Property, plant and equipment. Academic Resource Center Property, plant, and equipment Page 2...

71

Property, plant and equipment

-

Upload

sibyl-wright -

Category

Documents

-

view

214 -

download

0

Transcript of Property, plant and equipment. Academic Resource Center Property, plant, and equipment Page 2...

Property, plant and equipment

Academic Resource Center

Property, plant, and equipment Page 2

Typical coverage of US GAAP

► Definition► Acquisition of PP&E:

► General► Self-constructed assets► Interest costs during construction

► Valuation at acquisition:► Exchange of non-monetary assets► Lump-sum purchases► Deferred payment contracts► Purchase paid for using company stock

► Costs incurred subsequent to acquisition

► Periodic valuation:► Carrying value► Impairment

Academic Resource Center

Property, plant, and equipment Page 3

Typical coverage of US GAAP

► Cost allocation issues:► Depreciation

► Definition► Useful life► Depreciable base► Depreciation method

► PPE Disposition:► Sale► Involuntary conversion

► Fully depreciated fixed assets

► Disclosure requirements

Academic Resource Center

Property, plant, and equipment Page 4

Executive summary

► IFRS permits periodic revaluation of an entire class of fixed assets to fair value. US GAAP does not allow revaluation.

► IFRS has a one-step approach for determining impairment of fixed assets while US GAAP has a two-step approach.

► IFRS allows reversal of impairment losses on fixed assets, while this is prohibited using US GAAP.

► IFRS requires depreciation of components of an asset when the components have different periods of benefit. Component depreciation is permissible using US GAAP but is not a common practice.

Academic Resource Center

Property, plant, and equipment Page 5

Primary pronouncements

US GAAP

► ASC 360, Property, Plant and Equipment

► ASC 410-20, Asset Retirement and Environmental Obligations-Asset Retirement Obligations

► ASC 835-20, Interest-Capitalization of Interest

IFRS

► IAS 16, Property, Plant and Equipment

► IAS 36, Impairment of Assets

Academic Resource Center

Property, plant, and equipment Page 6

Progress on convergence

► The FASB and IASB are working a joint project which focuses on impairment of financial assets. There is no current plan to expand this work to impairment of tangible assets. Convergence on other fixed-asset-related accounting matters is not planned at this time.

► The IASB issued an amendment to IAS 16, Clarification of Acceptable Methods of Depreciation and Amortisation, in May 2014. The guidance prohibits the use of a depreciation method that is based on revenue generated from the asset because this reflects future benefits generated from the asset instead of reflecting the expected consumption of future benefits from the asset. This results in divergence from current US GAAP.

Academic Resource Center

Property, plant, and equipment Page 7

Definition

PP&E includes long-term tangible assets acquired for use in operations and not for resale.

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 8

AcquisitionGeneral

PP&E should be recorded based on the fair value given up or the value received, whichever is more clearly evident.

Costs include purchase price and related taxes, directly attributable costs and estimated retirement obligation costs.

Similar

Similar

Costs that are not directly attributable should be expensed as a period cost.

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 9

Acquisition General

US GAAP

► Voluntary investments in safety or environmental equipment are capitalized.

IFRS

► Voluntary investments in safety or environmental equipment are expensed, unless they extend the economic life of the related asset or a constructive obligation exists to improve the asset’s safety or environmental standards.

Academic Resource Center

Property, plant, and equipment Page 10

Acquisition General

Example 1:

Clean Company wants to be viewed as the most environmentally friendly company in its industry. As a result, the company installs equipment on its smoke stacks to reduce emissions. The equipment costs $30,000 and has a three-year life.

► How would this equipment be accounted for using US GAAP and IFRS?

Academic Resource Center

Property, plant, and equipment Page 11

Example 1 solution:

Using US GAAP, this equipment would be capitalized and depreciated over its three-year life. Using IFRS, the $30,000 cost of this voluntary investment in environmental equipment might be expensed in year one, unless it extends the economic life of the smoke stacks or this expenditure fulfills a constructive obligation.

Acquisition General

Academic Resource Center

Property, plant, and equipment Page 12

Acquisition Self-constructed assets

Direct cost of materials and labor should be capitalized.

A portion of indirect costs can be included in capitalized costs.

Similar

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 13

Acquisition Interest costs during construction

The qualifying asset must take a period of time to complete.

Interest capitalization commences and continues as long as expenditures and progress are made to get the asset ready for its intended use.

Similar, although IFRS says a “substantial” period of time.

Similar

Capitalizable interest is based on specific borrowing if available or weighted-average costs of borrowings, and cannot exceed actual interest for the period.

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 14

Acquisition Interest costs during construction

US GAAP► Interest costs are capitalized to the extent

that these costs could have been avoided had the expenditures been used to repay the debt rather than to acquire or construct the asset.

IFRS► Borrowing costs related to a loan obtained

specifically to acquire or construct the asset are capitalized in their entirety (reduced by any income from temporary investment of these funds).

► Borrowing costs related to funds obtained for a purpose other than acquisition or construction of the asset are determined by applying an average capitalization rate to the expenditures on the asset.

