Profiting From Broadband - bbpmag.com · Profiting From Broadband ... revenue side of the equation...

6

80 | BROADBAND COMMUNITIES | www.broadbandcommunities.com | JULY 2013 SUMMIT COVERAGE Profiting From Broadband At the 2013 Broadband Communities Summit in April, many presenters tackled the subject of making broadband a financially sustainable proposition. Here, three of the magazine’s regular contributors recap their own Summit presentations and panels. T oday’s high cost of borrowing for FTTH builds scares many potential rural deployers. However, a look at the revenue side of the equation may change their thinking. You can build and profitably operate a fiber network with as few as eight customers a mile even if lenders charge 10 percent interest on the money you need to build the system. is is not mainly a matter of cost cutting. Although economies and logistical tricks can cut the need for up-front cash by 10 percent to 20 percent, the real path to first-mile fiber is not on the cost side. It is in realizing revenue potential. Verizon has figured it out. With an average monthly revenue per customer (ARPU) of more than $150 (and rising – it was $143 a year ago), Verizon enjoys a gross profit before overhead and marketing costs of at least $50 per customer per month. A rural deployer can play in the same league even if it cannot afford the upfront cost of developing and marketing hundreds of customer services and even if its marketing staff can fit into a single room or even sit at a single desk. Fully loading the loan payments, overhead, and marketing and operating costs (not including video content) for fiber to the home adds costs of $10 to $50 per month per subscriber. Potential deployers think of that in a negative way – it eats up most of the extra profit from offering new, high-margin services. But of course the reverse is true: e margin on these services is what allows the investment in the first place. Raising money still isn’t easy, in large part because Wall Street sees a quicker return on money spent expanding wireless capacity. us, investors penalize investment in fiber and in other landline broadband technologies such as DSL and DOCSIS not because they are particularly bad bets but because wireless appears to be a better bet in the short term. In reality, revenue opportunities abound, even for providers serving just a few thousand premises with fiber. e revenue potential is high enough that even municipal systems can keep their low-price promise on basic services – broadband, voice and linear video – while offering profitable custom services, each of which is used by a small percentage of customers. ese are services that larger national providers cannot or will not offer in small markets. ese are also services that spur local economic growth. RETHINKING REVENUE Let’s look at some of the revenue opportunities. As Figure 2 shows, getting close to $200 a month ARPU, on average, with close to an $80 monthly profit is at least conceivable. at’s far more than is needed. However, some of that income will soon disappear, and some of the revenue produces little for the bottom line. Eight Customers Per Mile! By Steven S. Ross / Broadband Communities

Transcript of Profiting From Broadband - bbpmag.com · Profiting From Broadband ... revenue side of the equation...

80 | BROADBAND COMMUNITIES | www.broadbandcommunities.com | July 2013

SUMMIT COVERAGE

Profiting From Broadband At the 2013 Broadband Communities Summit in April, many presenters tackled the subject of making broadband a financially sustainable proposition. Here, three of the magazine’s regular contributors recap their own Summit presentations and panels.

Today’s high cost of borrowing for FTTH builds scares many potential rural deployers. However, a look at the

revenue side of the equation may change their thinking.

You can build and profitably operate a fiber network with as few as eight customers a mile even if lenders charge 10 percent interest on the money you need to build the system. This is not mainly a matter of cost cutting. Although economies and logistical tricks can cut the need for up-front cash by 10 percent to 20 percent, the real path to first-mile fiber is not on the cost side. It is in realizing revenue potential.

Verizon has figured it out. With an average monthly revenue per customer (ARPU) of more than $150 (and rising – it was $143 a year ago), Verizon enjoys a gross profit before overhead and marketing costs of at least $50 per customer per month.

A rural deployer can play in the same league even if it cannot afford the upfront cost of developing and marketing hundreds of customer services and even if its marketing staff can fit into a single room or even sit at a single desk.

Fully loading the loan payments, overhead, and marketing and operating costs (not including video content) for fiber to the home adds costs of $10 to $50 per month per subscriber. Potential deployers think of that in a negative way – it eats up most of the extra profit from offering new, high-margin services. But of

course the reverse is true: The margin on these services is what allows the investment in the first place.

Raising money still isn’t easy, in large part because Wall Street sees a quicker return on money spent expanding wireless capacity. Thus, investors penalize investment in fiber and in other landline broadband technologies such as DSL and DOCSIS not because they are particularly bad bets but because wireless appears to be a better bet in the short term.

