![What Can a Professional Employer Organization (PEO) Do for Your Business? [Infographic]](https://static.fdocuments.net/doc/165x107/55a8ca411a28ab1f628b467f/what-can-a-professional-employer-organization-peo-do-for-your-business-infographic.jpg)

What Can a Professional Employer Organization (PEO) Do for Your Business? [Infographic]

2012 NCCI Holdings, Inc.

Professional Employer Organizations(PEO) and Workers Compensation

Implications for Ratemaking

Harry ShufordPractice Leader & Chief Economist, NCCI

Use of Workers Compensation Data for Workplace Safety and Health

Washington, DCJune 19-20, 2012

2012 NCCI Holdings, Inc.

1

Today’s Presentation

Background on PEOs and the Labor Market

PEO Services

State Regulation of PEOs

Background on PEOs and Workers Compensation

Regulation of PEOs in Workers Compensation

Objectives of Actuarial Ratemaking

Comparing WC Claims Experience – PEOs and All Other

• 2004 - 2009

• Broken down by industry group in policy year 2007

Preliminary Observations

2012 NCCI Holdings, Inc.

2

Background on PEOs

• PEO services

− employee benefits

− payroll

− workers’ compensation

− risk management

− recruiting

− training and development

• “Employer of record” for the leased workers from a PEO client

company

NAPEO Contends that PEOs Create Safer Work Environments

-Effective safety practices such as:• pre-employment drug tests,• loss control and safety procedures, • claims management of injuries, • safety training, • employee assistance plans, • back-to-work programs, and • drug-free workplace programs

- According to NAPEO many of these safety practices are new to the typical PEO client-a small to mid-sized business without the time, expertise, or resources to cater to worker safety concerns

PEOs in Workers Compensation a Good Thing?

3

Source: National Association of Professional Employer Organizations (NAPEO) ©NAPEO 2012. Used with permission.

2012 NCCI Holdings, Inc.

Licensing

4

The Number of States Requiring Licensing of PEOs Has Grown Steadily:

5

Licensing States Map 1991 & 1995

Added in 1995

Source: National Association of Professional Employer Organizations (NAPEO) ©NAPEO 2012. Used with permission.

Licensing States Map2000 & 2005

Added in 2000

Added in 2005

6

Source: National Association of Professional Employer Organizations (NAPEO) ©NAPEO 2012. Used with permission.

Licensing States List2012

Current StatusAL, AZ, AR, CO, CT, FL, HI, ID, IL, IN, KY, LA, ME, MI, MN, MT, NE, NV, NH, NJ, NM, NY, NC, ND, OH, OK, OR, RI, SC, TN, TX, UT, VT, VA, WV, WI

CA, PA

Added in 2012

7

Source: National Association of Professional Employer Organizations (NAPEO) ©NAPEO 2012. Used with permission.

2012 NCCI Holdings, Inc.

8

One to Two Percent of Insured Payroll in Voluntary Market Is from PEOsResidual Market Share Has Been Approximately Four Percent

There Was a Marked Decline over the Great Recession

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

1.7%2.0%

2.1%2.0% 1.9%

1.8%

6.7%

3.7%

4.3%

4.9%

4.2%

2.3%

1.0%1.2%

1.5%1.1% 1.1% 1.1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2004 2005 2006 2007 2008 2009

PEO

Pay

roll

Shar

e

Policy Year

Voluntary Market PEO Payroll Share in 37 NCCI Ratemaking States

Residual Market PEO Payroll Share in 25 NCCI Ratemaking States

Voluntary Market PEO Payroll Share in 25 NCCI Ratemaking States

2012 NCCI Holdings, Inc.

Workers Compensation Data Indicate thatThe Role of PEOs Varies Greatly Across States

