PROGRAM IMPLEMENTATION PLAN - World Banksiteresources.worldbank.org/.../PSCAP/pip_vol_2.pdf ·...

145

Federal Democratic Republic of Ethiopia PROGRAM IMPLEMENTATION PLAN for PUBLIC SECTOR CAPACITY BUILDING PROGRAM (PSCAP) Volume II Draft Dated: October 28, 2004

Transcript of PROGRAM IMPLEMENTATION PLAN - World Banksiteresources.worldbank.org/.../PSCAP/pip_vol_2.pdf ·...

Federal Democratic Republic of Ethiopia

PROGRAM IMPLEMENTATION PLAN

for

PUBLIC SECTOR CAPACITY BUILDING PROGRAM

(PSCAP)

Volume II

Draft Dated: October 28, 2004

Table of Contents

PARTICIPATION AND PERFORMANCE AGREEMENTS............................................................. 4

PSCAP ANNUAL PERFORMANCE AGREEMENT MATRIX..........Error! Bookmark not defined.

FINANCIAL MANAGEMENT GUIDELINES ................................................................................. 4

Introduction............................................................................................................................... 4

Background ............................................................................................................................... 4

Institutional Arrangement ....................................................................................................... 5

Funding Modalities................................................................................................................... 6

Accounting Policies and Procedures ....................................................................................... 6

Budget and Budgetary Control................................................................................................ 7

Budget Code17 Regions that are using single entry accounting code ....................................................................... Budget preparation and control.....................................................................................................

Chart of Account .........................................................................................................................

Accounting Cycle.........................................................................................................................

Receipt of Money.........................................................................................................................

Transfer of Fund to Beneficiaries..............................................................................................

Disbursements .............................................................................................................................

Check Payments and Bank Transfers .......................................................................................

Cash Payments ............................................................................................................................

Journal Vouchers ........................................................................................................................

Accounting Records ....................................................................................................................

Transactions in Register.............................................................................................................

Budget Ledger Card ...................................................................................................................

General Ledger............................................................................................................................

Subsidiary Ledger.......................................................................................................................

Reporting Types and Frequency of Reporting ........................................................................

Report Preparation Responsibilities .........................................................................................

Methods of Report Preparation................................................................................................. Monthly Reporting ...................................................................................................................... Statement of Expenditures (SOE) ................................................................................................. Financial Monitoring Reports (FMR)............................................................................................

2

Quarterly Financial Reports.......................................................................................................... Annual Reports ...........................................................................................................................

Travel Expenses ..........................................................................................................................

Procurement ................................................................................................................................

Receipt and Issuance of Goods ..................................................................................................

Management and Control of Program Assets ..........................................................................

Internal Controls .........................................................................................................................

Auditing........................................................................................................................................ External Audit ............................................................................................................................. Internal Audit .............................................................................................................................. Retaining Documents...................................................................................................................

Revision of Financial Manual ....................................................................................................

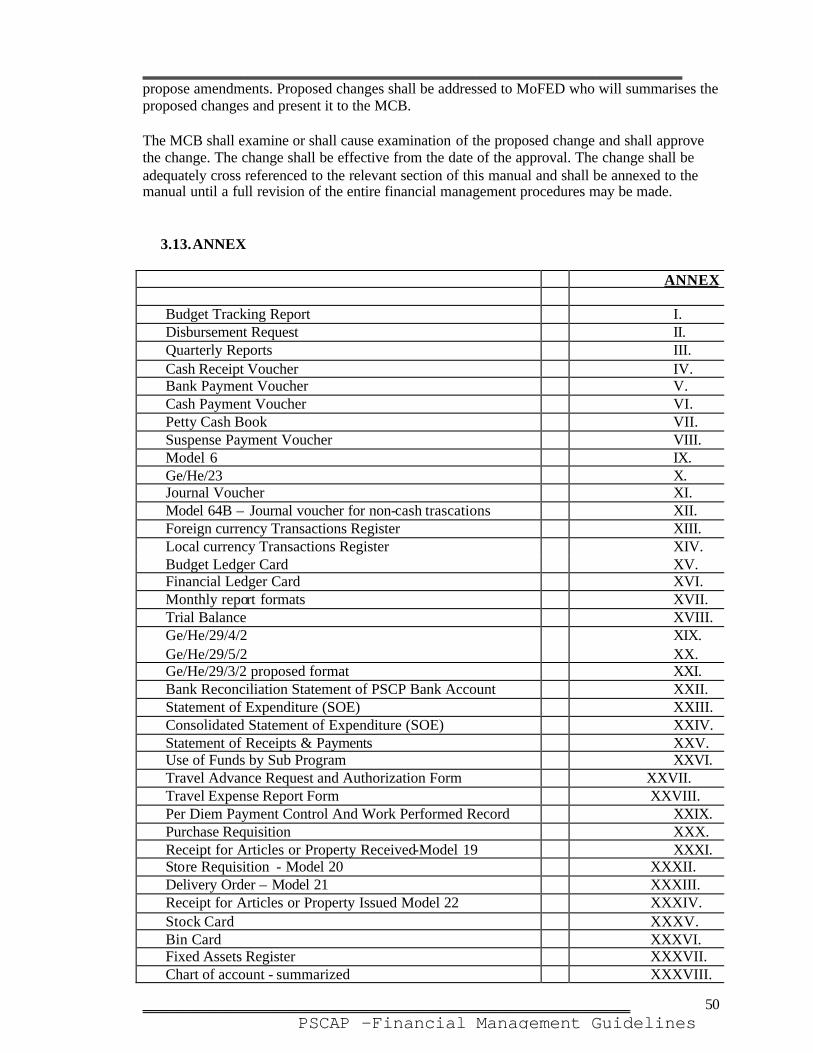

Annex................................................................................................................................................

Sample Financial Monitoring Report .......................................................................................

Sample Procurement Status Report .......................................................................................... SAMPLE PROCUREMENT TEMPLATES AND FORMS..................................................................

Procurement Planning Template - Goods ................................................................................

Procurement Planning Template - Consultants .......................................................................

Sample Training Plan.................................................................................................................

Sample General Procurement Notice ........................................................................................

Sample Request for Expressions of Interest - Consultants .....................................................

Sample Invitation for Prequalification .....................................................................................

Sample Standard Unit Rates...................................................................................................... DETAILED PROGRAM DESCRIPTION ...........................................................................................

Subprogram 1—Civil service reform........................................................................................

Subprogram 2—District-level decentralization .......................................................................

Subprogram 3—Justice system reform ....................................................................................

Subprogram 4—Urban management capacity building .........................................................

Subprogram 5—Tax systems reform........................................................................................

Subprogram 6—Information and communications technologies...........................................

Mandatory activity—Program support ....................................................................................

SAMPLE TERMS OF REFERENCE – CIVIL SERVICE REFORM SUBPROGRM...........................

Report Card/Client Survey Consultancy ..................................................................................

Route 1 Sub-project Proposal ....................................................................................................

3

Route 1 Business Process Review (BPR) and Reengineering ..................................................

Training of Frontline Staff for Route 1.....................................................................................

Training in Strategic Planning for Route 2 ..............................................................................

Preparation of a Strategic Plan for Route 2 .............................................................................

Training in core Civil Service Reform Activities for Route 2.................................................

Implementation Support for Route 2 Implementation............................................................

Job Classification, Grading, and Pay Policy Consultancy ......................................................

Pay Reform Consultancy............................................................................................................

Chief Technical Advisor. Civil Service Reform Program.......................................................

Performance Tracking Facility—Preparation of Operational Manual................................. SAMPLE TERMS OF REFERENCE – DLDP & URBAN...................................................................

Core Capacity for Local Governance .......................................................................................

Medium Term Capacity Building Advisor. District Level Decentralisation Program ........

Pilot Local Government Fiscal/Financial Analyses .................................................................

Assistance in Pilot Infrastructure Rehabilitation Design........................................................ SAMPLE TERMS OF REFERENCE – PROGRAM SUPPORT..........................................................

Planning & Programming Directorate (PPD)..........................................................................

Technical Team (TT) ..................................................................................................................

Procurement Specialist (International).....................................................................................

Procurement Specialist (National).............................................................................................

