Presented by: Life Insurance Planning in a Low Interest Rate Environment Grantor-Retained Annuity...

39

NOT INSURED BY FDIC OR ANY FEDERAL GOVERNMENT AGENCY M AY LOSE VALUE NOT A DEPOSIT OF OR GUARANTEED BY ANY BANK OR ANY BANK AFFILIATE FDIC BANK NOT INSURED BY FDIC OR ANY FEDERAL GOVERNMENT AGENCY M AY LOSE VALUE NOT A DEPOSIT OF OR GUARANTEED BY ANY BANK OR ANY BANK AFFILIATE FDIC BANK INSURANCE PRODUCTS: Presented by: Life Insurance Planning in a Low Interest Rate Environment Grantor-Retained Annuity Trust 0259907-00001-00 Ed. 04/2014 Exp.10/07/2015

-

Upload

collin-flowers -

Category

Documents

-

view

215 -

download

0

Transcript of Presented by: Life Insurance Planning in a Low Interest Rate Environment Grantor-Retained Annuity...

NOT INSURED BY FDIC OR ANYFEDERAL GOVERNMENT AGENCY

MAY LOSEVALUE

NOT A DEPOSIT OF OR GUARANTEEDBY ANY BANK OR ANY BANK AFFILIATE

FDIC BANK

INSURANCE PRODUCTS:

NOT INSURED BY FDIC OR ANYFEDERAL GOVERNMENT AGENCY

MAY LOSEVALUE

NOT A DEPOSIT OF OR GUARANTEEDBY ANY BANK OR ANY BANK AFFILIATE

FDIC BANK

INSURANCE PRODUCTS:

Presented by:

Life Insurance Planning in a Low Interest Rate Environment

Grantor-Retained Annuity Trust

0259907-00001-00 Ed. 04/2014 Exp.10/07/2015

Introduction

• Why are interest rates so low?• What may cause rates to rise?• How can low rates help with HNW planning?

• Economy is in recovery mode

• Low interest rates => households, businesses spend, invest more

• More spending, investing => employment growth, rising GDP

Why low interest rates?

The Recovery Cycle – At a Glance

Low Fed Rates

Low Lending Rates

Spending, Investment

Employment, GDP

Consumer, Investor

ConfidenceRecovery

New Demand for Goods, Services

• The Good: Increased consumer, investor demand for credit vs. limited lending capital

• The Bad: Rising inflation

• The Ugly: U.S. debt ratings downgrade

Why could rates rise?

Long-Term Growth – At a Glance

Fed Relaxes Target

Low Fed Rates

Low Lending Rates

Recovery: Sustained

Demand for Credit

Rising Treasury

Yields

Treasury yields determine the AFR (borrowing) and § 7520 (discounting) rates for individual taxpayers

Impact of Rising Treasury Yields

Treasury Yields

AFR § 7520

The Planning Benefits of Low Rates

• Lower interest rates make some wealth transfer strategies more efficient:

– Interest-only borrowing

– Sale of property where buyer has limited ability to pay

– Valuing a donor’s retained interest in property

9

Profile – Grantor Retained Annuity Trust

• Works in low rate environment because:– A low discount rate makes it easier for assets to achieve gains

that can be transferred to beneficiaries gift and estate tax-free

• For individual clients who… Own large income producing and/or highly

appreciated/appreciating assets Would like to pass future income and appreciation to the next

generation without making large gifts Have a current life insurance need

GRATs…Overview

• An Irrevocable Trust• Grantor Retains A Right To Payment of a

Fixed Amount from the trust for a Fixed Period Of Years

• At The End of the GRAT Period, The Remaining Value Passes to a Non-Charitable Beneficiary (such as a trust or a child)

• General Rule: A shorter term is more desirable than a longer term

GRATs….Overview

• Allow Large Transfers of Property With Little or No Gift Tax Cost WHY?

