Presentation to North East Dairy Leadership Team · Presentation to North East Dairy Leadership...

32

1 Presentation to North East Dairy Leadership Team 2 nd June 2009 Andrei Mikhalevsky | Managing Director Fonterra Ingredients Agenda Global marketplace Worldwide demand Trends and their impact What does this mean for dairy? Dairy in New Zealand and Fonterra Dairy in New Zealand and Fonterra Worldwide supply

Transcript of Presentation to North East Dairy Leadership Team · Presentation to North East Dairy Leadership...

1

Presentation toNorth East Dairy Leadership Team2nd June 2009

Andrei Mikhalevsky | Managing Director Fonterra Ingredients

Agenda

Global marketplace

Worldwide demand

Trends and their impact

What does this mean for dairy?

Dairy in New Zealand and FonterraDairy in New Zealand and Fonterra

Worldwide supply

2

Global marketplace

Summary & outlook

Our assessment of the macro environment outlook suggests we’re in for a difficult 12 months

C b i tt h h d b t l t d h tConsumer buying patterns have changed but clear trends have yet to emerge, making forecasting difficult

Dairy commodity demand recently picked up as lower price levels improved margins and opportunities emerged

This provided welcome relief and renewed confidence after a challenging period of extreme price volatility and a lowerchallenging period of extreme price volatility and a lower consumption response

The rate of global milk growth is slowing with the current oversupply onto the market, particularly within protected markets likely to slow further

3

Summary & outlook

Milk prices, with above average input costs will continue to constrain milk growth

The materiality and speed of supplier responses to cash pressures will be a key dynamic over the next 6 –12 months

Slower US & EU consumption growth for higher value fresh dairy and cheese means more SMP & Butter (& EU WMP), with SMP prices aligned near support levels

A b ild f bli t k d th t f iA build up of public stock dampens the prospect for price recovery

Politically driven protectionist responses have become a real threat to market stability

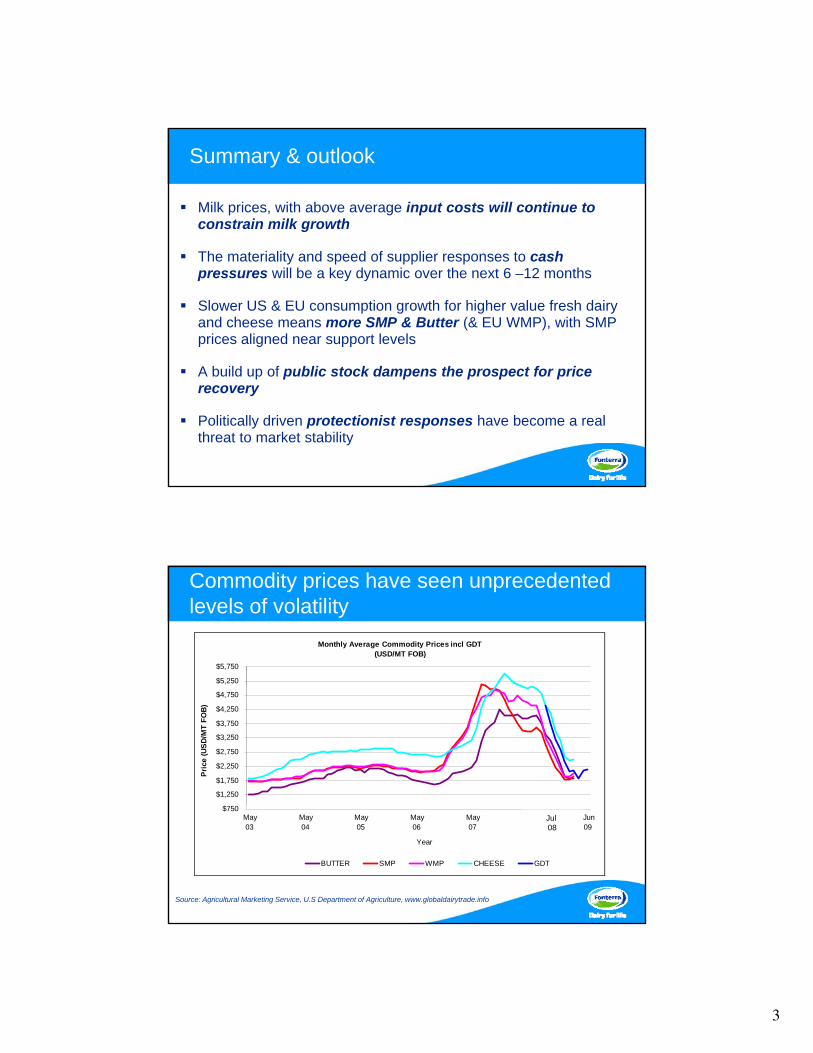

Commodity prices have seen unprecedented levels of volatility

Monthly Average Commodity Prices incl GDT(USD/MT FOB)

