Price Developments Evaluating Sector Attractiveness · Price Developments – Evaluating Sector...

37

Price Developments – Evaluating Sector Attractiveness Dr Adam Kent - Maritime Strategies International (MSI) 7th Annual Marine Money London Ship Finance Forum – 27 th Jan 2016

Transcript of Price Developments Evaluating Sector Attractiveness · Price Developments – Evaluating Sector...

Price Developments –

Evaluating Sector Attractiveness

Dr Adam Kent - Maritime Strategies International (MSI)

7th Annual Marine Money London Ship Finance Forum – 27th Jan 2016

Agenda

© Maritime Strategies International www.msiltd.com2

Price Developments – Evaluating Sector Attractiveness

1. What determines secondhand prices

2. Newbuilding prices

3. Scrap prices

4. Earnings

5. Secondhand prices

6. Forecast Maritime eValuator (FMV)

Prices - Conundrum

© Maritime Strategies International www.msiltd.com3

15

20

25

30

35

40

45

50

0

5

10

15

20

25

30

35

07

/14

08

/14

09

/14

10

/14

11

/14

12

/14

01

/15

02

/15

03

/15

04

/15

05

/15

06

/15

07

/15

08

/15

09

/15

10

/15

11

/15

12/1

5

Mn US$‘000 $/day 1 Year TC Rate 5 Year Old Price

Static Prices

Break Even v Earnings

© Maritime Strategies International www.msiltd.com4

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

-60

-40

-20

0

20

40

60

Ha

nd

y

Afr

am

ax

Su

ezm

ax

VL

CC

Ha

nd

y

Pa

na

max

Ca

pe

siz

e

1.7

k T

EU

3.6

k T

EU

4.4

k T

EU

8 k

TE

U

‘000 $/day

BreakevenTC Rate% Net Cash Flow (RH Axis)

Based on 60% financing

The Complete Pricing Jigsaw

© Maritime Strategies International www.msiltd.com5

What Determines Secondhand Vessel Prices?

• Current Replacement Cost - Sets Upper Reference

(Yard Prices: Highly Unstable; Major Market Risk)

6© Maritime Strategies International Ltd.

• Residual Scrap Values - Sets Floor to S&P Market ($/LDT:Limited Influence or Up-/Downside Risk)

• Expected Earnings - Sets Depreciation Rate

(TC Rate, Vessel Life Expectancy)

Newbuilding Prices

© Maritime Strategies International www.msiltd.com

Price Developments

MSI’s Shipbuilding Model

8© Maritime Strategies International Ltd.

Sector Specific

Freight RatesSector Specific

Contracting

Global

Orderbook

Forward Berth

Cover

(years)Regional Yard

Developments &

Capacity

Global Yard

Capacity

Global Cost Components

(steel & machinery price,

exchange rates)Weighted

Average of Yard

Costs

Regional Cost Components

(wage, inflation, productivity)

Average Yard

Price Index

($ CGT)

Newbuilding

Price

(by vessel

type by size)

Forward Cover = Pricing Power

Costs = Pricing Floor

Are the Yards Panicking Yet?

© Maritime Strategies International www.msiltd.com9

0%

20%

40%

60%

80%

100%

120%

0

5

10

15

20

25

30

2016

2017

2018

2019

2016

2017

2018

2019

2016

2017

2018

2019

% CapacityMn CGT Mn CGT Historical Max % of Max Historical Output (RH Axis)

South Korea Japan China

Beyond 2016 yards are significantly

underemployed

EmptyCapacity

EmptyCapacity

EmptyCapacity

Chinese Orderbook – Whose Responsible?

