Presents Who Blows the Whistle on Corporate Fraud? · PDF file · 2007-10-22Who...

62

THE UNIVERSITY OF MICHIGAN LAW SCHOOL The Law and Economics Workshop Presents Who Blows the Whistle on Corporate Fraud? by Adair Morse, Michigan Business School THURSDAY, December 1, 2005 3:40-5:15 Room 236 Hutchins Hall Additional hard copies of the paper are available in Room 972LR or available electronically at http://www.law.umich.edu/centersandprograms/olin/workshops.htm

-

Upload

truongtruc -

Category

Documents

-

view

219 -

download

3

Transcript of Presents Who Blows the Whistle on Corporate Fraud? · PDF file · 2007-10-22Who...

THE UNIVERSITY OF MICHIGAN LAW SCHOOL

The Law and Economics Workshop

Presents

Who Blows the Whistle

on Corporate Fraud?

by

Adair Morse, Michigan Business School

THURSDAY, December 1, 2005 3:40-5:15

Room 236 Hutchins Hall

Additional hard copies of the paper are available in Room 972LR or available electronically at http://www.law.umich.edu/centersandprograms/olin/workshops.htm

November 2005

Preliminary and Very Incomplete

WHO BLOWS THE WHISTLE ON CORPORATE FRAUD?

Alexander Dyck

University of Toronto

Adair Morse

University of Michigan

Luigi Zingales*

Harvard University, University of Chicago, NBER, & CEPR

ABSTRACT

What control mechanisms are most effective in preventing corporate fraud? To answer this question, we study all reported cases of corporate fraud in companies with more than half a billion dollars in assets between 1996 and 2004. We find that no single mechanism dominates the revelation of fraud. The most important sources of information are employees (13% of the cases), analysts (12%), and newspapers (another 11%). Industry regulators play a small role in whistle blowing but the SEC does not contribute much to the discovery of fraud. Auditors also serve only a minor role, albeit their activity increased after the Enron scandal. Remarkable for their absence are underwriters and banks. Moreover, examining the duration of these improprieties allows us to infer the relative efficiency of these mechanisms. The most efficient external whistleblowers are the analysts (on average they discover a fraud after 395 days). When they fail it takes two years on average for a fraud to be discovered.

*Alexander Dyck thanks the Connaught Fund of the University of Toronto and Luigi Zingales the Stigler Center at the University of Chicago for financial support. We would like to thank Alexander Phung for truly outstanding research assistantship.

2

The onset of the new millennium coincided with remarkable revelations of corporate

fraud, not only in the United States, but around the world. These frauds are remarkable

not only in their magnitude, but also their duration. For instance, the HealthSouth fraud,

where all 5 former CFOs pleaded guilty to criminal charges surrounding earnings and

asset manipulation of more than $2.5 billion, had been in existence for over ten years. In

the Parmalat case, it appears that fraud persisted throughout the 13 years the company

was public. In the end, not only were the earnings false, but liabilities were 14 billion

euros more than Parmalat’s official accounts. The magnitude and the duration of these

frauds suggest a systematic failure of many standard mechanisms of control: the board of

directors, the external auditors, the banks, the underwriters, the analysts, and the financial

market regulators.

Fortunately, these extreme examples are rare, especially in the United States.

Nevertheless, more modest and less long-lasting frauds do occur frequently in the U.S.

The fact that these frauds remain limited in size and scope suggests that some control

mechanisms work.

In this paper we examine which control mechanisms work in an important

dimension of governance – exposing improprieties. The better the process for exposing

misdeeds, the more limited will be the extent and impact of corporate frauds, stopping

transgressors before insider misdeeds reach levels of an Enron or a Healthsouth. The

results from this exercise can be used to help limit the extent and impact of corporate

frauds in the United States and to highlight which corporate governance mechanisms

would be most important for other countries to adopt.

Just as the Federal Aviation Authority (FAA) studies all airplane accidents,

however minor, to identify ways to prevent failures which might lead to major crashes, in

this paper we assemble a sample that includes major and minor episodes of alleged fraud

to identify which mechanisms bring the alleged fraud into the light. To assemble a

sample that captures the most significant cases of corporate fraud, we start from the

Stanford database of security class actions brought against companies with at least a half

billion in assets between 1996 and 2004. Since in major companies (i.e. companies with

sufficient assets and insurance at stake) any fraud will lead to a security class action

(Choi, Nelson and Pritchard, 2005), we are confident that we have all the (detected) cases

3

of fraud in the set of large companies. To eliminate alleged frauds that are indeed

frivolous suits we restrict our attention to the period after passage of the Private

Securities Litigation Reform Act of 1995 (PSLRA) that was designed to reduce frivolous

suits (e.g., Johnson, Kasznik, and Nelson, 2000; Johnson, Nelson and Pritchard, 2003),

and further restrict our attention to cases that settled for at least $2.5 million, a level of

payment previous studies suggested helps divide frivolous suits from meritorious ones

(Grundfest, 1995).

This sample of frauds allows us to ask a number of questions that probe the

governance process: who blows the whistle on corporate fraud? Why do these actors

blow the whistle when they do? Which whistleblowers act more quickly than others,

lowering the duration of the impropriety? Why do insiders engage in fraud in the first

place? And is this fraud detection process influenced by increased public pressure and

awareness, as occurred after the spectacular downfall of Enron in 2001?

We collect all news articles surrounding the event, as well as the news up to the

settlement or dismissal of the case. By reading allegations, news articles and newswires,

we identify who blew the whistle on the fraud and under what circumstances. We also try

to infer the motivation of the fraud. Finally, we record the duration and the monetary

settlement amount.

Analyzing these data, we find that in one quarter of the cases, it is the firm that

reveals the wrongdoing. This generally occurs after a change in company’s management

or when the company finds it difficult to keep lying to analysts regarding its losses. Two

thirds of the alleged frauds, however, were identified by actors that are not part of the

internal governance of the firm. The second most important class of whistle blowers is

information intermediaries: analysts (who blow the whistle in 12% of the cases) and

newspapers (another 11%). Third are the employees who blow the whistle in 13% of the

cases. Fourth are regulators, collectively accounting for 14% of cases. The SEC accounts

for just 2% of these cases, while industry regulators account for four times as many cases

(8%). As interesting as these results are in identifying who blew the whistle, perhaps a

more striking result is who did not blow the whistle. Prominent actors in traditional

discussions of governance are completely absent or so trivial as not to matter,;stock

4

exchange regulators, commercial banks, and reputation intermediaries of lawyers and

underwriters are all noticeably absent from our findings.

Having established these facts behind the uncovering of corporate fraud, we ask

three additional questions. First, why did these actors act when they did? To address this

question we gather information about the context surrounding this decision. We find that

routine earnings announcements are the single greatest trigger factor in the uncovering of

the fraud – when faced with disappointing earnings, and lacking a convincing alternative

story, firms can simply admit their misdeeds, accounting for 16% of our observations.

External events also seem to force a revelation of the fraud. A negative operations shock

(16% of cases) such as a product failure or loss of a client may also force the firm to

admit the fraud. Earning announcements and operational failures also appear as

triggering factors for outside whistleblowers, providing motivation and source material

for outside investigations into firm practices and financial imbalances. Added scrutiny

need not be induced by firm announcements; outside scrutiny events (also 16% of cases)

such as due diligence and industry routine investigations also are important in bringing

fraud to light.

Next, how efficient were the various actors? Since all whistleblowers can be

considered competing sources for bringing fraud-limiting news to light, the speed with

which the information is brought to light provides an indication of the relative efficiency

of these different mechanisms. By this measure, analysts and the firm itself are the most

efficient actors in curtailing fraud to durations of just more than a year, significantly less

than the average duration of 1.6 years. When this first line of defense fails, other actors

seem to bring the information to light in similar periods of time, almost 2 years on

average.

Finally, what was the motivation surrounding the frauds?. Capital raising of

multiple sorts, most notably through organic growth or merger/acquisitions accounts for

41% our sample. Smoothing of earnings is second most common, at 17%. Interestingly,

self-enrichment is less prominent than either of these two motivations, accounting for just

11% of observations.

In conducting analyses of the actors, the trigger factors, duration and motivation,

we also pay attention to changes over time. Notably we divide our sample into a pre- and

5

post-Enron subsamples, motivated by the change in public attention to corporate scandals

surrounding Enron’s rapid fall in October of 2001, and the ensuing discovery of huge

frauds elsewhere including Worldcom that collectively spurred the passage of Sarbanes

Oxley. This division provides some direct evidence that heightened scrutiny and public

attention changed the enforcement environment.

This work relates most directly to the burgeoning literature on corporate

governance and law and finance that has focused on the allocation of rights between

investors and insiders, and the legal sanctions, processes and penalties available to

investors. Here, by highlighting the discovery rather than the penalty phase, we provide

complementary evidence on critical actors and processes. Our findings provide support

for a broad view of governance that incorporates a range of actors outside of the firm, and

notably outside of the usual discussion of governance - including newspapers, employees,

and industry-specific regulators. These actors are pivotal in the governance process of

exposing fraud.

The remainder of the paper proceeds as follows. Section 2 explains the sample

selection process. Section 3 describes the timing of these improprieties, their nature, and

their magnitude as indicated by the settlement amount. Section 4 presents the data on the

identity of the whistleblower and the timing of their interventions. Section 5 tests some

hypotheses regarding the relative effectiveness of the different control mechanisms.

Section 6 provides conclusions and implications.

2. Data

Selecting the Sample

Ideally, to identify the most frequent whistleblowers, we would like the sample of

all firms where a fraud was brought to light. To collect this sample we start from the

Stanford Securities Class Action Clearinghouse and select all the cases after 1995, the

period after passage of the Private Securities Litigation Reform Act of 1995 (PSLRA)

that was designed to reduce frivolous suits. The Stanford Securities Class Action

6

Clearinghouse provides the litigant name, date of class action filing, summary of

complaint, and court of certification for 2,102 class action suits filed after 1995.1

We focus our attention on larger firms by restricting our attention initially to those

firms with at least a half billion in assets. To this sample we added another sample of 50

firms randomly selected from the entire dataset that includes firms of varying sizes. We

further restrict our attention to frauds that are not IPos and do not involve mutual fund

trading manipulation. The size, IPO and mutual trading filters results in a sample of 338

firms, plus the 50 randomly selected firms producing a sample of 388 firms.

Several existing mechanisms instill confidence that our sample is complete. For

one, class action law firms have automated the mechanism of filing class action suits

such that in the case of any negative shock to share prices they immediately start

searching for a cause to file a suit. Since in the United States stock prices drop following

revelation of most serious corporate frauds it is therefore highly unlikely that a corporate

fraud would emerge without a subsequent class action suit being filed. In most cases,

investigations by the SEC or other authorities come subsequent to class action suits.

The concern in using class action cases to identify corporate fraud is the possible

inclusion of firms which are falsely accused of fraud violations. After a class action suit

is filed, the class lawyers submit for court certification. Certification rests not on the

validity of the fraud allegations but primarily on the class having proper shareholder

representation (the Eisen rule). After certification, the accused firm generally petitions

the court for dismissal, which is discretionary and sometimes granted. Here we take

some comfort from the fact that we selected our sample to being in 1996, following the

passage of the Private Securities Litigation Reform Act of 1995 which was designed in

large part to deter frivolous law suits. We further restrict our attention to suits that have

not been dismissed, something that was easier to achieve following the PSLRA. 2

1 The number of suits filed is actually much larger as multiple class action suits almost always appear for each case but are usually collapsed into a single case before reaching the court. Stanford has condensed multiple suits aimed at the same firm for the same events into one record. The count of suits is from November 2004.

2 If the suit is not dismissed, negotiations commence among the parties, which can be prolonged by waiting

for the outcome of other investigation testifying to the validity of fraud claims. Cases never reach the point of having a court verdict for the simple reason that Directors and Officers’ Liability insurance contracts do not cover liabilities in which securities fraud are proven in court. Thus, if the suits are not dismissed in initial hearings, the executives of the defendant firm always force settlement of the case. The time in between the dismissal ruling and the settlement is spent bargaining for settlement on the strength of the claim.

