Presentation

17

Page 1 of 17 EIGHTH ASSET MANAGEMENT LTD. PORTFOLIO A SYSTEMATIC WAY OF MANAGING YOUR MONEY

-

Upload

eighth-asset-management-ltd -

Category

Business

-

view

76 -

download

1

Transcript of Presentation

Page 1 of 17

EIGHTH ASSET MANAGEMENT LTD.

PORTFOLIO

A SYSTEMATIC WAY OF MANAGING YOUR MONEY

Page 2 of 17

CONTENTS

Introduction 2

Investment Philosophy 3

Table Long Term Performance VS S&P 4

Table Medium Term Performance 5

Table Stress Test 6

Table Asset Correlations 7

Investment Strategy 8

Why Eighth Asset Management Ltd? 10

Hedging 11

Appendix 12

Risk Warning 20

Page 3 of 17

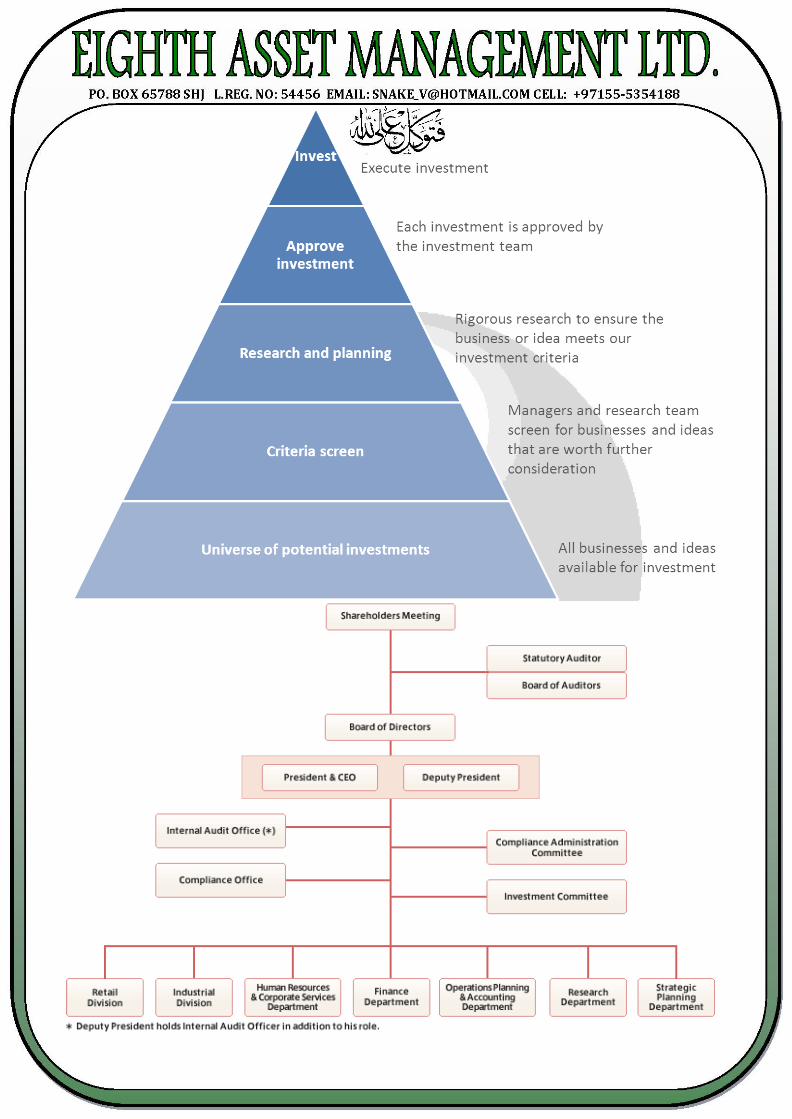

INTRODUCTION

THE Q U E S T FACING every investor in dealing with accumulated capital is to presser-

preserve and enhances wealth. In order to achieve these two objectives, investors aim for an ideal balance a

tailor-made structure that can produce consistent returns over the long run while minimizing volatility.