© Maritime Strategies International www.msiltd.com10

2017+ Bulker orderbook low

Domestic orders are low

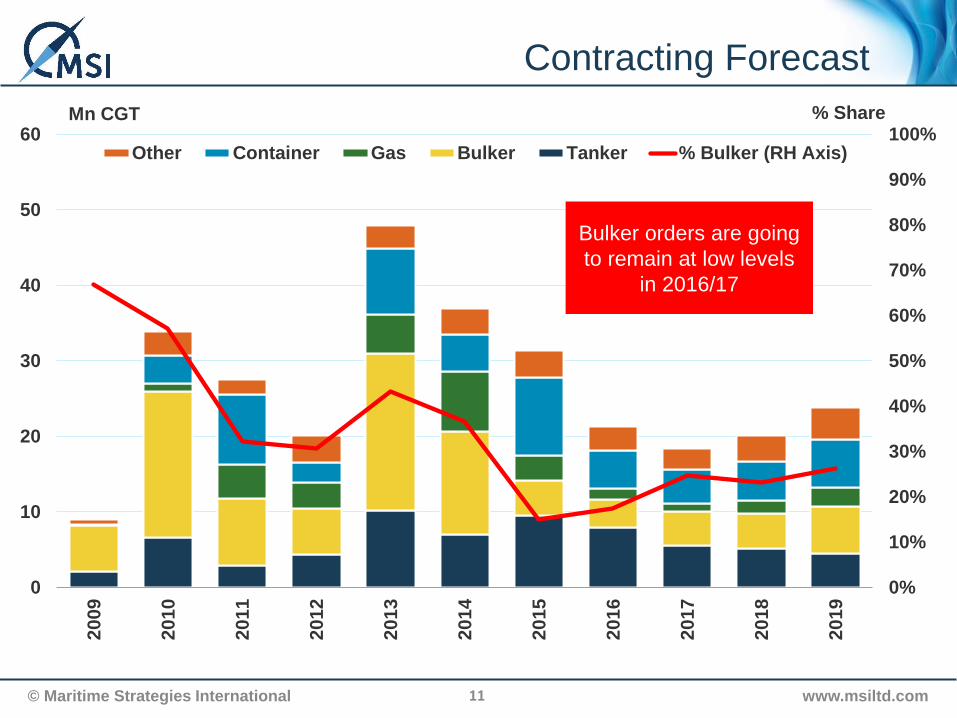

Contracting Forecast

© Maritime Strategies International www.msiltd.com11

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10

20

30

40

50

60

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

% ShareMn CGT

Other Container Gas Bulker Tanker % Bulker (RH Axis)

Bulker orders are going

to remain at low levels

in 2016/17

# Quarter Since Last Order – Chinese Yards

© Maritime Strategies International www.msiltd.com12

0

5

10

15

20

25

30

35

40

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

# of Yards

Quarters Since Last Contract Secured

Redundant/Closed Capacity

Diversified Portfolio Route to Survival

© Maritime Strategies International www.msiltd.com13

Shipyard Turmoil

14© Maritime Strategies International Ltd.

Effective Shipyard Capacity (Merchant)

© Maritime Strategies International www.msiltd.com15

0

10

20

30

40

50

60

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Mn CGT Other Europe China Korea Japan