Academic Resource Center

Property, plant, and equipment Page 15

Acquisition Interest costs during construction

US GAAP► Interest revenue cannot be netted against

interest cost.

IFRS► Interest revenue is netted against interest

cost. When funds borrowed to finance the acquisition of a qualified asset are temporarily invested, the interest cost should be reduced by any investment income earned on these funds.

Academic Resource Center

Property, plant, and equipment Page 16

AcquisitionInterest costs during construction

US GAAP

► Exchange rate differences on borrowing costs cannot be included in capitalizable interest costs.

IFRS

► Exchange rate differences related to foreign currency borrowings to the extent they are an adjustment to interest costs can be capitalized using IAS 23.

Academic Resource Center

Property, plant, and equipment Page 17

Example 2:

To finance construction of a qualifying asset, the company borrows $250,000 on January 1, 2013, at an interest rate of 8%. The company makes the following disbursements during the 24-month construction period: $100,000 on January 1, 2013; $50,000 on June 30, 2013; $50,000 on January 1, 2014, and $50,000 on June 30, 2014. Construction of the asset is completed on December 31, 2014, and it is ready for its intended use. During the construction period, excess funds are invested, which earn 5% in 2013 and 4% in 2014.

► What is the amount of interest that should be capitalized using US GAAP and IFRS?

AcquisitionInterest costs during construction

Academic Resource Center

Property, plant, and equipment Page 18

Example 2 solution:

US GAAP: The interest cost capitalized for the two-year period of $28,000 is calculated by determining the portion of the interest cost the company incurs during the construction of the building that theoretically could have been avoided. Interest revenue is not netted against interest expense.

AcquisitionInterest costs during construction

Date Amount disbursedMonths

outstandingWeighted

disbursement

January 1, 2011 $ 100,000 24/12 $ 200,000

June 30, 2011 50,000 18/12 75,000

January 1, 2012 50,000 12/12 50,000

June 30, 2012 50,000 6/12 25,000

Weighted-average accumulated expenditures $ 350,000

Interest capitalized at an 8% interest rate $ 28,000

Academic Resource Center

Property, plant, and equipment Page 19

Example 2 solution (continued):

IFRS: IAS 23 allows all the interest cost incurred of $40,000 (250,000 x 8% x 2 years) to be capitalized less the income earned from temporary investment of those borrowings (paragraph 12). Therefore, under IFRS, the investment income earned is calculated as follows:

Thus, the net interest cost to be capitalized for this asset is $32,750 ($40,000-$7,250) using IFRS.

AcquisitionInterest costs during construction

Date Amount available Earnings rate Year Investment income

January 1, 2013 $ 150,000 5% 1/2 $ 3,750

June 30, 2013 100,000 5% 1/2 2,500

January 1, 2014 50,000 4% 1/2 1,000

June 30, 2014 – 0% 1/2 –

$ 7,250

Academic Resource Center

Property, plant, and equipment Page 20

Example 3:

To construct an asset, a French company borrows US dollars during a 24-month construction period of: $100,000 on January 1, 2013; $50,000 on June 30, 2013; $50,000 on January 1, 2014; and $50,000 on June 30, 2014. Construction of the asset is completed on December 31, 2014, and it is ready for its intended use. The specific interest rate on this borrowing is 8% with the amounts being borrowed as the expenditures are made. On December 31, 2014, the French company uses euros to repay its US-dollar loan and incurs an exchange loss of $5,000.

► What costs should be capitalized using US GAAP and IFRS?