The process of defining an ideal investment strategy is influenced by the following additional requirements:

• To grow capital above prevailing inflation

• To invest in liquid assets that can provide for regular cash flows

• To build a transparent portfolio while avoiding mistakes that could cause major setbacks or permanent

portfolio impairment.

There is an obvious trade-off in achieving these objectives and requirements. Moreover, investor psychology

often adds an extra layer of uncertainty to the process of wealth management.

Page 4 of 17

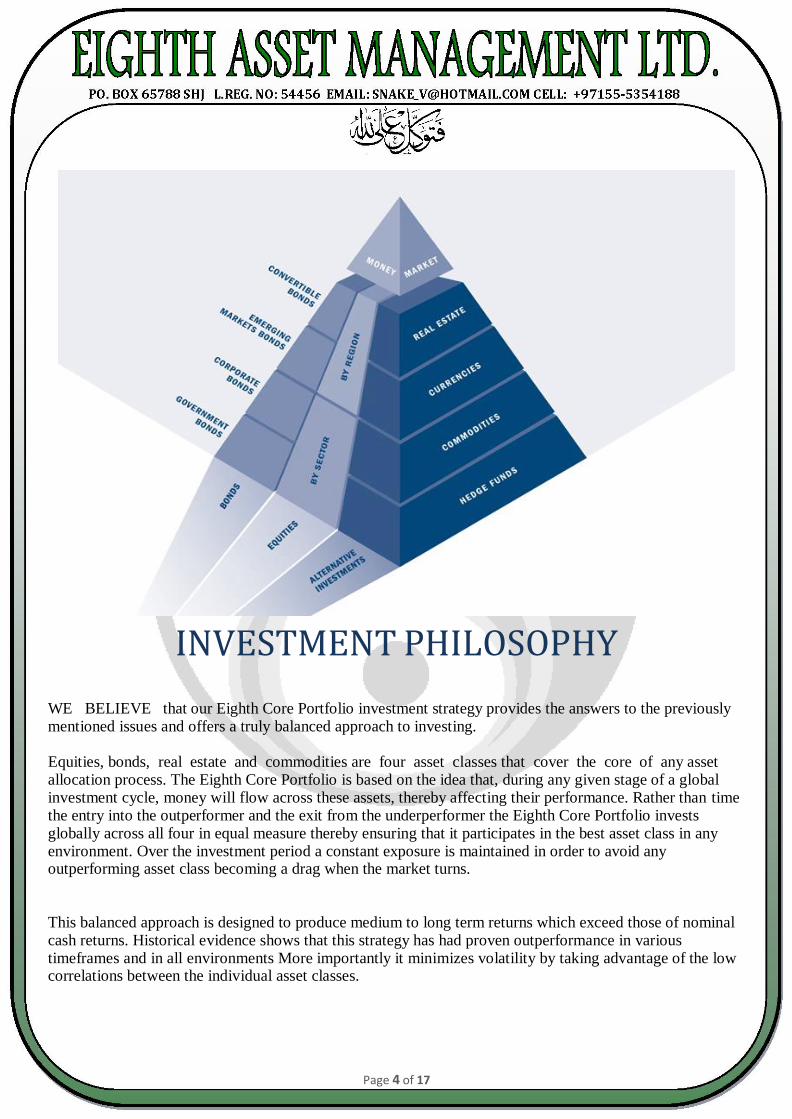

INVESTMENT PHILOSOPHY WE BELIEVE that our Eighth Core Portfolio investment strategy provides the answers to the previously mentioned issues and offers a truly balanced approach to investing. Equities, bonds, real estate and commodities are four asset classes that cover the core of any asset allocation process. The Eighth Core Portfolio is based on the idea that, during any given stage of a global investment cycle, money will flow across these assets, thereby affecting their performance. Rather than time the entry into the outperformer and the exit from the underperformer the Eighth Core Portfolio invests globally across all four in equal measure thereby ensuring that it participates in the best asset class in any environment. Over the investment period a constant exposure is maintained in order to avoid any outperforming asset class becoming a drag when the market turns. This balanced approach is designed to produce medium to long term returns which exceed those of nominal cash returns. Historical evidence shows that this strategy has had proven outperformance in various timeframes and in all environments More importantly it minimizes volatility by taking advantage of the low correlations between the individual asset classes.

