Presentation to: Association of California Community ...

23

Association of California Community College Administrators Top 10 Q&A on Retiree Health Benefits February 21, 2008 Presentation to:

Transcript of Presentation to: Association of California Community ...

Association of CaliforniaCommunity College Administrators

Top 10 Q&A on Retiree Health Benefits

February 21, 2008

Presentation to:

Panelists & ProtocolQ&A on Retiree Health Benefits

Moderator

– Lori Koh, Vice President, Lehman Brothers

Panelists

Protocol

– Panelists to each address question, followed by audience comments and questions

C.M. BrahmbhattVice Chancellor for Administrative Services

Coast Community College District

Elizabeth YeeSenior Vice President

Lehman Brothers

Heidi WhitePartner

Vavrinek, Trine, Day & Co., LLP

1

Public Employee Post-Employment Benefits Commission Developed an Eight-Point Plan to Address OPEB

Q&A on Retiree Health Benefits

On January 7, 2008, the bi-partisan, 12-member PEBC released a comprehensive report, including a plan for public agencies in California to address OPEB

Identify and Prefund Financial Obligations

Limit Contribution Volatility & UseSmoothing Methods Judiciously

Increase Transparency and Accountability

Improve Plan Design and Communications with Employees

Provide Independent Analysis

Strengthen Governance andEnhance Transparency

Coordinate with Medicare

Advocate Federal Tax Law Changes

Commission to write a letter to the IRS on several proposed tax changes, including the commingling of OPEB and pension investment funds

Identify individuals eligible for Medicare and inform and encourage them to enroll in a timely manner

Boards that govern pension and/or OPEB trusts should abide by strong conflict of interest policies, review the actuarial assumptions and sensitivity analyses to those assumptions, and enlist qualified individuals to serve on the boards

Create an actuarial advisory panel at the state level, conduct periodic performance audits of public pension plans

Design plans to reward longer careers, provide tax-advantaged supplemental savings plans, explain benefit packages and eligibility, and notify employees promptly of changes

Direct State Controller’s office to collect and OPEB data from public agencies regularly and publish its findings. Public agencies should publicly disclose the liability and the cost of granting additional OPEB benefits and in language easily understood by the layperson

Consider longer asset-smoothing periods to reduce volatility, refrain from altering smoothing methods for short-term gains, restrict use of employer contribution “holidays”, and use any pension surpluses to address OPEB liability

Adopt prefunding as a policy, adopt a prefunding plan and make it public. Those considering OPEB bonds should understand the potential risks.

2

Survey Response RateQ&A on Retiree Health Benefits

66%46%4751,036School Districts

100%100%11State of California (includes CSU)

100%100%11University of California

67%54%3972Community Colleges

73%18%3742,052Special Districts

100%100%5858Counties

78%48%231478Cities

Percent of Total Revenues

Percent of Total Entities

Total Returns

Total EntitiesContacted

Public Entity

A majority of community college districts participated in the PEBC survey

3

California Public Employers UAALQ&A on Retiree Health Benefits

$118,126,505,346Total

15,902,000,433School Districts

47,880,000,000State of California (includes CSU)

11,500,000,000University of California

2,523,812,196Community Colleges

3,493,610,596Special Districts

28,008,890,314Counties

8,818,191,807Cities

Total Value ($)Public Entity

The community college districts who responded to the survey collectively have an unfunded OPEB liability exceeding $2.5 billion

4

Approaches to Funding OPEB BenefitsQ&A on Retiree Health Benefits

22%78%Total

21%79%School Districts

0%100%State of California (includes CSU)

0%100%University of California

49%51%Community Colleges

22%78%Special Districts

23%77%Counties

20%80%Cities

PrefundingPay-As-You-GoPublic Entity

49% of the community college district respondents have started prefunding their OPEBliability

5

Panel QuestionsQ&A on Retiree Health Benefits

Question 1 What is your reaction to the Governor’s PEBC findings?Why do you think the community colleges appear to be

ahead of other public agencies?

C.M. Brahmbhatt

Elizabeth Yee

6

Does your district have OPEB “retiree benefits” liabilities?

What is the date of the last actuarial study of your district’s OPEB liabilities?

Community College Districts Are Aware of OPEBIn May 2006, the Chancellor’s Office surveyed the 72 community college districts regarding their OPEB “retiree benefits” liabilities

Q&A on Retiree Health Benefits

1.4%1No100.0%72Total

98.6%71YesPercentageNumber of Districts

100.0%72Total1.4%1No OPEB, no study required (no OPEB)

20.8%15Not been performed

16.7%12Between two to four years ago11.1%8More than four years ago

50.0%36Within last two yearsPercentage# of DistrictsAn actuarial study has been performed:

Total unfunded liability reported as of the study was $3,066,146,41915 districts had not completed an actuarial study as of May 1, 2006 so their unfunded liability could not be determined

What was your district’s unfunded liability at the time of the latest study?55 districts reported unfunded liabilities in the following dollar ranges:

49

2311

43

1

0 5 10 15 20 25

Less than or equal to $5MGreater than $5M and less than or equal to $10M

Greater than $10M and less than or equal to $50MGreater than $50M and less than or equal to $100M

Greater than $100M and less than or equal to $150MGreater than $150M and less than or equal to $200M

Greater than $500M

7

Panel QuestionsQ&A on Retiree Health Benefits

Question 2Can you summarize where your district is on OPEB? Have you done an actuarial study? What steps have

you taken to reduce the liability? Do you have a funding plan in place?

