![Muslim Law of Marriage [Nikah] It is Contract and Object is the procreation and legalising of children. [Mulla, principle of Mohamedan Law] It is Contract.](https://static.fdocuments.net/doc/165x107/5697bf871a28abf838c88f12/muslim-law-of-marriage-nikah-it-is-contract-and-object-is-the-procreation.jpg)

PRINCIPLE OF CONTRACT LAW (PART 1 OF 3) · PRINCIPLE OF CONTRACT LAW (PART 2 OF 3) 23 ......

112

PRINCIPLE OF CONTRACT LAW (PART 1 OF 3) 1 Learning Outcome Understand the principles of contract law & construction contract law 2

Transcript of PRINCIPLE OF CONTRACT LAW (PART 1 OF 3) · PRINCIPLE OF CONTRACT LAW (PART 2 OF 3) 23 ......

PRINCIPLE OF CONTRACT LAW

(PART 1 OF 3)

1

Learning Outcome

�Understand the principles of contract law & construction contract law

2

What is a Contract?

“A legally binding agreement made between two or more parties,by which rights are acquired by one or more to acts or forbearanceson the part of other.”

Bearson, J. (2002). Anson’s Law of Contract (28th Edition). Oxford:Oxford University Press.

3

What is a Contract? (Cont’d)

�An agreement formed between 2 parties to:

� Do something� Not to do something; or� Acquire rights

�With the intention� to have legal consequences� Intended to be legally enforceable

4

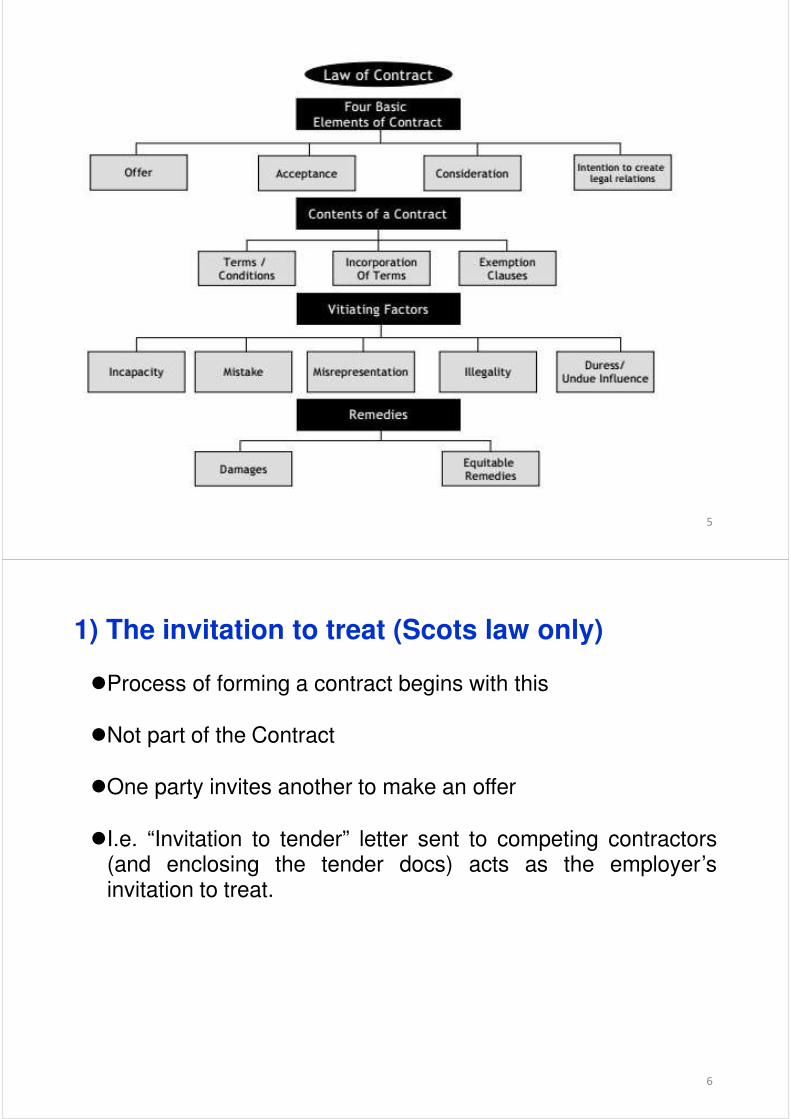

5

1) The invitation to treat (Scots law only)

�Process of forming a contract begins with this

�Not part of the Contract

�One party invites another to make an offer

�I.e. “Invitation to tender” letter sent to competing contractors(and enclosing the tender docs) acts as the employer’sinvitation to treat.

6

7

2) The offer

�Express willingness to be bound by the proposed contractterms

�Time-bound (States a period of time in which the offer must beaccepted before the offer will lapse)

�I.e. The tender price submitted by a contractor after pricing thedesign and proposed contract terms contained in the tenderdocuments is its offer

�I.e. The employer will receive several offers from competingtendering contractors/tenderers

8

9

3) The acceptance

�An offer made by one party must be accepted by the other partyfor the contract to exist

�Must be unconditional (matching the terms of the offer)

�Negotiation will be required if any terms/qualifications added bythe contractor to its tender offer are unacceptable – “counteroffer” from the employer to the contractor

10

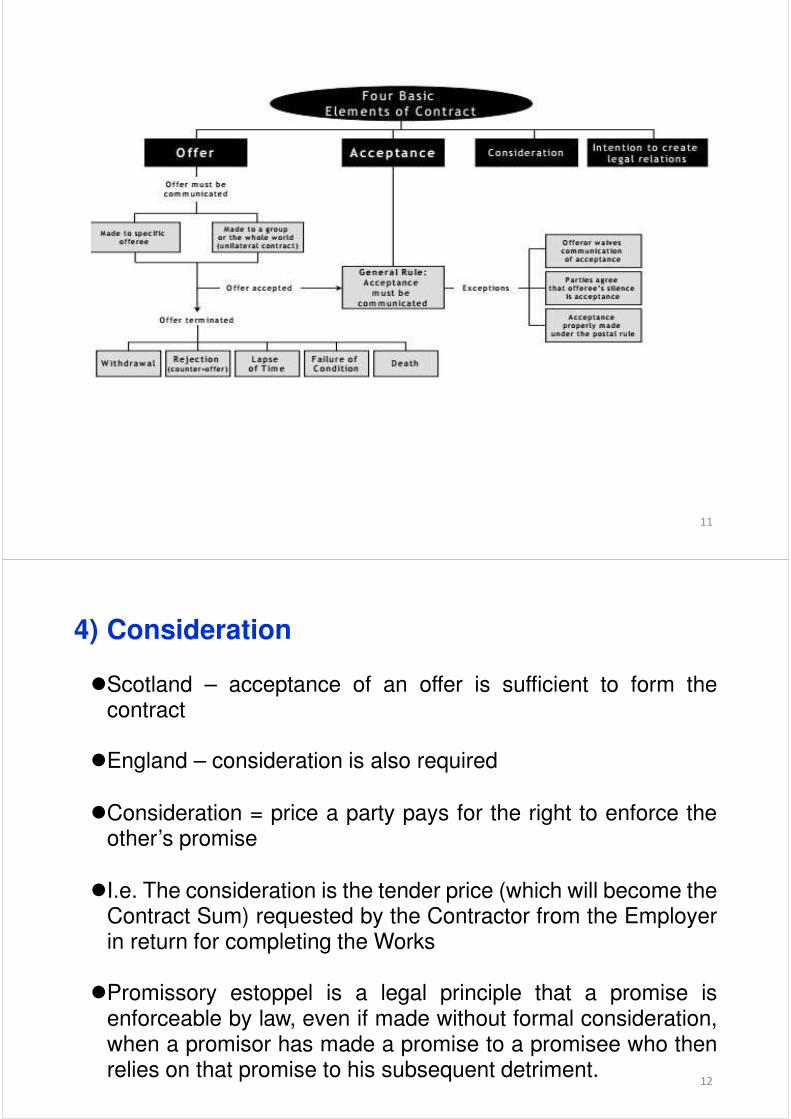

11

4) Consideration

�Scotland – acceptance of an offer is sufficient to form thecontract

�England – consideration is also required

�Consideration = price a party pays for the right to enforce theother’s promise

�I.e. The consideration is the tender price (which will become theContract Sum) requested by the Contractor from the Employerin return for completing the Works

�Promissory estoppel is a legal principle that a promise isenforceable by law, even if made without formal consideration,when a promisor has made a promise to a promisee who thenrelies on that promise to his subsequent detriment.

12

13

5) Capacity

�The parties must be legally able to enter into a contract.

� Parties must not be insane, drunk, incapable, etc.

� Companies must comply with any limitations of their legal incorporation

14

6) Intent

�Both parties must mean to create a contract

�Each party must:

� Understand what they are “agreeing” to

� Form the agreement of their own free will

15

16

7) Form (Formalities)

�The contract is created by agreement alone (i.e. an offer and acceptance)

�Other aspects provide clarity about what has been agreed and how long the agreement will last for.

�These refer to the “formalities” of the contract, not the standard “ forms” of construction contract

�The formalities of the contract are its terms.

�The contract terms are defined in its clauses.

�The contract clauses establish certainty about what has been agreed

17

8) Execution

�The act of signing the Contract to bring it into effect is called “execution”.

�Together with attestation, it formalises the agreement and puts the Contract into place.

�The method of executing the contract determines the duration of liabilities arising from it:-

� In Scotland, 5 years for a “simple” contract, 20 years for a “probative writ”

� In England, 6 years for a “simple” contract, 12 years for a deed

18

Other issuesCommunication of acceptance

�The party making an offer can state how its acceptance must be communicated (i.e. fax, email, phone)

�If such a condition is set, an acceptance that does not comply with it is invalid

�When and acceptance is to be communicated by post, the “postal rule” applies.

� The contract is created when the letter of acceptance is posted, not when it is received

19

Other issues (Cont’d)Forming a construction contract

�Ensure the contractual relationship between the parties is formed without ambiguity

�A letter of intent is not a suitable substitute for an executed contract.

�Bad practice where organisation often “forget” or delay in executing the Contract

�The agreement between Employer and Contractor must be formalised in a way that:

� Defines and incorporates the agreed conditions� Defines and incorporates the Contract Documents� Defines the Contract Sum� Distributes risks to the parties by assigning liabilities

20

Other issues (Cont’d)Expressed & Implied Contract Terms

�Contract terms impose obligations on parties, grant them rights or duties of parties

�Contract terms can be expressed or implied

�Expressed terms are written into the Contract or are made verbally

�Implied terms are not stated in the Contract but are understood to be present by the parties

21

Other issues (Cont’d)Fit for Purpose -v- Skill and Care

�Where an employer relies solely on a Contractor to design andconstruct an entire building, a term of reasonable fitness forpurpose will be implied

�JCT Design and Build have amended this usual implication byinserting a special clause, cl.2.17.1.

