Purchase and Material Management -...

137

Purchase and Material Management

Transcript of Purchase and Material Management -...

Purchase and Material Management

I/JNU OLE

Index

ContentI. ......................................................................II

List of FiguresII. .........................................................VI

List of TablesIII. ........................................................VII

AbbreviationsIV. .....................................................VIII

Case StudyV. ..............................................................116

BibliographyVI. ........................................................124

Self Assessment AnswersVII. ...................................127

Book at a Glance

II/JNU OLE

Contents

Chapter I ....................................................................... ...............................................................................1Material Management ................................................................................................................................. 1Aim ....................................................................... ........................................................................................ 1Objectives ....................................................................... .............................................................................. 1Learning outcome .......................................................................................................................................... 11.1 Introduction to Material Management ..................................................................................................... 21.2 Classification of Inventory .......................................................................................................................21.3 Meaning of Material Management ...........................................................................................................31.4 Objectives of Material Management ........................................................................................................41.5 Motives of Material Management ............................................................................................................41.6 Scope of Material Management ...............................................................................................................51.7 Material Planning .....................................................................................................................................51.8 Technique of Planning Materials ............................................................................................................. 51.9 Process of Codification ............................................................................................................................61.10 Standardisation .......................................................................................................................................71.11 Scheduling .............................................................................................................................................81.12 Procurement .......................................................................................................................................... 81.13 Purchasing .............................................................................................................................................81.14 Inspection ..............................................................................................................................................91.15 Quality Control ..................................................................................................................................... 91.16 Packaging ..............................................................................................................................................91.17 Storage ....................................................................... ........................................................................... 91.18 Inventory Control ................................................................................................................................101.19 Distribution ......................................................................................................................................... 101.20 Disposal ............................................................................................................................................... 101.21 Functions of Material Manager ............................................................................................................101.22 Effects of Over Stocking and Under Stocking ....................................................................................10Summary ....................................................................... ..............................................................................11References ....................................................................... ............................................................................11Recommended Reading ..............................................................................................................................11Self Assessment ...........................................................................................................................................12

Chapter II ....................................................................... ........................................................................... 14Material Cost Management ...................................................................................................................... 14Aim ....................................................................... ...................................................................................... 14Objectives ....................................................................... ............................................................................ 14Learning outcome ........................................................................................................................................ 142.1 Introduction to Material Cost Management ...........................................................................................152.2 Material Cost ..........................................................................................................................................152.3 Economic Order Quantity (EOQ) Models ............................................................................................. 172.4 Determination of Various Inventory Levels ..........................................................................................19 2.4.1 Maximum Level ....................................................................................................................20 2.4.2 Minimum Level ..................................................................................................................... 20 2.4.3 Re-order Level ....................................................................................................................... 20 2.4.4 Danger Level ..........................................................................................................................20 2.4.5 Calculation of Various Levels ...............................................................................................202.5 ABC Analysis ........................................................................................................................................232.6 XYZ Analysis ........................................................................................................................................ 25Summary ....................................................................... .............................................................................27References ....................................................................... ...........................................................................27Recommended Reading .............................................................................................................................27Self Assessment ...........................................................................................................................................28

III/JNU OLE

Chapter III ....................................................................... ..........................................................................30Material Requirements Planning ............................................................................................................. 30Aim ....................................................................... ...................................................................................... 30Objectives ....................................................................... ............................................................................ 30Learning outcome ........................................................................................................................................ 303.1 Introduction ............................................................................................................................................313.2 Definition of MRP ................................................................................................................................. 313.3 System Components............................................................................................................................... 323.4 Demand Dependency .............................................................................................................................333.5 Objectives of MRP .................................................................................................................................333.6 Advantages of MRP ............................................................................................................................... 343.7 Limitations of MRP ............................................................................................................................... 353.8 Evaluation of MRP .................................................................................................................................353.9 Keeping MRP Current in a Changing Environment .............................................................................. 353.10 Manufacturing Resource Planning (MRP II) .......................................................................................363.11 JIT ....................................................................... ............................................................................... 363.12 KANBAN ............................................................................................................................................ 36Summary ....................................................................... .............................................................................38References ....................................................................... ...........................................................................38Recommended Reading .............................................................................................................................38Self Assessment ...........................................................................................................................................39

Chapter IV ....................................................................... ..........................................................................41Introduction to Enterprise Resource Planning (ERP) ............................................................................41Aim ....................................................................... ...................................................................................... 41Objectives ....................................................................... ............................................................................ 41Learning outcome ........................................................................................................................................ 414.1 Introduction ............................................................................................................................................424.2 History and Evolution ............................................................................................................................424.3 Meaning ....................................................................... ........................................................................ 434.4 Definition ............................................................................................................................................... 434.5 Concept ....................................................................... .......................................................................... 434.6 Implementation of an ERP System ........................................................................................................ 444.7 Advantages of ERP ................................................................................................................................ 444.8 Disadvantages of ERP ............................................................................................................................454.9 Applicability of ERP .............................................................................................................................. 454.10 Reasons for the Growth of the ERP Market ........................................................................................ 464.11 Success of the ERP ...............................................................................................................................46Summary ....................................................................... .............................................................................47References ....................................................................... ...........................................................................47Recommended Reading .............................................................................................................................47Self Assessment ...........................................................................................................................................48

Chapter V ....................................................................... ............................................................................50Inventory Models ....................................................................................................................................... 50Aim ....................................................................... ...................................................................................... 50Objectives ....................................................................... ............................................................................ 50Learning outcome ........................................................................................................................................ 505.1 Introduction to Inventory Models .......................................................................................................... 515.2 Models for Accepting/Rejecting Discounts on Purchases ..................................................................... 515.3 Fixed Order vs. Fixed Interval System .................................................................................................. 55 5.3.1 Cyclical Ordering or Fixed Period System (Time Based) .................................................... 555.4 Material Requirement Planning (MRP) ................................................................................................60 5.4.1 Applicability of the MRP System .......................................................................................... 61 5.4.2 Inputs for MRP ..................................................................................................................... 61

IV/JNU OLE

5.4.3 MRP Process ..........................................................................................................................61 5.4.4 Outputs of MRP .................................................................................................................... 61 5.4.5 Benefits of MRP ................................................................................................................... 625.5 Inventory Turnover ............................................................................................................................... 62 5.5.1 Interpretation of Inventory Turnover ..................................................................................... 63Summary ....................................................................... .............................................................................64References ....................................................................... ...........................................................................64Recommended Reading .............................................................................................................................64Self Assessment ...........................................................................................................................................65

Chapter VI ....................................................................... ..........................................................................67Purchase Management .............................................................................................................................. 67Aim ....................................................................... ...................................................................................... 67Objectives ....................................................................... ............................................................................ 67Learning outcome ........................................................................................................................................ 676.1 Introduction to Purchase Management .................................................................................................. 68 6.1.1 Objectives of Material Management ......................................................................................686.2 Functions of Purchase Department ........................................................................................................ 68 6.2.1 Purchasing Function vs. Purchase Department .....................................................................69 6.2.2 Procurement vs. Purchasing ..................................................................................................70 6.2.3 Objectives of Purchasing ....................................................................................................... 706.3 Purchase Requisition ..............................................................................................................................70 6.3.1 Types of Purchase Requisitions ............................................................................................. 706.4 Purchase Procedure ...............................................................................................................................716.5 Types of Purchasing ..............................................................................................................................71 6.5.1 Forward Buying .................................................................................................................... 71 6.5.2 Tender Buying ........................................................................................................................72 6.5.3 Systems Contract .................................................................................................................. 73 6.5.4 Speculative Buying ...............................................................................................................74 6.5.5 Rate Contracts .......................................................................................................................74 6.5.6 Reciprocity in Buying ...........................................................................................................74 6.5.7 Zero Stock Buying ................................................................................................................75 6.5.8 Blanket Orders ...................................................................................................................... 756.6 Vendor Management ............................................................................................................................. 756.7 Inspection of Materials .......................................................................................................................... 76 6.7.1 Pre Dispatch Inspection ......................................................................................................... 76 6.7.2 Stage Inspection/Final Inspection ..........................................................................................77 6.7.3 Document Inspection ............................................................................................................. 77 6.7.4 Stores/Receipt Inspection ...................................................................................................... 77 6.7.5 Third Party Inspection............................................................................................................ 77Summary ....................................................................... .............................................................................80References ....................................................................... ...........................................................................80Recommended Reading .............................................................................................................................81Self Assessment ...........................................................................................................................................82