$5,250

$5,750

$1,250

$1,750

$2,250

$2,750

$3,250

$3,750

$4,250

$4,750

Pric

e (U

SD/M

T FO

B)

Source: Agricultural Marketing Service, U.S Department of Agriculture, www.globaldairytrade.info

$750 May

03 Nov03

May04

Nov04

May05

Nov05

May06

Nov06

May07

Nov07

Jul08

Dec08

Jun09

Year

BUTTER SMP WMP CHEESE GDT

Jul 08

4

Government intervention could cause more volatility for commodity prices over longer period

SMP Government Stocks

US & EU have US & EU have now reinstated now reinstated

Export SubsidiesExport Subsidies

The world has entered its deepest financial and business crisis in more than 60 years

World industrial production

Source:Eichengreen and O'Rourke

5

…and the world trade collapse is steepWorld trade

Source:Eichengreen and O'Rourke

Recent economic headlines have been mostly dismal

Japan’s economy shrank a record 15.2% in the first quarter of 2009

Russia's economy contracted 9.5% in the first quarter of 2009

Europe’s economy contracted at the fastest pace in at least 13 years during Q1 2009 as companies cut output and jobs to survive

UK GDP fell by 1.9% Q1 2009 vs Q4 2008, the steepest quarterly decline in 30 yearsdecline in 30 years

6

… but amongst the negative there are signs of improvementIMF report highlighted “acute lack of confidence” and world GDP declining -1.3% in 2009

In April the J P Morgan Global Manufacturing PMI was 41.8, the eleventh successive month reading below the neutral mark of 50

However, rising from 37.3 in March, the PMI posted its greatest month-on-month gain in the series history and reached a seven-month highmonth high

Ferocious de-stocking rates appear to be slowing

Recovery still seems some way off but the pace of global economic contraction is beginning to slow

