PRICING ORIENTATION IN INDUSTRIAL MARKETS: …lp-website.s3.amazonaws.com/pdfs/Pricing Orientation...

63

PRICING ORIENTATION IN INDUSTRIAL MARKETS: THE ORGANIZATIONAL TRANSFORMATION TO VALUE-BASED PRICING By Stephan M. Liozu Submitted in Partial Fulfillment of the Requirements for the Qualitative Research Report in the Doctor of Management Program at the Weatherhead School of Management Advisors: Richard Boland, Ph.D., Case Western Reserve University Andreas Hinterhuber, Ph.D., Bocconi University, Milano, Italy Sheri Perelli, D.M., Case Western Reserve University Tim Timura, D.M., Case Western Reserve University CASE WESTERN RESERVE UNIVERSITY December 2010 Do not Cite or Distribute Without Permission From the Author Comments Welcome

Transcript of PRICING ORIENTATION IN INDUSTRIAL MARKETS: …lp-website.s3.amazonaws.com/pdfs/Pricing Orientation...

PRICING ORIENTATION IN INDUSTRIAL MARKETS: THE ORGANIZATIONAL TRANSFORMATION TO VALUE-BASED PRICING

By

Stephan M. Liozu

Submitted in Partial Fulfillment of the Requirements for the Qualitative Research Report in the Doctor of Management Program

at the Weatherhead School of Management

Advisors: Richard Boland, Ph.D., Case Western Reserve University

Andreas Hinterhuber, Ph.D., Bocconi University, Milano, Italy Sheri Perelli, D.M., Case Western Reserve University Tim Timura, D.M., Case Western Reserve University

CASE WESTERN RESERVE UNIVERSITY

December 2010

Do not Cite or Distribute Without Permission From the Author Comments Welcome

PRICING ORIENTATION IN INDUSTRIAL MARKETS: THE ORGANIZATIONAL TRANSFORMATION TO VALUE-BASED PRICING

ABSTRACT

Of three main orientations to pricing in industrial markets −cost-based, competition-

based and customer value-based − most marketing and pricing scholars consider the latter superior – but few firms use it. The literature is silent about how organizational and behavioral characteristics of industrial firms may affect pricing orientation and, more specifically, value-based pricing. Semi-structured interviews with 44 managers of small to medium size U.S. industrial firms yielded insights into firm pricing orientations, processes and decision making patterns. We identified five organizational characteristics common to firms implementing value-based pricing: ability to effect deep transformational change, presence of a champion, skill in diffusing organizational capabilities, organizational confidence, and center-led pricing process specialization.

Our data demonstrates that value-based pricing is not simply adopted but internalized through a long, tenuous and deep transformation process supported by an experiential and transformative learning environment. Key Words: Industrial pricing; pricing orientation; pricing process; value-based pricing; organizational structure; decision making theory; organizational change; transformative learning.

TABLE OF CONTENTS Abstract ..................................................................................................................................... 2 Introduction ............................................................................................................................... 4 Theoretical Foundation ............................................................................................................. 5 Methods................................................................................................................................... 13 Findings................................................................................................................................... 17 Discussion ............................................................................................................................... 30 Limitations .............................................................................................................................. 42 Implications for Practice and Future Research ....................................................................... 42 Appendices

Appendix A: Detailed Sample Information ............................................................... 44 Appendix B: Interview Protocol and Questions ........................................................ 46 Appendix C: Themes and Sub-Themes ..................................................................... 49 Appendix D: Stimulus for Change and Duration of Transformation for Firm

Which Adopted Value-Based Pricing ................................................. 52 Appendix E: Raw Understanding of Value-Based Pricing in Firms ......................... 53

References ............................................................................................................................... 57 List of Figures

Figure 1: Price Point Definition Process for Value-Based Pricing (VBP) ................ 18 Figure 2: Differences in the Decision Making Process between Firms Using Value-

Based Pricing and Those That Did Not ...................................................... 19 Figure 3: Price Point Definition Process for Cost-Based Pricing (CBP) ................... 19 Figure 4: Price Point Definition Process for Competition-Based Pricing (COBP) .. 20 Figure 5: Evidence of Decision Making Factors in Firms Using Cost-Based or

Competition-Based Pricing Orientation ..................................................... 21 Figure 6: Evidence of Role Specialization in Firms That Use Value-Based Pricing 23 Figure 7: Evidence of Expertise Centralization in Firms That Use Value-Based

Pricing ........................................................................................................ 24 Figure 8: Pricing Process Formalization by Pricing Orientation ............................... 25 Figure 9: Differences in the Training Focus among Firms with Different Pricing

Orientations ................................................................................................ 26 Figure 10: Evidence of Leader’s Decisive Influence ................................................. 28 Figure 11: Importance of Employee's Beliefs on Confidence ................................... 29 Figure 12: Importance of Courage and Pricing Heroes on Confidence ..................... 30 Figure 13: Importance of Success Stories on Confidence ......................................... 30 Figure 14: Evidence of Cost-Plus Mentality in Firm’s Culture or DNA ................... 32 Figure 15: Evidence of Firm’s DNA Transformation to Value-based Pricing .......... 32 Figure 16: Understanding of Value-based Pricing by Executive Leaders in Firms

Using it ..................................................................................................... 39 Figure 17: Conceptual Model for the Internalization of and Transformation Towards

VBP .......................................................................................................... 41 List of Tables

Table 1: Identified Value-Based Pricing Methodologies in Business Publications .. 40

4

INTRODUCTION Of three main approaches to pricing in industrial markets ─ cost-based, competition-

based and value-based ─ the latter is considered superior by most marketing scholars

(Anderson & Narus, 1998; Cressman, Jr., 1999; Nagle & Holden, 2002; Ingenbleek,

Debruyne, Frambach, & Verhallen, 2003; Hinterhuber, 2004) and pricing practitioners,

(Forbis & Mehta, 1981; Dolan & Simon, 1996; Nagle & Holden, 2002; Fox & Gregory,

2004). Paradoxically, few industrial firms have adopted it. A meta-analysis of pricing

approach surveys between 1983 and 2006 reveals an average adoption rate of 17%

(Hinterhuber, 2008). Cost-based and competition-based approaches still play a dominant role

in industrial pricing practice (Coe, 1990; Shipley & Bourdon, 1990).

Historically, pricing has received little attention from practitioners and marketing

scholars (Malhotra, 1996; Noble & Gruca, 1999; Hinterhuber, 2004, 2008). A review of 53

empirical pricing studies conducted by Ingenbleek (2007) concluded that pricing literature is

highly descriptive and fragmented and that theoretical development on how price decisions

are made in firms is limited.

The marketing and pricing literature is silent about both the consequences of pricing

orientations on overall company performance (Cressman Jr., 1999; Ingenbleek, 2007;

Hinterhuber, 2008) and how organizational and behavioral characteristics of industrial firms

may affect pricing orientation (Ingenbleek, 2007). Specifically, the potential influence of

organizational factors on the successful and systemic adoption of value-based pricing

orientation in industrial firms has not been empirically and holistically investigated.

To address this phenomenological gap, we designed a qualitative inquiry based on

semi-structured interviews with managers in small and medium U.S. industrial firms that

5

have successfully adopted value-based pricing as a pricing orientation and with managers in

similar firms that have not. By probing the "lived worlds" of these executives, our hope was

to generate a grounded theory about the organizational practices that contribute to or hinder

the development and implementation of value-based pricing strategies in industrial markets.

Our results reflect similarities and differences in the experiences of managers in

industrial firms using all three pricing orientations. They contrast firms and leaders with

respect to how they organize for pricing, manage the pricing process, manage the transition

to more advanced pricing orientations and develop internal capabilities to face uncertain and

ambiguous decisions.

THEORETICAL FOUNDATION

Our work was informed by two key management theories: organizational theory and

the theory of the firm – as well as by pricing literature focused on firm pricing orientation.

Among the vast array of derivative theories and multiple schools of thought that surround

organizational theory and theory of the firm, we focused, relative to the first, on

organizational decision making theory (March & Simon, 1958; March, 1994).and, with

regard to the latter, on the behavioral theory of the firm (Cyert & March, 1992) and the

resource-based view of the firm (Wernerfelt, 1984).

