Price $98.47 October 21, 2015 (from $120.00) Equity Analyst … · By 2017, we think the online...

50

USD Prev. 2013A Prev. 2014A Prev. 2015E Prev. 2016E Rev. (MM) -- 7,872.0 -- 12,466.0 -- 17,001.0 22,904.0 24,196.0 EPS Non-GAAP Mar -- 0.12 -- 0.36 -- 0.42A -- -- Jun -- 0.19 -- 0.43 -- 0.50A -- -- Sep -- 0.25 -- 0.43 -- 0.50 -- -- Dec -- 0.31 -- 0.54 -- 0.62 -- -- FY Dec -- 0.87 -- 1.77 -- 1.97 2.68 2.78 FY P/EPS Non- GAAP 113.2x 55.6x 50.0x 35.4x Price Performance OCT-14 FEB-15 JUN-15 OCT-15 100 90 80 70 Target Change USA | Technology | Internet October 21, 2015 Facebook, Inc. (FB) Video Ads and Instagram - Facebook's Next Billion-Dollar Businesses EQUITY RESEARCH AMERICAS BUY Price target $130.00 (from $120.00) Price $98.47 Financial Summary Net Debt (MM): ($14,125.0) Cash/Share: $5.39 5 Yr. Rev. CAGR: 24.0% Market Data 52 Week Range: $99.24 - $72.00 Total Entprs. Value (MM): $286,503.9 Market Cap. (MM): $300,628.9 Shares Out. (MM): 3,053.0 Float (MM): 2,168.3 Avg. Daily Vol.: 32,975,148 Jefferies US Internet Team * Jefferies Equity Research [email protected] Brian Pitz * Equity Analyst (212) 336-7413 [email protected] Brian Fitzgerald * Equity Analyst (212) 284-2491 [email protected] Timothy O'Shea * Equity Associate (212) 284-3415 [email protected] Stan Velikov, CFA * Equity Associate (415) 229-1534 [email protected] Corey Werbelow * Equity Associate (212) 284-2191 [email protected] John Streppa, CFA * Equity Associate (212) 738-5794 [email protected] * Jefferies LLC Key Takeaway We are raising estimates and PT to $130 as we grow increasingly confident around key growth drivers especially Instagram, video ads, & the Audience Network. For Instagram we model base case revs of $531MM in '16, growing to $1.4B in '17. See our detailed analysis starting page 25. We also believe they will become a multi-billion dollar business for FB within the next two years as TV ad budgets shift online. Video ads: the perfect storm. As video consumption explodes across FB's massive user base, we think FB looks well positioned to capture an increasing portion of TV ad budgets as marketers migrate toward data-driven, highly-targeted online video ad campaigns. By '17, we think the online video ad opportunity could be worth ~$17B / year in the US alone. We think Facebook and YouTube look best positioned to capture the bulk of that spend. As such, we believe video ads will become a multi-billion dollar business for FB within the next two years. We are optimistic as Instagram opens up to all advertisers. With its beautiful visual layout & massive (400MM MAUs), highly engaged audience, Instagram looks like a natural ad platform to us. Importantly, Instagram ads will leverage FB's anonymized user data, which nearly ensures these ads will deliver a similar bang-for-your-buck as core FB mobile ads. Our base case 2016 Instagram rev estimate is $531MM, which we grow to $1.4B in 2017. See our analysis and detailed rev build starting p. 25. We are raising estimates as we grow increasingly confident around key go-forward growth drivers especially Instagram, video ads, and the Facebook Audience Network. Also, we note several other growth levers including WhatsApp, Messenger, Oculus, and a mix shift towards pricier ad formats over time (bottom funnel, video). 3Q checks suggest robust growth as expense levels remain the wild card. IgnitionOne noted FB continues to outpace the market in programmatic display during 3Q. Also, AdRoll noted its retargeting clients increased their ad spend on FB by 31% Y/Y, suggesting uptake of FB's Dynamic Product Ads (DPAs) could be robust as we head toward the holiday shopping season. For 3Q, we model $4.31B rev, $3.25B mobile rev, and $0.50 NG EPS vs. $4.37B, $3.24B, and $0.52 consensus, respectively. Valuation/Risks We raise our PT from $120 to $130 on optimism around key go-forward growth drivers. Our PT is based on a 10-year DCF (4% LTGR; 10% WACC). FB trades at ~16x our '16 Adj. EBITDA estimate vs. our 35% 3-year EBITDA CAGR. Risks: User declines. Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 46 to 50 of this report.

Transcript of Price $98.47 October 21, 2015 (from $120.00) Equity Analyst … · By 2017, we think the online...

USD Prev. 2013A Prev. 2014A Prev. 2015E Prev. 2016E

Rev. (MM) -- 7,872.0 -- 12,466.0 -- 17,001.0 22,904.0 24,196.0

EPS Non-GAAP

Mar -- 0.12 -- 0.36 -- 0.42A -- --

Jun -- 0.19 -- 0.43 -- 0.50A -- --

Sep -- 0.25 -- 0.43 -- 0.50 -- --

Dec -- 0.31 -- 0.54 -- 0.62 -- --

FY Dec -- 0.87 -- 1.77 -- 1.97 2.68 2.78

FY P/EPS Non-GAAP

113.2x 55.6x 50.0x 35.4x

Price Performance

OCT-14 FEB-15 JUN-15 OCT-15

100

90

80

70

Target Change

USA | Technology | Internet October 21, 2015

Facebook, Inc. (FB)Video Ads and Instagram - Facebook's NextBillion-Dollar Businesses

EQU

ITY R

ESEARC

H A

MERIC

AS

BUYPrice target $130.00

(from $120.00)Price $98.47

Financial SummaryNet Debt (MM): ($14,125.0)Cash/Share: $5.395 Yr. Rev. CAGR: 24.0%

Market Data52 Week Range: $99.24 - $72.00Total Entprs. Value (MM): $286,503.9Market Cap. (MM): $300,628.9Shares Out. (MM): 3,053.0Float (MM): 2,168.3Avg. Daily Vol.: 32,975,148

Jefferies US Internet Team *Jefferies Equity Research

[email protected] Pitz *

Equity Analyst(212) 336-7413 [email protected]

Brian Fitzgerald *Equity Analyst

(212) 284-2491 [email protected] O'Shea *

Equity Associate(212) 284-3415 [email protected]

Stan Velikov, CFA *Equity Associate

(415) 229-1534 [email protected] Werbelow *

Equity Associate(212) 284-2191 [email protected]

John Streppa, CFA *Equity Associate

(212) 738-5794 [email protected]

* Jefferies LLC

Key TakeawayWe are raising estimates and PT to $130 as we grow increasingly confidentaround key growth drivers especially Instagram, video ads, & the AudienceNetwork. For Instagram we model base case revs of $531MM in '16, growing to$1.4B in '17. See our detailed analysis starting page 25. We also believe theywill become a multi-billion dollar business for FB within the next two years asTV ad budgets shift online.

Video ads: the perfect storm. As video consumption explodes across FB's massive userbase, we think FB looks well positioned to capture an increasing portion of TV ad budgetsas marketers migrate toward data-driven, highly-targeted online video ad campaigns. By'17, we think the online video ad opportunity could be worth ~$17B / year in the US alone.We think Facebook and YouTube look best positioned to capture the bulk of that spend.As such, we believe video ads will become a multi-billion dollar business for FBwithin the next two years.

We are optimistic as Instagram opens up to all advertisers. With its beautiful visuallayout & massive (400MM MAUs), highly engaged audience, Instagram looks like a naturalad platform to us. Importantly, Instagram ads will leverage FB's anonymized user data,which nearly ensures these ads will deliver a similar bang-for-your-buck as core FB mobileads. Our base case 2016 Instagram rev estimate is $531MM, which we grow to$1.4B in 2017. See our analysis and detailed rev build starting p. 25.

We are raising estimates as we grow increasingly confident around key go-forwardgrowth drivers especially Instagram, video ads, and the Facebook Audience Network. Also,we note several other growth levers including WhatsApp, Messenger, Oculus, and a mixshift towards pricier ad formats over time (bottom funnel, video).

3Q checks suggest robust growth as expense levels remain the wild card.IgnitionOne noted FB continues to outpace the market in programmatic display during3Q. Also, AdRoll noted its retargeting clients increased their ad spend on FB by 31% Y/Y,suggesting uptake of FB's Dynamic Product Ads (DPAs) could be robust as we head towardthe holiday shopping season. For 3Q, we model $4.31B rev, $3.25B mobile rev, and $0.50NG EPS vs. $4.37B, $3.24B, and $0.52 consensus, respectively.

Valuation/RisksWe raise our PT from $120 to $130 on optimism around key go-forward growth drivers. OurPT is based on a 10-year DCF (4% LTGR; 10% WACC). FB trades at ~16x our '16 Adj. EBITDAestimate vs. our 35% 3-year EBITDA CAGR. Risks: User declines.

Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have a conflictof interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 46 to 50 of this report.

Table of Contents The Perfect Storm: Online Video Ads Page 3

Video Consumption on Facebook is Soaring -- Page 4

Early Video Ad Trends Look Encouraging – Page 5

New Immersive Video Formats – Page 8

Sizing the Video Advertising Opportunity – Page 15 Omnicom Advises Advertisers to Shift 10-25% of TV Ad-Dollars to Online Video – Page 17 Discussions with Media Firms to Produce Professional Videos for FB – Page 17

TV + Online Video Convergence: A Deeper Dive Page 18 A Bit of Background on Gross Rating Point (GRP) Definition and Calculations – Page 19

Traditional GRP to iGRP Translation – Page 20 Practical Example – Online Video Advertising – Page 21 What are the Near-Term Impacts? – Page 23

Instagram: A Picture Perfect Ad Platform Page 25

Sizing Instagram’s Revenue Opportunity – Page 25 Visualizing an Instagram Ad – Page 31

Facebook Audience Network Page 35 Instant Articles Bring High Quality Content Direct to the Mobile Feed Page 36 3Q Checks and Recent KPI Trends Page 38 Raising Estimates Page 40 Facebook Model Page 41 Comp Sheet Page 44

FB

Target Change

October 21, 2015

page 2 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

The Perfect Storm: Online Video Ads

Video usage on Facebook is soaring as (portions of) TV ad budgets shift online As video consumption explodes across Facebook’s massive user base, we think the

company looks well positioned to capture an increasing portion of TV ad budgets as

marketers migrate towards data-driven, highly-targeted online video ad campaigns.

From an advertiser’s perspective, FB offers a compelling video ad product defined by:

Massive reach: A global audience of ~900MM+ people each day. A mobile

Super Bowl in the US every single day.

High engagement: FB users are already viewing 4B videos per day.

A clean, well-lit environment: A brand-safe advertising environment.

Best-in-class user data and ad-tech stack: Advertisers can leverage

Facebook’s data-set to run targeted ad campaigns.

By 2017, we think the online video advertising opportunity will be worth ~$17B per year

in the US alone. We think Facebook and Google (YouTube) look best positioned to

capture a meaningful portion of this spend.

The implication here is that video ads should become a multi-billion dollar business for

Facebook within the next two years, with significant upside if TV ad budgets shift online

faster than expected.

Note this new revenue stream won’t be 100% incremental given video ads will displace

other, lower priced ads (as FB keeps ad-loads mostly stable).

We believe video ads will become a

multi-billion dollar business for

Facebook within the next two years.

