PTTZ. activities ANS 1213 - osbornebooks.co.uk€¦ · answers to chapter activities 11 7.3 £ ......

12

Osborne Books Tutor Zone Personal Tax Finance Act 2016 Answers to chapter activities © Osborne Books Limited, 2016

Transcript of PTTZ. activities ANS 1213 - osbornebooks.co.uk€¦ · answers to chapter activities 11 7.3 £ ......

Osborne Books Tutor Zone

Personal TaxFinance Act 2016

Answers to chapter activities

© Osborne Books Limited, 2016

2 p e r s o n a l t a x ( F i n a n c e A c t 2 0 1 6 ) t u t o r z o n e

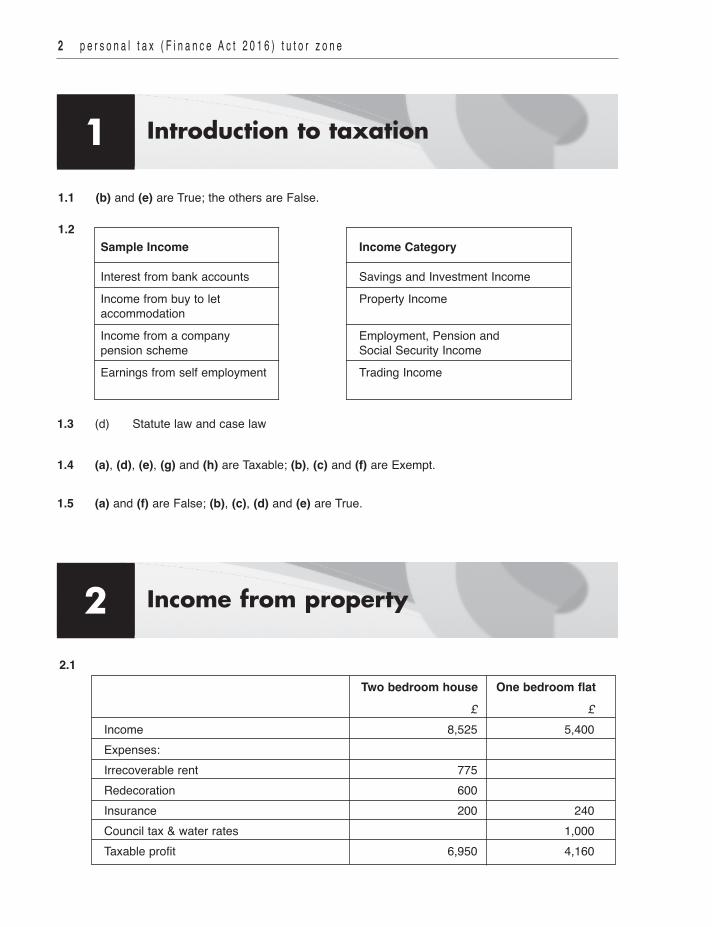

1.1 (b) and (e) are True; the others are False.

1.2Sample Income Income Category

Interest from bank accounts Savings and Investment IncomeIncome from buy to let Property IncomeaccommodationIncome from a company Employment, Pension and pension scheme Social Security IncomeEarnings from self employment Trading Income

1.3 (d) Statute law and case law

1.4 (a), (d), (e), (g) and (h) are Taxable; (b), (c) and (f) are Exempt.

1.5 (a) and (f) are False; (b), (c), (d) and (e) are True.

2.1 Two bedroom house One bedroom flat £ £Income 8,525 5,400Expenses:Irrecoverable rent 775Redecoration 600Insurance 200 240Council tax & water rates 1,000Taxable profit 6,950 4,160