C.M. Brahmbhatt

8

Coast Community College District is Addressing Its OPEB Liability Q&A on Retiree Health Benefits

Quantify liabilities

Select investment vehicle

Identify one-time funds

Find ongoing sources

Negotiate employee contributions

A liability of $70,310,982 as of May 1, 2006 per actuarial study dated August 31, 2006.Updated actuarial study in progress

Irrevocable trust through the Community College League of California’s Investment Joint Powers Authority

District ending balanceExcess ending balance over required reserve for self insurance programNet proceeds from sale of TV station

First $250,000 of new revenue growth in the baseLand lease for District site ($480,000 annually for 50 years)Salary savings from sale of TV station ($1.2 million ongoing annually)

Percentage of salaries for contract employees charged as a benefit (originally 2%, now 3%)Once the liability is fully funded, current year retiree benefit costs will be withdrawn from the fund, and pre-funding amounts will be deposited. On-going funding streams will be available for District use

9

Panel QuestionsQ&A on Retiree Health Benefits

Question 3 What kind of OPEB funding vehicles are your clients seeing, considering or using?

Elizabeth Yee

10

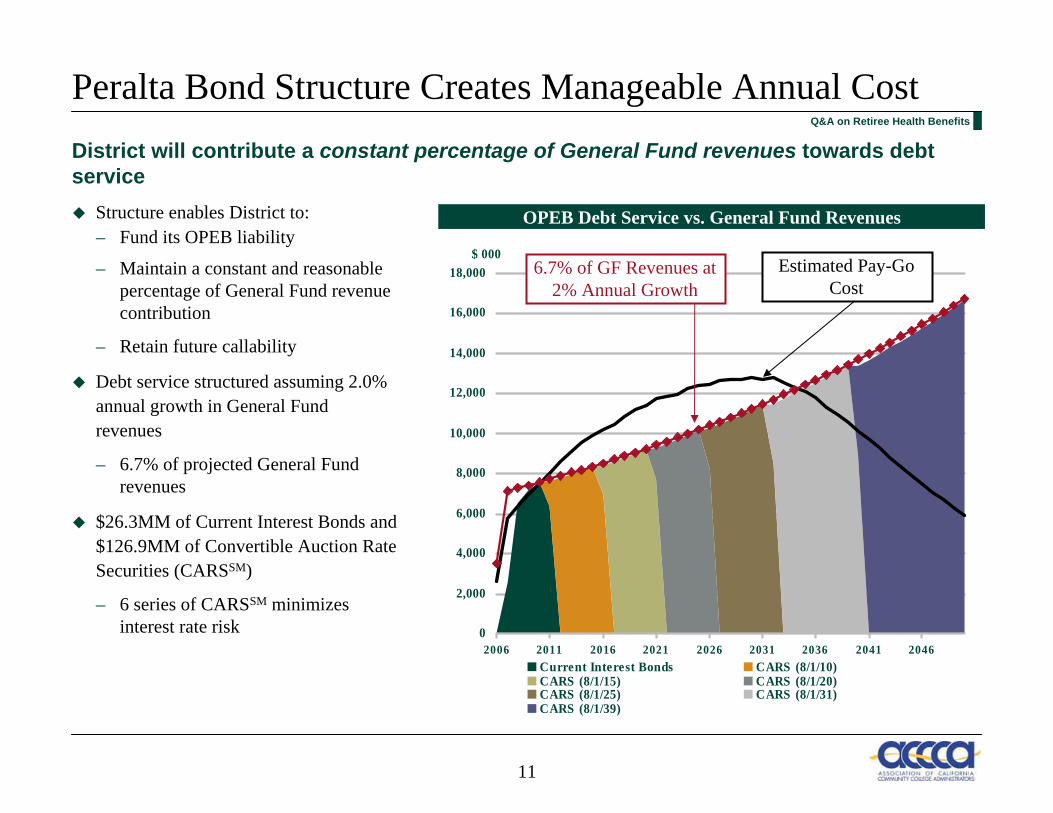

Peralta Bond Structure Creates Manageable Annual Cost

Structure enables District to: – Fund its OPEB liability

– Maintain a constant and reasonable percentage of General Fund revenue contribution

– Retain future callability

Debt service structured assuming 2.0% annual growth in General Fund revenues

– 6.7% of projected General Fund revenues

$26.3MM of Current Interest Bonds and $126.9MM of Convertible Auction Rate Securities (CARSSM)

– 6 series of CARSSM minimizes interest rate risk

OPEB Debt Service vs. General Fund Revenues

District will contribute a constant percentage of General Fund revenues towards debt service

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2006 2011 2016 2021 2026 2031 2036 2041 2046

$ 000

Current Interest Bonds CARS (8/1/10)CARS (8/1/15) CARS (8/1/20)CARS (8/1/25) CARS (8/1/31)CARS (8/1/39)

Estimated Pay-Go Cost

6.7% of GF Revenues at 2% Annual Growth

Q&A on Retiree Health Benefits

11

Panel QuestionsQ&A on Retiree Health Benefits

Question 4 What role did your District's OPEB liability and funding plan play in the accreditation of your colleges?