• Because of The Gift Formula: FMV Of Property Contributed – Value of Retained Interest = Taxable Gift

• Discount Rate Uses IRC §7520 Rate in effect when the GRAT is created

• Estate Tax Advantages

GRATs….Overview

• What Types of Property Are Suitable For A GRAT?– Virtually Any Type – Special Rules For Personal

Residences– High Yielding And/Or Expected to Appreciate

Substantially Are Ideal– FLPs: Even Better Gift Tax Leverage If FLP

Interests Are Transferred To A GRAT

The Sleeper GRAT

Question:• What if a client doesn’t have the right assets to fund a

GRAT today, but wants to lock in today’s low 7520 rate?

Answer:• The Sleeper GRAT:

– Locks in the right to value income at today’s rates, until a time when the GRAT strategy is truly appropriate

– “Stores” fixed income assets while returning 100% of their value to the grantor

History of 7520

The Sleeper GRAT

Question:• You said if the 7520 Rate goes up, that’s because Treasury

yields have risen. If that’s the case, won’t investment returns in general also go up, and be adequate to “clear” whatever discount hurdle is then in effect?

Answer:• Not for all clients. Those with long term fixed assets giving

income at today’s relatively modest rates won’t see their returns “float” with the interest rate tide.

• Locking in a rate today might benefit these clients by letting them participate in a low-discount GRAT strategy now, and buy them time to re-tool the rest of their portfolio should rates rise.

The Sleeper GRAT

• The concept: create and fund one or a series of GRATs today (say, 4, 6, 8, and 10 year terms), and fund them with fixed income assets

• The fixed income assets earn the same or slightly more than the hurdle rate – a.k.a. the 7520 rate

• The GRAT is therefore scheduled to return all of the grantor’s asset to him/her over the term, with a zero remainder, unless and until …

The Sleeper GRAT

• § 7520 rate rises significantly, OR• Short-term GRATs are eliminated due to tax law

changes, OR• Grantor acquires an asset that has higher appreciation

potential.

THEN:• One or more of the GRATs could be “switched on” by

swapping volatile assets of equal value (with high appreciation potential) into the GRAT

• Net effect: a short-term GRAT (remaining term) pegged at today’s 7520 rate

The Sleeper GRAT - Examples

– Assume the client has an asset worth $3,094,430 currently earning fixed interest at a rate of 2.2% per year

– The client is interested in the short-term GRAT idea with de minimus gifting consequences

– At the current 7520 rate of 2.2%*, is the client in a good position to fund a GRAT?

– The following slide should provide the answer ..

*March 2014

The Sleeper GRAT - Examples

Year Start Value2.2%

Annual Income

Annuity Balance

1 $3,094,430 $68,077 ($1,077,185 ) $2,085,322

2 $ 2,085,322 $45,877 ($1,077,185 ) $1,054,015

3 $ 1,054,015 $23,188 ($ 1,077,185) $17.84

Short-Term GRAT (Gift = $0)Uses 2.2% 7520 Discount Rate, 2.2% Annual Income from Assets

Switching on the Sleeper GRAT

To preserve the ability to have the three-year GRAT we just saw eight years from now, and use today’s rate of 2.2%:

Fund a 10-year sleeper GRAT now with the $3,094,430 asset, which would produce the values on the following slide.