Project Accountant .....................................................................................................................

Information, Education & Communication Specialist............................................................

Audit of Project Account Statement .........................................................................................

Program Management Assistance .............................................................................................

Assistance in Project Design & Implementation......................................................................

4

Public Sector Capacity Building Program (PSCAP) PARTICIPATION AND PERFORMANCE AGREEMENTS

Whereas the Ministry of Finance and Economic Development has entered into an agreement with the International Development Association (IDA) to be known as Development Credit Agreement of Public Sector Capacity Building Program (PSCAP) and whereas the Ministry of Finance and Economic Development has agreed to make finances available to the Ministry of Capacity Building for the provision of goods, training and services to Executing Agency (EA). Now therefore the Ministry of Capacity Building (hereinafter refereed to as the “Ministry” and the [insert official name the [Executing Agency (EA)] (hereinafter referred to as [insert official shortened form of name]); Agree as follows: That the Ministry has agreed to fund technical assistance services, training and goods (except – vehicles) for the period [insert start date of TA, training and goods provision] to the [insert end date of TA, training and goods provision] on a non-reimbursable basis as outlined in [insert relevant section of DCA- Schedule 4: section 5 and 6] of the Development Credit Agreement of Public Sector Capacity Building Program (PSCAP) The funding made available may be used for supporting Technical Assistance, training and goods provision for EAs. The funding will be provided in the form of (----- cash transfers) based upon Annual Action Plan reviewed by (Regional Technical Team / the relevant sub-program directors), submitted by the [insert official shortened form of the name of EA] and approved by the PSCAP Federal Technical Team of the Federal Government of the Democratic Republic of Ethiopia. The [insert official shortened form of name of the EA] hereby agrees that the goods, consultants’ services and training to be financed from PSCAP shall be procured in accordance with procedures ensuring efficiency and economy and in accordance with the provisions made available in the PIP and shall be used exclusively in the carrying out of agreed program activities; and The [insert official shortened form of name of the EA] hereby agrees that the source of technical assistance, training and goods provided will only be from “participating countries” i.e. those countries that meet requirements set forth in Section 5(e) of Resolution No. IDA 184 of the Board of Governors of the International Development Association adopted on June 26, 1996. As at September 2002 the following countries are not eligible to supply technical assistance service, training and goods paid by Public Sector Capacity Building Program (PSCAP) Fund [insert list of countries – Andora, cuba, Democratic People’s Republic of Korea (North Korea), Liechtenstein, Monaco, Nauru, San Marino and Tuvalu]. The list will be updated from time to time. The [insert official shortened form of name of the EA] further certifies that:

5

The [insert official shortened form of name of the EA] desires to build capacity to contribute

to the delivery of the overall PSCAP development objectives, namely improve the scale, efficiency and responsiveness of public service delivery at the (EA); empower citizens to participate more effectively in shaping their own development; and promote good governance and accountability.

The EA has agreed to comply with the rules of access allocation and execution of the

Program, as specifically set forth in the Program Implementation Plan, and commit to deliver on agreed performance outputs on a semi-annual basis summarized in the attached Performance Matrix.

The EA has agreed to establish appropriate governance and implementation arrangements

and secured adequate technical, financial management and procurement capacity to implement the proposed PSCAP activities in compliance with the guidelines set forth in the Program Implementation Plan, or has adopted a specific, time-bound plan of actions satisfactory to Federal Technical Team, to strengthen its capacity;

The EA has committed to timely submission of endorsed and costed medium-term rolling

plans, including technically sound, feasible annual implementation and procurement plans for the subsequent Fiscal Year and agreed to complete the minimum capacity building activities before engaging on others; and

The EA has agreed to make adequate provision for carrying out an adequate evaluation of

annual performance for the subsequent year, reporting on progress made to Federal PPD including evidence of dissemination of such evaluation to the public as part of consultative planning process.

The EA has given Federal Technical Team to: (A) inspect by itself, or jointly with the

donors, if the donors shall so request, the goods, services and training included in PSCAP activities and any relevant records and documents; and (B) obtain all information as it, or the donors, shall reasonably request regarding the administration, operation and financial conditions of PSCAP activities.

The EA has attached the documentary evidence for provisions under b, c, d and e including

the action plans, detailed description of the implementation arrangement and performance matirx

In witness of whereof the parties hereto, acting through their duly authorized representatives, have caused this Agreement to be signed in their respective names as of the day and year first below written. The Minister of Capacity Building on behalf of the Federal Government of the Republic of Ethiopia:

6

___________________________________________________ [insert date of signature] witnessed by: Witness 1 Witness 2 Name______________________________ Name:________________________ Title:______________________________ Title:_________________________ Date:_______________________________ Date:_________________________ Signature: Signature The [insert title of signee] on behalf of the [insert official shortened form of name of the EA] ___________________________________________________ [insert date of signature] witnessed by: Witness 1 Witness 2 Name______________________________ Name:________________________ Title:______________________________ Title:_________________________ Date:_______________________________ Date:_________________________ Signature: Signature

7

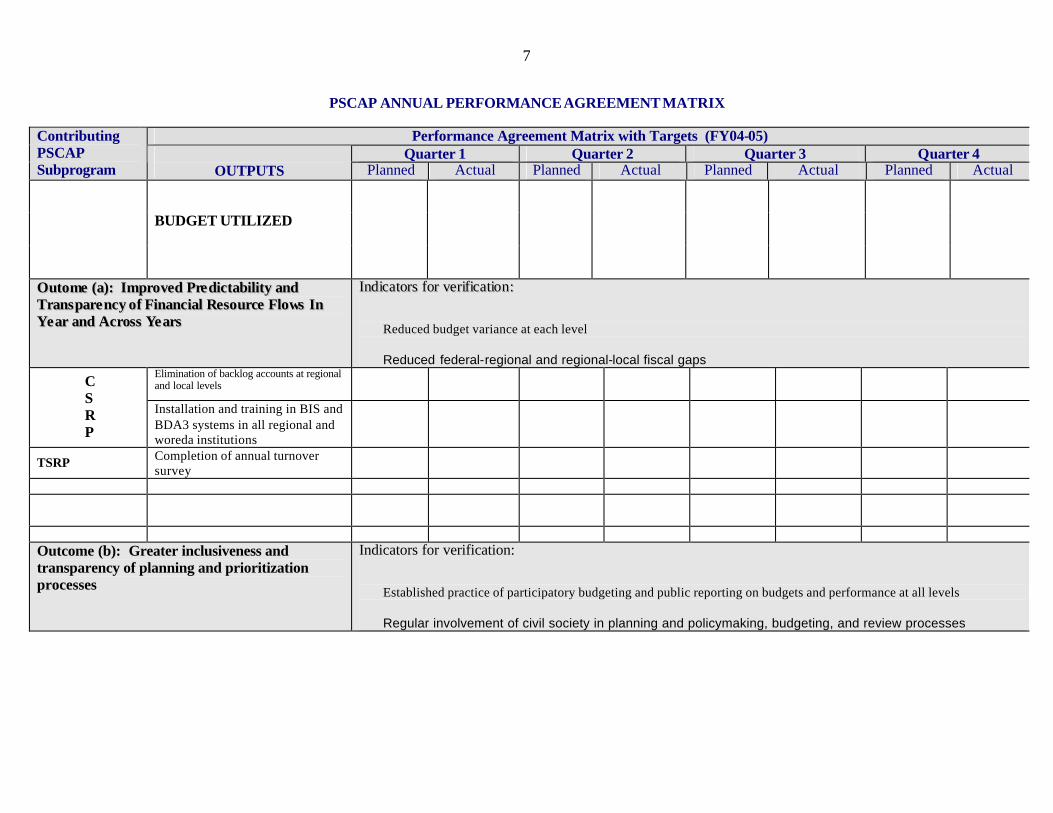

PSCAP ANNUAL PERFORMANCE AGREEMENT MATRIX

Performance Agreement Matrix with Targets (FY04-05) Quarter 1 Quarter 2 Quarter 3 Quarter 4

