Presentation to IDC Conference 24 – 25 June 2012 The impact of various legislative frameworks on...

21

Presentation to IDC Conference 24 – 25 June 2012 The impact of various legislative frameworks on Effective and Sustainable Employee Ownership Model (US, UK and Australia examined)

-

Upload

marybeth-norris -

Category

Documents

-

view

218 -

download

2

Transcript of Presentation to IDC Conference 24 – 25 June 2012 The impact of various legislative frameworks on...

Presentation to IDC Conference24 – 25 June 2012

The impact of various legislative frameworks on Effective and Sustainable Employee Ownership Model (US, UK and Australia

examined)

2

Key Impacts on Employee Share Ownership

Securities and Corporations Law

Foreign Exchange requirements

Tax legislation

Market sentiment

Executive remuneration structures

3

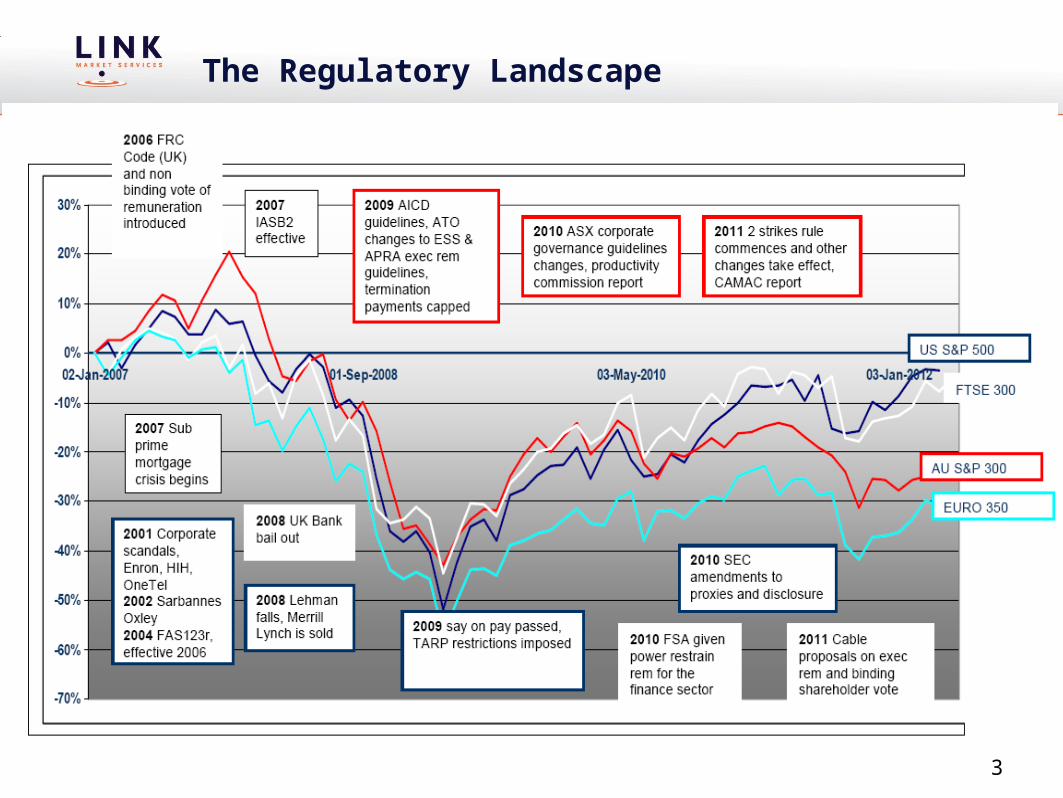

The Regulatory Landscape

4

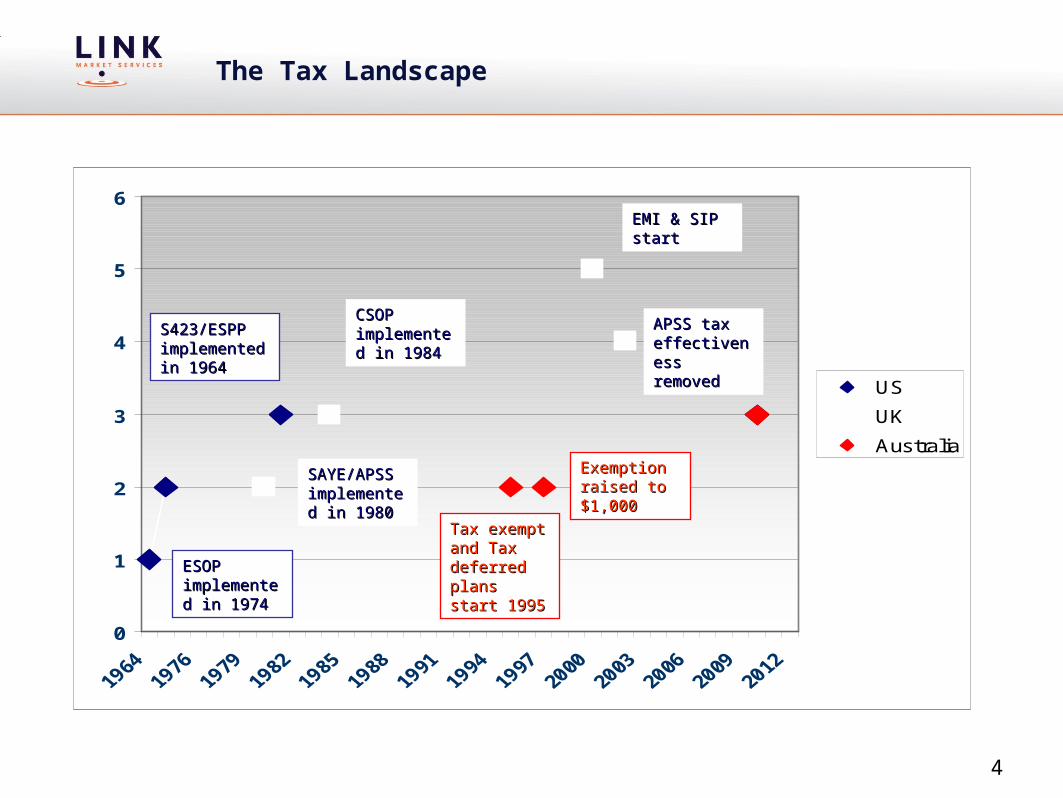

The Tax Landscape

0

1

2

3

4

5

6

US

UK

Australia

S423/ESPP S423/ESPP implemented in implemented in 19641964

ESOP ESOP implemented implemented in 1974in 1974

SAYE/APSS SAYE/APSS implemented implemented in 1980in 1980

CSOP CSOP implemented implemented in 1984in 1984

EMI & SIP EMI & SIP startstart

APSS tax APSS tax effectiveness effectiveness removedremoved

Tax exempt Tax exempt and Tax and Tax deferred deferred plans start plans start 19951995

