Private Equity Spotlight - Preqindocs.preqin.com/newsletters/pe/SpotlightOctober2006.pdf · A...

13

Dear Spotlight Reader, Welcome to October’s new look Spotlight, redesigned to bring you the same unique quality content in a fresh new format. This month’s edition brings you vital insights on a range of topics: We hope that you like the new Spotlight – as ever, we welcome your feedback and suggestions. Subscribers to our online services will also notice that these have been completely redesigned. The new website brings you: If you haven’t yet tried out Performance Analyst, Funds in Market and Investor Intelligence why not arrange trial access at no cost or obligation – please call +44 (0)20 7038 1650 or visit www.preqin.com With kindest regards from all of us at Private Equity Intelligence, Mark O’Hare Managing Director Private Equity Spotlight Buyouts Dealflow: new analysis from Dealogic on the continuing pace of global buyouts deal activity. Carry Review: how much carry has the industry earned in recent years, and how does 2006 compare with 2005? Where has most wealth been generated for LPs and GPs alike? Q3 Fundraising Update: details on the booming fundraising market as commitments made in 2006 exceed $300 billion for the first time in the history of the industry Enhanced Navigation and Speed: easier and quicker to find precisely the data you need. New Features: e.g. see at a glance which LP profiles on Investor Intelligence have been updated during the past month. New Data: Performance Analyst now includes information from Dealogic on the latest deals done by all the leading firms. More Funds: Performance Analyst now has returns data for over 3,000 funds. • • • • • • •

Transcript of Private Equity Spotlight - Preqindocs.preqin.com/newsletters/pe/SpotlightOctober2006.pdf · A...

Dear Spotlight Reader,

Welcome to October’s new look Spotlight, redesigned to bring you the same unique quality content in a fresh new format.This month’s edition brings you vital insights on a range of topics:

We hope that you like the new Spotlight – as ever, we welcome your feedback and suggestions.

Subscribers to our online services will also notice that these have been completely redesigned. The new website bringsyou:

If you haven’t yet tried out Performance Analyst, Funds in Market and Investor Intelligence why not arrange trial accessat no cost or obligation – please call +44 (0)20 7038 1650 or visit www.preqin.com

With kindest regards from all of us at Private Equity Intelligence,

Mark O’HareManaging Director

Private EquitySpotlight

Buyouts Dealflow: new analysis from Dealogic on the continuing pace of globalbuyouts deal activity.

Carry Review: how much carry has the industry earned in recent years, and howdoes 2006 compare with 2005? Where has most wealth been generated for LPsand GPs alike?

Q3 Fundraising Update: details on the booming fundraising market ascommitments made in 2006 exceed $300 billion for the first time in the history ofthe industry

Enhanced Navigation and Speed: easier and quicker to find precisely the datayou need.

New Features: e.g. see at a glance which LP profiles on Investor Intelligencehave been updated during the past month.

New Data: Performance Analyst now includes information from Dealogic on thelatest deals done by all the leading firms.

More Funds: Performance Analyst now has returns data for over 3,000 funds.

•

•

•

•

•

•

•

Private EquitySpotlight October 2006 / Volume 2 - Issue 10

FEATURE ARTICLE page 02

Private Equity as an M&A

Market Driver:

Private equity’s continuing

growth has transformed it into

a key driver of worldwide M&A

activity. Salim Mohammed of

Dealogic digs beneath the

surface to identify some of the

key trends at work – and

debunks some popular myths.

PERFORMANCE SPOTLIGHT page 04

Using data taken from our forthcoming publication The 2006

Carry Review, we examine private equity’s performance in

creating value added for LPs and Carry for GPs.

GLOBAL FUNDRAISING UPDATE Q3 page 07

Fundraising in 2006 has smashed all previous records, with

436 funds already achieving final closes raising an aggregate

$300 billion to date. Our third quarterly review of 2006

examines another excellent period for private equity

fundraising.

NEW

The 2006 Carry Review

More information available at:

www.preqin.com/CARRY

No. of Funds onRoad US

197

103

67

59

47

473

Venture

Buyout

Funds of Funds

Other

Real Estate

Total

77

48

35

16

10

186

90

39

9

7

10

155

364

190

111

82

67

814

Europe ROW

INVESTOR NEWS page 16

All the latest news on investors in private equity:

• Railways Pension Trustee Company (Railpen) increases

private equity allocation.

• LACERA doubles commitment to private equity real estate

funds.

• Pension Benefits Guaranty Corp. (PBGC) to auction off $1

billion worth of private equity fund stakes.

INVESTOR SPOTLIGHT page 14

This month we focus on investors in secondaries funds

• Who are the most active LPs in secondaries?

• Why are they investing in secondaries?

• Where are they investing?

SUBSCRIPTIONS

If you would like to receive Private Equity Spotlight each month

please email [email protected].

Subscribers to Performance Analyst and Investor Intelligence

receive additional information not available in the free version.

If you would like further details please email [email protected]

Publisher: Private Equity Intelligence Ltd

10 Old Bailey, London EC4M 7NG. Tel: +44 (0)207 038 1650

Welcome to the latest edition of Private Equity Spotlight, the monthly newsletter fromPrivate Equity Intelligence, providing insights into private equity performance,investors and fund raising. Private Equity Spotlight combines information from ouronline products Performance Analyst, Investor Intelligence and Funds in Market.

• PERFORMANCE • INVESTORS • FUND RAISING • FUND TERMS

Total

A benchmark transaction in the eighties, the RJR Nabisco deal

brought the concept of the LBO to main street and spawned a

must read book for every banker working on Wall Street:

Barbarians at the Gate.

It took over fifteen years for the mega-buyout to return. Private

equity firms have steadily increased their spending power in the

last five years, but with eleven buyout bids of $10 billion or more

announced in the last eighteen months, they have made their

presence felt even more. With blockbuster deals announced

every few weeks, many have begun to ask if this is the making

of another buyout bubble. Or, if we are already in the midst of

the bubble, when will it burst?

