Preparing to SOAR - Shane Convery · “Preparing to SOAR” ... GE 9-Cell ... BCG Portfolio Matrix...

82

A Comprehensive Strategic Analysis Jonathan Romero Brooke Williams Alex Buschmann Shane Convery Chendong Yin “Preparing to ” SOAR

Transcript of Preparing to SOAR - Shane Convery · “Preparing to SOAR” ... GE 9-Cell ... BCG Portfolio Matrix...

A Comprehensive Strategic Analysis

Jonathan Romero

Brooke Williams

Alex Buschmann

Shane Convery

Chendong Yin

“Preparing to ” SOAR

P a g e | 1

Table of Contents

Company Summary and History ..................................................................................................... 4

Timeline .......................................................................................................................................... 5

Key Strategists and Personnel ......................................................................................................... 6

Organizational Structure ............................................................................................................... 12

Mission Statement ......................................................................................................................... 13

Goals ............................................................................................................................................. 13

Objectives ..................................................................................................................................... 14

Organization Culture ..................................................................................................................... 14

Leadership Style............................................................................................................................ 15

Industry and Competition ............................................................................................................. 16

Current Strategies.......................................................................................................................... 17

Grand ......................................................................................................................................... 17

Corporate ................................................................................................................................... 17

Business ..................................................................................................................................... 17

Functional .................................................................................................................................. 18

Marketing............................................................................................................................... 18

Finance................................................................................................................................... 18

Operations .............................................................................................................................. 19

Human Resources .................................................................................................................. 20

Information ............................................................................................................................ 20

Management .......................................................................................................................... 20

Marketing Audit ............................................................................................................................ 21

Product ...................................................................................................................................... 21

Price ........................................................................................................................................... 23

Promotion .................................................................................................................................. 24

Place .......................................................................................................................................... 24

Financial Statements ..................................................................................................................... 26

P a g e | 2

Financial Ratio Analysis ............................................................................................................... 29

Liquidity .................................................................................................................................... 29

Profitability................................................................................................................................ 31

Activity/Efficiency .................................................................................................................... 33

Solvency .................................................................................................................................... 35

Stock Valuation and Performance ............................................................................................. 38

Financial Summary and Outlook............................................................................................... 38

Value Chain .................................................................................................................................. 40

Inbound Logistics ...................................................................................................................... 40

Operations ................................................................................................................................. 41

Outbound Logistics ................................................................................................................... 42

Marketing and Sales .................................................................................................................. 43

Customer Service ...................................................................................................................... 44

McKinsey’s Seven S’s .................................................................................................................. 45

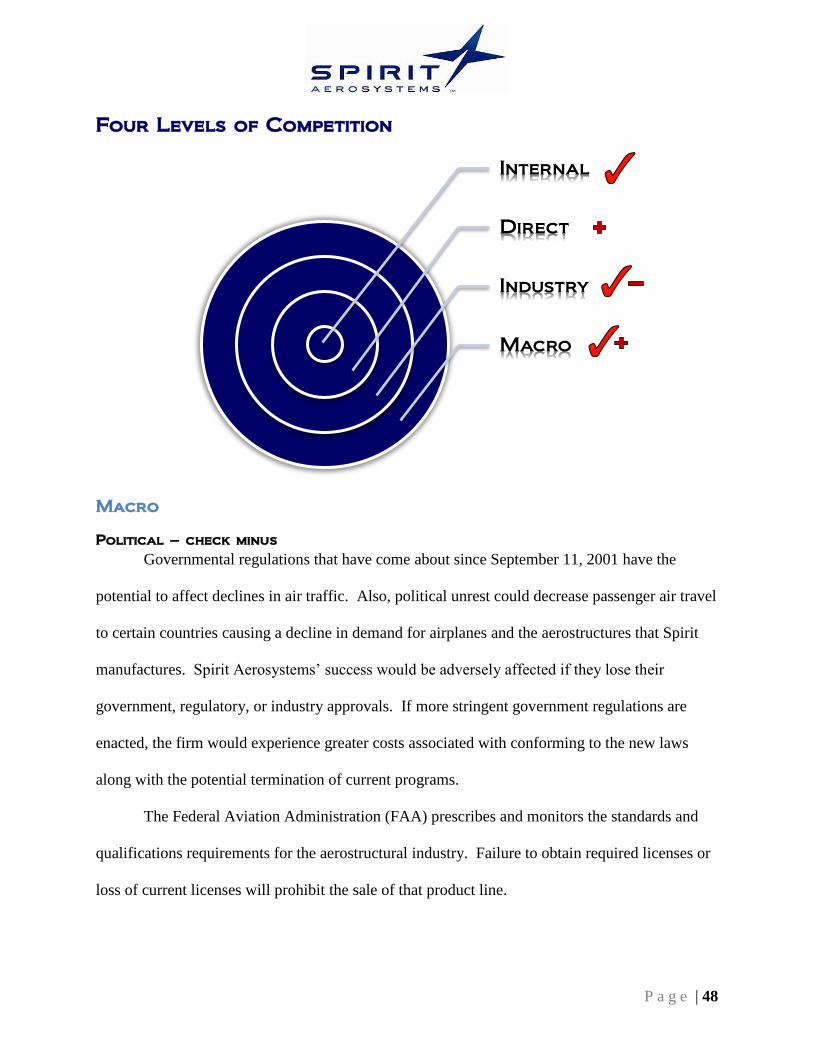

Four Levels of Competition .......................................................................................................... 48

Macro ........................................................................................................................................ 48

Industry...................................................................................................................................... 50

Porter’s 5 Forces ........................................................................................................................... 51

Industry Attractiveness .......................................................................................................... 51

Threat of New Entrants .......................................................................................................... 52

Power of Suppliers................................................................................................................. 52

Threat of Substitutes .............................................................................................................. 52

Power of Buyers .................................................................................................................... 53

Industry Rivalry ..................................................................................................................... 53

Direct ......................................................................................................................................... 54

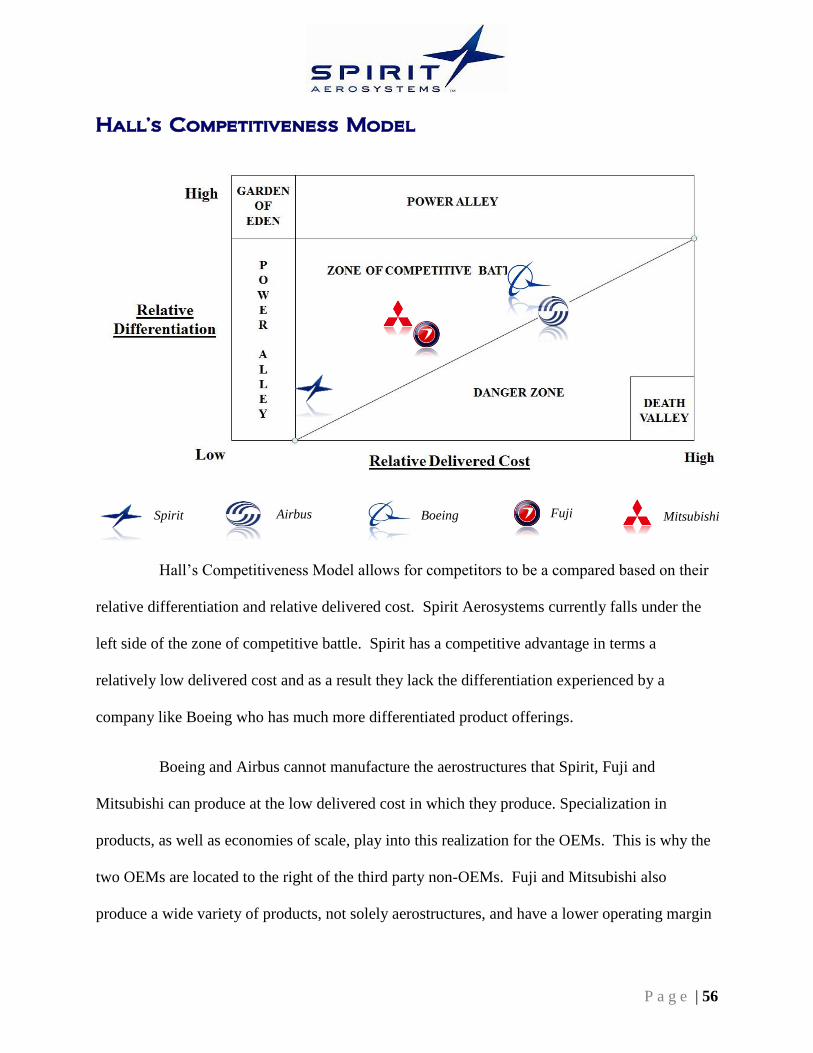

Hall’s Competitiveness Model ...................................................................................................... 56

Strategy Evolution ........................................................................................................................ 58

Internal .......................................................................................................................................... 59

