Private Company Accounting - Chris Rouse

31

PRIVATE COMPANY ACCOUNTING UPDATE Little gaap is now GAAP Chris Rouse, CPA November 13, 2014

-

Upload

windhampresentations -

Category

Business

-

view

74 -

download

0

Transcript of Private Company Accounting - Chris Rouse

PRIVATE COMPANY ACCOUNTING UPDATELittle gaap is now GAAP

Chris Rouse, CPA

November 13, 2014

Private Company Accounting Update

Agenda

• The Private Company Council

• PCC Accounting Standards Updates

• PCC Project Agenda

• The AICPA’s Financial Reporting Framework for Small and Medium-sized Entities

2

Private Company Accounting Update

The Private Company Council• Established by the Financial Accounting Foundation in

2012 to address concerns of private companies

• PCC members are from industry and public accounting

– Appointed by FAF and serve as volunteers

• Objectives of the PCC

– Study existing GAAP to determine changes necessary to enhance financial reporting by private companies

– Serve as advisory board to FASB as new standards are deliberated

3

Private Company Accounting Update

The Private Company Council• PCC proposed changes are exposed for comment as

“issues”

– After comments are considered, PCC approves with two-thirds vote

– Proposed standard is submitted to FASB for endorsement

– Issued as “Consensus of PCC”

• FAF will assess after 3 years (spring of 2015?)

4

Private Company Accounting Update

PCC Accounting Standards Updates• ASU 2013-12 – Definition of a Public Business Entity

– Issued by FASB to define what entities PCC ASUs cover

– Includes entities required to file financial statements with the SEC

• A non-filing subsidiary would not fit the definition of a public business entity

5

Private Company Accounting Update

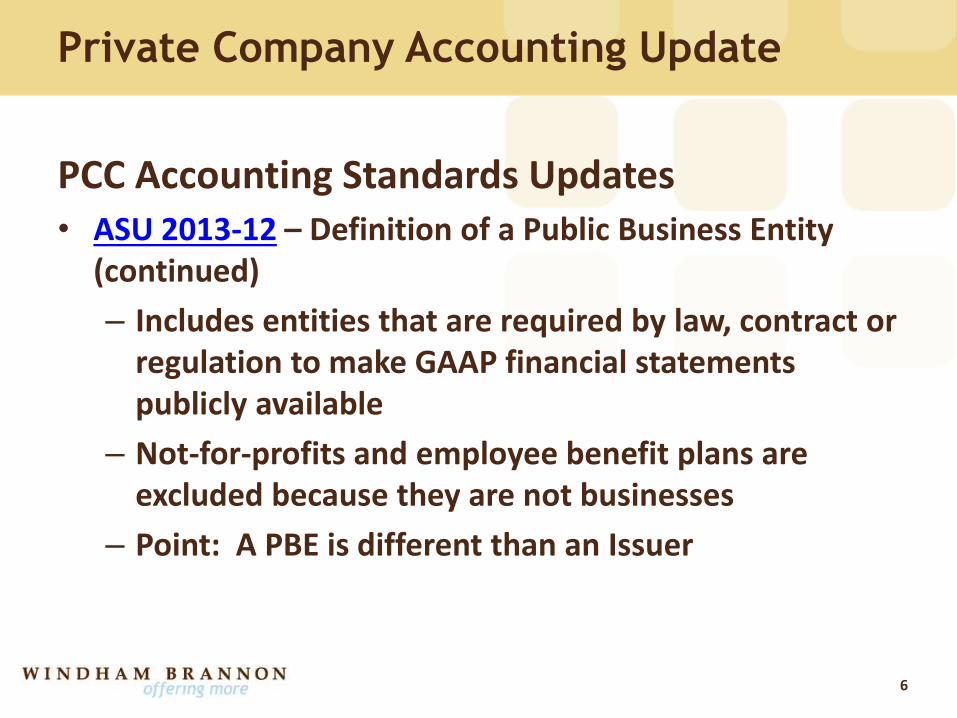

PCC Accounting Standards Updates• ASU 2013-12 – Definition of a Public Business Entity

(continued)

– Includes entities that are required by law, contract or regulation to make GAAP financial statements publicly available

– Not-for-profits and employee benefit plans are excluded because they are not businesses

– Point: A PBE is different than an Issuer

6

Private Company Accounting Update

PCC Accounting Standards Updates• ASU 2014-02 – Intangibles – Goodwill and Other:

Accounting for Goodwill (a consensus of the Private Company Council)

– Many businesses find it difficult to make the annual determination of whether goodwill has been impaired

– This ASU permits non-public business entities to amortize goodwill over 10 years, or less if more appropriate