7

As a third step, we introduce additional criteria for removing what might be

frivolous suits by following the legal literature of Grundfest (1995), Choi (2004) and

Choi, Nelson, and Pritchard (2005) that suggest a dollar value for settlement as an

indicator of whether a suit is frivolous or has merit. Grundfest establishes a regularity

that suits which settle below a $2.5 -$1.5 million threshold are on average frivolous. The

range on average reflects the cost to the law firm for its effort in filing. A firm settling

for less than $1.5 million is most almost certainly just paying lawyers fees to avoid

negative court exposure. To be sure, we employ the high end of the range ($2.5 million)

as our cutoff.

Imposing these criteria that the cases not be subsequently dismissed by the court

or they be settled for more than $3 million, results in a sample of 192 corporate frauds.3

Figure 1 shows how our final sample relates to the larger sample of suits in the Stanford

Class Action Database. In broad measure the number of observations by year in our

sample reflects the underlying number of observations in the broader database, with an

overrepresentation of observations from 2002.

Although this procedure filters out 50% of our cases, we employ a final stringent

rule to remove cases from our dataset which may not represent fraud. In the course of

doing the case studies, we discover a handful of mostly high profile firms that settle for

amounts greater than $3 million, but against whom allegations of misrepresentation fraud

seem difficult to prove. The rule we apply to remove cases in which the firm’s poor ex

post realization could not have been known to the firm at the time when the firm or its

executives issued a positive outlook statement for which they are later sued. This filter

removes 12 cases. Our resultant dataset of 179 cases are those with a high likelihood of a

true fraud.

The moral for us is that beyond ruling out cases which are dismissed or not certified, there is no verdict to which we can default in asserting that the firms we study have in fact committed fraud. Some cases are settled by firms to remove the nuisance, insurance risk and publicity exposure of going to court. Therefore, the fact that a case settles does not directly imply that the firm actions were fraudulent. 3 As a robustness check on our findings, we also employ the additional filter suggested by Choi, Nelson, and Pritchard, (2005), who suggest a more stringent filter of removing firms who are not investigated by a regulator for the alleged fraud and frauds for which the settlement amount does not reach 4% of the market capitalization at risk.

8

Variables

For each of the 179 cases, we manually collect information on the fraud and its

detection from Factiva newswires. We compile data for 11, often categorical, fields –

settlement date, settlement amount, class period, impropriety, whistleblower, whistle

blown to whom, trigger factor, timing factor, motivation, auditor change, and

resignations. In this subsection we define these fields and describe the data collection in

the context of the flow of preparing a case study. A listing of the categories applied in

each of the fields is provided as Table 1.

In the pre-screening searches to determine if a case is dismissed or settled below

the $2.5 million threshold, we collect settlement amounts and settlement dates. Firms are

not required by law to disclose settlement details, but they frequently do. Their balance

sheets generally have already accrued for the expense, and their annual reports have

already notified shareholders of an exposure to the suit. Thus, a settlement represents a

closure to an uncertainty.

The second step in each case study is to identify the time period and allegations

for the fraud. We search Factiva over the range one month before and after the suit date

given in the Stanford Clearinghouse, looking specifically for law firm newswires

announcing the class action suit. Often there are multiple law firms announcing suits for

a particular litigant. From the suit announcements, we extracted the class period defined

as the maximum spread of time over which the fraud was allegedly committed.4

The next step in each case is to conduct a thorough search of news reports on the

firm beginning three months prior to the class period and going until the settlement date

or until current (summer, 2005) if the case is yet pending. We limit searches to having

the firm name in the first 30 words of the article, but we do not restrict the media source

from which the article might be drawn. In a number of cases, local newspapers conduct

more thorough investigative reporting of local firms, and thus we sacrifice having to read

more articles rather than miss such important fact-finding.

4 The Stanford Clearinghouse also contains information on allegation categories and class periods. We supplemented our information with that in Stanford when Stanford had additional information. Unfortunately, the Stanford allegation data are yet incomplete for periods past 1999, and upon occasion, the class periods in Stanford are inconsistent with those reported in newswires.

9

Our searches return an approximate average of 600 articles per case. The number

of articles increases with length of the class period, the severity of the allegation, and the

size or media exposure of the litigant firm. The number of articles per firm also generally

increases during and following the Enron scandal.

The large set of articles first provides us with material to develop a full

understanding of the chain of events surrounding the scandal, and second allows us to

uncover answers to a series of questions. Our first question is: what misconducts are

behind the allegation? We call the answer the impropriety field and allow up to three

selections from the list reported in Table 1. The improprieties generally fall into false

disclosures, misrepresentations, and engagement in illegal activities.

A second question follows from the identification of improprieties: what was the

motive for the fraud? The motive category tries to understand why the fraud occurred.

For example, frauds often occur when a firm wants to keep its stock price artificially

elevated for raising capital or using stock to acquire another firm. The motive category

helps us to understand the context of the fraud.

The third, and most central, question we ask of the newswires is: who is the

whistleblower? The whistleblower field is not restricted to be a person; rather we define

the whistleblower as the entity which forces the fraud to light. Our set of whistleblowers

includes items falling under the broad categories of internal governance, stakeholders,

reputation intermediaries, regulators, and information intermediaries. A full listing of the

categories is presented in Table 1.

Often, we find that the whistleblower is not the person labeled by the media as

such. A chain of events initiated by another entity may already be forcing the scandal to

light when an individual expedites the process by disclosing internal information. For

instance, Enron’s whistleblower by our classification is the Texas edition of the Wall

Street Journal not Sherron Watkins who is called the Enron whistleblower in the media.

Of course, we do not want to discredit the importance of internal individuals identified as

bringing fraudulent activity to the public. However, our aim is to identify the initial force

that starts the snowball of a scandal coming to light. In the Enron example, investigative

reporting by the Texas version of the Wall Street Journal raises concern about Enron’s

10

marking-to-market practices and the source of firm revenues a full 8 months prior to

employee whistle blowing.

The next three data questions are closely linked to the whistleblower. To whom

did the whistleblower blow the whistle? The whistle blown to whom field is intrinsically

attached to the whistleblower in that the existence of a to whom entity often facilitates the

public disclosure of the scandal. The set of to whoms includes much the same entities

and the whistleblower category.

Also closely associated with the whistleblower are the fifth and sixth questions.

What were the triggering factors that forced the whistle to be blown in general? And,

what is the timing factor that forces the information to be disclosed on that particular

day? Of the trigger and timing factors, the timing factor is more modest in its role of

claiming that the particular day for disclosure is related to pressures from a factor internal

or external to the firm. The trigger factors field captures up to two conditions

surrounding the firm, the industry or the whistleblower that cause the fraud to come to the

fore. An understanding of the trigger factors is entirely tied to the identification of the

whistleblower. We also provide a taxonomy of trigger and timing factors in Table 1 .

3. When does corporate fraud occur?

Before we look at the entities which reveal corporate fraud, we should better understand

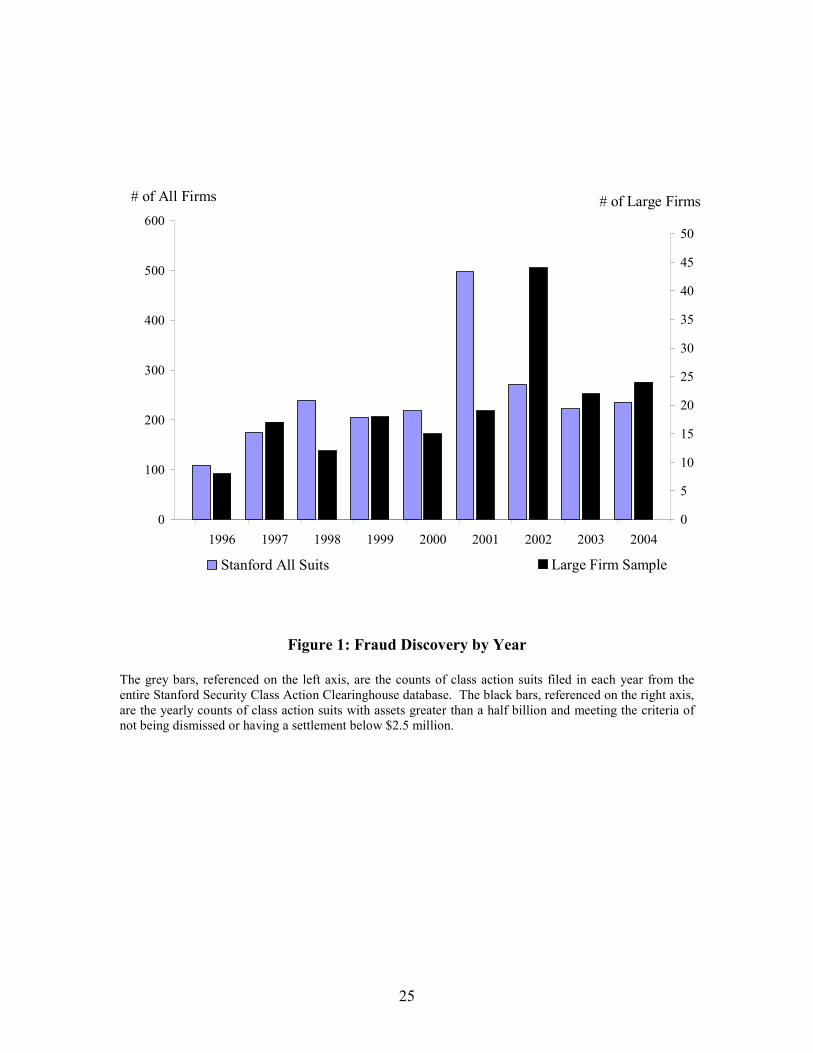

when corporate fraud occurs. In Figure 1 we plot the frequency of corporate fraud by year

of discovery since the 1995 PSLRA class action reform. The gray bars report the number

of all the cases included in the Stanford Security Class Action Clearinghouse. The black

bars (scale on the right) report the number of cases in our dataset (after we filter for

companies with more than half a billion in assets and apply the non frivolous screenings).

If we exclude the first year, where there might have been reaction to the PSLRA

and thus some learning on how to file the new class action suits, the number of class

actions suits is fairly constant, except in exhibiting a peak between 2001 and 2002. The

major difference between the two series is the timing of the peak. While the peak for all

class action suits occurs in 2001, the one for “screened” class action suits brought against

large companies peak the following year.

11

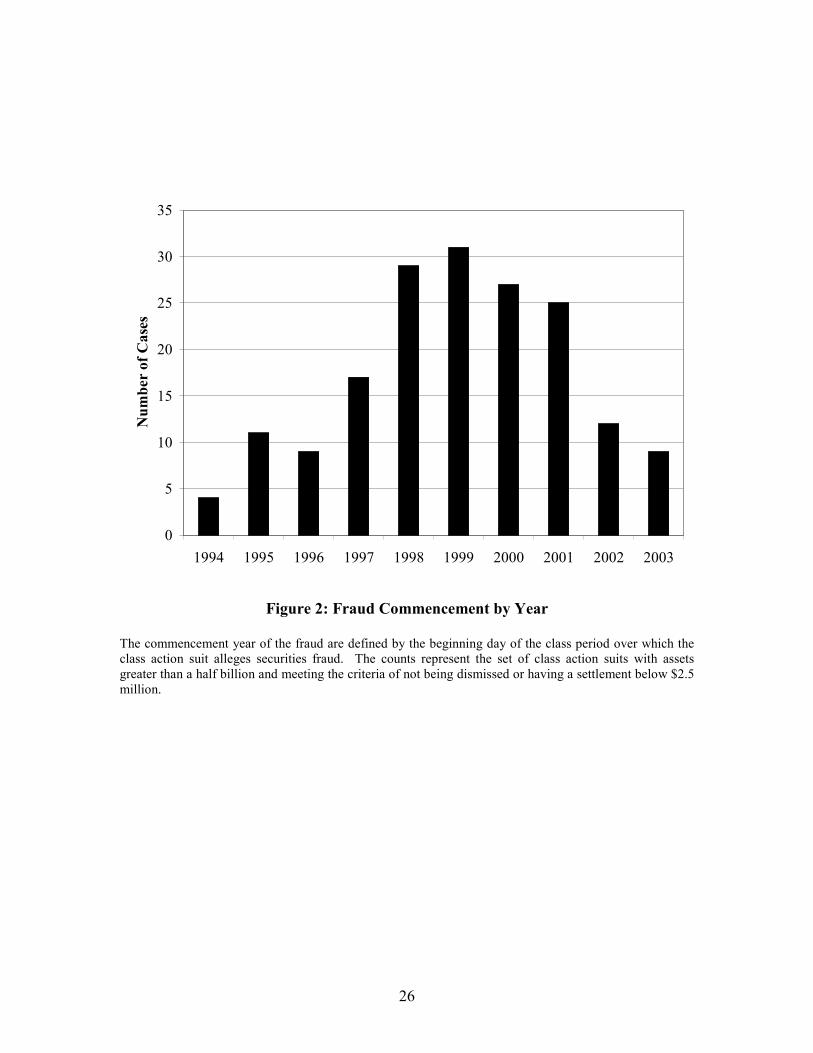

Figure 1 reports the alleged frauds according to the date the class action is filed.

