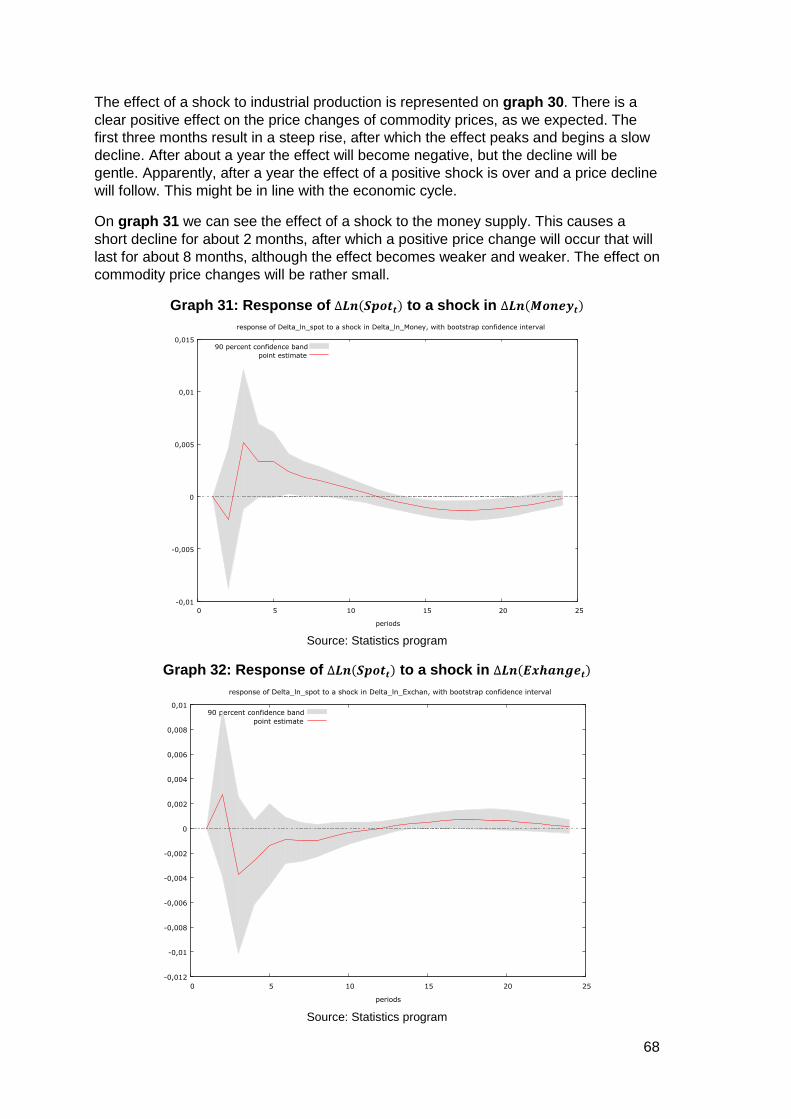

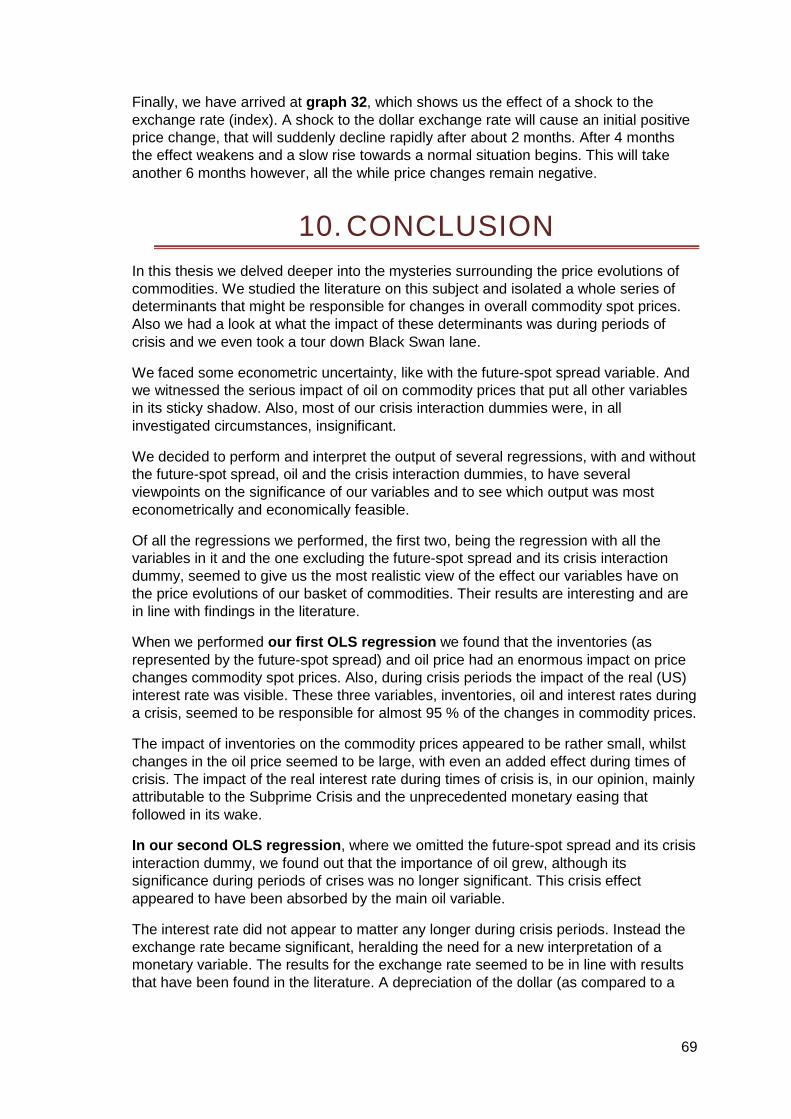

Price evolutions on the commodity markets.

77

Departement Handelswetenschappen en Bestuurskunde Masterproef PRICE EVOLUTIONS ON THE COMMODITY MARKETS: DETERMINANTS IN NORMAL AND CRISIS PERIODS Tim De Smedt Master Handelswetenschappen Afstudeerrichting Finance and Risk Management Promotor: Dr. Koen Inghelbrecht Academiejaar 2010-11

Transcript of Price evolutions on the commodity markets.

Departement Handelswetenschappen en Bestuurskunde

Masterproef

PRICE EVOLUTIONS ON THE COMMODITY MARKETS:

DETERMINANTS IN NORMAL AND CRISIS PERIODS

Tim De Smedt

Master Handelswetenschappen

Afstudeerrichting Finance and Risk Management

Promotor: Dr. Koen Inghelbrecht

Academiejaar 2010-11

1

2

PRICE EVOLUTIONS ON THE COMMODITY MARKETS:

DETERMINANTS IN NORMAL AND CRISIS PERIODS

MASTER THESIS

Academic Year 2010-2011

Author: Tim De Smedt

Promotor: Koen Inghelbrecht, PhD

3

4

ABSTRACT

Through a univariate OLS model, we investigate which variables are responsible for price evolutions in commodity spot prices. The variables we investigated were: the future-spot spread (proxy for inventories), oil price (to measure spill-over effects), expected inflation, real interest rate, dollar exchange rate, industrial production, money supply, a crisis dummy and a Black Swan dummy. For all these independent variables (excluding the crisis and black swan dummy), we also added a crisis interaction dummy to measure their effect in times of crisis. Our regression outputs (we performed several) showed us that the future-spot spread, oil, interest rates during a crisis and the exchange rate were responsible for most of the price changes in commodity prices. A multivariate VAR model showed us that changes in commodity prices are Granger Caused by lags of itself and changes in industrial production. We also determined the presence of an industrial production channel through which monetary variables influence the prices of commodities. Impulse responses showed us the impact of exogenous shocks given to the independent variables. In most cases the effect disappears after 1 year.

PRELUDE

This master thesis is written in English, as you, most cautious reader already might have noticed. This is done for two reasons.

Firstly, most of scientific literature these days is written in English. I find it not more than normal, that in our modern society and school system a thesis that is deemed (and urged) to be of a certain scientific level is written in English as well.

Furthermore, a thesis in English might open some doors for me in the future should I opt for a career abroad. The fact that it is already written in English saves me the burden of translating it from Dutch to English should the need arise.

I would like to apologize to the reader for the size of this work. It has become a bit larger than I had originally anticipated, but I wanted to deliver a thesis that was as complete as possible.

Furthermore, the research process kept providing me with more and more exiting results, which I couldn’t exclude. Even now I feel that despite its massive size, there are still many questions unanswered in regard to the studied subject.

To end this prelude I would like to thank my promoter, Koen Inghelbrecht, PhD, for his support, guidance and comments on earlier versions of this master thesis. This thesis wouldn’t have been what it is today without your help.

I hope that you, dear reader, enjoy reading this work as much as I enjoyed writing it.

Kind regards,

Tim De Smedt

Buggenhout, May 22, 2011.

5

6

CONTENTS

1. Introduction ........................................................................................................... 8

2. Basic concepts .................................................................................................... 10

2.1 Definition ...................................................................................................... 10

2.2 Commodity Markets ..................................................................................... 10

2.2.1 The spot market .................................................................................... 11

2.2.2 The forward market ............................................................................... 11

2.2.3 The futures market ................................................................................ 11

2.3 The term structure of commodity futures ...................................................... 12

2.4 Commodity futures return ............................................................................. 14

2.5 Commodity Indices ....................................................................................... 15

3. Literature overview .............................................................................................. 17

3.1 Price evolutions of commodities and its determinants .................................. 17

3.2 Crisis periods and Black Swans ................................................................... 21

3.3 The financialization of commodity Markets ................................................... 22

4. Research questions and Methodology ................................................................. 25

5. The variables ....................................................................................................... 26

5.1 Commodity Prices ........................................................................................ 26

5.2 Inventories ................................................................................................... 27

5.3 US Money Supply ........................................................................................ 31

5.4 Expected Inflation ......................................................................................... 31

5.5 Real Interest Rates ...................................................................................... 33

5.6 Industrial Production..................................................................................... 34

5.7 Spill-over Effects .......................................................................................... 35

5.8 The Dollar Exchange Rate ........................................................................... 36

5.9 Crisis events ................................................................................................ 37

5.10 Black Swan Events ...................................................................................... 38

5.11 Summary ...................................................................................................... 38

6. The Model ........................................................................................................... 39