FB

Target Change

October 21, 2015

page 3 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

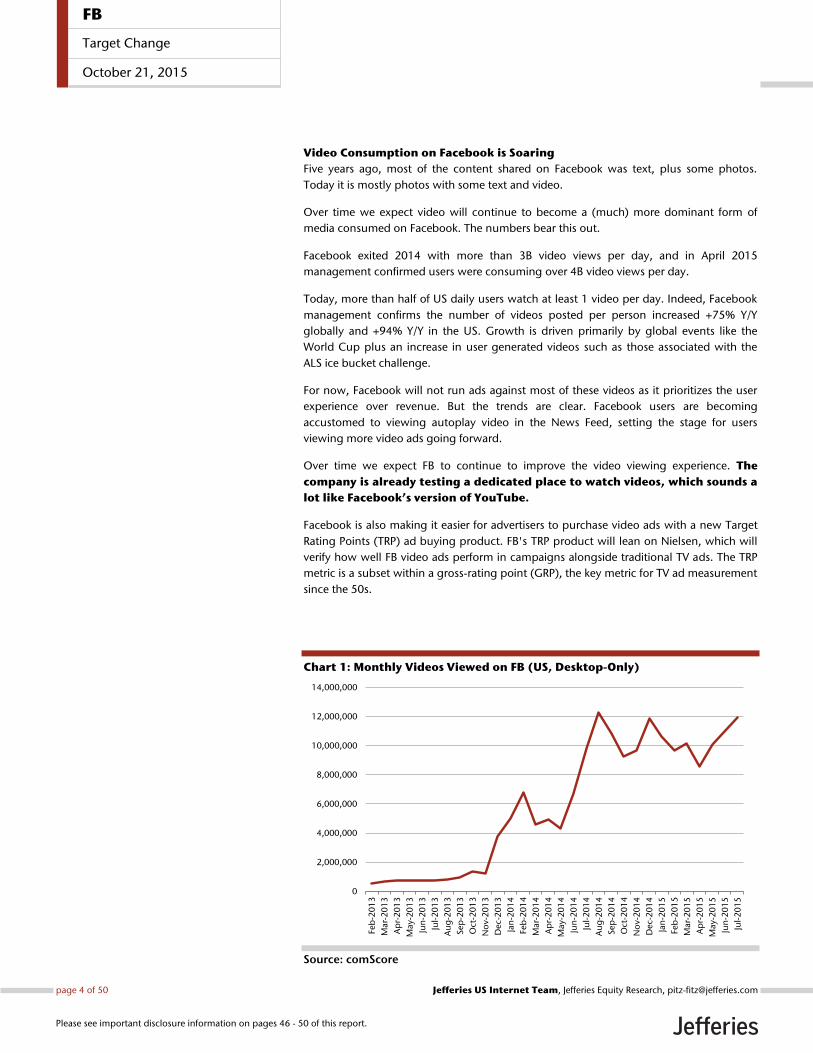

Video Consumption on Facebook is Soaring

Five years ago, most of the content shared on Facebook was text, plus some photos.

Today it is mostly photos with some text and video.

Over time we expect video will continue to become a (much) more dominant form of

media consumed on Facebook. The numbers bear this out.

Facebook exited 2014 with more than 3B video views per day, and in April 2015

management confirmed users were consuming over 4B video views per day.

Today, more than half of US daily users watch at least 1 video per day. Indeed, Facebook

management confirms the number of videos posted per person increased +75% Y/Y

globally and +94% Y/Y in the US. Growth is driven primarily by global events like the

World Cup plus an increase in user generated videos such as those associated with the

ALS ice bucket challenge.

For now, Facebook will not run ads against most of these videos as it prioritizes the user

experience over revenue. But the trends are clear. Facebook users are becoming

accustomed to viewing autoplay video in the News Feed, setting the stage for users

viewing more video ads going forward.

Over time we expect FB to continue to improve the video viewing experience. The

company is already testing a dedicated place to watch videos, which sounds a

lot like Facebook’s version of YouTube.

Facebook is also making it easier for advertisers to purchase video ads with a new Target

Rating Points (TRP) ad buying product. FB's TRP product will lean on Nielsen, which will

verify how well FB video ads perform in campaigns alongside traditional TV ads. The TRP

metric is a subset within a gross-rating point (GRP), the key metric for TV ad measurement

since the 50s.

Chart 1: Monthly Videos Viewed on FB (US, Desktop-Only)

Source: comScore

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

Feb

-20

13

Mar-

20

13

Ap

r-2

01

3

May-

20

13

Jun

-20

13

Jul-

20

13

Au

g-2

01

3

Sep

-20

13

Oct

-20

13

No

v-2

01

3

Dec-

20

13

Jan

-20

14

Feb

-20

14

Mar-

20

14

Ap

r-2

01

4

May-

20

14

Jun

-20

14

Jul-

20

14

Au

g-2

01

4

Sep

-20

14

Oct

-20

14

No

v-2

01

4

Dec-

20

14

Jan

-20

15

Feb

-20

15

Mar-

20

15

Ap

r-2

01

5

May-

20

15

Jun

-20

15

Jul-

20

15

FB

Target Change

October 21, 2015

page 4 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Early Video Ad Trends Look Encouraging

While Facebook’s video ad business is in the early stages, early trends look encouraging.

1) Per comScore, on a 3 month rolling basis (Apr – June 2015 vs. 2014), the number of

video ads on Facebook increased +649% Y/Y.

Additionally, the number of video ads viewed per user continues to rise. Currently,

users in the US (desktop only) view ~1.6 ads. This is a low number and should rise

over time; another growth lever.

Chart 2: Video Ads on Facebook (US, Desktop-Only)

Source: comScore

0

500

1,000

1,500

2,000

FB

Target Change

October 21, 2015

page 5 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Chart 3: Video Ad Loads on Facebook (US, Desktop-Only)

Source: comScore

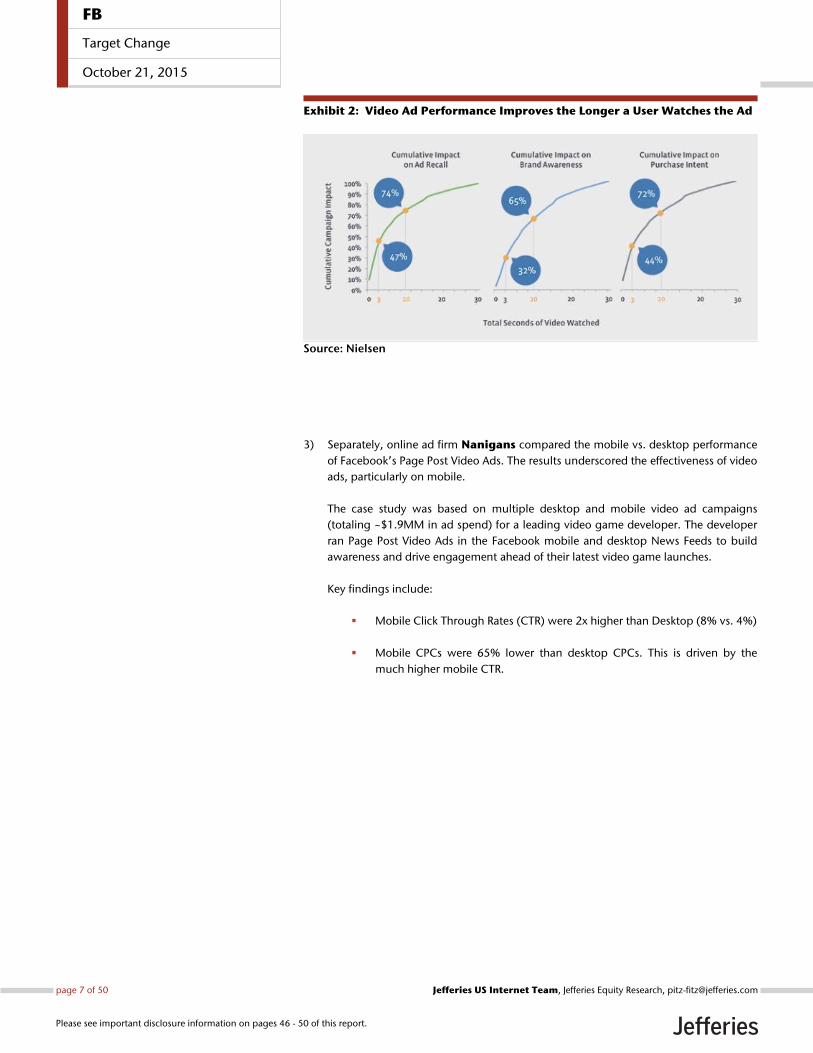

2) According to a Facebook-commissioned Nielsen study, Facebook users are

impacted by video ads even before viewing them for a full second. According to the

study:

Results show that from the moment a video ad was viewed (even before one

second), lift happened across ad recall, brand awareness and purchase

consideration. This means that even people who never watched the video but did

see the impression were still impacted by the ad. And, as expected, lift increased the

longer people watch the ad.

Exhibit 1: Example Facebook Video Ad Unit

Source: Nielsen

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

FB

Target Change

October 21, 2015

page 6 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Exhibit 2: Video Ad Performance Improves the Longer a User Watches the Ad

Source: Nielsen

3) Separately, online ad firm Nanigans compared the mobile vs. desktop performance

of Facebook’s Page Post Video Ads. The results underscored the effectiveness of video

ads, particularly on mobile.

The case study was based on multiple desktop and mobile video ad campaigns

(totaling ~$1.9MM in ad spend) for a leading video game developer. The developer

ran Page Post Video Ads in the Facebook mobile and desktop News Feeds to build

awareness and drive engagement ahead of their latest video game launches.

Key findings include:

Mobile Click Through Rates (CTR) were 2x higher than Desktop (8% vs. 4%)

Mobile CPCs were 65% lower than desktop CPCs. This is driven by the

much higher mobile CTR.

FB

Target Change

October 21, 2015

page 7 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

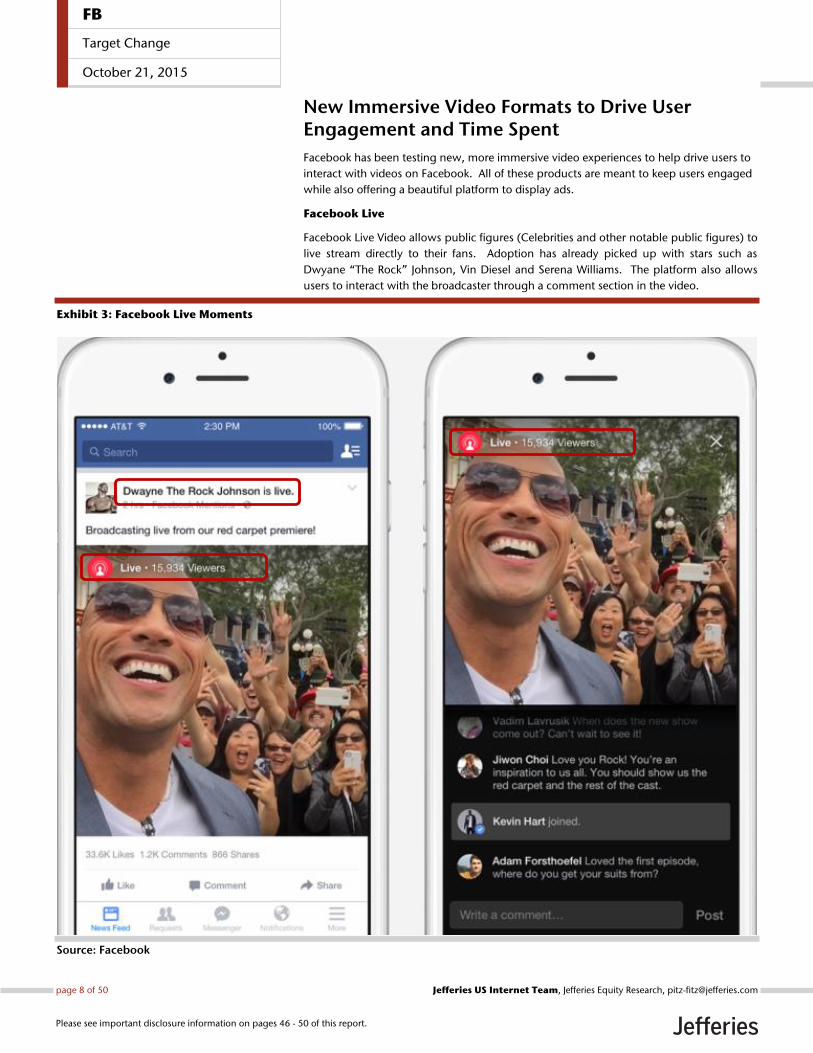

New Immersive Video Formats to Drive User Engagement and Time Spent

Facebook has been testing new, more immersive video experiences to help drive users to

interact with videos on Facebook. All of these products are meant to keep users engaged

while also offering a beautiful platform to display ads.

Facebook Live

Facebook Live Video allows public figures (Celebrities and other notable public figures) to

live stream directly to their fans. Adoption has already picked up with stars such as

Dwyane “The Rock” Johnson, Vin Diesel and Serena Williams. The platform also allows

users to interact with the broadcaster through a comment section in the video.

Exhibit 3: Facebook Live Moments

Source: Facebook

FB

Target Change

October 21, 2015

page 8 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

The NBA used Facebook Live to simulcast “NBA Real Training Camp” earlier in the year.