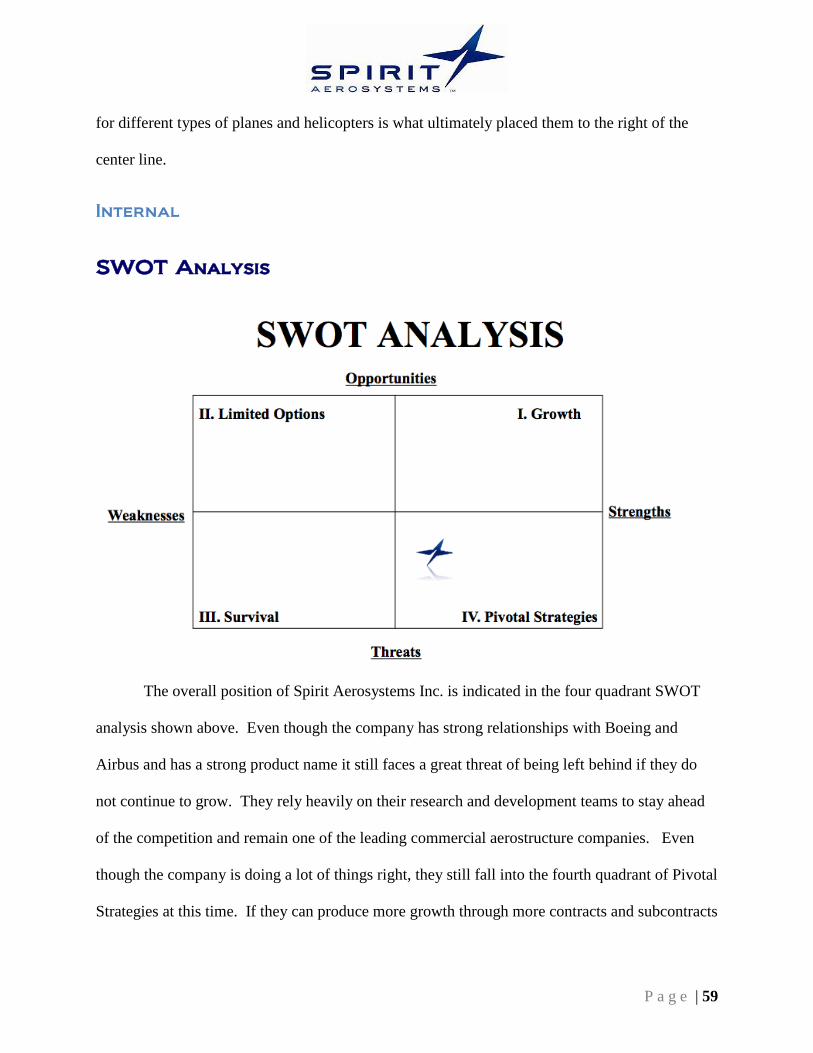

SWOT Analysis ............................................................................................................................ 59

Strengths .................................................................................................................................... 60

P a g e | 3

Weaknesses ............................................................................................................................... 61

Opportunities ............................................................................................................................. 62

Threats ....................................................................................................................................... 63

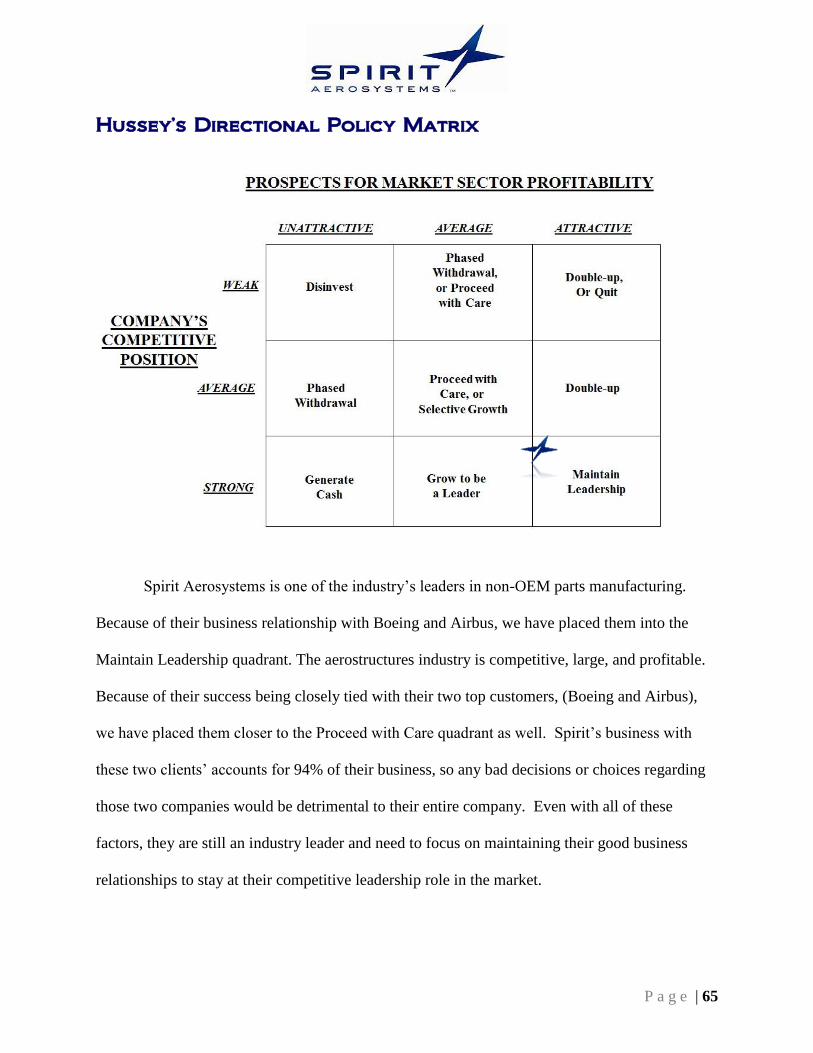

Hussey’s Directional Policy Matrix .............................................................................................. 65

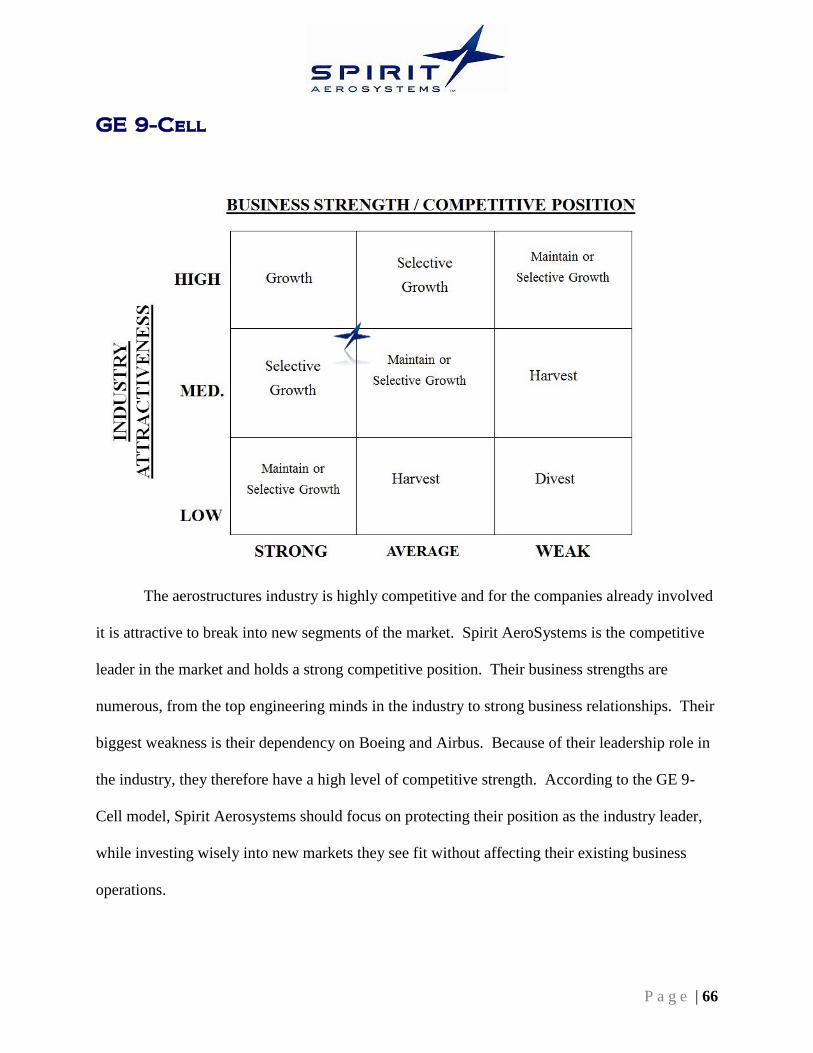

GE 9-Cell ...................................................................................................................................... 66