C.M. Brahmbhatt

12

How is OPEB Liability Reflected in Accreditation Review?Q&A on Retiree Health Benefits

The district is commended for its comprehensive plan to address its future retiree benefits liability… the district has a plan to meet its future retiree benefit obligation to be in compliance with GASB 45 by July 1, 2007

Evaluation Report, March 8, 2007

When making short-range financial plans, the institution considers its long-range financial priorities to assure financial stability. The institution clearly identifies and plans for payment of liabilities and future obligations.

Accreditation Standards

Long term indebtedness and future liabilities are budgeted for and managed adequately at the district level, which has implemented a GASB 45 mechanism to address long term health insurance liabilities, although the Board has yet to adopt a formal plan.

Evaluation Report, July 12, 2007

Orange Coast College Coastline Community College

Coast’s GASB 45 approach was viewed positively during accreditation

On the checklist circulated by the System Office:Retiree Health Benefits – Is this area acceptable? Yes / No– Has the District completed an actuarial calculation to determine the unfunded liability?– Does the district have a plan for addressing the retiree benefits liabilities?

Sound Fiscal Management Self-Assessment Checklist

13

Panel QuestionsQ&A on Retiree Health Benefits

Question 5 Does your firm have a view on whether any part of OPEB expenses can fall under the good side

of meeting the 50% Law?

Heidi White

14

Panel QuestionsQ&A on Retiree Health Benefits

Question 6GASB 45 requires disclosure of a public agency’s retiree

health benefits liability in its financials. What is the required funding level upon implementation? Could you give more

specifics on what information needs to be disclosed?

Heidi White

15

Panel QuestionsQ&A on Retiree Health Benefits

Question 7The concept of an irrevocable trust is daunting.

Is the District required to set up an irrevocable trust for the payments of OPEB liabilities?

How do you handle the potential loss of budgeting flexibility?

Heidi White

C.M. Brahmbhatt

16

Panel QuestionsQ&A on Retiree Health Benefits

Question 8 What happens if I issue bonds and then there is universal healthcare?

Elizabeth Yee

17

Panel QuestionsQ&A on Retiree Health Benefits

Question 9 How does a District charge OPEB expense to federal and state categorical programs?

Heidi White

C.M. Brahmbhatt

18

Panel QuestionsQ&A on Retiree Health Benefits

Question 10 If my District issues OPEB Bonds, how will debt service be treated for federal cost sharing purposes?

Elizabeth Yee

19

Reimbursement IssuesOPEB costs should be reimbursable, so long as OPEB bond debt service is less than actuarially certified UAAL payments

The risk to a public agency, as with all grant programs, is the level of future grant funding

Lehman Brothers’ Benefit Burden Model allows a community college district to quantify that risk

The cost of fringe benefits in the form of employer contributions or expenses for social security; employee life, health, unemployment, and worker’s compensation insurance (except as indicated in section 25, insurance and indemnification); pension plan costs (see subsection e.); and other similar benefits are allowable, provided such benefits are granted under established written policies. Such benefits whether treated as indirect costs or as direct costs, shall be allocated to Federal awards and all other activities in a manner consistent with the pattern of benefits attributable to the individuals or group(s) of employees whose salaries and wages are chargeable to such Federal awards and other activities.

OMB Circular A-87 (Revised 5/4/95, as further amended 8/29/97)

20

Appendix

Useful Definitions Q&A on Retiree Health Benefits

What is OPEB?

What is GASB 45?

When does GASB 45 need to be implemented?

What is Annual OPEB Cost?

What is the ARC?

What is a net OPEBobligation?

Other Post-Employment Benefits consists of retirement benefits other than pension (medical, dental, etc.)Often used interchangeably with “retiree health benefits”

Governmental Accounting Standards Board issued a Standard #45 which requires public agencies to quantify and disclose their OPEB liabilities.

Phased implementation– FY2007-08 for Districts with revenues of $100 million or more– FY 2008-09 for Districts with revenues between $10 million and $100 million– FY 2009-10 for Districts with revenues less than $10 million

Employer’s annual required contribution to the plan (ARC)Adjustments for net OPEB obligation caused by past under- or over-contributions

Normal cost for the yearAmortization of total unfunded actuarial accrued liabilities (UAAL) or funding excess of the plan over period not longer than 30 years.

Cumulative difference between annual OPEB cost and the employer’s contributions to a plan, including any OPEB liability or asset at transition.OPEB liability will likely be zero (measurement is not retroactive at the transition).Net OPEB obligation to be reported as a general long-term liability

21