In contrast, in Figure 2 we report the distribution of “screened” class action suits brought

against large companies according to the date the alleged fraud started. The picture here

is very different. There is a steady increase in the number of alleged frauds up to 1999

and then a sharp decline after 2001.

The difference between the two series is due to the following facts. Many of the

frauds brought to light after Enron had continued for a longer period of time than the

fraud brought to light before. (This is later shown in Table 7.) While the frauds exposed

before Enron had lasted for 376 days, the ones brought to light afterward had persisted

for 775 days, over twice the length of the earlier revelations.

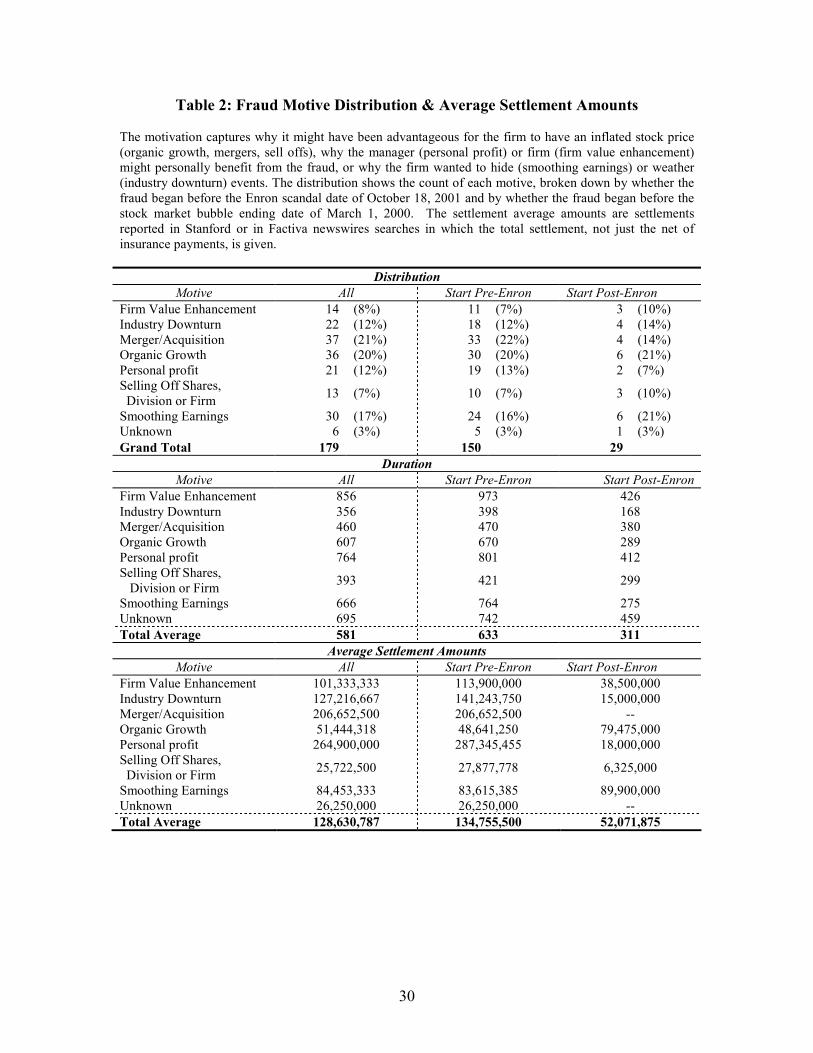

Table 2 reports the alleged motive for the frauds. Interestingly, 41% of the frauds

are committed to keep the company growing: either to finance an acquisition (21%) or

internal growth (20%). The other big motive is to smooth earnings (17% of the cases).

Personal profits appear a motivation in only 12% of the cases. The image often portrayed

in the press, of sleazy managers trying to enrich themselves at the expense of their

shareholders does not seem to be so true in the vast majority of the cases. In fact, in 8%

of the cases managers commit an impropriety (like price fixing) trying to maximize

profits.

There does not appear to be an enormous difference in the distribution of motives

for the frauds which start pre- and post-Enron. The major difference is the drop in the

number of improprieties motivated by the desire to do an acquisition. But this is not that

surprising, since the volume of M&A activity dropped significantly in the post bubble

period.

Table 3 also reports the average amount of settlement. On average, the set of class

action suits against large firms settle for $129 million. The biggest settlements occur

when the impropriety was motivated by personal profit ($264M). It is difficult to know

whether this reflects the fact that these frauds are larger or that the presence of a

managerial profit motive increases the likelihood the company would lose the case. If the

latter is true, the managers may fear personal liability and be held up for larger

settlements.

12

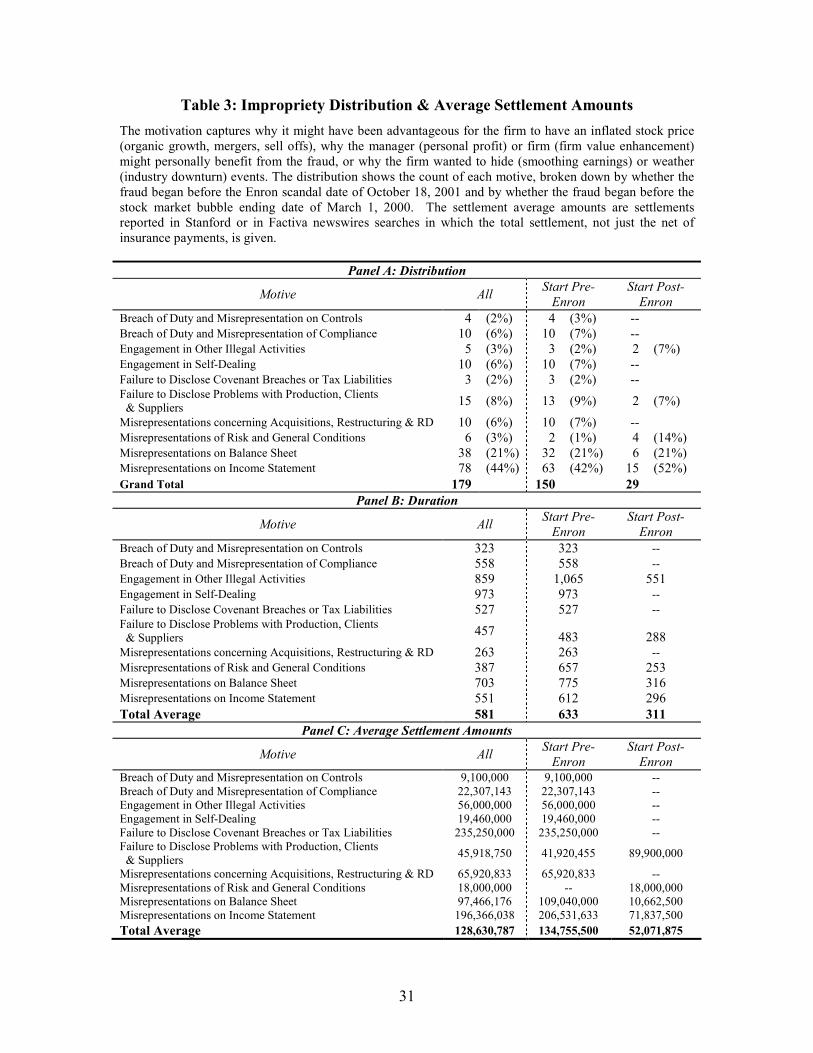

The other large frauds, in terms of settlements, seem to be the motivated by

mergers ($206). The frauds which are aimed at smoothing earnings and supporting

organic growth are much smaller ($84 and $51 M respectively). All the other impropriety

categories result in a much smaller damage settlements with the exception of

misrepresentations of tax liabilities ($235M), which is driven primarily by Dynergy,

whose Enron-style debt hiding also involved hiding from taxes.

In addition, Table 3 reports the distribution by type of impropriety. There is not a

lot of variation. Forty-four percent of the alleged frauds are misrepresentation of income,

while another 21% misrepresentation of assets. Of the two, misrepresentation of income

cases seems to be more egregious, since they settle for almost $200M on average. The

misrepresentation of assets cases settle on average for almost $100M.

Finally, Table 3 presents the duration by impropriety type. By far the longest-

lasting frauds were those related to the most severe crimes. Both engaging in self-dealing

(e.g., Adelphia and Tyco) and engaging in other illegal activities (e.g., price fixing of

Soetheby’s) are activities with fairly high probabilities of criminal prosecution if

discovered.

4. Who blows the whistle?

Now that we have a sense of the type of improprieties that have been uncovered during

the 1996-2004 period, we can investigate what leads to their discovery. Table 4 presents

the distribution of whistleblowers. We distinguish between five big categories

(information intermediaries, internal governance mechanisms, regulators, reputation

intermediaries, and stakeholders). Within each of these categories, we have the main

components of each group. The first column reports the number of cases (and the

percentages) over the whole period, while the last two columns report the same figure for

those discovered pre-Enron5 and post-Enron.

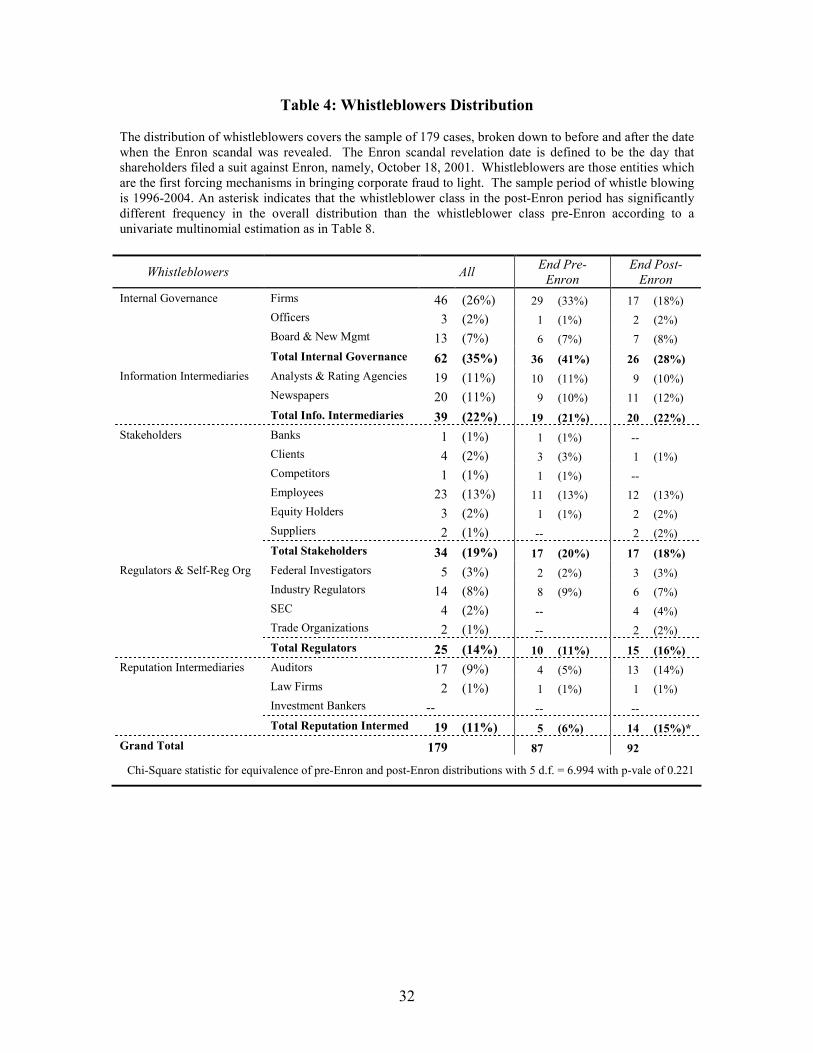

As Table 4 shows, more than a third of the cases are brought to light by the firm

itself (26%), its officers (2%), and its Board (7%). Interestingly, the role of firms as

5 Pre-Enron is defined to be the time up to October 18, 2001, the date that class action suits were filed against Enron.

13

whistleblowers has dropped dramatically, by 15%, in the post-Enron period. Although

care must be taken as this seemingly large drop in the role of the firm does not reflect a

significant distributional shift in the distribution of whistleblowers,6 the magnitude might

suggest that other mechanisms have become more active, outpacing the confessions of

the firm. Alternatively, the seemingly large shift from firm whistle blowing after Enron

may be due to the observing of fewer minor improprieties (which firms are more willing

to admit) and more severe cases which require outside governance to bring to light. We

will return to this.

