Private – Public Partnerships in Urban Water Supply Sector

86

Electronic copy available at: http://ssrn.com/abstract=2004761 Lee Kuan Yew School of Public Policy Working Paper Series Private – Public Partnerships in Urban Water Supply Sector: A Study of the Regional Trends Asanga Gunawansa Assistant Professor, Department of Building, School of Design and Environment National University of Singapore Email: [email protected] Sonia Ferdous Hoque Research Associate Institute of Water Policy, Lee Kuan Yew School of Public Policy, National University of Singapore. Email: [email protected] Lovleen Bhullar Researcher Environmental Law Research Society New Delhi, India. Email: [email protected] Date: 10 January 2012 Paper No.: LKYSPP 12 – 04 IWP [This paper is part of the ‘Water Governance: An Evaluation of Alternative Architectures’’ research project] [This paper should be of interest to academics and professionals working in the field of Urban Water Supply Management] 469C Bukit Timah Road Oei Tiong Ham Building Singapore 259772 Tel: (65) 6516 6134 Fax: (65) 6778 1020 Website: www.lkyspp.nus.edu.sg

-

Upload

ankush-singh -

Category

Documents

-

view

271 -

download

17

description

Private – Public Partnerships in Urban Water Supply Sector

Transcript of Private – Public Partnerships in Urban Water Supply Sector

Electronic copy available at: http://ssrn.com/abstract=2004761

Lee Kuan Yew School of Public Policy Working Paper Series

Private – Public Partnerships in Urban Water Supply Sector:

A Study of the Regional Trends

Asanga Gunawansa

Assistant Professor,

Department of Building,

School of Design and Environment

National University of Singapore

Email: [email protected]

Sonia Ferdous Hoque

Research Associate

Institute of Water Policy,

Lee Kuan Yew School of Public Policy,

National University of Singapore.

Email: [email protected]

Lovleen Bhullar

Researcher

Environmental Law Research Society

New Delhi, India.

Email: [email protected]

Date: 10 January 2012

Paper No.: LKYSPP 12 – 04 IWP

[This paper is part of the ‘Water Governance: An Evaluation of Alternative Architectures’’

research project]

[This paper should be of interest to academics and professionals working in the field of Urban

Water Supply Management]

469C Bukit Timah Road Oei Tiong Ham Building Singapore 259772 Tel: (65) 6516 6134 Fax: (65) 6778 1020 Website: www.lkyspp.nus.edu.sg

Electronic copy available at: http://ssrn.com/abstract=2004761

PRIVATE – PUBLIC PARTNERSHIPS IN URBAN WATER SUPPLY SECTOR:

A STUDY OF THE REGIONAL TRENDS

Asanga Gunawansa, Lovleen Bhullar and Sonia Ferdous Hoque

ABSTRACT

Historically, public utilities have been mainly delivered by the public sector. However, as a

result of financial and technological constraints faced by public sector entities in developing

infrastructure facilities and due to management related inefficiencies in the public sector, various

alternative governance mechanisms have been considered by governments in developing public

utility infrastructure and providing the related services to the end-users. Consequently, for nearly

three decades now countries have relied on the procurement model of public-private partnerships

(PPP) to finance, develop and manage infrastructure facilities in the water sector. In order to

analyze the viability of PPP as an alternative governance model for water, it is important to

examine a sample of PPP projects from around the world and analyze the reasons for their

successes and failures. For this purpose, Institute of Water Policy, Lee Kuan Yew School of

Public Policy, National University of Singapore, has undertaken a research project to compile a

database of PPP projects in the urban water supply sector in different regions (Africa, Asia,

Europe, Latin America, Australia and Middle East and North Africa). This paper presents a brief

analysis of PPPs as a water governance architecture based on the study of 672 PPP projects from

the said database, the selection being made on the basis of availability of data, and presents the

preliminary findings on current usage of PPP for water governance.

Keywords: Private Public Partnerships; Urban Water Management; Water Governance; Build-

Own-Operate; Concession.

Electronic copy available at: http://ssrn.com/abstract=2004761

1. INTRODUCTION

Traditionally, a formal public authority or authorities (local, regional or national) has been

responsible, partly or fully, for the provision of water services (including infrastructure

development and funding, operation of the supply system, billing and collection of tariffs - if

they are raised, and system management and maintenance). Such entity also retained full

ownership of the related water infrastructure. In this scenario, private sector involvement was

considered inappropriate given the public good and basic need characteristics of water supply,

the inherent monopolistic tendency of water systems due to economies of scale in service

provision and the externalities involved (Johnstone and Wood 2001).

Although there are examples of successful public water utilities, such as Singapore, there are

several other cases where public management of urban water supply has not been successful.

This can be attributed to a variety of reasons such as the lack of financial capacity, the absence of

technology and management skills to develop, maintain and operate urban water facilities, and

the inability to cater to the rising demand for new water connections as a result of rapid

population growth in urban areas. Especially in developing countries, governments have found it

difficult to finance expensive engineering solutions with scarce public funds, and difficult to

continue government subsidies offered to water users given the resources required for financing

and operating urban water facilities. Further, politicization of personal appointments and

management and other bureaucratic weaknesses in public administration have also rendered

many public water facilities unsustainable. As a result, the effectiveness of public management

as water governance architecture has been questioned. The reduction in financial assistance from

international development agencies for infrastructure development projects, which are totally

controlled by public sector entities in developing countries, has also led to the search for

alternative water governance architectures. In this context, private sector participation in the

water governance process has been considered and promoted in several countries.

2. ROLE OF PRIVATE SECTOR IN PUBLIC INFRASTRUCTURE

Two alternative mechanisms have been considered for private sector engagement in the

provision of urban water supply: total privatization of public facilities and public-private

partnerships (PPPs) (Ford and Zussman 1997). Total privatization enables governments to

transfer the total responsibility of developing, managing, and providing public services to the

private sector, whereas PPP enables governments to invite private sector entities to finance and

develop infrastructure projects without losing state control over the regulatory aspects of service

delivery, including the pricing of the services provided by the infrastructure facility (Savas 2000;

Gunawansa 2001; Abdul-Aziz 2007). Total privatization of public infrastructure facilities that

provide public services at heavily subsidized prices (by the government) was considered

politically controversial. Further, governments were hesitant to subject certain facilities to total

privatization due to reasons such as national security. Thus, PPPs became the popular option.

In Europe, private investment in public infrastructure can be traced back to the 18th

PPPs are based on the idea that the private sector is better positioned to generate the capital

investment required to undertake network rehabilitation, maintenance and expansion. The

private sector’s potential for increased efficiency is also emphasized. In practice, however, there

may be other reasons for the introduction of PPPs, including loan conditionalities imposed by

international development banks. In short, a PPP is a procurement method which involves

private sector supply of infrastructure assets and services that have traditionally been provided

by the public sector. According to Khanom (2009), there is no precise and commonly accepted

definition of PPP. This is the result of the diverse interests and objectives of the public and

private parties in entering into PPPs as well as the different needs of the entities defining PPPs.

The following table shows the different interpretations given to PPPs by four different countries.

century

(Kumaraswamy and Morris 2002). However, the increasing adoption of PPPs in the late 1990s

was due to the success of PPPs in the United Kingdom (Harris 2004). The development and

refinement of private finance initiative (PFI) by the United Kingdom in 1992, as one of a range

of government policies designed to increase private sector involvement in the provision of public

services, led to the renewed international interest in PPPs. Since then, many countries around the

world have either embarked on or considered the adoption of a PPP programme (Harris 2004).

Table 1: Different Definitions of PPP

Country Definition Source

Canada A cooperative venture between the public and private

sectors, built on the expertise of each partner that best

meets clearly defined public needs through the

appropriate allocation of resources, risks and rewards.

Canadian Council for

Public Private

Partnerships

United

Kingdom

An arrangement between two or more entities that

enables them to do public service work cooperatively

towards shared or compatible objectives and in which

there is some degree of shared authority and

responsibility, joint investment of resources, shared risk

taking and mutual benefit.

Her Majesty’s

Treasury (1998)

Singapore PPP refers to long-term partnering relationships

between the public and private sector to deliver

services. It is a new approach that Government is

adopting to increase private sector involvement in the

delivery of public services.

MOF (2004)

India The Public-Private Partnership (PPP) Project means a

project based on contract or concession agreement

between a Government or statutory entity on the one

side and a private sector company on the other side, for

delivering an infrastructure service on payment of user

charges.

Department of

Economic Affairs of

the Ministry of

Finance (2005)

The Canadian definition appears to focus on the cooperative venture between the public and

private parties and the appropriate allocation of resources and risks. This indicates that PPPs are

looked at as partnering arrangements between parties with equal bargaining power. Similarly,

the UK definition focuses on compatibility between the parties and sharing of responsibilities,

risks, resources, and profits.

The Singapore definition focuses on PPPs as a long term relationship between public and private

sectors which enables the public sector to involve the private sector in providing services to the

people. This definition does not give any indication as to the real need for the public sector to

enter into PPPs. Further, in Singapore, PPPs are viewed as a source of specialist private sector

expertise to stimulate an exchange of ideas and to bring more international players into the

domestic market (KPMG 2007). According to the Government of India’s definition of PPP, the

government grants a concession to the private sector. The public sector has limited engagement

in the partnership due to financial constraints and lack of modern technologies and the private

sector is required to finance and develop the project and offer services in return for payments.