Introduction to taxation1

Income from property2

a n s w e r s t o c h a p t e r a c t i v i t i e s 3

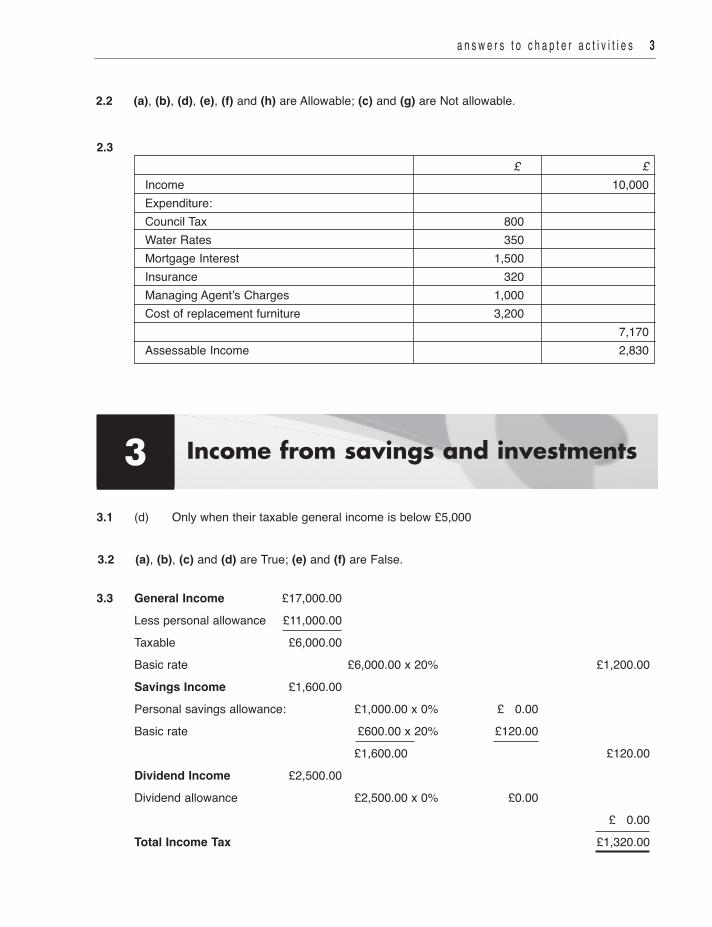

2.2 (a), (b), (d), (e), (f) and (h) are Allowable; (c) and (g) are Not allowable.

2.3

£ £Income 10,000Expenditure:Council Tax 800Water Rates 350Mortgage Interest 1,500Insurance 320Managing Agent’s Charges 1,000Cost of replacement furniture 3,200 7,170Assessable Income 2,830

Income from savings and investments3

3.1 (d) Only when their taxable general income is below £5,000

3.3 General Income £17,000.00Less personal allowance £11,000.00Taxable £6,000.00Basic rate £6,000.00 x 20% £1,200.00Savings Income £1,600.00Personal savings allowance: £1,000.00 x 0% £ 0.00Basic rate £600.00 x 20% £120.00 £1,600.00 £120.00Dividend Income £2,500.00Dividend allowance £2,500.00 x 0% £0.00 £ 0.00Total Income Tax £1,320.00

3.2 (a), (b), (c) and (d) are True; (e) and (f) are False.