�Cl.2.17.1 expressly states that the contractor has the sameliability as an architect, i.e. reasonable skill and care

�This is a valuable concession to contractors which is not availableunder most other design and build contracts

22

PRINCIPLE OF CONTRACT LAW

(PART 2 OF 3)

23

Learning Outcome

�Ending a contract

�Remedies

�Assignment and novation

�Third party rights and collateral warranties

�Sub-letting

�Insurance, guarantees and bonds

24

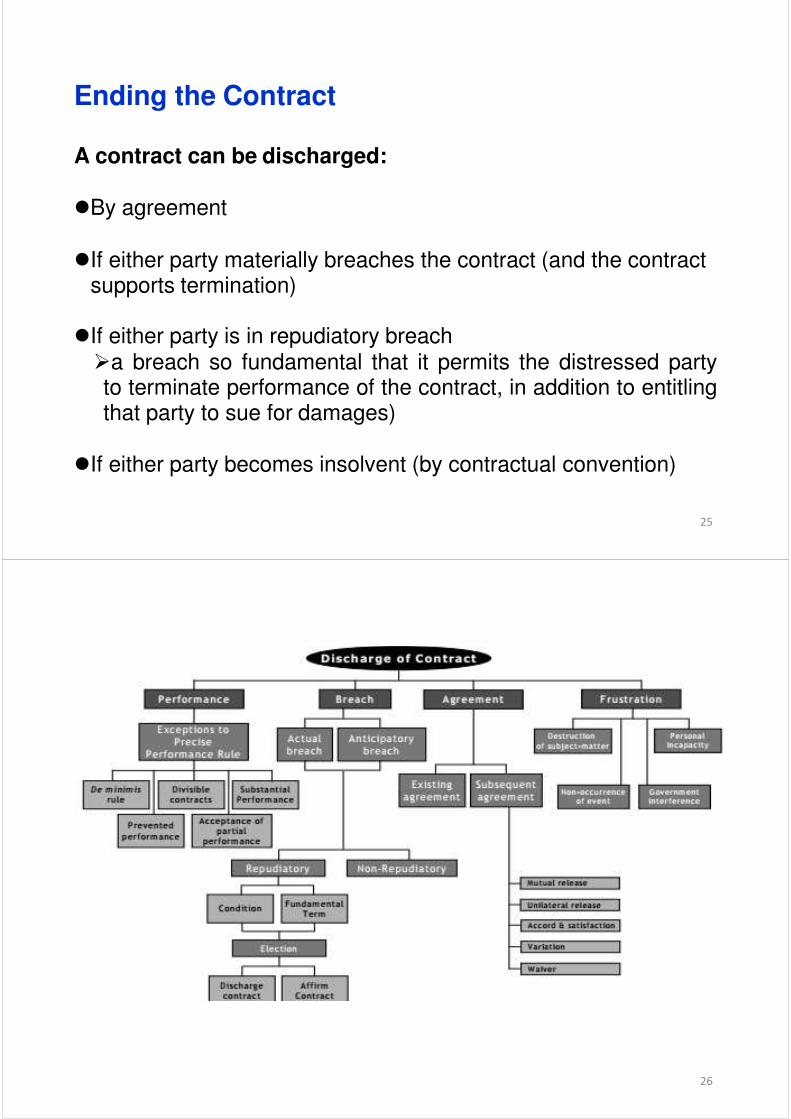

Ending the Contract

A contract can be discharged:

�By agreement

�If either party materially breaches the contract (and the contract supports termination)

�If either party is in repudiatory breach�a breach so fundamental that it permits the distressed partyto terminate performance of the contract, in addition to entitlingthat party to sue for damages)

�If either party becomes insolvent (by contractual convention)

25

26

Frustration/impossibility:

�Frustration arises when a party is unable to fulfil its obligations under the Contract, but is not in breach.

�Frustration occurs without the liability of either party.

�Circumstances change, preventing the project from being completed.

�Frustration typically occurs in two ways:1) If the task becomes impossible (supervening impossibility)�Such impossibility usually arises due to facts that the

promisor had no reason to anticipate and did not contributeto the occurrence of. (i.e. landslip, flooding)

2) If the task becomes illegal (supervening legality)

�Supervening illegality is when a statute or regulation orcourt decision makes the object of an offer illegal.

27

Termination (Ending the Contract)

�Section 8 of SBC/Q governs Termination

�Defines the processes that parties must follow to “determine” the Contract - i.e. bring it to an end.

�Termination does not completely end the Contract.

�After termination:�Principal obligations can no longer be enforced.

�e.g. Contractor no longer obliged to complete the Works; Employer no longer obliged to pay for the Works.

�Remaining obligations continue to have effect.

�e.g. Dispute resolution methods continue to exist.

28

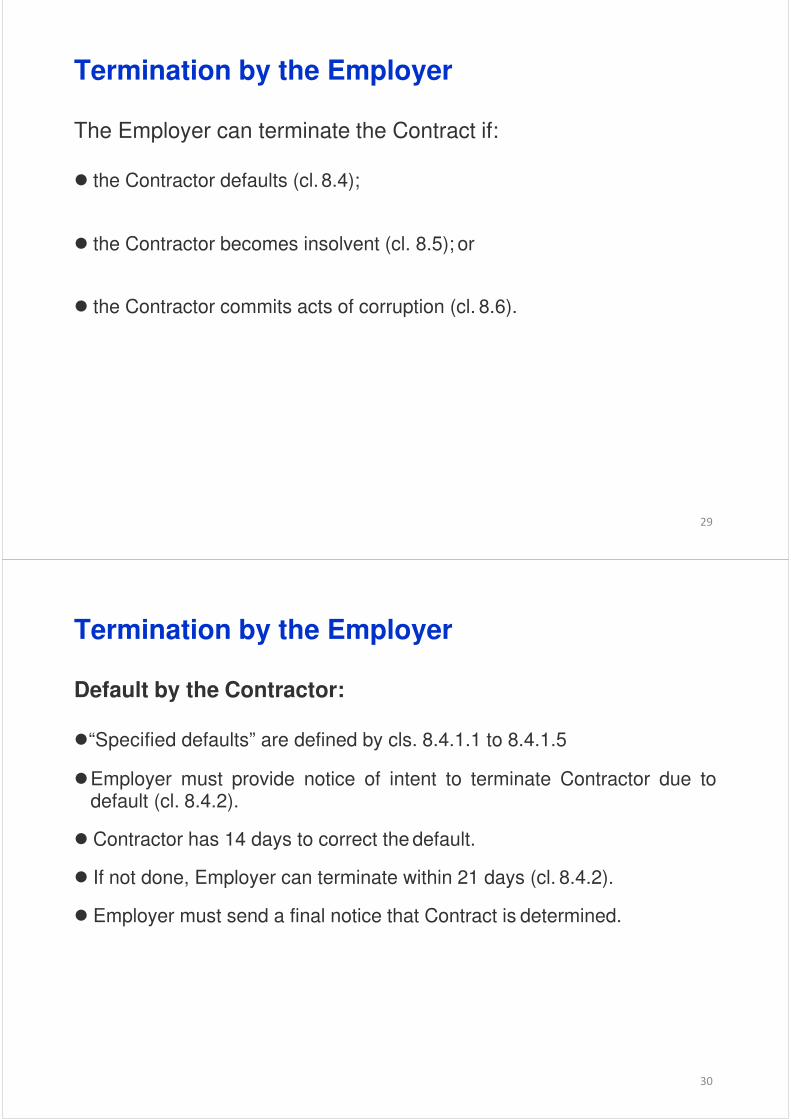

Termination by the Employer

The Employer can terminate the Contract if:

� the Contractor defaults (cl. 8.4);

� the Contractor becomes insolvent (cl. 8.5); or

� the Contractor commits acts of corruption (cl. 8.6).

29

Termination by the Employer

Default by the Contractor:

�“Specified defaults” are defined by cls. 8.4.1.1 to 8.4.1.5

�Employer must provide notice of intent to terminate Contractor due to default (cl. 8.4.2).

� Contractor has 14 days to correct the default.

� If not done, Employer can terminate within 21 days (cl. 8.4.2).

� Employer must send a final notice that Contract is determined.

30

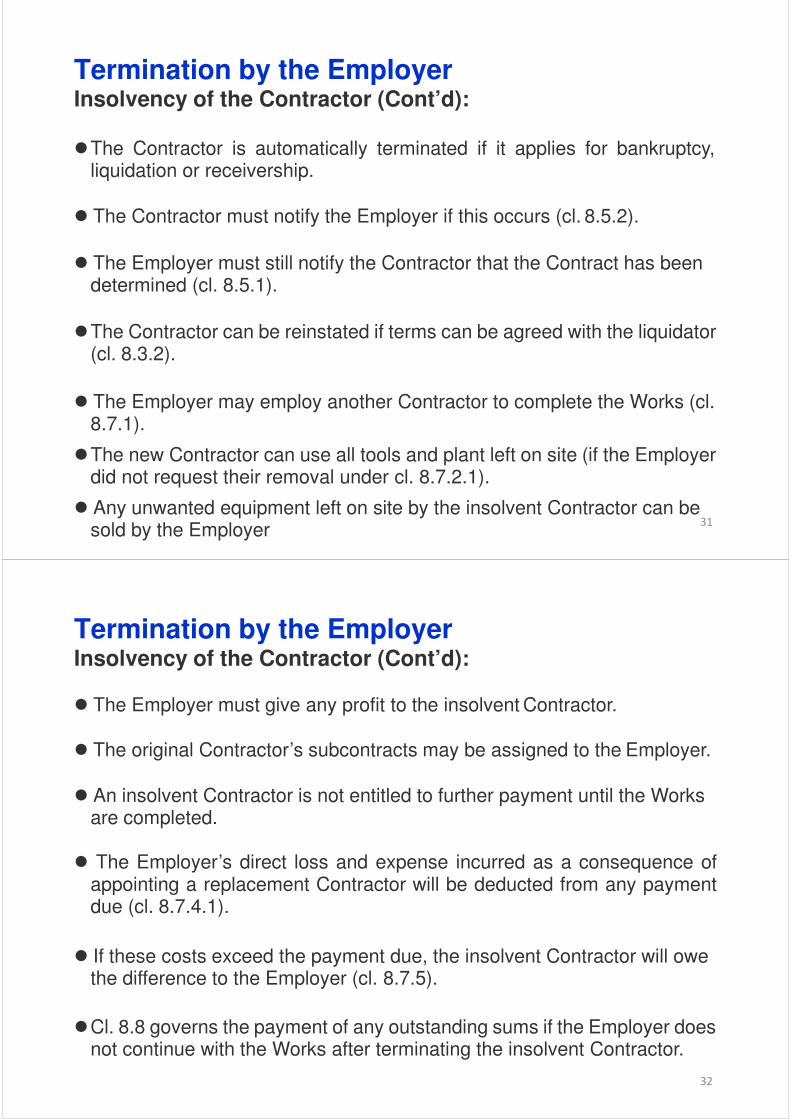

Termination by the EmployerInsolvency of the Contractor (Cont’d):

�The Contractor is automatically terminated if it applies for bankruptcy, liquidation or receivership.

� The Contractor must notify the Employer if this occurs (cl. 8.5.2).

� The Employer must still notify the Contractor that the Contract has been determined (cl. 8.5.1).

�The Contractor can be reinstated if terms can be agreed with the liquidator (cl. 8.3.2).

� The Employer may employ another Contractor to complete the Works (cl. 8.7.1).

�The new Contractor can use all tools and plant left on site (if the Employer did not request their removal under cl. 8.7.2.1).

� Any unwanted equipment left on site by the insolvent Contractor can be sold by the Employer

31

Termination by the EmployerInsolvency of the Contractor (Cont’d):

� The Employer must give any profit to the insolvent Contractor.

� The original Contractor’s subcontracts may be assigned to the Employer.

� An insolvent Contractor is not entitled to further payment until the Works are completed.

� The Employer’s direct loss and expense incurred as a consequence ofappointing a replacement Contractor will be deducted from any paymentdue (cl. 8.7.4.1).

� If these costs exceed the payment due, the insolvent Contractor will owe the difference to the Employer (cl. 8.7.5).

�Cl. 8.8 governs the payment of any outstanding sums if the Employer does not continue with the Works after terminating the insolvent Contractor.

32

Termination by the Contractor

�The Contractor can terminate the Contract if:

�the Employer defaults (cl. 8.9); or

�the Employer becomes insolvent (cl. 8.10).

�The Contractor can determine its own employment under the Contract if:

�the Employer causes certain “specified defaults” (cl. 8.9.1); or

�certain “specified suspension events” arise (cl. 8.9.2).

�The Contractor‟s notification procedure mirrors the Employer's (cls. 8.9.1; 8.9.2; 8.9.3).

33

Termination by the Contractor

Insolvency of the Employer

�The Contractor can determine the Contract if the Employer become insolvent.

� Cl. 8.10 defines the Contractor’s procedure, and mirrors cl. 8.5, which the Employer must follow to determine the Contractor.

�The definition of “insolvency” provided by cl. 8.1 dictates when the Employer or the Contractor can determine the Contract.

34

Termination by Employer or Contractor

�Cl. 8.11 governs determination of the Contract by either party.

�Cl. 8.11.1 defines the events that can cause either party to determine the Contract.

�These are events that frustrate the Contract.

�Neither party is liable for causing them

�e.g. supervening illegality or supervening impossibility make it impossible to complete the Works.

35

Remedies for Breach of Contract

Required when a party fails to perform its obligations arising from the Contract

�Material breach

�The contract will be brought to an end “determination of the contract”.

�Non-material Breach

�Damages will be paid by the party in breach to return the affected party to their original position

�These damages are unliquidated (Their amount must be determined by the Court because it was not agreed beforehand)

36

Specific implement or damages?

�A remedy is the device provided by the Contract to compensatean innocent party for the loss or expense it incurs as aconsequence of the other party’s breach.

�Specific implement:

�It requires the court to grant an order requiring a party to perform aspecific act. (In England, specific performance is an equitableremedy available for breach of contract and may be granted in additionto or instead of damages.)

�Allows the innocent party to compel the party in breach to fulfil itsobligations.

�Only possible when the innocent party must be able to insist on theWorks being completed.

