Profit related pay - Learmond-Criqui Sokel LLP VOL V, Number 01... · Profit related pay Creating a...

10

PRACTICE BRIEF Profit related pay Creating a win-win situation Salaries and wages are two of the highest costs for an employer. JESSICA LEARMOND-CRIQUI looks at how an employer can adjust its staff costs through profit related pay. • By substituting PRP for part of exist- ing pay, PRP can be used by an employ- er to reduce or maintain gross pay levels whilst increasing employees' net pay. Where gross pay is reduced this also achieves National Insurance savings for an employer. • If part of pay moves up and down with profits, it may give employees a more direct personal interest and com- mitment in the company’s success. Advantages for an employee • Substituting part of existing pay for PRP may result in more take home pay because the employee pays less income P rofit related pay (PRP) is a part of salary which is linked to the profits of a company. It may be paid to an employee free of tax. For an employee to receive this benefit, the employer must establish a PRP scheme which complies with the legislation introduced in 1987 and must register it with the Inland Rev- enue. A PRP scheme is suitable for a private or public company, a partnership or a sole trader. There are a variety of ways of in- troducing it: • As part of a pay award. • Instead of a pay award. • Instead of current pay (when it may reduce the employer’s salary costs). The rules for PRP when introduced were complicated, but they have been simpli- fied in subsequent budgets. Before the 1991 Budget, the tax benefit was not a big enough incentive, and it has taken time for companies to respond to the re- vised, more generous tax environment. As at 30th September, 1993, there are more than 1,228,200 employ- ees in PRP schemes as compared with 26,411 in October, 1987 and 5,405 live schemes as compared with 145 in October, 1987. Advantages for an employer • Many employers of- fer performance-related pay packages. PRP can be blended into the prof- it-related element of ex- isting remuneration packages. tax. Even if gross pay is reduced, net pay may therefore increase and the employ- ee will also pay less national insurance (if his gross income is below £21,840 per annum) (see inset box “More take home pay ’’). • The restrictions on participation in a PRP scheme for employee shareholders are more generous than restrictions ap- plying to employee shareholders under say, an Inland Revenue approved execu- tive share option scheme. This is be- cause under an executive scheme, em- ployees whose beneficial interest, when taken with that of their associates, ex- ceeds 10 per cent, of the ordinary share capital of a close company cannot par- ticipate in an executive scheme, whereas the relevant percentage in a PRP scheme is 25 per cent.. • If pay levels respond more rapidly to changing market conditions, employ- ment may be more stable. Disadvantages for an employee • The PRP element of pay may not be taken into account by a mortgage lender in determining the maximum amount of an advance. 0 There is an element of risk that the PRP ele- ment of pay may not be paid. Employees may seek guarantees that they will receive the same basic pay after the introduction of a PRP scheme as before. An employer could not give such a guarantee as the concept of a PRP scheme involves some risk to the employee and the Inland Revenue is unlikely to register a PIC JANUARY/FEBRUARY 1994 21

-

Upload

dinhkhuong -

Category

Documents

-

view

214 -

download

0

Transcript of Profit related pay - Learmond-Criqui Sokel LLP VOL V, Number 01... · Profit related pay Creating a...

PRACTICE BRIEF

Profit related payCreating a win-win situation

Salaries and w ages are tw o of

the highest costs for an

em ployer.

JESSICA LEARMOND-CRIQUI

looks at how an em ployer can

adjust its staff costs through

profit related pay.

• By substituting PRP for part of existing pay, PRP can be used by an employer to reduce or maintain gross pay levels whilst increasing employees' net pay. Where gross pay is reduced this also achieves National Insurance savings for an employer.

• If part of pay moves up and down with profits, it may give employees a more direct personal interest and commitment in the company’s success.

A dvantages for an em ployee

• Substituting part of existing pay for PRP may result in more take home pay because the employee pays less income

Profit related pay (PRP) is a part o f salary which is linked to the profits of a company. It may be paid to an employee free of tax.

For an employee to receive this benefit, the employer must establish a PRP scheme which complies with the legislation introduced in 1987 and must register it with the Inland Revenue.

A PRP scheme is suitable for a private or public company, a partnership or a sole trader. There are a variety of ways of introducing it:

• As part o f a pay award.

• Instead of a pay award.

• Instead of current pay (when it may reduce the employer’s salary costs).

The rules for PRP when introduced were complicated, but they have been simplified in subsequent budgets. Before the 1991 Budget, the tax benefit was not a big enough incentive, and it has taken time for companies to respond to the revised, more generous tax environment. As at 30th September,1993, there are more than 1,228,200 employees in PRP schemes as compared with 26,411 in October, 1987 and 5,405 live schemes as compared with 145 in October, 1987.

A dvantages for an em ployer

• Many employers offer performance-related pay packages. PRP can be blended into the profit-related element of existing remuneration packages.

tax. Even if gross pay is reduced, net pay may therefore increase and the employee will also pay less national insurance (if his gross income is below £21,840 per annum) (see inset box “More take home pay ’’).