Chapter VII ....................................................................... ........................................................................ 84Stores Management.................................................................................................................................... 84Aim ....................................................................... ...................................................................................... 84Objectives ....................................................................... ............................................................................ 84Learning outcome ........................................................................................................................................ 847.1 Introduction to Stores Management .......................................................................................................85 7.1.1 Motive to Hold Inventory ...................................................................................................... 857.2 Functions of Stores Department ............................................................................................................85 7.2.1 Receipt of Material ................................................................................................................ 85 7.2.2 Issue of Material .................................................................................................................... 86

V/JNU OLE

7.2.3 Return of Material ..................................................................................................................87 7.2.4 Transfer of Materials ..............................................................................................................88 7.2.5 Proper Storage Function ........................................................................................................ 887.3 Valuation of Material ............................................................................................................................ 907.4 Valuation of Receipts ............................................................................................................................. 907.5 Valuation of Issues ................................................................................................................................. 91 7.5.1 First In First Out (FIFO) Method ..........................................................................................92 7.5.2 Last In First out (LIFO) Method ...........................................................................................93 7.5.3 Highest In First Out (HIFO) Method .....................................................................................94 7.5.4 Average Rate Method ............................................................................................................95 7.5.4.1 Simple Average (SAR) Method ..............................................................................95 7.5.4.2 Weighted Average Rate (WAR) Method ................................................................. 96 7.5.5 Market Rate ............................................................................................................................977.6 Valuation of Returns .............................................................................................................................. 98Summary ....................................................................... ...........................................................................100References ....................................................................... .........................................................................100Recommended Reading ...........................................................................................................................100Self Assessment .........................................................................................................................................101

Chapter VIII .............................................................................................................................................103Quality Management ............................................................................................................................... 103Aim ....................................................................... .................................................................................... 103Objectives ....................................................................... .......................................................................... 103Learning outcome ...................................................................................................................................... 1038.1 Introduction ..........................................................................................................................................1048.2 Definition of Total Quality Management .............................................................................................104 8.2.1 Defining Quality .................................................................................................................. 1048.3 Cost of Quality .....................................................................................................................................1048.4 Continuous Improvement (Kaizen) ......................................................................................................106 8.4.1 Plan to Study Cycle ..............................................................................................................106 8.4.2 Benchmarking ......................................................................................................................1078.5 Employee Empowerment .....................................................................................................................107 8.5.1 Team Approach .................................................................................................................... 1088.6 Tools of Quality Control ...................................................................................................................... 108 8.6.1 Cause-and-Effect Diagrams .................................................................................................108 8.6.2 Flowcharts ............................................................................................................................109 8.6.3 Checklists .............................................................................................................................109 8.6.4 Control Charts ......................................................................................................................109 8.6.5 Scatter Diagrams ..................................................................................................................109 8.6.6 Pareto Analysis .....................................................................................................................110 8.6.7 Histograms ............................................................................................................................1108.7 Process Management ............................................................................................................................1118.8 Quality Standards ..................................................................................................................................111 8.8.1 ISO 9000 Standards ..............................................................................................................111 8.8.2 ISO 14000 Standards ............................................................................................................1128.9 Reason for TQM Failure .......................................................................................................................112Summary ....................................................................... ............................................................................113References ....................................................................... ..........................................................................113Recommended Reading ............................................................................................................................113Self Assessment ..........................................................................................................................................114

VI/JNU OLE

List of Figures

Fig. 1.1 Inventory classification .....................................................................................................................2Fig. 2.1 Process from procurement to realisation of money ........................................................................17Fig. 3.1 Computer architecture for MRP ..................................................................................................... 31Fig. 3.2 Material requirements planning system ..........................................................................................32Fig. 8.1 Cost of defects .............................................................................................................................. 106Fig. 8.2 PDSA cycle ...................................................................................................................................107Fig. 8.3 Seven tools of quality control ........................................................................................................110

VII/JNU OLE

List of Tables

Table 1.1 List of classification of inventories ................................................................................................7Table 4.1 Evolution of ERP from 1960s to 1990s ....................................................................................... 43Table 5.1 Model developed for accepting/rejecting discounts on purchases in excel spread sheet .............52Table 6.1 Purchasing function vs. purchase department ..............................................................................69Table 6.2 Matrix of price and quality of the tenders ....................................................................................72Table 8.1 Cost of quality ............................................................................................................................105

VIII/JNU OLE

Abbreviations

BOM - Bill of MaterialsDGS & D - Directorate General of Supply & DisposalDIL - Desired Inventory LevelEDI - Electronic Data InterchangeEOQ - Economic Order QuantitiesERP - Enterprise Resource PlanningFIFO - First In First OutGC Guara-nteCeertifcateGRN - Goods Returned NoteGRR - Goods Received ReportHIFO - Highest In First OutIR - Inspection RequestIRF - Inventory Record FileIT - Information TechnologyLIFO - Last In First OutLTE - Limited Tender EnquiryMPS - Master Production ScheduleMRO - Maintenance, Repair and Operating InventoriesMRP - Materials Requirement PlanningMTC Mat-erial TestCertifcatePO - Purchase OrderQA - Quality AssuranceROI - Return on InvestmentROL - Re-Order LevelSAR - Simple Average RateSTE - Single Tender EnquiryVDC - Vendor Development CellWAR - Weighted Average Rate

1/JNU OLE

Chapter I

Material Management

Aim

The aim of this chapter is to:

introduce the students to material management•

explain the scope of material management•

elucidate the various motives of inventory•

Objectives

The objectives of this chapter are to:

defnetheclassifcationofinventory•

explicate the key objectives of material management•

enlist the functions of material manager•

Learning outcome

At the end of this chapter, you will be able to:

understand the materials requirement planning technique (MRP)•

analyse about the process of purchasing•

identify the effects of overstocking and under stocking•

Purchase and Material Management

2/JNU OLE

1.1 Introduction to Material Management

Every organisation depends on materials and services from other organisations to varying extents. These materials and services are obtained through exchange of money. Various materials are used as inputs such as raw materials, consumables and spares. These are required to be purchased and made available to the shops/users as and when neededtoensureuninterruptedproduction.Effcient managementofinputmaterialsisofparamountimportanceinabusinessorganisationformaximisingmaterialsproductivity,whichultimatelyaddstotheproftability oftheorganisation.

Material cost is probably the most important element of cost. In the case of certain industries like cement, sugar,chemicals,ironandsteel,etc.,thematerialscostformsaverysignifcant portionoftheoverallcostofproduction.