Pricing Orientation

Marketing and management literature is rich in studies related to market orientation

and strategic firm orientation. Both streams of literature have taken a central role in

discussions about marketing management and firm strategy (Day, 1994). Studies on market

orientation have focused on defining its nature, antecedents and its consequences on firm

performance (Narver & Slater, 1990; Jaworski & Kohli, 1993; Slater & Narver, 1994; Kirca,

6

Jayachandran, & Bearden, 2005). Jaworski and Kohli (1993) define market orientation as “an

organization-wide generation of, dissemination of and responsiveness to market intelligence”

while Narver and Slater (1990) describe its three components as customer orientation,

competition orientation and interfunctional coordination. Strategic orientation of the firm is

close to that of market orientation and is defined as the strategic direction implemented by a

firm to “create the proper behavior for the continuous superior performance of the business”

(Narver & Slater, 1990). Technological orientation is added as a fourth component of firm

orientation (Gatignon & Xuereb, 1997). The prolific literature on market and firm orientation

strongly influenced the advancement of the modern marketing concept by providing firms

with behavioral and organizational perspectives on how to achieve sustainable performance.

Consistent with the lack of interest by marketing scholars in researching the pricing

field (Malhotra, 1996; Noble & Gruca, 1999; Hinterhuber, 2008), the notion of pricing

orientation in firms has not been appropriately defined and explored. Only a handful of

academic papers have discussed pricing orientation in business markets. In 2008,

Hinterhuber made a strong contribution to the topic by conducting a broad and

comprehensive review of two dozen surveys conducted between 1983 and 2006. The meta-

analysis revealed the adoption rates of alternative pricing approaches (cost-based,

competition-based and value-based) in business markets and concluded that the competition-

based approach still dominated in the industrial pricing.

Managerial pricing orientation “deals with decisions relating to setting or changing

prices. It also includes price positioning and product decisions introducing new pricing points

to the business unit’s product or service mix” (Smith, 1995). Smith defined it as consisting of

four dimensions (information getting and processing, pricing objectives, policies and beliefs,

7

organizational decision processing, and organizational responsiveness) and proposed four

distinct managerial pricing orientations - cost, sales, competition and strategy. We, however,

adopt the widely accepted three dimensions of cost, competition, and customer value

(Hinterhuber, 2008). Furthermore we consider pricing orientation from a firm’s strategic

perspective and define it as all pricing practices, methods, behaviors and processes leading to

pricing decisions with the goal of maintaining and sustaining firm competitive advantage.

Organizational Theory and Organizational Decision Making Theory

Organizational theory focuses on the internal structure of the firm and the

relationships between its units and departments (Grant, 1996). Organizations are “systems of

coordinated actions among individuals and groups whose preferences, information, interests,

knowledge differ” (March & Simon, 1958: 2). The first of two key streams in traditional

organization theory (March & Simon, 1958: 31) focuses on the basic physical activities

involved in production while the second is concerned with the problems of departmental

work and coordination. Both streams address the limitations of not exploring knowledge

about the motivational, conflict of interest, cognitive and computational constraints (March,

1978) that human beings place on organizations. Decision making theory addresses the flow

of information within organizations supporting and influencing decision making processes.

Taking into account these constraints, we have embraced organizational theory from a

decision making perspective drawing from the work of March (1994; 1999) and Simon

(1961). The critical question is how pricing decisions occur in organizations and what

organizational factors strongly influence managerial judgment when making these decisions.

Previous work by leading behavioral and social researchers covered many important aspects

of organizational theory. Below, we focus on the most relevant ones including bounded

8

rationality (March & Simon, 1958; Simon, 1961; Cyert & March, 1992), uncertainty and

ambiguity in decision making (Daft & Weick, 1984; Spender, 1989; Brownlie & Spender,

1995; March, 1999) and organizational structure (Hall, Johnson, & Haas, 1967; Hall, 1977;

Aiken, Bacharach, & French, 1980; Miller, Droge, & Toulouse, 1988).

Rationality. Simon (1961: 93) posits that actual behavior of managers in firms when

making decisions or making choices falls short of objective rationality in three ways: 1) the

incompleteness of knowledge; 2) the difficulties in anticipation of the consequences that will

follow choice; and 3) the choice among all possible alternative behaviors. Managers also

suffer from possible “bottleneck of attention” that impacts their ability to deal with more than

a few things at a time (Simon, 1961: 90). Bounded rationality refers to the notion that rational

actors are significantly constrained by limitations of information and calculations (Cyert &

March, 1992: 214). These constraints create an environment of uncertainty and ambiguity

that managers in firms have to deal with on a daily basis. For example, the degree of

complexity, analyzability (Daft & Weick, 1984) and dynamics of the environment affect the

level of uncertainty and ambiguity in the decision-making process (Duncan, 1972). As the

environment becomes more and more complex, managers shift their assessments from

objective parameters to intuitive and subjective ones (Daft & Weick, 1984). The type of

uncertainty that pricing decision-makers face is mostly a function of data and information

incompleteness as well as the incommensurability of information in the areas of customer

value and competition (Spender, 1989: 188; Brownlie & Spender, 1995; Anderson, Kumar,

& Narus, 2007: 23).

According to behavioral theorists, managers in organizations simplify the decision-

making process by using various behaviors (Cyert & March, 1992: 264): satisficing (March,

9

1978); following rules of thumb (Schwenk, 1988); and defining standard operating

procedures and organizational routines (Pentland & Reuter, 1994; Feldman, 2000). Others

will define frames of reference (March & Simon, 1958: 159) which will be determined “by

the limitations of the rational man’s knowledge”. Experienced managers will draw from their

memory, training and experience (Simon, 1961: 134). They construct and use “cognitive

heuristics” (Brownlie & Spender, 1995) or mental models (Porac, Thomas, & Baden-Fuller,

1989) to simplify complex strategic issues and engage in intuitive and judgmental responses

to decision-demanding situations (Barnard & Andrews, 1968). The resolution of uncertainty

is “to create a rationality, a recipe or an interpretative scheme” (Brownlie & Spender, 1995)

leading to a choice or a decision.

Organizational structure. Organization structure can be defined in many ways and

can take many forms in organizations. Several reviews (Hall, 1977; John & Martin, 1984;

Miller et al., 1988) have suggested that formalization, centralization and complexity are the

most common and consistent characteristics of structure. Organizational structure relates to

dimensions of organization that “cannot be reduced to or deduced from properties of the

organization’s members” (Aiken et al., 1980). We select as the level of analysis the

organizational activities and programs associated with the pricing function. We consider

structural differentiation, formalization and centralization as the critical characteristics of

organization structure.

Lawrence and Lorsh (1967) note that structural differentiation “includes differences

in attitudes and behaviors on the part of the members of the differentiated departments”. It is

defined as the differences in occupational specialties present in the organization and their

degrees of professionalism (Hage & Aiken, 1967; Hage & Aiken, 1970). The specialization

10

of pricing experts in the organization is needed in order to perform specialized tasks

supporting a broad array of pricing-related activities in marketing, sales, R&D and

management.

The degree to which a firm is formalized is an indication of the perceived capabilities

of its members in exercising judgment and self control (Hall, 1977: 95). Formalization

involves control to make sure members follow defined and standardized rules, roles and

procedures (Hage & Aiken, 1967; Hall et al., 1967; Hall, 1977) as well as instructions and

communications (Pugh et al., 1963). We define formalization as the emphasis placed on

following defined or standardized rules, roles and procedures in conducting firm pricing

activities, making pricing decisions and implementing pricing process in a formalized way.

The notion of control and routinization associated with process formalization has a negative

connotation. However, we take the opposite position by stating that well documented,

structured and communicated sets of rules, procedures and instructions for the activities

connected to pricing might increase the level of organization commitment and confidence in

executing pricing activities as well as providing a strong message about top leadership

commitment to the pricing process. Top management should avoid over- or under-

specification of the formalized process that could lead to negative organizational

consequences (Hall, 1977: 112).

Centralization, which reflects the hierarchical nature of the organization, is one of its

most critical structural dimensions (John & Martin, 1984). Van de Ven and Ferry (1980)

define centralization as the “locus of decision making authority within an organization.”

However, for complex decision making that requires professional competencies, decisions

are often left to experts.” The notion of expertise therefore takes a central part in our

11

definition of centralization. Locus of authority in pricing decisions is highly dependent on

locus of pricing expertise. We define pricing centralization or center-led pricing management

(Deaker & Zang, 2006) as the extent to which expertise and specialized skills related to

pricing decisions are concentrated within a few positions. Because these central positions are

non routine and highly specialized, they are likely to gain power and influence (Pfeffer,

1978) because of their expertise while not, however, having pricing decision making

authority. Center-led pricing teams might be considered as a central unit of pricing

excellence or internal consultants. Here too, how centralization is perceived greatly depends

on top leadership’s definition and its communication with the rest of the organization. The

consequences of a high degree of centralization can be positive or negative for the

organization (Hall, 1977: 125) depending on the complexity of pricing decisions and the

adopted pricing orientation. Additionally because the adoption and implementation of pricing

orientation is transformational in nature with several stages (Hall, 1977: 215), a more

centralized approach might be more appropriate for the implementation stage to ensure

organizational buy-in.