• The restrictions on participation in a PRP scheme for employee shareholders are more generous than restrictions applying to employee shareholders under say, an Inland Revenue approved executive share option scheme. This is because under an executive scheme, employees whose beneficial interest, when taken with that of their associates, exceeds 10 per cent, o f the ordinary share capital of a close company cannot participate in an executive scheme, whereas the relevant percentage in a PRP scheme is 25 per cent..

• If pay levels respond more rapidly to changing market conditions, employment may be more stable.

D isadvantages for an em ployee

• The PRP element o f pay may not be taken into account by a mortgage lender

in determining the maximum amount of an advance.

0 There is an element of risk that the PRP element of pay may not be paid. Employees may seek guarantees that they will receive the same basic pay after the introduction of a PRP scheme as before. An employer could not give such a guarantee as the concept of a PRP scheme involves some risk to the employee and the Inland Revenue is unlikely to register a

P IC JA N U A R Y /F E B R U A R Y 1994 21

PRACTICE BRIEF

scheme which guarantees a fixed payment as PRP. However, it may be possible, with professional advice, to reduce the risk of fluctuations in profits under a PRP scheme to a minimum.

• As the definitions of salary and relevant emoluments relate to those liable to PAYE deductions, the exempt part of any PRP is not included in calculating the limits to an employee’s entitlement under an approved profit sharing scheme and an approved share option scheme.This may result in an employee receiving less benefit under the approved scheme than if the PRP element was included in the calculation.

D isadvantages for an em ployer

9 An employer will have to obtain a high degree of employees’ support to the introduction of a PRP scheme.

• In introducing the scheme, contracts of employment, collective bargaining agreements and pension arrangements may have to be reviewed and perhaps renegotiated. For example, if PRP is introduced by means of a salary sacrifice, then it amounts to a change in the terms and conditions of employment and employees' consent is required (this may be obtained by requesting employees to sign and return a copy letter varying the terms of employment). Negotiations may have to take place with trade unions which may resist the introduction of a PRP scheme on this basis unless the company is prepared to share its savings with the employees.

• Sole traders and partners may have to be more forthcoming with employees on how the business is performing and to accept that the profit and loss account may well be made public for the first time. However, if employees of a sole trader or partnership are employed by a service company which is limited, their access to profit and loss accounts will be limited to those of the service company. If, however, the service company is an unlimited company (which is not obliged to publish its profit and loss accounts), then employees will not have access to its accounts.

• The method of calculating the pool of

profits to be distributed to employees must be determined before the scheme is registered and therefore before profits are known.

• Unlike approved share option schemes and approved profit sharing schemes, PRP schemes are only registered and not approved by the Inland Revenue, this can lead to claw-backs of tax if the Inland Revenue later challenges the scheme.

Setting up a schem e

The legislation governing PRP was first introduced by the Finance (No. 2) Act 1987 and is now contained in sections 169 to 184 of, and Schedule 8 to the Income and Corporation Taxes Act 1988. It is supplemented by a 75 page set of Guidance Notes which is available free from the Profit-Related Pay Office at St Mungo’s Road in Cumbernauld. Glasgow.

In addition, the Inland Revenue has provided two sets o f model rules which are contained in the Inland Revenue Booklet “Tax relief for Profit-Related Pay - Setting up a Scheme”. Many options and variations available for a PRP scheme have not been included in the model rules. Nevertheless, the rules are useful and are designed to be used as a starting point, although they should be adapted specifically for use by each company. The principal conditions for registration are discussed below.

• Form. The terms of the scheme must be set out in writing.

9 Duration. The rules must specify how long a scheme is to last, but it must be for a minimum period of one year unless it is the first period of a short term replacement scheme or the scheme allows registration to be cancelled during a profit period.

• Employment unit. The scheme must identify clearly the undertaking to which it relates which may be:

- A single company.

- A group.

- A subsidiary.

- The whole or part of a business, whether incorporated or unincorporated, including an individual division or profit centre.

The undertaking is referred to in the legislation as an “employment unit” (Income and Corporation Taxes Act 1988, section 169(1)). It must be possible, from the description of the unit, to identify all the employees who work for that unit. The employment unit must usually be carried on with a view to profit, although there are special rules which would allow, say, the research and development division of a company to qualify.

Normally, separate audited figures must be available for each employment unit. This means that if the employment unit is at an individual division or profit centre level, the cost o f arranging audited accounts in respect of that division or centre may have to be incurred. However, it may be possible to use the profits of the whole undertaking (see ‘Parts o f an Undertaking ’).

• Scheme employer. The scheme must identify the scheme employer. This is the person who can apply for registration of a PRP scheme (see 'Registration ’) and is responsible for operating the scheme. This will either be an individual, partnership or company.

• Profit periods. The PRP scheme must define the periods by reference to which any PRP is calculated. Generally, these must be 12 month periods, although there is no requirement that they coincide with the statutory accounting period of a business or company. However, a company may, to reduce the costs of running the PRP scheme, arrange for the frequency of determination of the PRP pool to be in line with its arrangements for producing audited accounts.