Contributing PSCAP Subprogram

OUTPUTS Planned Actual Planned Actual Planned Actual Planned Actual

BUDGET UTILIZED

OOuuttoommee ((aa)):: IImmpprroovveedd PPrree ddiiccttaabbiilliittyy aanndd TTrraannss ppaarree nnccyy ooff FFiinnaanncciiaall RReessoouurrccee FFlloowwss IInn YYee aarr aanndd AAccrroossss YYee aarrss

IInnddiiccaattoorrss ffoorr vveerriiffiiccaattiioonn::

Reduced budget variance at each level

Reduced federal-regional and regional-local fiscal gaps Elimination of backlog accounts at regional and local levels

CSRP

Installation and training in BIS and BDA3 systems in all regional and woreda institutions

TSRP Completion of annual turnover survey

Outcome (b): Greater inclusiveness and transparency of planning and prioritization processes

Indicators for verification:

Established practice of participatory budgeting and public reporting on budgets and performance at all levels

Regular involvement of civil society in planning and policymaking, budgeting, and review processes

8

Performance Agreement Matrix with Targets (FY04-05) Quarter 1 Quarter 2 Quarter 3 Quarter 4

Contributing PSCAP Subprogram

OUTPUTS Planned Actual Planned Actual Planned Actual Planned Actual

DLDP

Finalization of strategy and action plan for gender sensitized community participation

CSRP Installation and training in medium term expenditure management procedures manual;

Program Support Completion of training in PIP, procurement, financial management, and M&E

Outcome (c): Enhanced fiscal autonomy and revenue performance

Indicators for verification: Increased own revenues and unconditional transfers as a share of total expenditures at sub-national levels

Increased tax effort at all levels

9

Performance Agreement Matrix with Targets (FY04-05) Quarter 1 Quarter 2 Quarter 3 Quarter 4

Contributing PSCAP Subprogram

OUTPUTS Planned Actual Planned Actual Planned Actual Planned Actual

Adoption of proclamations, regulations, and directives for income and TOT

TSRP Completion of training on laws for tax administrators at regional and city administration levels

Completion of review and preparation of decentralization legal framework, functional assignments, and structures

Review for adoption of region’s decentralization strategy document

DLDP

Technical assistance for implementation of region’s woreda decentralization strategy and policy development, benchmarking and review of plans

Development and adoption of region’s urban development policy and strategy

UMCBP Development and adoption of urban land legislation and the municipal proclamation

10

Performance Agreement Matrix with Targets (FY04-05) Quarter 1 Quarter 2 Quarter 3 Quarter 4

Contributing PSCAP Subprogram

OUTPUTS Planned Actual Planned Actual Planned Actual Planned Actual

Outcome (d): Enhanced incentive environment for public servants (gender disaggregated)

Indicators for verification:

Increased average civil service salary as percentage of living wage Private-public wage comparison

Wage decompression ratios CSRP Completion of training in and

adoption of result oriented performance evaluation (ROPE) system in all regional bureaus and woredas.

DLDP

Completion of assessments for human resource and training needs for woredas; and the required office infrastructure and equipment for woredas

UMCBP Development and adaptation for implementation of personnel management manuals for local government authorities

11

Performance Agreement Matrix with Targets (FY04-05) Quarter 1 Quarter 2 Quarter 3 Quarter 4

Contributing PSCAP Subprogram

OUTPUTS Planned Actual Planned Actual Planned Actual Planned Actual

Outcome (d): Improved quality and efficiency of operations

Indicators for verification:

Improved service levels (access, responsiveness and cost efficiency) in priority sectors

Reduced unit costs and processing time for essential rural, urban, social, and legal services in priority sectors

Completion of client score cards in 75% of regional bureaus

Initiation of business process re-engineering in 75% of regional bureaus

CSRP

Completion of top management training in Strategic Planning and Management, Change Management, Performance Management, and Leadership Development for agency heads of 75% of bureaus

DLDP Review for adoption for prototype minimum service standards

Installation of court case management and case recording & transcribing systems in all regional supreme & high courts

JSRP

Installation of color coded filing system in all woreda courts

12

Performance Agreement Matrix with Targets (FY04-05) Quarter 1 Quarter 2 Quarter 3 Quarter 4

Contributing PSCAP Subprogram

OUTPUTS Planned Actual Planned Actual Planned Actual Planned Actual

Initiation of in-service training and professional development of all judges, lawyers and court clerks

Completion of technical training on network management and system administration for the Regional Date Center staff

Completion of one round of bulk generic training to all relevant regional and municipal staff

ICT

Initiate basic training (computing) for designated ICT focal persons from all woredas

Outcome (d): Improved transparency and accountability

Indicators for verification:

Reduced incidence of corruption and arbitrariness in rule enforcement (as judged by economic agents) Increased access to justice, recourse and redress

Enhanced independence of the judiciary

Increased access to government information

13

Performance Agreement Matrix with Targets (FY04-05) Quarter 1 Quarter 2 Quarter 3 Quarter 4

Contributing PSCAP Subprogram

OUTPUTS Planned Actual Planned Actual Planned Actual Planned Actual

JSRP Establishment of information counters in all regional high courts and woreda courts

TSRP Completion of 50% coverage for computerized tax payers identification number (TIN)

ICT Establishment and strengthening of Regional Data Centers

Program Support Preparation and dissemination of basic IEC materials on PSCAP

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

14

Financial management guidelines: 1. INTRODUCTION: The Public Sector Capacity Building Program, PSCAP is a large national program planned to be implemented by different government offices in different government structures. The MoFED will be responsible for the disbursement of program fund to the different beneficiaries and for the eventual gathering of financial reports, consolidating them and preparation of financial reports to the government, donors and other stakeholders. This will only be possible if uniform and agreed procedures are followed by all the concerned. Uniformity of action facilitates bottom-up consolidation of financial monitoring reports in relatively easy, accurate and speedy way, whic h in effect ensures full accountability to providers of the funds. The purpose of this manual is to provide simple and user-friendly reference material for all the people involved to help them in transactions processing from the initial identification of transactions to the final financial reporting. It discusses the detailed procedures in receiving fund (from all donors of PSCAP), keeping the fund, spending it, recording the expenditures, reporting to the appropriate body and in safeguarding the assets acquired using the fund. The basic policies of Financial Management are explained in the Operational Manual/PIP . This manual provides the procedures that will be followed to adhere to the broad policies stipulated in the PIP. In the section that follows, the background of the program, as relevant to the understanding of the manual, is explained. This is essential for the quick grasp of the nature of the program, the purpose and out put of the program especially for the people that will join the structure at a latter date. Auditors will only be involved after the start of the program. The background provided would be a tip to them to kick-off their job. Section three deals with the detail policies and procedures necessary for the management of the fund. Each and every item that will be encountered during the execution of the project are identified and explained in a clear and simple way.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

15

2. BACK GROUND

2.1. PSCAP In May 2003, the Government launched a new state transformation agenda. Specifically, the MCB announced its intention to rapidly scale up support for the six, out of the fifteen National Capacity Building Programs, core public sector reform programs as subprograms under a consolidated five-year federal program called the PSCAP. 1 The fifteen programs are Civil service reform, Justice reform, Tax reform, District-level decentralization, Urban management, Information and communication technology, Cooperatives, Private sector, Textiles and garments, Construction sector, Banking sector, Agricultural training of vocational and technical levels, Industrial training of vocational and technical levels, Higher education, Civil society. The first six are those covered under PSCAP. The objective of PSCAP Support Project for Ethiopia is to improve the scale, efficiency, and responsiveness of public service delivery at the federal, regional, and local level; to empower citizens to participate more effectively in shaping their own development; and to promote good governance and accountability. This objective will be achieved by scaling up Ethiopia's ongoing capacity building and institutional transformation efforts in the six priority areas under PSCAP.2 There are two main project components. Component 1, Federal PSCAP, supports federal level activities across each of the six subprograms including those capacity building activities for which there are scale and network economies including those activities that require national level prototyping. Component 2 , Regional PSCAP, constitutes the bulk of the Program and is designed to empower regions to adapt and implement national reform and capacity building priorities envisaged under PSCAP's six subprograms in a manner that is efficient, accountable, and sustainable. 3 The components are required to include basic program support activities to ensure effective implementation.