Organization structure and its defining characteristics have a strong relationship to

decision making theory and the notion of rationality. The complexity of conditions under

which decisions are made, the locus of decision making authority and the design of

organizational life all create difficulties in predicting outcomes and affect how decisions are

made (Hall, 1977). Miller (1987) and Fredrickson (1986) posit that rationality in decision

making may have a strong relationship with three aspects of formalization: controls,

specialization, and policies and procedures. Rationality may be associated with centralization

of authority (Fredrickson, 1986) or to structural integration devices such as task forces and

12

committees (Miller, 1987). Accordingly, we conjecture that rationality and organizational

structure are central to pricing orientation and to how pricing decisions are made in

organizations.

Theory of the Firm: Behavioral Theory and Resource-Based View

Theories of the firm are “conceptualizations and models of business enterprises which

explain and predict their structure and behaviors” (Grant, 1996). There is no single multi-

purpose theory of the firm. Interest by social and behavioral scientists in the firm as an

institution has been stimulated by the question of why firms exist at all. Among the four most

influential theories of the firm (Slater, 1997), behavioral theory of the firm and the resource-

based view of the firm contribute to the development of our theoretical foundation.

Cyert and March (1992), building on the work of Barnard and Andrews (1968),

March and Simon (1958) and Simon (1961) developed their behavioral theory of the firm to

challenge the assumptions of rationality in the neoclassical theory of the firm that consists of

the firm’s access to perfect information and the firm operating to maximize profits. That

theory addresses the process of decision making in modern firms from the perspective of

organizational expectations; organizational goals; and organizational choice (Cyert & March,

1992: 162). Behavioral theory of the firm’s concerns with task specialization, role and

responsibilities, avoidance of uncertainty, problemistic search and satisficing behaviors have

been integrated in our theoretical approach.

While providing useful insights about decision making in organizations, the

behavioral theory of the firm, however, does not explain performance differences among

firms. The resource-based view of the firm (Wernerfelt, 1984), which seeks to explain and

predict why some firms are able to establish positions of sustainable competitive advantage

13

leading to superior returns or economic rent, perceives the firm as a “unique bundle of

resources and capabilities where the primary task of management is to maximize value”

(Grant, 1996). These resources include “all assets (physical and non physical), capabilities,

organizational processes, firm attributes, information, knowledge etc. controlled by the firm

that enable a firm to conceive and implement strategies that improve its efficiency and

effectiveness” (Bamey, 1991: 101). A specific combination of these tangible and intangibles

resources and capabilities is valuable, rare and difficult to imitate or acquire by competitors

(Dierickx & Cool, 1989; Hall, 1993; Barney & Clark, 2007) and cannot be captured on a

piece of paper (Nadler & Tushman, 1990: 18). These unique capabilities are “a function of

traditions, shared values, informal patterns of interaction and careful attention to recruiting

and promoting the right kind of people” (Nadler & Tushman, 1990). Firms derive their

competitive strengths from their “small number of capabilities clusters” (Dosi, Nelson, &

Winter, 2000). Because organizations face more and more complexity, they need to

constantly “re-evaluate and re-package” the required set of capabilities (Cohen & Levinthal,

1990) making them dynamic in nature (Teece, Pisano, & Shuen, 1997). The development of

unique strategic pricing capabilities and the deployment of strategic resources to grow these

capabilities can lead to superior pricing decisions, greater organizational capital and greater

competitive advantage in the marketplace (Dutta, Bergen, Levy, Ritson, & Zbaracki, 2002;

Dutta, Zbaracki, & Bergen, 2003).

METHODS

Methodological Approach

We conducted a qualitative study using semi-structured interviews to develop a

grounded theory (Corbin & Strauss, 2008) about how organizational factors affect the

14

adoption of a pricing approach in industrial firms. We aimed to get a better understanding of

how managers in these firms make pricing decisions and what roles they play in the firm’s

pricing process. Grounded theory is an explorative, iterative and cumulative way of building

theory (Glaser & Strauss, 1977). The main features of this approach involve constant

comparison of data and theoretical sampling (Corbin & Strauss, 2008). Constant comparison

is a rigorous method of analysis that involves intensive interaction with the data (Maxwell,

2005) to contrast emerging with already emergent ideas and themes. Simultaneous collection

and processing of data (Lincoln & Guba, 1985: 335) leads to the generation of firmly

grounded theory. Theoretical sampling refers to ongoing decisions about who to interview

next and how. As the constant comparison of data yielded insights about our phenomena of

interest, research modifications were made to gain broader comparative and deeper personal

narratives regarding pricing experiences, and the sample was adjusted in response to

emerging ideas and themes.

Sample

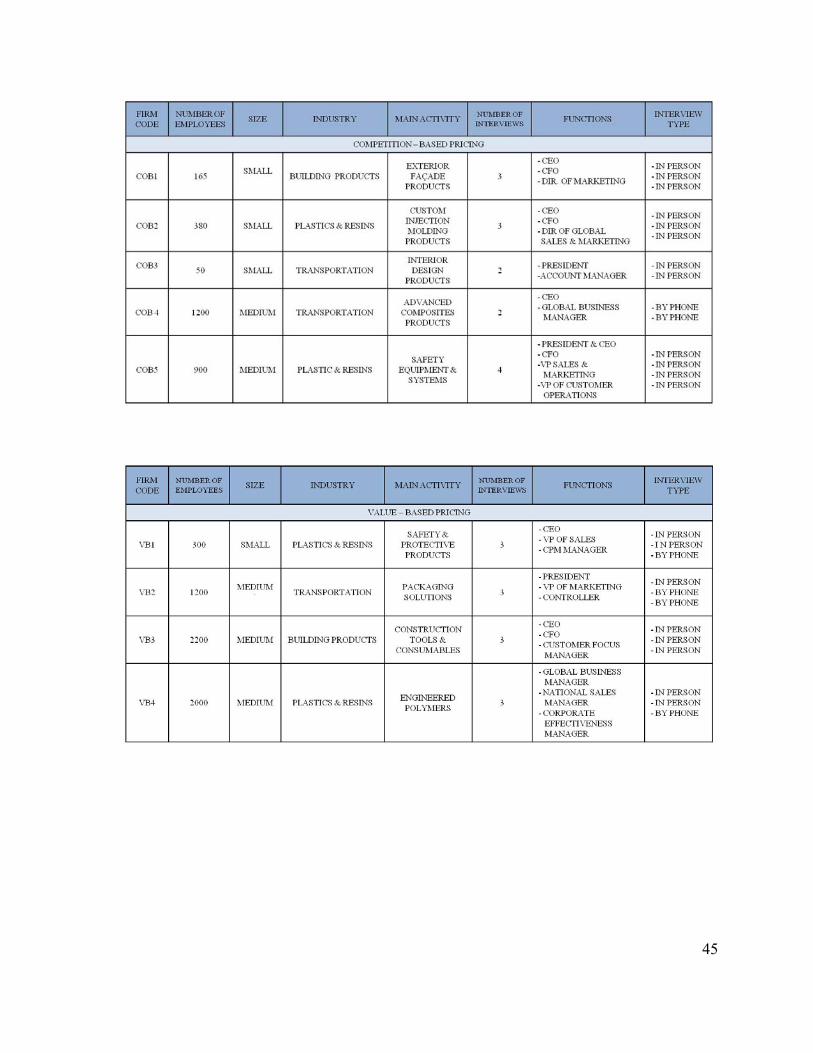

Our sample consisted of forty-four managers in fifteen small and medium U.S.

industrial firms. Relying on the principle researcher’s professional network and advice by the

Professional Pricing Society, over thirty-six small and medium U.S. firms were identified in

three industries: building materials, transportation products and resins & plastics products.

Managers in each firm were contacted for initial qualification with respect to their pricing

orientation. The intention was then to request participation in the research project from small

and medium firms using the three basic pricing orientations. Fifteen of the qualified

companies agreed to participate in our study. Additional sample details are available in

Appendix A.

15

Seven firms were small as defined by the Small Business Administration 2007 size

standards by industry (www.sba.com/size) as having between 50 and 380 employees; and

eight were medium-sized with between 900 and 2200 employees. Two divisions of large

corporations where pricing decisions were taken independently were also included in the

sample.

