Price It Right Interior v2018-08-23-10 · price your services to maximize your fees and...

32

Price It Right How to Value Accounting Services AUGUST J.AQUILA Author of What Makes a Successful Partnership and Engaging Partners in the Firm’s Future

Transcript of Price It Right Interior v2018-08-23-10 · price your services to maximize your fees and...

Price It Right How to Value Accounting Services

AUGUST J. AQUILA

Author of What Makes a Successful Partnership

and Engaging Partners in the Firm’s Future

Copyright 2017 August J. Aquila. All rights reserved.

Published by CPA Trendlines, an imprint of Bay Street Group, LLC. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including, but not limited to, photocopying, recording or using any information storage or retrieval system for any purpose without the express written permission of the author, August Aquila, or the publisher. Contact the author at [email protected]. Contact the publisher at Bay Street Group LLC, P.O. Box 5139, East Hampton, NY 11937 USA. www.baystreetgroup.com.

Price It Right: How to Value Accounting Services does not represent an official position of CPA Trendlines or Bay Street Group LLC and it is distributed with the understanding that the author and publisher are not rendering legal, accounting or other professional services in the publication. If legal advice or other expert assistance is required, the services of a competent professional should be sought.

Registered and/or pending trademarks in the United States are used throughout this work. Use of the trademark symbols or “TM” is limited to one or two prominent trademark usages for each mark. Trademarks understood to be owned by others are used in a non-trademark manner for explanatory purposes only, or ownership by others is indicated to the extent known.

All persons, companies and organizations listed in examples and case studies herein are purely fictitious for teaching purposes, unless the example states otherwise. Any resemblance to existing organizations or persons is purely coincidental.

CPA Trendlines ISBN-13: 978-0999035610 ISBN-10: 0999035614 BISAC: Business & Economics / Accounting / General

Book Design by DittoDoesDesign.com

ii

Contents

Preface ......................................................................................... ix Introduction................................................................................. xiii CHAPTER 1: Traditional Pricing Methods and Marketplace

Orientation ............................................................................. 1 The Two Traditional Methods...................................................... 3

The Rule of Three Method ...................................................... 3 The Cost-Plus Method............................................................. 5

Marketplace Orientation .............................................................. 8 Selling Orientation.................................................................. 8 Product Orientation ................................................................ 10 Production Orientation ........................................................... 10 Marketing Orientation ............................................................ 11

How a Production Orientation Can Be Harmful to a Firm .......... 13 Changing from a Production Orientation to a Marketing Orientation .............................................................. 16

CHAPTER 2: Marketing and Pricing .............................................. 21 The Marketing Mix .......................................................................... 23

People .................................................................................................. 24 Product/Service ........................................................................... 24 Promotion ......................................................................................... 25 Place ............................................................................................ 27 Price ............................................................................................ 27

Various Pricing Strategies ................................................................ 28 Pricing on Cost ............................................................................ 28 Price Leaders ............................................................................... 31 Prestige Pricing ........................................................................... 31 Bait and Switch ................................................................................ 32 Market Penetration .......................................................................... 32

vi

Market Skimming................................................................... 33 What the Market Will Bear .................................................... 34

The Product Life Cycle ................................................................. 35 Introduction Phase .................................................................. 36 Growth Phase.......................................................................... 36 Mature Phase .......................................................................... 37 Decline Phase.......................................................................... 40

Demand ....................................................................................... 41 Competition................................................................................. 44

Perfect Competition ................................................................ 46 Monopolistic Competition ...................................................... 45 Oligopoly ................................................................................ 46

Monopoly................................................................................ 47

CHAPTER 3: Utility and Value: How They Affect Pricing.......... 49 How Clients Perceive Utility ........................................................ 51 How Clients Perceive Value .......................................................... 53 Value and the Services Provided ................................................... 58

The Value Curve...................................................................... 60 Categories of Services on the Value Curve ............................... 61 Other Considerations When Using the Value Curve .................... 63 Using the Value Curve to Define Market Position ................... 65

CHAPTER 4: Alternative Pricing Methods ................................. 69 Ethical Pricing Issues for CPAs..................................................... 71

Discussion of Rule 302, “Contingency Fees” ........................... 72 Discussion of Rule 503, “Commissions and Referral Fees” ...... 75

Subjective Pricing Issues ............................................................... 76 Alternative Pricing Methods......................................................... 80 Fixed or Flat Fee...................................................................... 81

vii

Unit Fee ....................................................................................... 82 Contingent Fee ............................................................................ 83 Hourly Rate ................................................................................. 85 Blended Hourly Rate ................................................................... 87 Fixed or Flat Fee Plus an Hourly Rate ......................................... 90 Hourly Rate Plus a Contingency ................................................. 92 Retrospective Fee Based on Value .................................................. 93 Availability-Only Retainer .......................................................... 94 Retainer as a Deposit Against Future Services ............................ 95 Statutory or Other Scheduled Fee System ................................... 96 Final Thoughts ............................................................................ 96

CHAPTER 5: How to Implement a Change in Your Firm’s Pricing Philosophy .......................................................................... 99

Preparation for Making a Change in Pricing Philosophy ................. 101 Getting Partners to Accept a New Pricing Philosophy ..................... 103 Getting Clients to Accept a New Pricing Philosophy ....................... 109 Making It Happen .......................................................................... 113

CHAPTER 6: How to Bill and Collect Effectively ........................ 119 Developing an Effective Billing Philosophy ..................................... 121

CHAPTER 7: What’s Next? ........................................................... 131

About the Author ........................................................................... 135 About CPA Trendlines ........................................................................ 137

viii

Preface

It is hard to believe that it has been over 22 years since I first wrote about pricing accounting services. Much has changed in the accounting profession, the world and my personal life in that time. Technology is now a driving force in the profession, professional marketing is well established and accepted by firms, United Kingdom voted to leave the European Union (Brexit), and Donald Trump was elected president of the United States of America. I have moved away from the marketing and business development for professional service firms to be a leader in the area of mergers and acquisitions, leadership development, compensation design and change management.

During this time, a lot has been added to the body of knowledge on pricing accounting services. In fact, one of my colleagues, Ron Baker, has spent his career trying to eradicate the time sheet and to educate partners on how to maximize their revenue1. In spite of Ron’s valiant efforts, too many accountants continue to merely charge their clients by the old formula of time spent times some billing rate without thinking about the value of the service provided to the client. It’s now time for accountants and other professional service providers to move beyond this archaic method and to implement other methods of pricing their services.

1 Books by Ron Baker include The Professional Guide to Value Pricing (2000), Implementing Value Pricing: A Radical Business Model for Professional Firms (2010), Pricing on Purpose: Creating and Capturing Value (2007), The Firm of the Future (2003)

ix

true: Selling 20% of the remaining seats for $1,500 is more profitable than selling half of them for a discounted fare of $550.

Pricing of professional and non-professional services can be a complex and often a difficult task. Competition is fiercer today than ever. Firms continue to undercut audit fees. Technology may no longer provide a pricing edge. Clients are more sophisticated than ever, and are demanding more value for the fees they pay. Partners seems to be working harder just to stay even. They are hanging on to a “this is the way we have always done it” attitude rather than taking advantage of newer technologies and global resources to reduce cost.

As you will see in the following pages, the fee you are able to charge for a particular service is predicated on the demand and type of service you are offering – commodity, brand name, hired for experience and unique service. You also have to take into consideration your competition in the market and what they are doing, their cost structure, ethical restrictions, and the fact that accounting, tax and consulting services are intangible and perishable. In other words, once you lose an hour you can never make it up. It’s like an airplane that takes off with too many empty seats. They can never be filled. The airlines maximize the value of each seat sold; shouldn’t you maximize the value of each engagement in order to maximize your profits?