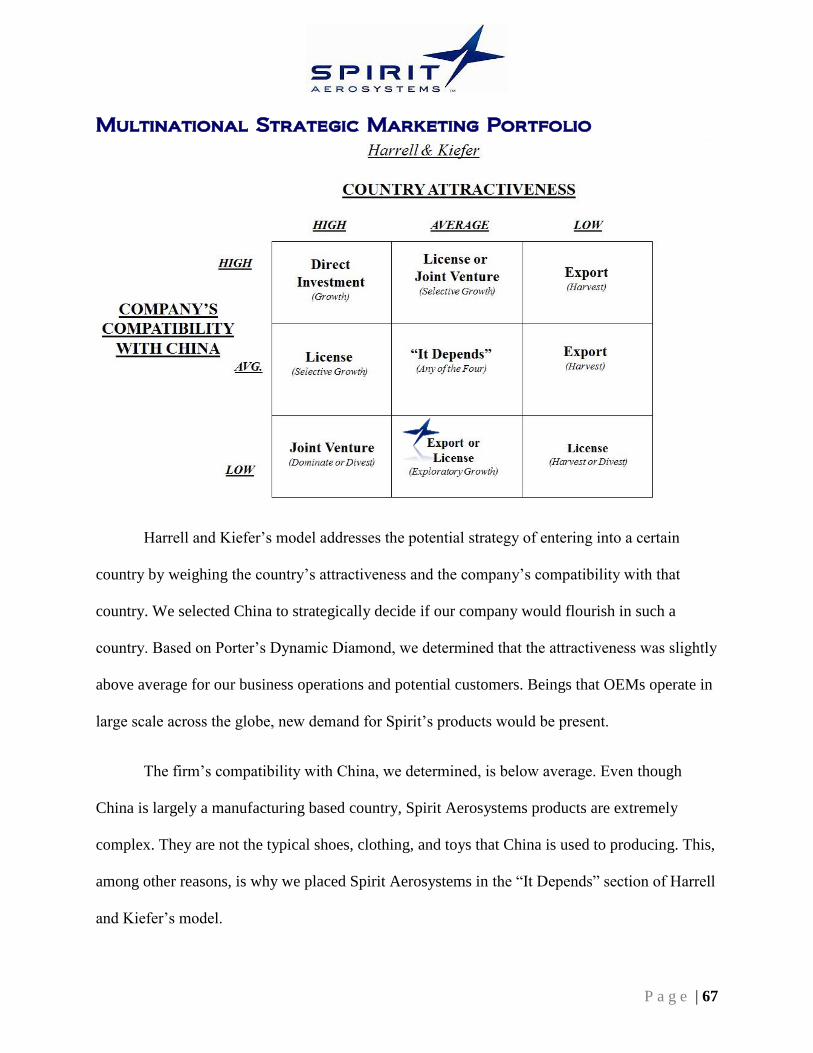

Multinational Strategic Marketing Portfolio ................................................................................. 67

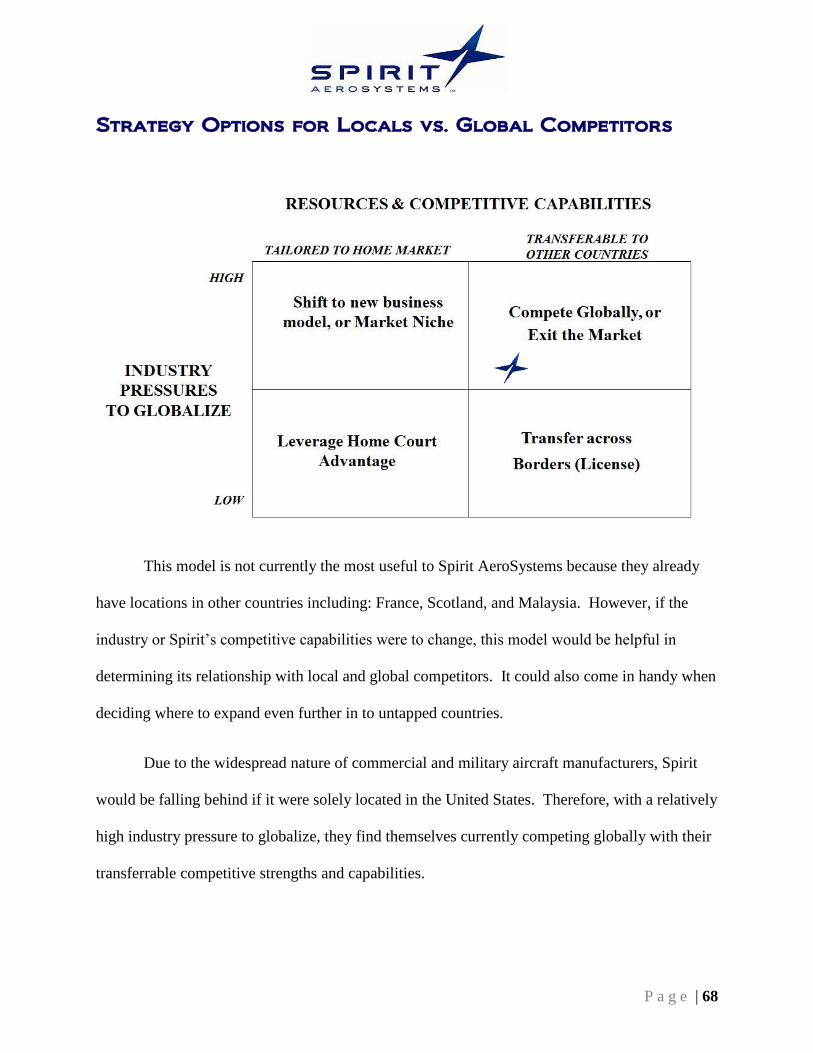

Strategy Options for Locals vs. Global Competitors .................................................................... 68

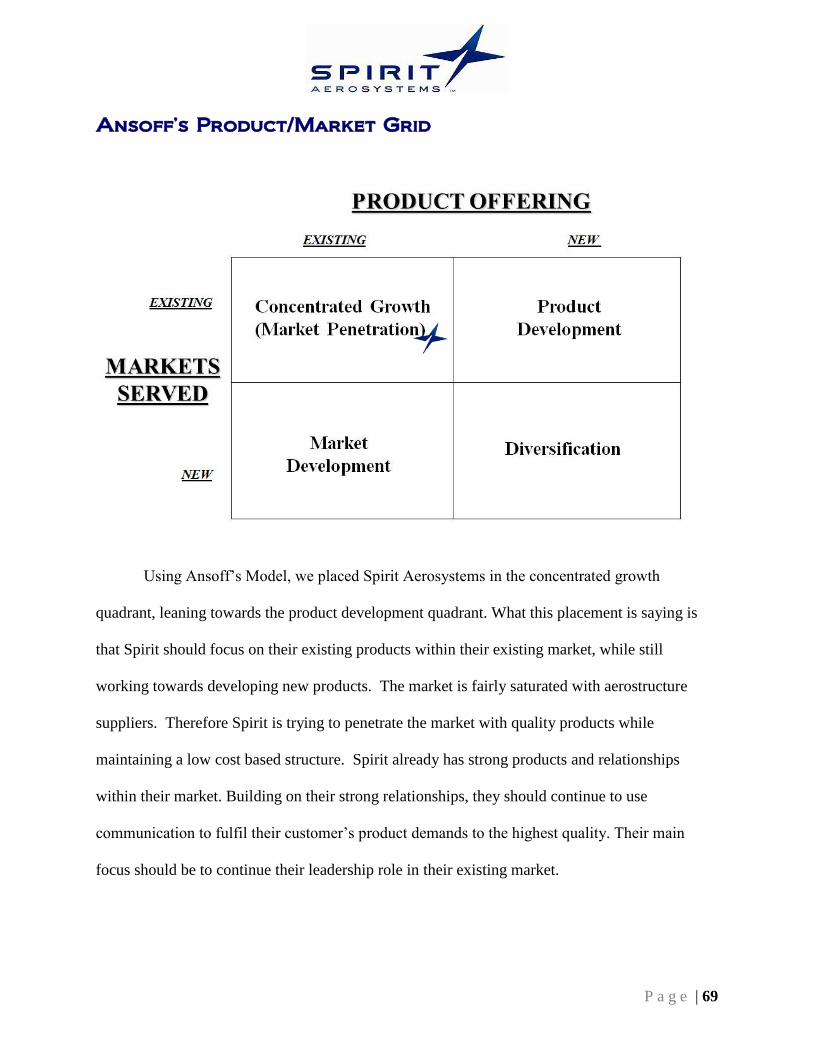

Ansoff’s Product/Market Grid ...................................................................................................... 69

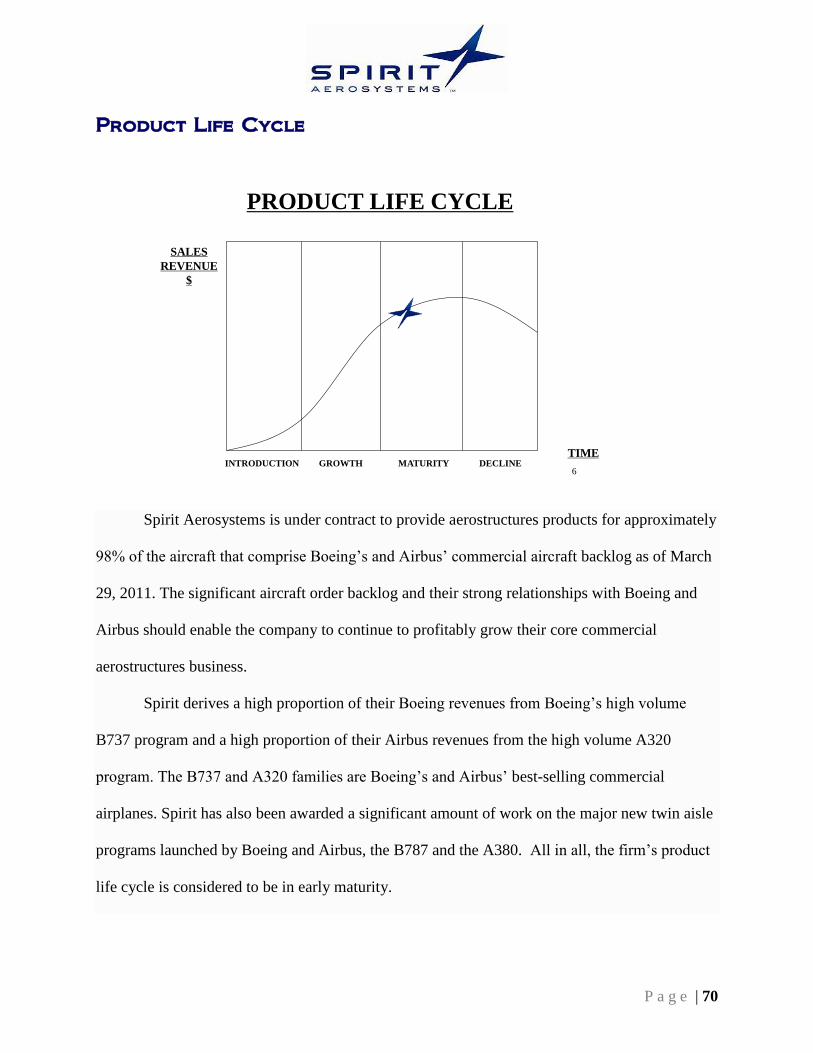

Product Life Cycle ........................................................................................................................ 70