1.2 Classifcation of Inventory

The term material refers to all commodities which are consumed in the production process. The materials which canbeconsumedintheproductionprocesscanbebasicallyclassifedas:

Direct Materials•

Indirect Materials•

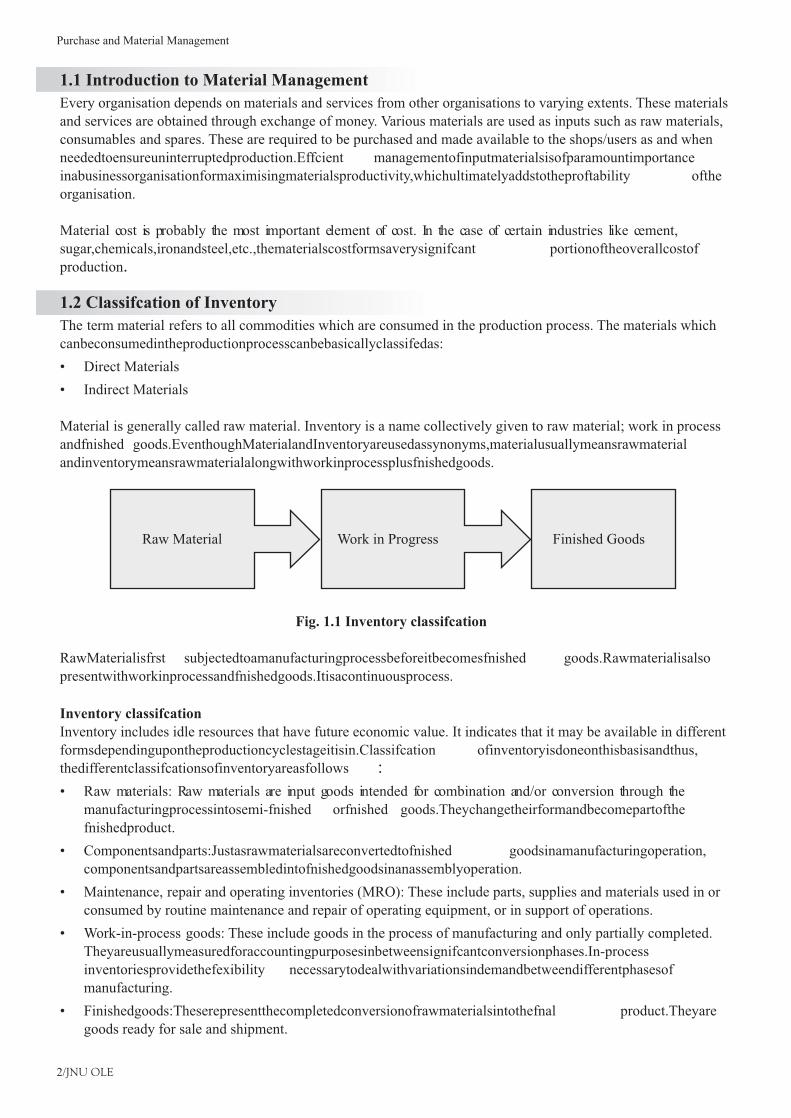

Material is generally called raw material. Inventory is a name collectively given to raw material; work in process andfnished goods.EventhoughMaterialandInventoryareusedassynonyms,materialusuallymeansrawmaterialandinventorymeansrawmaterialalongwithworkinprocessplusfnishedgoods.

Raw Material Work in Progress Finished Goods

Fig. 1.1 Inventory classifcation

RawMaterialisfrst subjectedtoamanufacturingprocessbeforeitbecomesfnished goods.Rawmaterialisalsopresentwithworkinprocessandfnishedgoods.Itisacontinuousprocess.

Inventory classifcationInventory includes idle resources that have future economic value. It indicates that it may be available in different formsdependingupontheproductioncyclestageitisin.Classifcation ofinventoryisdoneonthisbasisandthus,thedifferentclassifcationsofinventoryareasfollows :

Raw materials: Raw materials are input goods intended for combination and/or conversion through the •manufacturingprocessintosemi-fnished orfnished goods.Theychangetheirformandbecomepartofthefnishedproduct.

Componentsandparts:Justasrawmaterialsareconvertedtofnished goodsinamanufacturingoperation,•componentsandpartsareassembledintofnishedgoodsinanassemblyoperation.

Maintenance, repair and operating inventories (MRO): These include parts, supplies and materials used in or •consumed by routine maintenance and repair of operating equipment, or in support of operations.

Work-in-process goods: These include goods in the process of manufacturing and only partially completed. •Theyareusuallymeasuredforaccountingpurposesinbetweensignifcantconversionphases.In-processinventoriesprovidethefexibility necessarytodealwithvariationsindemandbetweendifferentphasesofmanufacturing.

Finishedgoods:Theserepresentthecompletedconversionofrawmaterialsintothefnal product.Theyare•goods ready for sale and shipment.

3/JNU OLE

Resale goods: These are goods acquired for resale. Such goods may be purchased by a wholesaler for resale to •distributors, or by distributors for resale to consumers, etc.

Capital goods: These are items (such as, equipment) that are not used or consumed during a single operating •period, but have extended useful lives and must be utilised over multiple operating periods. Tax laws require that such an item be capitalised, and a predetermined percentage of its cost be recognised as an expense, each operating period, over a predetermined time frame, according to equipment classes.

Construction materials: These are raw materials and components for construction projects such as a building, •bridge, etc.

Hardgoods/softgoods:Whatoneidentifes ashardgoodsandsoftgoodswillvarydependingontheindustry•involved. For example, in data processing, hard goods include apparatus such as, computers and terminals, while soft goods include software, data storage media and the like.

Fuel and lubricants: Fuel and lubricants are used for the oiling purpose for the equipment used in the process •which again varies with the type of industry.

Stationery goods: It includes writing material like, paper, pen, ink, etc., which are used by the people involved •in the process.

Primarypackingmaterial:Packingmateriallike,plastic,paper,etc.areusedtopackthefnished goodsfor•sale.

1.3 Meaning of Material Management

Materialsmanagementcanbedefnedas“anintegratedmanagementapproachtoplanning,acquiring,processinganddistributingproductionmaterialsfrom theraw materialstateto thefnished productstate”.Materialsmanagementis a key business function that is responsible for the coordination of planning, sourcing, purchasing, moving, storing and controlling materials in an optimum manner, so as to provide pre-determined service to the customer at a minimum cost.

Materialsmanagementhassuchsub-feldsas:

inventory management•

value analysis•

receiving•

stores and management of the obsolete•

slow moving and non moving materials•

Materials management is the branch of logistics that deals with tangible components of a supply chain. It covers the acquisition of spare parts and replacements, quality control of purchasing and ordering such parts, and the standards involved in ordering, shipping, and warehousing the said parts. The physical arrangement of materials/spare parts is called materials management.

Planningandcontrolofthefunctionssupportingthecompletecycle(fow) ofmaterials,andtheassociatedfow ofinformation is called materials management. Materials management is concerned with the control of materials in such a manner which ensures maximum return on working capital. Materials management is concerned with the location and purchase of materials needed, their storage and movement. It also arranges to keep an account of them. It is also responsible for planning their movement through manufacturing processes, store rooms and distribution channels.

Materials management provides an integrated systems approach to the coordination of the materials activities and the control of total material costs. The materials management function ranges from receiving the material requisitions from user department to placement of purchase orders and then, on the other hand, receiving the materials from vendors and making it available to the users departments.

Purchase and Material Management

4/JNU OLE

1.4 Objectives of Material Management

The fundamental objectives of the materials management function are acquisition of materials and services:

of the right quality •

in the right quantity •

at the right time •

from the right source •

The key objectives of material management are as follows:

Buying at the lowest price, consistent with the desired quality and service•

Maintaining a high inventory turnover, by reducing excess storage, carrying costs and inventory losses occurring •due to deteriorations, obsolescence and pilferage