7

Private Company Accounting Update

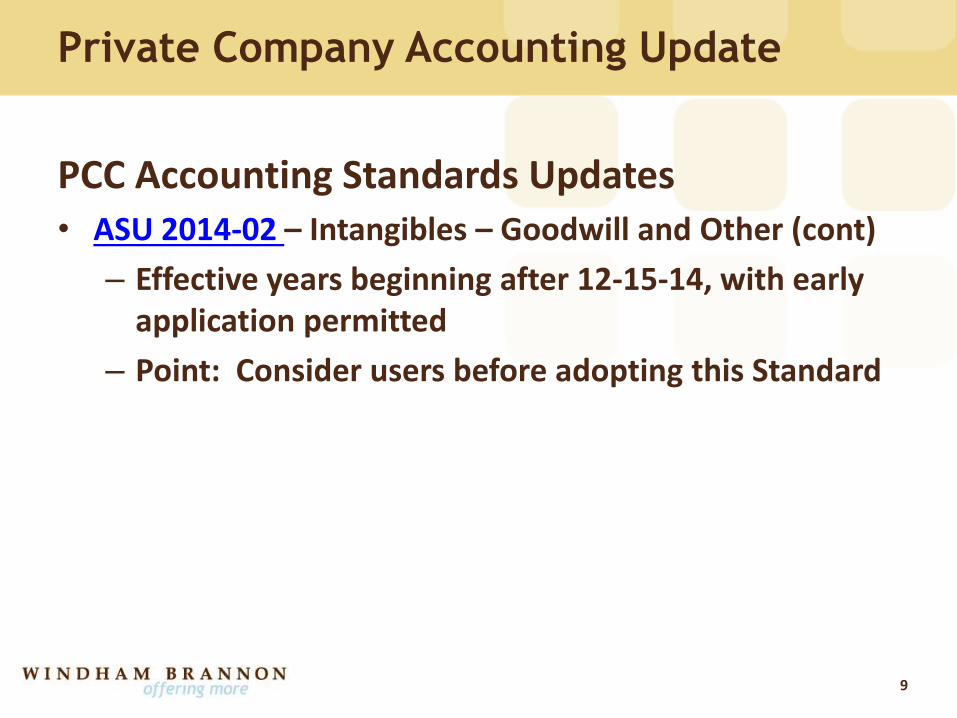

PCC Accounting Standards Updates• ASU 2014-02 – Intangibles – Goodwill and Other (cont)

– Only required to perform impairment test when a triggering event occurs (see list in Standard)

• Qualitative test is done first, and if no impairment is assessed, stop there

• Provides for a “one step” test if qualitative test indicates impairment

– Enterprise fair value is determined at either the entity level or the reporting unit level

–Goodwill impairment is the excess of enterprise carrying amount (i.e., equity) less enterprise fair value 8

Private Company Accounting Update

PCC Accounting Standards Updates• ASU 2014-02 – Intangibles – Goodwill and Other (cont)

– Effective years beginning after 12-15-14, with early application permitted

– Point: Consider users before adopting this Standard

9

Private Company Accounting Update

PCC Accounting Standards Updates

• ASU 2014-03 – Derivatives and Hedging: Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps – Simplified Hedge Accounting Approach (a consensus of the Private Company Council)

– This ASU permits non-public business entities to elect hedge accounting for “plain vanilla” interest rate swaps without testing hedge effectiveness

• “Plain vanilla” is defined in Standard – the common form of interest rate swaps

– May account for at fair value or settlement value

• Settlement value does not consider non-performance risk

10

–

Private Company Accounting Update

PCC Accounting Standards Updates

• ASU 2014-03 – Derivatives and Hedging (continued)

– Point: Applies to private companies that currently do not use hedge accounting for interest rate swaps, i.e., changes in fair value are included in current earnings rather than Other Comprehensive Income

– Point: In the future, private companies do not have to determine hedge effectiveness

– Point: The settlement value option is not much help with the beans of determining swap carrying amount

– Effective years beginning after 12-15-14, with early application permitted

11

Private Company Accounting Update

PCC Accounting Standards Updates

• ASU 2014-03 – Derivatives and Hedging (continued)

– Point: The settlement value option is not much help with the beans of determining swap carrying amount

– Effective years beginning after 12-15-14, with early application permitted

12

Private Company Accounting Update

PCC Accounting Standards Updates• ASU 2014-07 – Consolidation: Applying Variable Interest

Entities Guidance to Common Control Leasing Arrangements (a consensus of the Private Company Council)

– This ASU permits non-public business entities to not determine whether a lessor entity under common control is a variable interest entity

– Requires disclosures in addition to related party matters

13

Private Company Accounting Update

PCC Accounting Standards Updates• ASU 2014-07 – Consolidation: Applying Variable Interest

Entities Guidance to Common Control Leasing Arrangements (continued)

– Point: Consider financial statement user needs

– Point: Consider combined financials

– Effective years beginning after 12-15-14, with early application permitted

14

Private Company Accounting Update

PCC Project Agenda• Business Combinations; Accounting for Identifiable

Intangible Assets in a Business Combination

– Would exempt private companies from separately recognizing and measuring non-competition agreements and customer-related intangible assets that are not capable of being sold or licensed independently in a business combination

– Would importantly simplify the fair value effort in a business combination

– Has been approved by the PCC, and sent to FASB for endorsement

15

Private Company Accounting Update

PCC Project Agenda• Business Combinations

– Point: Would result in any such fair value being included in goodwill, which may or may not be amortized

– Effective date might be years beginning after 12-15-14, but in any event early application would be permitted

16

Private Company Accounting Update

PCC Project Agenda• Stock-based Compensation: The PCC has discussed

potential ways to improve the accounting for stock-based compensation for private companies.