6.1 The Basic Model .......................................................................................... 39

6.2 Transformations ........................................................................................... 39

6.2.1 Logaritms .............................................................................................. 39

6.2.2 First Differences (Unit Root Testing) ..................................................... 40

6.2.3 Co-integration relations ......................................................................... 42

6.3 The Final Model ........................................................................................... 43

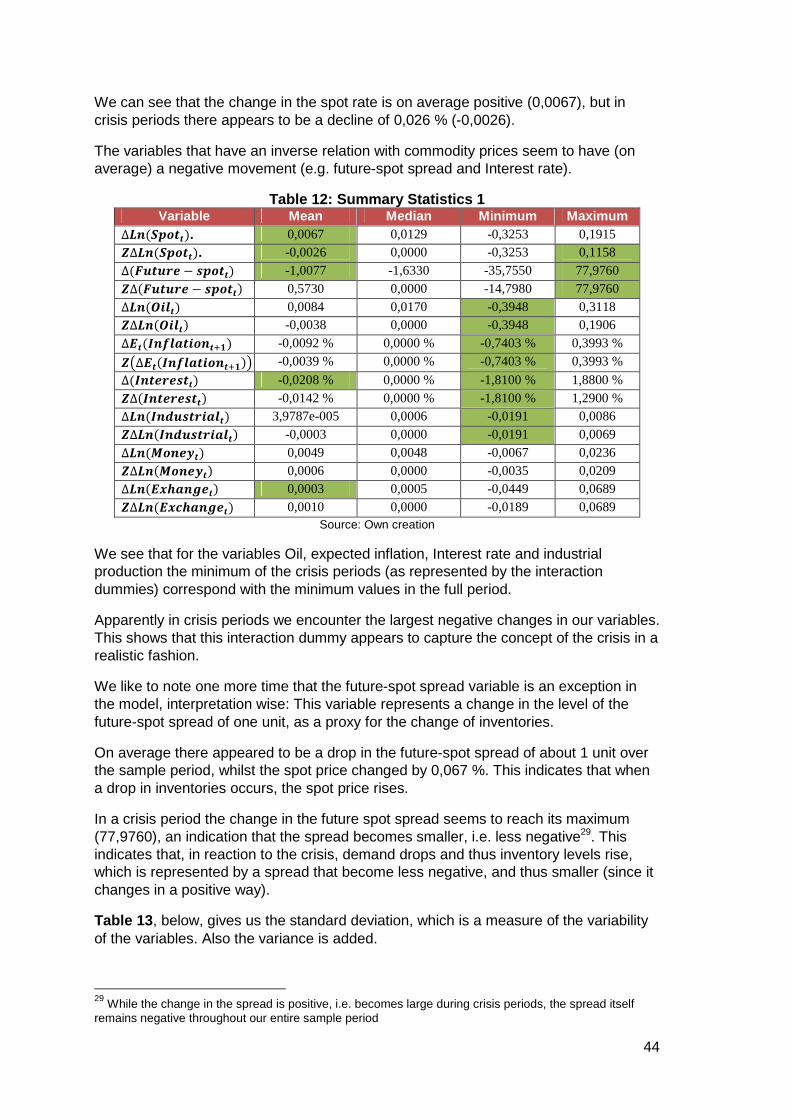

6.4 Descriptive Statistics .................................................................................... 43

6.4.1 Summary Statistics ............................................................................... 43

7

6.4.2 XY-Plots and Correlation ........................................................................45

7. The univariate model: OLS-regression .................................................................52

7.1 OLS-regressions and tests ............................................................................52

7.2 Prelude: OLS on levels..................................................................................52

7.3 Basic regression: first differences ..................................................................53

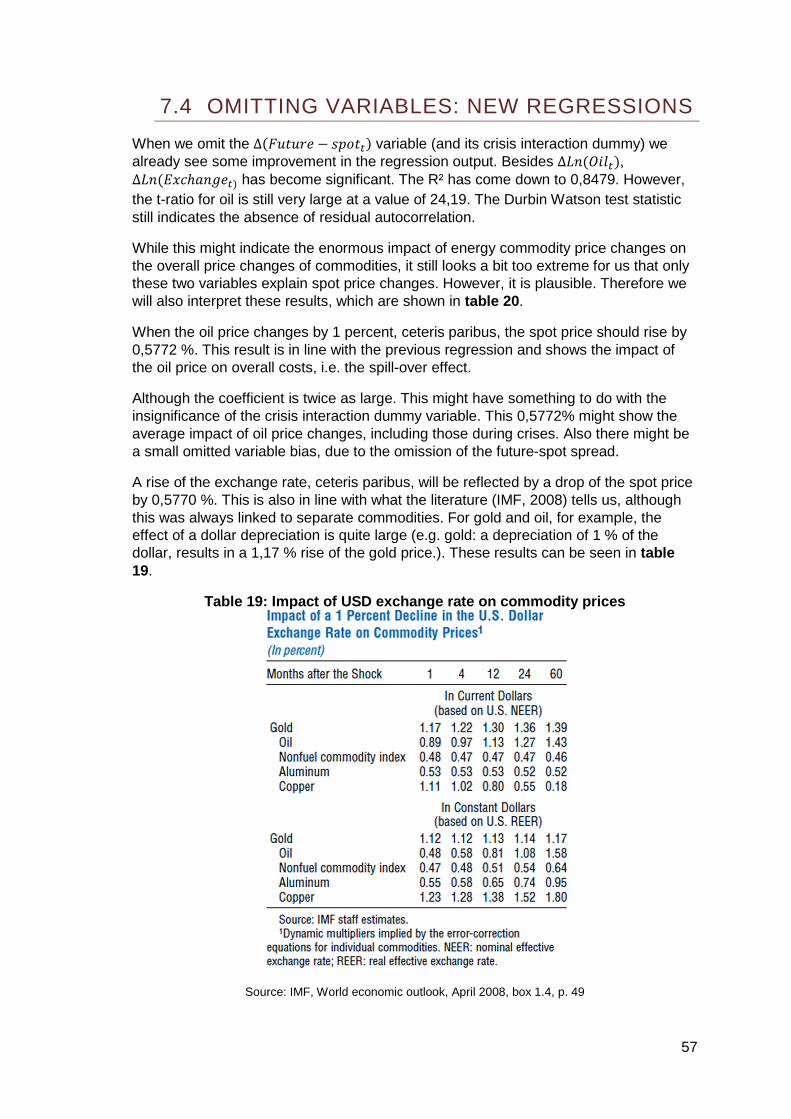

7.4 Omitting variables: new regressions ..............................................................57

7.5 A Final OLS regression .................................................................................59

7.6 Aside on lagged variables .............................................................................61

7.7 Choosing the right model ..............................................................................61

8. The multivariate Model: VAR ................................................................................61

8.1 Vector Autoregression ...................................................................................61

8.2 Lag selection .................................................................................................62

8.3 The Model .....................................................................................................62

8.3.1 The Equation ..........................................................................................62

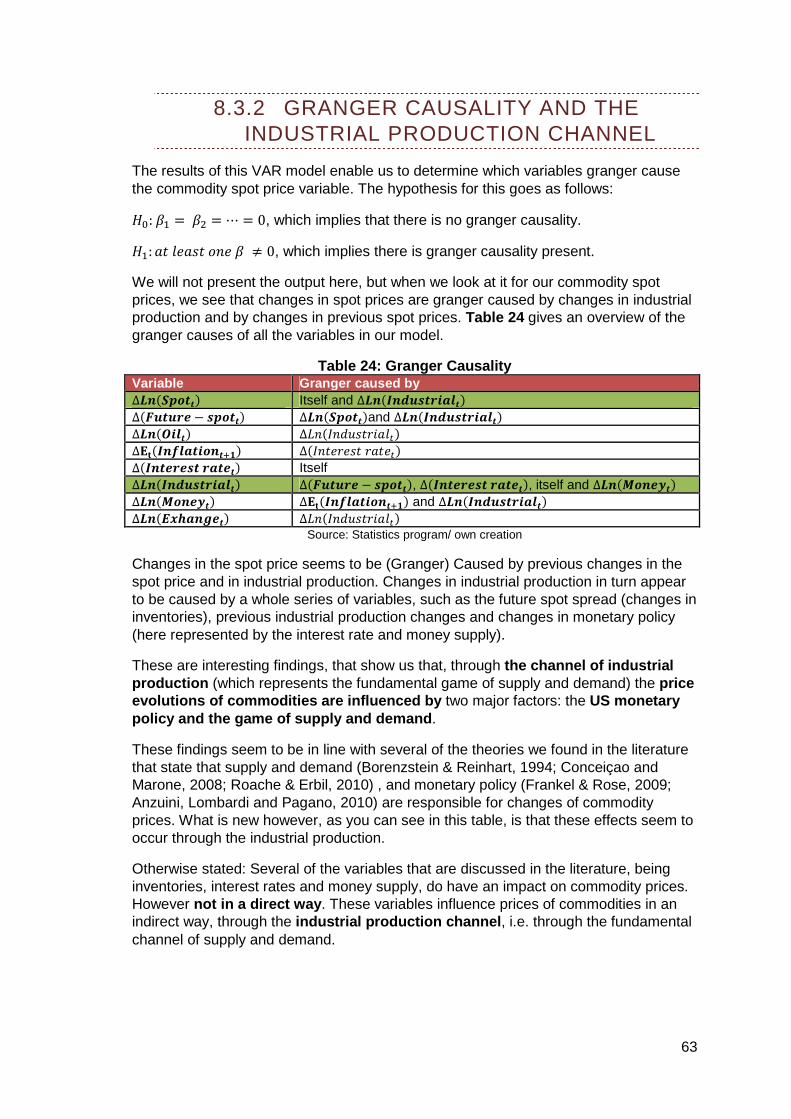

8.3.2 Granger Causality and the Industrial Production Channel .........63

9. Impulse responses ...............................................................................................64

10. Conclusion ........................................................................................................69

11. Overview of Tables, Graphs and figures ...........................................................72

11.1 Graphs ..........................................................................................................72

11.2 Tables ...........................................................................................................73

11.3 Figures ..........................................................................................................73

12. Bibliography ......................................................................................................74

Websites ..................................................................................................................74

Non-Scientific Sources.............................................................................................74

Scientific Sources ....................................................................................................75

Books ...................................................................................................................75

Papers..................................................................................................................75

Scientific Journals ................................................................................................76

8

1. INTRODUCTION Commodities are everywhere. You hear about oil and gold rising to levels never heard of. You see the price of copper rising to such levels that stealing it becomes a very lucrative business. You taste the bitterness of the silver price dropping more than 20 % in one week. Commodities have reached unprecedented highs and scaring depths in the last few years. And they are everywhere…

But what are they exactly? How are they priced? By which factors are they influenced? Now that commodities are available as an alternative source to invest hard earned savings in, we deem it necessary to know which variables are responsible for the price evolutions on the commodity markets. This in order to, at least, shed some light onto the shiny grains of gold, drops of oil or wires of copper we put our money in.

In the literature, as we shall see, there are different paths followed. Researchers focus on the fundamentals (supply and demand) or on the impact monetary policy has on the prices of commodities, sometimes even in regime shifting environments. Or they focus on the impact oil has on other commodities.

The impact of inventories on prices is examined and the role of speculation is looked into. Research involves the study of booms and busts in commodities, over several periods of time, and looks into the role of futures.

All this research, however, often focused just on a single commodity, or a certain subclass. Only rarely a more general approach was taken by looking at a whole basket of commodities (through the use of an index). Also the number of variables researchers put into their models was limited. We also found that the literature involving the impact of crisis periods on commodity prices was rather rare.

These shortcomings we will try to overcome, by using a general model, which incorporates a large(r) amount of variables, whilst also looking into the impact a crisis might have on the prices of commodities. We combine the variables that were used throughout several research paths in the literature into one single model. And while we are at it, we add some interesting new variables as well, like a proxy for inventories and a Black Swan dummy.

Now we know the questions we pose ourselves. We had a glimpse on previous research and on the approach we will take to find some answers. Let us now look at the path we will follow in order to find those answers.

First, we will go over some basic concepts , in order to be able to understand the very nature of the commodities we are investigating. Once some definitions are known, and some insight is gained into the term structure of commodities we move on.

We will give an overview of the scientific literature that we have found. We will look at what authors have written about the price evolutions of commodities and its determinants. We show some things about crisis periods and Black Swans. And we will talk about the financialization of the commodity markets, better known by the dreaded word: Speculation.

Once we dug through all this literature we present you the research questions and the tools we will use to find an answer to these questions.

9

After that, we will introduce the variables . These are the determinants we believe to be responsible for the price evolutions on the commodity markets.