�It is seldom possible to prove this requirement, causing most remediesto be in the form of damages. 37

Withholding payment under the Construction Act

�The Housing Grants, Construction and Regeneration Act 1996clearly defines the circumstances in which payment due under aconstruction contract can be withheld.

�Before withholding payment, a party intending to do so must givenotice of this intention to withhold payment, sating:

�the amounts that will be withheld; and

�the grounds justifying each withholding.

�Cl. 4.13 defines the process the Employer must follow if intendingto deduct from the amount due under an Interim Certificate.

�In Singapore context, refer to Security of Payment Act (SOPA)

38

Suspending performance

�The Housing Grants, Construction and Regeneration Act 1996 clearly gives a party the right to suspend work if:

�payment has not been made by the due date; and

�notice explaining why payment is being withheld has not been received.

�The Contractor’s statutory right of suspension is accommodated by cl.4.14 in SBC/Q.

39

Recourse under Tort

�A party can owe a duty to another in the absence of a contract (Each party has a Duty of Care towards the other)

�Organisations still have obligations to each other irrespective of contract

�In construction, liability under delict (Tort) is most likely to arise due to negligence.

� All other possibilities are governed by standard contracts.

�A claim for recompense under delict requires:�a duty of care to not be fulfilled; and

�the innocent party to suffer loss.

40

PRINCIPLE OF CONTRACT LAW

(PART 3 OF 3)

41

Learning Outcome

�Understand Privity of Contract

�Assignment and novation

�Third party rights and collateral warranties

�Sub-letting

�Insurance, guarantees and bonds

42

Privity of contract�A contract between two parties can only create rights and liabilities

between those two parties.

�Historically, third parties cannot be affected, and cannot affect, acontract to which they are not a party.

�The “privity principle” = the rights and obligations created by acontract are only enforceable by the parties to it

�In construction, third parties often require rights as a consequence ofthe Contract between two parties as they are affected by the parties‟work (i.e. owners of adjoining buildings, underwriters, etc.)

�The construction industry has historically used collateral warrantiesto create a duty of care between a party to a Contract and a third partythat is not part of the Contract.

43

Privity of contract (Cont’d)

The strict application of the doctrine of Privity of Contract can now be moderated in one of the following ways:

1) Assignment.

2) Novation.

3) Contracts (Rights of Third Parties) Act 1999

4) Collateral Warranties.

44

Assignment

�Under common law, a party can assign its rights to another party, butnot its obligations.

�Assignment takes place when the original party transfers some or allof the contractual rights to someone who is otherwise outside thecontract.Eg:- a contractor obtain finance by assigning the rights of payment under a contract as collateral (security) for a loan

�Cl. 7.1 requires a party wishing to assign rights arising from SBC/Qto obtain the written consent of the other party.

�Cl. 7.2 allows the Employer to assign its rights with regard to theContractor's obligations to the purchaser or tenant of the Works.This gives the purchaser the Employer’s rights to the correction of defects, for example.

45

Novation

�It is not possible for one party to a contract to assign the wholecontract (i.e. rights and obligations), to a third party and simplydisappear

�Novation is the creation of a completely new contract to replacethe original one.

�Instead of assigning rights created under the Contract, theContract is terminated and a new one created with the new party.

�In design and build procurement, novation allows the Employer’sdesign team to be transferred to the winning Contractor.

�Novation creates problems of liability

46

The Contracts (Rights of Third Parties) Act 1999

�Empowers third parties by expressly given rights by a contractbetween two other parties (e.g. SBC/Q between Employer andContractor) to enforce those rights.

�Construction examples:

�The Contractor may be obliged to not disrupt an adjoining business. The adjoining business is the third party. The Contractor would be liable to it if disruption did occur.

�A third party may be given the right to damages if the actions (orinactions) of the Employer or Contractor cause it to incur loss and/orexpense.

�SBC/Q applies the Construction Act through cls. 7A and 7B; plusSchedule 5.

47

Collateral warranties�A collateral warranty is another contract formed between one of

the parties to the main contract and a third party.

�For example, the Contractor takes out a collateral warranty with a third

party to satisfy a condition of the main Contract with the Employer.

�“Collateral” = related to and dependent on another contract

�“Warranty” = captures a promise made from one party to another

�A collateral warranty overcomes the problems caused by the privity principle.

�SBC/Q accommodates the use of collateral warranties as an alternative to third party rights in:� Part 2 of the Contract Particulars� Defines the warranties the Contractor must provide� C.l.s. 7C to 7E 48

49

Sub-contracting under SBC/Q�Two methods (i.e. appointing subcontractors / “sub-letting”).

�The Contractor can select and appoint subcontractors tocomplete all or part of the Works (cl. 3.7).

�The Contractor must obtain the CA‟s written consent beforeappointing (cl. 3.7.1).

�The CA will not withhold the provision of consent (cl. 3.7.1).

�The Contractor is vicariously liable for the performance of allsubcontractors.

�“Listed” subcontractors are chosen by the Contractor tocomplete a designated part of the Works from a list of at leastthree subcontractors provided by the Employer (cl. 3.8).TheContractor is free to choose any subcontractor from the listprovided. The Contractor or Employer can add to the list (cl.3.8.2). 50

Sub-contracting under SBC/Q (Cont’d)�From a contractual viewpoint:

�“Domestic” subcontractor = listed subcontractor.

� “Domestic subcontractor” is not defined by SBC/Q.

� “Listed subcontractor” is not defined by SBC/Q.

� All subcontractors have the same contractual standing

�Both domestic and listed subcontractors are “sub-contractors” under SBC/Q (cl. 3.8.4).

�The Contractor is vicariously liable for their performance, irrespective of how they were introduced to the project.

�Cl. 3.9 defines mandatory terms of sub-contractors‟ appointment. Note cl. 3.9.2.5 (re collateral warranties).

51

Nominated subcontractors

�Why does JCT SBC/Q not allow “nominated subcontractors?”

�Nominated subcontractors and nominated suppliers were widely used under JCT98.

“There appears to have been little use of the provisions for Nominated Sub-contractors and little appropriateuse of the Nominated Supplier Provisions. The provisions of JCT98 for listing of sub-contractors have beenretained and, in the JCT's view, the specifying of a supplier is a matter generally better dealt with in theContract Bills or other Contract Documents.”

JCT (2005). Standard Building Contract: Guide (SBC/G). London: Maxwell & Sweet.

�JCT2011 share the same stand as JCT2005.

52

Indemnity

= a legal exemption from incurred liabilities or�“Indemnity” penalties.

�When a risk is transferred to another party, it indemnifies (pays compensation) that party against that risk.

�If an event against which a party has sought an indemnity occurs, it will not bear the cost of resolving it.

�Insurance policies provide an indemnity.

�The insurance company indemnifies the policy holder against specified risks in return for payment of a premium.

�The indemnity should return the policy holder to their original position.

53

Insurance

“An insurance contract is an agreement whereby one party, the insurer, inreturn for a consideration, the premium, undertakes to pay the other party,the insured, a sum of money or its equivalent upon the happening of aspecified event which is against the insured’s financial interest.”

Eaglestone, F. Insurance under the JCT Forms.

54

Two types of insurance must be considered:

1) Liability insurance� The insurance company undertakes to indemnify the insured against the

damages and legal costs which would occur if the insured became liablefor those damages or costs.

� This causes the risk borne by the insured to be passed to the insurer.

� Examples: Car insurance, Public liability insurance, Professional Indemnityinsurance (“PI” insurance)

2) Loss insurance� The insurance company undertakes to compensate the insured for loss or

damage that the insured suffers itself rather than loss or damage that athird party suffers (which would be covered under liability insurance).

� The insurance company is not required to provide an indemnity against theactions of third parties as loss insurance does not consider third parties;only the insured.

� Loss insurance remains valid even if the insured incurs loss or damagedue to its own mistakes (and negligence in some policies).

55

Guarantees and bonds

�The Contractor may be required to provide a guarantee or a bond to prevent it non-performance.

�Although often required, guarantees and bonds are not accommodated in a non-amended SBC/Q.

�Bonds and/or guarantees are usually requested by the Employer.

�A bond is provided by a third party which underwrites the Contractor’s fulfillment of its Contractual obligations.

�A guarantee is provided by the Contractor's parent company for the same purpose.

�Performance Bonds are common.

�Retention bonds are becoming common.56

TYPES OF CONTRACTS

57

Learning Outcomes

�Understand types of Contracts

�Identify various types of construction contract

58

Types of Contract

Contracts have different types based on their payment systems.

Two main payment systems are:

�Price based:

�These involve lump sum and measure (re-measurement)contracts. Prices are submitted by the contractor in his tender.

�Cost based:�These involve cost-reimbursable and target cost contracts.The actual costs incurred by the contractor are reimbursed,together with a fee for overheads and profit.

59

Three types of contract available:1)Lump Sum Contracts:

�Where the Contract Sum is determined before constructionstarts.

�A “lump sum” contract fully completes the design so that theContract Sum can be accurately determined before constructionworks is started. The Contractor undertakes a defined amount ofwork in return for an agreed sum (Relevant standard form is TheJTC2011 SBC/Q)

�Pros: high degree of certainty about the final price, easiercontract administration in the event of no or minimal change

� Cons: not suitable when substantial change is expected

60

Three types of contract available (Cont’d):2)Measured Contracts:�Contract Sum is not finalised until after completion, howeverthe method of determining the Contract Sum (i.e. measuring theWorks) is agreed between the Employer and the Contractorbefore the Works start (Relevant standard form is The JTC2011SBC/Q)

�Pros: some flexible for design change, time is saved in notpreparing full BQs at initial stage (but re-measurement of theWorks are required once complete), allow work to commence onsite when the design is only in outline form

�Cons: contract is quantity based and adversarial (only therates form part of the contract not the quantities, more risk thanlump sum contracts (but probably with programme advantage),final price may not be determined until long after the Works arecomplete, less initiative for designer to complete designs atearlier stage

61

Three types of contract available (Cont’d):3)Cost Reimbursement Contracts:

�Contract Sum is determined by calculation of the Contractor’sactual labour, plant and materials cost, to which a previousagreed percentage addition is made to cover the Contractor’soverheads and profit (cost plus).

� Cost plus a percentage fee� Cost plus fixed fee� Cost plus fluctuating fee� Cost reimbursement based on a target cost

�Pros: provide extreme flexibility, allow and require high level of client involvement

�Cons: little incentive for the contractor to perform efficiently, no estimate of final price at tender

62

Using NEC Contract as example:

63

Principles of Standard Forms of Contract

The construction industry uses Standard Forms of Contract to:

�Save time in writing new contracts

�Provide a check list of issues to agree

� Incorporate previous judicial decision

�Promote familiarity

64

65

The Contract Documents

�Contract incorporate several documents

�Under traditional procurement, these are:� Articles ofAgreement� Conditions of Contract� Contract Drawings� Contract Bills of Quantities� Specification

66

Families of Standard Forms of Contract

�JCT (and SBCC) - Scottish Building Contract Committee

�NEC

�FIDIC

�ICE

�GC/General Works

�ACA

67

Families of Standard Forms of Contract (Cont’d)

�JCT (Joint Contracts Tribunal) – comprehensive, cover every procurement route relationship, most widely used.

�NEC (New Engineering Contract)

68

Families of Standard Forms of Contract (Cont’d)

69

Families of Standard Forms of Contract (Cont’d)

70

Families of Standard Forms of Contract (Cont’d)

71

Families of Standard Forms of Contract (Cont’d)

72

Families of Standard Forms of Contract (Cont’d)

73

Families of Standard Forms of Contract (Cont’d)

74

Families of Standard Forms of Contract (Cont’d)

75

Families of Standard Forms of Contract (Cont’d)

�FIDIC (Fédération Internationale Des Ingénieurs-Conseils) –international standard, used predominantly for infrastructureprojects

� ICE (Institution of Civil Engineers) – for civil engineeringprojects

76

Families of Standard Forms of Contract (Cont’d)�GC/Works – used by central Government, becoming less

common

77

Families of Standard Forms of Contract (Cont’d)

�IChemE (Institution of Chemicals Engineer)

�Partnering Contracts (i.e. ACA PPC 2000 (2004 revision) - ACA(Association of Consultants Architect), NEC3 X 12 Option,JCT/Be Constructing Excellence contract)

78

TENDERING & PROCUREMENT

(PART 1 OF 2)

79

Learning Outcomes

and difference between�Understand tendering strategies tendering and procurement

�Discuss practical application of Tender Strategies

�Understand Project Constraints and Procurement Assessment Criteria (PAC)

�Study main features, pros and cons of Traditional Procurement routes

�Appreciate importance of procurement strategy to influence project success

80

between tendering andDifference procurement:-

1)Procurement is the overall act of obtaining goods and servicesfrom external sources (i.e. building contractor) and includesdeciding the strategy on how those goods are to be acquired byreviewing the client’s requirements (i.e. time, quality and cost)and their attitude to ask.

