Presentation3 Investor Meetings - Alicorp · Presentation3 Disclaimer (Forward looking statements)...

28

[CLIENT NAME] Presentation3 Investor Meetings August 2013

Transcript of Presentation3 Investor Meetings - Alicorp · Presentation3 Disclaimer (Forward looking statements)...

[ C L I E N T N AM E ]

Presentation3

Investor Meetings

August 2013

[ C L I E N T N AM E ]

Presentation3

Disclaimer (Forward looking statements)

This presentation may contain forward‐looking statements concerning recent acquisitions, its financial and

business impact, management’s beliefs and objectives with respect thereto, and management’s current

expectations for future operating and financial performance, based on assumptions currently believed to be valid.

Forward‐looking statements are all statements other than statements of historical facts. The words “anticipates,”

“may,” “can,” “plans,” “believes,” “estimates,” “expects,” “projects,” “intends,” “likely,” “will,” “should,” “to be,”

and any similar expressions or other words of similar meaning are intended to identify those assertions as forward‐

looking statements. It is uncertain whether the events anticipated will transpire, or if they do occur what impact

they will have on the results of operations and financial condition of Alicorp or of the consolidated company.

Alicorp does not undertake any obligation to update the forward‐looking statements included in this presentation

to reflect subsequent events or circumstances.

1

[ C L I E N T N AM E ]

Business Overview

2

[ C L I E N T N AM E ]

Presentation3

Extensive and unique distribution network throughout Peru

Best‐in‐class product portfolio with significant brand recognition and strong market share penetration

Business Overview

Leading consumer branded products company in Peru and South America

Exposure to highly attractive markets with solid macro and industry fundamentals

Experienced management team

1

2

3

4

7

Diversified product portfolio participating across all relevant consumer segments and socioeconomic levels5

3

Successful track record of organic and inorganic growth allowing consistent cash flow generation and profitability6

[ C L I E N T N AM E ]

Presentation3

Consumer goods61%

B2B Branded Products29%

Animal nutrition

9%

Consumer goods59%

B2B Branded Products27%

Animal nutrition14%

Ownership Structure

Grupo Romero45.3%

Pension Funds29.8%

Inv. & Mutual Funds12.2%

Other12.7%

Alicorp is a leading consumer branded products company in Peru and South America…

Business overview

Consumer Goods B2B Branded

Products Animal Nutrition

Overview

Food, home and personal care products

Industrial flour for bakeries, and food‐based products for restaurants

Shrimp and fish feed

Main brands

# of Brands1 120 Brands 31 Brands

2 Brands

Presence

EcuadorColombiaPeru

ChileColombiaArgentina

Ecuador

Peru

Peru

Guatemala

Strong growth track record (US$mm)

Diversified Revenue and EBITDA base (US$mm – 2Q131)

Revenues: US$1,958.4mm EBITDA: US$243mm

1

4

Brazil

900

1,253 1,233 1,326 1,547

1,700 1,805 1,958

101 104 163 192 200 213 217 243

11.2%

8.3%

13.2% 14.5%

12.9% 12.5% 12.0% 12.4%

2007 2008 2009 2010 2011 2012 1Q13 2Q13

Revenue EBITDA EBITDA Margin

Source: Cavali as of June 30, 2012

Chile

Panama CR Venezuela

1 LTM

Revenue CAGR 2007-2012: 13.6%

EBITDA CAGR 2007-2012: 16.1%

11

[ C L I E N T N AM E ]

Presentation3

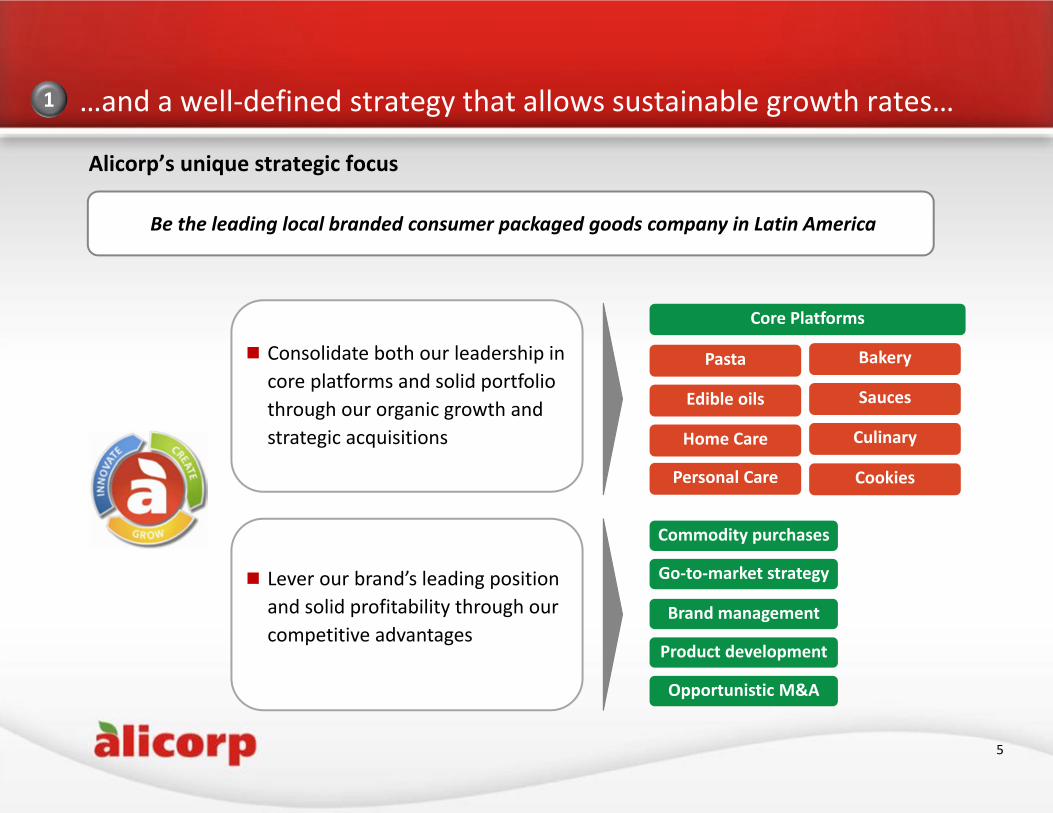

…and a well‐defined strategy that allows sustainable growth rates…1

5

Alicorp’s unique strategic focus

Pasta

Edible oils

Home Care

Bakery

Sauces

Culinary

Personal Care

Core Platforms

Be the leading local branded consumer packaged goods company in Latin America

Consolidate both our leadership in core platforms and solid portfolio through our organic growth and strategic acquisitions

Lever our brand’s leading position and solid profitability through our competitive advantages

Commodity purchases

Go‐to‐market strategy

Brand management

Opportunistic M&A

Product development

Cookies

[ C L I E N T N AM E ]