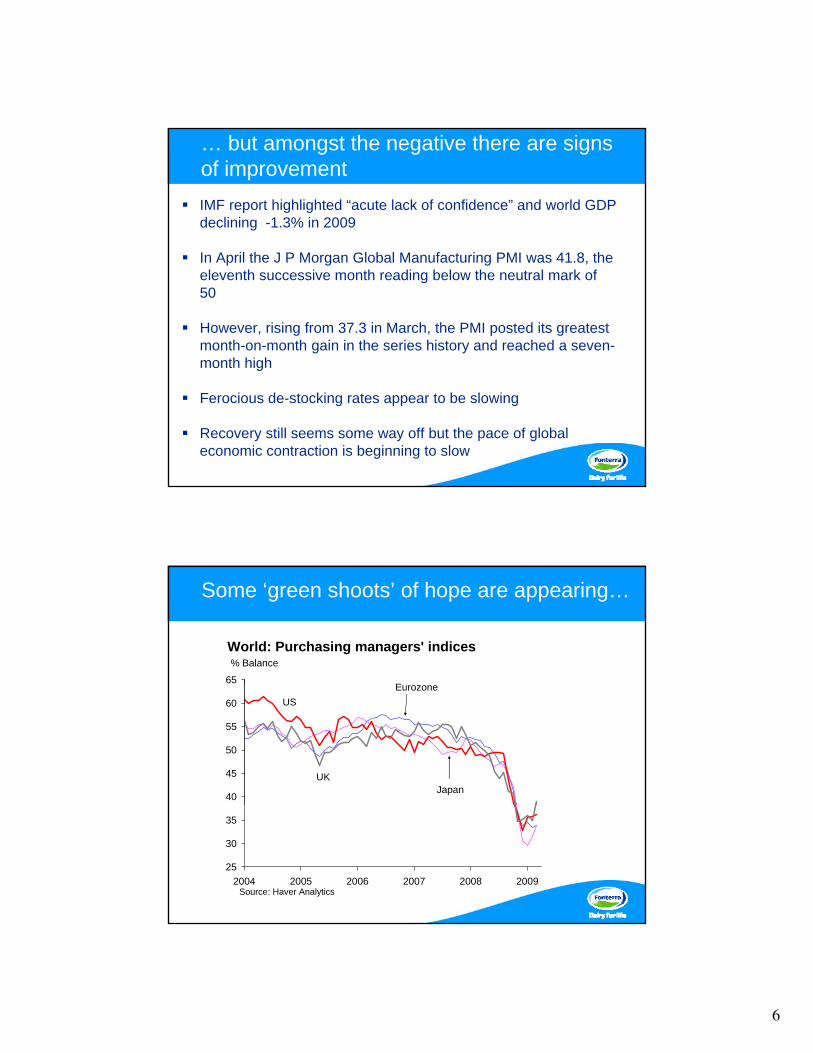

Some ‘green shoots’ of hope are appearing…

65E

World: Purchasing managers' indices% Balance

40

45

50

55

60Eurozone

Japan

US

UK

25

30

35

2004 2005 2006 2007 2008 2009Source: Haver Analytics

7

…especially in China

65

US & China: Manufacturing surveysIndices

45

50

55

60China manufacturing PMIExpansion

Contraction

30

35

40

2005 2006 2007 2008 2009Source : Oxford Economics/Haver Analytics

US manufacturing ISM

These factors result in an uncertain and dynamic marketplace for our products

Today’s world is a very uncertain world

Key uncertainties continue around:

– milk production reduction in response to lower farm gate milk price

– the levels of demand recovery as retailer promotional activity and lower commodity prices begin to reach consumers

The global economic recession and increased government interventions still leaves uncertainty over the market and its implications on the dairy supply and demand balance

8

Global milk growth continues at a lower rate

Even with the combined impact of sluggish consumption, low milk prices and weather, 2008 global milk growth was still

2 0%+2.0%

We estimate 2009 global milk growth to be 0.8%

We estimate 2010 global milk growth to be 1.0%

Key drivers of milk growth remain:

– Domestic policy settings

– Trade access

– Currency relativities

The US accounted for >60% of dairy commodity export growth from 2005 to 2008

Variance (t)2005 vs. 2008

-200

,000

-100

,000

0 100,00

0

200,00

0

300,00

0

400,00

0

500,00

0

EU27N Z l dNew ZealandUnited States

AustraliaArgentina

Other EuropeBrazil

Other AsiaRussia

UruguayMalaysiaThailand

ChiChinaChile

CanadaIndia

MexicoSouth Africa

IndonesiaROW

Other Europe principally Ukraine and Belarus. Malaysia involves significant re-export.

9

Worldwide demand

Cheese consumption underpins the global dairy engine

Over the past decade, cheese has underpinned dairy consumption growth in Europe and USA

Declining cheese consumption has driven milk back intoDeclining cheese consumption has driven milk back into powder and butter pushing up stock holdings and putting pressure on prices

EU Cheese consumption growth has slowed and is flat at -0.05%, but signs of pick up are emerging on the back of retail promotions in some markets e.g. France and Germany

USA Ch ti th i 0 6% b t i fUSA Cheese consumption growth is -0.6% but signs of increased promotional activity are emerging which should help recover and stabilise consumption patterns

Consumer confidence is expected to remain weak through 2009, demand recovery is likely to be slow

Growth rates:12 months to end March 2009

10

In Europe, cheese consumption underpins EU market prices and production

European Milk Production & Cheese Consumption* Trends 2006-9

3 50%

4.00%Forecast

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Ann

ual G

row

th %

* Cheese Consumption = Total Production + Imports – Exports

-1.00%

-0.50%

0.00%

0.50%

Jan-0

6

Apr-06

Jul-0

6

Oct-06

Jan-0

7

Apr-07

Jul-0

7

Oct-07

Jan-0

8

Apr-08

Jul-0

8

Oct-08

Jan-0

9

Apr-09

Jul-0

9

Oct-09

Milk Production growth % Cheese Consumption Growth %

French retail cheese sales have been recovering and are in positive growth territory

145,000 4%

125,000

130,000

135,000

140,000

Ret

ail S

ales

vol

ume

(1,0

00 k

g)