2.2. INSTITUTIONAL ARRANGEMENT

As mentioned above the PSCAP is a nation wide program involving different tiers of the government. The structure of PSCAP is fundamental to the financial mana gement of the program. Funds flow down the channel and reports flow up the channel.

1 Ibid 2 http://web.world ban k.org/ 3 Ibid.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

16

FEDERAL PSCAP REGIONAL PSCAP Key Fund flow Report flow

Figure 1 - PSCAP Fund and report flow chart The MCB, the MoFED, the MOR, the MFA , Federal Supreme Court, and ICTDA implement the Federal PSCAP. The BCB (BCB), the BoFED, Justice Bureau and the BoTIUD are the implementers of PSCAP at regional level. However, the financial management function will be fully carried out by BoFEDs of the respective regions. The overall coordinator of the program at national level is the MCB. The BCB in regions are the coordinators of the program in their respective regions. The MoFED (MoFED) is responsible for the overall financial management aspect of the program. It opens accounts for the program, receives funds from the donors, release funds to beneficiaries, collect reports from the beneficiaries and consolidate and report on the use of funds to donors, government and other stakeholders. At regional level, BoFED (BoFED) perform the same activity. The detail procedure is explained in the latter chapters.

IDA credit account Washington DC (Foreign currency)

Government of

Ethiopia‘s

Contr ibution

IDA special

account in USD in

Special USD account in

Ethiopia for each of the

Birr account for

PSCAP at each

Birr account for PSCAP

at each federal executing

Birr account for the

pool at MoFED

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

17

2.3. FUNDING MODALITIES Funding modalities or disbursement modalities specify how funds flow from the donors to the government and/or to the relevant public body. They also specify the way reports on the spending of the funds are submitted to the donors. The MoFED has identified three Channels or instruments for the flow of donor funds. 4 CHANNEL I – Aid and Loan funds that flow through the MoFED or BoFEDs are included here and the reporting system has to follow the same procedures. CHANNEL II – This is one of the aid disbursement channels used by bilateral donors for releasing resources to beneficiary institutions under projects financed by them. The donors provide goods and/or funds to beneficiaries usually ministries. CHANNEL III – Under this instrument, the donor directly controls all funds. The donors maintain their own bank account, pays invoices directly to contractors and/or suppliers. Channel I is the recommended funding modality for PSCAP.

4 MoF, Donor Fund Flow, Keeping, Recording and Reporting System (Amharic Version), Addis Ababa, Tir 5, 1991.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

18

3. ACCOUNTING POLICIES AND PROCEDURES In the remaining part of this manual, detailed discussion of accounting procedures is presented. The first paragraph in each section is given in a box. The text in the box is the accounting policy on the basis of which the detailed procedures are provided. The financial management provisions in the PIP are taken as financial management policies as appropriate to ensure consistency between this manual and the PIP.

3.1. BUDGET AND BUDGETARY CONTROL

Budget codes for PSCAP The budget for PSCAP shall be proclaimed under the name of MCB, MoFED , MFA, MOR, Federal Supreme Court and ICTDA. Once identified and used, the budget code for PSCAP shall remain unchanged through out the life of PSCAP. Budget calendar (as provided in the PIP) The federal lead institutions prepare their PSCAP budget and submit to the FTT) through the PPD no latter than 1st March. The regional lead institutions prepare their PSCAP budget and submit to the RTT through the RPPD no latter than 22nd February. RTT shall forward the regional PSCAP budget toFTT no latter than 1 st March. FTT shall submit the annual regional and federal plan to IDA for no objection no later then 15 th March. FTT shall submit the annual regional and federal plan to cabinet no later then 22nd March. Annual plan for PSCAP, along with the over all budget, shall be submitted to the Council of Ministers and, regional matching fund requirements in the regional budgets shall be submitted to regional council, no latter than 22nd May. The Cabinets shall recommend PSCAP budget no latter than 2nd June. Approval and adoption by federal legislature will be undertaken before 2nd July. Execution of PSCAP budget begins at the start of the fiscal year on 8 th July Mid-year reallocation of budget shall be made between regions and between the federal lead institutions based on rules set out in the PIP by the FTT on or before 1st February. MoFED issues final reallocations on or before 8th February. Supplemental budget proposals shall be finalized by the MCB on or before 8th February.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

19

a) Budget Codes

In the government accounting system, the coding system starts from budgeting. In the process of budget preparation, all the recipients of the fund from MoFED are identified with specific budget code. That code is basic to understand how much budget is allocated to a public body for the budget year. The public body is the institution that is entitled to request and receive a budget. A pubic body is an institution that has a legal mandate, receives budget directly from the concerned finance and planning body, submits its final accounts directly to the MoFED. The budget proclamation is the basic document. Transfer to the public body shall be made under the code identified in the budget proclamation and the recipient of the budget is responsible to account for the budget it has received.. Using that code, it is possible to produce a report for the transfer, expenditures and the fund balance of a recipient. Under PSCAP, the budget recipient shall be the MCB for the programs that will be implemented by it and all regional PSCAP. All expenditures incurred by the MCB and those incurred by regional BoFEDs shall be given similar code –318. However as MoFED shall make cash transfers direct to BoFEDs, for cash transfer purpose the code shall be the codes that are currently used by BoFEDs when receving cash from MoFED. This code is 154 for regions using the old single entry system: namely Afar, Somali and Gambela. All other regions and MoFED shall use 152 when recording the cash transfer. Five federal implementing agencies shall be recipients of funds for the program each of them will be implementing. These are the MFA, MoFED, MOR, Federal Supreme Court and ICTDA. PSCAP budget shall be proclaimed under the name of these five public bodies. The budget code that will appear in the budget proclamation and thence on each accounting document and report shall be the following. The budget code presented below shall remain the same through out the life of PSCAP, as change of codes from year to year shall hinder preparation of reports correctly.

BUDGET CATAGORY

CODE

Public body MCB 15/318 MFA 15/118 MoFED 15/152 MOR 15/156 ICTDA 15/325 Federal Supreme Court 15/122 Program PSCAP 08 Sub- agency Plan and Program Department 01 Federal implementing agencies other than MCB 00 Sub-program PSCAP - Tigray 01 PSCAP – Afar 02

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

20

PSCAP – Amhara 03 PSCAP – Oromia 04 PSCAP – Sumali 05 PSCAP – Benishangul gumuz 06 PSCAP – SNNPR 07 PSCAP – Gambela 08 PSCAP – Harari 09 PSCAP – Addis Ababa City 10 PSCAP – DireDawa Administration Council 11 Federal implementing agencies 00 Project Civil Service Reform 001 Justice System Reform 002 Tax System Reform 003 Urban Management Reform 004 Information & Communication Technology Reform 005 District Level Decentralization Reform 006 Expenditure Management & Control Reform 007 Program Support 008

Figure 2- PSCAP account code

A complete budget code can be written as follows: Example 1 – Budget for Civil Service Reform sub program at federal level is identified as

15/318/08/01/00/001 Example 2 – Budget for Urban Management and Reform Project in Gambella region is identified as

15/318/08/01/08/004 Example 3 – Budget for Tax system reform at federal level is identified as

15/156/08/00/00/003

Note that in the above code, only the last three fields are variable. If the implementing agency is the MCB, the sub-agency code shall be 01. If the implementing agency is any of the federal lead institutes other than MCB, the sub-agency code shall be 00 . Regions that are using single entry accounting code The budget for PSCAP shall be proclaimed as a federal project under the MCB. Hence the double entry budget coding system shall be used. However, those regions using single entry accounting cannot use the budget code because, firstly, the formats they are using are not designed to include all the information in the double entry system, secondly, the accountants may not be familiar with the double entry. New codes have to be identified so that it will be possib le to identify PSCAP expenditure by both regional and federal users.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

21

The account code under single entry accounting is organized to show three major elements: the location code, organization code and receipts and payments code. Location code has four fields, each field having two-digit code. The first field is standard, 01 for central government and 02 for regional government. The next field is also a standard two digit, which identifies regions. The third filed which has also two digits is to identify zones and the last filed having two digits is to identify woreda.

E.g.: Ministry of Agriculture in the federal government is located as 01 00 00 00.

Organization code identifies the sector (the budget institution in the sector) and the Project or report ing unit. It has three fields. The first field has three digits the sector and the supervising institution.