2)Tendering is an important phase in the procurement strategybut procurement involves much more than simply obtaining aprice. Tendering is the bidding process, to obtain a price and howa contractor is actually appointed.

81

Three main types of tendering strategy:

1) Single-stage tendering – most common strategy by obtaining a price for the whole of the construction Works through issuanceof Invitation to tender documents to a number of competing contractors who are all given the chance to bid for the projectbased on identical tender documents.

82

Three main types of tendering strategy (Cont’d):

2)Two-stage tendering – become more common in recent yearsand is often used where time is constrained (enable overlap ofdesign and tendering process).

�Used when the design process would benefit from thetechnical input of a contractor in the later design stage (to obtainthe early appointment of contractor.

� Preferred contractor is chosen on the basis of the quality oftheir bid,overhead

the quality of their team and and profit allowance rather

their prelim price, than via bid for

constructing the entire project.� Pre-construction services agreement will be put in place for

work with the professional tothe preferred contractor to complete the design.

83

Three main types of tendering strategy (Cont’d):

3)Negotiated Tender - effectively a single-stage tender with a single contractor who returns with an initial price.�This is then negotiated with the client’s professional team

(usually quantity surveyor (PQS)). Competitive advantage of aformal bidding process is compromised.

� Not viable for quasi-government projects.

84

85

86

Practical Application of Tender Strategies– Part 1 of 4

�Producing the pre-tender estimate (PTE)

�Choosing the most suitable tender Strategy

�RIBA Plan of Works/APM work plan

�Setting up the tender including selection of tendering contractors

�Assessing a suitable tender period

87

Practical Application of Tender Strategies– Part 2 of 4�Producing/compiling the tender documents�Invitation to tender letter

� Form of tender

� Contract conditions

� Instructions to tenderers documents

�Project information (preliminaries/works/information/employer’s requirements)

� Design information

� Pricing document

� Typical appendices88

Practical Application of Tender Strategies– Part 3 of 4

�Considering how project-specific factors/abnormal influence a tender

�Issuing the tenders

�During the tender process� Tender queries

� Tender adduenda

� Mind-tender interviews

� Tender withdrawals

89

Practical Application of Tender Strategies– Part 4 of 4

�Receiving tenders� Opening tenders

� Reviewing the tenders

�Checking for errors and conflicts�Equalisation / Normalise process

�Post-tender interviews

�Checklist of further items to review

�Post Tender (draft scoring and evaluation of findings)

�Tender report and notifying tenderers90

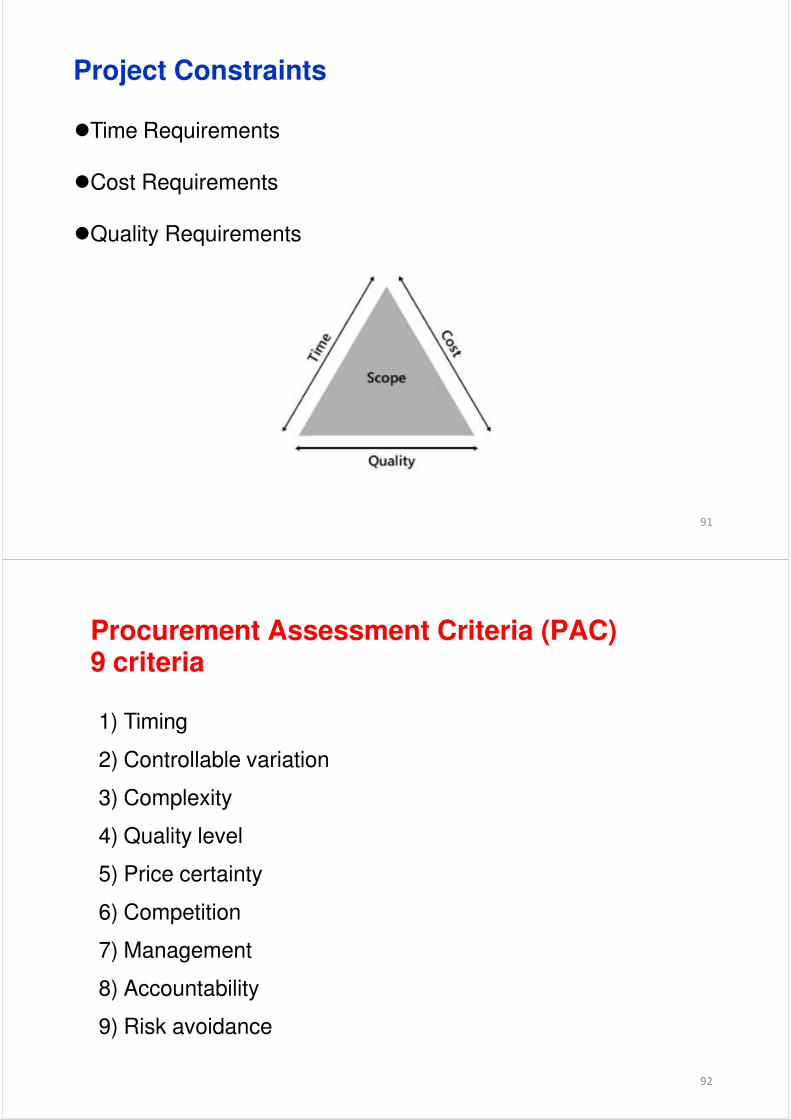

Project Constraints

�Time Requirements

�Cost Requirements

�Quality Requirements

91

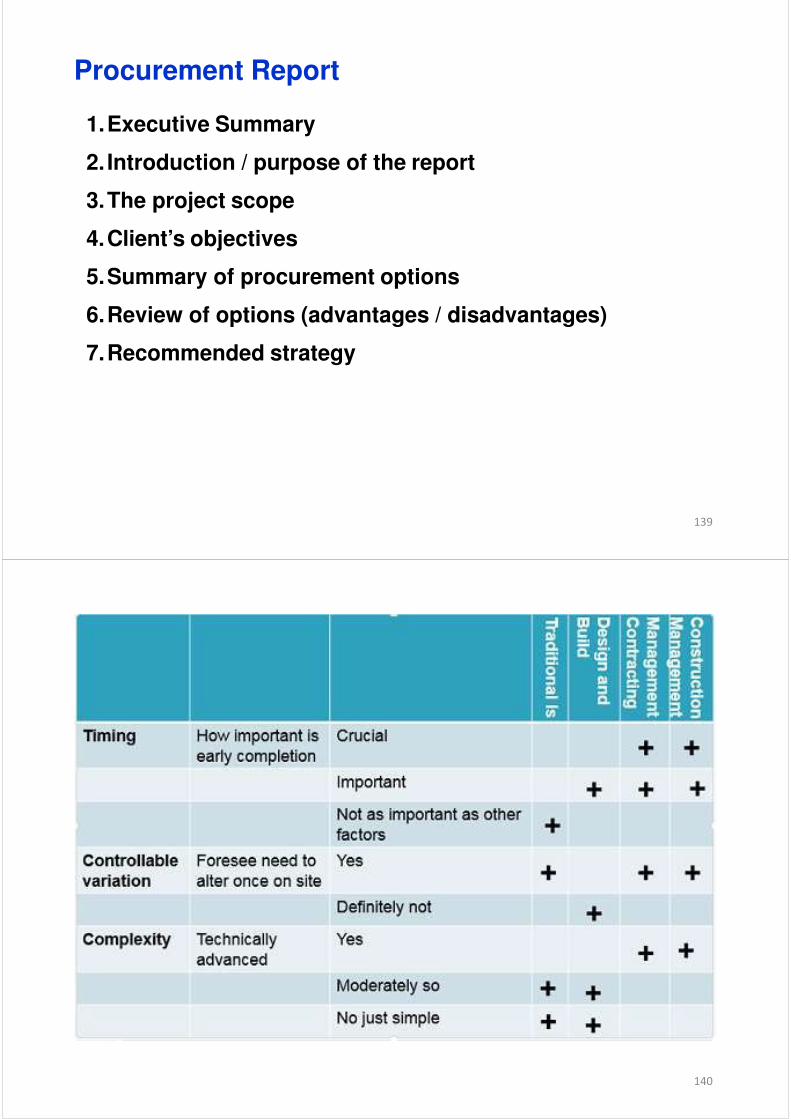

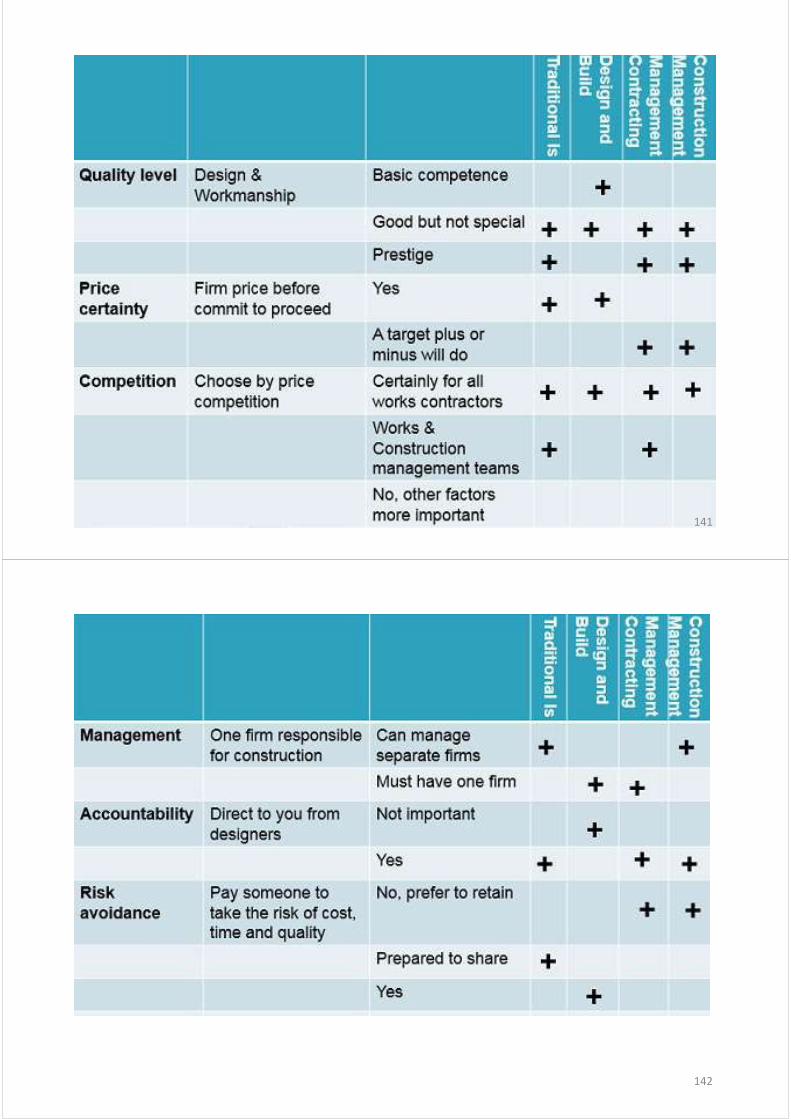

Procurement Assessment Criteria (PAC) 9 criteria

1) Timing

2) Controllable variation

3) Complexity

4) Quality level

5) Price certainty

6) Competition

7) Management

8) Accountability

9) Risk avoidance

92

Procurement Options- Procurement Arrangement Options(PAO)

1) Traditional

2) Design and Build

3) Construction Management

4) Management Contracting

5) Prime contracting

6) Private Finance Initiative (PFI)

93

Traditional Procurement Route Main Features:

�Design is fully developed before commencement of construction

�Follow RIBA Plan of Work

�Tender documentation based on drawings, specifications and Bills of Quantities, Approximate Quantities or Without Quantities

�Tenderers are invited to tender a price to complete thedescribed Works

management of) design &

�Cost relatively certain upfront

�Split of responsibility for (and production

94

95

Traditional Advantages:

�Fair competition, satisfactory public accountability

�Relatively low tender preparation/tendering costs

�Procedures are well known

�Changes to design are reasonably easy to implement and value

�Full control over design quality

96

Traditional

Disadvantages:�No concurrent working (slow to start on site and long duration)

�Vulnerable to claims (additional time and money) in the event that design is incomplete

�Non-involvement of Contractor in planning or design (poor buildability)

�Design risk rests with the client

�Fragmented nature leads to adversarialparticipants, possible conflict

relationships, poorandcommunication between

confrontation

97

Traditional

98

TraditionalTraditional Procurement Variant Route:

1) Traditional sequentialContractors bid on completed design and cost documents

basis of partial2) Traditional accelerated

A Contractor is appointed earlier on the information, by negotiation or in competition

3) Traditional with re-measurementA re-measurement contract uses bills of approximate quantities.The accepted tender sum is a lump sum based on a fixed period,but the quantities used to prepare the tender will be re-measured on completion

99

TENDERING & PROCUREMENT

(PART 2 OF 2)

100

Learning Outcomes

pros and cons of Non-traditional�Study main features, Procurement routes

of procurement strategy to influence�Appreciate importance project success

�Understand Partnering Concepts

�Procurement Report

101

Design & Build Main Features:�Tender doc usually comprise brief to outline scheme stage :

�Building function�Space requirements�Building services performance criteria

�Outline specification of key elements (i.e. finishes, key features, etc.)

