Project on Profits and Gaind from Business and Prof. (PGBP)

42

UNIVERSITY OF MUMBAI PROJECT REPORT ON PROFITS AND GAINS FROM BUSINESS AND PROFESSION BY Mr. OJAS NITIN NARSALE M.COM (Part-II) (SEM-III) (Roll No.28) ACADEMIC YEAR 2016-2017 PROJECT GUIDE CA PRASHANT KANVINDE PARLE TILAK VIDYALAYA ASSOCIATION’S M.L. DAHANUKAR COLLEGE OF COMMERCE DIXIT ROAD, VILE PARLE ( E) MUMBAI- 400057

-

Upload

ojas-narsale -

Category

Education

-

view

68 -

download

2

Transcript of Project on Profits and Gaind from Business and Prof. (PGBP)

UNIVERSITY OF MUMBAI PROJECT REPORT ON PROFITS AND GAINS FROM

BUSINESS AND PROFESSION BY

Mr. OJAS NITIN NARSALE M.COM (Part-II) (SEM-III) (Roll No.28) ACADEMIC YEAR 2016-2017 PROJECT GUIDE

CA PRASHANT KANVINDE

PARLE TILAK VIDYALAYA ASSOCIATION’S M.L. DAHANUKAR COLLEGE OF COMMERCE DIXIT ROAD, VILE PARLE ( E) MUMBAI- 400057

DECLERATION

I, Mr. OJAS NITIN NARSALE of PARLE TILAK VIDYALAYA ASSOCIATION’S M.L. DAHANUKAR COLLEGE OF COMMERCE of M.COM(Part-II) (SEM-III) (Roll No.28) hereby declare that I have completed this project on PROFITS AND GAINS FROM BUSINESS AND PROFESSION in the ACADEMIC YEAR 2016-2017. This information submitted is true and original to the best of my knowledge.

(Signature of Student)

ACKNOWLEDGEMENT

To list who all helped me is difficult because they are so numerous and the depth is so enormous. I would like to acknowledge the following as being idealistic channels and fresh dimensions in the completion of this project. I would firstly thank the University of Mumbai for giving me chance to do this project. I would like to thank my Principal, Dr. Madhavi Pethe for providing the necessary facilities required for completion of this project. I even will like to thank our co-ordinator, for the moral support that I received. I would like to thank our College Library, for providing various books and magazines related to my project. Finally I proudly thank my Parents and Friends for their support throughout the Project.

INDEX

Sr No Topic Page

1 Introduction 5

2 Chargeability 6

3 Deductions under Sections 30 to 37 9

4 Amount expressly disallowed under the Act 19

5 Expenses deductible on actual payment basis

21

6 Other provisions 22

7 Provisions applicable to Non-Resident/Foreign Company

23

8 Accounts and Audit and Presumptive Taxation

25

9 Some Important FAQs With Case Laws From Income From Profits And Gains Of Business Or Profession

26

10 ICDS 37

11 Depreciation 39

12 Bibliography 42

Introduction Under the Income Tax Act, 'Profits and Gains of Business or Profession' are also subjected to taxation. The term "business" includes any (a) trade, (b)commerce, (c)manufacture, or (d) any adventure or concern in the nature of trade, commerce or manufacture. The term "profession" implies professed attainments in special knowledge as distinguished from mere skill; "special knowledge" which is "to be acquired only after patient study and application". The words 'profits and gains' are defined as the surplus by which the receipts from the business or profession exceed the expenditure necessary for the purpose of earning those receipts. These words should be understood to include losses also, so that in one sense 'profit and gains' represent plus income while 'losses' represent minus income.

The following types of income are chargeable to tax under the heads profits and gains of business or profession:-

Profits and gains of any business or profession Any compensation or other payments due to or received by any person specified in

section 28 of the Act Income derived by a trade, profession or similar association from specific services

performed for its members Profit on sale of import entitlement licences, incentives by way of cash compensatory

support and drawback of duty The value of any benefit or perquisite, whether converted into money or not, arising from

business Any interest, salary, bonus, commission, or remuneration received by a partner of a firm,

from such a firm Any sum whether received or receivable in cash or kind, under an agreement for not

carrying out any activity in relation to any business or not to share any know-how, patent, copyright, franchise, or any other business or commercial right of similar nature or technique likely to assist in the manufacture or processing of good

Any sum received under a keyman insurance policy Income from speculative transactions.

In the following cases, income from trading or business is not taxable under the head "profits and gains of business or profession":-

Rent of house property is taxable under the head " Income from house property". Even if the property constitutes stock in trade of recipient of rent or the recipient of rent is engaged in the business of letting properties on rent.

Deemed dividends on shares are taxable under the head "Income from other sources". Winnings from lotteries, races etc. are taxable under the head "Income from other

sources".

Profits and gains of any other business are taxable, unless such profits are subjected to exemption. General principals governing the computation of taxable income under the head "profits and gains of business or profession:-

Business or profession should be carried on by the assessee. It is not the ownership of business which is important , but it is the person carrying on a business or profession, who is chargeable to tax.

Income from business or profession is chargeable to tax under this head only if the business or profession is carried on by the assessee at any time during the previous year. This income is taxable during the following assessment year.

Profits and gains of different business or profession carried on by the assessee are not separately chargeable to tax i.e. tax incidence arises on aggregate income from all businesses or professions carried on by the assessee. But, profits and loss of a speculative business are kept separately.

It is not only the legal ownership but also the beneficial ownership that has to be considered.

Profits made by an assessee in winding up of a business or profession are not taxable, as no business is carried on in that case. However, such profits may be taxable as capital gains or as business income, if the process of winding up is such as to involve the carrying on of a trade.

Taxable profit is the profit accrued or arising in the accounting year. Anticipated or potential profits or losses, which may occur in future, are not considered for arriving at taxable income. Also, the profits, which are taxable, are the real profits and not notional profits. Real profits from the commercial point of view, mean a gain to the person carrying on the business and not profits from narrow, technical or legalistic point of view.

The yield of income by a commercial asset is the profit of the business irrespective of the manner in which that asset is exploited by the owner of the business.

Any sum recovered by the assessee during the previous year, in respect of an amount or expenditure which was earlier allowed as deduction, is taxable as business income of the year in which it is recovered.

Modes of book entries are generally not determinative of the question whether the assessee has earned any profit or loss.

The Income tax act is not concerned with the legality or illegality of business or profession. Hence, income of illegal business or profession is not exempt from tax.

Chargeability

The following incomes are chargeable to tax under the head Profit and Gains from Business or Profession:

28(i) - Profit and gains from any business or profession carried on by the assessee at any time during the previous year

28(ii) - Any compensation or other payment due to or received by any specified person 28(iii) - Income derived by a trade, professional or similar association from specific

services performed for its members 28(iiia) - Profit on sale of a license granted under the Imports (Control) Order 1955, made

under the Import Export Control Act, 1947 28(iiib) - Cash assistance (by whatever name called) received or receivable by any person

against exports under any scheme of Government of India 28(iiic) - Any duty of Customs or Excise repaid or repayable as drawback to any person

against exports under the Customs and Central Excise Duties Drawback Rules, 1971. 28(iiid) - Profit on transfer of Duty Entitlement Pass Book Scheme, under Section 5 of

Foreign Trade (Development and Regulation) Act, 1992 28(iiie) - Profit on transfer of Duty Free Replenishment Certificate, under Section 5 of

Foreign Trade (Development and Regulation) Act 1992 28(iv) - Value of any benefits or perquisites arising from a business or the exercise of a

profession. 28(v) - Interest, salary, bonus, commission or remuneration due to or received by a

partner from partnership firm 28(va) - a) Any sum received or receivable for not carrying out any activity in relation to

any business or profession; or b) Any sum received or receivable for not sharing any know-how, patent, copyright, trademark, licence, franchise, or any other business or commercial right or information or technique likely to assist in the manufacture of goods or provision of services.

28(vi) - Any sum received under a Key man Insurance policy including the sum of bonus on such policy

28(vii) - Any sum received ( or receivable) in cash or in kind, on account of any capital assets (other than land or goodwill or financial instrument) being demolished, destroyed, discarded or transferred, if the whole of the expenditure on such capital assets has been allowed as a deduction under section 35AD ,Income from speculative transactions. However, it shall be deemed to be distinct and separate from any other business.

41(1) – o Remission or cessation of liability in respect of any loss, expenditure or trading

liability incurred by the taxpayers o Recovery of trading liability by successor which was allowed to the predecessor

shall be chargeable to tax in the hands of successor. Succession could be due to amalgamation or demerger or succession of a firm succeeded by another firm or company, etc.

o Any liability which is unilaterally written off by the taxpayer from the books of accounts shall be deemed as remission or cessation of such liability and shall be chargeable to tax.