In reality, revenue opportunities abound, even for providers serving just a few thousand premises with fiber. The revenue potential is high enough that even municipal systems can keep their low-price promise on basic services – broadband, voice and linear video – while offering profitable custom services, each of which is used by a small percentage of customers. These are services that larger national providers cannot or will not offer in small markets. These are also services that spur local economic growth.

RETHINKING REVENUELet’s look at some of the revenue opportunities. As Figure 2 shows, getting close to $200 a month ARPU, on average, with close to an $80 monthly profit is at least conceivable. That’s far more than is needed. However, some of that income will soon disappear, and some of the revenue produces little for the bottom line.

Eight Customers Per Mile!By Steven S. Ross / Broadband Communities

July 2013 | www.broadbandcommunities.com | BROADBAND COMMUNITIES | 81

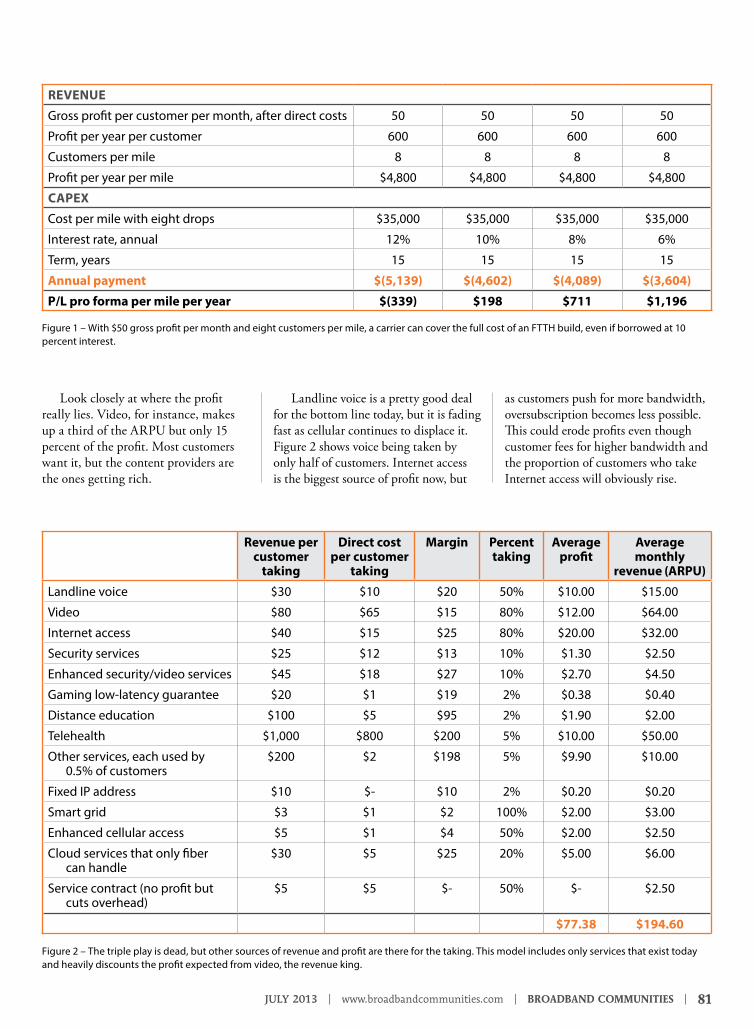

Look closely at where the profit really lies. Video, for instance, makes up a third of the ARPU but only 15 percent of the profit. Most customers want it, but the content providers are the ones getting rich.

Landline voice is a pretty good deal for the bottom line today, but it is fading fast as cellular continues to displace it. Figure 2 shows voice being taken by only half of customers. Internet access is the biggest source of profit now, but

as customers push for more bandwidth, oversubscription becomes less possible. This could erode profits even though customer fees for higher bandwidth and the proportion of customers who take Internet access will obviously rise.

Revenue per customer

taking

Direct cost per customer

taking

Margin Percent taking

Average profit

Average monthly

revenue (ARPU)

Landline voice $30 $10 $20 50% $10.00 $15.00

Video $80 $65 $15 80% $12.00 $64.00

Internet access $40 $15 $25 80% $20.00 $32.00

Security services $25 $12 $13 10% $1.30 $2.50

Enhanced security/video services $45 $18 $27 10% $2.70 $4.50

Gaming low-latency guarantee $20 $1 $19 2% $0.38 $0.40

Distance education $100 $5 $95 2% $1.90 $2.00

Telehealth $1,000 $800 $200 5% $10.00 $50.00

Other services, each used by 0.5% of customers

$200 $2 $198 5% $9.90 $10.00

Fixed IP address $10 $- $10 2% $0.20 $0.20

Smart grid $3 $1 $2 100% $2.00 $3.00

Enhanced cellular access $5 $1 $4 50% $2.00 $2.50

Cloud services that only fiber can handle

$30 $5 $25 20% $5.00 $6.00

Service contract (no profit but cuts overhead)