and Between the Voluntary and Residual Markets

10

2012 NCCI Holdings, Inc.

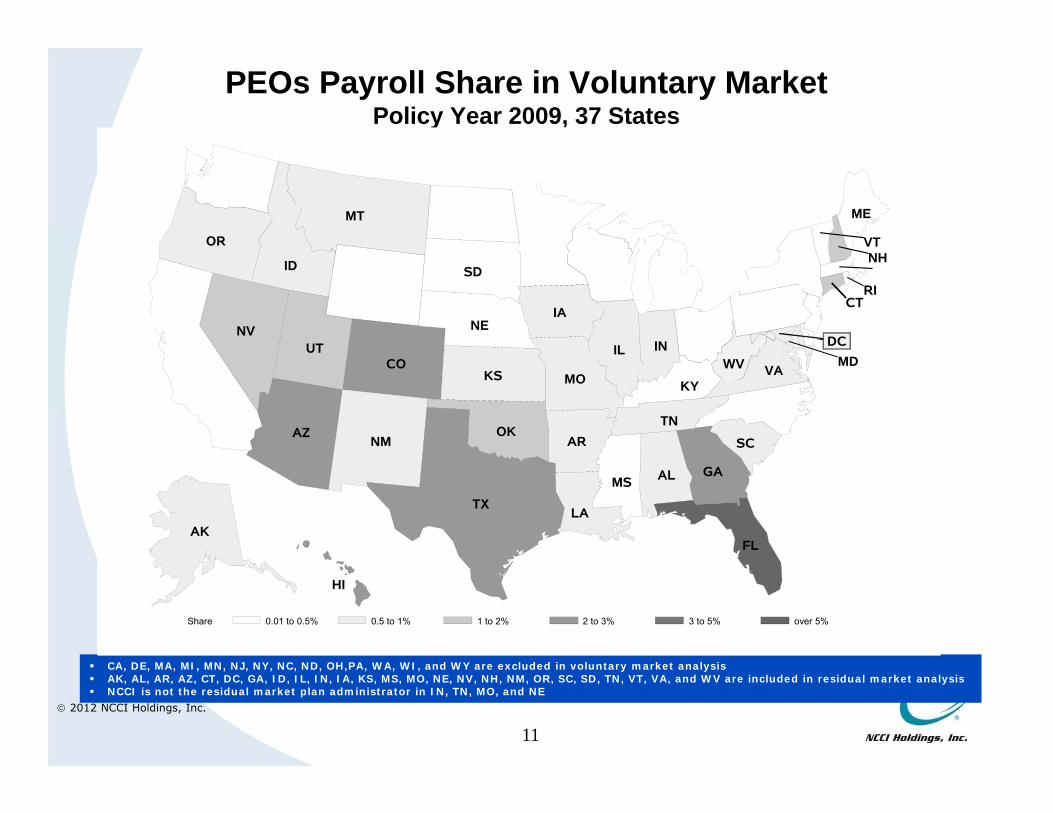

11

PEOs Payroll Share in Voluntary MarketPolicy Year 2009, 37 States

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

Share 0.01 to 0.5% 0.5 to 1% 1 to 2% 2 to 3% 3 to 5% over 5%

AL

AK

AZ AR

CO

CT

FL

GA

HI

ID

IL IN

IA

KSKY

LA

ME

MD

MS

MO

MT

NENV

NH

NMOK

OR

RI

SC

SD

TN

TX

UT

VT

VAWV

DC

2012 NCCI Holdings, Inc.

13

PEOs Payroll Share in Residual MarketPolicy Year 2009, 25 States

Share 0.01 to 0.5% 0.5 to 1% 1 to 2% 2 to 3% 3 to 5% over 5%

AL

AK

AZ AR

CT

GA

ID

IL IN

IA

KS

MS

MO

NENV

NH

NM

OR

SC

SD

TN

VT

VAWVDC

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

Workers Compensation Data Suggest thatthe PEO Market is Highly Concentrated

14

2012 NCCI Holdings, Inc.

15

National PEOs Account for the Majority PEO Activity

222.9

693.4

9.7 8.622.9

79.2

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

PEOs National PEOs

Number Workers per PEO Master Policy

Number of Workers per PEO Client

Number of Clients per PEO

Master PEO policy data is used National PEOs list was based on membership list at napeo.org in April, 2012 Source: NCCI, National Association of Professional Employer Organizations (NAPEO) ©NAPEO 2012. Used with permission.

2012 NCCI Holdings, Inc.

15 Largest PEO Companies Comprise Approximately Two Thirds Market;National PEOs Members Make up Majority of PEO Industry

Policy Year 2009 Data

48.8%

8.5%2.6%

Top 5

Next 5

Next 5

Other

PEO policy models – Master policy, MCP policies, Multiple PEO policies, and PEO direct employee policies are included National PEOs list was based on membership list at napeo.org in April, 2012 MCP policies may not have PEO information as named insured; NCCI 37 ratemaking states only Source: NCCI, National Association of Professional Employer Organizations (NAPEO) ©NAPEO 2012. Used with permission.

16

2012 NCCI Holdings, Inc.

Background on PEOs and Workers Compensation

17

2012 NCCI Holdings, Inc.

18

PEO State Regulation of PEOs:Workers Compensation

• In 1992, NCCI filed Item B-1276—Employee Leasing Arrangements to

provide rules and policy forms for employee arrangements in workers

compensation markets. Most states implemented, some states passed

modified versions, and some states have yet to implement.

• In July 2005, NCCI filed Item RM-W-8027 for residual market requiring

MCP* PEO policy model when underwriting PEO policy. Most states have

implemented.

• Overall, there is no national “NCCI rule” for underwriting policies of PEO

arrangements in the voluntary market.

MCP refers to multiple coordinated policy form; the MCP is described on the next slide

2012 NCCI Holdings, Inc.

19

PEO Policy Models• Master Policy

− A single policy that covers the leased workers of a PEO’s client companies with the

PEO as the primary insured; the client companies may be attached to the policy by

endorsement; may also cover PEO direct employees

• Multiple Coordinated Client Policies (MCP)

− A separate policy to cover the leased workers of single PEO client company with the

client as the primary insured

• Multiple PEO Policies

− A separate policy to cover the leased workers of single PEO client company with the

PEO as the primary insured making reference to the client company

2012 NCCI Holdings, Inc.

20

Recent Trends in the Voluntary Market: Multiple PEO Policy Has Been Substituting MCP for Client Policies

96.5%

97.0%

97.5%

98.0%

98.5%

99.0%

99.5%

100.0%

2004 2005 2006 2007 2008 2009

Multiple PEO PolicyMCP PolicyMaster PolicyPEO Direct Employee PolicyClient Direct Purchase PolicyNon-Leased Workers Client PolicyNon-PEO Policy

2012 NCCI Holdings, Inc.

21

Recent Trends in the Residual Market: Master Policy Share Has Declined Since 2005

88.0%

90.0%

92.0%

94.0%

96.0%

98.0%

100.0%

2004 2005 2006 2007 2008 2009

Multiple PEO PolicyMCP PolicyMaster PolicyPEO Direct Employee PolicyClient Direct Purchase PolicyNon-Leased Workers Client PolicyNon-PEO Policy

2012 NCCI Holdings, Inc.

22

Comparing PEO WC PoliciesIn All Cases

PEO Clients Appear to be Small Businesses

222.9

6.7 9.219.4

9.722.9

0.0

50.0

100.0

150.0

200.0

250.0

Master PEO Policy MCP Client Policy Multiple PEO Policy Non-PEO Policies

Average # Workers per Policy

Average # of Workers per Client

Average # of Clients per PEO

2012 NCCI Holdings, Inc.

In the Voluntary Market in 2009Most PEO Leased Workers Are Covered Under Master Policies

37 NCCI Ratemaking States

Master PEO Policy80.7%

Multiple PEO Policy13.7%

MCP Client Policy4.0%

PEO Direct Employee Policy1.5%

23

2012 NCCI Holdings, Inc.

25

In the Residual Market in 2009Many More Workers Are Covered Under MCP or Multiple PEO Policies

25 NCCI Ratemaking States

Master PEO Policy49.7%

Multiple PEO Policy18.7%

MCP Client Policy28.2%

PEO Direct Employee Policy3.5%

2012 NCCI Holdings, Inc.

26

Wide Variation Across States in the Voluntary MarketPEO Payroll Share by Policy Type