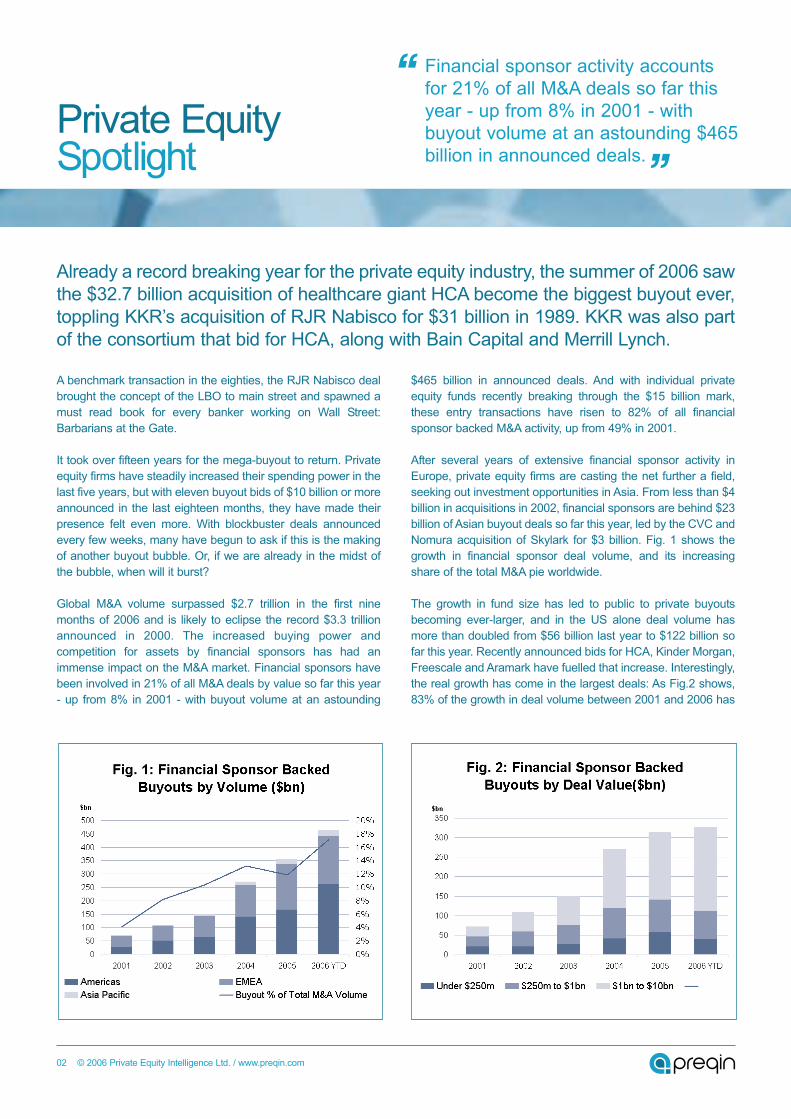

Global M&A volume surpassed $2.7 trillion in the first nine

months of 2006 and is likely to eclipse the record $3.3 trillion

announced in 2000. The increased buying power and

competition for assets by financial sponsors has had an

immense impact on the M&A market. Financial sponsors have

been involved in 21% of all M&A deals by value so far this year

- up from 8% in 2001 - with buyout volume at an astounding

$465 billion in announced deals. And with individual private

equity funds recently breaking through the $15 billion mark,

these entry transactions have risen to 82% of all financial

sponsor backed M&A activity, up from 49% in 2001.

After several years of extensive financial sponsor activity in

Europe, private equity firms are casting the net further a field,

seeking out investment opportunities in Asia. From less than $4

billion in acquisitions in 2002, financial sponsors are behind $23

billion of Asian buyout deals so far this year, led by the CVC and

Nomura acquisition of Skylark for $3 billion. Fig. 1 shows the

growth in financial sponsor deal volume, and its increasing

share of the total M&A pie worldwide.

The growth in fund size has led to public to private buyouts

becoming ever-larger, and in the US alone deal volume has

more than doubled from $56 billion last year to $122 billion so

far this year. Recently announced bids for HCA, Kinder Morgan,

Freescale and Aramark have fuelled that increase. Interestingly,

the real growth has come in the largest deals: As Fig.2 shows,

83% of the growth in deal volume between 2001 and 2006 has

Private EquitySpotlight

02 © 2006 Private Equity Intelligence Ltd. / www.preqin.com

Already a record breaking year for the private equity industry, the summer of 2006 sawthe $32.7 billion acquisition of healthcare giant HCA become the biggest buyout ever,toppling KKR’s acquisition of RJR Nabisco for $31 billion in 1989. KKR was also partof the consortium that bid for HCA, along with Bain Capital and Merrill Lynch.

Financial sponsor activity accountsfor 21% of all M&A deals so far thisyear - up from 8% in 2001 - withbuyout volume at an astounding $465billion in announced deals.

come from deals above $1 billion. Smaller and mid-market deals

have seen growth too, but nothing like the explosion of activity

in $1 billion-plus deals.