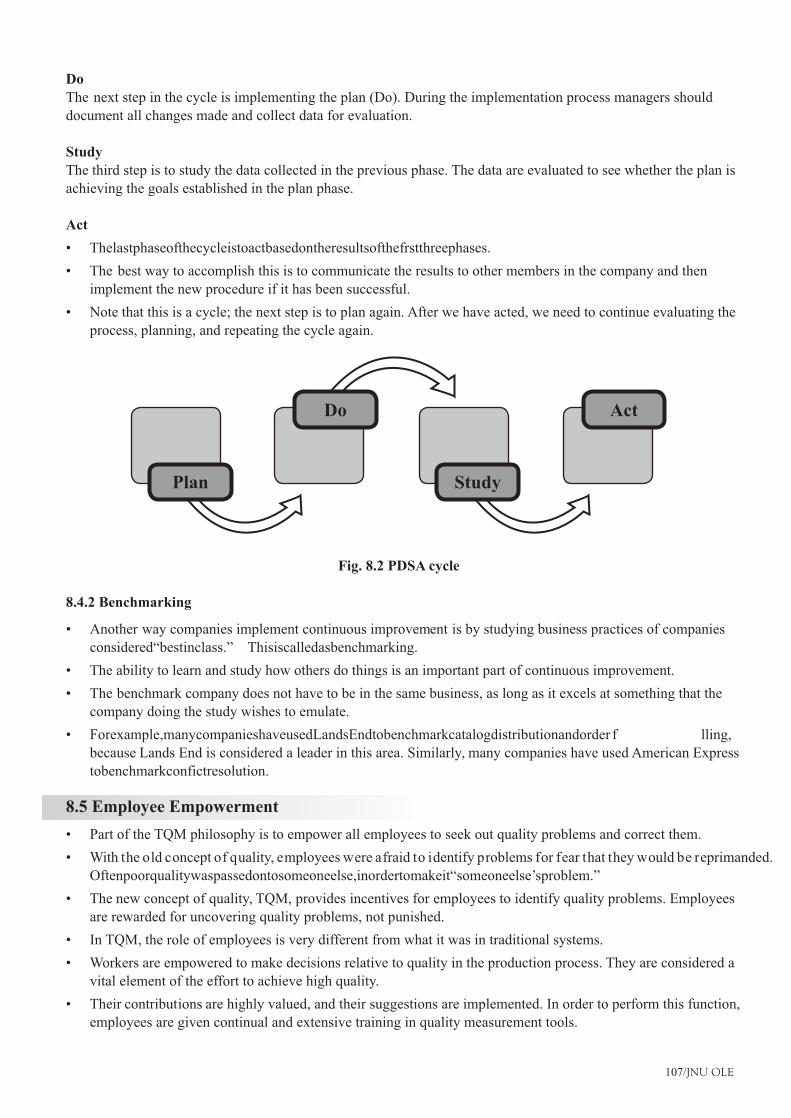

Maintainingcontinuityofsupply,preventinginterruptionofthefowofmaterialsandservicestousers•

Maintainingthespecifed materialqualitylevelandaconsistencyofquality.Thispermitseffcient andeffective•operation

Developing reliable alternate sources of supply to promote a competitive atmosphere in performance and •pricing

Minimisingtheoverallcostofacquisitionbyimprovingtheeffciencyofoperationsandprocedures•

Hiring, developing, motivating and training personnel and providing a reservoir of talent•

Developing and maintaining good supplier relationships in order to create a supplier attitude and desire furnish •the organisation with new ideas, products, and better prices and service

Achieving a high degree of cooperation and coordination with user departments•

Maintaininggoodrecordsandcontrolsthatprovidesanaudittrailandensureseffciencyandhonesty•

Participating in 'Make or Buy' decisions •

1.5 Motives of Material Management

A company may hold the inventory with the various motives as stated below: Transaction motiveThe company may be required to hold the inventories in order to facilitate the smooth and uninterrupted production and sales operations. It may not be possible for the company to procure raw material whenever necessary. There may be a time lag between the demand for the material and its supply. Hence, it is needed to hold the raw material inventory. Similarly, it may not be possible to produce the goods immediately after they are demanded by the customers.Hence,itisneededtoholdthefnished goodsinventory.Theneedtoholdworkinprogressmayarisedue to production cycle.

Precautionary motiveIn addition to the requirement to hold the inventories for routine transactions, the company may like to hold them to guard against the risk of unpredictable changes in demand and supply forces. For example, the supply of raw material may get delayed due to the factors like strike, transport, disruption, short supply, lengthy processes involved in import of the raw materials, etc.

Hencethecompanyshouldmaintainsuffcient levelofinventoriestotakecareofsuchsituations.Similarly,thedemandforfnished goodsmaysuddenlyincrease(especiallyincaseofseasonaltypesofproducts)andifthecompany is unable to supply them, it may indicate gain for the competitions. Hence, the company will like to maintainsuffcientstockoffnishedgoods.

5/JNU OLE

Speculative motiveThe company may like to purchase and stock the inventory in the quantity which is more than needed for production and sales purpose. This may be with the intention to get the advantages in terms of quantity discounts connected with bulk purchasing or anticipated price rise.

1.6 Scope of Material ManagementThe scope of material management includes the following aspects:

Material planning•

Cataloguing or coding the materials•

Standardisation•

Scheduling•

Procurement•

Inspection•

Quality control•

Packaging•

Storage•

Inventory control•

Distribution •

Disposal•

1.7 Material PlanningMaterial management involves the process of planning to get the materials. It is the starting point for the whole materialmanagementfunction.Materialplanningisascientifc wayofdeterminingtherequirementsstartingwithraw materials, consumables, spare parts and all other materials that are required to meet the given production plan for a certain period. Material planning is derived from overall organisational planning and hence, it is always a sub-plan of the broad organisational plan. What it does is forecast and initiate the procurement of materials.

Factors affecting material planningThe factors affecting material planning are:

Macro factors: Global factors such as price trends, business cycles, government’s import and export policies •etc., are called macro factors. Credit policy of the government is a critical factor as banks follow these guidelines onlywhileextendingfnancialsupporttoabusinessentity.

Micro factors: These are essentially the factors existing within the organisation such as corporate policy •on inventory holding, production plan, investments etc., For any organisation, factors such as lead time of procurement, acceptable inventory levels, working capital, seasonality, delegation of power are micro factors

1.8 Technique of Planning MaterialsMaterials Requirement Planning (MRP) considers the annual production plan of the manufacturing concern. Once afrm determinesitsannualproductionplan,theoverallmaterialrequirementtomeetthegivenproductionplanis worked out. It is a detailed analysis encompassing the materials and quantities available for use, materials with quantities not available and hence, needing procurement, the actual lead time of procurement, etc.

It is always possible to have a situation where some parts of an assembly are available and some others are not available.TheBillofMaterials(BOM)isprepared.Itquantifes allthematerials(components)neededforvariousassemblies as per the production plan. BOM is thus a list displaying the code, nomenclature of an item, its unit and quantity, location of use and also the estimated price of each component. An explosion chart is a series of bills of materials grouped together in a matrix form so that combining the requirements for different components can be made. Once the BOM is ready, the same is handed over to the Purchasing wing which initiates the purchasing activities. MRP, thus, keeps in view the lead time also. Using computers, preparation of BOM through explosion of lists is quite easy and smooth.

Purchase and Material Management

6/JNU OLE

Materials required for any operation are based on the sales forecasts and production plans. Planning and control is done for the materials taking into account the materials not available for the operation and those in hand or in the pipe line. This involves estimating the individual requirements of parts, preparing materials budget, forecasting the levels of inventories, scheduling the orders and monitoring the performance, in relation to production and sales.

Cataloguing or coding the materialsFor easy procurement, storage, retrieval and the distribution of the inventories, it is essential to classify them into differentcategories.Thisclassifcation canbedonethroughcodifcation orcataloguing.Codifcation orcataloguingisbasicallyanidentifcationsystemforeachitemoftheinventory.

Therearethreebroadapproachestodevelopingasuitableidentifcationsystem. Theseare:

Arbitrary approach•

Symbolic approach •

Use of drawing numbers•

Arbitrary approachAs and when an item is received by stores in its receiving bay, a running and unique serial number is assigned to it. Thisnumberbecomesthecodeoftheitemforsubsequentuseatdifferentstages.Itdoesnothelpinthescientifcmanagement of inventory. Arbitrary approach is useful only where perhaps items are non-repetitive and the inventory managementneednotbescientifc.

Symbolic approachIt assigns code in such a manner that the same item number is not allotted to two different materials. The code is designed such that it can be used to tell many things about an item of material.

Thesystemuseseitheranumericcodifcation systemoranalphanumericsystem.Underthenumericsystem,asetofnumeric code (length pre-decided) is assigned to each item where different parts of the code describe different aspects of an item: class, subclass, unique running number of that item, location of the storage suppliers’ code, etc.