The second major source of fraud detection comes from the information

intermediaries (22%), equally divided between analysts (11%) and newspapers (11%).

Their role is substantially unchanged after the Enron scandal. The post-Enron reforms

did not provide these institutions with more access to the firm. Thus, whereas regulators,

for example, would be able to respond to an increased public concern for bad firm

behavior with more investigations, it is unclear how much improvement in whistle

blowing technologies information intermediaries could achieve.

The third major source for information on fraudulent behavior is stakeholders

(19%). By far the most important group in this category is the employees (13%).

Surprisingly, their relative importance in whistle blowing has not increased after Enron,

in spite of the public support they enjoyed and the protection introduced with Sarbanes

Oxley. The other stakeholders do not frequently serve as whistle blowers, perhaps

because they are unlikely to want information disclosed that damages their claims to the

firm. If stakeholders happen upon a fraud during their monitoring access to the firm, they

would instead prefer to re-contract privately with the firm or to withdraw from

investment in the entity.

The fourth category is the regulators (14%). The lion share of these cases is

brought to light by industry regulators, not the SEC. Before Enron the SEC did not

discover any fraud; afterwards it only uprooted 4 cases (4%). A full discrediting of the

SEC may not yet be in order; the SEC may better serve as a forcing mechanism,

implicitly bringing fraud to light with letters of query and regulations. The point that this

6 Surprisingly, a multinomial logistic estimation fails to find significance in the interaction of a post-Enron dummy and the internal governance category, but many of the categories are not sufficiently filled on both sides of the Enron date weakening identification of the distributional shifts.

14

simple tabulation elucidates is that the informal and formal SEC investigations do not

seem to discover fraud. Whistle blowing by industry regulators was surprisingly

distributed among different industries. Of course, during the period, energy regulators

were very active, but insurance, banking, medical and pharmaceutical regulators all

contributed to bringing the large frauds to light.

Finally, the last source of negative news is the reputation intermediaries (11%).

Although multiple intermediaries have regular access to the firm, it is the external

auditors (9%) who do the whistle blowing for this class. Here we do see a dramatic and

significant change after the emergence of the Enron scandal. While before auditors blew

the whistle in only 5% of the cases, after Enron begins to unravel, their share jumped to

14%. As we will see, this is a natural and healthy response to scandals: all the parties

involved become more concerned about the possible reputation effect of missing a sign of

fraud.

One unexpected result is that there are zero instances of an investment banker

whistleblower. Reputation is of course very important in investment banking contracting,

but there would be little benefit for investment bankers to disclose fraudulent activity

discovered in their preferred access to client records versus just to discontinue

representing the firm.

Why blow the whistle?

Blowing the whistle is very costly. Individuals face shunning by their co-workers; firms

may lose product market clients and reputation; auditors lose contracts; etc. Therefore, it

is very rare that frauds are brought to light by accident. There is usually a context or

triggering factor that leads a firm or an individual to blow the whistle. Table 5

summarizes the major triggering factors. In order to emphasize the importance of the role

of triggers, we describe the key results from Table 5 with our case examples.

One of the major triggering factors is routine earning announcements. Firms and

their management are very aware of these quarterly obligations and are afraid to face the

analysts without a compelling story. When one cannot be found, it is potentially easier to

admit the possible wrongdoing. Earnings announcement are equally important as fodder

for external governance mechanisms. A stereotypical example is found in hardware

15

maker 3Com. The firm’s unusual inventory-to-revenue quarterly figures sufficiently

intrigued the San Francisco Chronicle as to lead the paper to investigate the production

of 3Com’s newly acquired U.S. Robotics division. The truth soon emerged that contrary

to its revenue reporting, U.S. Robotics had not even been in production, and that much of

3Com’s other revenues were only the result of channel stuffing.7

An equally important triggering factor is a negative shock to the business (16%).

The business shocks often appear in the form of a product failure or loss of a client. A

prime example comes from the case of FirstEnergy, whose poorly maintained power

facility caused the largest power outage in North American history. The product failure,

ironically, triggered the discovery of accounting fraud. An interesting observation from

Table 5 is that business shocks were much more of a factor before Enron (21%), than

afterwards (11%).

The third major factor in bringing negative news to light is some form of outside

scrutiny (16%), such as investigations and due diligence. El Paso Corporation gives us

two concurrent examples of such scrutinizing. The Houston office of the U.S. Attorney

General uncovered El Paso Corp.’s $3.6 billion hedge accounting irregularity while

investigating local energy companies for round trip trades, which had been common in

the Enron era. At almost the same time, the Federal Energy Regulatory Commission

uncovered that El Paso had been involved in the price fixing scandal in California. The

investigation in the latter case was specifically searching for impropriety that was found,

but as the former El Paso case illustrates, it need not be so.

After Enron, another category that surges in importance is the fallout from the

scandals (14%). This is another example of the automatic response to scandals. An

increase in the alertness of the public to certain problems can force firms to come clean or

facilitate potential whistle blowers to come forward. Scandal fallout is not only an

energy firm phenomenon; widespread usage of financing vehicles, for example, became

an automatic trigger for attention by regulators.

Another very important triggering factor is managerial turnover (13%). Not only

do new CEOs undo previous CEOs’ acquisitions (Weisbach, 1998), but they also expose

7 Channel stuffing is accomplished by filling the downstream distribution lines with excess production to inflate current sales revenues, at the expense of future revenue recognition.

16

their wrongdoings. In the case of Rite Aid, after the former CEO is fired for inventory

irregularities and general poor performance, the new CEO discovers that the previous

executive had pledged the company’s assets on short-term debt and then falsified the

records for board approval. Because managerial turnover is a key governance mechanism

for the board, it is not surprising (and perhaps even reassuring) that the triggering effect

of turnover like Rite Aid’s example is stronger after Enron (15% vs. 10%).

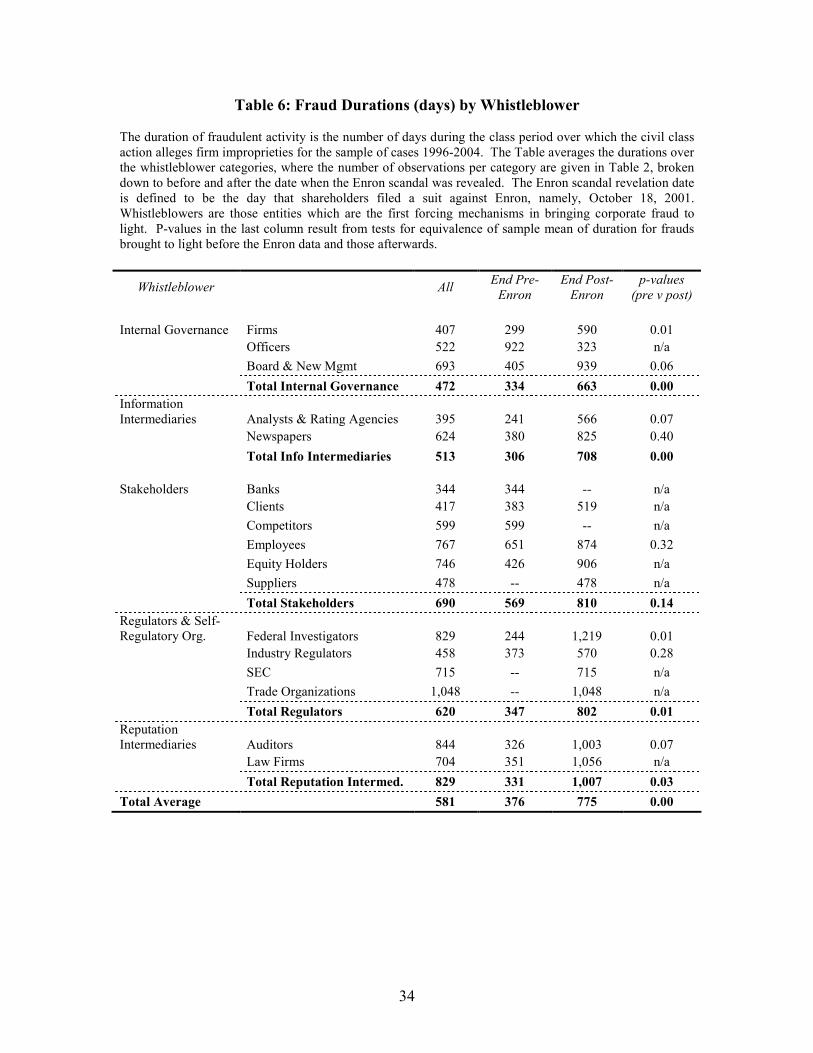

How promptly did they blow the whistle?

All the whistleblowers can be considered as competing sources of negative news. If we

start from the safe assumption that the sooner news about fraud emerges, the better, then

we can measure the relative efficiency of the various mechanisms by comparing the

relative duration of the fraud uncovered. This is what we do in Table 6. Before analyzing

the data, however, it is important to recall that the duration means come from very

selected samples: frauds that have been uncovered.

From the simple cross sectional variation in Table 6, the earliest warning system

is the analysts. On average, analysts identify fraud that lasted for only 395 days (vs. an

average of 581). The second most efficient source of misdeeds is the firm itself (407

days). A surprising fact is the relative similarities of the duration of frauds uncovered by

the other sources. Board, officers and external auditors do not seem to be more effective

than the newspapers and employees (all at roughly 2 years).

The picture that emerges is the following. Analysts and the firm are able to bring

to light some frauds relatively early. When this first line of defense fails, the second line

takes much longer. This could be due to the fact that such frauds are more hidden or that

these alternative mechanisms take much longer to have an effect.

The most striking result of Table 6, however, is that the average duration of fraud

discovered after Enron is twice as long as the average duration of fraud discovered before

it. T-tests in the Table show that the pre-Enron durations are almost always significant

different from post-Enron ones for most categories of whistleblower. With the exception

of the officers category, which has only two cases, not only is the trend of increased

duration present in all the categories, but the doubling of the duration is also systematic in

most subcategories. The likely interpretation is that the increased alertedness after Enron

17

contributes to bringing to light a set of more rooted and long lasting frauds, notably those

which were not intercepted before Enron.

