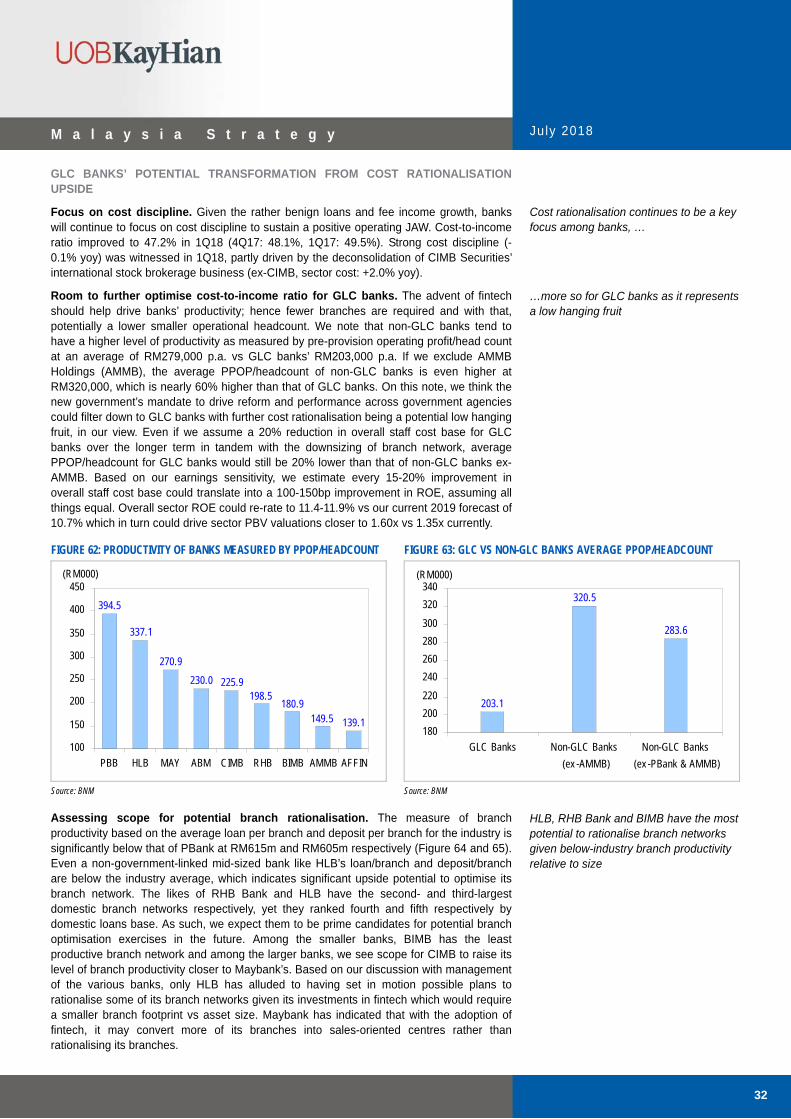

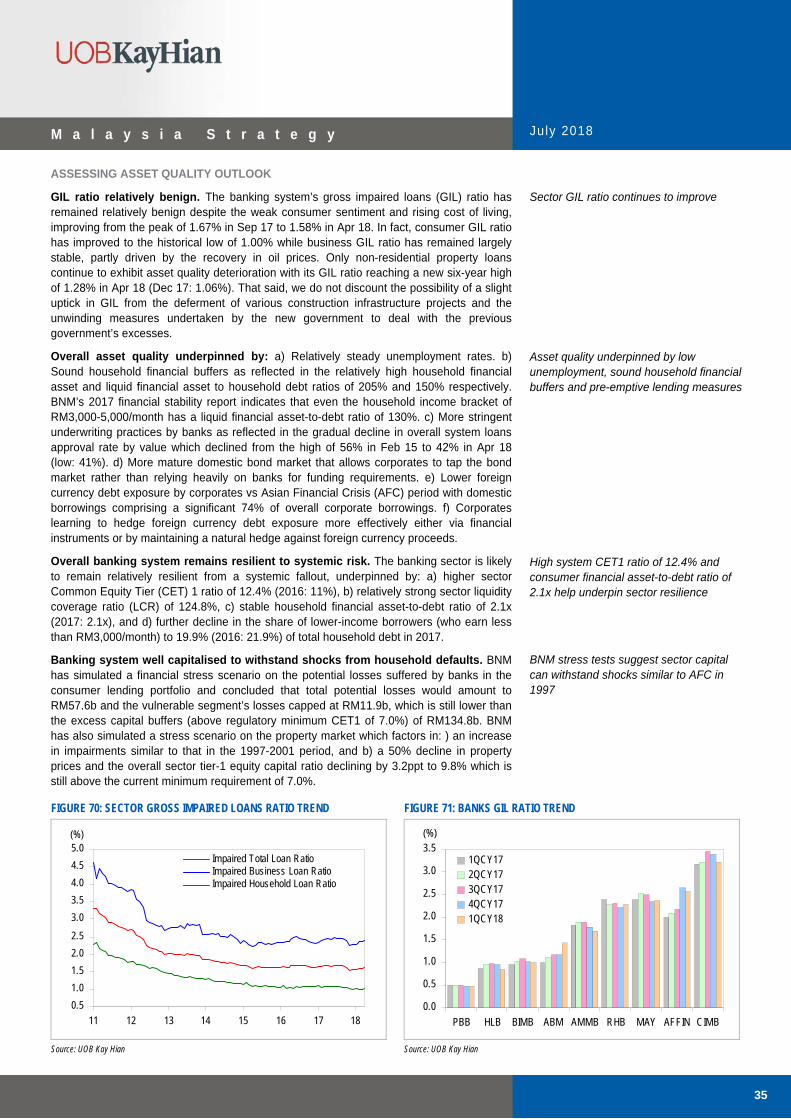

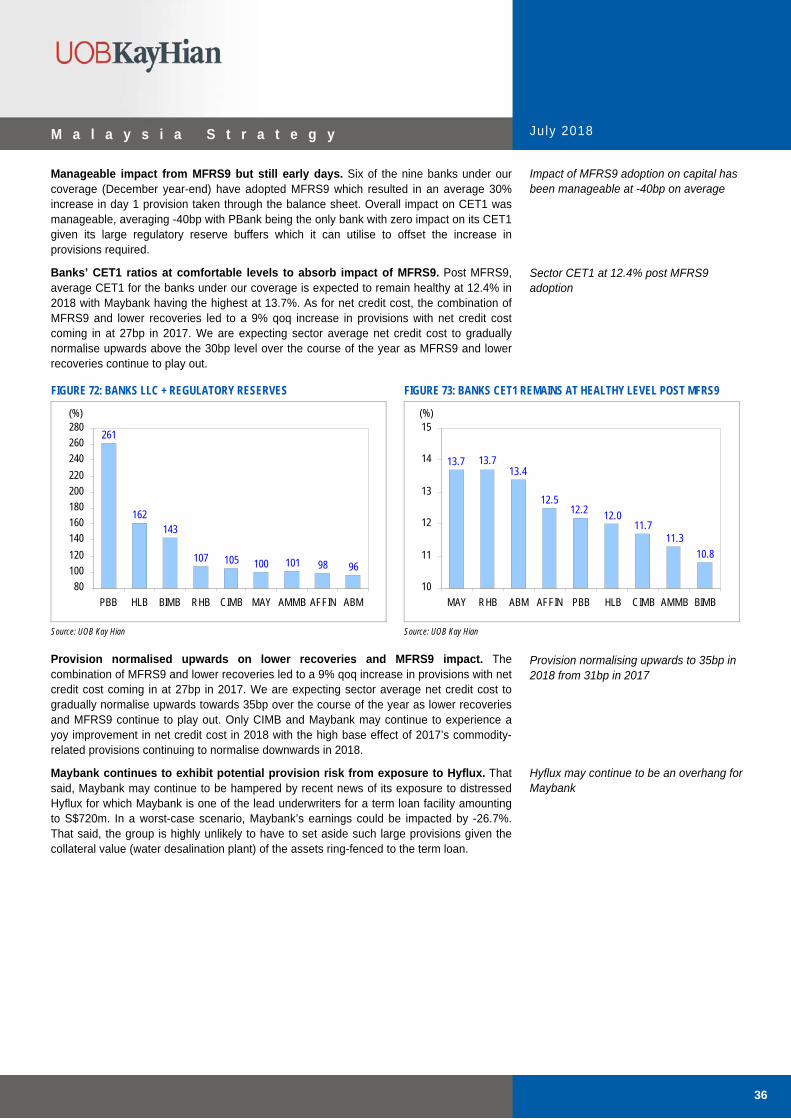

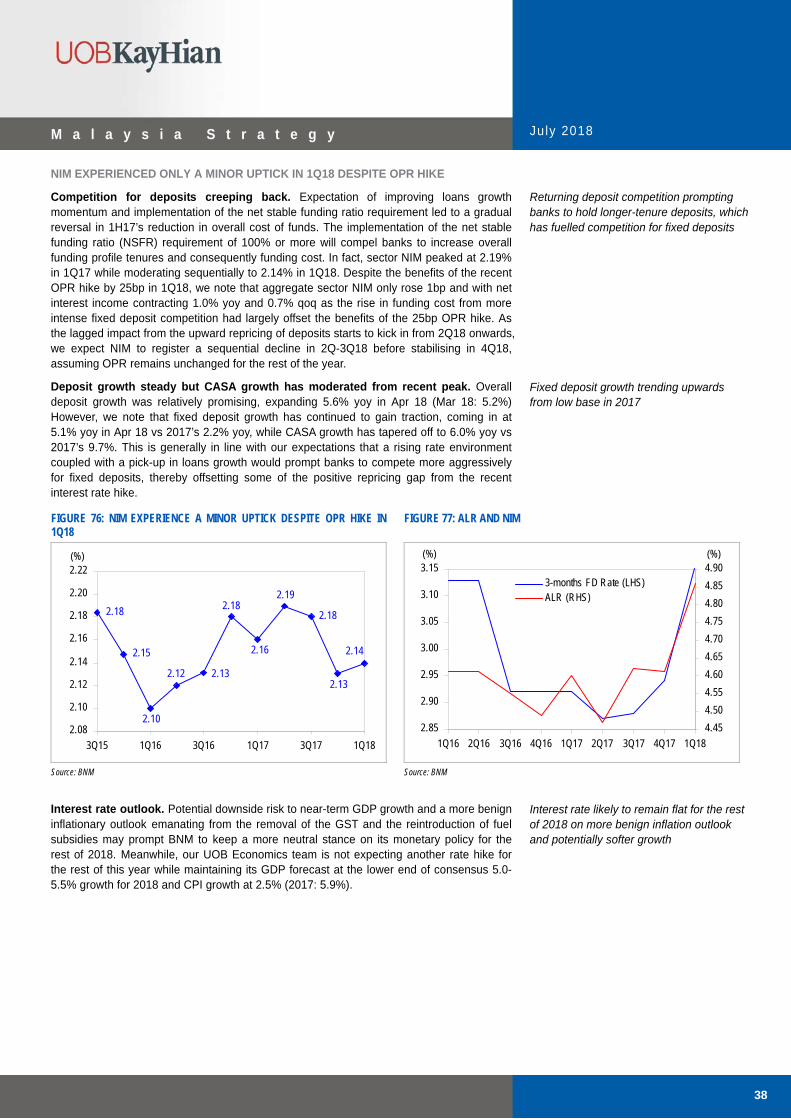

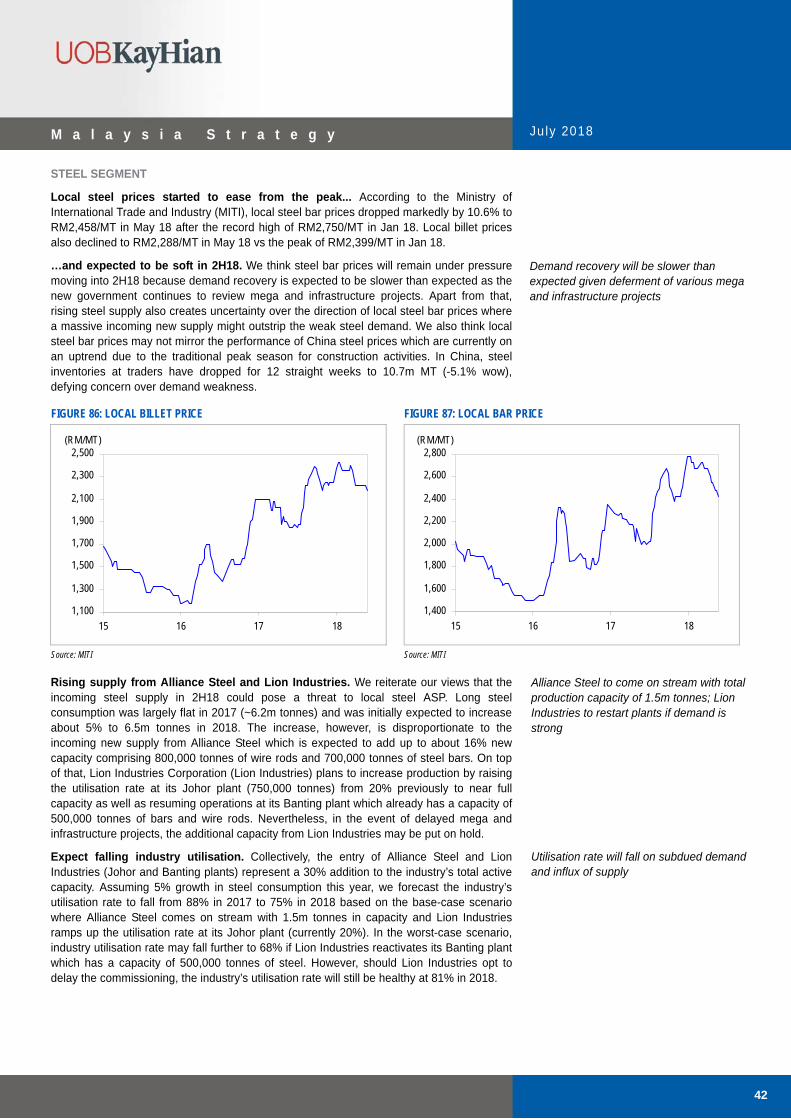

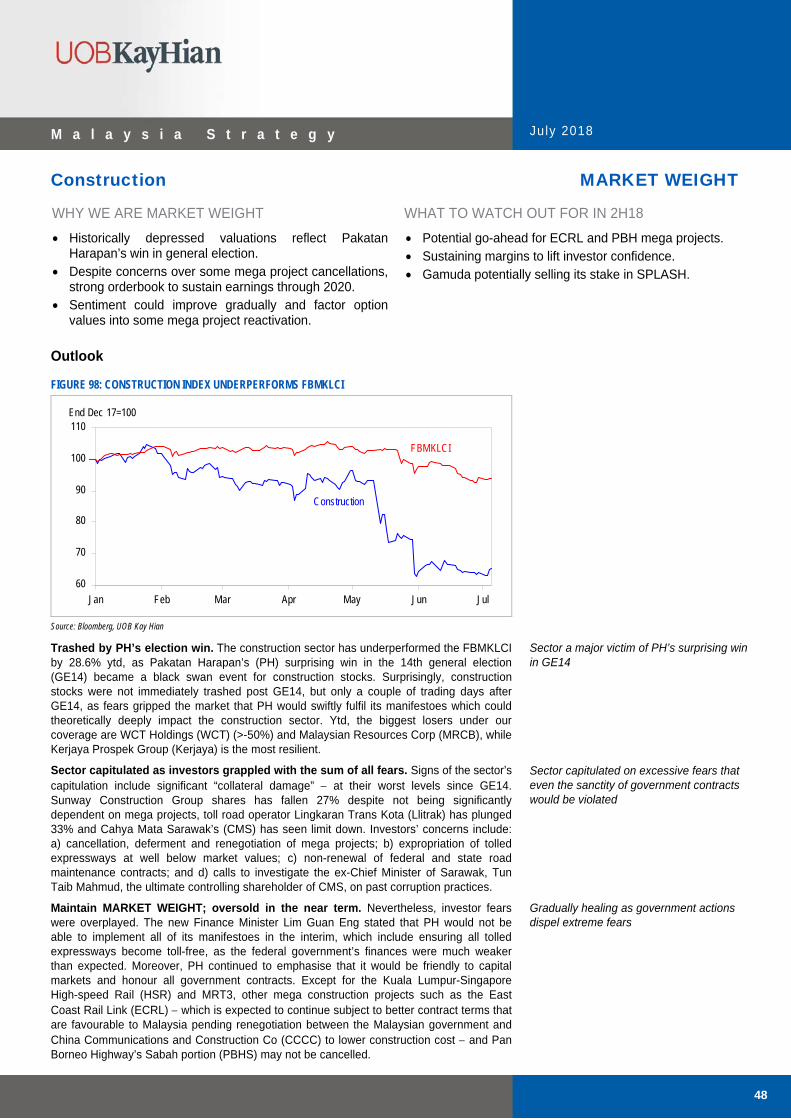

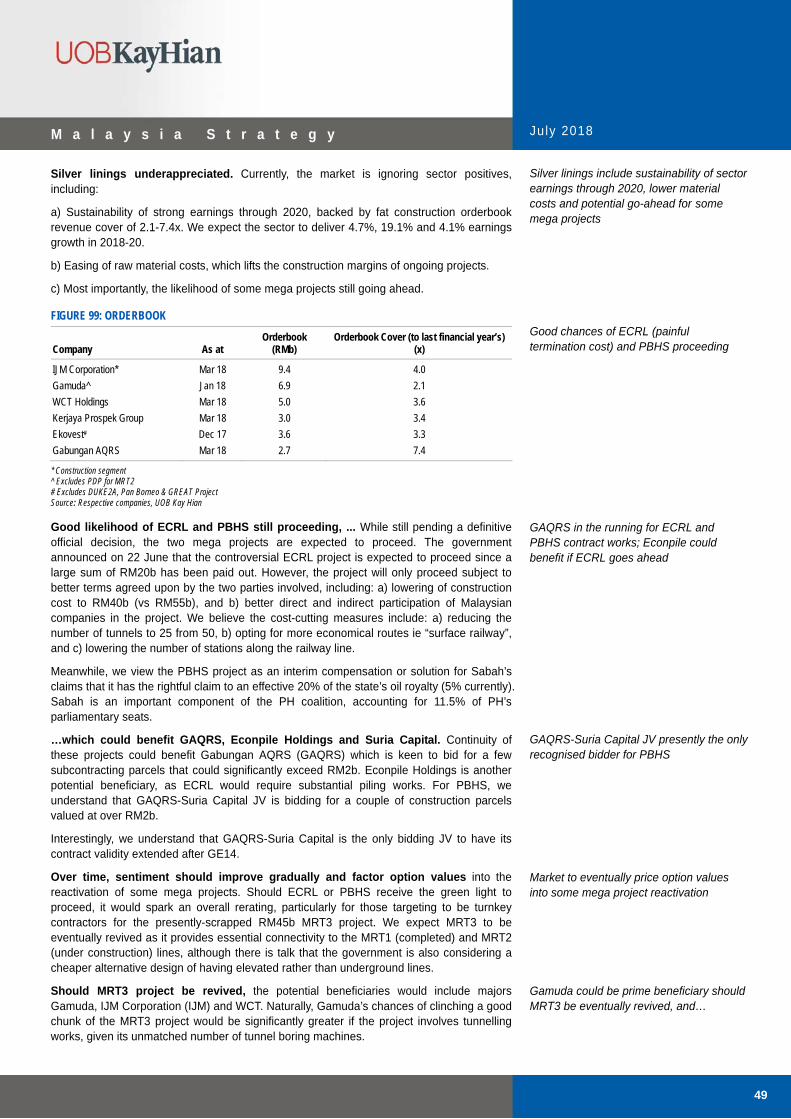

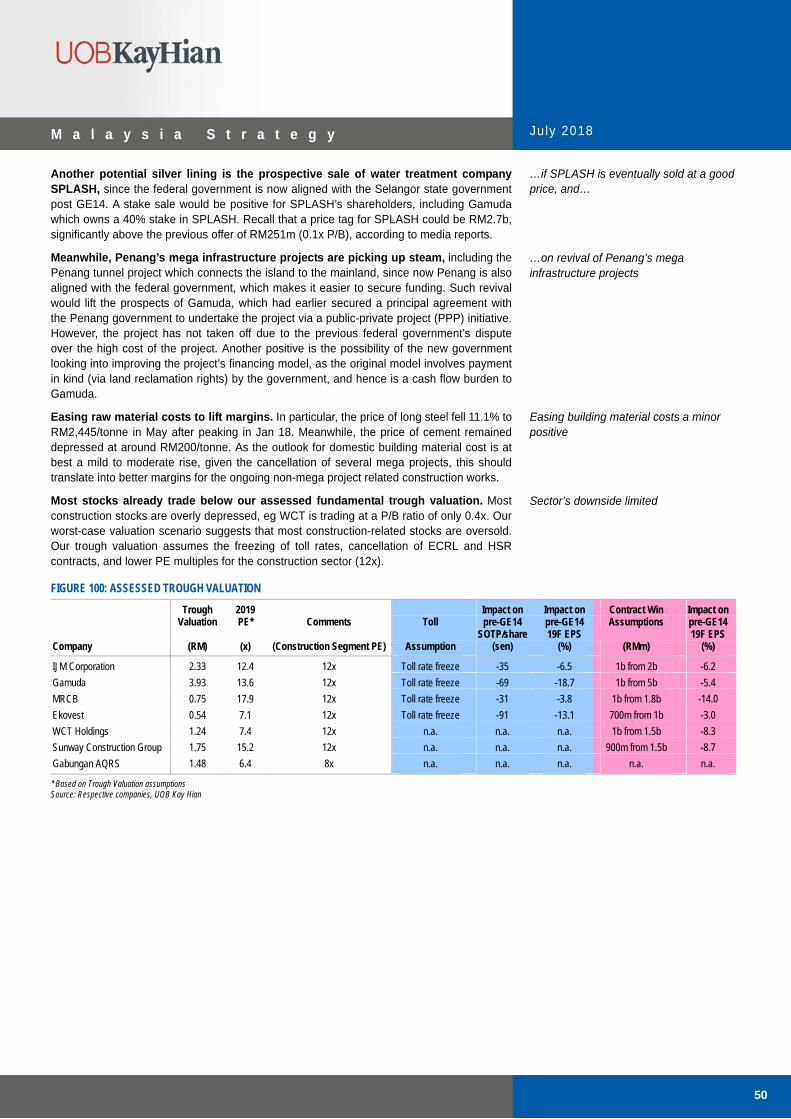

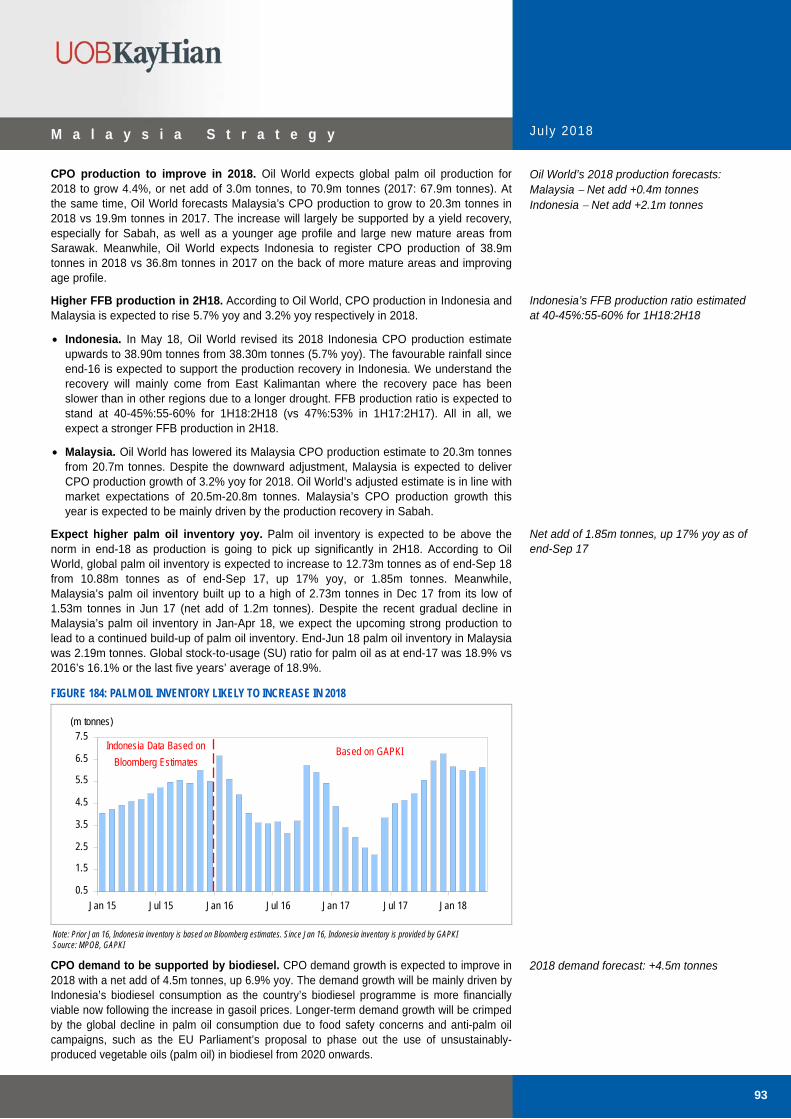

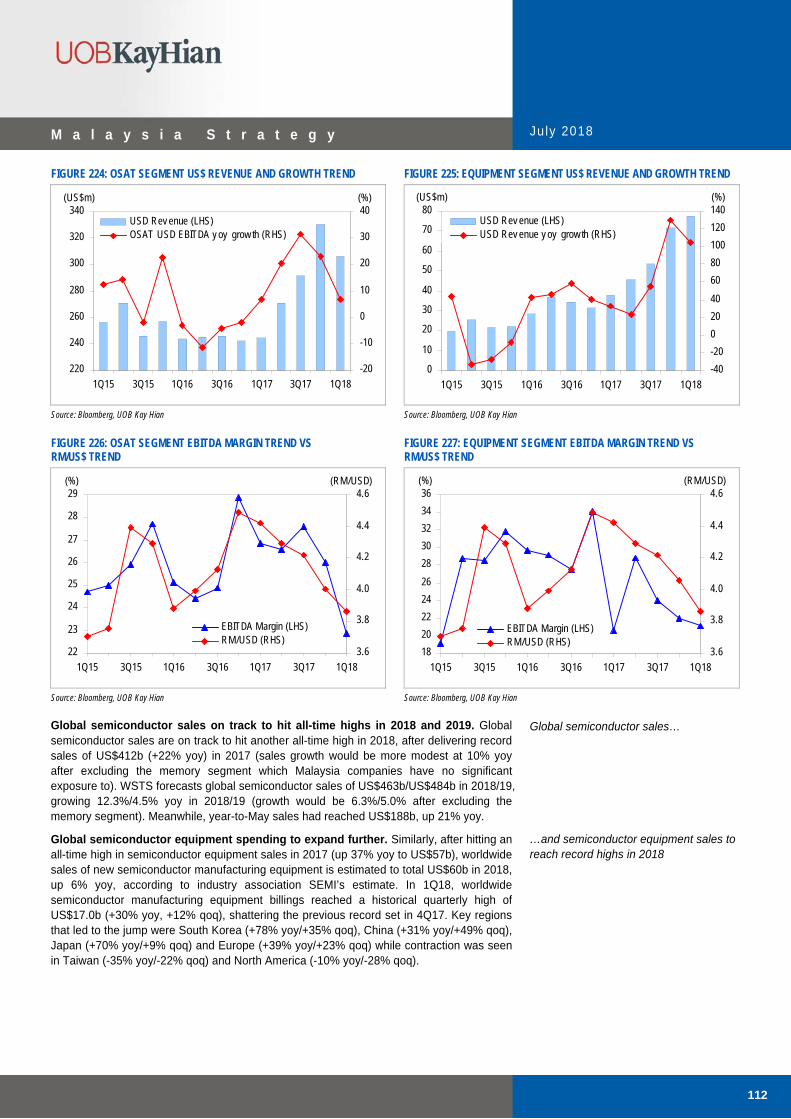

Prescription For Anaemic Conditions

164

S i n g a p o r e S t r a t e g y January 2014 Prescription For Anaemic Conditions M a l a y s i a S t r a t e g y July 2018 PP14218/11/2012(031278) Refer to last page for important disclosures. July 2018 E&E

Transcript of Prescription For Anaemic Conditions

S i n g a p o r e S t r a t e g y January 2014

Prescription For Anaemic Conditions

M a l a y s i a S t r a t e g y July 2018

PP14218 /11 / 2012(031278 )

Refer to last page for important disclosures.

Ju ly 2018

E&E

M a l a y s i a S t r a t e g y July 2018

Contents Executive Summary .......................................................................................................................... 1

Prescription For Anaemic Conditions

- 1H18 Review .................................................................................................................................... 2

- 2H18 Outlook ................................................................................................................................... 4

Earnings Outlook............................................................................................................................... 9

Strategy ............................................................................................................................................ 11

Investment Themes ......................................................................................................................... 13

Top Picks.......................................................................................................................................... 16

Sector Review

- Automobile : MARKET WEIGHT.................................................................................................... 18

- Banking : MARKET WEIGHT........................................................................................................ .25

- Building Materials : MARKET WEIGHT ........................................................................................ .41