Page 5 of 17

LONG TERM PERFORMANCE VS S&P

Metrics of long-term strategic health show the ability of an enterprise to sustain its current operating

activities and to identify and exploit new areas of growth. A company must periodically assess and measure

the threats—including new technologies, changes in public opinion and in the preferences of customers, and

new ways of serving them—that could make its current business less attractive. In assessing a company's

long-term strategic health, specific metrics are sometimes hard to identify, so more qualitative milestones,

such as progress in selecting partners for mergers or for entering a market, are needed.

While Home Depot's leading position in the home-improvement business appears to be solid in the medium

term, a longer-term threat comes from Wal-Mart, which sells many of the same fast-moving items, such as

light bulbs. The cost base of Wal-Mart is lower because it provides less in-store help than does Home Depot,

which must therefore ensure that store associates focus on higher-margin areas where support is critical

(such as plumbing) rather than on products whose price doesn't incorporate assistance to customers.

Short-term metrics explore the factors that underlie historical performance and help indicate whether

growth and ROIC can be sustained at a given level or will probably rise or fall. These metrics might include

costs per unit (for a manufacturing company) or same-store sales growth (for a retailer). They fall into three

categories:

Sales productivity metrics explore the factors underlying recent sales growth. For retailers, these

metrics include market share, a retailer's ability to charge higher prices than its peers, the pace of

store openings, and same-store sales increases.

Operating-cost productivity metrics explore the factors underlying unit costs, such as the cost of

building a car or delivering a package. UPS, for example, is well known for charting out the optimal

delivery paths of its drivers to enhance their productivity and for developing well-defined standards

on how to deliver packages.

Capital productivity metrics show how well a company uses its working capital (inventories,

receivables, and payables) and its property, plant, and equipment. Dell revolutionized the personal-

computer business by building products to order and thus minimizing inventories. Because the

company keeps them so low and has few receivables to boot, it can operate with negative working

capital.

Page 6 of 17

MEDIUM TERM PERFORMANCE Medium-term metrics go beyond short-term performance by looking forward

to indicate whether a company can maintain and improve its growth and

ROIC over the next one to five years (or longer for companies with extended

product cycles, as in pharmaceuticals). These metrics fall into three

categories:

Commercial-health metrics, indicating whether a company can

sustain or improve its current revenue growth, include the metrics for

its product pipeline (the talent and technology to market new products

over the medium term), brand strength (investments in brand

building), regulatory risk, and customer satisfaction. Metrics for

medium-term commercial health vary widely by industry. For a

pharmaceutical company, the obvious priority is its product pipeline

and its relationship with governments—a major customer and

regulator. For an online retailer, customer satisfaction and brand

strength may be the most important considerations.

Cost structure health metrics gauge a company's ability, as

compared with that of its competitors, to manage its costs over three to

five years. These metrics might include assessments of programs like Six Sigma, which companies

such as General Electric use to reduce their costs continually and to maintain a cost advantage

relative to their competitors across most of their businesses.

Asset health metrics show how well a company maintains and develops its assets. For a hotel or

restaurant chain, to give one example, the average time between remodeling may be an important

driver of health.

Page 7 of 17

STRESS TEST

Capital Assessment Program, or SCAP, popularly known as the bank stress tests.

The stress tests were limited to banking organizations with assets in excess of $100 billion dollars; banks

that the Fed considered "too big to fail". The requirements of the stress tests measured each institution's Tier

1 common capital against a baseline scenario and a hypothetical scenario that was deemed more adverse.

The final results showed that 10 of the 19 banks were deemed to have inadequate capital. That being said,

every bank tested met the legally mandated capital requirements.

Every year since the financial crisis in the year 2007 the US Federal Reserve (Central Bank) has put the

nation’s banks through "stress tests" designed to assess their reaction to hypothetical scenarios such as the

financial crisis.