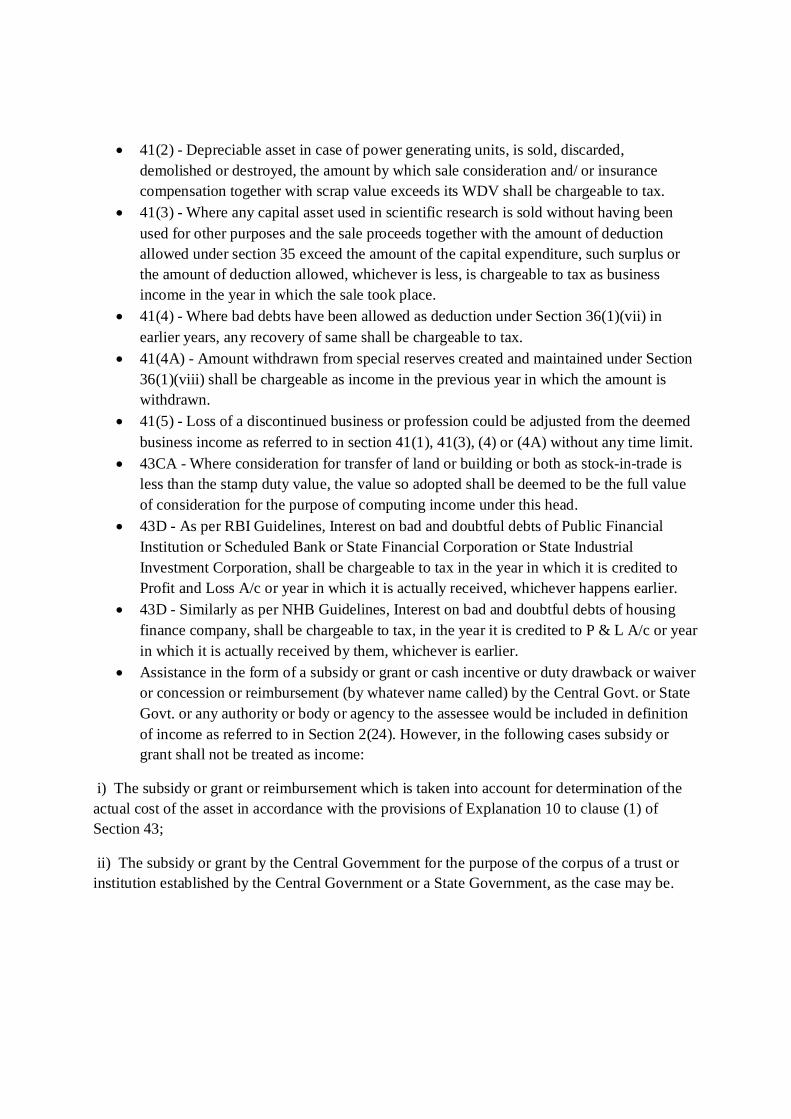

41(2) - Depreciable asset in case of power generating units, is sold, discarded, demolished or destroyed, the amount by which sale consideration and/ or insurance compensation together with scrap value exceeds its WDV shall be chargeable to tax.

41(3) - Where any capital asset used in scientific research is sold without having been used for other purposes and the sale proceeds together with the amount of deduction allowed under section 35 exceed the amount of the capital expenditure, such surplus or the amount of deduction allowed, whichever is less, is chargeable to tax as business income in the year in which the sale took place.

41(4) - Where bad debts have been allowed as deduction under Section 36(1)(vii) in earlier years, any recovery of same shall be chargeable to tax.

41(4A) - Amount withdrawn from special reserves created and maintained under Section 36(1)(viii) shall be chargeable as income in the previous year in which the amount is withdrawn.

41(5) - Loss of a discontinued business or profession could be adjusted from the deemed business income as referred to in section 41(1), 41(3), (4) or (4A) without any time limit.

43CA - Where consideration for transfer of land or building or both as stock-in-trade is less than the stamp duty value, the value so adopted shall be deemed to be the full value of consideration for the purpose of computing income under this head.

43D - As per RBI Guidelines, Interest on bad and doubtful debts of Public Financial Institution or Scheduled Bank or State Financial Corporation or State Industrial Investment Corporation, shall be chargeable to tax in the year in which it is credited to Profit and Loss A/c or year in which it is actually received, whichever happens earlier.

43D - Similarly as per NHB Guidelines, Interest on bad and doubtful debts of housing finance company, shall be chargeable to tax, in the year it is credited to P & L A/c or year in which it is actually received by them, whichever is earlier.

Assistance in the form of a subsidy or grant or cash incentive or duty drawback or waiver or concession or reimbursement (by whatever name called) by the Central Govt. or State Govt. or any authority or body or agency to the assessee would be included in definition of income as referred to in Section 2(24). However, in the following cases subsidy or grant shall not be treated as income:

i) The subsidy or grant or reimbursement which is taken into account for determination of the actual cost of the asset in accordance with the provisions of Explanation 10 to clause (1) of Section 43;

ii) The subsidy or grant by the Central Government for the purpose of the corpus of a trust or institution established by the Central Government or a State Government, as the case may be.

Section Nature of expenditure Quantum of deduction Assessee

30Rent, rates, taxes, repairs (excluding capital

expenditure) and insurance for premisesActual expenditure incurred excluding

capital expenditureAll assessee

31Repairs (excluding capital expenditure) and insurance of machinery, plant and furniture

Actual expenditure incurred excluding capital expenditure

All assessee

32(1)(i)

Depreciation on i) buildings, machinery, plant or furniture,

being tangible assets; ii) know-how, patents, copyrights, trademarks, licenses, franchises, or any other business or commercial rights of similar nature, being

intangible assets Allowed at prescribed percentage on Straight

Line Method for each asset

Provided that where an asset is acquired by the assessee during the previous year and is

put to use for a period of less than one hundred and eighty days in that previous

year, the deduction in respect of such asset shall be restricted to fifty per cent of the

amount calculated at the percentage prescribed for an asset.

Assessees engaged in business of generation or generation and distribution of power

Note:Taxpayers engaged in the business of

generation or generation and distribution of power shall have the option to claim

depreciation either on basis of straight line basis method or written down value method on

each block of asset.

32(1)(ii)

Depreciation on i) buildings, machinery, plant or furniture,

being tangible assets; ii) know-how, patents, copyrights, trademarks, licenses, franchises, or any other business or commercial rights of similar nature, being

intangible assets. Allowed at prescribed percentage on WDV

method for each block of asset

Provided that where an asset is acquired by the assessee during the previous year and is

put to use for a period of less than one hundred and eighty days in that previous

year, the deduction in respect of such asset shall be restricted to fifty per cent of the

amount calculated at the percentage prescribed for an asset.

All assessees

32(1)(iia)

Additional depreciation on new plant and machinery (other than ships, aircraft, office appliances, second hand plant or machinery,

etc.).(subject to certain conditions)

Additional depreciation shall be available @20 % of the actual cost of new plant and

machinery.

in– manufacture or production of any article or thing; or– generation, transmission or distribution of power (if taxpayer is not claiming depreciation on basis of straight line method)

Provided that where an asset is acquired by the assessee during the previous year and is put to use for a period of less than one hundred and eighty days in that previous year, then deduction of additional depreciation would be restricted to 50% in

the year of acquisition and balance 50% would be allowed in the next year

Proviso to Section 32(1)(iia) Additional depreciation on new plant and machinery (other than ships, aircraft,office appliances, second hand plant or

machinery, etc.))(Subject to certain conditions)

Additional depreciation shall be available @35 % of the actual cost of new plant and machinery.Provided that where an asset is acquired by the assessee during the previous year and is put to use for a period of less than one hundred and eighty days in that previous year, then deduction of additional depreciation would be restricted to 50% of

actual cost in the year of acquisition and balance 50% would be allowed in the next year

Deductions under Sections 30 to 37Amount deductible, while computing, Profits and Gains of Business or Profession are:-

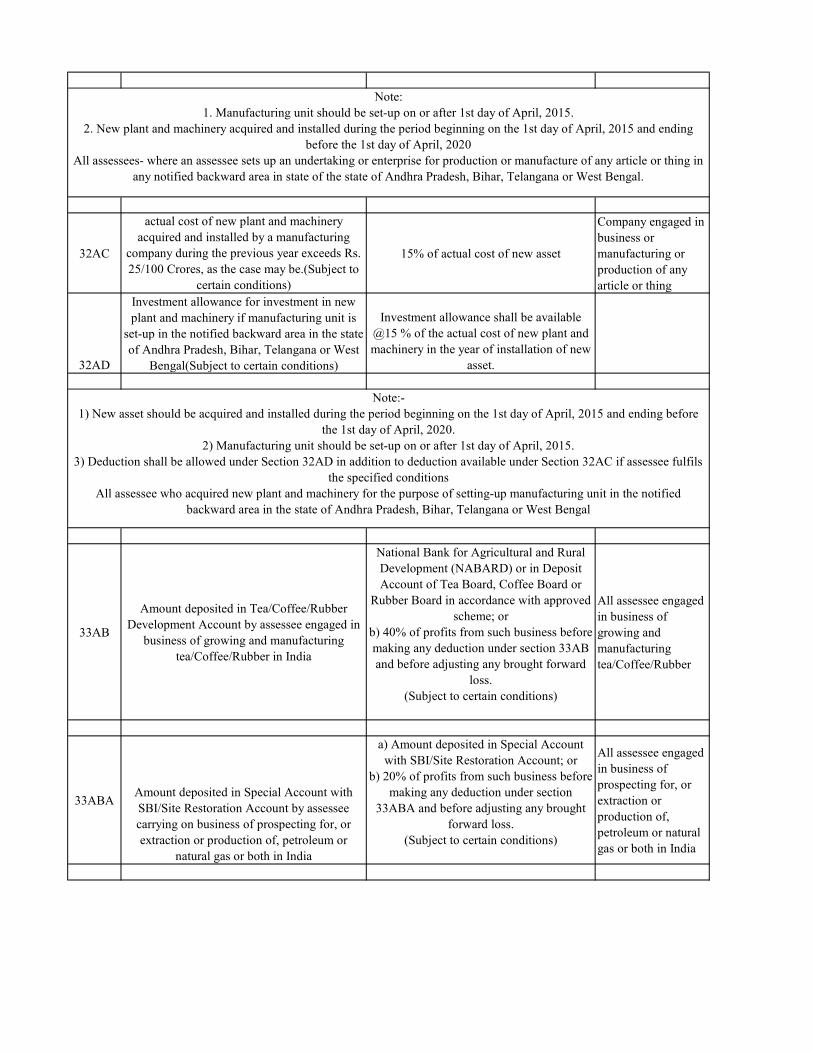

32AC

actual cost of new plant and machinery acquired and installed by a manufacturing

company during the previous year exceeds Rs. 25/100 Crores, as the case may be.(Subject to

certain conditions)

15% of actual cost of new asset

Company engaged in business or manufacturing or production of any article or thing

32AD

Investment allowance for investment in new plant and machinery if manufacturing unit is

set-up in the notified backward area in the state of Andhra Pradesh, Bihar, Telangana or West

Bengal(Subject to certain conditions)

Investment allowance shall be available @15 % of the actual cost of new plant and machinery in the year of installation of new

asset.