- Construction : MARKET WEIGHT.................................................................................................. 48

- Consumer : MARKET WEIGHT ..................................................................................................... 53

- Gaming : OVERWEIGHT ............................................................................................................... 62

- Glove Manufacturing : UNDERWEIGHT........................................................................................ 72

- Media : MARKET WEIGHT ............................................................................................................ 79

- Oil & Gas : MARKET WEIGHT ...................................................................................................... 85

- Plantation : MARKET WEIGHT ..................................................................................................... 91

- Property – Developers & REITs : MARKET WEIGHT ................................................................... 99

- Technology : OVERWEIGHT ...................................................................................................... 107

- Telecommunications : MARKET WEIGHT .................................................................................. 117

- Utilities : OVERWEIGHT .............................................................................................................. 123

Top Stocks

- Bumi Armada (BUY/RM0.71/Target: RM1.06)............................................................................ 130

- Genting Malaysia (BUY/RM4.85/Target: RM6.28)...................................................................... 132

- Inari Amertron (BUY/RM2.25/Target: RM2.68) .......................................................................... 134

- Public Bank (BUY/RM22.90/Target: RM25.20)........................................................................... 136

- Tenaga Nasional (BUY/RM14.30/Target: RM17.70) .................................................................. 138

- Cahya Mata Sarawak (BUY/RM2.42/Target: RM4.00) ............................................................... 140

- Gabungan AQRS (BUY/RM1.19/Target: RM1.86)...................................................................... 142

- Scientex (BUY/RM7.16/Target: RM8.20) .................................................................................... 144