There are two exceptions to the 12 month rule:

- The first applies when the scheme rules provide for the registration of a scheme to be cancelled during a profit period and for a shortened period (the part prior to the cancellation) to be used for the profit period in such a case.

22 PLC JA N U A R Y /F E B R U A R Y 1994

PRACTICE BRIEF

More take home pay

In the case of a single employee earning £20,000 per annum, by substituting £4,000 o f his existing pay with PRP, the employee may enjoy an increase in pay

of £1,000.

Gross salary PRP element

Total taxable salary

20 per cent, tax on first £2,500 after deducting single person's allowance o f £3,445

25% tax on balance

Employee's NIC on gross salary (a t 2% on first £56 per week and 9% on the balance)

BalanceAdd back PRP to determine net salary

Net salary

BeforePRP£

20,000.00

0.00

20,000.00

500.00

3,513.75

1,596.165,609.91

14.390.09

0.00

14.390.09

AfterPRP£

20,000.00

-4,000.00

16,000.00

500.00

2,513.75

1,596.164,609.91

11,390.09

+ 4,000.00 PRP

15,390.09

* These figures are based on the tax rates for 1993/1994 and will ultimately depend on the rates of income tax, national insurance (whether contracted in or out), the amount of personal allowances and the maximum limit o f £4,000 of PRP.

Before PRP A fte r PRP

salary NIC£14,390.09 £1,596.16

tax£4,013.75

salary NIC£15,390.09 £1,596.16

tax£3,013.75

- The second applies when a new scheme replaces a previous one whose registration has been cancelled (a short-term replacement scheme). If the replacement scheme provides for two profit periods it can commence with a period of less than 12 months, thereby offering continuity. A replacement scheme has simplified features and cannot extend beyond two years. This would give time to put fresh arrangements in place.

• Employees. Generally, it is for the employer to decide who is to participate. The scheme must make it clear which employees are to receive payments under the scheme. The following employees must however be excluded:

- Any employee with a material interest in the employing company, or its parent.

- Any employee whose emoluments are not assessable under the Income and Corporation Taxes Act 1988, Schedule E.

A person has a material interest if he, together with one or more associates {as defined in the Income and Corporation Taxes Act 1988, section 417(3) and (4)), has beneficial ownership of, or ability to control, more than 25 per cent of the ordinary share capital of the company or, in the case of close companies, the entitlement to more than 25 per cent, of assets available for distribution in a winding up.

Other employees may, at the employer’s discretion, be excluded. These are:

• Part-time employees who are required to work less than 20 hours per week.

• New recruits with three or less years’ service with the employer.

In addition, PRP cannot apply to employees in “excluded employments”, for example, nationalised industries, the Crown or a local authority.

An employer should consider whether the scheme should make provision for payments to former employees. Since the whole o f the PRP pool must be dis

tributed to employees who are entitled to receive payments under the PRP scheme, an employer may have difficulty tracing an employee who has already left at the time of payment. This difficulty can be avoided by including a rule in the PRP scheme that payment will be made only to employees working in the

business at the time of payment.

In addition, all employees must participate on “similar terms”. “Similar terms” could mean that:

- All employees receive exactly the same amount (by splitting the distrib-

PLC JA N U A R Y /F E B R U A R Y 1994 23

PRACTICE BRIEF

utable pool between the number of eligible employees).

- The entitlement is proportionate to salary.

- The entitlement is linked to other objective factors such as the number of hours worked (which may discourage absenteeism) and length of service (which may discourage staff turnover).

In any event, distribution of PRP cannot be based on a subjective view of individual performance. There is nothing to prevent additional (taxable) payments being made to deserving employees which would be outside the PRP scheme.

• Level of participation in the PRP

scheme. After deciding which employees are to be excluded, the remainder are eligible to participate. But, the scheme must contain provisions ensuring that no payment is made under it in respect of profit period in which the employees to whom the scheme relates constitute less than 80 per cent, of all the employees in the employment unit at the beginning of that profit period.

• Parts of undertaking. The 80 percent, rule is adapted for cost centres within a company for which the preparation of separate profit and loss accounts in respect of that employment unit would be difficult and costly. Examples of such cost centres would be head office administration, research and development units or any other unit in which the work performed is not profit-related. In these circumstances, the profits and

losses of the cost centre can be taken, for the purposes of the PRP scheme, to be those of the undertaking of which it forms part. But such a special scheme would qualify only if at the beginning of the profit period:

- There is at least one other “normal” scheme covering other employees in the undertaking of which the cost centre forms part.

- The number of employees in the special scheme covering the cost centre does not exceed 33 per cent, o f the number in the normal scheme.

At present, there are no rules linking the sums received under a special scheme with sums received under the normal scheme, but this will change for special schemes registered on or after 1st December, 1993 if Parliament approves the Chancellor’s proposals (announced in his Budget on 19th November, 1993). Such schemes will have to satisfy a further condition. At the start of each profit period the scheme must ensure that its fixed percentage (if it is a Method A scheme) or its notional or distributable pool (if it is a Method B scheme) does not exceed a limit to be calculated by reference to the ratio of total pay to PRP in the other scheme registered for the undertaking in question. The ratio will be calculated by reference to the figures for pay and PRP paid in a specified earlier period.