Shipyard Capacity – Déjà Vu

© Maritime Strategies International www.msiltd.com16

0

2

4

6

8

10

12

14

16

18

20

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

Mn CGT Other Europe China South Korea Japan

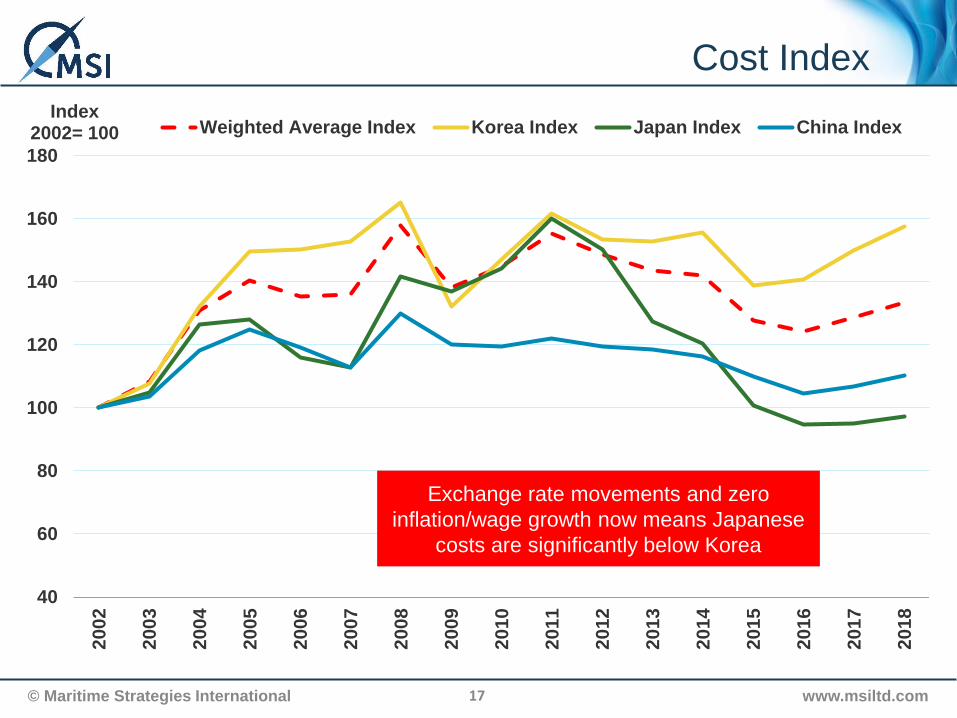

Cost Index

© Maritime Strategies International www.msiltd.com17

40

60

80

100

120

140

160

180

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Index 2002= 100 Weighted Average Index Korea Index Japan Index China Index

Exchange rate movements and zero

inflation/wage growth now means Japanese

costs are significantly below Korea

Exchange Rate Impact – Panamax Bulker

© Maritime Strategies International www.msiltd.com18

0

10

20

30

40

50

60

70

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Value

US$ (Mn) Japan Yen ('00 Mn) Korea Won ('000 Mn) China Yuan ('0 Mn)