The first of its kind event highlighted the ability of brands to bring their content directly to

the consumers. The show had pre-season practice content and interviews with players,

coaches, and other team personnel. The stream happened at noon ET which the NBA said

was “perfect for this type of initiative. A large portion of your audience is going to be at

their computer or on their mobile phone or tablet.”

Exhibit 4: "NBA Real Training Camp"

Source: Facebook

FB

Target Change

October 21, 2015

page 9 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

360 Videos

Facebook has also revealed 360 Videos that allow the user to view a video from all angles

in their News Feed. Star Wars, Discovery, GoPro, and Lebron James have all published

360 videos. Similar to the YouTube product, the 360 videos allow an immersive

experience where users can explore their surroundings in a video by moving their device

around. Facebook envisions this as a product where friends can join their friends on a

vacation or discover new content from their favorite publishers. Vice News has even used

this feature to broadcast the news so users can have a real sense of what is happening.

The Facebook team worked closely with the Oculus team to develop this technology

which could hint at bringing more 360 degree content to the Oculus Rift (owned by

Facebook).

Exhibit 5: Facebook 360 Videos

Source: Facebook

FB

Target Change

October 21, 2015

page 10 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Suggested Videos

Facebook is also testing new video delivery services such as Suggested Videos. Currently

being tested on iPhones, Suggested Videos allows users the ability to discover multiple

related videos after a video has been watched from the News Feed. Suggested Videos has

rolled out to iPhones globally and Facebook is starting to test ads within the experience.

This feature will help increase the amount of time that Facebook users are viewing videos.

Exhibit 6: Suggested Videos

Source: Facebook

FB

Target Change

October 21, 2015

page 11 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Floating Video Displays – Videos for the Multi-tasker

Facebook has also been testing ways to allow the user to continue to consume his/her

favorite video content while also being able to continue to scroll through his/her news

feed. Floating videos will let users start watching a video and then place it in the top

corner of the screen to allow access to the rest of their News Feed.

Exhibit 7: Floating Videos

Source: Facebook

FB

Target Change

October 21, 2015

page 12 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Videos- A Dedicated Page for Videos

Lastly, Facebook has also tested a dedicated page on Facebook exclusively for video

content. Videos from friends, pages a user follows, or videos a user has saved for later,

and other video publishers will be available for users on the page. This tool will be a

destination for users to discover, share, and like new video content and will serve as

another platform for Facebook to serve video ads on.

Exhibit 8: Dedicated Videos Page

Source: Facebook

FB

Target Change

October 21, 2015

page 13 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

New Tools For Publishers As Well

With these new video platforms, Facebook is also working on developing the tools for

publishers to understand how their content is being consumed. Page owners will now be

able to analyze the number of views and 30-second views across the entire page

(previously this was limited to a per video basis). Page owners will also be able to see

breakdowns of organic vs. paid, auto-played vs. clicked-to-play, and unique vs. repeat

views to gain insights into the Page’s audience. Publishers will also be able to examine

their top videos over a specific time period as well as have access to information such as

views, reach, and other helpful video metrics.

Exhibit 9: Facebook Video Insights

Source: Facebook

Exhibit 10: Top Video Insights

Source: Facebook

FB

Target Change

October 21, 2015

page 14 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Sizing the Video Advertising Opportunity

The Online Advertising Industry is one of the fastest growing subsections of the

advertising ecosystem. According to our estimates, online video advertising spend is

expected to reach $10B+ in spend by 2015 (surpassing $17B by 2017) in the U.S

alone, or a 3 year CAGR of 35% (’13-’17) vs. 16% (’13-’17) for overall online

advertising spend.

Chart 4: US Online Video as a Percentage of the Overall Online Ad Spend ($B)

Source: Jefferies, Magna, IAB

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2010 2011 2012 2013 2014 2015 2016 2017

Total Online Advertising Spend Online Video

By 2017, we believe online video ads

will be a $17B / year opportunity in

the US alone.

FB

Target Change

October 21, 2015

page 15 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Table 1: Jefferies US Online Advertising Model (includes mobile)

Source: Jefferies, IAB, eMarketer

Table 2: Facebook Video Advertising Revenue Estimates ($MM)

FB US Video Advertising 0 150 910 1,853 2,600

% YoY Growth - - 507% 104% 40%

FB Int’l Video Advertising 50 490 998 1,400

% YoY Growth - - 880% 104% 40%

TOTAL FB Video Advertising - 200 1,400 2,850 4,000

% YoY Growth - - 600% 104% 40%

Source: IAB, MagnaGlobal, Company Reports, Jefferies Estimates

2012A 2013A 2014A 2015E 2016E 2017E 13-17 CAGR

Search 18,039 20,726 23,201 26,541 30,252 34,160

growth Y/Y 15.9% 14.9% 11.9% 14.4% 14.0% 12.9% 13.3%

% of Total Spend 49.3% 48.4% 46.8% 46.1% 45.9% 45.8%

Banner + Rich Media + Sponsorship 10,802 12,398 13,650 15,343 16,971 18,385

growth Y/Y 16.8% 14.8% 10.1% 12.4% 10.6% 8.3% 10.4%

% of Total Spend 29.5% 29.0% 27.5% 26.7% 25.8% 24.7%

Banner 8,844 10,304 11,469 13,127 14,697 16,110

growth Y/Y 29.9% 16.5% 11.3% 14.5% 12.0% 9.6% 11.8%

% of Total Spend 24.2% 24.1% 23.1% 22.8% 22.3% 21.6%

Rich Media 1,113 1,328 1,438 1,497 1,582 1,604

growth Y/Y -15.4% 19.3% 8.3% 4.1% 5.7% 1.4% 4.8%

% of Total Spend 3.0% 3.1% 2.9% 2.6% 2.4% 2.2%

Sponsorship 845 766 744 720 692 671

growth Y/Y -24.6% -9.3% -2.9% -3.2% -3.8% -3.0% -3.2%

% of Total Spend 2.3% 1.8% 1.5% 1.3% 1.1% 0.9%

Video 3,453 5,145 7,295 9,903 13,050 16,856

growth Y/Y 32.5% 49.0% 41.8% 35.7% 31.8% 29.2% 34.5%

% of Total Spend 9.4% 12.0% 14.7% 17.2% 19.8% 22.6%

Classified (& auctions) 2,430 2,597 2,925 3,109 3,164 3,356

growth Y/Y -5.8% 6.9% 12.6% 6.3% 1.8% 6.1% 6.6%

% of Total Spend 6.6% 6.1% 5.9% 5.4% 4.8% 4.5%

Referrals/Lead Generation 1,689 1,749 2,355 2,533 2,373 1,753

growth Y/Y 11.0% 3.6% 34.6% 7.6% -6.3% -26.1% 0.1%

% of Total Spend 4.6% 4.1% 4.8% 4.4% 3.6% 2.4%

Email 156 165 149 144 99 75

growth Y/Y -26.8% 5.8% -9.9% -3.2% -31.3% -24.6% -18.0%

% of Total Spend 0.4% 0.4% 0.3% 0.3% 0.2% 0.1%

FB

Target Change

October 21, 2015

page 16 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Omnicom CEO Advises Marketers to Shift 10-25% of TV Ad-Dollars to Online

Video

In late 2014, the CEO of ad-giant Omnicom’s media operations Daryl Simm advised

marketers to move 10% to 25% of TV ad dollars to online video. Omnicom oversees

~$54B of annual ad spend, including major brand campaigns from the likes of PepsiCo,

Visa, McDonald’s and Apple.

We believe this is yet more evidence we are approaching an inflection point where

meaningful chunks of TV ad budgets will begin to shift online, with Facebook being an

obvious beneficiary.

The offline-to-online shift will be driven by a surge in marketers’ desire for more

measurement around video ad campaigns. Measurement and accountability are the

hallmarks of online advertising, where advertisers can more easily calculate the ‘bang for

their advertising buck’.

Simm also said the amount of [high] quality online video is still an issue. In order for more

money to shift to online video, there is a need for even more premium and relevant

content. This brings us to our next point.

Facebook is Reportedly in Discussions With Several Media Firms to Produce

More Professional Short-Form Videos for the Social Network

According to a March 24 article in The Information, Facebook is in discussions with media

firms like Vice, The Onion and Vox Media to produce short-form video that will be

injected directly into users’ News Feeds.

The videos are expected to be rolled out later this year, and Facebook and its content

partners will be looking for advertisers to sponsor the videos in the coming weeks.

FB

Target Change

October 21, 2015

page 17 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

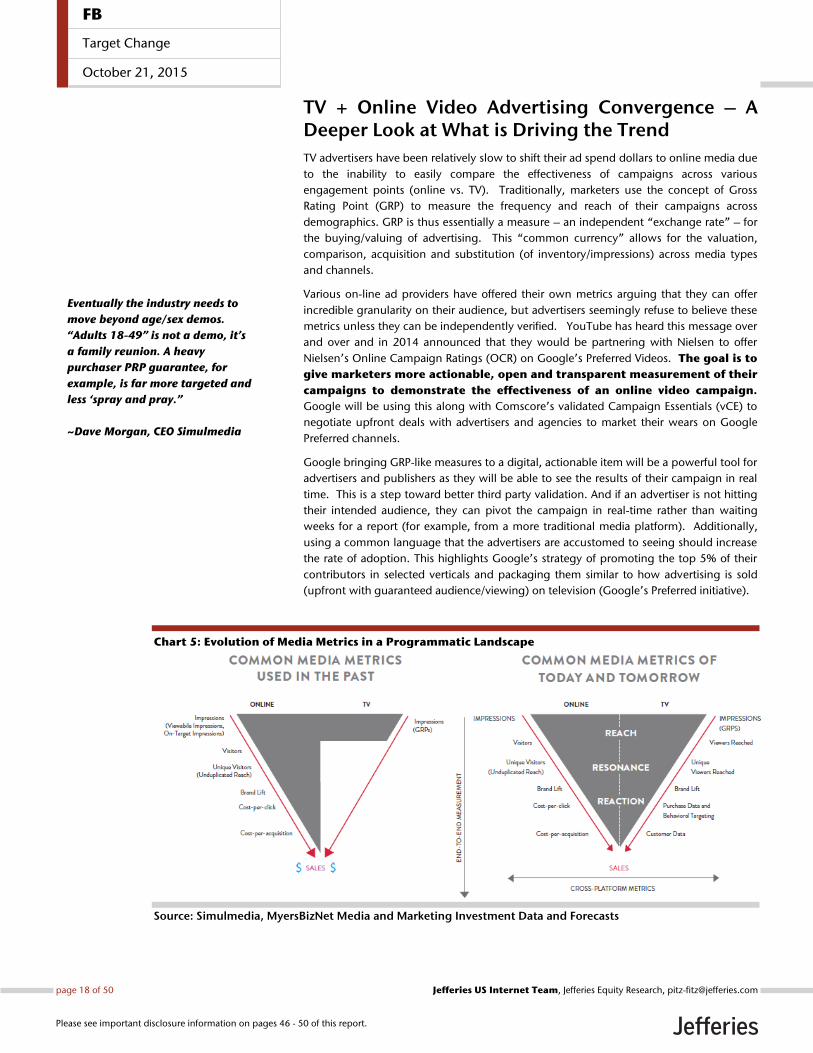

TV + Online Video Advertising Convergence – A Deeper Look at What is Driving the Trend

TV advertisers have been relatively slow to shift their ad spend dollars to online media due

to the inability to easily compare the effectiveness of campaigns across various

engagement points (online vs. TV). Traditionally, marketers use the concept of Gross

Rating Point (GRP) to measure the frequency and reach of their campaigns across

demographics. GRP is thus essentially a measure – an independent “exchange rate” – for

the buying/valuing of advertising. This “common currency” allows for the valuation,

comparison, acquisition and substitution (of inventory/impressions) across media types

and channels.

Various on-line ad providers have offered their own metrics arguing that they can offer

incredible granularity on their audience, but advertisers seemingly refuse to believe these

metrics unless they can be independently verified. YouTube has heard this message over

and over and in 2014 announced that they would be partnering with Nielsen to offer

Nielsen’s Online Campaign Ratings (OCR) on Google’s Preferred Videos. The goal is to

give marketers more actionable, open and transparent measurement of their

campaigns to demonstrate the effectiveness of an online video campaign.

Google will be using this along with Comscore’s validated Campaign Essentials (vCE) to

negotiate upfront deals with advertisers and agencies to market their wears on Google

Preferred channels.