This change is designed to stop exploitation of the special scheme provisions by employers who set up a registered normal scheme or schemes for the bulk of their employees - paying out only nominal amounts of PRP - so that they can then set up a special scheme for selected employees which pays out substantial amounts of PRP.

• Distributable pool. This describes the size of the total amount of PRP payments to employees (Income and Corporation Taxes Act 1988, paragraph 11, Schedule 8). It is determined from the profit and loss account as adapted for PRP puiposes. Except in the case of a replacement scheme, there are two methods for determining the size of the PRP pool, only one of which may be chosen.

Chancellor's proposalsIf Parliament approves the Chancellor’s proposals announced in his Budget on 19th November, 1993, then, a scheme registered on or after 1st December, 1993 which includes an upper percentage limit will have to take account o f the following:

• It must include a provision which ensures that the basic upper percentage limit of 160 per cent, (or more) will be increased by a further percentage whenever the taxable pay o f employees in the business (or part o f the business) covered by the scheme is less than it was in the previous period or base year.

In those circumstances, the total decrease in taxable pay must in future be expressed as a percentage of the profits in the previous period or base year and that percentage must be added to the basic upper percentage limit of 160 per cent, (or more). The increased percentage will then become the upper percentage limit for the profit period in question.

This is to prevent exploitation o f the PRP legislation by using a PRP scheme to make payments exactly equal to a pay sacrifice made by employees and without reference to fluctuations in profits.

• It will be a requirement that, for the purposes of the upper percentage limit, the same definition o f profits must be used for both the current and previous PRP profit periods. Thus, current profits before PRP will have to be compared with previous profits before any PRP was paid out (whether under the same PRP scheme or any other) - in order to determine whether the upper percentage limit has been exceeded.

This new requirement will also apply to:

- The calculation of the lower profits limit.

- The calculation o f profits for the purposes o f a Method B PRP scheme.

24 PLC JA N U A R Y /F E B R U A R Y 1994

PRACTICE BRIEF

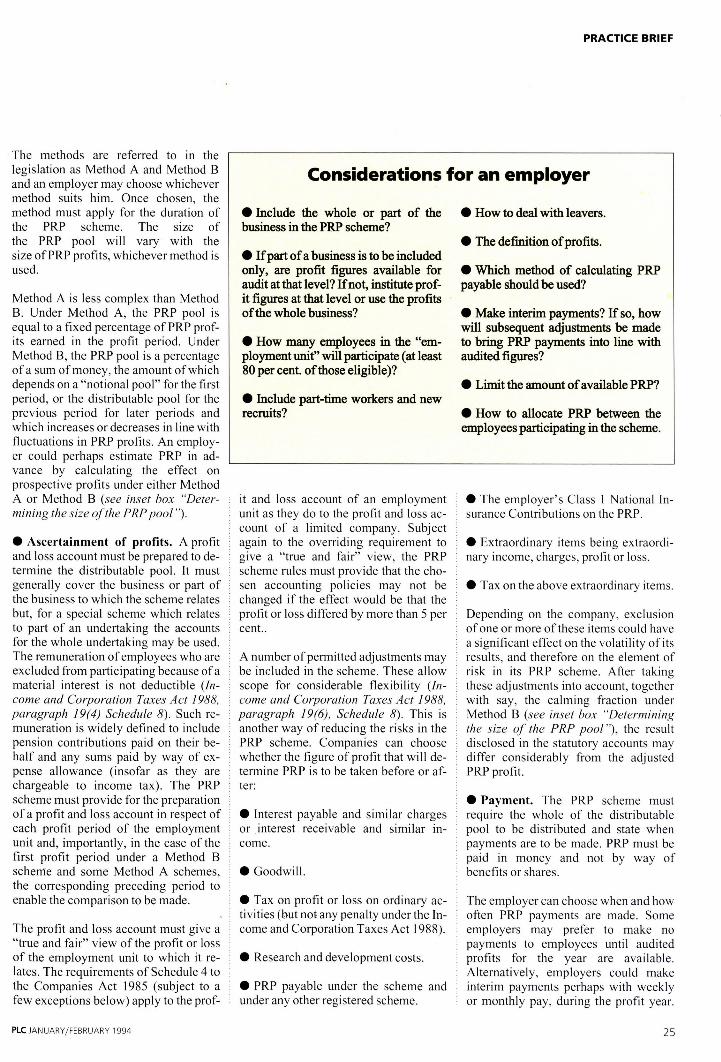

Considerations for an employer

• Include the whole or part o f the business in the PRP scheme?

• If part o f a business is to be included only, are profit figures available for audit at that level? If not, institute profit figures at that level or use the profits o f the whole business?

• How many employees in the “employment unit” will participate (at least 80 per cent, o f those eligible)?

• Include part-time workers and new recruits?

• How to deal with leavers.