August Aquila Minnetonka, MN

xi

Introduction

The primary purpose of this book is to bring before the reader ideas, concepts and tools on how to price the various services that accountants now provide to their clients. You won’t find anything in the following pages about getting rid of the time sheet. Ron Baker has already written and said quite a bit about that. What you will find are practical ideas to help you price your services accordingly.

Twenty-two years ago, there weren’t many articles or books written about pricing methods. Most of the literature at that time dealt with billing and collection. If you search the topic today, you will find hundreds of articles, videos and books to read or watch.

Even if your billing methods and philosophy are diligently followed and your collections are under control, if you are not pricing your services properly, you are still leaving significant dollars on the table. This book will show you how you can price your services to receive the maximum fees possible.

Most other professionals today price their services based on what the market will bear. Just think for a minute about the following professionals. What do they all have in common? A physician, real estate broker, insurance broker, stock broker, business broker. Their fees are not based on hourly rates, rather they are based on the relative value of the procedure, the size of the real estate transaction, the premium of the life

xiii

insurance policy, the number and value of the stocks bought or sold and the value of the business sold.

This book is as much about the term value as it is about pricing. The underlying concept of this book is that pricing is a marketing activity. Think of designer clothes. They cost a lot more than clothes you can buy off the rack at any store. It’s not that the clothes themselves are that much different. What’s different is the market. The buyers of designer clothes are willing to pay a much higher price than the buyers in a department store. Ultimately the market (i.e. your clients) will determine the value of your services. For most customers, price by itself is not the key factor when a purchase is being considered. This is because most customers compare the entire offering and do not simply make their purchase decision based solely on a service’s or product’s price. In essence, when a purchase situation arises, price is one of several variables customers evaluate when they mentally assess a service’s or product’s overall value.

Value thus refers to the perception of benefits received for what someone must give up. Since price often reflects an important part of what someone gives up, a customer’s perceived value of a service or product will be affected by a marketer’s pricing decision. Any easy way to see this is to view value as a calculation:

Value = perceived benefits received perceived price paid

For the buyer, value of a product will change as perceived price paid and/or perceived benefits received change. But the price paid in a transaction is not only financial; it can

xiv

also involve other things that a buyer may be giving up. For example, in addition to paying money a customer may have to spend time learning to use a new software product, pay to have an old product removed or close down current operations while a product is installed or incur other expenses.

The current hourly billing method unfortunately is based on cost estimates and not on value. Think for a moment; what does this imply? When you determine your fees based on cost you are looking inward. It is as if you are working in a vacuum. Unfortunately, too many accountants actually function this way. If, on the other hand, you are truly client- centered, you realize that it is the client who is at the center of your thought process and that everything you do, whether it is developing an internal process to turn tax returns around quicker or to start a new service, is done to better service the client. Client-centered firms never forget that it is the client who ultimately determines the value of their service.

If you do things right from the start of getting a new client, you won’t have problems billing or collecting. If you are not pricing your services properly, you are leaving significant dollars on the table. This book will show you how you can price your services to maximize your fees and profitability.

Let’s look at the following example. As a partner in a three-partner firm you have always achieved 100 percent realization. And you are very proud of this. Your billing rate is $190 per hour. You provide a variety of services to your clients. The services range from monthly write-up to more complex tax consulting and business consultation.

Is this practitioner maximizing his revenue and profitability?

xv

Is he doing justice to himself? Is he doing justice to his clients by charging the same hourly rate to review a simple 1040 with a Schedule C as to assist the clients in a more complex merger and acquisition tax issue?

What would you do in this scenario?

Our partner in the above example is probably pricing some of his services too low. Since his experience has been to achieve 100 percent of his $190 billing rate for basic work, why couldn’t he charge more for more complex, valuable services? Wouldn’t a client see more value in the merger and acquisition services than in the tax compliance? And wouldn’t it be more profitable to get 90 percent of $230 for the basic work?

Perhaps you are beginning to see the importance of determining the true value for your services. Making more money in the profession today does not require that you work more hours or work harder. It does require that you work smarter and learn how to price your services accordingly.

We have lost the art of pricing our services based on value. Instead, the profession has created an hourly billing method that is based on cost. The computed hourly rate often bears little relationship to the client’s perception of the value of the services rendered.

This is nothing new. The AICPA’s Management of an Accounting Practice (MAP) Handbook from 1993 states:

“Time charges at standard rates should only be the starting point for determining the amount to be billed. The real criterion is the value of the service to the clients.

xvi

Too often, this is recognized only negatively by billing at less than standard rates. Actually, standard rates should not represent a maximum that can be billed for services, rather they should represent a minimum.”

We need to focus on value and leave pricing alone for a while. For the most part, we are not providing a product, but a service, and it is a service that can have a great degree of value. The value is ultimately determined by the client and not by the service provider. We need to become better at understanding and determining what the value is to the client. When we learn how to do that, we will be able to use the tools presented in this book. Pricing is a representation of the value the client receives and pricing has to be a win-win situation or there can be no long-term relationship with the client.

I have tried to look at value and the ways that you can become more profitable by using the ideas and tools presented here in your day-to-day operations. A number of the examples presented in this book come from practitioners throughout the U.S., Canada and England. Many are ideas that I have suggested to firms during my years of consulting. It is important to remember that the ideas presented here are meant for use by all accountants, from the sole practitioner to the Top 100 Accounting Firms.

The book contains seven chapters.

Chapter 1, “Traditional Pricing Methods and Marketplace Orientation,” provides insights into why the traditional methods of pricing our services are outdated and need to be challenged.

xvii

Chapter 2, “Marketing and Pricing,” explores the concepts of marketing and pricing, the product/service life cycle, the importance of demand in pricing and different competitive environments, and explains why pricing is actually a marketing activity.

Chapter 3, “Utility and Value and How They Affect Pricing,” explores how clients perceive utility and value, the value curve and categories of services on the value curve.

Chapter 4, “Alternative Pricing Methods,” presents a variety of alternative pricing methods and how and when they can be used.

Chapter 5, “How to Implement a Change in Pricing Philosophy,” provides tools to implement a change in your firm’s pricing philosophy.

Chapter 6, “How to Bill and Collect Effectively,” tackles the key elements for an effective billing philosophy.

Chapter 7, “What’s Next,” gets you going.

That’s it, so let’s start.

xviii

Chapter 1

Traditional Pricing Methods and Marketplace Orientation

Price is what you pay. Value is what you get.

Warren Buffett

1

professionals who do not understand the marketing orientation or its importance to the firm. Such professionals equate marketing with marketing tools, such as newsletters, public relations, advertising, seminars and webinars, while failing to acknowledge the strategic value of decisions on pricing, client service and product, and delivery.