33AB

Amount deposited in Tea/Coffee/Rubber Development Account by assessee engaged in

business of growing and manufacturing tea/Coffee/Rubber in India

National Bank for Agricultural and Rural Development (NABARD) or in Deposit Account of Tea Board, Coffee Board or

Rubber Board in accordance with approved scheme; or

b) 40% of profits from such business before making any deduction under section 33AB and before adjusting any brought forward

loss.(Subject to certain conditions)

All assessee engaged in business of growing and manufacturing tea/Coffee/Rubber

33ABAAmount deposited in Special Account with SBI/Site Restoration Account by assessee carrying on business of prospecting for, or extraction or production of, petroleum or

natural gas or both in India

a) Amount deposited in Special Account with SBI/Site Restoration Account; or

b) 20% of profits from such business before making any deduction under section

33ABA and before adjusting any brought forward loss.

(Subject to certain conditions)

All assessee engaged in business of prospecting for, or extraction or production of, petroleum or natural gas or both in India

Note:1. Manufacturing unit should be set-up on or after 1st day of April, 2015.

2. New plant and machinery acquired and installed during the period beginning on the 1st day of April, 2015 and ending before the 1st day of April, 2020

All assessees- where an assessee sets up an undertaking or enterprise for production or manufacture of any article or thing in any notified backward area in state of the state of Andhra Pradesh, Bihar, Telangana or West Bengal.

Note:-1) New asset should be acquired and installed during the period beginning on the 1st day of April, 2015 and ending before

the 1st day of April, 2020.2) Manufacturing unit should be set-up on or after 1st day of April, 2015.

3) Deduction shall be allowed under Section 32AD in addition to deduction available under Section 32AC if assessee fulfils the specified conditions

All assessee who acquired new plant and machinery for the purpose of setting-up manufacturing unit in the notified backward area in the state of Andhra Pradesh, Bihar, Telangana or West Bengal

35(1)(i)

Revenue expenditure on scientific research pertaining to business of assessee is allowed as

deduction (Subject to certain conditions).

research is allowed as deduction.Expenditure on scientific research within 3 years before commencement of business (in

the nature of purchase of materials and salary of employees other than perquisite) is

allowed as deduction in the year of commencement of business to the extent

certified by prescribed authority.

All assessee

35(1)(ii)

Contribution to approved research association, university, college or other institution to be

used for scientific research shall be allowed as deduction (Subject to certain conditions)

university, college, or other institution is allowed as deduction.

150% of sum paid to such association, university, college or other institution is

allowed as deduction (applicable from AY 2018-19)

Note:- From the AY beginning on or after the 1st day of April, 2021, the deduction

shall be equal to the sum so paid.

All assessee

35(1)(iia)

Contribution to an approved company registered in India to be used for the purpose of

scientific research is allowed as deduction (Subject to certain conditions)

125% of sum paid to the company is allowed as deduction Entire sum paid to the

company is allowed as deduction (applicable from AY 2018-19)

All assessee

35(1)(iii)Contribution to approved research association,

university, college or other institution with objects of undertaking statistical research or

research in social sciences shall be allowed as deduction (Subject to certain conditions)

125% of sum paid to such association, university, college, or other institution is

allowed as deductionEntire sum paid to such association,

university, college or other institution is allowed as deduction (applicable from AY

2018-19)

All assessee

35(1)(iv) read with

35(2)

Capital expenditure incurred during the year on scientific research relating to the business carried on by the assessee is allowed as

deduction (Subject to certain conditions)

Entire capital expenditure incurred on scientific research is allowed as deduction.Capital expenditure incurred within 3 years

before commencement of business is allowed as deduction in the year of

commencement of business.Note:

i. Capital expenditure excludes land and any interest in land;

ii. No depreciation shall be allowed on such assets.

All assessee

35(2AA)

Payment to a National Laboratory or University or an Indian Institute of Technology or a specified person is allowed as deduction.

The payment should be made with the specified direction that the sum shall be used in

a scientific research undertaken under an approved programme.

200% of payment is allowed as deduction (Subject to certain conditions).

150% of payment is allowed as deduction (applicable from AY 2018-19)

Note:-From the A.Y. beginning on or after the 1st day of April, 2021, the deduction shall be

equal to the sum so paid.

All assessee

35(2AB)

Any expenditure incurred by a company on scientific research (including capital

expenditure other than on land and building) on in-house scientific research and

development facilities as approved by the prescribed authorities shall be allowed as deduction (Subject to certain conditions).

Expenditure on scientific research in relation to Drug and Pharmaceuticals shall include

expenses incurred on clinical trials, obtaining approvals from authorities and for filing an

application for patent.

allowed as deduction.150% of expenditure so incurred shall be

allowed as deduction (applicable from AY 2018-19)

Note:i. Company should enter into an agreement

with the prescribed authority for co-operation in such research and development

and fulfils conditions with regard to maintenance of accounts and audit thereof and furnishing of reports in such manner as

may be prescribed.ii. From the A.Y. beginning on or after the 1st day of April, 2021, the deduction shall

be equal to the expend the so incurred.

Company engaged in business of bio-technology or in any business of manufacturing or production of eligible articles or things

35ABA

Capital expenditure incurred and actually paid for acquiring any right to use spectrum for

telecommunication services shall be allowed as deduction over the useful life of the spectrum.

Deduction will be available in equal installments starting from the year in which actual payment is made and ending in the year in which spectrum comes to an end.

Note:If spectrum fee is actually paid before the commencement of business, the deduction

will be available from the year in which business is commenced.

All Assessee engaged in telecommunication services

35ABB

Capital expenditure incurred for acquiring any license or right to operate telecommunication

services shall be allowed as deduction over the term of the license.

Deduction would be allowed in equal installments starting from the year in which such payment has been made and ending in the year in which license comes to an end.

All Assessee engaged in telecommunication services

35ACExpenditure by way of payment of any sum to

a public sector company/local authority/approved association or institution

for carrying out any eligible scheme or project (Subject to certain conditions).

Actual payment made to prescribed entities. However, a company can also claim

deduction for expenditure incurred by it directly on eligible projects.

Note:-No deduction in any A.Y. commencing on

or after the 1st day of April, 2018

All assessee. However, deduction for direct expenditure is allowed only to a company

35AD

Deduction in respect of `expenditure on specified businesses, as under:

a) Setting up and operating a cold chain facilityb) Setting up and operating a warehousing facility for storage of agricultural produce

c) Building and operating, anywhere in India, a hospital with at least 100 beds for patients

d) Developing and building a housing project under a notified scheme for affordable housing

e) Production of fertilizer in India(Subject to certain conditions)

deduction provided the specified business has commenced its operation on or after 01-

04-2012.100% of capital expenditure will be allowed

to be deducted from the assessment year 2018-19 onwards

Note: If such specified businesses commence operations on or before 31-03-2012 but after prescribed dates, deduction

shall be limited to 100% of capital expenditure.

All assessee

35AD

specified businesses, as under:a) Laying and operating a cross-country natural gas or crude or petroleum oil pipeline network

for distribution, including storage facilities being an integral part of such network;

b) Building and operating, anywhere in India, a hotel of two-star or above category;

c) Developing and building a housing project under a scheme for slum redevelopment or

rehabilitationd) Setting up and operating an inland container

depot or a container freight statione) Bee-keeping and production of honey and

beeswaxf) Setting up and operating a warehousing

facility for storage of sugarg) Laying and operating a slurry pipeline for

the transportation of iron oreh) Setting up and operating a semi-conductor

wafer fabrication manufacturing unit i) Developing or maintaining and operating, or developing, maintaining and operating a

new infrastructure facility(Subject to certain conditions)

100% of capital expenditure incurred for the purpose of business is allowed as

deduction provided specified businesses commence operations on or after the

prescribed dates.

All assesseeNote: Such deduction is available to Indian company in case of following business, namely;- i) Business of laying and operating a cross-country natural gas or crude or petroleum oil pipeline networkii) Developing or maintaining and operating or developing, maintaining and operating a new infrastructure facility.

35CCA

Payment to following Funds are allowed as deduction:

a) National Fund for Rural Development; andb) Notified National Urban Poverty Eradication

FundActual payment to specified funds

All assessee

35CCC

incurred on notified agricultural extension project for the purpose of training, educating and guiding the farmers shall be allowed as deduction, provided the expenditure to be

incurred is expected to be more than Rs. 25 lakhs (Subject to certain conditions).