• The definition o f profits.

• Which method of calculating PRP payable should be used?

• Make interim payments? If so, how will subsequent adjustments be made to bring PRP payments into line with audited figures?

• Limit the amount of available PRP?

• How to allocate PRP between the employees participating in the scheme.

The methods are referred to in the legislation as Method A and Method B and an employer may choose whichever method suits him. Once chosen, the method must apply for the duration of the PRP scheme. The size of the PRP pool will vary with the size of PRP profits, whichever method is used.

Method A is less complex than Method B. Under Method A, the PRP pool is equal to a fixed percentage of PRP profits earned in the profit period. Under Method B, the PRP pool is a percentage of a sum of money, the amount of which depends on a “notional pool” for the first period, or the distributable pool for the previous period for later periods and which increases or decreases in line with fluctuations in PRP profits. An employer could perhaps estimate PRP in advance by calculating the effect on prospective profits under either Method A or Method B (see inset box “Determining the size o f the PRP pool ”).

• Ascertainment of profits. A profit and loss account must be prepared to determine the distributable pool. It must generally cover the business or part of the business to which the scheme relates but, for a special scheme which relates to part of an undertaking the accounts for the whole undertaking may be used. The remuneration of employees who are excluded from participating because of a material interest is not deductible (Income and Corporation Taxes Act 1988, paragraph 19(4) Schedule 8). Such remuneration is widely defined to include pension contributions paid on their behalf and any sums paid by way of expense allowance (insofar as they are chargeable to income tax). The PRP scheme must provide for the preparation of a profit and loss account in respect of each profit period of the employment unit and, importantly, in the case of the first profit period under a Method B scheme and some Method A schemes, the corresponding preceding period to enable the comparison to be made.

The profit and loss account must give a “true and fair” view of the profit or loss of the employment unit to which it relates. The requirements of Schedule 4 to the Companies Act 1985 (subject to a few exceptions below) apply to the prof-

PLC JA N U A R Y /F E B R U A R Y 1994

it and loss account of an employment unit as they do to the profit and loss account of a limited company. Subject again to the overriding requirement to give a “true and fair” view, the PRP scheme rules must provide that the chosen accounting policies may not be changed if the effect would be that the profit or loss differed by more than 5 per cent..

A number of permitted adjustments may be included in the scheme. These allow scope for considerable flexibility (Income and Corporation Taxes Act 1988, paragraph 19(6), Schedule 8). This is another way of reducing the risks in the PRP scheme. Companies can choose whether the figure of profit that will determine PRP is to be taken before or after:

# Interest payable and similar charges or interest receivable and similar income.

• Goodwill.

0 Tax on profit or loss on ordinary activities (but not any penalty under the Income and Corporation Taxes Act 1988).

• Research and development costs.

# PRP payable under the scheme and under any other registered scheme.

• The employer’s Class 1 National Insurance Contributions on the PRP.

• Extraordinary items being extraordinary income, charges, profit or loss.

• Tax on the above extraordinary items.

Depending on the company, exclusion of one or more of these items could have a significant effect on the volatility of its results, and therefore on the element of risk in its PRP scheme. After taking these adjustments into account, together with say, the calming fraction under Method B (see inset box "Determining the size o f the PRP p o o l”), the result disclosed in the statutory accounts may differ considerably from the adjusted PRP profit.

• Payment. The PRP scheme must require the whole of the distributable pool to be distributed and state when payments are to be made. PRP must be paid in money and not by way of benefits or shares.

The employer can choose when and how often PRP payments are made. Some employers may prefer to make no payments to employees until audited profits for the year are available. Alternatively, employers could make interim payments perhaps with weekly or monthly pay, during the profit year.

25

PRACTICE BRIEF

These payments could be based on interim profit figures and, ifthought appropriate, take account of anticipated seasonal variations in profits and the expected trend in profits over the rest o f the profit year. This would allow profits to affect PRP much sooner.

However, care should be taken to avoid overpayment. If the total amount of interim payments is more than the final PRP allocation, any income tax relief allowed on the interim payments may be

M ethod AfOOOs

PRP profits

This graph shows the effect of setting an upper limit of 200% (of PRP profits for the previous profit period) and a lower limit of base year (1989) profits where the distributable pool is set at 30% of PRP profits. Note that there is no payment where PRP profits dropped below the lower limit in 1993.

Method A. The distributable pool may be expressed simply as a fixed percentage of PRP profits. Alternatively, the

recoverable by the Inland Revenue from the employer.

Registration

Application for registration normally has to be made by the person who is responsible for paying the emoluments o f all the scheme’s employees. However, there are exceptions:

# Group Companies. If there are two or more group companies (that is, a company and its 51 per cent.

subsidiaries) paying the emoluments of the scheme employees, then the parent of the whole group can apply for registration, even if it does not have any of its own employees in the PRP scheme. Alternatively, the immediate parent of those companies with employees in the PRP scheme can apply. Each of the employers who pays the employees in the PRP scheme must be identified.