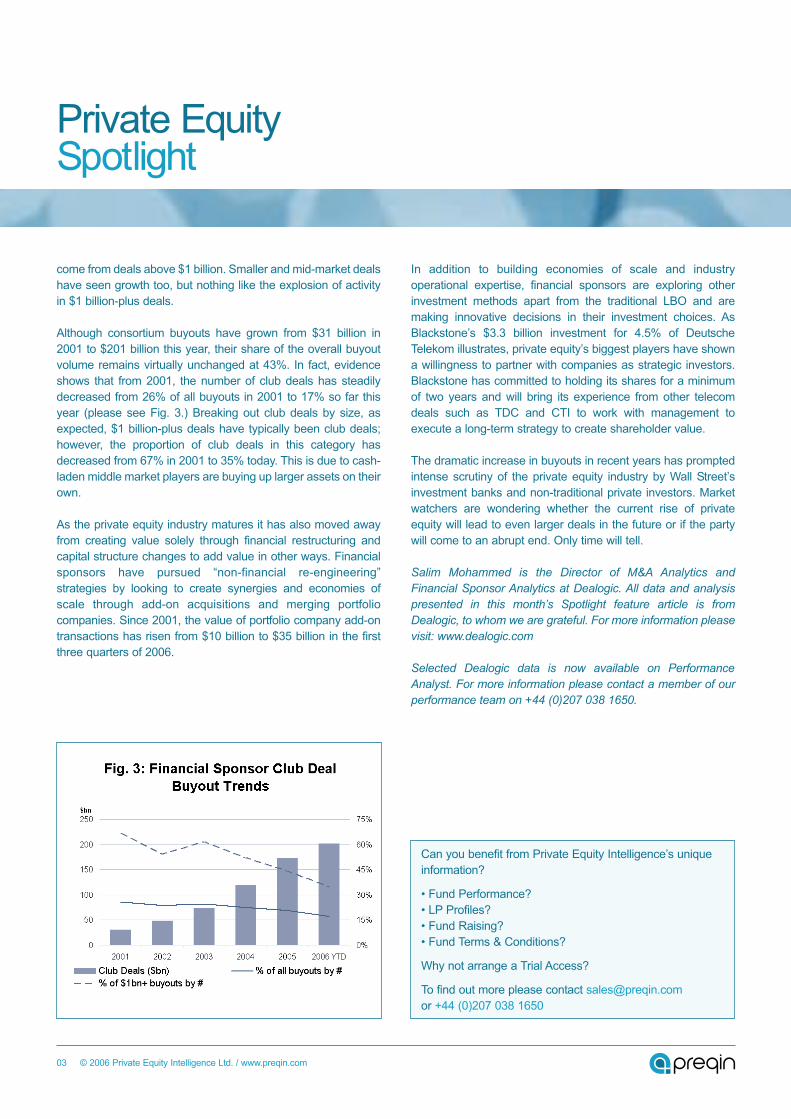

Although consortium buyouts have grown from $31 billion in

2001 to $201 billion this year, their share of the overall buyout

volume remains virtually unchanged at 43%. In fact, evidence

shows that from 2001, the number of club deals has steadily

decreased from 26% of all buyouts in 2001 to 17% so far this

year (please see Fig. 3.) Breaking out club deals by size, as

expected, $1 billion-plus deals have typically been club deals;

however, the proportion of club deals in this category has

decreased from 67% in 2001 to 35% today. This is due to cash-

laden middle market players are buying up larger assets on their

own.

As the private equity industry matures it has also moved away

from creating value solely through financial restructuring and

capital structure changes to add value in other ways. Financial

sponsors have pursued “non-financial re-engineering”

strategies by looking to create synergies and economies of

scale through add-on acquisitions and merging portfolio

companies. Since 2001, the value of portfolio company add-on

transactions has risen from $10 billion to $35 billion in the first

three quarters of 2006.

In addition to building economies of scale and industry

operational expertise, financial sponsors are exploring other

investment methods apart from the traditional LBO and are

making innovative decisions in their investment choices. As

Blackstone’s $3.3 billion investment for 4.5% of Deutsche

Telekom illustrates, private equity’s biggest players have shown

a willingness to partner with companies as strategic investors.

Blackstone has committed to holding its shares for a minimum

of two years and will bring its experience from other telecom

deals such as TDC and CTI to work with management to

execute a long-term strategy to create shareholder value.

The dramatic increase in buyouts in recent years has prompted

intense scrutiny of the private equity industry by Wall Street’s

investment banks and non-traditional private investors. Market

watchers are wondering whether the current rise of private

equity will lead to even larger deals in the future or if the party

will come to an abrupt end. Only time will tell.

Salim Mohammed is the Director of M&A Analytics andFinancial Sponsor Analytics at Dealogic. All data and analysispresented in this month’s Spotlight feature article is fromDealogic, to whom we are grateful. For more information pleasevisit: www.dealogic.com

Selected Dealogic data is now available on PerformanceAnalyst. For more information please contact a member of ourperformance team on +44 (0)207 038 1650.

Private EquitySpotlight

Can you benefit from Private Equity Intelligence’s unique

information?

• Fund Performance?

• LP Profiles?

• Fund Raising?

• Fund Terms & Conditions?

Why not arrange a Trial Access?

To find out more please contact [email protected]

or +44 (0)207 038 1650

03 © 2006 Private Equity Intelligence Ltd. / www.preqin.com

PerformanceSpotlight

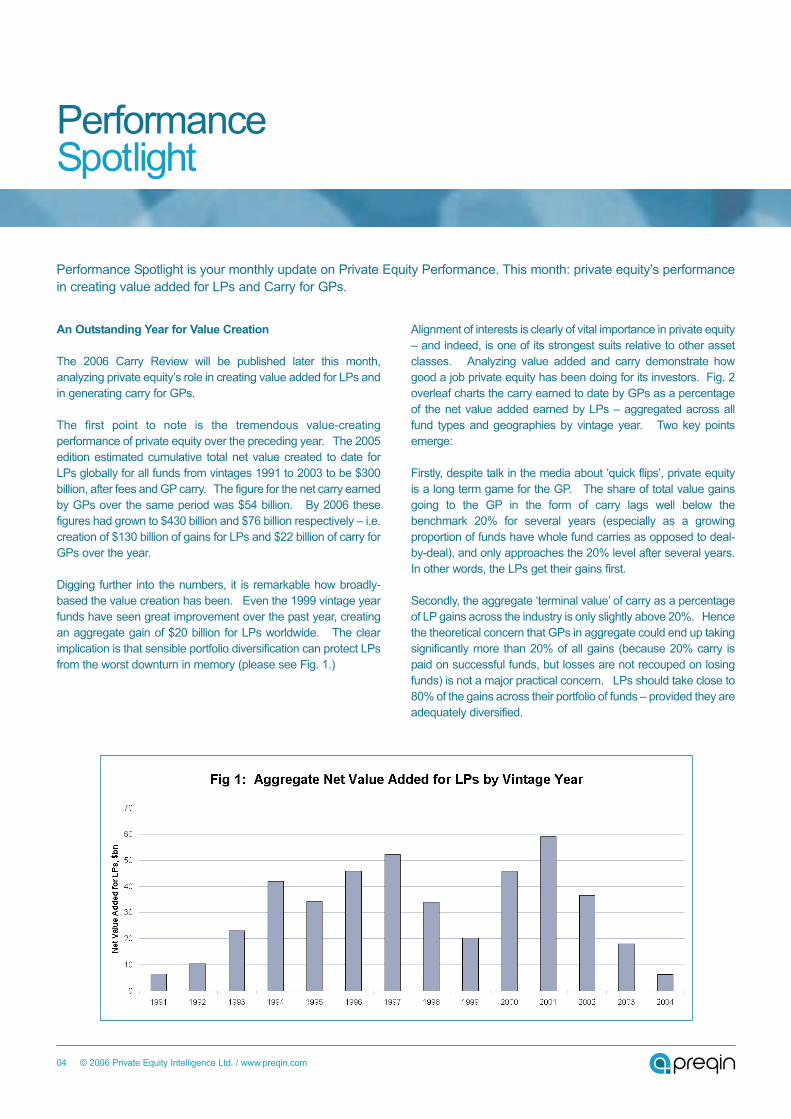

An Outstanding Year for Value Creation

The 2006 Carry Review will be published later this month,

analyzing private equity’s role in creating value added for LPs and

in generating carry for GPs.