150% of the expenditure (Subject to certain conditions)

Note:-100% deduction shall be allowed from the

1st day of April, 2021

All assessee

35CCD Expenditure incurred by a company (not being expenditure in the nature of cost of any land or

building) on any notified skill development project is allowed as deduction (Subject to

certain conditions).

conditions)Note:

(i) No deduction shall be allowed to a company engaged in manufacturing alcoholic spirits or tobacco products.

(ii) 100% deduction shall be allowed for the AY beginning on or after the 1st day of

April, 2021

Company engaged in manufacturing of any article or providing specified services

35DAn Indian company can amortize certain

preliminary expenses (Subject to certain conditions and nature of

expenditures)

project or capital employed, whichever is more) Qualifying preliminary expenditure is

allowable in each of 5 successive years beginning with the previous year in which the extension of undertaking is completed or the new unit commences production or

operation.

Indian Company

35D

Non-corporate taxpayers can amortize certain preliminary expenses

(Subject to certain conditions and nature of expenditures)

project) Qualifying preliminary expenditure is allowable in each of 5 successive years beginning with the previous year in which the extension of undertaking is completed or the new unit commences production or

operation.

Resident Non-corporate assessees

35DDExpenditure incurred after 31-3-1999 in

respect of amalgamation or demerger can be amortized by an Indian Company

Expenditure is allowed as deduction in five equal installments in 5 previous years

starting with the year in which amalgamation or demerger took place.

Indian Company

35DDA Expenditure incurred under Voluntary Retirement Scheme is allowed as deduction.

Each payment under VRS is allowed as deduction in five equal installments in 5

previous years.All Assessee

35E

persons on prospecting for the minerals or on the

development of mine or other natural deposit of such minerals shall be allowed as deduction

(Subject to certain conditions).Eligible expenditure is allowed as deduction

in ten equal installments in 10 previous years.

Resident persons

36(1)(i)Insurance premium covering risk of damage or

destruction of stocks/stores Actual expenditure incurredAll Assessee

36(1)(ia)owned by a member of co-operative society

engaged in supplying milk to federal milk co-operative society Actual expenditure incurred

All Assessee

36(1)(ib)

other than cash, to insure employee’s health under (a) scheme framed by GIC of India and

approved by Central Government; or (b) scheme framed by any other insurer and

approved by IRDA Actual expenditure incurred

All Assessee

36(1)(ii)would not have been payable as profit or

dividend if it had not been paid as bonus or commission Actual expenditure incurred

All Assessee

36(1)(iii)

Interest on borrowed capital (Subject to certain conditions)

for the purposes of the business or profession shall be allowed as deduction.

However, if capital is borrowed for acquiring an asset, then interest for any

period beginning from the date on which capital was borrowed till the date on which

asset was first put to use, shall not be allowed as deduction.

All Assessee

36(1)(iiia)

Discount on Zero Coupon Bonds (Subject to certain conditions)

Pro-rata amount of discount on zero coupon bonds shall be allowed as deduction over

the life of such bondSpecified Assessee

36(1)(iv)Employer’s contributions to recognized

provident fund and approved superannuation fund [subject to certain limits and conditions] Actual expenditure incurred

All Assessee

36(1)(iva)

Any sum paid by assessee-employer by way of contribution towards a pension scheme, as

referred to in section 80CCD, on account of an employee.

Actual expenditure not exceeding 10% of the salary* of the employee

*Salary = Basic Pay + Dearness Allowance (to the extent it forms part of retirement benefits)+ turnover based commission

All Assessee – Employer

36(1)(v)

gratuity fund created exclusively for the benefit of employees under an irrevocable trust shall be allowed as deduction (Subject to certain

conditions).Actual expenditure not exceeding 8.33% of

salary of each employee

All Assessee – Employer

36(1)(va)

Deposit of employee’s contributions in their respective provident fund or superannuation fund or any fund set up under Employees’

State Insurance Act, 1948

Actual amount received if credited to the employee’s account in relevant fund on or

before due date specified under relevant Act

All Assessee – Employer

36(1)(vi)Allowance in respect of animals which have died or become permanently useless (Subject

to certain conditions)

Actual cost of acquisition of such animals less realization on sale of carcasses of

animalsAll Assessee

36(1)(vii)

Bad debts which have been written off as irrecoverable (Subject to certain conditions)

off from books of accounts Note:-However, if amount of debt or part thereof has been taken into account in computing the income of assessee on basis of income

computation and disclosure standards notified under Section 145(2) without

recording the same in accounts then, such debt shall be allowed in the previous year in

which such debt or part therof becomes irrecoverable. It shall be deemed that such debt or part thereof has been written off as

irrecoverable in the accounts.

All Assessee

36(1)(viia)

Deductions for provision for bad and doubtful debts created by certain banks, financial institutions and non-banking financial

company (Subject to certain conditions).

limited to that amount of bad debts which exceed the provision for bad and doubtful debts created under section 36(1)(viia).Deductions for provision for bad and doubtful debts shall be limited to following:(a) In case of scheduled and non-scheduled banks: Sum not exceeding aggregate of 7.5% of total income (before any deductions under this provision and Chapter VI-A) and 10% of aggregate average advances made by rural branches of such bank;(b) In case of Financial Institutions: Up to 5% of total income before any deductions under this provision and Chapter VI-A; and(c) In case of foreign banks: Up to 5% of total income before any deductions under this provision and Chapter VI-A(d) In case of non-banking financial company: Up to 5% of total income before any deduction under this provision and chapter VI-A

Banks, Public Financial Institutions, Non-banking financial company, State Financial Corporation, State Industrial Investment Corporations

36(1)(viii)

Deduction under this provisions is allowed to following entities in respect of amount transferred to special reserve account:

a) Financial Corporation which is engaged in providing long-term finance for industrial or agricultural development or development of

infrastructure facility in India; orb) Public company registered in India with the

main object of carrying on the business of providing long-term finance for construction or

purchase of residential houses in India.[Subject to certain conditions]

Deduction shall be allowed to the extent of lower of following:

a) Amounts transferred to special reserve account

b) 20% of profits derived from eligible business

c) 200% of paid-up capital and general reserve (on last day of previous year) minus balance in special reserve account (on first

day of previous year)

Specified financial corporations or public company

36(1)(ix)

Expenditure incurred by a company on promotion of family planning amongst

employees is allowed as deduction

1) Entire revenue expenditure is allowed as deduction

2) Capital expenditure shall be allowed as deduction in five equal installment in five

years

Company

36(1)(xii)

Any expenditure incurred by a notified corporation or body corporate constituted or established by a Central, State or Provincial

Act, for the objects and purposes authorized by the respective Act is allowed as deduction

Actual expenditure incurred (not being in the nature of capital expenditure)

Notified corporations

36(1)(xiv)

for micro and small industries is allowed as deduction Actual expenditure incurred

Public Financial Institutions

36(1)(xv)Securities Transaction Tax paid

corresponding income is included as income under the head profits and gains of

business or professionAll Assessee

36(1)(xvi)

paid by an assessee in respect of taxable commodities transactions entered into in the

course of his business during the previous year is allowed as deduction

Actual expenditure incurred if corresponding income is included as

income under the head profits and gains of business or profession

All Assessee

36(1)(xvii)

Amount of expenditure incurred by a co-operative society engaged in the business of

manufacture of sugar for purchase of sugarcane.

Deduction would be allowed the extent of lower of following:

a) Actual purchase price of sugarcane, orb) Price of sugarcane fixed or approved by

the Government

Co-operative society engaged in the business of manufacture of sugar

37(1)

capital expenditure and expenditure mentioned in sections 30 to 36] laid out wholly and exclusively for purposes of business or

profession Actual expenditure incurred

All Assessee

37(2B)Expenditure on advertisement in any souvenir,

brochure etc. published by a political party shall not be allowed as deduction Not Allowed

All Assessee

Section Description

40(a)(i)

Any sum (other than salary) payable outside India or to a non-resident, which is chargeable to tax in India in the hands of the recipient, shall not be allowed to be deducted if it was paid without deduction of tax at source or if tax was deducted but not deposited with the Central Government till the due date of filing of return.However, if tax is deducted or deposited in subsequent year, as the case may be, the expenditure shall be allowed as deduction in that year.

40(a)(ia)

Any sum payable to a resident, which is subject to deduction of tax at source, would attract 30% disallowance if it was paid without deduction of tax at source or if tax was deducted but not deposited with the Central Government till the due date of filing of return.However, where in respect of any such sum, tax is deducted or deposited in subsequent year, as the case may be, the expenditure so disallowed shall be allowed as deduction in that year.

40(a)(ib)

Any sum paid or payable to a non-resident which is subject to a deduction of Equalisation levy would attract disallowance if such sum was paid without deduction of such levy or if it was deducted but not deposited with the Central Government till the due date of filing of return.However, where in respect of any such sum, Equalisation levy is deducted or deposited in subsequent year, as the case may be, the expenditure so disallowed shall be allowed as deduction in that year.Note: This provision has beeninserted by the Finance Act, 2016, w.e.f. 1-6-2016

40(a)(ii)Any sum paid on account of any rate or tax levied on the profits and gains of business or profession is not deductible

40(a)(iia) Wealth-tax or any other tax of similar nature shall not be deductible

40(a)(iib)

Amount paid by way of royalty, license fee, service fee, privilege fee, service charge or any other fee or charge, by whatever name called, which is levied exclusively on (or any amount appropriated) a State Government undertaking by the State Government shall not be deductible.

40(a)(iii)Salaries payable outside India, or in India to a non-resident, on which tax has not been paid/deducted at source is not deductible.