3. PPPS IN URBAN WATER

Private involvement in water supply has a long history. In the United States, historically, private

ownership and provision of water, and not public ownership, was the norm. It was only in the

latter half of the 19th century that private water systems in the United States began to be

municipalized because private operators were found to be inequitable when providing access and

service to all citizens or making necessary infrastructure investments (Wolff and Palaniappan

2004).

In its strict sense, ‘privatization’ implies a full divestiture or the sale of public assets to a private

operator, which is rare in the water supply sector (except England and Chile), which represents

the furthest point on the private sector engagement spectrum (see section 3.1). Otherwise,

‘privatization’ is said to have taken place when a specific function is turned over to the private

sector and regulatory control remains a public sector responsibility. On the other hand, a

‘public-private partnership’ describes an arrangement where the governments and private

companies assume shared responsibilities for the provision of water supply. In many countries

where total privatization of water, a public good, is considered a sensitive issue, the preferred

mode of engaging private sector in water governance has thus become PPP.

Based on data published in the Pinsent Masons Water Yearbook 2011 – 2012, Figure – 1 shows

the number of new PPP contracts awarded each year for water supply since 1991.

Figure – 1: Number of new PPP contracts awarded each year in the last two decades.

(Source: Pinsent Masons Water Yearbook 2011 – 2012)

3.1 Spectrum of PPP Models

There exists a spectrum of PPP models for urban water supply depending on several factors,

including the distribution of decision and property rights and risks and incentives between the

public and private entities.

(i) Service contract: A private entity provides specific services, such as leak detection, meter

reading, billing or collecting invoices, and water quality measurements, for a short time

period. The fees are fixed per unit of work. The private entity is required to make very

limited capital investment, and these are short-term contracts. This form of PPP allocates

the least responsibility to the private operator. The government retains ownership, control

and responsibility (and risk).

(ii) Management contract: A private operator manages and maintains the water facility for

the contract period without any investment obligations. A management contract can be

used to bring in new management systems, organizations and skills, or as a preliminary

step to restructure a dilapidated utility before a concession. The government compensates

the private operator (costs-plus-fee). The government retains most of the operational and

commercial risks, though some risk-sharing may be built into the contract using

performance bonuses or contingent fees.

(iii) Lease contract: The government leases the right to operate and maintain a water system,

and to collect user charges to a private operator, and the latter is compensated with an

agreed portion of the revenues. The private operator takes on the operational risk but the

public authority retains ownership and responsibility for system finance and expansion,

and replacement of major assets, and it recovers parts or all of its costs from its own share

of user charges. The lease holder may also administer investment funds as agent to the

municipality, without taking related risks.

In several African countries with substantial French influence, affermage contracts are

common. Lease and affermage contracts differ mostly in the way the commercial risk is

shared between the operator and the owner of the contract. In a lease, the private

operator’s fee depends on the amount of tariff collected from customers vis-à-vis the

specified lease fee payable to the public. In an affermage, on the other hand, the private

operator and the public authority share the collected revenue and the private operator is

paid an agreed-upon affermage fee for each unit of water produced and distributed (Budds

& McGranahan, 2003; World Bank, 2006).

(iv) Greenfield contract: The private entity finances, designs, constructs, and operates the

water infrastructure for a certain period of time to fulfill private economic interests, that is,

to pay the capital debt and earn a reasonable rate of return from the operating revenue.

This is followed by transfer of ownership to the government at no cost or an agreed upon

price. The government usually provides revenue guarantees through long-term take-or-pay

contracts for bulk supply facilities or minimum traffic revenue guarantees. The widely

used Greenfield contracts in the water sector are:

(a) Build, own, operate and transfer (BOOT) or Build, operate and transfer (BOT): The

private entity builds and operates a new water facility, for a specified period, at its own

risk, and then transfers the facility to the government at the end of the contract period.

The private entity may or may not have the ownership of the assets during the contract

period.

(b) Build, own, and operate (BOO): The private entity builds a new facility at its own risk,

then owns and operates the facility at its own risk.

(v) Concession (or reverse BOT): The public authority transfers ownerships and control of

the entire water system, which is already constructed, to a private operator for a given

period. The private operator assumes responsibilities for operation and maintenance as

well as additional investment and service obligations. The operator bills and retains user

charges for the concession period and the government retains ownership of the assets. The

following three types of concession agreements are usually agreed between the public and

private parties:

(a) Rehabilitate, operate, and transfer (ROT): The private entity rehabilitates an existing

facility, then operates and maintains the facility at its own risk for the contract period.

(b) Rehabilitate, lease or rent, and transfer (RLT): The private entity rehabilitates an

existing facility at its own risk, leases or rents the facility from the government owner,

then operates and maintains the facility at its own risk for the contract period.

(c) Build, rehabilitate, operate, and transfer (BROT): The private entity builds an add-on to

an existing facility or completes a partially built facility and rehabilitates existing assets,

then operates and maintains the facility at its own risk for the contract period.

(vi) Joint venture: The private company forms a legal entity with the public sector, and both

parties share responsibilities and investment obligations. The municipality can share

ownership with private shareholders. The joint venture company itself may either own the

assets or (most often) be given a franchise by the local government.

(vii) Divestiture: A private entity buys an equity stake in a state-owned enterprise through an

asset sale, public offering, or mass privatization program. The private stake may or may

not imply private management of the facility. There are two types of divestiture:

(a) Full divestiture: The government transfers 100 percent of the equity in the state-owned

company to private entities. This could thus be interpreted as a total privatization of a

state owned facility. For example, ten public water authorities in England and Wales,

which had been created under the 1973 Water Act, became private limited companies

with the introduction of the 1989 Water Act (OFWAT 1993).

(b) Partial divestiture: The government transfers part of the equity in the state-owned

company to private entities. In 1998, five of Chile’s 13 regional water companies

originally owned by the public sector were privatized with partial sales to multinational

companies (Birtran and Arellano 2005). Another good example comes from the Czech

Republic where a total of 11 public sector enterprises that operated water supply and

sewage systems were partially privatized following the Czech Government Resolution

No. 222 of 3 July 1991, which sought to introduce reforms to the drinking water, sewage

and wastewater systems (TI 2009).

3.2 Allocation of Responsibilities between Public-Private Partners

Under a PPP, a public entity would typically specify the outputs or services required from a

facility, and a private company or consortium would be responsible for the finance, design,

construction, operation and maintenance of a facility. The following table shows the allocation

of key responsibilities between the public and private entities, in the above mentioned models of

PPPs for urban water supply, and their duration (World Bank, 1997):

Table 2: Allocation of Key Responsibilities in PPPs

Option Asset

Ownership

Operation &

Maintenance

Capital

Investment

Commercial

Risk

Duration

Service

Contract

Public Shared Public Public 1-2 years

Management

Contract

Public Private Public Public 3-5 years

Lease/

Affermage

Public Private Public Shared 8-15 years

Build Operate

Transfer (BOT)

Contract

Shared Private Private Private 20-30 years

Concession Public Private Private Private 25-30 years

Joint Venture Shared Private Private Private Indefinite

Divestiture Private or

shared

Private Private Private Indefinite

(may be

limited by

license)

3.3 Is PPP a Viable Alternative Architecture for Urban Water Governance?

It is argued that PPPs can address the financial constraints faced by the public sector. They

provide access to private capital in exchange for giving private companies the right to raise tolls

on the water sold (which might also be supplemented by government grants or subsidies). The

involvement of a new service provider helps the government to overcome the political barriers of

unsustainably low tariff levels. It is also argued that PPPs overcome the capacity constraints by

introducing competition (Jooste 2008).

However, this competition, where introduced, is limited to the tender stage for concession

contracts (in other words, it is competition for the market, rather than competition in the market),

and it may or may not increase efficiency, and/ or ensure higher quality service, more

sophisticated technology, and greater financial and environmental sustainability. For instance,

the private sector lacks sufficient incentive to improve access in poor areas, with higher costs of

provision and lower levels of demand, in the absence of regulation. Further, traditionally, private

sector participation in urban water supply has been overwhelmingly dominated by large water

multinationals, such as Veolia and Suez. The grant of contracts without a competitive tendering

process also raises doubts about the ability of PPPs to improve competition in the water sector.

The creation of ‘alliances’ to overcome competition is also not uncommon.

Endemic uncertainty and lack of information about the local milieu may also tie the hands of

private sector. The success of PPPs for urban water supply is heavily dependent on the presence

of effective regulatory mechanisms. This represents a paradox as public mismanagement is one

of the justifications for private sector participation. Further, PPPs suffer from several other

problems that relate to tariff increases, under-investment, especially towards the ending period of

contracts, risk-averse strategies of private operators so that public authorities tend to bear most of

the uncertainties, and the very high rate of renegotiations, which undermine the credibility of the

parties involved and involve very high transaction costs. Further, high capital intensity, large

initial outlays, long pay-back periods, and the immobility of assets generate high risks. These

factors, when combined with poor initial information and a weak investment environment,

constitute important constraints on private sector participation in water and sanitation

infrastructure.