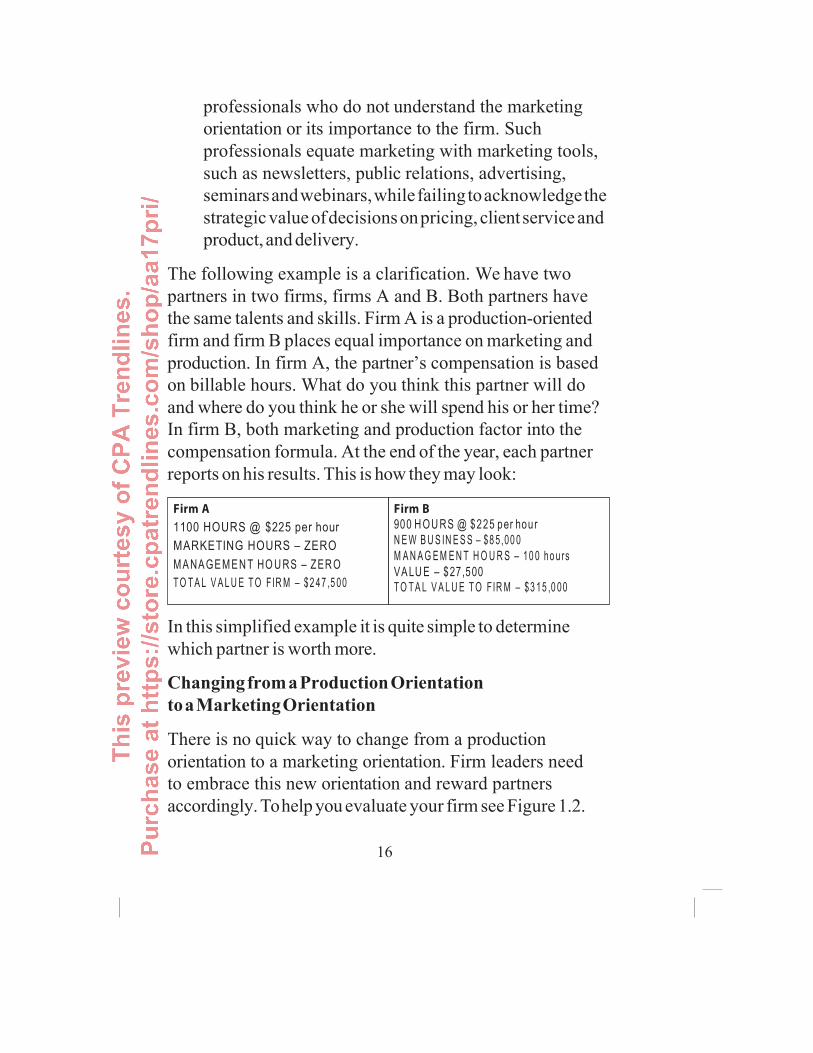

The following example is a clarification. We have two partners in two firms, firms A and B. Both partners have the same talents and skills. Firm A is a production-oriented firm and firm B places equal importance on marketing and production. In firm A, the partner’s compensation is based on billable hours. What do you think this partner will do and where do you think he or she will spend his or her time? In firm B, both marketing and production factor into the compensation formula. At the end of the year, each partner reports on his results. This is how they may look:

In this simplified example it is quite simple to determine which partner is worth more.

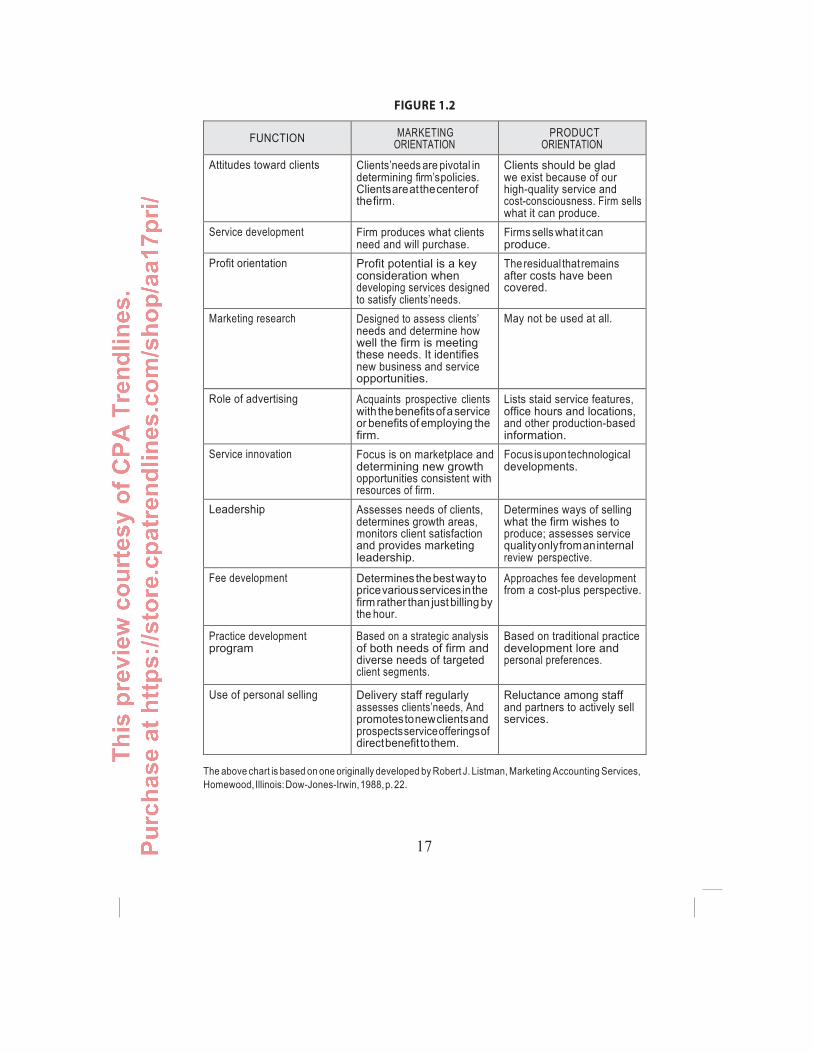

Changing from a Production Orientation to a Marketing Orientation

There is no quick way to change from a production orientation to a marketing orientation. Firm leaders need to embrace this new orientation and reward partners accordingly. To help you evaluate your firm see Figure 1.2.

16

FIGURE 1.2

FUNCTION MARKETING ORIENTATION

PRODUCT ORIENTATION

Attitudes toward clients Clients’needs are pivotal in determining firm’s policies. Clients are at the center of the firm.

Clients should be glad we exist because of our high-quality service and cost-consciousness. Firm sells what it can produce.

Service development Firm produces what clients need and will purchase.

Firms sells what it can produce.

Profit orientation Profit potential is a key consideration when developing services designed to satisfy clients’needs.

The residual that remains after costs have been covered.

Marketing research Designed to assess clients’ needs and determine how well the firm is meeting these needs. It identifies new business and service opportunities.

May not be used at all.

Role of advertising Acquaints prospective clients with the benefits of a service or benefits of employing the firm.

Lists staid service features, office hours and locations, and other production-based information.

Service innovation Focus is on marketplace and determining new growth opportunities consistent with resources of firm.

Focus is upon technological developments.

Leadership Assesses needs of clients, determines growth areas, monitors client satisfaction and provides marketing leadership.

Determines ways of selling what the firm wishes to produce; assesses service quality only from an internal review perspective.

Fee development Determines the best way to price various services in the firm rather than just billing by the hour.

Approaches fee development from a cost-plus perspective.

Practice development program

Based on a strategic analysis of both needs of firm and diverse needs of targeted client segments.

Based on traditional practice development lore and personal preferences.

Use of personal selling Delivery staff regularly assesses clients’needs, And promotes to new clients and prospects service offerings of direct benefit to them.

Reluctance among staff and partners to actively sell services.

The above chart is based on one originally developed by Robert J. Listman, Marketing Accounting Services, Homewood, Illinois: Dow-Jones-Irwin, 1988, p. 22.