The first point to note is the tremendous value-creating

performance of private equity over the preceding year. The 2005

edition estimated cumulative total net value created to date for

LPs globally for all funds from vintages 1991 to 2003 to be $300

billion, after fees and GP carry. The figure for the net carry earned

by GPs over the same period was $54 billion. By 2006 these

figures had grown to $430 billion and $76 billion respectively – i.e.

creation of $130 billion of gains for LPs and $22 billion of carry for

GPs over the year.

Digging further into the numbers, it is remarkable how broadly-

based the value creation has been. Even the 1999 vintage year

funds have seen great improvement over the past year, creating

an aggregate gain of $20 billion for LPs worldwide. The clear

implication is that sensible portfolio diversification can protect LPs

from the worst downturn in memory (please see Fig. 1.)

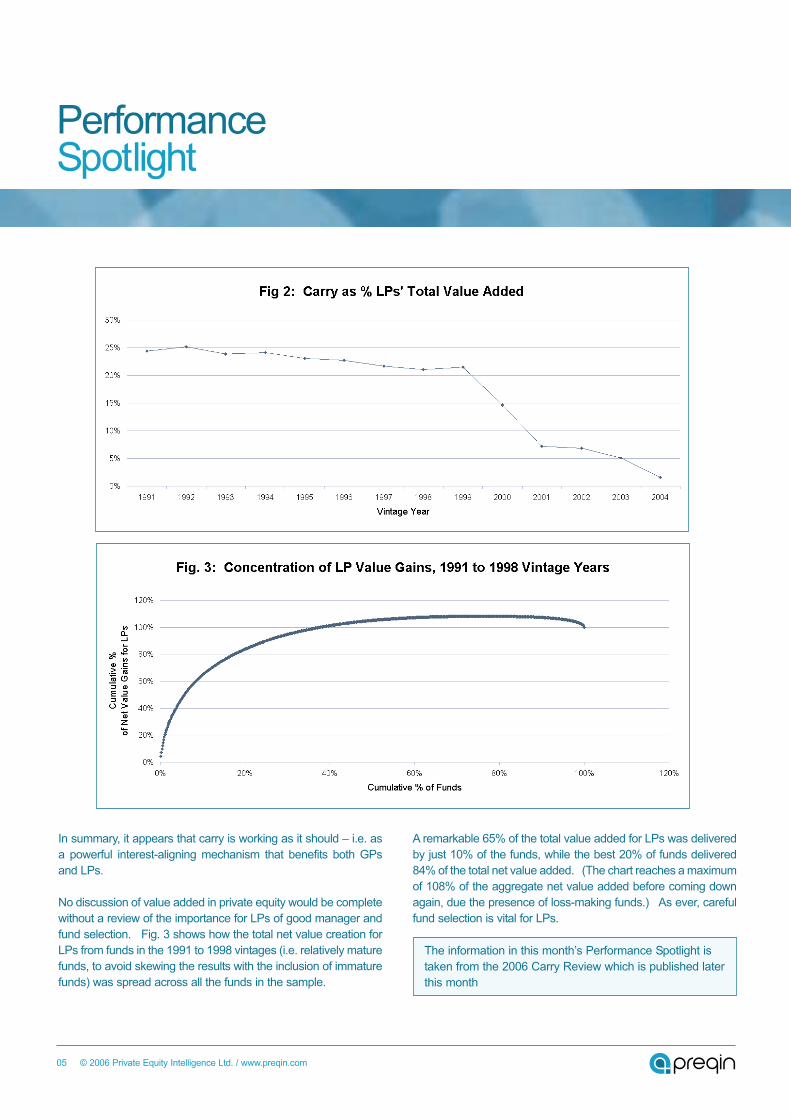

Alignment of interests is clearly of vital importance in private equity

– and indeed, is one of its strongest suits relative to other asset

classes. Analyzing value added and carry demonstrate how

good a job private equity has been doing for its investors. Fig. 2

overleaf charts the carry earned to date by GPs as a percentage

of the net value added earned by LPs – aggregated across all

fund types and geographies by vintage year. Two key points

emerge:

Firstly, despite talk in the media about ‘quick flips’, private equity

is a long term game for the GP. The share of total value gains

going to the GP in the form of carry lags well below the

benchmark 20% for several years (especially as a growing

proportion of funds have whole fund carries as opposed to deal-

by-deal), and only approaches the 20% level after several years.

In other words, the LPs get their gains first.

Secondly, the aggregate ‘terminal value’ of carry as a percentage

of LP gains across the industry is only slightly above 20%. Hence

the theoretical concern that GPs in aggregate could end up taking

significantly more than 20% of all gains (because 20% carry is

paid on successful funds, but losses are not recouped on losing

funds) is not a major practical concern. LPs should take close to

80% of the gains across their portfolio of funds – provided they are

adequately diversified.

Performance Spotlight is your monthly update on Private Equity Performance. This month: private equity’s performance

in creating value added for LPs and Carry for GPs.

04 © 2006 Private Equity Intelligence Ltd. / www.preqin.com

PerformanceSpotlight

In summary, it appears that carry is working as it should – i.e. as

a powerful interest-aligning mechanism that benefits both GPs

and LPs.