4 p e r s o n a l t a x ( F i n a n c e A c t 2 0 1 6 ) t u t o r z o n e

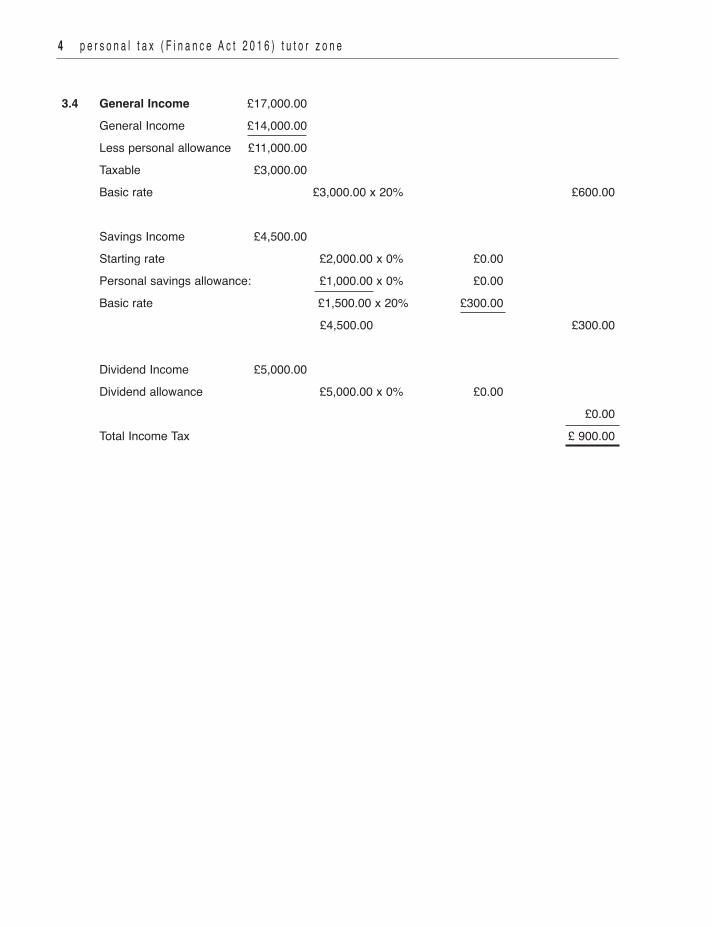

3.4 General Income £17,000.00General Income £14,000.00Less personal allowance £11,000.00Taxable £3,000.00Basic rate £3,000.00 x 20% £600.00

Savings Income £4,500.00Starting rate £2,000.00 x 0% £0.00Personal savings allowance: £1,000.00 x 0% £0.00Basic rate £1,500.00 x 20% £300.00 £4,500.00 £300.00

Dividend Income £5,000.00Dividend allowance £5,000.00 x 0% £0.00 £0.00Total Income Tax £ 900.00

a n s w e r s t o c h a p t e r a c t i v i t i e s 5

4.1 (a)

Ford Vauxhall

List Price £ £15,000 £14,500Car Benefit Percentage 28% 29%Car Benefit £ £4,200 £4,205Fuel Benefit £ £6,216 £6,438Total Benefit £ £10,416 £10,643

Note that the limit on private fuel imposed by the employer makes no difference to theassessable fuel benefit.

(b) The option with the lowest assessable benefit is the Ford.

Income from employment4

4.2 (b), (c) and (f) are Taxable; (a), (d), (e), (g) and (h) are Tax exempt.

4.3 (c) It reduces her tax by £160

4.4 Benefit / (Deduction) £Salary 30,000Company car benefit 2,800Company car fuel benefit 4,440Interest free loan benefit 420Professional subscription (200)Total assessable employment income 37,460

6 p e r s o n a l t a x ( F i n a n c e A c t 2 0 1 6 ) t u t o r z o n e

Preparing income tax computations5

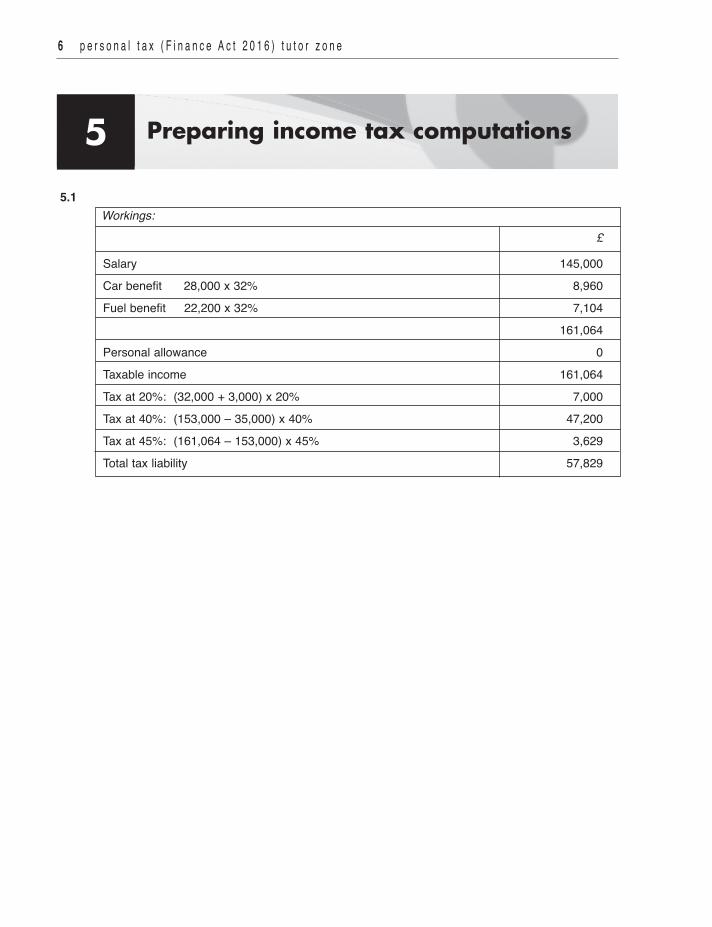

5.1Workings: £

Salary 145,000Car benefit 28,000 x 32% 8,960Fuel benefit 22,200 x 32% 7,104 161,064Personal allowance 0Taxable income 161,064Tax at 20%: (32,000 + 3,000) x 20% 7,000Tax at 40%: (153,000 – 35,000) x 40% 47,200Tax at 45%: (161,064 – 153,000) x 45% 3,629Total tax liability 57,829