• Overseas parent companies. Anoverseas parent company can apply to register its UK subsidiaries belonging to

Determining the PRP pool

percentage may be expressed as a formula which must be capable of producing one percentage only. Such a formula must be capable of producing a fixed result at the time the scheme is written. Once determined, the percentage will apply for the duration of the PRP scheme.

It is also possible to set upper and lower profit limits beyond which PRP profits are ignored. They may be expressed as percentages and applied to the profits of the previous period in setting the limits on profits used to calculate the size of the PRP pool for the current period. If an upper limit is to apply from the scheme’s first year, the percentage is applied to the profits of a period which may be any 12 month period ending at some time within 2 years immediately before a PRP scheme’s start date (a base year). The lowest permitted upper limit is 160 per cent, of the previous profit period or base year (but see inset box “Chancellor's Proposals ”) although a higher figure may be used.

For example,

Profits in the year before start o f scheme (1991)

Profit in first year o f operation of scheme (1992)

£500,000

£1.5 million

If the Method A percentage is set at 10 per cent, this produces a distributable pool o f

£150,000 in 1992. But if an upper percentage lim it o f 200 per cent, has been set, this results in an upper pro fit lim it in 1992 o f £1 million, against which the Method A percentage is applied. This gives a distributable pool in 1992 o f £100,000.

The use of an upper percentage limit can cushion the effect on the payroll costs of volatile trading results. But the limit cannot be applied in a profit period if the previous period showed losses.

The lower profit limit must not be more than the profits o f the base year, although it can be set at less than the base year profits (but see “Chancellor’s Proposals”). Thus, employers could not treat a PRP scheme as a bonus scheme requiring their employees to aim for higher profits than the previous period before making PRP payments under the scheme.

If a lower limit is set and profits fall below that limit, then there is no distributable pool for the year in question. Losses in a base year will mean that a lower limit cannot be set.

Although the Method A fixed percentage cannot be changed, the employer can introduce, amend, or remove upper percentage and lower profits limits. Such changes will apply from the beginning of the next profit period.

Method B. This involves use of the percentage change in profits from one

26 PLC JA N U A R Y /F E B R U A R Y 1994

PRACTICE BRIEF

the same group. Alternatively, a UK subsidiary of a foreign company can apply for registration of a PRP scheme for its own employees or, if it is a parent of other UK subsidiaries in the same group, a group PRP scheme covering the employees of those subsidiaries.

The application for registration may be made to the PRP office. Inland Revenue Cumbernauld (on form PRP 10). It must be accompanied by a report by an independent accountant giving an opinion that the PRP scheme complies with all

statutory conditions for registration and that the books and records maintained will be adequate for completing an annual return to the Inland Revenue. An applicant must undertake that any employee covered by the PRP scheme to whom the minimum wage legislation applies will receive emoluments which satisfy that legislation before any PRP entitlement is taken into account. It is not necessary to submit the actual rules of the PRP scheme with the application form, but the Inland Revenue may however request a copy if it raises further queries.

If application for registration is made more than three months before the start date, the Inland Revenue must register the scheme unless within 30 days it refuses to register the scheme, giving reasons, or asks for an amendment to the application or further information. If amendments or information are requested the PRP office will still register the scheme if the points are dealt with satisfactorily within, normally, 30 days. Where the PRP office is required to send a notice refusing registration there is a right to appeal to the Special Commis-

year to another to increase or decrease the PRP pool. This is in contrast to the fixed percentage used under Method A.

To calculate the first PRP pool. Method B requires the employer to choose an amount at the start of the first year as the “notional pool”. The notional pool (or in future years, the previous year's distributable pool) is then adjusted upwards or downwards in line with the percentage change in profits from one year to the next. For example:

The chosen notional pool is:

Current year profits:

Previous year's profits:

£20,000

£300,000

£200,000

Percentage changein profits = 300.000-200.000 x 100 = 50%

200,000

Apply percentageto notional = £20,000 + (£20,000 x 50)pool 100

Distributable pool ■ £30,000

Under Method B, if a loss occurs in any profit period, the PRP pool will not be able to be calculated in that year or in subsequent years and the registration of the PRP scheme will have to be cancelled.

As with Method A, the employer may use an upper or lower profit limit. The

M ethod B

Distributablepool afterapplying thecalming fraction

1988 1989 1990 1991 1992 1993Start of scheme

PRP profit periods

This graph shows the effect of applying a calming fraction of ’/ i to the distributable pool calculated under Method B. This will reduce the distributable pool when profits rise and increase it when they fall, thereby reducing the risks in the PRP scheme. But if a loss occurs in any profit period, the PRP scheme will have to be cancelled.

upper limit cannot be set at a figure which is less than 160 per cent, of the previous period’s profits and the lower profits limit must not be more than the profits in the 12 month period before the scheme’s start date (but see inset box "Chancellor’sProposals").

It is possible to limit the percentage change in the profits by a fraction, which must not exceed one half, to reduce fluctuations in profit (“the calming fraction”). This applies to reduce the distributable pool when profits rise and to increase it when they fall. For example, a 20 per cent, fall in profits can be translated into a fall o f only 10 per cent, in the PRP pool if a calming fraction of one half is chosen. This is therefore one way of reducing the risks in the PRP scheme.