Now that we have knowledge of the scientific literature, stated our research question and introduced the variables it is time to create an econometric model . This is not done in 1-2-3, but requires some transformations in order to make our variables econometrically feasible.

Once that task is complete, we go over some descriptive statistics , in order to get a first glimpse of the impact our select club of variables has on the evolutions of commodity prices.

Then we move on to our univariate model and we perform several OLS regressions in order to find out which determinants are really responsible for price evolutions of commodities.

Once we have a suitable answer on our main question, we move on to our multivariate VAR model . With this model, we will try to determine which variables cause the price evolutions, and we will have a look at the impact exogenous shocks given to the independent variables have on the dependent variable.

This thesis then ends with a conclusion , where we give an overview of our results and try to give some advice to policy makers, investors and future researchers.

10

2. BASIC CONCEPTS

In this chapter we will present some definitions and concepts that are in our opinion necessary for a good understanding of this thesis.

2.1 DEFINITION

A commodity can be defined as a homogeneous base product , a raw (unprocessed) or already processed material, which is used as an input in the production of other goods (or services). These base products are traded on the commodity markets (e.g. London Metal Exchange, Chicago Mercantile Exchange) and are subjected to strict quality standards, known as the base grade .

This base grade is the minimum acceptable quality standard a commodity must have in order to be eligible for trade on a commodity market. The goal of this quality standard is to ensure uniformity (and thus a minimal quality) of the exchanged commodities1.

Furthermore, commodities can be divided in a series of subclasses, based on their properties. We can put most commodities in the following 4 classes (Coenraets, 2006):

• Industrial Metals : These are metals used in industrial production and can in turn be divided into two subclasses:

o Ferro Metals : Iron and all alloys based on iron (like steel). o Non-Ferro Metals : Metals that aren’t based on iron (such as zinc).

• Soft Commodities : This are the commodities that aren’t mined, but are grown (or bred). Here it is also possible to divide this class into two subclasses:

o Agricultural Commodities : This are the raw materials that are grown, like coffee and sugar.

o Livestock : Animals, used in the food industry (e.g. hogs). • Energy Commodities : This are materials required to generate energy, like oil. • Precious Metals : In theory, these are part of the non-Ferro metals. But since

they are usable as an investment tool on their own, they get their own class

2.2 COMMODITY MARKETS

Commodities can be traded by using 3 types of contracts, which also represent 3 types of markets. We have the spot market, forward market and the futures market (Dubofsky and Miller, 2002).

The transactions on the spot and futures market occur on commodity exchanges. This is a more secure place to trade than the over the counter (OTC) derivative market, where forwards are traded. This because of the clearing house of a commodity exchange which guarantees that settlements between parties occur, whilst on the OTC market such an institution does not exist.

Forward contracts are not traded on an exchange due to their nature of being tailored to the needs of the parties that created the contract. And because they are strictly bilateral contracts, their liquidity is too low for them to be allowed on an exchange (because that wouldn’t be cost-effective).

1http://www.economist.com/research/economics/searchActionTerms.cfm?query=commodity – 26/02/2011

11

2.2.1 THE SPOT MARKET

The spot market is the market where commodities are paid and delivered within 2 days after the sale takes place. Contracts on this market are executed immediately (“on the spot”).The spot market is also referred to as the “cash market”, since transactions are settled in cash at the price that is valid at the moment of the trade. This price is called the spot price2.

Also futures with delivery within a month are traded at the spot price. Trading of these contracts ,however, still occurs on the futures market.

2.2.2 THE FORWARD MARKET

A forward contract is a financial contract that gives the owner the right and obligation to buy a specified commodity on a certain date at a predetermined price. The seller of the forward contract, on the other hand, has the right and obligation to sell the commodity on the predetermined date at the agreed price. At the end of the contract the commodity is delivered and payment will occur. The maturity of a forward contract varies from a period of 3 days to 5 years.

Forward contracts are traded over-the-counter (OTC) , which means they are privately negotiated between the buyer and seller and are often tailored to the specific needs of the parties, like for example to hedge against a specific risk. A consequence of this customization is that these contracts are not easily traded, thus liquidity is very low.

Payments are only done at the time of execution of the contract, but it might be possible that the dealers of forward contracts require collateral. This collateral is an insurance against the possibility that the counterparty will default (Dubofsky and Miller, 2002).

This counterparty risk is inherent to the forward market (which is an OTC derivative market), since there is no such thing as a clearinghouse or frequent trade of forward contracts (liquidity of the market). A possible other solution against this counterparty risk is the creation of a CCP, a central clearing party, that works like a clearinghouse does on a regular exchange3.

2.2.3 THE FUTURES MARKET

A future is a financial contract that gives the owner the right and obligation to buy a commodity on a certain date at a predetermined price. The seller of the future contract has the right and obligation to sell the commodity on the predetermined date at the agreed price. At the end of the contract the commodity is delivered and payment will occur. The maturity of a future contract varies from a period of 3 days to 5 years.

As you can see, a future is similar to a forward contract, except for the following differences. First of all, futures are standardized contracts , which means that they are more liquid than forwards.

2 http://www.economist.com/research/economics/searchActionTerms.cfm?query=spot+market – 27/02/2011 3 The discussion about the necessity of a CCP falls beyond the scope of this thesis. For more information on this subject, see: OTC derivatives and post- trading infra structures, ECB Eurosystem, September 2009

12

Secondly, because of this increased liquidity, futures are traded on exchanges , which in turn lowers the counterparty risk (the clearinghouse of the exchange guarantees payment).

Finally, futures contracts are marked to market , which means that are resettled on a daily basis (Dubofsky and Miller, 2002). These daily changes in the contract price also lowers the risk, because the parties can see how the price evolves. The following table gives a clear overview of the differences between forwards and futures.

Table 1: Differences between forwards and futures Forwards Futures

Private contract between 2 parties Exchange traded Customized contract (tailored) Standard contract

1 specified delivery date Range of delivery dates Settled at maturity Settled daily

Delivery or final cash settlement usually occurs

Contract usually closed out prior to maturity

Source: Fundamentals of futures and options markets, John C. Hull, fourth edition, 2001.

The price of a future will on one hand be determined by the supply and demand for it, and on the other hand by price of the underlying commodity where it is derived from. Eventually though, the price of a future is based on the expectations of the various trading parties. So a future gives an indication of the expected price of a commodity.

In reality, future contracts will seldom be exercised when they come to maturity. This happens, because at the closing of the futures contract it wasn’t the intention of the seller of the contract to actually deliver the goods. Also the buyer of a future never had the intention to actually buy the commodities, but to hedge against the risk of price changes of this specific commodity (or to speculate on them).

The position of the futures contract is offset by taking an opposite position in the same contract type. The buyer of the future sells it back at the seller before the future comes to maturity. Profits or losses are settled in cash at the end of the contract, so there is no exchange of the underlying commodity (De Standaard, 2005).

In some cases a party might want to hold a position in futures for a longer period than the actual maturity of that futures contract (for example 3 month futures). In this case, the owner of the future needs to sell it, just before it reaches its maturity, and then buy a new future (again a 3 month future) which has the same underlying commodity, but a later expiration date. This transaction is called a future roll , because the future is rolled over to a later maturity date.

2.3 THE TERM STRUCTURE OF COMMODITY FUTURES

When we look at the behavior of the prices of commodity futures, as compared to the spot prices of those commodities, there are 2 possible term structures: Backwardation and contango.

When the spot price is higher than the future price with maturity in three months, and this futures price in turn lies higher than the future price with maturity in six months, then we are in a situation which is called backwardation . In this case there is a negative futures curve.

13

This represents the premium a commodity buyer is willing to pay in order to get immediate delivery of a commodity (De Standaard, 2005). On the other side, the seller of a commodity is willing to accept a future price that is lower than the spot price in exchange for the certainty that his commodity will get sold at the predetermined price, i.e. he hedges against changes in the spot price (KBC Securities, November 2010).

When we have backwardation, this means that the current demand for a certain commodity is larger than the demand that is expected in the future. Because of this higher demand in the present, the spot price (the present price) will be higher than the futures price. A market with backwardation gives a signal that traders expect a decline in demand, and thus in prices.

When contango occurs, the spot price will be lower than the futures price. Contango is de facto the opposite of backwardation, and is represented by a positive futures curve. In this case the market expects an excess of supply, or there happens a sudden (unexpected) decline in demand, which causes the spot price to fall. Also, the higher future price incorporates costs for storage, transportation and insurance of the commodities.

When the market is in contango, market parties expect prices to rise in the future (Coenraets, 2006). This is the normal situation on the commodity markets.

The following graph shows the term structure of two commodity futures. On the left hand scale the gold futures are in a state of contango, whilst on the right hand scale the copper futures are in a state of backwardation. The graph clearly shows that these two term structures are opposites of each other.

Graph 1: The term structure of commodity futures

Source: I want to break free or, Strategic Asset Allocation ≠ Static Asset Allocation, GMO, James Montier, May 2010, p.10

14

2.4 COMMODITY FUTURES RETURN

The return of investments in commodity futures has four distinctive components: The spot return, the collateral return, the recomposition yield and the roll yield.

The spot return is the change in the spot price of the underlying commodity between the moment of purchase and the moment the future is sold again.

When agents invest in commodities, they take precautions against possible losses. These precautions come in the form of collateral that these investors set aside as a margin. The collateral return is the return they earn on this collateral (UNCTAD, 2009). This is also referred to as the cash return (KBC Securities, November 2010), since the collateral comes in the form of cash, which is then invested on the money market (and thus generates an extra return this way).

Another part of the return of investing in commodities is the recomposition yield . This yield arises from a periodic redefinition of the basket of commodities that is part of an investment portfolio (UNCTAD, 2009).

The roll yield is the return investors get when the future is rolled over into another future with a later date of maturity. If the term structure knows a negative slope (backwardation), thus when the price of a future that reaches maturity (the one that needs to be sold) is higher than the price of a future with a longer maturity (the future that needs to be bought), than selling the first and buying the latter will result in a profit.

However, when the market has a positive term structure (contango), the roll yield will be negative. The future that needs to be sold will have a lower price than the one with a longer maturity that needs to be bought, which results in a loss (since you have to pay more for the new future than you got from the old one).

The roll yield can be seen as a sort of risk premium that financial investors require for taking a position opposite to that of hedgers (which use futures to limit their price risk). The roll yield is different in one aspect: the contract isn’t held until maturity.

One of the original purposes of futures contracts was to transfer the price risk from market participants that have an interest in the underlying commodity to other participants, willing to take the price risk (UNCTAD, 2009). The commercial market participant (i.e. the participant with an interest in the underlying commodity) pays some sort of (insurance) premium for the transfer of that risk (in the form of the hedging cost) and the counterparty receives this as a premium for assuming the risk.

This risk premium encompasses the difference between the current future price and the expected future spot price, both at the time the future contract is purchased. However, there is no certainty yet at this point which party will benefit from the contract.

When the futures price is lower than the expected future spot price, then the investor (or speculator if you will) will have earned his risk premium. Otherwise, if the price of the future is higher than the expected future spot price, than it will be the seller of the futures contract that earns the premium.

In a normal situation hedgers would outnumber speculators and thus the futures price would be lower than the expected future spot price. This means that speculators wouldn’t earn their risk premium when the contract reaches maturity.

15

If we transfer this to the (slightly different) roll yield, we see the same occurring (the contract just isn’t held till the expiration date).

Research (UNCTAD, 2009) has shown something peculiar. Because of the huge amount of investors in the commodity markets that take long positions in commodities, the term structure has changed from backwardation to contango. This happens because, when a large number of parties takes long positions, there won’t be enough counterparties willing to cover that position.

