Product Development in - Institute of National Affairs product development-Madhu Moulik.pdf ·...

39

Product Development in Emerging Markets Institute of National Affairs 8th August, 2012

Transcript of Product Development in - Institute of National Affairs product development-Madhu Moulik.pdf ·...

Product Development in Emerging Markets

Institute of National Affairs8th August, 2012

• “A world in which all people have access to high-quality, affordable, market-led financial services.”

Our Inspiration

• “Strengthening the capacity of financial service providers to deliver market-led financial solutions.”

OurMission

About MicroSave

Innovations• Savings

product design • Electronic and

mobile banking

• Value-chain design – silk, fisheries, retail

• Microfinance plus programmes

Implementation• Business

planning• Market research

and product development

• Process mapping and risk management

• Customer service and branding

Our Approach Focuses on

MicroSaveMarket-led solutions for financial services

Innovations• Savings

product design • Electronic and

mobile banking

• Value-chain design – silk, fisheries, retail

• Microfinance plus programmes

Implementation• Business

planning• Market research

and product development

• Process mapping and risk management

• Customer service and branding

Our Areas of Expertise

Product and Channel

Innovation

Product and Channel

Innovation

OrganisationalStrengthening

and Risk Management

OrganisationalStrengthening

and Risk Management

Research andDisseminationResearch andDissemination

Training andWorkshops

Training andWorkshops

Electronic and Mobile Banking

Solutions

Electronic and Mobile Banking

Solutions

MicroSaveMarket-led solutions for financial services

MicroSave’sAreas of

Expertise

MicroSave’sAreas of

Expertise

Strategy Development

and Governance

Strategy Development

and Governance

Investment andDonor ServicesInvestment andDonor Services

We have implemented projects across Africa, Asia and Latin America including:Afghanistan, Bangladesh, Cambodia, Colombia, Democratic Republic of the Congo,

Egypt, Ethiopia, Ghana, India, Indonesia, Kenya, Malawi, Nepal, Nigeria, Papua New Guinea, the Philippines, Sierra Leone, South Africa, Sri Lanka, Tanzania, Uganda, and

Zambia.

Years of experience

Worked with wide variety of institutionsExperience

Knowledge

Talented consultants

Practical solutions

Unique tools

4

5

3

2

1

Examples

30+ toolkits being used extensively

We Create Value Through

100+ staff

150+ clients in Asia and Africa

2 decades of experience of BOEP market

NGOs, MFIs, Banks, Corporates

MicroSaveMarket-led solutions for financial services

Worked with wide variety of institutionsExperience

Strategy

Impact

Create strategic opportunities

Align strategies with organization and cultureHelped financial institutions achieve very significant growth

Managed institutions attain sustainability

6

7

8

9

10

Experienced working with myriad strategic issues and business drivers

NGOs, MFIs, Banks, Corporates

Innovation to implementation

E and M Banking, Value chain financing

Practical implementable recommendations

Equity Bank, Eko, OK Bank

Increased revenues and decreased costs

MicroSaveMarket-led solutions for financial services

MicroSaveMarket-led solutions for financial services

Level 5, Pacific Place, Email: [email protected]. Musgrave St. & Champion Pde. Port Moresby, NCD, Papua New Guinea Website: http://www.MicroSave.net

Product Development in Emerging Markets

MicroSaveMarket-led solutions for financial services

Institute of National Affairs8th August, 2012

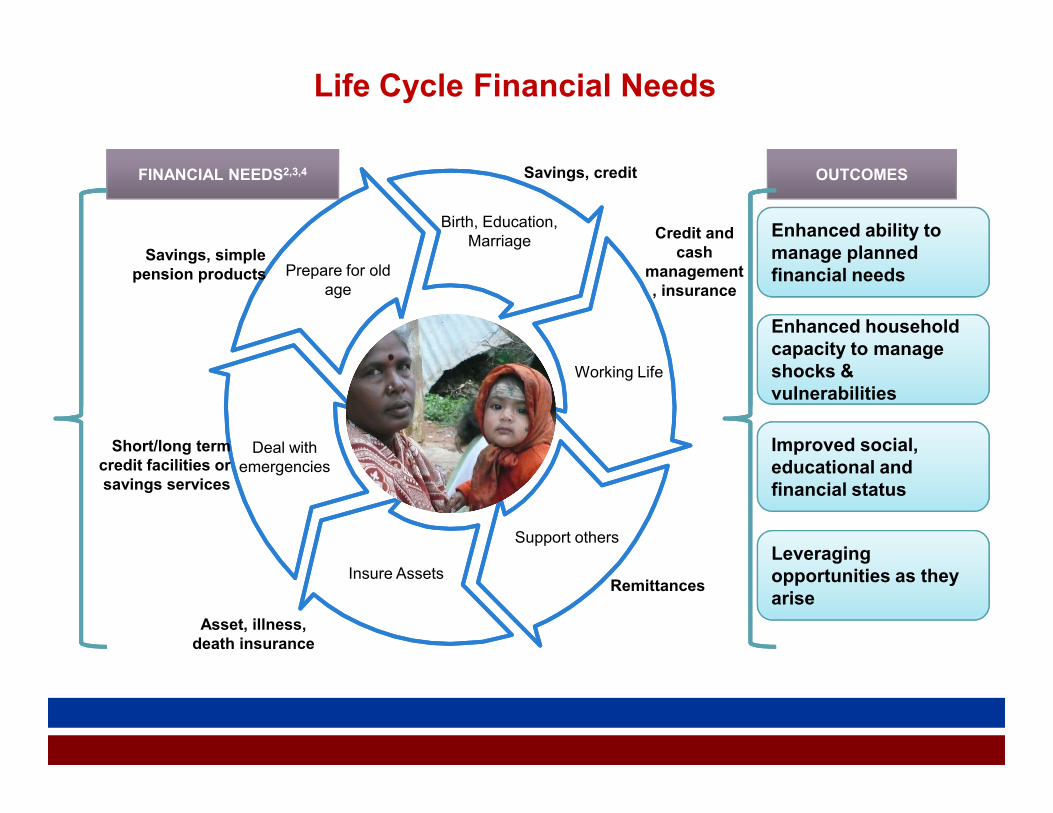

Life Cycle Financial Needs

Birth, Education, Marriage

Working Life

Prepare for old age

Savings, simple pension products

Savings, credit

Credit and cash

management, insurance

Enhanced ability to manage planned financial needs

Enhanced ability to manage planned financial needs

Enhanced household capacity to manage shocks & vulnerabilities

Enhanced household capacity to manage shocks & vulnerabilities

FINANCIAL NEEDS2,3,4FINANCIAL NEEDS2,3,4 OUTCOMESOUTCOMES

Support others

Insure Assets

Deal with emergencies

Short/long term credit facilities or savings services

Asset, illness, death insurance

Remittances

Improved social, educational and financial status

Improved social, educational and financial status

Leveraging opportunities as they arise

Leveraging opportunities as they arise

3 Needs That Drive Financial Activity

Managing basics:Cash-flow management to transform irregular income flows into a dependable resource to meet daily needs