Switching on the Sleeper GRAT

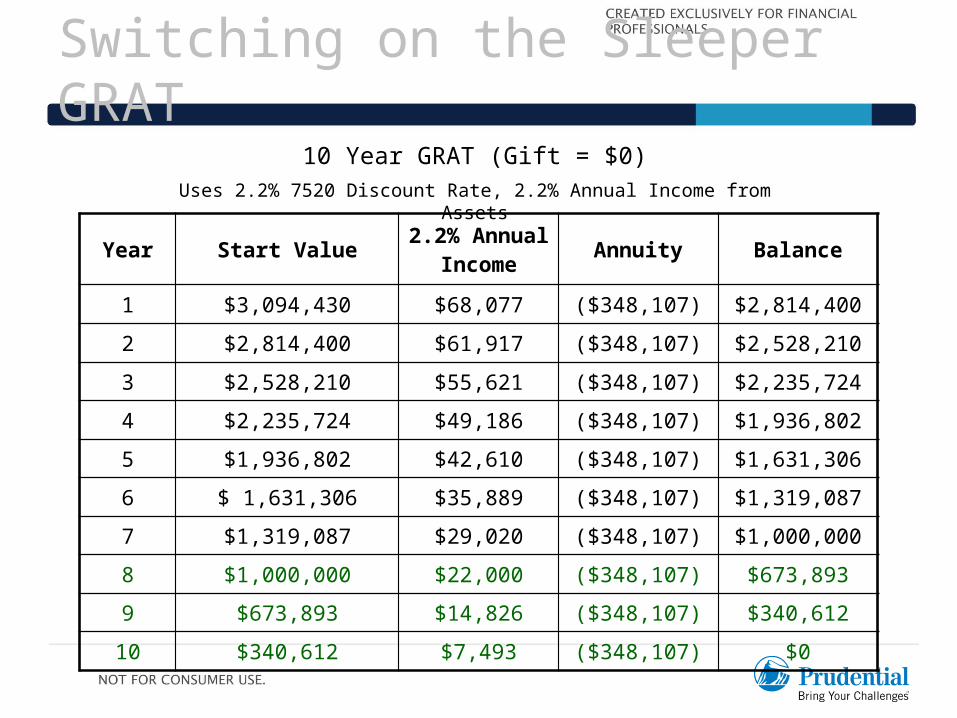

Year Start Value 2.2% Annual Income Annuity Balance

1 $3,094,430 $68,077 ($348,107) $2,814,400

2 $2,814,400 $61,917 ($348,107) $2,528,210

3 $2,528,210 $55,621 ($348,107) $2,235,724

4 $2,235,724 $49,186 ($348,107) $1,936,802

5 $1,936,802 $42,610 ($348,107) $1,631,306

6 $ 1,631,306 $35,889 ($348,107) $1,319,087

7 $1,319,087 $29,020 ($348,107) $1,000,000

8 $1,000,000 $22,000 ($348,107) $673,893

9 $673,893 $14,826 ($348,107) $340,612

10 $340,612 $7,493 ($348,107) $0

10 Year GRAT (Gift = $0)Uses 2.2% 7520 Discount Rate, 2.2% Annual Income from Assets

Switching on the Sleeper GRAT

Year Start Value Annual Income Annuity Balance

1 $3,094,430 $68,077 ($348,107) $2,814,400

2 $2,814,400 $61,917 ($348,107) $2,528,210

3 $2,528,210 $55,621 ($348,107) $2,235,724

4 $2,235,724 $49,186 ($348,107) $1,936,802

5 $1,936,802 $42,610 ($348,107) $1,631,306

6 $ 1,631,306 $35,889 ($348,107) $1,319,087

7 $1,319,087 $29,020 ($348,107) $1,000,000

8 $1,000,000 $200,000 ($348,107) $851,893

9 $851,893 $170,379 ($348,107) $674,165

10 $ 674,165 $134,833 ($348,107) $460,891

10 Year GRAT (Gift = $0)Uses 2.2% 7520 Discount Rate, 20% Annual Income Years 8-10

Why Life Insurance?

Why Life Insurance?– Counters risk of the client dying during the term of the GRAT– Provides estate liquidity – the GRAT only removes the appreciation

from the estate, not the original asset value, which is paid back via the annuity:• A GRAT is an estate freeze, not an estate reducer

– An ILIT can be the remainder beneficiary of a GRAT– Grantor can allocate GSTT exemption amounts to an ILIT, but not to