Google bringing GRP-like measures to a digital, actionable item will be a powerful tool for

advertisers and publishers as they will be able to see the results of their campaign in real

time. This is a step toward better third party validation. And if an advertiser is not hitting

their intended audience, they can pivot the campaign in real-time rather than waiting

weeks for a report (for example, from a more traditional media platform). Additionally,

using a common language that the advertisers are accustomed to seeing should increase

the rate of adoption. This highlights Google’s strategy of promoting the top 5% of their

contributors in selected verticals and packaging them similar to how advertising is sold

(upfront with guaranteed audience/viewing) on television (Google’s Preferred initiative).

Chart 5: Evolution of Media Metrics in a Programmatic Landscape

Source: Simulmedia, MyersBizNet Media and Marketing Investment Data and Forecasts

Eventually the industry needs to

move beyond age/sex demos.

“Adults 18-49” is not a demo, it’s

a family reunion. A heavy

purchaser PRP guarantee, for

example, is far more targeted and

less ‘spray and pray.”

~Dave Morgan, CEO Simulmedia

FB

Target Change

October 21, 2015

page 18 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Reaching specific audiences remains key for advertisers— and that means hitting the right

consumers, not just the most / largest audience. So there is a need for campaign-specific

ratings (“currencies”) standardized across platforms. Accordingly, OCR integration offers

metrics comparable to TV ratings – so all parties have the ability to observe an audience in

real-time and compare data across devices and platforms. As Dave Morgan from

Simulmedia points out -- the need for impact-based (vs reach-based) advertising

mechanisms will increasingly play a part in leading the convergence of TV and online.

A Bit of Background -- Gross Rating Point (GRP) Definition and Calculation

While GRP began as a manual process of multiplying the number of insertions with each

rating point and then summing them together to form GRP, a simpler formula has since

been developed -- GRP is an advertising measurement term used to express the size of an

audience reached by a specific media or schedule. Specifically, GRPs quantify impressions

as a percentage of the population reached (versus absolute numbers reached). Target

Rating Points (TRP) are also used in similar fashion, but focus on a more narrowly defined

target audience.

GRP is the sum of ratings achieved by a specific media vehicle or schedule. It measures the

total volume of delivery of an advertiser’s message to the target audience. The formula is:

GRP= Reach x Frequency x 100

where

Reach = Unique Target audience segment/Target Universe size -- The numerator

is the target audience reached (actual unduplicated impressions delivered); the

denominator is the universe size based on the total US population for that

specific target (i.e., the number of TV households tuned into a program / total

number of TV households)

Frequency = the number of times that the average household or person is

exposed to the advertising schedule (i.e., how many times the audience has the

opportunity to see a commercial)

The chart below illustrates GRP calculation, reach and frequency. Each home shows

which days the TV set was turned on during the time which a specific show was playing.

Each home represents 10% of the universe of 10 homes, therefore, each represents a 10

rating every time the show plays.

Chart 6: Sample GRP, Reach and Frequency Calculation

Source: Jefferies

M, ThM, T, W

T, W, FTh, FT W, Th

W, F

FB

Target Change

October 21, 2015

page 19 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

So the total GRP for this selected campaign can be calculated as follows:

Monday = 20 Rating

Tuesday = 30 Rating

Wednesday = 40 Rating

Thursday = 30 Rating

Friday = 30 Rating

Total GRP: 150

Reach: 70 (Viewing households/ Total TV households = 7/10 * 100 = 70)

Frequency: 2.14 (GRP/Reach = 150/70 = 2.143)

Alternatively, GRPs may be calculated as a specific number of impressions delivered to a

target universe as outlined in this formula:

GRP= (Target Impressions / Target Universe Size) x 100

For example, a sample GRP calculation using this Target Impressions formula:

Male 18-24 Impressions

US Population Male 18-24

GRP

23,512,500 15,675,000 = (23,512,500 / 15,675,000) x 100 = 150

Nielsen National People Meter further extended the rating originally based on HH to

individual, further allowing rating points to be assigned to different demographic

populations.

The widespread adoption of GRP allowed it to become the common currency for media

planning and reporting for TV commercials.

Traditional GRP to iGRP Translation

While still early days, Comscore’s vCE and Nielsen’s OCR provide data that may help

advertisers bridge the gap between offline and online media campaign weighted reach

metrics to compare the advertising strength of various media vehicles.

Comscore’s Campaign Essentials utilizes one million UVs (with 250,000 contributing to

demographic projections monthly). Validated CE (vCE) expanded upon CE in 2012,

incorporating impressions served to PCs, in-geo (country) and viewability and outlier

activities into score reporting. Though vCE is not universally applicable (especially for

pre-roll video due to iFrame limitations), it is widely accepted as a trusted third-party

reporting for impressions in target, UVs in target and average frequency – all necessary

components for computing iGRPs.

Nielsen holds the industry standard in TV rating and can be seen as the founder of TV

GRP. Online Campaign Ratings (OCR) were launched in 2011, originally leveraging

Facebook registrations calculated with the Nielsen multiplatform home panel for demo

reporting. Placement and geo reporting were added in 2012, and Nielsen currently

utilizes its access to more than 150 million privacy-protected registered users, directly

assigning actual demographics to 30-50% of campaign impressions. Nielsen’s strong tie

to traditional media planning has made OCR a highly demanded tool.

FB

Target Change

October 21, 2015

page 20 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Chart 7: Nielsen OCR and comScore vCE Comparison

Source: BrightRoll, Nielsen, comScore

Online video advertisements are often compared to TV commercials, creating this

growing demand for the GRP metric to be applied to the new media form. Thus, iGRP

was adapted as:

Chart 8: iGRP Formula

Source: BrightRoll

Practical Example – Online Video Advertising

Let’s look at a practical example of delivering a 150 GRP campaign to US adults aged 18-

49. Holding the frequency constant, we see that based on Nielsen estimates the

campaign reach would be 92.3M Adults aged 18-49, and based on Comscore estimates

the reach would be 95.5M Adults aged 19-49. Total impressions for the Nielsen

campaign equal 197.8M (92.3M*2.143), while total impressions for the Comscore

campaign equal 204.7M (95.5M*2.143).

Chart 9: Calculating iGRP using Individuals

Source: Jefferies

Nielsen's Online Campaigns Ratings (OCR) comScore's validated Campaign Essentials (vCE)

MRC Accreditation Yes Yes

Demographic ProjectionsHas access to more than 150 million privacy-

protected registered users

1 Million UVs, 250K contributing to demographics on a

monthly basis

Impression Reporting "IMPRESSIONS" Verification and Viewability measures in place Only those that had the opportunity to be seen

Total US Population Estimates "UNIVERSE" 298,315,476 303,318,091

Cross-Platform MeasurementCross-Platform Campaign Ratings - TV, online and

tablets

validated Campaign Essentlials Multi-Platform - TV,

online, mobile, tablet

Campaign Reach Nielsen Population

A 18-49

Nielsen Total US Population Frequency A 18-49 GRP

92,286,261 131,846,305 298,315,476 2.143 150

Campaign Reach Comscore Population

A 18-49

Comscore Total US Population Frequency A 18-49 GRP

95,536,452 136,489,745 303,318,091 2.143 150

FB

Target Change

October 21, 2015

page 21 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

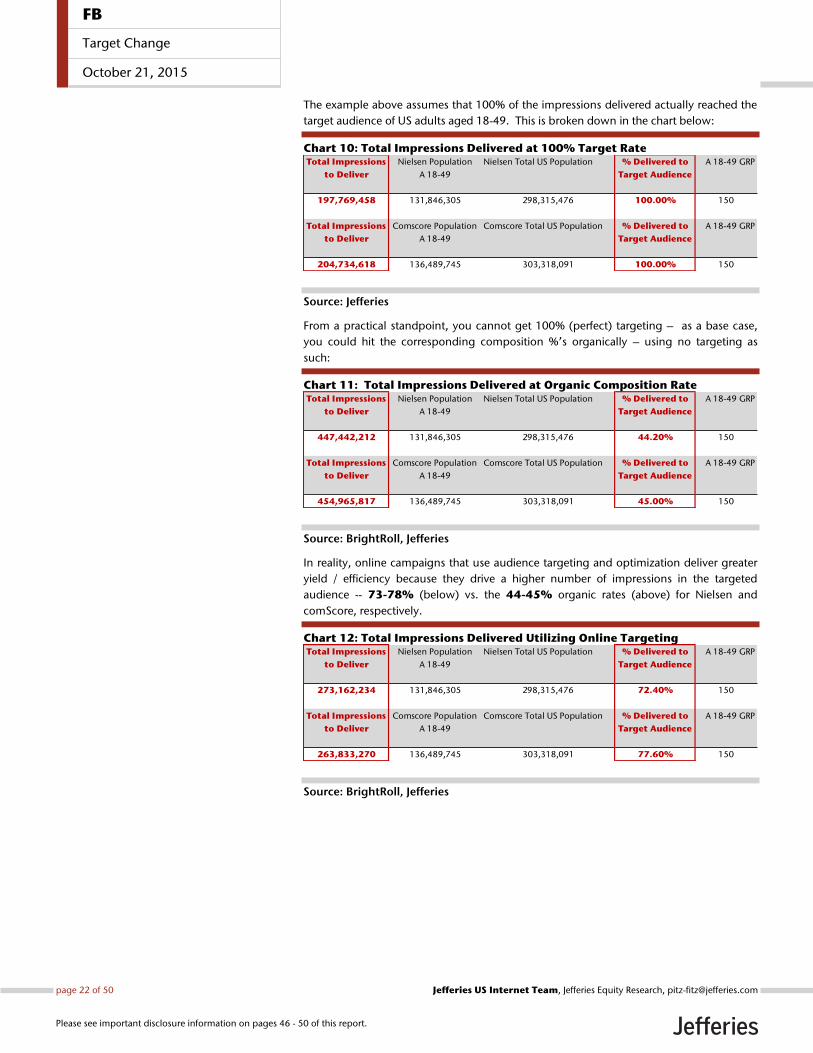

The example above assumes that 100% of the impressions delivered actually reached the

target audience of US adults aged 18-49. This is broken down in the chart below:

Chart 10: Total Impressions Delivered at 100% Target Rate

Source: Jefferies

From a practical standpoint, you cannot get 100% (perfect) targeting – as a base case,

you could hit the corresponding composition %’s organically – using no targeting as

such:

Chart 11: Total Impressions Delivered at Organic Composition Rate

Source: BrightRoll, Jefferies

In reality, online campaigns that use audience targeting and optimization deliver greater

yield / efficiency because they drive a higher number of impressions in the targeted

audience -- 73-78% (below) vs. the 44-45% organic rates (above) for Nielsen and

comScore, respectively.

Chart 12: Total Impressions Delivered Utilizing Online Targeting

Source: BrightRoll, Jefferies

Total Impressions

to Deliver

Nielsen Population

A 18-49

Nielsen Total US Population % Delivered to

Target Audience

A 18-49 GRP

197,769,458 131,846,305 298,315,476 100.00% 150

Total Impressions

to Deliver

Comscore Population

A 18-49

Comscore Total US Population % Delivered to

Target Audience

A 18-49 GRP

204,734,618 136,489,745 303,318,091 100.00% 150

Total Impressions

to Deliver

Nielsen Population

A 18-49

Nielsen Total US Population % Delivered to

Target Audience

A 18-49 GRP

447,442,212 131,846,305 298,315,476 44.20% 150

Total Impressions

to Deliver

Comscore Population

A 18-49

Comscore Total US Population % Delivered to

Target Audience

A 18-49 GRP

454,965,817 136,489,745 303,318,091 45.00% 150

Total Impressions

to Deliver

Nielsen Population

A 18-49

Nielsen Total US Population % Delivered to

Target Audience

A 18-49 GRP

273,162,234 131,846,305 298,315,476 72.40% 150

Total Impressions

to Deliver

Comscore Population

A 18-49

Comscore Total US Population % Delivered to

Target Audience

A 18-49 GRP

263,833,270 136,489,745 303,318,091 77.60% 150

FB

Target Change

October 21, 2015

page 22 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

What Are The Near-Term Impacts?

Media owners should continue to sell against classic GRP and cost-per-thousand (CPM)

metrics in the near term, but with better data & measurement tools shouldn’t we see the

adoption of more sophisticated, granular and immediate (maybe real-time) processes?

Media/video suppliers and aggregators would be able to commit to verifiable deliverables

across their total video reach -- cross-channel (and eventually cross media too – video,

display, search, mobile, TV, etc.). Enhanced measures of Return on Ad Spend (ROAS)

should follow, leading to truer performance-based advertising processes.