a n s w e r s t o c h a p t e r a c t i v i t i e s 7

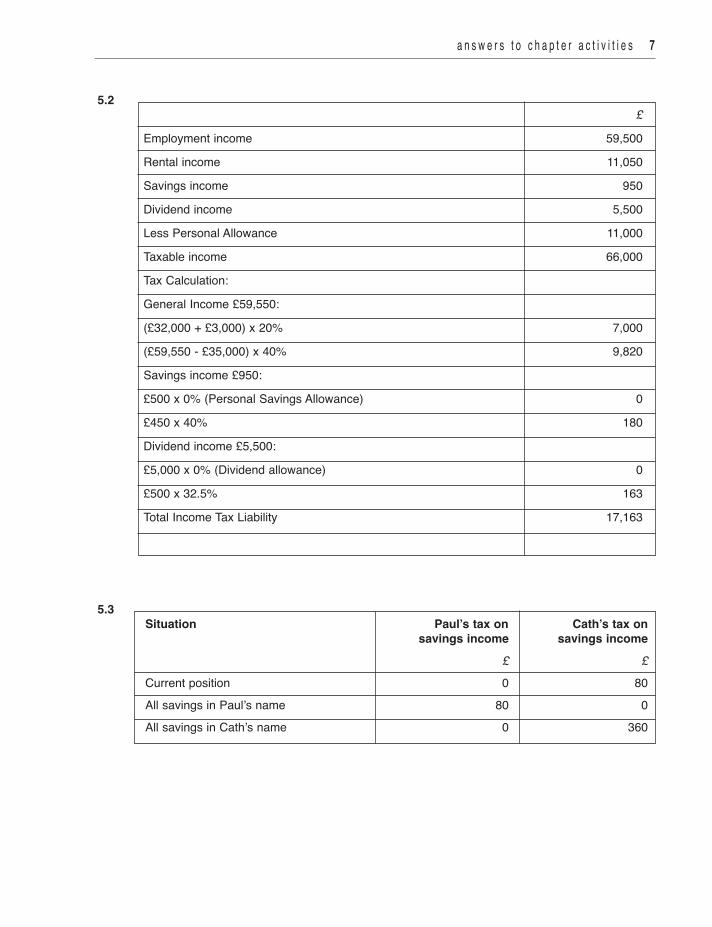

5.2 £Employment income 59,500Rental income 11,050Savings income 950Dividend income 5,500Less Personal Allowance 11,000Taxable income 66,000Tax Calculation: General Income £59,550: (£32,000 + £3,000) x 20% 7,000(£59,550 - £35,000) x 40% 9,820Savings income £950: £500 x 0% (Personal Savings Allowance) 0£450 x 40% 180Dividend income £5,500: £5,000 x 0% (Dividend allowance) 0£500 x 32.5% 163Total Income Tax Liability 17,163

5.3Situation Paul’s tax on Cath’s tax on savings income savings income £ £Current position 0 80All savings in Paul’s name 80 0All savings in Cath’s name 0 360

8 p e r s o n a l t a x ( F i n a n c e A c t 2 0 1 6 ) t u t o r z o n e

6.1 (a) (d) £4,920 (b) False

6.2 (b), (d) and (e) are True

6.3 (a) The gain on the asset is £11,600(b) The amount of loss that will be relieved is £500(c) The capital gains tax payable is £0(d) The loss to be carried forwards to the next tax year is £1,900

6.4 (a), (b), (d) and (h) are Chargeable; (c), (e), (f) and (g) are Exempt.