a GRAT

Large Case Sales Idea

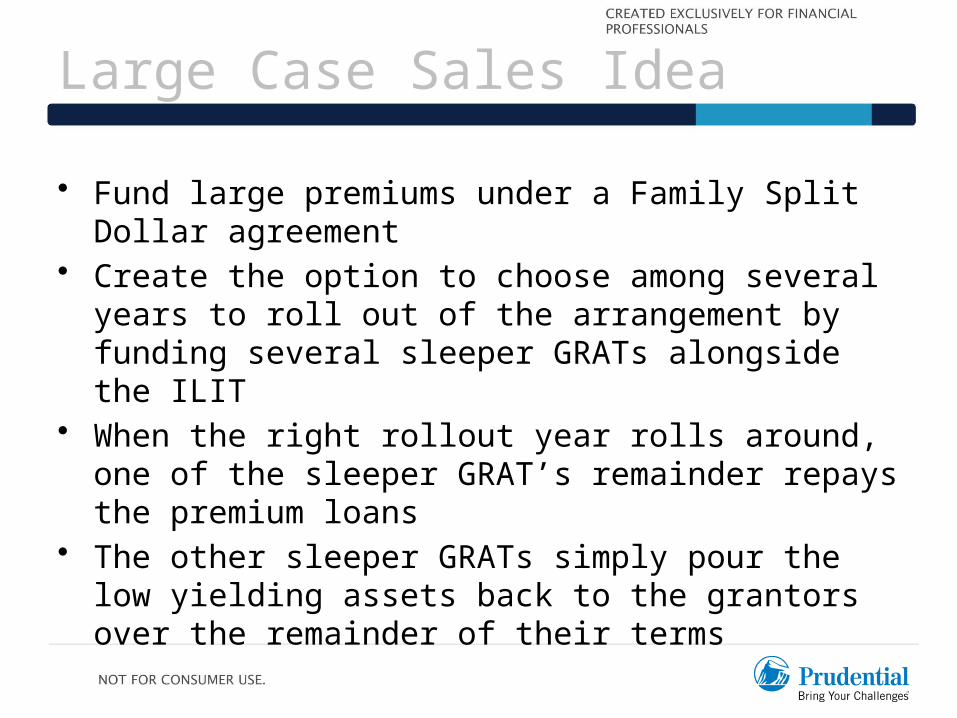

• Fund large premiums under a Family Split Dollar agreement

• Create the option to choose among several years to roll out of the arrangement by funding several sleeper GRATs alongside the ILIT

• When the right rollout year rolls around, one of the sleeper GRAT’s remainder repays the premium loans

• The other sleeper GRATs simply pour the low yielding assets back to the grantors over the remainder of their terms

Potential concerns:• Don’t want to make large gifts• Access to Policy Cash Values

Mr. and Mrs. Krepps

Hypothetical case facts:• Mr. and Mrs. Krepps, ages 45 and 44• Seven figure income and $30MM net worth• Need life insurance; interested in its role in

estate protection• Want to allocate $100,000 yearly over 10

years for premiums

This is a hypothetical example used for illustrative purposes only to describe how the strategies may work. Which strategy works best for clients will depend on their individual facts and circumstances. Actual results will vary. Any representation of life insurance premium or death benefit is purely hypothetical in amount and is not a guarantee of cost or death benefit now or in the future from a specific life insurance policy. Any assumptions for life insurance policy values on subsequent slides are based on a male age 45, Preferred Non-Tobacco underwriting class, and female, age 44 and Preferred Best underwriting class, PruLife SUL Protector, $108,750 annual premium for 10 years, $10,000,000 Level death benefit. The rates for the SUL are Current Assumptions.

Family Split Dollar Arrangement

• Need $10 Million of Life Insurance• 10 Pay Premium To Guarantee DB through

Mrs. Krepps’ Age 105 = $108,757

This hypothetical example is for illustrative purposes.Actual results will vary.

Sample Case

Family Split Dollar Arrangement with Sleeper GRAT

Beneficiaries (estate tax-free, if structured

properly)

Irrevocable Life Insurance Trust

Second-to-Die Cash Value Life

Insurance Policy

$5,000,000 GRAT funding

$108,757 annual premium loans

$562,474 annuity Payment

Collateral assignment (ILIT)

Loan interest payment (ILIT)

Access to trust values by spouse, if necessary

Death benefit proceeds distributed on the second death

Mrs. Krepps

1

2

3

4

1

2

4

3

Mr. Krepps(sole grantor of ILIT)

Mrs. Krepps(co-grantor of GRAT)

10 Year Sleeper GRAT (and other

GRATs with different terms)