We continue to see evidence that brands are allocating a larger portion of their budgets

toward digital media. For example, Acura is launching its new TLX luxury sedan in the US

with a robust campaign that will allocate 30% of its budget toward digital. Importantly,

this campaign will not run a single ad on broadcast TV during prime-time. Of course, TV is

still a meaningful part of Acura’s marketing plan, accounting for more than half the

campaign’s budget. But Acura’s definition of TV is evolving to now include long-form,

high-quality content that will run on digital platforms (where the company’s ads will

complement the more traditional TV buys on cable channels like ESPN).

Exhibit 11: Acura Sponsored Web Series “Comedians in Cars Getting Coffee”

Source: YouTube

FB

Target Change

October 21, 2015

page 23 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Within the context of measuring media advertising strength, we would also highlight that

video consumption habits continue to shift away from linear / live TV to “what you want”

/ “where you want” / “when you want”:

Time spent watching TV in America is at an all-time high, yet the majority of this time

continues to shift away from live programing. Viewers are increasingly watching TV on

their own schedule as opposed to the pre-determined air times of their favorite shows.

The chart below highlights a growing trend among premium cable shows; in 2006 nearly

70% of the audience for Dexter’s first season watched the show live, while the proportion

of live viewing for Homeland is now almost the mirror opposite. Showtime’s executive VP

of program planning, Kim Lemon, went so far to say that for some of Showtime’s Sunday

shows the debut live rating can be “only 15% of what the ultimate weekly number will

be.”

Chart 13: Evolution Away from Live TV

Source: Nielsen, Rentrak, qz.com (http://qz.com/237600/charts-how-we-watch-tv-now/)

FB

Target Change

October 21, 2015

page 24 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Instagram: A Picture Perfect Ad Platform With its beautiful visual layout (photos and video) and a massive (400MM MAUs, larger

than Twitter), highly engaged audience, Instagram looks like a natural ad platform to us.

To date, Instagram’s ad load has been noticeably lower than core Facebook’s. But this is

about to change as Facebook recently opened Instagram to all advertisers. Instagram has

also unveiled the 30 second video ad available to advertisers. Thus, Instagram’s revenue

growth will now begin in earnest, and we are optimistic.

Importantly, Instagram ads leverage Facebook’s anonymized user data, which nearly

ensures these ads will deliver a similar bang-for-your-buck as Facebook’s core mobile

News Feed ads. And if we assume Instagram ads deliver similar ROI to Facebook’s core

mobile ads, advertiser demand should be robust.

To size the revenue opportunity, we compare Instagram’s user base to the core Facebook

mobile user base in terms of 1) the number of users across each geography, 2) ARPU, and

3) the expected ad load.

Our base case 2016 Instagram revenue estimate is $531MM, which we grow to $1.44B in

2017.

By 2019, we model Instagram revenue of $3.2B (generated from a global user base of

1.23B MAUs). For comparison, FB generated more than twice that amount of from a

similarly sized mobile user base in 2014. (2014 FB actual: $7.43B mobile rev from ~1.2B

mobile users).

Sizing Instagram’s Revenue Opportunity Based on Comps with Facebook’s

Core Mobile Business

1) First, we project Instagram’s Monthly Active Users per geography

through 2019.

Since Facebook acquired Instagram in April 2012 (for ~$1B cash + stock), user

levels have grown tenfold to 400 million MAUs.

This is roughly 31% as large as Facebook’s core mobile business, which has ~1.3

million MAUs and generated ~$7.43B in revenue in 2014.

Note when Facebook acquired Instagram it had only 30MM+ users; or only 6%

as large as Facebook’s 543MM mobile users at the time.

Our base case 2016 Instagram

revenue estimate is $531MM, which

we grow to 1.44B in 2017.

FB

Target Change

October 21, 2015

page 25 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Chart 14: Instagram Monthly Active Users (MAUs) Continue to Rise

Source: Facebook

Importantly, we assume Instagram has similar user engagement levels to core

Facebook.

On its 4Q’14 earnings call, the company noted Instagram and Facebook

account for 20% of people’s time on mobile in the US. Third party data confirms

Instagram has very high engagement levels.

Facebook says 30% of Instagram’s users located in the US. For core Facebook,

about 15-18% of users are outside the US (and Canada).

Facebook has recently confirmed Instagram has 400MM monthly active users.

Also, management has previously stated that ~30% of users are located in the

US, where ad prices are highest.

For the remaining 70% of users, we assume 95MM are located in Europe,

105MM are located in Asia, and the remaining 90MM are in Rest of World.

Table 3: Facebook and Instagram Users by Geography

Facebook Core Instagram*

US & Canada 213 110

Europe 311 95

Asia 496 105

Rest of World 471 90

Total 1,491 400

Source: Facebook, Jefferies Estimates (* denotes an estimate)

The geographic mix is important because Facebook earns far more revenue per

user in North America than anywhere else. To underscore this point, the US and

Canada account for nearly half of revenue despite the fact they account for 15-

18% of total Facebook users.

0

50

100

150

200

250

300

350

400

450

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

De

c-1

2

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

De

c-1

3

Feb

-14

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct

-14

De

c-1

4

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

FB

Target Change

October 21, 2015

page 26 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Table 4: Facebook Monthly and Daily Active Users by Geographic Region

Monthly Active Users (MM) Q1’14 Q2’14 Q3’14 Q4’14 % Users / Geo

US & Canada 202 204 206 208 14.9%

Europe 289 292 296 301

85.1% Asia 390 410 426 449

Rest of World 395 411 423 436

Total MAU's 1276 1317 1351 1394 100.0%

Daily Active Users (MM)

US & Canada 150 152 155 157 17.6%

Europe 203 206 212 217

82.4% Asia 216 228 242 253

Rest of World 233 243 256 263

Total DAU's 802 829 865 890 100.0%

Source: Facebook

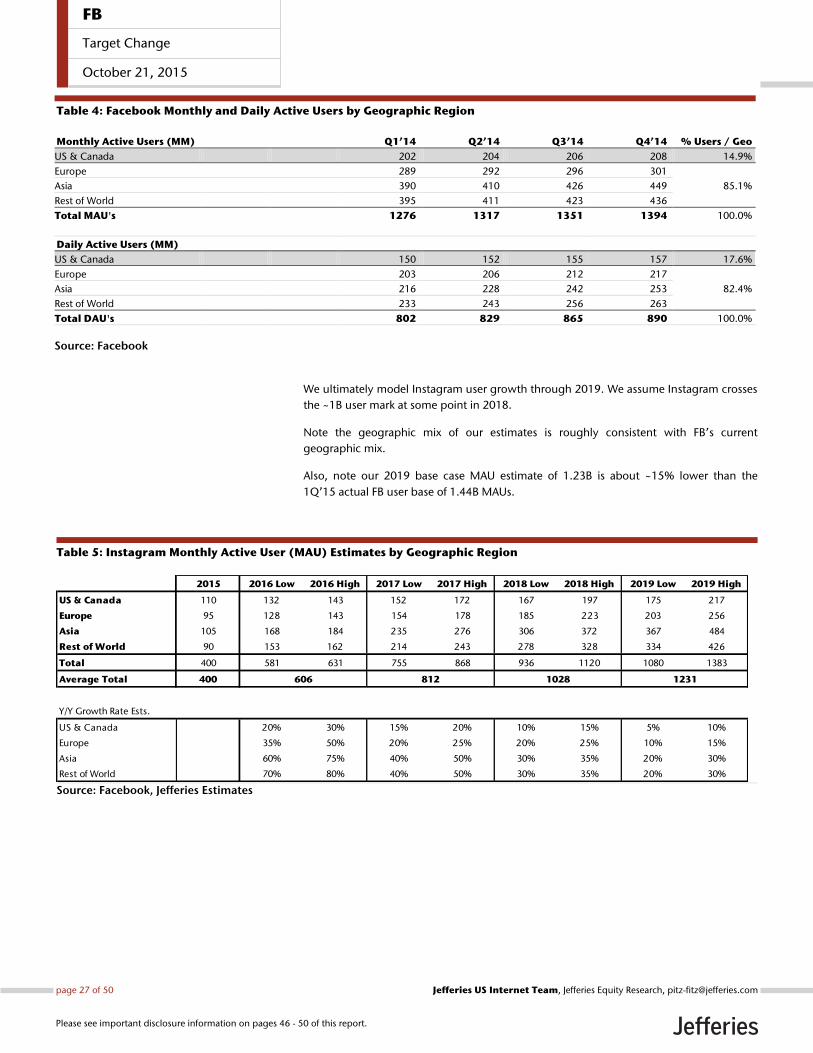

We ultimately model Instagram user growth through 2019. We assume Instagram crosses

the ~1B user mark at some point in 2018.

Note the geographic mix of our estimates is roughly consistent with FB’s current

geographic mix.

Also, note our 2019 base case MAU estimate of 1.23B is about ~15% lower than the

1Q’15 actual FB user base of 1.44B MAUs.

Table 5: Instagram Monthly Active User (MAU) Estimates by Geographic Region

Source: Facebook, Jefferies Estimates

2015 2016 Low 2016 High 2017 Low 2017 High 2018 Low 2018 High 2019 Low 2019 High

US & Canada 110 132 143 152 172 167 197 175 217

Europe 95 128 143 154 178 185 223 203 256

Asia 105 168 184 235 276 306 372 367 484

Rest of World 90 153 162 214 243 278 328 334 426

Total 400 581 631 755 868 936 1120 1080 1383

Average Total 400

Y/Y Growth Rate Ests.

US & Canada 20% 30% 15% 20% 10% 15% 5% 10%

Europe 35% 50% 20% 25% 20% 25% 10% 15%

Asia 60% 75% 40% 50% 30% 35% 20% 30%

Rest of World 70% 80% 40% 50% 30% 35% 20% 30%

606 812 1028 1231

FB

Target Change

October 21, 2015

page 27 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Chart 15: Instagram Monthly Active User (MAU) Projections (MM)

Source: Jefferies Estimates

2) Next, we model go-forward Facebook ARPU projections based off

historic actual results for core Facebook.

Ad prices continue to ramp quickly as FB’s mobile news feed ads command ever

higher prices. This is driven in part by 1) a mix shift towards lower-funnel

eCommerce / direct response oriented ad formats like DPAs and Mobile App

Install Ads and 2) more advertisers spending more money across a roughly fixed

number of ad impressions.

Over time we assume ad prices continue to rise across all geographies.

Table 6: Facebook ARPU Estimates by Geographic Region

Source: Facebook, Jefferies Estimates

0

200

400

600

800

1,000

1,200

1,400

1,600

2015 2016 2017 2018 2019

high

base

low

high

base

low

2016 Low 2016 High 2017 Low 2017 High 2018 Low 2018 High 2019 Low 2019 High

US & Canada $8.96 $9.35 $9.85 $10.75 $10.64 $11.82 $10.64 $12.41

Europe $3.95 $4.10 $5.53 $5.95 $6.63 $7.43 $7.30 $8.55

Asia $1.53 $1.59 $1.99 $2.15 $2.39 $2.68 $2.63 $3.08

Rest of World $1.04 $1.08 $1.24 $1.35 $1.43 $1.62 $1.57 $1.86

Y/Y Growth Rate Ests.

US & Canada 15% 20% 10% 15% 8% 10% 0% 5%

Europe 30% 35% 40% 45% 20% 25% 10% 15%

Asia 30% 35% 30% 35% 20% 25% 10% 15%

Rest of World 20% 25% 20% 25% 15% 20% 10% 15%

FB

Target Change

October 21, 2015

page 28 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

3) Third, we model go-forward Instagram ARPU projections by applying

a discount to core FB ARPU projections.

At first blush, it broadly makes sense that Instagram ad prices will be lower than

FB for several reasons. Over time we believe this gap will converge across all

geographies.

But in the US currently, we are seeing evidence that Instagram ad prices are

actually higher than for core FB, per Salesforce.com.

For the most part, Instagram ad pricing should be relatively similar to Facebook

over time, and our model assumes the gap narrows over time.

This rings true given both platforms leverage the same data, and both platforms

should have similar ad units (display, video). Additionally, Instagram will

leverage the same kinds of direct-response ads as core-FB, which have naturally

higher ad prices.

This will have a positive effect on ARPU over time.

See our Instagram ARPU assumptions below.