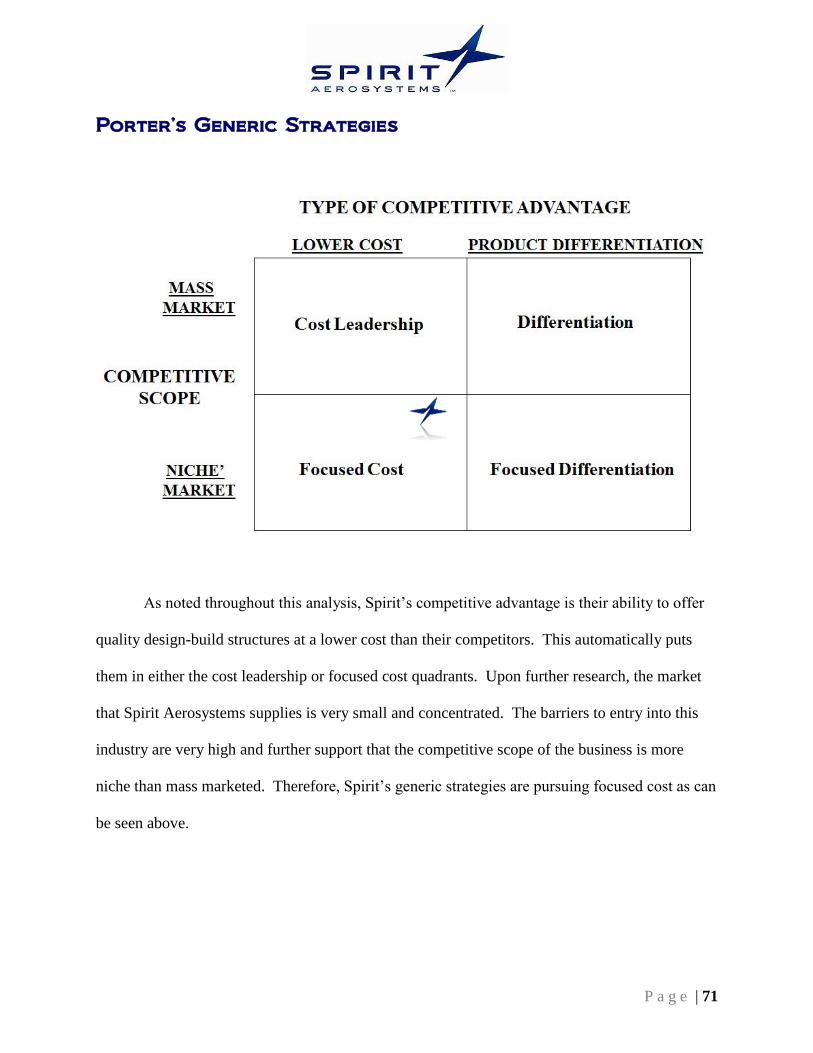

Porter’s Generic Strategies ........................................................................................................... 71

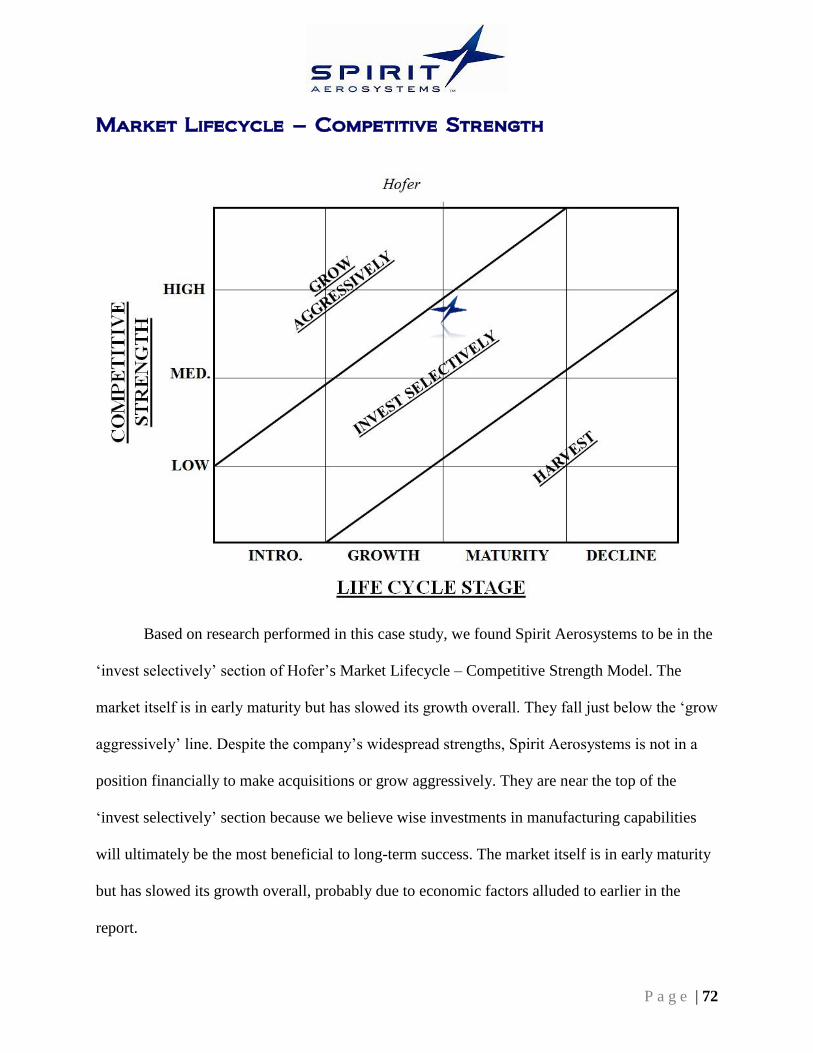

Market Lifecycle – Competitive Strength..................................................................................... 72

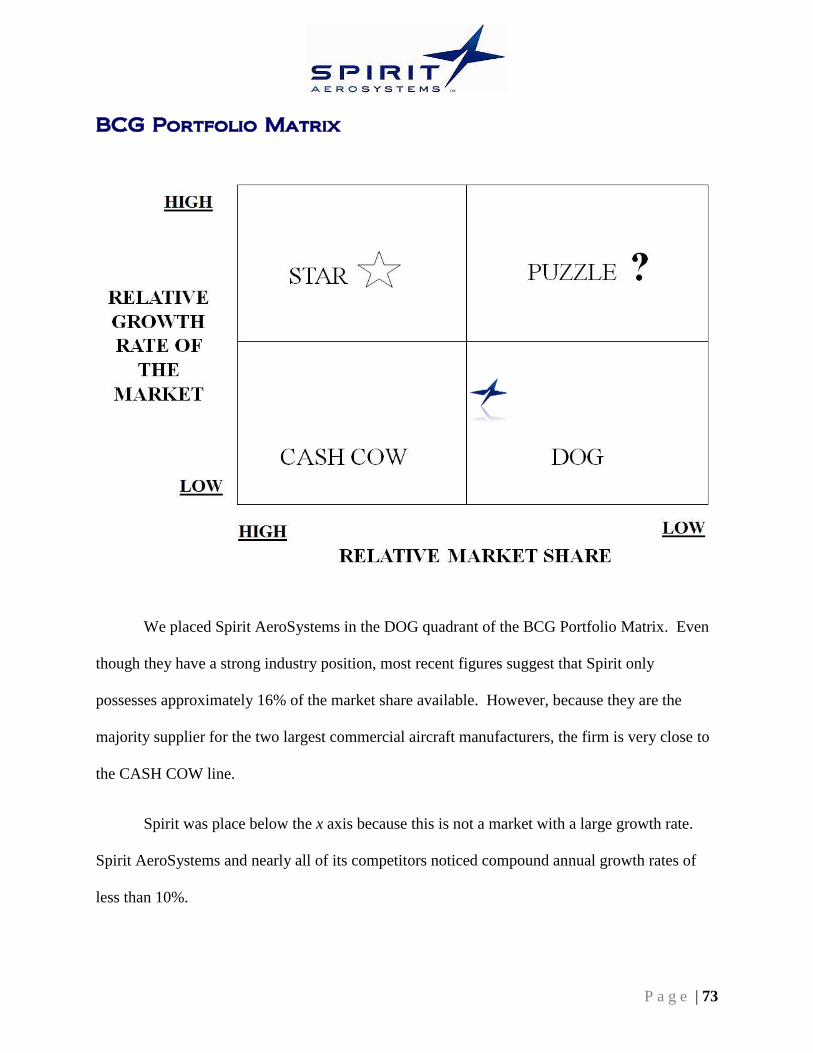

BCG Portfolio Matrix ................................................................................................................... 73