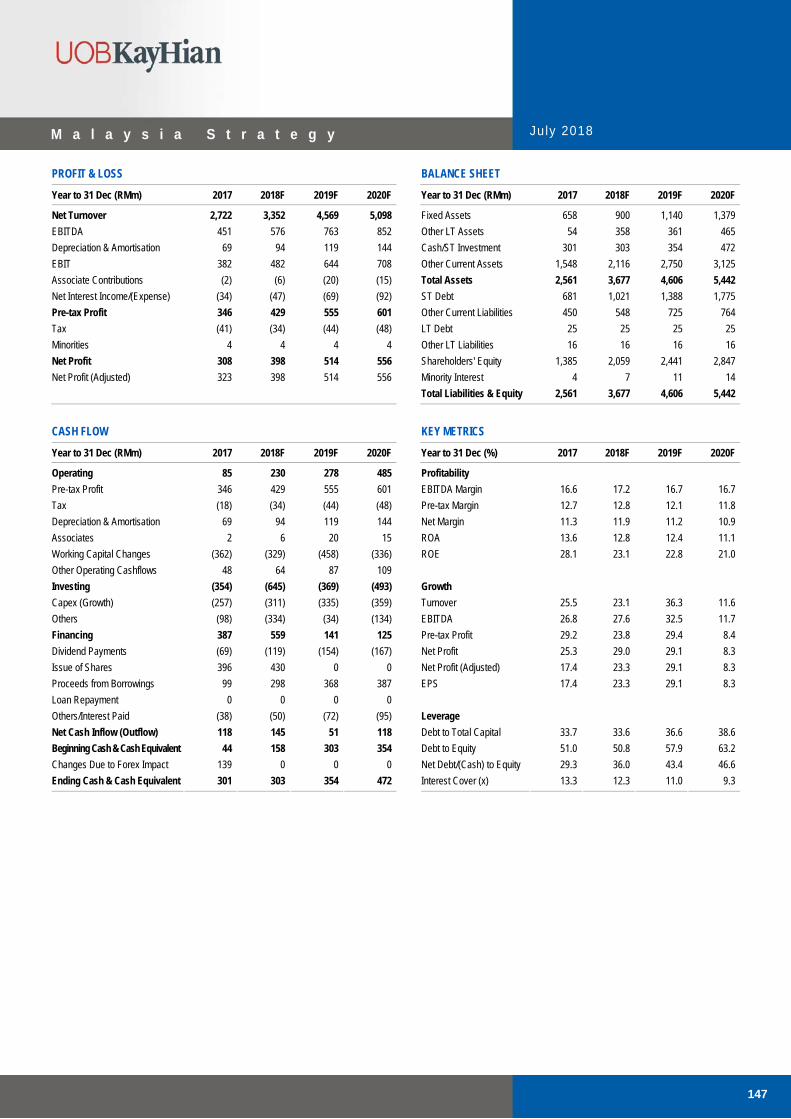

- Serba Dinamik (BUY/RM3.34/Target: RM4.30) .......................................................................... 146

- VS Industry (BUY/RM1.68/Target: RM1.85) ............................................................................... 148

- Yong Tai (BUY/RM1.47/Target: RM2.10) ................................................................................... 150

Corporate Statistics .................................................................................................................... 152

Appendix 1: GE14 Results............................................................................................................ 156

Appendix 2: 2018 Malaysia Cabinet Members............................................................................ 157

Appendix 3: Key Economic Indicators........................................................................................ 159

Appendix 4: Foreign Shareholding ............................................................................................. 160

Disclosures/Disclaimers ............................................................................................................... 161

Ju ly 2018

1

M a l a y s i a S t r a t e g y

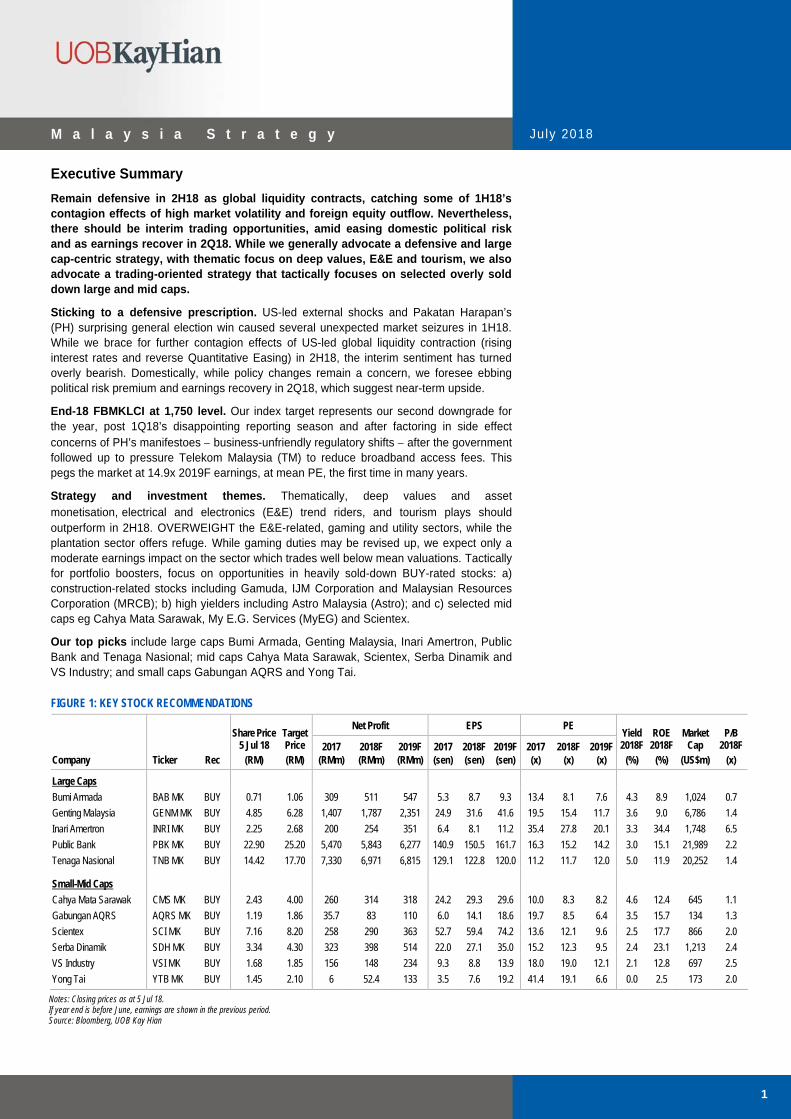

Executive Summary

Remain defensive in 2H18 as global liquidity contracts, catching some of 1H18’s contagion effects of high market volatility and foreign equity outflow. Nevertheless, there should be interim trading opportunities, amid easing domestic political risk and as earnings recover in 2Q18. While we generally advocate a defensive and large cap-centric strategy, with thematic focus on deep values, E&E and tourism, we also advocate a trading-oriented strategy that tactically focuses on selected overly sold down large and mid caps.

Sticking to a defensive prescription. US-led external shocks and Pakatan Harapan’s (PH) surprising general election win caused several unexpected market seizures in 1H18. While we brace for further contagion effects of US-led global liquidity contraction (rising interest rates and reverse Quantitative Easing) in 2H18, the interim sentiment has turned overly bearish. Domestically, while policy changes remain a concern, we foresee ebbing political risk premium and earnings recovery in 2Q18, which suggest near-term upside.

End-18 FBMKLCI at 1,750 level. Our index target represents our second downgrade for the year, post 1Q18’s disappointing reporting season and after factoring in side effect concerns of PH’s manifestoes business-unfriendly regulatory shifts after the government followed up to pressure Telekom Malaysia (TM) to reduce broadband access fees. This pegs the market at 14.9x 2019F earnings, at mean PE, the first time in many years.

Strategy and investment themes. Thematically, deep values and asset monetisation, electrical and electronics (E&E) trend riders, and tourism plays should outperform in 2H18. OVERWEIGHT the E&E-related, gaming and utility sectors, while the plantation sector offers refuge. While gaming duties may be revised up, we expect only a moderate earnings impact on the sector which trades well below mean valuations. Tactically for portfolio boosters, focus on opportunities in heavily sold-down BUY-rated stocks: a) construction-related stocks including Gamuda, IJM Corporation and Malaysian Resources Corporation (MRCB); b) high yielders including Astro Malaysia (Astro); and c) selected mid caps eg Cahya Mata Sarawak, My E.G. Services (MyEG) and Scientex.

Our top picks include large caps Bumi Armada, Genting Malaysia, Inari Amertron, Public Bank and Tenaga Nasional; mid caps Cahya Mata Sarawak, Scientex, Serba Dinamik and VS Industry; and small caps Gabungan AQRS and Yong Tai.

FIGURE 1: KEY STOCK RECOMMENDATIONS

Net Profit EPS PE

Share Price

5 Jul 18 Target Price 2017 2018F 2019F 2017 2018F 2019F 2017 2018F 2019F

Yield 2018F

ROE 2018F

Market Cap

P/B 2018F

Company Ticker Rec (RM) (RM) (RMm) (RMm) (RMm) (sen) (sen) (sen) (x) (x) (x) (%) (%) (US$m) (x)

Large Caps

Bumi Armada BAB MK BUY 0.71 1.06 309 511 547 5.3 8.7 9.3 13.4 8.1 7.6 4.3 8.9 1,024 0.7

Genting Malaysia GENM MK BUY 4.85 6.28 1,407 1,787 2,351 24.9 31.6 41.6 19.5 15.4 11.7 3.6 9.0 6,786 1.4

Inari Amertron INRI MK BUY 2.25 2.68 200 254 351 6.4 8.1 11.2 35.4 27.8 20.1 3.3 34.4 1,748 6.5

Public Bank PBK MK BUY 22.90 25.20 5,470 5,843 6,277 140.9 150.5 161.7 16.3 15.2 14.2 3.0 15.1 21,989 2.2

Tenaga Nasional TNB MK BUY 14.42 17.70 7,330 6,971 6,815 129.1 122.8 120.0 11.2 11.7 12.0 5.0 11.9 20,252 1.4

Small-Mid Caps

Cahya Mata Sarawak CMS MK BUY 2.43 4.00 260 314 318 24.2 29.3 29.6 10.0 8.3 8.2 4.6 12.4 645 1.1

Gabungan AQRS AQRS MK BUY 1.19 1.86 35.7 83 110 6.0 14.1 18.6 19.7 8.5 6.4 3.5 15.7 134 1.3

Scientex SCI MK BUY 7.16 8.20 258 290 363 52.7 59.4 74.2 13.6 12.1 9.6 2.5 17.7 866 2.0

Serba Dinamik SDH MK BUY 3.34 4.30 323 398 514 22.0 27.1 35.0 15.2 12.3 9.5 2.4 23.1 1,213 2.4

VS Industry VSI MK BUY 1.68 1.85 156 148 234 9.3 8.8 13.9 18.0 19.0 12.1 2.1 12.8 697 2.5

Yong Tai YTB MK BUY 1.45 2.10 6 52.4 133 3.5 7.6 19.2 41.4 19.1 6.6 0.0 2.5 173 2.0

Notes: Closing prices as at 5 Jul 18. If year end is before June, earnings are shown in the previous period. Source: Bloomberg, UOB Kay Hian

Ju ly 2018

2

M a l a y s i a S t r a t e g y

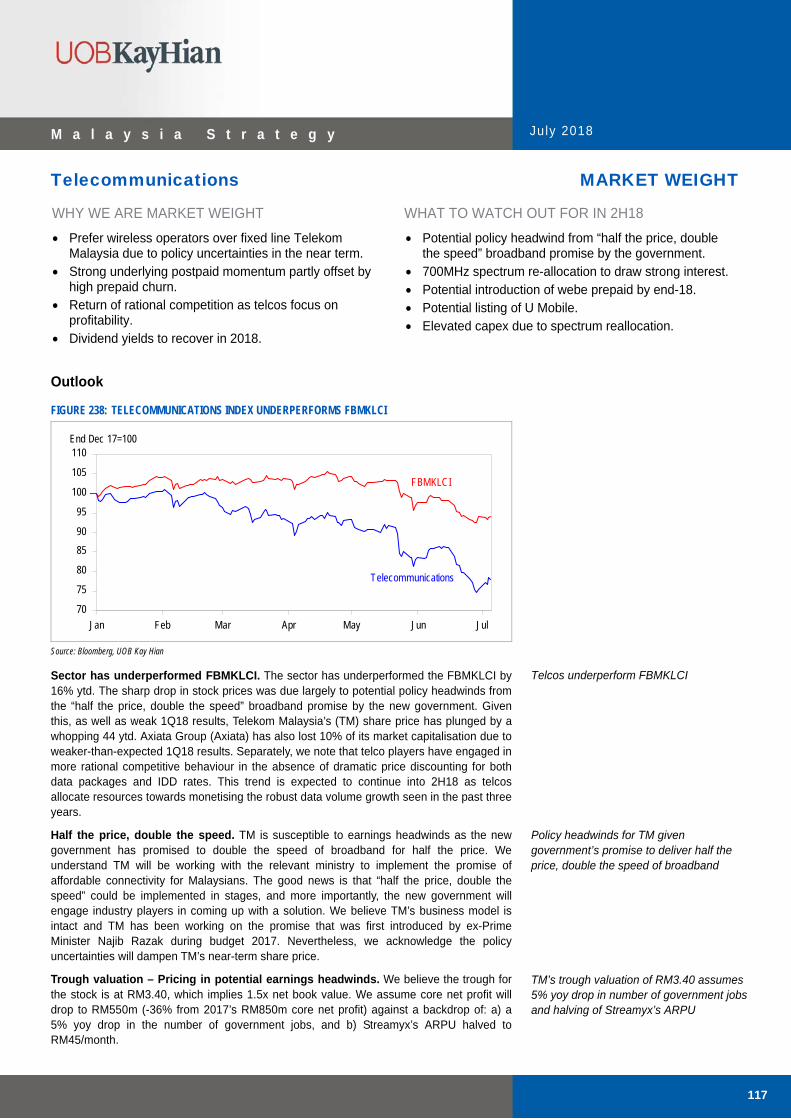

Review Of 1H18: Episodes Of Panic Attacks Market seizures... Although we had expected 2018 to be a challenging year, the broad market downturn came quicker than expected, after reaching an euphoric year-high in end-Jan 18, when surveys by political experts showed that Barisan Nasional (BN) would retain power in the 14th general election (GE14). The FBMKLCI, FBM70 and FBM Small Cap (FBMSC) indices were up 5.5%, 4.4% and 6.1% at their respective year highs. However, the market euphoria was short-lived and steep profit-taking started to set in for small/mid caps in Mar 18, followed by the FBMKLCI in early May (which had been held up by only a handful of stocks), as a series of external and domestic events took shape. As at 5 Jul 18, the FBMKLCI, FBM70 and FBMSC had fallen 5.9%, 8.6% and 18.0%. Subsequently, the FBMKLCI became a prominent regional underperformer post GE14 (Figure 3). Interestingly, many small/mid-cap stocks were already being sold down well before GE14 fears gripped the market.

…roiled by external and domestic events. Market sentiment was initially roiled by the 10-year US treasury breaching the 3% psychological threshold and later, US President Donald Trump’s threat to wage a trade war against China, which worsened the then fragile outlook for technology stocks (tied to poor mobile sales outlook for Apple). These events spiked up global trading volatility – in the US, the CBOE Volatility Index (VIX) rose to a three-year high of 37.3 from exceptionally low levels (below 9.2). Then came PH coalition’s shocking GE14 victory on 9 May, winning 113 out of the 222 parliamentary seats and 8 states.

Sweeping changes from GE14… The broad market tumbled following PH’s surprising win in GE14. PH, under the leadership of 92-year old Tun Mahathir, successfully toppled the then ruling coalition BN’s over-60-year rule of the country. The trail leading to GE14, dubbed as the “mother of all elections”, has been extremely colourful. PH’s open accusations of then prime minister Datuk Seri Najib Razak’s complicity with scandalised Ministry of Finance unit 1MDB, plus its manifestoes (eg to abolish GST and allow freedom of speech), resonated with the majority of the voters. Tun Mahathir’s leadership brought swift measures, including cancelling mega projects the Kuala Lumpur-Singapore High-Speed Rail (HSR) and MRT3, abolishing GST and reintroducing fuel subsidy, and making sweeping changes in the leadership of government agencies and government-linked companies (GLC). Tun Mahathir also appointed the country’s first ethnic Chinese Minister of Finance in decades.