Coping with risk: Dealing with the emergencies that can derail families with little in reserve

Raising lump sums: Seizing opportunities and paying for big-ticket expenses by accumulating usefully large sums of money

Managing basics:Cash-flow management to transform irregular income flows into a dependable resource to meet daily needs

Coping with risk: Dealing with the emergencies that can derail families with little in reserve

Raising lump sums: Seizing opportunities and paying for big-ticket expenses by accumulating usefully large sums of money

http://www.microsave.org/popbn From: “Portfolios of the Poor”

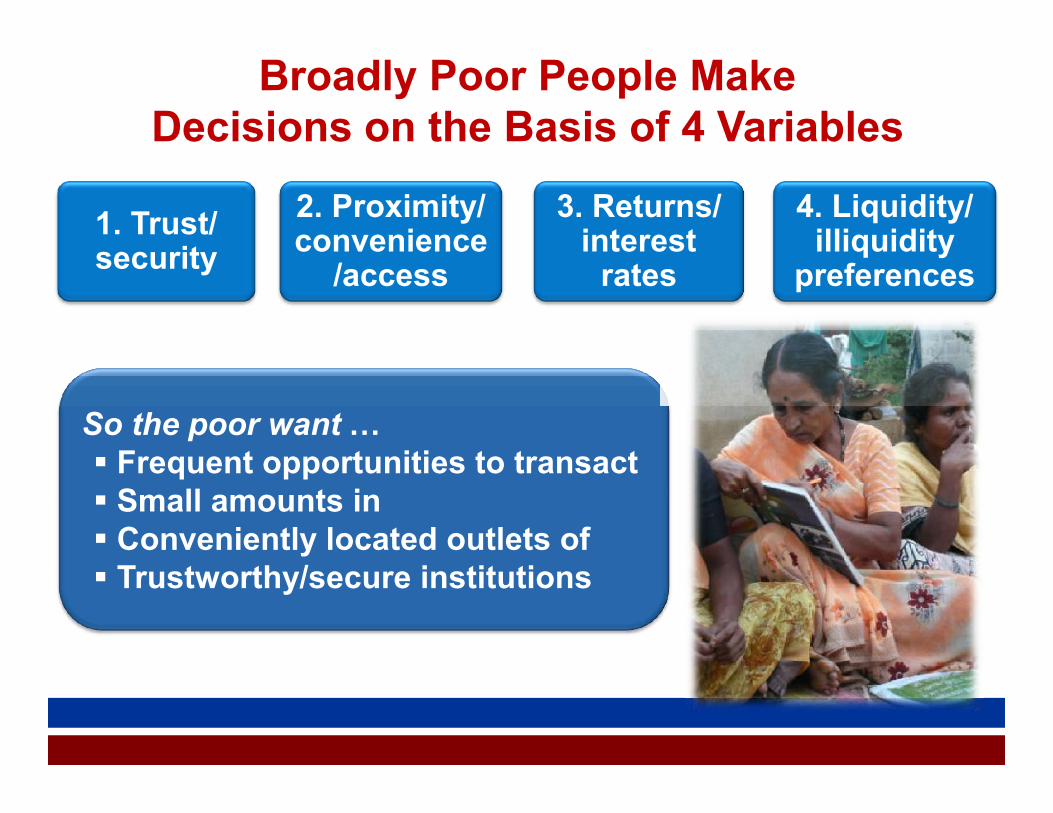

Broadly Poor People Make Decisions on the Basis of 4 Variables

1. Trust/ security

2. Proximity/ convenience

/access

3. Returns/ interest

rates

4. Liquidity/ illiquidity

preferences

So the poor want … Frequent opportunities to transact Small amounts in Conveniently located outlets of Trustworthy/secure institutions

So the poor want … Frequent opportunities to transact Small amounts in Conveniently located outlets of Trustworthy/secure institutions

Karim, a Taxi Driver (Bangladesh)Karim is from Gaibanda. He shifted to Dhaka 12 years back in search for income and has been running a taxi since. You can often find him at the Motijheel Taxi stand with a yellow Navana Taxi.

His wife joined him in Dhaka 8 years back.

His daughter and two sons continue to live in the village with Karim’s parents. They go to the village school.

We found Karim Bhai to be very keen to save from his daily income, through all possible options. So this is how he manages his finances!

His wife joined him in Dhaka 8 years back.

His daughter and two sons continue to live in the village with Karim’s parents. They go to the village school.

We found Karim Bhai to be very keen to save from his daily income, through all possible options. So this is how he manages his finances!

Karim’s Daily Cashflows

On a typical day, Karim Bhai after driving for 13-14 hours would….

• Earn BDT 2,000 (USD 24.5)• Give daily rent of BDT 1,100 (USD13.05) to the taxi owner• Spend about BDT 300 (USD3.6) on fuel• Spend BDT 100-150 (USD 1.2 – 1.8) - for his daily for his

expenses (food - BDT 100, airtime – BDT 10, miscellaneous BDT 100

That leaves him with ….(assuming 25 working days a month)• Daily : BDT 350 – 400 (USD4.2)• Monthly: BDT 9,000 (USD110.4)

On a typical day, Karim Bhai after driving for 13-14 hours would….

• Earn BDT 2,000 (USD 24.5)• Give daily rent of BDT 1,100 (USD13.05) to the taxi owner• Spend about BDT 300 (USD3.6) on fuel• Spend BDT 100-150 (USD 1.2 – 1.8) - for his daily for his

expenses (food - BDT 100, airtime – BDT 10, miscellaneous BDT 100

That leaves him with ….(assuming 25 working days a month)• Daily : BDT 350 – 400 (USD4.2)• Monthly: BDT 9,000 (USD110.4)

Karim’s Other Cashflows• Karim also has a small piece of land yields from

which help cover some of his household expenses, such as rice, both here and in Gaibanda. Its yields him some seasonal income too from growing vegetables.

• House rent in Dhaka : BDT 2,000• Expenses in Gaibanda: BDT 1,800 (sends quarterly

or once in two months)• Household expenses in Dhaka: BDT 2,000

• Karim also has a small piece of land yields from which help cover some of his household expenses, such as rice, both here and in Gaibanda. Its yields him some seasonal income too from growing vegetables.