No discussion of value added in private equity would be complete

without a review of the importance for LPs of good manager and

fund selection. Fig. 3 shows how the total net value creation for

LPs from funds in the 1991 to 1998 vintages (i.e. relatively mature

funds, to avoid skewing the results with the inclusion of immature

funds) was spread across all the funds in the sample.

A remarkable 65% of the total value added for LPs was delivered

by just 10% of the funds, while the best 20% of funds delivered

84% of the total net value added. (The chart reaches a maximum

of 108% of the aggregate net value added before coming down

again, due the presence of loss-making funds.) As ever, careful

fund selection is vital for LPs.

05 © 2006 Private Equity Intelligence Ltd. / www.preqin.com

The information in this month’s Performance Spotlight is

taken from the 2006 Carry Review which is published later

this month

I would like to order my copy of the 2006 Carry Review at the special Pre-Publication Price:

More information is available at:

www.preqin.com/carry

OCTOBER PRE-PUBLICATION DISCOUNT

Order during October to take advantage of a

10% off pre-publication offer!

Payment Options:

Additional Copies:

£95 + £5 shipping $180 + $20 shipping €135 + €12 shipping

(Shipping Costs will not exceed a maximum of: £15 / $60 / €37 per order)

£445 + £10 shipping $845 + $40 shipping €645 + €20 shipping Promotional Code

Name:

Firm: Job Title:

Address:

City: Post/Zip Code: Country:

Telephone: Email:

Card No: Expiration Date:

Name on Card: Promotion Code:

Cheque enclosed (please make the cheque payable to ‘Private Equity Intelligence’)

Credit Card Visa Amex MasterCard

Private Equity Intelligence - 10 Old Bailey, London EC4M 7NG, UK.

w: www.preqin.com / e: [email protected] / t: +44 (0)20 7038 1650 / f: +44 (0)87 0330 5892 or +1 440 445 9595

PUBLICATION ORDER FORM: Complete this form and return it by post/fax

2006 Carry Review

Detailed analysis of value added and carry fund by fund. See how the private equity industry has

created value for LPs and GPs

• LPs gained $430 billion from their investments in 1991 - 2004 vintage funds, while GPs earned $76 billion in Carry.

• See fund-by-fund detail for over 750 funds worldwide

© 2006 Private Equity Intelligence Ltd. / www.preqin.com

OverviewGlobal Fundraising Update - Q3 2006

07 © 2006 Private Equity Intelligence Ltd. / www.preqin.com

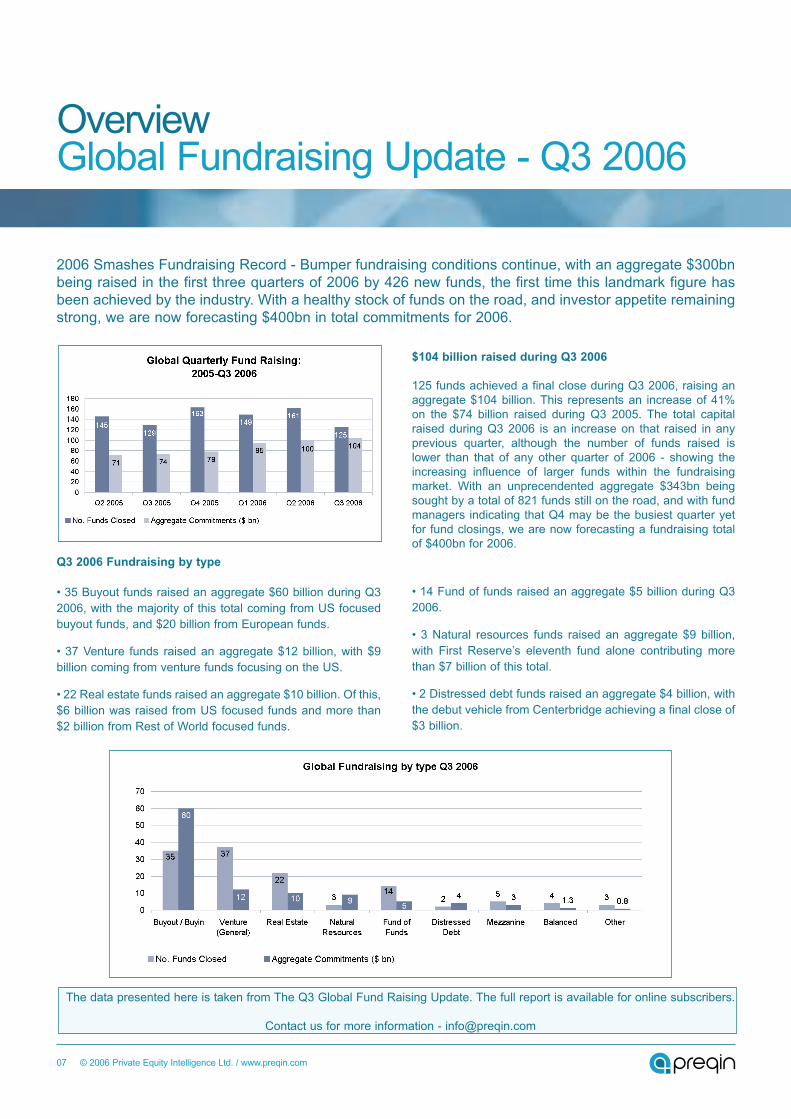

2006 Smashes Fundraising Record - Bumper fundraising conditions continue, with an aggregate $300bnbeing raised in the first three quarters of 2006 by 426 new funds, the first time this landmark figure hasbeen achieved by the industry. With a healthy stock of funds on the road, and investor appetite remainingstrong, we are now forecasting $400bn in total commitments for 2006.

$104 billion raised during Q3 2006

125 funds achieved a final close during Q3 2006, raising anaggregate $104 billion. This represents an increase of 41%on the $74 billion raised during Q3 2005. The total capitalraised during Q3 2006 is an increase on that raised in anyprevious quarter, although the number of funds raised islower than that of any other quarter of 2006 - showing theincreasing influence of larger funds within the fundraisingmarket. With an unprecendented aggregate $343bn beingsought by a total of 821 funds still on the road, and with fundmanagers indicating that Q4 may be the busiest quarter yetfor fund closings, we are now forecasting a fundraising totalof $400bn for 2006.