Six firms (providing 18 interviews) adopted cost-based pricing, five (resulting in 14

interviews) used competition-based pricing and four (yielding 12 interviews) relied on value-

based pricing. Two to four interviews were conducted at each firm. Respondents included

fifteen CEOs or top executives, eighteen sales and marketing managers with full or partial

responsibility for pricing, and eleven finance and accounting managers with decision-making

authority. The firms were geographical diverse as interviews were conducted in ten U.S.

states.

Data Collection

The primary method of data collection was semi-structured interviews conducted over

a three month period from April to June 2010. Thirty-seven interviews were conducted in

person at the respondents’ place of employment and seven were conducted by telephone. The

interviews, averaging 60+ minutes, were digitally recorded and subsequently transcribed by a

professional service.

We focused on managers’ experiences in making pricing decisions and in

participating in the firm’s pricing process. We asked open-ended questions to elicit rich and

specific narratives and used probes when needed to clarify and amplify responses (the

interview protocol is presented in Appendix B). Informants were first invited to talk about

themselves, their backgrounds, and their work. We then asked them to describe their specific

16

experience with the most recent pricing decision made in their firm or a very recent meeting

during which pricing was discussed or a pricing decision was made. Third, informants were

asked to focus on the most significant pricing decision made in their firm over the past 12 to

24 months and to describe that experience in great detail. For both questions we used probes

to provoke specific details about the pricing process. Finally, we asked the respondents about

their experience with pricing innovation and value-based pricing. The overall goal was to

elicit experience-based practitioner perspectives on the organizational factors that influenced

the firm’s pricing orientation.

Data Analysis

Consistent with a grounded theory approach, data analysis commenced

simultaneously with data collection. The audio recordings of each interview were listened to

several times and the transcripts of each interview read repeatedly. Three stages of rigorous

coding then ensued. First, all of the transcripts were “open-coded”, a process that requires the

researcher to identify every fragment of data with potential interest (commonly called

“codable moments” (Boyatzis, 1998)). Open coding, which can be compared to a

brainstorming process for the analysis of data (Corbin & Strauss, 2008), requires detailed

line-by-line readings of each transcript. We read each transcript four times to ensure capture

of all codable moments which were documented on index cards. Manual coding on cards

allowed the researcher to nearly “memorize” the data and to capture the essence and richness

of the general themes and trends emerging from the voice of the informants. We identified

and labeled (Boyatzis, 1998) 2554 such words, phrases, or longer sections of text in the

forty-four interviews. These “codable moments” were sorted and assigned to pre-existing or

new categories that included similar excerpts from other interviews. In a second phase of

17

coding (“axial coding”) these categories were further refined as we compared and contrasted

them, a process that resulted in the emergence of patterns and themes. During the axial

coding phase we reduced the number of categories to 92. Finally, in the third phase of the

coding process (“selective coding”), we focused on key categories and themes that generated

our findings. The selective coding process resulted in a reduction in the number of categories

from 92 to 40 yielding 7 major themes and capturing 781 of the total “codable moments”.

Additional information relating to the definitions of themes and sub-themes is presented in

Appendix C.

FINDINGS

Our data reveals that the decision-making process and the factors influencing price

setting and price point definition for existing and new products in U.S. small and medium

industrial firms varies dramatically by pricing orientation i.e. value, competition and cost.

We discovered stark differences in the locus of the pricing function, the nature of the pricing

process, the organizational structure, the diffusion of pricing capabilities and in leaders’

behaviors in firms with a value-based pricing orientation versus those with cost- or

competition-based orientations.

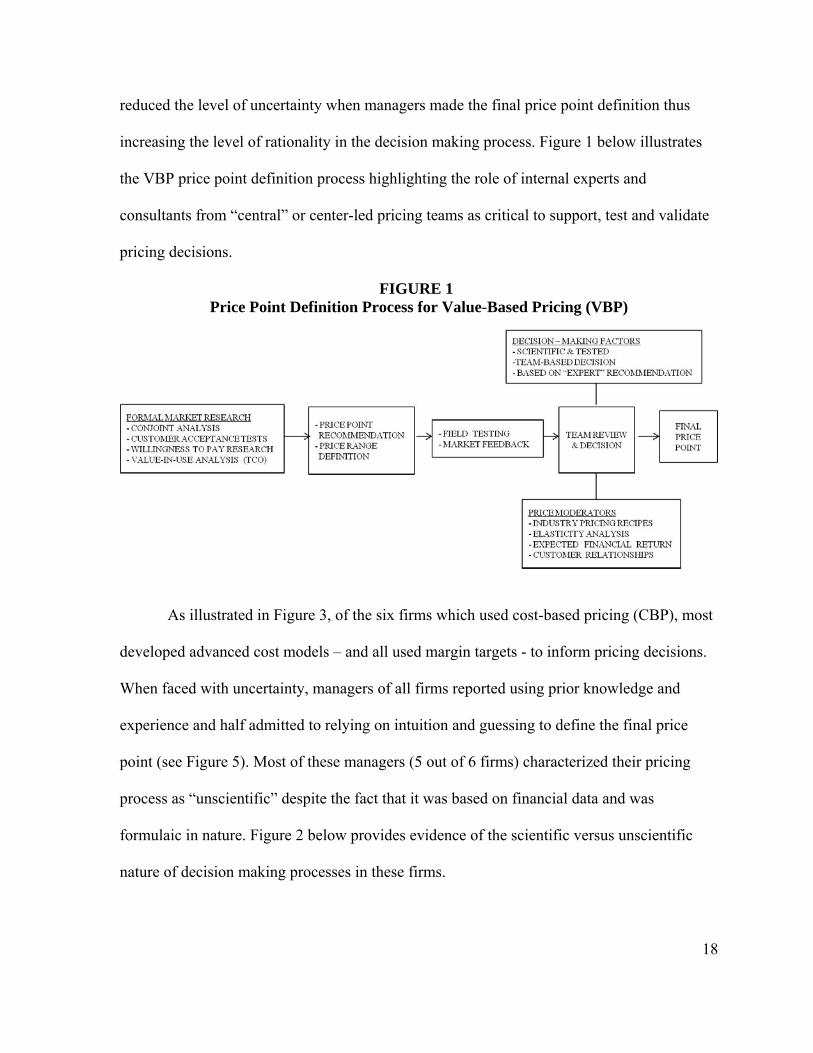

Finding 1: Firms using value-based pricing (VBP) support pricing decisions by reliance on formal market research, scientific pricing methods and “expert” recommendations while those using other orientations (cost or competition) rely on experience, prior knowledge, gut and intuition.

Three out of four firms in our sample that had adopted VBP conducted formal

quantitative market research to calculate customers’ value and to derive final pricing points.

These firms used scientific methods, such as conjoint analysis, KANO, and customer

acceptance testing, to define a range for the price point. Respondents claimed these methods

18

reduced the level of uncertainty when managers made the final price point definition thus

increasing the level of rationality in the decision making process. Figure 1 below illustrates

the VBP price point definition process highlighting the role of internal experts and

consultants from “central” or center-led pricing teams as critical to support, test and validate

pricing decisions.

FIGURE 1: Price Point Definition Process for Value-Based Pricing (VBP)

As illustrated in Figure 3, of the six firms which used cost-based pricing (CBP), most

developed advanced cost models – and all used margin targets - to inform pricing decisions.

When faced with uncertainty, managers of all firms reported using prior knowledge and

experience and half admitted to relying on intuition and guessing to define the final price

point (see Figure 5). Most of these managers (5 out of 6 firms) characterized their pricing

process as “unscientific” despite the fact that it was based on financial data and was

formulaic in nature. Figure 2 below provides evidence of the scientific versus unscientific

nature of decision making processes in these firms.

19

FIGURE 2: Differences in the Decision Making Process between Firms Using Value-Based Pricing

and Those That Did Not

Scientific Decision Making Process

VB1 - SM

"Basically, we give one recommendation...and we try to make this recommendation with a proof, with an evidence that this is right. And this is done in this Phase 4 (of Stage Gate), for example, within the second customer contact phase, which can be a conjoint analysis because then you have facts and data that support your recommendation."

VB1 - EL

"The large decision-making is up to the product manager, of course. He will follow the recommendation of the (functional) guy based on the controlled research."

VB4 - SM

"We try and get feedback from our testing. So whenever you have tests done and you can quantify the performance of the new product versus the other alternatives that customers have access to (and) then we try and see if we can quantify the benefit that this product will deliver based on all the benefits we think it brings. We will survey as many as many customers as we have access to, or as much test data as we have generated and have access to...We ask them to test it, test the hypothesis. Instead of saying every analysis you come up with is wrong and therefore cannot be implemented, you create an implementation plan that allows you to test."

