Presentation of the Q2/2019 results

27

Presentation of the Q2/2019 results Martin Lindqvist, President & CEO Håkan Folin, CFO July 19, 2019

Transcript of Presentation of the Q2/2019 results

Presentation of the Q2/2019 resultsMartin Lindqvist, President & CEOHåkan Folin, CFO

July 19, 2019

Agenda

►Summary of Q2/2019

►Performance by division

►Financials

►Outlook

►Q&A

2

3

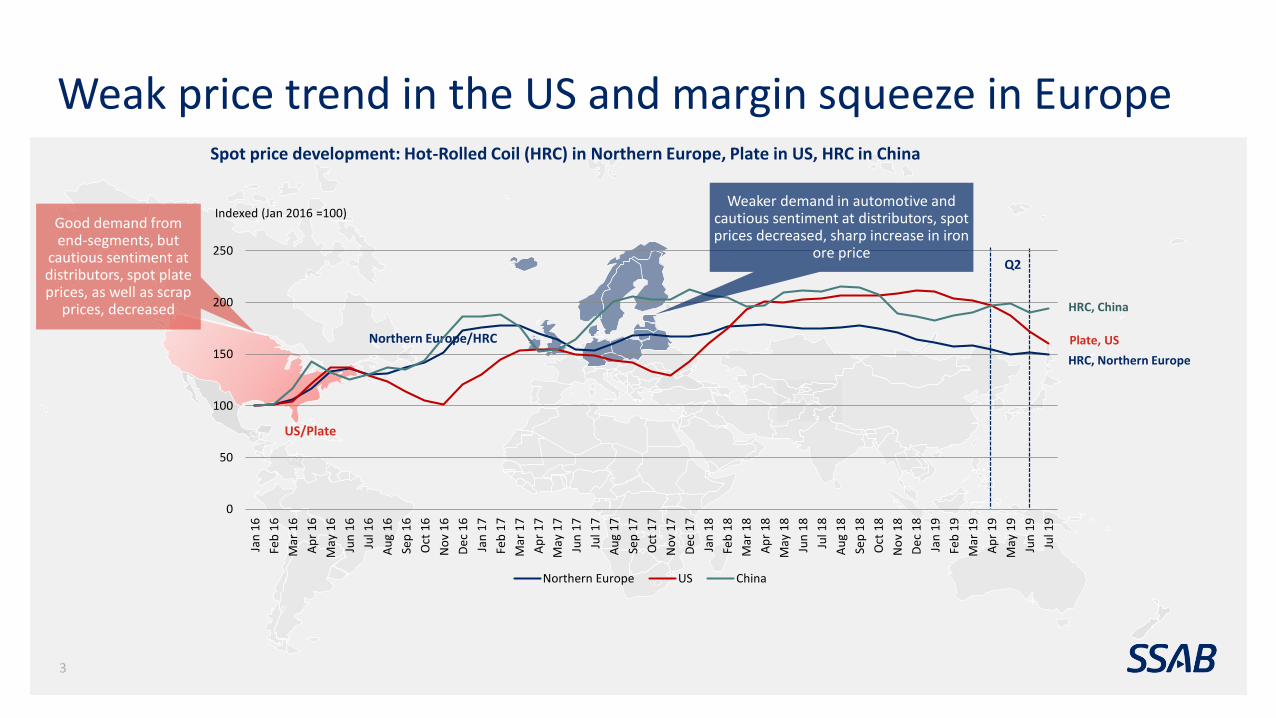

Spot price development: Hot-Rolled Coil (HRC) in Northern Europe, Plate in US, HRC in China

Indexed (Jan 2016 =100)

Q2

Northern Europe/HRC

US/Plate

HRC, Northern Europe

Plate, US

HRC, China

Weak price trend in the US and margin squeeze in Europe

Good demand from end-segments, but

cautious sentiment at distributors, spot plate prices, as well as scrap

prices, decreased

0

50

100

150

200

250Ja

n 1

6

Feb

16

Mar

16

Ap

r 1

6

May

16

Jun

16

Jul 1

6

Au

g 1

6

Sep

16

Oct

16

No

v 1

6

De

c 1

6

Jan

17

Feb

17

Mar

17

Ap

r 1

7

May

17

Jun

17

Jul 1

7

Au

g 1

7

Sep

17

Oct

17

No

v 1

7

De

c 1

7

Jan

18

Feb

18

Mar

18

Ap

r 1

8

May

18

Jun

18

Jul 1

8

Au

g 1

8

Sep

18

Oct

18

No

v 1

8

De

c 1

8

Jan

19

Feb

19

Mar

19

Ap

r 1

9

May

19

Jun

19

Jul 1

9

Northern Europe US China

Weaker demand in automotive and cautious sentiment at distributors, spot prices decreased, sharp increase in iron

ore price

Summary of Q2/2019Improved earnings for SSAB Americas, decline in SSAB Europe

►EBIT of SEK 1,316m, down SEK 314m vs. Q2/18, and SEK 358m vs. Q1/19+ SSAB Americas’ result improved y-on-y driven by

higher prices

+ SSAB Special Steels’ result improved slightly

- SSAB Europe’s result declined mainly due to higher iron ore costs

►Strong operating cash flow of SEK 1.7bn

►Earnings per share SEK 0.98 (1.27)

SEKm Q2/2019 Q2/2018 Q1/2019 2018

Sales 20,654 19,263 20,017 74,941

EBITDA 2,419 2,582 2,755 8,712

EBIT 1,316 1,630 1,674 4,940

Operating cash flow

1,696 1,325 1,139 5,969

Earnings per share (SEK)

