Product Design 101: Developing Products That … Calvin Foo.pdf · Product Design 101: Developing...

17

Product Design 101: Developing Products That Cater to Client’s Needs Calvin Foo CFP Asia Regional Head Financial Advisory, Worksite Marketing & High Net Worth Development 13 July 2011

Transcript of Product Design 101: Developing Products That … Calvin Foo.pdf · Product Design 101: Developing...

Product Design 101: Developing Products That Cater to Client’s Needs

Calvin Foo CFP

Asia Regional Head

Financial Advisory, Worksite Marketing & High Net Worth Development

13 July 2011

2

Agenda

Objective

� Discuss the strategy behind designing products from a client-centric viewpoint

Content

� Product Strategy

� Client Segmentation

� Product Positioning

Result

� Apply these principles when developing products

33

Manulife FinancialStrong & Diversified Businesses

3

InvestmentsUnited States, Canada,

United Kingdom, Japan,

Australia, Hong Kong,

Southeast Asia

AsiaHong Kong, Philippines, Singapore,

Indonesia, Vietnam, Malaysia, Thailand,

Taiwan, China, Cambodia

• Individual Life Insurance

• Group Life & Health Insurance

• Pension Products

• Mutual Funds

Canada• Individual Insurance

• Individual Wealth Management

• Group Benefits

• Group Pensions

United States• Insurance

• Long Term Care

• Annuities

• Group Pensions

• Mutual Funds

Reinsurance• United States

• Canada

• Europe

• Asia

Japan • Individual Insurance

• Variable Annuities

3

44

Manulife FinancialCompetitive Strength

Excellent brand recognition and reputation

Strong claims paying ability / financial strength ratings

Strong capital position - C$28.9 billion @ June 30, 2011

Significant scale

Product diversity

Strong, multi-channel distribution

Superior asset quality

��������������������������������������������������������

4

55

Manulife Financial Strong Multi-Channel Distribution

AdvisorsFinancial Planners

Independent Agents

Brokers

DealersWirehouses

Banks

In-house Agents

• Deep & growing relationships across multiple channels worldwide

• Over 110 Bank partnerships across Insurance and Mutual Funds distribution in Asia

• Meet varying needs of our international base of customers, regardless of their chosen distribution channel.

