Presentation of D/S NORDEN in rates and tonnage prices; ... – Mainly Handymax focus: Coal, iron...

17

1 DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com Presentation of D/S NORDEN Copenhagen, April 2006

Transcript of Presentation of D/S NORDEN in rates and tonnage prices; ... – Mainly Handymax focus: Coal, iron...

1DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Presentation of D/S NORDEN

Copenhagen, April 2006

2DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

FORWARD-LOOKING STATEMENTS

This presentation contains certain forward-looking statements reflecting the

management’s present judgment of future events and financial results.

Statements relating to 2006 and subsequent years are subject to uncertainty,

and “NORDEN”s actual results may therefore differ from the projections.

Factors that may cause such variance include, but are not limited to, changes in

macro-economic and political conditions, particularly in the Company’s principal

markets; changes to the Company’s rate assumptions and operating costs;

volatility in rates and tonnage prices; regulatory changes; any disruptions to

traffic and operations as a result of external events, etc.

The presentation should not be interpreted as a recommendation to trade

shares in Dampskibsselskabet NORDEN A/S.

3DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

TODAY’S AGENDA

Overview

Operating model

Dry Cargo

Tanker

2006 Headlines

Q&A Session

This presentation can be found on www.ds-norden.com

4DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

NORDEN in Brief

2005 revenue: USD 1.3 bn75% drycargo earnings, but tank share growing

– Mainly Handymax focus: Coal, iron ore, cement etc.

– Mainly oil product focus – with some crude exposure

124 vessels trading with 50 for delivery– 110 in Drycargo (+35)

– 14 in Tank (+15)

Growth supported by high coverage– Extensive risk management focus

– Customer partnerships

TankUSD 124 mill.

A fully integrated global operator within drycargo and tank

BulkUSD 1.2 bn.

2005 EBITDA: USD 216 mill.*

TankUSD 57 mill.

BulkUSD 165 mill.

Expected net result 2006: USD 110-130 mill.

Current market cap: USD 1 bn*Note: Includes USD 6 mill. in unallocated costs

OVERVIEW

5DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Operating model

Owned (7)

Chartered w. POP (17)

Short term chartered

(86)

Flexible fleet Coverage & customer focus

Contracts of Affreightment

TC out

FFA market

FlexibilityAdds scaleArbitrage opportunities

*Note: Figures indicate drycargo fleet as of end 2005. POP= Purchase option

Asset playTechnical competences in-house

Option based flexibility5-7 year firm periods

Quick and easy cover

Customer relationsLogistical efficiencies

2-5 year firm periods

Total capacity* Coverage

Spot market

The right people make it all work

OVERVIEW

6DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Customer Focused Organisation

Annapolis

Rio de Janeiro

Shanghai

Mumbai

Singapore

Copenhagen

SPOT MARKET

Fulfil individual customer needs on day-to-day basis by fast, reliable and cost efficient transportation.

Market approach

CORE CUSTOMERS

Develop long lasting relationships by constantly adapting to meet customers’ needs and requirements.

KEY PARTNERS

Add value to our partners’ business through exchange of knowledge and share risks and rewards

Core Values: Reliability, Flexibility and Empathy

OVERVIEW

7DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

NORDEN Drycargo Overview

0

200

400

600

800

1000

1200

1400

2001 2002 2003 2004 2005

USDm

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Margin

Revenue

EBITDA margin

Revenue and EBITDA margin

1172

Fleet data Q4-04 Q4-05Own 2 7Long term TC with POPs 21 17Total active core fleet 23 24

Other 84 86Total active 107 110

Gross for delivery 27 35

Gross fleet 134 145

Financials 2004 2005 GrowthRevenues 1.062 1.172 10%Costs 864 1.007 17%EBITDA 198 165 -17%