Presentation3

Peru82%

Argentina5%

Ecuador5%

Chile4%

Brazil4%

Peru69%Argentina

11%

Ecuador6%

Chile6%

Brazil4% Others

4%

Peru100%

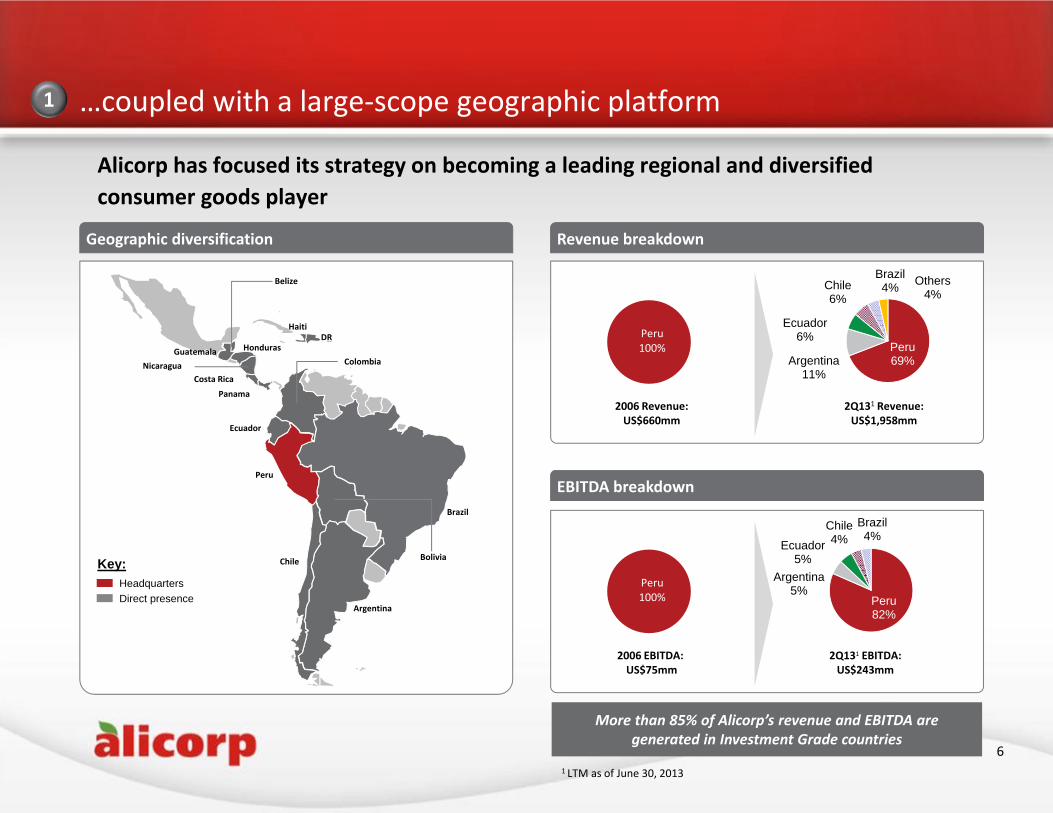

…coupled with a large‐scope geographic platform

Alicorp has focused its strategy on becoming a leading regional and diversified consumer goods player

Geographic diversification Revenue breakdown

EBITDA breakdown

Bolivia

Argentina

Chile

Haiti

Ecuador

ColombiaGuatemala Honduras

Nicaragua

Peru

DR

Panama

Belize

Costa Rica

Brazil

2006 Revenue:US$660mm

Peru100%

2006 EBITDA: US$75mm

1

More than 85% of Alicorp’s revenue and EBITDA are generated in Investment Grade countries

6

Key:HeadquartersDirect presence

2Q131 Revenue:US$1,958mm

2Q131 EBITDA:US$243mm

1 LTM as of June 30, 2013

[ C L I E N T N AM E ]

Presentation3

5.9%5.2% 4.8% 4.3%

3.9%3.3% 2.6%

Peru Chile Brazil Latin America Mexico US Euro Zone

Consumer food products

46%

B2B branded products39%

Home & personal care products13%

Animal nutrition products

3%

…and compelling industry dynamics2

Peruvian consumer industry is poised to benefit from a booming economy with ample room for growth

2012 consumer basket structure favors Alicorp product mix

Alicorp product mix

Ample room for consumer expenditure growth

Strong upside potential of consumer expenditure current levels

Consumer expenditure per capita LatAm 2012 (US$)

4,0596,491 6,519 6,862

8,960 10,254

Peru Argentina Mexico Brazil Chile Uruguay

Sustained personal disposable income growth

’12E‐'15E expected average growth of GDP per capita (PPP adjusted)

Sources: US Census Bureau, EIU, International Monetary Fund

7

31%

13%

11%7%

10%

5%11%

5%8%

Peru consumer basket

Food at homeFood away from homeOther goods and servicesHealthEducationClothing and footwearRent, fuel and electricityFurnitureTransport and communication

Alicorp’s products reach

Average = 7,190

Revenues in Peru as of 2Q13

US$ 348.9mm

[ C L I E N T N AM E ]

Presentation3

Category Brands Market share Position % of sales2 % of EBITDA2 Competitors

Industrial Baking Flour3 53% #1 12.6% 13.9%

Pasta5 50% #1 7.2% 13.3%

Laundry Detergents5 55% #1 7.7% 10.8%

Edible Oils5 57% #1 10.5% 8.1%

Mayonnaise5 96% #1 2.9% 6.7%

Cookies & Crackers 3 45% #1 5.1% 5.3%

Margarines5 63% #1 1.9% 4.0%

Shrimp feed 70% #1 1.6% 1.9%

Juice Powders4, 5 66% #1 1.6% 2.8%

Alicorp is the leading consumer goods company, competing with global and local players, such as Procter & Gamble, Unilever, Kraft, Nestle, Carozzi, among others

Best‐in‐class diversified product portfolio with unmatched brand leadership in Peru…3

8

Ranked #1 in over 9 product categories1

51% 67%Source: Kantar World Panel¹ Market share Sales and EBITDA participation as of December 20122 Based on consolidated LTM sales and EBITDA as of March 31, 2013 3 Internal estimates4 Value share as of December 20125 Market share as of JF’13

[ C L I E N T N AM E ]

Presentation3…through a strategy that focuses on effective market and customer segmentation reaching all socioeconomic levels …3

Source: IPSOS Apoyo1 Includes industrial baking flour and household flour2 Includes laundry detergents and laundry soap

Prem

ium

Mainstream

Value

9

Market and customer segmentation allows a more efficient pricing process and pass‐through of commodities price increasesProduct classification

Edible Oils Pasta Home care2 Cookies & CrackersFlour1

[ C L I E N T N AM E ]

Presentation3

Category Brands Market share Position % of sales3 Competitors

Argentina

Hair Care 27% #2 3.8%

Personal Care Soap 18% #2 2.1%

Laundry Detergents 6% #3 2.4%

Cookies & Crackers 3% #7 1.1%

Pasta 2% #11 0.8%

Ecuador

Shrimp feed 32% #2 5.0%

Pet Food4 23% #2 0.1%

Mayonnaise4 14% #2 0.1%

Pasta5 13% #3 0.5%

Hair Care 3% #6 0.1%

Juice Powders 5% #4 0.0%

Colombia

Cookies & Crackers5 2% #7 0.3%

…with increasing relevance and brand recognition in the rest of the countries…3

10

One of the largest consumer goods products companies in Latin America1,2

16%

Source: Kantar World Panel¹ Market share as of December 20112 Financial information as of December 20123 Based on consolidated sales4 Market share as of June 20125 Market share as of April 2013

Alicorp’s business model has proven to be successfully replicable in other countries

[ C L I E N T N AM E ]