Q3 2006 Fundraising by type

• 35 Buyout funds raised an aggregate $60 billion during Q3

2006, with the majority of this total coming from US focused

buyout funds, and $20 billion from European funds.

• 37 Venture funds raised an aggregate $12 billion, with $9

billion coming from venture funds focusing on the US.

• 22 Real estate funds raised an aggregate $10 billion. Of this,

$6 billion was raised from US focused funds and more than

$2 billion from Rest of World focused funds.

• 14 Fund of funds raised an aggregate $5 billion during Q3

2006.

• 3 Natural resources funds raised an aggregate $9 billion,

with First Reserve’s eleventh fund alone contributing more

than $7 billion of this total.

• 2 Distressed debt funds raised an aggregate $4 billion, with

the debut vehicle from Centerbridge achieving a final close of

$3 billion.

The data presented here is taken from The Q3 Global Fund Raising Update. The full report is available for online subscribers.

Contact us for more information - [email protected]

The 2006 Private Equity Real Estate Review isavailable now at $945 / £495 / €725

For more information and sample pages,please visit:

www.preqin.com/re2006

Product Spotlight:2006 Real Estate Review

Each Month Spotlight takes a closer look at one of the many products and services provided by Private Equity

Intelligence, exploring the features offered; how it can help you in your job; who uses it and how you can get it.

This month: The 2006 Private Equity Real Estate Review

08 © 2006 Private Equity Intelligence Ltd. / www.preqin.com

The Private Equity Real Estate Review is theworld's most comprehensive guide to privateequity real estate, with information on:

• Key Trends and Market Conditions

• Fund Raising Listings

• General Partner Profiles

• Limited Partner Profiles

Benefit from thorough and detailed analysis ofthe key trends shaping today’s real estatemarket:

• Over 25 pages of analysis on all aspects of the private equity real estate market.

• Key trends established for real estate fund raising

• Performance of real estate funds revealed

• LP investment patterns established

• Dedicated chapter detailing typical terms for real estate funds

Comprehensive Profiles and Listings:

Full Details for all funds closed since 2005, currently raisingand expected to launch, with information on fund strategy,placement agents, sector focus, sample investors and more

Profiles for 225 real estate firms, with contact details, history,firm preferences and more. Key performance metrics for over240 funds, including IRRs and multiples with benchmarksenabling easy comparison between funds.

Comprehensive profiles for nearly 300 leading real estateLPs, with contact details, investment plans, key financial dataand sample investments.

•

•

•

InvestorSpotlight

Specialist secondaries funds are of growing interest to

sophisticated Limited Partners worldwide. As of October 2006,

Investor Intelligence lists nearly 200 LPs who have already

invested in a secondaries fund, and a further 100 who list this as

an area of interest for future investment.

The reason underlying LP interest in secondaries funds is not

hard to find: performance. Performance Analyst benchmarks

secondaries funds against all private equity funds, and relative

to this benchmark no fewer than 43% of the secondaries funds

fall into Q1, and 33% into Q2 - only 24% of secondaries funds

are in Q3 or Q4. As investors’ portfolios become more mature

and sophisticated they often opt to invest in secondaries to

generate additional returns through diversification.

In spite of the added layer of fees, secondaries funds have

generally performed extremely well when compared to other

private equity funds. They give investors the advantage of

hindsight, enabling them to invest immediately into well-

performing underlying funds after their initial period. This causes

the “J-Curve” to flatten out, as management fees fall and cash

flows become more predictable, thereby reducing risk.

Secondaries also offer significant diversification across strategy,

geography and industry. Investments can also be made for a

shorter period of time and in a larger spread of vintages than

traditional fund of funds vehicles.

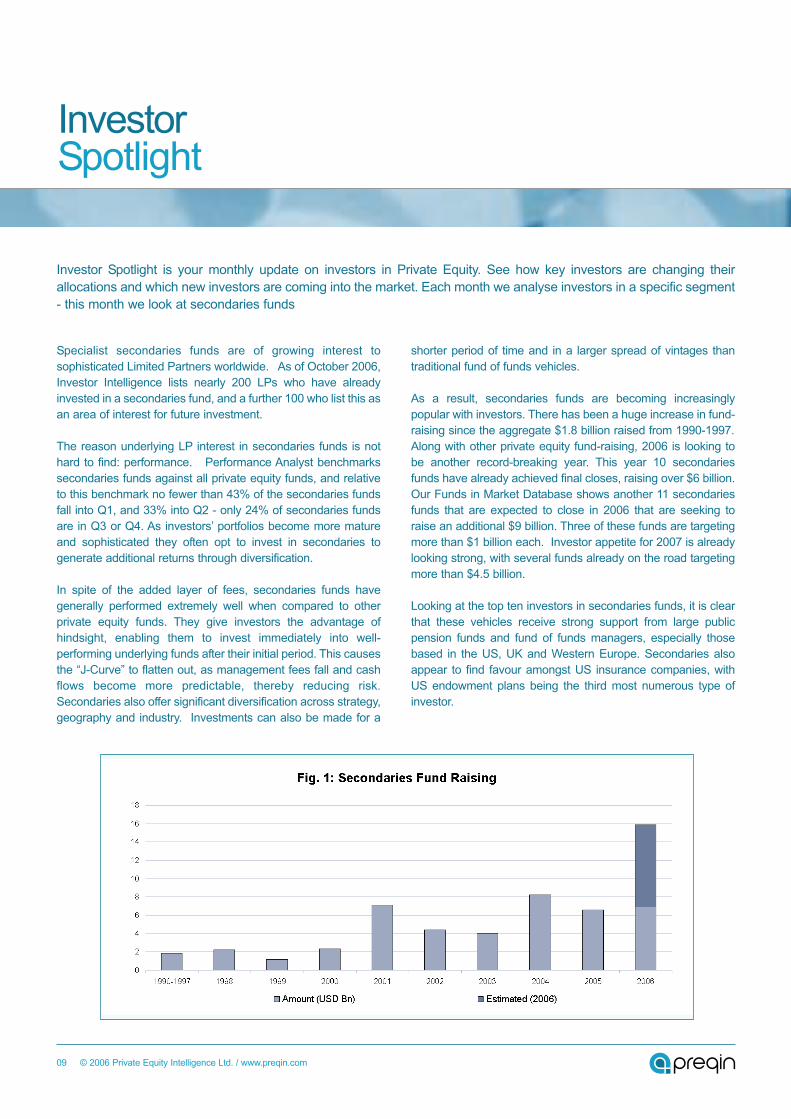

As a result, secondaries funds are becoming increasingly

popular with investors. There has been a huge increase in fund-

raising since the aggregate $1.8 billion raised from 1990-1997.

