Property Market Report_ 3rd Quarter 2009

of 7

Transcript of Property Market Report_ 3rd Quarter 2009

-

8/14/2019 Property Market Report_ 3rd Quarter 2009

1/7

1 NAI Qatar|P.O.Box:12625 |Doha -Qatar |+ 974 4316717, 4316743 |www.nai-qatar.com|Dr. Rajesh Krishna Nair

NAI QatarBuild on the power of our network TM

QUARTERLY REAL ESTATE PROPERTY MARKET REPORT - 2009

Qatar real estate market continued to prove its stability and reliability in the third quarter of 2009. The asking

rates are more or less same and there is a promising movement in the residential sector. There are approximatel

140 residential buildings and around 50 commercial buildings in and around Doha under construction or close to

completion. It shows the strength of the property market of Qatar. The hopeful aspects in the market are the

developers are bring together with timely transfer of high quality, value-added projects, banks improved to

managing the risks associated with over exposure to the real estate sector and government efforts to overcome

the difficulties and all these created good fundamentals in the real estate market.

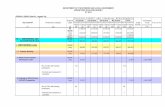

12.9014.02

15.99 15.83

21.7723.23

17.69 18.20

9.71 9.17 10.18 9.88

2.22 2.31 2.94 2.894.70 4.67 5.26 5.52

10.44 10.70 11.33 11.44

Q3 2008 Q4 2008 Q1 2009 Q2 2009

Credit facilities by sectors (in %)real estate Govt. Sector General Trade

Industry Contractors Service sectors

Market Overview

3rdQARTERJulyAugustSeptember

Figure1From third quarter of 2008 to second

quarter of 2009, the real estate sector

has got the highest credit facilities

after government sector (figure1).

This shows the positive attitude o

banks towards real estate sector and

the vibrant real estate market in Qatar

1.85

5.57 5.60 5.24

2.87

Q1 Q2 Q3 Q4 Q1

2008 2009

GDP changeGDP change The significance of construction sector is still

growing. The contribution of this sector to GDP is

continuously increasing. But it is important to note

that the contribution is increasing at a decreasingrate. This means that, the construction process are

going at a very slow pace due to the short-term low

demand in the real estate sector (figure 2)

Figure 2

Data Source: QCB

-

8/14/2019 Property Market Report_ 3rd Quarter 2009

2/7

2 NAI Qatar|P.O.Box:12625 |Doha -Qatar |+ 974 4316717, 4316743 |www.nai-qatar.com|Dr. Rajesh Krishna Nair

In the third quarter of 2009, there was a promising growth in the demand for residential apartment units/flats. The

average asking rate for apartment units in most of the residential areas in Doha were increased as compared it

with second quarter. Areas like Al Sadd, West bay, Mumtaza,Mansoura, Bin Muhmoud, Um Gualina, Airport, Ein

Khalid etc, the average asking rate increased substantially (figure 3 & 4). Whereas areas like, Madinat Khalifa, Bin

Omaran, Najma, Salatha, Musheireb etc, the asking rates were decreased considerably. It is found that the

middle and lower income group of expatriates is largely located in these areas and perhaps this may be the

reason for fall of asking rate in these areas.

There was a mixed response for the demand for villa units in this quarter. Abu Hamour, Al Sadd and Airport Area

the average asking rate decreased considerably and other locations there was a positive rate of growth of

demand (figure5)

-20.00

-10.00

0.00

10.0020.00

30.00

40.00

3BHK

2 BHK

1 BHK

-20.00

-10.00

0.00

10.00

20.00

30.00

3 BHK

2 BHK

1 BHK

-40.00

-20.00

0.00

20.00

40.00

60.00

FF

UF

DOHATRENDS: RESIDENTIAL 2009

Figure 3Apartments F/F

Figure 4Apartments U/F

VillaFigure 5

-

8/14/2019 Property Market Report_ 3rd Quarter 2009

3/7

3 NAI Qatar|P.O.Box:12625 |Doha -Qatar |+ 974 4316717, 4316743 |www.nai-qatar.com|Dr. Rajesh Krishna Nair

DOHATRENDS: RESIDENTIAL

The average asking rate for 3 bedrooms fully furnished apartment rose by 7.37 percentages during the third

quarter. Whereas the average asking rate for 2 bedrooms fully furnished apartments have fallen by (-) 1.31

percent. The rate for single bedroom fully furnished apartment rose by 7.52 percent. When we consider the

unfurnished apartment units, the average asking rate for 3 bedrooms apartments rose by 11.55 percent, whereas

the 2 bedrooms apartment rate have fallen by (-) 0.53 percent. The average asking rate for single bedroom

apartment has gained by 3.09 percent (figure 6). It is observed that the 2 bedroom apartments demand was

most deteriorated in the year 2009.