Table 7: Instagram ARPU Estimates by Geographic Region

Source: Facebook, Jefferies Estimates

2016 Low 2016 High 2017 Low 2017 High 2018 Low 2018 High 2019 Low 2019 High

US & Canada $8.96 $9.81 $9.85 $11.28 $10.64 $11.82 $10.64 $12.41

Europe $2.96 $3.49 $4.42 $5.05 $5.64 $7.06 $6.93 $8.55

Asia $0.61 $0.79 $1.19 $1.72 $1.91 $2.28 $2.36 $3.08

Rest of World $0.31 $0.22 $0.43 $0.54 $0.86 $1.21 $1.26 $1.58

Instagram ARPU Discount vs. Core FB

US & Canada 0% -5% 0% -5% 0% 0% 0% 0%

Europe 25% 15% 20% 15% 15% 5% 5% 0%

Asia 60% 50% 40% 20% 20% 15% 10% 0%

Rest of World 70% 80% 65% 60% 40% 25% 20% 15%

FB

Target Change

October 21, 2015

page 29 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

4) Finally, we model go-forward Instagram revenue projections based

on ad load as a percentage of core FB.

Our base case 2016 Instagram revenue estimate is $531MM, which we grow to

$1.44B in 2017.

By 2019, we model Instagram revenue of $3.2B (generated from a global user

base of 1.23B MAUs). For comparison, FB generated more than twice that

amount of from a similarly sized mobile user base in 2014. (2014 FB actual:

$7.43B mobile rev from ~1.2B mobile users).

Table 8: Instagram Revenue Estimates by Geographic Region

Source: Facebook, Jefferies Estimates

Chart 16: Instagram Annual Revenue Projections ($MM)

Source: Jefferies Estimates

2016 Low 2016 High 2017 Low 2017 High 2018 Low 2018 High 2019 Low 2019 High

US & Canada $296 $491 $822 $1,259 $1,066 $1,516 $1,399 $2,156

Europe $76 $149 $204 $360 $417 $865 $563 $985

Asia $10 $29 $56 $142 $146 $297 $260 $597

Rest of World $5 $7 $9 $26 $60 $139 $126 $270

Total $387 $676 $1,092 $1,787 $1,688 $2,817 $2,349 $4,007

Average Total

Ad Load as % of FB

US & Canada 25% 35% 55% 65% 60% 65% 75% 80%

Europe 20% 30% 30% 40% 40% 55% 40% 45%

Asia 10% 20% 20% 30% 25% 35% 30% 40%

Rest of World 10% 20% 10% 20% 25% 35% 30% 40%

$3,178$2,253$1,440$531

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2016 2017 2018 2019

high

base

low

FB

Target Change

October 21, 2015

page 30 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Visualizing an Instagram Ad

Below is an example of an Instagram Ad utilizing the carousel image format. The user first

sees the image with ad copy informing the user on the product. The user can than scroll

to see additional images and is promted with a “Learn More” button. Users can also

“Like” and “Comment” on the ad providing interaction and engagement. Kinetic Social,

a social marketing firm, has stated that on Facebook carousel ads can increase traffic to

sites by as much as 10x more than static ads. The ads also get about 1% click-thru rate

while non-carousel ads get 0.1% and the best mobile banner ads get 0.5%

Exhibit 12: Tiffany & Co. CT60 Watch Collection Advertisement on Instagram (Four Pages, Carousel Format)

Source: Facebook

Tiffany & Co. Sponsored Post

Ad copy and hashtag:

Introducing the Tiffany CT60 watch collection. Inspired by New York, crafted in

Switzerland.#TiffanyNYMinute

4 page ad - swipe right for more info

51,688 likes1,147 comments

Clicking “Learn More” takes user to Tiffany web page with

product video

FB

Target Change

October 21, 2015

page 31 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

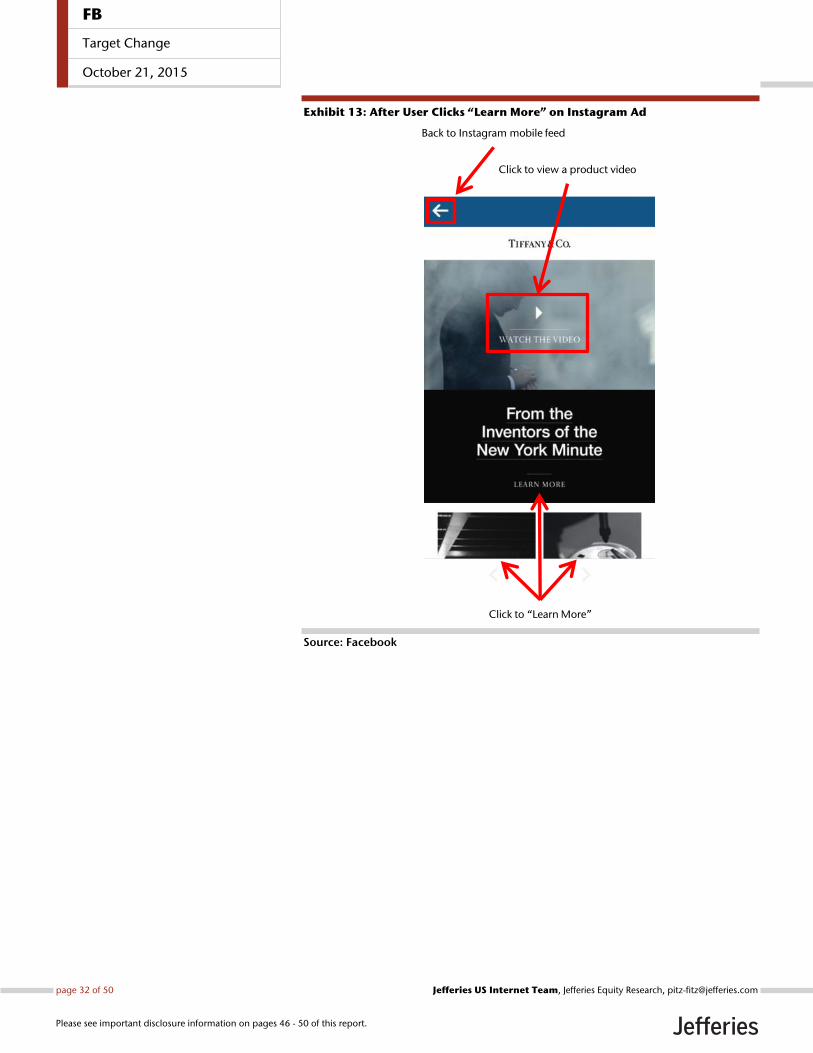

Exhibit 13: After User Clicks “Learn More” on Instagram Ad

Source: Facebook

Click to view a product video

Back to Instagram mobile feed

Click to “Learn More”

FB

Target Change

October 21, 2015

page 32 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Instagram Auto-Play Video Ads

Instagram has also started to integrate auto-playing video ads in the user’s stream. Below

is an example of a Dewar’s ad featured in a user’s stream. The high quality video is

engaging and begins playing when the ad enters the stream similar to user generated

content. The user can then click on the video to enable sound (same as user generated

content). On certain video ads users can click “Watch More” which will redirect

the user to the brand’s web page.

Exhibit 14: Dewar’s Instagram Video Ad - Autoplay

Source: Instagram

FB

Target Change

October 21, 2015

page 33 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

App Install Ad on Instagram

Instagram has also allowed App Install Ads as seen below for Fan Duel. The user is

presented with the ad in stream including ad copy in the comment section. When the

user clicks on “Install Now” it redirects them to their devices app store

directly to the app’s download page.

Exhibit 15: Fan Duel App Install Ad on Instagram

Source: Instagram

FB

Target Change

October 21, 2015

page 34 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Growth Driver #3: Facebook Audience Network Serving Ads in 3rd Party Mobile Apps

As the app economy grows, Facebook continues to roll out products designed to appeal

to app developers. The newest product is called the Audience Network, which is designed

to help apps generate revenue by running small Facebook ads. The network was

announced in April 2014, and opened up to all advertisers in October.

App developers are already working closely with Facebook. The company’s Mobile App

Install Ads, which help apps to acquire new users, have been a smash hit since they were

launched.

Facebook does not break out the revenue contribution from Mobile App Install Ads, but it

likely accounted for a large chunk of FB’s $7.4B mobile business (2014 actual).

With the Facebook Audience Network, developers can now work with Facebook for both

user acquisition / distribution (Mobile App Install Ads) and monetization (Facebook

Audience Network). We think this is a powerful one-two punch, with both products

complimenting each other nicely. We think developers will see plenty of utility from the

Audience Network.

Exhibit 16: Facebook Audience Network Ad from the Popular “2048” App

Source: Facebook, Jefferies

Facebook AudienceNetwork

“Banner Ad” Format

As Facebook limits the ad-load on its

own core app, the Audience

Network is an easy way to serve

more ads over time (without ruining

the user experience).

FB

Target Change

October 21, 2015

page 35 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

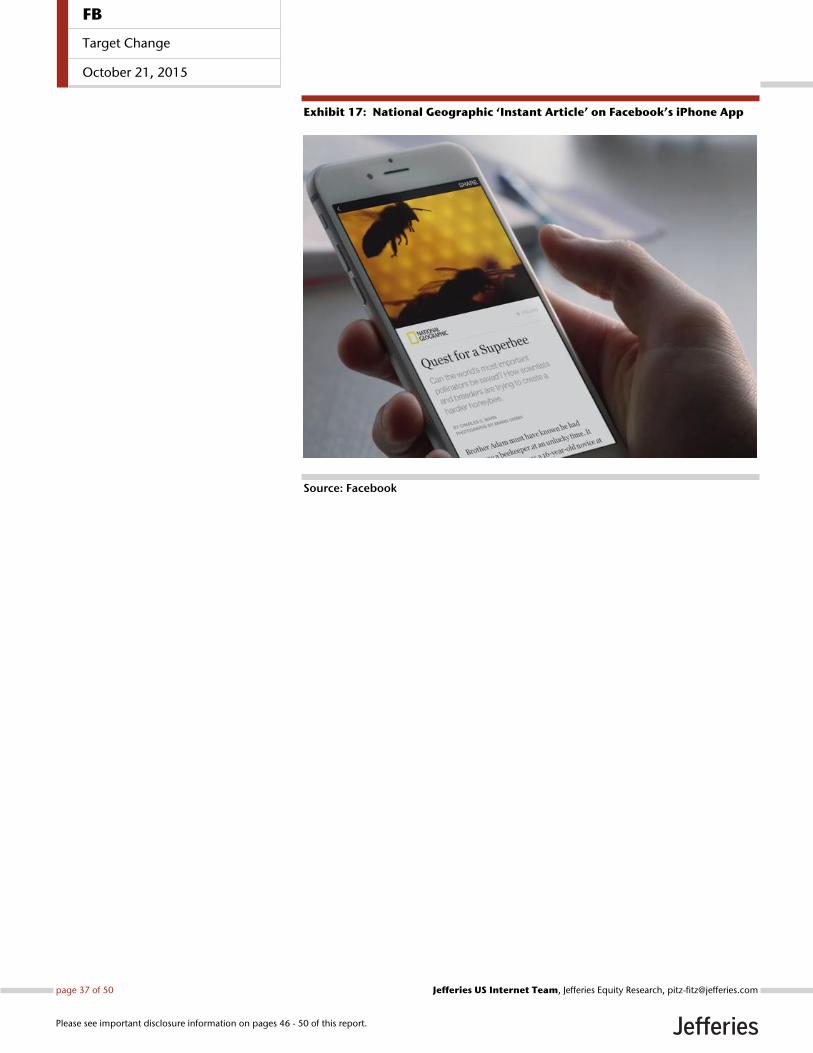

‘Instant Articles’ Bring High-Quality Content Direct to FB’s Mobile News Feed In May, Facebook introduced Instant Articles, a new tool for publishers to deliver articles

directly inside the user’s mobile news feed.

For the initial rollout, Facebook partnered with nine of the biggest websites in the world

like The New York Times, The Guardian, BBC News, National Geographic and Buzzfeed.

Already, publishers like Conde Nast, Hearst, Time Inc., CNN and Bustle have expressed

interest in participating as Facebook opens the service to more publishers over time.

Instant Articles furthers the company’s ambitions to be a one-stop-shop for the discovery

and consumption of content. Additionally, this content will bring premium, brand-safe ad

inventory directly into users’ mobile News Feeds.

Instant Articles uses FB’s photo and video technology to serve these same articles up to

10x faster than standard web articles, which are (by far) the slowest loading content type

on Facebook.