0%

1%

2%

3%

% G

row

th

115,000

120,000

Aug-06

Sep-06

Oct-06

Nov-06

Dec-06

Jan-0

7

Feb-07

Mar-07

Apr-07

May-07

Jun-07

Jul-0

7

Aug-07

Sep-07

Oct-07

Nov-07

Dec-07

Jan-0

8

Feb-08

Mar-08

Apr-08

May-08

Jun-0

8Ju

l-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-0

9

Feb-09

-2%

-1%

3m Rolling Volume (1,000 kgs) 12m Volume Growth % 3m Volume Growth vs Previous Year

11

US retail cheese consumption growth is negative, but price has assisted volume recovery

760

780

2%

3%

620

640

660

680

700

720

740

Ret

ail S

ales

Vol

ume

(mill

ion

lbs)

-4%

-3%

-2%

-1%

0%

1%

% G

row

th

* AC Nielsen Retail Scan Data

580

600

Aug-06

Sep-06

Oct-06

Nov-06

Dec-06

Jan-0

7

Feb-07

Mar-07

Apr-07

May-07

Jun-0

7Ju

l-07

Aug-07

Sep-07

Oct-07

Nov-07

Dec-07

Jan-0

8

Feb-08

Mar-08

Apr-08

May-08

Jun-0

8Ju

l-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-0

9

Feb-09

-6%

-5%

3m Rolling Volume (million lbs) 12m Volume Growth % 3m Volume Growth vs Previous Year

The demand sentiment is mixed

Dairy markets have been steady over recent weeks with no clear direction evident. After a flurry of sales activity the market has gone quiet - June US NFDM orders are not materialising for Dairy Am

International buyers really only have Northern hemisphere supply options through the short term and demand is not running hot

Sentiment is a mixed bag - some customers are reporting early signs of recovery while others have cash flow issues or remain over stocked

Sustained low pricing is supporting promotional activity and there’s evidence of increased A&P spend which should help

Seasonal and religious festival demand will hopefully assist in coming months

12

The pricing outlook is for gradual recovery in 2010

The outlook for the balance of 2009 has prices bouncing along in a trough

Evidence of a sustained supply side correction and demand recovery are required before prices re-bound

We expect a gradual recovery to emerge in 2010

Upsides: speedy supply side correction or shock; oil price recovery; corn price increase, emerging economic recovery; favourable weather patterns; water access issues

Downsides: lower prices fail to stimulate a demand rebound; tit for tat retaliatory action by the EU and the US; ‘toughing it out’ delays the supply side correction

Trends and their impact

13

Consumer trends

Unbalanced diet & obesity

Valuing food qualities

Time pressures

Older & younger age groups

Value for food dollar d groupsspend

The obesity burden is rising – the US is gaining weight fast but…

Source: Business Week - Inside Drugmakers' War on Fat, March 2008: Data on 30 pounds or more over weight

14

… this is not just a US problem

Source: OECD Factbook 2005 – Percentage of population older than 15 with a body-mass index greater than 30 (classified as obese)

Developing countries spend a greater portion of disposable income on food

Amount of disposable income spent on food at home

USDA Economic Research Service, 2005

15

More consumers are buying organic food

• Organic food sales are anticipated to increase an average of 18 percent each year from 2007 to 2010

Health and wellness trends are expected to grow

Euromonitor InternationalNote: Organic, Better for you and Naturally healthy products include food and beverages

16

…and the ‘premiumisation’ trend is still apparent

Premiumisation: consumers seeking better quality products, services and experiences across the board

Indulgence

Abundance of choiceEconomic growth

Key drivers:

Changing aspirationsRising affluence

Birth rates are higher in developing regions

World net birth rate percentages 2008

Source CIA World Factbook 2008

17

… and there is a growing older population

Proportion of the Population over 60 years of age

20

25

30

35

33

5

10

15

1950 19

55 1960 19

65 1970 19

75 1980 19

85 1990 19

95 2000 2005 2010 2015 2020 2025 2030 2035

2040

2045

2050

Customers are responding to these consumer trends

Unbalanced diet & obesity

Valuing food qualities

Time pressures

Older & younger age gro ps

Value for food dollar

Health & wellness offerings including functional foods

On-the-go & out-of-home eating offers

Differentiated flavours& textures

groupsspend

Reduced cost in useTargeted paediatric &

senior product offerings

18

Dairy offers innovative dairy solutions to consumer trends

Unbalanced diet & obesity

Valuing food qualities

N i di t & i

Time pressures

Older & younger age Value for food dollar

Protein ingredients with unique health & wellness benefits

New ingredients & processing systems that deliver

differentiated flavours & textures

Flexibility in product functionality

groupsspend

Unique health & wellness benefits

Specialised ingredients to address nutrition, digestion &

immunityCost effective ingredients,

processes & services

What does this mean for the dairy industry?