VB2 - FA

"We do an analysis of the investment, definitely...For something like that, because it would be like a new product and we would be investing, we have a process internally where, before we finalize anything, it goes before the executive team, and we review the pricing. We review our returns on the project "

Unscientific Decision Making Process CB5 -

EL "I would love to say it’s scientific, but it ain’t, I mean, it ain’t….it’s a gut check that’s made that."

CB3 - EL

"Yeah, it’s not a highly scientific, there’s not an algorithm I could give you."

COB1 - SM

"Now what that premium is, is highly, in my mind, unscientific. That’s almost (as much) art as it is science...A quantification of the value of the system is the Holy Grail for me."

COB3 - EL

"We had information coming in from Japan. We had information coming in from China. So we knew we were in a favorable position, which I think gave us the confidence to go a little bit higher, but I can’t say at the end of the day I did a spreadsheet and put in all the factors and came out with a number and said, “That’s the number we’re going to"."

COB2 - EL

"As far as having some working formula that enables us to say that this marketplace enables us to mark up 50 percent of what we would normally do, it’s probably not as sophisticated as that. It is more a sense of understanding the marketplace and the pricing associated with the applications, and then the value add that we bring to the table to ensure that we achieve maximum pricing."

FIGURE 3:

Price Point Definition Process for Cost-Based Pricing (CBP)

20

All of the firms in our sample using competition-based pricing (COBP) similarly

relied on prior knowledge and experience as well as intuition and gut feeling to define the

final price point. Our data, as reflected in Figure 4, demonstrates that managers in these firms

typically considered the price of the best competitive products and added a premium to it.

While using cost models (4 out of 5 firms) and margin targets (4 out of 5 firms) to set their

minimum prices, the final price point setting was reported to be set based on “gut feeling”

and judgment call (see Figure 5). Pressed to specify how and by whom the final price point

was defined, managers of these firms as well as those in firms using CBP admitted to

reliance on “collective intuition.”

FIGURE 4: Price Point Definition Process for Competition-Based Pricing (COBP)

21

FIGURE 5: Evidence of Decision Making Factors in Firms Using Cost-Based or Competition-Based

Pricing Orientation

Decision Making Based on Gut and Feeling

CB5 - EL

"It’s based on their gut…it’s their experience and their gut."

CB3 - EL

"Think about the person involved, but mostly, it’s got to be a gut – there’s no certainty. So there’s no analytical (process)."

CB3 - FA

"…how much do we go in compared to our competition? That’s more, you know, a feeling thing…."

COB5 - EL

"It is not structured at all, and I guess that’s one of the things that I find repeatedly through pricing discussions...there’s so much intuition around it that’s used…..to be very, very honest, at the end of it, it’s a gut thing. I said, “I wanna price it higher. I wanna go with a more premium. We’re a premium brand. "

CB4 - FA

"And it's just gut-feel experience...They pretty much took what we had...there wasn't a lot of changes – just some small tweaks. Maybe this went up a little bit. Sometimes if you're working so close to it, you don't see the forest through the trees. And then when they look at it, they have a different perspective."

Decision Making Based on Judgment Call and Guessing CB2 -

EL "Judgment call. Judgment call. Not a written down process. It’s just a judgment call…..no scientific mechanism."

COB2 - SM

"No. I mean if we know that they’re losing – one of their packs may sell for $100, you can find some of that information to get close. Some of it is good guessing. Others are you get limited information."

COB3 - EL

"We basically made a somewhat educated guess that we were going to go higher than our typical market price because we were unique in the marketplace.."

Finding 2: The locus of pricing and the organization of the pricing function in industrial firms varies greatly based on pricing orientations.

Finding 2.1: Pricing is an orphan in industrial firms using cost or competition pricing orientation. No dedicated pricing function existed in the 11 firms in our sample using cost or

competition pricing orientation. In these firms, pricing activities were highly fragmented,

followed informal pricing review processes, and focused only on margins versus prices (7 out

of 11 firms). By contrast all firms using VBP had dedicated pricing functions (involving 3 to

15 members), tracked specific pricing KPI’s and led specific weekly or monthly pricing

reviews.

22

Finding 2.2: The locus of pricing responsibility varies based on pricing orientation. In the 11 firms using CBP and COBP, the locus of both tactical and strategic pricing

responsibility was situated in sales function. In all firms using VBP, the pricing function

reported into the marketing organization. In these industrial firms, marketing was

responsible for strategic pricing resulting in greater integration of pricing programs in the

overall marketing planning process.

Finding 3: The implementation of VBP is associated with significant changes in organizational structure and with the diffusion of pricing capability throughout the firm.

Finding 3.1: Firms using VBP designed formalized processes and established centralized or center-led pricing expertise. All firms using VBP created specialized units composed of highly skilled

professionals whose mission was to support the pricing decision-making process. These units

included, as illustrated in Figure 6, a packaging engineering group, a dedicated pricing team

acting as internal consultants or a specialized market research team dedicated to voice of the

customer projects. The role of these units was to provide project-related support to managers

who made business unit-specific pricing decisions.

23

FIGURE 6: Evidence of Role Specialization in Firms That Use Value-Based Pricing

VB1 - EL

"We have dedicated (functional) managers. They don’t do anything else, and then just (customer research), and this is observation of the customer. It’s videotaping of the customer. It’s understanding what is the unarticulated needs of the customer, and of course, also the articulated needs."

VB3 - EL

"The way (company) works is we have the business units in (country) which are in charge of development. So they bring the products and then they bring overall pricing guidelines worldwide."

VB3 -

SM

"You've got the senior manager of pricing, which is responsible for the pricing processes; continuous improvement for (Corporation) overall...and then within that group you have a few analysts who help manage the pricing within the system: one technical person, one person who helps on the reporting..., one individual who helps out with projects like agreement review process (and) strategic business pricing. And we also have group that focuses in on day-to-day maintenance of making sure price points in the system don't go below a certain threshold."

VB4 - EL

"In a development group...there’s three people like (name) who are development managers. We’ve got hundreds of development people in the world...That’s all they do. They don’t sell a thing......So they’re doing the advanced design, advanced development."

VB2 -

SM

"We have engineering services, our project managers...(who) can put together is a cost justification analysis…The department is called Engineering Services...they’ll bring in all the formulas/cost justifications from our customer’s end."

VB2 - EL

"We have a pricing department. It's four people that are split by market segment, and they're responsible for doing quotes for new business or large – anything that's not under contract should come to them for pricing, to do a quote."

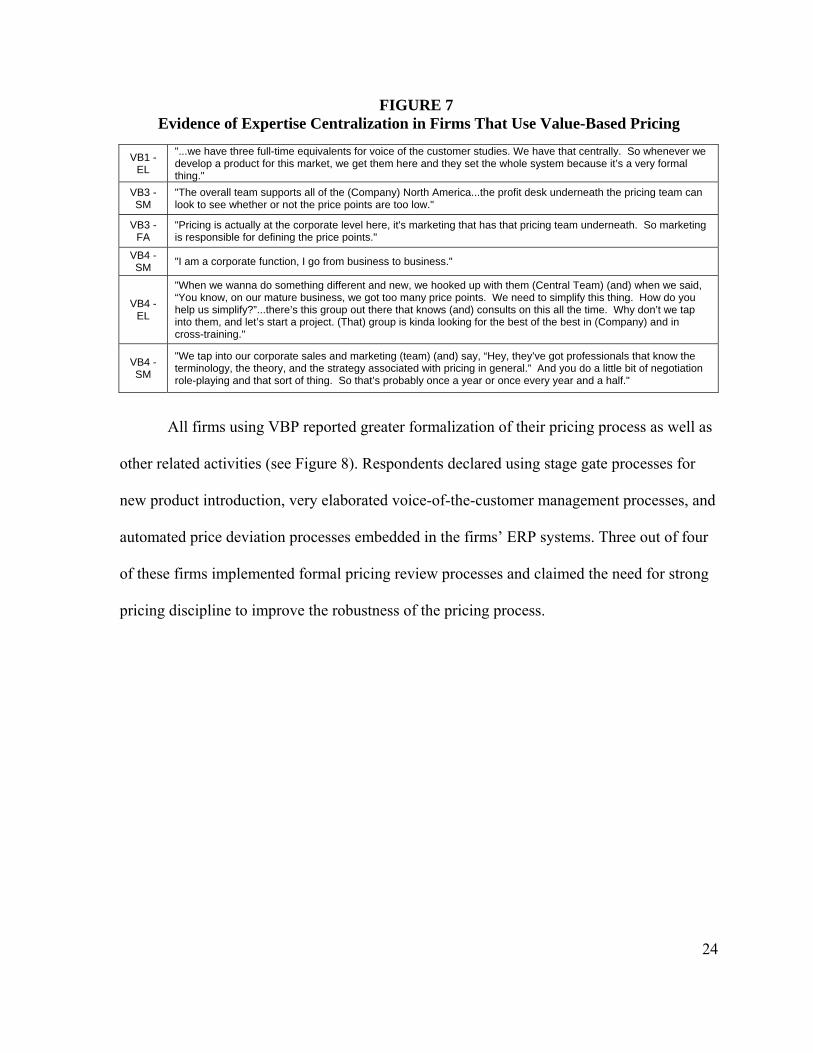

In these firms, pricing responsibility was center-led and the department provided