For example:

Notional pool: £50,000(in first year o f operation o f PRP scheme or PRP pool from previous year)

Current year profits: £80,000

Previous year's profits: £100,000

Percentage = 80.000 -100.000 x 100change in profits 100,000

= - 20%

Apply percentage = £50,000+[50,000 x -20] change to notional 100pool

Distributable pool = £40,000

If a calming fraction o f the ’/ 4 is applied to the percentage change in profits this results in a larger PRP pool.

Percentagereduced by = -20 - (-20 x 1/4) = -15%calming fraction

Distributable pool = £50,000 + [50,000 x -151100

= £42,500

P LC JA N U A R Y /F E B R U A R Y 1994 27

PRACTICE BRIEF

sioners of the Inland Revenue. If application is made within three months before the start date there is no guarantee of registration but the PRP office will make every effort to register the scheme in time.

Registration of the PRP scheme does not mean that the scheme has been approved by the Inland Revenue or that it accepts that the scheme rules satisfy the legal requirements. A scheme which does not comply with the requirements of Schedule 8 is not entitled to be registered (Income and Corporation Taxes Act 1988, section 176(9)) and if it obtains registration while not complying with Schedule 8, it is liable to be de-registered in the future with retrospective effect (Income and Corporation Taxes Act 1988, section 178(2)). This will have adverse tax consequences for an employer.

Operating the schem e

After each profit period of a registered PRP scheme, the employer must send to the Inland Revenue:

• A return on form PRP 20 providing certain specified information together with the PRP scheme profit and loss accounts.

• A report by an independent accountant stating, among other things, that in his opinion the terms of the scheme have been complied with in the profit period.

These returns must be submitted within seven months of the end of the profit period of a public company and 10 months from the end of the profit period in all other cases. This accords with the time limits required by the Companies Act for filing annual accounts with the Registrar. However, limited companies with overseas interests can obtain three month extensions if they have done so under section 242(3) of the Companies Act 1985.

The employer will be responsible for operating the tax relief under PAYE. If it subsequently transpires that the terms of the PRP scheme were not followed, or the conditions applying to the tax relief were not met (for example, satisfactory audit reports were not provided), the Inland Revenue may recover from the employer tax relief incorrectly given.

The PRP scheme rules may be called for and inspected by the PRP office at any time.

Cancellation of registration

The registration of a PRP scheme may be cancelled either by the Inland Revenue or by the employer. It may be cancelled by the Inland Revenue if:

• At the time of registration the PRP scheme did not comply with the statutory requirements.

• The PRP scheme has not been or will not be administered in accordance with the PRP scheme rules or statutory requirements.

• During the period, the employment to which the PRP scheme relates has become an “excluded” employment for which no application to register a PRP scheme is permitted to be made.

• The undertaking given in respect of satisfaction of the minimum wage legislation has not been complied with.

• The PRP scheme employer fails to make an annual return in relation to a profit period within the time limit.

• Method B is used and losses are made in the profit period or in the 12 month period preceding the start of the PRP scheme.

The Inland Revenue may recover from the PRP scheme employer all tax relief given on payments after the effective date of cancellation. While there is no right to tax relief on payments relating to periods after the effective date of cancellation, a PRP scheme may continue without the benefit o f the relief. Payments made after cancellation, but which relate to the period before cancellation, will still qualify for relief.

The PRP scheme employer can, by giving written notice, require the Inland Revenue to cancel the PRP scheme registration with effect from the beginning o f a profit period. This provision gives the employer some flexibility and it enables the employer to cancel the scheme if, for example, there is a significant decline in profits in a particular year.

Changing the PRP schem e rules

Some of the relevant points relating to rule changes are:

O No change is permitted to the description of the employment unit.

P LC JA N U A R Y /F E B R U A R Y 1994

PRACTICE BRIEF

• Rules indicating which employees in an employment unit can participate in the PRP scheme may be changed (with effect from the start of the following profit period).

• Rules providing for when PRP payments are to be made may be changed (with effect from the beginning of the following profit period).

• Rules relating to lower profit limits, upper percentage limits or calming fractions (Method B) may be added, removed or changed (with effect from the beginning of the following profit period).

• Rules relating to shortened profit periods may be introduced.

• Rules which are not covered by the PRP legislation may be added or removed at any time.

• Employers may change a rule which does not comply with the law, add a rule which is required by law, or change a rule which is not clear.

Changes to rules must be registered with the PRP office using form PRP 12 within one month of any change. The application must contain a statement from the employer, supported by a report from an independent accountant, that the change is allowed under the law and that the amended scheme complies with the law.