2009 Policy Year

VOL

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

09FL

42TX

02AZ

05CO

52HI

10GA

VOL 27NV

43UT

35OK

06CT

28NH

47WV

12IL

01AL

41TN

39SC

24MO

45VA

03AR

08DC

25MT

19MD

54AK

30NM

15KS

36OR

17LA

11ID

13IN

14IA

26NE

18ME

16KY

38RI

23MS

40SD

44VT

PEO Direct Employee Policy Master Policy MCP Client Policy Multiple PEO Policy

2012 NCCI Holdings, Inc.

28

RES

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

02AZ

01AL

27NV

12IL

28NH

14IA

36OR

23MS

30NM

10GA

RES 13IN

24MO

45VA

03AR

26NE

11ID

39SC

15KS

41TN

08DC

40SD

06CT

44VT

47WV

54AK

PEO Direct Employee Policy Master Policy MCP Client Policy Multiple PEO Policy

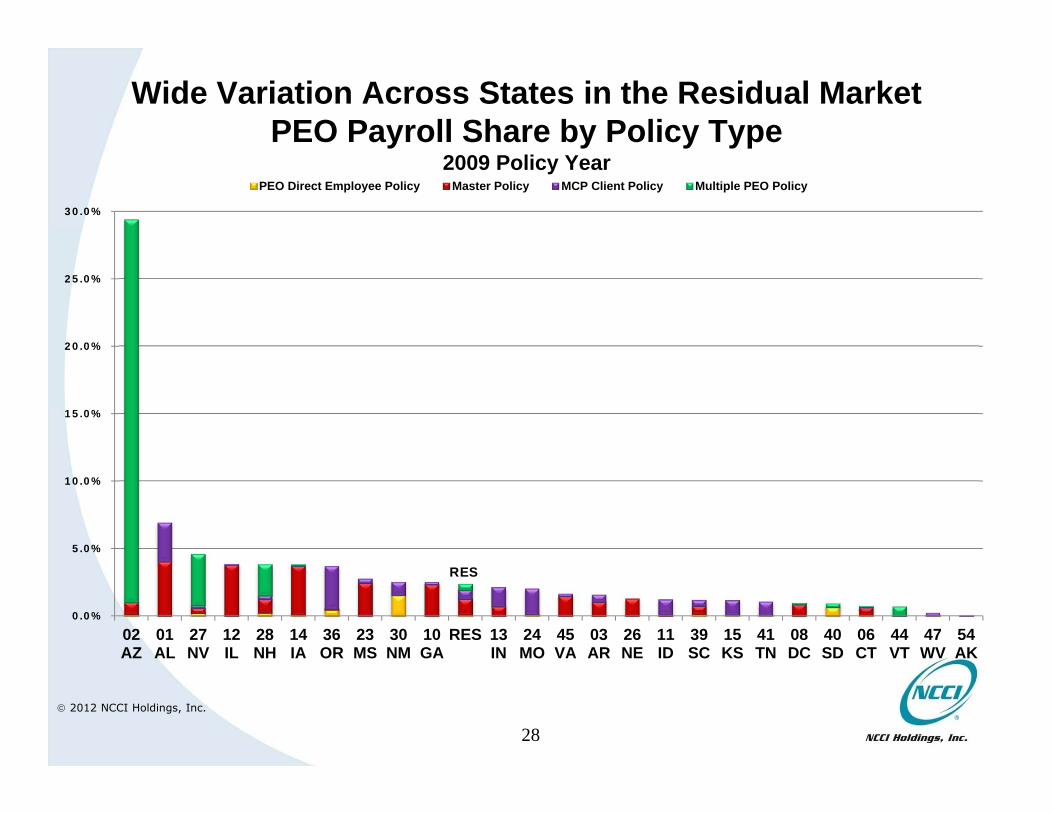

Wide Variation Across States in the Residual MarketPEO Payroll Share by Policy Type

2009 Policy Year

2012 NCCI Holdings, Inc.

29

Implications of PEOs for Workers Compensation Ratemaking

2012 NCCI Holdings, Inc.

30

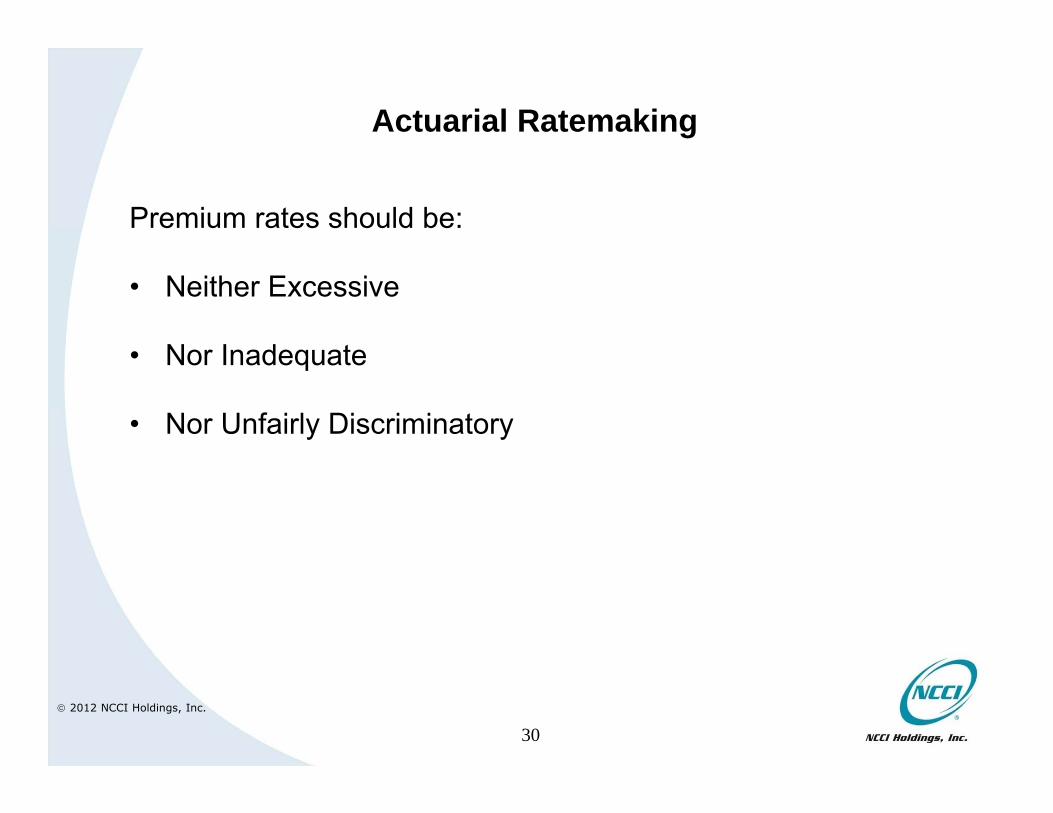

Actuarial Ratemaking

Premium rates should be:

• Neither Excessive

• Nor Inadequate

• Nor Unfairly Discriminatory

2012 NCCI Holdings, Inc.

31

Actuarial Ratemaking

Aggregate Ratemaking:

• Neither Excessive

• Nor Inadequate

Requires Aggregated State Level Data

• Financial Call Data

2012 NCCI Holdings, Inc.

32

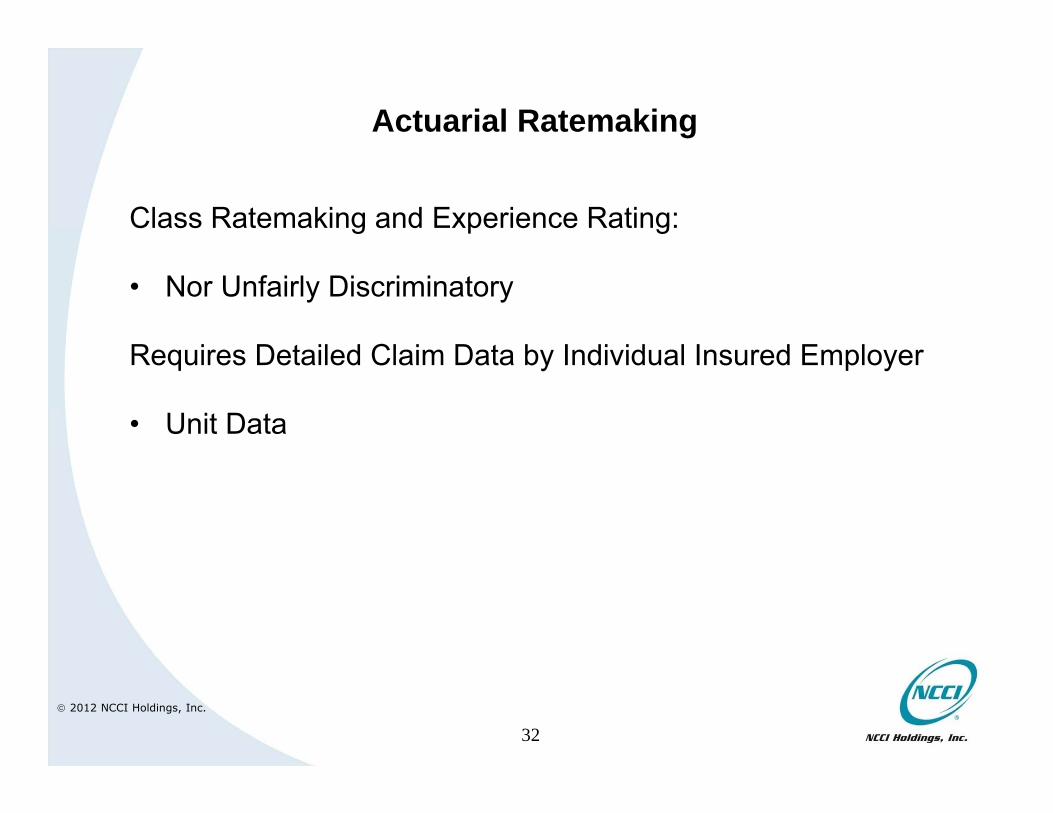

Actuarial Ratemaking

Class Ratemaking and Experience Rating:

• Nor Unfairly Discriminatory

Requires Detailed Claim Data by Individual Insured Employer

• Unit Data

2012 NCCI Holdings, Inc.

33

Potential Ratemaking Concerns Related to PEOsHow These Compare with Concerns in BLS Data

• Incorrectly Classified Payroll

[BLS – inaccurate counts of employment by occupation]

• Underreporting of Claims

[BLS SOII – Underreporting of injuries]

• Bulk Reporting of Claim Experience

[BLS SOII – Inability to Estimate Injury Rates by

Occupation/Industry]

• Difficulty in tracking the experience rating modification

2012 NCCI Holdings, Inc.

Does PEO Claim Experience Differ Materially from Non-PEO Experience?

34

2012 NCCI Holdings, Inc.

Market Segments• Voluntary market analysis includes 37 NCCI ratemaking states

• Residual market analysis includes 25 NCCI ratemaking states:

− 21 NCCI Plan states

− IN, TN, MO, and NE where NCCI is not the Plan Administrator

• “PEOs” in our data analysis refers to workers covered in PEO:− Master policy− MCP policies− Multiple PEO policies− PEO direct employees

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

35

2012 NCCI Holdings, Inc.

36

Workers Compensation Data at the Policy Level

Policy data:

• Proof of Coverage (POC) compliance reports issued at policy

inception

• Provides information on the type of policy including PEOs

Unit data:

• Unit reports used for class ratemaking

• Contains detail on

– payroll by class (typically a blend of occupation and industry) plus

– detail on individual claims

2012 NCCI Holdings, Inc.

37

Data Used in This Analysis

• NCCI policy and unit data in policy years 2004–2010

• Industry group level data in policy year 2007

• Losses are evaluated at 2nd report

• PEO policy type is as reported in the policy data

2012 NCCI Holdings, Inc.

PEO Loss Experience in Workers Compensation

2012 NCCI Holdings, Inc.

38

Loss Experience for 2004-2009: PEOs versus Non-PEO Policies

2012 NCCI Holdings, Inc.

39

Key Measures of Workers Compensation Loss Experience

EstimatedNumberofWorkersinThousands PayrollAWW ∗ 52 ∗ 1000LostTimeClaimsFrequency NumberofLostTimeClaimsNumberofWorkersinThousandsLostTimeClaimsSeverity IncurredLossesonLostTimeClaimsNumberofLostTimeClaimsLostTimeClaimsLossRatio IncurredLossesonLostTimeClaimsManualorModifiedPremium

2012 NCCI Holdings, Inc.

Loss Experience for 2004-2009: PEOs versus Non-PEO Policies

Frequency in the Voluntary Market

40

2012 NCCI Holdings, Inc.

42

In the Voluntary MarketFrequency Is Higher for PEOs than for Non-PEOS

Voluntary Market, 2004-2009, @2nd Report

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Fr

eque

ncy

per 1

000

Wor

kers

Policy Year

Non-PEO Large Deductible Non-PEO Other than Large DeductiblePEOs Large Deductible PEOs Other than Large Deductible

2012 NCCI Holdings, Inc.

43

Loss Experience for 2004-2009: PEOs versus Non-PEO Policies

Voluntary Market – Large Deductible(Typically Master Policies for PEOs, Larger

Employers for Non-PEOs)

2012 NCCI Holdings, Inc.

44

In the Voluntary Market Frequency Has DeclinedBut PEOs Higher than Non-PEOs

Large Deductible Policies(Typically Master Policies for PEOs; Larger Employers for Non-PEOs)

2004-2009, @2nd Report

10.39.7

9.2 8.98.1 7.8

16.315.7

14.1

11.110.4

9.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Fr

eque

ncy

per 1

000

Wor

kers

Policy Year

Lost Time Claims Frequency per 1000 WorkersNon-PEOs PEOs

2012 NCCI Holdings, Inc.

45

In the Voluntary Market Severity Trends for PEOs and Non-PEOs Are Comparable

Large Deductible Policies(Typically Master Policies for PEOs; Larger Employers for Non-PEOs)

2004-2009, @2nd Report

27.2 27.629.1

31.3

34.132.0

23.0

26.9 27.5

34.235.4

30.7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Se

verit

yin

Tho

usan

ds

Policy Year

Lost Time Claims Severity in ThousandsNon-PEOs PEOs

2012 NCCI Holdings, Inc.

46

In the Voluntary Market Manual Premium Loss Ratios for PEOs Have Increased Relative to Non-PEOs

Large Deductible Policies(Typically Master Policies for PEOs; Larger Employers for Non-PEOs)

2004-2009, @2nd Report

0.30

0.28 0.280.30

0.32 0.32

0.24

0.28 0.29

0.31

0.37

0.41

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

anua

l Pre

miu

m

Policy Year

Lost Time Claims Loss Ratio – Manual PremiumNon-PEOs PEOs

2012 NCCI Holdings, Inc.

47

In the Voluntary Market Modified Premium Loss Ratios for PEOs Have Been Lower than for Non-PEOs

Large Deductible Policies(Typically Master Policies for PEOs; Larger Employers for Non-PEOs)