$5 $5 $- 50% $- $2.50

$77.38 $194.60

RevenUe

Gross profit per customer per month, after direct costs 50 50 50 50

Profit per year per customer 600 600 600 600

Customers per mile 8 8 8 8

Profit per year per mile $4,800 $4,800 $4,800 $4,800

CAPex

Cost per mile with eight drops $35,000 $35,000 $35,000 $35,000

Interest rate, annual 12% 10% 8% 6%

Term, years 15 15 15 15

Annual payment $(5,139) $(4,602) $(4,089) $(3,604)

P/L pro forma per mile per year $(339) $198 $711 $1,196

Figure 1 – With $50 gross profit per month and eight customers per mile, a carrier can cover the full cost of an FTTH build, even if borrowed at 10 percent interest.

Figure 2 – The triple play is dead, but other sources of revenue and profit are there for the taking. This model includes only services that exist today and heavily discounts the profit expected from video, the revenue king.

82 | BROADBAND COMMUNITIES | www.broadbandcommunities.com | July 2013

SUMMIT COVERAGE

This is exactly what spooks investors.

But are they considering telehealth? Depending on what services a carrier offers, this alone could yield $100 to $1,000 a month per customer. At the low end is two-way videoconferencing with health professionals and maybe a little bit of monitoring for emergency use. There is much greater potential when a customer’s home is equipped well enough to allow aging in place. State Medicaid plans, for instance, pay between $6,000 and $12,000 a month for nursing home care. Delay the need for even six months, and Medicaid saves $36,000 to $72,000. There are few Medicaid- or disabled Medicare-eligible customers now, but there is a small private sector operating in this area, and Medicaid eligibility rules are likely to change.

What’s that worth for the network deployer? Here we show a modest $1,000 a month revenue to the network operator with a profit of $200 a month. That leaves plenty of room for fees by the third-party providers that actually do the monitoring work and install temporary equipment. If just 5 percent of customers need the service at any one time, the $10 monthly profit and $50 ARPU is comparable to revenues from video! If the carrier keeps the full $1,000, it needs just 1 percent of its customer base to make the indicated revenue.

Few areas of the United States are likely to have enough elderly and disabled in their population to hit that 5 percent target right now. True. Just 13 percent of the population is over 65 today, and about 1 percent of the population is in its final year of life. But that’s a national average, and more than

11,000 people reach age 65 every day in the United States!

The security and remote video presence industry has changed enormously in just the last few years, thanks in large part to the smartphone. Security was once a simple business, with network providers marketing the services of local security operators and taking about half the revenue, but household and small-business video monitoring is fast becoming the new norm. This approach requires more upstream bandwidth than is easily available in DSL and cable networks. Fiber makes it easy – plenty of upstream bandwidth and much greater reliability. Result: almost twice the revenue and profit potential with less carrier liability.

What about distance learning? Two percent of all children are home-schooled. Increased bandwidth, where available, has been growing that market – and parents value it highly. Fiber providers can provide it with enhanced reliability at little extra cost because the educational peak use times differ from normal evening peak use.

Market research conducted by RVA shows that one of eight FTTH homes has an at-home business. Serving these homes with virtual private networks, fixed IP addresses and better service-level agreements costs FTTH carriers very little, but customers value these business perks highly. Think about the piano, violin and other music instructors who teach remotely, using appliances available at music stores. They are customers for enhanced services, and so are their students’ families.

Other major moneymakers include smart-grid and cloud services, shunting wireless traffic to landlines through

home wireless hotspots and providing low-latency connections for interactive gaming. By “major,” we’re talking about profits that rival what carriers make now by providing video to a much greater customer base!

Obviously, not every service will find a market in every area, but this simple model shows almost $80 direct profit per month – enough to allow shortfalls and still cover SG&A. It includes only services that are available today. It does not include, for instance, carrier revenue for access to reliable over-the-top video services. That could be a great business, but it isn’t here – yet.

ADJUSTING THE BUSINESS PLANObviously, small carriers should not be thinking about bringing all these services to market themselves. That’s why so many consultants have new respect for the potential of open-access systems in the United States. Before dismissing that model out of hand, consider that there are many types of open access. Even the largest telephone companies, Verizon and AT&T, sell many services they didn’t create and don’t own – especially to their customers in multifamily housing.