AcquisitionInterest costs during construction

Academic Resource Center

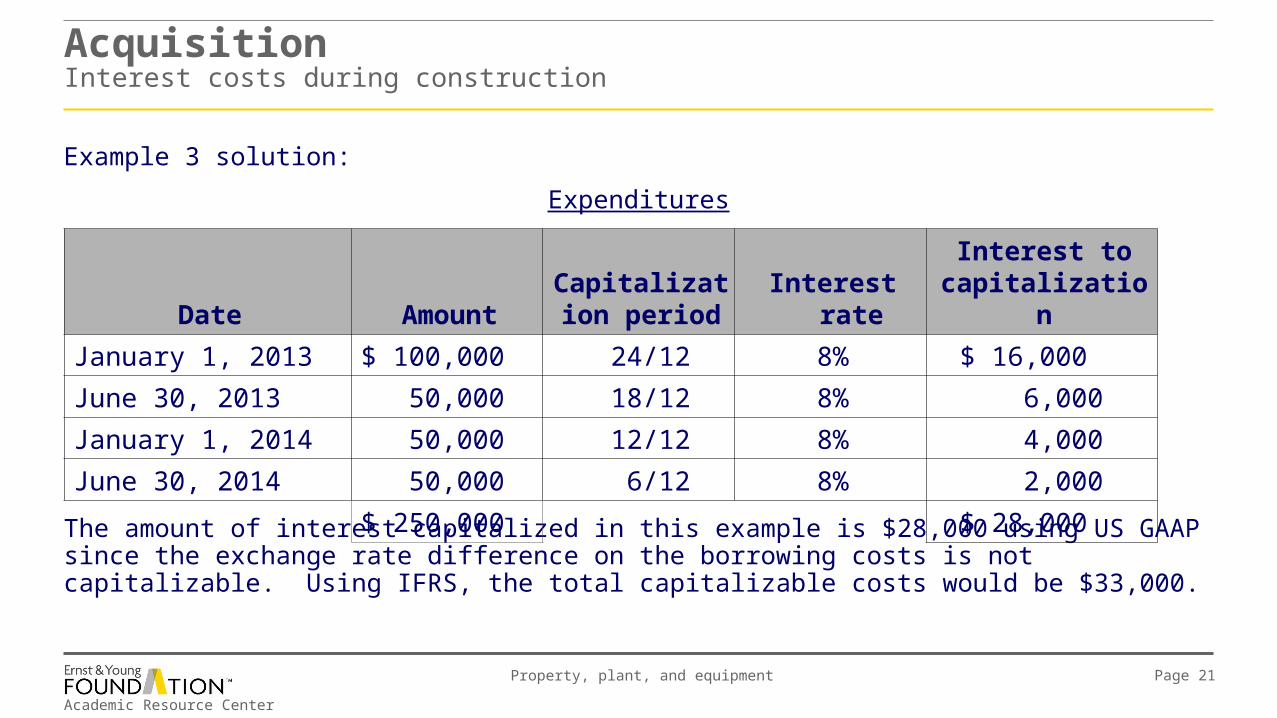

Property, plant, and equipment Page 21

Example 3 solution:

Expenditures

The amount of interest capitalized in this example is $28,000 using US GAAP since the exchange rate difference on the borrowing costs is not capitalizable. Using IFRS, the total capitalizable costs would be $33,000.

AcquisitionInterest costs during construction

Date AmountCapitalization

period Interest rateInterest to

capitalization

January 1, 2013 $ 100,000 24/12 8% $ 16,000

June 30, 2013 50,000 18/12 8% 6,000

January 1, 2014 50,000 12/12 8% 4,000

June 30, 2014 50,000 6/12 8% 2,000

$ 250,000 $ 28,000

Academic Resource Center

Property, plant, and equipment Page 22

Valuation at acquisitionExchange of non-monetary assets

Valuation should be based on fair value given up or fair value received, whichever is more clearly evident.

If the transaction has commercial substance, any related gain or loss should be recognized in income.

Similar

Similar

If the exchange lacks commercial substance, losses should be recognized immediately and gains should be deferred if no cash is received as part of the exchange.

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 23

Valuation at acquisitionExchange of non-monetary assets

US GAAP► If the exchange lacks commercial

substance and some cash is received, a portion of the gain can be recognized:

► The formula for recognizing gain is: (cash received/(fair value of assets received plus cash received)) x total gain.

► When cash represents 25% or more of the exchanged value, the transaction should be accounted for as a monetary exchange.

IFRS► The value of the acquired item is

measured at fair value except when the exchange lacks commercial substance or the fair value of both the asset received and the asset given up cannot be reliably determined. If the exchange lacks commercial substance or the fair value of neither asset is reliably measurable, then the cost is measured as the cost of the asset given up. In this case, this would result in gains being deferred using IFRS.

Academic Resource Center

Property, plant, and equipment Page 24

Example 4:

A company exchanges two used printing presses with a total net book value of $24,000 ($40,000 cost less accumulated depreciation of $16,000) for a new printing press with a fair value of $24,000 and $3,000 in cash. The fair value of the two used printing presses is $27,000. The transaction is deemed to lack commercial substance.

► What gain or loss would be recognized using US GAAP and IFRS? Show corresponding journal entries.

Valuation at acquisitionExchange of non-monetary assets

Academic Resource Center

Property, plant, and equipment Page 25

Example 4 solution:

The portion of the gain to be recognized using US GAAP would be computed as follows: cash received of $3,000/(fair value of assets of $24,000 + cash received of $3,000) x total the gain of $3,000 = recognized gain of $333.

New printing press $ 21,333Cash 3,000Accumulated depreciation 16,000

Old printing presses $ 40,000Gain on disposal 333

The cost of the new printing press is the $24,000 fair value reduced by the unrecognized gain of $2,667.

Valuation at acquisitionExchange of non-monetary assets

Academic Resource Center

Property, plant, and equipment Page 26

Example 4 solution (continued):

Using IFRS, no gain would be recognized since the transaction lacks commercial substance. The entry would be as follows:

New printing press $ 21,000Cash 3,000Accumulated depreciation 16,000

Old printing presses $ 40,000

If there is a computed loss on the exchange, recognize the amount of the loss immediately.

Valuation at acquisitionExchange of non-monetary assets

Academic Resource Center

Property, plant, and equipment Page 27

Valuation at acquisitionLump-sum purchases

Allocate lump-sum purchase costs based on the relative fair value of the assets acquired. Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 28

Valuation at acquisitionDeferred payment contracts

The asset is recorded at the present value of the asset on the date of acquisition.

