Publication semestrielle - marsamaroc.co.ma · Safi Agadir Laayoune Tanger Med Nador ... • OCP...

17

Communication financière Publication semestrielle Octobre 2016 Investor Presentation

Transcript of Publication semestrielle - marsamaroc.co.ma · Safi Agadir Laayoune Tanger Med Nador ... • OCP...

Communication financière

Publication semestrielle

Octobre 2016

Investor Presentation

36,3 millions

of tons

Traffic (2016)

60% Moroccan state

30% free float

10% pool of 3 investors

Shareholder structure

Mad 2 567 mn

USD 254 mn

Consolidated turnover

(2016)

> 2 100

Employees (2016)

Mad 580 mn

USD 57 mn

Consolidated Net Income

(2016)

Mad 1 155 mn

USD 114 mn

Consolidated EBITDA

(2016)

Company at a glance : the leading port operator in Morocco

2

Morocco: a Growing Gateway Market

Company overview : the leading port operator in Morocco

Sound Financials

Growth opportunities

3

23 25 25 28

18 22 23

26 9

8 10 13

12 11 8

6 5

6 6 6

4 4 4

5

3 3 2

3

2 3 3

3 76.6

84.2 81.3

90.3

2013 2014 2015 2016

Morocco: a Growing Gateway Market

Evolution of traffic per port(1)

Evolution of port operators(1) market shares

Source : ANP Marsa Maroc

74 % of national traffic

Casablanca

Jorf Lasfar

Mohammedia Safi

Agadir Laayoune

Tanger Med

Nador

• The traffic generated by maritime trade has seen an average growth of 5.6% p.a. since 2013, reaching 90.3 MT in 2016;

• In 2015, the traffic decreased by 3.4% following the shutdown of of Moroccan refinery activities in August 2015;

• The traffic has know a growth of 11% in 2016.

Marsa Maroc

OCP

Tanger Med

Somaport

Taqa Morocco

Mass Céréales Sosipo

Hydrocarb Jorf

• Marsa Maroc had a market share of 42% by the end of 2016 . This fall is explained by the liquid bulk traffic decreased following the shutdown of SAMIR’s activity in August 2015.

• OCP operates close to a third of the traffic, mainly in the ports of Casablanca and Jorf Lasfar;

• The Tanger Med operators have close to 10% of the national market share;

• Operators in the grains sector (Sosipo and Mass Céréales) had 5% market share by the end of 2016;

• OCP, Taqa Morocco, (industrial companies) etc. handle their own traffic on dedicated terminals without resorting to port operators .

(1) Excluding transhipment

In million of tons

4

49% 46% 44% 42%

28% 27% 27% 27%

7% 8% 10% 11%

5% 7% 7% 6%

6% 5% 6% 5%

3% 4% 3% 4% 2% 3% 2% 3% 1% 1%

2013 2014 2015 2016

Morocco: a Growing Gateway Market

Company overview : the leading port operator in Morocco

Sound Financials

Growth opportunities

5

Business model of Marsa Maroc

Ships Dock Storage Truck unloading /

loading

Entry /

exit of the port

Import flows

Export flows

Maritime services (towing,

steering, boatage, etc.)

1

2

Handling (loading/unloading vessels and transfer of cargo

to storage area.)

Storage and Truck loading/

unloading

Other services : services to ships, weighing, etc.

3

90% of

turnover *

3% of

turnover *

7% of

turnover *

GATEWAY

Concession

agreements

Clients / suppliers

Third parties

Financing

contracts,

subcontracts, etc.

Business

contracts

• 9 ports via the concession contract with the ANP

• 1 terminal (TC3 Casablanca) conceded by the ANP

• 1 terminal (TC3 Tanger Med) conceded by TMPA

• 1 terminal (Quai Nord Agadir) conceded by ANP to a subsidiary controlled by Marsa Maroc (51%)