17

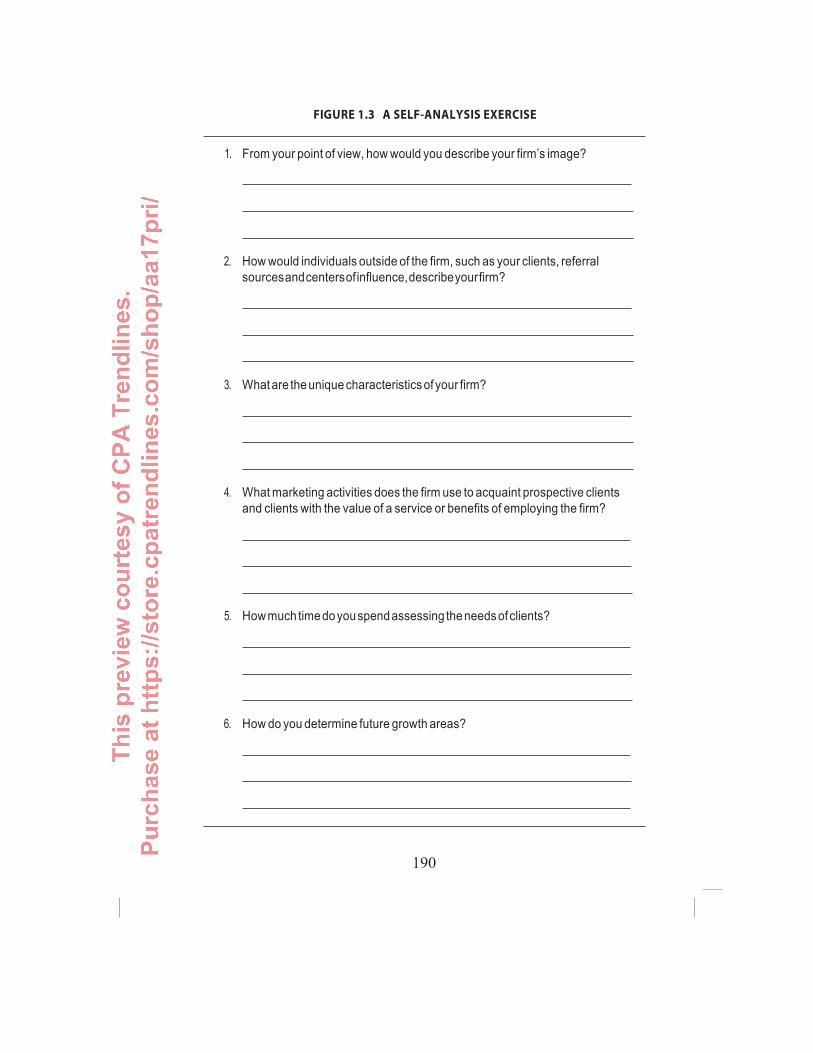

FIGURE 1.3 A SELF-ANALYSIS EXERCISE

1. From your point of view, how would you describe your firm’s image?

2. How would individuals outside of the firm, such as your clients, referralsources and centers of influence, describe your firm?

3. What are the unique characteristics of your firm?

4. What marketing activities does the firm use to acquaint prospective clientsand clients with the value of a service or benefits of employing the firm?

5. How much time do you spend assessing the needs of clients?

6. How do you determine future growth areas?

190

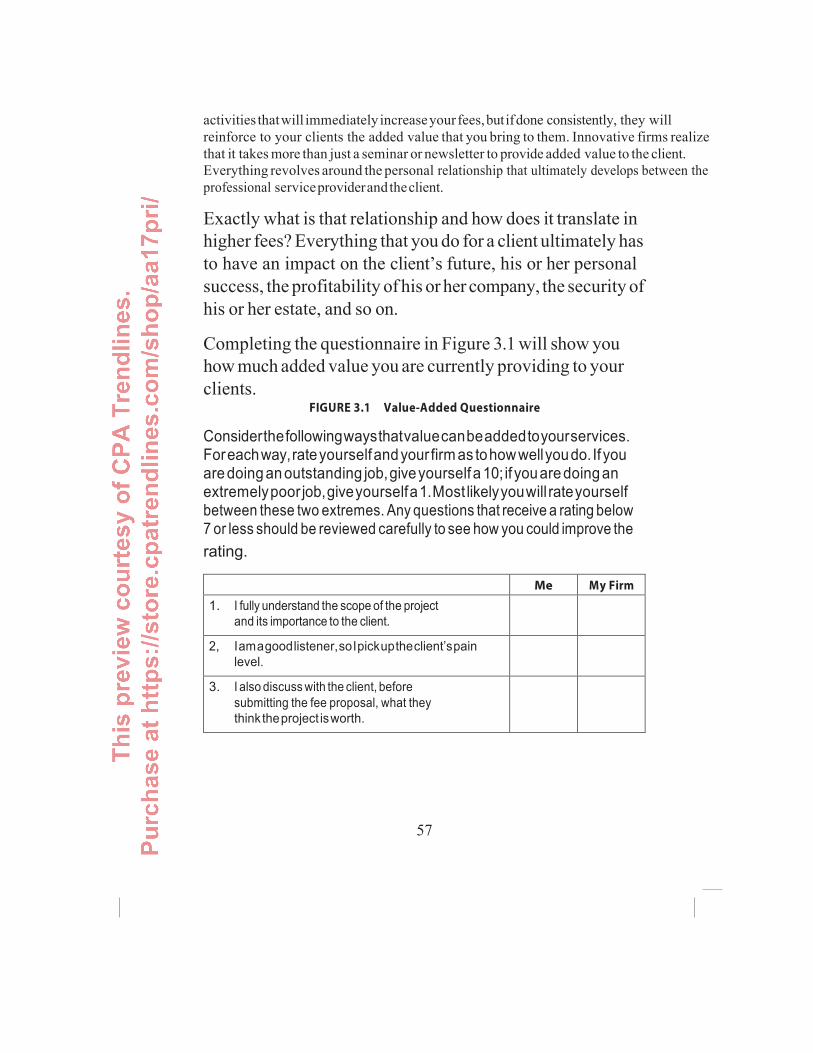

activities that will immediately increase your fees, but if done consistently, they will reinforce to your clients the added value that you bring to them. Innovative firms realize that it takes more than just a seminar or newsletter to provide added value to the client. Everything revolves around the personal relationship that ultimately develops between the professional service provider and the client.

Exactly what is that relationship and how does it translate in higher fees? Everything that you do for a client ultimately has to have an impact on the client’s future, his or her personal success, the profitability of his or her company, the security of his or her estate, and so on.

Completing the questionnaire in Figure 3.1 will show you how much added value you are currently providing to your clients.

FIGURE 3.1 Value-Added Questionnaire

Consider the following ways that value can be added to your services. For each way, rate yourself and your firm as to how well you do. If you are doing an outstanding job, give yourself a 10; if you are doing an extremely poor job, give yourself a 1. Most likely you will rate yourself between these two extremes. Any questions that receive a rating below 7 or less should be reviewed carefully to see how you could improve the rating.

Me My Firm

1. I fully understand the scope of the projectand its importance to the client.

2, I am a good listener, so I pick up the client’s pain level.