Financing costs should be treated as period interest costs and expensed.

Similar

Similar

While there are some minor differences, there are no significant differences.

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 29

Valuation at acquisitionPurchases paid for using company stock

If the fair value of the company’s stock can be reliably determined, then the fair value of the company’s stock given up in the exchange is used as the value of the asset received, unless the fair value of the asset received is more clearly evident.

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 30

Costs incurred subsequent to acquisition

These costs should be capitalized if the useful life is extended, items produced are enhanced or the quantity produced has increased.

Similarly, IAS 16 applies the same principles in accounting for initial costs or subsequent expenditures on fixed assets.

Recurring maintenance and repairs that do not benefit future periods should be expensed.

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 31

Periodic valuationCarrying value

Assuming no impairment, PP&E is valued using the cost method at cost less accumulated depreciation.

Similar, although this is a permitted and not required method.

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 32

Periodic valuationCarrying value

US GAAP► Revaluation of

fixed assets is not allowed.

IFRS► A company can choose to account for PP&E and natural resources

at fair value using the revaluation method:► Cost or fair value must be applied to an entire class of PP&E.► Different classes can have different policies.► Fair value is the amount at which an asset could be exchanged in an

arm’s length transaction between knowledgeable and willing parties.► A professional appraiser may be used to establish fair value.► Revaluations must be performed periodically to ensure the carrying value

of that asset class is not materially different than its fair value.

Academic Resource Center

Property, plant, and equipment Page 33

Periodic valuationCarrying value

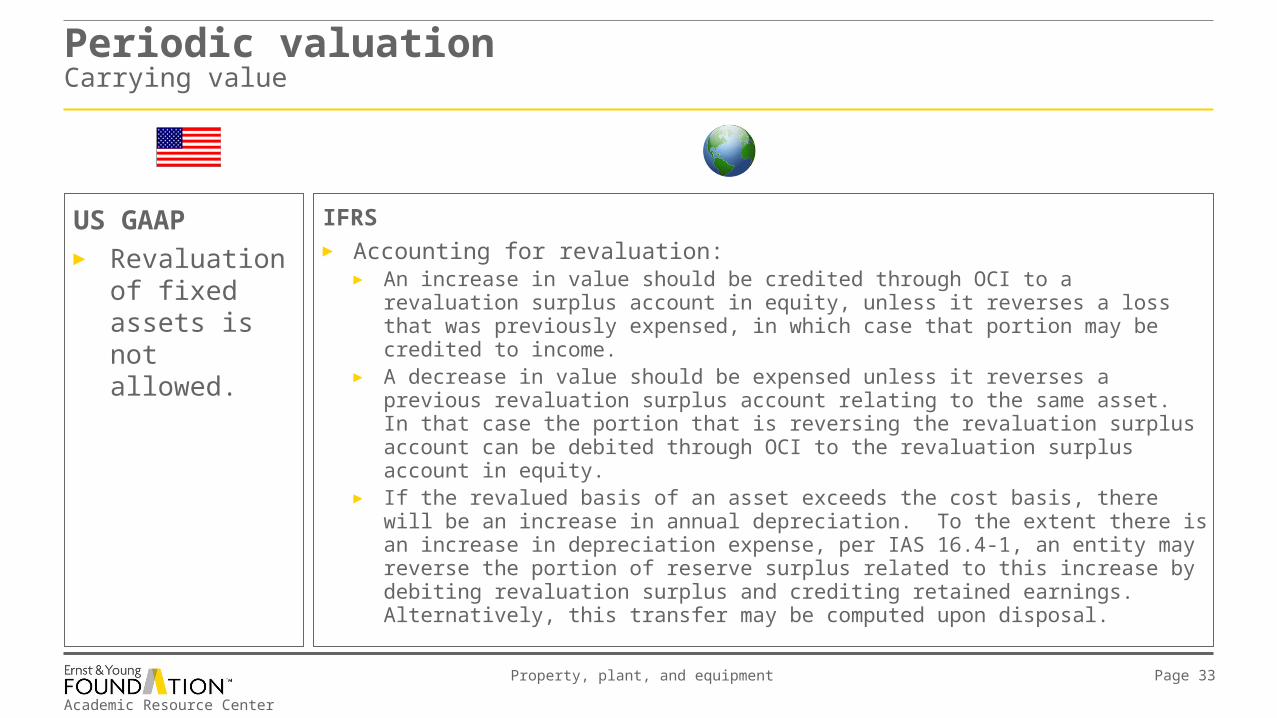

IFRS► Accounting for revaluation:

► An increase in value should be credited through OCI to a revaluation surplus account in equity, unless it reverses a loss that was previously expensed, in which case that portion may be credited to income.

► A decrease in value should be expensed unless it reverses a previous revaluation surplus account relating to the same asset. In that case the portion that is reversing the revaluation surplus account can be debited through OCI to the revaluation surplus account in equity.

► If the revalued basis of an asset exceeds the cost basis, there will be an increase in annual depreciation. To the extent there is an increase in depreciation expense, per IAS 16.4-1, an entity may reverse the portion of reserve surplus related to this increase by debiting revaluation surplus and crediting retained earnings. Alternatively, this transfer may be computed upon disposal.