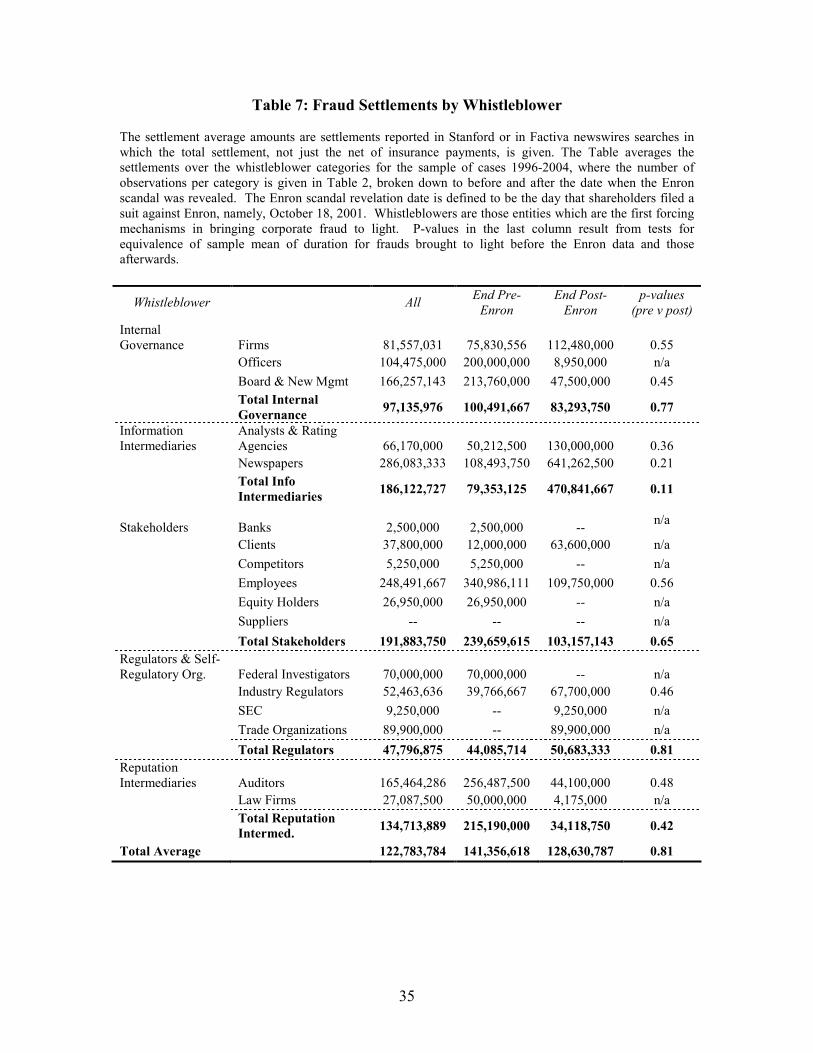

How loud does the whistle blow?

Table 7 shows the mean fraud settlement amounts by whistleblower. If settlement

amounts are a reasonable measure of the size of the fraud, we can infer which

mechanisms bring the important frauds to light. Employees and newspapers are the most

important sources of information for large improprieties (roughly $250M for both). The

second most important source of information on big cases is the auditors, who on average

blow the whistle on cases that settle for $165M. The third most important source is the

firm itself and its officers, with almost $100M on average. Analysts and federal

investigators seem to be most effective against smaller cases (average around $60M).

Table 7 also illustrates that the size of frauds brought to light by the various

whistleblowers did not change much after Enron. Auditors and employees start to be

more active on smaller cases, while analysts and newspapers seem to be left only with the

really big cases. Significance tests for the difference in settlement amounts pre- and post-

Enron for individual whistleblower categories are all insignificant, in stark contrast to the

duration analysis. Although very large settlements make such tests difficult to interpret,

even at the aggregate level, settlements do not vary by period.

There are two potential explanations for this result. The first is simply that the

accelerated attention to corporate fraud induced by the Enron scandal did not change the

distribution of fraud types or size. Rather, Enron only served to alter the whistle blowing

competition and thereby to affect the types of crimes and the embeddedness of crimes

discovered by whistle blowers. The tabulations presented in this section lend much

support to this hypothesis. The second explanation for the relatively stable settlement

amounts may be that fear of detection has changed the magnitude of fraud but that greater

attention to the discovery of fraud may have uprooted some large skeletons in the closets

of U.S. corporations.

The key findings that emerge from simple cross-tabulations are four-fold. First,

the firm blows the whistle on itself in a quarter of the cases, but other internal governance

18

mechanisms only serve as whistle blowers in an additional 7% of the cases. Second,

although auditors do share in the whistle blowing, external whistle blowing occurrences

are not dominated by reputation intermediaries. Instead, analyst, newspapers and industry

regulators all are important whistle blowers which suggests that good governance is

characterized by multiple enforcement mechanisms. Third, firms and analysts blow the

whistle quicker than all other parties. And forth, frauds discovered after Enron are

roughly the same size in settlements as those discovered prior to Enron; however, the

duration of the frauds discovered in the later period are twice as long, no matter who

blew the whistle.

5. Cross-sectional analysis

To draw a coherent picture of the effectiveness of whistleblowers and the impact of the

Enron scandal fallout, we delve more into the relationship between the type of

impropriety and the whistle blower identity. Already, we have shown that it does not

appear that some whistleblowers have an absolute advantage over others. In order to

make proper inferences about the relative success of whistle blowing groups, it is useful

to ascertain whether whistleblowers compete in the market for information with each

having its own comparative advantage. To begin to address comparative advantages, we

look more closely at whether certain whistle blowing entities curtail frauds quicker. The

answer from Table 6 would seem to be ‘yes’ – analysts and the firm blow the whistle on

fraud quicker. That conclusion, however, would not be the correct inference if each

whistle blower type has a comparative advantage for discovering some type of fraud, and

the types of fraud vary in their degree of difficulty to detect.

In the remainder of this section, we first look at a multinomial analysis to test

whether whistleblowers specialize in detecting certain types of fraud. Then, we test

whether some types of whistle blowers are able to bring information to light more quickly

than others after controlling for the impropriety type. As a final important step in our

analysis, we ask whether specialization and the speed of fraud detection have changed

post-Enron. If so, we draw inference on how the public outrage toward such corporate

governance abuses has altered the landscape of monitoring for fraud.

19

Whistleblower specialization

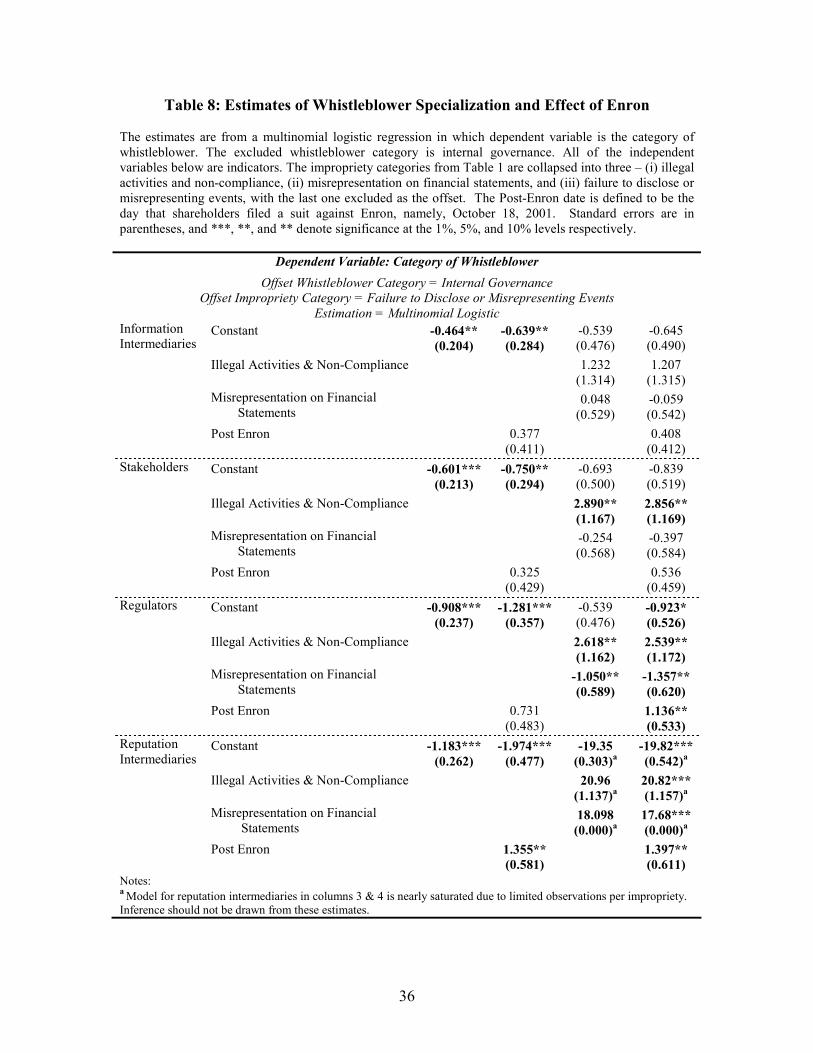

Table 8 presents the estimates from a multinomial logistic regression in which the

dependent variable is the categorical variable of the five big whistleblower types. The

multinomial model is used to understand whether the realization of a particular whistle

blower type is associated with types of improprieties. The model estimates coefficients

capturing each specific whistle blower’s association with each type of impropriety

committed. Because the number of coefficients grows large in the multinomial block, we

collapse improprieties into three categories to allow us to focus on the whistle blower

variation. The three impropriety categories are illegal activities and non-compliances,

misrepresentations on financial statements, and failures to disclose events or realizations

pertinent to the firm. The last category will serve as our offset in the estimation since we

would like to make inferences on the well-understood categories of financial mis-

statements and actions which are illegal even without mis-reportings. We likewise must

choose an offset for the whistle blower. Since our contribution is in looking outside the

firm for governance, we set the internal governance whistle as the offset.

Column 1 of Table 8 shows an estimation that essentially replicates the

distributional findings. Relative to internal governance mechanisms, whistle blowers are

less likely, in increasing order, to be information intermediaries, stakeholders, regulators

and then reputation intermediaries. As mentioned earlier, column 2 reports that only

reputation intermediaries’ frequency of whistle blowing is significantly impacted

(positively) by Enron.

Column 3 asks the central issue of whether there is a greater likelihood for whistle

blowers to be linked to particular improprieties. We cannot draw inferences from the

reputation coefficients, as the model is close to being saturated with the few whistle

blowers of that type, but results from the other categories are quite intuitive. Information

intermediaries do not seem to specialize in any particular type of discovery. Relative to

internal governance whistle blowers, both stakeholders and regulators are more skilled at

bringing illegal activities to light. Finally, regulators (primarily industry regulators)

specialize less in financial statement misrepresentations than do the internal governance

whistle blowers.

20

Column 4 again adds an indicator for the post-Enron period. Ideally, we would

like to estimate the associations of pre-and post-Enron coefficients on the specific

relationships between whistle blowers and improprieties, but our data do not contain

sufficient post-Enron observations to interact the post-Enron dummy with the

improprieties. However, we can see if the associations change once we control for an

Enron time effect.

We find that after including a control for the fraud emerging post-Enron,

information intermediaries remain non-specialists relative to internal governance

whistleblowers and have no change in frequency of discovery post-Enron. Likewise, the

results pertaining to stakeholders do not change; stakeholders are more specialized to

uncovering illegal activities than are internal governance whistle blowers. Regulators,

however grow significantly stronger as whistleblowers in the post-Enron period. Our

univariate results had previously not been able to identify this natural ramping-up of the

role of regulators following the Enron scandal. Controlling for the Enron period does not

negate the column 3 finding that compared to internal governance whistle blowers,

regulators are more effective in bringing illegal activities to light and less effective in

uncovering financial mis-statements.