In the circumstances, it would appear that although the private sector participation can help

countries to benefit from financial, technological and managerial inputs from the private sector to

improve water governance, there are various impediments to private sector participation in the

water sector in many countries. This statement is supported by the fact that, despite the interest

in private sector participation in water since the 1990s, most of the water and wastewater related

services worldwide, nearly 95 percent (according to some estimates), are provided by public

sector companies (CPI 2003). Nevertheless, it is noteworthy that the number of people served by

private companies has grown from 563 million in 2005 to approximately 805 million in 2009

(GWI 2009). This figure is expected to increase further to approximately 1163 million people by

the year 2015.

4. DATABASE OF PPPS IN THE URBAN WATER SUPPLY SECTOR

The database of PPP projects compiled by the researchers is based on a search of publicly

available documents (e.g., newspaper articles, web logs and journal/research papers). The

database also uses information from databases compiled by other organizations, such as the

Private Participation in Infrastructure (PPI) online database managed by the World Bank Group,

the database of the Global Water Market 2009 published by Global Water Intelligence and

information from Pinsent Masons Water Yearbook 2011 - 2012. However, a review of the

available databases revealed a gap in certain number of projects. Further, a large number of the

details are either missing or conflicting, although certain records are complementary. In order to

meet the requirements of the research, rigorous clarifications and supplements have been made

by reviewing relevant articles, reports, project track records, and websites of water companies.

For the purpose of this paper, 672 projects have been chosen from the database on the basis of

the adequacy of the information available.

The distribution of PPP projects (considered for this paper) in the six regions is as follows:

Figure 2: Distribution of PPP Projects by Region

Based on the data collected, it is observed that Europe has the largest number of documented

PPP projects, followed by Latin America and Asia.

The selected PPP projects from the database, organised according to the regions in a list, is

attached as Appendix. It contains information on location, type of contract, period - both

planned and actual, main private players, and status/ outcome. Some of these projects have

reached financial closure or are operational. Others are distressed or have concluded or

cancelled/ terminated. This may be the result of several factors, including poorly designed

contracts, unsuitable regulatory mechanisms, economic and/ or public health problems. The

relevant terms are explained below:

Financial closure: There is legally binding commitment of private sponsors to

mobilize funding or provide services.

Operational: The project has started providing services to the public.

Distressed: The government or the private operator has either requested

contract termination or are in international arbitration.

Expired: The contract period has expired and it was neither renewed nor

extended by either the government or the private operator.

Terminated/ Remunicipalised: The private sector has exited from the project by:

selling or transferring its economic interest back to the

government before fulfilling the contract terms;

removing all management and personnel; or

ceasing operation, service provision, or construction for an

agreed percentage of the license or concession period,

following the revocation of the license or repudiation of the

contract.

5. PRELIMINARY FINDINGS

Based on the literature review and the database, the researchers have developed the following

preliminary findings.

5.1 Regional Trends

Africa

In Africa, a majority of the projects involve management contracts, with no joint ventures or

privatized projects. Figure 3 and 4 show the type of PPP projects in Africa and their current

status:

Figure 3: Types of PPP Contracts (Africa)

Figure 4: Status of Contracts (Africa)

Some lease - affermages have elements of a concession contract, such as in the case of Cote

d’Ivoire and Senegal. In these projects, the government retains asset ownership and assumes the

risk of investment. They mostly rely on the private operators for their expertise and efficiency in

managing the water supply network. This trend could also be due to pressure from the World

Bank to promote privatization in order for the local governments to receive financial aid. By

issuing out management contracts and lease/affermages, a greater degree of control could still be

maintained over the public assets while fulfilling their obligations to the World Bank. Local

governments in the region could also be wary of these private operators and their cost-recovery

practices. This could explain their reluctance to hand over control of their public assets for long

periods of time.

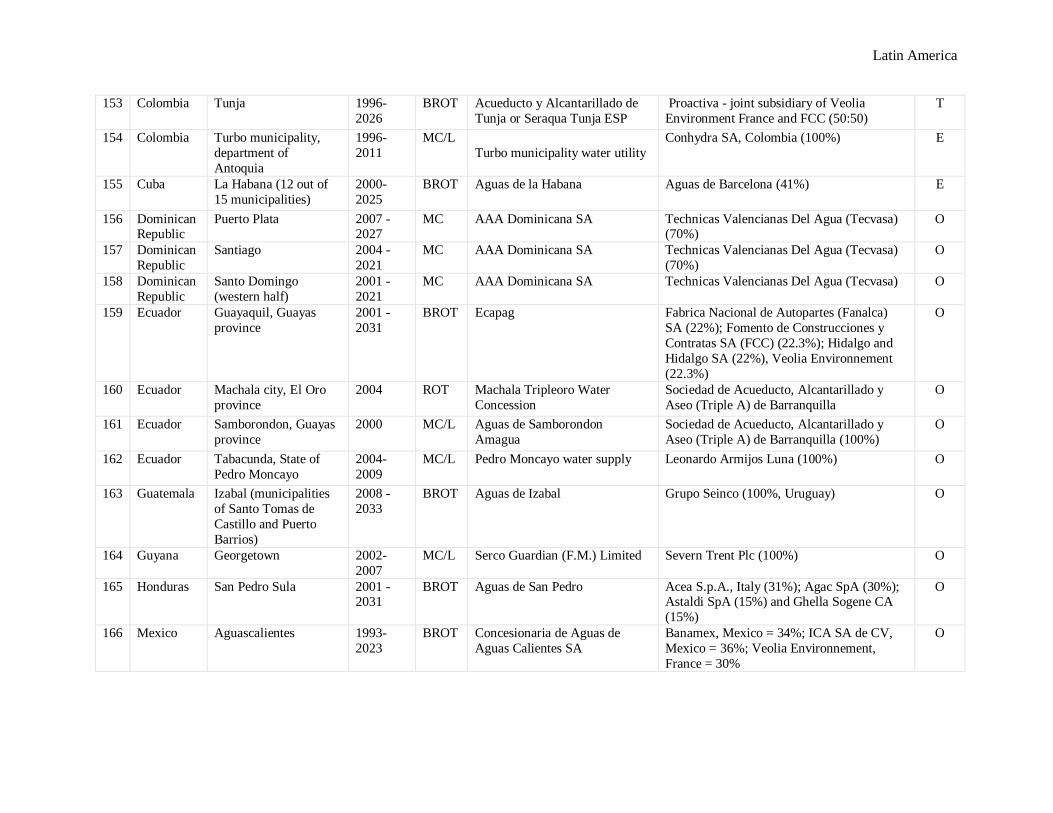

Latin America

In Latin America, a majority of the PPP projects for urban water supply are long term

concessions. There are a few management contracts and some partial divestitures in Brazil and

Chile. This could be due to the fact that Latin American countries do not have the necessary

financial clout to undertake the commercial risk of the partnership. It could also be due to strong

influence from the multi-national companies to convince the governments to take up these

contracts. Concession contracts would allow the private players more freedom to allocate their

resources and provide a steady stream of income. Figure 5 and 6 show the type of PPP projects

in Latin America and their current status.

Figure 5: Types of PPP Contracts (Latin America)

Figure 6: Status of Contracts (Latin America)

Asia

A majority of the PPP projects for urban water supply in Asia are concessions. There are also

several projects developed on the basis of BOT and BOOT. Here too, strong influence of

multinational agencies could be identified as a reason behind the popularity of long term

concessions and BOT/BOOT type of contractual arrangements with private sector entities.

Further, the technological and management constraints faced by the public sector entities in

Asian countries to develop and operate efficient water facilities may have contributed towards

this trend. It is also noted that Asia was one of the last regions to be hit by the privatization

wave. This meant that concession contracts would have been better spelt out, and conflicts

arising from earlier contracts signed would have been resolved. This would make the Asian

governments more willing to commit to these long-term concession contracts. Figure 7 and 8

show the type of PPP projects in Asia and their current status.

Figure 7: Types of PPP Contracts (Asia)

Figure 8: Status of Contracts (Asia)

MENA

In the Middle East and North Africa, while PPPs have received significant attention for

desalination projects, water supply usually falls under public management (Bruch 2007).

However, examples of private sector participation are visible. A large majority of the 28 urban

water supply projects involving the private sector are management contracts, and the three

concession contracts in the region are all found in Morocco. Several new management contracts

are expected to be awarded to the private sector. Countries in MENA are more affluent and can

afford to bear the commercial risk of the PPP projects. Private operators were needed to provide

the technical know-how and efficient means of management. Figure 9 and 10 show the type of

PPP projects in MENA and their current status.

Figure 9: Types of PPP Contracts (MENA)

Figure 10: Status of Contracts (MENA)

Europe

The largest percentage of projects in Europe fall into the category of long term concessions

whilst 18 percent of the projects have been given to the private sector on management contracts.

Europe was the first to be hit by the privatization wave. As a result, private players typically

fought for long term concession contracts or, in the alternative for long term leases/ affermages

to maximize their profits.