pricing support to the entire organization. Our findings (see Figure 7) suggest a definition of

centralization in which knowledge and capabilities were concentrated to create the concept of

a center of excellence for pricing. Five out of six sales and marketing respondents in firms

using VBP indicated that this central pricing function acted as a strong resource to improve

managerial pricing management. None of the firms using CBP (0 out of 6 firms) reported the

existence of a centralized pricing function.

24

FIGURE 7: Evidence of Expertise Centralization in Firms That Use Value-Based Pricing

VB1 - EL

"...we have three full-time equivalents for voice of the customer studies. We have that centrally. So whenever we develop a product for this market, we get them here and they set the whole system because it’s a very formal thing."

VB3 - SM

"The overall team supports all of the (Company) North America...the profit desk underneath the pricing team can look to see whether or not the price points are too low."

VB3 - FA

"Pricing is actually at the corporate level here, it's marketing that has that pricing team underneath. So marketing is responsible for defining the price points."

VB4 - SM

"I am a corporate function, I go from business to business."

VB4 - EL

"When we wanna do something different and new, we hooked up with them (Central Team) (and) when we said, “You know, on our mature business, we got too many price points. We need to simplify this thing. How do you help us simplify?”...there’s this group out there that knows (and) consults on this all the time. Why don’t we tap into them, and let’s start a project. (That) group is kinda looking for the best of the best in (Company) and in cross-training."

VB4 - SM

"We tap into our corporate sales and marketing (team) (and) say, “Hey, they’ve got professionals that know the terminology, the theory, and the strategy associated with pricing in general.” And you do a little bit of negotiation role-playing and that sort of thing. So that’s probably once a year or once every year and a half."

All firms using VBP reported greater formalization of their pricing process as well as

other related activities (see Figure 8). Respondents declared using stage gate processes for

new product introduction, very elaborated voice-of-the-customer management processes, and

automated price deviation processes embedded in the firms’ ERP systems. Three out of four

of these firms implemented formal pricing review processes and claimed the need for strong

pricing discipline to improve the robustness of the pricing process.

25

FIGURE 8: Pricing Process Formalization by Pricing Orientation

Formal Pricing Process

VB3 - EL

"...there’s a time to money process. From product development to product launch, there’s a gate system...in Gate 3 or 4 is where the finalized product along with the defined marketing plan of the market organization has to come together. And in that model you’ll have seen this customer work that has been done with prototypes and you’ll see our pricing models that we’ll put together in order to go after our piece of the marketplace."

VB3 - SM

"We have the prices structured in the system, the what we call the profit desk underneath the pricing team can look to see whether or not the price points are too low, or are at least profitable and value-based enough to go, regardless of what business or trade it is. It's all set up, up front in the system."

VB3 - SM

"We'll have monthly reports that show the trends...on a monthly basis, (CEO's Name) along with other individuals get a report to see how has our NSP (Net Sales Price) along with (our) template utilization...But it's basically seeing how consistent are we with our pricing to customers."

VB2 - EL

"...there will be a general price list that will have a high and low on it. And if somebody tries to price outside of that high and low, that will automatically trigger what we call a workflow, which will require an approval from a higher-level marketing manager."

VB1 - EL

"this process is not just a nice book. This is standard. That (is) one of the key elements that...a cross-functional internal team has come up with. So that’s embedded internally (and) deployed internally, and that’s (a) very critical success factor..."

Informal Pricing Process

COB5 - EL

"More (of) the formality is around costing and the stage gates are you either proceed or don’t proceed based on costing (and) cost targets. We set a cost target based on the margin expectations...So we put more formality around costing analysis, and there’s less formality around the pricing...it’s funny how this works."

COB3 - EL

"We look at programs we thought we would get and didn’t get and do an autopsy on why did we not get them...But honestly, once we get a business, we don’t review the pricing on a regular basis."

CB2 - EL

"It’s not reviewed formally. I guess I would call it informal. It’s a process, but it’s not something we sit down and have a meeting to review all the quotes...I’d say that’s a little more informal."

CB5 - FA

"The pricing was decided among sales and the CEO. There really wasn’t a formal meeting that took place with finance related to the pricing. There was no real formal meeting that involved finance at least. "

CB4 - EL

"I mean I apply those principles and disciplines personally. I don’t think we embrace that (pricing) philosophy necessarily formally here."

CB6 - EL

"...somewhat formalized...There wasn’t a formal...formula that I recall ever having to go to say, “Okay, if it does this give that a factor of 10 percent. Or this gives a factor of 30 percent.” Nothing like that. I’m sure that exists, but that was nothing we ever used."

Finding 3.2: Firms using VBP – but not those using COBP or CBP – purposefully diffused pricing capability throughout the firm by training and designing proprietary tools. All firms using VBP in our sample emphasized the importance of training and

designed specific formalized training programs for both existing and newly hired personnel.

Only one in six firms using CBP, however, did so despite recognizing the importance of

training (Figure 9).

26

FIGURE 9: Differences in the Training Focus among Firms with Different Pricing Orientations

Firms That Conduct Specific Pricing Training

VB4 - SM

"We do a lot of training on to get ready for a specific price increase because every single one (price increase)..is a little bit different. So there is some specific training on this one."

VB4 - SM

"Specific (pricing) training for price is probably done in three ways. One way is probably once every year or so, we tap into our corporate sales and marketing.....“they’ve got professionals that know the terminology, the theory, and the strategy associated with pricing in general.” And you do a little bit of negotiation role-playing. So that’s probably once a year or once every year and a half. And then our own team does training about every year and a half on sales basics."

VB4 - SM2

"As corporate marketing we've launched a number of initiatives which train people at multiple levels. So you have the everyday practitioners...(trained) not just pricing but general aspects of marketing. We are doing training for senior leaders. We are also trying to train people who are running important projects...I am very focused on the pricing. I do it as sessions in seminars. I do it on the project kind of work."

VB3 - SM

"Every account manager learns how the pricing is done through the BTS which is three weeks of training when an account manager (or) a sales rep starts. And so that's been one of the main ways to train the individuals on how to price, what the value is for selling trade templates."

VB1 - EL

"train, train, train, train...we are just making a contract with a training company in the U.S…. to really teach them value selling, strategic selling and distribution management...that’s a program for the next 18 month."

Firms That Do Not Conduct Specific Pricing Training

CB3 - SM

"Not a lot. We are very lean on all of our expenses, and so you won’t see us spend a lot of money on training. It’s expected that I try and convey that to the RVPs, and they convey it to their people. So we just do it by doing it."

CB3 - EL

"You know I don’t think we’re going to do formal training on it."

CB2 - SM

"As a company, we used to be really, really good at training. We’ve lost that over the last six years or so, and ...we probably don’t train 15 percent of what we used to. And that’s a little disheartening."

COB4 - EL

"...training hasn't been as big an impact or driver. We haven't spent as much in training or done as much training as I guess we probably could have."

COB4 - SM

"No, we haven’t done (training) and honestly that’s probably something that you know we should be doing."

COB5 - EL

"No, not so much. We haven’t (done training), not as formal. Now they have training, certainly, that’s specific to their areas, but we’ve not done pricing training or anything like that."

Firms using VBP also focused on developing internal capabilities in the areas of

market research (4 out of 4 firms), pricing research (3 out of 4 firms) and the development of

proprietary tools (4 out of 4 firms) to capture and quantify customer value that were more

sophisticated than those described by firms using CBP and COBP. Top executives (4 out of

4) and sales and marketing respondents (4 out of 6) in these firms using VBP were among the

respondents who reinforced the importance of these proprietary tools to support the

implementation of the total cost of ownership and value-in-use pricing methodologies.