2004-2009, @2nd Report

0.330.32

0.33

0.360.39

0.38

0.250.27

0.29

0.34

0.39

0.43

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

odifi

ed P

rem

ium

Policy Year

Lost Time Claims Loss Ratio – Modified PremiumNon-PEOs PEOs

2012 NCCI Holdings, Inc.

48

Loss Experience for 2004-2009: PEOs versus Standard Policies

Voluntary Market – Other than Large Deductible Policies

Typically Smaller Employers

2012 NCCI Holdings, Inc.

49

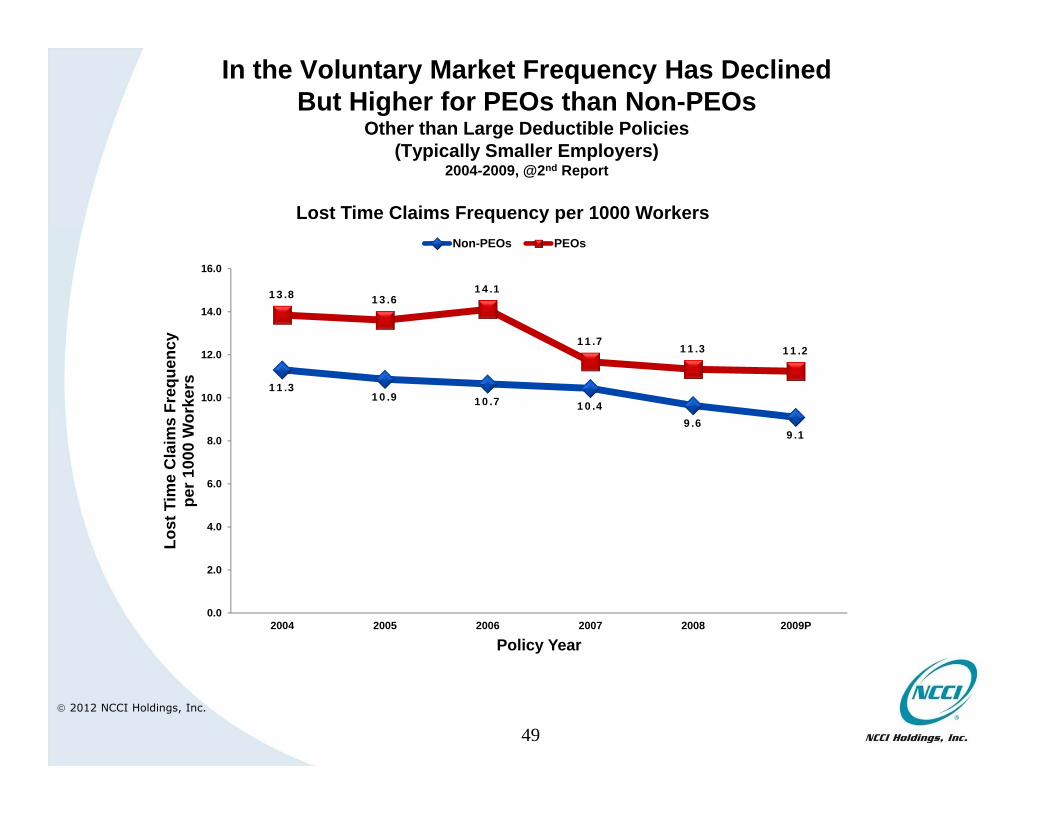

In the Voluntary Market Frequency Has DeclinedBut Higher for PEOs than Non-PEOs

Other than Large Deductible Policies(Typically Smaller Employers)

2004-2009, @2nd Report

11.310.9 10.7 10.4

9.69.1

13.8 13.614.1

11.711.3 11.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Fr

eque

ncy

per 1

000

Wor

kers

Policy Year

Lost Time Claims Frequency per 1000 WorkersNon-PEOs PEOs

2012 NCCI Holdings, Inc.

50

In the Voluntary Market Severity Trends Are Comparable But Severity Lower for PEOs than Non-PEOs

Other than Large Deductible Policies(Typically Smaller Employers)

2004-2009, @2nd Report

29.430.7

32.534.3

37.236.2

26.2

29.430.4

28.1

32.533.4

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Se

verit

yin

Tho

usan

ds

Policy Year

Lost Time Claims Severity in ThousandsNon-PEOs PEOs

2012 NCCI Holdings, Inc.

51

In the Voluntary Market Manual Premium Loss Ratio Trends Are Comparable for PEOs and Non-PEOs

Other than Large Deductible Policies(Typically Smaller Employers)

2004-2009, @2nd Report

0.34

0.33 0.34

0.36

0.39

0.39

0.32

0.34 0.35

0.29

0.36

0.42

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

anua

l Pre

miu

m

Policy Year

Lost Time Claims Loss Ratio – Manual PremiumNon-PEOs PEOs

2012 NCCI Holdings, Inc.

52

In the Voluntary Market Modified Premium Loss Ratio Trends Are Comparable for PEOs and Non-PEOs

Other than Large Deductible Policies(Typically Smaller Employers)

2004-2009, @2nd Report

0.36

0.35 0.35

0.38

0.41

0.41

0.32

0.36 0.36

0.31

0.38

0.43

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

odifi

ed P

rem

ium

Policy Year

Lost Time Claims Loss Ratio – Modified PremiumNon-PEO PEOs

2012 NCCI Holdings, Inc.

53

Loss Experience for 2004-2009: PEOs versus Standard Policies

Residual Market

2012 NCCI Holdings, Inc.

54

In the Residual Market Frequency Has Been Higher for PEOs than for Non-PEOs

Both Exhibit Slight Downtrends2004-2009, @2nd Report

22.3 21.9 21.9 21.620.0 20.1

30.5

28.026.7

29.0

25.727.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Fr

eque

ncy

per 1

000

Wor

kers

Policy Year

Lost Time Claims Frequency per 1000 WorkersNon-PEOs PEOs

2012 NCCI Holdings, Inc.

55

In the Residual Market Severity Has Been Higher for Non-PEOs than for PEOs

Both Exhibit a Marked Uptrend*

2004-2009, @2nd Report

36.1

40.8

44.8

52.8

56.0

46.1

23.7

27.8 27.929.2

42.7

34.7

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Se

verit

yin

Tho

usan

ds

Policy Year

Lost Time Claims Severity in ThousandsNon-PEOs PEOs

The data for 2009 is preliminary and reflects the impact of the recession on the results of that policy year

2012 NCCI Holdings, Inc.

56

In the Residual Market Manual Premium Loss Ratios Often Have Been Lower for PEOs than for Non-PEOs

2004-2009, @2nd Report

0.55 0.56 0.57

0.66

0.68

0.60

0.520.49 0.50

0.54

0.74

0.63

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

anua

l Pre

miu

m

Policy Year

Lost Time Claims Loss Ratio – Manual PremiumNon-PEOs PEOs

2012 NCCI Holdings, Inc.

57

In the Residual Market Modified Premium Loss Ratios Often Have Been Lower for PEOs than for Non-PEOs