Presentation3

34.2% 40.1% 46.9% 53.4% 54.6%

88.1% 79.3% 81.3% 74.6%75.6%

2008 2009 2010 2011 2012

54.6% 53.2% 56.7% 51.0% 54.9%

43.9% 46.0% 45.2% 46.2% 44.7%

2008 2009 2010 2011 2012

Pasta

Personal home & care products

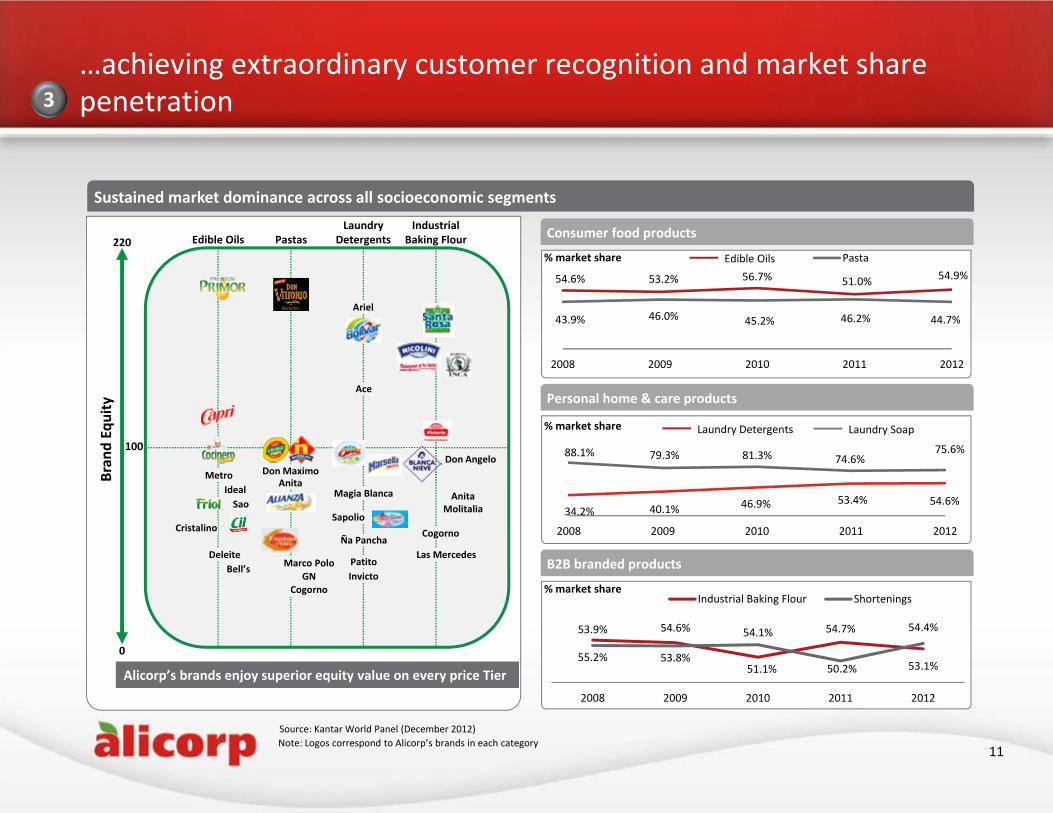

…achieving extraordinary customer recognition and market share penetration3

Sustained market dominance across all socioeconomic segments

% market share

% market share

% market share

Consumer food products

B2B branded products

11Note: Logos correspond to Alicorp’s brands in each categorySource: Kantar World Panel (December 2012)

Edible Oils

55.2%

54.6%

51.1%

54.7%

53.1%

53.9%

53.8%

54.1%

50.2%

54.4%

2008 2009 2010 2011 2012

Industrial Baking Flour Shortenings

Laundry Detergents Laundry Soap

Alicorp’s brands enjoy superior equity value on every price Tier

Bran

d Equity

Edible Oils PastasLaundry

DetergentsIndustrial

Baking Flour220

0

100

Ideal Metro

Cristalino

Sao

Bell’sDeleite

Don MaximoAnita

Ariel

Ace

Magia Blanca

Sapolio

Ña Pancha

PatitoInvicto

Las Mercedes

Cogorno

Don Angelo

AnitaMolitalia

Marco PoloGN

Cogorno

[ C L I E N T N AM E ]

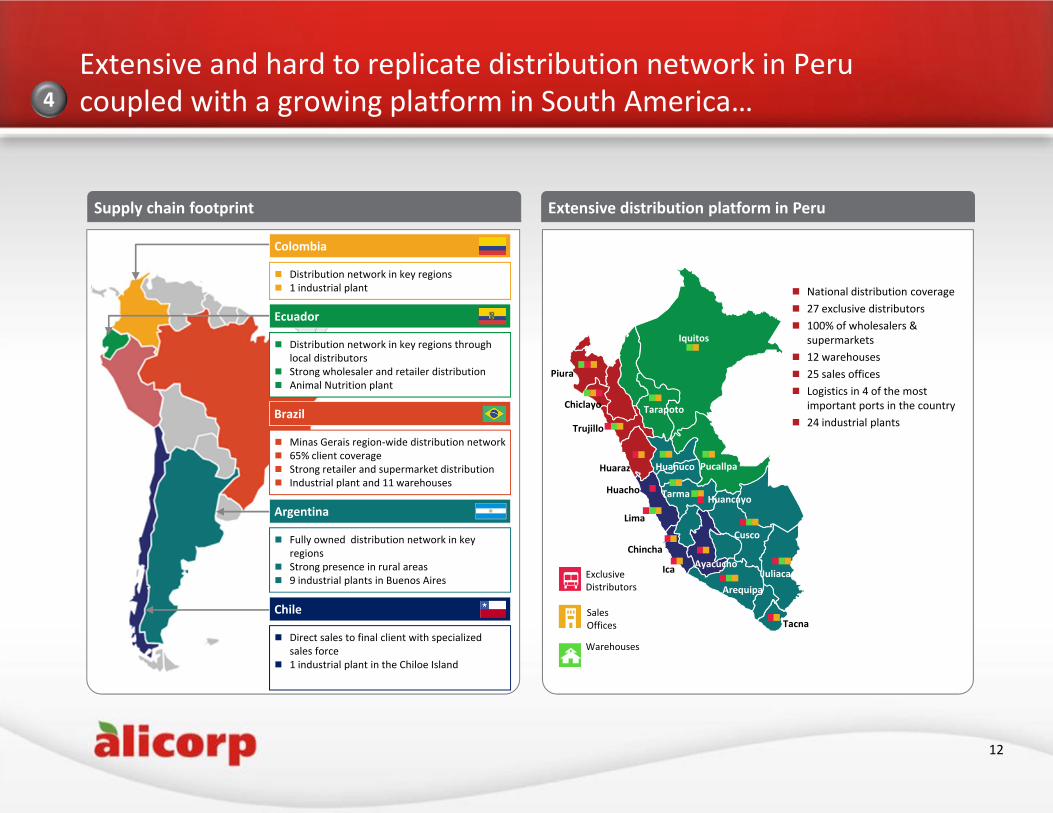

Presentation3Extensive and hard to replicate distribution network in Peru coupled with a growing platform in South America…