E.g. Ministry of Agriculture is in the Economic sector 200 and is number 11. So the code is 211 .

The second field has two digits and identifies the sub unit. The third field has also two digits identifying the sub-sub-unit.

E.g.: To complete the above example – Ministry of Agriculture Administration and General Services Section is identified by 211 01 00.

If the above budgetary institution is implementing a capital budget, another three fields shall be used to identify the project. The first field has three digits and identifies the sector. The next field has two digits and identifies program. The last field has two digits and identifies the specific project.

E.g.: If the Ministry of Agriculture has a project at Gode under a program called Irrigation Development and the sector is Natural Resource Development the code can be 721 02 02.

If the payment in the above example is for land preparation and other construction the code can be 8203. The combined code can be presented as:

01 00 00 00 - 211 01 00 - 721 02 02 - 8203 The above structure can be used to identify a unique code that all the single entry using regions can use so that the program’s expenditure can easily and effectively be identified. Since PSCAP has two components, the first two digits in the location code can be used to identify those. Federal PSCAP is 01 and regional PSCAP is 02. The next two digits are to identify regions. Under PSCAP these shall be used to identify the sub-programs, which are the regional PSCAPs. The list is as shown in the table for double entry budget codes. The zone and woreda digits will not be used.

Egg: PSCAP – Dire Dawa-Bureau of Urban & Works (BoTIUD) is identified as 02 11 00 00 .

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

22

The Public Body or the supervising institution in whose name the budget is proclaimed is the MCB. The Plan and Program Department of MCB is the sub units responsible for PSCAP. Sub-sub-units codes will not be used. Hence the second three fields can be written as 318 01 00. The third group is to identify a capital project code. PSCAP is a capital project. The sector code cannot be used. The program code can be identified as 08. The project code under double entry accounting has three digits. Under single entry the first digit shall be dropped and the last two digits shall be used as follows: Project Civil Service Reform 01 Justice System Reform 02 Tax System Reform 03 Urban Management and Reform 04 Information & Communication Technology Reform 05 District Level Decentralization Reform 06 Expenditure Management & Control Reform 07 Program Support 08

The last group of code is the receipts and payments code. This code is more or less the same as the code under the double entry. The codes relevant for PSCAP are identified in the next section. The combined code for PSCAP under single entry can be written as follows. Take for example, the Dire Dawa- PSCAP has paid for land preparation and other cons truction the code being 8203. Assume the payment is made under Urban Management and Reform sub program.

02 11 00 00 - 318 01 00 - 000 08 04 - 8203 The formats that shall be used under single entry shall be filled with the above codes. It will therefore be possible to identify transactions by source and it is also possible to summarize transactions as needed. Additional information box shall be added on the existing Ge/He/29/4, the Trial Balance, Ge/He/29/5, Monthly Transfer Summary and Ge/He/29/3, Capital Expenditure summary. The heading of, for example, the Ge/He/29/4 can be presented as follows.

This is on the reports this will be added

Reporting unit Code Central government/ region Zone Woreda Unit Sub-unit Sub-sub-unit

Supervising unit Code Name of Public Body Name of Program Name of Sub-agency Name of Sub-program Name of Project Source of finance Bank account No

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

23

All the remaining details shall remain the same as in the existing Ge/He/29/xx. The above will enable the processing of accounts by CAD in an effective way. In addition, the regions that are not yet implementing the accounting reform shall start familiarizing themselves to the requirements of the double entry accounting. Codes to be used for cash and non-cash transfers As mentioned above, implementing agencies shall get transfer from MoFED. Hence, even if the budget is proclaimed in the name of MCB and that the expenditure code for regional PSCAP shall be 318, the cash transfer code will be different. The MoFED code as sender of the mone y and the BoFED code as recipient of the money shall be used. This is not a new requirement but the one that is being used currently. To illustrate: Example 1: MoFED transferred Birr 1 million to Tigray BoFED

• MoFED shall record the transaction as follows:

Account code Debit Credit 01/000/00/152/01/001 4015 1,000,000

15/000/00/152/00/22 4115 1,000,000

• Tigray BoFED shall record the transaction as follows:

Account code Debit Credit 01/000/00/152/01/001 4103 1,000,000

15/000/00/152/00/22 4015 1,000,000 Example 1: MoFED transferred Birr 1 million to Somali BoFED

• Somali BoFED shall record the transaction on Ge/He 23 as follows:

Account code Received 15/000/00/154/00/22 4015 1,000,000

• MoFED shall record the transaction as follows:

Account code Debit Credit 05/000/00/152/01/001 4015 1,000,000

15/000/00/152/00/22 4115 1,000,000 Note: that 4015 represents transfer and 4115 represents cash at bank accounts.

b) Budget preparation and control The budget preparation at the implementing agency level starts before March 1st of the year. The budget is the annual fiscal plan (annualised drawing rights) in monitory terms. The procedure for the preparation, Appraisal Adoption, Execution, and Re-allocation of budget is provided in the PIP. The relevant section of the PIP (section IV – Resource allocation and Management) is attached at the end of this manual as Annex XXXIX.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

24

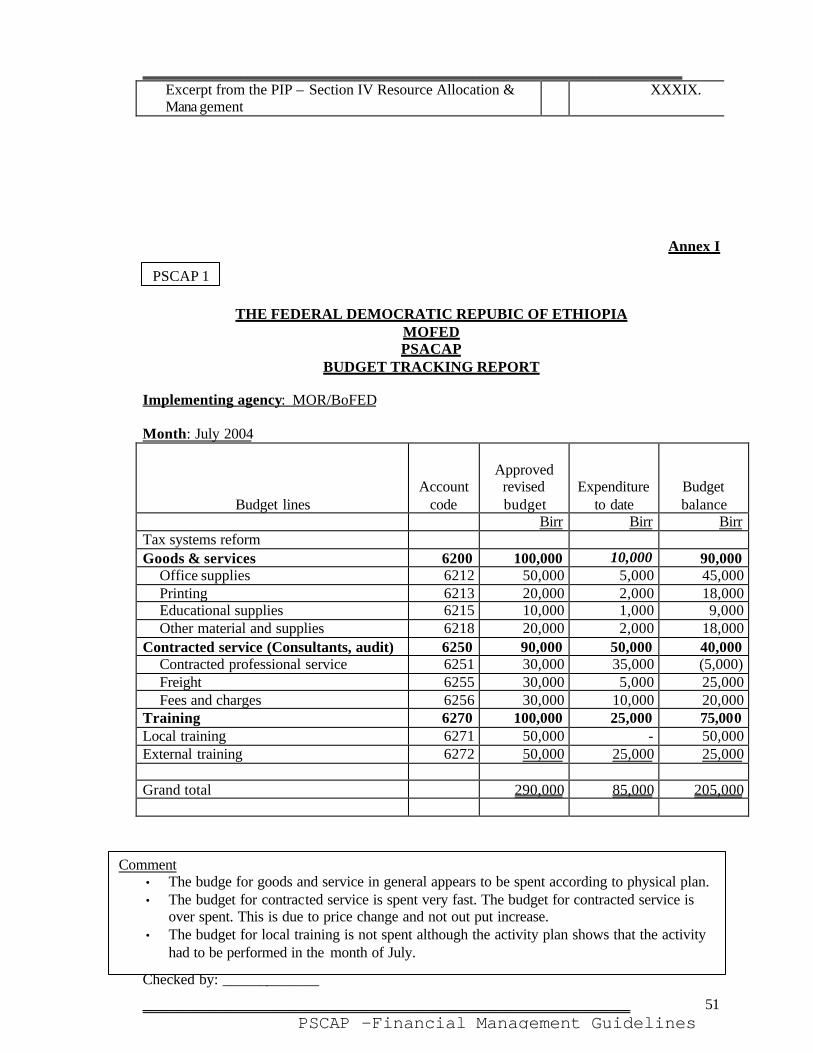

It is very important that the accountants responsible for keeping the records of PSCAP and the budget section representatives in the implementing agencies are fully participated in the budget preparation process so that they can fully understand the budget and they will not be in problem when they perform the control function. The account codes that will be recommended in subsequent sections shall be used for the detailed budget purpose. Expenditure codes shall be assigned to each item in the budget based on the chart of account and that code must be used in keeping the accounting records to ensure comparison of budget with actual spending. The budget ledger card, as described in the following section, shall be used in the budget control exercise. The detail procedure is described in that section. The budget section shall prepare monthly budget tracking report. Preparation of this report is not a difficult task if the budget ledger is kept up-to-date at all time. The budget section shall extract the approved revised budget for each item of expenditure from the budget ledger card. Expenditure to date is also extracted from the same ledger and put in the budget tracking report. Comparison is made between the two and a third column showing the budget balance. The budget balance shall be normal, under spent or over spent. The budget section shall give comments on the budget balance in bullet points to give warnings to the budget users. The accountant shall agree the report by signing on the face of it. The report shall then be circulated to the procurement officer, the section that follows up the program and the head of the implementing agency on the basis of which they can take appropriate corrective action. In regions, BoFED is responsible for the financial management function. The preparation of budget tracking report is therefore the responsibility of BoFEDs. The circulation of the report will be to the above-identified three officers of the implementing agencies. Sample budget tracking report is given in annex I.