�Single point of contact (Contractor is appointed to complete the design and construct project

�Suitability (suited to all clients, including inexperienced clients,suited to project requires cost and time certainty), not suitablefor complex or high quality buildings

�Minimisation of variations (design responsibility lies with theContractor, leading to cost and time savings (compared withtraditional procurement 102

Design & Build Advantages:

�Client interacts with a single point of responsibility

�Inherent buildability

�A firm price can be agreed prior to construction

�Shorter overall duration (compared to traditional)

�Contractor’s design liability can be extended to include fitness for purpose

103

Design & Build Disadvantages:

�Client needs to appoint Contractor before design is complete

�No design overview unless Consultants are appointed by Client

�Difficult for clients to prepare an adequate brief

�Contractors’ bids are difficult to compare

�Design liability limited by use of standard contracts

�Client changes can be expensive

104

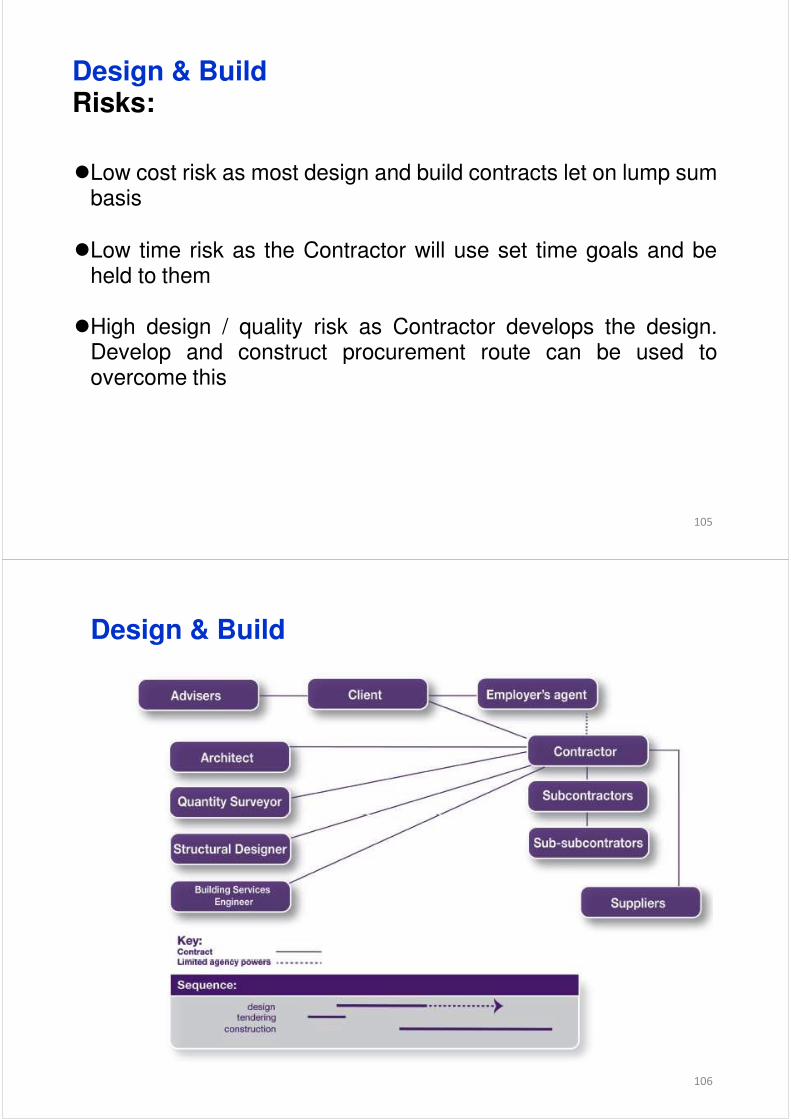

Design & Build Risks:

�Low cost risk as most design and build contracts let on lump sumbasis

�Low time risk as the Contractor will use set time goals and beheld to them

�High design / quality risk as Contractor develops the design.Develop and construct procurement route can be used toovercome this

105

Design & Build

106

Design & Build Variant The Design & Build Variant

107

Design & BuildThe Design & Build VariantNovated Design & Build / Two-Stage Design:

�Competitive Design and Build

�Client prepares “client’s requirements” documents

�Several Contractors tender design proposals brought to (typically) scheme design stage

�Winning contractor appointed on basis of design content (including predicted cost)

�The appointed Contractor then completes and constructs the design

�Novation of the initial design team is required 108

Design & BuildThe Design & Build Variant Develop & Construct Contractor develops the concept design, contractor onlyresponsible for the design development

109

Design & BuildThe Design & Build Variant

Package Deal�“Off the shelf” product�Employer able to view similar completed buildings

Turnkey�Complete package handled by Contractor from commencement

to completion�Contractor does everything including fit-out�Idea : Take possession = turn the key

110

Construction Management Main Features:

�A Construction Manager advises the client

�The Employer contracts directly with the numerous Works Contractors

�Shorter communication lines give quicker responses

111

Construction Management Advantages:

�Potential to reduce project duration

�Individual packages let competitively

�Opportunities to improve buildability

�Breaks down traditional adversarial barriers

�Concurrent working is inherent

�Clarity of roles, risks and relationships for all organisations

�Late changes easily accommodated112

Construction Management Disadvantages:

�No cost certainty at outset

�Needs informed client, able to take an active role in the project

�Clients may not appreciate their risk exposure

�Risks adopted by clients in return for control

�Needs a good quality brief

�Requires a competent project team

�Needs effective control of time and information113

Construction Management Risks:

�Medium cost risk as total cost is not known until last package let

�Medium time risk as no single organisation is solely response fortimed completion

�Low quality/design risk due to close working of client, designersand Works Contractors

�Clients have historically had problems with ConstructionManagement as they have not appreciated the risks associatedwith control

114

Construction Management

115

Management Contracting Main Features:

�Management Contractor advises Client on programming, division of the project into work packages and buildability and obtain tenders

�Work divided into series of packages

�Each package is awarded on a lump sum, fixed price basis to separate Works Contractors

�Construction of each package can start as soon as the Client approves its design

�Design and construction overlap considerably

�Relies on clear communication and co-operation, and mutual trust between Employer and Contractors

116

Management Contracting Advantages:

�Concurrent working is inherent

�Potential to reduce project duration

�Opportunities to improve buildability

�Breaks down traditional adversarial barriers

�Late changes easily accommodated

�Work packages tendered competitively

117

Management Contracting Disadvantages:

�Needs a good quality brief

�Poor price certainty

�Requires a good quality project team

�Difficult to resist Works Contractors’ claims

118

Management Contracting Risks:

�Medium cost risk as total cost is not known until last package let

�Medium time risk as total duration is determined by package selection

�Low quality/design risk due to close working of client, designers and Works Contractors

�Client relies on estimated costs until the last package has been tendered and let

�A Guaranteed Maximum Price (GMP) may be negotiated with the Management Contractor to move cost risk from the client

119

Management Contract

120

121

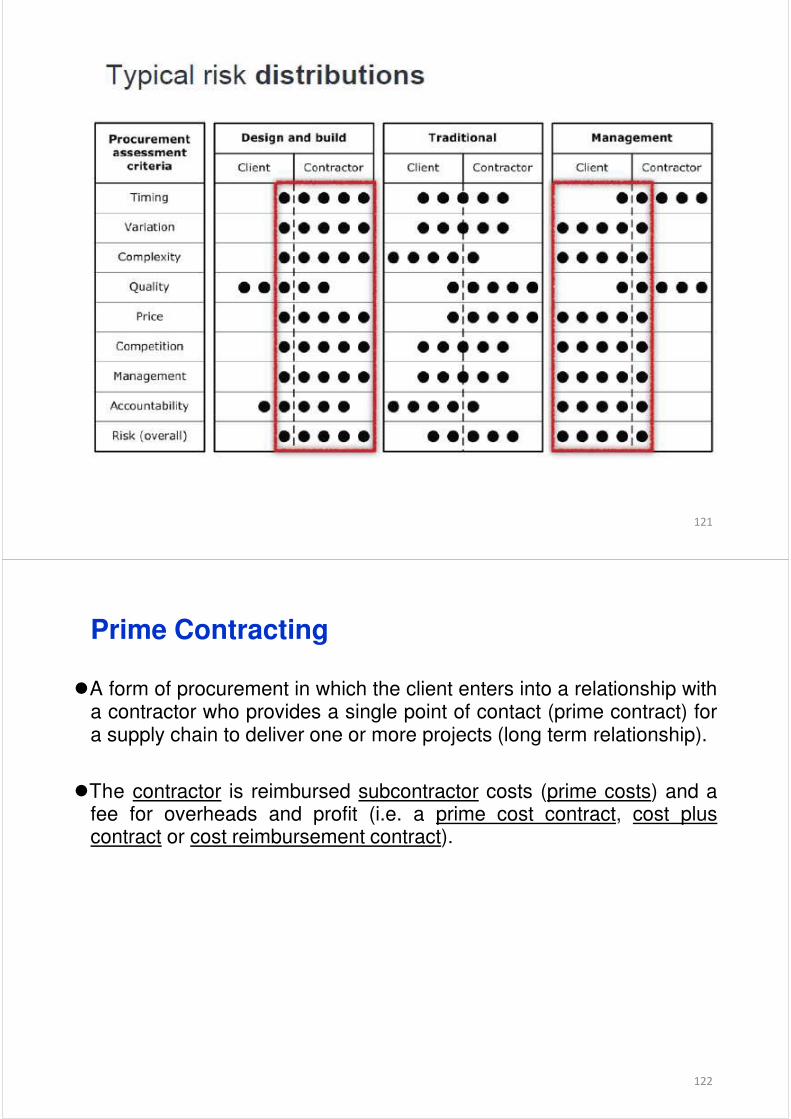

Prime Contracting

�A form of procurement in which the client enters into a relationship witha contractor who provides a single point of contact (prime contract) fora supply chain to deliver one or more projects (long term relationship).

�The contractor is reimbursed subcontractor costs (prime costs) and afee for overheads and profit (i.e. a prime cost contract, cost pluscontract or cost reimbursement contract).