FIGURE 2: SWIFT AND SWEEPING CHANGES BY PAKATAN HARAPAN

Categories Changes

Mega Projects HSR and MRT3 cancelled, Sabah portion of Pan Borneo Highway pending government decision

However, ECRL to proceed and funding for TRX’s infrastructure intact

Subsidies GST abolished from June onwards

Sales and services tax to be revived from September onwards

Fuel subsidy reintroduced for the lower octane RON95, fixed at RM2.20/litre

Government Agency Heads

Dismissed: Attorney General, 1MDB CEO

Resigned: BNM Governor, MACC Chief Commissioner, Senior Judges and Court of Appeal President

GLC Heads Purported 100 GLC heads on the “watchlist”

Resigned: Telekom Malaysia CEO, PNB chief, Petronas Chairman

Not Renewed: MAHB CEO Source: Media, UOB Kay Hian

…a black swan event for construction sector, BN-aligned stocks. Perceivedly BN crony stocks and the construction sector were the worst hit as investors reacted to fears that PH would implement key manifestoes in its first 100 days in office. This stoked fears that faced with tight finances, the PH would renege on past contracts to benefit the citizens, most prominently contracts with toll road concessionaires. Key construction-related stocks have been sold down by >50% since GE14 while MyEG has touched three limit downs.

From euphoria to panic, small caps were the first to be sold down

Initially roiled by US interest rate cycle and potential US-China trade war

PH’s win followed by cancellation of some mega projects, abolishment of GST, introduction of measures to cut living costs, changes in GLC/government agency heads

Mega project-dependent construction stocks and perceivedly BN-aligned stocks among the worst hit

Ju ly 2018

3

M a l a y s i a S t r a t e g y

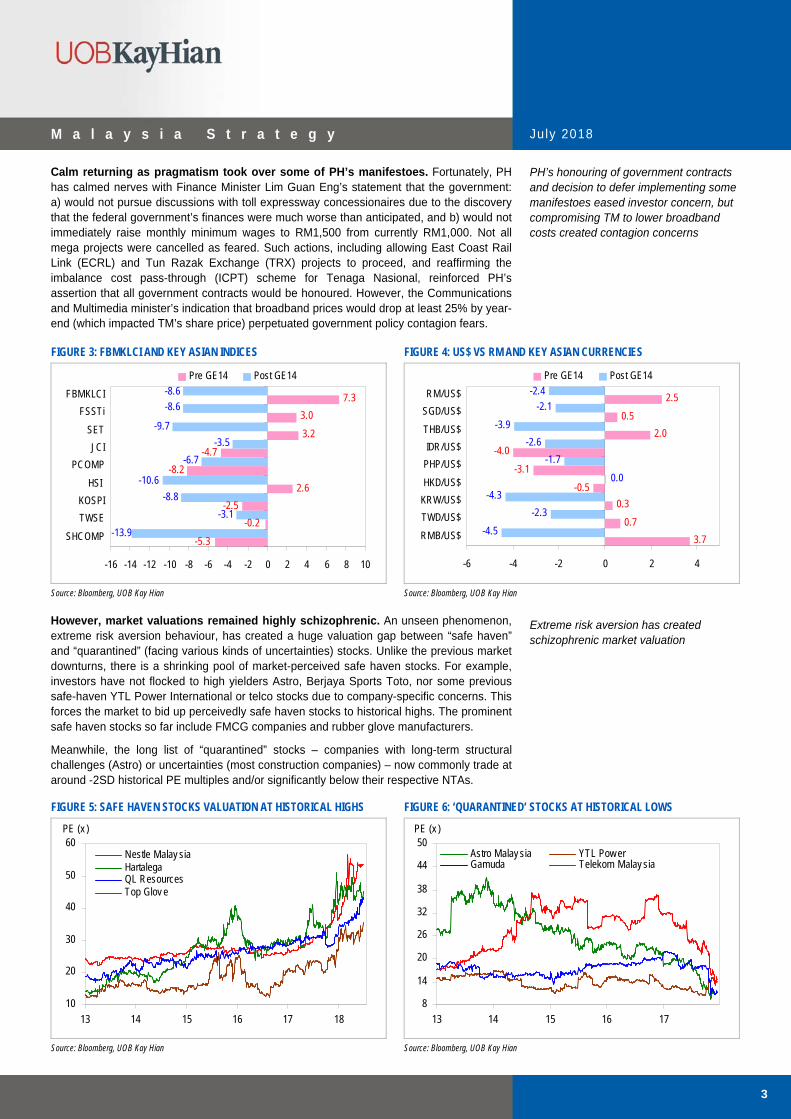

Calm returning as pragmatism took over some of PH’s manifestoes. Fortunately, PH has calmed nerves with Finance Minister Lim Guan Eng’s statement that the government: a) would not pursue discussions with toll expressway concessionaires due to the discovery that the federal government’s finances were much worse than anticipated, and b) would not immediately raise monthly minimum wages to RM1,500 from currently RM1,000. Not all mega projects were cancelled as feared. Such actions, including allowing East Coast Rail Link (ECRL) and Tun Razak Exchange (TRX) projects to proceed, and reaffirming the imbalance cost pass-through (ICPT) scheme for Tenaga Nasional, reinforced PH’s assertion that all government contracts would be honoured. However, the Communications and Multimedia minister’s indication that broadband prices would drop at least 25% by year-end (which impacted TM’s share price) perpetuated government policy contagion fears.

FIGURE 3: FBMKLCI AND KEY ASIAN INDICES FIGURE 4: US$ VS RM AND KEY ASIAN CURRENCIES

-5.3

-0.2

-2.5

2.6

-8.2

-4.7

3.2

3.0

7.3

-13.9

-3.1

-8.8

-10.6

-6.7

-3.5

-9.7

-8.6

-8.6

-16 -14 -12 -10 -8 -6 -4 -2 0 2 4 6 8 10

SHCOMP

TWSE

KOSPI

HSI

PCOMP

JCI

SET

FSSTi

FBMKLCI

Pre GE14 Post GE14

3.7

0.7

0.3

-3.1

-4.0

0.5

2.5

-4.5

-4.3

-1.7

-2.6

-3.9

-2.1

-0.5

2.0

0.0

-2.3

-2.4

-6 -4 -2 0 2 4

RMB/US$

TWD/US$

KRW/US$

HKD/US$

PHP/US$

IDR/US$

THB/US$

SGD/US$

RM/US$

Pre GE14 Post GE14

Source: Bloomberg, UOB Kay Hian Source: Bloomberg, UOB Kay Hian However, market valuations remained highly schizophrenic. An unseen phenomenon, extreme risk aversion behaviour, has created a huge valuation gap between “safe haven” and “quarantined” (facing various kinds of uncertainties) stocks. Unlike the previous market downturns, there is a shrinking pool of market-perceived safe haven stocks. For example, investors have not flocked to high yielders Astro, Berjaya Sports Toto, nor some previous safe-haven YTL Power International or telco stocks due to company-specific concerns. This forces the market to bid up perceivedly safe haven stocks to historical highs. The prominent safe haven stocks so far include FMCG companies and rubber glove manufacturers.

Meanwhile, the long list of “quarantined” stocks – companies with long-term structural challenges (Astro) or uncertainties (most construction companies) – now commonly trade at around -2SD historical PE multiples and/or significantly below their respective NTAs.

FIGURE 5: SAFE HAVEN STOCKS VALUATION AT HISTORICAL HIGHS FIGURE 6: ‘QUARANTINED’ STOCKS AT HISTORICAL LOWS

10

20

30

40

50

60

13 14 15 16 17 18

Nestle Malay siaHartalegaQL ResourcesTop Glov e

PE (x )

8

14

20

26

32

38

44

50

13 14 15 16 17

Astro Malay sia YTL Pow erGamuda Telekom Malay sia

PE (x )

Source: Bloomberg, UOB Kay Hian Source: Bloomberg, UOB Kay Hian

PH’s honouring of government contracts and decision to defer implementing some manifestoes eased investor concern, but compromising TM to lower broadband costs created contagion concerns

Extreme risk aversion has created schizophrenic market valuation

Ju ly 2018

4

M a l a y s i a S t r a t e g y

2H18 Outlook

End-18 FBMKLCI at 1,750 level. Post 1Q18 reporting season in May, and policy spillover concerns exacerbated by the Ministry of Communications and Multimedia’s comments, we cut our end-18 FBMKLCI forecast to 1,750 from 1,830. This pegs the market at a mean PE of 14.9x, the first time in 4 years when the FBMKLCI did not end the year at above-mean valuation. Nevertheless, our assessment still takes into account easing political risk premium and still-ample domestic liquidity that would allow the FBMKLCI to close the year higher above the current level.

Our key macro predictions are tabulated below:

FIGURE 7: KEY ECONOMIC/MARKET PROJECTIONS AND ASSESSMENTS

Indicator Prediction/Assessment for 2018

GDP Growth 5.0% in 2018 (2017: 5.9%)

Improvement in net export growth

Moderate improvement in domestic consumption trends from 2H17

Current Account End-18: 3.0% of GDP

Interest Rate End-18 OPR: 3.25%

MGS yield should rise moderately, driven by US interest rate hikes

Inflation 2.5%

Currency 3Q18: RM3.90/US$; 4Q18: RM3.85/US$; 1Q19: RM3.80/US$

FBMKLCI 1,750 (14.9x 2019F PE)

FBMKLCI Earnings c.2.9% core earnings growth in 2018

ROE remain stagnant at 10.7% in 2018 (Bloomberg data)

Liquidity Foreign ownership of Malaysian equities expected to slide modestly in 2H18, following post-GE14 outflows (ytd 24.2%)

External Factors US: 10-year treasury breaching 3% and reversal of QE

Source: UOB Global Economics & Market Research, UOB Kay Hian

FIGURE 8: FBMKLCI AND PE FIGURE 9: FBMKLCI AND P/B

500

700

900

1,100

1,300

1,500

1,700

1,900

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

10

12

14

16

18

20

22

mean = 14.9x

1sd = 16.4x

2sd = 18.0x

-1sd = 13.4x

(Index ) (x )

FBMKLCI (LHS)

1-y ear PE (RHS) -2sd = 11.9x

500

700

900

1,100

1,300

1,500

1,700

1,900

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

mean = 1.9x

1sd = 2.2x

2sd = 2.5x

-1sd = 1.6x

(Index ) (x)

FBMKLCI (LHS)

1-y ear P/B (RHS)-2sd = 1.3x

Source: Bloomberg, UOB Kay Hian Source: Bloomberg, UOB Kay Hian

A moderately lower FBMKLCI target of 1,750 post 1Q18 results season

Ju ly 2018

5

M a l a y s i a S t r a t e g y

Bracing for global liquidity contraction. Global markets are still bracing for rising global interest rates and the reverse Quantitative Easing (QE) effect, as the respective central banks in the US, EU and Japan are unlikely to stray significantly from their respective schedules of reversing (US) or reducing (EU and Japan) QE activities. Since the Global Financial Crisis (GFC) a decade ago, these countries’ federal budgets have been indirectly supported by their respective central banks via QE, resulting in the central banks having exceptionally swollen balance sheets. The reversal or reduction of QE activities raises interest rate expectations and elevates risk aversion, which implies lower equity valuation and aversion to the perceivedly riskier emerging markets.

FIGURE 10: UPDATES ON QE SCHEDULES IN US, EU AND JAPAN FIGURE 11: CENTRAL BANK ASSETS – CURRENT VS PRE-GFC

Central 2018F QE as a 2017 QE as a Bank % to Govt Deficit % to Govt Deficit QE Policies Projections

US Fed (52.2) 0.54 Total assets reduced by US$0.14t (end 17-Jun 18). BSR programme to increase to US$40b in July 18. Annual cuts to increase to US$420b in 2018 and US$600b in 2019 (US$30b in 4Q17).

ECB 219.2 520.5 Total assets expanded by €0.81t (end 16-end 17). Monthly net asset purchases of €30b until Sep 18 and later decreased to €15b in 4Q18.

BoJ 94.8 162 Total assets expanded by ¥15.6t (end 17-Jun 18). Bond buying has moderated to an annualised ¥33.8t (as of 1H18), way below its official target of ¥80t.

Pre GFC Current Central Bank (2007) (2017)

US Fed US$0.9t US$4.4t

ECB EUR1.5t EUR4.5t

BoJ JPY111.3t JPY521.4.0t

Note: All values are expressed in US$ unless stated otherwise Source: BOJ, ECB, FOMC, Media, UOB Global Economics & Market Research, UOB Kay Hian

Source: BOJ, ECB, FOMC, Media, UOB Kay Hian

Rising interest rate expectations. While we expect Malaysia’s policy rate to be held steady at 3.25% in 2H18, the Malaysian Government Securities (MGS) rate is bound to rise, in tandem with the expected rise in US treasury rate. We also note that the interest rate spread between the 10-year MGS and US treasury of around 1.32ppt (vs 10-year average of 1.38ppt) may be too benign in the current environment.

FIGURE 12: 10-YEAR MGS AND 10-YEAR US TREASURY RATE DIFFERENTIAL

0

10

20

30

40

50

60

06 07 08 09 10 11 12 13 14 15 16 17 18

-2

-1

0

1

2

3Foreign Holdings of MGS (%) (LHS)MGS-US Treasury Differential (RHS)

(%) (%)

Source: Bloomberg, UOB Kay Hian

Nevertheless, easing risk premium on domestic factors could lead to near-term market recovery. Despite lingering policy uncertainties (eg fate of some mega projects and heads of GLCs/government agencies) and the prime minister’s curious wish to have a new national car company (since a significant stake in Proton was sold to China’s Geely), PH’s commitment to maintaining the sanctity of contracts and honouring all government debts/contracts, plus earnings recovery from a widely disappointing 1Q18 season, should lead to further recoveries in many heavily sold-down stocks. In addition, 2Q-3Q18 domestic consumption trends should be positive, following the abolishment of the 6% GST in June, and the delayed reinstatement of the old sales and services tax (SST) in Sep 18.