• House rent in Dhaka : BDT 2,000• Expenses in Gaibanda: BDT 1,800 (sends quarterly

or once in two months)• Household expenses in Dhaka: BDT 2,000

Karim’ s Financial Needs

• Regular cash flow for taking care of consumption needs such as…• Household expenses in Dhaka and in Gaibanda• Education expenses for his children• Medical expenses for his mother • Airtime to be in touch with his family and taxi owner

• Long term financial need• Daughter’s marriage• A lump sum to help his sons set up a business as they

complete school • Purchase a small room in Dhaka to avoid paying rent • Coverage of family from death risk, since he perceives

his occupation as risky

• Regular cash flow for taking care of consumption needs such as…• Household expenses in Dhaka and in Gaibanda• Education expenses for his children• Medical expenses for his mother • Airtime to be in touch with his family and taxi owner

• Long term financial need• Daughter’s marriage• A lump sum to help his sons set up a business as they

complete school • Purchase a small room in Dhaka to avoid paying rent • Coverage of family from death risk, since he perceives

his occupation as risky

Karim’s Transactions (1/2)

Quarterly Lottery Based RoSCA► Members contribute BDT 600 per month (or BDT 20 per day)

for 3 months. When the fund becomes BDT 90,000, the entire amount will be allocated to one person, selected by lottery. That person will have to continue to save , but will not be a part of lottery till al the other members have received the amount at least once.

► Use: Major household expenses, medical expenses, expense for festivals/scheduled events, book a room in Dhaka

Weekly Lottery based RoSCA► 100 members save BDT 100 per week; the lottery happens

every week for the entire fund. Once winner will not be allowed to participate in lottery for 1 year.

► Use: Expense for expense for festivals/scheduled events, repay debts taken at time of emergency

Quarterly Lottery Based RoSCA► Members contribute BDT 600 per month (or BDT 20 per day)

for 3 months. When the fund becomes BDT 90,000, the entire amount will be allocated to one person, selected by lottery. That person will have to continue to save , but will not be a part of lottery till al the other members have received the amount at least once.

► Use: Major household expenses, medical expenses, expense for festivals/scheduled events, book a room in Dhaka

Weekly Lottery based RoSCA► 100 members save BDT 100 per week; the lottery happens

every week for the entire fund. Once winner will not be allowed to participate in lottery for 1 year.

► Use: Expense for expense for festivals/scheduled events, repay debts taken at time of emergency

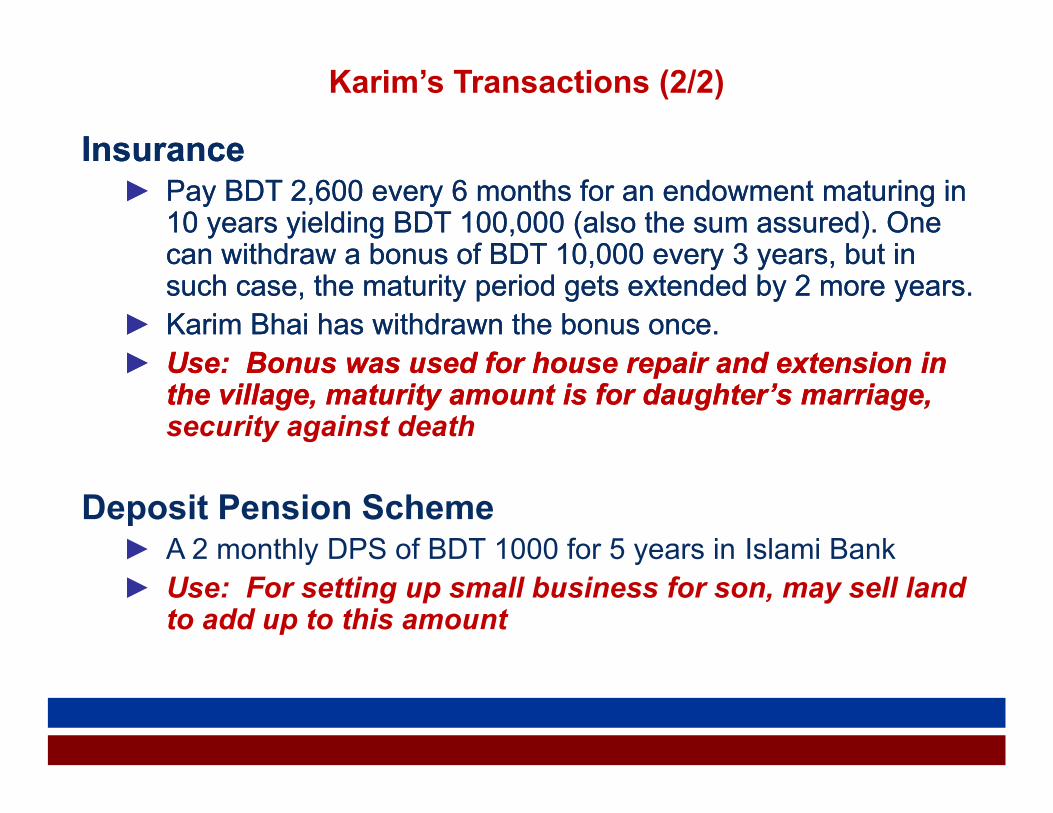

Insurance► Pay BDT 2,600 every 6 months for an endowment maturing in

10 years yielding BDT 100,000 (also the sum assured). One can withdraw a bonus of BDT 10,000 every 3 years, but in such case, the maturity period gets extended by 2 more years.

► Karim Bhai has withdrawn the bonus once. ► Use: Bonus was used for house repair and extension in

the village, maturity amount is for daughter’s marriage, security against death

Deposit Pension Scheme► A 2 monthly DPS of BDT 1000 for 5 years in Islami Bank► Use: For setting up small business for son, may sell land

to add up to this amount

Karim’s Transactions (2/2)

Insurance► Pay BDT 2,600 every 6 months for an endowment maturing in

10 years yielding BDT 100,000 (also the sum assured). One can withdraw a bonus of BDT 10,000 every 3 years, but in such case, the maturity period gets extended by 2 more years.