Changing the schem e em ployer

When a PRP scheme employer changes, for example if the employment unit is sold or transferred, a PRP scheme is normally cancelled. However, the new employer may be substituted as the PRP scheme employer if there is no material change in the employment unit, and both employers make a joint application in writing before or within one month after the change. There is no special form for making this application. However, if a purchaser of an undertaking with a PRP scheme does join in making the application with the vendor of the scheme, it should seek an indemnity from the vendor against any tax liabilities which might arise in respect o f the PRP scheme. This is because, if substituted, the purchaser will be exposed to poten

PLC JA N U A R Y /F E B R U A R Y 1994

tial tax liabilities if, for example, registration is retrospectively withdrawn or payments in excess of the PRP limits were made under the scheme. On the acquisition of a company which has operated a PRP scheme, the normal tax warranties and indemnities should specifically cover liabilities relating to the PRP scheme.

Partnerships are treated as a continuing single body of persons, notwithstanding changes in their members (Income and Corporation Taxes Act 1988, section 183). Therefore, registration of a PRP scheme continues following a change in partners without the need to apply to the PRP office to have the change of the PRP scheme employer registered.

Replacem ent schem es

If a PRP scheme’s registration is cancelled because of a material change in the employment unit (for example, as a result of a merger or reconstruction) or in the circumstances relating to the PRP scheme (for example, a change in accounting date), then an application (on form PRP 10) may be made to register a replacement scheme. It is intended as a temporary measure to allow an employer time to set up a new PRP scheme during which tax-free PRP payments may continue to be made. It may run for a maximum of two profit periods. For replacement schemes, there are various conditions which must be met including:

• At least half of the employees covered by the replacement scheme at its start must have been covered by the original scheme at the time of the change.

9 The circumstances must not be such that the necessary amendment could have been made merely by a change of scheme employer.

9 The registration of a replacement scheme must be within three months of the material change in the employment unit or circumstances of the original scheme.

• If there is to be only one profit period in the replacement scheme, that period must be for 12 months.

Using PRP to cut pay

Checklist

If an employer is to pay part o f existing employees’ salaries through PRP:

• Set up a PRP scheme with the company’s auditors’ opinion.

• Obtain consent from 80 per cent, of employees.

• Apply for registration with the Inland Revenue at least three months before the start o f a profit period.

• Determine the amount of PRP based on the rules of the scheme and “true and fair” accounts of the employment unit.

• Make PRP payments giving tax relief to employees under PAYE.

• Make an annual return with an auditors’ report o f the operation o f the PRP scheme together with profit and loss accounts for the employment unit.

A replacement scheme does not use either Method A or Method B to determine the distributable pool. There is a simplified arrangement under which the pool is a fixed percentage of profits. No fractions, upper percentage or lower profits limits are permitted.

Tax and N ational Insurance

The set-up and annual costs of PRP schemes arc deductible for the employer's corporation tax purposes.

PRP constitutes earnings for National Insurance purposes. PRP paid under a scheme registered with the Inland Revenue is wholly exempt from income tax subject to a maximum of the lower of the following three limits (Income and Corporation Taxes Act 1988, section 171):

• 20 per cent, o f the sum of:

29

PRACTICE BRIEF

- the employee's pay during the profit period, less PRP, superannuation contributions and charitable payroll giving; and

- the employee's PRP for that period, regardless of when it is actually paid.

• £4,000 (for a whole year).

• The actual amount of PRP for the profit period in question.

Not all payments made under registered schemes qualify for tax relief. Payments will not qualify for tax relief if:

• PRP which qualifies for tax relief is received in respect of another employment at the same time.

• Secondary Class 1 National Insurance Contributions (that is, employer’s contributions) are not payable (except where it is not payable because the employee’s earnings are below the lower earnings limit for such contributions).

Effect on pension contributions and other benefits

An employee’s pension contributions in respect of an employer’s pension scheme which are deductible under section 592(7) of the Income and Corporation Taxes Act 1988, are limited to 15 per cent, of his remuneration for the year (section 592(8)). For this purpose, it is understood that the Inland Revenue takes the view that the part of the PRP which is exempt from income tax is included as remuneration. In addition, if a company pays PRP in excess of the maximum exempt amount for income tax purposes, then the whole of the payment will be included as remuneration contributions. Similarly, personal pension schemes are limited by reference to the net relevant

earnings which, in practice, are computed by reference to the whole of any PRP.

PRP may be taken into account in calculating entitlement to other benefits including overtime, sick pay, permanent health insurance and life assurance but the rules governing each benefit should be checked to determine whether this is the case.

The benefits

While it may be cost effective for an employer to set up a PRP scheme, whether to replace existing pay with PRP or to use PRP to make pay increases, its success will depend on the type of business involved, what profits are expected in the long term, and the type of employee relations the business enjoys. If introduced at the right time and if the strategy is communicated properly to employees, it may well contribute to the business, give the employees a sense that they are participating in the profits of the company and stem the need to reduce staffing levels in which a great deal of investment of money and time may already have been spent.

Is THIS A PHOTOCOPY OF PLC?

Photocopying of PLC requires written permission - so why not subscribeinstead?

Bulk subscription rates are available on request.

Invest in know-how - subscribe for your own copy of PLC.

Phone (071) 738 2303 for details.

30 PLC JA N U A R Y /F E B R U A R Y 1994