0.98 1.27 1.24 3.45

Gearing %1) 16 20 13 14

Shipments, ktonnes

1,722 1,811 1,744 6,899

Key figures

1) Excluding IFRS 16

Performance by division

Sales and EBITDA marginSEKm

6

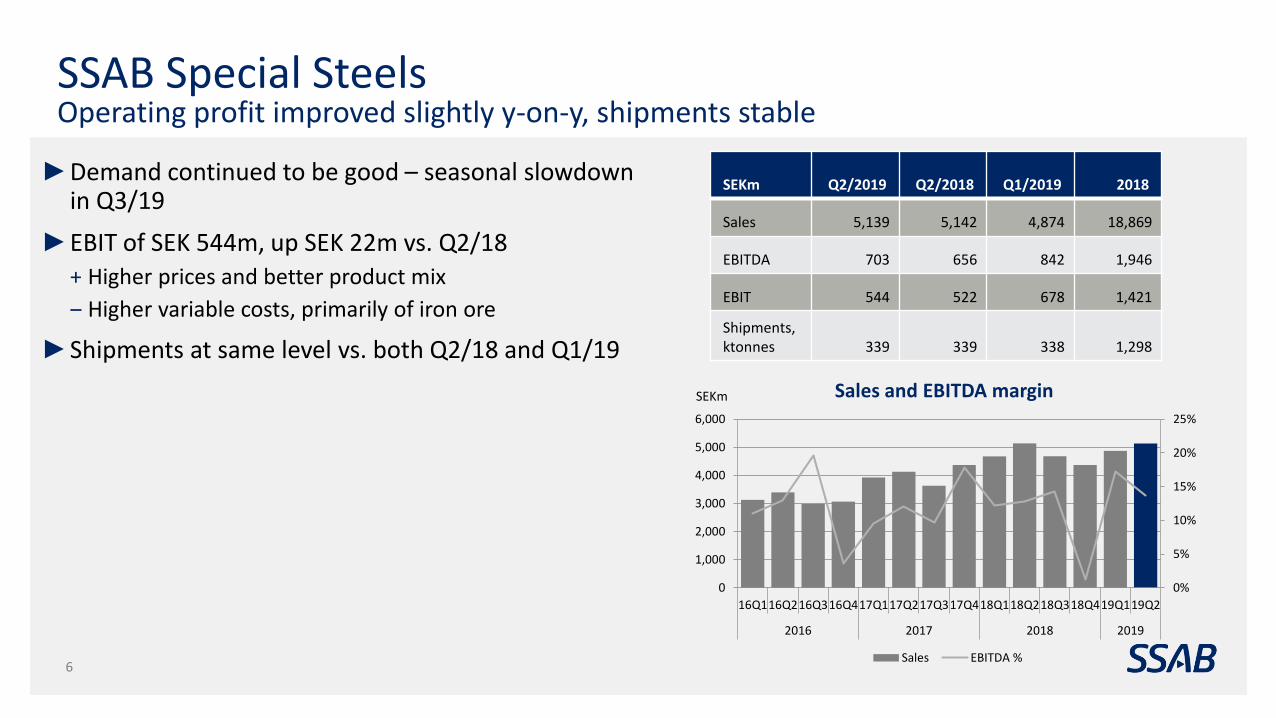

SSAB Special SteelsOperating profit improved slightly y-on-y, shipments stable

►Demand continued to be good – seasonal slowdown in Q3/19

►EBIT of SEK 544m, up SEK 22m vs. Q2/18+ Higher prices and better product mix

‒ Higher variable costs, primarily of iron ore

►Shipments at same level vs. both Q2/18 and Q1/19

SEKm Q2/2019 Q2/2018 Q1/2019 2018

Sales 5,139 5,142 4,874 18,869

EBITDA 703 656 842 1,946

EBIT 544 522 678 1,421

Shipments,ktonnes 339 339 338 1,298

0%

5%

10%

15%

20%

25%

0

1,000

2,000

3,000

4,000

5,000

6,000

16Q116Q216Q316Q417Q117Q217Q317Q418Q118Q218Q318Q419Q119Q2

2016 2017 2018 2019

Sales EBITDA %

SEKm

7

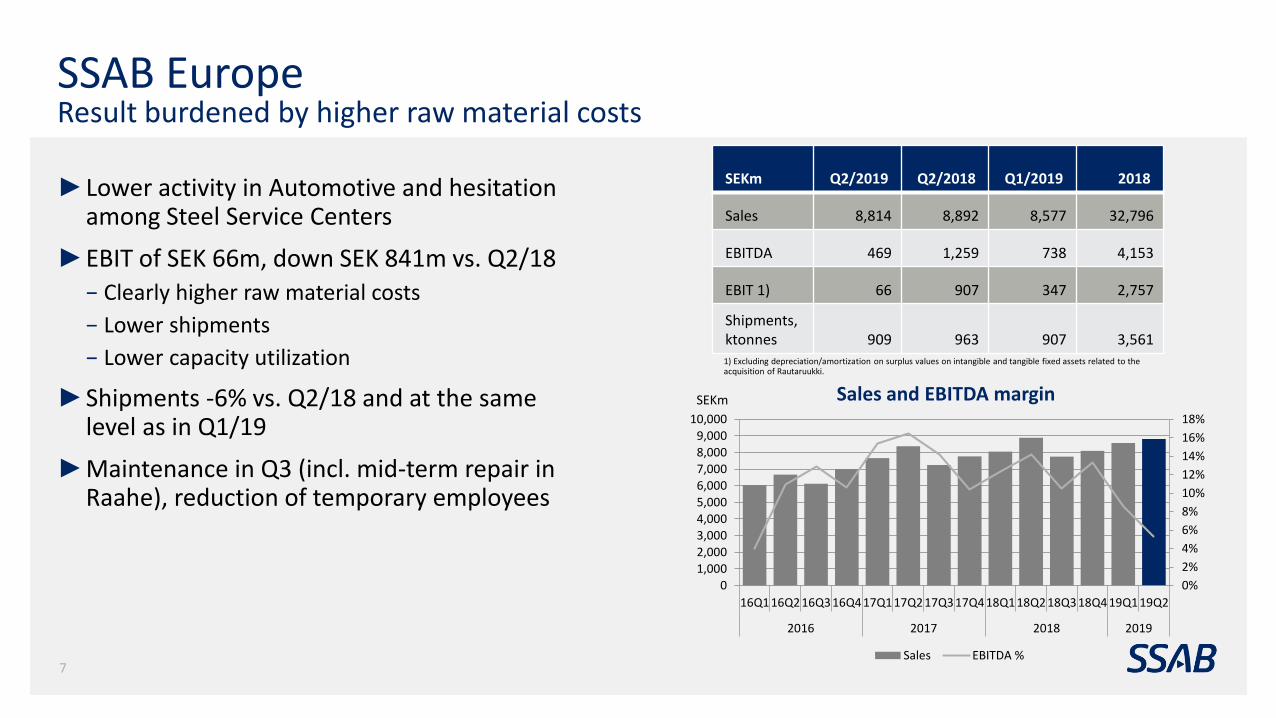

SSAB Europe Result burdened by higher raw material costs

►Lower activity in Automotive and hesitation among Steel Service Centers

►EBIT of SEK 66m, down SEK 841m vs. Q2/18− Clearly higher raw material costs

− Lower shipments

− Lower capacity utilization

►Shipments -6% vs. Q2/18 and at the same level as in Q1/19