Main Problems .............................................................................................................................. 74

Cost Control .............................................................................................................................. 74

Lack of Customer Diversity ...................................................................................................... 74

Untapped Foreign Markets ........................................................................................................ 75

Alternative Strategies .................................................................................................................... 76

Final Strategic Choice ................................................................................................................... 79

Concentric Diversification into Military/Defense Sector.......................................................... 79

Implementation ............................................................................................................................. 80

Who, How, When ...................................................................................................................... 80

Bibliography ................................................................................................................................. 81

P a g e | 4

Company Summary and History

Headquartered in Wichita, Kansas, Spirit AeroSystems, Inc. is one of the largest,

independent non-original equipment manufacturers (OEM) aircraft parts designers and

manufacturers of commercial aero structures in the world (based on annual revenues). They are

also the largest independent supplier of aero structures to Boeing and Airbus, the two largest

aircraft OEMs in the world. Aero structures are structural components such as fuselages,

propulsion systems and wing systems for commercial and military aircraft. For the twelve

months ended December 31, 2013, Spirit generated net revenues of $5.9 billion, and had net loss

of $621.4 million.

Spirit manufactures aero structures for every Boeing commercial aircraft currently in

production. This includes the majority of the airframe content for the Boeing B737, the most

popular major commercial aircraft in history. As a result of its unique capabilities both in

process design and composite materials, Spirit AeroSystems was awarded a contract to be the

aero structures content supplier for the Boeing B787, Boeing's next generation twin aisle aircraft.

In addition, Spirit is one of the largest content suppliers of wing systems for the Airbus

A320 family. They are a significant supplier for the Airbus A380, and will be a significant

supplier for the new Airbus A350 XWB (Extra Wide-Body) after the development stage of the

program.

Revenues are derived primarily through long-term contracts with Boeing and Airbus. For

the 2013 year, approximately 84% and 10% of net revenues were generated from sales to Boeing

and Airbus, respectively. Due to the broad range of products supplied, the leading design, and

P a g e | 5

manufacturing capabilities using both metallic and composite materials, Spirit has significant

sustainable competitive advantages (SCAs).

Since Spirit's incorporation, the company has expanded its customer base to include

Sikorsky, Rolls-Royce, Gulfstream, Israel Aerospace Industries, Bombardier, Mitsubishi Aircraft

Corporation, Bell Helicopter, Southwest Airlines, United Airlines and American Airlines. Spirit

holds manufacturing facilities in Tulsa and McAlester, Oklahoma; Prestwick, Scotland; Wichita

and Chanute, Kansas; Kinston, North Carolina; Saint-Nazaire, France; and Subang, Malaysia.

Timeline

February 2005 Boeing Company’s Wichita Division is acquired by Onex and renamed

Spirit AeroSystems.

June 2005 Acquisition is complete and Tulsa becomes Aerostructures Business Unit.

April 2006 Acquired BAE Aerostructures unit facilities in Scotland, England.

November 2006 Spirit went Public in Initial Public Offering (IPO).

May 2007 Secondary Public offering of Class A Common Stock at $33.50/share.

May 2007 Wins 7 year contract to build major composite structure for CH-53k

heavy-lift helicopter.

March 2008 Selected to design and manufacture Nacelle Systems for Rolls-Royce

BR725

May 2008 Announces expansion and new facility in North Carolina.

July 2008 Wins contract for fuselage structure and wing leading edge for Airbus 350

XWB.

October 2008 Selected to design and build wings for Gulfstream G650 business jet and

G250 super mid-size business jet.

P a g e | 6

October 2009 Ground was broken for Spirit's new A350XWB facility in Saint-Nazaire,

France.

November 2009 Spirit opened a new maintenance, repair, and overhaul (MRO) center in

Asia.

March 2010 Spirit was named a member of the Boeing NewGen Tanker Supplier

Team.

May 2011 Spirit and Boeing enter into B787 Amendment.

May 2013 Larry Lawson joins as new Chief Executive Officer.

July 2013 Heidi Wood joins as Senior Vice President of Strategy, Mergers and

Acquisitions and Investor Relations.

September 2013 Philip Anderson joins as Senior Vice President Sanjay Kapoor joins as

Senior Vice President and Chief Financial Officer

Key Strategists and Personnel

Larry Lawson

Mr. Lawson joined Spirit as President and

Chief Executive Officer on April 6, 2013. Prior to

joining the firm, Mr. Lawson was Executive Vice

President of Lockheed Martin's Aeronautics

business segment. Mr. Lawson began his career

as a flight control engineer working on the F-15

Eagle at McDonnell Douglas. He has since held a

broad range of leadership positions in

engineering, advanced development, business development, and program management in a

P a g e | 7

career spanning more than 30 years. In his work at Lockheed Martin, Mr. Lawson has overseen

key aircraft production programs such as the F-35, F-22, F-16, C-130J, and C-5, including highly

classified programs in the world-renowned Skunk Works organization. Mr. Lawson holds a

bachelor's degree in Electrical Engineering from Lawrence Technological University, where he

also serves on the board of trustees, has a master's degree in Electrical Engineering from the

University of Missouri, and is a graduate of the Harvard Business School Advanced

Management Program and an MIT Seminar XXI Fellow.

Philip Anderson

Mr. Anderson became the Senior Vice President of Defense and Contracts of Spirit

Holdings effective September 23, 2013. Mr. Anderson previously served as Senior Vice

President and Chief Financial Officer of the company from February 12, 2010 to September

2013. From October 2009 to February 2010, Mr. Anderson served as Vice President and Interim

Chief Financial Officer. Mr. Anderson also served as Treasurer of Spirit from November 2006 to

July 2010. From March 2003 to November 2006, Mr. Anderson was the Director of Corporate

Finance and Banking for Boeing. Mr. Anderson began his career at Boeing in 1989 as a defense

program analyst and served in a variety of finance and manufacturing operations leadership

positions at Boeing Defense Systems and Boeing Commercial Airplanes. Mr. Anderson received

his Bachelor of Arts and Masters of Business from Wichita State University and holds a Six

Sigma Black Belt certification from the University of Michigan.

P a g e | 8

David M. Coleal

Mr. Coleal assumed the role of Executive Vice President/General Manager — Boeing,

Military, Business & Regional Jet Programs & Aftermarket in May 2013 after previously serving

as Senior Vice President /General Manager of the Fuselage Segment since July 2011. Prior to

joining Spirit AeroSystems, Mr. Coleal was Vice President and General Manager of Bombardier-

Learjet. He joined Bombardier Aerospace in March 2008 and was responsible for all engineering

and manufacturing operations, program change management, quality and material logistics for

the Learjet family of aircraft, including development of the pioneering all-composite Learjet 85

mid-size business jet. From 2001 to 2008, Mr. Coleal worked at Cirrus Design Corporation,

where he was initially responsible for operations, and he assumed positions of increasing

responsibility until being named President and Chief Operating Officer in 2005. Mr. Coleal

earned his Masters of Business Administration in Management Science from California State

University — Hayward in 1997. He graduated from California State University in Sacramento in

1990 with a Bachelor of Science degree in Mechanical Engineering Technology.

Sanjay Kapoor

Mr. Kapoor joined Spirit AeroSystems as Senior Vice President and Chief Financial

Officer on September 23, 2013. Mr. Kapoor joined Spirit from Raytheon where he most recently

served as Vice President of Integrated Air & Missile Defense for Raytheon Integrated Defense

Systems (IDS). Prior to this role, Mr. Kapoor was IDS Vice President of Finance and Chief

Financial Officer from 2004 to 2008. Mr. Kapoor also served as CFO at United Technologies'

Pratt and Whitney Power Systems Division. His tenure at Pratt and Whitney also included roles

as Director of Aftermarket Services for the Power Systems Business, controller for the Turbine

P a g e | 9

Module Center and business manager for new commercial programs. Mr. Kapoor received his

bachelor's degree in technology from the Indian Institute of Technology and a dual Masters of

Business Administration in finance and entrepreneurial management from The Wharton School

at the University of Pennsylvania.

Jon D. Lammers

Mr. Lammers was named Senior Vice President — Secretary of Spirit AeroSystems in

July 2012, and General Counsel in October 2012. Mr. Lammers brings more than 20 years of

legal experience, including 15 years at Cargill, Incorporated, where he served from July 1997 to

July 2012. He served as Cargill's Asia Pacific general counsel in Singapore from June 2006 to

June 2010 as well as Cargill's deputy North American general counsel in Wayzata, Minnesota

from July 2010 to July 2012. Mr. Lammers earned his Bachelor of Science in Business

Administration from the University of Southern California and his Juris Doctor degree from the

University of Virginia.