Extensive distribution platform in Peru

ExclusiveDistributors

Warehouses

SalesOffices

Iquitos

Piura

Chiclayo Tarapoto

Huanuco

Tarma Huancayo

Lima

Ica Ayacucho

Cusco

ArequipaJuliaca

Tacna

Pucallpa

Trujillo

Huaraz

Chincha

Huacho

4

National distribution coverage 27 exclusive distributors 100% of wholesalers &

supermarkets 12 warehouses 25 sales offices Logistics in 4 of the most

important ports in the country 24 industrial plants

12

Supply chain footprint

Brazil

Minas Gerais region‐wide distribution network 65% client coverage Strong retailer and supermarket distribution Industrial plant and 11 warehouses

Colombia

Distribution network in key regions 1 industrial plant

Ecuador

Distribution network in key regions through local distributors

Strong wholesaler and retailer distribution Animal Nutrition plant

Argentina

Fully owned distribution network in key regions

Strong presence in rural areas 9 industrial plants in Buenos Aires

Chile

Direct sales to final client with specialized sales force

1 industrial plant in the Chiloe Island

[ C L I E N T N AM E ]

Presentation3

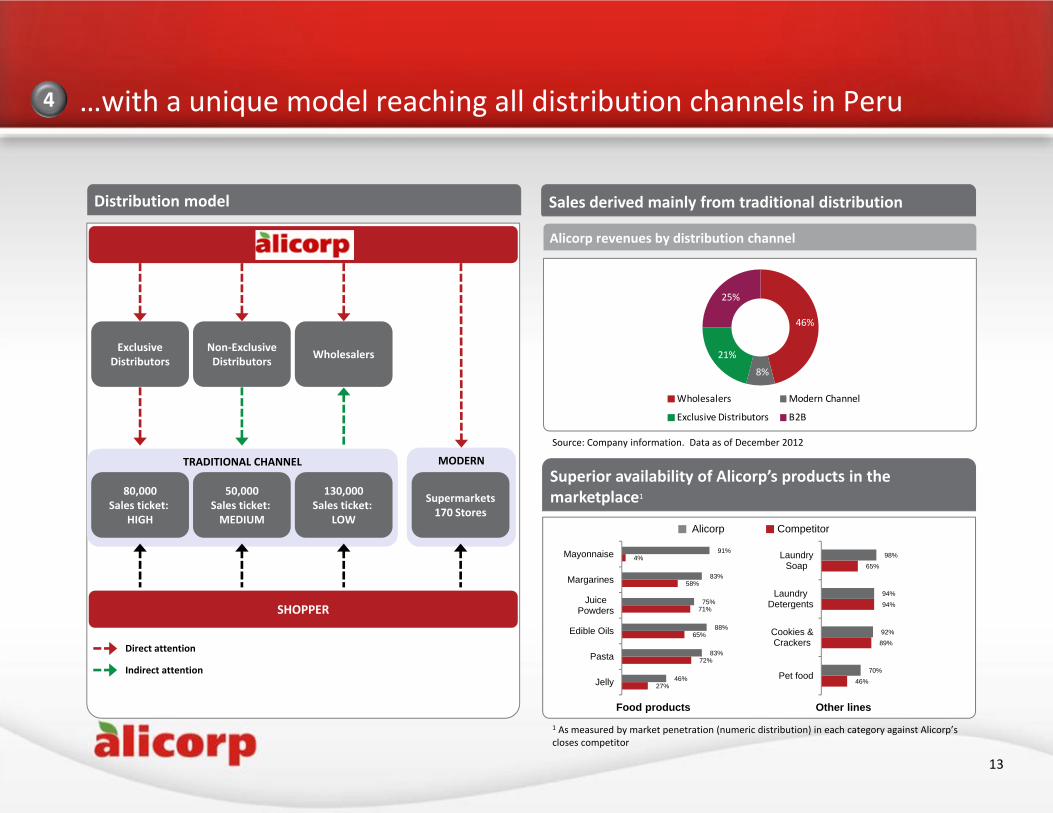

…with a unique model reaching all distribution channels in Peru

Distribution model Barriers of entry

MODERN TRADITIONAL CHANNEL

ALICORP

SHOPPER

80,000Sales ticket:

HIGH

50,000Sales ticket: MEDIUM

130,000Sales ticket:

LOW

Supermarkets170 Stores

Exclusive Distributors

Non‐ExclusiveDistributors Wholesalers

Direct attention

Indirect attention

Alicorp revenues by distribution channel

Sales derived mainly from traditional distribution

Superior availability of Alicorp’s products in the marketplace1

46%

8%

21%

25%

Wholesalers Modern Channel

Exclusive Distributors B2B

4

13

27%

72%

65%

71%

58%

4%

46%

83%

88%

75%

83%

91%

Jelly

Pasta

Edible Oils

JuicePowders

Margarines

Mayonnaise

Food products Other lines

46%

89%

94%

65%

70%

92%

94%

98%

Pet food

Cookies &Crackers

LaundryDetergents

LaundrySoap

Alicorp Competitor

1 As measured by market penetration (numeric distribution) in each category against Alicorp’scloses competitor

Source: Company information. Data as of December 2012

[ C L I E N T N AM E ]

Presentation3

Peru

International

Food Products

Home & Personal

Care ProductsConsumer Goods

B2B branded products

Animal Nutrition

Food Products

Home & Personal

Care Products

Consumer Goods

B2B branded products

Animal Nutrition

15%14%

9% 9% 8%6% 5% 5% 4%

Flou

r

Pasta

Anim

alNutrition

Detergen

ts

Edible Oils

Sauces

Cookies &

Crackers

Hair C

are

Margarin

es

2Q131 revenue breakdown by business line

Diversified product portfolio participating in all relevant categories and tiers…5

Well‐diversified across 3 business lines

2Q131 EBITDA breakdown by business line

65%

73%27%

63%28%

9%

65%59%

14%

Product mix breakdown by revenue

Increase in product diversification

Ranking by contribution to 2Q131 EBITDA

EBITDA diversification

54% 38% 39% 40%

31%30% 28% 27%

9%21% 20% 19%

6% 11% 13% 14%

2007 2012 1Q13 2Q13

Consumer Food Products B2B branded productsHome & Personal Care Products Animal Nutrition

Source: Company information

27%

32%

68%

14

2

1 LTM 2 Includes industrial baking flour and household flour

1

Peru

International83%

17%

Consumer GoodsConsumer Goods

69%

31%

1

[ C L I E N T N AM E ]

Presentation3

17% 16% 16%

12%

6%5% 5% 4% 3%

Pasta

Eddible Oils

Laun

dry

Detergen

ts

Cookies &

Crackers

Hair C

are

Sauces

Laun

dry

Soap

Beauty Soap

Margarin

es

22%

14%12%

10%8% 8% 6% 5%

Pasta

Laun

dry

Detergen

ts

Edible Oils

Sauces

Cookies &

Crackers

Hair C

are

Margarin

es

Househ

old

Flou

r

45%

26%

11%7%

4% 2%

IndustrialBaking Flour

Edible Oils Shortenings NutritionalInputs

Food ServiceSauces

Margarines

44%

29%

14%9%

6%2%

IndustrialBaking Flour

Edible Oils Shortenings Food ServiceSauces

Margarines FattyDerivatives

Consumer goods ranked by 2Q131 revenue (% of line revenues)