– The FASB will consider adding a project to its agenda to address the accounting of stock-based compensation for public and private companies

– If the project is added to the FASB’s agenda, the PCC will continue to directly advise the FASB on private company issues relating to the topic

17

Private Company Accounting Update

PCC Project Agenda

• The PCC will consider other projects after the FAF completes the 3-year assessment, supposedly in 2015

18

Private Company Accounting Update

The AICPA’s Financial Reporting Framework for Small and Medium-sized Entities• AICPA Council’s response to concerns of non-

responsiveness of FAF and FASB to needs of private company financial reporting

– Initiated in October 2011, exposure draft in November 2012, and issued in June 2013, effective immediately

– 200+ pages, plus implementation resources at www.aicpa.org in the Financial Reporting Center section of the website

19

Private Company Accounting Update

The AICPA’s FRF for SMEs• Overarching principles

– Users of non-public company financials have access to management for additional information

• Including info regarding existence of assets, liabilities, rights and obligations in financial statements puts users on notice, and additional info can be obtained directly from management

– The entity does not operate in an industry with highly specialized accounting guidance

– The entity does not engage in complicated transactions

20

The AICPA’s FRF for SMEs• Some of the details

– Blend of current (and former) GAAP and accrual basis accounting

– Comprehensive set of standards

• 172 pages, covering financial statement concepts and general principles, basic financial statements and accounts, and specific transactions common to SMEs

– No specific industry guidance

21

Private Company Accounting Update

Private Company Accounting Update

The AICPA’s FRF for SMEs• Some of the details

– Consolidated financials are a choice

• If not consolidated, disclosures are substantial

• No VIEs!!

– No “fair value” accounting

• Uses net realizable value, market, etc.

– Requires bad debt reserve

22

Private Company Accounting Update

The AICPA’s FRF for SMEs • Some of the details

– Calls for inventory to be carried at lower of cost or market

• Permits FIFO, LIFO, weighted average, standard cost, retail method, etc. so long as they approximate cost

– Investments accounted for at cost (less than 20% ownership), equity method (greater than 20%)

23

Private Company Accounting Update

The AICPA’s FRF for SMEs • Some of the details

– Equity and debt investments held for sale carried at market value with change in market value reported in income

• Held for sale is “currently attempting to sell”

• Disclose name and description of each significant investment

24

Private Company Accounting Update

The AICPA’s FRF for SMEs • Some of the details

– Derivatives carried at cost, with disclosures of open instruments, except no fair value required (no hedge accounting)

– Requires depreciation of buildings and equipment over their useful life

25

Private Company Accounting Update

The AICPA’s FRF for SMEs • Some of the details

– Intangibles and goodwill amortized over tax life, or 15 years if not amortized for tax

• No impairment testing necessary

– Commitments are measured if probable

• Defined benefit plans may use current contribution method or accrued benefit method

• Accrue deferred compensation arrangements• Leases are accounted for similar to current GAAP

(75% and 90% retained)

26

Private Company Accounting Update

The AICPA’s FRF for SMEs• Some of the details

– Contingencies retain probable, possible and remote considerations

– No measurement of stock options, but substantial disclosures

– Revenues similar to current GAAP

– Income taxes determined using either taxes payable or deferred methods

27

Private Company Accounting Update

The AICPA’s FRF for SMEs • Some of the details

– Disclosures consistent with current GAAP

• Risk and uncertainties

• Discontinued operations

• Retirement and post-employment benefits

• Related party transactions

• Subsequent events

28

Private Company Accounting Update

The AICPA’s FRF for SMEs • Some of the details

– Business combinations accounted for using current acquisition method, except may opt to not measure intangibles

• Purchase price allocated based on market values

• Provides for push-down accounting

– Other topics are more GAAP-like

– If not covered in FRF for SMEs, may use GAAP or other basis of accounting

29

Private Company Accounting Update

The AICPA’s FRF for SMEs

• Point: Consider areas of GAAP that currently cause additional time and expense in preparing your financial statements, any relief FRF for SMEs would provide, and needs of users of your financial statements

30

31

Private Company Accounting Update

In Conclusion….

Bon Auditpetite!Questions??

Contact any WB professional, or contact Chris Rouse

404-898-2000