The ownership of private water companies in Europe is overwhelmingly dominated by Suez and

Veolia, who together with other private water companies are increasingly dependent on their

national government and international development banks for capital (Hall and Lobina 2010).

There have been cases of termination of privatization, resulting in remunicipalisation and return

to public ownership. Examples include Paris (France), Potsdam (Germany) and Kaspovar and

Pecs (Hungary). Public resistance to privatization is increasing, for example, in Italy. Figures 11

and 12 show the type of PPP projects in Europe and their current status.

Figure 11: Types of PPP Contracts (Europe)

Figure 12: Status of Contracts (Europe)

Australia

Of the total 16 PPP projects in Australia and New Zealand, 10 are Greenfield projects and 6 are

Management Contracts, with no projects of the other types of models. Except for one project that

has expired, all the rest 15 are currently operational. The main private player in this region is

United Water of Veolia.

5.2 Countries with no PPPs in the Water Sector

In compiling the database, we have observed that in some countries there are no evidences of any

PPP projects in the urban water sector. These countries are shown in Table 3.

Table 3: Countries with no evidence of any PPP projects in the water sector

Region Countries

Africa Angola, Benin, Botswana, Burundi, Democratic Republic of Congo, Equatorial

Guinea, Eritrea, Ethiopia, Lesotho, Liberia, Malawi, Mauritania, Mauritius,

Sierra Leone, Sudan, Swaziland, Togo and Zimbabwe

Asia Brunei, Cambodia, Lao PDR, Myanmar, Singapore and South Korea

Europe Croatia and Denmark

Pacific Fiji, Kiribati, Marshall Islands, Federated States of Micronesia, Nauru, Palau,

Papua New Guinea, Samoa, Solomon Islands, Timor-Leste, Tonga, Tuvalu and

Vanuatu

MENA Bahrain, Djibouti, Iran, Iraq, Israel, Kuwait, Libya, Qatar, Syria, Tunisia,

United Arab Emirates and Yemen

5.3 General Observations

Figure 13 shows the preferences in each of the six regions for the different types of PPP projects

for urban water sector.

Figure 13: Proportions of different types of PPP projects in six regions

From the 672 projects that have been considered from the six regions, it is observed that

strongest preference for concession contracts is found in Latin America. This comes as a surprise

given that less than three decades ago, the Latin American countries had a reputation for

expropriating various investment projects, which eventually led to the development of Calvo

doctrine1 and the subsequent development in international law that investors “shall be paid

appropriate compensation in accordance with international law”, in the event of nationalization2

Next to Latin America, Europe and Asia are the two other regions with the largest number of

PPP projects in urban water being developed under long term concessions. The legal stability of

the countries concerned, the recognition of contractual privity in both civil law and common law

jurisdictions in Europe, and the strong influence of European Union laws and harmonization of

laws and regulations of EU member nations are the likely reasons behind investor and State

confidence in entering into long term concessions.

.

The political developments during the post 1980 period in the Latin American countries where

principles of open economy have been embraced may have contributed to investor confidence in

participating in long term concession contracts in Latin America. Further, the developments in

international law, especially in the area of international investments, where the right to adequate

compensation in the event of expropriation is now recognised and the development of alternative

dispute resolution mechanisms such as arbitration and the recognition of the enforceability of

international arbitration awards following the New York Convention (Convention on the

Recognition and Enforcement of Foreign Arbitral Awards, 1958) by most countries, including

Latin American nations may have contributed towards this trend.

Asia is a rapidly developing region with countries such as China and India during the last decade

and the East Asian nations (tiger economies) in the 1980s showing rapid economic growth. Thus,

it is not surprising that private and public sector entities in the region have not found it too

difficult to agree on long term concessions for developing water infrastructure facilities.

1 The Calvo doctrine was advanced by the Argentine diplomat and legal scholar Carlos Calvo, in his International Law of Europe and America in Theory and Practice (1868). It affirmed that rules governing the jurisdiction of a country over aliens and the collection of indemnities should apply equally to all nations, regardless of size. Further, it stated that foreigners who held property in Latin American states and who had claims against the governments of such states should apply to the relevant courts within such nations for redress instead of seeking diplomatic intervention. 2 In 1974, the UN General Assembly decisively adopted the Charter of Economic Rights and Duties of States, which recognises the “appropriate compensation” standard and provides further that “in any case where the question of compensation gives rise to a controversy, it shall be settled under the domestic law of the nationalizing State and by its tribunals…”

The regions that have preferred models of PPPs other than concessions are MENA and Africa.

Interestingly, whilst MENAs reluctance to go into long term concessions and prefer management

contracts seems to be motivated by the financial capacity of the public sector to finance and own

water infrastructure facilities, whilst engaging the private sector chiefly for technological and

management input, the African region may be suffering from lack of investor confidence in

investing in water infrastructure in a region stricken with poverty and thus the substantial

economic risk involved. Further, the political instability in the region and the lack of appropriate

legal and regulatory environments to support long term commercial contracts may have

contributed towards this trend.

The region that has the largest number of projects falling into the greenfield category is Asia.

The key idea behind developing infrastructure projects following this model is that it creates

win-win options for all stakeholders. For example, whilst the private investors can enter a sector

over which previously there were by state monopolies, the public sector can benefit from private

capital, technology and management. Further, it is a concept that could be defended against

political criticism on the basis that private sector ownership is limited to an agreed number of

years, after which a fully operational project has to be transferred back to the public sector.

Technology transfer and training of a local workforce are other key features of this type of PPPs.

Thus, from a long term development perspective, the Asian region is in a good position to benefit

by having embraced the concept.

Whilst the lack of interest in greenfield type of PPPs in the water sector in Europe and MENA

could be put down to the fiscal capacity in most of the countries in the region to finance and

develop projects on their own or the lack of interest in committing the public sector to take over

and run projects developed and managed by the private sector after a long duration of private

sector operation and management, it is surprising that the Latin American countries have not

shown an interest. The same explanation provided above with regard to long term concessions

could be provided for the lack of greenfield PPPs in the African region.

As far as joint ventures are concerned, none of the six regions considered in this research project

have a significant number of projects developed in the urban water sector. Thus, it could be

concluded that there is an overall reluctance in all six regions for active partnering of public and

private sectors with financial, technological and management contributions from both sides to

develop urban water projects. The preference seems to be for either engaging the private sector

to finance, develop and manage on a long term basis (e.g. concessions, greenfield) or to procure

the services of the private sector to manage and operate a project developed with public sector

funds (e.g. management contracts, service contracts, leases).

As far as divesture is concerned, again, not a significant number of projects have been totally

privatized or subjected to majority share control by the private sector in any of the six regions.

Whilst Africa has no projects falling into this category, likely for the reasons explained above

relating to economic viability and the additional reason of strong political opposition to

nationalization, there are no divestures in MENA, probably for the reason that due to lack of

water as a natural resource in the region, public sector control is of strategic and political

importance. Although there are some divestures in Asia, Latin America and Europe, the number

is insignificant.

5.4 Viability of Concessions

As noted above, the general preference in three of the regions, namely, Latin America, Europe

and Asia seems to develop urban water projects by granting long term concessions to private

sector entities. However, the long duration of concession contracts is an obstacle to competition;

it is difficult to cancel these contracts even where performance is unsatisfactory due to legal

constraints and the administrative processes involved. Further, concessions require private

operators to assume significant financial and foreign exchange risks and long-term commitments.

In the circumstances, in countries suffering from political, economic and/or social instability and

uncertainty, long-term concession contracts may not be the most suitable form of private sector

engagement in the water sector, as many contractual and other disputes could arise at various

points during the long duration of the partnership and parties might find it difficult to resolve

such disputes effectively, thus leading to project interruptions, takeovers and terminations.

Further, historically, large water multinationals have dominated the urban water supply sector

partly owing to colonial structures. However, in recent years, these companies are withdrawing

from the water markets in developing countries due to currency devaluations, economic crises,

over-optimistic projections, and public resistance to price rises, and the impossibility of making

profitable investment in extensions and improvements for poor households who were unable to

pay the full cost of water supplied, without substantial public subsidy.

The above aspects are illustrated by the recent exit of large multinational water companies from

several developing countries (Hall et al. 2010). Some examples provided in the table below.

Table 4: Recent exits of large companies from developing countries

Country Project Date of

Termination

Multinational

involved

Reasons for Termination

Argentina Tucuman 30-year

water concession

contract

2004 Vivendi Poor service quality, high

tariffs, serious operational

failures.

Contract disputes, public

protests, failure of

regulatory body.

Bolivia Cochabamba 40-

year concession

contract

2000 Agua de Tunari

(consortium of

International

Water and

Bechtel)

High water tariffs,

Cochabamba water war in

2000.

Contract disputes, public

protests, failure of

regulatory body.

South

Africa

Fort Beaufort 10-

year concession

contract

2001 WSSA (Suez –

Ondeo)

High water tariffs, poor

service quality.

Contract disputes, public

protests.

Hungary Pecs 25-year

concession

contract

2010 Suez High water tariffs, failure to

fulfill investment

obligations.

Contract disputes.

Colombia Bogota 30-year

Greenfield

contract

2004 Suez Overpricing of water by the

developer led to take over

of the project by the City

council.