Tighter global liquidity a negative for emerging markets

Rising interest rate expectation for MGS also reflects a too benign rate spread to US treasury

Modest market recovery despite some lingering issues relating to…

Ju ly 2018

6

M a l a y s i a S t r a t e g y

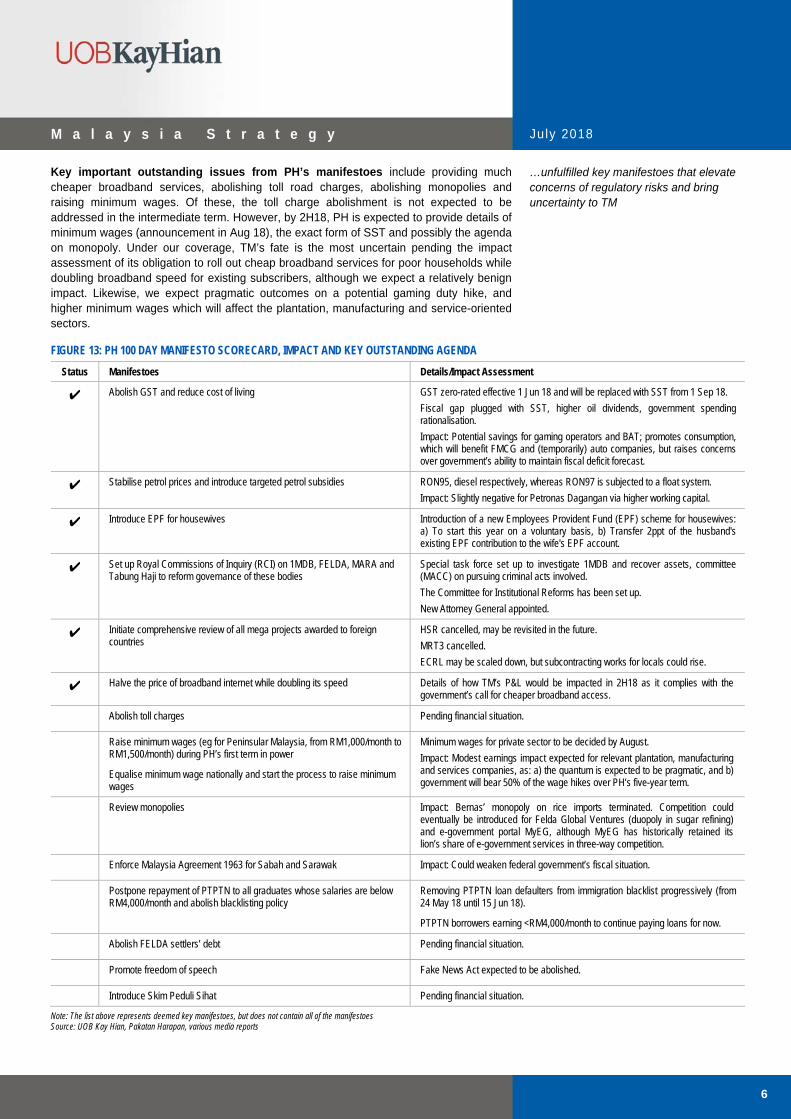

Key important outstanding issues from PH’s manifestoes include providing much cheaper broadband services, abolishing toll road charges, abolishing monopolies and raising minimum wages. Of these, the toll charge abolishment is not expected to be addressed in the intermediate term. However, by 2H18, PH is expected to provide details of minimum wages (announcement in Aug 18), the exact form of SST and possibly the agenda on monopoly. Under our coverage, TM’s fate is the most uncertain pending the impact assessment of its obligation to roll out cheap broadband services for poor households while doubling broadband speed for existing subscribers, although we expect a relatively benign impact. Likewise, we expect pragmatic outcomes on a potential gaming duty hike, and higher minimum wages which will affect the plantation, manufacturing and service-oriented sectors.

FIGURE 13: PH 100 DAY MANIFESTO SCORECARD, IMPACT AND KEY OUTSTANDING AGENDA

Status Manifestoes Details/Impact Assessment

✔ Abolish GST and reduce cost of living GST zero-rated effective 1 Jun 18 and will be replaced with SST from 1 Sep 18.

Fiscal gap plugged with SST, higher oil dividends, government spending rationalisation.

Impact: Potential savings for gaming operators and BAT; promotes consumption, which will benefit FMCG and (temporarily) auto companies, but raises concerns over government’s ability to maintain fiscal deficit forecast.

✔ Stabilise petrol prices and introduce targeted petrol subsidies RON95, diesel respectively, whereas RON97 is subjected to a float system.

Impact: Slightly negative for Petronas Dagangan via higher working capital.

✔ Introduce EPF for housewives Introduction of a new Employees Provident Fund (EPF) scheme for housewives: a) To start this year on a voluntary basis, b) Transfer 2ppt of the husband's existing EPF contribution to the wife's EPF account.

✔ Set up Royal Commissions of Inquiry (RCI) on 1MDB, FELDA, MARA and Tabung Haji to reform governance of these bodies

Special task force set up to investigate 1MDB and recover assets, committee (MACC) on pursuing criminal acts involved.

The Committee for Institutional Reforms has been set up.

New Attorney General appointed.

✔ Initiate comprehensive review of all mega projects awarded to foreign countries

HSR cancelled, may be revisited in the future.

MRT3 cancelled.

ECRL may be scaled down, but subcontracting works for locals could rise.

✔ Halve the price of broadband internet while doubling its speed Details of how TM’s P&L would be impacted in 2H18 as it complies with the government’s call for cheaper broadband access.

Abolish toll charges Pending financial situation.

Raise minimum wages (eg for Peninsular Malaysia, from RM1,000/month to RM1,500/month) during PH’s first term in power

Equalise minimum wage nationally and start the process to raise minimum wages

Minimum wages for private sector to be decided by August.

Impact: Modest earnings impact expected for relevant plantation, manufacturing and services companies, as: a) the quantum is expected to be pragmatic, and b) government will bear 50% of the wage hikes over PH’s five-year term.

Review monopolies Impact: Bernas’ monopoly on rice imports terminated. Competition could eventually be introduced for Felda Global Ventures (duopoly in sugar refining) and e-government portal MyEG, although MyEG has historically retained its lion’s share of e-government services in three-way competition.

Enforce Malaysia Agreement 1963 for Sabah and Sarawak Impact: Could weaken federal government’s fiscal situation.

Postpone repayment of PTPTN to all graduates whose salaries are below RM4,000/month and abolish blacklisting policy

Removing PTPTN loan defaulters from immigration blacklist progressively (from 24 May 18 until 15 Jun 18).

PTPTN borrowers earning <RM4,000/month to continue paying loans for now.

Abolish FELDA settlers’ debt Pending financial situation.

Promote freedom of speech Fake News Act expected to be abolished.

Introduce Skim Peduli Sihat Pending financial situation.

Note: The list above represents deemed key manifestoes, but does not contain all of the manifestoes Source: UOB Kay Hian, Pakatan Harapan, various media reports

…unfulfilled key manifestoes that elevate concerns of regulatory risks and bring uncertainty to TM

Ju ly 2018

7

M a l a y s i a S t r a t e g y

Malaysia’s economic fundamentals are generally intact. Supporting our view are: a) real GDP growth which remains strong at >5% (although the newly-installed prime minister suspected that the officially released 1Q18 GDP growth of 5.4% may be too high); and b) improving current account which is currently at a surplus of RM15b, or 4.5% of GNI (2017: 3.1% of GNI). Our channel checks have already detected a discernible consumption pick-up post CNY, and we expect the three-month reprieve from the abolishment of GST (Jun-Sep 18) to at least temporarily spur domestic consumption (eg long booking queues for cars).

FIGURE 14: ANECDOTES AND CHANNEL CHECKS

Sector Channel Checks

Automobile Vehicle sales should spike up during the three-month tax-free period from 1 Jun until end-Aug 18, and tank thereafter following the introduction of the SST on 1 Sep 18.

Cumulative 4M18 TIV dipped 0.7% yoy to 182,229 units. We forecast 2017 TIV of 595,000 units (+2.5% yoy), while MAA’s 2017 TIV forecast stands at 590,000 units (+1.7% yoy).

Building Materials Demand for steel and cement should improve in 2H18 with ECRL proceeding but not as strong as originally hoped.

Banking & Insurance 4M18 loans growth remained modest at 4.8% while residential approval rate by value remained a relatively low 42% vs five-year average of 47%.

General insurance net premium growth was sluggish at 0.71% in 2017 and is likely to have remained weak in 1H18 as motor insurance, which is a major segment, will continue to remain lacklustre given the flattish 4M18 auto sales trend.

Life insurance business grew 3.9% in 2017, in line with 10-year historical average.

Consumer - F&B,

Brewery and Food Retail

F&B: Sales volumes of low-ticket staple products remained resilient, although demand for carbonated soft drinks still contracted.

Brewery: Mid-single-digit sales volume growth in 1Q18 driven by hefty CNY promotions.

Food Retail: Positive SSSG was charted by Starbucks operations and momentum should continue in 2H18.

Consumer - Retail Retail Group Malaysia projects a 5.3% growth in retail sales for 2018. This is driven by: a) boost in consumer confidence on the three-month tax break, and b) surge in discounts and promotions offered by retailers during this once-in-a-lifetime opportunity.

Consumer - Tobacco Demand stabilising with lower (low single digit) yoy volume decline in 1Q18.

Gaming - NFO NFOs’ ticket sales per draw stable to improving.

High-single-digit gaming volume growth (both VIP and mass market) ytd, led by capacity expansion.

Healthcare Signs of improvement in demand seeing the pickup in inpatient traffic (+3% yoy) in 1Q18.

Media Print media still impacted by weak ad spending.

Weaker contribution from subscription segment (-4.0% yoy).

Property 1Q18 sales meeting modest annual targets, but demand outlook remains sluggish, requiring developers to offer steep discounts.

REITs Tenant sales remain sluggish at general retail and have moderated at prime retail malls.

Rental reversion at low single digits for high-end retail malls but flat/lower rentals for mass retail.

Telecommunications The Big 3 celcos (ie Celcom, DiGi.Com and Maxis) experienced a 1% decline in service revenue in 1Q18 high prepaid customer churn.

Source: UOB Kay Hian

A relatively benign outlook for the ringgit. Surprisingly the ringgit has softened by only 1.4% against the greenback (as at 5 July) since GE14, despite massive foreign selloffs, particularly in the bond market. While Bank Negara Malaysia’s (BNM) foreign reserves eased by only US$1b in May to US$108.5b, BNM’s net short position in forex swaps widened to US$9.7b (8.8% of total foreign reserves) in May vs US$6.9b net short in April. Supporting a relatively benign worst-case scenario for only a moderate drop (consensus: RM4.00/US$) is the view that the federal government’s debt (50.8% of 2018F GDP, 36.1% including all contingent liabilities) remains manageable, especially with a much more financially prudent government in place.

The market, however, would need to be convinced that the PH government can maintain the 2.8% fiscal deficit target for 2018, given the balancing act of cutting money politics from the federal budget to fund public goods (eg abolishing GST, reinstating fuel subsidy). Adding to such an uncertainty, Daim Zainuddin, the country’s former Finance Minister and currently a member of the Council of Elders that serves as an advisory role to the government, said there were other “mini 1MDBs” in the government. There is also the overhanging issue of Sabah’s and Sarawak’s demands for a much higher oil revenue royalty from 5% currently.

Benign outlook for hitherto resilient ringgit despite massive foreign selloffs in capital market

Much depends on fiscal deficit assessment

Generally healthy economic vital signs

Ju ly 2018

8

M a l a y s i a S t r a t e g y

FIGURE 15: TWEAKINGS IN 2018 FEDERAL BUDGET

Budget 2018 Revised Difference (RMb) (RMb) (RMb) Change vs Budget 2018

Total Federal Government Revenue (A) 239.9 233.3 (6.6) RM6.6b net decrease in revenue

Direct Tax 127.7 133.1 +5.4

of which PITA 11.4 16.8 +5.4 Increase in taxes due to rise in global oil prices

Indirect Tax 63.9 46.9 (17)

of which GST 43.8 22.8 (21) Income loss from zero-rated GST

SST n.a. 4 +4 New proceeds from SST (effective 1 Sep 18)

Non-tax Revenue 48.3 53.3 +5

of which Investment Income 24.6 29.6 +5 Higher dividend from GLCs

Operating Expenditure (B) 234.3 228.0 (6.3) RM6.3b net decrease in opex

0.7 Additional spending for Hari Raya special assistance

3.0 Additional spending for petrol stabilisation programme

(10.0) Savings from expenditure rationalisation programme

Net Development Expenditure (C) 45.4 45.4 Unchanged Development expenditure less RM600m loan recovery

Overall Balance (A) - (B) - (C) (39.8) (40.1) (0.3) RM300m net increase in expenditure

Fiscal/Budget Deficit (as a % of GDP) 2.80% 2.82%

Source: The Edge Weekly, UOB Kay Hian

Modest foreign equity outflows anticipated. Foreign investors continued to be net sellers after selling RM5.6b in equities in May, resulting in a year-to-May net outflow of RM3.6b. Nevertheless, we expect foreign outflow to slow down given the moderate estimated foreign portfolio ownership of only 16% (the overall foreign equity shareholding improved by 0.8ppt in Jan-Mar 18 to 24.2%).

The bond market experienced a heavy selldown in May, with foreign investors selling RM12.9b in May (Apr: -RM4.7b), reducing their collective ownership of government bonds to 14.2% (mainly represented by the 41.9% ownership of MGS). Nevertheless, going forward, mitigation factors include a relatively resilient ringgit outlook and the lower amount of MGS maturing in 2018 vs 2017.

FIGURE 16: MGS MONTHLY MATURITY AND NET FOREIGN FUND FLOWS IN MALAYSIAN BOND MARKET

MGS Monthly Maturity Net Foreign Fund Flows in the Malaysian Bond Market

2018 2019 2018 Month (RMb) (RMb) (RMb)

Jan 2.0 0.0 4.47

Feb 14.1 0.0 (3.94)

Mar 8.8 7.2 2.88

Apr 0.0 0.0 (4.69)

May 0.0 0.0 (12.91)

Jun 0.0 0.0 n.a.

Jul 0.0 7.3 n.a.

Aug 0.0 0.0 n.a.

Sep 11.4 0.0 n.a.

Oct 2.0 11.8 n.a.

Nov 0.0 17.1 n.a.

Dec 0.0 0.0 n.a.

Source: Bloomberg, CEIC, UOB Kay Hian

Foreign net selling of equities to abate in 2H18, given the already low portfolio ownership

Bond selloff should also moderate in 2H18

Ju ly 2018

9

M a l a y s i a S t r a t e g y

Earnings Outlook

2018-19 earnings forecasts cut. Following the dismal 1Q18 results, we cut our 2018 and 2019 earnings forecasts by 2.6% and 2.4% for the FBMKLCI, and 3.3% and 2.1% for our coverage universe. We now expect the FBMKLCI’s and our universe’s earnings to grow 2.5% and 3.9% in 2018, and 7.5% and 9.3% in 2019. By sector, 12 suffered significant downward earnings revisions (particularly aviation, O&G offshore contractors and plantation, shipping segments, technology, telecommunications and utility), while only two sectors (automobile and gaming) had notable upgrades (Figure 17).

1Q18 was especially rocky for government-reliant companies. For 1Q18, only 8.5% of the companies in our universe beat expectations while 26.4% disappointed, making it one of the worst quarters (Figure 20). While disappointments were seen across the board, some prominent earnings disappointments were presumably linked to GE14 (particularly in the telecommunications sector) and weak US dollar losers (E&E and furniture). Among the large caps, Axiata Group and TM significantly disappointed but banks mildly beat expectations. Prominent beaters are a handful of banks and automobile companies.

FIGURE 17: CORPORATE EARNINGS GROWTH BY SECTOR

Earnings Growth (%)

Sector Weight (%) 2017 2018F 2019F

Automobile 0.9 (0.6) 41.0 16.0

Aviation 1.8 2.8 (20.5) 14.0

Banking 39.8 14.3 9.5 7.1

Building Material 1.1 27.8 14.7 43.8

Conglomerate 2.0 1.5 (1.5) 9.9

Construction 2.6 (3.9) 32.2 7.9

Consumer 3.2 (8.8) 3.5 8.9

Exchange 0.3 15.2 4.2 (4.7)

Gaming 7.0 8.1 28.3 15.4

Glove Manufacturing 1.6 7.4 28.8 15.7

Healthcare 0.3 11.9 3.4 5.1

Insurance 0.4 (0.5) 9.0 8.1

Manufacturing 1.0 30.8 8.6 33.2

Media 0.9 3.5 (0.4) 3.5

O&G - Heavy Engineering 1.2 23.4 22.9 24.0

O&G - Asset Owners 2.5 75.5 1.7 6.7

O&G - Offshore Contractors (0.1) (166.3) n.m. n.m.