19

Current financial turmoil, medium term trend is expected to be positive

Demand for dairy will continue to grow, although rate of growth may be slower in short term

20

Recent re-introduction of subsidies in EU & US, longer term possibility of increased FTAs

Changing supply in dairy producing countries

21

Short term global stocks of dairy, possibility of longer term shortages

The impact of environmental issues will remain

22

Dairying in New Zealand & Fonterra

Today New Zealand is the most deregulated dairy industry in the world

• No subsidies • Dairy Industry Restructuring Act 2001 and Dairy Industry

Key Features Regulatory Framework

• Grass-based milk production• Scale• Temperate climate• Geographic isolation• Strict border controls and food

safety regulations

Act 2001 and Dairy Industry Restructuring Amendment Act 2007

• Removal of exclusive rights to export dairy products

• Supply milk to all who seek it • Open entry

• Herd quality • Open exit

23

Dairy farming in New Zealand has a long history

The Challenge….• Protein-based food and health building blocks become more important to an

ageing demographic and developing nations• Commodity profits attract increased world-wide investment• Vertical integration creates wealth• Global trade challenge moves from across borders to behind borders

Forecast CAGR 2004-2014

< 0%0% - 2.5%2.5% - 5.0%> 5.0%

LATAM +14

AME +14CN +52

EU +5

CIS/FSU +6

CA/US +7

PK/IN +22Forecast CAGR 2004-2014

< 0%0% - 2.5%2.5% - 5.0%> 5.0%

Forecast CAGR 2004-2014

< 0%0% - 2.5%2.5% - 5.0%> 5.0%

LATAM +14

AME +14CN +52

EU +5

CIS/FSU +6

CA/US +7

PK/IN +22

1960s – 1990s… “Diversify ahead of the pack”

• Land, labour and fuel prices increase on-farm costs over 60%• 24/7/365 days in the plants – shortage of on-farm labour

• Britain joins the EEU, introduction of UK butter quotas• Oil prices spike further; NZ subsidies disappear• Production capabilities develop globally, new markets develop

g

• July 2001, Fonterra is created• Moves from 19% of traded market in

1990, to 40% in 2007• Globally sourced product increases

from 30,000MT to 300,000MT with a projected supply gap of 1.5bn MT

• Partnering with the world’s leading dairy companies

1930s – 1960s… “Advances in Technology”

• The “Grasslands Revolution”• 18million acres cleared by hand - fired, and cleared from swamp, bush, and tussock land impacted by rabbit infestation

– average life expectancy 72yrs• Larger than the entire English pasture lands

• Waikato farmer Ron Sharp invents herringbone milking shed; artificial breeding introduced in 1951• Tankers collect wholemilk from 1951, and cooling of milk on-farm introduced in 1955• Consolidation - by the 1960s, the number of cooperatives had become 168

• 400+ cooperatives struggle to keep plants running

1800s – 1930s… “Pioneering grit”

• No cows, no land, no expertise

Dairy farming in New Zealand today

11,500 farms

4 million cows

Average farm size - 115 hectares

Average herd size - 337 cows

Average production per herd - 113,182 kgMS

Average production per cow - 330 kgMS

Average total capital value - NZ$3 3Average total capital value - NZ$3.3 million

Source: LIC New Zealand Dairy Statistics 2006-2007

24

Fonterra today

Co-operative owned by 10,900 supplier shareholders

Operating revenue of USD $14 billion

P d 2 9 illi t f d t llProduce 2.9 million tonnes of products annually

Export 96% of production to more than 140 markets around the world

Employ 16,400 people worldwide

Approximately 20% of New Zealand’s export earnings

Handles more than 40% of the world’s traded dairy commodities

Fonterra’s Trade Flow: 2000

Fonterra - evolving from New Zealand based exporter

25

… to a major global player

Fonterra’s Trade Flow: 2006

Global dairy consumption and trade

WorldTraded Internationally 7%

New ZealandConsumed

Domestically 4%

C d D ti ll 93%

Exported 96%

Consumed Domestically 93%

26

Worldwide supply

Fonterra’s Supply Outlook

Summer conditions proved challenging in key regions but great autumn weather helped most farmers’ cause