► Karim Bhai has withdrawn the bonus once. ► Use: Bonus was used for house repair and extension in

the village, maturity amount is for daughter’s marriage, security against death

Deposit Pension Scheme► A 2 monthly DPS of BDT 1000 for 5 years in Islami Bank► Use: For setting up small business for son, may sell land

to add up to this amount

Summary of Financial Transactions of KarimTransaction Details AmountIncome and Expense - DailyDaily income from taxi 2000Daily expenses on road (food etc.) 100Air time top up 20Miscellaneous 100Fuel 300Rent for taxi 1100Amount in hand at the of the day 380Amount in hand at the end of the month 9500Amount in hand at the end of the month 9500Expenses - Monthly 5800Rent 2000Sends to Gaibanda (but sends every 2-3 months) 1800Household expenses in Dhaka 2000Saving - Monthly 3433Quarterly RoSCA, paid daily (20*30) 600Weekly RoSCA (100*4) 400Insurance, paid six monthly (2600/6) 4332 monthly DPS of BDT 1000 each 2000Amount in hand 267

Prudence from Karatina in Kenya

She uses the following:► 2 RoSCAs► 1 ASCA► Informal funeral insurance► Cash savings at home► In-kind saving► Loan from Faulu MFI

She uses the following:► 2 RoSCAs► 1 ASCA► Informal funeral insurance► Cash savings at home► In-kind saving► Loan from Faulu MFI

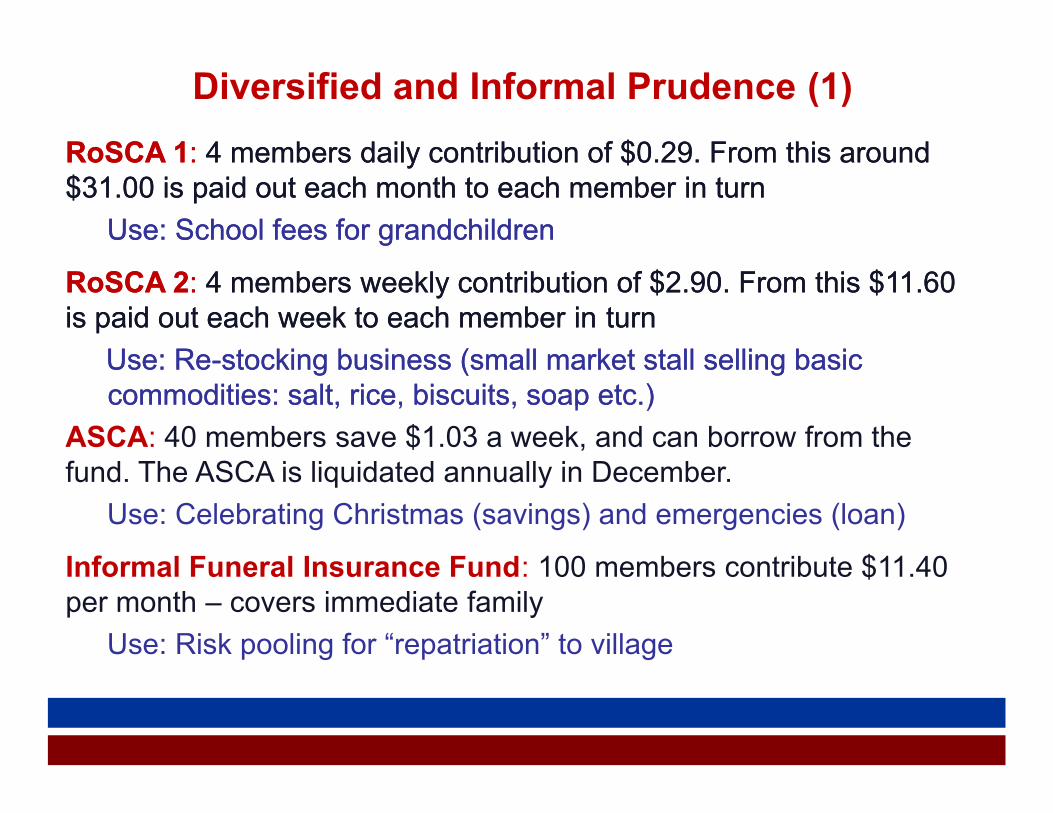

Diversified and Informal Prudence (1)RoSCA 1: 4 members daily contribution of $0.29. From this around $31.00 is paid out each month to each member in turn

Use: School fees for grandchildren

RoSCA 2: 4 members weekly contribution of $2.90. From this $11.60 is paid out each week to each member in turn

Use: Re-stocking business (small market stall selling basic commodities: salt, rice, biscuits, soap etc.)

ASCA: 40 members save $1.03 a week, and can borrow from the fund. The ASCA is liquidated annually in December.

Use: Celebrating Christmas (savings) and emergencies (loan)

Informal Funeral Insurance Fund: 100 members contribute $11.40 per month – covers immediate family

Use: Risk pooling for “repatriation” to village

RoSCA 1: 4 members daily contribution of $0.29. From this around $31.00 is paid out each month to each member in turn

Use: School fees for grandchildren

RoSCA 2: 4 members weekly contribution of $2.90. From this $11.60 is paid out each week to each member in turn

Use: Re-stocking business (small market stall selling basic commodities: salt, rice, biscuits, soap etc.)

ASCA: 40 members save $1.03 a week, and can borrow from the fund. The ASCA is liquidated annually in December.

Use: Celebrating Christmas (savings) and emergencies (loan)

Informal Funeral Insurance Fund: 100 members contribute $11.40 per month – covers immediate family

Use: Risk pooling for “repatriation” to village

Emergency cash in the home: $3-$5► Use: Emergencies requiring immediate cash

A cow back in the village: looked after by Prudence’s brother► Use: Provision for old age/social capital maintenance

Working capital loan from Faulu MFI ($356)► Building a small room to rent out (to provide stable income

for old age)

Diversified and Informal Prudence (2)

Emergency cash in the home: $3-$5► Use: Emergencies requiring immediate cash

A cow back in the village: looked after by Prudence’s brother► Use: Provision for old age/social capital maintenance

Working capital loan from Faulu MFI ($356)► Building a small room to rent out (to provide stable income

for old age)

Veena from Rajapur, in Uttar Pradesh, India

She uses the following:► Reciprocal borrowing and

from lending to neighbours► A savings club (or ASCA)

that is liquidated annually► Cash savings in a mud

bank► Borrowing for business and

emergencies from SKS

She uses the following:► Reciprocal borrowing and

from lending to neighbours► A savings club (or ASCA)