►Maintenance in Q3 (incl. mid-term repair in Raahe), reduction of temporary employees

Sales and EBITDA margin

SEKm Q2/2019 Q2/2018 Q1/2019 2018

Sales 8,814 8,892 8,577 32,796

EBITDA 469 1,259 738 4,153

EBIT 1) 66 907 347 2,757

Shipments,ktonnes 909 963 907 3,5611) Excluding depreciation/amortization on surplus values on intangible and tangible fixed assets related to the acquisition of Rautaruukki.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

16Q1 16Q2 16Q3 16Q4 17Q1 17Q2 17Q3 17Q4 18Q1 18Q2 18Q3 18Q4 19Q1 19Q2

2016 2017 2018 2019

Sales EBITDA %

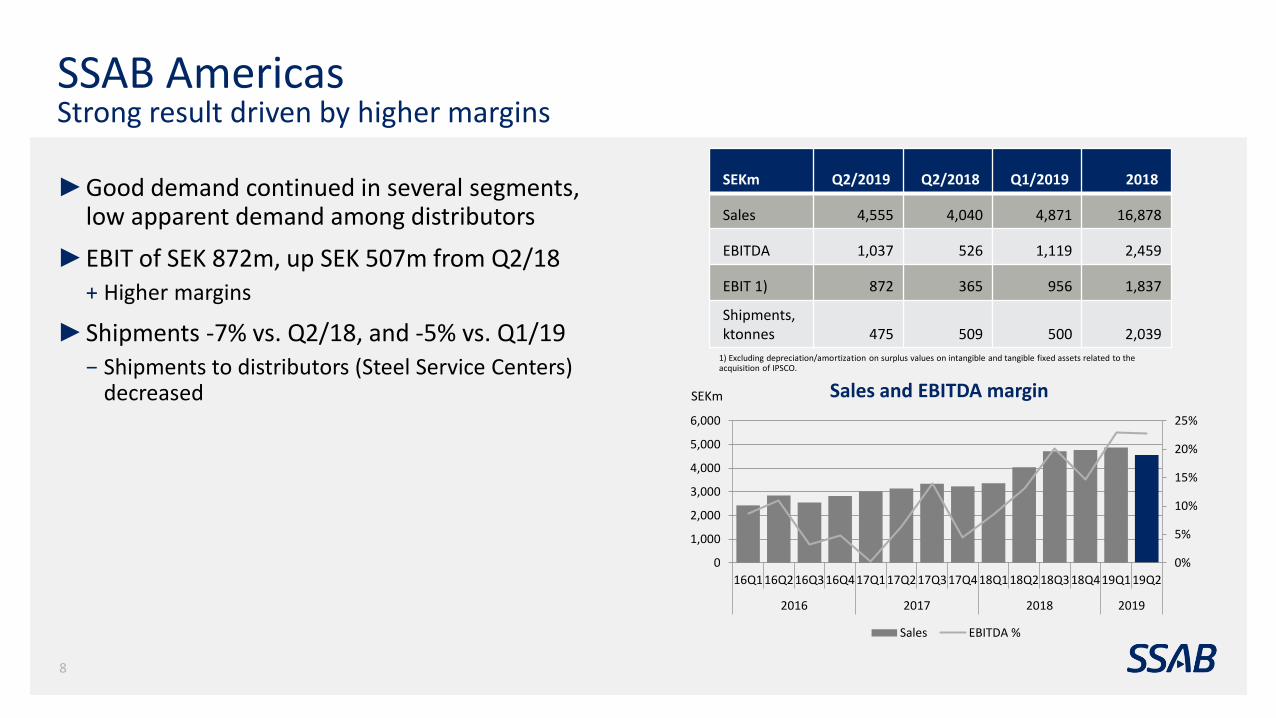

SSAB AmericasStrong result driven by higher margins

►Good demand continued in several segments, low apparent demand among distributors

►EBIT of SEK 872m, up SEK 507m from Q2/18+ Higher margins

►Shipments -7% vs. Q2/18, and -5% vs. Q1/19− Shipments to distributors (Steel Service Centers)

decreased SEKm Sales and EBITDA margin

SEKm Q2/2019 Q2/2018 Q1/2019 2018

Sales 4,555 4,040 4,871 16,878

EBITDA 1,037 526 1,119 2,459

EBIT 1) 872 365 956 1,837

Shipments,ktonnes 475 509 500 2,039

1) Excluding depreciation/amortization on surplus values on intangible and tangible fixed assets related to the acquisition of IPSCO.