US GAAP► Revaluation of

fixed assets is not allowed.

Academic Resource Center

Property, plant, and equipment Page 34

Periodic valuationCarrying value

IFRS► Accounting for revaluation (continued):

► When an asset is disposed of, any remaining related revaluation surplus account in equity may be transferred to retained earnings. The revaluation surplus can never be credited to income.

► If an asset is revalued, an entity may account for the accumulated depreciation at the date of revaluation in two ways:► Depreciation elimination method: The accumulated depreciation can

be eliminated against the asset itself.► Proportionate restatement method: The accumulated depreciation

can be restated proportionately with the change in the gross carrying value of the asset so that the carrying value of the asset after revaluation equals its revalued amount.

US GAAP► Revaluation of

fixed assets is not allowed.

Academic Resource Center

Property, plant, and equipment Page 35

Periodic valuationCarrying value

US GAAP► Revaluation of fixed

assets is not allowed.

IFRS► In 2006, Ernst & Young LLP provided an overview of 65 selected

large, multinational companies reporting using IFRS. Only one company used the revaluation option for any of its PP&E.

► In a recent study, Hans B. Christensen and Valeri Nikolaev of the University of Chicago Booth School of Business looked at the valuation choices made by 1,539 German and UK companies in the first year of preparing IFRS financial statements. They found that only 3% of the companies chose to use fair value accounting for at least one class of assets.

Academic Resource Center

Property, plant, and equipment Page 36

Example 5:

A company that reports using IFRS acquired weight-lifting equipment on January 1, 2013, at a cost of $10,000. This is the company’s only equipment. The company uses fair value for its equipment using IAS 16. On December 31, 2014, the net book value is $8,000 (cost of $10,000 less accumulated depreciation of $2,000), while the fair value is determined to be $8,800.

► What journal entries would be required to record the revaluations in 2014?

Periodic valuationCarrying value

Academic Resource Center

Property, plant, and equipment Page 37

Example 5 solution:

Accumulated depreciation $ 2,000Equipment $ 2,000

(To eliminate accumulated depreciation.)

Equipment $ 800Revaluation surplus – equipment (OCI) $ 800

(To write equipment up to fair value.)

Periodic valuationCarrying value

Academic Resource Center

Property, plant, and equipment Page 38

Example 6:

A company that reports using IFRS acquired an excavator on January 1, 2012, at a cost of $10,000. This excavator represents the company’s only piece of equipment. The company uses fair value for its equipment using IAS 16. This excavator is being depreciated on a straight-line basis over its 10-year useful life. There is no residual value at the end of the 10-year period. In both 2012 and 2013, depreciation would be $1,000. On December 31, 2013, the fair value is determined to be $8,800. On December 31, 2015, the fair value is determined to be $5,000. The company’s accounting policy is to reverse a portion of revaluation surplus related to the increased depreciation expense.

► Determine what accounts would be impacted if this activity is recorded for 2012 through 2015.

Periodic valuationCarrying value

Academic Resource Center

Property, plant, and equipment Page 39

Periodic valuationCarrying value

Example 6 solution:

Date CostDepreciation

expenseAccumulated depreciation Net

Revaluation surplus (OCI) Expense

Retained earnings

January 1, 2012 $10,000 $ – $ – $10,000 $ – $ – $ –

December 31, 2012 10,000 1,000 (1,000) 9,000 – – –

December 31, 2013 10,000 1,000 (2,000) 8,000 – – –

Revalue (1,200) 2,000 800 (800) – –

8,800 – 8,800 – –

December 31, 2014 8,800 1,100 (1,100) 7,700 (700) – (100)

December 31, 2015 8,800 1,100 (2,200) 6,600 (600) – (200)

Revalue (3,800) 2,200 (1,600) 600 1,000

$ 5,000 $ – $ 5,000 $ – $ 1,000 $ (200)

Academic Resource Center

Property, plant, and equipment Page 40

Periodic valuationCarrying value

Example 6 solution (continued):2012:Equipment $ 10,000

Cash $ 10,000(To record purchase of equipment.)

Depreciation expense $ 1,000Accumulated depreciation $ 1,000

(To record depreciation.)

2013:Depreciation expense $ 1,000

Accumulated depreciation $ 1,000(To record depreciation.)

Accumulated depreciation $ 2,000Equipment $ 1,200Revaluation surplus – equipment (OCI) 800

(To record revaluation.)

2014:Depreciation expense $ 1,100

Accumulated depreciation $ 1,100(To record depreciation.) Revaluation surplus – equipment (OCI) $ 100

Retained earnings $ 100(To reverse portion of reserve surplus related to increased depreciation expense. Note that this journal entry is optional.)

Academic Resource Center

Property, plant, and equipment Page 41

Periodic valuationCarrying value

Example 6 solution (continued):2015:Depreciation expense $ 1,100

Accumulated depreciation $ 1,100(To record depreciation.) Revaluation surplus – equipment (OCI) $ 100

Retained earnings $ 100(To reverse portion of reserve surplus related to increased depreciation expense. Note that this journal entry is optional.)