Along with other private equity fund-raising, 2006 is looking to

be another record-breaking year. This year 10 secondaries

funds have already achieved final closes, raising over $6 billion.

Our Funds in Market Database shows another 11 secondaries

funds that are expected to close in 2006 that are seeking to

raise an additional $9 billion. Three of these funds are targeting

more than $1 billion each. Investor appetite for 2007 is already

looking strong, with several funds already on the road targeting

more than $4.5 billion.

Looking at the top ten investors in secondaries funds, it is clear

that these vehicles receive strong support from large public

pension funds and fund of funds managers, especially those

based in the US, UK and Western Europe. Secondaries also

appear to find favour amongst US insurance companies, with

US endowment plans being the third most numerous type of

investor.

Investor Spotlight is your monthly update on investors in Private Equity. See how key investors are changing their

allocations and which new investors are coming into the market. Each month we analyse investors in a specific segment

- this month we look at secondaries funds

09 © 2006 Private Equity Intelligence Ltd. / www.preqin.com

InvestorSpotlight

Demand appears to be very strong for the latest fund offering by

Coller Capital. Coller is the largest secondaries fund manager

and is looking to raise $3.75 billion through its Coller Capital V

fund. The fund has recently secured two $100 million

commitments by California Public Employees' Retirement

System (CalPERS) and Oregon Public Employees’ Retirement

Funds (OPERF). The fact that all of Coller’s previous funds have

been top quartile is clearly driving LP appetite for the latest

offering. Both of these US pension funds are active and

sophisticated private equity fund investors: CalPERS is a major

investor in secondaries and uses this fund type to extract extra

returns from the private equity asset class, while OPERF

appears to invest in secondaries on a more opportunistic basis.

CPP Investment Board (CPPIB) is one of the largest investors

in secondaries, having committed CAD 1 billion to the fund type,

with almost CAD 400 million of this in the last twelve months

alone. CPPIB is also looking to recruit a director to run its

secondaries market activities, who will oversee direct

investment opportunities in secondaries market offerings,

secondaries vehicles and other types of private equity funds

along with the responsibility of shaping the pension plan's

secondaries investment strategy.

Several fund of fund managers invest heavily in secondaries

funds and some have raised multiple vehicles dedicated to

investing in secondaries. Lexington Partners’ latest offering

recently closed on $3.5 billion. LGT Capital Partners, the Swiss

fund of funds manager with $8 billion of assets under

management, invests 20% of its assets into global secondaries

funds. Other fund of fund managers who manage dedicated

secondaries funds include: Adams Street Partners, Harbourvest

Partners and Pantheon Ventures.

Recent coverage of the secondaries transaction market reveals

that some big-name LPs are getting in on the action. One of the

largest secondaries transactions in 2005 saw AlpInvest team up

with secondaries expert Lexington Partners to acquire the

private equity portfolio of DPL (the parent company of Dayton

Power & Light). The portfolio of around 46 private equity fund

interests was purchased for $850 million. Similarly, in early April

2006, Canada's CPP Investment Board and Goldman Sachs

Private Equity Group were involved in one of the largest

secondaries transactions ever, buying a $925 million interest in

buyout fund JP Morgan Partners Global. Additionally, the limited

partnership portfolios of Natwest, AIG and Abbey National were

all sold to secondaries fund managers.

In conclusion, with the added benefits of low risk and good

performance, it’s no surprise that investor appetite is strong for

this fund type and fund-raising is reaching record highs.

The data for this month’s investor article hasbeen gathered from the Investor Intelligencedatabase.

For more information, please see:www.preqin.com/II

10 © 2006 Private Equity Intelligence Ltd. / www.preqin.com

InvestorNews

Railways Pension Trustee Company (Railpen), the UK

Railways Pensions Scheme, is increasing its allocation to the

private equity asset class to 10%. Railpen has been investing in

alternatives such as private equity for 20 years and the

increased allocation is part of the firm’s plan to diversify its

portfolio. Chief executive Chris Hitchen forecasts allocations of

10% to property, infrastructure and hedge funds in addition to

private equity. Railpen began investing in hedge funds two years

ago and is increasing its weighting; it should reach its target in

two years. Railpen doubled its investment returns to 16.3% last

year, raising its assets to EUR 17 billion.

Following a strategic review in early 2005 conducted by

advisors Hymans Robertson, the GBP 741 million Gwynedd

Council Pension Fund has opted to allocate 5% of its assets

to private equity to help address its GBP 129 million deficit. The

pension fund will be investing through fund of funds managers

and, according to Investments & Pensions Europe, has

tendered a mandate worth £37 million. Hymans Robertson

attributed their recommendation for the pension fund’s move

into private equity to the strong projected returns of 15%-20%

expected by most fund of funds managers.

The University of St. Thomas Endowment is considering

placing up to $30 million in alternatives and has appointed

Cambridge Associates as its investment consultant. The

endowment will decide how to implement this move over the

next six months reports Alternative Investment News.

Keen to expand its real estate portfolio, the Los Angeles

County Employees’ Retirement Association (LACERA) is

set to double its commitments to private equity real estate funds,

reports Private Equity Intelligence. LACERA plans to commit

$90 million to private equity real estate funds in the next 12

months. The $33 billion pension fund sees exciting opportunities

in the asset class and in particular is looking to invest in

international funds. It sees private equity real estate funds as the

perfect way of entering the international market and exploring

global opportunities.