The prices of futures will be higher when maturity increases, resulting in losses for the financial investors. So, ironically, the enormous interest of financial investors, which have no commercial interest in the underlying commodity, (they already account for almost 50 % of transactions in commodity futures markets) have caused the roll yield, which made investments in commodities in the 80s and 90s so attractive, to become negative (Montier, 2010).

The following graph illustrates this. There was a positive roll yield in the period 1970-2000. But at the last decennium, we can see that the roll yield has become negative, whilst the spot return amounts for most of the return in commodities. The relative importance of the collateral return has diminished, mostly due to low interest rates.

Figure 1: Breakdown of commodity futures returns

Source: I want to break free or, Strategic Asset Allocation ≠ Static Asset Allocation, GMO, James Montier, May 2010, p.11

2.5 COMMODITY INDICES

The best way to measure the prices of commodities is through the use of commodity indices. These indices are made up from a basket of commodities, starting at a certain base year. There are several indices in existence, such as the CRB Index4, the Thomson Reuters Indices5 and the S&P GSCI (and many more).

For the purposes of this thesis we will only focus on the index that is in our opinion the best representation of the role commodities play in the world economy.

4 http://www.crbtrader.com/crbindex/spot_background.asp - 01/03/2011 5http://thomsonreuters.com/products_services/financial/thomson_reuters_indices/indices/commodity_indices/#tab1 – 01/03/2011

16

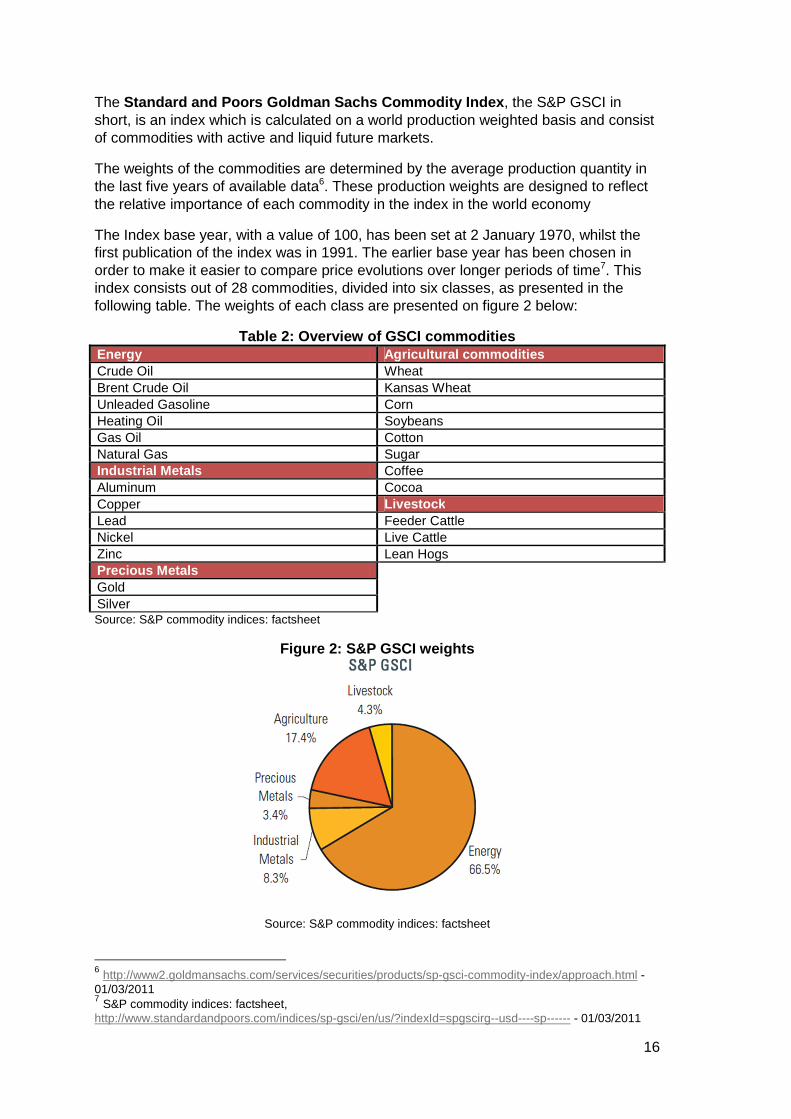

The Standard and Poors Goldman Sachs Commodity Index , the S&P GSCI in short, is an index which is calculated on a world production weighted basis and consist of commodities with active and liquid future markets.

The weights of the commodities are determined by the average production quantity in the last five years of available data6. These production weights are designed to reflect the relative importance of each commodity in the index in the world economy

The Index base year, with a value of 100, has been set at 2 January 1970, whilst the first publication of the index was in 1991. The earlier base year has been chosen in order to make it easier to compare price evolutions over longer periods of time7. This index consists out of 28 commodities, divided into six classes, as presented in the following table. The weights of each class are presented on figure 2 below:

Table 2: Overview of GSCI commodities Energy Agricultural commodities Crude Oil Wheat Brent Crude Oil Kansas Wheat Unleaded Gasoline Corn Heating Oil Soybeans Gas Oil Cotton Natural Gas Sugar Industrial Metals Coffee Aluminum Cocoa Copper Livestock Lead Feeder Cattle Nickel Live Cattle Zinc Lean Hogs Precious Metals Gold Silver Source: S&P commodity indices: factsheet

Figure 2: S&P GSCI weights

Source: S&P commodity indices: factsheet

6 http://www2.goldmansachs.com/services/securities/products/sp-gsci-commodity-index/approach.html - 01/03/2011 7 S&P commodity indices: factsheet, http://www.standardandpoors.com/indices/sp-gsci/en/us/?indexId=spgscirg--usd----sp------ - 01/03/2011

17

3. LITERATURE OVERVIEW In this section we will give an overview of the research that has been done about the determinants of commodity prices and price evolutions in recent scientific literature.

This part will be divided in three chapters. The first chapter will be about the research on price evolutions of commodities and its determinant s. A second chapter will focus on the crisis periods and Black Swan events that might have a profound effect on the prices of commodities. Finally we will look into the role that the financial markets play on the commodity markets in recent years and their impact on prices.

3.1 PRICE EVOLUTIONS OF COMMODITIES AND ITS DETERMINANTS

Early research on the determinants of commodity prices relied solely on demand as the fundamental factor. Demand alone, however, was insufficient to explain weaknesses in commodity prices in the 1980s and 1990s. Borenszstein and Reinhart (1994) extended the model. They added supply and extended demand beyond the demand for commodities in the industrialized world. The view of what was fundamental for commodity prices was widened. However, the focus still lay solely on supply and demand as explanatory variables for the prices of commodities.

Cashin and McDermott (2001) took a different approach and investigated the behavior of commodity prices over a period of almost 140 years (1862-1999) by using the longest dataset available (The Economist’s index of industrial commodity prices). They discovered that there has been a downward trend in commodity prices over this long period of about 1.3% a year. They found no evidence that there would come an end to this trend.

Although this might look like a grim situation, evidence was also found that the variability of commodity prices has been rising. A first hike of variability started in the 1900s and a second increase appeared in the early 1970s, when there came an end to the system of fixed exchange rates. The figure below illustrates this.

Figure 3: Percentage change in real industrial comm odity prices 1862-1999

Source: IMF working paper WP/01/68, The long-run behavior of commodity prices: small trends and big

variability, Paul Cashin and C. John McDermott, May 2001, p. 16

18

This rise in variability, when exchange rates began to float against each other, is already a first indication that exchange rates might have a profound effect on commodity prices, as will be proven later on (IMF, 2008; Akram,2009).

While there is a long running downward trend in commodity prices, this trend is irrelevant since it is quite small and offset entirely by the high variability in prices .

Cashin, McDermott and Scott (2002) expanded the research on commodity price evolutions and investigate the “duration and magnitude of cycles in world commodity prices”. They discovered four characteristics of commodity price booms and slumps :

1. There is an asymmetry in commodity price cycles: Slumps last longer than price booms.

2. Prices appear to fall more in a slump than they rebound in a sub-sequent boom. 3. Cycles of commodity prices don’t appear to have a pattern. The magnitude of

price booms or slumps has nothing to do with the duration. 4. The chance that a slump (boom) ends is independent of the time already spent

in that slump (boom).

It is indeed interesting to know the behavior of commodity prices when in certain situations, but this does not tell us anything about the causes of these booms or slumps. Radetzki (2006) looked into this and studied three separate commodity booms, looking for the reasons why prices rose.

The first boom in 1950-51 was caused by an inventory buildup in response to the Korean war. A second boom in 1973-74 occurred due to a global harvest failure and by the OPEC price politics. A third boom began in 2004 and ran till 20088, and was fueled (to an extent) by the growth of the emerging economies, most notably China and India.

We now know, however, that there was also a serious speculative factor9 present as shown by an increase of the number of financial market participants on the commodity markets (Conceiçao and Marone, 2008; UNCTAD, 2009).

All booms collapsed and subsequently the world economy stumbled into a recession and excessive inventories were sold out. The author believed the third boom to be more durable. Although it also collapsed, the new boom in commodity prices that is underway is apparently still, for a big part, driven by fundamental factors, like demand in the emerging economies, as was previously determined by Borenszstein and Reinhart (1994). Conceiçao and Marone (2008) studied the drivers and the impact of this boom in the 21 st century.

The boom that lasted till halfway 2008 was the largest one in the last 50 years. It lasted longer than usual, affected more commodities and caused larger price increases. And it appeared to be unexpected, since most forecasts underestimated price increases and even when price increase occurred, most predictions stated that a quick and sharp decreases would follow very soon.

The subsequent slump in the second half of 2008 and in 2009 was over rather quickly, negating the first characteristic of price booms as stated by Cashin, McDermott and Scott (2002). The slump did not last longer than the boom.

8 Own addition, since the boom was still underway when the article was published in 2006. 9 More on the role of speculation in chapter 3.3: The financialization of commodity markets.

19

The boom was a mix of fundamentals, speculation and macroeconomic factors. On the fundamentals side we had the strong demand for commodities and supply constraints. Concerning these supply constraints Roache and Erbil (2010) tried to find out how commodity prices and inventories react to a short-run scarcity shock.

They found a long-run relationship between the spot and future p rice, inventories and interest rates . So when a short-run shock occurs, prices will revert back to a stable equilibrium. The pace of this adjustment to the equilibrium appear to depend on the level of the inventories at the time of the shock.

This brings us to the important role inventories play in the price determination of commodities. Research (Gorton and Rouwenhorst, 2005; IMF, 2008, Frankel and Rose, 2009; Carpantier, 2010; Roache and Erbil, 2010) has shown that there is an inverse relationship between the level of inventories and the prices of commodities. The lower the levels of inventories fall, the more the price will rise (i.e. a form of inverse leverage). This is called the inventory effect10.

Speculation also had a role to play in the commodity boom, in the form of market participants that were fully disconnected from fundamentals that normally drive the commodity markets (Conceiçao and Marone, 2008; UNCTAD, 2009).

Although many commodities experienced increasing price levels and the same had underlying factors that caused these price rises, the weight of these drivers appeared to be very different between commodities. For oil and food the price boom was driven mostly by strong demand and supply constraints. For metals on the other hand, speculation seemed to be the most dominant factor (Conceiçao and Marone, 2008).