that is liquidated annually► Cash savings in a mud

bank► Borrowing for business and

emergencies from SKS

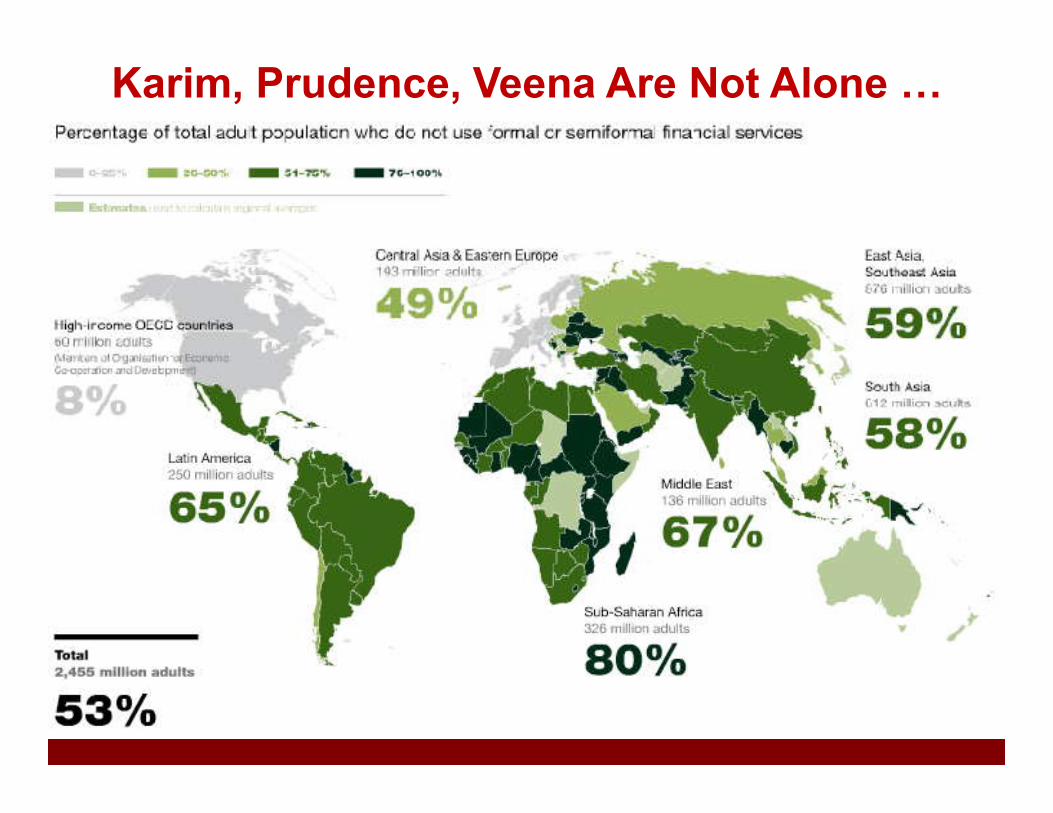

Karim, Prudence, Veena Are Not Alone …

Microfinance in Asia• Largest and most profitable MFIs: BRI, ASA etc.• Large numbers of weak MFIs• Cost efficient (best at 5% operating efficiency)• 528 million estimated clients• But … 200-400 million un-served in India and 200-400 un-

served in China

2

3

4

5

6

7

8

9

400

600

800

1000

1200

1400B

alan

ce in

Mill

ion

USD

Deposit and Loan Balance of Grameen Bank

Rollout of GB II started here

Rollout of GB II started here

Leveraging existing visits to groups reduces

the cost of deposit

mobilisation

Bangladesh: Opportunities Can Even Be Dangerous

0

1

2

0

200

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Loans Outstanding Deposits of non - GB Members (Balance) Deposits of GB Members (Balance) Number of Clients

Products Introduced Top-Up Loans Flexi-Loans Individual Enterprise Loans

Products Introduced Voluntary Savings Recurring Deposit (GPS) Fixed Deposits

0

200

400

600

800

1000

1200

1400

US$

Mill

ions

Loans O/S Deposits O/S

Ever Increasing problem of matching

Assets with Liabilities

Ever Increasing problem of matching

Assets with Liabilities

Bangladesh: Opportunities Can Even Be Dangerous

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

• Generous interest on fixed & recurring deposits (of around 12% per annum) has yielded a $400 million excess of savings over loans

• Fixed deposit rates in the Bangladesh market are 8-10%

• Grameen is accelerating its individual lending programme to absorb more of the deposits http://www.microsave.org/briefing_notes/grameen-ii-8-lessons-from-the-grameen-ii-revolution

Microfinance in Africa

• Many diverse institutional models • Most clients served by credit unions & coops• Rural and agricultural finance is particularly challenging• Only 8 sustainable institutions (MBB)• 25 million estimated clients – this may be an under-estimation• International and domestic banks starting to take an interest

4000

5000

6000

4000

5000

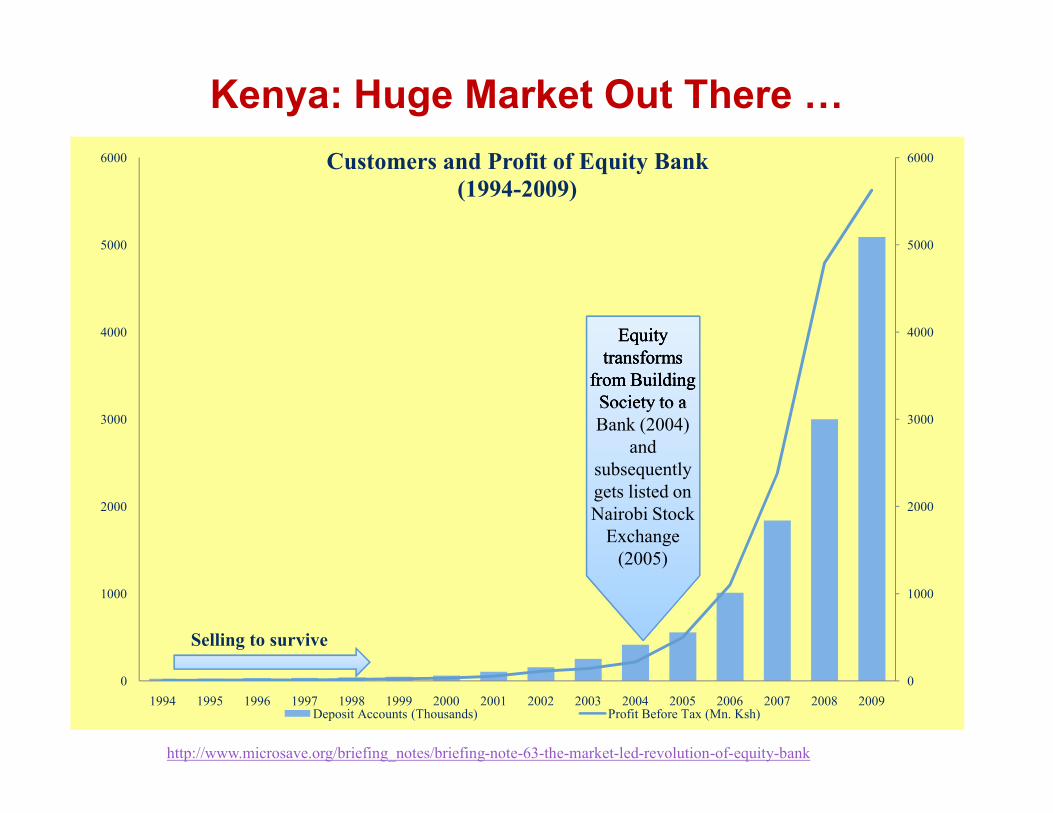

6000 Customers and Profit of Equity Bank (1994-2009)

Kenya: Huge Market Out There …

Equity transforms

from Building Society to a Bank (2004)

and subsequently gets listed on Nairobi Stock

Exchange (2005)