Pension Benefits Guaranty Corp. (PBGC) is set to issue a

request for proposals as it prepares to auction off $1 billion worth

of private equity fund stakes that it acquired when United

Airlines and US Airlines defaulted on their pension obligations

last year. According to Private Equity Insider, there has already

been much interest from the secondary-market, but the

government insurance agency has turned down any off-market

offers as it believes it could raise more money through a formal

bidding process. It is not clear how the sale will be split – while

it is possible the stakes could be sold as a single package, there

are rumours that it will be repackaged as two to three smaller

offerings. About $700 million of the offering will be from United’s

fund stakes with the remaining coming from the $400 million

alternative-investment portfolio held by US Airways. This sale

should go a small way to recuperating the agencies $30 billion

deficit.

According to Investment and Pensions Europe, AlpInvest and

Finnish local government pensions institution KEVA have both

committed to Polish Enterprise Fund VI. The fund has received

€200 million in commitments from pension funds. CalPERS is

also said to be looking to commit. This is the second time that

both AlpInvest and KEVA have made commitments to Polish-

based enterprise investors.

Pensioenfonds Horeca & Catering (PH&C), the EUR 2 billion

corporate pension fund, has awarded SPF Beheer a EUR 40

million private equity mandate, according to Investment and

Pensions Europe. The move comes as part of Horeca’s strategy

to get closer to its 5% target allocation to the asset class, with

the firm promising further private equity mandates to be

awarded shortly. With previous commitments of EUR 200 million

to AlpInvest, HarbourVest and Goldman Sachs Private Equity in

addition to the SPF Beheer mandate which was awarded on

September 1st, Horeca’s private equity rating will rise to nearly

2%. Jet Gerla, senior manager for investment management said

SPF will look to invest over the next two years, targeting

between five and ten international private equity funds, adding

that the mandate went to SPF Beheer on the basis of the firm’s

good results and transparent investment process.

Each month Spotlight provides a selection of the recent news on LPs

More news and updates are available online for Investor Intelligence subscribers.

Contact us for more information - [email protected]

11 © 2006 Private Equity Intelligence Ltd. / www.preqin.com

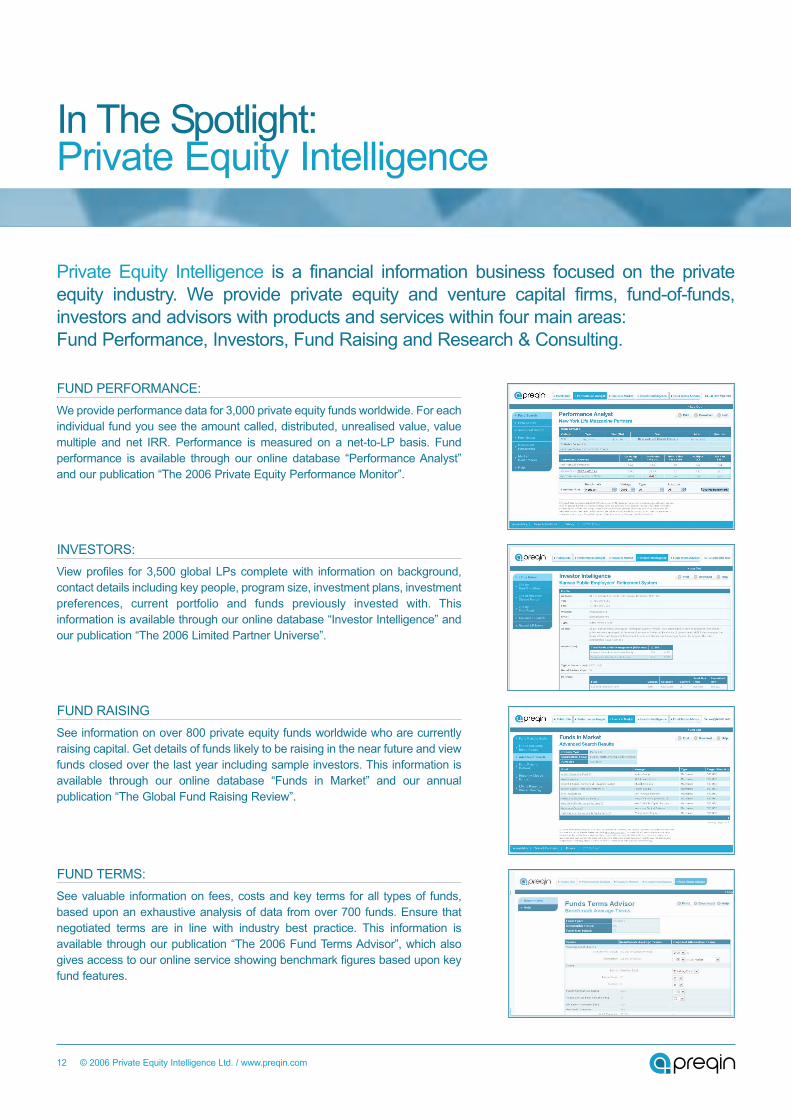

In The Spotlight:Private Equity Intelligence

Private Equity Intelligence is a financial information business focused on the privateequity industry. We provide private equity and venture capital firms, fund-of-funds,investors and advisors with products and services within four main areas: Fund Performance, Investors, Fund Raising and Research & Consulting.

We provide performance data for 3,000 private equity funds worldwide. For each

individual fund you see the amount called, distributed, unrealised value, value

multiple and net IRR. Performance is measured on a net-to-LP basis. Fund

performance is available through our online database “Performance Analyst”

and our publication “The 2006 Private Equity Performance Monitor”.

FUND PERFORMANCE:

View profiles for 3,500 global LPs complete with information on background,

contact details including key people, program size, investment plans, investment

preferences, current portfolio and funds previously invested with. This

information is available through our online database “Investor Intelligence” and

our publication “The 2006 Limited Partner Universe”.

INVESTORS:

See information on over 800 private equity funds worldwide who are currently

raising capital. Get details of funds likely to be raising in the near future and view

funds closed over the last year including sample investors. This information is

available through our online database “Funds in Market” and our annual

publication “The Global Fund Raising Review”.

FUND RAISING

See valuable information on fees, costs and key terms for all types of funds,

based upon an exhaustive analysis of data from over 700 funds. Ensure that

negotiated terms are in line with industry best practice. This information is

available through our publication “The 2006 Fund Terms Advisor”, which also

gives access to our online service showing benchmark figures based upon key

fund features.

FUND TERMS:

12 © 2006 Private Equity Intelligence Ltd. / www.preqin.com