A commodity boom of this magnitude has advantages for many commodity exporting developing countries, whilst it is not so good for developed countries and developing countries that are importers of commodities. However, China, which is a net importer of commodities, does not seem to be affected much by this because of the strong manufacturing exports that compensate for commodity imports.

Frankel and Rose (2009) wanted to examine the macro-and micro economic factors that drive commodity prices and wrote a paper about the determinants of agricultural and mineral commodity prices. They implement several previously separately used variables (Frankel 2006; Gorton and Rouwenhorst, 2007; Conceiçao and Marone, 2008), and some new ones into one model

This model includes: Global GDP, real interest rates, inventory levels, measures of uncertainty (volatility) and the spot-forward spread (which measures expectations). The model is used on eleven different commodities. Global output and inflation have a positive effect commodity prices although this effect was rather small. It are the microeconomic variables volatility, inventories and spot-forward-spread that have the strongest effect.

There was little support that easy monetary policy and low interest rates were an important source of upward pressure on real commodity prices. This might indicate that there is more to the monetary policy variable than just the interest rates, as stated by Anzuini, Lombardi and Pagano (2010).

10 More on the relation between inventories and the price of commodities can be found in chapter 5.2.

20

These findings about the role of monetary policy and interest rates were curious, since Frankel (2006) already examined the relationship between monetary policy and agricultural and mineral commodities. He found that low interest rates lead to high commodity prices. He examined this for the US and a series of other countries. The evidence appeared to be impressive and the effect of real interest rates on commodities is significant not only for the US, but also for a whole series of (open) economies.

Also Akram (2009) looked into the role of interest rates and investigates the hypothesis that a decline in real interest rates and the US dollar causes commodity prices to rise. The results from his research suggest that “commodity prices increase significantly in response to reductions in real interest rates.” For certain commodities, like oil, there is evidence of overshooting behavior when the real interest rate changes.

Browne and Cronin (2010), stipulate that there should be a long run relationship between commodity prices, consumer prices and money. They tested this hypothesis on US data and found that there is indeed an equilibrium relationship between commodity prices, money and consumer prices . Commodity and consumer prices appeared to be proportional to the money supply in the long run. The authors state that money has to be added to analyses between commodity and consumer prices, an opinion Anzuini, Lombardi and Pagano (2010) follow.

Their research tells us it is important to understand what the impact of the large monetary policy easing is that happened during and after the recent recession. The authors believe that the monetary easing of the last two years will be responsible for a “new surge in commodity prices”.

Previous literature (Frankel, 2006; Akram, 2009) focused on the interest rate as the sole connection between monetary policy and commodity prices. Researchers of the ECB (Anzuini, Lombardi and Pagano, 2010) think, that interest rates do not fully represent the impact of a monetary policy shock. They add the following variables (beside the interest rate which is represented by the federal funds rate): money stock (M2), consumer price index, industrial production index and a commodity price index.

There is empirical evidence that there is a significant impact of monetary policy on commodity prices (Frankel 2006, Akram 2009, Browne and Cronin 2010, Anzuini, Lombardi and Pagano 2010). More specifically: an expansionary monetary policy shock drives up commodity prices.

Anzuini, Lombardi and Pagano (2010) however found that the variance composition shows that the actual impact of monetary policy on commodity price s is rather small but still significant , as opposed to the findings of Frankel and Rose (2009).

Much research done on the impact of the interest rates and monetary policy focused on the US dollar. Akram (2009) looked, besides the interest rate, at the dollar exchange rate and investigated whether the depreciation of the US dollar leads to higher commodity prices. He discovered that a shock in the dollar exchange rate leads to a significant movement of commodity prices, and indeed a decline of the US dollar exchange rate causes commodity prices to rise.

Akram (2009) states that the value of the dollar (together with the US real interest rate) could be good indicators for the movement of commodity prices. Other research (IMF, 2008; UNCTAD, 2009; Bhar and Hammoudeh, 2010) on the relation of the dollar exchange rate with commodity prices seems to verify this.

21

In the IMF world economic outlook of April 2008, the author examines the relation between the dollar exchange rate and commodity prices. Over the past 20 years commodity prices have been (mostly) negatively corr elated with the US dollar .

The dollar exchange rate has a significant impact on gold and oil prices in the short and long run. A one percent depreciation of the dollar results, in the long run, in a increase of the gold and oil prices with more than one percent. For other commodities there is also an increase, but smaller than one percent.

This difference between commodities can be explained by the fact that commodities such as gold and oil are more usable as a “storage of value”, where this is not really possible with perishable commodities (the impact of the dollar exchange rate on grain, for example is not significant).

The relation between the dollar exchange rate and the oil price has also been found by Bhar and Hammoudeh (2010). They looked at the influence of both interest rates and exchange rates on commodity prices in a regime shifting environment.

The relationship between the dollar and the oil price is negative, which means that in times of crisis, a weakening dollar leads to higher oil prices. In a normal economic state this effect is weaker. This discrepancy between a normal state and a crisis state leads us to the next chapter on crises and Black Swan events.

3.2 CRISIS PERIODS AND BLACK SWANS

Bhar and Hammoudeh (2010) looked, as previously stated, into the influence of several variables on commodity prices in regime shifting environments. Although we won’t go into regime changing environments in this thesis, it is interesting to see what the influence of the various variables is on commodity prices in a normal and crisis period.

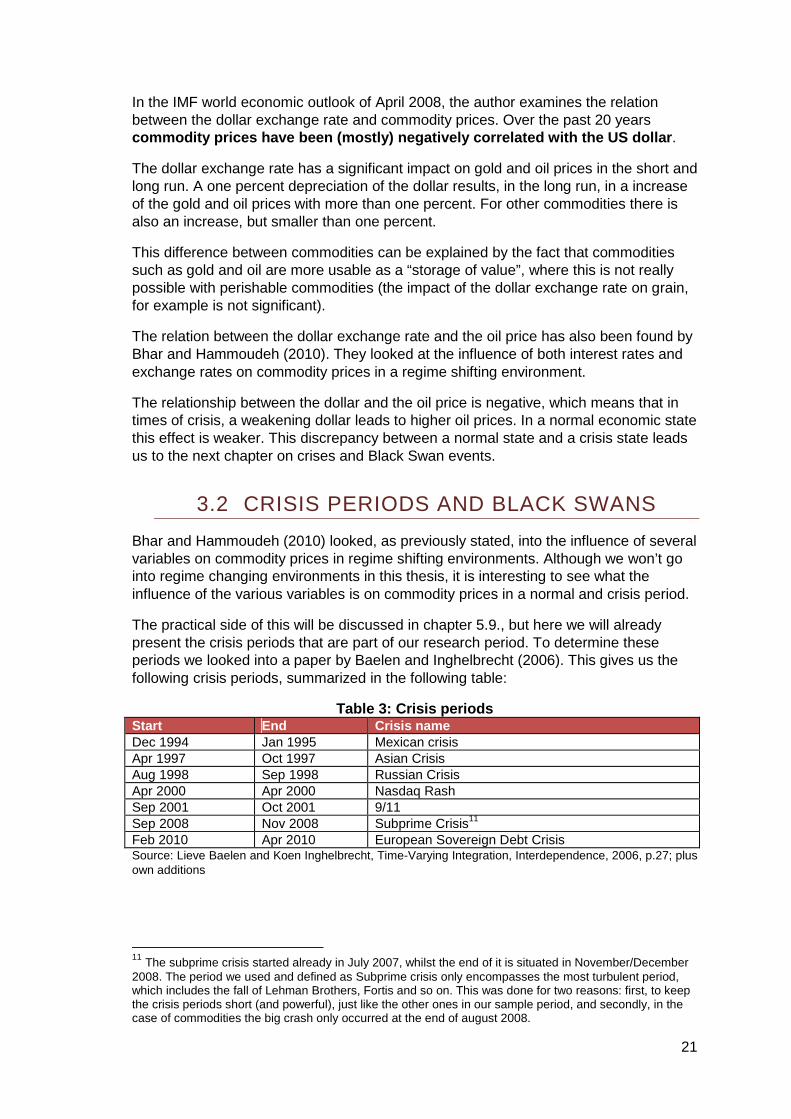

The practical side of this will be discussed in chapter 5.9., but here we will already present the crisis periods that are part of our research period. To determine these periods we looked into a paper by Baelen and Inghelbrecht (2006). This gives us the following crisis periods, summarized in the following table:

Table 3: Crisis periods Start End Crisis name Dec 1994 Jan 1995 Mexican crisis Apr 1997 Oct 1997 Asian Crisis Aug 1998 Sep 1998 Russian Crisis Apr 2000 Apr 2000 Nasdaq Rash Sep 2001 Oct 2001 9/11 Sep 2008 Nov 2008 Subprime Crisis11 Feb 2010 Apr 2010 European Sovereign Debt Crisis Source: Lieve Baelen and Koen Inghelbrecht, Time-Varying Integration, Interdependence, 2006, p.27; plus own additions

11 The subprime crisis started already in July 2007, whilst the end of it is situated in November/December 2008. The period we used and defined as Subprime crisis only encompasses the most turbulent period, which includes the fall of Lehman Brothers, Fortis and so on. This was done for two reasons: first, to keep the crisis periods short (and powerful), just like the other ones in our sample period, and secondly, in the case of commodities the big crash only occurred at the end of august 2008.

22

Besides (relatively frequent) crisis moments, there are also those very rare events, with a huge impact, known as Black Swan events . A Black Swan, a term invented by Nassim Nicholas Taleb (2010), is an event with the following three attributes:

• First of all, a Black Swan event is an outlier , which means that is an event we can’t really expect to occur, based on regular expectations. Nothing in the past points to this event.

• Secondly, a Black Swan event has an enormous impact . • And finally, humans begin to search for logical explanations after the event

took place , in an attempt to make it explainable and predictable.

The interesting thing about these Black Swans is their low predictability and large impact. The rarity of the events, makes people act as if Black Swans don’t exist. Thus believing they could measure uncertainty. So, most measures in modern economic models exclude the possibility of Black Swan events, which implicates that they have “ no better predictive value for assessing the total risk than astrology” (Taleb, 2010).

However, people need some form of model to base expectations upon , even if it is not the right one, or the one that incorporates all possible events (which is, in our opinion, impossible). Thus, the very essence of human nature, the need for those models/reference cadre, makes it hard for us to predict Black Swan events (which lie, per definition, outside those models). It is, however, interesting to see what the impact of such an event might be on commodity prices (even in hindsight).

Therefore we will implement three Black Swan events into our research period. Events that incorporate the three attributes previously mentioned. These events are: The 9/11 terrorist attack on the twin towers (September 2001), the Tsunami of 2004 (December 2004) and finally the fall of Lehman Brothers in September 2008 , triggering a world-wide financial storm and the Great Recession.

3.3 THE FINANCIALIZATION OF COMMODITY MARKETS

We can define the financialization of the commodity markets as the growing presence of financial institutions and players on t he commodity markets who, on the contrary to commercial market participants (like producers of commodities hedging their positions), have no real connection to the underlying commodity. The financial players are driven by motives of portfolio diversification (UNCTAD, 2009). Speculation can be defined as the purchase of a commodity (contract) in anticipation of financial gain at the time of resale (Frankel and Rose, 2009).

It has been said that the recent commodity boom was largely driven by financial players that speculated on commodities. Evidence that prices of commodities are not aligned with fundamentals is not all that clear. Conceiçao and Marone (2008) state that the most conclusive evidence about speculation can be found at the metal commodities, more specifically copper and nickel.

The question that we need to ask ourselves in regard to the boom of 2008 is: How detached were price levels from fundamentals, as co mpared to earlier booms?