Equity transforms

from Building Society to a Bank (2004)

and subsequently gets listed on Nairobi Stock

Exchange (2005)

0

1000

2000

3000

0

1000

2000

3000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009Deposit Accounts (Thousands) Profit Before Tax (Mn. Ksh)

Selling to survive

Equity transforms

from Building Society to a Bank (2004)

and subsequently gets listed on Nairobi Stock

Exchange (2005)

Equity transforms

from Building Society to a Bank (2004)

and subsequently gets listed on Nairobi Stock

Exchange (2005)

http://www.microsave.org/briefing_notes/briefing-note-63-the-market-led-revolution-of-equity-bank

Kenya: What Fuelled the Growth?Build on a commitment to:• Listening to clients and responding to their needs• Excellent customer service• Technology/delivery channels: IT/ATMs /POS/m-banking

This involved:• Commitment to customer focus and market research/product

development• Harnessing the market-led approach, word of mouth and PR for

growth• Maintaining corporate culture and optimising corporate

governance• Management of donor inputs• Strategy development/execution: remaining a broad based bank • Re-engineering processes

Build on a commitment to:• Listening to clients and responding to their needs• Excellent customer service• Technology/delivery channels: IT/ATMs /POS/m-banking

This involved:• Commitment to customer focus and market research/product

development• Harnessing the market-led approach, word of mouth and PR for

growth• Maintaining corporate culture and optimising corporate

governance• Management of donor inputs• Strategy development/execution: remaining a broad based bank • Re-engineering processes

Microfinance in Middle East & North Africa

• Mostly NGOs • Heavy donor dependence• In infant stages of development• Mostly small working capital loans• 48 million estimated clients

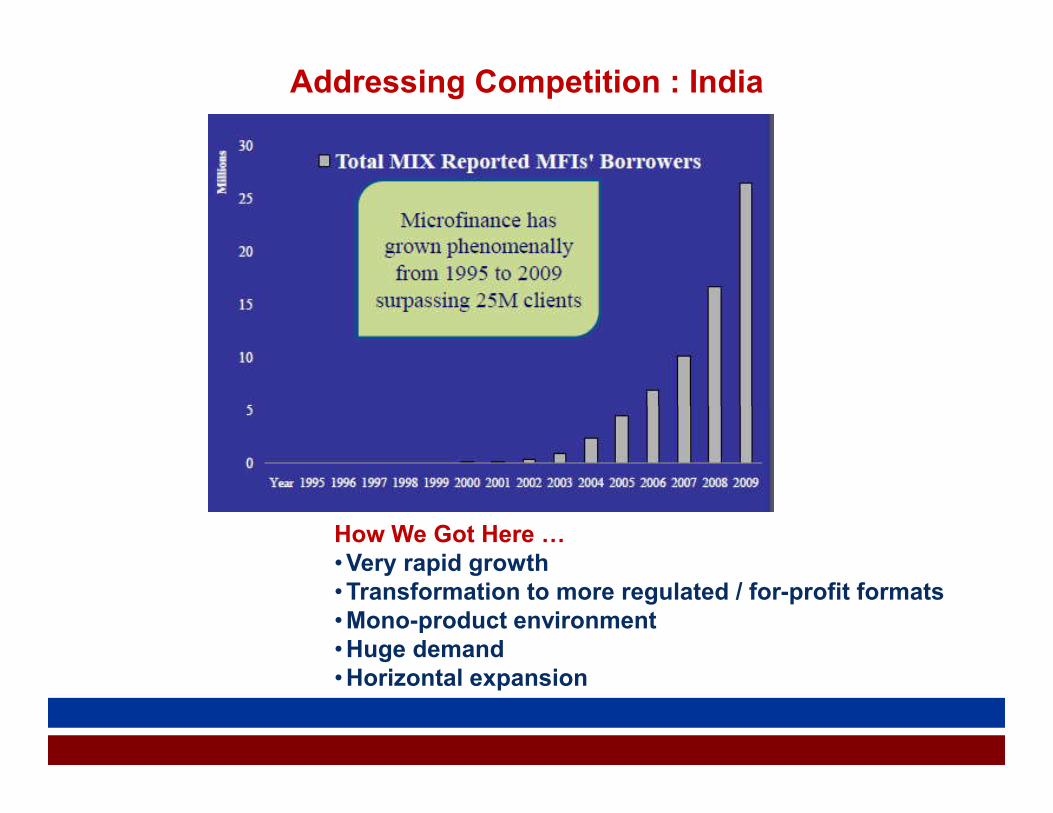

Addressing Competition : India

How We Got Here …• Very rapid growth• Transformation to more regulated / for-profit formats• Mono-product environment• Huge demand• Horizontal expansion

Led to….• Multiple lending / over-indebtedness• Reserve Bank and Government worried about interest

rates• State Governments putting restrictions/ classifying MFIs

as moneylenders• Banks and investors looking at MF as a high risk sector• Stridently negative press –national and regional

• Multiple lending / over-indebtedness• Reserve Bank and Government worried about interest

rates• State Governments putting restrictions/ classifying MFIs

as moneylenders• Banks and investors looking at MF as a high risk sector• Stridently negative press –national and regional