Fixed Income Assets

ILIT is Remainder Beneficiary

1

2

2

Sample Case

After 7 Years

Mr. Krepps(sole grantor of ILIT)

Mrs. Krepps(co-grantor of GRAT)

1

2

10 Year GRAT

High Yield Assets

ILIT is Remainder Beneficiary

1

2

$1,615,807 high yielding assets

$1,615,807 Fixed Income Assets

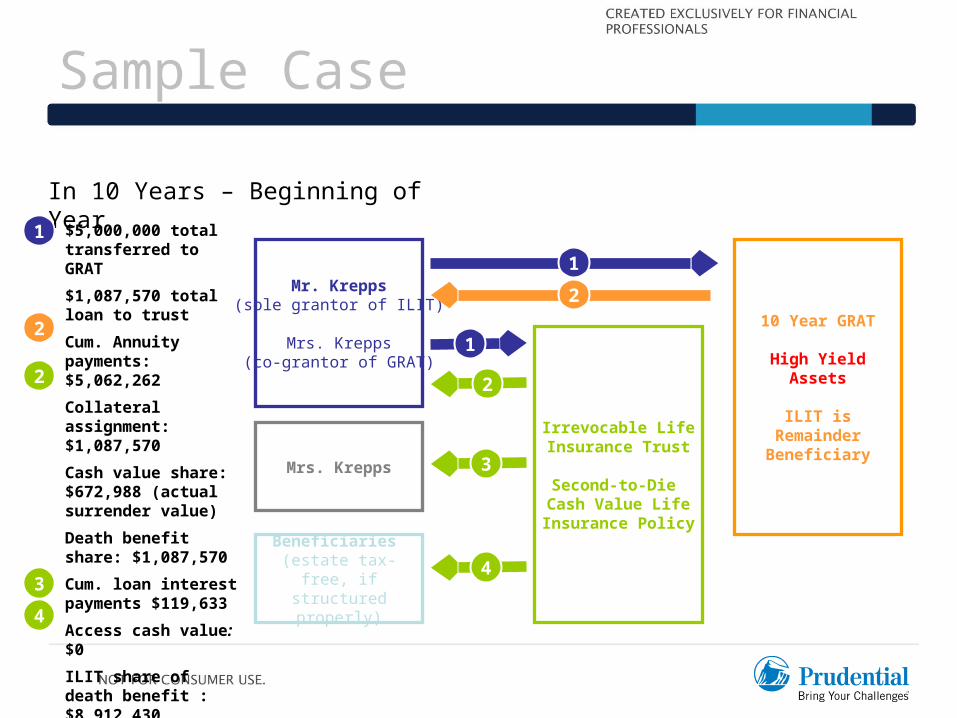

$5,000,000 total transferred to GRAT

$1,087,570 total loan to trust

Cum. Annuity payments: $5,062,262

Collateral assignment: $1,087,570

Cash value share: $672,988 (actual surrender value)

Death benefit share: $1,087,570

Cum. loan interest payments $119,633

Access cash value: $0

ILIT share of death benefit : $8,912,430

Sample Case

In 10 Years – Beginning of Year

Mr. Krepps(sole grantor of ILIT)

Mrs. Krepps(co-grantor of GRAT)

Beneficiaries (estate tax-free, if structured

properly)

Irrevocable Life Insurance Trust

Second-to-Die Cash Value Life

Insurance Policy

Mrs. Krepps

1

2

3

4

1

2

4

3

10 Year GRAT

High Yield Assets

ILIT is Remainder Beneficiary

1

2

2

Final annuity payment of $562,474

$1,098,027 GRAT remainder paid to ILIT

$1,087,570 loan paid back to Mr. Krepps

Cash value available to access, if necessary: $776,365

ILIT share of future death benefit proceeds: $10,000,000

Sample Case

In 10 Years – End of Year

Mr. Krepps(sole grantor of ILIT)

Mrs. Krepps(co-grantor of GRAT)

Beneficiaries (estate tax-free, if structured

properly)