40(a)(iv)Payments to provident fund or other funds for employees’ benefit shall not be deductible if no effective arrangements have been made to ensure deduction of at source from payments made from such funds to employees which shall be chargeable to tax as ‘salaries’.

40(a)(v)Tax paid by the employer on non-monetary perquisites provided to employees is not deductible if the tax so paid is not taxable in the hands of employees by virtue of Section 10(10CC).

Amount expressly disallowed under the Act

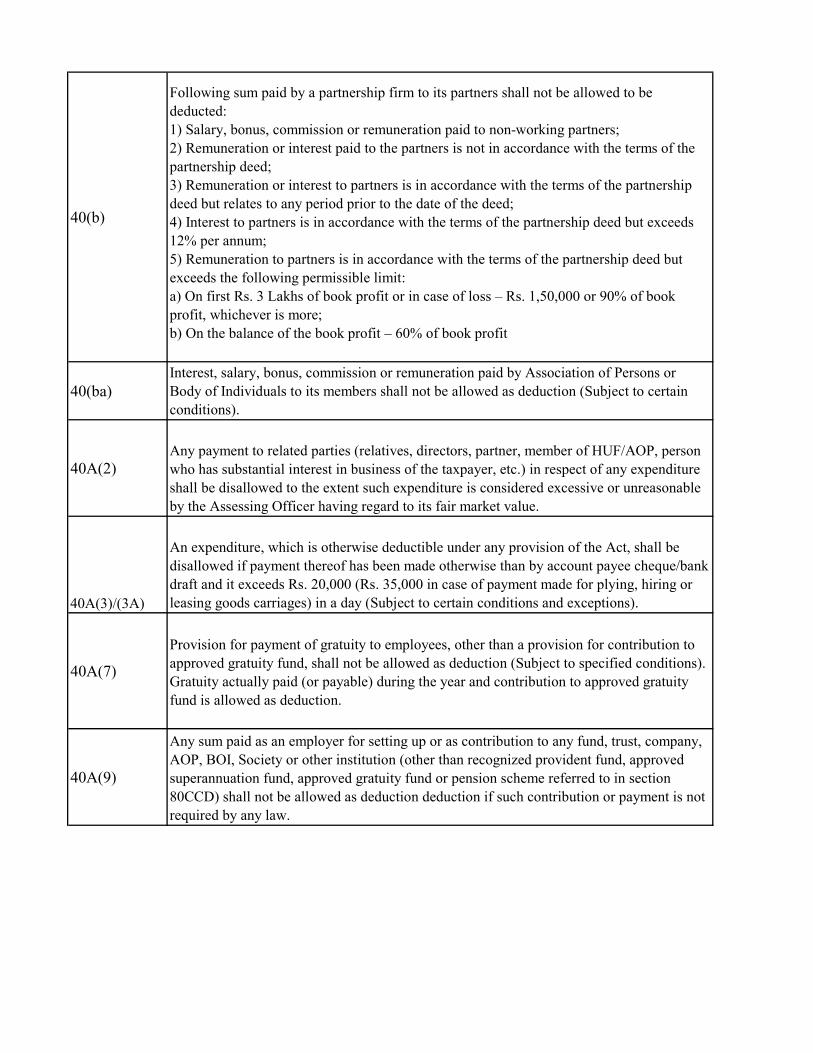

40(b)

Following sum paid by a partnership firm to its partners shall not be allowed to be deducted:1) Salary, bonus, commission or remuneration paid to non-working partners;2) Remuneration or interest paid to the partners is not in accordance with the terms of the partnership deed;3) Remuneration or interest to partners is in accordance with the terms of the partnership deed but relates to any period prior to the date of the deed;4) Interest to partners is in accordance with the terms of the partnership deed but exceeds 12% per annum;5) Remuneration to partners is in accordance with the terms of the partnership deed but exceeds the following permissible limit:a) On first Rs. 3 Lakhs of book profit or in case of loss – Rs. 1,50,000 or 90% of book profit, whichever is more;b) On the balance of the book profit – 60% of book profit

40(ba)Interest, salary, bonus, commission or remuneration paid by Association of Persons or Body of Individuals to its members shall not be allowed as deduction (Subject to certain conditions).

40A(2)Any payment to related parties (relatives, directors, partner, member of HUF/AOP, person who has substantial interest in business of the taxpayer, etc.) in respect of any expenditure shall be disallowed to the extent such expenditure is considered excessive or unreasonable by the Assessing Officer having regard to its fair market value.

40A(3)/(3A)

An expenditure, which is otherwise deductible under any provision of the Act, shall be disallowed if payment thereof has been made otherwise than by account payee cheque/bank draft and it exceeds Rs. 20,000 (Rs. 35,000 in case of payment made for plying, hiring or leasing goods carriages) in a day (Subject to certain conditions and exceptions).

40A(7)

Provision for payment of gratuity to employees, other than a provision for contribution to approved gratuity fund, shall not be allowed as deduction (Subject to specified conditions).Gratuity actually paid (or payable) during the year and contribution to approved gratuity fund is allowed as deduction.

40A(9)

Any sum paid as an employer for setting up or as contribution to any fund, trust, company, AOP, BOI, Society or other institution (other than recognized provident fund, approved superannuation fund, approved gratuity fund or pension scheme referred to in section 80CCD) shall not be allowed as deduction deduction if such contribution or payment is not required by any law.

Section Particulars

43B(a) Any Tax, Duty, Cess or Fees under any Law

43B(b) Any contribution to Provident Fund/Superannuation Fund/Gratuity Fund/Welfare Fund

43B(c)Bonus or Commission paid to employees which would not have been payable as profit or dividend

43B(d)Interest on Loan or Borrowings from Public Financial Institutions/State Financial Institutions etc.

43B(e) Interest on loan or advance from bank

43B(f) Payment of Leave Encashment

43B(g) Sum payable to the Indian Railways for the use of railway assets.

Expenses deductible on actual payment basis

The following expenses shall be allowed as deduction if such expenditure are actually paid on or before the due date of filing of return of income:-

Section Particulars Provision

42

Special allowance in case of business of prospecting etc. for mineral oil (including petroleum and natural gas) in relation to which the Central Government has entered into an agreement with the taxpayer for the association or participation (Subject to certain conditions).

Following deductions shall be allowed as deductions:a) Any infructuous exploration expenditureb) Expenditure on drilling or exploration activities or services, etc.c) Allowance in relation to depletion of mineral oil, etc.

43ASpecial provisions consequential to changes in rate of exchange of Currency (Subject to certain conditions).

Any increase or decrease in the liability incurred in foreign currency (to acquire a capital asset) pursuant to fluctuation in the foreign exchange rates shall be adjusted with the actual cost of such asset only on actual payment of the liability.

43CAcquisition of any asset (except stock-in-trade) by the taxpayer in the scheme of amalgamation or by way of gift, will etc.

Cost of acquisition of any asset (except stock-in-trade) acquired by the taxpayer in the scheme of amalgamation or by way of gift, will etc. from the transferor (who sold it as stock-in-trade) shall be the cost of acquisition in the hands of transferor as increased by cost of any improvement made

Other provisions

Section ParticularsLimit of exemption or

Computation of income/deduction

Available to

44B read with 172

Income from shipping business shall be computed on presumptive basis (Subject to certain conditions).

7.5% of specified sum shall be deemed to be the presumptive income

Non-resident engaged in shipping business

44BB

Income of a non-resident engaged in the business of providing services or facilities in connection with, or supplying plant and machinery on hire used, or to be used, in the prospecting for, or extraction or production of, mineral oils shall be computed on presumptive basis (Subject to certain conditions).

10% of specified sum shall be deemed to be the presumptive income

Non-resident engaged in activities connected with exploration of mineral oils

44BBA

Income of a non-resident engaged in the business of operation of aircraft shall be computed on presumptive basis (Subject to certain conditions).

5% of specified sum shall be deemed to be the presumptive income

Non-resident engaged in the business of operating of aircraft

44BBB

Income of a foreign company engaged in the business of civil construction or the business of erection of plant or machinery or testing or commissioning thereof, in connection with turnkey power projects shall be computed on presumptive basis (Subject to certain conditions).

10% of specified sum shall be deemed to be the presumptive income

Foreign Company

Provisions applicable to Non-Resident/Foreign Company

44CDeduction for Head office Expenditure (Subject to certain conditions and limits)

Deduction for head-office expenditure shall be limited to lower of following:a) 5% of adjusted total income*b) Head office exp. as attributable to business or profession of taxpayer in India* In case adjusted total income of the assessee is a loss, adjusted total income shall be substituted by average adjusted total income** Adjusted total income or average adjusted total income shall be computed after prescribed adjustments i.e. unabsorbed depreciations, carry forward losses, etc.

Non-resident

44DA

Deduction of expenditure from royalty and FTS received under an agreement made after 31-03-2003 which is effectively connected to the PE of non-resident in India (Subject to certain conditions)

Expenditure incurred wholly and exclusively for the business of PE or fixed place of profession in India shall be allowed as deduction.

Non-resident

Section Particulars Threshold

44AA

account – Specified Profession(Subject to certain conditions and circumstances)

Persons carrying on specified profession and their gross receipts exceed Rs. 1,50,000 in all the three years immediately preceding the previous year

44AA

Compulsory maintenance of books of account – Other business or profession(Subject to certain conditions and circumstances)

1) If total sales, turnover or gross receipts exceeds Rs. 10,00,000 in any one of the three years immediately preceding the previous year; or2) If income from business or profession exceeds Rs. 1,20,000 in any one of the three years immediately preceding the previous year

44ABCompulsory Audit of books of accounts (Subject to certain conditions and circumstances)

1) If total sales, turnover or gross receipts exceeds Rs. 1 Crore in any previous year, in case of business; or2) If gross receipts exceeds Rs. 50 Lakhs in any previous year, in case of profession.