Port authorities

(*) 2016

6

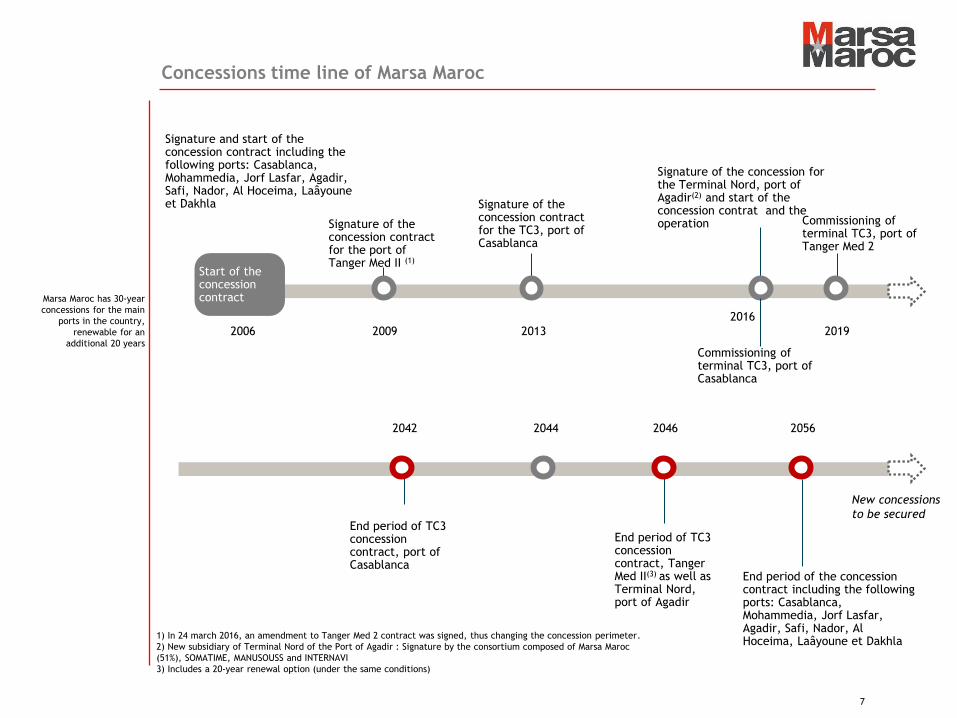

Marsa Maroc has 30-year

concessions for the main

ports in the country,

renewable for an

additional 20 years

2009 2006

Signature and start of the concession contract including the following ports: Casablanca, Mohammedia, Jorf Lasfar, Agadir, Safi, Nador, Al Hoceima, Laâyoune et Dakhla

2013 2019

Start of the concession contract

Commissioning of terminal TC3, port of Tanger Med 2

2016

Signature of the concession for the Terminal Nord, port of Agadir(2) and start of the concession contrat and the operation

1) In 24 march 2016, an amendment to Tanger Med 2 contract was signed, thus changing the concession perimeter.

2) New subsidiary of Terminal Nord of the Port of Agadir : Signature by the consortium composed of Marsa Maroc

(51%), SOMATIME, MANUSOUSS and INTERNAVI

3) Includes a 20-year renewal option (under the same conditions)

Signature of the concession contract for the TC3, port of Casablanca

End period of the concession contract including the following ports: Casablanca, Mohammedia, Jorf Lasfar, Agadir, Safi, Nador, Al Hoceima, Laâyoune et Dakhla

2044 2042 2046

End period of TC3 concession contract, port of Casablanca

2056

New concessions

to be secured

Signature of the concession contract for the port of Tanger Med II (1)

Commissioning of terminal TC3, port of Casablanca

End period of TC3 concession contract, Tanger Med II(3) as well as Terminal Nord, port of Agadir