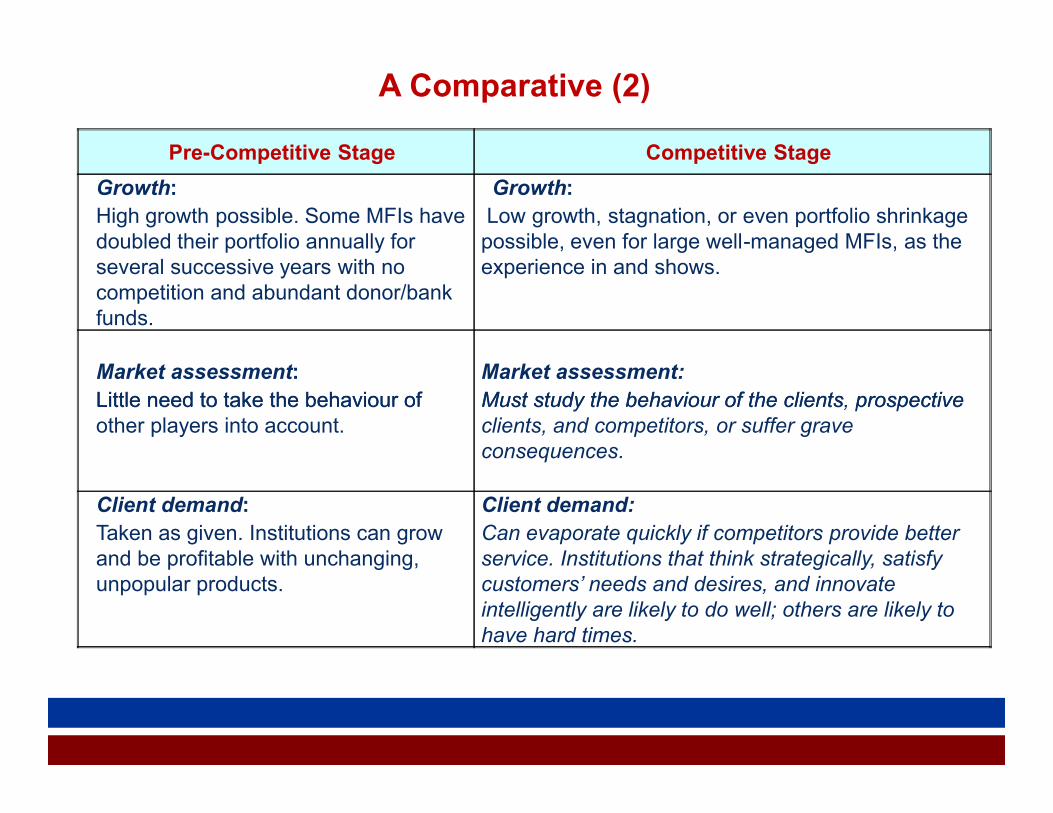

A Comparative (1)

Pre-Competitive Stage Competitive Stage

Objective: To reach more people and to become financially viable.

Objective: To retain or increase market share, while remaining profitable

Internal focus: Developing the institution’s internal capabilities and optimising efficiency.

Internal issues remain important, but external focus is added: Understanding the external environment and incorporating that understanding into business strategy. Issues like corporate branding, strategic marketing and governance gain importance.

Internal focus: Developing the institution’s internal capabilities and optimising efficiency.

Internal issues remain important, but external focus is added: Understanding the external environment and incorporating that understanding into business strategy. Issues like corporate branding, strategic marketing and governance gain importance.

Driving motivation: Access to funding.

Driving motivation:Attracting and retaining customers.

Pre-Competitive Stage Competitive StageGrowth: High growth possible. Some MFIs have doubled their portfolio annually for several successive years with no competition and abundant donor/bank funds.

Growth:Low growth, stagnation, or even portfolio shrinkage possible, even for large well-managed MFIs, as the experience in and shows.

Market assessment: Little need to take the behaviour of other players into account.

Market assessment: Must study the behaviour of the clients, prospective clients, and competitors, or suffer grave consequences.

A Comparative (2)

Market assessment: Little need to take the behaviour of other players into account.

Market assessment: Must study the behaviour of the clients, prospective clients, and competitors, or suffer grave consequences.

Client demand: Taken as given. Institutions can grow and be profitable with unchanging, unpopular products.

Client demand: Can evaporate quickly if competitors provide better service. Institutions that think strategically, satisfy customers’ needs and desires, and innovate intelligently are likely to do well; others are likely to have hard times.

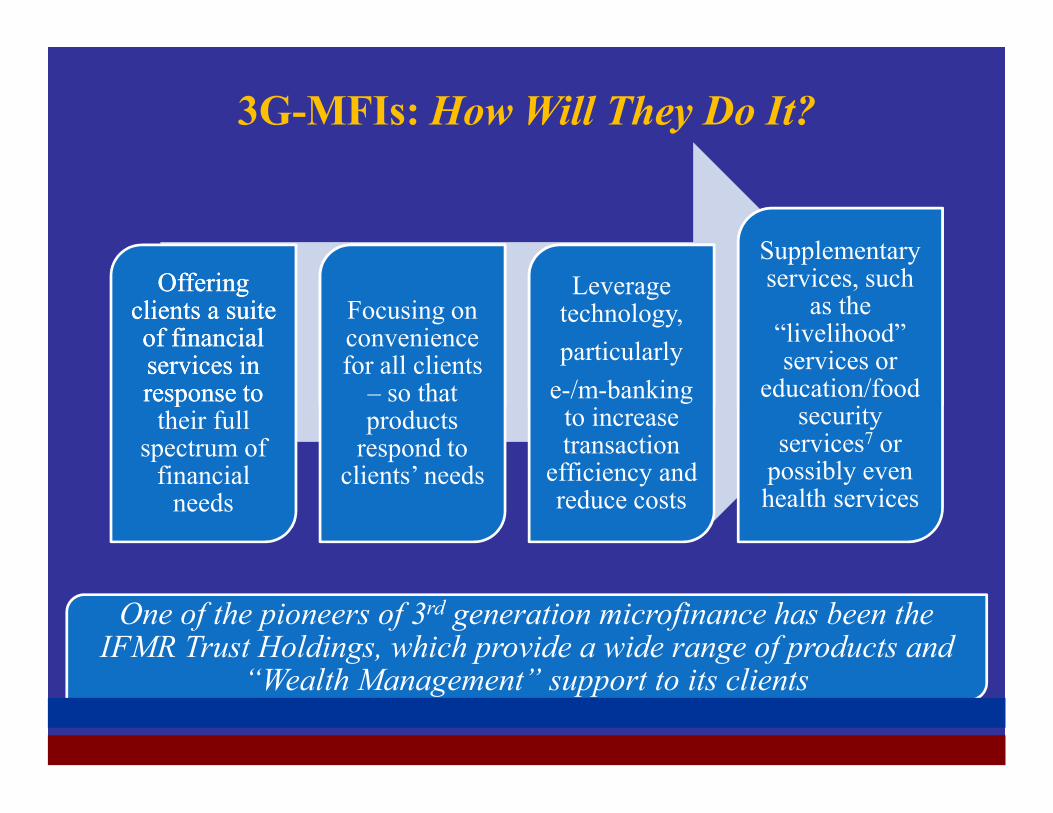

3G Microfinance Institutions“Expansion” to “Engagement”

3G-MFIs see growth in terms of improvements in

their clients’ financial well-being, and MFIs’ ability to serve them over a long time

Some MFIs are even looking at using full life time value of customer

analysis as a basis of their planning

Some MFIs are even looking at using full life time value of customer

analysis as a basis of their planning

3G-MFIs grow horizontally, but they grow

horizontally only to an extent that does not compromise their

engagement with existing client segments

3G-MFIs: How Will They Do It?