0%

5%

10%

15%

20%

25%

0

1,000

2,000

3,000

4,000

5,000

6,000

16Q1 16Q216Q316Q417Q1 17Q217Q3 17Q418Q118Q218Q3 18Q419Q1 19Q2

2016 2017 2018 2019

Sales EBITDA %

8

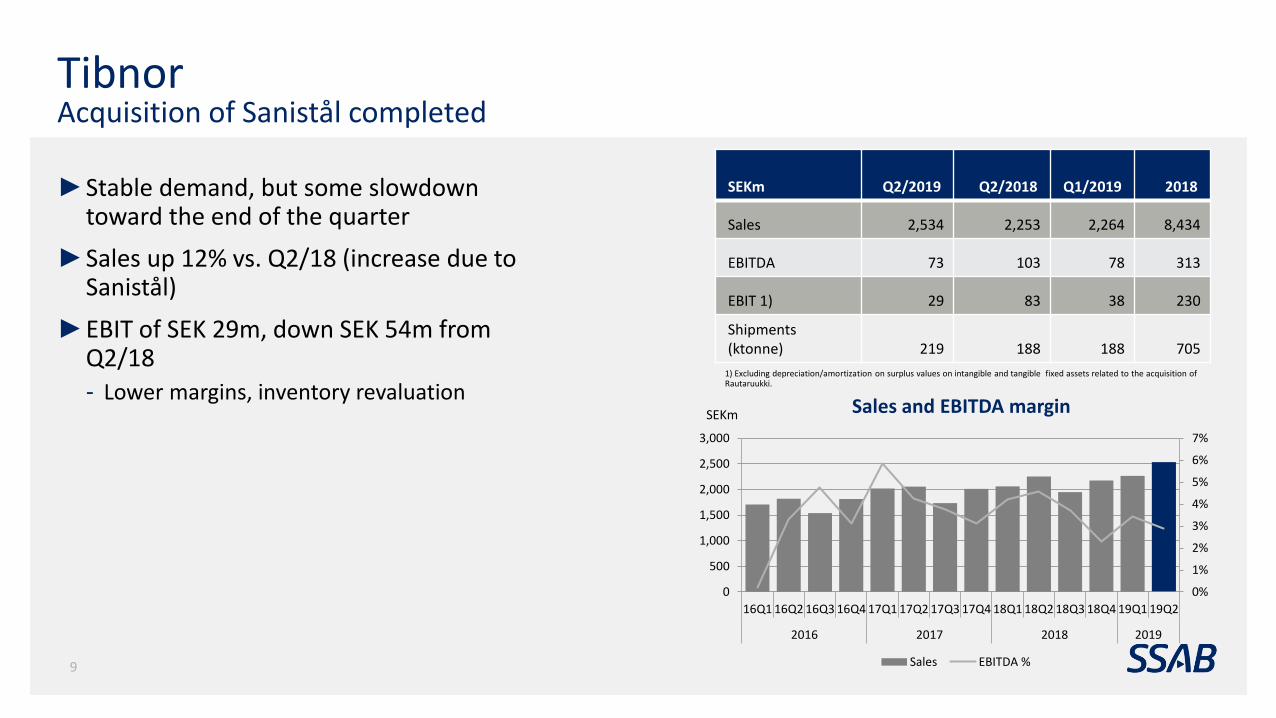

TibnorAcquisition of Sanistål completed

►Stable demand, but some slowdown toward the end of the quarter

►Sales up 12% vs. Q2/18 (increase due to Sanistål)

►EBIT of SEK 29m, down SEK 54m from Q2/18- Lower margins, inventory revaluation

9

SEKm Sales and EBITDA margin

SEKm Q2/2019 Q2/2018 Q1/2019 2018

Sales 2,534 2,253 2,264 8,434

EBITDA 73 103 78 313

EBIT 1) 29 83 38 230

Shipments(ktonne) 219 188 188 705

1) Excluding depreciation/amortization on surplus values on intangible and tangible fixed assets related to the acquisition of Rautaruukki.

0%

1%

2%

3%

4%

5%

6%

7%

0

500

1,000

1,500

2,000

2,500

3,000

16Q1 16Q2 16Q3 16Q4 17Q1 17Q2 17Q3 17Q4 18Q1 18Q2 18Q3 18Q4 19Q1 19Q2

2016 2017 2018 2019

Sales EBITDA %

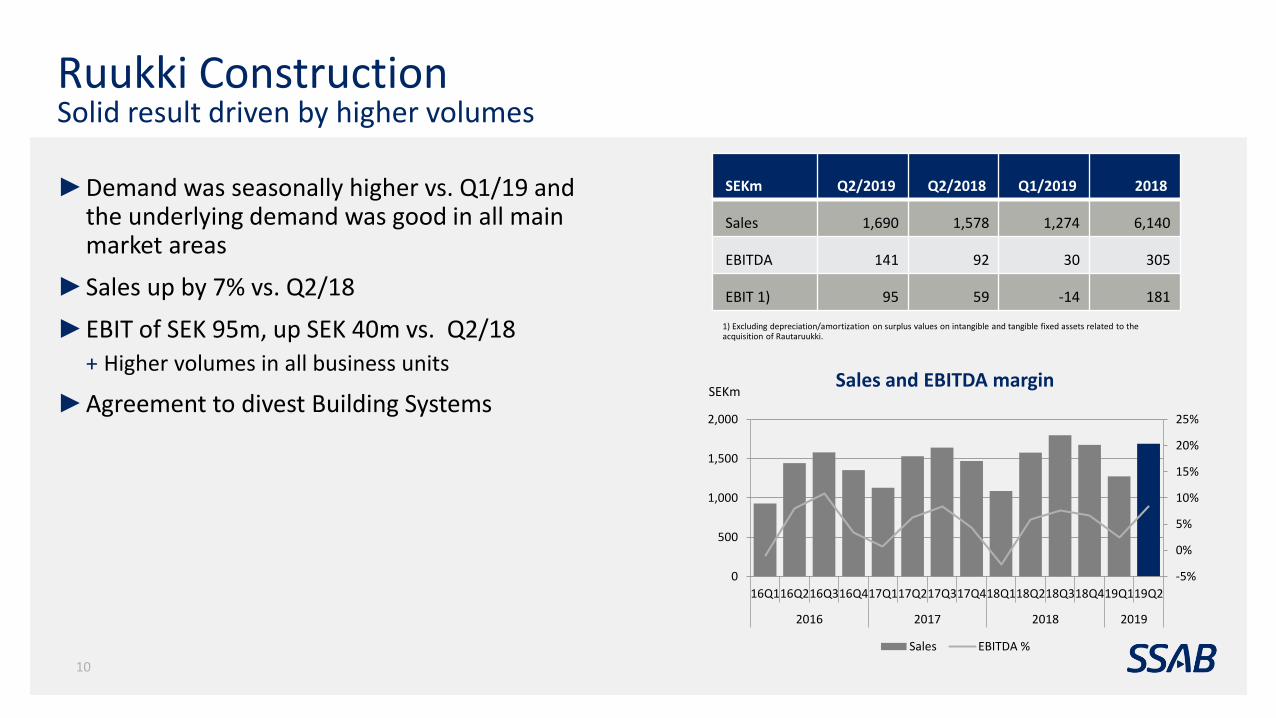

Ruukki ConstructionSolid result driven by higher volumes

►Demand was seasonally higher vs. Q1/19 and the underlying demand was good in all main market areas