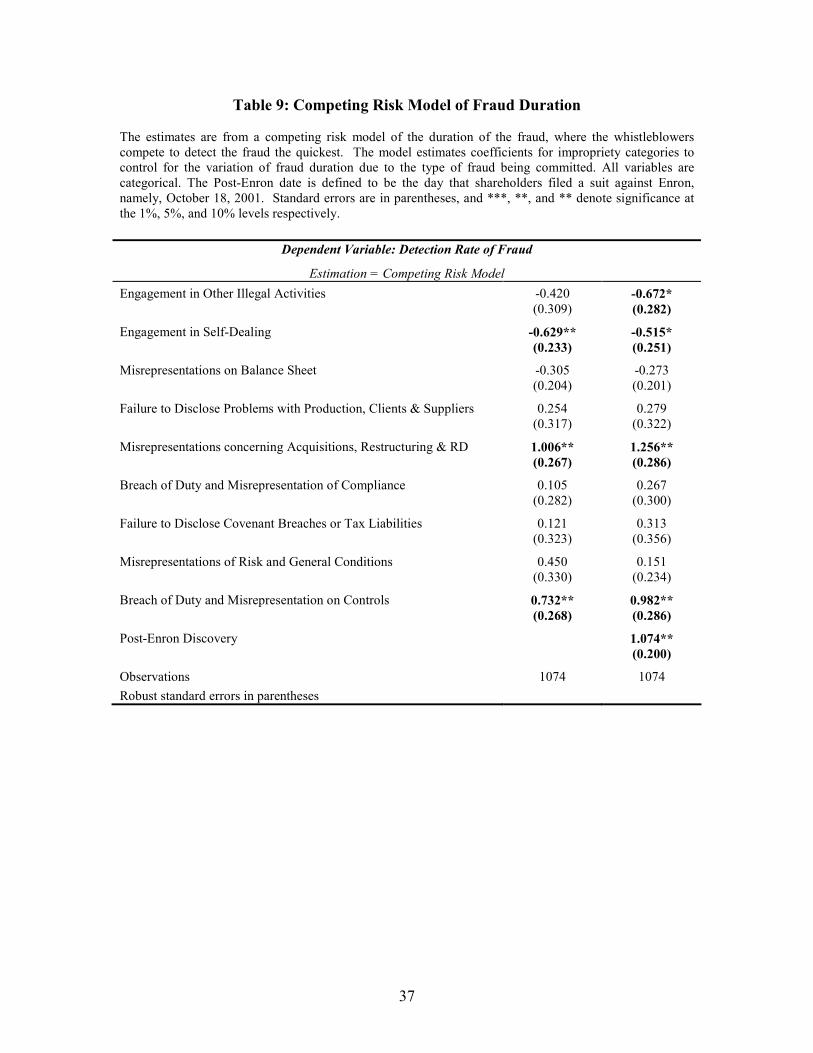

Competing risk model

We are now in a position to analyze the speed with which whistle blowers uncover fraud.

We want to determine whether our univariate duration finding that analysts and firms are

the fastest whistle blowers might be related to the type of fraud in which these whistle

blowers specialize. From the previous section, we know that there is some specialization

of whistle blowers. Analysts do not specialize in the type of impropriety revealed more

than internal governance mechanisms do, but other whistle blowers do have particular

types of improprieties which they seem to have an advantage in discovering. These

findings are relative and do not rule out the possibility that speed of discovery and

impropriety type revealed are related.

We can address the time efficiency of whistleblowers more formally in a

competing risk framework. Competing risk models are variants of hazard rate analyses in

21

which outcomes compete to occur first.8 We estimate the risk of being detected by

competing whistle blowers after controlling for an adjustment to the risk, common to all

whistle blower categories, for the type of impropriety being committed. In other words,

after taking out the risk of exposure due to the fact that some types of fraud are simply

easier to detect, we calculate the risk of having one’s fraud detected by the competing

whistle blowers.

Table 9 presents the estimation results. Self dealing and engaging in illegal

activities are significantly harder to detect. Conversely, misrepresentations regarding

firm opportunities, acquisitions and controls result in quicker detection. Both of these

results are consistent with our intuition. More serious crimes will be more deeply rooted

in the firm, and thus, detection should take longer. Misrepresentation about opportunities

can be short-term by definition. When mergers or R&D finish their implementation, the

frauds are often forced to surface. Column 2 of Table 9 also shows that the detection rate

has increased after the Enron scandal.

Although these results are interesting by themselves, our primary goal of the

competing risk model is to assess the speed of detection among whistleblower classes.

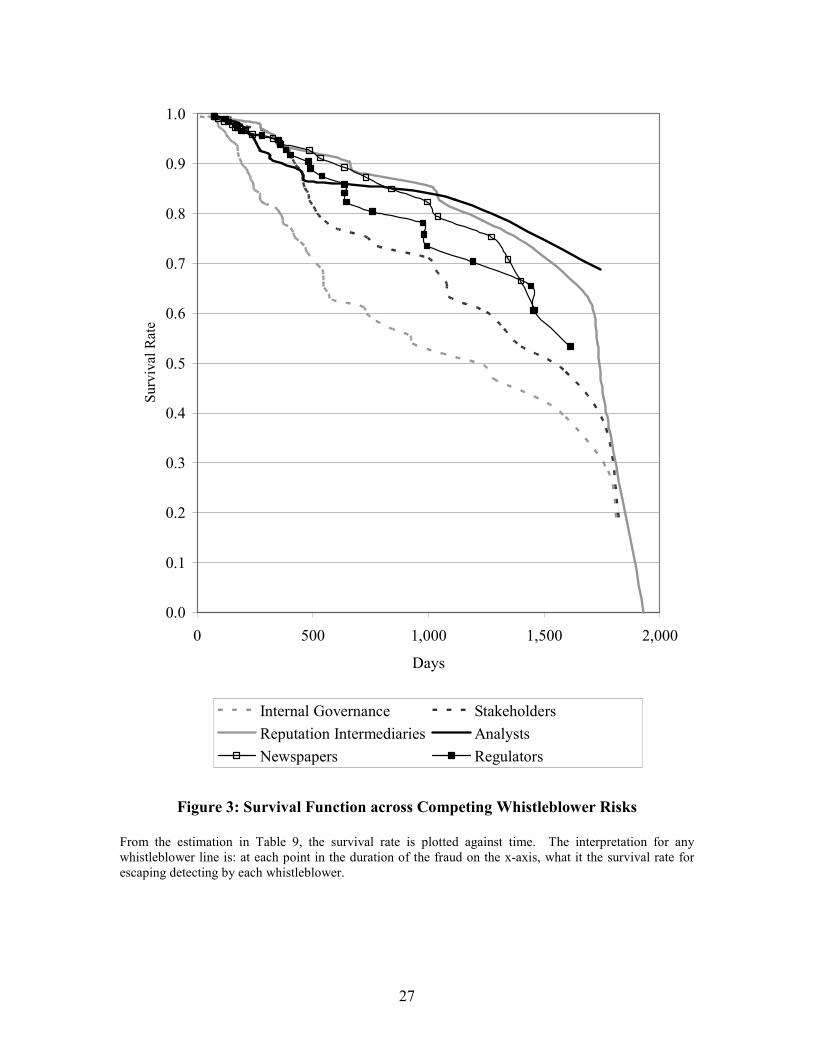

For this, we estimate the survival rate from the estimation in column 1 of Table 9 for each

of the stratified classes of whistleblowers. The survival function, defined as the

probability of surviving another day given that the fraud has survived up to the point in

question, is plotted in Figure 3 by whistleblower.

It is easiest to understand Figure 3 by interpreting the dashed grey line for the

internal governance whistleblowers. The internal governance line is always beneath all

other lines, implying that if the fraud has not already been detected, the probability of

surviving detection by the internal mechanisms of the firm are always lower than the

probability of surviving other whistle blowing risk. Said another way, internal

governance mechanisms pose the greater hazard for managers committing fraud. Even

after controlling for impropriety type, the firm’s internal governance detects fraud the

quickest.

8 The word ‘risk’ comes from the fact that this genre of models first was, and still most frequently is, used in epidemiology studies.

22

If the firm’s governance mechanisms do not reveal the fraud, which we know to

be true in 75% of the cases, which whistle blower moves with the greatest speed to

uncover the misdeeds? From our earlier summary statistics, we know that analysts have

significantly shorter detection times than other whistle blower groups, equivalent to that

of the firm. The solid black line shows that compared against all other whistle blower

classes except internal governance mechanisms, analysts detect corporate fraud the most

easily (as shown through lower survival rates) but only for a short window in the fraud

life – from a half-year to a year and a half. Not coincidentally, the bulk of analyst whistle

blowing occurs in this duration window. After that point, it is the stakeholders, primarily

employees, who pose the greatest risk for detecting frauds missed by internal governance.

Figure 3 leaves one final impression that is worth note. Although this discussion

has used the competing risk model to offer a ranking of whistle blowing speeds, the order

of magnitude for the risk of detection is very comparable across whistle blower groups,

other than internal governance mechanism. Also, there is no absolute ordering of

whistleblower risk once internal governance fails.

6. Conclusions

Much of the literature in corporate governance emphasizes the role of regulators (Glaeser

et al., 2000) or private enforcement (La Porta et al., 2003) as primary mechanisms to

protect shareholders. Our analysis suggests that if we focus on the discovery process,

neither channel seems to be important. Derivative suits and the SEC have only a very

minor role in the discovery process. By contrast, analysts, employees, and newspapers

seem to play a much bigger (and not properly emphasized) role. Of course, securities

regulators and private enforcement are not useless as governance institutions. They play

an important role in shaping the magnitude of penalties, once corporate frauds are

discovered. Nevertheless, no penalty can be assessed until the impropriety is brought to

light. Hence, we establish that non-traditional mechanisms such as analysts, employees,

and newspapers are at least as important (if not more) than the ones emphasized in the

literature.

23

Our findings also suggest how difficult it is to export the U.S. system of corporate

governance abroad. Even in the best of systems, internal governance fails to expose the

majority of frauds. Furthermore, the failures of internal mechanisms cannot be solved by

simply introducing derivative suits or copying the SEC. An effective corporate

governance system relies on a complex web of mechanisms that complement each other.

Reproducing such a myriad in other countries is more difficult than copy a single

institution.

24

References

Choi, Stephen J. 2004, "Do the Merits Matter Less after the Private Securities Litigation

Reform Act?" Working Paper.

Choi, Stephen J. 2005, "Behavioral Economics and the SEC.” Working Paper

Choi, Stephen J., Karen K. Nelson and A.C. Pritchard. 2005. “The Screening Effect of

the Securities Litigation Reform Act.” Working Paper.

Cox, James D., Randall S. Thomas and Diku Kiku. 2003. "SEC Enforcement Heuristics:

An Empirical Inquiry." Duke Law Journal, 53(2), pp. 737-79.

Grundfest, Joseph A. 1995. “Why Disimply?” Harvard Law Review, 108, 740-741. Johnson, Marilyn F., Ron Kasznik, and Karen K. Nelson. 2000. “Shareholder Wealth Effects of the Private Securities Litigation Reform Act of 1995.” Review of Accounting Studies,” 5(3) 217-233. Johnson, Marilyn F., Karen K. Nelson and A.C. Pritchard. 2003. “Do the Merits Matter More? Class Actions under the Private Securities Litigation Reform Act.” Working Paper.

25

# of All Firms # of Large Firms

0

100

200

300

400

500

600

1996 1997 1998 1999 2000 2001 2002 2003 2004

Stanford All Suits

0

5

10

15

20

25

30

35

40

45

50

1996 1997 1998 1999 2000 2001 2002 2003 2004

Large Firm Sample

Figure 1: Fraud Discovery by Year

The grey bars, referenced on the left axis, are the counts of class action suits filed in each year from the entire Stanford Security Class Action Clearinghouse database. The black bars, referenced on the right axis, are the yearly counts of class action suits with assets greater than a half billion and meeting the criteria of not being dismissed or having a settlement below $2.5 million.

26

0

5

10

15

20

25

30

35

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Number of Cases

Figure 2: Fraud Commencement by Year

The commencement year of the fraud are defined by the beginning day of the class period over which the class action suit alleges securities fraud. The counts represent the set of class action suits with assets greater than a half billion and meeting the criteria of not being dismissed or having a settlement below $2.5 million.

27

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0 500 1,000 1,500 2,000

Days

Survival Rate

Internal Governance Stakeholders

Reputation Intermediaries Analysts

Newspapers Regulators

Figure 3: Survival Function across Competing Whistleblower Risks

From the estimation in Table 9, the survival rate is plotted against time. The interpretation for any whistleblower line is: at each point in the duration of the fraud on the x-axis, what it the survival rate for escaping detecting by each whistleblower.