27

Finding 4: VBP requires firm-wide internalization and the decisively influence of champions

The role of top executives in firms using CBP and COBP was reported to be limited

to approval of unusual pricing deviations, input on large contract negotiations, and

clarification of uncertain and ambiguous pricing opportunities and the conduct of general

business reviews. Top management in these firms were described by managers as involved

only in to day-to-day and tactical pricing. All of the executives in firms using VBP, in

contrast, were actively engaged in championing its implementation (see Figure 10).

Managers characterized these executives as driving the internalization of VBP throughout the

firm and motivating organizational changes required to support it. Sales and marketing

managers (5 out of 6) reported that support and conviction from top leaders was essential to

the VBP adoption.

28

FIGURE 10: Evidence of Leader’s Decisive Influence

Leadership Emphasis

VB4 - SM

"they (top executives) end up being sponsors of the projects I lead and they understand full well what the issues are and why that kind of a project is required. The project is periodically reviewed by the leadership people...they look at our results...they understand why our results are what they are and then they look at our strategy recommendations and approach. They are big partners in that because if they don't bless it, implementation will never happen."

VB1 - EL

"Make sure that top management does support the initial rollout (of the VOC process) because the rollout is critical."

VB3 - SM

"The fact that top management was behind (VBP implementation) – and that was probably the critical piece that made it successful - that top management was willing to go through the pain of making this change because not everybody was on board...Again, I go back to the top management buy-in."

VB3 - FA

"You have to have a compelling idea or concept that you want to rally the troops behind...And you need to I would say buy in from top executives."

Executive Commitment

VB4 - EL

"(We) really did stand behind (VBP strategy)…It is a commitment we are not gonna change next year....But in the last, I would say, the last 10 we’ve been pretty consistent in terms of our (pricing) strategy. Very consistent."

VB3 - EL

"Look, we’re a (Country) based company. ..We believe in long term (and) sustainable management based on a well-defined (VBP) strategy, which needs to be executed over a large group of people. There’s nothing else to be said."

VB1 - SM

"(Value strategies) are our core strengths in the company, and it’s highly supported. So that’s why I’m not facing too much resistance."

COB5 - SM

"…executive commitment to the (service and value model) initiative (is)….made it the No. 1 strategic initiative for (Company)...and from that stemmed everything else."

Driving Force

VB3 - SM

"What made (VBP) work was, looking back,..was definitely the fact that top management helped sell it, helped, honestly, push it along as well. And over time, it's proven that they were correct. But without the top management, it wouldn't have happened."

COB4 - EL

"I'm a very big driver (of value strategies). I'm the biggest pain."

Respondents in all firms using VBP described its implementation as a long and

difficult process triggered by a specific stimulus (e.g. customer pressure, an acquisition, a

product launch failure or a desire to escape a cyclical industry pattern), purposefully

championed by top executive and requiring organizational transformation. As one manager

observed, “the biggest barrier was the change itself – (overcoming) the belief that this will

not be positive for (Company) and going from complete field control to corporate

helping…by giving suggestions on pricing. And it was not easy at all”.

29

Finding 5: The internalization of VBP requires a high level of organization-wide confidence.

All firms using VBP reported that confidence of employees in their organization was

increased when they strongly believed in the team’s ability to implement VBP as well as if

they shared strong beliefs in the firm’s products, technologies and values (see Figure 11).

These beliefs gave sales staff greater courage to stand firm to customers’ pricing objections

and to be, as one respondent stated, “superman for one second” when facing customers’

objections (see Figure 12). CEO’s and top executives in these firms seemed to be most aware

of the criticality of developing these internal beliefs (4 out of 4) and implemented specific

programs and activities to boost organizational confidence. Three out of four firms using

VBP focused on specific people development activities such as coaching sales staff,

designing specific performance management programs and targeted talent development plans

around value orientation. This phenomenon was not observed in firms using CBP and was

observed to a lesser extent in firms using COBP.

FIGURE 11: Importance of Employee's Beliefs on Confidence

VB4 - SM

"…you have to look (customers) in the eye and say, “Ours (product) costs more. This costs more, and it’s worth it. You should pay more for that. You have to be pretty confident to do that."

VB4 - SM2

"We have to look people in the eye and say “we deserve to be paid more for our products.” We have to look them in the eye and you have to have confidence...and say “we got engineers, we got scientists...and so ours do cost more".”

COB1 - EL

"I think it’s more a belief that you actually do have a premium product. You have to have a culture that the people inside believe that what you’re doing is better than the next guy, that you’re using better ingredients, that you have better technology behind the product formulation, that you can – the product consistently has to be there."

COB5 - SM

"I think the top three factors to (value strategies) success: getting our people to believe in it, No. 1. Getting the customer to see value in it. Those are clearly the two (because) if you don't have your people in alignment, going after it, and understanding it, and believing in it, they're not gonna sell it. And they didn't at first. There was a few people that adopted it – when I mean "few," less than a handful. But they were very successful with it…and people started to pay attention."

30

FIGURE 12: Importance of Courage and Pricing Heroes on Confidence

VB4 - SM2

"Constant interaction. Every week...we give examples of how this worked…celebrating (Name) as a hero because he implemented that price."

VB3 - EL

"The confidence of the sales force is to walk in and display the innovation that we have. And when it gets to the pricing objection because we will always be above our competition, (having) the ability to stand firm and explain why the price is correct."

VB3 - SM

"That gets people courage when you start having a lot of success in areas that they might have viewed as, “That’ll never happen"."

COB5 - EL

"...this was a great little quote: “You only need to be brave for one second, and it’s when the guy asks for a discount and you say no. And then you justify it. That takes bravery.” So how do you get salespeople in a mindset to justify the price? You don’t have to go in there and be Superman for two hours. You have to be Superman for one second."

Firms using VBP (3 out of 4) also reported that they consistently communicated internal

wins as well as market challenges in order to accelerate the organizational buy-in and to

facilitate the internalization of VBP. Our findings (see Figure 13) indicate that success stories

in the area of pricing increased organizational confidence and created “organizational

heroes” with respect to successful pricing activities.

FIGURE 13: Importance of Success Stories on Confidence

VB4 - EL

"And you try to get people allied around the success stories that we have. That gets people courage when you start having a lot of success in areas that they might have viewed as, “That’ll never happen.” Holy mackerel. We’re being very successful with this thing? We’ve had so many price increases recently that it’s very contagious...".

VB4 - SM2

"So we try to show people examples of "here’s more value". In these meetings, we’ll have some success stories".

VB3 - SM

"But the marketing and the pricing team constantly giving feedback....And here are some account managers whom we converted. They're a believer in this. This helps out. They have to spend less time on pricing now. They don't have to worry about which price point, or what was the price point in the past."

VB1 - EL

"No. 2 (key success factor to VBP), create success stories and proven track records before you implement the process."

Finally, three out of four firms using VBP emphasized the criticality of getting teams

energized in order to promote its implementation. Two out of four CEO’s working in these

firms engaged in specific activities and behaviors in order to energize teams and to create

emotional contagion in their organization.

DISCUSSION

31

Our data contradicts the widely held assumption (Ingenbleek, 2007; Hinterhuber,

2008; Cressman, Jr., 2010) that value-based pricing (VBP) can simply be “adopted.” Rather,

they strongly suggest that implementation and internalization of VBP requires deep

organizational changes that transform the fabric of the firm. We expected to find significant

differences in how small and medium industrial firms organized their pricing functions and

how pricing decisions were made – and our findings proved us right. But stark contrasts

among firms with different pricing orientations were uncovered and were related to

organizational characteristics and leaders’ behaviors in these firms.

We begin by discussing the deep transformational change required to implement

VBP; then we examine the transformation to VBP from a learning theory perspective. Next

we discuss the essential role of champions in this organizational transformation; and we

conclude by reviewing the current position of the pricing dimension in the industrial

marketing concept. Finally, we propose a conceptual model for the internalization of and the

transformation towards value-based pricing.

Value-Based Pricing Requires Deep Transformational Change

Marketing and pricing studies concerned with the adoption of the three main pricing

orientations in business markets recommend VBP as a modern and advanced pricing

approach (Monroe, 1990; Nagle & Holden, 2002; Hinterhuber, 2004; Ingenbleek, 2007;

Hinterhuber, 2008; Cressman, Jr., 2010). However, we argue that the implementation and

internalization of VBP requires deep organizational change that transforms the firm’s

organizational life and identity as well as the identity of actors within it. This transformation

is manifested by a slow “mutation” of what our informants called their firm DNA from cost

32

or competition to customer value. The respondent excerpts in Figure 14 illustrate how cost

mentality is engrained in firm DNA while Figure 15 suggests that the transformation process

does not happen swiftly.