Section Nature of business Presumptive income

44AD

Income from eligible business can be computed on presumptive basis if turnover of such business does not exceed two crore rupees.Note: If an assessee opts out of the presumptive taxation scheme, after a specified period, he cannot choose to revert back to the presumptive taxation scheme for a period of five assessment years thereafter. [Section 44AD(4)](Subject to conditions)

Presumptive income of eligible business shall be 8% of gross receipt or total turnover.

44ADA

Income from eligible profession u/s 44AA(1) can be computed on presumptive basis if the total gross receipts from such profession do not exceed fifty lakh rupees in a previous year.(Subject to conditions) Presumptive income of such profession

shall be 50% of total gross receipt.

44AE

Presumptive income of business of plying, hiring or leasing of goods carriage if taxpayer does not own more than 10 goods carriage (Subject to certain conditions)

Rs. 7,500 for every month during which the goods carriage is owned by the taxpayer

Accounts and Audit

Presumptive Taxation

SOME IMPORTANT FAQs WITH CASE LAWS FROM INCOME FROM PROFITS AND GAINS OF BUSINESS OR PROFESSION :-

1. Can the assessee treat shares held in subsidiary company, which is ordered to be wound up, as trading loss? Relevant Case Law - CIT v. H. P. Mineral and Industrial Development Corporation Ltd. (2008) 305 ITR 111 (HP) Relevant Section - 28

One of the assessee’s subsidiary companies was ordered to be wound up and the assessee decided to write off the value of the shares held by it in the subsidiary company.

The lower authorities decided in favour of the assessee holding that there was no question of selling off the shares as the subsidiary company had gone into liquidation.

The High Court held that once a company had been ordered to be wound up, there was no

question of any party dealing in the shares of that company.

The Tribunal had come to a finding that the shares were stock-in-trade and had therefore allowed the loss. The loss had to be treated as a trading loss. The mere fact that the shares were not sold was of no significance since in fact the shares could not have been sold and had become worthless.

2. Whether the amount transferred to the reserve fund account as per the provisions of section 67 of the Gujarat Co-operative Societies Act, 1962, was diversion of income at source by overriding title or could such transfer be treated as business expenditure deductible either under section 28 or section 37? Relevant Case Law - CIT v. Mehsana District Co-op. Milk Producers’ Union Ltd. (2008) 307 ITR 83 (Guj.) Relevant Section - 28

The assessee contended that under sub-section (2) of section 67 of the Gujarat Co-operative Societies Act, 1962, at least one-fourth of the net profits of the society were required to be carried to the reserve fund every year, and hence there was a diversion at source by virtue of the provisions of section 67 which operates as an overriding title.

Hence, it was submitted that the amount transferred to the reserve fund could not be charged as income liable to tax under the Act. Alternatively, it was pleaded that the amount of profits transferred to the reserve fund would constitute a charge on the taxable income under the provisions of section 28 of the Income-tax Act, 1961, or an expenditure

having the characteristics of business expenditure under section 37. The Assessing Officer rejected the contention and this was upheld by the Tribunal.

The High Court held that it was only in the event the society did not choose to use the

reserve fund for the business of the society that the question about investing the reserve fund in the specified category of investments and thereafter utilizing the same for the objects specified by the State Government could arise.

Hence, not only was there no diversion of income by overriding title but in fact there was no outgoing of funds from the domain of the assessee society. In fact, the profits at the specified percentage were set apart so as to be available to the society for use in the business of the society at a later point of time.

Once the society was in a position to use the funds lying in the reserve fund for the business of the society as and when the society so chose, there could be no question of keeping out such profits from the purview of taxation.

The Tribunal was right in law in holding that the amount transferred to the reserve fund account as per the provisions of section 67 of the Gujarat Co-operative Societies Act, 1962, was not diversion of income at source by overriding title nor could such transfer be treated as business expenditure deductible either under section 28 or section 37.

3. Whether the amount received by the assessee under a lease agreement is income from other sources or business income? Relevant Case Law - East West Hotels Ltd. v. DCIT (2009) 309 ITR 149 (Kar.) Relevant Section - 28

The assessee was engaged in the hotel business activities. The assessee by an agreement with IHC gave one of its hotels on lease for an initial period of 33 years with an option to renew for a further period of 33 years.

The assessee claimed that the amount received from IHC had to be treated as its business income. The claim was rejected by the Assessing Officer on the ground that the assessee was not getting any business income as the hotel had been leased out by the assessee to IHC and any amount received by the assessee from such company had to be treated as income from other sources and not business income.

The Commissioner (Appeals) as well as the Tribunal held that the income received by the assessee from such hotel building was income from other sources.

The High Court held that the clauses in the agreement were more in the nature of a lease

deed and not a licence given for a particular period with no intention to resume its business of hotel in the premises.

It could not be said that the assessee had been managing the hotel through IHC. Therefore, the amount received from IHC had to be treated as income from other sources and not as business income.

4. Whether the swapping premium is profit derived from the business of providing long term finance in terms of section 36(1)(viii) of the Income-tax Act, 1961 ? Relevant Case Law - Rural Electrification Corporation Ltd., In re (2009) 308 ITR 321 (AAR) Relevant Section: 36(1)(viii)

The main object of the applicant, a public sector undertaking, was to provide long-term finance, primarily to State Electricity Boards, for the purpose of transmission, distribution and generation of electricity to enable industrial, agricultural and infrastructure development.

The applicant was filing income-tax returns right from the beginning and the Department had all along, in the past, allowed deduction under section 36(1)(viii) of the Income-tax Act, 1961, in respect of the special reserve created and maintained for providing long-term finance for industrial or agricultural development or development of infrastructure.

For the assessment year 2004-05, the applicant credited Rs.170.85 crores as “swapping premium” received and claimed deduction thereon under section 36(1)(viii). “Swapping premium” was a scheme under which long-term finance given at a higher percentage of interest was converted to a lower rate of interest.

The applicant itself had declared the swapping premium receipt in its balance-sheet as “Other income” and not income from lending operations. The Assessing Officer held that the applicant forfeited the claim for allowance of deduction under section 36(1)(viii) in respect of the “swapping premium”.

The Commissioner (Appeals) agreed with the Assessing Officer. The applicant appealed to the Appellate Tribunal but withdrew the appeal. Meanwhile, the applicant obtained permission of the Committee on Disputes to pursue the matter before the Authority.

The Authority ruled: (i) That the applicant was an eligible entity, i.e., a financial corporation as laid down in section 36(1)(viii). (ii) That the applicant was engaged in the business of providing long-term finance to its clients for rural electrification which paved the way for industrial, agricultural and infrastructural development. The availability of electricity contributed significantly to the overall development of the country including that

of industry, agriculture and infrastructure. The provision of electricity was essential for modernization and growth of agriculture and also catered to the requirements of industry including small and medium industries, agro-industries, Khadi and village industries, etc. The applicant had been providing finance for industrial and agricultural development and, keeping in view these very goals, the Government of India had granted approval to the applicant for deduction under section 36(1)(viii). The applicant could be said to be engaged in providing longterm finance for industrial and agricultural development in India. (iii) That the long-term loan financed by the applicant to its clients in the beginning had not been tampered with on rescheduling of the interest and no fresh loan agreements had also been drawn. (iv) That clause (e) of the Explanation to section 36(1)(viii) defined long-term finance as “any loan or advance where the terms under which moneys are loaned or advanced provide for repayment along with interest thereon during a period of not less than five years”. In this case, the loans had been advanced in the beginning for five years and those loan amounts had not undergone any change, so the period of five years had to be counted from the date of advancing the initial loans and not from the date of rescheduling the interest rates. (v) That the “swapping premium” was nothing but discounted interest and had “originated” in the long-term finance initially advanced. The premium was actually traced to the original source and was not a step removed from the business of providing long-term finance. No fresh agreement had been entered into for advancing long-term financing and the one-time measure for rescheduling the interest had been actuated by business expediency. The swapping premium was simply a compensation received for agreeing to a lesser amount as against a higher fixed rate of interest initially fixed. The business of providing long-term finance was the immediate and effective source of the swapping premium received. (vi) That the swapping premium could not be termed as compensation for breach of contract because neither party had breached the contract. The disclosure of the swapping premium in the balance-sheet as “Other income” instead of business income was also immaterial since entries in the books of account are not determinative of the true character of a receipt. (vii) That, therefore, the applicant was entitled to deduction under section 36(1) (viii) in respect of the swapping premium received.