Example:

2 145 098 344

Class Subclass Running number Location code

Thus, the code of this item shall be a 10 digit code, 2145098344 and it shall always remain so for this item. It shall then be easy to communicate about this item among the concerned agencies. Similarly, there can be a code using alpha numeric value like AA223B234 with different alpha and numerical value describing some pre-decided meaning. It is also called mnemonic system. Since this code has certain logic, it is also called intelligent code and this system is widely used everywhere.

Use of drawing numbersManyfrms usedrawingnumbersascodestoidentifyanitem.Sincethedrawingnumberforafrm remainsunique,assigningacodeonthisbasisassumesauniquecodeforthatitemandhence,confrms therequirementofauniqueidentifcationfortheitem.

1.9 Process of Codifcation

Theprocessofcodifcationislistedbelow:

Decideifthefrmwantstogoforarbitrarysystem,symbolicsystemorengineeringdrawingsystem•

List the inventory items•

Defnetheclassofitems•

Defnethesubclassundereachclass•

7/JNU OLE

Depending upon the number of classes, their subclasses and probable number of items under each sub class •decidethelengthofcodeswhichshallremainfxedforalltheinventoryitems(10digit,alphanumeric,etc.)

Start assigning codes as per the detailed list of inventory•

Anillustrativelistofclassifcationofinventories:

Abrasives Bearings Belt and beltings

Bolts, nuts & washers Brooms & brushes Building materials

Cans & containers Chemicals & reagents Cloth, leather & rubber

Electrical Gases Glassware

Oil & lubricants Pipe&pipefttings Raw materials

Rolls Refractory Stationery

Safety items Tools & tackles Photographic items

Table 1.1 List of classifcation of inventories

Codifcationisusuallydonebyateamconsistingofrepresentativesdrawnfromstores,userdepartmentandindustrialengineeringdepartment.Themajorresponsibilitylieswiththestoresdepartment.Codifcation identifes anitem.Also it acts as a communicating medium for an item among the different users of that item in whatever way such asstores,userdepartment,planningdepartment,fnance, purchasing,etc.Assoonastheitemisreceivedinthestores(iftheitemisanewone),itiscodifed. Oncecodifed, thesamecodeisusedinthecycleofprocurement,throughout and for ever.

1.10 Standardisation

Standardisationmeans“formulation,publicationandimplementationofguidelines,rulesandspecifcations forcommon and repeated use, aimed at achieving optimum degree of order or uniformity in a given context, discipline, orfeld”. Publicationmeanscommunicationofamessage,statement,ortextthroughanymeanssuchasaudio,video,print,electronicallyasane-bookorontheweb.Specifcation meansexactstatementoftheparticularneedstobesatisfed oressentialcharacteristicsthatacustomerrequiresingoods,material,method,process,service,system,orworkandwhichavendormustdeliver.Specifcations arewrittenusuallyinamannerthatenablesbothparties(and/oranindependentcertifer)tomeasurethedegreeofconformity

Specifcationsaredividedgenerallyintotwomaincategories:

Performancespecifcations: Conformtoknowncustomerrequirementssuchaskeepingaroom’stemperature•withinaspecifedrange.

Technicalspecifcations: Expressthelevelofperformanceoftheindividualunits,andaresubdividedintothe•following:

Individualunitspecifcations whichstateboundaries(parameters)oftheunit’sperformanceconsistingofa ?nominal (desired or mandated) value and tolerance (allowable departure from the nominal value)

Acceptablequalitylevelwhichstateslimitsthataretobesatisfed bymostoftheunits,butacertain ?percentage of the units is allowed to exceed those limits, and

Distributionspecifcations whichdefne anacceptablestatisticaldistribution(intermsofmeandeviation ?and standard deviation) for each unit, and are used by a producer to monitor its production processes

Purchase and Material Management

8/JNU OLE

1.11 Scheduling

Schedulingmeans“assigninganappropriatenumberofworkerstothejobsduringeachdayofworkanddeterminingwhenanactivityshouldstartorend”.Scheduledependsonthefollowing:

duration•

predecessor activity (or activities)•

predecessor relationships•

resource availability•

target completion date of the project•

1.12 Procurement

Procurement means acquisition. It includes the complete process of obtaining goods and services from preparation and processing of a requisition to receipt and approval of the invoice for payment. It is also called sourcing.

Procurement involves the following activities:

purchase planning•

standards determination •

specifcationsdevelopment•

supplier research and selection•

value analysis•

fnancing•

price negotiation •

making the purchase •

supply contract administration•

inventory control and stores, and•

disposals and other related functions•

1.13 Purchasing

Basically, the job of a materials manager is to provide to the user departments, right material at the right time in right quantity of right quality at right price, from the right source. To meet these objectives, the activities undertaken includeselectionofsourcesofsupply,fnalisation ofthetermsofpurchase,placementofpurchaseorders,followup, maintenance of relations with vendors, approval of payments to vendors, evaluating, rating and developing vendors.

Before deciding the quantity to be purchased, the following factors should be taken into consideration:

Quantity already ordered•

Quantity reserved - It may happen that a particular quantity, though in hand, might have been reserved for a •particular job which is not available for other purposes. In such cases, this quantity is such, as if it is not in stock

Funds availability - Amounts which are kept aside for drawing up purchase budget should be considered•

Normally, the process of purchasing the materials involves the following stages:

Requisitioning:Atthisstage,thepurchasingoffcershouldreceiveanaccuratedescriptionofthegoodsorservice•required.Therequisitionformbywhichamemberofstaffnotifes purchasingoffcer ofaneedforgoodsorservices should be simple, but clear. The more accurate and detailed the requisition form is, the more are the chances that the purchase will meet the expectations.

Financialapproval:Here,thepurchasingoffcer mustbegiventheapprovalfromaresponsibleperson.Itshould•be done before the purchasing commitment is made, and the purchasing system should ensure that this is done at the right time and by the right person.

9/JNU OLE

Marketassessment:Thepurchasingoffcer receivesanapprovedrequisitionandstartsmarketresearchinthis•stage. He should check that the item is not already in stock, that there is a competitive market for the item, if thereisalistof“approvedsuppliers”fortheitem,ifalowerpricecanbenegotiated,andsoon.

Purchasedecision:Duringpurchasedecisionstage,afterthepurchasingoffcercompletedthemarketassessment•and determined the method of purchase, he decides on the supplier or suppliers. To avoid internal customer complaints or audit reproof, the decision must be well documented to provide clear reasons as to why a particular supplier has been chosen.

Ordering:Attheorderingstage,themaininstrumentpurchasingoffcer workswithisanorderform.Theorder•formisanoffcial, numbereddocumentwhichdetailsthepurchaserequirementsandauthorisesthesuppliertodeliverthegoodsorservicestothecompany. Also,itcanfulflotherimportantfunctions.

Delivery:Atthedeliverystage,thepurchasingoffcercontrolsthemethod,termsandtimeofdeliveryestablished•while ordering. In case there is a competitive transport market, wise freighting decisions can lead to considerable cost savings.

Receiptingandaccounting:Atthisstage,thepurchasingoffcer shouldcheckwhetherthequalityandquantity•of delivered goods or services are relevant to ones in the purchase order. Usually, suppliers are not paid until the goods are checked however, this procedure should be taken up without unnecessary delays to ensure that payment terms are met.

Payment:Atthepaymentstage,thepurchasingoffcer makessurethatthepaymentsaremadeonthedatesthey•are due, because maintaining good supplier relations is very important. Also, he should control the terms of payment in case, they include previously negotiated discounts, progress payments or postponement of payment during warranty period.

1.14 Inspection

Inspection involves critical appraisal involving examination, measurement, testing, gauging, and comparison of materials or items. An inspection determines if the material or item is in proper quantity and condition, and if it conformstotheapplicableorspecifedrequirements.