122

The Private Finance Initiative (PFI) Main Features:

�A public sector client procures a service from the private sector

�Several private sector organisations collaborate to provide the service

�New buildings or infrastructure is usually required

�The quality of service is specified; the quality of capital assets is not (other than functionality)

�Capital assets are financed, designed, constructed, and operated by the private sector

�Capital assets may be retained by the private sector at the end of the agreement

123

The Private Finance Initiative (PFI) Main Features (Cont’d):

�PFI schemes run for long time periods

�The private sector is exposed to many risks

�Financing risks

�Demand risk (continuity and certainty)

�Technology risk

�PFI schemes convert public sector capital expenditure into revenue expenditure

�PFI schemes are complex collaborations and generally involves 3 types of organization:-

�The public sector client

�The private sector provider of the required service

�Funders and investors124

The Private Finance Initiative (PFI) PFI Scheme Participants:

The public sector client:�instigates the project to advance its primary strategy

�is usually inexperienced in PFI procurement

�is advised by central government bodies

�procures the service from the private sector via a singlecontractual link

�procures the service from a Special Purpose Vehicle (SPV) created by the private sector

125

The Private Finance Initiative (PFI) PFI Scheme Participants (Cont’d):

The private sector service provider:�The private sector service provider comprises several private

sector organisations that collaborate to provide the service viathe Special Purpose Vehicle (SPV)

�The SPV is an legal entity created by the collaborating privatesector organisations that:

� Procures design, construction and operating expertise from the construction industry

� Secures finance from funders and investors

� Distributes risks inherited from the client

126

The Private Finance Initiative (PFI) PFI Scheme Participants (Cont’d):

the capital required to

The funders and investors:�The funders and investors provide

construct new infrastructure

�Funders provide the majority of finance as loans that arerepaid during scheme operation

�Investors provide further finance through part ownership ofthe scheme. They are paid dividends in addition to repaymentof stock investments

�Funders and investors influence the private sector serviceprovider to ensure they will earn the required return on theirinvestments 127

The Private Finance Initiative (PFI) PFI Scheme Participants (Cont’d):

�“The consortium” comprises all the collaborating private sector organisations

� Construction designers, constructors, operators

� Funders and investors

� The SPV

128

129

The Unitary Charge:

�In return for access to the service the client makes regular payments to the SPV

�This is the “unitary charge”

�The private sector uses the unitary charge to:

� Finance the construction of new infrastructure

� Finance the operation of that infrastructure to a performance level agreed with the client

� Earn a profit130

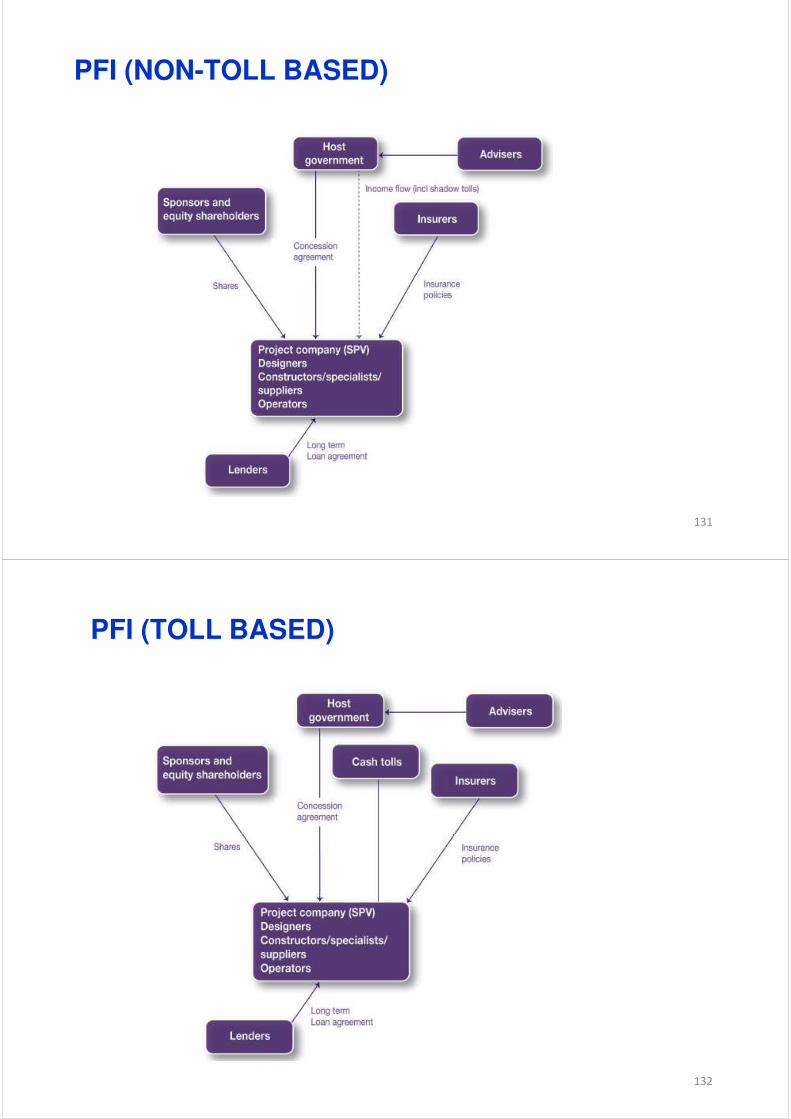

PFI (NON-TOLL BASED)

131

PFI (TOLL BASED)

132

Partnering concepts

Collaborative approaches:

�Recognise that success is more likely if organisations worktogether for the good of the project, rather than themselves

�Are implemented as:

� Short term project partnerships; or

� Long term strategic partnerships

�Reply on a neutral third party to help organisations partner byfacilitating the process of establishing common ground andshared attitudes

133

Partnering defined “Partnering is a set of strategic actions,

which embody the mutual objectives of a number of firms achieved by co-operative decision making aimed at using feedback to continuously improve their joint performance.”

JCT Constructing Excellence contract

134

Partnering defined

�All partnerships must:

� Develop mutual objectives

� Solving problems collaboratively and simplyescalate into disputes

� Measure performance to characterise

before they

continuousimprovement (Measuring continuous improvement)

�In addition, they should:

� Share common values and cultural norms among partners

� Incentivise partners to continually improve

� Provide value for money to the client

135

Forming Partnerships

�Forming a partnership requires a step-change from traditional practice

�An independent facilitator will guide the process

�Usually through a series of workshops

� Linked to commercial development if strategic partnering

� Linked to project process if project partnering

�Facilitator aims to build common understanding, practices and goals among partners

136

Value for money and partnering

�A criticism of partnering is the difficulty of ensuring value for money

�Achieving VFM from partnering requires:

� Comparison of partnership performance against otherprocurement routes (using additional metrics than costalone)

� Demonstrating continual improvements in performance throughout partnership life

� Reforming the partnership after periods of operation

� Removing underperforming organisations

137

Target Costing

�If actual cost < target cost

� Contractor and client share the saving

� Target cost must be realistic and not inflated

�If actual cost > target cost

� Contractor and client share the additional cost

�If actual cost > GMP

� Contractor and client share the additional cost below GMP

� Contractor bears all additional cost above GMP

138

Procurement Report

1.Executive Summary

2. Introduction / purpose of the report

3.The project scope

4.Client’s objectives

5.Summary of procurement options

6.Review of options (advantages / disadvantages)

7.Recommended strategy

139

140

141

142

*Providing all issues resolved during 2nd stage, if not the 2 stage would score lower

** Client at risk during the 2nd stage negotiations143

*Providing all issues resolved during 2nd stage, if not the 2 stage would score lower

** Client at risk during the 2nd stage negotiations144

STAKEHOLDER MANAGEMENT

145

Learning Outcome

�Understand Stakeholder

�Stakeholder Management & Engagement

�Stakeholder Analysis and Register

146

What should you do with stakeholder throughout the project?

1)Identify all of them2) Determine their requirements3) Determine their expectations4) Determine their interest5) Determine their level of influence6) Plan how you will manage them

7)Plan how you will communicate with them 8) influence andManage their expectations,

engagement9) Communicate with them

and stakeholder10) Control communications engagement 147

1) Identify all of them

�As early as possible

�Stakeholders discovered late in the project will likely request changes, which can lead to delays

�Internal/External, Primary/Secondary, Direct/Indirect, Overt / Covert

� People, groups or organisations that couldpositively or negatively impact or be impacted by the project

148

2) Determine their requirements

consequences if

�Conduct requirements reviews

�Inform people the negative requirements are found later

149

3) Determine their expectations

�More ambiguous than stated expectation, may beunidentified requirements

� Intentionally or unintentionally hidden

�Unidentified expectations will have major impactsacross all constraints

�Once captured, expectations are analysed andmay be converted to requirements and becomepart of the project

150

4) Determine their interest�Determine level of interest to plan strategy to

increase stakeholder’s interest and level ofengagement

�Determine stakeholder’s interests related to theproject and, where appropriate, attempt to eitherbuild these interests into the project or implementthem as reward

�Engagement levels: unaware, resistant, neutral,supportive, leading

151

5) Determine their level of influence�To some degree, each stakeholder will be able to

negatively or positively effect a project

�Should be identified upfront and managed accordingly

�Power / Interest, Power / Influence, Influence / Impact, Power / Urgency / Legitimacy

� Analyse potential impact or support (i.e. keepsatisfied, manage closely, monitor (minimumeffort), keep informed.

152

used forMultiple classification models stakeholders’ analysis such as:

�Power / Interest

� Grouping the stakeholders based on their level ofauthority (power) and their level of concern(interest)

�Power / Influence� Grouping the stakeholders based on their level of

authority (power) and their active involvement(influence)

153

Multiple classification models used for stakeholders’ analysis such as (Cont’d):�Influence / Impact� Grouping the stakeholders based on their active

involvement (influence) in the project and theirability to effect changes to the project’s planningor execution (impact)

�Salience model (Power / Urgency / Legitimacy)� Describing classes of stakeholders based on their

power (ability to impose their urgency (need forimmediate attention), and legitimacy (theirinvolvement is appropriate).

154

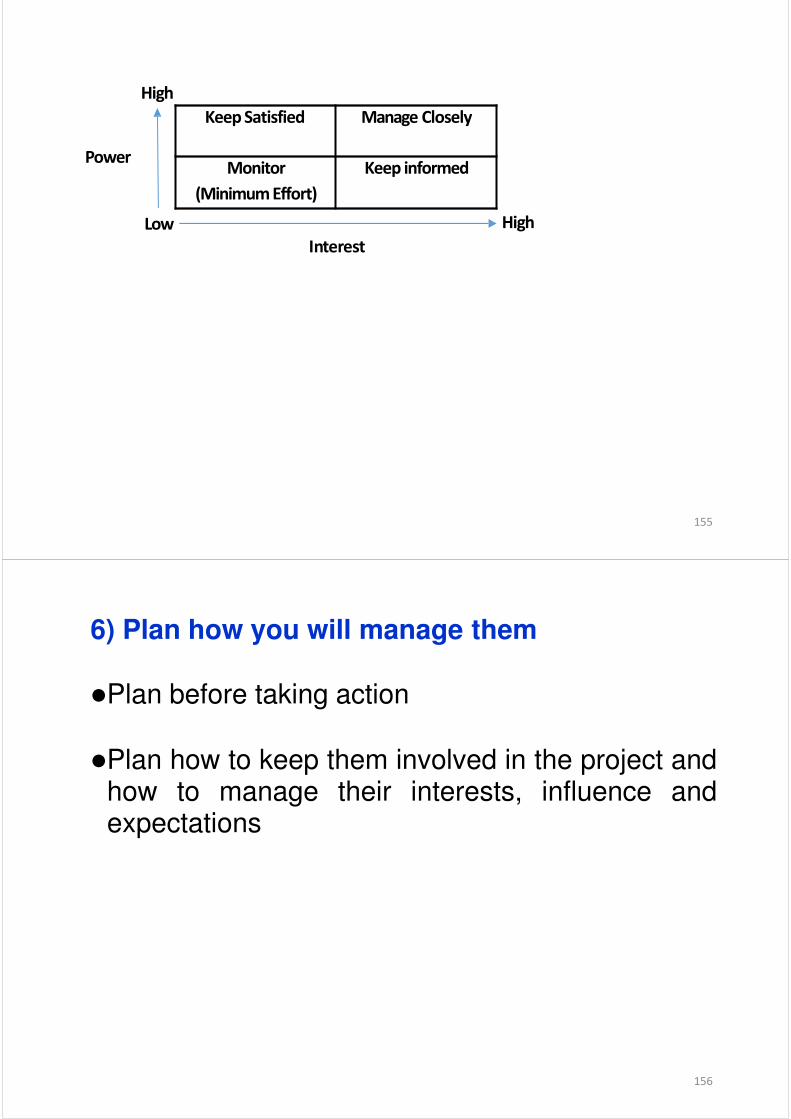

High

High

Power

Low

Interest

Keep Satisfied Manage Closely

Monitor

(Minimum Effort)

Keep informed

155

6) Plan how you will manage them

�Plan before taking action

�Plan how to keep them involved in the project andhow to manage their interests, influence andexpectations

156

7) Plan how you will communicate with them

�To keep stakeholders involved and get them torelate their thoughts and concerns to plan howinformation will be shared

� Remember communication as the most frequentcauses of problems on projects so careful

preventcommunication planning can help problems

157

expectations, influence and8) Manage their engagement

doesn’t end during�Managing stakeholders project initial stage

the life of the�On-going process throughout project

158

9) Communicate with them

�Stakeholders are included in projectpresentations and receive project information,including progress reports, updates, changes, etc.

� Regular engagement with stakeholders

159

10) Control communications and stakeholder

withengagement

�Good communication and relationships stakeholders are critical to success

�Essential to monitor both areas and to determineif and where communication and/or relationshipsare breaking down and then adjust approach asnecessary

�Manage closely, keep satisfied, keep informed,monitor

160

Stakeholder Analysis

�Classification tools such as power/interest grids can be used to group stakeholders

�Group by qualifications lie authority level, impact or influence, or requirements

� Help better manage stakeholders on the project

161

Stakeholder Register� Compilation of stakeholders’ information

� May include stakeholders’ name, title, supervisor,

requirements and expectations, influence, attitude about the

impact project,

project role, contact information, major

and the

classification the individual falls into, and other relevant information

STAKEHOLDER REGISTER

Project Title Project No.