…with additional diversification within product categories5

Substantial & diverse consumer goods products portfolio

Consumer goods products ranked by 2Q131 EBITDA (% of line EBITDA)

B2B branded products ranked by 2Q131 revenue (% of line revenues) B2B branded products ranked by 2Q131 EBITDA (% of line EBITDA)

Diversified B2B branded products portfolio

Source: Company information

15

1 LTM as of June 30, 2013

[ C L I E N T N AM E ]

Presentation3

Selected products launched in 2Q13

Alicorp has a strong and successful track record of organic and inorganic expansion…6

Successful new product launch strategy, with over 25% of 2012 revenues generated from products launched since 2006

Growth through Mergers & Acquisitions

2318

15

20

12

25

6 7

2007 2008 2009 2010 2011 2012 1Q13 2Q13

International AcquisitionsDomestic Acquisitions

20122004 2005 2006 2007 2008 2010 2011

Since 2006, Alicorp’s growth comes 25% from Acquisitions, 75% from organic growth

16

Growth focused on core and next‐to‐core platforms

Food products & Personal and Home Care

B2B Branded Products

# of products

2013

[ C L I E N T N AM E ]

Presentation3

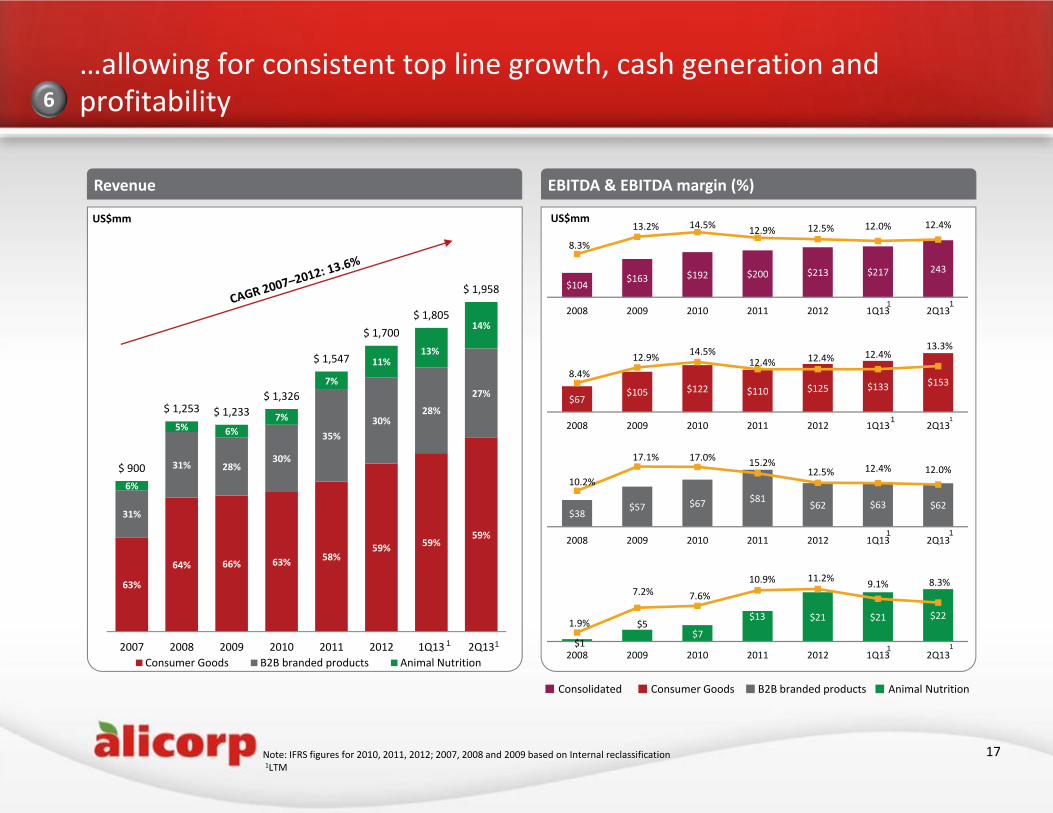

63%

64% 66% 63% 58%59% 59%

59%

31%

31% 28%30%

35%30%

28%

27%

6%

5% 6%7%

7%

11%13%

14%

$ 900

$ 1,253 $ 1,233$ 1,326

$ 1,547

$ 1,700$ 1,805

$ 1,958

2007 2008 2009 2010 2011 2012 1Q13 2Q13Consumer Goods B2B branded products Animal Nutrition

…allowing for consistent top line growth, cash generation and profitability 6

Revenue EBITDA & EBITDA margin (%)

Note: IFRS figures for 2010, 2011, 2012; 2007, 2008 and 2009 based on Internal reclassification1LTM

$104 $163 $192 $200 $213 $217 243

8.3%

13.2% 14.5% 12.9% 12.5% 12.0% 12.4%

2008 2009 2010 2011 2012 1Q13 2Q13

Consumer Goods B2B branded products Animal NutritionConsolidated

US$mmUS$mm

$67 $105 $122 $110 $125 $133 $153

8.4%12.9% 14.5%

12.4% 12.4% 12.4%13.3%

2008 2009 2010 2011 2012 1Q13 2Q13

$38 $57 $67 $81

$62 $63 $62

10.2%

17.1% 17.0% 15.2%12.5% 12.4% 12.0%

2008 2009 2010 2011 2012 1Q13 2Q13

$1

$5 $7

$13 $21 $21 $22 1.9%

7.2% 7.6%

10.9% 11.2% 9.1% 8.3%

2008 2009 2010 2011 2012 1Q13 2Q13

17

1

1

1

11

1

1

1

11

[ C L I E N T N AM E ]

Presentation3Alicorp operations are conducted by an experienced management team

Alicorp’s management team has accomplished consistent and outstanding results

7

18

Paolo SacchiChief Executive Officer

Renato FalboInternational Consumer Goods

Martin CarrionAnimal Nutrition

Hugo CarrilloB2B Branded Products

Mario RossiConsumer Goods Marketing

Business Units Business Partners

Former Manager Director – Senior Consultant of Prisma Consultores (Peru)

Former Corporate Director , Ajegroup(Mexico)

Carnegie‐Mellon University, Pittsburgh, Pennsylvania, USA ‐ Master of Science

BSc. Civil Engineering, UNI (Peru)

Manager Animal Nutrition, AlicorpManager Calixto Romero, AlicorpMore than 25 years in food and animal nutrition products

BSC. Busines Administration, Universidad de Piura (Peru)

Consumer Goods Marketing VP, AlicorpMarketing Manager, AlicorpMBA, Universidad del Pacifico (Peru) BSC in Industrial Engineering, UNI (Peru)

Former CEO, The Value Brands Company (Argentina)

Former CEO, The Dial Corp (Argentina) Former Commercial Manager, Molinos Rio dela Plata (Argentina)

BSC. Business Administration, Universidad Argentina de la Empresa

Diego RosadoChief Financial Officer

Corporate Financial Director, Alicorp Corporate Development and FP&A, Amazon.com (Seattle) Former Investment Banker at JP Morgan (Lima, New York)MBA, Stephen M. Ross School of Business (Michigan) BSC in Economics, Universidad del Pacifico (Peru)

Anthony MiddlebrookHuman Resources

Marketing Manager, Alicorp Former Advertising Services Associate Director, P&G (Lima, Sao Paulo)MBA, ESAN (Peru) BSC in Industrial Engineering, Universidad de Lima (Peru)