3.2. CHART OF ACCOUNT The FGE accounting system provides the FGE Chart of Accounts which is a system of coding government uses to identify and classify financial entities and events.5

5 The Civil Service Reform Account Design Team of MoFED with the support of the Decentralisation Support Activity (DSA) Project, Manual 3 FGE Accounting System, Volume II, FGE Chart of Accounts, Version 1.0, January, 2002.

The Federal Government of Ethiopia’s (FGE) financial management system shall be used in the overall management of the Program. A supplemental chart of account is provided. The purpose of the supplemental chart of account is to enable MOFED to capture and classify the funds received from donors by subprograms. The intent is to enable project costs to be directly related to specific work activities and outputs under PSCAP and to enable MOFED to monitor funds utilization across subprograms and to serve as one of the source of information for assessing performance by relevant entities.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

25

Under PSCAP, the final financial report that will be produced is the Statement of Cash Receipts and Payments. The Chart of Account that is recommended in this manual is sufficient to capture transactions in a way that enables the preparation of this statement. The account codes shall enable the preparation of the detailed budget, accounting for the transfers from donors and transfers to beneficiaries (receipt from MoFED), capturing the transactions that will occur, and preparation of periodic financial reports and the year-end financial statement. The Chart of Account is developed based on the accounts classification and coding system used in the FGE Accounting system for Modified Cash Basis transactions. The equivalent codes for those agencies that are using single entry bookkeeping is also provided. Under the Modified Cash Basis of accounting, the following accounts shall be used. CAD shall officially issue the final codes .

PSCAP

TRIAL BALANCE

MoFED Implementing

agencies Account

code Debit Credit Debit Credit

Cash on hand 4101 XXX XXX Cash at Bank – Foreign Currency -IDA 4102 XXX Cash at Bank – Foreign Currency – XXX 4102 XXX Cash at Bank – Foreign Currency - XXX 4102 XXX Cash at Bank – Pooled Birr Account 4115 XXX Cash at Bank – Implementing agencies 4103 XXX Cash shortage & overage 4202 XXX XXX Other advance within government 4210 XXX XXX Advance to consultants 4252 XXX Adva nce to suppliers 4253 XXX Due to MoFED 5027 XXX XXX Other payables within government 5028 XXX XXX Transfers - cash 4015 XXX XXX Transfers –non cash 4050 XXX XXX Net asset equity 5601 XXX XXX Revenue - External assistance 2000-2999 XXX Revenue - External loan 3000-3999 XXX Expenditure 6000-6999 XXX _____ XXX _____ XXX XXX XXX XXX

NB: The specific codes for revenue, both assistance and loan, is given in the budget proclamation which will be available soon. Those codes shall be used by MoFED to open ledger accounts and record the income. For example, external loan from IDA is given a code number “3014”. The chart of account shall be expanded as and when the new donors or lenders are identified.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

26

Under the single entry booking, the following accounts shall be used:

PSCAP TRIAL BALANCE

MoFED Implementing

agencies Account code Account code Cash 4005 4005 Cash at bank 4115 4006 Staff debtors 4101 4101 Cash shortage 4201 4201 Custom deposit 5300 5300 Other paya ble 5400 5400 Transfers – capital 4015 4015 Other cash transfers 4020 4020 Expenditure 8000-8999 8000-8999

The definition and purpose of the above accounts is as provided in the FGE Accounting System. The definition serves for both the single entry using entities and the double entry using entities. Cash: - Under PSCAP, MoFED shall maintain one special account each for the donors. A pooled

local currency account shall be opened wherein transfer from the special accounts and from the treasury (the government contribution) shall be kept. Each of the implementing agencies at federal level and BoFEDs at regional level will have Birr accounts, type “A” which will not be closed at the end of the budget year, opened for PSCAP purpose to receive transfers from MoFED. BoFEDs shall have only one bank account although the fund they are going to handle is for all implementing agencies in the region. In addition each federal beneficiary and BoFEDs will have cash on hand account to handle petty cash. The definition for cash therefore embraces all this accounts.

Receivables: - Included in this category are cash shortage, advances, prepayments and other

receivables. Advances include prepayments to consultants and suppliers. Other receivable is to account for other kinds of advance that will not fall in the other categories.

Payables: - Payables under PSCAP are expected to be short term. Only two accounts are

suggested in the double entry, Due to MoFED and other payables within government. Similar purpose payables shall be identified in the single entry.

Transfers: - This account is not a permanent account and is closed at the end of every year.

During the year it will be used to record monthly transfer of money to implementing agencies at Federal level and the BoFED at region level. The implementing agencies and BoFED shall debit their respective bank account for PSCAP and credit the transfer account. The transfer in the single entry has the same purpose.

The rule is that the total debit in the transfer account of MoFED shall equal the total of credits in all implementing agencies. In effect at the time of consolidation, the transfer account will have a balance of ZERO. The same rule applies for the single entry although the debits and credits are not there.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

27

The accounting for non-cash transfers will be the same as above except that the implementing agency shall debited the appropriate expense account instead of the bank account.

Revenue : - Only MoFED shall use this account, as the distinction of revenue by source (donor)

in all the implementing agencies is irrelevant and impossible because transfer to the agencies will be made from one pooled Birr account.

There are three categories of revenue under PSCAP: the transfer from central treasury being the Government’s contribution shall be kept in the first revenue account. Income from IDA will be a credit and is categorized as external loan. A separate account shall be maintained for it. Income from other donors can be either external loan or external assistance. Separate account for each of the donor shall be kept according to the nature of the transfer, i.e., either loan or assistance.

Expenditures: - The major and most important section of the Chart of Account is this

section. Most of the expenditure types can be captured by the expenditure account codes being used in the accounting system at present. The expenditure codes have sufficient detail accounts and control accounts as well such that there is no need at all to create new codes.

The expenditure codes have also control account and subsidiary account code system. Fore example 6200 is the general category for Goods and Services and accounts from 6210 to 6224 are the subsidiary ledgers. The control account shall be used to provide summary report by category for the donors’ purpose.

Matching of the single entry code with the double entry code is very important and it is done like shown in the following table. As mentioned earlier PSCAP is a capital budget program. The capital budget expenditures under the single entry are in the 8000 group. It is also possible to establish major categories for donor reporting purpose so that the system can directly produce the donor report. Using the IDA’s category, the chart of account can be designed as follows.