Accumulated depreciation $ 2,200Revaluation surplus – equipment (OCI) 600Loss 1,000

Equipment $ 3,800(To record devaluation of equipment.)

Academic Resource Center

Property, plant, and equipment Page 42

Periodic valuation Impairment

Impairment indicators for an asset include such items as significant change in its use, projected losses related to its use, a significant decline in its market value, etc.

An impaired asset must be written down, and the charge is recorded in income.

Similar

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 43

Periodic valuationImpairment – impairment indicators and recoverability test

US GAAP

► ASC 360-10-35-21 requires a review for impairment indicators in PP&E “whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable.”

► A recoverability test is required:

► If the carrying amount of the asset exceeds the sum of the expected net future undiscounted cash flows, then the asset is not recoverable and an impairment loss must be calculated.

IFRS

► IAS 36 requires an entity to assess annually whether there are any indicators of impairment.

► There is no recoverability test, simply calculate an impairment loss if impairment indicators are present.

Academic Resource Center

Property, plant, and equipment Page 44

Periodic valuationImpairment – calculating the impairment loss

US GAAP

► The impairment loss is the excess of the carrying value of the asset compared to its fair value (with fair value calculated according to ASC 820-10-35).

► Note that per ASC 820-10-35-9B, transaction costs (selling costs) are not included in the determination of fair value; however, these costs would be used to help determine the most advantageous market per ASC 820-10-55-45 to then determine the appropriate fair value for that market.

IFRS

► IAS 36 determines the impairment loss as the excess of the carrying value of the asset over its recoverable amount:

► The recoverable amount is the higher of the fair value less costs to sell or value in use (the discounted net present value of expected future cash flows from the asset).

Academic Resource Center

Property, plant, and equipment Page 45

Periodic valuationImpairment – recording the impairment loss

US GAAP

► The impairment loss is always reported through net income.

IFRS

► The impairment loss is recognized in OCI to the extent that it is reversing a prior upward revaluation. Otherwise, it is included in net income.

Academic Resource Center

Property, plant, and equipment Page 46

Periodic valuationImpairment – reversal of the impairment loss

US GAAP

► A reversal of the impairment loss is prohibited.

IFRS

► The impairment loss can be reversed up to the newly calculated recoverable amount, but it cannot exceed what the original carrying amount, net of depreciation, would have been.

Academic Resource Center

Property, plant, and equipment Page 47

Periodic valuationImpairment

Example 7:

On January 1, 20011, a company acquired a piece of equipment for $100,000. It was decided that the equipment would be depreciated over ten years with zero salvage value. At December 31, 2014, the equipment has significantly decreased in value due to technological innovations in the industry in which the company operates. The current carrying value of the equipment is $60,000 ($100,000 cost less $40,000 of accumulated depreciation). The expected future undiscounted cash flows from the use of this equipment are $61,000. The discounted net present value of expected cash flows from this piece of equipment is $51,000. Additionally, the fair value of the piece of equipment is $50,000 and the selling costs are minimal.

► Is the equipment impaired under either US GAAP or IFRS?

Academic Resource Center

Property, plant, and equipment Page 48

Periodic valuationImpairment

Example 7 solution:

Using US GAAP, the carrying value of the equipment of $60,000 is less than the expected future undiscounted cash flows of $61,000, so the equipment is not impaired.

Using IFRS, the equipment is impaired because the carrying value of $60,000 is greater than the recoverable amount of $51,000.

Academic Resource Center

Property, plant, and equipment Page 49

Periodic valuationImpairment

Example 8:

Use the same facts as the previous example, except the expected future undiscounted cash flows from the use of this equipment are $59,000.

► What, if any, impairment loss should be recorded using US GAAP and IFRS?

► Show any required journal entries.

Academic Resource Center

Property, plant, and equipment Page 50

Periodic valuationImpairment

Example 8 solution:

Using US GAAP, the piece of equipment now fails the recoverability test. The $60,000 carrying value of the equipment exceeds the sum of the expected net future undiscounted cash flows of $59,000. Therefore, an impairment loss must be calculated. The impairment loss is the difference between the carrying value of $60,000 and the fair value of $50,000. A $10,000 impairment loss would be recorded as follows:

Impairment loss $ 10,000Equipment $ 10,000

Using IFRS, there are impairment indicators so an impairment loss must be calculated. Using IAS 36, the recoverable amount is $51,000 (the higher of the net fair value of $50,000 or the discounted net present value of the cash flows of $51,000). Therefore, a $9,000 impairment loss needs to be recorded as follows:

Impairment loss $ 9,000Equipment* $ 9,000

*Note that the credit could be recorded to an accumulated impairment loss account instead of being recorded directly to the asset account. This would allow management to easily track accumulated impairment losses for potential reversal as discussed in example 9.