Facebook has introduced new features like tilt-to-pan photos, auto-play video, embedded

video captions, and interactive maps. By publishing direct to Facebook, publishers can

create slick looking, interactive mobile articles that still retain the brand’s look and feel.

Publishers will have full control over advertising.

There are two primary options for monetization.

First, the publisher can manage their own inventory on the Instant Articles platform. In

this scenario, the publisher keeps 100% of ad revenue and also receives readership data

from Facebook.

Most of Facebook’s early partners have selected this option.

Second, the publisher can elect for Facebook to handle the ad placements. In this

scenario, Facebook would take a ~30% revenue share. The ads can be customized to align

with the look and feel of the publisher’s other content, and will leverage FB’s massive data

set.

The influx of content will bring premium, brand-safe ad inventory directly

into users’ mobile News Feeds.

Over time Instant Articles should drive an influx of premium, brand safe-content directly

in the Facebook mobile News Feed. This in-turn gives Facebook the ability to sell high-

priced brand ads against each Instant Article.

Importantly, Instant Articles will be integrated directly into the Facebook Audience

Network.

FB

Target Change

October 21, 2015

page 36 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Exhibit 17: National Geographic ‘Instant Article’ on Facebook’s iPhone App

Source: Facebook

FB

Target Change

October 21, 2015

page 37 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

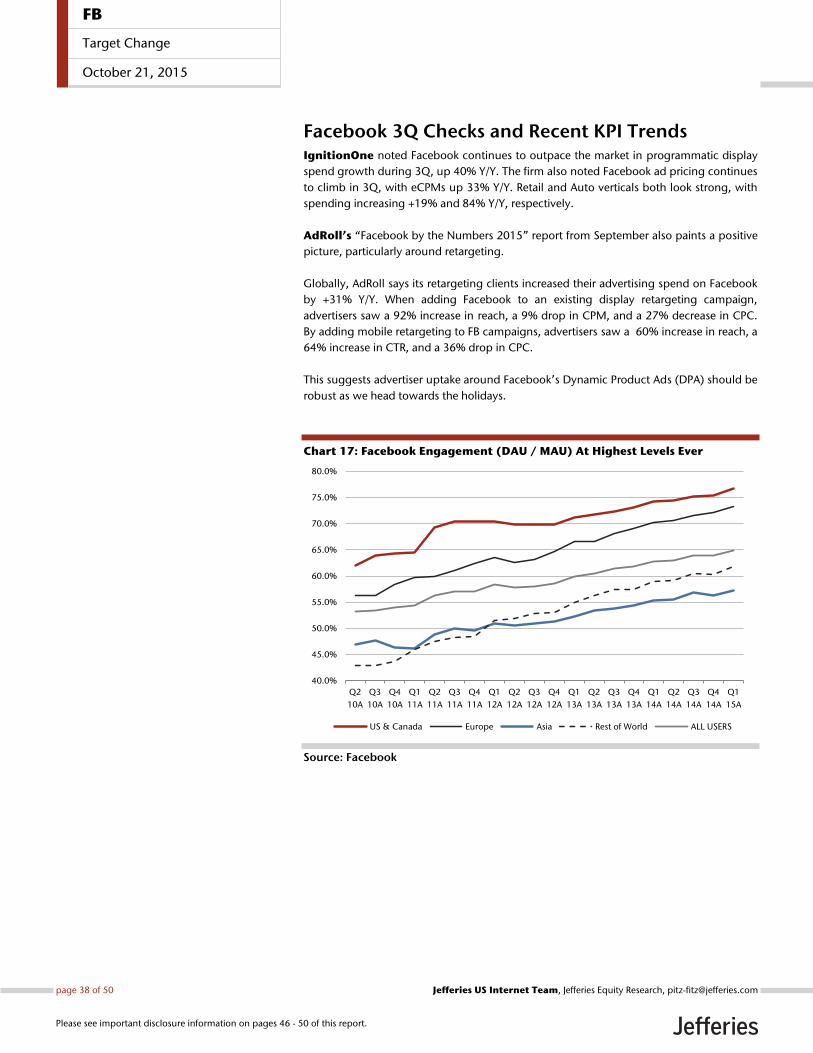

Facebook 3Q Checks and Recent KPI Trends IgnitionOne noted Facebook continues to outpace the market in programmatic display

spend growth during 3Q, up 40% Y/Y. The firm also noted Facebook ad pricing continues

to climb in 3Q, with eCPMs up 33% Y/Y. Retail and Auto verticals both look strong, with

spending increasing +19% and 84% Y/Y, respectively.

AdRoll’s “Facebook by the Numbers 2015” report from September also paints a positive

picture, particularly around retargeting.

Globally, AdRoll says its retargeting clients increased their advertising spend on Facebook

by +31% Y/Y. When adding Facebook to an existing display retargeting campaign,

advertisers saw a 92% increase in reach, a 9% drop in CPM, and a 27% decrease in CPC.

By adding mobile retargeting to FB campaigns, advertisers saw a 60% increase in reach, a

64% increase in CTR, and a 36% drop in CPC.

This suggests advertiser uptake around Facebook’s Dynamic Product Ads (DPA) should be

robust as we head towards the holidays.

Chart 17: Facebook Engagement (DAU / MAU) At Highest Levels Ever

Source: Facebook

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

80.0%

Q2

10A

Q3

10A

Q4

10A

Q1

11A

Q2

11A

Q3

11A

Q4

11A

Q1

12A

Q2

12A

Q3

12A

Q4

12A

Q1

13A

Q2

13A

Q3

13A

Q4

13A

Q1

14A

Q2

14A

Q3

14A

Q4

14A

Q1

15A

US & Canada Europe Asia Rest of World ALL USERS

FB

Target Change

October 21, 2015

page 38 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Chart 18: Quarterly Revenue ($MM) per Geographic Region

Source: Facebook

Chart 19: Monthly Active Users (MM) per Geographic Region

Source: Facebook

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Q2

10A

Q3

10A

Q4

10A

Q1

11A

Q2

11A

Q3

11A

Q4

11A

Q1

12A

Q2

12A

Q3

12A

Q4

12A

Q1

13A

Q2

13A

Q3

13A

Q4

13A

Q1

14A

Q2

14A

Q3

14A

Q4

14A

Q1

15A

US & Canada Europe Asia Rest of World

50

100

150

200

250

300

350

400

450

500

Q2

10A

Q3

10A

Q4

10A

Q1

11A

Q2

11A

Q3

11A

Q4

11A

Q1

12A

Q2

12A

Q3

12A

Q4

12A

Q1

13A

Q2

13A

Q3

13A

Q4

13A

Q1

14A

Q2

14A

Q3

14A

Q4

14A

Q1

15A

US & Canada Europe Asia Rest of World

FB

Target Change

October 21, 2015

page 39 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

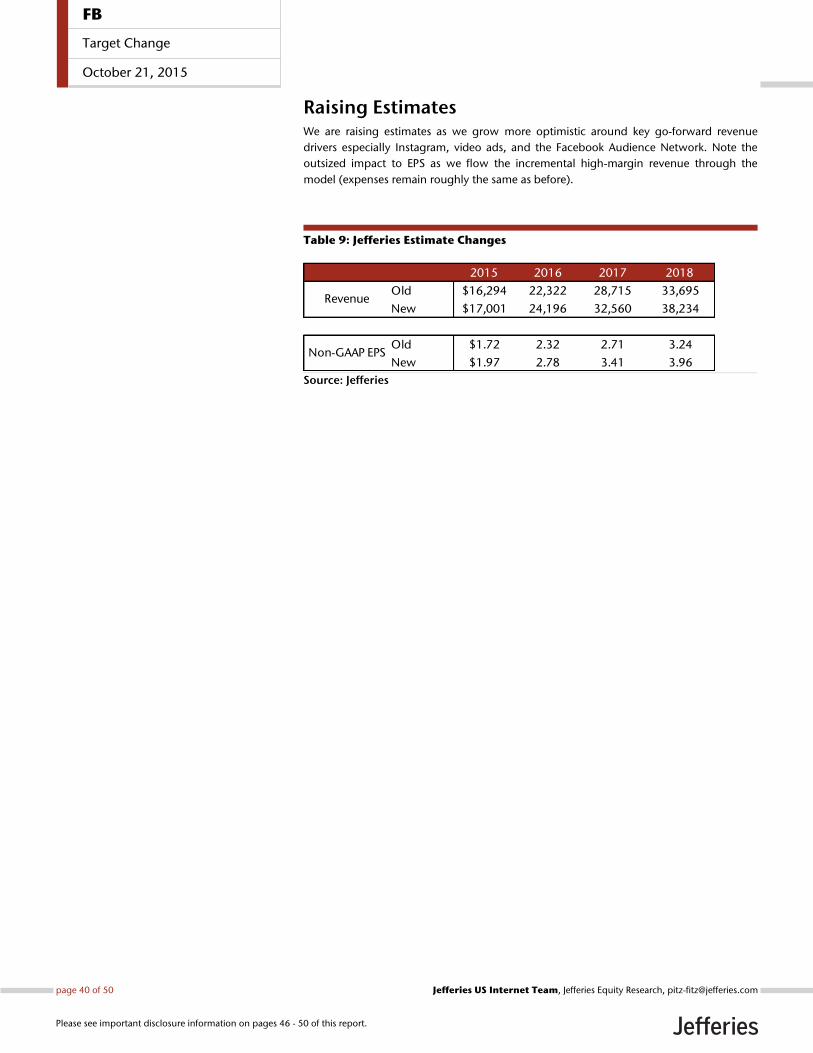

Raising Estimates We are raising estimates as we grow more optimistic around key go-forward revenue

drivers especially Instagram, video ads, and the Facebook Audience Network. Note the

outsized impact to EPS as we flow the incremental high-margin revenue through the

model (expenses remain roughly the same as before).

Table 9: Jefferies Estimate Changes

Source: Jefferies

2015 2016 2017 2018

Old $16,294 22,322 28,715 33,695

New $17,001 24,196 32,560 38,234

Old $1.72 2.32 2.71 3.24

New $1.97 2.78 3.41 3.96Non-GAAP EPS

Revenue

FB

Target Change

October 21, 2015

page 40 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

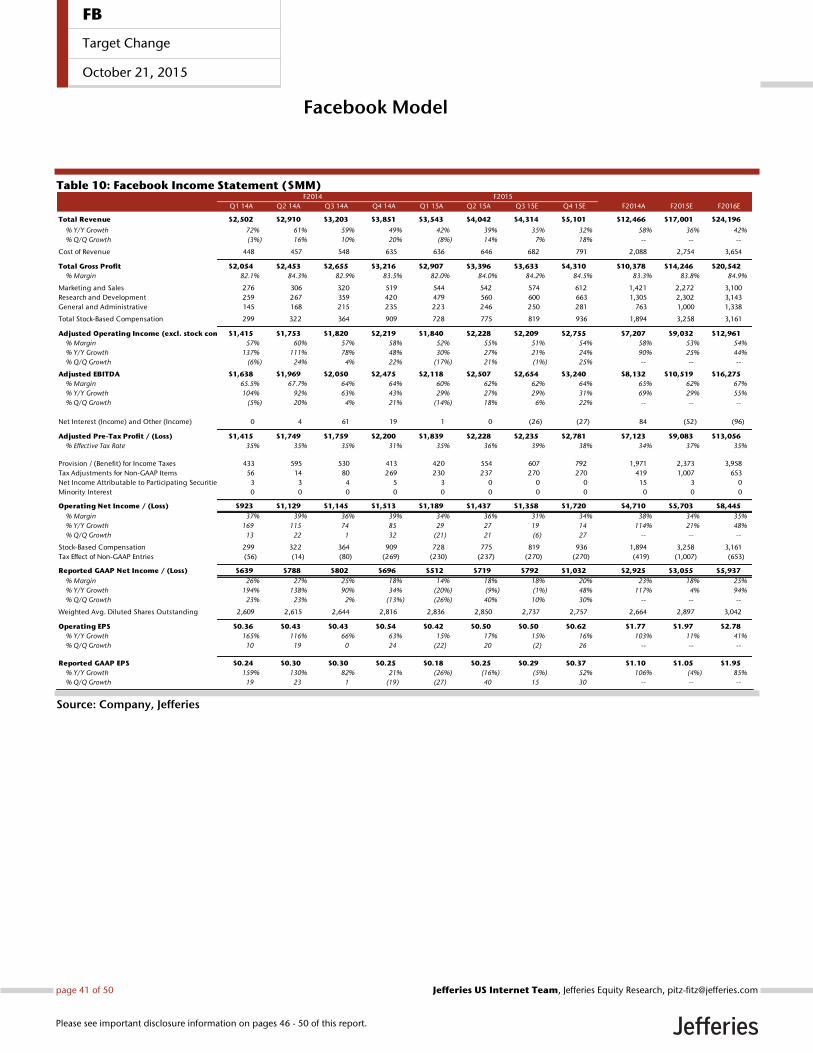

Facebook Model

Table 10: Facebook Income Statement ($MM)