The 2013 Stress Test involved:

Unemployment at 12.1%

Fall in equity prices of more than 50%

Fall in housing prices of more than 20%

An interesting caveat of this is the political amusement it brings. We clearly are safe if all 18 (except one) of

the largest banks would have survived such a scenario. I do wonder why they didn't include a spike in bond

yields and a fall in their value - Banks are major holders of Government Debt after all...

Guess that would have ruined the illusion of safety?

Page 8 of 17

ASSET CORRELATIONS

The following table shows return correlations between various asset classes (as represented by exchange

traded funds) over the past three months.

Page 9 of 17

INVESTMENT STRATEGY

THE S T R A T E G Y i n v e s t s globally in four main asset classes Equities, Bonds, and Real

Estate & Commodities in equal proportion i.e. 25% in each asset class. The allocations to these asset classes are monitored quarterly and systematically rebalanced to the original 25% allocation, regardless of performance during the period. By doing this we periodically realize the profit on the outperforming asset class so that we do not become unduly overexposed to it, and allocate further funds to the underperforming asset class in order to maintain our equal allocation. Our research indicates that a quarterly rebalancing time period provides the optimal trade-off between the benefits and costs of rebalancing.

Page 10 of 17

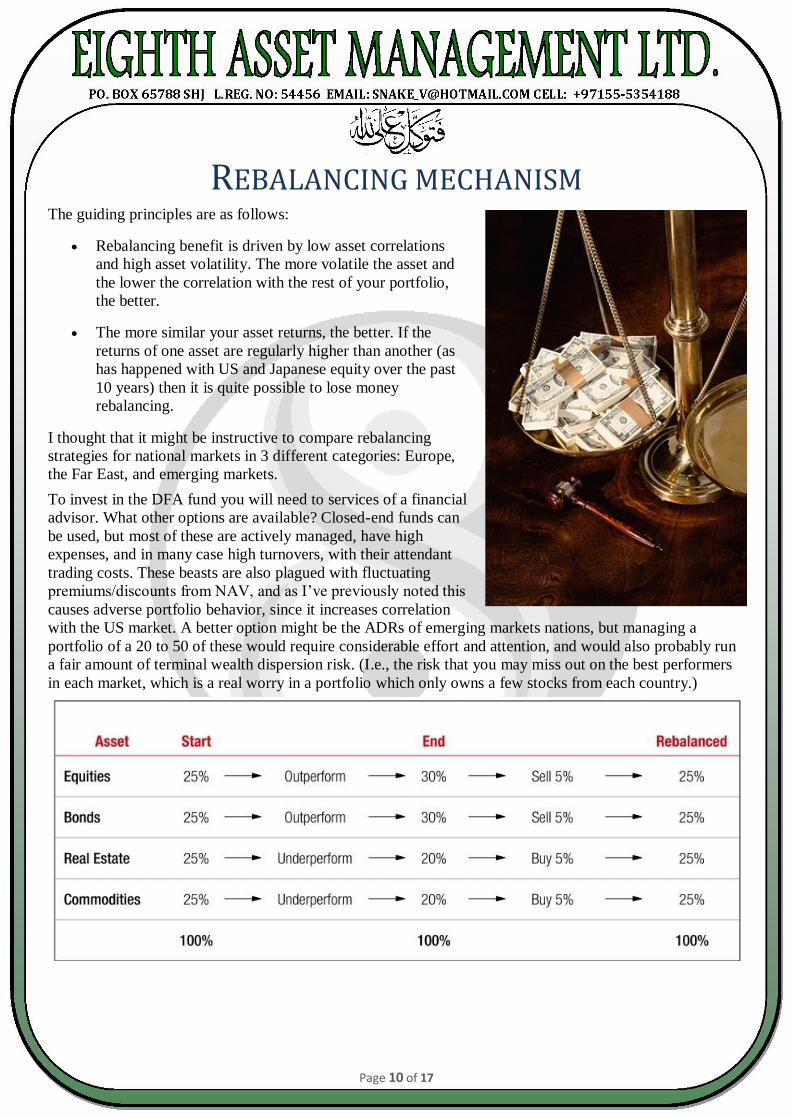

REBALANCING MECHANISM The guiding principles are as follows:

Rebalancing benefit is driven by low asset correlations

and high asset volatility. The more volatile the asset and

the lower the correlation with the rest of your portfolio,

the better.