Exemption Exemption raised to raised to $1,000$1,000

5

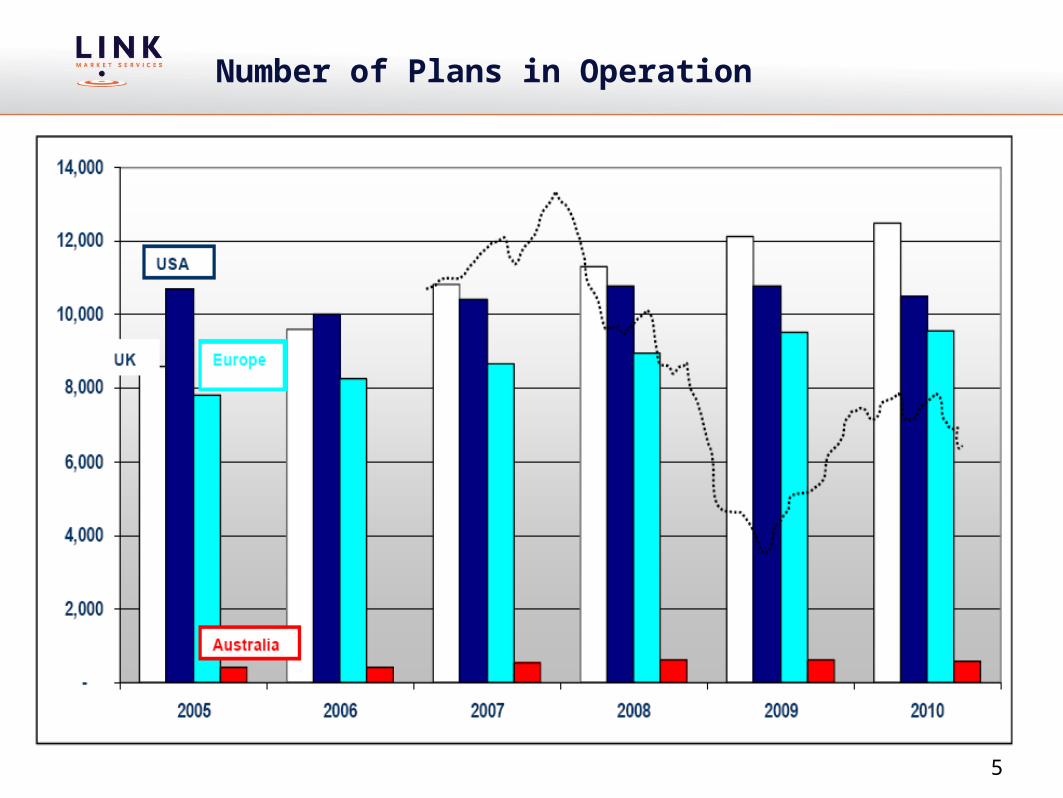

Number of Plans in Operation

6

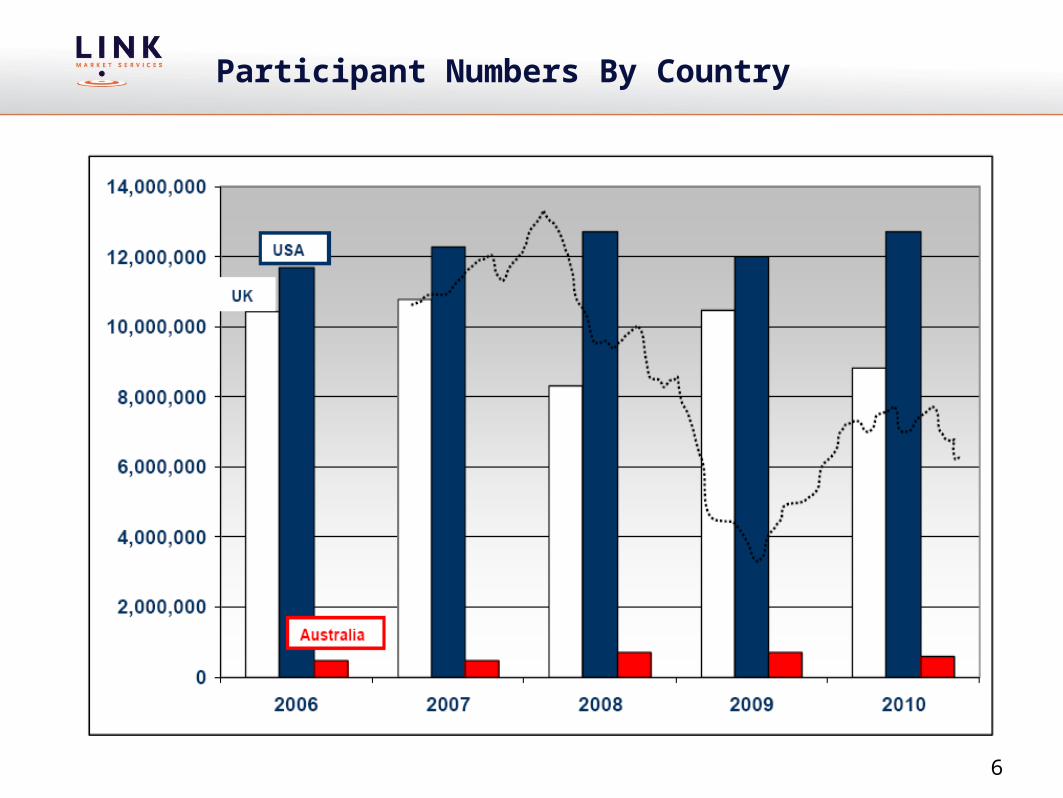

Participant Numbers By Country

7

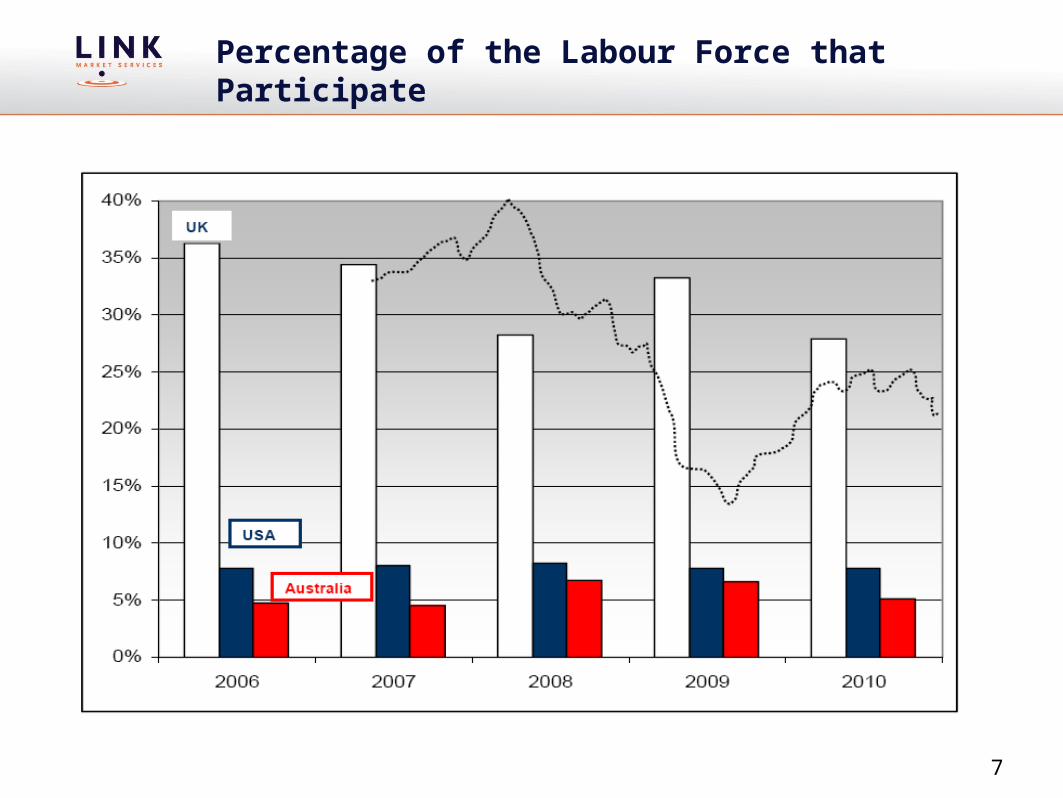

Percentage of the Labour Force that Participate

8

The UK Landscape

9

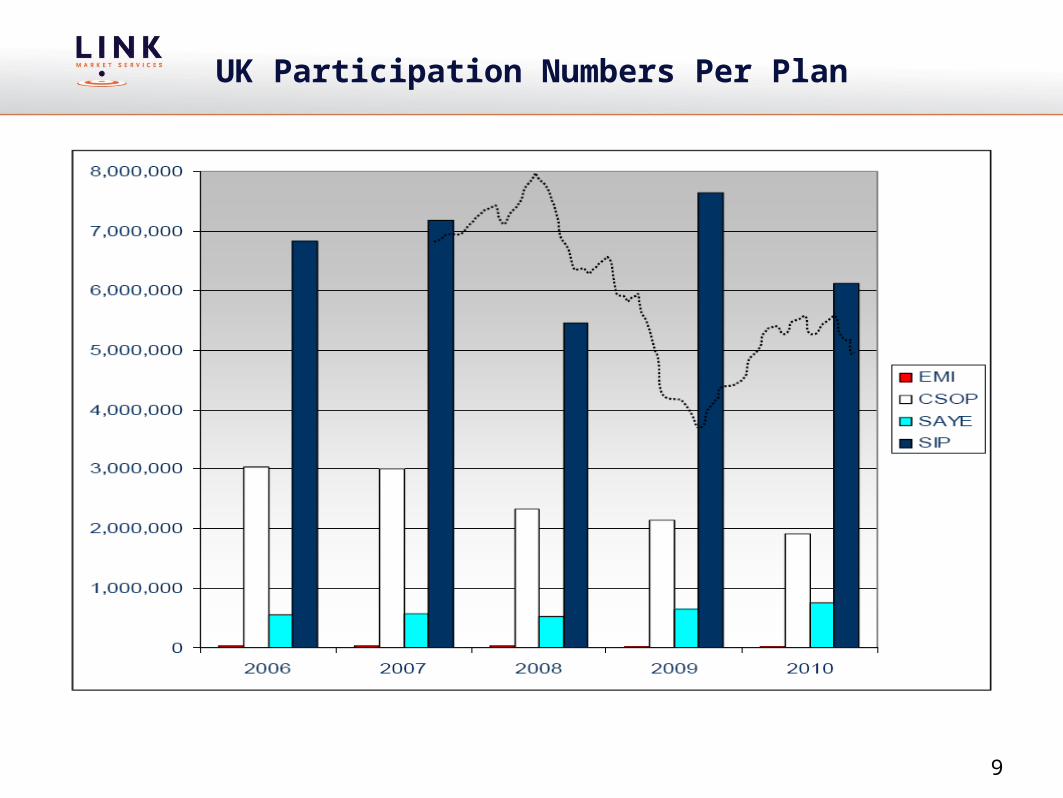

UK Participation Numbers Per Plan