Offering clients a suite of financial services in response to

their full spectrum of

financial needs

Focusing on convenience for all clients

– so that products

respond to clients’ needs

Leverage technology, particularly

e-/m-banking to increase transaction

efficiency and reduce costs

Supplementary services, such

as the “livelihood” services or

education/food security

services7 or possibly even health services

Offering clients a suite of financial services in response to

their full spectrum of

financial needs

Focusing on convenience for all clients

– so that products

respond to clients’ needs

Leverage technology, particularly

e-/m-banking to increase transaction

efficiency and reduce costs

Supplementary services, such

as the “livelihood” services or

education/food security

services7 or possibly even health services

One of the pioneers of 3rd generation microfinance has been the IFMR Trust Holdings, which provide a wide range of products and

“Wealth Management” support to its clients

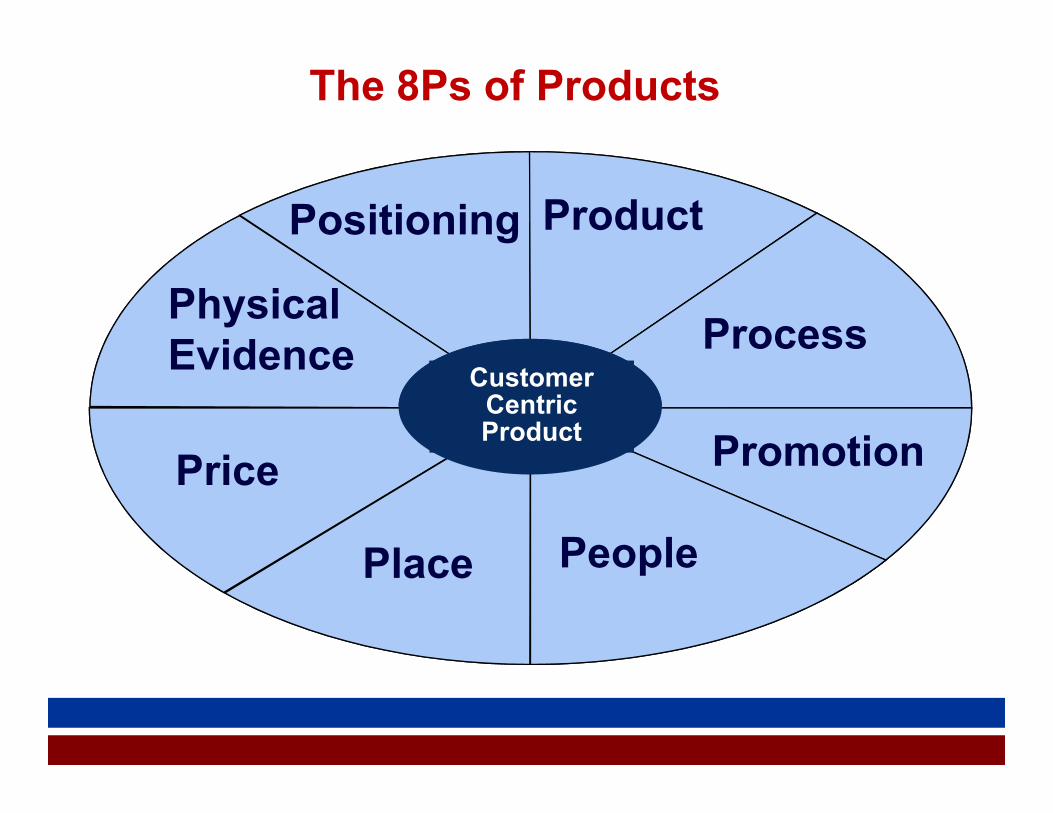

The 8Ps of Products

Process

ProductPositioning

Physical Evidence Customer

Centric Product

Price

Place People

Promotion

Customer Centric Product

The Customer’s Viewpoint

Customer SolutionsCommitted

Convincing ConciseCustomer

Centric Product

Convenient

Competitive

CostCompetent & Courteous

Communication

Customer Centric Product

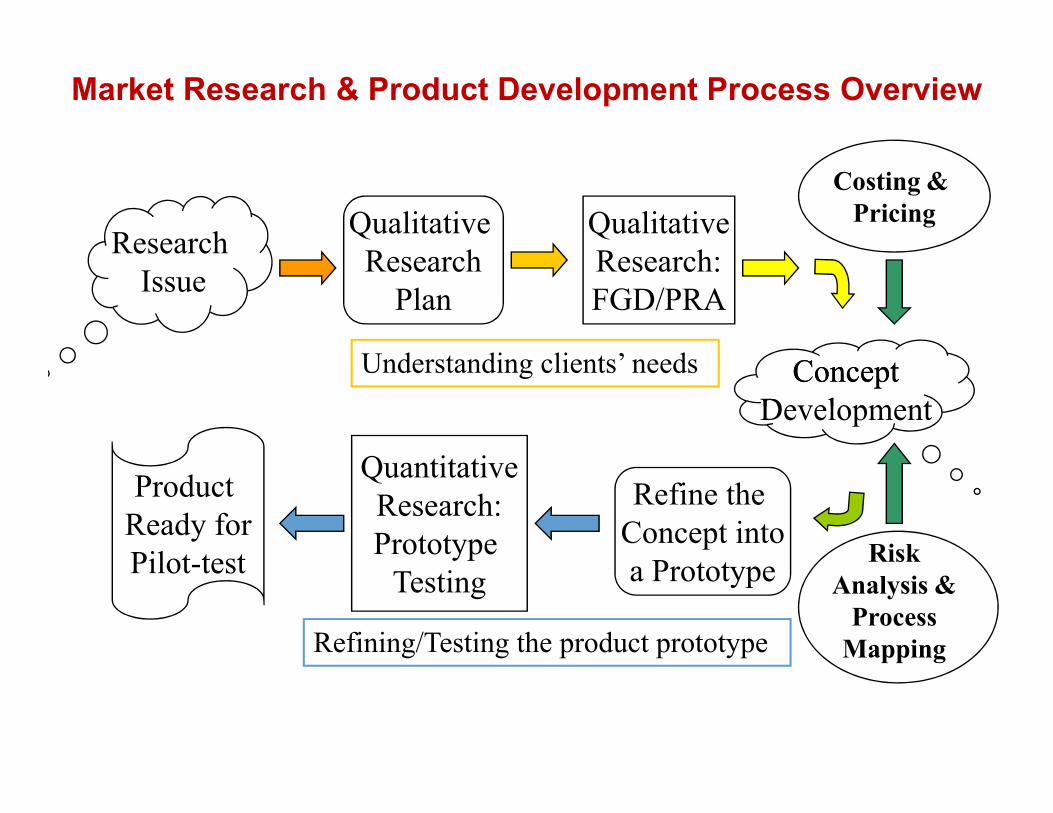

Market Research & Product Development Process Overview

QualitativeResearch:FGD/PRA

ConceptDevelopment

Qualitative Research

Plan

Research Issue

Understanding clients’ needs

Costing & Pricing

ConceptDevelopment

Refine the Concept intoa Prototype

QuantitativeResearch:Prototype

Testing

Product Ready forPilot-test

Refining/Testing the product prototype

Risk Analysis &

Process Mapping

Conclusions• Knowing your market is key to successful delivery of

services • And the market is constantly changing • The demand is huge and scope for innovation immense• Billions of people are waiting for us to do so …