The more similar your asset returns, the better. If the

returns of one asset are regularly higher than another (as

has happened with US and Japanese equity over the past

10 years) then it is quite possible to lose money

rebalancing.

I thought that it might be instructive to compare rebalancing

strategies for national markets in 3 different categories: Europe,

the Far East, and emerging markets.

To invest in the DFA fund you will need to services of a financial

advisor. What other options are available? Closed-end funds can

be used, but most of these are actively managed, have high

expenses, and in many case high turnovers, with their attendant

trading costs. These beasts are also plagued with fluctuating

premiums/discounts from NAV, and as I’ve previously noted this

causes adverse portfolio behavior, since it increases correlation

with the US market. A better option might be the ADRs of emerging markets nations, but managing a

portfolio of a 20 to 50 of these would require considerable effort and attention, and would also probably run

a fair amount of terminal wealth dispersion risk. (I.e., the risk that you may miss out on the best performers

in each market, which is a real worry in a portfolio which only owns a few stocks from each country.)

Page 11 of 17

INVESTMENT STRATEGY

IN OUR EXPERIENCE, the most

efficient way to track an index performance is by

using Exchange-Traded Funds (ETF) or Exchange-

Traded Commodity (ETC).

These are open-ended index tracking funds that are

listed and traded on major stock exchanges.

ETF’s/ETC’s trade like equities but have the structure

of a Collective Investment Scheme. Their aim is to

replicate an underlying index. In particular, they aim

to match the return (before tracking costs) and

volatility of their respective index. ETF’s/ETC’s

minimizing the possibility of losses due to human judgment and, as we have seen in the recent past, these

losses can be costly.

ETF’s/ETC’s evaluated against various criteria:

• Tracking error: how well it mirrors the return and volatility of the index it follows, a minimal

tracking error shows a close match to the index.

• Data Transparency: how accurate and easily available the data of the underlying index and

• ETF’s/ETC’s are and whether this captures the required universe that the index is supposed to

Represent.

• Liquidity: the liquidity and spread on ETF’s/ETC’s are mainly dependent on the liquidity and

spreads of the index constituents. Good ETF’s/ETC’s have good liquidity on primary and secondary

markets and tight spreads.

• Cost: ability to keep the rebalancing costs and management fees to a minimum.

• Investor acceptance: the more widely used the ETF/ETC is the more likely it is to be

representative of the asset class it is tracking.

• Income distribution: if the underlying asset has regular cash distribution, a good ETF/ETC can

collect these cash flows and distribute this to the ETF/ETC holder on a regular basis, thereby allowing the

investor to realize income.

The ETF’s/ETC’s we have selected are a fair reflection of the underlying asset classes and have the above

characteristics so we are comfortable with their ability to replicate the performance of the indices they

have been designed to follow.

Please be aware that the issuer risk of the ETC’s (Exchange Traded Commodities) is a Bank (e.g. UBS

AG for the UBS Bloomberg CMCI Composite) and not a Fund where the underlying cash is invested into

government/sovereign bonds.

Page 12 of 17

WHY EIGHTH ASSET

MANAGEMENT LTD?

AS WEALTH MANAGERS we

have several years of experience in the area of fund

management which enables us to efficiently manage

this type of portfolio. We aim to add value through

Research:

Implementing rigorous ETF’s/ETC’s selection &

monitoring processes.

Meeting ETF/ETC managers regularly to ensure

transparency on the ETF/ETC and getting updates on

available products.

Minimizing the tax drag by investing in tax-efficient

ETF’s/ETC’s with a focus on cash dividends.

Effective dealing:

Trading in large volume so as to minimize the cost of dealing and rebalancing.