Samantha J. Marnick

Ms. Marnick became Senior Vice President — Chief Administration Officer in October

2012. From January 2011 to September 2012, Ms. Marnick served as Senior Vice President of

Corporate Administration and Human Resources. From March 2008 to December 2010,

Ms. Marnick served as Vice President Labor Relations & Workforce Strategy responsible for

labor relations, global human resource project management office, compensation and benefits,

and workforce planning. Ms. Marnick previously served as Director of Communications and

Employee Engagement from March 2006 to March 2008. Prior to joining the Company,

P a g e | 10

Ms. Marnick was a senior consultant and Principal for Mercer Human Resource Consulting

holding management positions in both the United Kingdom and in the United States. Prior to that

Ms. Marnick worked for Watson Wyatt, the UK's Department of Health and Social Security and

the British Wool Marketing Board. Ms. Marnick holds a Master's degree from the University of

Salford in Corporate Communication Strategy and Management.

John Pilla

Mr. Pilla became the Senior Vice President/General Manager — Airbus and A350 XWB

Program Management in May 2013. Prior to that, Mr. Pilla served as the Senior Vice

President/General Manager, Propulsion Systems Segment of Spirit since July 2009 and added the

role of Senior Vice President/General Manager of the Wing segment in September 2012. From

July 2011 to May 2013, he was also responsible for the Aftermarket Customer Support

Organization. From April 2008 to July 2009, Mr. Pilla was Chief Technology Officer of Spirit

and he served as Vice President/General Manager, a position he assumed at the date of the

Boeing Acquisition in June 2005 and held until March 2008. Mr. Pilla began his career at

Boeing Commercial Airplanes in 1981 as a stress engineer and was promoted to Chief Engineer

of Structures and Liaison in 1995. In 1997, Mr. Pilla led the Next-Generation 737 engineering

programs and ultimately led the Define Team on the 737-900 fuselage and empennage in late

1997 as well as the 777LR airplane in May 2000. In July 2001, Mr. Pilla became the Director of

Business Operations, a position he held until July 2003 when he accepted an assignment as 787

Director of Product Definition and Manufacturing. He received his Master's degree in Aerospace

Structures Engineering in 1986 and a Masters in Business Administration in 2002 from Wichita

State University.

P a g e | 11

Heidi Wood

Ms. Wood joined the firm as Senior Vice President — Strategy, Mergers and

Acquisitions and Investor Relations in July 2013. Prior to joining the Company, Ms. Wood was

Senior Vice President and Co-head of Global Sales at Avjet Corporation. From 1999 to 2013,

Ms. Wood served as Managing Director and global head of aerospace/defense analysis at

Morgan Stanley. She was responsible for leading North American, Europe, Latin American and

Singapore-based teams. Prior to assuming her employment at Morgan Stanley, Ms. Wood was an

analyst at Cowen & Company from 1992 to 1999. Ms. Wood holds a Bachelor of Arts degree

with honors from Brown University.

P a g e | 12

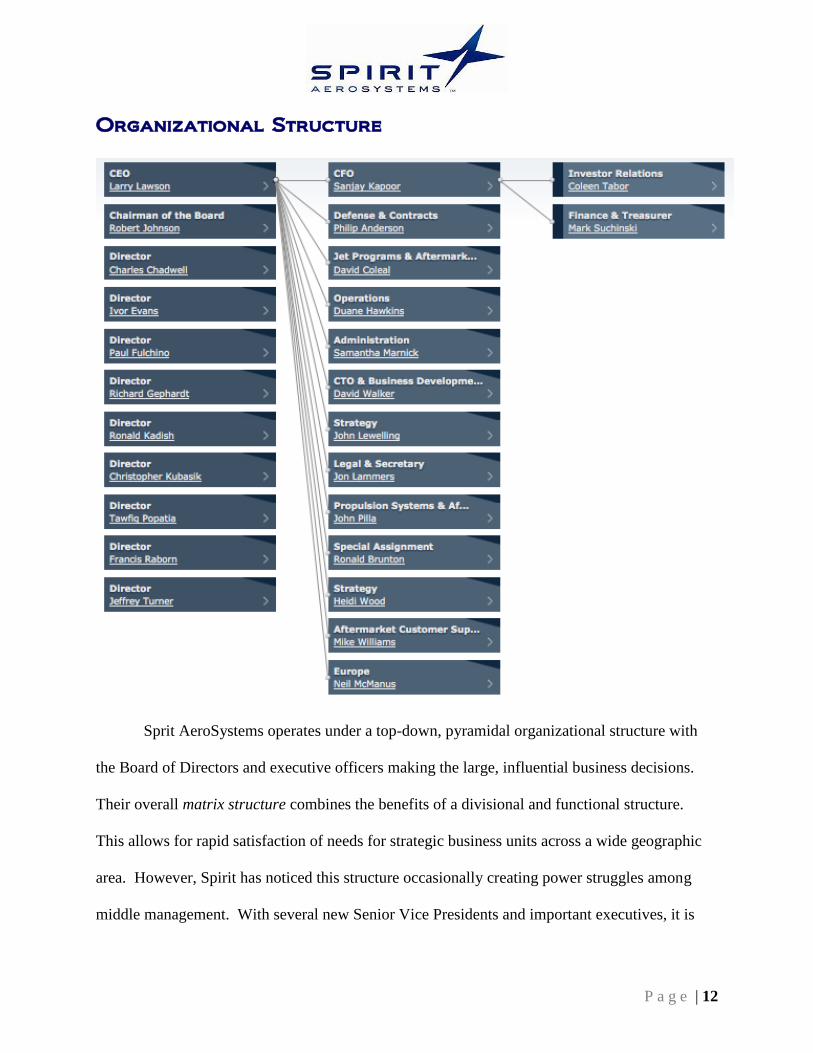

Organizational Structure

Sprit AeroSystems operates under a top-down, pyramidal organizational structure with

the Board of Directors and executive officers making the large, influential business decisions.

Their overall matrix structure combines the benefits of a divisional and functional structure.

This allows for rapid satisfaction of needs for strategic business units across a wide geographic

area. However, Spirit has noticed this structure occasionally creating power struggles among

middle management. With several new Senior Vice Presidents and important executives, it is

P a g e | 13

crucial that their leadership and people skills reach the employees on the bottom of the hierarchy

ladder.

Mission Statement

“Spirit AeroSystems, Inc. aims to create long-term value by providing industry-

leading aero structures and systems achieved through competitive cost and product

leadership, derived from our people, knowledge and technology.”

Goals

In its 2013 annual report, Spirit AeroSystems Holdings, Inc. outlined three specific goals.

They are as follows: Support Increased Aircraft Deliveries, Win New Business from Existing

and New Customers, and Research and Development Investments in Next Generation

Technologies. In order to achieve these goals, the company outlined specific initiatives for each

of its goals.

1. Support Increased Aircraft Deliveries. Spirit AeroSystems, Inc. values being the largest

independent aerostructures supplier to both Boeing and Airbus and core to their business strategy

is a determination to meet or exceed their expectations under their existing supply arrangements.

Spirit is constantly focused on improving their manufacturing efficiency maintaining their high

standards of quality and on-time delivery to meet these expectations. They are also focused on

supporting their customers’ increase in new aircraft production and the introduction of key

aircraft programs such as the Boeing B787 and the Airbus A380.

P a g e | 14

2. Win New Business from Existing and New Customers. Spirit AeroSystems have established a

sales and marketing infrastructure to support their efforts to win business from new and existing

customers. The firm believes that they are well positioned to win additional work from Boeing

and Airbus, given their strong relationships, their size, design and build capabilities and their

financial resources, which are necessary to make proper investments.

3. Research and Development Investment in Next Generation Technologies. Spirit invests in

direct research and development, or R&D, for current programs to strengthen their relationships

with their customers and new programs to generate new business. As part of their R&D effort,

they work closely with OEMs and integrate their engineering teams into their design processes.

Spirit believes their close coordination with OEMs positions them to win new business on new

commercial and military platforms.

Objectives

- Be the design build partner of choice

- Grow the business with a diversified portfolio

- Grow market share and volume to maintain #1 share position

Organization Culture

Spirit AeroSystems, Inc. has had a consistent culture for decades. Because of their long

term supply contracts with the biggest players in the aircraft manufacturing industry, Spirit has

shared in the successes throughout the development of the airline industry. Many of the

innovations and new technologies are product of genius in both the systems / structures

P a g e | 15

manufacturers’ and the aircraft manufactures’ personnel. Spirit’s market dominance has allowed

them to attract and recruit industry leaders and leadership to create the preeminent aeroSystems

manufacturer in the world with a focus on manufacturing on a global scale. It is what makes

Spirit competitive and why the biggest names in the industry are calling Spirit their “partner.”

For their employees, Spirit offers amenities, like onsite cafeteria, onsite medical staff,

onsite credit union, onsite Starbucks coffee, a tuition assistance program, health and wellness

programs, and the other appropriate benefits to fuel the creative fire and support the intuitive

minds responsible for their innovative product offerings. Spirit consistently employs ambitious

people who thrive in an environment of on-the-job training and continuous improvement.

Employees also get discounts at companies like Apple, major cell phone carriers, and Microsoft.

Leadership Style

Current employees were forced to bear some changes in leadership style when Larry

Lawson succeeded former CEO, Jeff Turner. Mr. Lawson, as a person, is quite respected

according to analysts within the aerospace and defense industry. When the board of directors set

out for a new CEO, they sought out someone, “with a strong record of operating and financial

performance on both mature and new aircraft programs with the ability to take Spirit to the next

level.”

With the acquisition of this position, Mr. Lawson obtains reward, and coercive powers.