Capital gains tax6

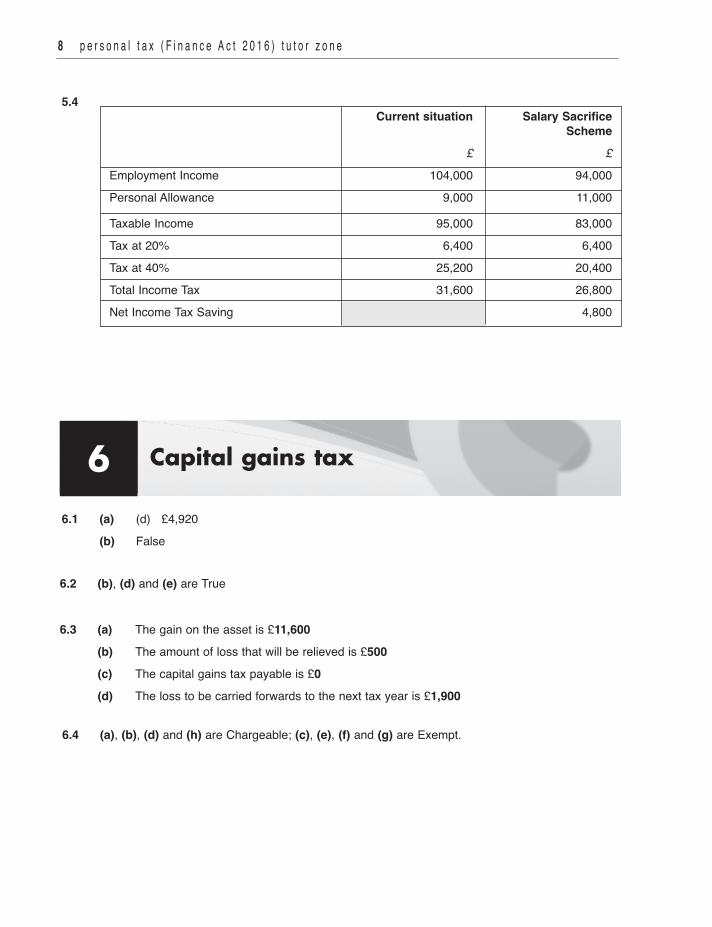

5.4 Current situation Salary Sacrifice Scheme £ £Employment Income 104,000 94,000Personal Allowance 9,000 11,000

Taxable Income 95,000 83,000Tax at 20% 6,400 6,400Tax at 40% 25,200 20,400Total Income Tax 31,600 26,800Net Income Tax Saving 4,800

a n s w e r s t o c h a p t e r a c t i v i t i e s 9

6.5 (a)

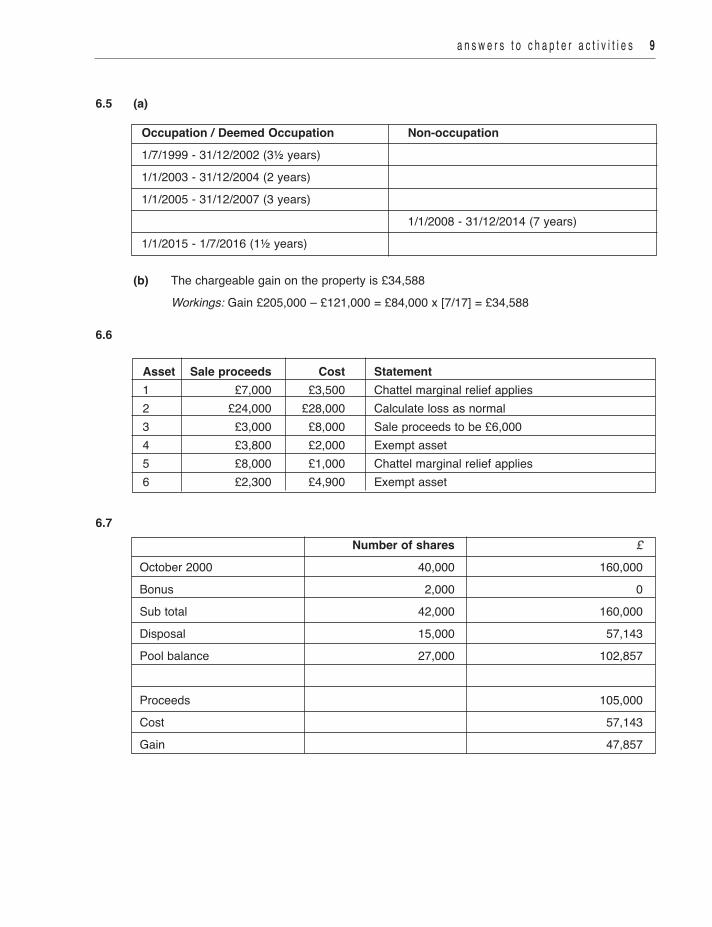

Occupation / Deemed Occupation Non-occupation1/7/1999 - 31/12/2002 (3½ years) 1/1/2003 - 31/12/2004 (2 years)1/1/2005 - 31/12/2007 (3 years) 1/1/2008 - 31/12/2014 (7 years)1/1/2015 - 1/7/2016 (1½ years)