10

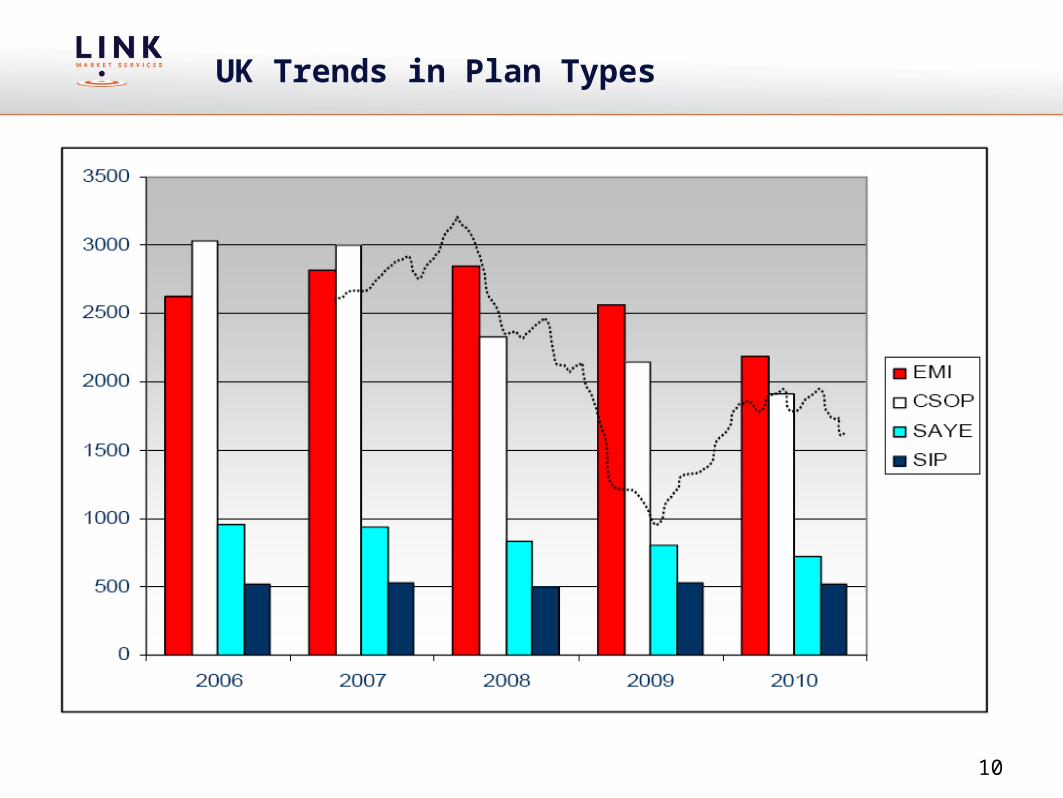

UK Trends in Plan Types

11

The US Landscape

12

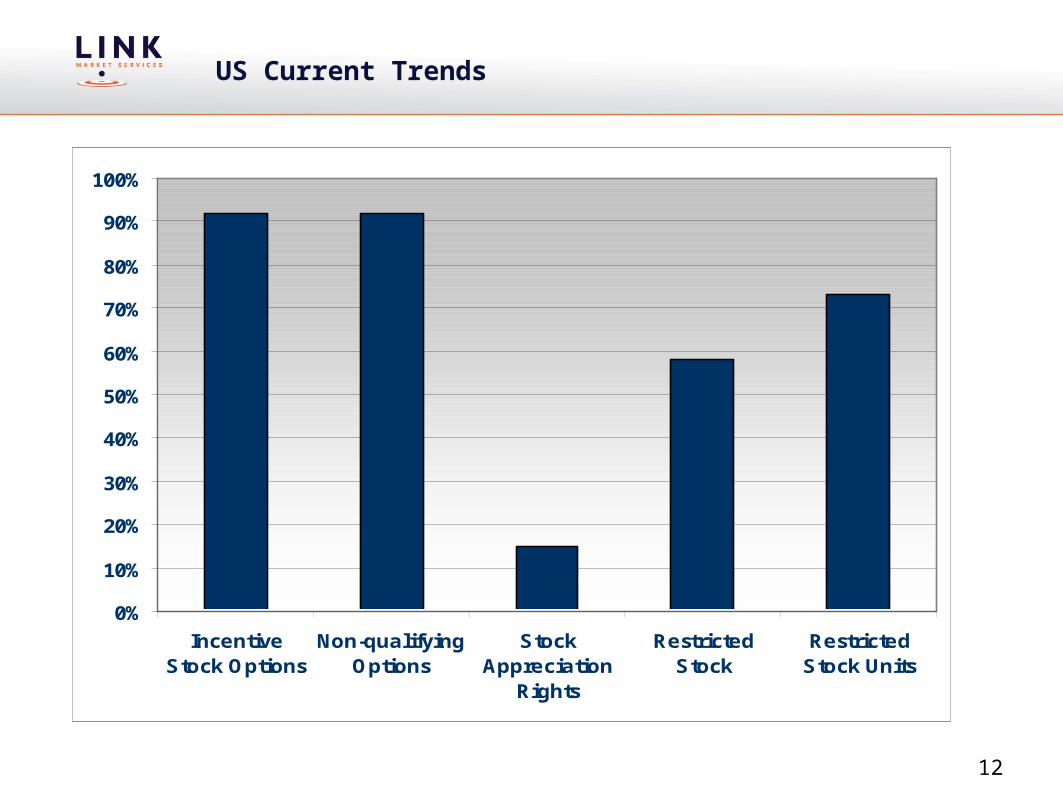

US Current Trends

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

IncentiveStock Options

Non-qualifyingOptions

StockAppreciation

Rights

RestrictedStock

RestrictedStock Units

13

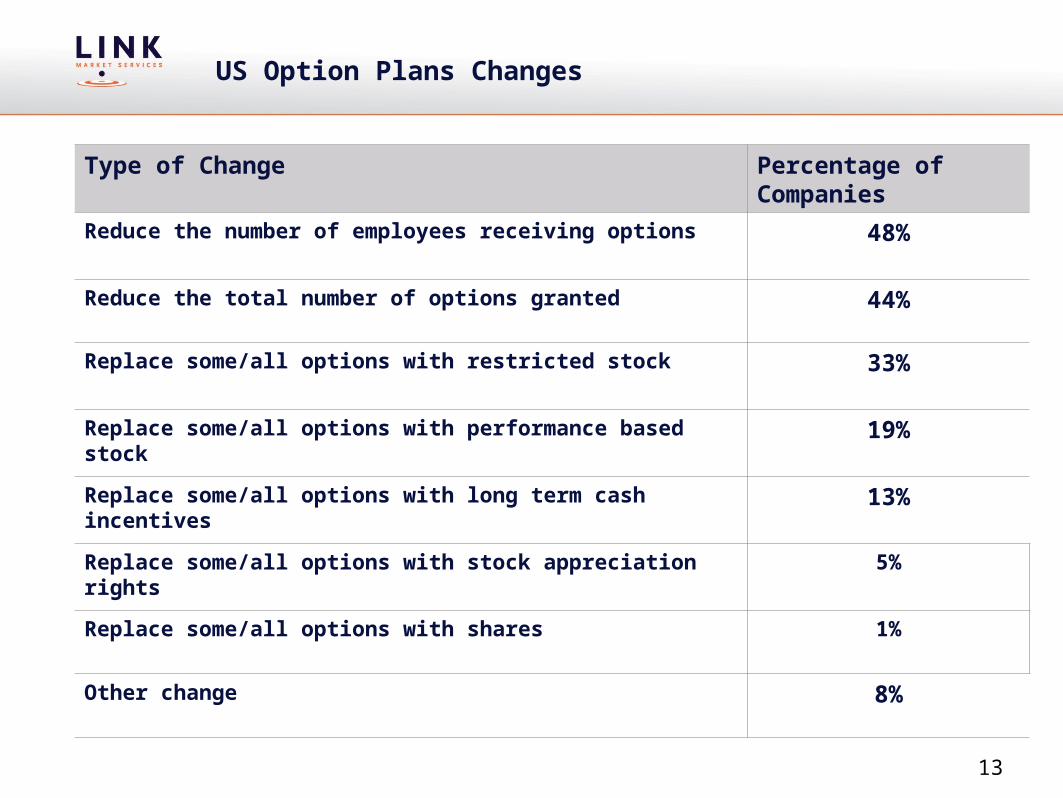