Inspection is generally divided into three categories:

Receiving inspection •

In-process inspection and •

Final inspection •

1.15 Quality Control

A subset of the quality assurance (QA) process, it comprises of activities employed in detection and measurement of the variability in the characteristics of output attributable to the production system, and includes corrective responses. In quality control the role of inspection is to verify and validate the variance data.

1.16 Packaging

Packaging includes processes (such as cleaning, drying, and preserving) and materials (such as glass, metal, paper or paperboard, plastic) employed to contain, handle, protect, and/or transport an article. The role of packaging is expandingandmayincludefunctionssuchastoattractattention,assistinpromotion,providemachineidentifcation(barcodes, etc.), impart essential or additional information, and help in utilisation.

1.17 Storage

Storage means non-transitory, semi-permanent containment, holding or placement of goods or materials, usually with the intention of retrieving them at a later time. It does not include the interim accumulation of a limited amount during processing, maintenance, or repair.

Purchase and Material Management

10/JNU OLE

1.18 Inventory Control

Inventory control covers aspects such as setting inventory levels, doing various analyses such as ABC, XYZ, etc, fxingeconomicorderquantities(EOQ),settingsafetystocklevels,leadtimeanalysisandreporting.

1.19 Distribution

Distribution means movement of goods and services from the source through the distribution channel, right up to thefnalcustomer,consumer,oruser.

1.20 Disposal

Disposalmeansfnal placementorriddanceofwastes,excess,scrap,etc.,underproperprocessandauthoritywith(unlike in storage) no intention to retrieve. Disposal may be accomplished by abandonment, destruction, internment, incineration, donation, sale, etc.

1.21 Functions of Material Manager

The functions of a material manager are as under:

materials planning and control•

purchasing•

management of stores•

inventory control•

useofinformationtechnologyforeffcientmaterialmanagement•

1.22 Effects of Over Stocking and Under Stocking

The objective of material is to maintain optimum stock. The principle which should be kept in mind is that there should not be any over stocking or under stocking of materials, as both these situations involve costs.

Overstocking will result into the following consequences:

blocking of working capital, resulting in escalating cost of capital investment •

riskofdeteriorationofqualityandobsolescenceresultinginthematerialbeingunftforuse•

more storage facilities, resulting in higher rental cost •

additional insurance cost •

more material handling and up-keeping•

risk of breakage/pilferage, etc. •

price of raw material may go down in future•

in a nut-shell, carrying cost goes up •

however, ordering cost goes down •

Understocking will result into the following consequences:

production hold-ups, resulting into disturbed delivery schedules•

frantic eleventh hour purchases which may result in unfavourable prices and quality•

payment for idle time to workers•

increase in the number of orders which will result in more transportation cost•

in nut shell ordering cost goes up •

however carrying cost goes down •

Overstocking or understocking of materials results in losses, hence a manufacturer should go for optimum stock.

11/JNU OLE

Summary

The term material refers to all commodities which are consumed in the production process. The materials •whichcanbeconsumedintheproductionprocesscanbebasicallyclassifed asdirectmaterialsandindirectmaterials.

Material is generally called as raw material. Inventory is a name collectively given to raw material, work in •processandfnishedgoods.

Inventory includes idle resources that have future economic value. It indicates that it may be available in different •forms depending upon the production cycle stage it is in.

Materialsmanagementcanbedefnedas“anintegratedmanagementapproachtoplanning,acquiring,processing•anddistributingproductionmaterialsfromtherawmaterialstatetothefnishedproductstate”.

The fundamental objectives of the materials management function are acquisition of materials and services: of •the right quality, in the right quantity, at the right time, from the right source, and at the right time.

A company may hold the inventory with the various motives such as: transaction motive, precautionary motive, •and speculative motive.

Materialplanningisascientifc wayofdeterminingtherequirementsstartingwithrawmaterials,consumables,•spare parts and all other materials that are required to meet the given production plan for a certain period.

Materials requirement planning (MRP) considers the annual production plan of the manufacturing concern.•

Codifcation orcataloguingisbasicallyanidentifcation systemforeachitemoftheinventory.Therearethree•broadapproachestodevelopingasuitableidentifcationsystem:arbitrary,symbolic,anduseofdrawingnumbersapproach.

Standardisationmeanstheformulation,publication,andimplementationofguidelines,rulesandspecifcations•for common and repeated use, aimed at achieving optimum degree of order or uniformity in a given context, discipline,orfeld.

Scheduling means assigning an appropriate number of workers to the jobs during each day of work and •determining when an activity should start or end.

References

Aswathappa, K. & Bhat, K. S., 2010. • Production and Operations Management , Introduction to operations Management, 2nd ed., Himalaya Publishing House.

Shim, J. K. & Siegel, J. G., 1999. • Operations Management, Scope of Operations Management, 1st ed., Barrons Education Series Inc.

Introduction to Operations Management• , [Pdf] Available at: <http://highered.mcgraw-hill.com/sites/dl/free/0073377848/609567/stevenson_sample_chapter1.pdf> [Accessed 13 February 2013].

Introduction to Operations Management• , [Pdf] Available at: <http://highered.mcgraw-hill.com/sites/dl/free/0073525251/886181/stevenson11_sample_ch01.pdf> [Accessed 13 February 2013].

Dr. Sumukadas, N., 2013. • [1.a] Introduction to Operations Management, [Video online] Available at: <http://www.youtube.com/watch?v=Y28MsljBgvU> [Accessed 13 February 2013].

Dr. Oke, A., 2012. • Introduction to Operations Management 1, [Video online] Available at: <http://www.youtube.com/watch?v=skg_lg-4m2o> [Accessed 13 February 2013].

Recommended Reading

Krajewski, L., Ritzman, L. P., & Malhotra, M, K., 2009. • Operations Management: Process and supply chain, Operations Management, Prentice Hall Publication.

Murthy, P. R., 2006. • Production and Operations Management, Introduction to Operations Management , 2nd ed., New Age International Publishers.

Gaither, N., & Fraizer, G., 2002. • Operations Management-Overview, Thompson Learning, 9th ed.

Purchase and Material Management

12/JNU OLE

Self Assessment

Whichofthefollowingisdefned as“assigninganappropriatenumberofworkerstothejobsduringeachday1. ofworkanddeterminingwhenanactivityshouldstartorend”?

Procurementa.

Schedulingb.

Planningc.

Disposald.

________________ provides an integrated systems approach to the coordination of the materials activities and 2. the control of total material costs.

Material managementa.

Planning and controlb.

Cost managementc.

Schedulingd.

Inventory is a name collectively given to raw material; work in process and __________.3. servicesa.

equipmentsb.

resources c.

fnishedgoodsd.

Which of the following statements is false?4. Over stocking or under stocking of materials results in losses, hence a manufacturer should go for optimum a. stock.

Specifcations arewrittenusuallyinamannerthatenablesbothparties(and/oranindependentcertifer) tob. measure the degree of conformity.

Codifcation isusuallydonebyateamconsistingofrepresentativesdrawnfromstores,userdepartmentandc. industrial engineering department

The code is designed such that it can be used to tell one thing about an item of material.d.

In quality control, the role of inspection is to verify and validate the ________data. 5. systema.

optimumb.

variancec.

materiald.

________isfrstsubjectedtoamanufacturingprocessbeforeitbecomesfnishedgoods.6. Procurementa.

Planningb.

Raw materialc.

Purchasingd.

13/JNU OLE

What do the idle resources have in an inventory?7. Future economic valuea.

Future purchasing valueb.

Futureproftvaluec.

Future manufacturing valued.

Thematerialswhichcanbeconsumedintheproductionprocesscanbebasicallyclassifedas__________.8. rawmaterialandfnishedmateriala.

direct material and indirect materialb.

minimum material and maximum materialc.

spare material and optimum materiald.

Which of the following statements is true?9. In-processinventoriesprovidethefexibility necessarytodealwithvariationsindemandbetweendifferenta. phases of manufacturing.