Converted to local currency

newbuilding prices have

gone up in Japan

Scrap Price

© Maritime Strategies International www.msiltd.com

Price Developments

20 Year Old Price - % Above Scrap

© Maritime Strategies International www.msiltd.com20

0%

100%

200%

300%

400%

500%

600%

20

k S

R L

PG

5/8

SR

LP

G

VL

GC

LP

G

6k

CE

U P

CT

C

9k

Ch

em

ical

20k C

hem

ical

MR

Ta

nk

er

VL

CC

Ta

nk

er

1.7

kT

EU

FC

C

Su

ezm

ax

Ta

nke

r

LR

2 T

an

ke

r

12

.5k

MP

P

Afr

am

ax

Tan

ker

6.1

kT

EU

FC

C

20

k M

PP

4.3

kT

EU

FC

C

Ca

pe

Bu

lke

r

Su

pra

Bu

lke

r

Pa

na

max

Bu

lker

%

Scrap prices heavily impacting old

tonnage at this end of the spectrum

Scrap Price - Drivers

www.msiltd.com21

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

19

80

-19

90

19

80

-19

91

19

80

-19

92

19

80

-19

93

19

80

-19

94

19

80

-19

95

19

80

-19

96

19

80

-19

97

19

80

-19

98

19

80

-19

99

19

80

-20

00

19

80

-20

01

19

80

-20

02

1980-2

003

19

80

-20

04

19

80

-20

05

19

80

-20

06

19

80

-20

07

19

80

-20

08

1980-2

009

19

80

-20

10

19

80

-20

11

19

80

-20

12

19

80

-20

13

19

80

-20

14

19

80

-20

15

r2

Correlation Period

Demolition Volume Steel Price

Scrap price

unrelated

to volumes

Scrap price

related to

general

steel priceHigh correlation with volume

ISC – Steel Imports from China

© Maritime Strategies International www.msiltd.com22

0.0

0.2

0.4

0.6

0.8

1.0

1.2

01

/20

13

02/2

013

03

/20

13

04

/20

13

05

/20

13

06

/20

13

07

/20

13

08

/20

13

09

/20

13

10

/20

13

11

/20

13

12

/20

13

01/2

014

02

/20

14

03

/20

14

04

/20

14

05

/20

14

06

/20

14

07

/20

14

08

/20

14

09

/20

14

10

/20

14

11

/20

14

12/2

014

01

/20

15

02

/20

15

03

/20

15

04

/20

15

05

/20

15

06

/20

15

07

/20

15

08

/20

15

09

/20

15

10

/20

15

11/2

015

12

/20

15

Mn T

Net increase in steel imports 2015 v

2013 = 700 Handymax Bulkers

Earnings

© Maritime Strategies International www.msiltd.com

Price Developments

Where on the Earnings Cycle Are We?

© Maritime Strategies International www.msiltd.com24

Cru

de a

nd P

roduct T

anker

LP

G C

arr

ier

OS

Vs

PC

TC

Bulk

er

LN

G

MP

P

Conta

iner

Chem

ical T

anker

RoR

o

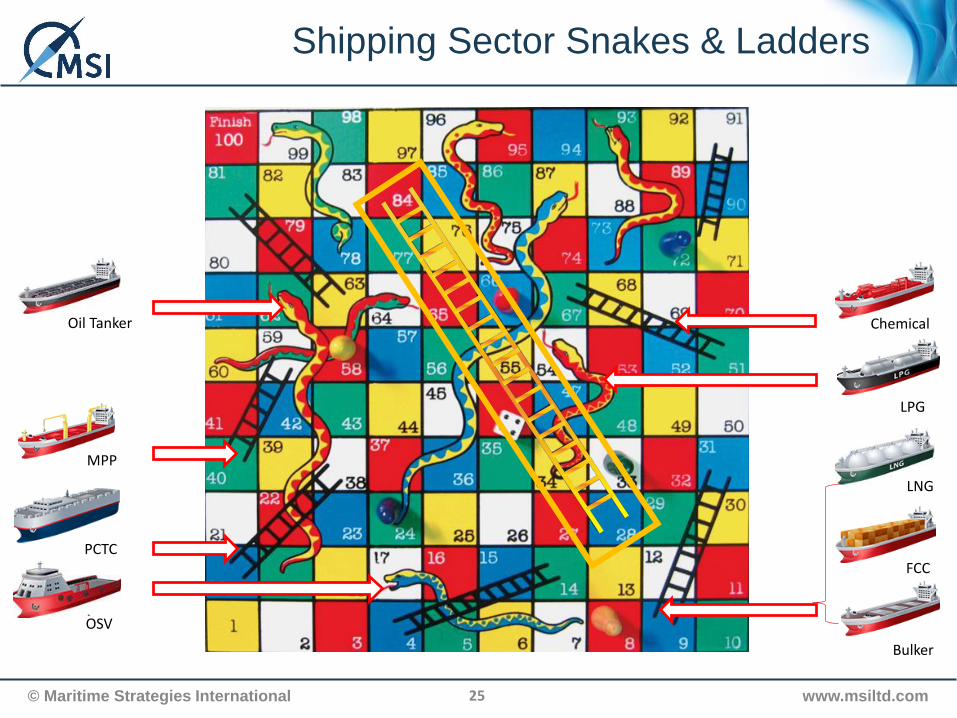

Shipping Sector Snakes & Ladders

© Maritime Strategies International www.msiltd.com25

Oil Tanker

OSV

LPG

PCTC

Bulker

MPP

FCC

LNG

Chemical

… and where are we heading?