Academic Resource Center

Property, plant, and equipment Page 51

Example 9:

Use the same facts as the previous example, except in 2016 it is discovered that the technological innovations related to this piece of equipment are not effective. As a result, the fair value of this piece of equipment is now $41,000. The discounted net present value of expected cash flows from this piece of equipment is also $41,000.

► Using IFRS, what amount of the original impairment loss of $9,000 can be reversed?

► Show any required journal entries to reverse the impairment loss.

Periodic valuationImpairment

Academic Resource Center

Property, plant, and equipment Page 52

Example 9 solution: The impairment loss can be reversed up to the newly calculated recoverable amount of 41,000, but it cannot exceed what the original carrying amount, net of depreciation, would have been.

Impaired Not impaired

Net asset value 2014 $ 60,000 $ 60,000Impairment 2014 (9,000)

51,000Depreciation 2015 $51,000/(6) (8,500) (10,000)Depreciation 2016 $51,000/(6) (8,500) (10,000)

34,000 $ 40,000Reversal of impairment loss 6,000

$ 40,000

Equipment* $ 6,000Impairment loss $ 6,000

Periodic valuationImpairment

*Note that if the impairment was initially credited to an accumulated impairment loss account instead of being recorded directly to the asset account , the accumulated impairment loss account would be debited instead of the asset account.

Academic Resource Center

Property, plant, and equipment Page 53

Cost allocation issuesDepreciation

Definition: the systematic and rational manner of allocating the cost of a tangible asset to expense over the asset’s expected life.

Useful life: the expected service period of the asset, which could be shorter than its physical life.

Similar

Similar

Depreciable base: if the cost basis is used, then the depreciable base is the cost of the asset less the estimated salvage value.

Similar, but IFRS requires each significant component of an asset to be identified and its depreciable base to be determined.

Depreciation method: attempt to match the cost of an asset to the period benefited from the use of the asset. Typical methods are the straight-line method, the units-of-production method and various accelerated methods.

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 54

Cost allocation issuesDepreciation

US GAAP

► Depreciable base: component depreciation is allowed, but is rarely done because it complicates the accounting.

IFRS

► Depreciable base: requires separate depreciation for each component part of property, plant, and equipment that is significant to the overall cost of the item.

Academic Resource Center

Property, plant, and equipment Page 55

Example 10:

A company acquires a truck at a cost of $60,000. The service life is expected to be four years. Based on reliable historical data, the company believes the truck can be sold at the end of four years for $10,000. Additionally, the tires must be replaced every two years. The transmission must be replaced every three years. On the initial date of acquisition, the tires have a cost of $4,000 and the transmission has a cost of $6,000.

► What is the depreciable base and service life using US GAAP and IFRS? Assume the company chooses not to use component depreciation using US GAAP.

Cost allocation issuesDepreciation

Academic Resource Center

Property, plant, and equipment Page 56

Example 10 solution:

Depreciable base

Service life US GAAP IFRSTruck 4 years $ 50,000 $ 40,000Tires 2 years – 4,000Transmission 3 years – 6,000

$ 50,000 $ 50,000

Cost allocation issuesDepreciation

Academic Resource Center

Property, plant, and equipment Page 57

Example 11:

Use the same facts as the previous example. Assume straight-line depreciation and compute the depreciation expense in year one using US GAAP and IFRS. Assume that all of the salvage value is assigned to the truck itself and none to the tires or transmission.

Cost allocation issuesDepreciation

Academic Resource Center

Property, plant, and equipment Page 58

Example 11 solution:

Service lifeTruck 4 years $ 50,000 $ 12,500

Service lifeTruck 4 years $ 40,000 $ 10,000Tires 2 years 4,000 2,000Transmission 3 years 6,000 2,000

$ 50,000 $ 14,000

US GAAP US GAAPdepreciable depreciation

base expense

IFRS IFRSdepreciable depreciation

base expense

Cost allocation issuesDepreciation

Academic Resource Center

Property, plant, and equipment Page 59

DispositionSale

Gain or loss is calculated based on the asset’s net cost less the sales proceeds. Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 60

DispositionSale

US GAAP► The revaluation method is not allowed.

IFRS► If the revaluation method is used, the

accounting for a sale may be slightly different, as follows:► If the revaluation resulted in a write-down of

the asset, then the gain or loss on the sale is calculated based on the sales proceeds less the net adjusted asset value.

► If the revaluation resulted in a write-up of the asset, then the revaluation surplus account can be reversed to retained earnings.

There are no significant differences if the cost method is used.

Academic Resource Center

Property, plant, and equipment Page 61

Example 12:

A company acquired its only building on January 1, 2012, at a cost of $4 million. The building has a 20-year life and is being depreciated on a straight-line basis. On December 31, 2013, the net book value of the building was $3.6 million. The company revalued the building when the fair value of the building was $3.78 million on December 31, 2013. On December 31, 2015, the company sold the building for $3.6 million.

The company’s accounting policy is to reverse a portion of the surplus account related to increased depreciation expense.

► Determine what accounts would be impacted and, in table format, show the activity for the years 2012 through 2015.

► Show the journal entry to record the sale.