3. I also discuss with the client, beforesubmitting the fee proposal, what theythink the project is worth.

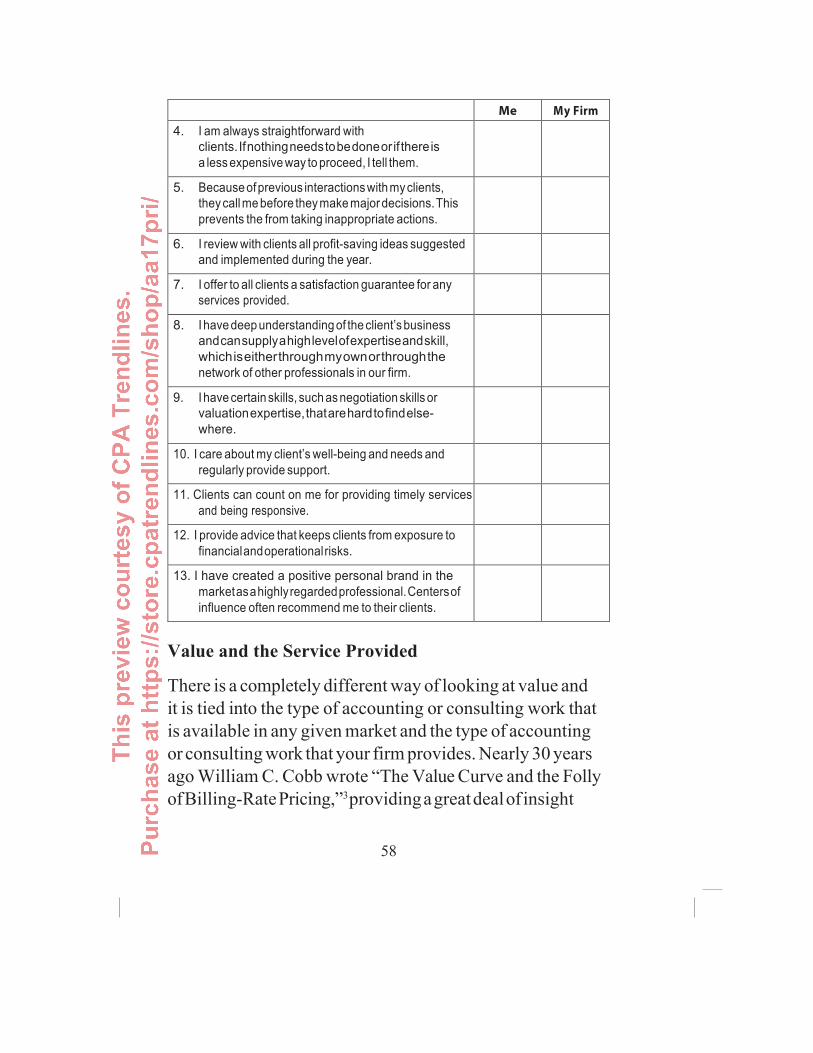

57

Me My Firm

4. I am always straightforward withclients. If nothing needs to be done or if there isa less expensive way to proceed, I tell them.

5. Because of previous interactions with my clients,they call me before they make major decisions. Thisprevents the from taking inappropriate actions.

6. I review with clients all profit-saving ideas suggestedand implemented during the year.

7. I offer to all clients a satisfaction guarantee for anyservices provided.

8. I have deep understanding of the client’s businessand can supply a high level of expertise and skill,which is either through my own or through thenetwork of other professionals in our firm.

9. I have certain skills, such as negotiation skills orvaluation expertise, that are hard to find else- where.

10. I care about my client’s well-being and needs andregularly provide support.

11. Clients can count on me for providing timely servicesand being responsive.

12. I provide advice that keeps clients from exposure tofinancial and operational risks.

13. I have created a positive personal brand in themarket as a highly regarded professional. Centers ofinfluence often recommend me to their clients.

Value and the Service Provided

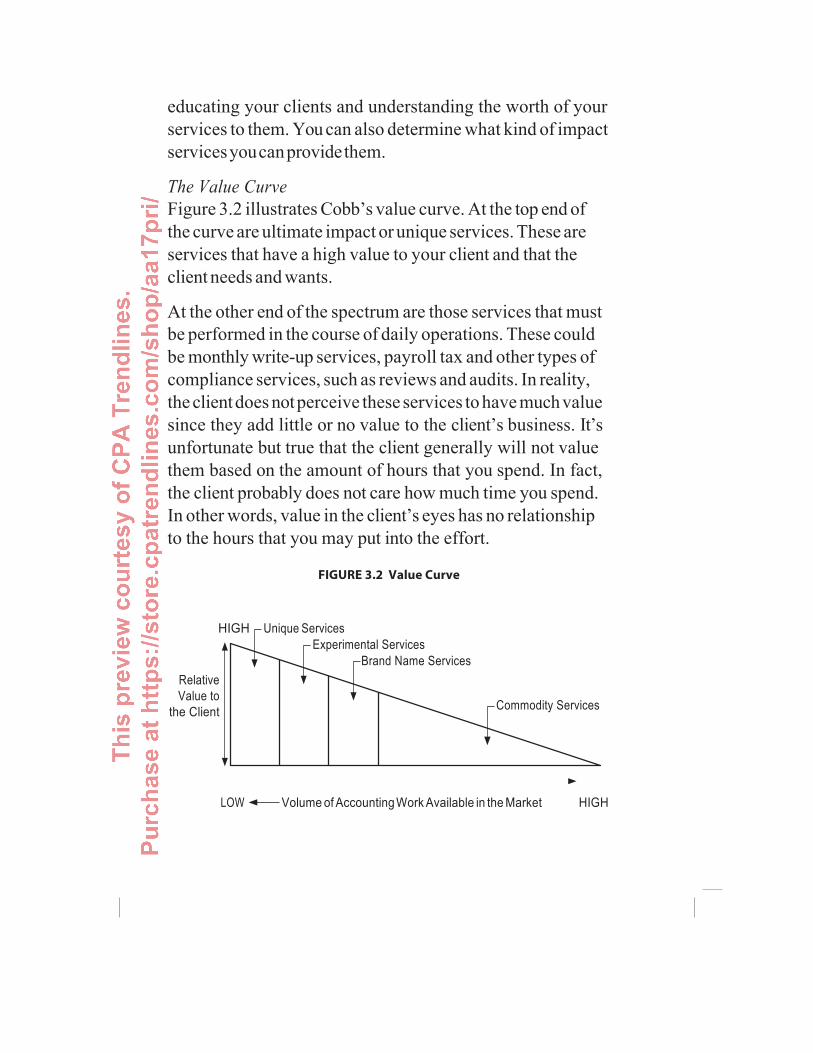

There is a completely different way of looking at value and it is tied into the type of accounting or consulting work that is available in any given market and the type of accounting or consulting work that your firm provides. Nearly 30 years ago William C. Cobb wrote “The Value Curve and the Folly of Billing-Rate Pricing,”3 providing a great deal of insight

58

educating your clients and understanding the worth of your services to them. You can also determine what kind of impact services you can provide them.

The Value Curve Figure 3.2 illustrates Cobb’s value curve. At the top end of the curve are ultimate impact or unique services. These are services that have a high value to your client and that the client needs and wants.

At the other end of the spectrum are those services that must be performed in the course of daily operations. These could be monthly write-up services, payroll tax and other types of compliance services, such as reviews and audits. In reality, the client does not perceive these services to have much value since they add little or no value to the client’s business. It’s unfortunate but true that the client generally will not value them based on the amount of hours that you spend. In fact, the client probably does not care how much time you spend. In other words, value in the client’s eyes has no relationship to the hours that you may put into the effort.