2004-2009, @2nd Report

0.52 0.53 0.55

0.64

0.66

0.58

0.490.47 0.48

0.50

0.69

0.59

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

2004 2005 2006 2007 2008 2009P

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

odifi

ed P

rem

ium

Policy Year

Lost Time Claims Loss Ratio – Modified PremiumNon-PEO PEOs

2012 NCCI Holdings, Inc.

58

Loss Experience for 2007 by Industry Group: PEO versus Non-PEO Policies

Voluntary Market

2012 NCCI Holdings, Inc.

59

In the Voluntary Market in 2007 Most PEO Leased Workers Were Covered Under Master Policies

Master PEO Policy75.3%

Multiple PEO Policy11.6%

MCP Client Policy12.4%

PEO Direct Employee Policy0.7%

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

60

In the Voluntary Market PEO Mix of Clients Comparable to Non-PEO Mix

Share of Insured Payroll by Industry GroupVoluntary Market , Policy Year 2007, @2nd Report

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Shar

e of

Pay

roll

PEOs Non-PEOs

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

61

In the Voluntary Market Lost-Time Claims Frequency by Industry GroupPEO Frequency Higher for Most Industry Groups

Voluntary Market , Policy Year 2007, @2nd Report

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Fr

eque

ncy

per 1

000

Wor

kers

PEOs Non-PEOs

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

62

In the Voluntary MarketLost-Time Claims Severity by Industry Group

PEO Severity Higher for MiscellaneousVoluntary Market , Policy Year 2007, @2nd Report

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Se

verit

yin

Tho

usan

ds

PEOs Non-PEOs

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

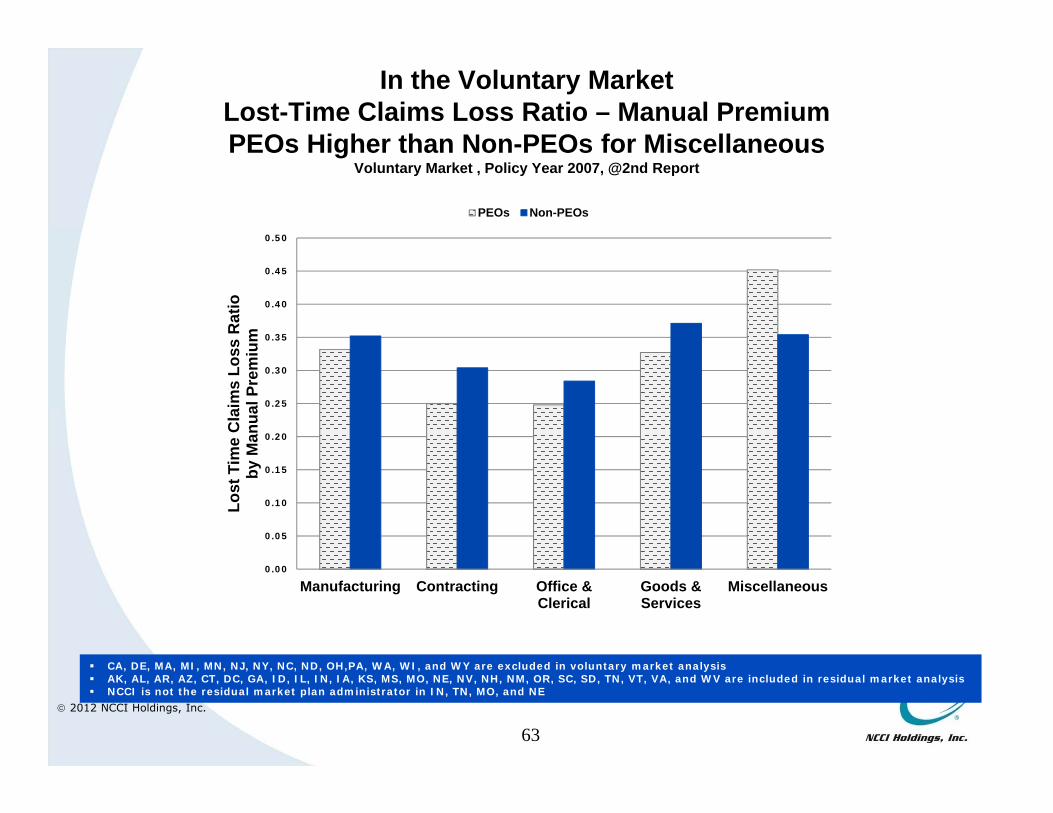

63

In the Voluntary MarketLost-Time Claims Loss Ratio – Manual PremiumPEOs Higher than Non-PEOs for Miscellaneous

Voluntary Market , Policy Year 2007, @2nd Report

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

anua

l Pre

miu

m

PEOs Non-PEOs

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

64

In the Voluntary MarketLost-Time Claims Loss Ratio – Modified PremiumPEOs Higher than Non-PEOs for Miscellaneous

Voluntary Market , Policy Year 2007, @2nd Report

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

odifi

ed P

rem

ium

PEOs Non-PEO

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

65

PEO Lost-Time Claims Indemnity Severity by Industry GroupVoluntary Market , Policy Year 2007, @2nd Report

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s In

dem

nity

Sev

erity

in T

hous

ands

PEOs Non-PEO

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

66

PEO Lost-Time Claims Medical Severity by Industry GroupVoluntary Market , Policy Year 2007, @2nd Report

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s M

edic

al S

ever

ityin

Tho

usan

ds

PEOs Non-PEO

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

67

Loss Experience for 2007 by Industry Group: PEO versus Non-PEO Policies

Residual Market

2012 NCCI Holdings, Inc.

68

In the Residual Market in 2007 Most Leased Workers Were Still Covered Under Master Policies