Account title

Donor Category

Double entry

Single entry

Control account Goods and Services Goods 6200 Subsidiary accounts Office supplies 6212 8303 Printing 6213 8303 Food 6216 8303 Fuel and lubricants 6217 8303 Other material & supplies 6218 8303 Miscellaneous equipment 6219 8303 Research & development supplies 6223 8303 Control account Fixed assets Goods 6310 Subsidiary accounts Purchase of equipment 6313 8204 Purchase of building s, furnishings & fixture 6314 8206 Control account

Contracted services

CONSULTANT

SERVICES

6250

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

28

Subsidiary accounts Contracted professional services 6251 8101 Control account

Personnel service

CONSULTANT

SERVICES

6100

Salaries to permanent staff 6111 8301 Wages to contract staff 6113 8302 Wages to external contract staff 6115 8302 Allowance to permanent staff 6121 8301 Allowances to contract staff 6123 8302 Allowance to external contract 6124 8301 Government contribution to permanent staff pension 6131 8301 Control account

Contracted services

Operating costs

6230

Rent 6252 8303 Advertising 6253 8303 Insurance 6254 8303 Fees and charges 6256 8304 Electricity charges 6257 8303 Telecommunication charges 6258 8303 Water & other utilitie s 6259 8303 Control account Travelling & official entertainment service Operating

costs 6230

Subsidiary accounts Perdiem 6231 8501 Transport fees 6232 8501 Official entertainment 6233 8303 Control account Training Training 6270 Subsidiary accounts Local training 6271 8501 External training 6272 8501 Training related Perdiem 6273 8501

Training related transport fee 6274 8501 Control account

Personnel service

Operating costs

6100

Subsidiary accounts Wages to causal staff 6114 8302 Control account

MAINTENANCE & REPAIR

Operating costs

6240

Subsidiary accounts Maintenance & repair of vehicle 6241 8303 Maintenance & repair of equipment 6243 8303 Maintenance & repair of building, furnishings & fixtures 6244 8303

Figure 3- PSCAP expenditure code

The PSCAP expenditures are not fully known at this stage. The above codes and accounts categories are drawn using the information at hand at the time of writing this guide. It will be mandatory to revise the chart of accounts once the expenditure items are clearer. The responsibility to establish new codes as the need arises shall be of CAD. The new codes shall be identified, organized and communicated in writing to all implementing agencies. The chart of account discussed above is attached as an annex at the end of this manual in a summarized and detachable format. Refer annex XXXVIII.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

29

3.3. ACOUNTING CYCLE The accounting cycle for PSCAP is not different from the government accounting cycle. It starts when money is received in the special accounts and ends when report of expenditures is presented to the CAD and CAD is closing the accounts. In the sections that follow we shall see the accounting process.

3.3.1. RECEIPT OF MONEY

There are two concerned units of the MoFED that are relevant in the management of the PSCAP. These are the Counterpart fund unit (CFU) in the Treasury Department and the Central Accounts Department (CAD). The CFU is the one authorized to open special bank accounts for programs. It will be requested to open the special accounts mentioned above. The initial deposits to the special accounts will be the advance payments from each donor as agreed in the respective agreements signed with the donors. Subsequent deposits shall be based on Statement Of Expenditure (SOE) that will be presented to the donor. After a certain initial period, the Financial Monitoring Report (FMR) shall replace the SOE. These two reports are discussed further in subsequent sections. The CAD shall be responsible for the accounting function, i.e., to record the receipt transaction, to prepare donor reports and annual financial statements for reporting to donors and for the annual audit. The PSCAP program shall receive money from the two major sources, from donors and from the government. The receipt transaction shall be recorded when bank advice is received from the bank. The accounting entry to record the transfers shall be as follows. Note that only MoFED shall receive money from donors. Hence the entries are relevant for CAD only. 1. If receipt of money is from IDA

Debit Credit Cash at Bank – Foreign currency IDA XXX

Revenue –External credit – IDA XXX 2. If receipt of money is other donors as assistance

Foreign exchange (FOREX) account shall be opened to each donor with the national bank of Ethiopia by the Treasury Department of the MoFED. One of the accounts shall be the IDA special account. The others shall be used to keep funds received from other donors. One pooled Birr account shall be opened to keep transfers from the special accounts and from central treasury being government’s contribution to the program. Transfers to the pooled Birr account shall be made monthly based on the approved annual plan.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

30

Debit Credit Cash at Bank – Foreign currency (donor name) XXX

Revenue –External Assistance - IDA XXX 3. If receipt of money is treasury

Debit Credit Cash at Bank – Pooled Birr account XXX

Transfer XXX Transfer shall be made from the special accounts to the pooled Birr account whenever the pool account balance is low. The follow up of the bank account balance, like the special account balances, shall be made by CFU. The entry to record the transfer shall be: 4. Transfer from special accounts to the pooled Birr account. Assume that transfer is from IDA

account Debit Credit Cash at Bank – Pooled Birr account XXX

Cash at Bank – Foreign currency IDA XXX

3.3.2. TRANSFER OF FUND TO BENEFICIERIES

All institutions receiving PSCAP fund from the PSCAP Pooled Birr account shall open bank accounts of type “A”. This type of account is more appropriate for the nature of PSCAP of all the account types identified in Guideline No 16/2004, Guideline to Open and Administer Government Bank Account, of MoFED. Transfer of fund to federal implementing agencies and BoFED shall be made by the MoFED, upon receiving instruction from the MCB who is the responsible agency for the overall program. BoFEDs shall not transfer funds to regional implementing agencies. Rather, the BoFEDs will handle the fund and effect all payments related with PSCAP upon request from the implementing agencies.

MoFED Treasury department shall make transfer from the pooled account to the federal beneficiaries and BoFED quarterly after the implementing agencies submit Disbursement Request approved and cleared by MCB and accompanied by Quarterly Report. The amount to be transferred to a beneficiary is calculated as the next quarter budget less procurement to be made centrally less any unused money from the previous quarter. Transfer to the beneficiaries and BoFED shall be made on the 12th day of the quarter. Each federal beneficiary shall open a separate Birr account for PSCAP and transfer from MoFED shall be to the PSCAP account. At region level, BoFED shall open a separate Birr account for PSCAP in which transfer from MoFED shall be deposited. The bank account shall be the only PSCAP account in the region. Transfer account shall be used to record transfer to the beneficiaries and transfer from MoFED. Cash receipt Voucher shall be used to recognize cash transfers received. The equivalent document for regions that are using single entry is Ge/He/21/1.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

31

BoFED shall be responsible to prepare the monthly reports and present to the MoFED. The first transfer from the pooled account to the federal beneficiaries and BoFEDs’ PSACAP account shall be made on the basis of the first quarter budget that shall be prepared with reference to the approved first year budget. Each beneficiary shall fill the Disbursement Request (see annex II) immediately after receiving its approved budget. Subsequent transfers shall be made on the basis of subsequent Disbursement Requests and quarterly reports. Disbursement Requests shall be identified by the name of the beneficiary and the request number referring to the quarter number for which request is made (the first advance shall be for the 1st quarter). Quarterly reports shall be in the form prescribed in annex III. This report shows the expenditures paid in the quarter on the approved budget lines. It shall also show the budget for next quarter. The amount to be requested for transfer is the budget for the next quarter less any procurement included in the beneficiary’s budget but that will be made centrally (using foreign exchange etc) less the balance of cash on hand and at bank at the end of the quarter. E.g.: If the budget for Quarter II is Birr 100,000, the budget includes Birr 50,000 for goods that

will be paid centrally and the cash on hand and at bank at the end of the quarter is Birr 10,000, and then the amount of transfer requested should equal Birr 40,000.

Disbursement requests from federal beneficiaries shall be forwarded to the MCB for approval. The approved request shall be submitted to the MoFED, CFU. The CFU shall collect quarterly disbursement requests from both federal beneficiaries and regional BoFED and request the Treasury Department to make the transfer to the beneficiaries. Disbursement request from BoFED shall be submitted to BCB, which will approve and forward it to MCB. After checking and approving, the MCB shall advice the MoFED to make transfer to the BoFED. MoFED shall receive final disbursement requests and quarterly reports from federal beneficiaries through MCB on the 10th day of the following quarter. MoFED shall transfer funds on the 12th day of the next quarter (within two working days after it received the approved request). For this to happen, the federal beneficiaries shall submit the Disbursement Request to the MCB on the 6 th day following the end of the quarter. BoFED shall forward its request to BCB’s approval on the 6th day. On the 8 th day, the BCB shall approve the request and forward it to the MCB. The MCB shall forward the approved Disbursement request on the 10th day. The deadlines are very tight that quarterly reports and requests could not be send physically. Reports and requests should therefore be submitted by fax whenever possible and the originals can follow latter for file. Two accounting entries shall be made at this point, one by the CAD and the second by the beneficiary receiving the transfer. The CAD will receive bank debit advice for the transfer. Upon receiving it will,

Debit Credit Transfer account XXX

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

32

Cash at Bank – Pooled Birr account XXX The beneficiaries shall receive bank credit advice when their bank deposits the money in their account. They will write cash receipt and pass the following entry:

Debit Credit Cash at Bank – Pooled Birr account XXX

Transfer account XXX The beneficiary shall use Cash Receipt Voucher as recommended in the FGE acc ounting system (see annex IV). According to the FGE accounting system Cash Receipt Voucher shall be used for all sorts of receipts. Cash may be received in notes and coins, in check, bank transfer or direct deposit in the bank account. Hence all transfers from MoFED to federal beneficiaries and to regional BoFED, and from BoFED shall be captured via Cash Receipt Vouchers. The budget and account code shall be written on the face of the cash receipts as follows: Example – The Amhara region BoFED received Birr 1,000,000 from the MoFED to cover expenditures of all PSCAP projects implemented in the region.