O&G - Shipping 2.3 7.5 (27.2) 17.2

Plantation 5.5 33.5 (3.3) 2.3

Port 0.7 (1.4) (20.3) 17.3

Property 3.1 (1.5) (19.8) 13.4

REITs 2.6 (2.0) 5.4 6.5

Technology 0.7 44.6 25.3 30.5

Telecommunications 7.4 (3.3) (8.3) 12.3

Utility 11.4 (4.9) (4.8) (0.3)

UOBKH Coverage 6.8 3.9 9.3

FBMKLCI 6.9 2.5 7.5

Source: Bloomberg, UOB Kay Hian

2018-19 FBMKLCI earnings expected to grow 2.5% and 7.5% in 2018-19…

…as 1Q18 reporting season turned out to be one of the worst in recent reporting seasons

Ju ly 2018

10

M a l a y s i a S t r a t e g y

FIGURE 18: FBMKLCI – EARNINGS BY SECTOR FIGURE 19: BLOOMBERG – FBMKLCI EPS ESTIMATES

Gaming

8%

Plantation

7%

Others

6%

O&G

9%

Consumer

1% Bank

43%

Utility

19%

Telco

7%

97

99

101

103

105

107

109

111

113

115

11 12 13 14 15 16 17 18

(Index )

Bloomberg Estimated EPS

Source: Bloomberg, UOB Kay Hian Source: Bloomberg, UOB Kay Hian

FIGURE 20: QUARTERLY RESULTS FIGURE 21: UOB KAY HIAN – NOTABLE EPS DOWNGRADES

7 9 1326

10 11 1427

17 11 16 198

62 57 51

51

58 5260

5157 62 59 56

65

32 33 3623

32 3726 23 26 27 25 25 26

0

20

40

60

80

100

1Q15 3Q15 1Q16 3Q16 1Q17 3Q17 1Q18

Abov e In line Below(%)

Quarter Sector With Earnings Downgrades

2Q16 Automobile, Banking, Gaming, Oil & Gas, Plantation, Technology, Telecommunications

3Q16 Automobile, Oil & Gas, Telecommunications

4Q16 Banking, Plantation

1Q17 Aviation, Consumer, Insurance, Ports, Telecommunications

2Q17 Automobile, Conglomerate, Oil & Gas, Small/mid Caps

3Q17 Automobile, Exchange, Healthcare, Oil & Gas

4Q17 Building Material, Insurance

1Q18 Oil & Gas, Manufacturing, Plantation, Technology, Telecommunications, Aviation

Source: UOB Kay Hian Source: UOB Kay Hian Nevertheless, corporate earnings should improve from 2Q18 onwards. We regard the 1Q18 reporting season as an anomaly and linked to GE14, eg TM’s annualised 1Q18 earnings represented merely under 50% of the pre-1Q18 consensus core profit forecast. We understand that TM’s earnings underperformance could be partially explained by higher variable wage costs. In addition, some other companies could have exercised more prudent revenue recognition post GE14.

2Q18’s core corporate earnings should recover from 1Q18’s anomalous earnings

Ju ly 2018

11

M a l a y s i a S t r a t e g y

Strategy

Maintaining a defensive stance in 2H18. We continue to expect a cautious investment environment in 2H18 to mainly reflect external concerns, noting as well that global risk-taking may moderate with the impact of cumulative interest rate hikes and the Fed’s deleveraging in the US. Stick to lower-beta, larger-cap stocks.

Nevertheless, we foresee near-term trading opportunities as many stocks have not sufficiently recovered from the post-GE14 shock selldown. Market valuations have turned too schizophrenic – bidding up many perceivedly safe haven and dependable growth stocks to stratospheric heights, while trampling down perceivedly vulnerable stocks to well under -1SD mean valuations.

We continue to expect selected mid caps in our universe to outperform the market, as economic conditions continue to support these companies to deliver relatively attractive two-year (2017-19) earnings CAGR of 13.5% vs the FBMKLCI’s 5.0%.

FIGURE 22: FBMKLCI , FBM70 & FBMSC – PERFORMANCE AND EARNINGS GROWTH

85

90

95

100

105

110

115

120

125

130

15 16 17 18

FBMKLCIFBM70FBMSC

Index = 100 (2015)

2016 2017 Year-to-5 Jul 18

(%) Index Perf

Earnings Growth

Index Perf

Earnings Growth

Index Perf

Earnings Growth

FBMKLCI (3.0) 5.4 9.5 5.4* (5.9) (7.2)*

FBM70 (0.8) (32.9) 23.4 77.1 (8.6) 5.8

FBMSC (7.7) 0.7 15.9 (73.0) (18.0) n.m.

Source: Bloomberg * UOBKH forecast differs Source: Bloomberg

Our calls are not unduly influenced by level of foreign shareholdings. Specifically, we do not expect stock performances to be dampened just because of high foreign portfolio ownership. We assess that the foreign investors who are currently invested in Malaysian equities are mostly driven by the fundamentals of their investee companies, are comfortable with the country’s macroeconomic situation, and at worst have only a modest negative bias on the ringgit’s outlook. Supporting this view that many foreign funds did not take the wholesale knee-jerk approach of selling out post GE14, we observed that many of the heavily sold-down stocks post GE14 which were well owned by foreign portfolio funds, had at worst modestly lower foreign shareholdings (eg MyEG, Cahya Mata Sarawak).

OVERWEIGHT E&E, gaming and utilities. We expect dependable growth stocks (particularly E&E stocks) and tourism-related beneficiaries (eg casino stocks) to outperform the market. While gaming duties could be raised to beef up government revenues, we expect at worst moderate earnings impact on an already cheap sector (see our gaming sector report). Defensive sectors like utilities and selected plantation stocks should also appeal. Market conditions are also favourable to selected O&G segments (FPSO).

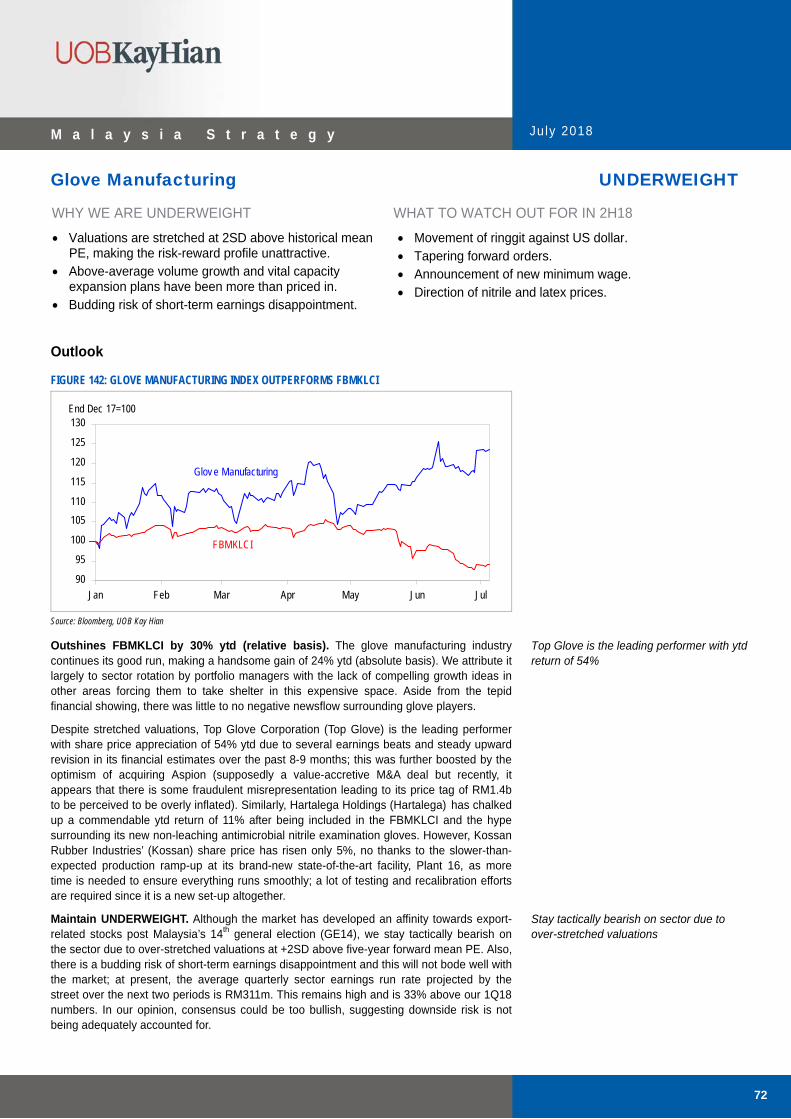

However, UNDERWEIGHT overly expensive sectors, most prominently the glove manufacturing sector, which has risen >104% since 2017, resulting in unhealthy valuations (sector’s 2017-19 PEG ratio at 1.6x). This sector’s earnings growth may continue to disappoint, particularly when more of China’s glove manufacturers reactivate their plants after complying with the government’s environmental regulation to run natural gas-operated plants. At some point in time, mean reversion trade would deflate the overly-expensive sectors and stocks (eg Nestle which sports a 2019F PE of 44x). Among the large-cap sectors, banks may also underperform in the interim period, should foreign investors continue to exit, as banks were primary recipients of foreign equity inflows in 2017.

Stay defensive amid global liquidity contraction

Position for trading opportunities in overly-sold GE14 losers

Expect some mid caps to remain robust

High foreign ownership not an undue concern for fundamentally strong companies

Plantation is a notable defensive sector

UNDERWEIGHT overstretched sectors and stocks, in view of eventual mean reversion trade; banks may mildly underperform should foreign investors continue to exit

Ju ly 2018

12

M a l a y s i a S t r a t e g y

We maintain MARKET WEIGHT on battered down construction-related sectors. Although the sector now lacks optimism on orderbook sustainability beyond 2021, trading opportunities abound as most construction stocks sport historically cheap valuations and fat orderbooks that will sustain earnings through 2020. We expect valuations to eventually reincorporate some option values for the government to reactivate selected mega projects on the longer horizon, which lifts earnings prospects beyond 2020.

FIGURE 23: 2017 SECTOR PERFORMANCES

-38

-15

-31

29

-7 -9 -11

-25 -26-19

-23

-34

-22

2317

13 127 7

4 2 0 -2

-7 -7

-50

-40

-30

-20

-10

0

10

20

30

40

Con

sum

er

Glo

ve M

anuf

actu

ring

O&G

- H

eavy

Eng

Auto

mob

ile

Exch

ange

Avia

tion

Hea

lthca

re

Con

glom

erat

e

O&G

- As

set

Insu

ranc

e

Bank

ing

Plan

tatio

n

Port

Util

ity

Gam

ing

REI

Ts

O&G

- O

ffsho

re

O&G

- Sh

ippi

ng

Tele

com

mun

icat

ions

Prop

erty

Man

ufac

turin

g

Build

ing

Mat

eria

l

Tech

nolo

gy

Con

stru

ctio

n

Med

ia

KLCI: -5.9%

(Ytd %)

Source: Bloomberg, UOB Kay Hian

FIGURE 24: SECTOR PE VALUATION VS HISTORICAL MEAN

PE (x) Historical (x)

Sector 2017 2018F 2019F -1SD Mean +1SD

Automobile 19.8 14.0 12.1 10.9 13.9 16.9

Aviation 15.5 19.5 17.1 11.5 16.0 20.6

Banking 13.4 12.2 11.4 11.1 13.4 15.6

Construction 14.7 11.1 10.3 9.4 16.1 22.8

Consumer 36.3 35.1 32.3 19.0 22.3 25.6

Exchange 27.3 26.2 27.5 21.0 26.0 31.0

Gaming 16.8 13.1 11.4 11.7 13.9 16.1

Glove Manufacturing 44.7 34.7 30.0 13.8 17.7 21.6

Healthcare 25.1 24.2 23.1 16.0 23.3 30.6

Manufacturing* 16.0 14.8 11.1 9.5 13.0 16.5

Media 12.5 12.6 12.2 19.4 24.3 29.1

Oil & Gas 21.0 22.1 18.1 13.2 16.7 19.5

Plantation 23.0 24.0 22.0 20.0 26.0 31.0

Port 18.2 22.8 19.4 18.1 21.3 24.0

Property 11.7 14.6 12.9 8.4 13.7 19.0

Technology 34.1 25.2 18.6 11.8 17.6 23.4

Telecommunications 21.8 23.8 21.2 14.4 16.3 18.2

Utility 11.4 12.0 12.1 11.6 13.9 16.3

Overall 17.0 16.4 15.0 13.4 14.9 16.4

Indicates sectors trading below mean PE

Indicates sectors trading over +1SD vs mean PE

* Based on calenderisation Source: UOB Kay Hian

MARKET WEIGHT the battered down construction sector, which provides good interim trading opportunities

Ju ly 2018

13

M a l a y s i a S t r a t e g y

Investment Themes

Key investment themes prescribed for 2H18 include: a) multi-year running E&E trend riders, b) tourism-related plays, c) M&A and asset monetisation, and d) deep value stocks. The first two themes relate to expected catalytic events in 2H18, eg selected E&E stocks are big beneficiaries of new contract manufacturing products, and the tourism-related theme is enlivened by the planned openings of Yong Tai’s iconic Encore Melaka theatre (July 18) and Genting Malaysia’s 20th Century Fox theme park (4Q18). Peering into 2019, celcos in advanced nations could be starting to adopt 5G technology, which should lift the outlook for semiconductor-related companies.

FIGURE 25: KEY EXTERNAL EVENTS AND ANTICIPATED EVENTS

Events that create potential flashes of good returns Source: Various sources, UOB Kay Hian

The clear beneficiaries of the first two investment themes include Globetronics Technology, Inari Amertron and VS Industry (E&E); Yong Tai and Genting Malaysia (tourism); as well as Magnum and MRCB (M&A/asset monetisation).

FIGURE 26: MULTI-YEAR INVESTMENT THEMES

Market Share Price Target PE P/B Div Yield Cap 5 Jul 18 Price 2018F 2018F 2018F Company Ticker Rec (US$m) (RM) (RM) (x) (x) (x) Catalyst

(A) E&E TREND RIDERS

Globetronics Technology

GTB MK BUY 370 2.24 2.52 17.7 5.0 4.5 Ramping up in sensor and laser headlamp production volume in 2H18-2019

Inari Amertron INRI MK BUY 1,748 2.25 2.68 20.5 6.5 3.3 Securing new businesses from existing clients, particularly OSRAM

VS Industry* VSI MK BUY 697 1.68 1.85 21.4 2.5 2.1 Backed by recent acquisition of an existing plant, and completion of a new plant in mid-18; to focus on securing new contracts from existing key customers and new customers

(B) TOURISM-RELATED

Genting Malaysia

GENM MK BUY 6,786 4.85 6.28 15.4 1.4 3.6 Opening of internationally iconic 20th Century Fox theme park by 4Q18 should lift visitorship by >20%

Yong Tai YTB MK BUY 173 1.45 2.10 19.1 2.0 0.0 Opening of Encore Melaka theatre in Jul 18 a key catalyst to multi-year earnings growth

(C) ASSET MONETISATION

Magnum MAG MK BUY 736 2.09 2.50 12.6 1.2 5.6 Potential listing or trade sale of 6.3%-owned U-Mobile allows restoration of generous dividend payout

MRCB MRC MK BUY 297 0.605 1.01 18.0 0.5 3.3 Stake sale of Bukit Jail property development to EPF lowers net debt to equity to 11%; still hopes to sell EDL (2H18) and Menara Celcom (in 2019)

* FY already expired; data reflects actual reported number. Source: Bloomberg, UOB Kay Hian

Key 2H18 investment themes include E&E trend riders, tourism-related plays, M&A/asset monetisation and deep value stocks

Globetronics Technology, Inari Amertron and VS Industry (E&E), Yong Tai and Genting Malaysia (tourism) to benefit