Maintaining contacts with the right brokers to ensure that we can deal in volume without affecting the

price.

Avoiding price slippage by applying effective limits on buying and selling. Effective rebalancing

Ensuring quarterly systematic monitoring on all portfolios.

Establishing and reviewing appropriate tolerance limits so that the benefit of a rebalanced portfolio is not

outweighed by the costs of rebalancing. Currency exposure management (see Table 6)

Maintaining a mechanical passive hedge of currency exposure to avoid undue translation risk on.

Annual review of hedging practice based on currency allocation of underlying ETF’s/ETC’s.

Page 13 of 17

HEDGING

A risk management strategy used in

limiting or offsetting probability of

loss from fluctuations in the prices of

commodities, currencies, or

securities. In effect, hedging is a

transfer of risk without buying

insurance policies.

Hedging employs various techniques

but, basically, involves taking equal

and opposite positions in two

different markets (such as cash and

futures markets). Hedging is used also

in protecting one's capital against

effects of inflation through investing

in high-yield financial instruments

(bonds, notes, shares), real estate, or

precious metals.

Making an investment to reduce the risk of adverse price movements in an asset.

Normally, a hedge consists of taking an offsetting position in a related security, such as a

futures contract.

To reduce the risk of an investment by making an offsetting investment. There are a large

number of hedging strategies that one can use. To give an example, one may take a long

position on a security and then sell short the same or a similar security. This means that

one will profit (or at least avoid a loss) no matter which direction the security's price takes.

Hedging may reduce risk, but it is important to note that it also reduces profit potential.

Page 14 of 17

JOINT VENTURE INVESTMENT

An agreement between two or more companies to cooperate on a specific initiative. The

joint venture may involve marketing a product, offering a service, or expanding into a new

geographical territory. Often, companies undertake joint ventures with companies in other

countries as a way to expand into new markets. While the local company will have the

business relationships and current business operations, the foreign company may bring a

brand name and managerial skills.

Foreign Invested Enterprise - FIE

Setting up an FIE is a common method of creating an operation in Asian countries,

especially in China. In China, any one of a number of legal entities can be considered FIEs

including equity joint ventures (EJV), cooperative joint ventures (CJV), wholly-owned

foreign enterprises (WFOE) and foreign-invested companies limited by shares (FCLS).

Any one of a number of legal structures under which a company can participate in the

foreign economy. FIEs tend to have tight government regulation at nearly every important

business juncture, which limits the efficiency at which any foreign company can profit

from foreign ventures as well as the amount of control that a foreign parent has over the

FIE.

RISK WARNING THE F O L L O W I N G I N F O R M A T I O N is very important and you should

read this information if you are unclear at any time as to the purposes of this document. Although information in this document has been obtained from sources believed to be reliable, EIGHTH ASSET MANAGEMENT Ltd does not represent or warrant its accuracy, and such information may be incomplete or condensed. All estimates and opinions in this document constitute our judgment as of the date of the document and may be subject to change without notice.

EIGHTH ASSET MANAGEMENT Ltd will not be responsible for the consequences of reliance upon

any opinion or statement contained herein or for any omission. This document is for the private use of

EIGHTH ASSET MANAGEMENT Ltd and may not be reproduced or disclosed (in whole or in part) to

any other person without our prior written permission.

The value of investments and the income derived from them can fall as well as rise, and past performance does not guarantee or predict future performance. Investment products may be subject to investment risks, involving but not limited to, currency exchange and market risks, fluctuations in value and, where applicable, possible loss of principal invested.

The manner in which this document is distributed may be restricted by regulation or law in certain

countries and persons who come into possession of this document should inform themselves of and Observe any restrictions. This document does not constitute an offer to sell, solicit or offer to buy any investment product, and is not intended to be a final representation of the terms and conditions of any product. The investments mentioned in this document may not be suitable for all recipients and you should seek professional advice if you have any doubts. Clients should obtain legal/taxation advice suitable to their particular circumstances.

Eighth ASSET MANAGEMENT Ltd

Head Office