28

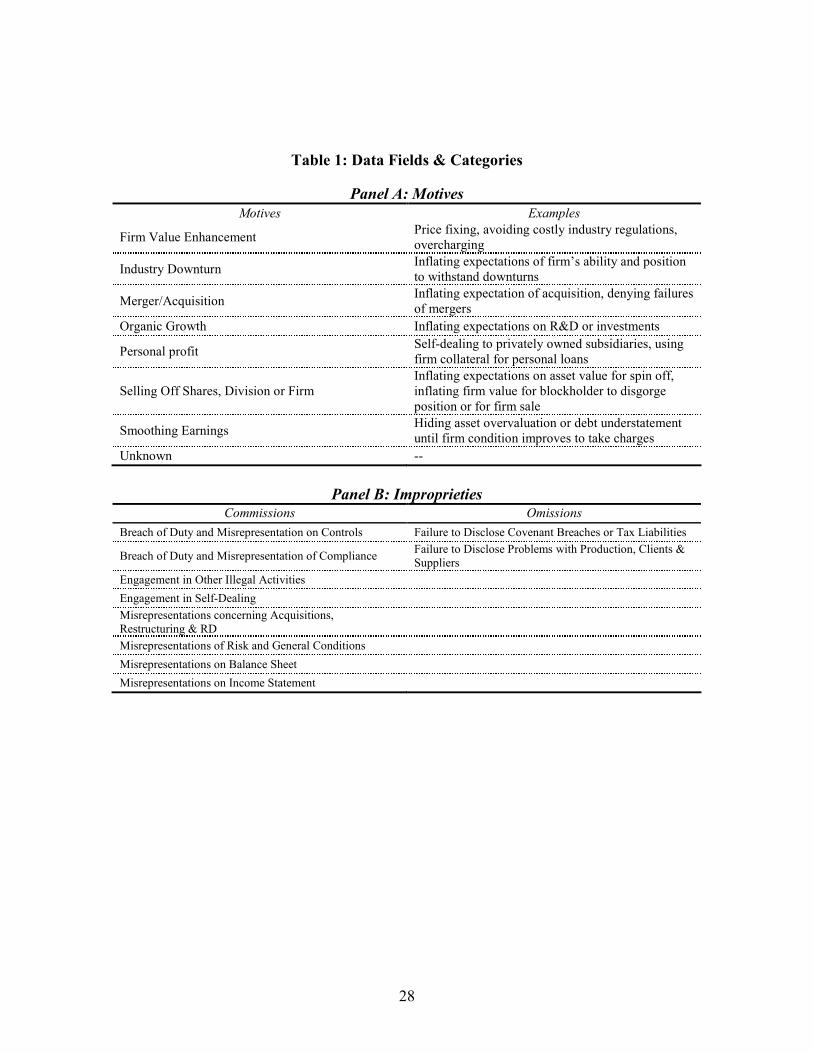

Table 1: Data Fields & Categories

Panel A: Motives

Motives Examples

Firm Value Enhancement Price fixing, avoiding costly industry regulations, overcharging

Industry Downturn Inflating expectations of firm’s ability and position to withstand downturns

Merger/Acquisition Inflating expectation of acquisition, denying failures of mergers

Organic Growth Inflating expectations on R&D or investments

Personal profit Self-dealing to privately owned subsidiaries, using firm collateral for personal loans

Selling Off Shares, Division or Firm Inflating expectations on asset value for spin off, inflating firm value for blockholder to disgorge position or for firm sale

Smoothing Earnings Hiding asset overvaluation or debt understatement until firm condition improves to take charges

Unknown --

Panel B: Improprieties Commissions Omissions

Breach of Duty and Misrepresentation on Controls Failure to Disclose Covenant Breaches or Tax Liabilities

Breach of Duty and Misrepresentation of Compliance Failure to Disclose Problems with Production, Clients & Suppliers

Engagement in Other Illegal Activities

Engagement in Self-Dealing

Misrepresentations concerning Acquisitions, Restructuring & RD

Misrepresentations of Risk and General Conditions

Misrepresentations on Balance Sheet

Misrepresentations on Income Statement

29

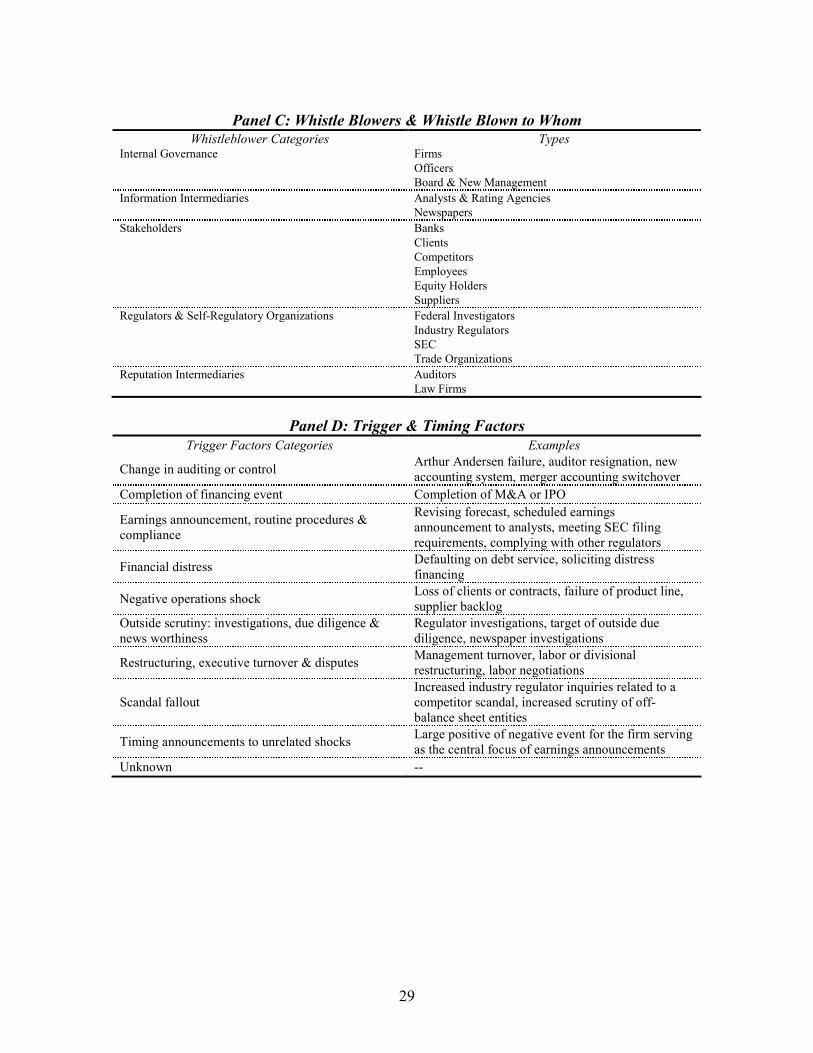

Panel C: Whistle Blowers & Whistle Blown to Whom Whistleblower Categories Types

Internal Governance Firms Officers Board & New Management

Information Intermediaries Analysts & Rating Agencies Newspapers

Stakeholders Banks Clients Competitors Employees Equity Holders Suppliers

Regulators & Self-Regulatory Organizations Federal Investigators Industry Regulators SEC Trade Organizations

Reputation Intermediaries Auditors Law Firms

Panel D: Trigger & Timing Factors

Trigger Factors Categories Examples

Change in auditing or control Arthur Andersen failure, auditor resignation, new accounting system, merger accounting switchover

Completion of financing event Completion of M&A or IPO

Earnings announcement, routine procedures & compliance

Revising forecast, scheduled earnings announcement to analysts, meeting SEC filing requirements, complying with other regulators

Financial distress Defaulting on debt service, soliciting distress financing

Negative operations shock Loss of clients or contracts, failure of product line, supplier backlog

Outside scrutiny: investigations, due diligence & news worthiness

Regulator investigations, target of outside due diligence, newspaper investigations

Restructuring, executive turnover & disputes Management turnover, labor or divisional restructuring, labor negotiations

Scandal fallout Increased industry regulator inquiries related to a competitor scandal, increased scrutiny of off-balance sheet entities

Timing announcements to unrelated shocks Large positive of negative event for the firm serving as the central focus of earnings announcements

Unknown --

30

Table 2: Fraud Motive Distribution & Average Settlement Amounts The motivation captures why it might have been advantageous for the firm to have an inflated stock price (organic growth, mergers, sell offs), why the manager (personal profit) or firm (firm value enhancement) might personally benefit from the fraud, or why the firm wanted to hide (smoothing earnings) or weather (industry downturn) events. The distribution shows the count of each motive, broken down by whether the fraud began before the Enron scandal date of October 18, 2001 and by whether the fraud began before the stock market bubble ending date of March 1, 2000. The settlement average amounts are settlements reported in Stanford or in Factiva newswires searches in which the total settlement, not just the net of insurance payments, is given.

Distribution

Motive All Start Pre-Enron Start Post-Enron

Firm Value Enhancement 14 (8%) 11 (7%) 3 (10%) Industry Downturn 22 (12%) 18 (12%) 4 (14%) Merger/Acquisition 37 (21%) 33 (22%) 4 (14%) Organic Growth 36 (20%) 30 (20%) 6 (21%) Personal profit 21 (12%) 19 (13%) 2 (7%) Selling Off Shares, Division or Firm

13 (7%) 10 (7%) 3 (10%)

Smoothing Earnings 30 (17%) 24 (16%) 6 (21%) Unknown 6 (3%) 5 (3%) 1 (3%)

Grand Total 179 150 29

Duration

Motive All Start Pre-Enron Start Post-Enron

Firm Value Enhancement 856 973 426

Industry Downturn 356 398 168 Merger/Acquisition 460 470 380 Organic Growth 607 670 289 Personal profit 764 801 412 Selling Off Shares, Division or Firm

393 421 299

Smoothing Earnings 666 764 275 Unknown 695 742 459

Total Average 581 633 311

Average Settlement Amounts

Motive All Start Pre-Enron Start Post-Enron

Firm Value Enhancement 101,333,333 113,900,000 38,500,000 Industry Downturn 127,216,667 141,243,750 15,000,000 Merger/Acquisition 206,652,500 206,652,500 -- Organic Growth 51,444,318 48,641,250 79,475,000 Personal profit 264,900,000 287,345,455 18,000,000 Selling Off Shares, Division or Firm

25,722,500 27,877,778 6,325,000

Smoothing Earnings 84,453,333 83,615,385 89,900,000 Unknown 26,250,000 26,250,000 --

Total Average 128,630,787 134,755,500 52,071,875

31

Table 3: Impropriety Distribution & Average Settlement Amounts

The motivation captures why it might have been advantageous for the firm to have an inflated stock price (organic growth, mergers, sell offs), why the manager (personal profit) or firm (firm value enhancement) might personally benefit from the fraud, or why the firm wanted to hide (smoothing earnings) or weather (industry downturn) events. The distribution shows the count of each motive, broken down by whether the fraud began before the Enron scandal date of October 18, 2001 and by whether the fraud began before the stock market bubble ending date of March 1, 2000. The settlement average amounts are settlements reported in Stanford or in Factiva newswires searches in which the total settlement, not just the net of insurance payments, is given.