Master PEO Policy70.4%

Multiple PEO Policy7.3%

MCP Client Policy17.8%

PEO Direct Employee Policy4.4%

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

69

In the Residual MarketPEOs Are Especially Prominent in Manufacturing

Share of PayrollPolicy Year 2007, @2nd Report

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Shar

e of

Pay

roll

PEOs Non-PEOs

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

70

In the Residual MarketPEO Frequency Higher than for Non-PEOs

Policy Year 2007, @2nd Report

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Fr

eque

ncy

per 1

000

Wor

kers

PEOs Non-PEOs

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

71

In the Residual MarketSeverity Was Lower for PEOs in All But Miscellaneous

Policy Year 2007, @2nd Report

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Se

verit

yin

Tho

usan

ds

PEOs Non-PEOs

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

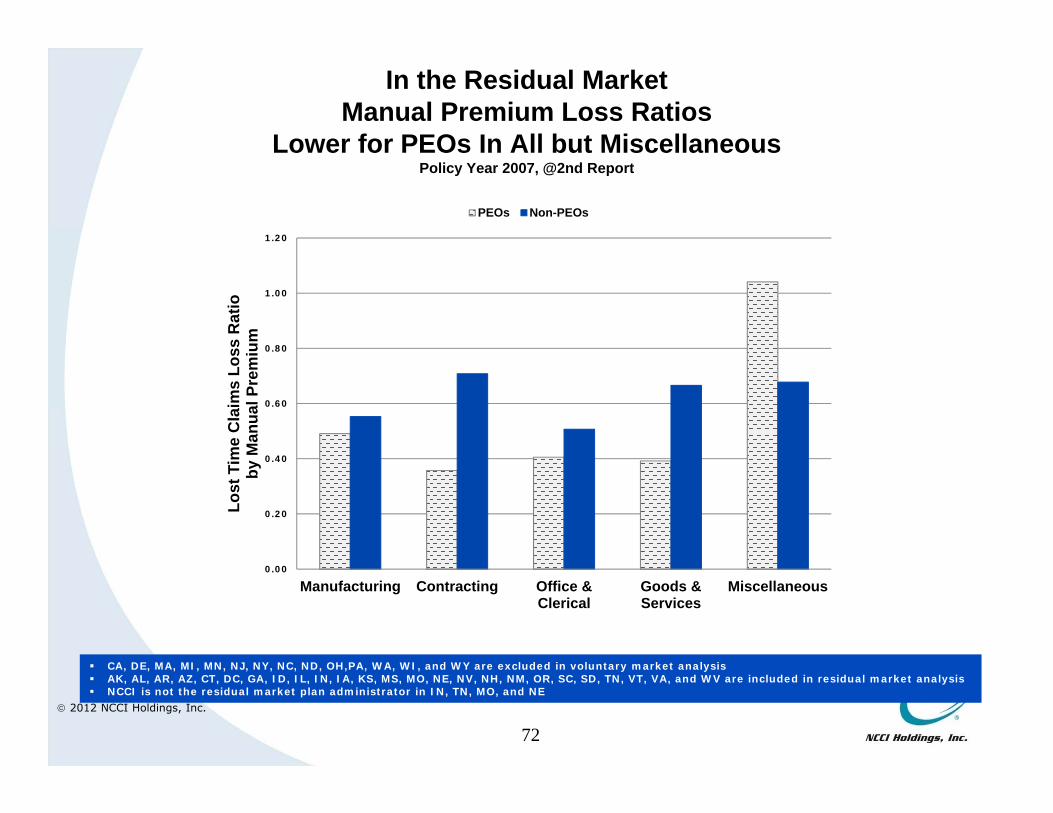

72

In the Residual MarketManual Premium Loss Ratios

Lower for PEOs In All but MiscellaneousPolicy Year 2007, @2nd Report

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

anua

l Pre

miu

m

PEOs Non-PEOs

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

73

In the Residual MarketModified Premium Loss Ratios

Lower for PEOs In All but MiscellaneousPolicy Year 2007, @2nd Report

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

odifi

ed P

rem

ium

PEOs Non-PEO

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

74

PEO Lost-Time Claims Indemnity Severity by Industry GroupResidual Market, Policy Year 2007, @2nd Report

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s In

dem

nity

Sev

erity

in T

hous

ands

PEOs Non-PEO

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

75

PEO Lost-Time Claims Medical Severity by Industry GroupResidual Market, Policy Year 2007, @2nd Report

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s M

edic

al S

ever

ityin

Tho

usan

ds

PEOs Non-PEO

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

Adverse PEO Experience in Miscellaneous Group

May Reflect Classes Of Employers Insured

76

2012 NCCI Holdings, Inc.

Industry Group Top Governing Class Code by Number of Unit Reports Description

Manufacturing 3632 MACHINE SHOP NOC

9521 HOUSE FURNISHINGS INSTALLATION NOC & UPHOLSTERING

4299 PRINTING

4484 PLASTICS MANUFACTURING: MOLDED PRODUCTS NOC

3681 TELEVISION, RADIO, TELEPHONE OR TELECOMMUNICATION DEVICE MFG. NOC

Contracting 5190 ELECTRICAL WIRING-WITHIN BUILDINGS & DRIVERS

3724 MACHINERY OR EQUIPMENT ERECTION OR REPAIR NOC & DRIVERS

5606 CONTRACTOR-EXECUTIVE SUPERVISOR OR CONSTRUCTION SUPERINTENDENT 1

5183 PLUMBING NOC & DRIVERS

5645 CARPENTRY-DETACHED ONE OR TWO FAMILY DWELLINGS

Office and Clerical 8810 CLERICAL OFFICE EMPLOYEES NOC

8742 SALESPERSONS, COLLECTORS OR MESSENGERS-OUTSIDE

8832 PHYSICIAN & CLERICAL

8833 HOSPITAL: PROFESSIONAL EMPLOYEES

8601 ARCHITECT OR ENGINEER- CONSULTING

Goods and Services 8017 STORE: RETAIL NOC

9015 BUILDINGS-OPERATION BY OWNER OR LESSEE

9014 BUILDINGS-OPERATION BY CONTRACTORS

8018 STORE: WHOLESALE NOC

9082 RESTAURANT NOC/CATERER

Miscellaneous 7229 TRUCKING-LONG DISTANCE HAULING-& DRIVERS

7228 TRUCKING-LOCAL HAULING ONLY-& DRIVERS

9102 PARK NOC-ALL EMPLOYEES & DRIVERS7219 TRUCKING: NOC-ALL EMPLOYEES & DRIVERS

7720 POLICE OFFICERS & DRIVERS

F-Class 6824 BOAT BUILDING OR REPAIR & DRIVERS

6826 MARINA & DRIVERS

6872 SHIP REPAIR CONVERSION-ALL OPERATIONS & DRIVERS

8709 STEVEDORING: TALLIERS AND CHECKING CLERKS ENGAGED IN CONNECTION WITH STEVE- DORE WORK

6843 SHIP BUILDING-IRON OR STEEL-NOC & DRIVERS

High Risk Classes Are Prominent PEO Miscellaneous Clients

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded Policy years 2004-2010 77

