Presentation I.F

24

(Jon Faust, John H. Rogers, Shing-Yi B. Wang and Jonathan H. Wright) PRESENTED BY: M. HAROON RASHEED AWAN MUHAMMAD W AQAR AKHTER

-

Upload

wicky-akhtar -

Category

Documents

-

view

221 -

download

0

Transcript of Presentation I.F

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 1/24

(Jon Faust, John H. Rogers, Shing-Yi B. Wang and

Jonathan H. Wright)

PRESENTED BY:

M. HAROON RASHEED AWAN

MUHAMMAD WAQAR AKHTER

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 2/24

This paper Study the effect of unexpected macroeconomicannouncement on

1. U.S exchange Rate in terms of D/M Euro and Pounds.

2. U.S., Euro & D.M interest rates of Various Maturities Securities.

Studied 20 minutes movement in term structure and exchange rate in

order to examine the effects of Ten macroeconomic announcementseffects.

Time span of the study comprises from 1987 to 2002.

Contribution To literature:

The contribution of the work is two folds, firstly most of Previous Work on thefield has only considered effect only on a single asset or Asset Class while on the otherhand the author used a much longer time span than used in other Papers, which alsoincluded two N.B.E.R recessions hence results are much more dependable & accurate.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 3/24

AUTHOR YEAR FINDINGS

Schwert 1981 The stock market reacts negatively to the

announcement of unexpected inflation in the

Consumer Price Index (C.P.I.), although the

magnitude of the reaction is small

Edwards 1982 “New information" plays an important role in

explaining the market forecasting error, or

difference between the spot rate and the forward

rate, determined in the previous period

Frankel and Engel 1984 Exchange Rate Fluctuation in response of

money supply announcement is due to

perception that Feds are tighten or relaxing the

money supply.

Ito & Roley 1987 Over the entire sample period, news concerning

the U.S. money stock had the only significant

effects.

Hardouvelis 1988 An increase (decrease) in interest rates is

accompanied by an appreciation (depreciation)

of the dollar

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 4/24

Culter et al. 1989 when information can be identified and that

the tone (i.e., positive versus negative) of

this information can be determined, there is

a much closer link between stock pricesand information.

McQueen & Roley 1993 When the economy is strong the stock market

responds negatively to news about bigger real

economic activity. This negative relation is

caused by the larger increase in discount rates

relative to expected cash flows.

Fleming and

Remolona

1997 The bond market's response to

announcements in general is consistent with

the way we would expect it to react to new

information.

Fair 2003 Macro announcements led to large and rapid

price changes in a stock future, a bond future,and exchange rate futures.

Anderson,

Bollerslev, Diebold

and Vega’s

2003 A greater than expected U.S retail sales

revalue the dollar exchange rate.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 5/24

15 Years

Time Series

Exchange rates are multiplied by 1000 to in order to

explain results in basis points. Surprise=Actual outcome – MMS Survey (Money

Market Services)

Model:

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 6/24

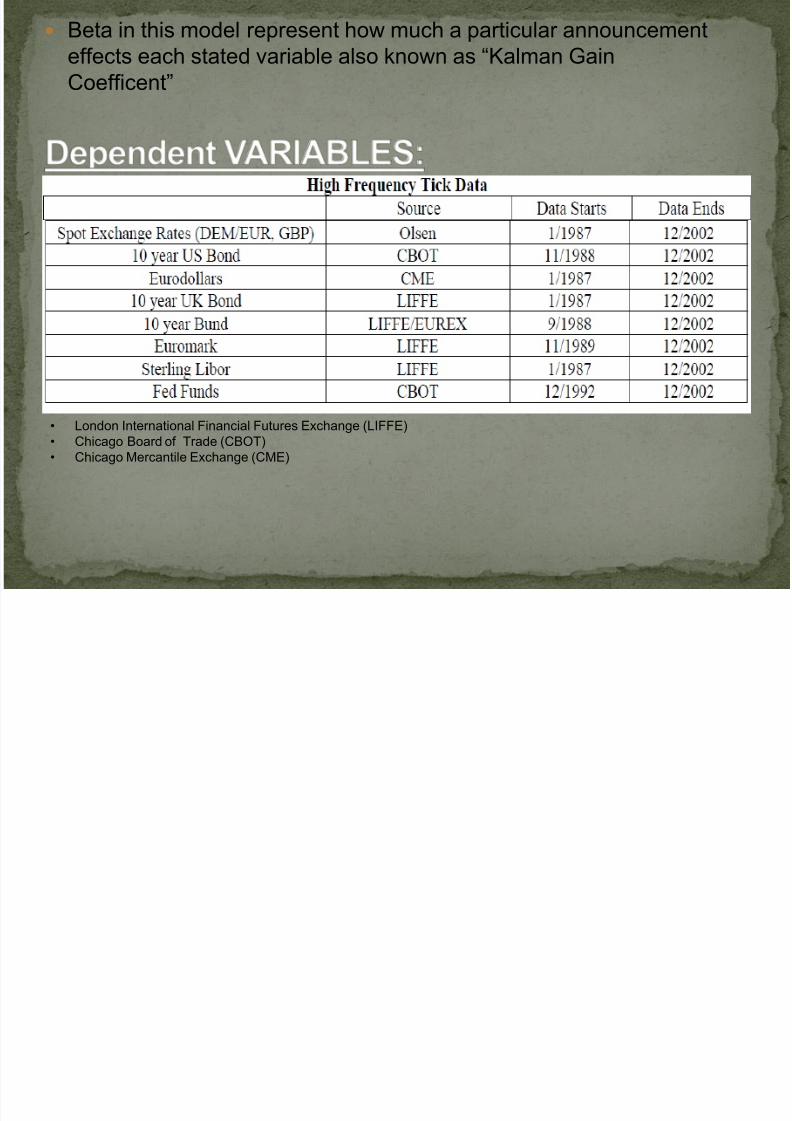

Beta in this model represent how much a particular announcement

effects each stated variable also known as “Kalman Gain

Coefficent”

• London International Financial Futures Exchange (LIFFE)

• Chicago Board of Trade (CBOT)

• Chicago Mercantile Exchange (CME)

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 7/24

INDEPENDENT

VARIABLES:

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 8/24

The point estimates in Table generally indicate that stronger-than-expected announcements lead to

negative exchange rate returns, i.e. dollar appreciation.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 9/24

The Nyblom-Hansen test is used to check the stability of the estimated parameters in a model.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 10/24

Stronger-than-expected releases tend to raise U.S. interest rates, including long term interestrates, and the effects are in many cases statistically significant. Stronger than- expected U.S.

releases also tend to raise foreign interest rates, although by a smaller amount.

Limitations:

The impact of macro announcement can be ambiguous if lower-than-expected inflation isperceived to be evidence of weak demand, then might expect monetary policy to be loosened,

causing interest rates to fall and the dollar to depreciate. But, if the unexpectedly low inflation is

perceived to be evidence of productivity growth, then in some models U.S. interest rates rise and

the dollar appreciates

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 11/24

They found that for several real U.S. macro announcements better than expected

news appreciates the dollar today.

From the responses of U.S. and foreign interest rate term structures , They are also

able to infer that such releases either lower the risk premium for holding foreign

currency or imply future expected dollar depreciation that exceeds the original

appreciation.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 12/24

By :

JOSHUA AIZENMAN, MICHAEL HUTCHISON

&

ILAN NOY

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 13/24

Inflation Targeting and non-Inflation Targeting in

emerging markets.

How central bank operates in Inflation targeting to

inflation, output gaps and real exchange rate using

Taylor Rule.

Volatility in Real Exchange Rates.

Extent to which countries are concentrated in

commodity exports.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 14/24

Author Years Findings

Johnson 2002 Announcement of Inflation Targets lowers expected inflation.

Ball & Sheridan 2005 They reject any long-term differences between advanced inflation targeters

and non-targeters.

Mishkin & Schmidt-Hebbel

2007 Inflation Targeting helps in achieving lower inflation in the long run.

Rose 2007 Inflation Targeters have both lower exchange rate volatility & less frequent

sudden stops of capital flows.

GonCalves & Salles 2008 Inflation Targeting leads to lower inflation rates and reduced volatility as

compared to non-targeters.

Lin & Ye 2009 Inflation Targeting leads to lower inflation rates and reduced volatility as

compared to non-targeters.

De Mello 2008 Adoption of Inflation Targeting regimes leads to positive outcomes.

Brito & Bystedt 2010 In common time trends, the positive benefits of IT regimes disappears

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 15/24

Author Years Findings

Clarida et al 1998 Central Banks in G3 countries respond to anticipated as oppose to

lagged inflation and respond to real exchange rates is significant.

Corbo et al 2001 Inflation Targeting countries exhibit the largest inflation gap

coefficient relative to output gap coefficient..Sehorfheide 2007 They find Australi and New Zealand change interest rate in respond

to exchange rate movements but Canada and UK do not.

Dueker & Fisher 2006 They found no difference in monetary policy rules followed by IT

countries and non-IT countries.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 16/24

Author Years Findings

Schmidt Hebbel & Warner 2002 Chile, Brazil and Mexico respond to exchange rate changes in short

term .

Mohanty & Klau 2004 The policy response to exchange rate change is larger than inflationand output gap.

Edwards 2006 High inflation and high exchange rate volatile countries have a

higher response to real exchange rate.

Aghion et al 2009 Adverse affects of exchange rate volatility are larger for less

financially developed countries.

Mishkin, Schmidt Hebbel &Warner

2007

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 17/24

Countries 16 (11 IT & 5 non-IT)

Years 1989Q1-2006Q4

Type of Data Panel

Dependent Variables Nominal Interest RateIndependent Variables GDP Growth

GDP Gap

Inflation

Inflation Gap

Interest Rate

Real Exchange Rate

Trade Openness

Reserve Changes

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 18/24

Taylor Rule Regression Model

Taylor rule is a monetary-policy rule that stipulates how much the central bankshould change the nominal interest rate in response to changes in inflation,

output, or other economic conditions.