© Maritime Strategies International www.msiltd.com26

Cru

de a

nd P

roduct T

anker

LP

G C

arr

ier

OS

Vs

PC

TC

Bulk

er

LN

G

MP

P

Conta

iner

Chem

ical T

anker

RoR

o

Secondhand Prices

© Maritime Strategies International www.msiltd.com

Price Developments

Net Replacement Value – Panamax Bulker

© Maritime Strategies International www.msiltd.com28

Modern Panamax values could fall

further based on historical evidence -

old tonnage is already at all time lows

Historical Range

(1980-2015)

YoS = Year of Sale

Current Depreciation

Net Replacement Value – VLCC Tanker

© Maritime Strategies International www.msiltd.com29

VLCCs are approaching their maximum

historical depreciation

Historical Range

(1980-2015)

YoS = Year of Sale

Current Depreciation

MSI - FMV

© Maritime Strategies International www.msiltd.com30

• MSI Forecast Marine eValuator (FMV) is the first web-based tool to provide forecast and

historical price data covering virtually all of the deepsea shipping fleet.

• Data includes forecasts of newbuilding, second-hand prices, 1 year timecharter rates and

operating costs for specific vessels.

• MSI FMV draws on MSI’s proven, proprietary models and a consistent cross-sectional view

across all principal shipping sectors. It puts asset values in the context of the near term

market to enable reliable benchmarking with outputs based on annual averages.

• Coverage:

Crude Oil Tanker

Product Oil Tanker

Dry Bulk Carrier

Chemical Tanker

LPG Carrier

LNG Carrier

Multi Purpose

Containership

PCC/PCTC

http://www.msiltd.com/fmv

FMV Output

© Maritime Strategies International www.msiltd.com31

Quarterly Fair Market Value &1 Year Time Charter Rate (1Qhistory, current Q, 2Q forecast

Annual average:• Newbuilding contract price• Fair Market Value• 1 Year Time Charter Rate• Operating Cost5 years history and 15 yearsforecast

Price Development Chartdetailing forecast pricedevelopment in relation tohistorical metrics

http://www.msiltd.com/fmv

Sector Attractiveness - IRR

© Maritime Strategies International www.msiltd.com32

Summary

© Maritime Strategies International www.msiltd.com33

• Current secondhand prices only make sense if all drivers are viewed together

• Many shipyards will be underemployed in 2017, especially those yards bulkers

focus

• There will be further yard capacity closures, this will help support newbuilding prices

in the medium term

• Costs and exchange rates will help determine what yards survive

• Scrap prices will not recover whilst ISC imports cheap Chinese steel

• Shipping remains cyclical and what goes down must go up (eventually!)

• Bulker and Tanker depreciations are currently at historical extremes

• MSI’s Forecast Marine eValuator (FMV) online product can show the attractiveness

of a specific vessel, in terms of both value and cash flow projections

© Maritime Strategies International www.msiltd.com34

Thank you

For over 30 years, MSI has developed integrated relationships with a diverse clientbase of financial institutions, ship owners, shipyards, brokers, investors, insurersand equipment and service providers.

MSI’s expertise covers a broad range of shipping sectors, providing clients with acombination of sector reports, forecasting models, vessel valuations and bespokeconsultancy services.

MSI is staffed by economists and scientists offering a structured quantitativeperspective to shipping analysis combined with a wide range of industryexperience.

MSI balances analytical power with service flexibility, offering a comprehensivesupport structure and a sound foundation on which to build investment strategiesand monitor/assess exposure to market risks.

MSI Background

© Maritime Strategies International www.msiltd.com35

While this document has been prepared, and is presented, in good faith, MaritimeStrategies International assumes no responsibility for errors of fact, opinion ormarket changes, and cannot be held responsible for any losses incurred or actionarising as a result of information contained in this document.

The copyright and other intellectual property rights in data, information or advicecontained in this document are and will at all times remain the property ofMaritime Strategies International.

Disclaimer

© Maritime Strategies International www.msiltd.com36

6 Baden Place

Crosby Row

London SE1 1YW

United Kingdom

Tel: +44 (0)207 940 0070

Fax: +44 (0)207 940 0071

Email: [email protected]

www.msiltd.com

Maritime Strategies International Ltd