FIGURE 14: Evidence of Cost-Plus Mentality in Firm’s Culture or DNA

COB5 - EL

"Our DNA is manufacturing ... I’m very used to standard cost....the very traditional cost plus. It just comes from being a manufacturing company.... I think we’re dynamic and moving in the service models but we’ve dragged along this cost plus kinda pricing model."

COB3 - EL

"We really do need to break away from the cost plus mentality and really look at what can we really get for this business. I do challenge that, but maybe if the starting point is cost plus, you’re never really breaking away from that thinking."

CB5 - SM

"I’m responsible for all costing…. in the way our business runs today, that’s the foundation of all pricing….in essence, most of our pricing is a cost plus mentality."

CB5 - FA

"The COO had put in these measures to increase sales by discounting, filling up the plant, and he had convinced the people underneath him...that absorption was the name of the game. so now that’s imbedded in the culture."

CB3 - SM

"So we were given a target that was very aggressive, so then since we had a target we had to decide do we come below...at...(or) above. And in the end because of the importance of the business and we have this mentality, you can’t miss, we came in slightly below and we eventually won the business."

FIGURE 15: Evidence of Firm’s DNA Transformation to Value-based Pricing

VB1 - EL

"As soon as (customer process management/VBP) is rolled out... it becomes part of your DNA, and that’s when you’re over the hill, when you’ve really passed the barrier. And then, that’s an integrated part of your company contract."

VB3 - SM

" We've realized that if you adjust a price up or down, you may also have to adjust cost because that's typically what happens. And so since this cost is more based on management accounting, we've held it steady throughout the years. So this idea that we have to be more dynamic is very much a culture shift, and to be honest, we're still going through it."

VB4 - SM

"I couldn't say that (it is yet in the DNA). I don't think it happens overnight. It's a journey. It's a journey with multiple, multiple small steps, and (we have) been on this journey for a while. A lot of progress was made, but the journey is not complete. We've got a ways to go, but there's a lot of energy behind it."

The implementation and internalization process of VBP is a long, tenuous, and

sometimes painful journey of change for the organization and its actors. The process

requires intense and sustained organizational mobilization to transform established structure,

culture, processes and systems. Marketers, sellers and developers have to change their

business mentality and their frames of reference and embrace new value-related concepts

which are expected to become a new “way of life” (Forbis & Mehta, 1981). They also must

33

learn a new language in order to carry the value message internally and externally. As a

result, people change and become “organizational heroes” or leave the organization. The

following quote from a VP of Global Sales and Marketing illustrates the difficulty in the

transformation of people:

“We put people on performance reviews….the guy who was No 1 in targeted attainment three years ago.. was No. 3 in sales target attainment last year…And he's on performance plan right now. The reason he's on a performance plan is because he's at the bottom of the barrel on (value selling)…We said to him, "This isn't acceptable. I can get anyone to look after the (equipment) side. What I need someone is to change the market"…We've released a couple of people who haven't been able to make the transition which has been difficult…That kind of performance management alignment is key.”

Our findings suggest that firms engaging in the transformation to VBP intentionally

designed programs focused on building organizational confidence to accelerate members’

buy-in and boost motivation levels to accept change. When confidence is high, people share

beliefs in their “collective power” to produce desired outcomes and ends (Bohn, 2001).

Bandura (1997: 476) posits that “an organization’s beliefs about its efficacy to produce

results is undoubtedly an important feature of its operative culture”. A meta-analysis

conducted by Gully, Incalcaterra, Joshi, & Beauien (2002) showed that the relationship

between collective efficacy and team performance was positive and significant supporting

the idea that efficacy is “a primary determinant to the extent to which individuals or teams

are likely to put the efforts required to perform successfully” (Bandura, 1986: 392). Our

findings support this notion of effort. Confidence consists of “positive expectations” for

favorable outcomes (Hoover & Valenti, 2005). It influences the individual member’s

willingness to invest money, time, reputation and emotional energy to shape the ability to

perform (Kanter, 2006: 7). Organizational confidence is a generative capacity of an

organization to cope effectively with the demands, challenges, stresses and opportunities it

encounters within the business environment. It exists as an aggregated judgment of an

34

organization’s individual members about their (1) sense of collective capacities, (2) sense of

mission or purpose, and (3) a sense of resilience. In its most basic form, organizational

efficacy is a sense of “can do” (Bohn, 2001, 2002).

We suggest that organizational confidence acts as the “fuel” that feeds the engine of

change and generates required organizational mobilization when organizations engage in the

transformation process towards VBP.

Value-based Pricing: at the Nexus of Experiential and Transformative Learning

The implementation and internalization of VBP requires a strong knowledge

foundation in pricing in the organization. Prior knowledge confers “an ability to recognize

the value of new information, assimilate it, and apply it to commercial ends” (Cohen &

Levinthal, 1990). As previously observed, pricing knowledge and capabilities are developed

over time (Dutta et al., 2003), are incrementally accumulated, and are dependent on

organizational absorptive capacities (Cohen & Levinthal, 1990; Szulanski, 1996; Zahra &

George, 2002) of the pricing process actors.

Experimentation is an important requirement for the internalization of VBP concepts,

frames of reference, language and forms of interaction. The transformational nature of VBP

requires that the organization learn through a process of experiential learning (Kolb, 1984;

Kolb, Boyatzis, & Mainemelis, 2001) or through trial-and-error experiments (Pfeffer &

Sutton, 2006). Experimentation matters because “it fuels the discovery and creation of

knowledge and thereby leads to the development and improvement of products, processes,

systems and organizations” (Thomke, 2003: 1). Experiments yield information that comes

from understanding what works and does not work. Learning from past failures can be rich in

findings (Thomke, 2003: 213). But, the most important advantage of experiential learning

35

through experiments is that it provides a valid way for managers to observe and interpret past

experiences (Green & Taber, 1978). Consistent with experiential learning theory (Kolb,

1984), the learning process related to VBP requires both assimilation and accommodation

learning styles. The organization and its members incrementally assimilate knowledge which

will “stick” (Szulanski, 1996) to existing pricing knowledge. However, because of the

innovative, subjective and sometimes contentious nature of VBP, organizational actors will

modify their frames of reference, learning patterns or schemas (Stein, 1995) to accommodate

the integration of unexpected and novel knowledge.

Experiential learning alone is not enough to assure the successful transformation to

VBP. In combination with transformative learning, it represents a powerful foundation that

can help the organization and its members face deep changes and uncertain frames of

reference. Transformative learning refers to the process of “effecting changes in a frame of

reference” or in “the structures of assumptions through which we understand our

experiences” (Mezirow, 1997) . Transformative learning relies on the use of prior

interpretation to “construe a new or revised interpretation of the meaning of one’s experience

in order to guide future action” (Mezirow, 1996, 2000). Our findings suggest that in firms

using CBP or COBP, frames of reference are very powerful in guiding pricing decisions as

they include habits of mind, routines, legacy practices and mentality or mind-sets (Mezirow,

2000) that are deeply engrained in the firm’s culture. Transformative learning refers to the

process of transformation of these frames or references, routines, norms, and schemas to

make them more inclusive, open and “emotionally capable of change” (Mezirow, 2000).

These changes have implications for both the organization and its individual members.

Change requires awareness of how knowledge is created and how information is processed

36

and what values lead us to perspectives. This process of transformation is equivalent to a

reformulation of the structure of meanings (Mezirow, 2000) that requires critical reflection

and a possible higher level of mindfulness (Langer, 1997). Mezirow has identified ten phases

of transformation (Mezirow & Welton, 1995: 50) that encompass factors revealed in our data

as critical in VBP internalization - experimentation with new roles, acquisition of skills and

knowledge and the building of confidence in new roles and relationships. Mezirow’s

conception of transformative learning touches on two critical elements of a successful

transformation to VBP- the enduring nature of change over time and the irreversibility of the

transformation (Taylor, 2007). Both are needed to transform the culture from cost to value

and to take the organization to a sustained process of transformation putting customer value

at the center of the firm’s reason to exist (Slater, 1997).

Champions Lead the Organizational Transformation

The organizational champion is a critical driver of VBP internalization as well as the

organizational transformation. Champions mobilize the organization by energizing teams,

making resources available, providing continuous emphasis and focus on the pricing

orientation, and by being willing to learn from failures to break down organizational and

behavioral barriers.

The literature on organizational champions from a technological innovation

perspective is rich. Forty seven years ago, a seminal article on radical military innovation