Others

4Q181Q18

Construction

Macro

2Q18 3Q18

CorporateYong Tai’s Impression Melaka

HSR, MRT3 Projects Cancelled

GE-14

GENM: Opening of 20th Century Fox

New Products ramp-up by E&E companies

PH’s win

Mega projects ECRL & TRX to proceed

GST AbolishedSST implementationUS-China

Trade War broke out

US 10 Yr Treasury

breached 3%

PH’s 1st Budget AnnouncementNew min wage to

be announced

Expected to proceed: Pan Borneo Sabah

MCMC: Fixed broadband prices to drop by ≥25%Others

4Q181Q18

Construction

Macro

2Q18 3Q18

CorporateYong Tai’s Impression Melaka

HSR, MRT3 Projects Cancelled

GE-14

GENM: Opening of 20th Century Fox

New Products ramp-up by E&E companies

PH’s win

Mega projects ECRL & TRX to proceed

GST AbolishedSST implementationUS-China

Trade War broke out

US 10 Yr Treasury

breached 3%

PH’s 1st Budget AnnouncementNew min wage to

be announced

Expected to proceed: Pan Borneo Sabah

MCMC: Fixed broadband prices to drop by ≥25%

Ju ly 2018

14

M a l a y s i a S t r a t e g y

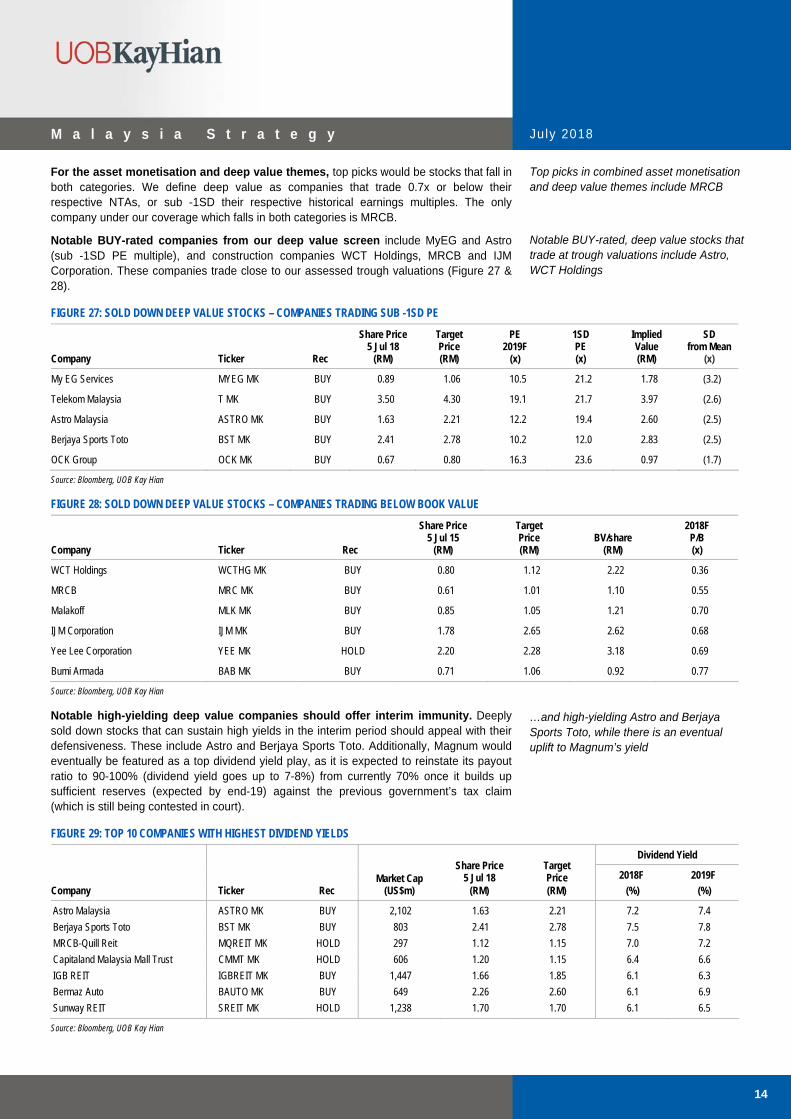

For the asset monetisation and deep value themes, top picks would be stocks that fall in both categories. We define deep value as companies that trade 0.7x or below their respective NTAs, or sub -1SD their respective historical earnings multiples. The only company under our coverage which falls in both categories is MRCB.

Notable BUY-rated companies from our deep value screen include MyEG and Astro (sub -1SD PE multiple), and construction companies WCT Holdings, MRCB and IJM Corporation. These companies trade close to our assessed trough valuations (Figure 27 & 28).

FIGURE 27: SOLD DOWN DEEP VALUE STOCKS – COMPANIES TRADING SUB -1SD PE

Share Price Target PE 1SD Implied SD 5 Jul 18 Price 2019F PE Value from Mean Company Ticker Rec (RM) (RM) (x) (x) (RM) (x)

My EG Services MYEG MK BUY 0.89 1.06 10.5 21.2 1.78 (3.2)

Telekom Malaysia T MK BUY 3.50 4.30 19.1 21.7 3.97 (2.6)

Astro Malaysia ASTRO MK BUY 1.63 2.21 12.2 19.4 2.60 (2.5)

Berjaya Sports Toto BST MK BUY 2.41 2.78 10.2 12.0 2.83 (2.5)

OCK Group OCK MK BUY 0.67 0.80 16.3 23.6 0.97 (1.7)

Source: Bloomberg, UOB Kay Hian

FIGURE 28: SOLD DOWN DEEP VALUE STOCKS – COMPANIES TRADING BELOW BOOK VALUE

Share Price Target 2018F 5 Jul 15 Price BV/share P/B Company Ticker Rec (RM) (RM) (RM) (x)

WCT Holdings WCTHG MK BUY 0.80 1.12 2.22 0.36

MRCB MRC MK BUY 0.61 1.01 1.10 0.55

Malakoff MLK MK BUY 0.85 1.05 1.21 0.70

IJM Corporation IJM MK BUY 1.78 2.65 2.62 0.68

Yee Lee Corporation YEE MK HOLD 2.20 2.28 3.18 0.69

Bumi Armada BAB MK BUY 0.71 1.06 0.92 0.77

Source: Bloomberg, UOB Kay Hian

Notable high-yielding deep value companies should offer interim immunity. Deeply sold down stocks that can sustain high yields in the interim period should appeal with their defensiveness. These include Astro and Berjaya Sports Toto. Additionally, Magnum would eventually be featured as a top dividend yield play, as it is expected to reinstate its payout ratio to 90-100% (dividend yield goes up to 7-8%) from currently 70% once it builds up sufficient reserves (expected by end-19) against the previous government’s tax claim (which is still being contested in court).

FIGURE 29: TOP 10 COMPANIES WITH HIGHEST DIVIDEND YIELDS Dividend Yield

Market Cap

Share Price 5 Jul 18

Target Price 2018F 2019F

Company Ticker Rec (US$m) (RM) (RM) (%) (%)

Astro Malaysia ASTRO MK BUY 2,102 1.63 2.21 7.2 7.4

Berjaya Sports Toto BST MK BUY 803 2.41 2.78 7.5 7.8

MRCB-Quill Reit MQREIT MK HOLD 297 1.12 1.15 7.0 7.2

Capitaland Malaysia Mall Trust CMMT MK HOLD 606 1.20 1.15 6.4 6.6

IGB REIT IGBREIT MK BUY 1,447 1.66 1.85 6.1 6.3

Bermaz Auto BAUTO MK BUY 649 2.26 2.60 6.1 6.9

Sunway REIT SREIT MK HOLD 1,238 1.70 1.70 6.1 6.5

Source: Bloomberg, UOB Kay Hian

Top picks in combined asset monetisation and deep value themes include MRCB

Notable BUY-rated, deep value stocks that trade at trough valuations include Astro, WCT Holdings

…and high-yielding Astro and Berjaya Sports Toto, while there is an eventual uplift to Magnum’s yield

Ju ly 2018

15

M a l a y s i a S t r a t e g y

FIGURE 30: FUNDAMENTAL TROUGH VALUATIONS FOR SELECTED COMPANIES

Share Price Target PE Trough Upside From 5 Jul 18 Price 2019F Value Trough Company Ticker Rec (RM) (RM) (x) (RM) (%)

WCT Holdings WCTHG MK BUY 0.80 1.12 6.8 1.24 55.0

IJM Corporation IJM MK BUY 1.78 2.65 11.3 2.33 30.9

Astro Malaysia ASTRO MK BUY 1.63 2.21 12.2 2.06 26.4

Gabungan AQRS AQRS MK BUY 1.19 1.86 10.0 1.48 24.4

Malaysian Resources Corporation MRC MK BUY 0.61 1.01 14.6 0.75 24.0

Ann Joo Resources AJR MK BUY 1.75 3.05 7.9 2.04 16.5

Gamuda GAM MK BUY 3.47 4.49 10.9 3.93 13.3

LBS Bina Group LBS MK HOLD 0.87 0.90 13.7 0.98 13.2

Eco World Development Group ECW MK HOLD 1.21 1.18 13.2 1.35 11.6

Scientex SCI MK BUY 7.16 8.20 9.5 7.92 10.6

Malakoff Corporation MLK MK BUY 0.85 1.05 13.5 0.93 10.1

Sarawak Oil Palms SOP MK BUY 2.98 4.15 13.0 3.20 7.4

Protasco PRTA MK HOLD 0.46 0.64 10.7 0.49 6.5

Cahya Mata Sarawak CMS MK BUY 2.43 4.00 13.7 2.59 6.5

Maxis MAXIS MK HOLD 5.39 6.40 21.0 5.48 1.7

DiGi.Com DIGI MK BUY 4.17 5.40 20.0 4.19 0.5

Source: Bloomberg, UOB Kay Hian

Ju ly 2018

16

M a l a y s i a S t r a t e g y

Top Picks

Our top stock picks include large caps Bumi Armada, Genting Malaysia, Inari Amertron, Public Bank and Tenaga Nasional, and small/mid caps Cahya Mata Sarawak, Gabuangan AQRS, Globetronics Technology, Scientex, Serba Dinamik, VS Industry and Yong Tai. We expect event catalysts to emerge in 2H18 for these companies, with the exception of Public Bank and Scientex (Figure 31 & 32).

Other noteworthy BUY-rated stocks include Yinson, while trading-oriented investors with above-average risk appetite should consider interim rebound plays eg construction companies Gamuda, IJM Corporation and MRCB, and mid cap MyEG.

FIGURE 31: TOP LARGE-CAP PICKS

Share Price Target PE P/B Div Yield 5 Jul 18 Price 2018F 2018F 2018F Company Ticker Rec (RM) (RM) (x) (x) (x) Catalyst

Bumi Armada BAB MK BUY 0.71 1.06 8.1 0.7 4.3 Kraken expected to receive full charter rate by 2H18

Genting Malaysia GENM MK BUY 4.85 6.28 15.4 1.4 3.6 Planned opening of iconic Fox theme park by end-18

Inari Amertron INRI MK BUY 2.25 2.68 20.5 6.5 3.3 Well poised to win new significant manufacturing contracts

Public Bank PBK MK BUY 22.90 25.20 15.2 2.2 3.0 Continued improvement in provisions and sustained non-interest income growth momentum

Tenaga Nasional TNB MK BUY 14.42 17.70 11.7 1.4 5.0 Good earnings visibility under IBR framework and undemanding valuation

Source: Bloomberg, UOB Kay Hian

FIGURE 32: TOP SMALL/MID-CAP PICKS

Share Price Target PE P/B Div Yield 5 Jul 18 Price 2018F 2018F 2018F Company Ticker Rec (RM) (RM) (x) (x) (x) Catalyst

Cahya Mata Sarawak CMS MK BUY 2.43 4.00 8.3 1.1 4.6 Earnings momentum at OM Sarawak

Groundbreaking for mega phosphate manufacturing project MPA

Gabungan AQRS AQRS MK BUY 1.19 1.86 8.5 1.3 3.5 Potential contract wins in mega projects which may still proceed (ECRL, Sabah portion of Pan Borneo Highway)

Expected successful launch of E island development

Globetronics Technology

GTB MK BUY 2.24 2.52 17.7 5.0 4.5 Earnings doubling in 2018

Further upside on potential commercialisation of sensors under development

Scientex SCI MK BUY 7.16 8.20 11.9 2.0 2.5 Expecting a stronger 4QFY18 core net profit from maiden contribution from Klang Hock Plastic Industries and normalised property segment performance post GE

Serba Dinamik SDH MK BUY 3.34 4.30 12.3 2.4 2.4 More upside to earnings expectations - high orderbook renewal rate and momentum of new orderbook wins

Yong Tai YTB MK BUY 1.45 2.10 19.1 2.0 0.0 Strong reception expected for Impression theatre (opening Mar 18); may explore opening more theatres in the region

VS Industry VSI MK BUY 1.68 1.85 21.4 2.5 2.1 High growth visibility, potential major contract wins

Source: Bloomberg, UOB Kay Hian

Top picks with expected catalysts in 2H18 include large caps Bumi Armada, Genting Malaysia and Inari Amertron, and small/mid caps Cahya Mata Sarawak, Gabungan AQRS, Globetronics Technology, Scientex, VS Industry and Yong Tai

Ju ly 2018

17

M a l a y s i a S t r a t e g y

SELL calls continue to be the pricey Hartalega Holdings and Nestle Malaysia which are priced to perfection and hence, vulnerable to negative developments or would significantly underperform when market risk aversion eases. Hartalega's valuation appears unsustainably stretched, given that some of China’s vinyl glove manufacturing plants would eventually come back on stream (after meeting the China government’s requirement to convert plants for natural gas feedstock). The potential vulnerability to bad news is aptly demonstrated by Top Glove's single-day 30% plunge (at the lowest point) after its shocking announcement to sue the vendors of recently acquired Apsion for at least over half of the RM1.4b acquisition price tag.

FIGURE 33: SELL CALLS

Share Price Target PE P/B Div Yield 5 Jul 18 Price 2018F 2018F 2018F Company Ticker Rec (RM) (RM) (x) (x) (x) Catalyst

Hartalega Holdings HART MK SELL 5.95 4.02 38.7 9.0 1.6 Subject to risk of valuation derating due to structural downtrend in nitrile glove margins over the longer term

Source: Bloomberg, UOB Kay Hian

Vincent Khoo, CFA +603 2147 1998

Malaysia Research Team +603 2147 1988

M a l a y s i a S t r a t e g y July 2018

18

Automobile MARKET WEIGHT

WHY WE ARE MARKET WEIGHT

Many automobile stocks are trading at mid-teens PE valuations from being in the red on better outlook driven by strengthening of the ringgit.

Stocks like Bermaz Auto with huge cash pile and zero long-term borrowing offer attractive yields.

WHAT TO WATCH OUT FOR IN 2H18

The quantum of the SST which is slated to be introduced on 1 Sep 18 after a three-month tax break.

Proton’s first SUV launch, which will be based on Geely’s Boyue in 4Q18.

Outlook

FIGURE 34: AUTOMOBILE INDEX OUTPERFORMS FBMKLCI

90

95

100

105

110

115

120

125

Jan Feb Mar Apr May Jun Jul

Automobile

FBMKLCI

End Dec 17=100

Source: Bloomberg, UOB Kay Hian

Outperforms FBMKLCI ytd. The sector’s stellar performance is led by UMW Holdings (UMW) which has outperformed the FBMKLCI by 18.5%. Most listed automobile stocks have recovered from their ytd lows driven by improving results on a stronger ringgit and higher sales volume, as well as a corporate deal between UMW and MBM Resources (MBMR). UMW plans to increase its stake in Perodua by acquiring a 10% stake in Perodua from PNB Equity Resources Corporation (PNB), and a 50.1% stake in MBMR from Med-Bumikar Mara (49.5%) and Central Shore (0.57%) at RM2.56/share, with a mandatory takeover to follow.

TIV to spike up during three-month tax break… On the back of a three-month tax break effective 1 Jun 18, we expect sales volume to spike up as consumers take advantage of the tax-free window. In addition, we note that carmakers have not scaled down their promotions and in fact have intensified their promotions, notably during the Hari Raya period.