FIGURE 3.2 Value Curve

HIGH Unique Services Experimental Services

Brand Name Services Relative Value to

the Client Commodity Services

LOW Volume of Accounting Work Available in the Market HIGH

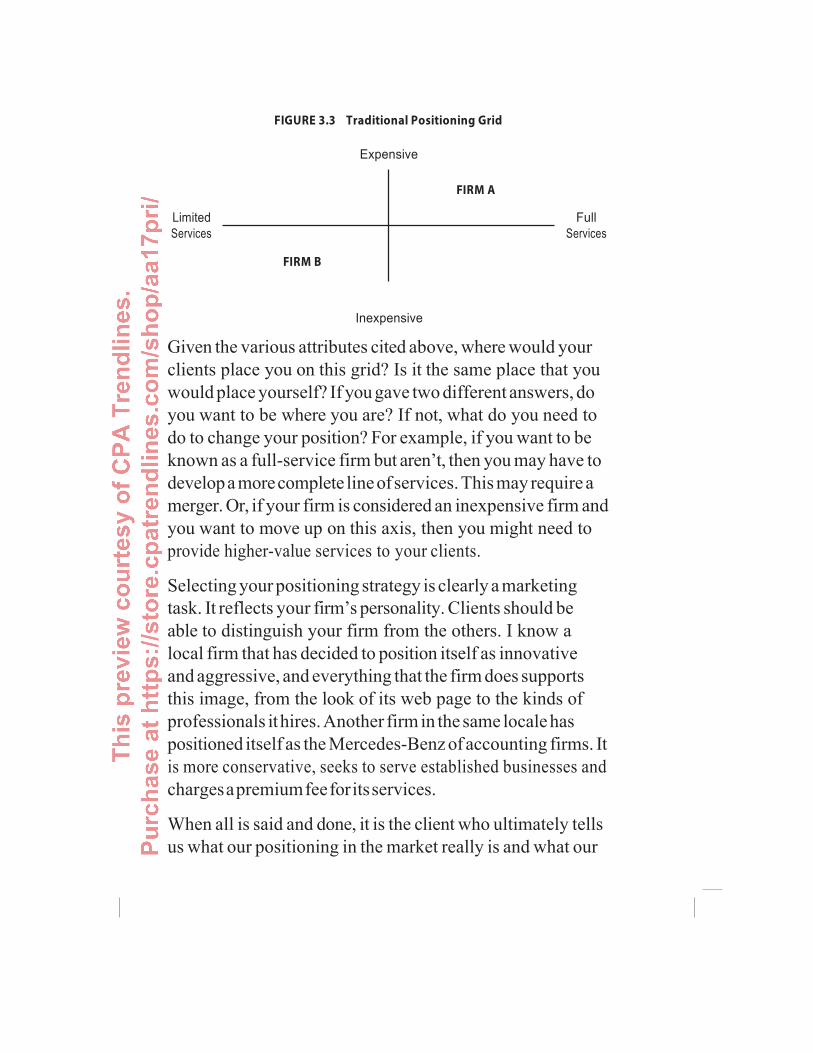

FIGURE 3.3 Traditional Positioning Grid

Expensive

Limited Services

Full Services

Inexpensive

Given the various attributes cited above, where would your clients place you on this grid? Is it the same place that you would place yourself? If you gave two different answers, do you want to be where you are? If not, what do you need to do to change your position? For example, if you want to be known as a full-service firm but aren’t, then you may have to develop a more complete line of services. This may require a merger. Or, if your firm is considered an inexpensive firm and you want to move up on this axis, then you might need to provide higher-value services to your clients.

Selecting your positioning strategy is clearly a marketing task. It reflects your firm’s personality. Clients should be able to distinguish your firm from the others. I know a local firm that has decided to position itself as innovative and aggressive, and everything that the firm does supports this image, from the look of its web page to the kinds of professionals it hires. Another firm in the same locale has positioned itself as the Mercedes-Benz of accounting firms. It is more conservative, seeks to serve established businesses and charges a premium fee for its services.

When all is said and done, it is the client who ultimately tells us what our positioning in the market really is and what our

for these words of wisdom is none other than the AICPA Management of an Accounting Practice Handbook. The Handbook goes on to say that “standard rates should not represent a maximum that can be billed for services; rather they should represent a minimum.”

Our brethren in the legal field have been much better in determining the “reasonableness” of a fee. In determining their fees lawyers usually consider the following 13 factors:

1. The time and labor required2. The novelty and difficulty of the questions involved3. The skill required to perform the service properly4. The fee customarily charged in the locality for similar legal

services5. The monetary amount involved and the results obtained in the

matter6. Awards in similar cases7. The desirability or undesirability of the case8. The experience, reputation and ability of the lawyer performing

the service9. The results obtained10. Whether the fee is fixed or contingent11. Nature and length of the professional relationship with the client12. Time limitations imposed by the client or the circumstances13. Preclusions of other employment due to acceptance of this case

According the AICPA’s MAP Handbook, there are nine subjective factors that can affect an accountant’s fee. Many of them are similar to the preceding 13 factors taken into consideration by attorneys. However, the unfortunate reality is that most accountants ignore these factors because they

77

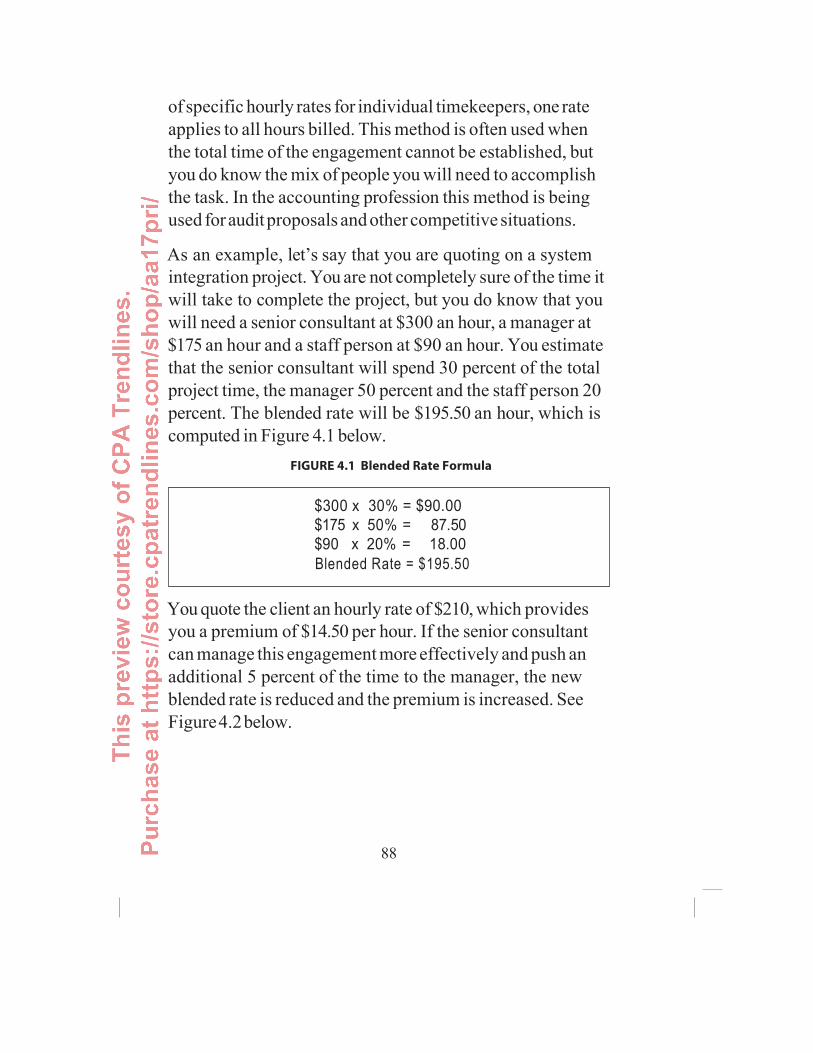

of specific hourly rates for individual timekeepers, one rate applies to all hours billed. This method is often used when the total time of the engagement cannot be established, but you do know the mix of people you will need to accomplish the task. In the accounting profession this method is being used for audit proposals and other competitive situations.

As an example, let’s say that you are quoting on a system integration project. You are not completely sure of the time it will take to complete the project, but you do know that you will need a senior consultant at $300 an hour, a manager at $175 an hour and a staff person at $90 an hour. You estimate that the senior consultant will spend 30 percent of the total project time, the manager 50 percent and the staff person 20 percent. The blended rate will be $195.50 an hour, which is computed in Figure 4.1 below.

FIGURE 4.1 Blended Rate Formula

You quote the client an hourly rate of $210, which provides you a premium of $14.50 per hour. If the senior consultant can manage this engagement more effectively and push an additional 5 percent of the time to the manager, the new blended rate is reduced and the premium is increased. See Figure 4.2 below.