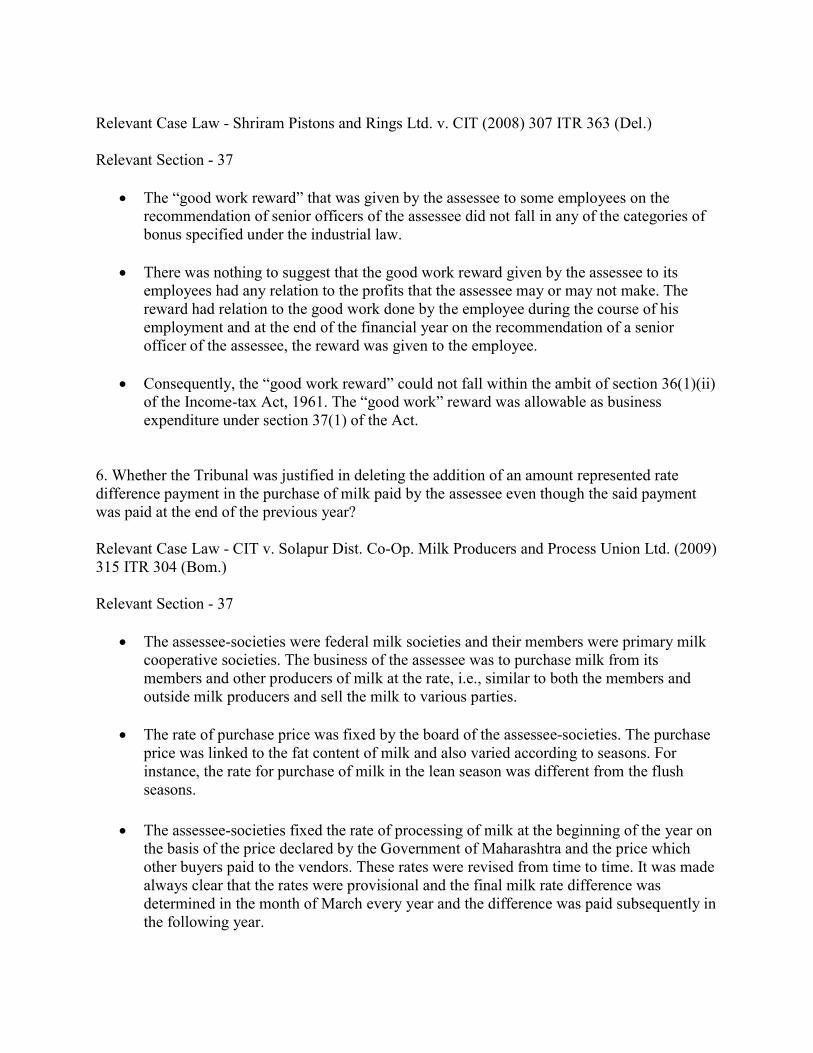

5. Whether the payments made by the assessee to its employees under the nomenclature ‘Good work reward’ constitute bonus within the meaning of section 36(1)(ii) of the Income-tax Act, 1961 or were allowable as normal business expenditure under section 37 ?

Relevant Case Law - Shriram Pistons and Rings Ltd. v. CIT (2008) 307 ITR 363 (Del.) Relevant Section - 37

The “good work reward” that was given by the assessee to some employees on the recommendation of senior officers of the assessee did not fall in any of the categories of bonus specified under the industrial law.

There was nothing to suggest that the good work reward given by the assessee to its employees had any relation to the profits that the assessee may or may not make. The reward had relation to the good work done by the employee during the course of his employment and at the end of the financial year on the recommendation of a senior officer of the assessee, the reward was given to the employee.

Consequently, the “good work reward” could not fall within the ambit of section 36(1)(ii) of the Income-tax Act, 1961. The “good work” reward was allowable as business expenditure under section 37(1) of the Act.

6. Whether the Tribunal was justified in deleting the addition of an amount represented rate difference payment in the purchase of milk paid by the assessee even though the said payment was paid at the end of the previous year? Relevant Case Law - CIT v. Solapur Dist. Co-Op. Milk Producers and Process Union Ltd. (2009) 315 ITR 304 (Bom.) Relevant Section - 37

The assessee-societies were federal milk societies and their members were primary milk cooperative societies. The business of the assessee was to purchase milk from its members and other producers of milk at the rate, i.e., similar to both the members and outside milk producers and sell the milk to various parties.

The rate of purchase price was fixed by the board of the assessee-societies. The purchase price was linked to the fat content of milk and also varied according to seasons. For instance, the rate for purchase of milk in the lean season was different from the flush seasons.

The assessee-societies fixed the rate of processing of milk at the beginning of the year on the basis of the price declared by the Government of Maharashtra and the price which other buyers paid to the vendors. These rates were revised from time to time. It was made always clear that the rates were provisional and the final milk rate difference was determined in the month of March every year and the difference was paid subsequently in the following year.

The primary milk society also in turn made payment of the final rate difference to the individual milk producers around Diwali. The assessees claimed deduction of the final rate difference. The Assessing Officer refused to exclude the final rate difference paid from the total amount paid by the assessee. The Commissioner (Appeals) upheld the order. The Tribunal allowed the appeal and allowed deductions of the final rate.

The High Court held that the amount to be paid was not out of the profits ascertained at

the annual general meeting. It was not paid to all shareholders. The amount which was the subject-matter was paid to members who supplied milk and in some case also to nonmembers.

The payment was for the quantity of milk supplied and in terms of the quality supplied. The commercial expediency for payment of this price was the market conditions and the need to procure more milk from the members and non-members to the assessee.

Therefore, the amount paid could not be said to be dividend to the members or shareholders or payment in the form of bonus as bonus also had to be paid from the accrued profits. It was deductible.

7. Whether the expenses incurred by the assessee for promotion films, slides, advertisement films is capital expenditure? Relevant Case Law - CIT v. Geoffrey Manners and Co. Ltd. (2009) 315 ITR 134 (Bom.) Relevant Section - 37

The assessee incurred expenditure on film production by way of advertisement for the marketing of products manufactured by it. The Assessing Officer disallowed the expenses incurred by the assessee for promotion films, slides, advertisement films and treated it as capital expenditure.

The Commissioner (Appeals) held that the films were in the form of advertisement whose life term could not be ascertained. Therefore, they could not be held as capital expenditure. The Tribunal upheld the order of the Commissioner (Appeals).

The High Court held that if the expenditure is in respect of an ongoing business of the assessee and there is no enduring benefit it can be treated as revenue expenditure. If the expenditure is in respect of business which is yet to commence then it cannot be treated as revenue expenditure since the expenditure is on a product yet to be marketed.

Hence, the expenditure incurred in respect of promoting ongoing products of the assessee was revenue expenditure.

8. Whether the expenditure incurred by the assessee in the machinery repairs could be treated as revenue expenditure though this related to the cost of motors and other items resulting in an enduring benefit to the assessee and was in the nature of capital expenditure? Relevant Case Law - CIT v. Hero Cycles P. Ltd (2009) 311 ITR 349 (P&H) Relevant Section - 37

The assessee claimed expenditure of Rs. 73,180 on purchase of motors and certain other items of machinery. The Assessing Officer rejected the claim for treating the amount as revenue expenditure on the ground that the items purchased by the amount were not spare parts but independent items and the amount had, thus, to be treated as capital expenditure.

On appeal, the plea of the assessee that most of the items purchased were electric motors for replacement of existing machinery, was upheld. The Tribunal affirmed the order and held that occasional replacements were necessary having regard to the machinery installed.

The High court held that the Tribunal was right in law in allowing expenditure of Rs.73,180 shown by the assessee in the machinery repairs account as revenue expenditure.

9. Whether the fine paid for belated payment of excise duty is a allowable business expenditure? Relevant Case Law - CIT v. Hoshiari Lal Kewal Krishan (2009) 311 ITR 336 (P&H) Relevant Section - 37

The assessee claimed deduction of Rs. 31,433 paid as fine for belated payment of the excise duty instalment. This was disallowed by the Assessing Officer as well as the appellate authority but the Tribunal allowed it.

The Supreme Court in Prakash Cotton Mills P. Ltd. v. CIT [1993] 201 ITR 684, observed that whenever any statutory impost paid by an assessee by way of damages or penalty or interest is claimed as an allowable expenditure under section 37(1) of the Income-tax Act, the assessing authority is required to examine the scheme of the provisions of the relevant statute providing for payment of such impost notwithstanding the nomenclature of the impost as given by the statute, to find whether it is compensatory or penal in nature.

The authority has to allow deduction under section 37(1) of the Income-tax Act, wherever such examination reveals the concerned impost to be purely compensatory in nature.

Hence, in the present case, the High Court held that it had been clearly found that though termed as fine, the payment was not in the nature of punishment but was by way of compensation. The payment was deductible.

10. Whether section 40(b) of the Income-tax Act, 1961, is applicable to the amount of salary and bonus paid by the assessee-firm to its partners for their individual service as against their Hindu undivided family character? Relevant Case Law - CIT v. Unimax Laboratories (2009) 311 ITR 191 (P&H) Relevant Section - 40(b)

The Assessing Officer made an addition under section 40(b) of the Income-tax Act, 1961, on account of salary and bonus paid by the assessee-firm to its four working partners. Those partners were partners in their representative capacity as karta of their Hindu undivided families.

Since these partners represented their respective Hindu undivided families, they were treated to be partners for the purpose of disallowance of benefits under section 40(b) of the Act by the Assessing Officer.

However, on appeal the addition was deleted on the ground that the salary and bonus were paid to these persons as individuals and in these circumstances section 40(b) of the Act had no application.

The High Court held that the Tribunal was right in allowing the amount of salary and bonus paid by the firm to partners for services rendered by them on the ground of having technical qualification and expertise, though they represented their Hindu undivided families and section 40(b) of the Act was not attracted.

11. Whether the amount written back by the assessee to the credit of its profit and loss account during the accounting period under consideration constituted income of the assessee-company under section 41(1) of the Income-tax Act 1961? Relevant Case Law - Jay Engineering Works Ltd. v. CIT (2009) 311 ITR 299 (Del.) Relevant Section: 41(1)

The assessee had written back in its accounts unclaimed balances totalling Rs.1,16,240. The Inspecting Assistant Commissioner added back this amount to the income of the assessee. This was upheld by the Commissioner (Appeals) as well the Tribunal.