►Sales up by 7% vs. Q2/18

►EBIT of SEK 95m, up SEK 40m vs. Q2/18 + Higher volumes in all business units

►Agreement to divest Building Systems

10

SEKmSales and EBITDA margin

SEKm Q2/2019 Q2/2018 Q1/2019 2018

Sales 1,690 1,578 1,274 6,140

EBITDA 141 92 30 305

EBIT 1) 95 59 -14 181

1) Excluding depreciation/amortization on surplus values on intangible and tangible fixed assets related to the acquisition of Rautaruukki.

-5%

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

16Q116Q216Q316Q417Q117Q217Q317Q418Q118Q218Q318Q419Q119Q2

2016 2017 2018 2019

Sales EBITDA %

Financials

Slightly weaker trend in Group earnings

12

Sales

EBITDA and EBITDA margin2

Shipments1

EBITDA per tonne delivered steel2

1) Including the steel operations: Special Steels, Europe and Americas

2) Excluding items affecting comparability

0

5,000

10,000

15,000

20,000

25,000

16Q1 16Q2 16Q3 16Q4 17Q1 17Q2 17Q3 17Q4 18Q1 18Q2 18Q3 18Q4 19Q1 19Q2

2016 2017 2018 2019

SEK

mill

ion

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

16Q1 16Q2 16Q3 16Q4 17Q1 17Q2 17Q3 17Q4 18Q1 18Q2 18Q3 18Q4 19Q1 19Q2

2016 2017 2018 2019

kto

ns

0%

2%

4%

6%

8%

10%

12%

14%

0

500

1,000

1,500

2,000

2,500

3,000

16Q1 16Q2 16Q3 16Q4 17Q1 17Q2 17Q3 17Q4 18Q1 18Q2 18Q3 18Q4 19Q1 19Q2

2016 2017 2018 2019

SEK

mill

ion

EBITDA EBITDA %

0

200

400

600

800

1000

1200

1400

1600

1800

16Q1 16Q2 16Q3 16Q4 17Q1 17Q2 17Q3 17Q4 18Q1 18Q2 18Q3 18Q4 19Q1 19Q2

2016 2017 2018 2019

SEK

/to

nn

e

Change in operating profit Q2/2019 vs. Q2/2018

SEKm

Note: Excluding items affecting comparability

620

80

Volume2018 Q2 Price Var COGS

-220

-365

Fixed cost

-390

FX

-39

Other 2019 Q2

1 630

1 316

13

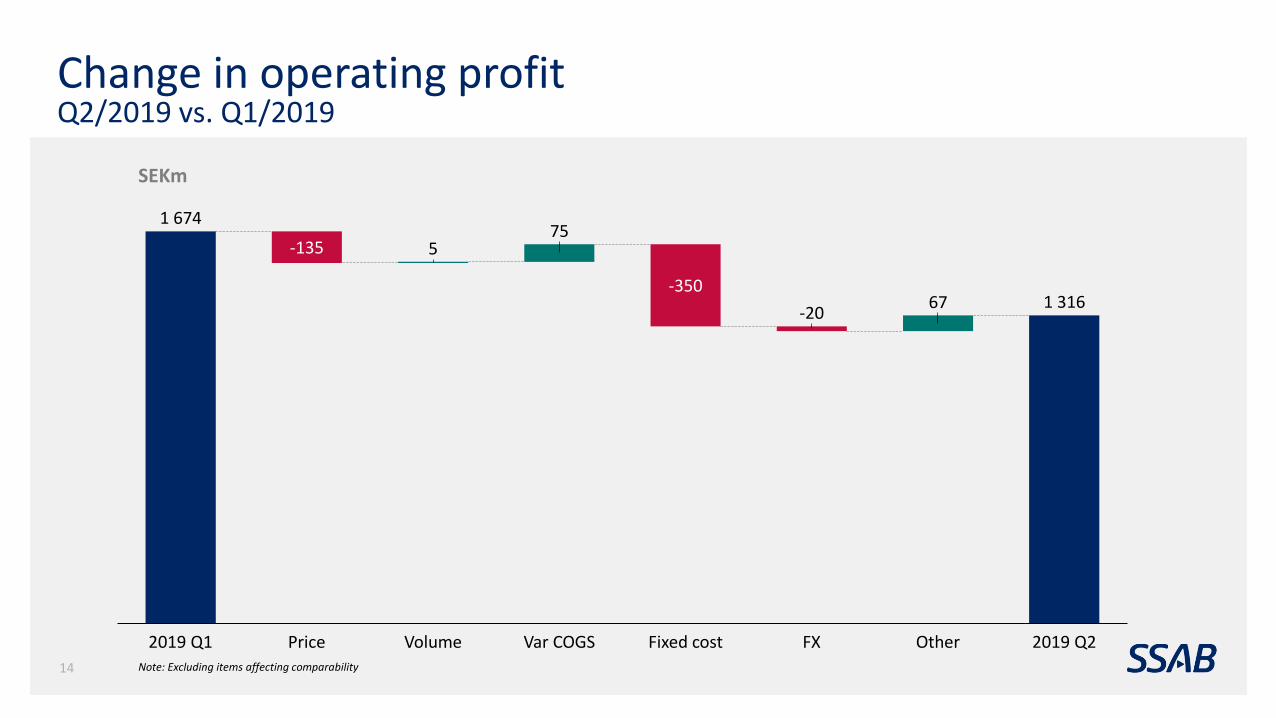

Change in operating profit Q2/2019 vs. Q1/2019

SEKm

Note: Excluding items affecting comparability

575

67

-135

2019 Q1 Var COGSPrice Volume

-350

Fixed cost

1 674

-20

FX Other 2019 Q2

1 316

14

Operating cash flow at good levelNet cash flow impacted by dividend payout and Sanistål acquisition