Follo ing recent cold eather the season has endedFollowing recent cold weather the season has ended earlier than forecast:– pasture growth has been restricted increasing herd dry

off rates– F09sn milk production is expected to reach ~ 1,280m

kgs milk solids or approx 15.1 billion litres, a record ilk th i ith th d ht ff t d– milk growth comparisons with the drought effected

F08sn are misleading

The outlook for F10 is for milk production to increase +2%

27

Fonterra milk collection is back on trackDaily Fonterra Milk Collection

80,000

30,000

40,000

50,000

60,000

70,000

Volu

me

(000

litr

es /

day)

2006-07 season actual 2007-08 season actual 2008-09 season actual

0

10,000

20,000

Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May

LegendLegend

Australian supply outlook is for growth this season, but maybe not for the next season

F09 season has been characterised by:

– rain at the right times and in the right places

l ti l ild t t th h th d f 2008– relatively mild temperatures through the end of 2008

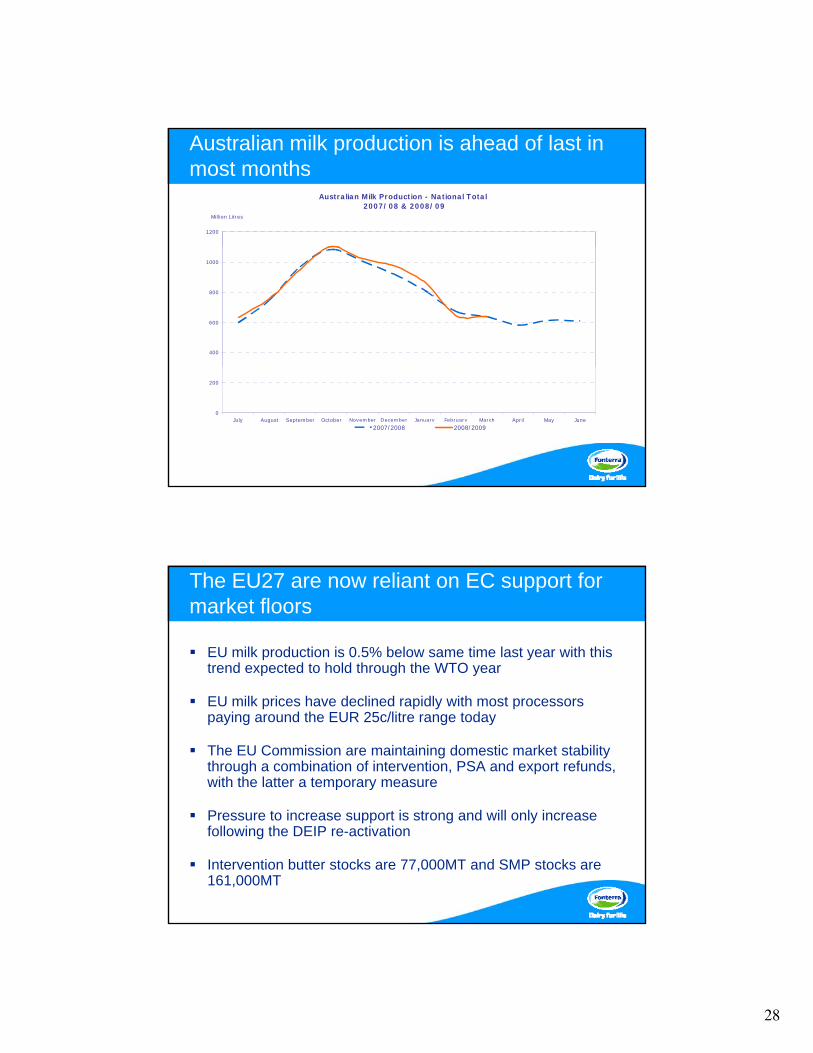

Australia's milk production is up 2.2% on last season (through March 09). Latest FYF is +2% to 9.4b litres.