5

7

Product StrategyActuary’s Role

Deals with the financial impact of risk & uncertainty

8

Product StrategyDistributor’s Role

Sells, solicits & negotiates for compensation

9

Product StrategyClient’s Role

Achieve financial security & independence for self & dependents

11

Product StrategyDifferent Stakeholder’s Point of View

• Actuary – Risks, Pricing, Experience, Profit

• Distributor – Features & Benefits, Market Competitiveness

• Client – Funds for Major Illness Protection, Peace of Mind

13

Product StrategyRecommended Point of View

Starts with the Client Ends with the Client

16

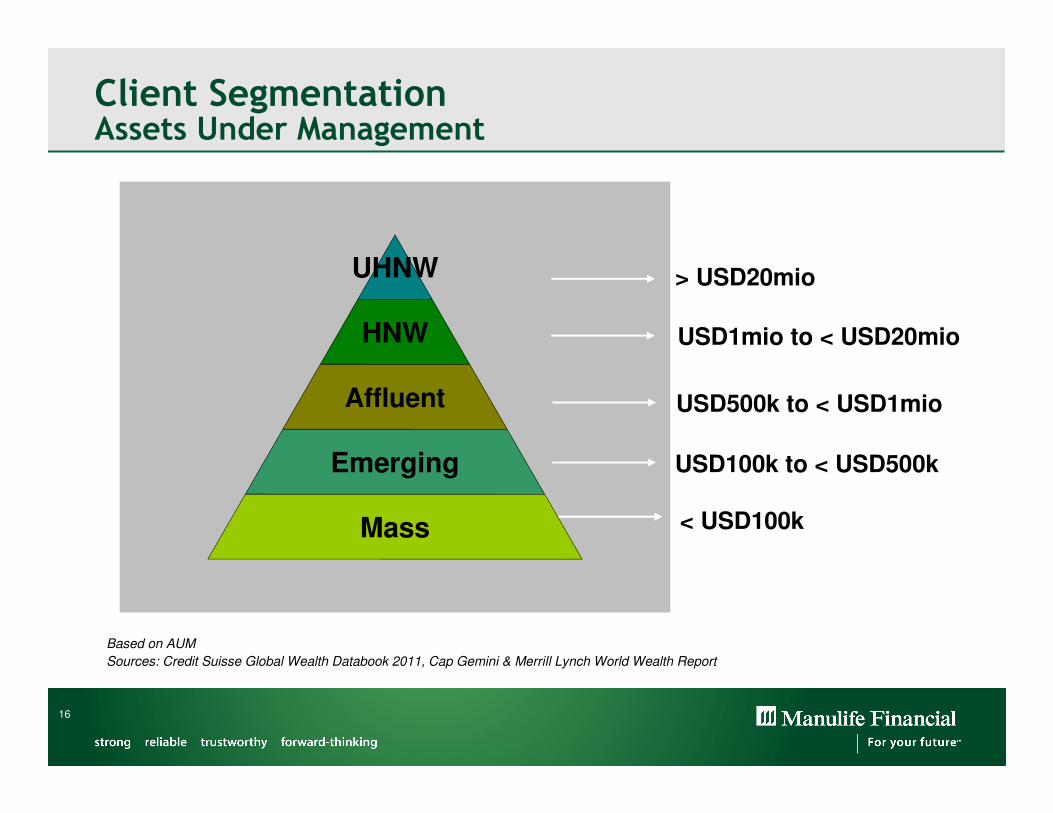

UHNW

HNW

Affluent

Emerging

Mass

> USD20mio

< USD100k

USD1mio to < USD20mio

USD500k to < USD1mio

USD100k to < USD500k

Client Segmentation Assets Under Management

Based on AUM

Sources: Credit Suisse Global Wealth Databook 2011, Cap Gemini & Merrill Lynch World Wealth Report

17

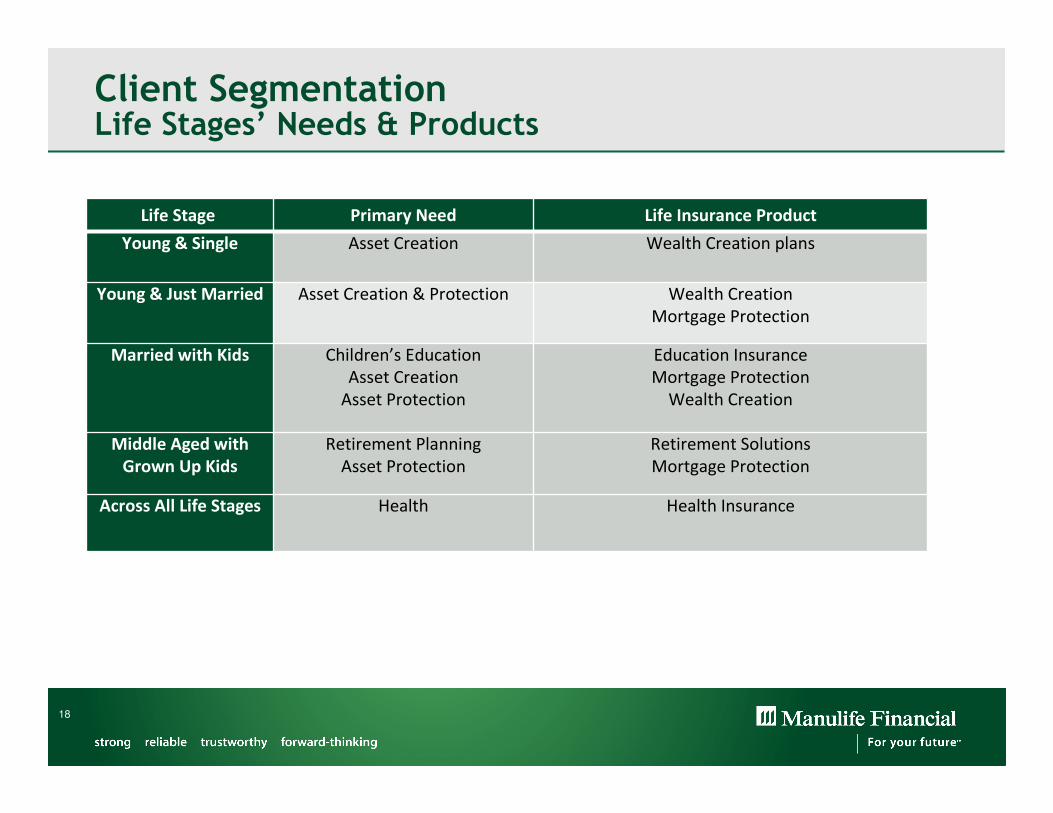

Client Segmentation Life Stages

18

Client Segmentation Life Stages’ Needs & Products

Education Insurance

Mortgage Protection

Wealth Creation

Children’s Education

Asset Creation

Asset Protection

Married with Kids

Retirement Solutions

Mortgage Protection

Retirement Planning

Asset Protection

Middle Aged with

Grown Up Kids

Health InsuranceHealthAcross All Life Stages

Life Stage Primary Need Life Insurance Product

Young & Single Asset Creation Wealth Creation plans

Young & Just Married Asset Creation & Protection Wealth Creation

Mortgage Protection

21

Product PositioningInfluencing Factors for Product Design

21

Marketing / After-sales Service Facilities

Regulation (Tax System, ILAS)

Clients’ Needs / Target Group

(Clients)

Competition(Insurers and Fund

Houses)

Profitability Fee Income

(Up-front and Annuity)

Persistency

Product

Positioning

Existing Product Range

Technology(POS, Underwriting,

MI, Web-site)