Chile Calama 20-year

Greenfield

contract

2006 Biwater Failure to meet the expected

performance standards.

Contract disputes.

Turkey Antalya 10-year

management and

lease contract

2002 Suez High water tariffs.

Contract disputes.

5.5 Cancellations

Regulation forms an integral function of the public/government in the partnership with the

private sector. Unfortunately, in several cases, public authorities are known to have turned their

backs once a PPP contract is signed. In the absence of effective and independent regulation

mechanisms, some cases of bribery/ corruption have been reported. There are also cases of

privatization involving efficient public water utilities. Moreover, confidentiality and secrecy

hamper transparency and deny access to the terms and conditions of contracts that hand over the

management of a public resource to the private sector. In some countries, community

involvement is relatively unknown. As far as the private sector is concerned, poor financial risk

allocation and political and legal instabilities have contributed to early project exits. Overall, all

these factors have contributed to the failure of projects.

The region with the highest percentage of project cancellations is Africa. Again, the reasons

setout above such as economic viability, political instability, and lack of legal and regulatory

infrastructure for long term project success can be listed as the key reasons for the large

percentage of projects cancelled in Africa. Study of the next two regions with the highest

percentage of projects cancellations has shown that public opposition to high prices charged by

the private developers and the political opposition to private sector engagements and the

developing trend of demand for public takeover of privatized or private operated water facilities

are the key contributing factors to project cancellations.

Cancellation of projects in Asia and MENA has been rather low compared to the other regions.

In Asia, the strong legal contracts and the fear of having to pay heavy compensations to investors

in the event of breaching contractual obligations concerning investment guarantees seems to

have contributed to the reluctance to cancel projects. Further, strong investment protection laws

and public interest laws, and the early public activism during the stages of project feasibility

studies and environmental impact assessments, outcomes of which are generally available in the

public domain, seem to filter the project procurement process at an early stage, thus reducing the

reasons for post development project cancellations. In MENA, the fact that only a small

percentage of projects are procured as totally private sector funded projects may be the key

reason behind the low project cancellation.

6. CONCLUSION

In recent times, in many cases, management of urban water facilities has reverted to national/

provincial governments or local municipalities. Further, the departure of international water

companies has provided a window of opportunity for local private companies, who have

emerged as the new owners of the water infrastructure. The domestic private players may be

independent, enter into joint ventures with foreign private companies, or act as subsidiaries of

foreign private companies. Local industrial conglomerates and domestic private companies, who

were already involved in water through construction or consulting / engineering, are also

diversifying into PPPs for urban water supply. They have experience of doing business in their

home country (and so, they are aware of the political environment and customer needs, and they

are able to adapt to social conditions); they tend to adopt a long-term perspective in relation to

their business operations, which is useful for volatile political, social and economic

environments, and they possess investment capacity as a result of access to local financial

markets. Further, they are not affected by foreign exchange rate fluctuations. Thus, many

changes can be expected in the development and management architecture for urban water

projects.

Water has been and will continue to remain a public good. Thus, if PPPs are to be successful in

the urban water sector, it is important for both public sector as well as private sector entities to

understand the relevant constraints applicable to the partnering agreements. It is unlikely,

especially in developing countries, that urban water projects can be developed purely on the

basis of profit making. Long term sustainability of such projects would thus depend on provision

of water to the people being the foremost obligation and educating the people to understand the

scarcity of water and thus the cost of developing infrastructure and the services required for

delivering water to them. If this can be achieved, making a just profit to compensate the investors

who develop the relevant technologies and invest in long term projects in partnership with public

sector entities would not be unachievable.

References

Abdel-Aziz, A.M. 2007. “Successful Delivery of Public-Private Partnerships for Infrastructure

Development”. Journal of Construction Engineering and Management. 133(12), pp 918-931.

Bitran, G. and P. Arellano. 2005. “Regulating Water Services, Sending the Right Signals to

Utilities in Chile”. Public Policy for the Private Sector, World Bank, Note No. 286, March 2005.

Accessed June 06, 2011.

http://rru.worldbank.org/Documents/PublicPolicyJournal/286Bitran_Arellano.pdf

Bruch, C. et al. 2007. “Legal Frameworks Governing Water in the Middle East and North

Africa”. International Journal of Water Resources Development, 23(4), pp 595-624.

Budds, J. and G. McGranahan 2003. “Privatisation and the Provision of Urban Water and

Sanitation in Africa, Asia and Latin America”. International Institute for Environment and

Development, London. Accessed June 06, 2011.

http://www.acquaevita.info/pag/pdf/Water_dp1.pdf

Center for Public Integrity. 2003. The water barons: How a few powerful companies are

privatizing your water. Center for Public Integrity, Washington, D.C.

Department of Economic Affairs, Ministry of Finance, Government of India. 2005. “Scheme for

Support to Public Private Partnership in Infrastructure”. Accessed June 08, 2011.

http://www.pppinindia.com/pdf/PPPGuidelines.pdf

Ford, R. and D. Zussman. 1997. “Alternative Service Delivery: Sharing Governance in Canada”.

Institutes of Public Administration of Canada (IPAC), Toronto.

Global Water Intelligence. 2009. “800m now served by private sector”. 10(1) Accessed June 06,

2011. http://www.globalwaterintel.com/archive/10/11/market-insight/800m-now-served-by-

private-sector.html

Gunawansa, Asanga. 2000. Legal Implications Concerning Project Financing Initiatives in

Developing Countries. Attorney General’s Law Review, July 2000.

Hall, D. and E. Lobina. 2010. “Water companies in Europe 2010”. PSIRU (Public Services

International Research Unit), University of Greenwich. Accessed June 06, 2011.

http://www.psiru.org/reports/2010-W-EWCS.doc

Hall, D., E. Lobina and V. Corral. 2010. “Replacing failed private water contracts”. PSIRU.

PSIRU, University of Greenwich, London.

Harris, S. 2004. “Public Private Partnerships: Delivering Better Infrastructure Services”.

Working Paper, Inter-American Development Bank, Washington, D.C.

HM Treasury, United Kingdom. 1998. “Partnerships for Prosperity: The Private Finance

Initiative”. HM Treasury, London.

Johnstone, N. and L. Wood (eds). (2001). Private Firms and Public Water – Realising Social

and Environmental Objectives in Developing Countries. Cheltenham UK: Edward Elgar.

Jooste, Stephan F. 2008. “Comparing Institutional Forms for Urban Water Supply”. Working

Paper #38, Collaboratory for Research on Global Projects, Stanford CA. Accessed June 06,

2011.

http://crgp.stanford.edu/publications/working_papers/S_Jooste_Inst_Forms_Urban_Water_WP0

038.pdf

Khanom, N.A. 2009. “Conceptual Issues in Defining Public Private Partnership”. Paper

presented at the Asian Business Research Conference 2009, Dhaka, Bangladesh.

KPMG. 2007. Building for Prosperity: Exploring the Prospects for Public Private Partnerships in

Asia Pacific. Accessed June 08, 2011.

www.kpmg.com.sg/publications/Industries_PPPinAsia2007.pdf

Kumaraswamy, M.M. and D.A. Morris. 2002. Build-Operate-Transfer-Type Procurement in

Asian Megaprojects. Journal of Construction Engineering and Management. 128(2), pp 93-102.

Ministry of Finance Singapore. 2009. Government Procurement. Accessed June 06, 2011.

http://app.mof.gov.sg/government_procurement.aspx

Ofwat. 1993. “Privatisation and History of the Water Industry”. Information Note No. 18,

February 1993.

Pinsent Masons LLP. 2011. “Pinsent Masons Water Yearbook 2011 – 2012”. 13th Edition.

Accessed November 15, 2011. http://wateryearbook.pinsentmasons.com/historical_editions.aspx

---. 2010. Pinsent Masons Water Yearbook 2010 – 2010. 12th Edition. Accessed November 15,

2011. http://wateryearbook.pinsentmasons.com/historical_editions.aspx

Savas, E. 2000. Privatisation and Public-Private Partnerships. Chatham House Publishers, New

York.

Transparency International. 2009. “Water Industry Privatization in the Czech Republic: money

down the drain?” Accessed June 06, 2011.

http://www.transparency.cz/pdf/TIC_vodarenstvi_en.pdf

Wolff, G. H. and M. Palaniappan. 2004. Public or Private Water Management? Cutting the

Gordian Knot. Journal of Water Resource Planning and Management, 130(1), pp 1-3.

World Bank. 2006. “Approaches to Private Participation in Water Services – A Toolkit”.

Washington, DC: IBRD/ World Bank.

APPENDIX: DATABASE OF PPP PROJECTS IN THE WATER SECTOR

Keys

Type of PPP:

Greenfield - BOT (Build Own Transfer), BOO (Build Own Operate), BOOT (Build Own Operate Transfer), BMO (Build Manage

Operate), DBO (Design Build Operate), DBFO (Design Build Finance Operate).

Concession – C (Concesssion), BROT (Build Rehabilitate Operate Transfer), ROT (Rehabilitate Operate Transfer), RLT (Rehabilitate

Lease Transfer), TOT (Transfer Operate Transfer).