DispositionSale

Academic Resource Center

Property, plant, and equipment Page 62

DispositionSale

Example 12 solution:

* Calculated as $3,780,000 NBV divided by remaining 18-year life.

Date CostAccumulated depreciation Net

Surplus account in

equity - OCI IncomeRetained earnings

January 1, 2012 $ 4,000,000 $ 4,000,000

December 31, 2012 4,000,000 $ (200,000) 3,800,000

December 31, 2013 4,000,000 (400,000) 3,600,000

December 31, 2013 (220,000) 400,000 180,000 $ (180,000)

$ 3,780,000 $ – $ 3,780,000

December 31, 2014 3,780,000 (210,000)* 3,570,000 10,000 $ (10,000)

December 31, 2015 3,780,000 (420,000) 3,360,000 10,000 (10,000)

$ 3,780,000 $ (420,000) $ 3,360,000 $ (160,000) $ (20,000)

Sale $(3,780,000) 420,000 3,360,000 160,000 $(240,000) (160,000)

$ – $ – $ – $ – $ (240,000) $ (180,000)

Academic Resource Center

Property, plant, and equipment Page 63

Example 12 solution (continued):The entry to record the sale would be as follows:

Cash $ 3,600,000Accumulated depreciation 420,000Revaluation surplus (OCI) 160,000

Building cost 3,780,000Gain on sale 240,000Retained earnings 160,000

Note: if the asset hadn’t been revalued, the NBV of the building would have been $3.2 million (cost of $4.0 million less $200,000 depreciation x 4 years). If the building was sold for $3.6 million, the gain would have been $400,000.

Since the building was revalued, the depreciation expense over the four years was $820,000 ($200,000 in 2012 and 2013 and $210,000 in 2014 and 2015). Reserve surplus was reduced by $20,000 during this period with the credit applied directly to retained earnings. Reserve surplus can never be credited to income. Therefore, after reversing the remaining reserve surplus of $160,000 to retained earnings, the resulting gain is $240,000.

DispositionSale

Academic Resource Center

Property, plant, and equipment Page 64

DispositionInvoluntary conversion

Occurs when the use of an asset is terminated by forces outside of the company’s control. Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 65

DispositionInvoluntary conversion

US GAAP► The difference between the net book

value and the recovered amounts results in a gain or loss when the recovered amounts are received. If the nature of the disposition is unusual and infrequent, these gains or losses may be reported in the income statement as an extraordinary item.

IFRS► If compensation from a third party is due

for PP&E that is impaired, lost or given-up, the entity records a receivable and includes the compensation in profit and loss. Disclosure of extraordinary items in the income statement is prohibited.

Academic Resource Center

Property, plant, and equipment Page 66

Example 13:

A fire destroys a company’s only warehouse. The net book value of the warehouse is $1,000,000 (cost of $4,000,000 less accumulated depreciation of $3,000,000). The company receives $800,000 from its insurance company.

► What accounting entries are necessary to record these events using US GAAP and IFRS?

DispositionInvoluntary conversion

Academic Resource Center

Property, plant, and equipment Page 67

Example 13 solution:

US GAAPCash $ 800,000Accumulated depreciation 3,000,000Extraordinary loss on fire 200,000

Warehouse $ 4,000,000

IFRSAccumulated depreciation $ 3,000,000Loss on disposal 1,000,000

Warehouse $ 4,000,000(Recorded at time of fire) Cash $ 800,000

Income on insurance policy $ 800,000(To record insurance proceeds)

DispositionInvoluntary conversion

Academic Resource Center

Property, plant, and equipment Page 68

Fully depreciated fixed assets

Fully depreciated assets still in use should be left on the books.

Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 69

Disclosures

The measurement basis used for each class of PP&E.

The balance of each class of PP&E as of the balance sheet date.

Similar

Similar

A description of the depreciation method, the useful lives of PP&E, the amount of accumulated depreciation and depreciation expense during the period.

Similar

The amount of impairment losses recognized in income during the year. Similar

IFRSUS GAAP

Academic Resource Center

Property, plant, and equipment Page 70

Disclosures

US GAAP► Revaluing PP&E is not allowed.

► Reversal of impairment losses is not allowed.

IFRS► For revalued assets:

► The effective date of the revaluation.► The methods and assumptions used in estimating fair

value.► Whether an independent appraiser was utilized.► For revalued classes of assets their net cost basis.► The changes to and balance in the revaluation

surplus.

► The amount of impairment losses reversed directly to equity or through net income.

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About the Ernst & Young Academic Resource Center

The Ernst & Young Academic Resource Center (EYARC) is an innovative collaboration between faculty and professionals to support higher education. The EYARC develops and provides free curriculum resources and other educational support to address leading-edge issues impacting the accounting profession. The EYARC is yet another example of the commitment of the global EY organization and the Ernst & Young Foundation to the academic community. The Ernst & Young Foundation is a 501(c)(3) tax exempt corporation associated with Ernst & Young LLP, which funds the Foundation, together with its present and former partners, principals and staff.

© 2014 Ernst & Young Foundation (US). All Rights Reserved.SCORE No. MM4164C.

www.ey.com/us/arc