88

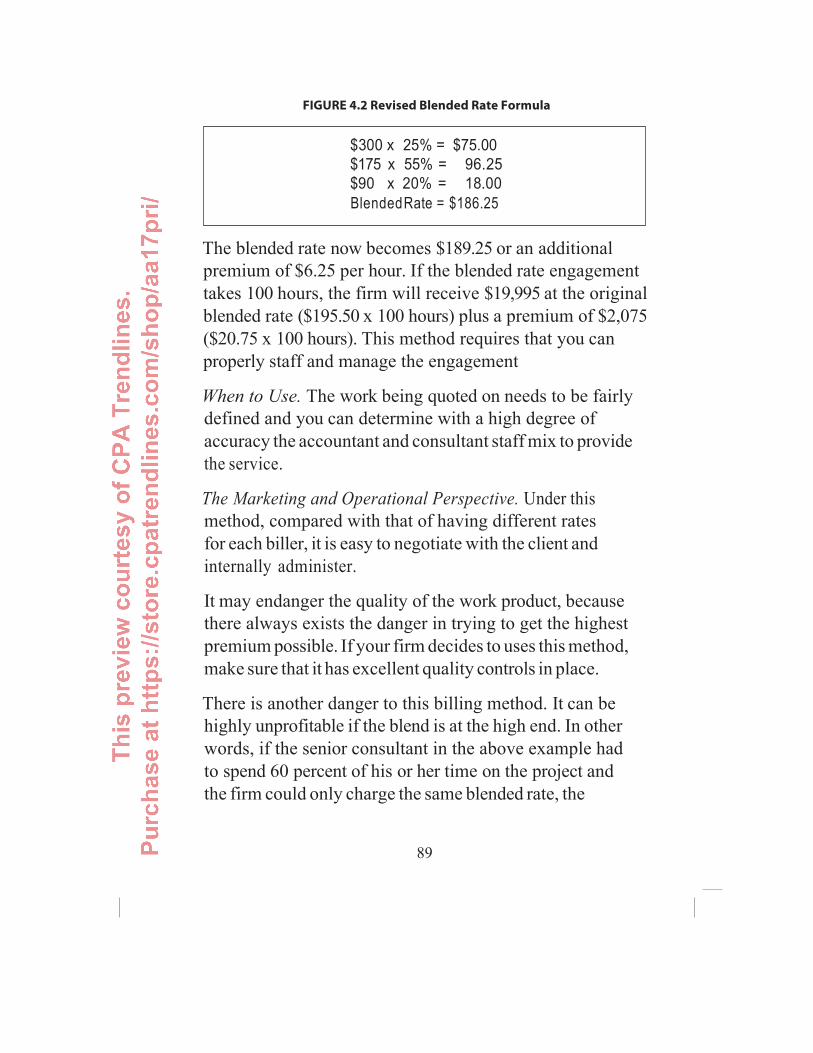

FIGURE 4.2 Revised Blended Rate Formula

The blended rate now becomes $189.25 or an additional premium of $6.25 per hour. If the blended rate engagement takes 100 hours, the firm will receive $19,995 at the original blended rate ($195.50 x 100 hours) plus a premium of $2,075 ($20.75 x 100 hours). This method requires that you can properly staff and manage the engagement

When to Use. The work being quoted on needs to be fairly defined and you can determine with a high degree of accuracy the accountant and consultant staff mix to provide the service.

The Marketing and Operational Perspective. Under this method, compared with that of having different rates for each biller, it is easy to negotiate with the client and internally administer.

It may endanger the quality of the work product, because there always exists the danger in trying to get the highest premium possible. If your firm decides to uses this method, make sure that it has excellent quality controls in place.

There is another danger to this billing method. It can be highly unprofitable if the blend is at the high end. In other words, if the senior consultant in the above example had to spend 60 percent of his or her time on the project and the firm could only charge the same blended rate, the

