five-year period. ______________________________________

_______________________________________________________________

• In this example, straight-line depreciation of $20,000 for each of five years will be used. The example contractor has a 40 percent tax rate, so the tax savings will be

16-52

Step 2: Comparing Income Tax Effect

• Tax savings = 40 percent*(Interest payment + Depreciation + Maintenance)

If the lease option is chosen, the tax savings wouldcalculate as follows:

• Tax savings (years 1–3) = 40 percent*Lease payment

• Tax savings (years 4 and 5) = 40 percent*(Lease payment + Depreciation + Maintenance)

• The table from step 1 can now be rewritten to include taxes, as shown below:

16-53

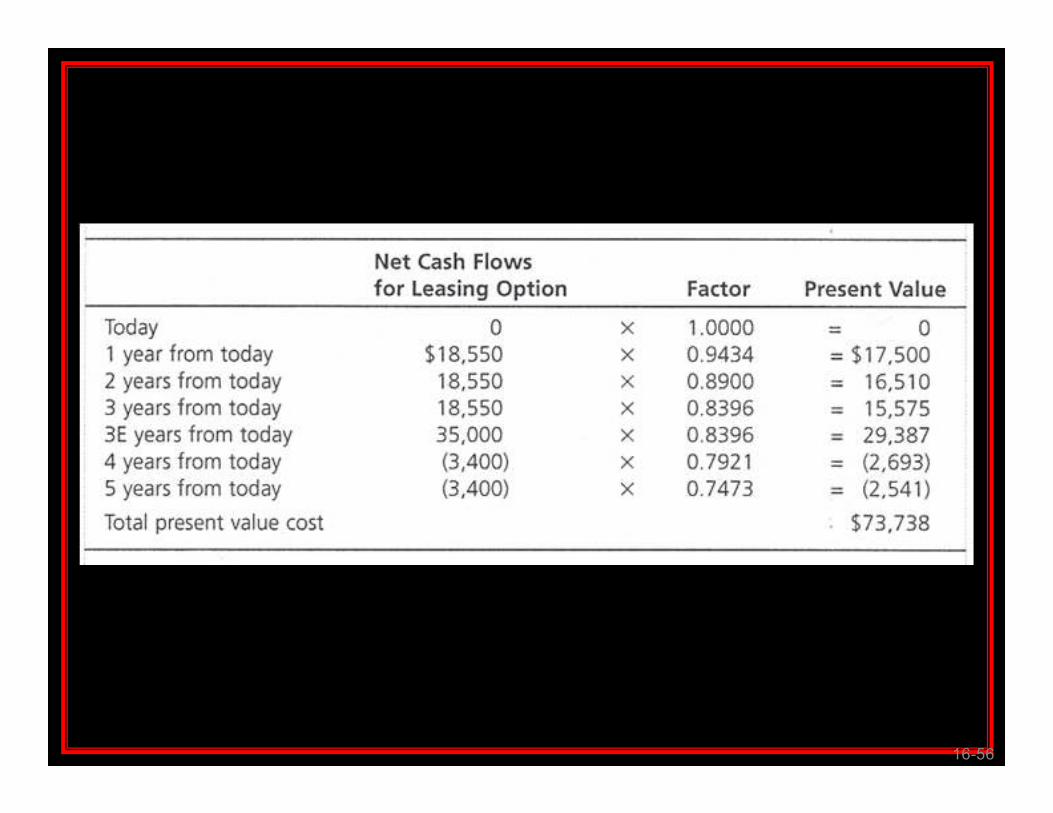

Step 3: Comparing Present Values

• The after-tax values of the leasing and buying costs have been considered, but the time at which these costs are incurred has not been taken into account.

• ______________________________________ ______________________________________.

• ______________________________________ ______________________________________ ______________________________________ ______________________________________.

16-54

16-55

16-56