Depreciations 1 6 304%Vessel sales & J/Vs 37 80 114%Operating profit 234 239 2%

14%

DRY CARGO

8DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

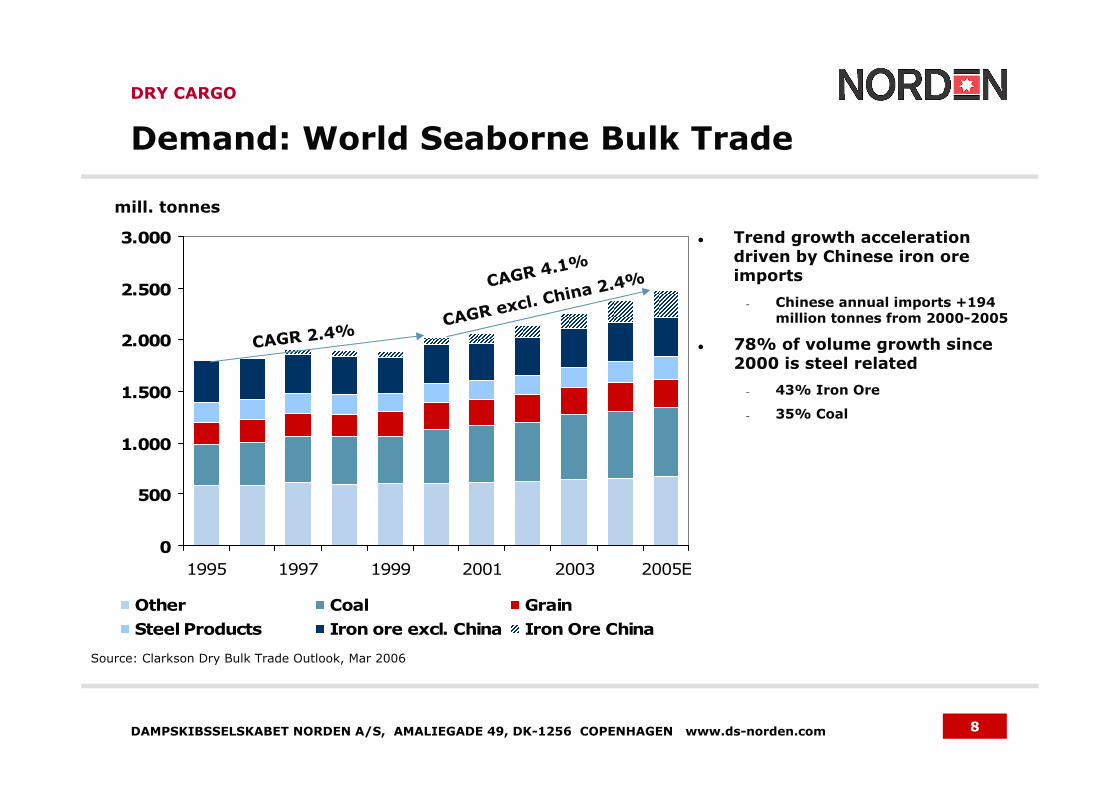

Demand: World Seaborne Bulk Trade

Trend growth acceleration driven by Chinese iron oreimports

– Chinese annual imports +194 million tonnes from 2000-2005

78% of volume growth since2000 is steel related

– 43% Iron Ore

– 35% Coal

0

500

1.000

1.500

2.000

2.500

3.000

1995 1997 1999 2001 2003 2005E

Other Coal GrainSteel Products Iron ore excl. China Iron Ore China

CAGR 2.4%

CAGR 4.1%

CAGR excl. China 2.4%

mill. tonnes

Source: Clarkson Dry Bulk Trade Outlook, Mar 2006

DRY CARGO

9DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Demand: Vast Long Term Potential Remains

419469

629

985

1.163

0

200

400

600

800

1.000

1.200

1.400

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Tai

wan

S. K

orea

Japan

Germ

any

USA

230

84

Consumption of crude steel per capita

China

During economic development, steel

consumption usually peaks at high level before falling back to long-term level of

350-400 kg/capita

Kg/capita

Source: International Iron and Steel Institute, Steel Statistics 2005

All things being equal, a doubling to 460kg/capita means iron ore imports have to increase by 210 mill. tonnes per year

DRY CARGO

10DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Supply: Factors Mitigating Fleet Growth

Share of vessels >20 years old exceedorderbook

Scrapping currentlyat historical low

Congestion back to low levels but remainpotential future swing factor

61%

22% 24%

15%

28%

7%

18%22% 22%

18%

0%

10%

20%

30%

40%

50%

60%

70%

Handysize Handymax Panamax Capesize Totaldrycargo

+20 years Orderbook

Orderbook and 20+ year old vessels in pct. of current fleet (dwt)

Source: Clarkson Dry Bulk Trade Outlook, mar 2006

DRY CARGO

11DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

DRY CARGO MARKET IS NORMALISING

DRY CARGO

Baltic Dry Index 2004 & 2005/06 YTD

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

Jan

Fe

b

Ma

r

2004

2004 avg.