ID Name Title Department Contact Info Impact

Major

Requirements

Major

Expectations

Influence

(1 to 5)

Role(s) in

Project

Responsibilities

in ProjectClassification

1

2

3

162

and

Stakeholder Analysis Matrix (SAM)

�Stakeholder analysis information management strategies

� Sensitive information not to be published

No. Stakeholder Influence/Interest

Impact Assessment

Potential Stakeholder ManagementStrategies

1

2

163

CONTRACT ADMINISTRATION

(PART 1 OF 3)(Refer to JCT2011/ SBC/Q for this Module)

164

Learning Outcome

�Structure of Contract Documents

�Purpose of clauses and parts of JCT2011 SBC/Q

165

Contract Documents comprise:(Refer to JCT2011 Notes 6.1)

�The Agreement and its Conditions (should be from a standard form)

�The Contract Drawings

�The Contract Bills (the Bills of Quantities, including their‘preambles’ & specifications)

166

The Contract Sum

�When the Contract is executed, the selected tenderer’s tenderprice becomes the Contract Sum

�The Contract Sum is the amount the Employer will pay to theContractor in the event that there is no design changes requiredduring construction and no damage arise.

�The Contract Sum is defined in JCT2011/ SBC/Q Article 2:

167

Employer’s Obligations:

�Payment of the Contract Sum (Article 2)

�Possession of the site (cl. 2.4)

�Administration of the Contract - Appoint:�The Architect / Contract Administrator (Article3)� The Quantity Surveyor (Article 4)

�The CDM Coordinator (i.e. planning supervisor”) if none then the Architect (Article 5)

� The Principal Contractor (Article 6)� An arbitrator, if agreed to have one (Article 8; cl. 9.3)

If QS or CA quits, Employer must appoint a replacement within 21 days (cl. 3.5)

168

Employer’s Obligations (Cont’d):

�Insurance and Indemnity (Cl. 6.7 to 6.11), in the event that the Employer will insure the Woks against “all risks” duringconstruction, Joint name policy, risks to be covered (cl. 6.8), Option B to the construction of new buildings (Schedule 3, cl. B.1to B.3), Option C applies to construction in or alteration of existing buildings (Schedule 3, cls. C.1 to C.4), Employer’s negligence isnot offset by Contractor’s public liability insurance, which is alsorequired (cl. 6.1)

�Confidentiality – prevents the commercial information relation

Employer from sharing to the Contractor with

any third

parties

�Health & Safety – must ensure that Works do not commence untilHSE plan is in place, The Construction (Design andManagement) Regulations (CDM) (Cls. 3.23, 3.24)

The Construction (Design and Management) Regulations (CDM) are the main set of regulations for managing the health, safety and welfare of construction projects.

169

Contractor’s Obligations:

�To construct the Works as described in the Contract. Obligationcreated by Article 2

�C.l. 2.1 requires the Contractor to complete the Works in a“proper and workmanlike manner” in compliance with theContract Documents.

�Quality of workmanship�Materials (cl. 2.3.1), workmanship (cl. 2.3.2) “as described”.

�If the BQ do not define the required quality of materials orworkmanship, the work must be “of a standard appropriate tothe Works” (cl. 2.3.3)

�If the CA is not satisfied with the quality of materials orworkmanship, he can instruct the Contractor to remedy this (cl.3.19) and cost to be borne by Contractor

170

Contractor’s Obligations (Cont’d):

�Insurance and Indemnity (Cl. 6.7), in the event that the Contractorwill insure the Woks against “all risks” during construction, Jointname policy to also indemnify the Employer (cl. 6.2), risks to be covered (cl. 6.8), Option A applies to the construction of newbuildings (Schedule 3, cl. A.1 to A.4), Public liability insurance is also required (cl. 6.1). Insurance against Personal Injury andProperty Damage & Insurance against Damage to the Works

�Access and supervision – Contractor is obliged to grant accessto the site to the CA (cl. 3.1), Employer’s representative (cl. 3.3)and keep a competent person-in-charge on the site at all times(cl. 3.2)

171

Contractor’s Obligations (Cont’d):

�Health & Safety – to comply with all relevant Statute (i.e. the law), even though they have to anyway (c.l. 2.1) – Contractor liable tothe Employer for any breach caused by non-compliance with Statute – CDM Regulations, Health and Safety at Work Act 1974.Health and Safety at Work Act 1974.

Often referred to as HASAW or HSW, this Act of Parliament is the main piece of UK health and safetylegislation. It places a duty on all employers "to ensure, so far as is reasonably practicable, the health,safety and welfare at work" of all their employees.

172

The Employer’s Agents

�An Agent is a person exercising contractual powers on behalf of someone else.

�The organisation employing the Agent is called the Principal.

�Once the Principal has employed an Agent, it will be bound by the acts of that Agent.

�Under JCT2011, the Architect, Engineers, Clerk of Works, and Quantity Surveyor are the Employer’s agents.

173

The Architect (CA)

� The rights and responsibilities of the Architect are definedby: the law;

� the terms of appointment (e.g. the RIBA StandardAgreement for the Appointment of an Architect);and

� the JCT2011 SBC/Q Contract Conditions.

174

The Architect (CA) (Cont’d)

�May not profit from his appointment other than his fee.

�May not delegate his responsibilities except as defined by the Contract.

�Under JCT2011 SBC/Q the Architect’s rights to delegate are narrow and accurately defined.

�Must act in his Principal’s interest.

�Owes a duty of care to his Principal (i.e. the Employer).

�Owes a duty of care to the Contractor.If the Contractor suffers loss due to false or negligent information from the Architect, then damages due.

175

The Clerk of Works

�The Employer is entitled to appoint a Clerk of Works to act as an inspector on site on his behalf (cl. 3.4)

�The Clerk of Works inspects the quality of materials and workmanship and may issue directions to the Contractor.

�The Clerk of Works can only direct the Contractor on matters that the CA can (later) instruct (cl. 3.4)

�A Clerk of Works direction has no effect until confirmed by the CA within 2 days of the direction being given (cl. 3.4)

�The CA’s confirmation is considered to be an Instruction

176

The Quantity Surveyor�Prepares interim valuations (cl. 4.11) and evaluates the Contractor’s

applications for payment, if submitted - they usually are (cl. 4.12)

�Calculates the amount of Retention on each interim valuation (cl.4.18.2)

�Ascertains the amount of the Contractor’s Loss and Expense, ifinstructed to by the CA following the Contractor’s submission of aclaim (cl. 4.23.3)

�Values Variations and provisional sum work (cl. 5.2) and re-measurework for interim valuations, if required (cl. 5.4)

�Agrees payment for Fluctuations with the Contractor (Schedule 7para. A.5, B.6, or C.4)

�Prepares each interim’s Gross Valuation in accordance with TheValuation Rules (cl. 5.6) – QS ascertain then CA issue an InterimCertificate.The QS will always prefer to value using cl. 5.6 rather than cl. 5.7(Daywork Rates). 177

Requirements of a certificate

�Certificates document achievement or occurrence of key events in a project

�Certificates must:� leave no doubt as to their content and consequences

� be issued when required by the Contract

� be issued in accordance with the procedure defined by the Contract

� be issued by the correct party

� be issued to the correct party

�The CA must give the Contractor a copy of all Certificates sent to the Employer (cl. 1.8).

178

CONTRACT ADMINISTRATION

(PART 2 OF 3)(Refer to JCT2011/ SBC/Q for this Module)

179

Learning Outcome

�Purpose of clauses and parts of JCT2011 SBC/Q

180

Payment under SBC

from the Construction Act regarding�Corporates several obligations payment practice, including:

� The Employer has 14 days from the issue of an Interim Certificate to pay the certified amount to the Contractor (cl. 4.13.1)

� If it does not, then:

� The Contractor can charge interest on the outstanding amount at 5%above the base rate (cl. 4.13.6; cl. 1.1);

� The Contractor can suspend the Works (cl. 4.14); and

� The Contractor can terminate its own employment if payment stilloutstanding a further 14 days past the due date (i.e. 28 days aftercertificate issue (cl. 8.9.1.1)

181

Interim payments

�Interim valuations are performed at agreed regular intervals bythe QS to ascertain the current value of the Works

�This is the Gross Valuation

�In principle, the difference between one Gross Valuation and theimmediately preceding Gross Valuation is the amount to be paidby the Employer for that period’s work

�This amount is subject to Retention (and other Employer “set-offs” as permitted by SBC/Q)

182

Retention

�Retention is governed by cls. 4.10, 4.18 and 4.20.

�An agreed Retention Percentage is withheld by the Employerfrom each payment due following a Gross Valuation.

�Retention is deducted at the full Retention Percentage stated inthe Contract Particulars from Works not yet covered by aPractical Completion Certificate (cl. 4.20.2.1)

�Retention is also deducted at the full Retention Percentage frommaterials on site and Listed Items (cl. 4.20.2.2)

�Retention is deducted at half the Retention Percentage stated inthe Contract Particulars from Works that are covered by aPractical Completion Certificate but are not yet covered by aCertificate of Making Good - i.e. during the Rectification Period(cl. 4.20.3) 183

Terminology� Interim - Something that happens several times at regular intervals - SBC/Q

defaults to valuations at monthly intervals.

� Gross Valuations (cl. 4.16) The QS’s ascertainment of the total value of the partiallycompleted Works on the date of each interim valuation.

� Interim valuations (cl. 4.11) The QS’s monthly activity of ascertaining the amountdue in an Interim Certificate. This requires a Gross Valuation.

� Interim Certificates (cls. 4.9, 4.10, 4.13) The regular certificates denoting the interimpayments that must be paid by the Employer to the Contractor.

� Retention (cls. 4.10, 4.18, 4.20) A proportion of the sums otherwise due toContractor withheld by the Employer until the end of the project to ensure theContractor to complete the Works.

� Retention Bond (cl. 4.19) As alternative of the Employer deducting Retention, theContractor can obtain a Retention Bond which will pay out to the Employer if theContractor defaults on its obligations. 184

Payment generally

Contract parties are free to agree:

�The sum to be paid for the Works.

�Whether payment is to be in instalments.

�When instalments are due and how they are to be paid.

185

Paid when paid” clauses

Grants, Construction and�Payment under The Housing Regeneration 1996 Act:

�Sections 109 and 110 establish the Contractor’s statutory right to periodic payment.

�Section 110(1) requires that a mechanism for ascertaining payments is provided by construction contracts.

�Section 113 prohibits “paid when paid” clausesThese were typically used by the Contractor with its subcontractors and were considered unfair.

186

Content of a Gross Valuation

When ascertaining each Gross Valuation, the QS will include:

�those parts of the Works “properly executed” on the date ofvaluation (cl. 4.16.1.1)

�materials or goods stored on site and clearly identifiable as beingdestined for inclusion in the Works (cl. 4.16.1.2)

�materials or goods stored off site but identified in the ContractDocuments as “Listed Items” and therefore clearly identified asbeing destined for inclusion in the Works, (cl. 4.16.1.2)

187

Interim Certificates: procedure

�The Contractor can (and usually does) make an application for payment under cl. 4.12 in advance of the interim valuation.

�The Contractor’s application will typically include:

�Works completed to date, charged at “bill rates.”

�Works completed in response to CA Instructions requiring variations, charged in accordance with the Valuation Rules (cls. 5.6 to 5.10).

�Wherever possible, variations should be measured and suitable bill rates applied (cl. 5.6 - “Measurable Work”).

�If a variation “cannot properly be valued by measurement,” Daywork may be used (cl. 5.7 - “Daywork”).

�All Dayworks sheets must be signed by the Clerk of Works.

188

Interim Certificates: procedure (Cont’d)

�The QS conducts an interim valuation as required by the CA toascertain the “Gross Valuation” so that an amount payable by theEmployer can be stated as due in an Interim Certificate (cl. 4.10).

�The QS will attend the site to:

�Confirm and value the work completed (cl. 4.16.1.1)

�Confirm and value any materials or goods stored on site and due to be incorporated in the Works (cl. 4.16.1.2)

�Confirm presence of any Listed Items (this may require a visit to the Contractor’s or supplier’s storage facility) (cl. 4.16.1.3)

189

Interim Certificates

Each Gross Valuation must “adjust” the Contract Sum to incorporateadditions or deductions caused by Variations, additions and deductions(cl. 4.16): here are some deductions…

�Liquidated Damages (if Non-Completion Certificate issued) (cl. 2.32.2.2)

�Errors in setting out that do not have to be amended (cl. 2.10)

�Cost of employing an alternative contractor to rectify defects the Contractor is refusing to fix (cl. 2.38)

�Cost of employing an alternative contractor to implement instructions the Contractor is refusing to do (cl. 3.11)

�Value of Works not in accordance with the Contract which does not require to be replaced (cl. 3.18.2)

�The updated Contract Sum is the Gross Valuation (cl. 4.16).