2012 NCCI Holdings, Inc.

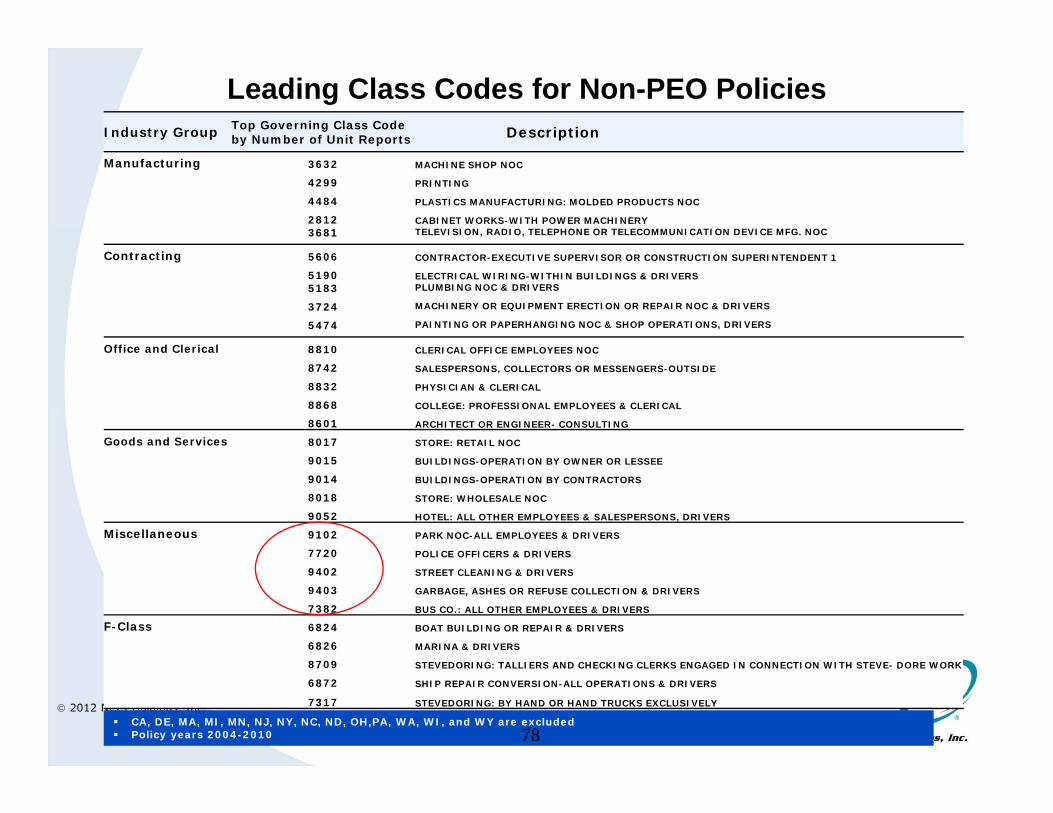

Leading Class Codes for Non-PEO PoliciesIndustry Group Top Governing Class Code

by Number of Unit Reports Description

Manufacturing 3632 MACHINE SHOP NOC

4299 PRINTING

4484 PLASTICS MANUFACTURING: MOLDED PRODUCTS NOC

2812 CABINET WORKS-WITH POWER MACHINERY3681 TELEVISION, RADIO, TELEPHONE OR TELECOMMUNICATION DEVICE MFG. NOC

Contracting 5606 CONTRACTOR-EXECUTIVE SUPERVISOR OR CONSTRUCTION SUPERINTENDENT 1

5190 ELECTRICAL WIRING-WITHIN BUILDINGS & DRIVERS5183 PLUMBING NOC & DRIVERS

3724 MACHINERY OR EQUIPMENT ERECTION OR REPAIR NOC & DRIVERS

5474 PAINTING OR PAPERHANGING NOC & SHOP OPERATIONS, DRIVERS

Office and Clerical 8810 CLERICAL OFFICE EMPLOYEES NOC

8742 SALESPERSONS, COLLECTORS OR MESSENGERS-OUTSIDE

8832 PHYSICIAN & CLERICAL

8868 COLLEGE: PROFESSIONAL EMPLOYEES & CLERICAL

8601 ARCHITECT OR ENGINEER- CONSULTING

Goods and Services 8017 STORE: RETAIL NOC

9015 BUILDINGS-OPERATION BY OWNER OR LESSEE

9014 BUILDINGS-OPERATION BY CONTRACTORS

8018 STORE: WHOLESALE NOC

9052 HOTEL: ALL OTHER EMPLOYEES & SALESPERSONS, DRIVERS

Miscellaneous 9102 PARK NOC-ALL EMPLOYEES & DRIVERS

7720 POLICE OFFICERS & DRIVERS

9402 STREET CLEANING & DRIVERS

9403 GARBAGE, ASHES OR REFUSE COLLECTION & DRIVERS

7382 BUS CO.: ALL OTHER EMPLOYEES & DRIVERS

F-Class 6824 BOAT BUILDING OR REPAIR & DRIVERS

6826 MARINA & DRIVERS

8709 STEVEDORING: TALLIERS AND CHECKING CLERKS ENGAGED IN CONNECTION WITH STEVE- DORE WORK

6872 SHIP REPAIR CONVERSION-ALL OPERATIONS & DRIVERS

7317 STEVEDORING: BY HAND OR HAND TRUCKS EXCLUSIVELY

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded Policy years 2004-2010 78

2012 NCCI Holdings, Inc.

79

Modified Loss Ratios for 2007 by Industry Group: PEO versus Non-PEO Policies

Residual and Voluntary Markets

Loss Ratios Higher in Residual Market: PEOs and Non-PEOsLoss Ratios Moderately Higher in Residual Market: PEOs

Loss Ratios Materially Greater in Residual Market: Non-PEOs

2012 NCCI Holdings, Inc.

80

In the Voluntary MarketLost-Time Claims Loss Ratio – Modified PremiumPEOs Higher than Non-PEOs for Miscellaneous

Voluntary Market , Policy Year 2007, @2nd Report

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

odifi

ed P

rem

ium

PEOs Non-PEO

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

81

In the Residual MarketModified Premium Loss Ratios

Lower for PEOs In All but MiscellaneousPolicy Year 2007, @2nd Report

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Manufacturing Contracting Office &Clerical

Goods &Services

Miscellaneous

Lost

Tim

e C

laim

s Lo

ss R

atio

by M

odifi

ed P

rem

ium

PEOs Non-PEO

CA, DE, MA, MI, MN, NJ, NY, NC, ND, OH,PA, WA, WI, and WY are excluded in voluntary market analysis AK, AL, AR, AZ, CT, DC, GA, ID, IL, IN, IA, KS, MS, MO, NE, NV, NH, NM, OR, SC, SD, TN, VT, VA, and WV are included in residual market analysis NCCI is not the residual market plan administrator in IN, TN, MO, and NE

2012 NCCI Holdings, Inc.

Observations

2012 NCCI Holdings, Inc.

Observations

• Regulation of PEOs has increased steadily over the past 20 years

• Across all NCCI states in total, PEOs account for a relatively small share of all workers covered by workers compensation

• PEOs are responsible for a material portion of employment in some states; especially in residual markets

• Reported frequency is typically higher for PEO policies suggesting that there is no compelling evidence that PEOs underreport claims

• Comparable loss ratios for PEO and Non-PEO policies suggests that there is no compelling evidence of inappropriate reporting of payroll and premium

89

2012 NCCI Holdings, Inc.

Comments Or Questions?