The High Court held that the amounts were not statutory liabilities but contractual liabilities. These amounts were unilaterally written off by the assessee. Therefore, the unclaimed liability written off by the assessee was taxable as income.

12. Whether the amount transferred to profit and loss account in case of waiver of loan taken by assessee for business purposes assessable as business income under section 41(1) of the Income-tax Act, 1961? Relevant Case Law - Solid Containers Ltd. v. DCIT (2009) 308 ITR 417 (Bom.) Relevant Section: 41(1)

The assessee had taken a loan for business purposes which was written back and directly credited to the reserves account, as a result of consent terms arrived at in a suit.

The assessee claimed this amount as capital receipt, even though it had offered the interest on the said loan as its income by crediting the same to its profit and loss account.

The Assessing Officer added the amount to the total income of the assessee as its income and this was upheld by the Tribunal.

The High Court held that it was a loan taken for trading activity and ultimately, upon waiver the amount was retained in the business by the assessee. The amount had become the assessee’s income and was assessable.

13. Is depreciation under section 32 allowable in respect of emergency spares of plant and machinery, which though acquired during the previous year, have not been put to use in that year? Relevant Case Law - CIT v. Insilco Ltd. (2009) 179 Taxman 55 (Del.) Relevant Section - 32

On this issue, the Delhi High Court observed that the expression “used for the purposes of business” appearing in section 32 also takes into account emergency spares, which, even though ready for use, yet are not consumed or used during the relevant period.

This is because these spares are specific to a fixed asset, namely plant and machinery, and form an integral part of the fixed asset. These spares will, in all probability, be useless once the asset is discarded and will also have to be disposed of. In this sense, the concept of passive use which applies to standby machinery will also apply to emergency spares.

Therefore, once the spares are considered as emergency spares required for plant and machinery, the assessee would be entitled to capitalize the entire cost of such spares and claim depreciation thereon.

Note – One of the conditions for claim of depreciation is that the asset must be “used for the purpose of business or profession”. In the past, courts have held that, in certain circumstances, an asset can be said to be in use even when it is “kept ready for use”. For example, depreciation can be claimed by a transport company on spare engines kept in store in case of need, though they have not actually been used by the company. Hence, in such cases, the term “use” embraces both active use and passive use. However, such passive use should also be for business purposes. 14. What is the tax treatment of pre-payment premium paid by the assessee-company to IDBI for restructuring its debt? Relevant Case Law - CIT v. Gujarat Guardian Ltd. (2009) 177 Taxman 434 (Del.) Relevant Section - 43B

The assessee-company paid pre-payment premium to IDBI during the relevant previous year for restructuring its debts and reducing the rate of interest. It claimed the full payment as business expenditure in that year on the reasoning that it was an upfront payment representing the present value of the differential rate of interest that would have been due on the loan if the restructuring of loan had not taken place.

The Assessing Officer and Commissioner (Appeals) were of the view that the premium has to be amortised over 10 years, and accordingly allowed only 1/10th of the premium as deduction for the relevant previous year. The Tribunal, however, concurred with the assessee’s view and held that in terms of section 36(1)(iii) read with section 2(28A), the deduction for pre-payment premium was allowable.

The issue under consideration is whether the deduction has to be allowed in one lump-sum as claimed by the assessee or should the same be deferred over a period of time as opined by the Assessing Officer and Commissioner (Appeals).

The Delhi High Court concurred with the Tribunal’s view that the deduction has to be allowed to the assessee-company in one lump sum according to the provisions of section 43B(d).

Section 43B(d) provides that any sum payable by the assessee as interest on any loan or borrowing from any public financial institution shall be allowed to the assessee in the year in which the same is paid, irrespective of the period or periods in which the liability to pay such sum is incurred by the assessee according to the method of accounting

regularly followed by the assessee. As there was no dispute that the pre-payment premium paid represented interest and that it was paid to a public financial institution

i.e. IDBI, the Court held that, as per the provisions of section 43B(d), the assessee’s claim for deduction has to be allowed in the year in which the actual payment was made i.e. the previous year relevant to the assessment year under consideration.

Note – Section 36(1)(iii) provides for deduction of interest paid in respect of capital borrowed for the purposes of business or profession. Section 2(28A) defines interest to include, inter alia, any other charge in respect of the moneys borrowed or debt incurred. Section 43B provides for certain deductions to be allowed only on actual payment. From a combined reading of these three sections, it can be inferred that – (i) pre-payment premium represents interest as per section 2(28A); (ii) such interest is deductible as business expenditure as per section 36(1)(iii); (iii) such interest is deductible in one lump-sum on actual payment as per section 43B(d).

Introduction

The Central Government recently notified 10 Income Tax Computation & Disclosure Standards (ICDS) effective financial year 2015–16. This will affect the compliance practice of all taxpayers following the mercantile system of accounting for computing income chargeable to income tax under the heads:

Profits and gains of business or profession or

Income from other sources

Objective of ICDS

ICDS were developed with a view to minimising tax related disputes by bringing greater consistency in the application of accounting principles governing the computation of income. These standards were developed using the old Indian General Audit and Accounting Practices (GAAP).

Main Features of ICDS

In case of conflict between the provisions of the Income-Tax Act, 1961 and ICDS, then the provisions of the Income-Tax Act would prevail.

No need to maintain separate books of accounts for ICDS. It only for income computation.

Applicability

Applicable to all Assesses following Mercantile System of Accounting and chargeable to tax under the head “Profit and Gains of Business or Profession” OR “Income from Other Source”

It is applicable to all assesses

o Irrespective of applicability of Tax Audit

o Irrespective of Turnover

o Irrespective of Status of Individual (AOP, Firm, Resident, Non Resident etc.)

Non Compliance of ICDS

Every assesse is required to implement ICDS and potential impact will be considered by companies while estimating advance tax liability for FY 15-16, due on 15 June 2015. Noncompliance of ICDS will result in best judgement assessment by tax authorities, which may lead to protracted litigations.

List of ICDS

No. Income Computation and Disclosure Standards Corresponding Accounting Standards

ICDS I Accounting Policies AS-1

ICDS II Valuation of Inventories AS-2

ICDS III Construction Contracts AS-7

ICDS IV

Revenue Recognition AS-9

ICDS V Tangible Fixed Assets AS-10

ICDS VI

The Effect of Changes in Foreign Exchange Rates AS-11

ICDS VII

Government Grants AS-12

ICDS VIII

Securities AS-13

ICDS IX

Borrowing Cost AS-16

ICDS X Provisions, Contingent Liabilities and Contingent Assets

AS-29

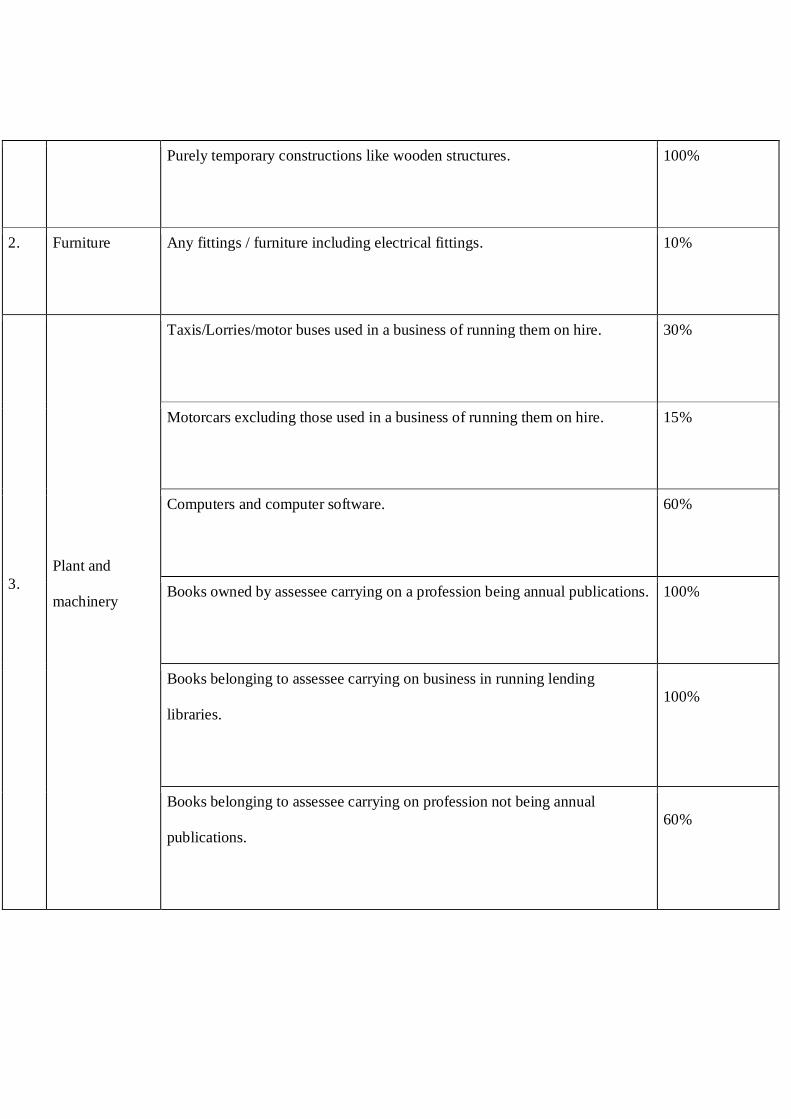

What is Depreciation?