23

As you can see in table 4 , for copper, during a trough in the economic cycle in 1985, the ratio of the market price to the marginal production cost (of the least efficient producers) was 1. Meaning that market prices were just sufficient to cover the costs of production. In the case of nickel and aluminum market prices were even too low to cover the marginal production costs of the least efficient producers.

Table 4:Cash Cost of Production of Basic Metals (US dollars per ton)

Source: UNDP working paper, Characterizing the 21st century first commodity boom: Drivers and impact, Pedro Conceiçao and Heloisa Marone, October 2008, p.24

During the last boom, we can see that, compared to marginal costs of 2005, the ratio of price to marginal cost was 2,8 for copper, showing that prices were getting detached from fundamentals, represented here as the marginal costs (the ratio was also much higher than during previous booms). For efficient producers the ratio was even much higher.

Frankel and Rose (2009), have a broader viewpoint and look at speculation from two distinct angles. Firstly speculation can be seen as an major (some might say evil) force that pushed up prices during the commodity boom of 2003-2008, in the absence of fundamental reasons. Thus, a bubble scenario.

A second interpretation on the role of speculation can be a less malevolent one, where speculation (or the activities of financial market participants), can be seen as a stabilizing factor .

In many cases, speculators are often “net short” on commodities, meaning that on average, during a certain period of time, they sold more contracts than they bought. They did this because they anticipated a reversion of prices to normal levels. By going short, based on this expectation, speculators might have kept prices lower than they otherwise would have been.

If we recapitulate this: because the speculators anticipated a possible reversion of commodity prices to normal levels, they took positions on this presumption. And by doing so they kept prices lower or might have even reversed the price rising trend eventually. Almost like a self-fulfilling prophecy.

24

Also Krugman (2008) doesn’t believe that speculation was responsible for the price rises. He states that “if the speculators were the main force pushing oil prices far above the level justified by fundamentals, excess supply should be observed”. Inventories have remained at more or less normal levels. This shows us that the rise in oil prices is not the result of speculation, but of the growing difficulty to find oil and the rapid growth of the emerging markets. Demand is simply growing faster than supply .

Frankel and Rose (2009) use a similar argument as well. The say that the level of inventories during the period 2003-2008 was historically low in some cases, thus causing increases in price levels12. Furthermore, Frankel and Rose (2009) point out another convincing argument against the destabilizing role of speculation: It appears that commodities without futures markets, which are less susceptible to the presence of financial players, encountered just as much volatility as commodities with active futures markets.

It is a fact however that the financialization of the commodity markets has increased in recent years. Because of this commodity prices have become more exposed to financial shocks and are more prone to overshooting behavior (UNCTAD, 2009). Given the small number of producers that are active on the futures markets, a large inflow of cash from financial participants could push the futures prices up; whilst uncertainty about supply and demand could increase volatility of the prices.

Data on this subject is not easy to found and is mostly obtained from the Commodities and Futures Trade Commission (CFTC). This makes it difficult to disentangle the pure speculators from the commercial market participants.

Furthermore it is interesting to note that the link between the financial and commodity markets has been around for quite some time and has been providing invaluable services to the economy (like hedging). The activity of financial parties on commodity markets is not a new phenomenon, what’s new is the increase of their presence.

The available data show that, in the US alone, the long positions held by index funds represent almost 50% of total positions in the main commodity market13. Estimations for the US go as far as claiming that almost 60% of all long positions in commodity markets are held by financial investors.

The influx of money by these financial investors , as stated before, is expected to be an important driver for price increases (Conceiçao and Marone, 2008).

Due to the difficulty to get data about speculation on commodity markets and the difficulty to disentangle speculators from commercial market parties, we have decided not to add a variable on this in our model. It was, in our opinion, absolutely necessary to add a chapter on the role of speculation and financialization, in order to be complete in our presentation of the literature and on the factors influencing commodity prices.

Indirectly of course, the influence of speculation can be measured through the monetary policy variables like interest rate and money supply, since cheap money might induce a larger inflow of capital into the commodity markets.

12 We will present you the link between commodity prices and inventories in chapter 5.2. This is done because we believe the presentation of that theory is necessary to explain the use of the inventory variable and is thus better off in a coherent chapter explaining everything on inventories at once rather than small bits and pieces scattered all over this thesis. 13 In this case the CBOT, Chicago Board Of Trade

25

4. RESEARCH QUESTIONS AND METHODOLOGY

To what extent do several determinants 14 have an impact on the price evolutions of commodities?

That is the question we ask ourselves when looking at the literature and our chosen variables. In order to find an answer to it, we will use a univariate model so we can estimate the impact of the independent variables on commodity prices. This univariate model will consist of an OLS regression of time series data for a sample period ranging from 31/01/1995 till 31/12/2010.

Once we have estimated the model and after we have interpreted the results, we can move on to a second phase. Our OLS-regression will tell us by which variable(s) the commodity spot price is influenced.

This model is, however, subject to the endogeneity problem, which means that the “independent” variables might also be affected by changes of the commodity prices, or by the other independent variables (and not just by exogenous factors). This means that our independent variables might not be so independent as we might believe.

To overcome this problem we will use a multivariate model, namely a VAR (Vector Auto Regression) model . This model will enable us to answer the following question:

Can we determine which variables cause changes in t he commodity prices and vice versa, which changes are caused by a change in commodity prices?

We will examine the impact of the variables on each other for our entire sample period. When we include lagged variables in this model, we might also be able to determine which variables Granger Cause others.

Once we have successfully estimated this VAR model, we will use impulse responses (i.e. we will give exogenous shocks to the variables in the model) to see which impact the change of one variable has on the price of commodities (we will limit ourselves to the impact on the commodity spot prices). This way we might answer the question below:

In which way do the variables in this model have an impact on commodity prices and to what extent?

This might give us some insight in how commodity prices behave and might even give us some possibility to forecast future price movements.

Before we can answer these questions, let us first have a look at the variables and the model we will use in the next few chapters.

14 These determinants, or variables, will be presented in the following chapter.

26

5. THE VARIABLES

5.1 COMMODITY PRICES

The commodity prices will be the dependent variable in this research. As a proxy for the prices of commodities we will use the GSCI spot price index. We opt for this index for three reasons:

(1) It exists since 1991, and consists of actively traded and liquid commodities. (2) The commodities in this index are weighted in such a way that this reflects the

relative importance of each commodity in the world economy15. (3) Since 1995 this index has also a futures version which will enable us to

calculate the Future-spot spread, which is required for one of the variables.

The following graph presents the evolution of the spot Index for the main period to give a first glimpse of the evolution of commodity prices.

As you can see there has been a steady rise in overall commodity prices since 2002. With an extreme growth in 2007, after which they suddenly plunged into the abyss halfway 2008. The decline only halted in 2009, after which a sharp rise once more began, although the high levels of 2008 are not yet reached.

Graph 2: S&P GSCI Commodity Spot - Price Index

Source: Datastream

This dependent variable will be represented in the model as �����.

15 http://www2.goldmansachs.com/services/securities/products/sp-gsci-commodity-index/approach.html - 01/03/2011

100

200

300

400

500

600

700

800

900

1996 1998 2000 2002 2004 2006 2008 2010

Spot_

Price_In

de

27

5.2 INVENTORIES

Inventory levels of various commodities are of importance for the price determination. There should be an inverse relation between inventories and the price of commodities. If inventories are low, prices will be high and vice versa (IMF, 2008). This is presented in the following graph.

Graph 3: Inverse relationship inventories and price s

Source: IMF, World economic outlook, April 2008. p. 57

In order to gather data on this variable, there are some issues. First, there is no common data source where data on commodity inventories worldwide are to be found. The data is scattered around and thus very difficult to gather.

A second problem that poses itself is the definition of an inventory. Are the inventories held (and reported) at the commodity exchanges sufficient? What about (unavailable) data about inventories held off exchange? Or proven reserves that are still in the ground? It is clear that just using data of inventories held at the exchanges is just the tip of the inventory iceberg (UNCTAD, 2009; Carpantier, 2010).

There is also a timing factor issue besides the previously mentioned problems. Data on inventories, if available, is published with a time lag and is often revised several times, lowering the reliability of the data even more (Gorton and Rouwenhorst, 2005).

Only if our research would have been limited to the price evolutions of specific commodities, like for example copper, then the data on the inventories from the London Metal Exchange (LME) could have been a good proxy for copper inventories in general , since about 95 % of the world trade in copper futures happens on the LME (Roache and Erbil, 2010).

In our case, however, this would not work because we look at a broader range of commodities. The use of inventory data to represent the influence of this variable on commodity prices in general, would be too unreliable and incomplete.

So, we had to look for a viable alternative, to represent the inventory variable. This alternative presented itself in the form of the Future-Spot spread , which we will explain in the following paragraphs. In order to understand the use of the future-spot spread as a proxy for the commodity inventories, we have to present you with the theory of storage .

28

This theory implies, that there is a cost adjusted equivalence between buying a future contract (i.e. receive the commodity at a predetermined date at a certain price.) or directly buying and storing a commodity (Carpantier, 2010). These storage costs, which include costs like insurance, interests, transport and the actual storage cost, are called the cost of carry (UNCTAD, 2009) .

This can be represented by the following formula (Carpantier, 2010):

��,�− �� = ��� > 0

With: ��,�: Future price, with delivery at time T. ��: Spot price at time t ����: Global cost of storage between time t and T (cost of carry)

In this case, as represented by the formula, the futures prices are higher than the spot price, thus the market is in contango. Although, as previously mentioned, markets aren’t always in this situation, since futures prices can also be lower than spot prices. In this case the market will be in backwardation. Now, the two possible term structures of the commodity markets brings us to the concept of the convenience yield.

The convenience yield , can be defined as the value of having a sufficient amount of a certain commodity in stock in the event of a disruption (Frankel and Rose, 2009). Or otherwise stated: Having a commodity in storage gives a good opportunity to the agent having that commodity in storage.

For example, when there is a sudden oil market disruption, this will lead to a price rise of oil, thus leading to extra yield for agents with oil at their disposal at that moment (when they sell it). This possible benefit for having a commodity in storage is the convenience yield and can be presented by the following formula (Carpantier, 2010):

�� = �� − ��,�+���

With: ��: The convenience yield at time t ��,�: Future price, with delivery at time T.

��: Spot price at time t ����: Global cost of storage between time t and T.

The convenience yield will rise when markets are tight and inventories are low. This represents the positive yield for agents that have the commodity already in stock, ready for direct delivery. Spot prices are higher than futures prices in such a situation, which makes it interesting to sell commodities on the spot.

If we look at the two possible term structures of commodity futures, we get the following two situations:

• Contango: �� − ��,� < � , which results in a negative convenience yield. (�� < 0).Now, when we reverse the calculation, we get ��,� – �� > 0. This situation implies high inventory levels. So it is not that interesting to have commodities in stock, since there is a higher cost of storage due to the high demand for this storage.

• Backwardation: �� − ��,� > � , which results in a positive convenience yield (�� > 0). When we reverse the calculation to get the future spot spread, we get: ��,� - �� < 0. In this case there are low inventory levels, so it is interesting for agents to have a stock of commodities, since prices will rise in the future. Also, due to low demand for storage, the cost of carry will be lower.

29

It has been shown empirically (Gorton, Hayashi and Rouwenhorst, 2008; Roache and Erbil, 2010) that the convenience yield is a decreasing, non-linear function of inventories, as illustrated by the following graph.