Though some carriers might simply lease dark fiber or existing lit bandwidth capacity (and some municipal carriers may be forced to do so by state law), a more typical arrangement for smaller carriers in the United States would be to open customers to third-party marketing, open central offices to co-located servers and provide customer service and billing for sellers of specialized services. Clearly, arrangements will vary by type of service offered. Vendors that have a long history of providing BSS/OSS services are already offering database products to help carriers adapt to a multiservice, multivendor environment.

What about rebuilding customers’ on-premises networks? Again, that can be turned into a revenue opportunity. A carrier’s crew can do the job less expensively than can crews contracted by third-party providers of services that run on the carrier’s system.

Carriers should be thinking about services beyond the triple play, such as telehealth, distance education, security, smart grid and more. These services are real today.

July 2013 | www.broadbandcommunities.com | BROADBAND COMMUNITIES | 83

Expanding with fiber also allows special flexibility. Small carriers can, and do, spread their overhead expenses by operating as CLECs in towns outside their traditional service areas. Now, they might also find it worthwhile to expand outward from small-town cores along rural roads as long as the large ARPU makes the new customers profitable at the margin. The new customers might cost only a few dollars per month each in extra overhead.

Carriers that have cash on hand to throw into the pot might find this approach especially enticing. Their internal rate of return target might be 6 or 8 percent. But is the nest egg earning anything sitting in the bank?

Offering enhanced services can also spur economic development, as so many

of the services help keep aging people in place or aid small businesses. This increases the chance that a carrier can find a partner that has lower borrowing costs – perhaps a public-private partnership or local anchor tenant.

This business model does not profiteer on triple-play services. Most of the value-add services are bought by people for whom the services have immense value, so there is little or no need for promotional pricing.

What’s more, the model can only get better. Yes, margins decline for any service over time. But the geniuses are always thinking of more services. There’s an app for that.

Reach Corporate editor Steve Ross at [email protected].

TEST yOUR OwN ASSUMPTIONS

To download the spreadsheet used to generate Figures 1 and 2, visit www.FTTHAnalyzer.com.

You’ll find other models there for investors and for monthly cash flow calculations.

Metrics for Low-Voltage Infrastructure In Student HousingBy David Daugherty / Korcett Holdings

A recurring problem area in student housing, especially when new properties are first put into service, is poorly designed and problematic low-voltage infrastructure. Students expect problem-free, high-performance Internet access from day one. This relatively simple concept is almost always overlooked in the chaos surrounding the construction and operation of a new multiple-dwelling-unit (MDU) community. Often there are too many independent parties with different business priorities.

To address this issue, property owners have begun to embrace the idea of standards for the design, installation and operation of low-

voltage infrastructure and Internet services. These standards begin with service-level expectations for subscribers and construction requirements for the underlying low-voltage infrastructure.

A panel of senior IT professionals (Taylor Jones of Elauwit Networks, David Lippke of Korcett Holdings and Mark Scifres of Pavlov Media) joined me to explore this problem and discuss passive and active components of low-voltage service level requirements, searching for common ground among all the parties involved. What single metric speaks loudest to merchant builders, owners, property managers and Internet service providers? Highlights of the discussion included:

84 | BROADBAND COMMUNITIES | www.broadbandcommunities.com | July 2013

SUMMIT COVERAGE

• Disparity of viewpoints: Deployment problems arise from a lack of communication between merchant builders and subsequent owners and operators. Merchant builders tend to “value engineer” or eliminate infrastructure without first understanding the longer-term impact on operating costs.

• Managed versus unmanaged bandwidth: Simply installing infrastructure (wiring and some

active electronics) is not sufficient. Advances in managing access to bandwidth can significantly reduce the consumption of bandwidth and can police usage to help ensure superior subscriber experiences. These improvements come with a price: standardization.

• Lessons from student housing (bulk Internet service) for traditional (non-bulk-service) MDUs: As the demand for superior

Internet access grows, MDU developers will be forced to consider providing Internet access as part of their competitive strategies. This means considering the purchase of bulk Internet services for residents. Bulk services are purchased on a wholesale basis by building owners, and residents are required to pay for them as part of the rent or common charges. Lessons learned in the deployment of managed services for student housing will make the deployment of such services possible.

David Daugherty is the founder and CEO of Korcett. He can be reached at [email protected]. Korcett is dedicated to the design, development, deployment and support of next-generation managed service solutions.