3 BHK 2 BHK 1 BHK villa

FF 7.37 -1.31 7.52 -0.37

UF 11.55 -0.53 3.09 -1.71

-4-202468

1012

14

RAT

Rate of Growth (Residential) There was a marginal fall in demand for villaunits. The average asking rate for both furnished

and unfurnished villa units have fallen in the third

quarter. The rates of growth of furnished villa

units were (-) 0.37 percent, whereas it was (-)

1.71 percent for unfurnished villa units.

9860 1007010587

8470 8385 8359

6065 6615 6521

16385 16694 16325

July August Sept.

F/F3 BHK 2 BHK 1 BHK VILLA

8335 82359298

6985 7100 6948

5315 5565 5479

14660 14195 14410

July August Sept.

U/F3 BHK 2 BHK 1 BHK VILLA

Average Monthly Asking Rates

Figure 7 Figure 8

Figure 6

-

8/14/2019 Property Market Report_ 3rd Quarter 2009

4/7

4 NAI Qatar|P.O.Box:12625 |Doha -Qatar |+ 974 43167

In the office segment, the average as

segment, the rate has fallen by (-) 4.23

ring roads are very attractive locations

respectively (figure 9). Whereas, the h

Mumtaza and Musheirib. The rates w

While most of the other areas, the aver

12.24

-28.19

-5.03

0.005.26

0.00

-6.

% change of rate (A grade office)Rent 'A' Grad

-1.57

-22.22

0.00

-12.00

10.532.83

-3

% cahnge of rate (B g

Rent 'B' Grad

The demand for B grade office units

most of the locations except Salwa ro

& jadeed (figure10). This is because

office units at a lower rate in all favorite

DOHA

Qatar |+ 974 4316717, 4316743 |www.nai-qatar.com|Dr. Rajesh Krishna Nair

ing rates were continued to fall in the third qu

percent and for B grade office segment, it fell

and the demand for A grade offices rose by

ighest fall in rate is marked in Corniche/Old S

re fell by (-) 28.19, (-) 6.03 and (-) 5.03 perce

ge asking rate per square meter was kept const

3-1.87

0.00 0.00

13.13

0.00

% change of rate (A grade office)office

.36

44.51

-14.29

15.56 8.33

-3.70

rade office)

office

Figure 10

TRENDS: O

C Ring

cornic

mus

R

B ring

ra

j

al

mu

salw

west bay/

airport road

Al

Industria

Bin

Rent/SQM/SeptemberB

were also fell considerably in

d,Airport, D ring road, Alsadd

f the availability of A grade

locations.

Figure 9

Dr. Rajesh Krishna Nair

arter. For A grade office

y (-) 4.17 percent. C & D

2.24 and 13.13 percen

latha region followed by

nt respectively (figure 9)

ant.

FICE

220

135

151

195

200

152

152

200

203

148

210

228

202

202.5

175

180

197

125

105

120

128

84

95

110

105

127

70

125

150

130

130

95

120

100

road

e/old

heirib

ajma

yyan

road

mada

deed

saad

taza

road

dafna

/area

ring

waab

l area

mran

Rent/SQM/Septembergrade A grade

Figure 11

-

8/14/2019 Property Market Report_ 3rd Quarter 2009

5/7

5 NAI Qatar|P.O.Box:12625 |Doha -Qatar |+ 974 4316717, 4316743 |www.nai-qatar.com|Dr. Rajesh Krishna Nair

DOHARetail

The retail sector has very promising future. Notwithstanding the precariousness in the market, the retail sector

showed its potency. The average rate of growth of retail sector in the third quarter was 21.34 percent (figure12).