Irrevocable Life Insurance Trust

Second-to-Die Cash Value Life

Insurance Policy

$10,457 Unspent GRAT Remainder

Mrs. Krepps

2

3

4

2

4

3

10 Year GRAT

Terminated, No Remaining Assets

2

1

12

Results

• Clients receive back value equal to all of their GRAT transfers, plus time value of money

• Clients had 10 years to re-tool non-GRAT investments, get higher returns

• Favorable investment returns channeled to benefit the next generation with no transfer tax

• Premium loans are paid back to the clients

• Excess remainder value stays in ILIT to benefit heirs

Benefits

Getting Started

Talking Points• Do you know some of the benefits that low interest rates

could provide for your wealth transfer planning?

• Are you aware of the factors that may bring the economy out of this low interest rate environment?

• “We don’t want to give up control of our assets.”

• If you could find ways to minimize the loss of control over your assets, would you be interested in knowing more?

• Let me share an idea with you…

NOT FOR CONSUMER USE32

Next Steps• Individual meeting

• Identify prospects

• Build and present case

Clients Who May Benefit High Net Worth ($10MM+) and family

oriented

Are concerned about the impact of transfer taxes on their financial legacy

Have sufficient income from other sources, besides the assets used in the strategies

NOT FOR CONSUMER USE33

• Enter the advanced planning club.

• Help clients to take action now.

• Preserve and/or increase assets under management (AUM).

• Support and Resources

What’s In It For You?

NOT FOR CONSUMER USE34

Summary

Why This Strategy, Why Now• Taking advantage of low interest rates using the strategy described

here can help to enhance wealth for heirs.

Why Life Insurance• Life insurance is essential in managing the risks inherent in the

strategy, and may also further enhance the amount of wealth going to heirs.

Getting Started• Implementing the strategy using simple talking points and our

resources

NOT FOR CONSUMER USE35

Important ConsiderationsBefore implementing this strategy• Clients should consider developing a comprehensive financial plan to take into account

current and future income and expenses in conjunction with implementing any of the strategies discussed here.

• We recommend that clients consult their tax and legal advisors to discuss their situation before implementing any strategy discussed here.

About this concept• This concept is only suited to high net worth clients who do not rely on the assets for living

expenses for the expected lifetime of the insured(s). It is the client’s responsibility to estimate these needs and expenses and it is recommended that they consider developing a comprehensive financial plan in conjunction with implementing the strategy being considered. The accuracy of determining future needs and expenses is more critical for clients at older ages who have less opportunity to replace assets used for the strategy.

If your client’s financial or legacy planning situation changes• If clients need to use the assets or income in the strategies for current or future income

needs and they can no longer make premium payments, the life insurance death benefit may terminate and the results illustrated may not be achieved.

36

Important ConsiderationsTax and other financial implications• There may be tax and other financial implications as a result of liquidating assets within an

investment portfolio. If contemplating such a strategy, it is important for clients to understand that life insurance is a long-term strategy to meeting particular needs.

About life insurance• The death benefit protection offered by a life insurance policy can be a key component of

a sound financial plan. It is important for clients to fully understand the terms and conditions of any financial product before purchasing it.

Other notes• Clients should consider that life insurance policies contain fees and expenses, including

cost of insurance, administrative fees, premium loads, surrender charges, and other charges or fees that will impact policy values.

• If premiums and/or performance are insufficient over time, the policy could lapse, which would require additional out-of-pocket premiums to keep it in force.

37

Important InformationThis material has been prepared by The Prudential Insurance Company of America to assist financial professionals. It is designed to provide general information in regard to the subject matter covered. It should be used with the understanding that we are not rendering legal, accounting or tax advice. Such services should be provided by the client’s own advisors. Accordingly, any information in this document cannot be used by any taxpayer for purposes of avoiding penalties under the Internal Revenue Code.

PruLife® SUL Protector is issued by Pruco Life Insurance Company, except in New York where, it is issued by Pruco Life Insurance Company of New Jersey. Both are Prudential Financial companies located in Newark, NJ. [Each is solely responsible for its own financial condition and contractual obligations.

NOT FOR CONSUMER USE38

Thank You