Fixed effects model is a statistical model that represents the observed quantities

in terms of explanatory variables that are treated as if the quantities were non-

random.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 19/24

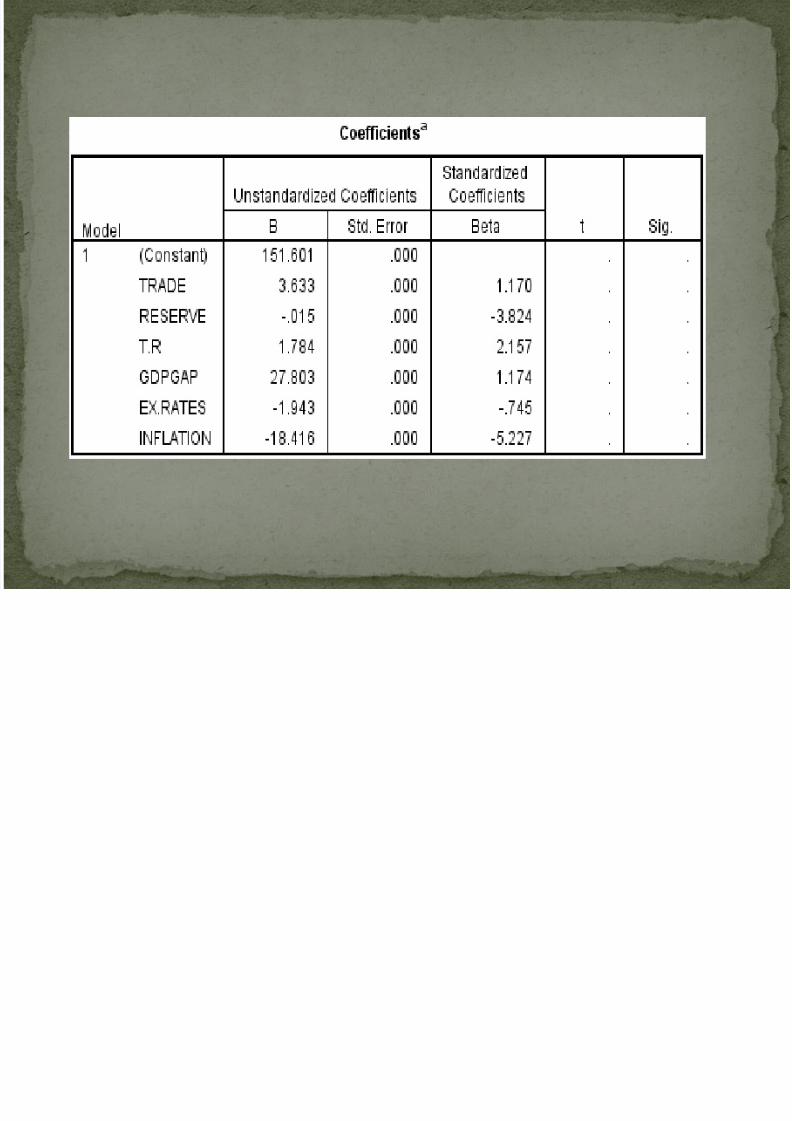

Taylor Rule Regression Results :

Interest Rate variation is much higher in inflation targeting group than in non-inflation targetinggroup.

The coefficient of inflation is highly significant, large and stable in inflation targeting regime ascompared with non inflation targeting regime.

The GDP gap is not significant in any of the regimes.

Response to real exchange rate is much smaller in IT countries as compared with non-IT countries.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 20/24

Results for Commodity & Non-Commodity Intensive Groups

The real exchange rate response is statistically strong and significaant in commodity export countriesand the degree of response is almost twice.

The response to inflation is only significant in commodity extensive group equation.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 21/24

We find clear evidence of a significant and stable response running from inflation topolicy interest rates in emerging markets that are following publically announced IT

policies.

We find strong evidence that IT emerging markets are following a mixed-IT strategy

whereby central banks respond to both inflation and real exchange rates in setting

policy interest rates.

We also find that the response to real exchange rates is strongest in those countriesfollowing IT policies that are relatively intensive in exporting basic commodities.

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 22/24

VARIABLE: SOURCE

Trade (% of GDP) WORLD BANK

Reserve Change

Total reserves (% of total external debt) WORLD BANK

GDP growth (annual %) WORLD BANK

GDP GAP (Estimating Output Gap for Pakistan Economy:Structural and Statistical Approaches) S. ADNAN

NOMINAL INTEREST RATES WORLD BANK

Real effective exchange rate WORLD BANK

Inflation, consumer prices (annual %) WORLD BANK

TIME SPAN: 7 YEARS (2000-2006)

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 23/24

8/10/2019 Presentation I.F

http://slidepdf.com/reader/full/presentation-if 24/24