Graph 4: Non-linearity of convenience yield and inv entories

Source: IMF working paper, How commodity price curves and inventories react to a short-run scarcity

shock, Shaun Roache and Nese Erbil, September 2010, p.5

This non-linearity implies that, the lower inventory levels get, the higher the convenience yield will be. And a higher convenience yield is linked to a higher spot price. Furthermore, when inventories reach a low level, a further decrease of the inventory levels will have a much larger impact on the price of commodities than an increase in these inventories.

The closer inventories get to a potential stock-out, the larger the impact of the non-linearity will be, or otherwise said: When inventory levels continue to drop, the increase in prices will become larger. This inverse leverage effect, where positive returns result into larger increases of volatility, is called the inventory effect (Carpantier, 2010).

This connection between the price of commodities and the inventory effect, via the convenience yield and the term structure of commodities, implies that the future-spot spread (�� ,� – �� ) can be considered as a valid proxy for commodity inventories: A small spread would imply low inventories and thus a high convenience yield, while a large spread would mean that inventory levels are high and the convenience yield is low.

There should also be a negative correlation between the spot price level and inventories (IMF, 2008). This implies that at high price levels, the spread will have dropped (i.e. it became more negative), thus representing low inventory levels. When commodity inventories rise, the future spot spread rises as well and becomes less negative.

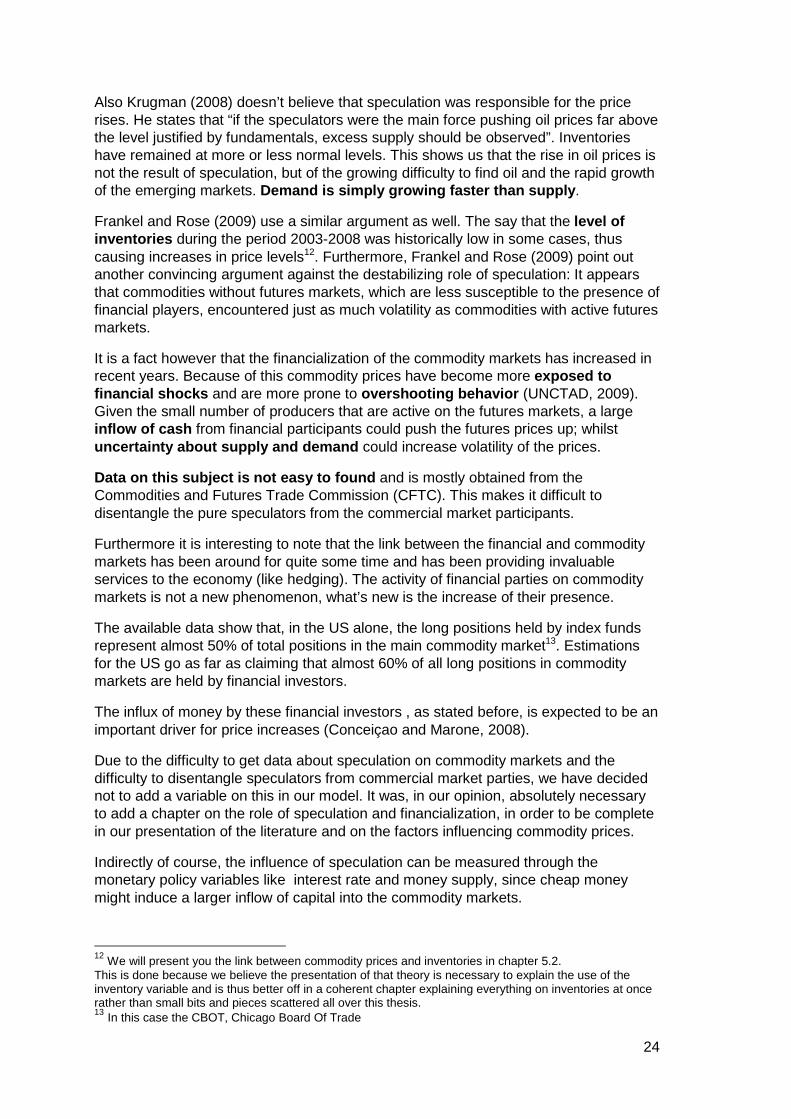

So, a drop in inventories (when demand is bigger than supply) will result in positive price change, meaning the inventory and price curves move in opposite directions, as shown in the following graph.

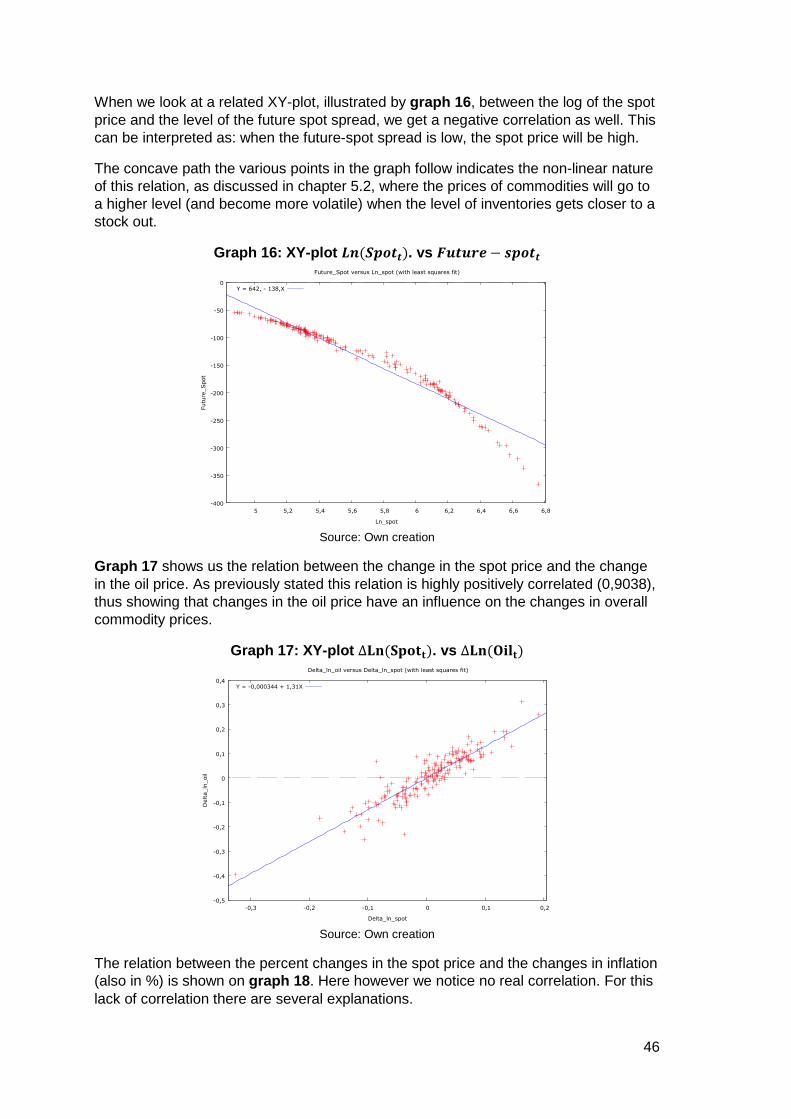

If you look closely to graph 5 on the following page, you will notice that when the future-spot spread drops, the price rises more than the drop of the spread.

30

Graph 5: Inverse relationship Future spot spread an d Spot prices

Source: Datastream, Own creation

Otherwise stated: when inventories drop, volatility of the commodity prices will increase. Graph 6 shows this and intuitively proves the existence of the inventory effect.

Graph 6: Relationship inventory levels and price vo latility

Source: Datastream, own creation

The explanation and graphs prove that the future-spot spread is an acceptable proxy for the level of inventories.

There might even be a link possible with the efficient market hypothesis (EMH), which in this case implies that all known information about inventories (above or still underground) is already present in the (future and spot) price (and can be made visible through use of the future-spot spread).

This variable will be implemented as: �������� − !"���, as a proxy for the effect of inventories. The # coefficient will measure the effect of this variable on the prices of commodities.

-600

-400

-200

0

200

400

600

800

1000Future spot spread

Spot price

Time

-400

-350

-300

-250

-200

-150

-100

-50

0

50

100

Future spotspreadVolatility spotprice

Time

31

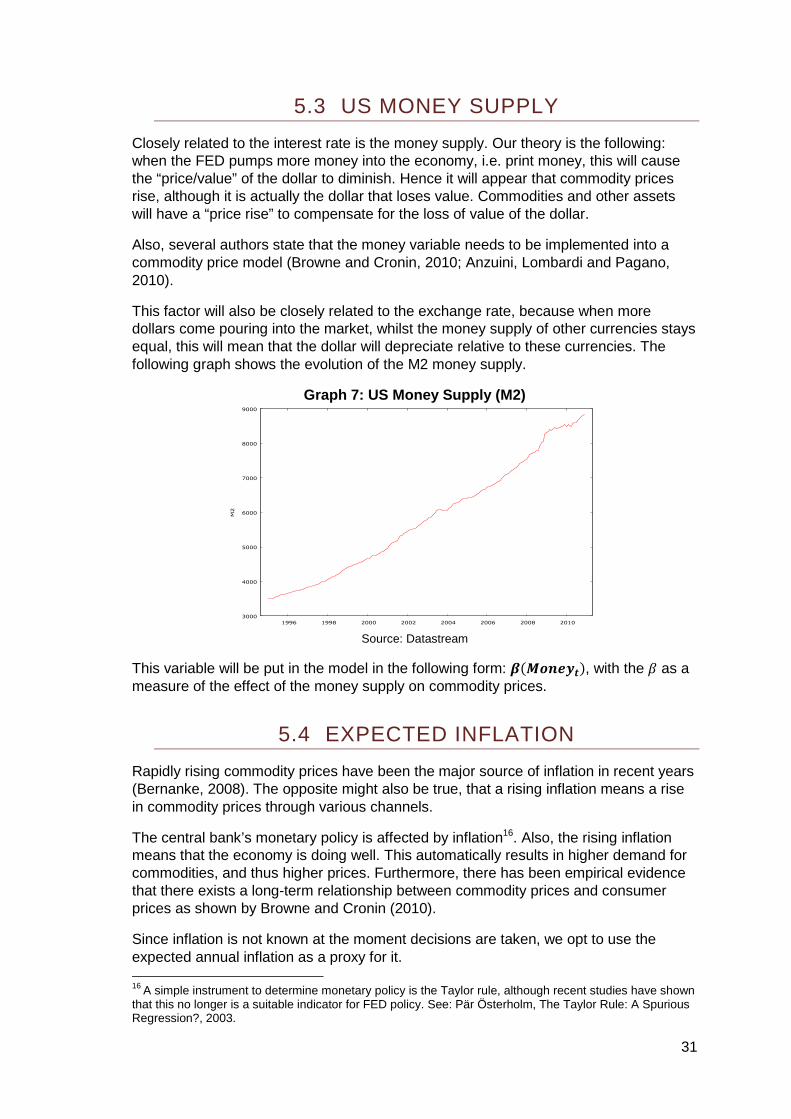

5.3 US MONEY SUPPLY

Closely related to the interest rate is the money supply. Our theory is the following: when the FED pumps more money into the economy, i.e. print money, this will cause the “price/value” of the dollar to diminish. Hence it will appear that commodity prices rise, although it is actually the dollar that loses value. Commodities and other assets will have a “price rise” to compensate for the loss of value of the dollar.

Also, several authors state that the money variable needs to be implemented into a commodity price model (Browne and Cronin, 2010; Anzuini, Lombardi and Pagano, 2010).