SEKm Q2/2019 Q2/2018 Q1/2019 2018

Operating profit before depreciation/amortization 2,419 2,582 2,755 8,712

Change in working capital -240 -805 -1,256 -967

Maintenance expenditure -401 -417 -352 -1,943

Other -82 -34 -9 167

Operating cash flow 1,696 1,325 1,139 5,969

Financial items -150 -235 -93 -541

Taxes -702 -105 -254 -628

Cash flow from current operations 845 986 791 4,800

Strategic capital expenditure in plant and machinery -231 -90 -113 -397

Acquisitions of shares and operations -595 - -175 -11

Divestments of shares and operations - - - 76

Cash flow before dividend 19 896 503 4,468

Dividend paid to shareholders -1,545 -1,030 - -1,030

Dividend, non-controlling interest -6 -2 - -3

Acquisition, non-controlling interest -45 - - -

Net cash flow -1,577 -136 503 3,435

0

2000

4000

6000

8000

10000

12000

Cash andback-upfacilities

2019 2020 2021 2022 2023 2024+

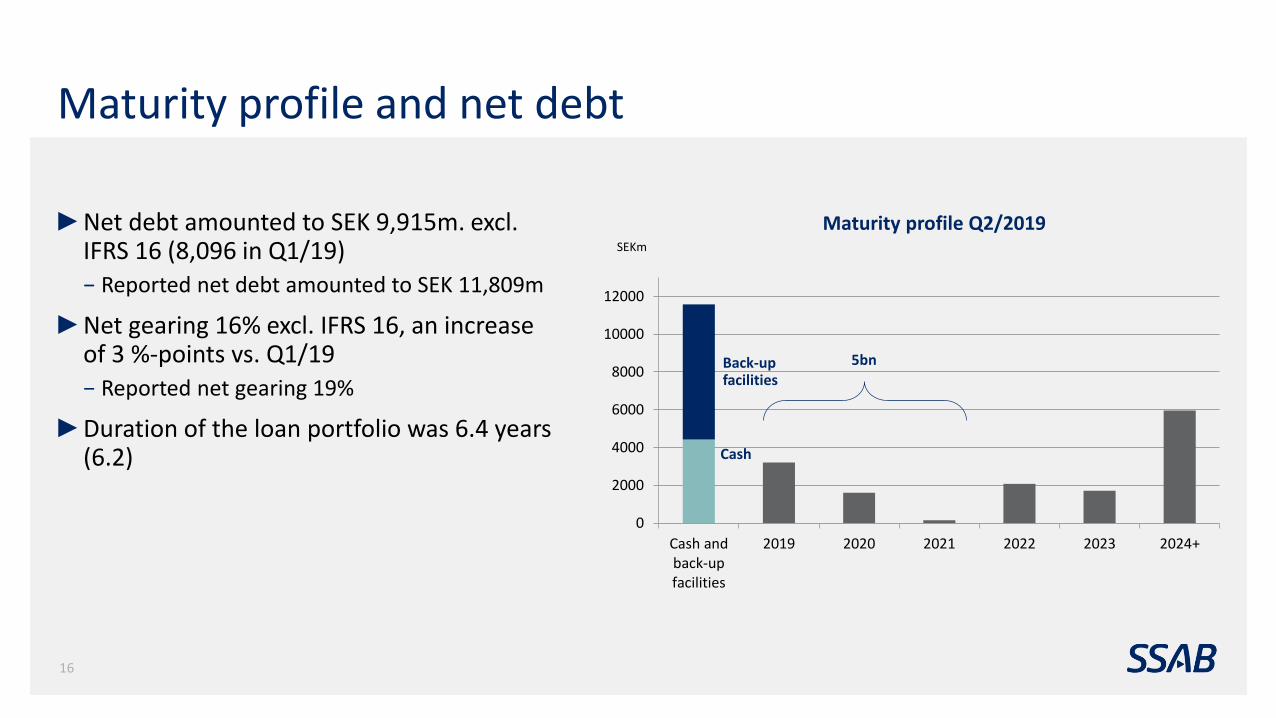

Maturity profile and net debt

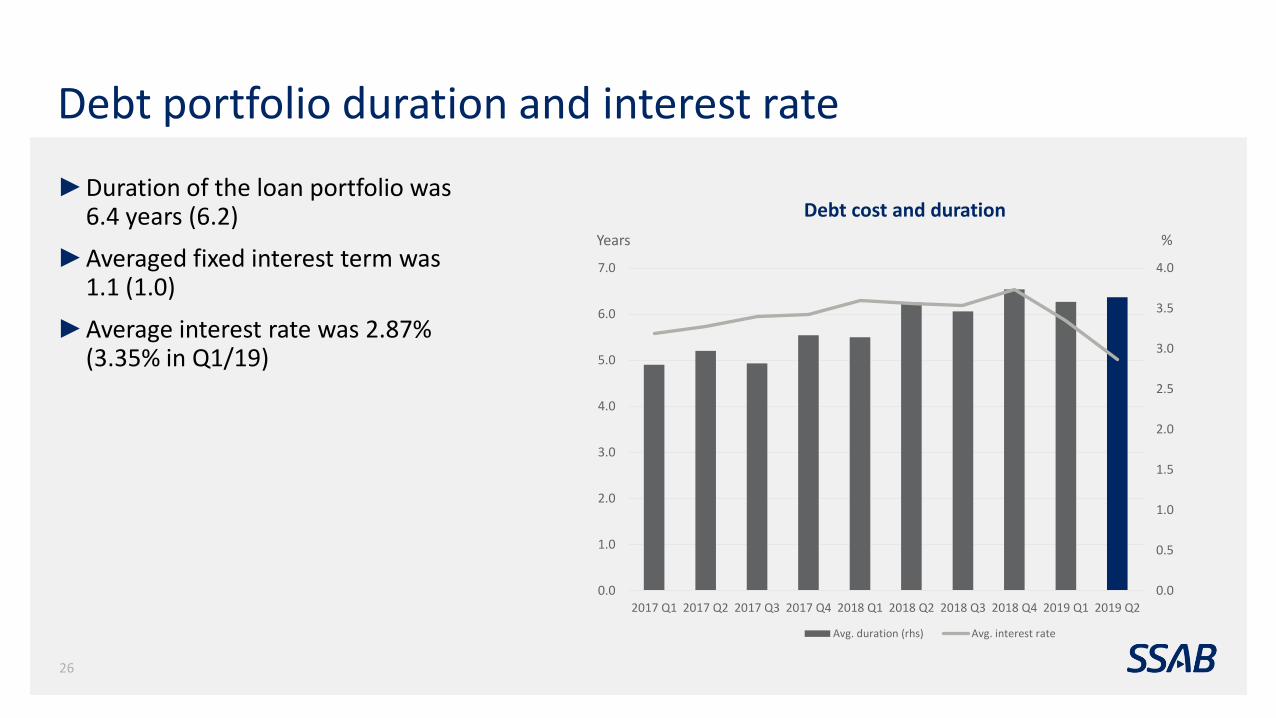

►Net debt amounted to SEK 9,915m. excl. IFRS 16 (8,096 in Q1/19)− Reported net debt amounted to SEK 11,809m

►Net gearing 16% excl. IFRS 16, an increase of 3 %-points vs. Q1/19− Reported net gearing 19%

►Duration of the loan portfolio was 6.4 years (6.2)

SEKm

Maturity profile Q2/2019

5bn

Cash

Back-upfacilities

16

Purchase prices for iron ore rose sharplyThe main impact will be in Q3/19

►Average coking coal purchase price in Q2/19 was 9% lower in terms of SEK (-11% in USD) vs. Q1/19

Coking coal

Iron ore

► Average pellet purchase price in Q2/19 was 18% higher in terms of SEK (14% in USD) vs. Q1/19