The promising nature of retails segment is mainly attributes to the fall of inflation and increased consumer

expenditure.

.

TRENDS: COMMERCIAL

-6.67 -7.17

21.24

-11.29

24.53

10.78

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

land ( commercial) land (Residential)

Retail Store

W. House Labor Accommodation

LandDuring the third quarter, there was a marginal

fall in the demand for land. The average selling

price for both commercial and residential land

fell considerably by (-) 6.67 and (-) 7.17

percent respectively (figure12). The low

demand may be due to the lack of complete

confidence from investors side.

% age changes: commercial Figure12

Stores/W. HousesThe average asking rate for stores fell by (-) 11.29 percent in the third quarter of 2009 and a number of stores are

vacant in the industrial area and other locations in and outside Doha. Whereas there is a good demand for

warehouses in Qatar and the average asking rate was increased by 24.53 percent in the third quarter (figure 12).

Labor Accommodation There is a very good demand for labor accommodation. The average rate of growth of a unit rose by 10.78

percent in the last quarter. This indicates the influx of labors and new projects. The average asking rate prevails in

Doha for a labor accommodation unit was QR1730/month or QR 97 per SQM

-

8/14/2019 Property Market Report_ 3rd Quarter 2009

6/7

6 NAI Qatar|P.O.Box:12625 |Doha -Qatar |+ 974 43167

DOHAResidentialBased on the past performance of the

is expected that there will be an upwa

rate of growth of rental rates for reside

in Doha. Whereas, for villa units, ther

percentages for the last quarter of 200

-3.00

-2.50

-2.00

-1.50

-1.00

-0.50

0.00

oct. nov.

Office - Growth rate

Retail, Store & W . HousesIt is expected that there is a good rat

commercial real estate market in th

2009. The asking rate for Retail, Stor

will increase from 10 to 30 percent in

Qatar |+ 974 4316717, 4316743 |www.nai-qatar.com|Dr. Rajesh Krishna Nair

What Future H

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

october nov

3 BHK 2 BHK

eal estate market, it

rd movement in the

tial apartment units

will be a fall of 2

.

dec.

Growth rate

OfficesThe third quarter of 2009

in the average asking rat

office spaces in Doha. It i

fall of 2 to 3 percent in t

The fall in rental rate do

demand for office spaces

numbers of office buildin

and around Doha with a

boom.

0.00

5.00

10.00

15.00

20.00

25.00

30.00

october nov

store W.h

of growth in the

e last quarter of

and Warehouse

the last quarter.

Dr. Rajesh Krishna Nair

lds?

mber december

1 BHK Villa

showed a continued fall

e per square meter for

s expected to a further

e last quarter of 2009.

s not imply the fall in

. This is because large

s are mushrooming in

anticipated economic

ember december

ouse Retail

-

8/14/2019 Property Market Report_ 3rd Quarter 2009

7/7

7 NAI Qatar|P.O.Box:12625 |Doha -Qatar |+ 974 4316717, 4316743 |www.nai-qatar.com|Dr. Rajesh Krishna Nair

What makes NAI Qatar different from other real estate providers is the system we bring people and

resources together globally wherever needed to deliver outstanding results for our clients. Our clients

come to us for our profound regional knowledge and experience. They build their businesses on the

power of our global managed network. We are different in attitude, structure, approach and Globa

Coverage.

NAI Global is the worlds only managednetwork. Dedicated core staff aroundthe world to manage andsupport our global network Award-winning REALTracOnline technology Proprietary STARS (StrategicTransaction Administration andReporting System)

NAI Qatar offers a full roster of real estate services:

Investment Services

Facilities Management Services

Advisory Services

Valuation Services

Project Management Services

Marketing Services Over 325 offices in 55 countries 5,000 professionals

This report is for information only and should not be a substitute for professional investment advice.

Duplication of the contents of this publication is prohibited without prior approval from NAI Qatar. The

estimates and information made available herein are made by NAI Qatar in its best judgment and from

available resources from various sources. Albeit. NAI Qatar guarantees to the precision of the report and

renounce any liability for errors and omissions made in respect of providing such information.

NAI Qatar- Build on the power of our network

Contact info:[email protected]

Contact: 974 5362199

www.nai-qatar.com/login