Source: Company, Jefferies

Q1 14A Q2 14A Q3 14A Q4 14A Q1 15A Q2 15A Q3 15E Q4 15E F2014A F2015E F2016E

Total Revenue $2,502 $2,910 $3,203 $3,851 $3,543 $4,042 $4,314 $5,101 $12,466 $17,001 $24,196

% Y/Y Growth 72% 61% 59% 49% 42% 39% 35% 32% 58% 36% 42%

% Q/Q Growth (3%) 16% 10% 20% (8%) 14% 7% 18% -- -- --

Cost of Revenue 448 457 548 635 636 646 682 791 2,088 2,754 3,654

Total Gross Profit $2,054 $2,453 $2,655 $3,216 $2,907 $3,396 $3,633 $4,310 $10,378 $14,246 $20,542

% Margin 82.1% 84.3% 82.9% 83.5% 82.0% 84.0% 84.2% 84.5% 83.3% 83.8% 84.9%

Marketing and Sales 276 306 320 519 544 542 574 612 1,421 2,272 3,100

Research and Development 259 267 359 420 479 560 600 663 1,305 2,302 3,143

General and Administrative 145 168 215 235 223 246 250 281 763 1,000 1,338

Total Stock-Based Compensation 299 322 364 909 728 775 819 936 1,894 3,258 3,161

Adjusted Operating Income (excl. stock comp.)$1,415 $1,753 $1,820 $2,219 $1,840 $2,228 $2,209 $2,755 $7,207 $9,032 $12,961

% Margin 57% 60% 57% 58% 52% 55% 51% 54% 58% 53% 54%

% Y/Y Growth 137% 111% 78% 48% 30% 27% 21% 24% 90% 25% 44%

% Q/Q Growth (6%) 24% 4% 22% (17%) 21% (1%) 25% -- -- --

Adjusted EBITDA $1,638 $1,969 $2,050 $2,475 $2,118 $2,507 $2,654 $3,240 $8,132 $10,519 $16,275

% Margin 65.5% 67.7% 64% 64% 60% 62% 62% 64% 65% 62% 67%

% Y/Y Growth 104% 92% 63% 43% 29% 27% 29% 31% 69% 29% 55%

% Q/Q Growth (5%) 20% 4% 21% (14%) 18% 6% 22% -- -- --

Net Interest (Income) and Other (Income) 0 4 61 19 1 0 (26) (27) 84 (52) (96)

Adjusted Pre-Tax Profit / (Loss) $1,415 $1,749 $1,759 $2,200 $1,839 $2,228 $2,235 $2,781 $7,123 $9,083 $13,056

% Effective Tax Rate 35% 35% 35% 31% 35% 36% 39% 38% 34% 37% 35%

Provision / (Benefit) for Income Taxes 433 595 530 413 420 554 607 792 1,971 2,373 3,958

Tax Adjustments for Non-GAAP Items 56 14 80 269 230 237 270 270 419 1,007 653

Net Income Attributable to Participating Securities 3 3 4 5 3 0 0 0 15 3 0

Minority Interest 0 0 0 0 0 0 0 0 0 0 0

Operating Net Income / (Loss) $923 $1,129 $1,145 $1,513 $1,189 $1,437 $1,358 $1,720 $4,710 $5,703 $8,445

% Margin 37% 39% 36% 39% 34% 36% 31% 34% 38% 34% 35%

% Y/Y Growth 169 115 74 85 29 27 19 14 114% 21% 48%

% Q/Q Growth 13 22 1 32 (21) 21 (6) 27 -- -- --0

Stock-Based Compensation 299 322 364 909 728 775 819 936 1,894 3,258 3,161

Tax Effect of Non-GAAP Entries (56) (14) (80) (269) (230) (237) (270) (270) (419) (1,007) (653)

Reported GAAP Net Income / (Loss) $639 $788 $802 $696 $512 $719 $792 $1,032 $2,925 $3,055 $5,937

% Margin 26% 27% 25% 18% 14% 18% 18% 20% 23% 18% 25%

% Y/Y Growth 194% 138% 90% 34% (20%) (9%) (1%) 48% 117% 4% 94%

% Q/Q Growth 23% 23% 2% (13%) (26%) 40% 10% 30% -- -- --

Weighted Avg. Diluted Shares Outstanding 2,609 2,615 2,644 2,816 2,836 2,850 2,737 2,757 2,664 2,897 3,042

Operating EPS $0.36 $0.43 $0.43 $0.54 $0.42 $0.50 $0.50 $0.62 $1.77 $1.97 $2.78

% Y/Y Growth 165% 116% 66% 63% 15% 17% 15% 16% 103% 11% 41%

% Q/Q Growth 10 19 0 24 (22) 20 (2) 26 -- -- --

Reported GAAP EPS $0.24 $0.30 $0.30 $0.25 $0.18 $0.25 $0.29 $0.37 $1.10 $1.05 $1.95

% Y/Y Growth 159% 130% 82% 21% (26%) (16%) (5%) 52% 106% (4%) 85%

% Q/Q Growth 19 23 1 (19) (27) 40 15 30 -- -- --

F2014 F2015

FB

Target Change

October 21, 2015

page 41 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Table 11: Facebook Revenue Build ($MM)

Source: Company, Jefferies

Table 12: Facebook Balance Sheet ($MM)

Source: Company, Jefferies

Q1 14A Q2 14A Q3 14A Q4 14A Q1 15A Q2 15A Q3 15E Q4 15E F2014A F2015E F2016E

Total Revenue $2,502 $2,910 $3,203 $3,851 $3,543 $4,042 $4,314 $5,101 $12,466 $17,001 $24,196

% Y/Y Growth 72% 61% 59% 49% 42% 39% 35% 32% 58% 36% 42%

% Q/Q Growth -3% 16% 10% 20% -8% 14% 7% 18% -- -- --

Advertising Revenue $2,265 $2,676 $2,957 $3,594 $3,317 $3,827 $4,110 $4,888 $11,492 $16,142 $23,406

% Y/Y Growth 82% 67% 64% 53% 46% 43% 39% 36% 65% 40% 45%

% Q/Q Growth -3% 18% 11% 22% -8% 15% 7% 19% -- -- --

% of Total Revenue 91% 92% 92% 93% 94% 95% 95% 96% 92% 95% 97%

Mobile Advertising Revenue $1,336 $1,659 $1,952 $2,480 $2,421 $2,909 $3,247 $3,959 $7,427 $12,536 $20,597

% Y/Y Growth 258% 153% 122% 100% 81% 75% 66% 60% 136% 69% 64%

% Q/Q Growth 8% 24% 18% 27% -2% 20% 12% 22% -- -- --

% of Advertising Revenue 59% 62% 66% 69% 73% 76% 79% 81% 65% 78% 88%

Desktop Advertising Revenue $929 $1,017 $1,005 $1,114 $896 $918 $863 $929 $4,065 $3,606 $2,809

% Y/Y Growth 7% 8% 10% 1% -4% -10% -14% -17% 6% -11% -22%

% Q/Q Growth -16% 10% -1% 11% -20% 3% -6% 8% -- -- --

% of Advertising Revenue 41% 38% 34% 31% 27% 24% 21% 19% 35% 22% 12%

Payments and Other Revenue $237 $234 $246 $257 $226 $215 $204 $213 $974 $858 $790

% Y/Y Growth 11% 9% 13% 7% -5% -8% -17% -17% 10% -12% -8%

% Q/Q Growth -2% -1% 5% 4% -12% -5% -5% 4% -- -- --

% of Total Revenue 9% 8% 8% 7% 6% 5% 5% 4% 8% 5% 3%

F2014 F2015

Q1 14A Q2 14A Q3 14A Q4 14A Q1 15A Q2 15A Q3 15E Q4 15E F2014A F2015E F2016E

Cash & Cash Equivalents $2,998 $4,384 $8,999 $4,315 $3,419 $5,123 $5,631 $6,848 4,315 6,848 $16,753

Marketable Securities 9,631 9,572 5,251 6,884 8,994 9,002 9,002 9,002 6,884 9,002 9,002

Accounts Receivable 1,006 1,190 1,363 1,678 1,508 1,815 1,937 2,291 1,678 2,291 3,258

Deferred Income Taxes 0 0 0 0 0 0 89 111 0 111 80

Prepaid Expenses and Other Current Assets 425 411 502 793 1,083 1,011 968 1,058 793 1,058 1,581

Current Assets $14,060 $15,557 $16,115 $13,670 $15,004 $16,951 $17,628 $19,310 $13,670 $19,310 $30,675

Property and Equipment 3,074 3,334 3,703 3,967 4,619 4,955 5,373 5,959 3,967 5,959 5,789

Long-Term Investments 0 0 0 0 0 0 0 0 0 0 0

Goodwill 0 0 0 0 0 0 0 0 0 0 0

Intangible Assets 1,682 1,672 3,929 21,910 21,779 21,630 21,630 21,630 21,910 21,630 21,630

Long-Term Deferred Income Taxes 0 0 0 0 0 0 0 0 0 0 0

Other Long-Term Assets 212 206 441 637 605 594 228 249 637 249 861

Total Assets $19,028 $20,769 $24,188 $40,184 $42,007 $44,130 $44,859 $47,147 $40,184 $47,147 $58,955

Accounts Payable $85 $146 $120 $176 $129 $139 $120 $139 176 139 $246

Platform Partners Payable 188 176 208 202 189 182 0 0 202 0 82

Accrued Expenses & Other Current Liabilities 525 666 709 866 1,300 1,472 1,196 1,307 866 1,307 1,830

Deferred Revenue & Deposits 38 53 48 66 55 49 86 102 66 102 137

Current Portion of Capital Lease Obligations 201 173 149 114 73 39 39 39 114 39 39

Current Portion of Long-Term Debt 0 0 0 0 0 0 0 0 0 0 0

Total Current Liabilities $1,037 $1,214 $1,234 $1,424 $1,746 $1,881 $1,441 $1,587 $1,424 $1,587 $2,333

Long-Term Debt 0 0 0 0 0 0 0 0 0 0 0

Capital Lease Obligations 191 153 129 119 113 110 110 110 119 110 104

Other Long-Term Liabilities 1,063 1,056 1,587 2,545 2,647 2,687 2,278 2,489 2,545 2,489 4,458

Total Liabilities $2,291 $2,423 $2,950 $4,088 $4,506 $4,678 $3,829 $4,186 $4,088 $4,186 $6,896

Convertible Preferred Stock 0 0 0 0 0 0 0 0 0 0 0

Common Stock 0 0 0 0 0 0 0 0 0 0 0

Retained Earnings (Accumulated Deficit) 3,801 4,592 5,398 6,099 6,611 7,330 8,122 9,154 6,099 9,154 15,091

Additional Paid-In Capital 12,921 13,759 15,949 30,225 31,337 32,479 33,265 34,164 30,225 34,164 37,326

Accumulated Other Comprehensive Loss 15 (5) (109) (228) (447) (357) (357) (357) (228) (357) (357)

Shareholders' Equity $16,737 $18,346 $21,238 $36,096 $37,501 $39,452 $41,030 $42,961 $36,096 $42,961 $52,060

Liabilities & Shareholders' Equity $19,028 $20,769 $24,188 $40,184 $42,007 $44,130 $44,859 $47,147 $40,184 $47,147 $58,955

F2014 F2015

FB

Target Change

October 21, 2015

page 42 of 50 , Jefferies Equity Research, [email protected] US Internet Team

Please see important disclosure information on pages 46 - 50 of this report.

Table 13: Facebook Cash Flow Statement ($MM)

Source: Company, Jefferies

Table 14: Facebook DCF ($MM)

Source: Company, Jefferies

Q1 14A Q2 14A Q3 14A Q4 14A Q1 15A Q2 15A Q3 15E Q4 15E F2014A F2015E F2016E

Net Income $639 $788 $802 $701 $512 $719 $792 $1,032 $2,930 $3,055 $5,937

Depreciation 264 257 289 433 457 459 445 485 1,243 1,847 3,315