He brought expert and personal power to the company and has potentially established some

referent power. The new individuals to fill these leadership positions were all hired as

“sustainers”. Their style allows for a participative and family aura among the organization.

P a g e | 16

However, each and every manager and leader is responsible for implementing the CEOs vision

adjustment without losing their origins.

Industry and Competition

Spirit AeroSystems falls within the “industrials” sector and “aerospace and defense”

industry. The company is traded in the New York Stock Exchange and is sometimes associated

with the “commercial aircraft” sub-industry. Expert analysts are forecasting significant revenue

and earnings growth, with record setting production levels within the commercial aerospace

industry. However, the defense aspect of the industry is expected to decrease in the coming

years.

Competitors within this industry fall under two categories: non original equipment

manufacturers, and original equipment manufacturers (OEMs). The most prevalent competition

comes from the internal divisions of OEMs and third-party aerostructure suppliers. Spirit is

considered a third-party non-OEM aerostructure manufacturer.

Spirit AeroSystems’ principal competitors among OEMs include: Airbus, Boeing,

Dassault Aviation, Embraer, Gulfstream (General Dynamics), Hawker Beechcraft, United

Technologies, and Bell Helicopter. These OEMs may chose to outsource production of certain

aerostructures due to their own direct labor and overhead considerations and capacity utilization

at their own facilities.

Their significant competitors among other non-OEM aerostructures suppliers are:

Aircelle S.A., Alenia Aeronautica, Fuji Heavy Industries, GKN Aerospace, Goodrich

Corporation, Kawasaki Heavy Industries, Mitsubishi Heavy Industries, Sonaca, Snecma,

Triumph Group, Premium Aerotech, and Nexcelle.

P a g e | 17

Current Strategies

Grand

Spirit AeroSystems, Inc. is currently pursuing a maintenance / turnaround strategy. Spirit

is attempting to maintain current partnerships with the leaders in the aircraft manufacturing

industry while working to restructure and refine its cost structure to help Spirit focus on rate

increases, consolidate resources, and create efficiencies to reach its goals of future growth. This

refine focus will hopefully reduce profit loss and allow for a consistent future net profit.

Corporate

Through redefinition of the corporate management structure, Spirit has added three top

executives with industry leaders who have proven success and experience, a VP of Strategy,

Mergers and Acquisitions, and Investor Relations, Senior VP of Operations, and a new Chief

Financial Officer. By replacing executives in positions with the greatest need for change, Spirit

hopes that this newly acquired talent will attract other individuals within the organizations that

will allow them to make strategic change toward profitability and growth.

Business

Spirit AeroSystems Inc. is the leading supplier of aerostructures such as fuselage systems,

propulsions systems, and wing systems to the world’s two largest aircraft manufacturers, Boeing

and Airbus. Their products are primarily used in the production of large commercial airplanes,

business and regional jets, as well as military aircraft, including helicopter and plane design.

P a g e | 18

Functional

Marketing

Spirit holds a strong market position in a very competitive market environment. The

company holds about 16% share of the global aerostructures market. It is the largest independent

suppliers of aerostructures to Airbus and Boeing, the two largest aircraft OEMs. Thus, strong

market position enhances its brand image of the company itself, and further increases the

bargaining power of the company. The sales directors establish and maintain relationships with

customers and are supported in their campaigns by sales teams within specific product specialties

and a market research team performing various analyses related to those products and customers.

The comprehensive sales and marketing teams work closely to ensure a consistent, single

message approach with customers both domestically and internationally.

Finance

The company divides its business into four segments: fuselage systems, wing systems,

propulsion systems, and other. As a result they are not reliant on any one segment of the business

for the entirety of their income. In addition to the diversified product portfolio, the company has

a well-balanced revenue mix and their net sales have continued to grow over the past four years.

Spirit relies on current and continued business with Boeing and Airbus, which combined made

up 94% of Spirit’s total sales revenue in 2013. In the past two years, Spirit has seen diminishing

profit margins while increasing sales, becoming less solvent. This may be a product of poor/over

investment in new product/designs, or the expensive ownership of certain SBUs not essential to

revenue-generating business.

P a g e | 19

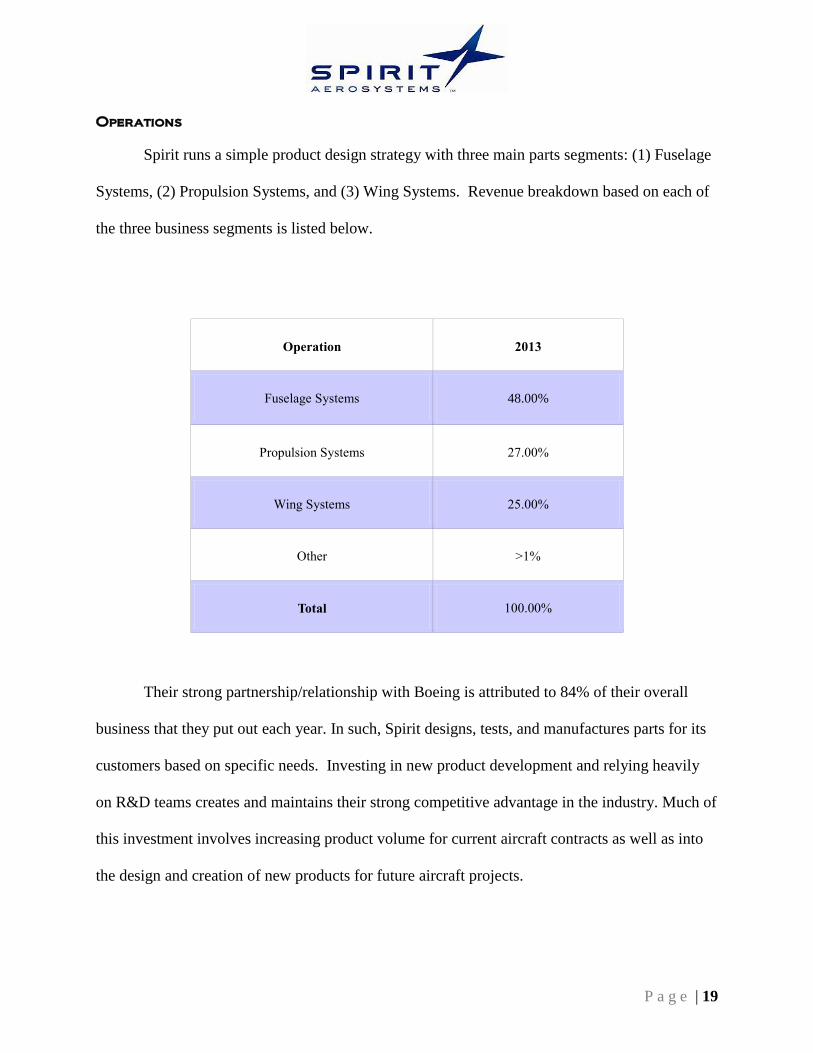

Operations

Spirit runs a simple product design strategy with three main parts segments: (1) Fuselage

Systems, (2) Propulsion Systems, and (3) Wing Systems. Revenue breakdown based on each of

the three business segments is listed below.

Operation 2013

Fuselage Systems 48.00%

Propulsion Systems 27.00%

Wing Systems 25.00%

Other >1%

Total 100.00%

Their strong partnership/relationship with Boeing is attributed to 84% of their overall

business that they put out each year. In such, Spirit designs, tests, and manufactures parts for its

customers based on specific needs. Investing in new product development and relying heavily

on R&D teams creates and maintains their strong competitive advantage in the industry. Much of

this investment involves increasing product volume for current aircraft contracts as well as into

the design and creation of new products for future aircraft projects.

P a g e | 20

Human Resources

Based on significant research into Spirit’s HR environment, employees of the company

are rewarded with competitive salaries and benefits, and a healthy, energizing work environment

in multiple sectors such as engineering, manufacturing, shipping, etc. Ratings of 4/5 or above

are consistent among most company reviews. The importance placed on new-product creation

and development lends a creative, competitive work environment that is challenging to all

employees of the company.

Information

The firm is constantly looking to implement systems that lower their production costs and

improve relationships with suppliers and customers. Spirit AeroSystems’ Information

Technology capabilities were built around the Infor/Exceed Warehouse Management System.

The majority of their information systems have been outsourced to a 3rd

party logistics company

called DB Schenker. Improvements in manufacturing efficiency, or lack thereof, can also be

attributed to Spirit’s motivated Research and Development Department.

Management

Spirit’s functional strategies concerning management include replacing top-level

executives with experienced individuals with vast knowledge of the industry. With over 16,000

employees globally, the new leadership is trying to reach everyone through a more efficient

middle management structure. Department heads within the different strategic business units

(SBUs) are in charge of implementing the most recent changes set forth by Mr. Larry Lawson

and his fellow executives.

P a g e | 21

Marketing Audit

Spirit AeroSystems, Inc. has an established sales and marketing infrastructure which

supports efforts to expand business with new and existing customers in three sectors of the

aerostructures industry: (1) large commercial airplanes, (2) business and regional jets and (3)

military/helicopter. The sales directors establish and maintain relationships with individual

customers and are supported in their campaigns by sales teams within specific product specialties

and a market research team performing various analyses related to those products and customers.

The comprehensive sales and marketing teams work closely to ensure a consistent, single

message approach with customers both domestically and internationally.