Bulk Broadband in MDUsBy Bryan Rader / Bandwidth Consulting LLC

The session called Bulk Broadband in Today’s MDUs focused on the very trend brought up by the Metrics panel. This well-attended session included operators who provide bulk broadband services to a growing number of MDUs today. If private cable operators (PCOs) or traditional cable operators are looking for a growing area of the MDU business to target, that appears to be bulk broadband.

The session, which I moderated, highlighted the fast-growing phenomenon of bulk broadband, which I believe presents a big opportunity for PCOs, Internet service providers and traditional cable providers. “It’s important for each provider to think about the opportunity in all areas of the MDU market, not just in traditional apartment communities,” I told the audience. The prospective market includes student housing, senior housing, condominiums and hospitality. Bulk broadband is becoming more commonplace in all these sectors.

Although bulk cable TV service has

existed for more than 30 years, there appears to be a trend toward adding broadband to the bulk TV package or replacing digital TV with bulk broadband. In a recent RVA survey of MDU residents (see the May-June 2013 issue of this magazine), 79 percent of the respondents found “fast broadband” an important housing amenity; the panel agreed that the value consumers placed on broadband was the reason bulk broadband has taken center stage in the amenities packages they are providing MDU owners today.

THE RESIDENT PROFILE Terry Koosed, CEO of BelAir Internet, based in Los Angeles, spoke to the property owner segment of the audience. “How do you know whether you should offer bulk Internet?” he asked. “Well, you should look at your market, your competitors and your resident profile. Is this something they value? Will they use it? Will it help differentiate you from others in the market?”

Farzad Moeinzadeh, president and

co-founder of Silver Communications in Chicago, stated that “very fast Internet is now becoming like any other utility. Your residents will want it just like they they want water or electricity. It’s not really an option anymore.” Silver Communications serves more than 35 luxury buildings in Chicago with bulk Internet and is rapidly expanding, he said. “It’s obvious to us that there is strong demand for this service.”

John Van Oppen, CEO of Seattle-based CondoInternet, shared a story about a recent resident who was interested in subscribing to his gigabit bulk service. “He was looking for a place to move to in downtown Seattle, and he wanted to look at only the buildings that had our service. So he plotted the building addresses where we offer service on Google Maps and uploaded it to our website for others to see.” Van Oppen said super-fast broadband (as fast as 1 Gbps) has been driving renters to the buildings he serves. “Everything we have is within a 6-mile radius of downtown Seattle,” he

Deployment problems arise from a lack of communication between merchant builders and the owners and operators who must live with the infrastructure they created.

July 2013 | www.broadbandcommunities.com | BROADBAND COMMUNITIES | 85

explained. “My resident profile tends to be younger and more tech-y, and they eat up this speed.”

Though the operators on our panel were in large markets – Los Angeles, Chicago and Seattle – I mentioned that bulk Internet was an opportunity for operators in areas outside those big markets, too. It’s been commonplace in student housing for quite some time, many of which are in Tier 2 or Tier 3 markets, and we are now seeing it expand to senior housing and condos throughout the United States.

RELIABILITy AND SERVICE One audience member asked about providing wireless Internet services in bulk. Koosed responded, “We think that wireless can be a vital part of your broadband strategy. In fact, we use wireless in common areas and in some buildings. But we have found other solutions to be more reliable.”

“We don’t use wireless as our delivery vehicle in our buildings,” answered Van Oppen. “We have our own network and use fiber feeds directly to each building.”

Another audience participant asked about quality standards for providing bulk broadband to MDUs.

“One of the most important parts of our service is the support,” said Moeinzadeh. “We have to be better than our competition – which means not just providing the speed to the building, but also giving them exceptional on-site

support if they need it.”Koosed agreed. “We believe on-site

service is critically important. In fact, our technicians will spend time with our customers helping them with a particular issue. It’s part of our bulk service.” v

Bryan Rader is CEO of Bandwidth Consulting LLC, which assists providers in the multifamily market. You can reach Bryan at [email protected] or at 636-536-0011. Learn more at www.bandwidthconsultingllc.com.

The Leading Conference on Broadband Technologies and Services

Broadband Communities Magazine Congratulates

For more information on Dish, visit www.dishnetwork.com.You are cordially invited to come see Dish at the upcoming

For becoming a Gold Sponsor at the 2014 Broadband Communities Summit.

For other inquiries: 877-588-1649 | www.bbcmag.com

To Exhibit or Sponsor contact: Scott DeGarmo [email protected] | 718-884-3797

Bulk Internet is an opportunity even for operators outside the largest markets. It’s expanding from student housing to senior housing and condos throughout the U.S.

Did you like this article? Subscribe here!Did you like this article? Subscribe here!