(b) The chargeable gain on the property is £34,588 Workings: Gain £205,000 – £121,000 = £84,000 x [7/17] = £34,588

6.6

Asset Sale proceeds Cost Statement1 £7,000 £3,500 Chattel marginal relief applies2 £24,000 £28,000 Calculate loss as normal3 £3,000 £8,000 Sale proceeds to be £6,0004 £3,800 £2,000 Exempt asset5 £8,000 £1,000 Chattel marginal relief applies6 £2,300 £4,900 Exempt asset

6.7 Number of shares £October 2000 40,000 160,000Bonus 2,000 0Sub total 42,000 160,000Disposal 15,000 57,143Pool balance 27,000 102,857

Proceeds 105,000Cost 57,143Gain 47,857

1 0 p e r s o n a l t a x ( F i n a n c e A c t 2 0 1 6 ) t u t o r z o n e

Inheritance tax77.1 £

Inheritance Tax calculation:Estate 825,000Less exempt transfer to Peter (375,000)Less exempt transfer to charity (5,000)Less nil rate band (325,000)Amount subject to IHT 120,000Inheritance tax at 40% 48,000

Calculation of amount received by John: Estate 825,000Less exempt transfer to Peter (375,000)Less exempt transfer to charity (5,000)Less Inheritance Tax (48,000)Balance due to John 397,000

7.2 Morag’s estate:Estate 530,000Less exempt transfer to Patrick (£530,000 - £140,000) (390,000)Less nil rate band used (140,000)Amount subject to IHT 0Inheritance tax at 40% 0

Patrick’s estate:Estate 780,000Less nil rate band (£325,000 + (£325,000 – £140,000)) (510,000)Chargeable to IHT 270,000Inheritance Tax at 40% 108,000

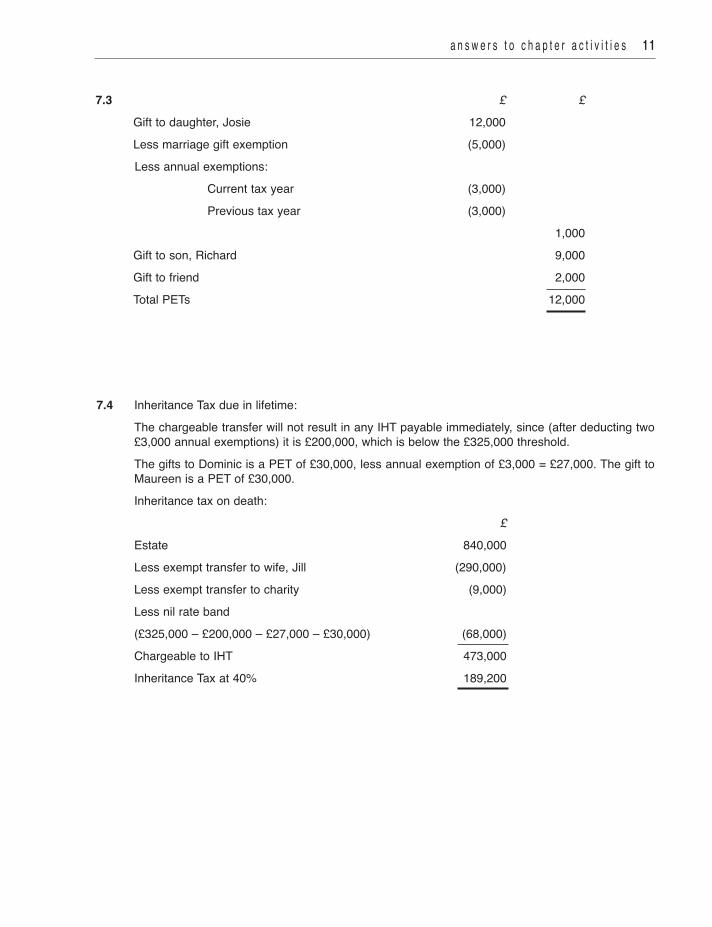

a n s w e r s t o c h a p t e r a c t i v i t i e s 1 1

7.3 £ £Gift to daughter, Josie 12,000Less marriage gift exemption (5,000)Less annual exemptions: Current tax year (3,000) Previous tax year (3,000) 1,000Gift to son, Richard 9,000Gift to friend 2,000Total PETs 12,000