This factor will also be closely related to the exchange rate, because when more dollars come pouring into the market, whilst the money supply of other currencies stays equal, this will mean that the dollar will depreciate relative to these currencies. The following graph shows the evolution of the M2 money supply.

Graph 7: US Money Supply (M2)

Source: Datastream

This variable will be put in the model in the following form: ��$�%&'��, with the # as a measure of the effect of the money supply on commodity prices.

5.4 EXPECTED INFLATION

Rapidly rising commodity prices have been the major source of inflation in recent years (Bernanke, 2008). The opposite might also be true, that a rising inflation means a rise in commodity prices through various channels.

The central bank’s monetary policy is affected by inflation16. Also, the rising inflation means that the economy is doing well. This automatically results in higher demand for commodities, and thus higher prices. Furthermore, there has been empirical evidence that there exists a long-term relationship between commodity prices and consumer prices as shown by Browne and Cronin (2010).

Since inflation is not known at the moment decisions are taken, we opt to use the expected annual inflation as a proxy for it. 16 A simple instrument to determine monetary policy is the Taylor rule, although recent studies have shown that this no longer is a suitable indicator for FED policy. See: Pär Österholm, The Taylor Rule: A Spurious Regression?, 2003.

3000

4000

5000

6000

7000

8000

9000

1996 1998 2000 2002 2004 2006 2008 2010

M2

32

The data necessary to calculate this variable will be obtained from the “survey of professional forecasters17”. For this variable we used the series CPIB, which represents the forecast for the inflation of the coming year.

This survey, however is taken every quarter, so there are no monthly data, which we need, available. To solve this issue we have transformed the quarterly data into monthly data by taking the forecast of the first quarter (which is taken in the first half of February) and then use this forecast value for the months February, March and April. The forecast for the second quarter is then used for the months May, June and July, and so on, as you can see in the following table.

Table 5: Timing of the Survey of Professional Forec asters

Source: SPF documentation, http://www.philadelphiafed.org/research-and-data/real-time-center/survey-of-

professional-forecasters/spf-documentation.pdf - 30/03/2011

In table 6, we present an example of the data transformation. Because the survey is taken in the first weeks of February, there is always a shift of one month. So in January we use the expected inflation from the November forecast of the previous year.

Table 6: Transformation to monthly data Month quarter Expected

Annual Inflation

Survey from:

31/01/1995 1 3,443 November 1994 28/02/1995 3,596 February 1995 31/03/1995 3,596 February 1995 28/04/1995 2 3,596 February 1995 31/05/1995 3,590 May 1995 30/06/1995 3,590 May 1995 31/07/1995 3 3,590 May 1995 31/08/1995 3,314 August 1995 29/09/1995 3,314 August 1995 31/10/1995 4 3,314 August 1995 30/11/1995 2,878 November 1995 29/12/1995 2,878 November 1995

Source: Survey of professional forecasters, own creation

17 http://www.philadelphiafed.org/research-and-data/real-time-center/survey-of-professional-forecasters/ - 02/03/2011, the file with the data can be found on http://www.philadelphiafed.org/research-and-data/real-time-center/survey-of-professional-forecasters/historical-data/mean-forecasts.cfm , Mean forecast data for levels.

33

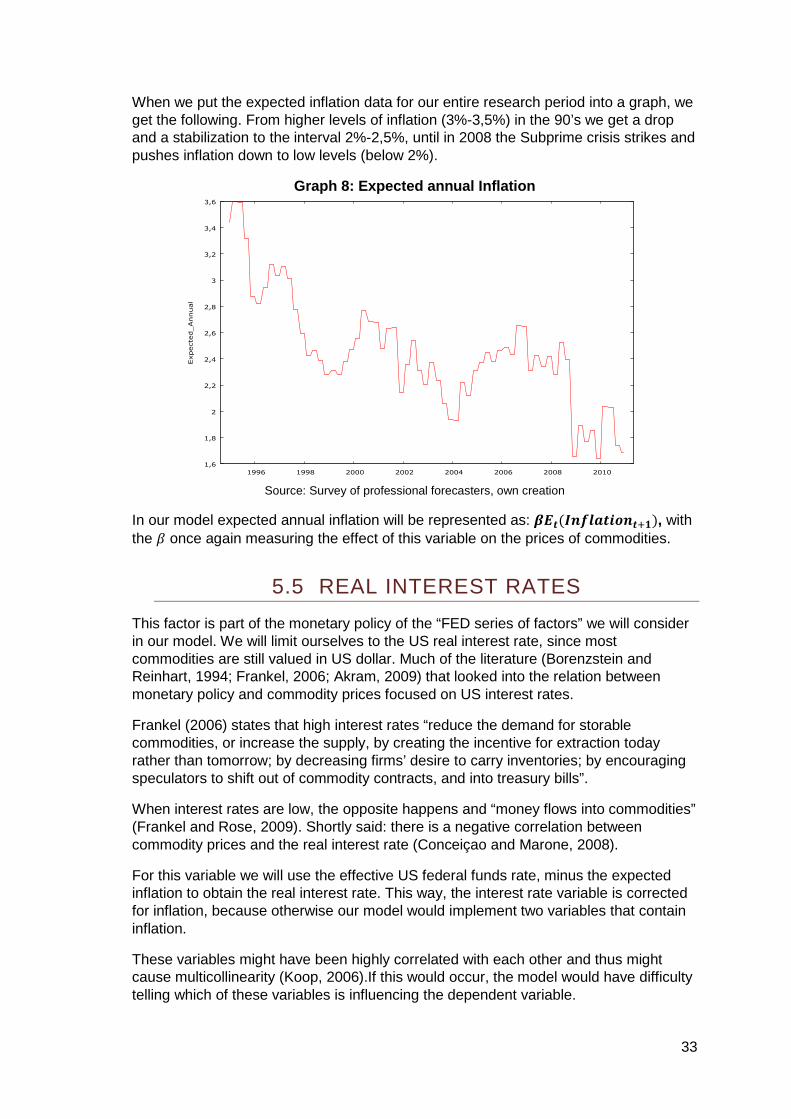

When we put the expected inflation data for our entire research period into a graph, we get the following. From higher levels of inflation (3%-3,5%) in the 90’s we get a drop and a stabilization to the interval 2%-2,5%, until in 2008 the Subprime crisis strikes and pushes inflation down to low levels (below 2%).

Graph 8: Expected annual Inflation

Source: Survey of professional forecasters, own creation

In our model expected annual inflation will be represented as: �(��)%*+,�-�%�./�, with the # once again measuring the effect of this variable on the prices of commodities.

5.5 REAL INTEREST RATES

This factor is part of the monetary policy of the “FED series of factors” we will consider in our model. We will limit ourselves to the US real interest rate, since most commodities are still valued in US dollar. Much of the literature (Borenzstein and Reinhart, 1994; Frankel, 2006; Akram, 2009) that looked into the relation between monetary policy and commodity prices focused on US interest rates.

Frankel (2006) states that high interest rates “reduce the demand for storable commodities, or increase the supply, by creating the incentive for extraction today rather than tomorrow; by decreasing firms’ desire to carry inventories; by encouraging speculators to shift out of commodity contracts, and into treasury bills”.

When interest rates are low, the opposite happens and “money flows into commodities” (Frankel and Rose, 2009). Shortly said: there is a negative correlation between commodity prices and the real interest rate (Conceiçao and Marone, 2008).

For this variable we will use the effective US federal funds rate, minus the expected inflation to obtain the real interest rate. This way, the interest rate variable is corrected for inflation, because otherwise our model would implement two variables that contain inflation.

These variables might have been highly correlated with each other and thus might cause multicollinearity (Koop, 2006).If this would occur, the model would have difficulty telling which of these variables is influencing the dependent variable.

1,6

1,8

2

2,2

2,4

2,6

2,8

3

3,2

3,4

3,6

1996 1998 2000 2002 2004 2006 2008 2010

Expecte

d_Annual

34

If we want to assess the real impact of monetary policy, we have to look at more factors of monetary policy than just the interest rate. This because interest rates alone may not fully capture the impact of monetary policy (shocks) and their movement can be just an endogenous response of monetary policy to general developments in the economy (Anzuini, Lombardi and Pagano, 2010).

This means that the movement of interest rates might just be caused by other variables in the model, like expected inflation or output and not by exogenous factors18.

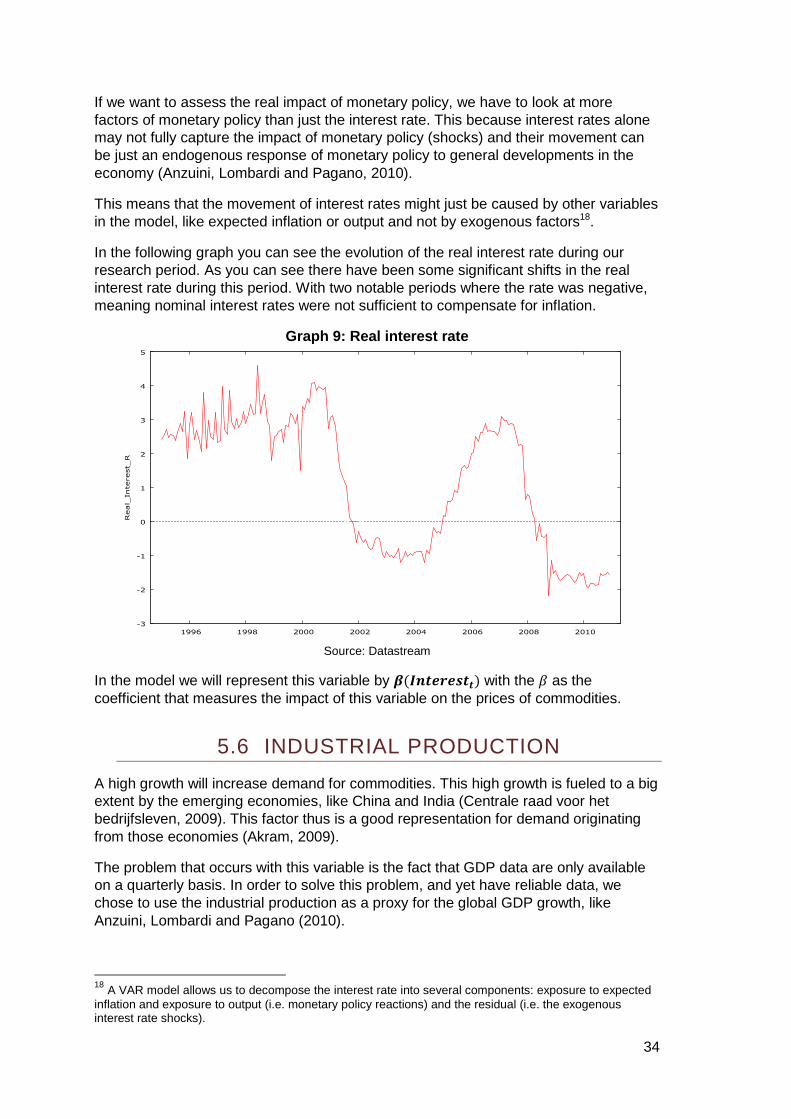

In the following graph you can see the evolution of the real interest rate during our research period. As you can see there have been some significant shifts in the real interest rate during this period. With two notable periods where the rate was negative, meaning nominal interest rates were not sufficient to compensate for inflation.

Graph 9: Real interest rate

Source: Datastream

In the model we will represent this variable by ��)%�&0&1��� with the # as the coefficient that measures the impact of this variable on the prices of commodities.

5.6 INDUSTRIAL PRODUCTION