Concessions time line of Marsa Maroc

7

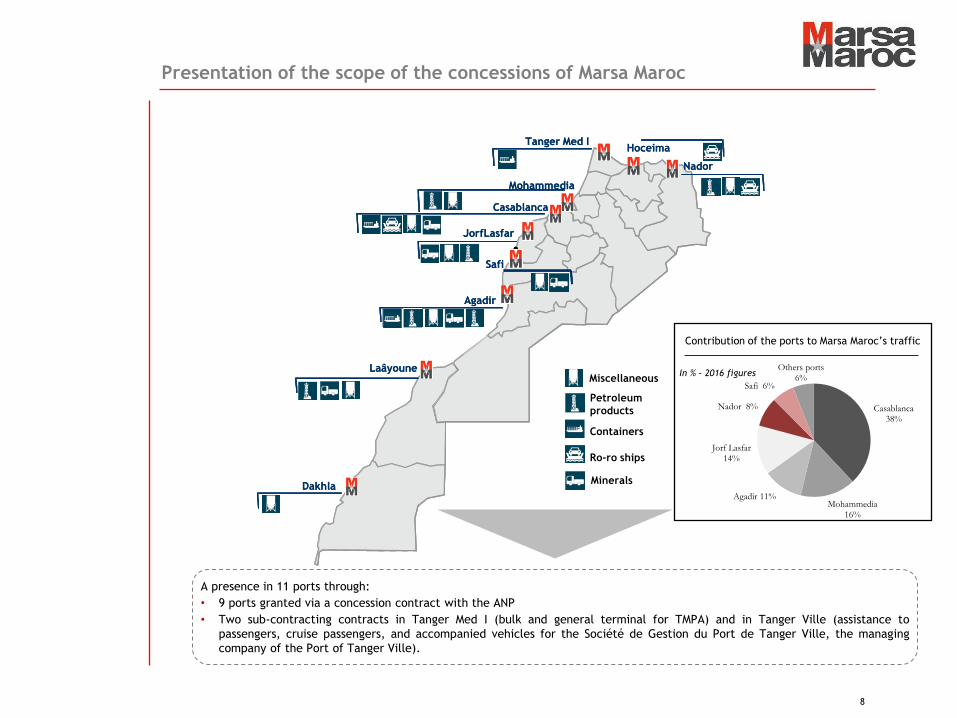

A presence in 11 ports through:

• 9 ports granted via a concession contract with the ANP

• Two sub-contracting contracts in Tanger Med I (bulk and general terminal for TMPA) and in Tanger Ville (assistance to

passengers, cruise passengers, and accompanied vehicles for the Société de Gestion du Port de Tanger Ville, the managing

company of the Port of Tanger Ville).

In % - 2016 figures

Contribution of the ports to Marsa Maroc’s traffic

Casablanca

Agadir

Tanger Med I

Dakhla

Mohammedia

Jorf Lasfar

Safi

Nador

Laâyoune

Minerals

Miscellaneous

Petroleum

products

Containers

Ro-ro ships

Hoceima

Casablanca

Agadir

Tanger Med I

Dakhla

Mohammedia

Jorf Lasfar

Safi

Nador

Laâyoune

Hoceima

Presentation of the scope of the concessions of Marsa Maroc

8

Casablanca 38%

Mohammedia 16%

Agadir 11%

Jorf Lasfar 14%

Nador 8%

Safi 6%

Others ports 6%

95 90

116 125

8 7

7

7

2013 2014 2015 2016

Vehicles and trucks TIR

505 533 537 624

143 160 170

192

62% 62% 62% 67%

0%

20%

40%

60%

80%

100%

120%

0

100

200

300

400

500

600

700

800

900

2013 2014 2015 2016

Casablanca Agadir Mkt share MM

15 487 15 186 11 742 10 235

11 120 13 780

13 057 14 497

3 040 2 835

3 287 3 350

2013 2014 2015 2016

Liquid bulk Dry bulk Conventional

Evolution of the overall traffic handled by Marsa Maroc Evolution of container traffic handled by Marsa Maroc

Evolution of bulk traffic Evolution of TIR and vehicle traffic

In thousand tons

650 694 707

29 647 31 801

28 086

In thousand tons

102 96

123

65

-13%

+11%

+2%

In thousand TEUs

In number of units 2013-2016 dry bulk CAGR : +9.2%

2013-2016 liquid bulk CAGR: -12.9%

2013-2016 conventional CAGR: +3.3%

2013-2016 CAGR: +0.5% 2013-2016 CAGR: 7.9%

A leader position in Morocco

2013-2016 CAGR: 9.1%

In 2015, liquid bulk

traffic decreased by

23% following the

shutdown of SAMIR’s

activity in August

2015, which also

explains the 8.4%

decline in the overall

traffic handled by

Marsa Maroc in 2015.

9

35 770 38 366

35 159 36 306

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

2013 2014 2015 2016

28 082

816

Impact of the national port development project on estimated Marsa Maroc’s traffics

Tanger ville

Casablanca

Nador

Jorf Lasfar LPG

Safi

Nador West Med

Mohammedia

Kenitra Atlantique

Jorf Lasfar

Tanger Med II

Agadir

Safi Grand

Vrac

Dakhla

Casablanca

Agadir

Tanger Med I & II

Mohammedia

Jorf LasfarSafi

Nador

Laâyoune

TanTan

Al Hoceima

Refined oil products

Refined oil products

Cereals

Cattle Feed

Cars (Peugeot Citroën)

Sulfur ;

Conventional Bulks

Coal

Coal

Oil products

Existing port

Port extension

New port

The port Capacities

reconfiguration as it is planned

by the 2030 national port

strategy adopted by the

Ministry of Equipment,

Transport and logistics should

involve the construction of new

terminals and port complexes.