89

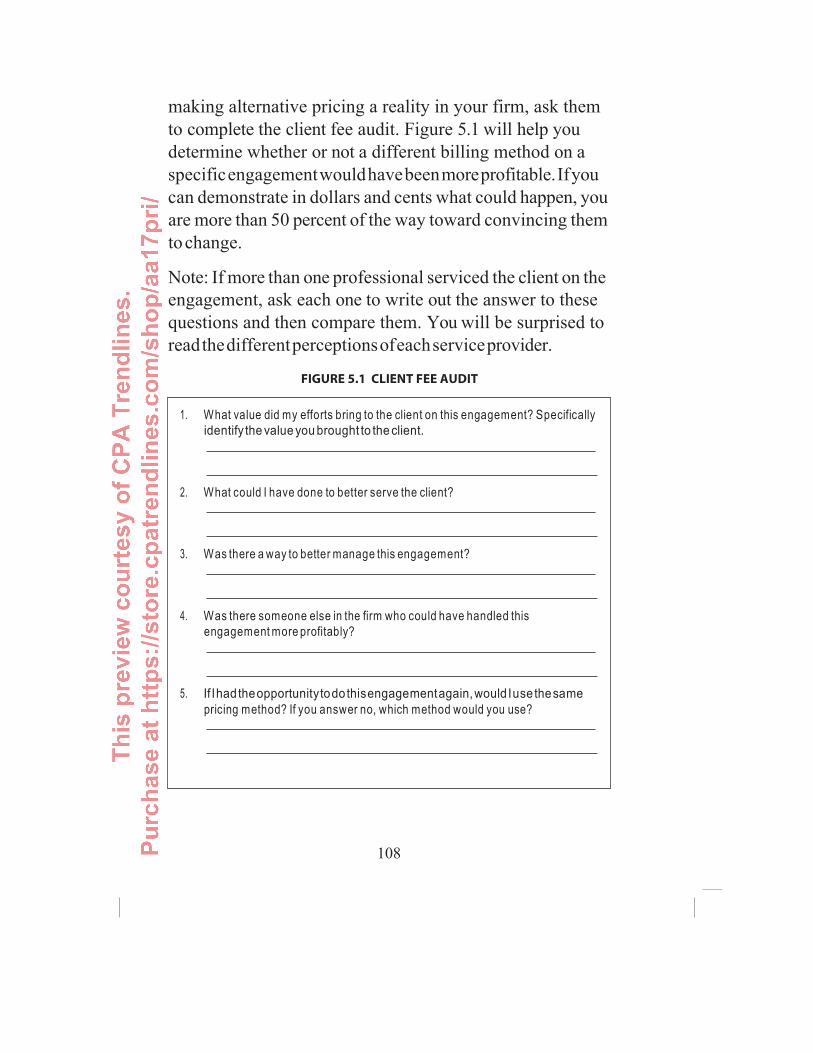

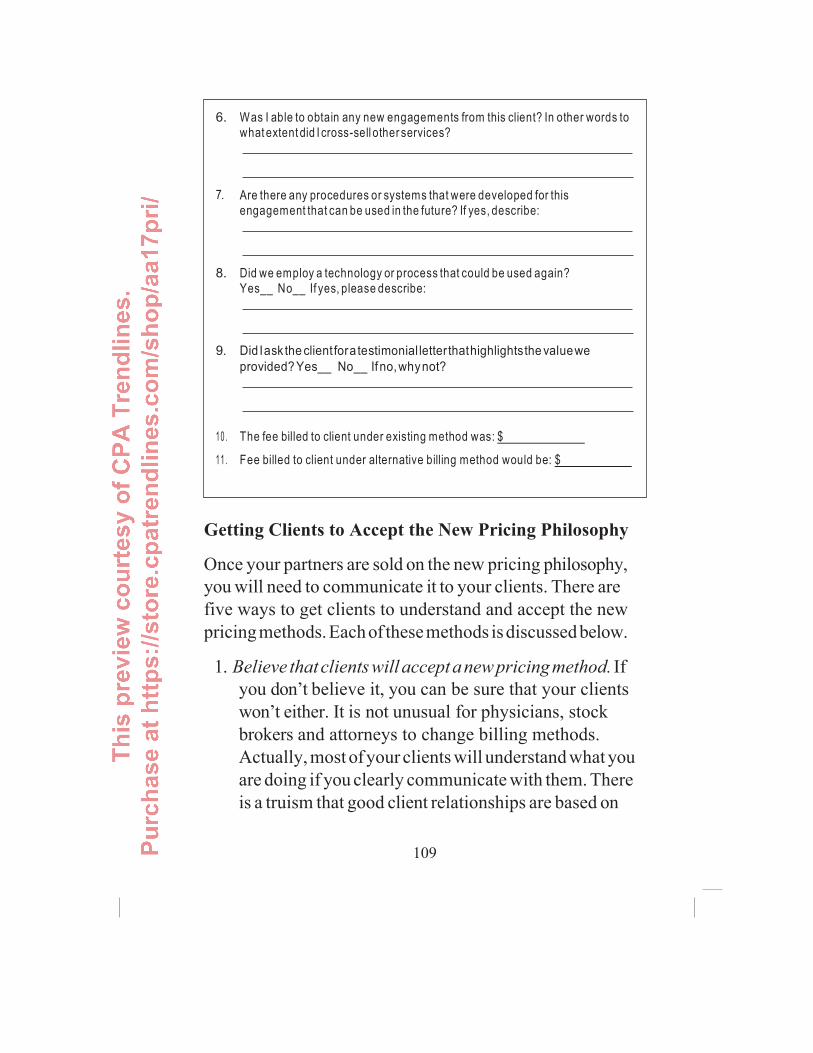

making alternative pricing a reality in your firm, ask them to complete the client fee audit. Figure 5.1 will help you determine whether or not a different billing method on a specific engagement would have been more profitable. If you can demonstrate in dollars and cents what could happen, you are more than 50 percent of the way toward convincing them to change.

Note: If more than one professional serviced the client on the engagement, ask each one to write out the answer to these questions and then compare them. You will be surprised to read the different perceptions of each service provider.

FIGURE 5.1 CLIENT FEE AUDIT

108

Getting Clients to Accept the New Pricing Philosophy

Once your partners are sold on the new pricing philosophy, you will need to communicate it to your clients. There are five ways to get clients to understand and accept the new pricing methods. Each of these methods is discussed below.

1. Believe that clients will accept a new pricing method. Ifyou don’t believe it, you can be sure that your clientswon’t either. It is not unusual for physicians, stockbrokers and attorneys to change billing methods.Actually, most of your clients will understand what youare doing if you clearly communicate with them. Thereis a truism that good client relationships are based on

109

6.

8.

9.

department or a communication consultant to help you.

2. Offer three levels of service. Whether it is a monthlyservice or a one-time project, offer your clients threeoptions. Think of it like the levels that AmericanExpress® offers its card members – green, gold andplatinum.

This is important because it gives your clients theopportunity to determine the perceived value of theservice. The following table provides an example of whatyou would provide a CAS client. Each level of higherservice includes all the services in the lower level.

EXHIBIT 5.1

GREEN SERVICE GOLD SERVICE PLATINUM SERVICE

• Individual tax return• Schedule C• Quarterly financial

statements

• Monthly financialstatements

• Client accountingsoftware installation

• Cloud-based support• Compilation• Two 15-minute calls

per month

• Individual family taxreturns

• Small business taxreturns

• Monthly andquarterly financialstatements

• Client accountingsoftware updates

• Business planningassistance

• Cloud-based support• Review or audit• Up to six calls per

month

$ Monthly Fee $$ Monthly Fee $$$ Monthly Fee

3. Create these levels of service for all of your compliance andconsulting services. Once this is done you can start to

114

lose your professional liability coverage completely. As much as 13 percent of all malpractice claims come from counterclaims against CPAs.

Some firms are getting around the legal issues by taking their clients to small claims court. Do not threaten to take a client to court unless you really are going to do it. A workable policy might be: After two or three broken promises to pay, notify the client that you will be filing in small claims court within 72 hours unless payment is received.

15. Bill for out-of-pocket expenses. Many firms do not chargeback to their clients the expenses incurred in servicingof their account. The term out-of-pocket expenses hascome to cover a large array of items. It is not unusual forfirms to bill clients for:• Technology charges• Local and long-distance telephone charges• Administrative support time• Computer processing time• Messenger services• Photocopying charges• Per-page charges for typed documents• New client and engagement set-up charges

Rather than having a separate charge for each of the above items, many firms just add a fixed amount per billable hour for overhead expenses. Clients do not like to be nickel and dimed for every little expense. However, the total amount of these charges can be significant.

127

About the Author

August Aquila is the founder and CEO of AQUILA Global Advisors, LLC and is a key thought leader for professional service firms (PSFs). He has worked with various types of PSFs in the US, Canada, India and England.

August brings a wealth of hands-on experience to his clients and presentations. He was a partner in a Top 50 US CPA firm and a senior executive with American Express Tax & Business Services, Inc. For 27 years he has advised PSFs in the areas of succession planning, mergers and acquisitions, compensation plan designs and partnership issues.

In 2004, 2007, 2009 to 2016 he was selected as one of the “Top 100 Most Influential People in The Accounting Profession” by Accounting Today. His articles have appeared in MP (Managing Partner), Journal of Accountancy, CA Magazine, Accounting Today, Of Counsel and other major publications.

Recent books include How to Become the Firm of Choice; What Makes a Great Partnership; How to Engage Partners in the Firm’s Future; Client at the Core: Marketing and Managing Today’s Professional Services Firm; Performance Is Everything – The Why, What and How of Designing Compensation Plans;Compensation as a Strategic Asset: The New Paradigm; andWhat Successful Managing Partner Do.

135

August holds an MBA from DePaul University (Chicago) and a PhD from Indiana University (Bloomington). August lives in Minnetonka, Minnesota, with his wife, Emily. When not working, August enjoys biking, traveling and gardening.

August J. Aquila, PhD Aquila Global Advisors, LLC 4732 Chantrey Place Minnetonka, MN 55345

[email protected] www.aquilaadvisors.com 952-930-1295

136

About CPA Trendlines

Price It Right: How to Value Accounting Services is published by CPA Trendlines, an imprint of Bay Street Group LLC.

CPA Trendlines provides actionable intelligence to help tax, accounting and finance professionals advance their firms and their careers at http://cpatrendlines.com

Join CPA Trendlines as a PRO Member

Get full site-wide access to exclusive content, insights and research, plus join a community of forward-thinking colleagues and get great offers and discounts on other CPA Trendlines products and services, GoProCPA.com

Find more products and services like this from CPA Trendlines at store.cpatrendlines.com

• What Really Makes CPA Firms Profitable?• The Rosenberg MAP Survey: The Leading Annual

National Study of CPA Firm Statistics• The CPA Trendlines Succession Institute• The CPA Trendlines Pathfinder Series for Practice

Owners• The Client Service Idea Book• Accountant’s Accelerator• The Accountant’s (Bad) Joke Book• The 90-Day Marketing Plan for CPA Firms• The 30:30 Training Method

137

• Tax Season Opportunity Guide• Strategic Planning and Goal Setting for Results• Sponsoring Women: What Men Need to Know• Quantum of Paperless: The Partners Guide to

Accounting Firm Optimization• Professional Services Marketing 3.0• Passport to Partnership• Leadership at its Strongest• Implementing Fee Increases• How to Review Tax Returns• How to Operate a Compensation Committee• How to Engage Partners in the Firm’s Future• How to Create the Roadmap for Your Firm’s Growth• How to Bring in New Partners• How CPA Firms Work: The Business of Public

Accounting• Guide to Planning the Firm Retreat• Effective Partner Relations and Communications• Creating the Effective Partnership: Two-Volume

Package• CPA Firm Succession Planning: A Perfect Storm• CPA Firm Partner Retirement / Buyout Plans• CPA Firm Mergers: Your Complete Guide CPA Firm

Management & Governance• Accounting Marketing 101 Partners• Accounting Firm Operations and Technology Survey• 101 Questions and Answers: Managing an Accounting

Practice138