Sales Competence of Distributor

22

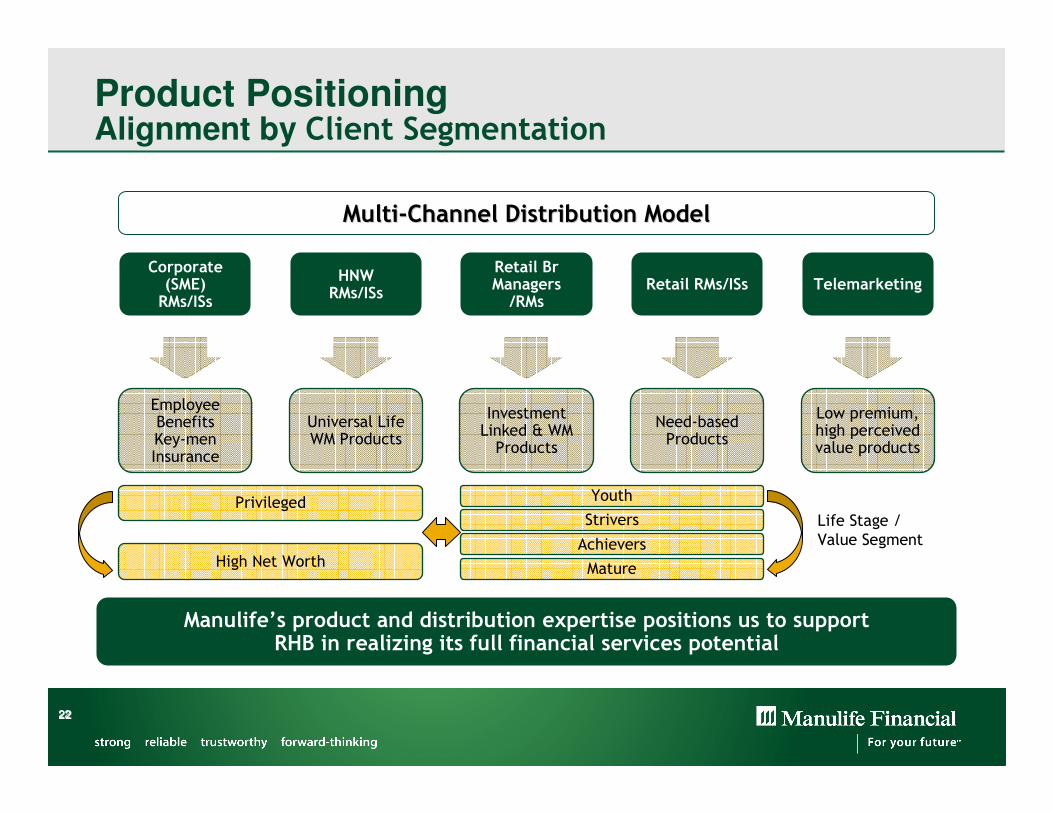

Corporate (SME)RMs/ISs

Employee BenefitsKey-men Insurance

HNWRMs/ISs

Universal LifeWM Products

Product PositioningAlignment by Client Segmentation

22

MultiMulti--Channel Distribution ModelChannel Distribution Model

Retail Br Managers/RMs

Investment Linked & WM Products

Retail RMs/ISs

Need-based Products

Telemarketing

Low premium, high perceived value products

Manulife’s product and distribution expertise positions us to support RHB in realizing its full financial services potential

Privileged

High Net WorthAchievers

Youth

Strivers

Mature

Life Stage /

Value Segment

26

Biography

Calvin Foo

Asia Regional Head

Financial Advisory, Worksite Marketing & High-Net-Worth Development

Calvin brings a unique blend of his 20 years experience in the financial services industry, including

sales management, agency management, bancassurance, broker management and worksite marketing.

Prior to joining Manulife, Calvin was with UBS Wealth Management and was responsible for the

management of Life Insurance for Ultra & High Net Worth Markets. Before that, he had extensive

regional responsibilities for 13 countries in Asia Pacific in both the life and non-life divisions of a large international insurance carrier.

Calvin has a Master’s degree in Business Administration and is a Certified Financial Planner. He is

a seasoned presenter and actively and frequently participates in many Asia conferences pertaining

to Client Needs, Bancassurance, Broker / FA / IFA and HNW topics. Calvin is also an experienced

Toastmaster (Public Speaker) having emerged as Champion and 1st Runner-Up for 2010 Hong Kong Toastmasters International Speech and Table-Topics Contests respectively.

Contact: [email protected]

27

The above is strictly for information and reference purposes only. Some information contained here is provided/sourced by our company or being re-transmitted in the ordinary course of business to you. Manulife endeavors to ensure the accuracy and reliability of the information provided but does not guarantee its accuracy or reliability and accept no liability (whether in tort or contract or otherwise) for any loss or damage arising from any inaccuracies or omission. Any opinion or estimate contained in this document is made on a general basis and is not to be relied on by the reader. Manulife reserves the right to make changes and corrections to its opinions expressed in this document at any time, without notice. Any unauthorised disclosure, use or dissemination, either whole or partial, of this document is prohibited and this document is not to be reproduced, copied, made available to others.

Disclaimer