Jaime ButrichSupply Chain Management

Manufacturing Manager, Alicorp Logistics and Planning Manager, Alicorp Former Commercial Manager, La Fabril (Peru)MBA, Universidad de Piura (Peru) BSC in Industrial Engineering, UNI (Peru)

CFO, Alicorp Industrial Products VP, Alicorp Flour Business Manager, Alicorp Business Planning, SCM and IT Manager, Alicorp Former banker at Banca Comerciale‐Mergers & Acquisitions (Madrid, Milan, Barcelona) BSC in Finance, University of Adelphi (New York)

[ C L I E N T N AM E ]

Finance Overview

19

[ C L I E N T N AM E ]

Presentation3

Finance Overview

20

Historical Performance8

Acquisition growth has been conservatively financed9

Diversified Capital Structure10

Risk diversification11

[ C L I E N T N AM E ]

Presentation3

Historical performance indicators

Revenue Volume

EBITDA and EBITDA margin (%) Normalized EBITDA margin (%) – comparison2

13%

8%10%

12% 13%

15%US$mm, %

$900

$1,253 $1,233 $1,330 $1,547

$1,700 $1,805

$1,958

2007 2008 2009 2010 2011 2012 1Q13 2Q13

$101 $104 $163 $192 $200 $213 $217 $243

11.3%

8.3%

13.2%14.5%

12.9% 12.5% 12.0% 12.4%

2007 2008 2009 2010 2011 2012 1Q13 2Q13

967 1,047

1,142 1,202 1,223

1,303 1,359

1,462

2007 2008 2009 2010 2011 2012 1Q13 2Q13

Note: Revenues and EBITDA for 07‐09 are IFRS estimations. 2010 and after under IFRS. CAGRs and growth rates were calculated in US dollars

US$mm ’000 TM

21

CAGR (’07-’12): 16.1% %

1

1

1 LTM 2 EBITA Margin as of Dec 2012

1

8

1 1

1

[ C L I E N T N AM E ]

Presentation3

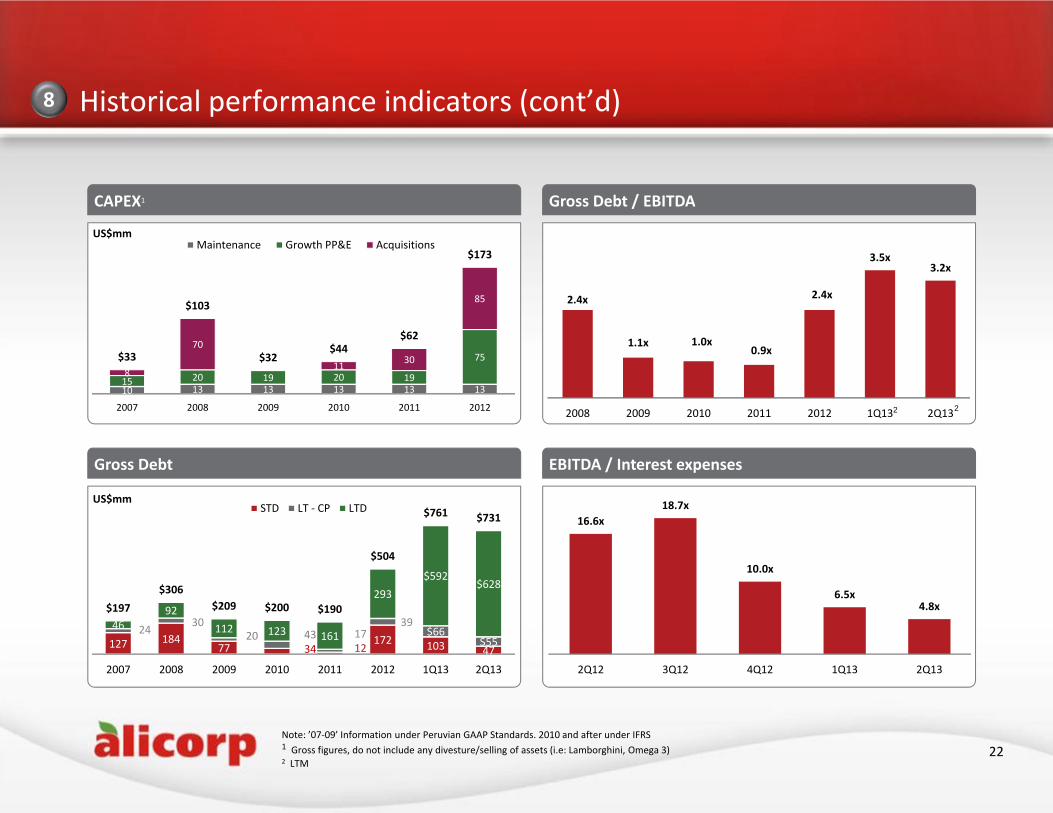

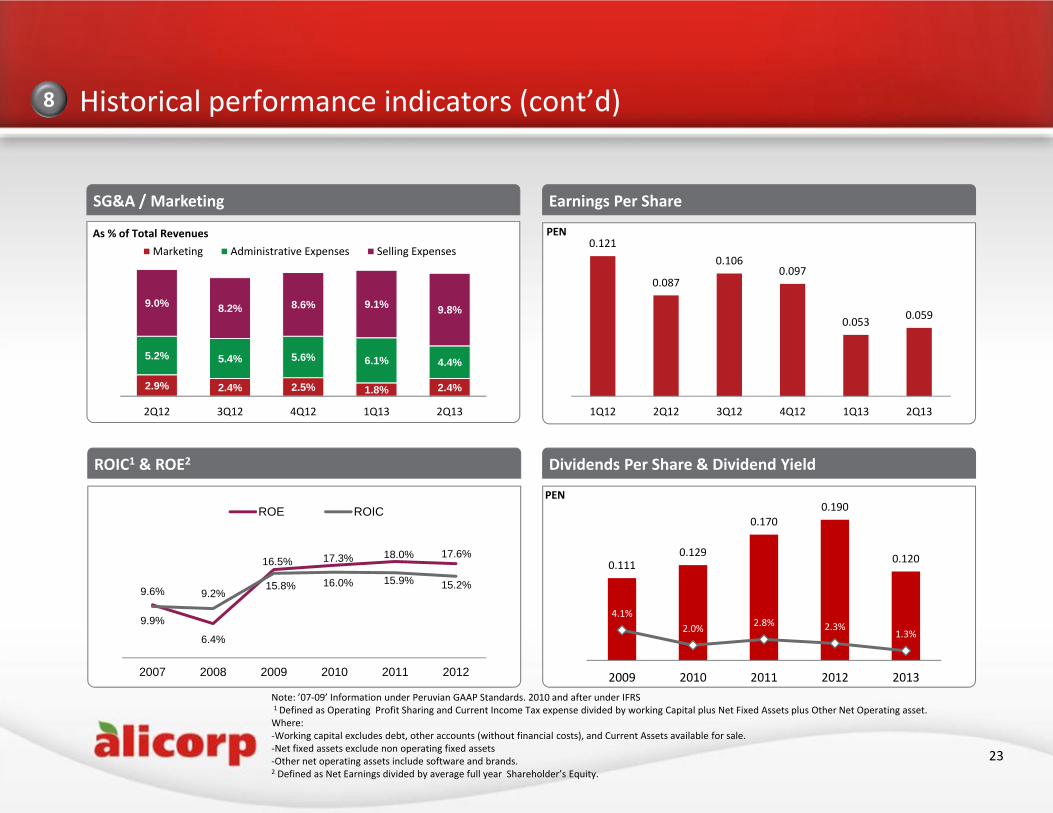

Historical performance indicators (cont’d)