US Option Plans Changes

Type of Change Percentage of Companies

Reduce the number of employees receiving options 48%

Reduce the total number of options granted 44%

Replace some/all options with restricted stock 33%

Replace some/all options with performance based stock 19%

Replace some/all options with long term cash incentives 13%

Replace some/all options with stock appreciation rights 5%

Replace some/all options with shares 1%

Other change 8%

14

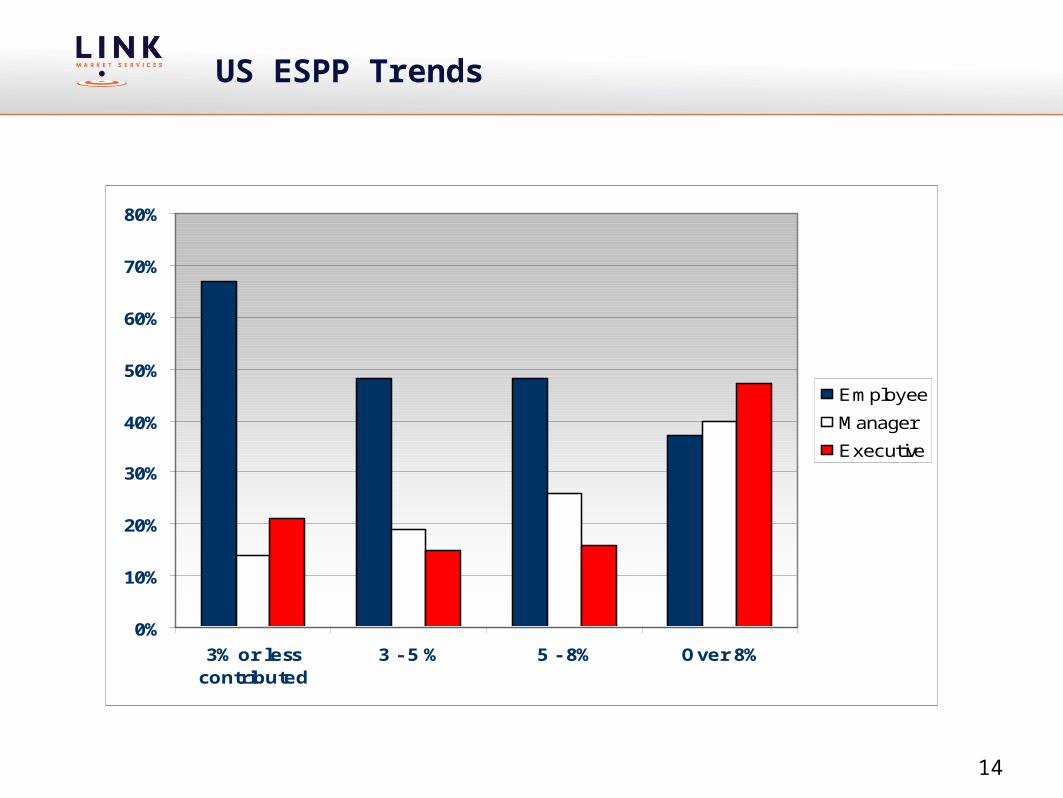

US ESPP Trends

0%

10%

20%

30%

40%

50%

60%

70%

80%

3% or lesscontributed

3 - 5 % 5 - 8% Over 8%

Employee

Manager

Executive

15

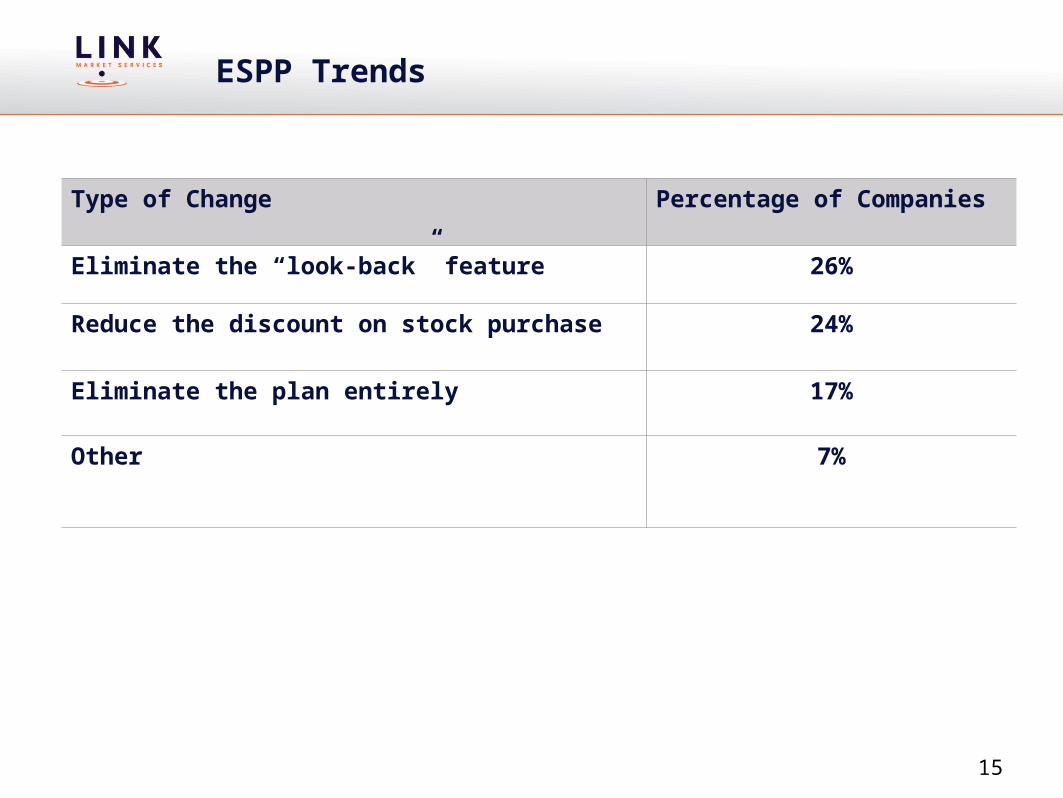

ESPP Trends

Type of Change Percentage of Companies

Eliminate the “look-back” feature 26%