190

Instructions vs. Variations

Instructions�Instructions address how the Works are being completed

(Instructions are issued to change the way in which Contractor are working or correct parts of the Works that have been assembled incorrectly)

�Instructions are usually issued when the CA or Clerk of Worksobserves the Contractor to be acting contrary to the ContractDocuments (e.g. work “not in accordance”)The Contractor will not be paid to comply with an instruction

�The instruction was required because the Contractor was notdoing what it should have been doing.

�The Contractor would be paid for complying with an instruction ifthe instruction was issued in error

191

Variations

�Variations change the definition of the Works themselves. CA canonly issue instructions in accordance with their right to do sounder SBC/Q cls. 3.14 to 3.22.

� Two types of Variations:

� Variations that change the content of the Contract Documents (cl. 5.1.1)

� Variations that oblige the Contractor to use certain working methods (e.g. working at night) (cl. 5.1.2)

192

CA’s instructions�Traditionally called “Architect’s instructions” (or “A.I.s”)

Contract “Contract

�Now that any suitable organisation can adopt the Administrator role, instructions are also called Administrator’s instructions”

�The purpose of an instruction is to direct the Contractor’s work.An instruction may:

�require site practice to be changed

�require the Contractor to correct its mistakes

�vary the definition of the Works - i.e. issue a “Variation” (‘Variation’ is an alteration of the Contract Document)

193

CA’s powers to instruct

�The CA can only issue instructions where allowed by SBC/Q

�All instructions must be in writing (cl. 3.12.1)

�Verbal instructions must be confirmed in writing within 7 days, or

�Contractor’s written acceptance of a verbal instruction becomesa CA’s instruction if a CA’s instruction is not issued within 7 daysof the Contractor’s acceptance

194

CA’s powers to instruct (Cont’d)

�A Variation is required cl. 3.14

�The Works are to be postponed cl. 3.15

�A Provisional Sum is to be spent cl. 3.16

�Inspection of the Works is required cl. 3.17

�Work not in accordance must be corrected cl. 3.18

�Workmanship not in accordance must be corrected cl. 3.19

�The work is otherwise not satisfactory cl. 3.20

�A person is to be excluded from the site cl. 3.21

�Antiquities have been discovered cl. 3.22

195

Contractor’s right to query instructions

�The Contractor has the right to “reasonably object” to an instruction if:

�the Contractor believes the CA cannot issue it, or has done so in error

�it would change the working conditions as given in clause cl. 5.1.2under which the Works are to be completed (cl. 3.10.1)

�The Contractor can ask the CA to prove that it has the right to issue the instruction (cl. 3.13)

�The CA must notify Contractor of the SBC/Q provision that empowers the instruction “forthwith”

196

Adjusting the Contract Sum

The Contract Sum can be increased or decreased if:

� a Variation has been issued (cl. 4.3.1.1)

� an Acceleration Quotation or a Variation Quotation hasbeen submitted by the Contractor and accepted by theEmployer (cl. 4.3.1.2)

� a change in premiums the Contractor must pay for any “allrisk” insurance of the Works they were obliged to take out(cl. 4.3.1.3).

197

Valuing variations (Measurable Work)5.6.1 To the extent that a Valuation relates to the execution ofadditional or substituted work which can properly be valued bymeasurement or to the execution of work for which an ApproximateQuantity is included in the Contract Bills and subject to clause 5.8 inthe case of CDP Works, such work shall be measured and shall be

valued in accordance with the following rules:1.where the additional or substituted work is of similar character to, is executed undersimilar conditions as, and does not significantly change the quantity of, work set out inthe Contract Bills, the rates and prices for the work so set out shall determine the valuation;

5.6.12.where the additional or substituted work is of similar character to work set out in theContract Bills but is not executed under similar conditions thereto and/or significantlychanges its quantity, the rates and prices for the work so set out shall be the basis fordetermining the valuation and the Valuation shall include a fair allowance for suchdifference in conditions and/or quantity;

3.where the additional or substituted work is not of similar character to work set out inthe Contract Bills, the work shall be valued at fair rates and prices;4.where the Approximate Quantity is a reasonably accurate forecast of the quantity ofwork required the rate or price for the Approximate Quantity shall determine the valuation;and

198

Valuing variations (Measurable Work) (Cont’d)5.6.1.5 where the Approximate Quantity is not a reasonably accurate forecast of the quantityof work required, the rate or price for that Approximate Quantity shall be the basis fordetermining the valuation and the Valuation shall include a fair allowance for suchdifference in quantity. Provided that clauses 5.6.1.4 and 5.6.1.5 shall apply only to theextent that the work has not been altered or modified other than in quantity.

2.To the extent that a Valuation relates to the omission of work setout in the Contract Bills and subject to clause 5.8 in the case ofCDP Works, the rates and prices for such work therein set out shalldetermine the valuation of the work omitted.

3. In any valuation of work under clauses 5.6.1 and 5.6.2:1.measurement shall be in accordance with the same principles as those governing thepreparation of the Contract Bills, as referred to in clause 2.13;2.allowance shall be made for any percentage or lump sum adjustments in the ContractBills; and3.allowance, where appropriate, shall be made for any addition to or reduction ofpreliminary items of the type referred to in the Standard Method of Measurement,provided that no such allowance shall be made in respect of compliance with anArchitect/Contract Administrator’s instruction for the expenditure of a Provisional Sum fordefined work.

199

Key events in project progression

�Date for Possession contract period starts

� Date for Completion [of the Works] / Completion Date contractperiod ends - these dates may, or may not, be the same

Note: If the CA judges the Works to be incomplete on the Completion Date (which may, or may not, bethe Date for Completion in the Contract Particulars), it issues a Non-completion Certificate (Clause 2.31).Issue of a Non-completion Certificate obliges the Contractor to pay Liquidated Damages to the Employerat the rate in the Contract Particulars

�Practical Completion the Works are practically completed - halfthe Retention is released (Practical Completion Cert, c.l. 2.30)

�Making Good Defects the Works and all snagging are fullycompleted - the remaining Retention is released (Certificate ofMaking Good, c.l. 2.39)

�Final Certificate the final account is settled (c.l. 4.15)

200

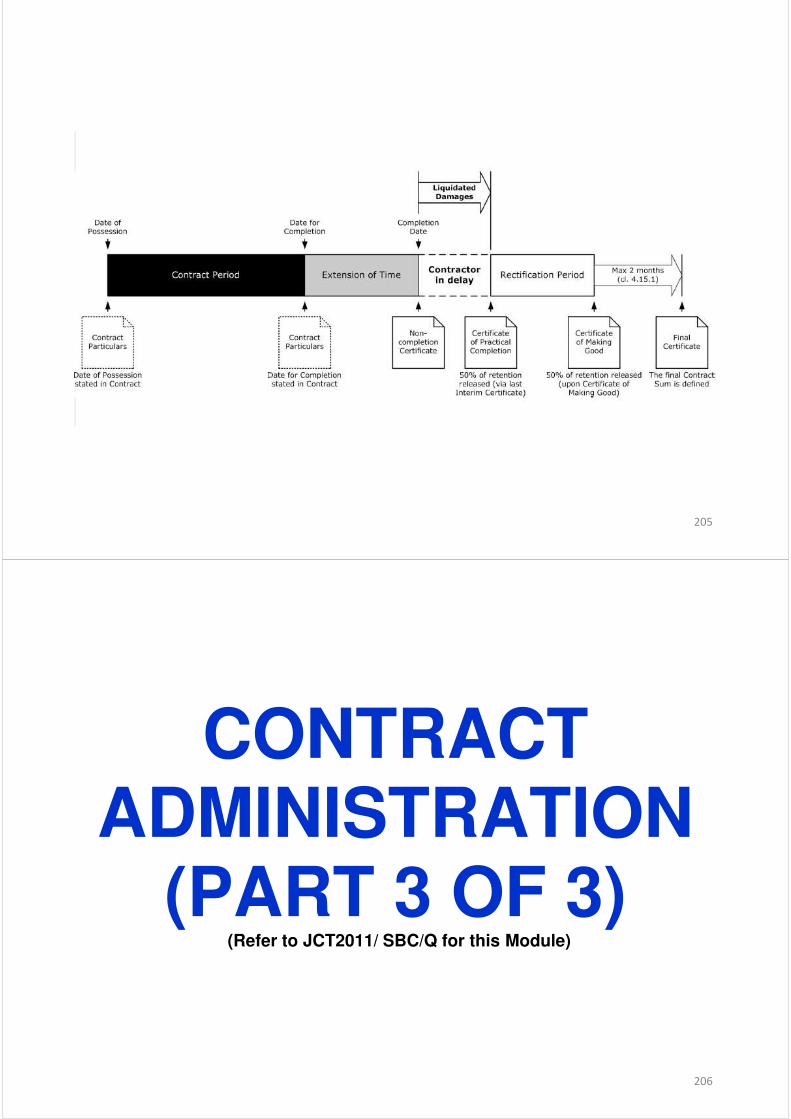

The Rectification Period

�The Final Certificate is the final outcome of the Contract, issued after Rectification Period has ended.

�The Rectification Period commences after issue of the Practical Completion Certificate (cl. 2.34).

which the�The Rectification Period is a period of time in Contractor must make good all defects (cl. 2.38).

�Default duration is 6 months (Contract Particulars).

201

Events prior to Final Certificate

�Interim Certificates will have been issued at regular intervals to directthe Employer's payments (cl. 4.9.1)

�The Practical Completion Certificate has been issued (cl.2.30)

�Further Interim Certificates have been issued every two monthsduring the Rectification Period to permit further adjustment of theContract Sum and any payments from Employer to Contractor (cl.4.9.2)

�Damages for Loss and Expense have been agreed in accordancewith clause 4.5.2 (because the Contract Sum has to be adjusted)

�The Certificate of Making Good has been issued (cl. 2.39)

202

The Final Certificate (cls. 1.10 & 4.15)

�Signifies the CA’s satisfaction with the Works.

�Issued within two months (cl. 4.15.1) after either:

�the end of the Rectification Period (cl. 4.15.1.1)

�the issue of the Certificate of Making Good (cl. 4.15.1.2); or

�settlement of the “final account” in accordance with cl. 4.5 (cl. 4.15.1.3)

�States the finally adjusted Contract Sum (4.15.2.1)

�States the sum previously certified (and paid) plus the amount of any advance payment paid pursuant to cl. 4.8 (4.15.2.2)

�States the final balance due

203

Legal standing of the Final Certificate

It providescl. 1.9 defines the effect of the Final Certificate.conclusive evidence that:

� the Works have been completed in accordance with the Contract Documents and all Instructions (cl. 1.9.1.1);

� all required adjustments of the Contract Sum have been taken into account (cl. 1.9.1.2);

� all extensions of time due under cl. 2.28 have been granted (cl. 1.9.1.3);

� all loss and expense due to the Contractor has been paid (cl. 1.9.1.4).

204

205

CONTRACT ADMINISTRATION

(PART 3 OF 3)(Refer to JCT2011/ SBC/Q for this Module)

206

Learning Outcome

�Purpose of clauses and parts of JCT2011 SBC/Q

207

Time generally

�When a contract is formed requiring the Contractor to do something that takes time to complete:

�Time is “at large” if the Employer doesn’t care how long the Contractor will take

�The Contract does not define the time available for the Works�The Works must be completed in a “reasonable” time

�Time is “of the essence” if the Employer must have the Works completed by a specified date

�The Contract will specify a date by which the Work must be completed

208

Delays – in essence

�In contract law, the “prevention principle” states:

�A party cannot benefit from its own breach of contract to thedetriment of the injured party.

�e.g. The Employer cannot oblige the Contractor to keep a Completion Date if the Employer’s actions (or inactions) have caused the delay.

�In this situation, time becomes “at large”

�The Contractor’s express obligation to complete the Works by theCompletion Date is replaced with an implied obligation to completethem within a “reasonable” time.

209

Delays – in essence (Cont’d)

�Delays caused by the Contractor (The Contractor bears its own costs and the Employer’s)

�Delays caused by the Employer (The Employer bears its own costs and the Contractor’s)

�Delays caused events that neither the Employer or Contractor cancontrol (These are known as “shared risk events” or “neutral events”,neither party is liable - so both bear their own costs

210

Extension of time: principles