MC (Management Contract), MC/L (Management Contract cum Lease)

SC (Service Contract)

L (Lease)

A (Affermage)

JV (Joint Venture)

D (Divestiture)

Status:

O (Operational), E (Expired), T (Termination or Remunicipalisation), D (Distressed)

Note: While every effort has been made to make this database as complete and accurate as possible, lack of availability of data from

secondary sources and discrepancies of data between sources may lead to gaps or inaccuracies in certain cases.

Africa

AFRICA Sl. Country City Duration Type

of PPP Project name/ Company Private players Status

1 Burkina Faso 2001 - 2006

SC Veolia Water, Cabinet Mazars and Guerard

O

2 Cameroon Nationwide 2007 - 2017

MC/L Camerounaise des Eaux Office National de l’Eau Potable (ONEP, 33%), Delta Holding SA (33%), Caisse de Dépôt et de Gestion (33%) and Ingema (1%), all Morocco

O

3 Cameroon 2000 - 2020

C Societe Nationale des Eaux du Cameroun (SNEC); since 2006, Cameroon Water Utilities Corporation (CAMWATER)

Suez (51%) O

4 Central African Republic

Bangui 1991 - 2006

MC/L Societe de Distribution d’Eau en Centrafrique (SODECA)

Saur (51%) T

5 Cote d'Ivoire Abidjan 1959, 1987 - 2007

L, then C

Societe Distribution d'Eau de Cote d'Ivoire (SODECI)

Finagestion (45%), SAUR (47%) and Government (8%)

O

6 Cote d'Ivoire Nationwide 1987 - 2007

MC/L Societe Distribution d'Eau de Cote d'Ivoire (SODECI)

Saur International, France (47%) E

7 Cote d'Ivoire Nationwide 2008 - 2032

MC/L Societe Distribution d'Eau de Cote d'Ivoire (SODECI)

Bouygues (46%, France) O

8 Guinea Conakry and 16 towns 1989 - 2011

MC/L Societe de Exploitation des Eaux de Guinee (SEEG)

SAUR & Vivendi (51%) T

9 Kenya Malindi 1999 - 2005

MC/L Malindi water utility contract H.P. Gauff Ingenieure (100%, Germany)

E

10 Kenya Malindi 1995 - 1999

SC H.P. Gauff Ingenieure (Germany) E

11 Mali Bamako and 16 urban centres [water and electricity]

2000 C Energie de Mali (EDM) 60% of EDM - SAUR (65%)/ IPS West Africa (35%)

T

12 Mali 1995 MC Energie de Mali (EDM) SAUR-EDF- Hydroquebec/CRC-Cogema

T

13 Mozambique Beira, Quelimane, Nampula, & Pemba

1999 - 2008

MC/L Aguas de Mozambique

Aguas de Portugal (73%) and Mazi-Mozambique (23%)

E

Africa

14 Mozambique Maputo 1999 - 2014

MC/L Aguas de Mocambique [5 national organisations included]

SAUR (38%) and Aguas de Portugal (32%)

O

15 Mozambique Matola 1999 - 2014

MC/L SAUR (38%) and Aguas de Portugal (32%)

O

16 Namibia Windhoek 2001 - 2021

MC/L Goreangab Water Plant Berlinwasser International AG (33%), Va Tech Wabag (33%) and Veolia Environnement (34%)

O

17 Niger Nationwide 2001 - 2011

MC/L Societe d'exploitation des eaux du Niger (SEEN)

Veolia Water AMI (51% ) O

18 Republic of Congo

Brazzaville 2002 - 2004

MC/L Societe Nationale de Distribution d'Eau (SNDE)

Biwater plc (100%) E

19 Senegal Dakar 1996 - 2006

MC/L Sénégalaise des Eaux (SdE) [local investors (+30%), employees and Senegal govt.]

Bouygues (57.8%) E

20 Senegal Dakar 2006 - 2012

MC/L Sénégalaise des Eaux (SdE) [local investors (+30%), employees and Senegal govt.]

Bouygues (57.8%) O

21 South Africa Dolphin Coast, iLembe District Municipality

1999 - 2029

ROT Siza Water Company Biwater (73%) and Metropolitan Life Lrd. (23%)

O

22 South Africa Johannesburg 2001 - 2006

MC/L Johannesburg Water Company Water and Sanitation Services South Africa (WSSA), a joint venture between Suez (ex-Lyonnaise des Eaux), its subsidiary Northumbrian Water Group and the South African company Group 5

E

23 South Africa Maluti-a-Phofung 2006 - 2011

MC/L Maluti-a-Phofung Water (Pty) Ltd

Uzinzo Services (JV of Amanz’ abantu Services (Eastern Cape) & WSSA)

O

24 South Africa Nelspruit, Mbombela 1999 - 2029

BROT Greater Nelspruit Utility Company (GNUC); later Silulumanzi

Cascal (Biwater) (40%), operating through Metsi a Sechaba, its JV with a local black empowerment group

O

25 South Africa Nkonkobe municipality 1995 - 2005

MC/L Water and Sanitation Services South Africa Ltd, (Fort Beaufort)

Suez (50%) and Everite (50%) T

26 South Africa Queenstown 1992 - 2017

MC/L Water and Sanitation Services South Africa Ltd (Queenstown)

Suez (50%) and Everite (50%) O

Africa

27 South Africa Stutterheim (Amahthali) 1993 - 2003

L Water and Sanitation Services South Africa Ltd (Stutterheim)

Suez (50%) and Everite (50%) E

28 Sudan Khartoum 2008 - 2021

DBO Biwater Holdings Limited O

29 Tanzania Dar-es-Salaam 2003 - 2013

MC/L Dar es Salaam Water Distribution

Biwater (UK 25.5%), Gauff Engineers (Germany 25.5%) and Superdoll (Tanzania 49%)

T

30 Uganda Kampala 1998 - 2001

MC/L Kampala Revenue Improvement Project

H.P. Gauff Ingenieure (100%, Germany)

E

31 Uganda Kampala 2002 - 2004

MC/L Ondeo Services Uganda Limited (OSUL)

Suez (100%) E

32 Zambia Nkana, Konkola, Nchanga, Mufulira, and Luanshya (mine townships)

2001 - 2005

MC/L AHC Mining Municipal Services Limited (AHC-MMS)

Saur (100%) E

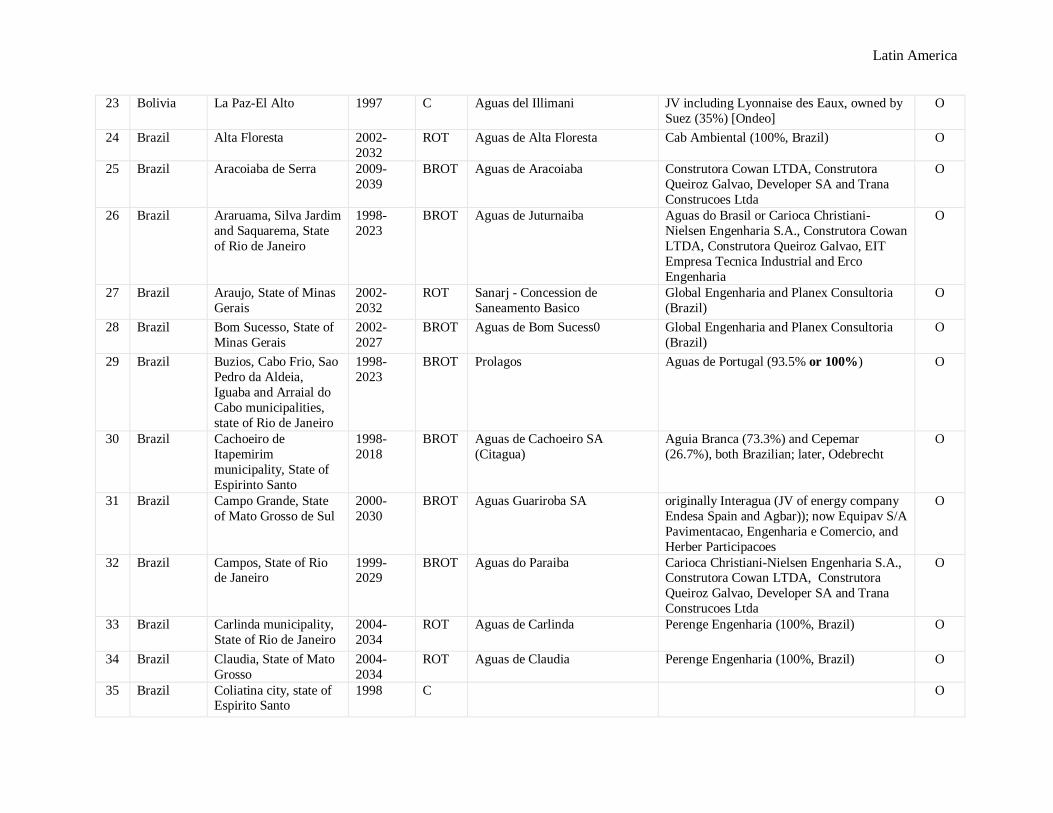

Latin America

LATIN AMERICA

Sl. Country City Duration Type of PPP

Project Name/ Company Private Players Status

1 Argentina Balcarce, Buenos Aires province

1994-2014

BROT Aguas de Balcarce, S.A. Camuzzi Gazometri SpA, Italy (70%) and Global Water Investments, LLC, Argentina (30%)