Hence, these new additional

capacities could impact

partially or totally by handling

the Marsa Maroc historical

traffic in the new facilities

(new LPG and chemical

terminal at the port of

Mohammedia, new ports of

Safi, Nador West Med and

Kenitra, etc.).

The opening of new port infrastructures will lead to a new distribution of import/export traffics between the ports and

will involve a risk of migration of some traffics currently handled in Marsa Maroc terminals, towards new infrastructure.

10

A new governance structure

3 Core investors

(institutional)

President of the

Supervisory Board

The initial public offering in july 2016 has allow Marsa Maroc to strengthen its governance whilst providing a strong signal to the market

regarding the Moroccan State’s will to strengthen the Company’s governance. Hence, the new structure of the Supervisory Board include 12

board members :

Ministry of Equipment,

Transport and Logistics

Ministry of Economy

and Finance

Ministry of Equipment,

Transport and Logistics

A shareholders’

agreement has been

concluded between

the Government

and the 3 leading

institutional

investors.

Independent Board

Members *

• Pension funds ;

• MAD 111 bn assets

under

management**

• Pension funds ;

• MAD 98 bn assets

under

management**

• ≠1 Insurance company

in morocco ;

• MAD 31 assets under

management **

• USD 1.3 bn market

Capitalization (7th

october 2016)

(*) not apppointed yet at this stage

(**) end of June 2016

11

Morocco: a Growing Gateway Market

Company overview : the leading port operator in Morocco

Sound Financials

Growth opportunities

1 750 1 822 1 981 2 314

153 158 151

182

37 42 38

70

2013 2014 2015 2016

Handling services Services to vessels Others services

Turnover EBITDA

Operating income

Net income

Sound Financials

2013-2016 CAGR: +9.8%

+18%

2013-2016 CAGR: +20% 2013-2016 CAGR: +31%

2013-2016 CAGR: +11% 2016 was characterized by a

significant improvement in the

company’s performance,

thanks to a growth in turnover

driven by containers and

cereals trafics.

In MAD mn

In MAD mn

In MAD mn In MAD mn

13

1 939 2 023

2 171

2 567

844 886

1 010

1 155

44% 44%

47% 45%

30%

35%

40%

45%

50%

55%

60%

0

200

400

600

800

1000

1200

1400

2013 2014 2015 2016

EBITDA Margin (%)

481 499

622

830

25% 25%

29% 32%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

0

100

200

300

400

500

600

700

800

900

2013 2014 2015 2016

Operating income Margin (%)

256

329

375

580

13% 16% 17%

23%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

0

100

200

300

400

500

600

700

2013 2014 2015 2016

Net Income Margin (%)

Financial structure Breakdown of net debt

Sound Financials

Dividends

In MAD mn

In MAD mn

14

2 812

2 235

1 347

744

2015 2016

Total shareholder equity Net debt (excess of cash)

113 207

1 415

1 171

-181

-633

2015 2016

Cash Investment securities Corporate debt

272

398

488

740

235 294

882

587

87% 74%

181%

79%

0%

50%

100%

150%

200%

250%

300%

350%

400%

0

100

200

300

400

500

600

700

800

900

1 000

2013 2014 2015 2016

Net Income Dividend Pay out ratio

Morocco: a Growing Gateway Market

Company overview : the leading port operator in Morocco

Sound Financials

Growth opportunities

A growth strategic plan

Conditions for success and change management

• Concessions currently

under development

• Secure new concessions

and authorizations

• Concessions and

authorizations in Africa

• Hinterland logistics and

related activities

Leading port operator in

Morocco

Contribution to

enhancement of logistics in

Morocco

Performance and agility

Sales approach • Operational Performance

• Strategic management

• Communication and change

management

• Organizational effectiveness and HR

• Institutional governance

1

2

3 4

5 6

7 9

8 10

Strong international

presence, particularly in

Africa

The business plan does not take

into account the

implementation of the

Company's development

strategy including securing new

port concessions in Morocco

and in the African continent.

16

Q & A

19