Whatoneidentifesashardgoodsandsoftgoodswillremainsamewitheveryindustry.b.

Materials management is the branch of statistics that deals with the tangible components of a supply c. chain.

Material management is not concerned with the location and purchase of materials needed, their storage d. and movement.

Whichofthefollowingarethreebroadapproachestodevelopingasuitableidentifcationsystem?10. Arbitrary, symbolic and use of drawing numbers approacha.

Arbitrary, random and use of drawing numbers approachb.

Arbitrary, supply and use of drawing numbers approachc.

Arbitrary, symbolic and use of prime numbers approachd.

Purchase and Material Management

14/JNU OLE

Chapter II

Material Cost Management

Aim

The aim of this chapter is to:

introduce the concept of economic order quantity•

explain the material cost management•

elucidate the various inventory levels•

Objectives

The objectives of this chapter are to:

defnematerialcost•

explicate the drawbacks of Economic Order Quantity model (EOQ)•

enlist the ABC analysis•

Learning outcome

At the end of this chapter, you will be able to:

defnetheXYZanalysis•

recognise about AX control•

identify the advantages of ABC analysis•

15/JNU OLE

2.1 Introduction to Material Cost Management

Theobjectofinventorycontrolistoreducetheinvestmentintheinventorywithoutaffectingtheeffciency intheareaofproductionandsales.Ifasuffcient stockofrawmaterialisnotavailable,theproductionactivityislikelytobeinterrupted.Ifsuffcient stockoffnished goodsisnotavailable,itmaynotbepossiblefortheorganisationtoserve the customers properly and they may shift to the competitors. The objective of inventory control is to avoid the situation of over stocking as well as under stocking. The level of inventories should be maintained at the optimum level. Excess stock results in higher carrying cost and less stock results in excess ordering cost. In case of a typical manufacturingtypeofoperation,theactivitymayconsistofconversionofrawmaterialintheformoffnishedgoodswiththehelpoflabourandotherservicesandsellingthefnished goodsinthemarkettoearntheprofts.Though inventory is an idle resource, it is almost essential to keep some inventory in order to promote smooth and effcientrunningofbusiness.

For example: Consider the case – an enterprise that does not have any inventory. Clearly, as soon as the enterprise receives a sales order, it will have to order for raw materials to complete the order. This will keep the customers waiting. It is quite possible that sales may be lost. Also the enterprise may have to pay high price for some other reasons. On the other hand, inventory may promote sales by reducing customers waiting time.

It is essential to maintain the inventories in order to enhance the stability of production and employment levels. Considerthecaseofseasonalitems.Anyfuctuation indemandcanbemetifpossible,byeitherchangingthatpartofproductionorwithinventories.Ifthefuctuation isnotfollowedbychangingtherateofproduction,onehastotake into account the following costs.

Cost of increasing production and employment level, involves the following:

employment and training•

additional staff and service activities•

added shifts•

overtime costs•

Cost of decreasing production and employment level, involves the following:

employee compensation•

other employee costs•

staff, clerical and service activities•

total time costs•

The functions of inventories are to:

protectagainstunpredictablevariations(fuctuations)indemandandsupply•

take advantage of the price discounts by bulk purchases•

take the advantage of batches and longer production run•

providefexibilitytoallowchangesinproductionplansinviewofchangeindemands,etc.•

facilitate intermittent production•

2.2 Material Cost

Material cost is the cost of commodities and materials used by the organisation. It can be direct or indirect.

DirectMaterialisindicativeofmaterialwhichcanbeidentifed withtheindividualproductandwhichbecomes•anintegralpartofthefnished goods.Itbasicallyconsistsofallrawmaterials,eitherpurchasedfromoutsideor manufactured in-house.

IndirectMaterialindicatesthatmaterialwhichcannotbeidentifed withtheindividualproduct.Thismaterial•assiststhemanufacturingprocessanddoesnotbecomeanintegralpartoffnished goods.Theexamplesofindirect material may be consumable stores, cotton waste, oils and lubricants, stationery material, primary packing material, etc.

Purchase and Material Management

16/JNU OLE

Material cost is categorised as variable cost. The cost increases with the increase in the level of production activity andviceversa.Theheartofinventoryanalysisresidesintheidentifcation ofrelevantcosts.Someoftheimportantcosts that apply to inventory situation are as follows:

Ordering or set up costs: These are the costs associated with ordering or manufacturing goods through purchasing •or manufacturing and are known as set up costs or cost of ordering. Set up costs are generally assumed to be independent of the quantity ordered or produced.

Purchase cost or production cost (Material cost): When large production runs are in process, these results in •reduction of production cost per unit. Often, discounts are offered for the purchase of large quantities. In other words, often the unit cost of an item depends on the quantity procured or produced.

Inventory holding cost or carrying cost: The cost associated with carrying or holding the goods in stock are •known as carrying or holding costs. These costs arise due to the storage costs, property taxes on the items in inventory, interest on the invested capital (interest on value of the inventory items, spillage of the inventory items, depreciation of the inventory items, transportation and handling of the items in inventory, etc).

Shortage or stock out costs: The costs that are incurred as a result of running out of stock are known as stock out •orshortagecosts.Asaresultofshortages,salesorgoodwillmaybelost.Iftheunfulflled demandfortheitemscanbesatisfed atalaterdate(backordercase).Inthiscase,thecostofbackordersareassumedtovarydirectlywiththeshortagequantity(inrupeevalue)andthedelayingtime.However,iftheunfulflled demandislost(lost-sales case), in this case, the cost of shortages are assumed to vary directly with the shortage quantity.

Example: For calculating material cost

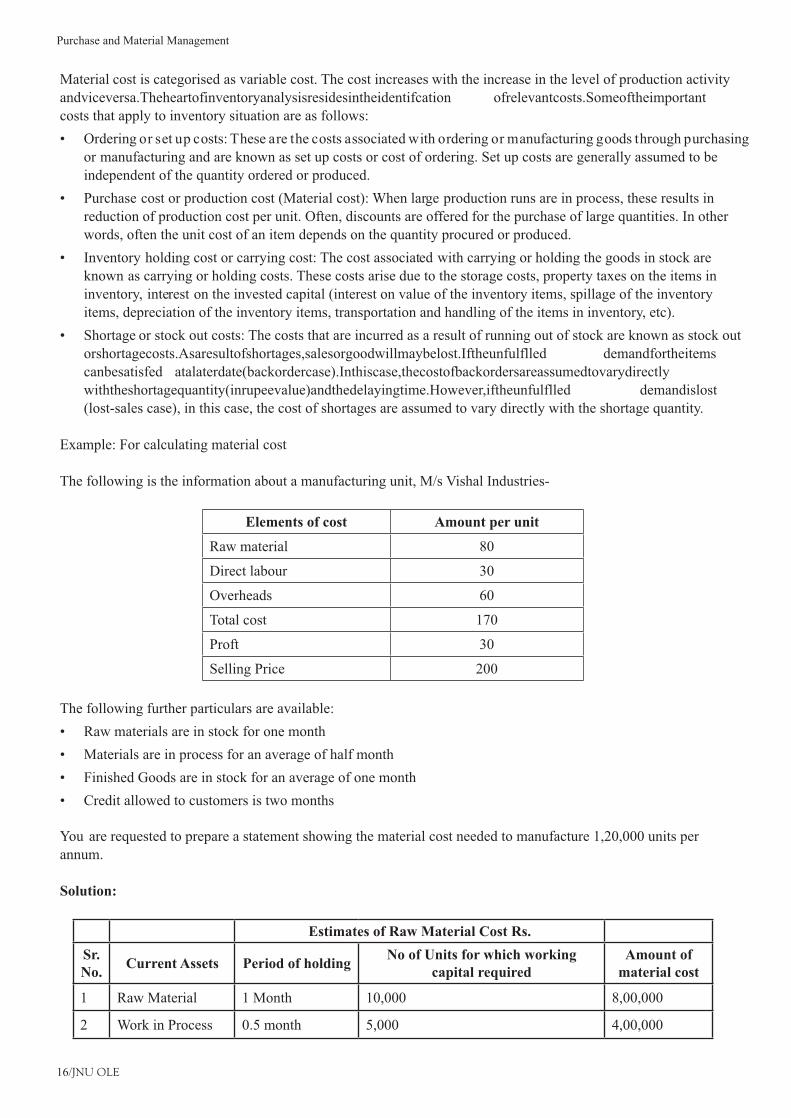

The following is the information about a manufacturing unit, M/s Vishal Industries-

Elements of cost Amount per unit

Raw material 80

Direct labour 30

Overheads 60

Total cost 170

Proft 30

Selling Price 200

The following further particulars are available:

Raw materials are in stock for one month•

Materials are in process for an average of half month•

Finished Goods are in stock for an average of one month•

Credit allowed to customers is two months•

You are requested to prepare a statement showing the material cost needed to manufacture 1,20,000 units per annum.