O

2 Argentina Buenos Aires city 1993-2023

BROT Aguas Argentinas S.A. (AASA) Lyonnaise des Eaux (Suez Group, 46.3%), Compagnie Generale des Eaux S.A. (Veolia Group), Anglian Water PLC, Aguas de Barcelona S.A. (23%), and local partners

O

3 Argentina Buenos Aires province (7 municipalities - Merlo, Moreno, San Miguel, General Rodriguez, Escobar, Malvinas Argentinas y Jose C P)

2000-2030

BROT Aguas del Gran Buenos Aires [employees (10%)]

Impregilo SpA, Italy (43%), ACS Group (Actividades de Construccion y Servicios) or Dragados, Spain (27%), Aguas de Bilbao Bizkaia, Spain (20%)

O

4 Argentina Campana, Buenos Aires province

1998-2027

BROT Aguas de Campana, S.A. Contreras Hermanos SA (51%) and Esuco SA (49%), both Argentinian

O

5 Argentina Clorinda, Formosa province

1995-2025

ROT Aguas de Formosa [province (10%)]

SAGUA Internacional, S.A. (South Water, 80%; Agbar, 15%; Suez, 5%)

O

6 Argentina Cordoba 1997-2027

BROT Aguas Cordobesas [only for water services]

consortium of Suez-Lyonnaise des Eaux and Agbar (56.5%)

O

7 Argentina Corrientes province 1991-2021

BROT Aguas de Corrientes consortium led by Thames Water, UK O

8 Argentina Formosa 1995-2025

ROT Aguas de Formosa Phoenix, Sagua International SA and Simali, all Argentinian

O

9 Argentina Greater Buenos Aires province (60 municipalities)

1999-2029

ROT Azurix Buenos Aires S.A. Azurix, a unit of Enron (100%, US) O

10 Argentina La Rioja 2002-2032

BROT Aguas de la Rioja, SA Latin Aguas (100%, Argentina) E

11 Argentina La Rioja 1999-2002

MC Aguas de la Rioja SA Latin Aguas (100%) E

12 Argentina Laprida, Buenos Aires province

1996-2016

BROT Aguas de Laprida, SA Camuzzi Gazometri SpA, Italy = 100% O

Latin America

13 Argentina Mendoza province 1998 ROT Obras Sanitarias de Mendoza (OSM) [The province controls 20% and the employees control 10%]

Enron-led consortium Inversores del Aconcagua (50%), which is made up of US firm Enron (57.5 %), the French firm SAUR International (17.5%), Italgas (5%) and Argentine investors (20%); operating company called Aguas de Mendoza, which is fully owned by Saur International owns 20%, now 32%

O

14 Argentina Pilar municipality, Buenos Aires province

1992-2016

ROT Sudamericana de Aguas, S.A. Sudamericana de Aguas, S.A. (80%) O

15 Argentina Posadas and Garupa cities, Misiones province

1999-2029

BROT Servicios de Aguas de Misiones SA (SAMSA)

Urbaser (27%), Dragados (18%), Urbaser Argentina (45%) and workers (10%); now ACS Group (Actividades de Construccion y Servicios) (90%, Spain)

O

16 Argentina Salta province 1998-2028

BROT Aguas de Salta S.A. (ASSA) (later SPASSA)

MECON, S.A.; later, Sociedad Prestadora Aguas de Salta, S.A. (JCR SA (45%); Latinaguas (45%), both Argentinian)

O

17 Argentina San Fernando del Valle de Catamarca, Valle Viejo, and Fray Mamerto Esquiu, Catamarca province

2000-2030

ROT Obras Sanitarias de Catamarca Aguas del Valle [Proactiva Medio Ambiente (joint subsidiary of Fomento de Construcciones y Contratas (FCC) and Veolia), 50:50]

O

18 Argentina Santa Fe province (15 districts)

1995-2025

BROT Aguas Provinciales de Santa Fe Suez-Lyonnaise des Eaux S.A. (51.69%), Aguas de Barcelona S.A. (10.89%), Interagua – Servicio Integral de Agua S.A. (14.92%), Banco de Galicia y Buenos Aires S.A. (12.5%) and Aguas Provinciales de Santa FE's employees (10%).

O

19 Argentina Santiago del Estero province (4 cities)

1997-2027

BROT Aguas de Santiago, SA Dipos (Cast TV SA (15%); Curi Hermanos SA (15%); Editorial El Liberal SRL (15%); Sagua International SA (45%), all Argentinian

O

20 Argentina Tucuman province 1995-2025

BROT Aguas del Aconquija consortium led by Compagnie Générale des Eaux (90%)

O

21 Belize National 2001 partial D

Belize Water Supply Limited Cascal/ Biwater, UK (45%) and Nuon, Netherlands (45%)

O

22 Bolivia Cochabamba 1999 C Aguas del Tunari consortium of International Water Ltd. (55%) (Bechtel (US) and Edison (Italy)), Riverstar International (25%) and four Bolivian companies (20%)

O

Latin America

23 Bolivia La Paz-El Alto 1997 C Aguas del Illimani JV including Lyonnaise des Eaux, owned by Suez (35%) [Ondeo]

O

24 Brazil Alta Floresta 2002-2032

ROT Aguas de Alta Floresta Cab Ambiental (100%, Brazil) O

25 Brazil Aracoiaba de Serra 2009-2039

BROT Aguas de Aracoiaba Construtora Cowan LTDA, Construtora Queiroz Galvao, Developer SA and Trana Construcoes Ltda

O

26 Brazil Araruama, Silva Jardim and Saquarema, State of Rio de Janeiro

1998-2023

BROT Aguas de Juturnaiba Aguas do Brasil or Carioca Christiani-Nielsen Engenharia S.A., Construtora Cowan LTDA, Construtora Queiroz Galvao, EIT Empresa Tecnica Industrial and Erco Engenharia

O

27 Brazil Araujo, State of Minas Gerais

2002-2032

ROT Sanarj - Concession de Saneamento Basico

Global Engenharia and Planex Consultoria (Brazil)

O

28 Brazil Bom Sucesso, State of Minas Gerais

2002-2027

BROT Aguas de Bom Sucess0 Global Engenharia and Planex Consultoria (Brazil)

O

29 Brazil Buzios, Cabo Frio, Sao Pedro da Aldeia, Iguaba and Arraial do Cabo municipalities, state of Rio de Janeiro

1998-2023

BROT Prolagos Aguas de Portugal (93.5% or 100%) O

30 Brazil Cachoeiro de Itapemirim municipality, State of Espirinto Santo

1998-2018

BROT Aguas de Cachoeiro SA (Citagua)

Aguia Branca (73.3%) and Cepemar (26.7%), both Brazilian; later, Odebrecht

O

31 Brazil Campo Grande, State of Mato Grosso de Sul

2000-2030

BROT Aguas Guariroba SA originally Interagua (JV of energy company Endesa Spain and Agbar)); now Equipav S/A Pavimentacao, Engenharia e Comercio, and Herber Participacoes

O

32 Brazil Campos, State of Rio de Janeiro

1999-2029

BROT Aguas do Paraiba Carioca Christiani-Nielsen Engenharia S.A., Construtora Cowan LTDA, Construtora Queiroz Galvao, Developer SA and Trana Construcoes Ltda

O

33 Brazil Carlinda municipality, State of Rio de Janeiro

2004-2034

ROT Aguas de Carlinda Perenge Engenharia (100%, Brazil) O

34 Brazil Claudia, State of Mato Grosso

2004-2034

ROT Aguas de Claudia Perenge Engenharia (100%, Brazil) O

35 Brazil Coliatina city, state of Espirito Santo

1998 C O

Latin America

36 Brazil Colider 2002-2032

BROT Colider Agua e Saneamento Ltda

Cab Ambiental (100%, Brazil) O

37 Brazil Comodoro 2007-2037

BROT Empresa Águas de Comodoro Ltda

Agrimat Engenharia Industria e Comercio (100%, Brazil)

O

38 Brazil Curitiba, State of Parana

2001 C O

39 Brazil Guapimir municipality, State of Rio de Janeiro

2004-2024

ROT Fontes da Serra Saneamento de Guapimirim Ltda

Emissao Engenharia (Brazil) O

40 Brazil Guara, State of Sao Paulo

2000-2025

ROT Aguas de Guara Hidrogesp (100%, Brazil) O

41 Brazil Guaranta do Norte municipality, State of Rio de Janeiro

2001-2031

ROT Aguas de Guaranta Ltda Perenge Engenharia (Brazil) O

42 Brazil Guariroba, Campo Grande, Mato Grosso

2000 - 2030

BROT Aguas de Guariroba 50% owned by Agbar, 41% by Cobel, and 9% by Mato Grosso state water company Sanesul

O

43 Brazil Itapema, State of Santa Catarina

2004-2029

ROT Aguas de Itapema Construtora Nascimento and Linear Participacoes e Construcoes de Cuiaba

O

44 Brazil Juturnaiba 1998 BROT Aguas de Juturnaiba Aguas de Juturnaiba (Carioca Christiani-Nielsen Engenharia S.A., Brazil; Construtora Cowan LTDA, Brazil; Construtora Queiroz Galvao, Brazil; EIT Empresa Tecnica Industrial; Erco Engenharia)

O

45 Brazil Limeira, State of Sao Paulo

1995-2025

ROT Aguas de Limeira SA consortium of Odebrecht, Brazil and Suez (50:50)

O

46 Brazil Machado & Baguacu 1996 - 2021

C Aguas de SANEAR (Saneamento de Araçatuba, S.A.)