…tank in 4Q18 and normalise thereafter. Sales volume should experience a rather significant drop in 4Q18 on the back of frontloading by consumers due to the three-month tax break and also in anticipation of higher car prices following the reintroduction of the Sales and Services Tax (SST). We maintain our 2018 total industry volume (TIV) growth forecast of 2-4% at 607,000-619,000 units.

Sector outperformance driven by better results on stronger ringgit, higher sales volume and UMW-MBMR deal

Sales volume to spike up during the three-month tax break, tank in 4Q18 and normalise thereafter

M a l a y s i a S t r a t e g y July 2018

19

Car prices could go up following reintroduction of SST. Before the implementation of the Goods and Services Tax (GST), SST for cars was 10%. In the case that the quantum of the SST for cars is back at the 10% rate, car prices are expected to be 1-3% higher than the GST-inclusive prices.

FIGURE 35: SALES & SERVICES TAX (SST) VS GOODS AND SERVICES TAX (GST)

SST GST

Government Approved Selling Price +

10% Sales Tax +

Margins

Government Approved Selling Price +

Margins

Net Selling Price Net Selling Price +

Inspection Fees, Accessories, etc. +

Inspection Fees, Accessories, etc. Retail Price Without Insurance Retail Price Without Insurance

+ Road Tax

+ Insurance

+ 6% GST

+ Road Tax (no GST)

+ Insurance (own 6% applied)

Final Price Final Price

Source: Paultan.org

Minimal to modest impact from reduction of excise duty on imported cars below 1,600cc for first-time buyers. The manifesto of Pakatan Harapan stated the reduction of excise duty on imported cars below 1,600cc for first-time buyers and limited to only one purchase for each family with household income below RM8,000/month. There are no further details yet on the timeline of the implementation and the quantum of the reduction of excise duty. We see minimal to modest impact to the automobile sector given that the reduction of excise duty is only applicable to first-time car buyers and limited to only one purchase for each family with household income below RM8,000/month. Furthermore, imported cars below 1,600cc account for only a small fraction of consumers.

A third national car project in the making? Speaking at the 24th Nikkei Conference in Tokyo last month, Prime Minister Tun Dr Mahathir Mohamad expressed his desire to form Malaysia’s third national car project with other countries in the region as Proton is no longer a national car brand after it was sold to China’s Geely last year. To recap, Geely acquired a 49.9% stake in Proton from DRB-Hicom in Sep 17. Given that the government is focusing on reducing its debt, the plan is not feasible if there is no strong partner that can offer solid financial support, modern technology and production capabilities. Moreover, the local automobile market is too small to accommodate another national car project.

Should SST for cars go back to 10%, car prices are expected to be 1-3% higher than GST-inclusive prices

Minimal to modest impact as reduction is only applicable to first-time buyers and limited to one purchase per family with household income <RM8,000/month

Third national car project not feasible given new government’s focus on debt reduction and small local automobile market

M a l a y s i a S t r a t e g y July 2018

20

FIGURE 36: MARKET SHARE (2017) FIGURE 37: MARKET SHARE (5M18)

Perodua

36%

Proton

12%Toy ota

17%

Honda

19%

Nissan

5%

Mazda

2%

EURO

5%

Others

4%

Perodua

43%

Others

9%EURO

5%

Nissan

4%

Mazda

2%

Honda

18%

Toy ota

9%Proton

9%

Source: Malaysian Automotive Association (MAA) Source: MAA

FIGURE 38: MONTHLY TIV BREAKDOWN

May 18 mom yoy 5M18 5M17 yoy (unit) % chg % chg (unit) (unit) % chg

Industry

Passenger 40,221 (4.2) (10.9) 203,299 210,402 (3.4)

Commercial 2,762 (45.9) (49.4) 21,913 23,778 (7.8)

Total 42,983 (8.7) (15.0) 225,212 234,180 (3.8) National

Passenger 26,452 8.5 6.4 120,627 116,868 3.2

Commercial 17 (73.8) (26.1) 144 139 3.6

Total 26,469 8.3 6.4 120,771 117,007 3.2 Non-National

Passenger 13,769 (21.8) (32.1) 82,672 93,534 (11.6)

Commercial 2,745 (45.6) (49.5) 21,769 23,639 (7.9)

Total 16,514 (27.1) (35.8) 104,441 117,173 (10.9)

Source: MAA

Perodua: Strong sales volume ytd driven by all-new Myvi. Perodua remains the market leader with its market share growing to 43% ytd (2017: 36%). We attribute this to the favourable reception to its all-new Myvi launched in Nov 17 (the previous model was six years old), and lack of new product offerings from Proton, its closest competitor so far. 5M18 sales volume growth grew 19.1% yoy to 97,487 units, driven by the all-new Myvi. Its highly-anticipated new SUV launch will only take place in 2019, which will be competing with Boyue, Proton’s first SUV, which is slated to be launched in 4Q18. Perodua plans to grow its 2018 sales target by 2% to 206,000 units (2017: 204,887 units).

Proton: To launch a new model each year until 2021, starting with highly-anticipated first SUV in 4Q18. As expected, Proton’s 5M18 sales volume was weak, declining a significant 34.9% yoy to 20,933 units. This was due to a lack of new product offerings so far this year as the carmaker focuses on restructuring following Geely’s acquisition of a 49.9% stake in Proton and a controlling stake in Lotus. However, Proton expects to launch its first SUV in 4Q18. The SUV, based on Geely’s Boyue, will be sold as a complete built-up (CBU) fully imported from China for its launch and then locally assembled at the carmaker’s Tanjung Malim plant in 2019. Boyue is Geely’s best-selling model, accounting for 23% of its 2017 sales volume with 286,885 units sold. Geely sold 1.25m units of cars in 2017, representing a 5% market share in China last year.

Proton’s Boyue to hit the market in 4Q18; Perodua to launch new SUV model in 2019

M a l a y s i a S t r a t e g y July 2018

21

Nissan: Focusing on improving margins instead of being a volume play. Nissan’s sales volume continued to be weak, with 5M18 sales volume declining 17.4% yoy to 8,918 units. The lacklustre performance was due to its lack of new product offerings, and the carmaker’s strategic shift to focus on improving its margin via high-margin car models instead of ramping up sales volume. We note that its strategy has borne fruit given that the 1Q18 results of Tan Chong Motor Holdings, the Nissan distributor in Malaysia, are back in the black after eight quarters in the red. Nissan launched the all-new Serena S-Hybrid in a complete knocked-down (CKD) version in May 18 and the next model to hit the market will be the all-new electric vehicle (EV) Leaf in 4Q18 or 1Q19.

Non-national marques’ market share to come off in 2018. We expect market share of non-national marques to shed from >50% in 2017, in view of: a) lack of attractive new models in 2018 (Figure 39), and b) highly-anticipated launch of the Boyue SUV by Proton in 4Q18. For 5M18, market share of non-national marques stood at 48% (2017: 52%).

FIGURE 39: MONTHLY TIV – NATIONAL VS NON-NATIONAL FIGURE 40: MONTHLY TIV OF BIG 3 NON-NATIONAL MARQUES

16

18

20

22

24

26

28

30

Jan 17 Apr 17 Jul 17 Oct 17 Jan 18 Apr 18

('000 units)

National Non-national

0

2

4

6

8

10

12

Jul 17 Sep 17 Nov 17 Jan 18 Mar 18 May 18

('000 units)

Toy ota Honda Nissan

Source: MAA Source: MAA

FIGURE 41: LAUNCH OF NOTABLE NEW AND FACELIFTED MODELS IN 2H18 AND 2019

Segment Model To be launched in

B-Segment Kia Picanto 2H18

Mazda 6 3Q18 C-Segment

Nissan Leaf 4Q18 or 1Q19

Hyundai Kona 2H18

Hyundai Santa Fe 2H18/2019

Mazda CX-8 (CKD) 2019

Perodua D38L 2019

SUV

Proton Geely Boyue 4Q18

MPV Mitsubishi Xpander 2H18

Pick-up Ford Raptor 2H18

Source: Media reports, Respective companies, UOB Kay Hian

Carmakers’ margins have bottomed out since 4Q17. We have seen a significant improvement in the margins of carmakers since 4Q17 on the back of a strengthening ringgit against major currencies (Figure 42). Provided that the US$/RM rate is maintained at the RM3.95-4.00 level, we expect carmakers’ margins to remain at the 1H18 level.

Nissan’s upcoming launch of all-new high-margin EV Leaf not expected to boost sales volume

Lack of new attractive models from non-national marques in 2H18

M a l a y s i a S t r a t e g y July 2018

22

FIGURE 42: LISTED AUTOMOBILE PLAYERS’ EBIT MARGINS

-4

-2

0

2

4

6

8

10

12

14

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

(%)

APM Automotiv e Bermaz AutoMBM Resources Tan Chong MotorUMW Holdings

Note: UMW’s margins are PBT margins. DRB-Hicom’s data is removed from the chart as its automobile segment has recorded losses for the past nine quarters. Source: Respective companies

M a l a y s i a S t r a t e g y July 2018

23

Strategy

Maintain MARKET WEIGHT on the sector. Although domestic sales volume growth will be limited in a saturated market, margins have bottomed out on the back of the strengthening of the ringgit against major currencies in 4Q17, and carmakers are ramping up export sales volume given the customised incentives offered by the government to make Malaysia a regional energy efficient vehicle (EEV) hub by 2022. Bermaz Auto (BAuto) is our top pick for the sector.

Bermaz Auto (BAUTO MK/BUY/RM2.26/Target: RM2.60). Given BAuto’s strong 4QFY18 results, we expect the growth momentum to continue on the back of the ramp-up of CX-5 sales volume by its associates, notably its 30%-owned Mazda Malaysia (MMSB) driven by exports. The all-new Mazda 6 is slated for launch in 3Q18 while CX-8 will only hit the market in 2QFY20 in CKD form. Management is still trying to list its 60.4%-owned Bermaz Auto Philippines (BAP) in the Philippines although there is no definite timeline yet. Given BAuto’s net cash position of RM261.5m (or 23 sen/share) and asset-light business model, we estimate a 75% payout for FY19-21, which represents attractive yields of 6.1-7.3%. Our target price is based on a 13x PE pegged to 2019F EPS.

UMW Holdings (UMWH MK/HOLD/RM6.07/Target: RM6.20). UMW reported a strong 1Q18 due to the strong comeback of its automobile segment where PBT rose 44.6% yoy on a stronger ringgit (despite a 14.3% yoy decline in sales). Its plans to increase its stake in Perodua via the acquisition of a 10% stake in Perodua from PNB, as well as a 50.1% stake in MBMR from Med-Bumikar Mara (49.5%) and Central Shore (0.57%), have hit a bump. Media reports indicated that the major impediment is Daihatsu’s objection to having UMW as the single largest shareholder of Perodua. According to The Edge Weekly, Daihatsu is adamant on this and has even threatened to stop all technological transfer to Perodua. Daihatsu has a 20.93% stake in Perodua a direct 20% stake and indirect stake of 0.93% via 18.5%-owned Daihatsu (Malaysia). Both acquisition proposals have been extended for the second time until end-Oct 18. Our target price implies 13.6x 2019F PE, which assumes UMW’s stake in Perodua at 48% post-completion of the 10% stake acquisition in Perodua from PNB. Entry price is RM5.80.

Fong Kah Yan

+603 2147 1993 [email protected]

Bermaz Auto is our top sector pick

Given its net cash position and asset-light business model, BAuto offers attractive yields of 6.1-7.3% based on 75% payout

UMW’s plan to raise its stake in Perodua via MBMR and PNB met with Daihatsu’s objection to having UMW as controlling shareholder of Perodua

M a l a y s i a S t r a t e g y July 2018

24

Sector At A Glance

FIGURE 43: DECADE-LONG AUTOMOBILE SALES CYCLE FIGURE 44: MARKET SHARE (5M18)

450

500

550

600

650

700

07 08 09 10 11 12 13 14 15 16 17

('000 units)

-15

-10

-5

0

5

10

15

20(%)

TIV (LHS) y oy % chg (RHS)

Perodua

43%

EURO

5%

Others

9%Mazda

2%Nissan

4%

Honda

18%

Toy ota

9%Proton

9%

Source: MAA, UOB Kay Hian Source: MAA

FIGURE 45: PERODUA SALES FIGURE 46: PROTON SALES

12

14

16

18

20

22

24

26

28

Jul 16 Jan 17 Jul 17 Jan 18

-30

-20

-10

0

10

20

30

40

50Sales (LHS) y oy % chg (RHS)

(%)('000 units)

\

3

4

5

6

7

8

9

Jul 16 Jan 17 Jul 17 Jan 18

-80

-60

-40

-20

0

20

40

60

80Sales (LHS) y oy % chg (RHS)

(%)('000 units)

Source: MAA Source: MAA

FIGURE 47: TOYOTA SALES FIGURE 48: HONDA SALES

123456789

10

Jul 16 Jan 17 Jul 17 Jan 18

-80-60-40-20020406080100

Sales (LHS)y oy % chg (RHS)

(%)('000 units)

456789

1011121314

Jul 16 Jan 17 Jul 17 Jan 18

-40

-20

0

20

40

60

80Sales (LHS)y oy % chg (RHS)

(%)('000 units)

Source: MAA Source: MAA FIGURE 49: SECTOR STATISTICS

Share Price Last Net Profit EPS PE Market BV Price/

Company Ticker Rec 5 Jul 18 Year 2017 2018F 2019F 2017 2018F 2019F 2017 2018F 2019F ROE Cap ps BV ps (RM) End (RMm) (RMm) (RMm) (sen) (sen) (sen) (x) (x) (x) (%) (RMm) (RM) (x)

Bermaz Auto BAUTO MK BUY 2.26 4/18 142 214 242 12.3 18.5 20.8 18.4 12.2 10.9 30.2 2,626 0.41 5.5

UMW Holdings UMWH MK HOLD 6.07 12/17 349 479 563 29.9 41.0 48.2 20.3 14.8 12.6 9.0 7,092 2.68 2.3

Sector 492 693 804 19.8 14.0 12.1 11.2 9,717 2.7

Note: If year end is before June, earnings are shown in the previous period. Source: Respective companies, Bloomberg, UOB Kay Hian

M a l a y s i a S t r a t e g y July 2018

25

Banking MARKET WEIGHT

WHY WE ARE MARKET WEIGHT

Loans growth to remain modest at 5.0-5.5%. Austerity measures by new government to create slight

downside risks on macro growth. Asset quality holding up better than expected. Healthy CET1 ratios post MFRS9 alleviate risk of equity

capital-raising.

WHAT TO WATCH OUT FOR IN 2H18

Gradual uptrend in provisions as MFRS9 takes effect. Time deposits to reprice upwards, placing a slight

pressure on sequential NIM. Automobile and consumer durable loans growth may

experience a short-term spike in 3Q18 in the absence of both GST and SST from Jun-Aug 18.

Rising bond yields to negatively impact marked-to-market gains with every 10bp change impacting sector earnings by 0.2%.

Outlook

FIGURE 50: BANKING INDEX OUTPERFORMS FBMKLCI

92

94

96

98

100102

104

106

108

110

112

Jan Feb Mar Apr May Jun Jul

Banking

FBMKLCI

End Dec 17=100

Source: Bloomberg, UOB Kay Hian

Outperforms FBMKLCI by 3.6% ytd. The banking sector has outperformed the FBMKLCI by 3.6% ytd. However, the sector had underperformed the FBMKLCI after the 14th general election (GE14), declining 9.5% vs the FBMKLCI’s 8.4% fall over the same period. The post GE14 selldown was notably intense for the likes of CIMB Group Holdings (CIMB) (-19.9%) and Malayan Banking (Maybank) (-15.6%) while large-cap non-GLC banks like Public Bank (PBank) and Hong Leong Bank (HLB), which are seen as more defensive (less directly affected by any slowdown in government-related project financing post GE14), registered milder 4.1% and 2.0% share price declines.