2005 avg.

2005/06

Super-cycle ended in 2005

Demand growth more than halved to 4%

– Chinese iron-ore import growth moderated

– Lower demand growth for coal

– Growth still strong in historical perspective

Some 5% increase in global fleet

Prices of 2nd hand and new-buildings down from historical highs in Q1 2005

Outlook for 2006

Rates below 2005 but still above historical average

– Supply growth of 6-7%

– Demand growth of 3,5-4,5%

Ship values expected to remain firm

BDI avg.-25%

12DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

NORDEN Tanker Overview

0

20

40

60

80

100

120

140

2001 2002 2003 2004 2005

USDm

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

MarginRevenue

EBITDA margin

Revenue and EBITDA margin

125

46%

Financials 2004 2005 GrowthRevenues 105 125 19%Costs 63 67 7%EBITDA 42 57 37%

Depreciations 11 9 -18%Vessel sales & J/Vs 13 49 284%Operating profit 43 97 122%

Fleet data Q4-04 Q4-05Own 5 3Long term TC with POPs 3 3Total active core fleet 8 6

Other 8 8Total active 16 14

Gross for delivery 9 15

Gross fleet 25 29

TANKER

13DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Tank Operations: Product Tankers

Singapore

Copenhagen

Handysize MR

NORDEN product tankers operated in Norient Product Pool

– 15 vessels trading in pool

– Primarily in spot market

– 35-40% period cover

Petrol, diesel, jet fuel, naphta

Customers: Oil traders and major oil companies

Flexible trading areas

Main trading areas:

Aim to become one of the 3 largest product tanker pools by 2007

TANKER

14DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Strong Market in 2005

Market up 7% on average

Strong Q4 due to hurricanes

Structural factors outweighed tough supply/demand balance

– supply +7.3%; oil demand +1.3%

– new refinery capacity built far from consuming areas

– huge impact of disruptions due to tight balance in market

Market outlook for 2006

Rates marginally below 2005-avg

Unexpected events may again shift supply/demand balance

TANKER

Baltic Clean Tanker Index 2004 & 2005/06 YTD

0

500

1.000

1.500

2.000

2.500

Jan Mar May Jul Sep Nov Jan Mar

2004 2005 2006 2004 avg 2005 avg

20042005/06

BCTI avg.+7%

15DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Value of Fleet

51Chartered vessels without POPs

20052004

49

159

36

25

10

123

92

24

7

9Vessels to be delivered:New-buildings (own)

174Total gross fleet

56Hereof with POPs

* POPs = Purchase options

50Total to be delivered

36Chartered vessels with POPs

124Total active vessels

94Chartered vessels without POPs

20Chartered vessels with POPs

10Active fleet:Owned vessels

Fleet

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

2002 2003 2004 2005

TCs with POPsNet Asset Value per shareShare price (year end)

On balance

Off balance

Total theoretical NAV DKK 4,059 per share

FLEET

16DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Well-Positioned for Continued Profitable Growth

Fleet quality and flexibility

– Competitive and “deep” tonnage book

– Option based model

People & systems

– Risk management

– Strong focus on ”software” quality

Strong market position

– Well-known brand with longreputation for quality and reliability

– Leading positions in Handymax and Panamax, and establishing one in product tank

Continued healthy growth in demand supports rates

– Global GDP growth expectations above 4% for 2006

– Vast potential remains in China

– Tonne-mile factor adds to tonnage demand growth in both drycargo and tank

Mitigating factors to large orderbook

– Scrapping is at historical low

– In drycargo, vessels above 20 years outweigh total current orderbook

Scalable business model Attractive market fundamentals

17DAMPSKIBSSELSKABET NORDEN A/S, AMALIEGADE 49, DK-1256 COPENHAGEN www.ds-norden.com

Questions and answers

This presentation can be found on www.ds-norden.com