CAPEX1

Gross Debt

10 13 13 13 13 1315 20 19 20 19

758

70

11 30

85

$33

$103

$32$44

$62

$173

2007 2008 2009 2010 2011 2012

Maintenance Growth PP&E Acquisitions

Note: ’07‐09’ Information under Peruvian GAAP Standards. 2010 and after under IFRS1 Gross figures, do not include any divesture/selling of assets (i.e: Lamborghini, Omega 3) 2 LTM

US$mm

127 184 77 34 12

172 103 47

24 3020 43 17

39$66

$55 46

92112 123 161

293$592

$628

$197 $306

$209 $200 $190

$504

$761 $731

2007 2008 2009 2010 2011 2012 1Q13 2Q13

STD LT ‐ CP LTDUS$mm

22

Gross Debt / EBITDA

EBITDA / Interest expenses

16.6x18.7x

10.0x

6.5x4.8x

2Q12 3Q12 4Q12 1Q13 2Q13

8

2.4x

1.1x 1.0x0.9x

2.4x

3.5x3.2x

2008 2009 2010 2011 2012 1Q13 2Q132 2

[ C L I E N T N AM E ]

Presentation3

Historical performance indicators (cont’d)

SG&A / Marketing

ROIC1 & ROE2

Note: ’07‐09’ Information under Peruvian GAAP Standards. 2010 and after under IFRS1 Defined as Operating Profit Sharing and Current Income Tax expense divided by working Capital plus Net Fixed Assets plus Other Net Operating asset.Where:‐Working capital excludes debt, other accounts (without financial costs), and Current Assets available for sale.‐Net fixed assets exclude non operating fixed assets‐Other net operating assets include software and brands.2 Defined as Net Earnings divided by average full year Shareholder’s Equity.

As % of Total Revenues

23

Earnings Per Share

Dividends Per Share & Dividend Yield

PEN

PEN

9.9%

6.4%

16.5% 17.3% 18.0% 17.6%

9.6% 9.2%15.8% 16.0% 15.9% 15.2%

2007 2008 2009 2010 2011 2012

ROE ROIC

8

2.9% 2.4% 2.5% 1.8% 2.4%

5.2% 5.4% 5.6% 6.1% 4.4%

9.0% 8.2% 8.6% 9.1% 9.8%

2Q12 3Q12 4Q12 1Q13 2Q13

Marketing Administrative Expenses Selling Expenses0.121

0.087

0.1060.097

0.053 0.059

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

0.1110.129

0.1700.190

0.120

4.1%2.0% 2.8% 2.3%

1.3%

2009 2010 2011 2012 2013

[ C L I E N T N AM E ]

Presentation3

Kallpa SAB Peru 9.75 Neutral Aug. 13BCP Peru 10.15 Maintain May.13

Scotia Capital Peru 10.90 Buy July. 13

Inteligo SAB Peru 10.35 Buy Aug. 13

BTG Pactual USA 9.90 Neutral May. 13

BBVA Peru 7.15 Neutral May. 12

Larrain Vial Peru 8.40 Sell Aug. 13

HSBC USA 9.60 Neutral July. 13

Historical performance indicators (cont’d)

Stock Price

Coverage

1 As of June 30, 2013 24

Common Stock

PEN

Valuation

2010 2011 2012 2013

Common shares Outs. (MM)Stock Price 1

Investment Shares Out. (MM) Stock Price 1

Market Capitalization

Net Debt 1 (MM)

Firm Value

847US$3.33

7US$2.19

US$676

US$2,841

US$3,517

Firm Country Target Price(PEN)

Recommendation Date EPS : S/. 0.3140P/E : 29.55414Dividend Yield 1 : 1.29%

Benchmark

ALICORC1 : 419%ALICORI1 : 385%IGBVL : 199%

January 2009 = 100

8

3.41 3.70

5.75 5.725.40 5.33

5.936.54 6.75 7.00

8.20 8.309.90

9.351

2.403.25

4.12 4.15 3.90 3.90 3.70 3.87 4.35 4.15 4.30

6.13 6.101

J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J

ALICORC1 ALICORI1

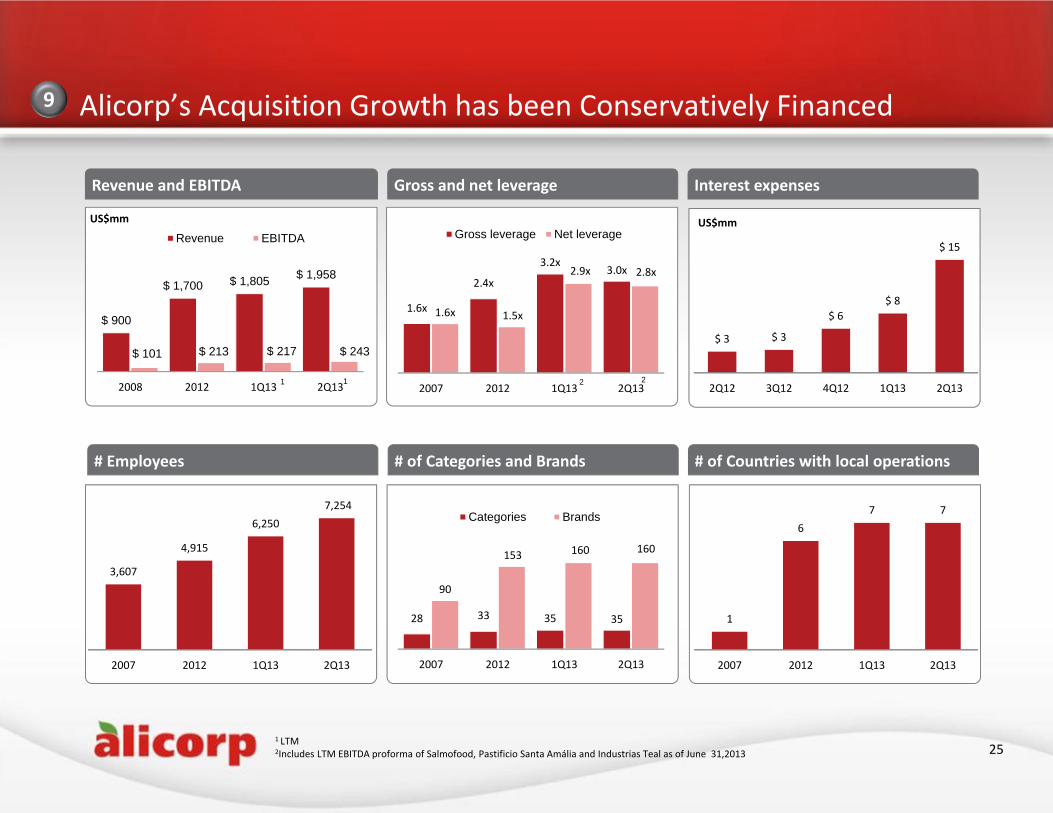

[ C L I E N T N AM E ]