Solution:

Estimates of Raw Material Cost Rs.

Sr. No.

Current Assets Period of holdingNo of Units for which working

capital requiredAmount of

material cost

1 Raw Material 1 Month 10,000 8,00,000

2 Work in Process 0.5 month 5,000 4,00,000

17/JNU OLE

3 Finished Goods 1 Month 10,000 8,00,000

4 Debtors 2 Months 10,000 16,00,000

Total 36,00,000

Working notes

Sr.No.

Category Period of holdingNo of units for which

working capital requiredAmount of

Material cost

1 Raw material 1 Month 10,000 8,00,000

2 Work in Process 0.5 Month 5,000 4,00,000

3 Finished Goods 1 Month 10,000 8,00,000

4 Debtors 2 Months 10,000 16,00,000

Total 36,00,000

Cash

Raw Material

Work in

Process

Finished

Goods

Debtors

Fig. 2.1 Process from procurement to realisation of money

Note: We have not considered the labour cost and other cost, since it is outside the purview of material cost. From the above example, it is clear that the cost of raw material is present in raw material stage, work in process stage, fnished goodstageanddebtors.Rawmaterialislikealifebloodoftheindustrywhichfows throughouttheprocessfrom procurement stage to realisation money from debtors.

2.3 Economic Order Quantity (EOQ) Models

Economic Order Quantity (EOQ) models are the most basic models of inventory management. EOQ model is essentially a trade-off between various relevant costs and derive an order quantity and time for placing an order in such a way that the total costs are minimised.

Economic lot size or economic order quantity model assumptions are:

The rate of demand for the item is deterministic and is constant D units per annum, independent of time•

Productionrateisinfnite,i.e.,productionisinstantaneous•

Shortages are not allowed •

Lead time is zero or constant independent of demand and the quantity ordered•

The entire quantity is delivered as a single package (or production in a single run)•

Purchase and Material Management

18/JNU OLE

Objective of the EOQThe prime objective of EO is to minimise the average annual variable cost. Economic Order Quantity (EOQ) indicates thatquantity,whichisfxed insuchawaythatthetotalvariablecostofmanagingtheinventory,canbeminimised.Such cost basically consists of two parts:

First, ordering cost (which in turn consists of the costs associated with the administrative efforts connected with •preparation of purchase requisitions, purchase enquiries, transportation cost and handling of more number of bills and receipts)

Second, carrying cost i.e., the cost of carrying or holding the inventory (which in turn consists of the cost like •godown rent, handling and upkeep expenses, insurance, opportunity cost of capital blocked i.e., interest etc.)

There is a reverse relationship between these two types of costs i.e.,

If the purchase quantity increases, ordering cost may get reduced but the carrying cost increases and vice versa.

A balance is to be struck between these two factors and it is possible at Economic Order Quantity (EOQ), where the total variable cost of managing the inventory is the least.

The following is the formula for calculating Economic Order Quantity: EOQ=√(2 AO)/C

Where,Q = Economic Order Quantity A = Annual Requirement in Units O = Cost of Placing an Order C = Cost of Carrying One Unit per Year

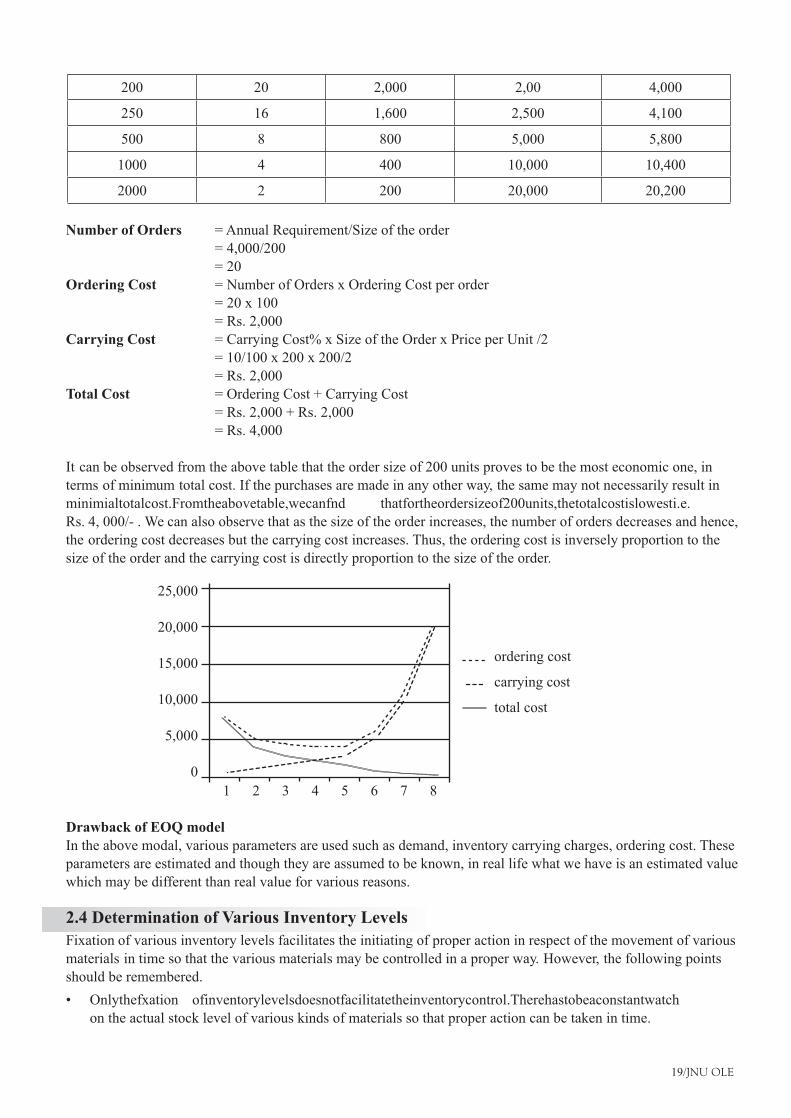

ExampleA manufacturer uses 4,000 units of a component every year and he buys them entirely from outside supplier. The order placing and receiving cost is Rs.100 per order and annual carrying cost is Rs. 10%. Unit cost of raw material is Rs 200/-. Calculate Economic Order Quantity.

Solution: EOQ=√(2 AO)/C√(2=x4,000x100)/10%of200√(8=,00,000/20)√4=0,000

= 200 units

Annual Requirement: 4,000 Ordering cost per order: 100 Carrying Cost: 10% Price per unit: 200

Lot size No. of orders Ordering cost Carrying cost Total cost

1 2 3 4 5

2=4000/col. 1 3=100xcol.2 4=col.1x100x0.10/2 5=3+4

50 80 8,000 500 8,500

100 40 4,000 1,000 5,000

150 27 2,667 1,500 4,167

19/JNU OLE

200 20 2,000 2,00 4,000

250 16 1,600 2,500 4,100

500 8 800 5,000 5,800

1000 4 400 10,000 10,400

2000 2 200 20,000 20,200