Forecast lower average prices for F10 is influencing more farmers to keep milking later despite payout step downs

Availability has tightened after a strong sales campaign over recent months

Farmer confidence is mixed. Those with high debt levels particularly in the North Victoria are under pressure. Dairy Aust F10 forecast is 9.0b litres

28

Australian milk production is ahead of last in most months

Australian Milk Production - National Total 2007/08 & 2008/09

1200

Million Litres

400

600

800

1000

0

200

July August September October November December January February March April May June

2007/2008 2008/2009

The EU27 are now reliant on EC support for market floors

EU milk production is 0.5% below same time last year with this trend expected to hold through the WTO year

EU milk prices have declined rapidly with most processors paying around the EUR 25c/litre range today

The EU Commission are maintaining domestic market stability through a combination of intervention, PSA and export refunds, with the latter a temporary measure

Pressure to increase support is strong and will only increase following the DEIP re-activation

Intervention butter stocks are 77,000MT and SMP stocks are 161,000MT

29

European milk prices have fallen away dramatically over recent months

45

50

25

30

35

40

Euro

Cen

ts p

er L

itre

EU Milk Management Committee Statistics May 20, 2009

20

25

Jan-06

Apr-06

Jul-0

6Oct-

06

Jan-0

7Apr-

07Ju

l-07

Oct-07

Jan-0

8Apr-0

8Ju

l-08

Oct-08

Jan-09

Germany France Ireland Netherlands EU25

The United States farmers are under significant pressure

US milk production is forecast to contract -0.3% in CY2009

CWT culling initiatives will assist but more is required - still too i th US h dmany cows in the US herd

CCC support for domestic school lunch and food bank programmes was a positive step, but the re-introduction of DEIP wasn’t

DEIP only encourages greater international market uncertainty, invites a response from the EU and doesn’t assist US dairymen

USDA’ tl k f CY2010 ilk d ti i f f th 0 5%USDA’s outlook for CY2010 milk production is for a further -0.5% reduction

How many dairymen are ‘toughing it out’ until September when prices are forecast to increase…….the slope of hope?

30

6 0%

7.0%

8.0%

The United States production surpluses have resulted in stock builds

Fluid : -0.5%

Fresh Dairy : -1.3%

Cheese : -0 6%

0 0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Ann

ual G

row

th %

Cheese : -0.6%

Milk Production : +1.2%

-2.0%

-1.0%

0.0%

Jan-0

2Ju

l-02

Jan-0

3Ju

l-03

Jan-0

4Ju

l-04

Jan-0

5Ju

l-05

Jan-0

6Ju

l-06

Jan-0

7Ju

l-07

Jan-0

8Ju

l-08

Jan-0

9Ju

l-09

Milk Production Growth % Fluid Consumption Growth %Fresh Dairy Consumption Growth % Cheese Consumption Growth %

* Consumption = Total Production + Imports – Exports

For the Southern Cone, Argentina is unlikely to feature on export stage until later in 2009

Drought has impacted milk production in CY2009 with the latest forecast now 10.2b litres (+2% on 2008)

With a 20% structural surplus and milk prices aligned with international commodity levels, Argentina is well placed to compete on export markets

But a combination of factors has kept Argentine supply contained:– export activity into Brazil earlier in the year– good domestic consumption – and now drought impacted milk collection

Looking further ahead– the 5% export tax and government retentions are now removed– domestic demand may falter as economic conditions worsen– the Peso has devalued

31

With the Brazilian local market strong there is little incentive to overproduce

Drought in the south (Rio Grande del Sul) and lower milk prices paid to farmers is forecast to hold milk production flat at 29b litres (vs +4% in 2008)

Drought and strong domestic demand meant imports from Argentina and Uruguay were required to cover the deficit

Brazilian milk prices remain above world market levels which should limit exports until at least early 2010 p y

While marginal milk can be turned on or off very quickly the high milk price is a disincentive even with a weaker Brazilian Real.

In China, despite high Chinese stocks import demand remains robust

Local milk powder stocks are building – some reports suggest anywhere from 100k to 300k MT is in store without a home -though 100 to 150k MT is probably more realistic

Stocks of local WMP are unlikely to have a major impact on imported WMP demand or the global market– domestic stock will deteriorate as it ages and summer

arrives– what can be re-worked for fresh applications will be– likely to be used as domestic aid in poor areas– likely to be used as domestic aid in poor areas– Government may provide subsidies to manufacturers and

allow them to write off the value and use in feed applications

32

Thank you

Thank you