Budget category Account code Birr Debit Credit 152/08/01/03/000 4103 1,000,000 00 152/08/01/03/000 4015 1,000,000 00

The regions that are using the single entry accounting will use Ge/He/21/1, which has the same function as the cash receipt under the double entry accounting. Obviously they will not make journal entries as shown above. However they will record the transfer using the account number 4015 (remember that PSCAP is a Capital project). The above transaction can be recorded as:

Revenue Item Purpose of payment Birr

4015 Transfer for PSCAP program 1,000,000 00 Bank charges to transfer money to regions shall be born by MoFED. This is important to reconcile the transfer account maintained by MoFED with the transfer accounts maintained by beneficiaries and BoFED.

3.3.3. DISBURSMENTS Disbursement can be made in the form of cash (notes & coins), bank check or bank transfer.

The general policy is that disbursement shall be made for goods and services acquired or to be acquired, if there is firm commitment.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

33

3.3.3.1.CHECK PAYMENTS & BANK TRANSFERS

As much as possible, all payments shall be made by check. Only small payments, the limit/demarcation being the one existing in each of the implementing agencies, shall be made in cash. Bank transfers shall be used to make payments to people in different places from the location of the implementing agency. The Bank Payment voucher that is being used in the FGE accounting system shall be used (see annex V). The payment voucher has all the necessary details to identify the payment and all the details have to be filled in. The account code is filled in the payment voucher as shown in the following examples: Examples

1. Payment of Birr 250,000 is made to MOENCO for the purchase of vehicle by Amahara region Bureau of Urban & Works for UMRP. The region’s BoFED makes payment.

Budget category Account code Birr

Debit Credit 15/318/08/01/03/004 6311 250,000 00 15/152/08/01/03/000 4103 250,000 00

Those regional BoFEDs that are using the single entry accounting shall continue using model 6 until they go through the accounting reform. There is a space to write the expenditure code/budget code and the account code on the payment voucher. Example

2. Payment of Birr 270,000 is made to MOENCO for the purchase of vehicle by Sumali region BCB for ICTD. The region’s BoFED makes payment.

All check payments and bank transfers shall be made via a payment voucher and shall be duly authorized by the responsible officer. Regions that are using single entry will use Model 6. The approval procedure and the authorization limits to approve check payments shall be the procedures existing in each implementing agency. In Regions, the implementing agency shall complete the approval process and present the payment documents for BoFED to effect the payment. Payments by bank transfer shall be made for payees who are in a distant place.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

34

Budget code shall be 02150000 -3180100-0000805 Account code shall be 8205

Each implementing agency shall use the existing procedures for payment process. This includes the decision as to who will sign checks and the threshold for approval of any one payment. In the regions, the implementing agencies are not check signatories. BoFEDs shall make the payment based on the request of the implementing agencies. All documentations and approval process shall be completed in each of the implementing agency, and on the basis of such document, BoFED will effect the payment. The list of signatories shall be provided to the bank where the PSCAP account is maintained.

3.3.3.2. CASH PAYMENTS The purpose of keeping this fund is to meet small payments for which writing of check is not recommended. The fund shall be replenished whenever the amount of cash in safe is believed to be small. A bank check in the name of the cashier shall be prepared for replenishment. The Cashier shall keep the fund. There should be cash safe and the Cash office should be strong enough. Payment of cash out of the fund shall be made via the Cash Payment Voucher (see annex VI). As in the check payments, the existing procedure for cash payment in each of the implementing agency shall be used. The cashier shall maintain a follow up book, Petty Cash Book given in the FGE accounting system, to track the balance of cash on hand (annex VII). What goes to the debit column is the amount of check to replenish the fund. On the payment column of the book, payment vouchers shall be recorded. Temporary advances, suspense, can be paid out of the petty cash fund. Suspense Payment Voucher given in the FGE accounting system (annex VIII) shall be used to process the suspense transaction. The voucher shall not be recorded in both the petty cash book and the Transaction Register. Under single entry accounting system, Model 6 (annex IX) is used for both check and cash payments. Model 6 is also used to make temporary advances such as travel advances and salary advances. When used as suspense vouchers, Model 6 is prepared in one copy only. When the advance is settled, the single voucher shall be cancelled and returned to the one settling the advance. The actual expense shall then be recorded following the normal procedure.

An imprest petty cash fund shall be established with each implementing agency at federal level and with each BoFED. The Cashier shall keep the fund in a safe. All small payments shall be paid out of petty cash. Every payment has to be duly approved. Suspense payments can be made form the petty cash account.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

35

Both the cash and check payment transactions shall be prepared for posting to the transaction register when double entry, or to Ge/He/23 (annex X) when single entry. The preparation for posting is the coding of the payment vouchers. The accountant shall write the appropriate accounting code on the face of the voucher as shown earlier. In regions, BoFED shall keep one petty cash fund for PSCAP purpose. Payments shall be made based on the request of implementing agencies just like for Check Payments.

3.3.4. JOURNAL VOUCHERS

Not all transactions involve payment of cash or receipt of cash. The purpose of the Journal Voucher is to capture such non-cash transactions. Other common Journal Entries are correction of errors. For example, a payment might have been debited to a wrong expenditure account and need correction. The correction shall be made via Journal Voucher. The Journal Voucher in the FGE Accounting System shall be used for PSCAP purpose (annex XI). It shall be prepared in two copies. The first copy is the accounts copy and the second copy is pad copy. The Head of Budget and Accounts must approve all Journal Vouchers after the accountant prepares it. The accountant then posts it to the transactions register. The following examples illustrate the way the Journal voucher is prepared.

Example 1 – The MoFED purchased ICT equipment for Oromia region PSCAP from Blue Nile Trading. The cost of the equipment is Birr 265,000. Oromia region BoFED will record the transaction as follows:

Description Budget Category Account Code Debit Credit Equipment 318/08/01/04/005 6313 265,000 00 Transfer 318/08/01/04/000 4050 265,000 00

Example 2 – In SNNPR’s JSRP, Birr 100,000 paid for external training was wrongly charged to local training. The correcting entry would be:

Description Budget Category Account Code Debit Credit External training 318/08/01/07/002 6272 265,000 00 Local training 318/08/01/07/002 6271 265,000 00

Under single entry accounting, there is no document equivalent to the Journal Voucher that exists under double entry accounting. But Model 64B (Annex XII) is used to account for non-cash transfers from the MoFED to implementing agencies and from one implementing agency

Journal Vouchers shall be used to capture transactions that do not result in payment or receipt of cash. The Head of the Budget and Accounts shall approve all Journal Vouchers.

________________________________________________________________________

_________________________________________________________________ PSCAP –Financial Management Guidelines

36

to the other, The implementing agency, when receiving Model 64B from MoFED shall treat it as if it has received money from MoFED and immediately transfer the back to MoFED. To illustrate the treatment of Model 64B, assume that MoFED paid for consultancy who provided service in Gambela region. The payment was Birr 100,000. MoFED shall write a letter to the region that it has paid for the service. The region shall record the following on Model 64. two entries shall be recorded. The first is to record the transfer as if it is a cash transfer.

Account code Receipts Payments 08/000/00/154/01/001 4012 100,000

The second is recording of the payment under the appropriate expense code;

Account code Receipts Payments 08/000/00/318/01/001 8101 100,000