7.4 Inheritance Tax due in lifetime:The chargeable transfer will not result in any IHT payable immediately, since (after deducting two£3,000 annual exemptions) it is £200,000, which is below the £325,000 threshold.The gifts to Dominic is a PET of £30,000, less annual exemption of £3,000 = £27,000. The gift toMaureen is a PET of £30,000.Inheritance tax on death: £Estate 840,000Less exempt transfer to wife, Jill (290,000) Less exempt transfer to charity (9,000)Less nil rate band (£325,000 – £200,000 – £27,000 – £30,000) (68,000)Chargeable to IHT 473,000Inheritance Tax at 40% 189,200

1 2 p e r s o n a l t a x ( F i n a n c e A c t 2 0 1 6 ) t u t o r z o n e

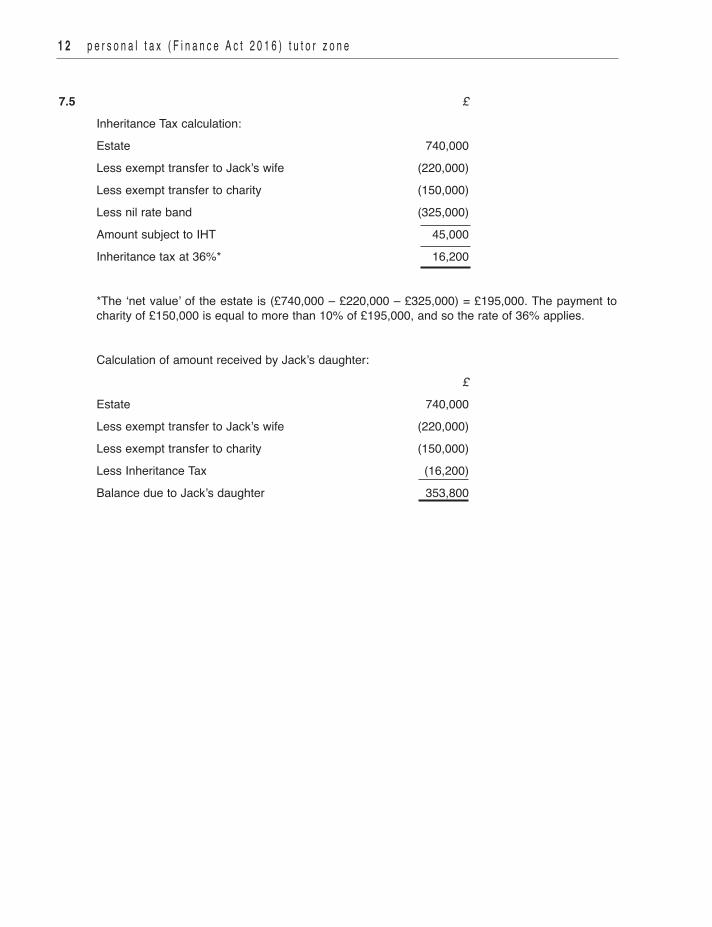

7.5 £Inheritance Tax calculation:Estate 740,000Less exempt transfer to Jack’s wife (220,000)Less exempt transfer to charity (150,000)Less nil rate band (325,000)Amount subject to IHT 45,000Inheritance tax at 36%* 16,200

*The ‘net value’ of the estate is (£740,000 – £220,000 – £325,000) = £195,000. The payment tocharity of £150,000 is equal to more than 10% of £195,000, and so the rate of 36% applies.

Calculation of amount received by Jack’s daughter: £Estate 740,000Less exempt transfer to Jack’s wife (220,000)Less exempt transfer to charity (150,000)Less Inheritance Tax (16,200)Balance due to Jack’s daughter 353,800