Presentation3

28 33 35 35

90

153 160 160

2007 2012 1Q13 2Q13

Categories Brands

Alicorp’s Acquisition Growth has been Conservatively Financed 9

Revenue and EBITDA

$ 3 $ 3

$ 6$ 8

$ 15

2Q12 3Q12 4Q12 1Q13 2Q13

Gross and net leverage Interest expenses

# Employees

1

67 7

2007 2012 1Q13 2Q13

# of Categories and Brands # of Countries with local operations

25

$ 900

$ 1,700 $ 1,805 $ 1,958

$ 101 $ 213 $ 217 $ 243

2008 2012 1Q13 2Q13

Revenue EBITDA

1 LTM2Includes LTM EBITDA proforma of Salmofood, Pastificio Santa Amália and Industrias Teal as of June 31,2013

1.6x

2.4x

3.2x3.0x

1.6x 1.5x

2.9x 2.8x

2007 2012 1Q13 2Q13

Gross leverage Net leverage

3,607

4,915

6,2507,254

2007 2012 1Q13 2Q13

US$mm US$mm

21 21

[ C L I E N T N AM E ]

Presentation3

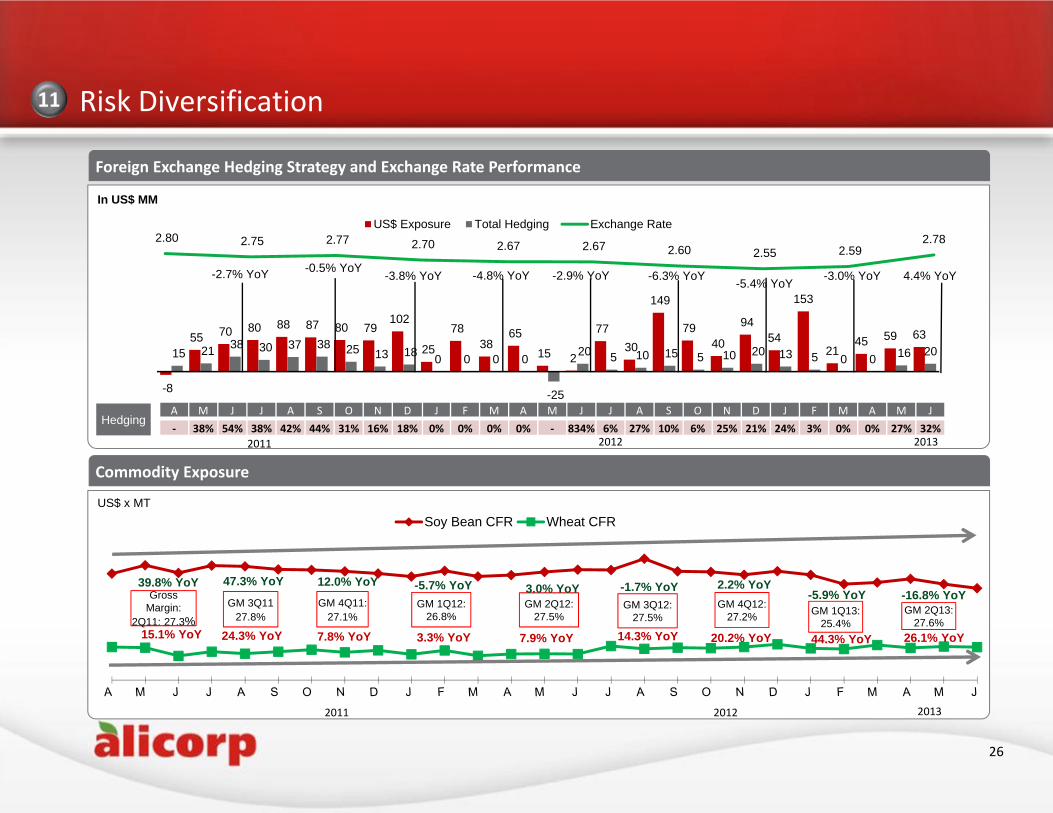

2.80 2.75 2.77 2.70 2.67 2.67 2.60 2.55 2.59 2.78

Exchange Rate

-8

55 70 80 88 87 80 79 102

25

78 38

65

15 2

77 30

149

79 40

94 54

153

2145 59 63

15 21 38 30 37 38 25 13 18 0 0 0 0

-25

20 5 10 15 5 10 20 13 5 0 0 16 20

US$ Exposure Total Hedging

Soy Bean CFR Wheat CFR

15.1% YoY 24.3% YoY 7.8% YoY

39.8% YoY 47.3% YoY 12.0% YoYGross

Margin:2Q11: 27.3%

GM 3Q1127.8%

GM 4Q11:27.1%

GM 1Q12: 26.8%

3.3% YoY

-5.7% YoYGM 2Q12:

27.5%GM 3Q12:

27.5%

3.0% YoY

7.9% YoY

GM 4Q12: 27.2%

-1.7% YoY

14.3% YoY

2.2% YoY

GM 1Q13: 25.4%

20.2% YoY

-5.9% YoY

44.3% YoY

-16.8% YoY

26.1% YoY

Risk Diversification

Foreign Exchange Hedging Strategy and Exchange Rate Performance

26

Commodity Exposure

In US$ MM

A M J J A S O N D J F M A M J J A S O N D J F M A M J‐ 38% 54% 38% 42% 44% 31% 16% 18% 0% 0% 0% 0% ‐ 834% 6% 27% 10% 6% 25% 21% 24% 3% 0% 0% 27% 32%

Hedging

US$ x MT

2011 2012

2011 2012 2013

2013

11

-2.7% YoY -0.5% YoY-3.8% YoY -4.8% YoY -2.9% YoY -6.3% YoY -5.4% YoY -3.0% YoY 4.4% YoY

GM 2Q13: 27.6%

[ C L I E N T N AM E ]

Presentation3

Capital Structure and Financial MetricsCapital Structure as of June 30, 2013

27

FINANCIAL METRICS 2009 2010 2011 2012 2008 – 2012 Growth %

2011-2012Growth % 1Q13 2Q13

Stock Price (S/.) 2.75 6.30 6.00 8.30 201.8% 38.3% 9.65 9.28

IGBVL 14,167 23,375 19,473 20,620 45.5% 5.9% 16,050 15,550

Market Cap (MM US$) 806 1,900 1,885 2,772 243.9% 46.2% 3,175 2,841

EBITDA Multiple 5.12 10.74 10.02 14.71 187.3% 66.2% 17.79 15.44

Daily average trading volume (US$) 344,405 479,522 725,103 569,665 65.4% -21.4% 732,304 987,016

Daily average trading volume 432,574 336,564 349,040 209,795 -51.5% -39.9% 224,239 278,397

P/E Ratio 10.66 18.92 15.50 20.94 96.4% 18.0% 23.26 29.55

ALICORC1 Performance

Grupo Romero45.3%

Pension Funds29.8%

Inv. & Mutual Funds12.2%

Others12.6%

10

![Looking back and looking forward[1]](https://static.fdocuments.net/doc/165x107/5559ad0dd8b42aa4288b511b/looking-back-and-looking-forward1.jpg)