Reduce the discount on stock purchase 24%

Eliminate the plan entirely 17%

Other 7%

16

The Australia Landscape

17

Australia – The Number of Plans that Companies Operate

12

34+

2009

2010

2011

0%

10%

20%

30%

40%

50%

60%

2009

2010

2011

perran

insert tax legislation change

18

Employee Plan Types Used in Australia

TE FreeTE SalarySacrifice TD Salary

Sacrifice Other

2009

2010

2011

0%

10%

20%

30%

40%

50%

60%

70%

2009

2010

2011

19

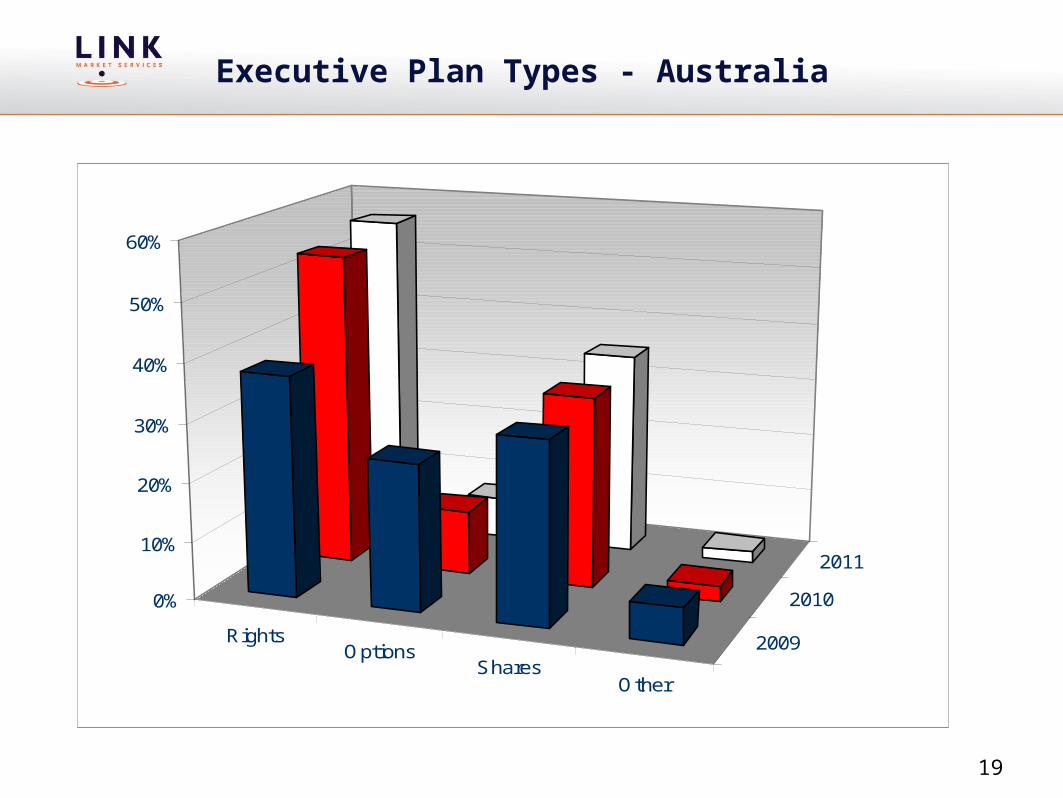

Executive Plan Types - Australia

RightsOptions

SharesOther

2009

2010

2011

0%

10%

20%

30%

40%

50%

60%

20

Conclusions

The biggest impacts: Employee taxation Executive remuneration sentiment Market sentiment, costs for a company

Securities law can be the killer

Discussion