Sacyr Vallehermoso‘s Somague – AGS (54%)

O

47 Brazil Manaus, State of Amazonas

2000-2030

BROT Aguas de Amazonas or Manaus Saneamento

Suez O

48 Brazil Mandaguahy 1995 - 2015

C Aguas de Mandaguahy Sacyr Vallehermoso‘s Somague – AGS (85%)

O

49 Brazil Marcelandia 2003-2033

BROT Aguas de Marcelandia Construtora Nascimento (100%, Brazil) O

50 Brazil Marilia, State of Sao Paolo

1997-2017

BROT Aguas de Marilia Hidrogesp, Paineira Participacoes, Telar, all Brazilian

O

51 Brazil Marinique, State of Sao Paolo

1997-2027

BROT Ciagua Concessionaria de Aguas de Mairinque

Villa Nova Engenharia O

Latin America

52 Brazil Matupa municipality, State of Rio de Janeiro

2001-2031

ROT Aguas de Matupa Perenge Engenharia (100%, Brazil) O

53 Brazil Minas Gerais, State of 2006 partial D

Companhia de Saneamento de Minas Gerais (Copasa)

O

54 Brazil Mineiros do Tietê municipality, State of Sao Paulo

1995-2015

BROT Saneciste Sacyr Vallehermoso SA (SyV) (60%, Spain) O

55 Brazil Mirassol municipality, State of Sao Paulo

2008-2038

BROT Paz Gestao Ambiental Paz Construcao e Prestacao de Servicoes Publicos Ltda (100%, Brazil)

O

56 Brazil Mirassol municipality, State of Sao Paulo

2001-2006

ROT Sanessol Cab Ambiental (90%, Brazil) O

57 Brazil Niteroi, State of Rio de Janeiro

1999-2029

BROT Aguas de Niteroi Carioca Christiani-Nielsen Engenharia S.A., Construtora Cowan LTDA, Construtora Queiroz Galvao and EIT Empresa Tecnica Industrial

O

58 Brazil Nobres, State of Mato Gross

1999-2029

BROT Empresa de Saneamento de Nobres

Encomind Engenharia Comercio e Industria, Brazil

O

59 Brazil Nova Canaa do Norte 2009-2039

BROT Aguas de Canaa Engenharia e Comercio Govic Ltda and Perenge Engenharia (Brazil)

O

60 Brazil Nova Friburgo, State of Rio de Janeiro

1999-2024

BROT Concessionaria de Aguas e Esgotos de Nova Friburgo Ltda (Caenf)

Tyco International, USA O

61 Brazil Novo Progresso, State of Para

1994-2034

ROT Aguas de Novo Progresso Perenge Engenharia (100%, Brazil) O

62 Brazil Ourinhos municipality 1996-2011

BROT Aguas de Esmeralda Hidrogesp, Brazil and Tyco International, USA

O

63 Brazil Paraguacu, State of Minas Gerais

2000-2030

BROT Cosagua Global Engenharia and Planex Consultoria (Brazil)

O

64 Brazil Paranagua state 1997-2027

BROT Aguas de Paranagua S.A. Cab Ambiental (100%) or Carioca Christiani-Nielsen Engenharia S.A., Brazil = 38%; Construtora Castilho de Porto Alegre SA, Brazil = 42%

O

65 Brazil Peixoto de Azevedo 2000-2030

BROT Aguas de Peixoto de Azevedo Construtora Nascimento (100%, Brazil) O

66 Brazil Pereiras municipality, State of Sao Paulo

1994-2017

BROT Pereiras Water Company Novacon, Brazil O

Latin America

67 Brazil Petropolis city, State of Rio de Janeiro

1998-2028

BROT Aguas do Imperador Carioca Christiani-Nielsen Engenharia S.A., Brazil; Construtora Cowan LTDA, Brazil; Construtora Queiroz Galvao, Brazil; EIT Empresa Tecnica Industrial

O

68 Brazil Pontes e Lacerda 2000-2031

BROT Aguas de Pontes e Lacerda Cab Ambiental (100%, Brazil) O

69 Brazil Primavera do Leste municipality, State of Rio de Janeiro

2000-2031

BROT Aguas de Primavera Primavera do Leste (100%, Brazil) O

70 Brazil Resende, State of Rio de Janeiro

2008-2038

BROT Aguas das Agulhas Negras Carioca Christiani-Nielsen Engenharia S.A., Construtora Queiroz Galvao and Trana Construcoes Ltda, all Brazilian

O

71 Brazil Ribeirao de Pantano, state of Sao Paulo

1996-2016

BROT Empresa de Saneamento de Tuiuti

Novacon, Brazil O

72 Brazil Sanepar, Parana state 1998 partial D

Companhia de Saneamento do Paraná (SANEPAR)

52.5% owned by the Parana state and 34.7% by the consortium Domino Holding, including French water MNC Veolia and the Brazilian Andrade Gutierrez Group

O

73 Brazil Santa Carmem 2002-2032

BROT Aguas de Santa Carmem Construtora Nascimento (100%, Brazil) O

74 Brazil Santo Antonio de Padua municipality, State of Rio de Janeiro

2004-2034

ROT Aguas de Santo Antonio Aguas de Santo Antonio (100%) O

75 Brazil Sao Carlos, State of Sao Paulo

1994-2004

ROT Sao Carlos Water System - DH Perfuracao de Pocos

Hidrogesp, Brazil O

76 Brazil Sao Paulo state 2007-2037

BROT Aguas de Itu Exploracao de Servicos de Agua e Esgoto SA

Grupo Equipav (100%, Brazil) O

77 Brazil Serrana, State of Sao Paolo

2000-2030

BROT Bela Fonte Saneamento Ltda Novacon, Brazil O

78 Brazil Sorriso, State of Mato Grosso

2000-2030

ROT Aguas de Sorriso Perenge Engenharia (Brazil) O

79 Brazil Tambau, State of Sao Paulo

2000-2030

BROT Rio Pardo Operadores Novacon, Brazil O

80 Brazil Tangara da Serra 2001 C O 81 Brazil Tocantins state 1999 partial

D Empresa de Saneamento do Tocantins (Saneatins)

Empresa Sul-Americana de Montagem S.A., Brazil

O

82 Brazil Tucurui municipality, PA

1999-2019

BROT Aguas de Tucurui Hidrogesp, Brazil T

Latin America

83 Brazil Uniao do Sul 2000-2030

BROT Aguas de Uniao do Sul Construtora Nascimento (100%, Brazil) T

84 Brazil Veracruz state 2004-2034

BROT Aguas de Vera Abastecimento e Distribuicao Ltda

Construtora Nascimento (100%, Brazil T

85 Chile Litoral Sur, Region V 1993-2028

BROT Aguesquinta, SA Agbar (70%, Spain) and Chilquinta (30%, Chile)

T

86 Chile Lo Barenchea community, Region M

1995- BROT Servicions de Agua Potable Barnechea SA

Biwater (100%, UK) T

87 Chile Pudahuel district of the Metropolitan Region

2007-2023

BROT Izarra de Lo Aguirre Water Concession

Empresa de Agua Potable Izarra de Lo Aguirre SA (100%)

T

88 Chile Region I 2004-2034

ROT Empresa de Servicios Sanitarios de Tarapacá S.A. (ESSAT) or Aguas del Altiplano

Inmobiliaria Punta de Rieles, a subsidiary of Grupo Solari (100%, Chile) T

89 Chile Region II 2003-2033

ROT Empresa de Servicios Sanitarios de Antofagasta S.A. (ESSAN) or Aguas de Antofagasta

Grupo Luksic (65%, Chile) T

90 Chile Region III 2004-2034

BROT Empresa de Servicios Sanitarios de Atacama S.A. (EMSSAT) or Aguas Chanar

Consorcio Aguas Norte Grande (Hydrosan, Chile = 45%; Icafal, Chile = 45%; Vecta, Chile = 10%)

O

91 Chile Region IV 2004-2034

ROT Empresa de Servicios Sanitarios de Coquimbo S.A.(ESSCO) or Aguas del Valle, SPV created by ESVAL

Consorcio Financiero S.A. - now, Fernandez Hurtado; Ontario Teachers Pension Plan, Canada = 69.4%

O

92 Chile Region IX 2004-2034

BROT Empresa de Servicios Sanitarios de La Araucanía S.A. (ESSAR) or Aguas Araucania

grupo Solari (100%) O

93 Chile Region M: Greater Santiago Metropolitan Region

1999 partial D