Panel A: Distribution

Motive All Start Pre-

Enron

Start Post-

Enron

Breach of Duty and Misrepresentation on Controls 4 (2%) 4 (3%) -- Breach of Duty and Misrepresentation of Compliance 10 (6%) 10 (7%) -- Engagement in Other Illegal Activities 5 (3%) 3 (2%) 2 (7%) Engagement in Self-Dealing 10 (6%) 10 (7%) -- Failure to Disclose Covenant Breaches or Tax Liabilities 3 (2%) 3 (2%) -- Failure to Disclose Problems with Production, Clients & Suppliers

15 (8%) 13 (9%) 2 (7%)

Misrepresentations concerning Acquisitions, Restructuring & RD 10 (6%) 10 (7%) -- Misrepresentations of Risk and General Conditions 6 (3%) 2 (1%) 4 (14%) Misrepresentations on Balance Sheet 38 (21%) 32 (21%) 6 (21%) Misrepresentations on Income Statement 78 (44%) 63 (42%) 15 (52%)

Grand Total 179 150 29

Panel B: Duration

Motive All Start Pre-

Enron

Start Post-

Enron

Breach of Duty and Misrepresentation on Controls 323 323 --

Breach of Duty and Misrepresentation of Compliance 558 558 --

Engagement in Other Illegal Activities 859 1,065 551 Engagement in Self-Dealing 973 973 --

Failure to Disclose Covenant Breaches or Tax Liabilities 527 527 --

Failure to Disclose Problems with Production, Clients & Suppliers

457 483 288

Misrepresentations concerning Acquisitions, Restructuring & RD 263 263 --

Misrepresentations of Risk and General Conditions 387 657 253 Misrepresentations on Balance Sheet 703 775 316 Misrepresentations on Income Statement 551 612 296

Total Average 581 633 311

Panel C: Average Settlement Amounts

Motive All Start Pre-

Enron

Start Post-

Enron Breach of Duty and Misrepresentation on Controls 9,100,000 9,100,000 -- Breach of Duty and Misrepresentation of Compliance 22,307,143 22,307,143 -- Engagement in Other Illegal Activities 56,000,000 56,000,000 -- Engagement in Self-Dealing 19,460,000 19,460,000 -- Failure to Disclose Covenant Breaches or Tax Liabilities 235,250,000 235,250,000 -- Failure to Disclose Problems with Production, Clients & Suppliers

45,918,750 41,920,455 89,900,000

Misrepresentations concerning Acquisitions, Restructuring & RD 65,920,833 65,920,833 -- Misrepresentations of Risk and General Conditions 18,000,000 -- 18,000,000 Misrepresentations on Balance Sheet 97,466,176 109,040,000 10,662,500 Misrepresentations on Income Statement 196,366,038 206,531,633 71,837,500

Total Average 128,630,787 134,755,500 52,071,875

32

Table 4: Whistleblowers Distribution The distribution of whistleblowers covers the sample of 179 cases, broken down to before and after the date when the Enron scandal was revealed. The Enron scandal revelation date is defined to be the day that shareholders filed a suit against Enron, namely, October 18, 2001. Whistleblowers are those entities which are the first forcing mechanisms in bringing corporate fraud to light. The sample period of whistle blowing is 1996-2004. An asterisk indicates that the whistleblower class in the post-Enron period has significantly different frequency in the overall distribution than the whistleblower class pre-Enron according to a univariate multinomial estimation as in Table 8.

Whistleblowers All End Pre-

Enron

End Post-

Enron

Internal Governance Firms 46 (26%) 29 (33%) 17 (18%)

Officers 3 (2%) 1 (1%) 2 (2%)

Board & New Mgmt 13 (7%) 6 (7%) 7 (8%)

Total Internal Governance 62 (35%) 36 (41%) 26 (28%)

Information Intermediaries Analysts & Rating Agencies 19 (11%) 10 (11%) 9 (10%)

Newspapers 20 (11%) 9 (10%) 11 (12%)

Total Info. Intermediaries 39 (22%) 19 (21%) 20 (22%)

Stakeholders Banks 1 (1%) 1 (1%) --

Clients 4 (2%) 3 (3%) 1 (1%)

Competitors 1 (1%) 1 (1%) --

Employees 23 (13%) 11 (13%) 12 (13%)

Equity Holders 3 (2%) 1 (1%) 2 (2%)

Suppliers 2 (1%) -- 2 (2%)

Total Stakeholders 34 (19%) 17 (20%) 17 (18%)

Regulators & Self-Reg Org Federal Investigators 5 (3%) 2 (2%) 3 (3%)

Industry Regulators 14 (8%) 8 (9%) 6 (7%)

SEC 4 (2%) -- 4 (4%)

Trade Organizations 2 (1%) -- 2 (2%)

Total Regulators 25 (14%) 10 (11%) 15 (16%)

Reputation Intermediaries Auditors 17 (9%) 4 (5%) 13 (14%)

Law Firms 2 (1%) 1 (1%) 1 (1%)

Investment Bankers -- -- --

Total Reputation Intermed 19 (11%) 5 (6%) 14 (15%)*

Grand Total 179 87 92

Chi-Square statistic for equivalence of pre-Enron and post-Enron distributions with 5 d.f. = 6.994 with p-vale of 0.221

33

Table 5: Triggering Factors Distribution Triggering factors are defined as the situation or event that forces the whistleblower to discover or act on information concerning the firm impropriety. The table shows the distribution of primary trigger factors before and after the date when the Enron scandal was revealed. The Enron scandal revelation date is defined to be the day that shareholders filed a suit against Enron, namely, October 18, 2001. An asterisk indicates that the whistleblower class in the post-Enron period has significantly different frequency in the overall distribution than the whistleblower class pre-Enron.

Triggering Factors All End Pre-Enron End Post-Enron

Change in auditing or control 12 (7%) 6 (7%) 6 (7%)

Completion of financing event 12 (7%) 7 (8%) 5 (5%)

Earnings announcement, routine procedures & compliance

29 (16%) 15 (17%) 14 (15%)

Financial distress 10 (6%) 7 (8%) 3 (3%)

Negative operations shock 28 (16%) 18 (21%) 10 (11%)

Outside scrutiny: investigations, due diligence & news worthiness

28 (16%) 13 (15%) 15 (16%)

Restructuring, executive turnover & disputes 23 (13%) 9 (10%) 14 (15%)

Scandal fallout 13 (7%) -- 13 (14%)*

Timing announcements to unrelated shocks 14 (8%) 6 (7%) 8 (9%)

Unknown 10 (6%) 6 (7%) 4 (4%)

Grand Total 179 87 92

Chi-Square statistic for equivalence of pre-Enron and post-Enron distributions with 9 d.f. = 18.64 with p-vale of 0.028

34

Table 6: Fraud Durations (days) by Whistleblower The duration of fraudulent activity is the number of days during the class period over which the civil class action alleges firm improprieties for the sample of cases 1996-2004. The Table averages the durations over the whistleblower categories, where the number of observations per category are given in Table 2, broken down to before and after the date when the Enron scandal was revealed. The Enron scandal revelation date is defined to be the day that shareholders filed a suit against Enron, namely, October 18, 2001. Whistleblowers are those entities which are the first forcing mechanisms in bringing corporate fraud to light. P-values in the last column result from tests for equivalence of sample mean of duration for frauds brought to light before the Enron data and those afterwards.

Whistleblower All End Pre-

Enron

End Post-

Enron

p-values

(pre v post)

Internal Governance Firms 407 299 590 0.01

Officers 522 922 323 n/a

Board & New Mgmt 693 405 939 0.06

Total Internal Governance 472 334 663 0.00

Information Intermediaries Analysts & Rating Agencies 395 241 566 0.07

Newspapers 624 380 825 0.40

Total Info Intermediaries 513 306 708 0.00

Stakeholders Banks 344 344 -- n/a

Clients 417 383 519 n/a

Competitors 599 599 -- n/a

Employees 767 651 874 0.32

Equity Holders 746 426 906 n/a

Suppliers 478 -- 478 n/a

Total Stakeholders 690 569 810 0.14

Regulators & Self-Regulatory Org. Federal Investigators 829 244 1,219 0.01

Industry Regulators 458 373 570 0.28

SEC 715 -- 715 n/a

Trade Organizations 1,048 -- 1,048 n/a

Total Regulators 620 347 802 0.01

Reputation Intermediaries Auditors 844 326 1,003 0.07

Law Firms 704 351 1,056 n/a

Total Reputation Intermed. 829 331 1,007 0.03

Total Average 581 376 775 0.00

35

Table 7: Fraud Settlements by Whistleblower The settlement average amounts are settlements reported in Stanford or in Factiva newswires searches in which the total settlement, not just the net of insurance payments, is given. The Table averages the settlements over the whistleblower categories for the sample of cases 1996-2004, where the number of observations per category is given in Table 2, broken down to before and after the date when the Enron scandal was revealed. The Enron scandal revelation date is defined to be the day that shareholders filed a suit against Enron, namely, October 18, 2001. Whistleblowers are those entities which are the first forcing mechanisms in bringing corporate fraud to light. P-values in the last column result from tests for equivalence of sample mean of duration for frauds brought to light before the Enron data and those afterwards.

Whistleblower All End Pre-

Enron

End Post-

Enron

p-values

(pre v post)

Internal Governance Firms 81,557,031 75,830,556 112,480,000 0.55

Officers 104,475,000 200,000,000 8,950,000 n/a

Board & New Mgmt 166,257,143 213,760,000 47,500,000 0.45

Total Internal

Governance 97,135,976 100,491,667 83,293,750 0.77

Information Intermediaries

Analysts & Rating Agencies 66,170,000 50,212,500 130,000,000 0.36

Newspapers 286,083,333 108,493,750 641,262,500 0.21

Total Info

Intermediaries 186,122,727 79,353,125 470,841,667 0.11

Stakeholders Banks 2,500,000 2,500,000 -- n/a

Clients 37,800,000 12,000,000 63,600,000 n/a

Competitors 5,250,000 5,250,000 -- n/a

Employees 248,491,667 340,986,111 109,750,000 0.56

Equity Holders 26,950,000 26,950,000 -- n/a

Suppliers -- -- -- n/a

Total Stakeholders 191,883,750 239,659,615 103,157,143 0.65

Regulators & Self-Regulatory Org. Federal Investigators 70,000,000 70,000,000 -- n/a

Industry Regulators 52,463,636 39,766,667 67,700,000 0.46

SEC 9,250,000 -- 9,250,000 n/a

Trade Organizations 89,900,000 -- 89,900,000 n/a

Total Regulators 47,796,875 44,085,714 50,683,333 0.81

Reputation Intermediaries Auditors 165,464,286 256,487,500 44,100,000 0.48

Law Firms 27,087,500 50,000,000 4,175,000 n/a

Total Reputation

Intermed. 134,713,889 215,190,000 34,118,750 0.42

Total Average 122,783,784 141,356,618 128,630,787 0.81

36

Table 8: Estimates of Whistleblower Specialization and Effect of Enron The estimates are from a multinomial logistic regression in which dependent variable is the category of whistleblower. The excluded whistleblower category is internal governance. All of the independent variables below are indicators. The impropriety categories from Table 1 are collapsed into three – (i) illegal activities and non-compliance, (ii) misrepresentation on financial statements, and (iii) failure to disclose or misrepresenting events, with the last one excluded as the offset. The Post-Enron date is defined to be the day that shareholders filed a suit against Enron, namely, October 18, 2001. Standard errors are in parentheses, and ***, **, and ** denote significance at the 1%, 5%, and 10% levels respectively.

Dependent Variable: Category of Whistleblower

Offset Whistleblower Category = Internal Governance

Offset Impropriety Category = Failure to Disclose or Misrepresenting Events

Estimation = Multinomial Logistic

Constant -0.464** -0.639** -0.539 -0.645 Information Intermediaries (0.204) (0.284) (0.476) (0.490)

Illegal Activities & Non-Compliance 1.232 1.207 (1.314) (1.315)

0.048 -0.059

Misrepresentation on Financial Statements (0.529) (0.542)

Post Enron 0.377 0.408 (0.411) (0.412)

Stakeholders Constant -0.601*** -0.750** -0.693 -0.839 (0.213) (0.294) (0.500) (0.519)

Illegal Activities & Non-Compliance 2.890** 2.856**

(1.167) (1.169)

-0.254 -0.397

Misrepresentation on Financial Statements (0.568) (0.584)

Post Enron 0.325 0.536 (0.429) (0.459)

Regulators Constant -0.908*** -1.281*** -0.539 -0.923*

(0.237) (0.357) (0.476) (0.526)

Illegal Activities & Non-Compliance 2.618** 2.539**

(1.162) (1.172)

-1.050** -1.357**

Misrepresentation on Financial Statements (0.589) (0.620)

Post Enron 0.731 1.136**

(0.483) (0.533)

Constant -1.183*** -1.974*** -19.35 -19.82*** Reputation Intermediaries (0.262) (0.477) (0.303)

a (0.542)

a

Illegal Activities & Non-Compliance 20.96 20.82***

(1.137)a (1.157)

a

18.098 17.68***

Misrepresentation on Financial Statements (0.000)

a (0.000)a

Post Enron 1.355** 1.397**

(0.581) (0.611)