► Higher purchase prices in Q2 will mostly affect the result of Q3 2019

SSAB’s purchase price, coking coal and iron ore

Indexed

50

100

150

200

250

300

350

Q12016

Q22016

Q32016

Q42016

Q12017

Q22017

Q32017

Q42017

Q12018

Q22018

Q32018

Q42018

Q12019

Q22019

Coal ( SSAB purchase price, index) Iron ore (SSAB purchase price, index)

17

Scrap spot prices continued to decrease in Q2

►SSAB’s average purchase price for scrap was 10% lower in Q2/19 vs. Q1/19 (USD)

Scrap spot priceUSD/gross ton

Q2

Source: AMM

0

50

100

150

200

250

300

350

400

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6M

ay-1

6Ju

n-1

6Ju

l-1

6A

ug-

16

Sep

-16

Oct

-16

No

v-1

6D

ec-

16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7M

ay-1

7Ju

n-1

7Ju

l-1

7A

ug-

17

Sep

-17

Oct

-17

No

v-1

7D

ec-

17

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8M

ay-1

8Ju

n-1

8Ju

l-1

8A

ug

18

Sep

18

Oct

18

No

v 2

01

8D

ec

20

18

Jan

19

Feb

19

Mar

19

Ap

r 1

9M

ay 1

9Ju

n 1

9Ju

l 19

Chicago #1HM Scrap (AMM) [USD/gross ton]

18

Outlook and summary

Outlook for Q1 for SSAB’s key customer segments

Segment Q3/2019 Comments

Heavy Transport Some reduction in European heavy truck production, from high level

Good activity in the US – rail cars and barges

Automotive Weak demand in main markets

Structural growth in AHSS

Construction Machinery Lower momentum, but still at good level

Material Handling High activity in Mining in several regions – both maintenance and new equipment

Energy Solid demand in wind energy

High activity in US oil and gas segment

Construction Good underlying demand level

Some uncertainty in residential market in Scandinavia

Service Centers Very cautious in US during Q2, potential restocking end of Q3

Hesitation in Europe20

WeakHealthyStrong

SSAB’s outlook for main customer segments Q3/2019

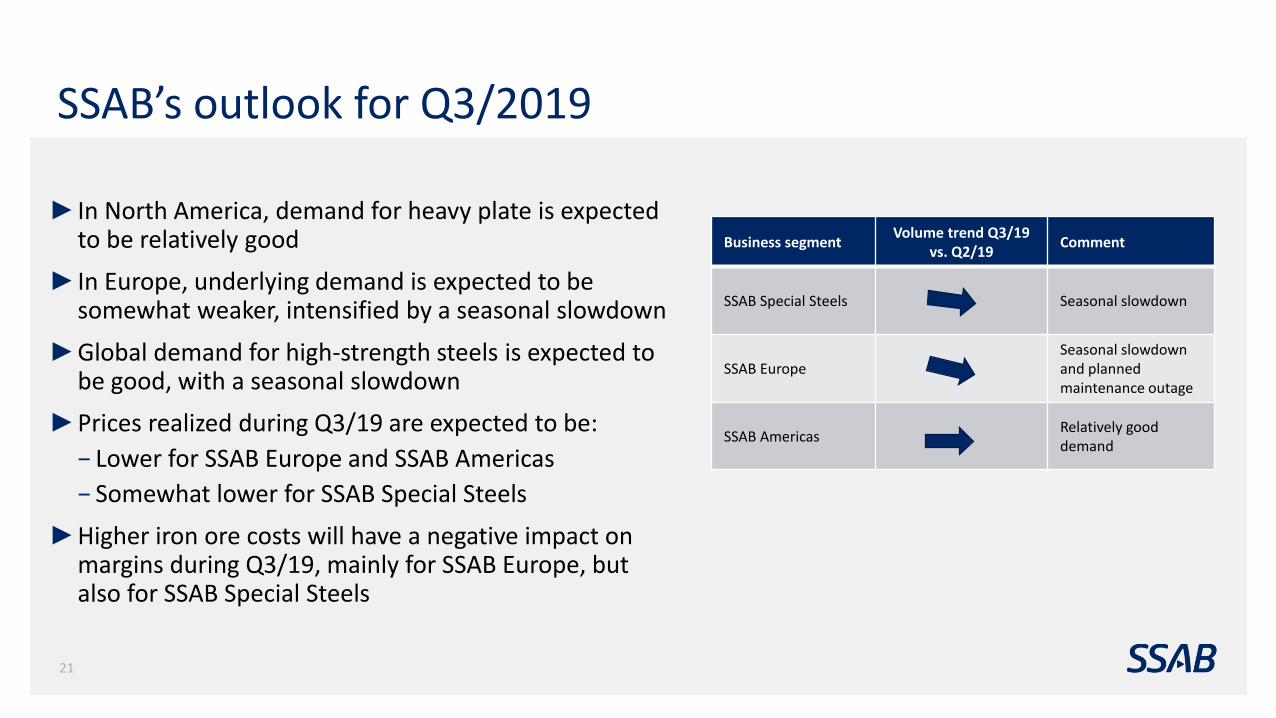

SSAB’s outlook for Q3/2019

Business segmentVolume trend Q3/19

vs. Q2/19Comment

SSAB Special Steels Seasonal slowdown

SSAB EuropeSeasonal slowdown and planned maintenance outage

SSAB AmericasRelatively good demand

► In North America, demand for heavy plate is expected to be relatively good

► In Europe, underlying demand is expected to be somewhat weaker, intensified by a seasonal slowdown

►Global demand for high-strength steels is expected to be good, with a seasonal slowdown

►Prices realized during Q3/19 are expected to be:

− Lower for SSAB Europe and SSAB Americas

− Somewhat lower for SSAB Special Steels

►Higher iron ore costs will have a negative impact on margins during Q3/19, mainly for SSAB Europe, but also for SSAB Special Steels

21

Summary

►Major result improvement from SSAB Americas

►SSAB Europe’s result dropped mainly due to iron ore

►Flexibility measures − Reduction of temporary employees

− Smaller BF in Oxelösund will be idled

− Execute planned cost reductions in all divisions

►Strong balance sheet – regardless of business cycle

22

Questions & Answers

Appendix

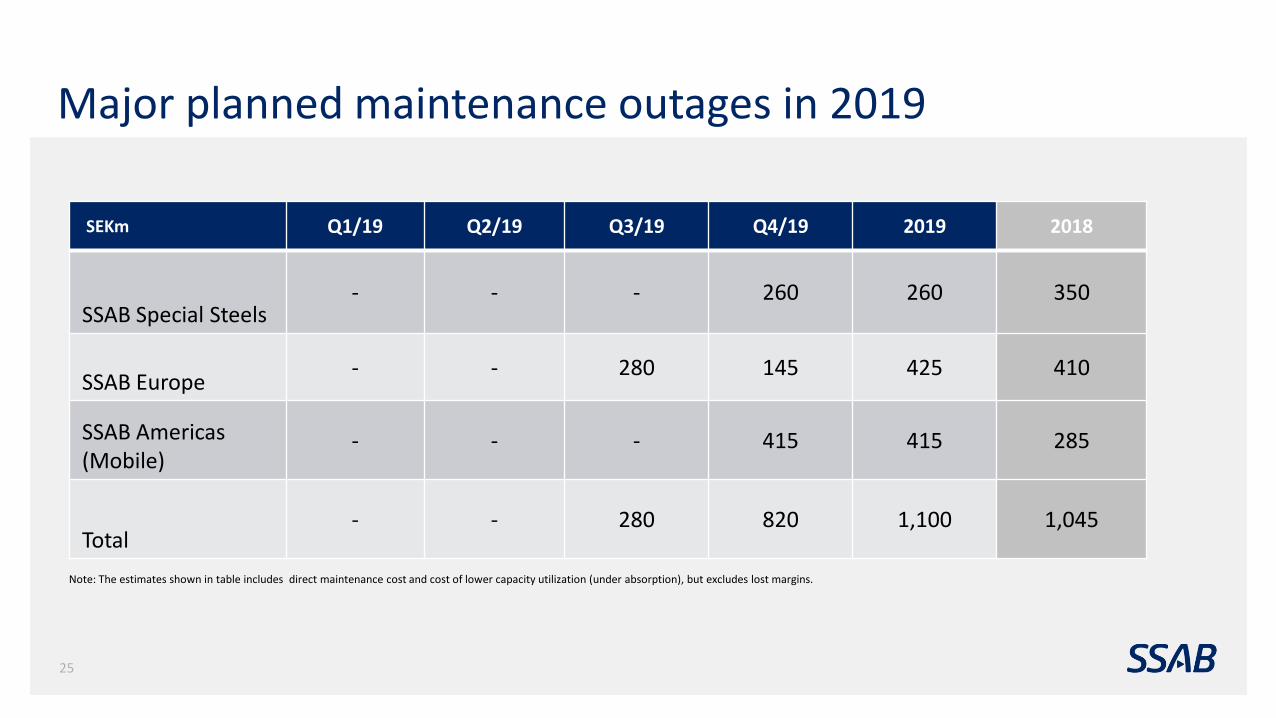

Major planned maintenance outages in 2019

SEKm Q1/19 Q2/19 Q3/19 Q4/19 2019 2018

SSAB Special Steels- - - 260 260 350

SSAB Europe - - 280 145 425 410

SSAB Americas (Mobile)

- - - 415 415 285

Total - - 280 820 1,100 1,045

Note: The estimates shown in table includes direct maintenance cost and cost of lower capacity utilization (under absorption), but excludes lost margins.

25

Debt cost and duration

%

Debt portfolio duration and interest rate

►Duration of the loan portfolio was 6.4 years (6.2)

►Averaged fixed interest term was 1.1 (1.0)

►Average interest rate was 2.87% (3.35% in Q1/19)

Years

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2017 Q1 2017 Q2 2017 Q3 2017 Q4 2018 Q1 2018 Q2 2018 Q3 2018 Q4 2019 Q1 2019 Q2

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Avg. duration (rhs) Avg. interest rate

26