Product

As noted before, Spirit AeroSystems, Inc. is one of the largest independent non-OEM

aircraft parts designers and manufacturers. Aerostructures are structural components which

Spirit produces for both commercial and military aircrafts. These aerostructures are organized

into three principal segments: (1) Fuselage Systems, which includes forward, mid and rear

fuselage sections, (2) Propulsion Systems, which includes nacelles, struts/pylons and engine

structural components; and (3) Wing Systems, which includes wing systems and components,

flight control surfaces and other structural parts. These products are result of many SBUs within

the company, including Research and Development, Manufacturing, and Engineering

departments which allow for complete control over the production, installation and service

processes.

P a g e | 22

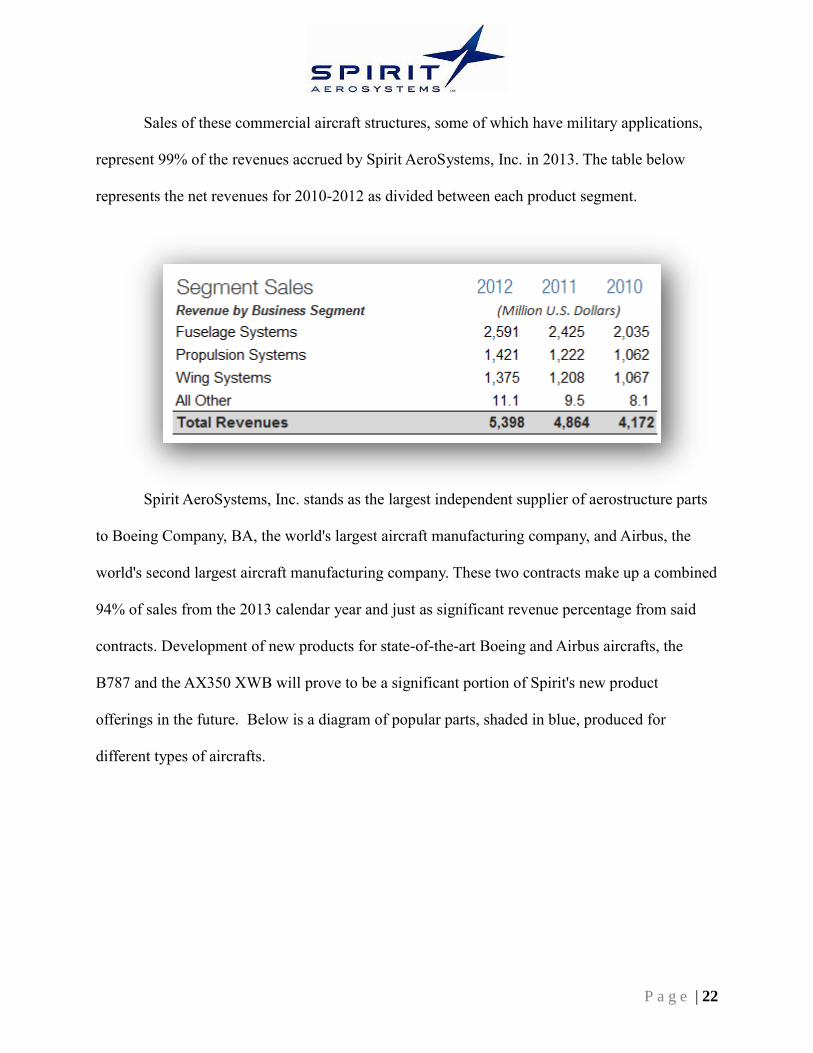

Sales of these commercial aircraft structures, some of which have military applications,

represent 99% of the revenues accrued by Spirit AeroSystems, Inc. in 2013. The table below

represents the net revenues for 2010-2012 as divided between each product segment.

Spirit AeroSystems, Inc. stands as the largest independent supplier of aerostructure parts

to Boeing Company, BA, the world's largest aircraft manufacturing company, and Airbus, the

world's second largest aircraft manufacturing company. These two contracts make up a combined

94% of sales from the 2013 calendar year and just as significant revenue percentage from said

contracts. Development of new products for state-of-the-art Boeing and Airbus aircrafts, the

B787 and the AX350 XWB will prove to be a significant portion of Spirit's new product

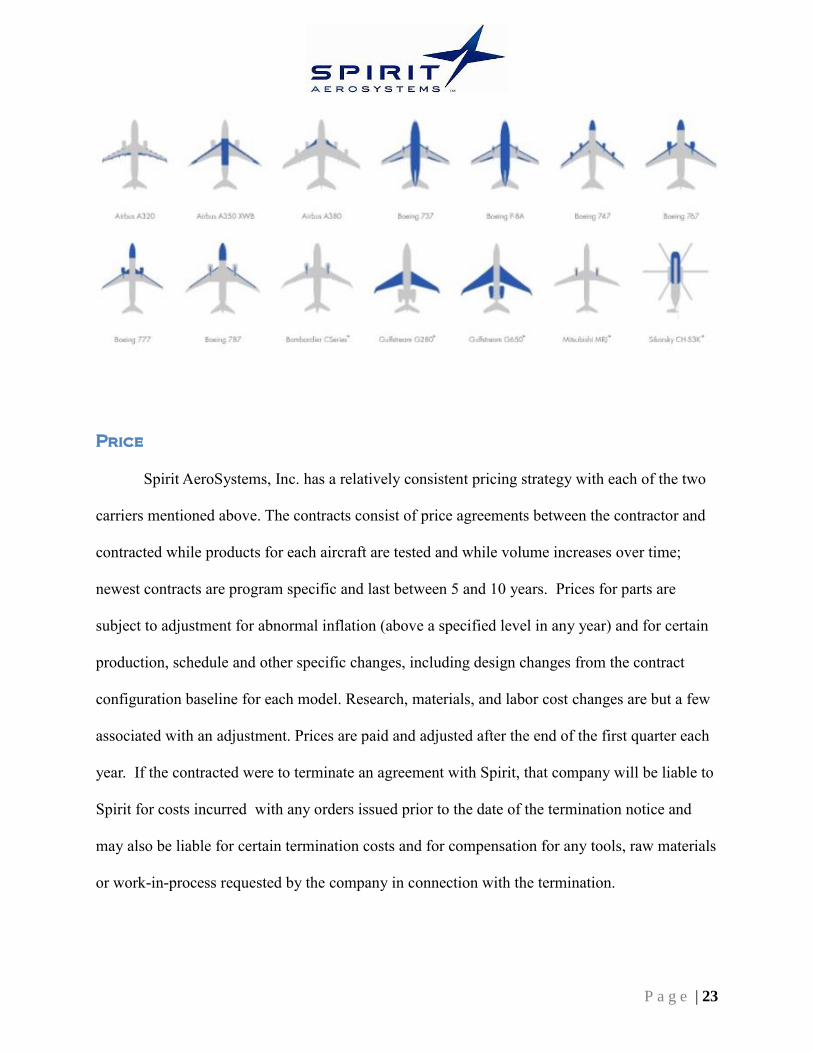

offerings in the future. Below is a diagram of popular parts, shaded in blue, produced for

different types of aircrafts.

P a g e | 23

Price

Spirit AeroSystems, Inc. has a relatively consistent pricing strategy with each of the two

carriers mentioned above. The contracts consist of price agreements between the contractor and

contracted while products for each aircraft are tested and while volume increases over time;

newest contracts are program specific and last between 5 and 10 years. Prices for parts are

subject to adjustment for abnormal inflation (above a specified level in any year) and for certain

production, schedule and other specific changes, including design changes from the contract

configuration baseline for each model. Research, materials, and labor cost changes are but a few

associated with an adjustment. Prices are paid and adjusted after the end of the first quarter each

year. If the contracted were to terminate an agreement with Spirit, that company will be liable to

Spirit for costs incurred with any orders issued prior to the date of the termination notice and

may also be liable for certain termination costs and for compensation for any tools, raw materials

or work-in-process requested by the company in connection with the termination.

P a g e | 24

Promotion

Spirit AeroSystems, Inc. has long-term contracts with Boeing and Airbus on many of

their major aircraft development programs, such as the B737, B787, A320, A350 XWB and

A380. OEMs generally desire to minimize costs by retaining established aerostructure suppliers

Spirit’s sales and marketing team continues to maintain strong relationships with these OEMs to

position Spirit for future business opportunities with these manufacturers by maintaining regular

contact with key Boeing and Airbus decision-makers.

Spirit maintains a customer contact database to maximize interactions with existing and

potential customers. In the time that Spirit has existed as an independent company, they have

been successful in building a positive identity and name recognition for the company brand

through advertising, trade shows, sponsorships and Spirit customer events. In order to diversify

and win new customers globally, Spirit markets their expertise in the design and manufacture of

major aerostructures and advanced manufacturing capabilities, all with both composites and

traditional metals processes. This ensures Spirit is on the cutting edge of aerostructure

technology.

Place

Aerostructures and systems developed by Spirit AeroSystems, Inc. very clearly cannot be

purchased online or in a retail store. Many of their products reach contracted customer directly

from the manufacturing centers. Though Spirit does participate in industry trade shows and hold

customer events to advertise new products, most developments are demand-driven. As holder of

contracts from the two largest aircraft manufacturers in the world, Spirit's research and

development, design, manufacturing, and testing processes are organized around the needs of

P a g e | 25

those customers, Boeing and Airbus. Private meetings and test demonstrations prove to be the

location of most points of sale for Spirit.

P a g e | 26

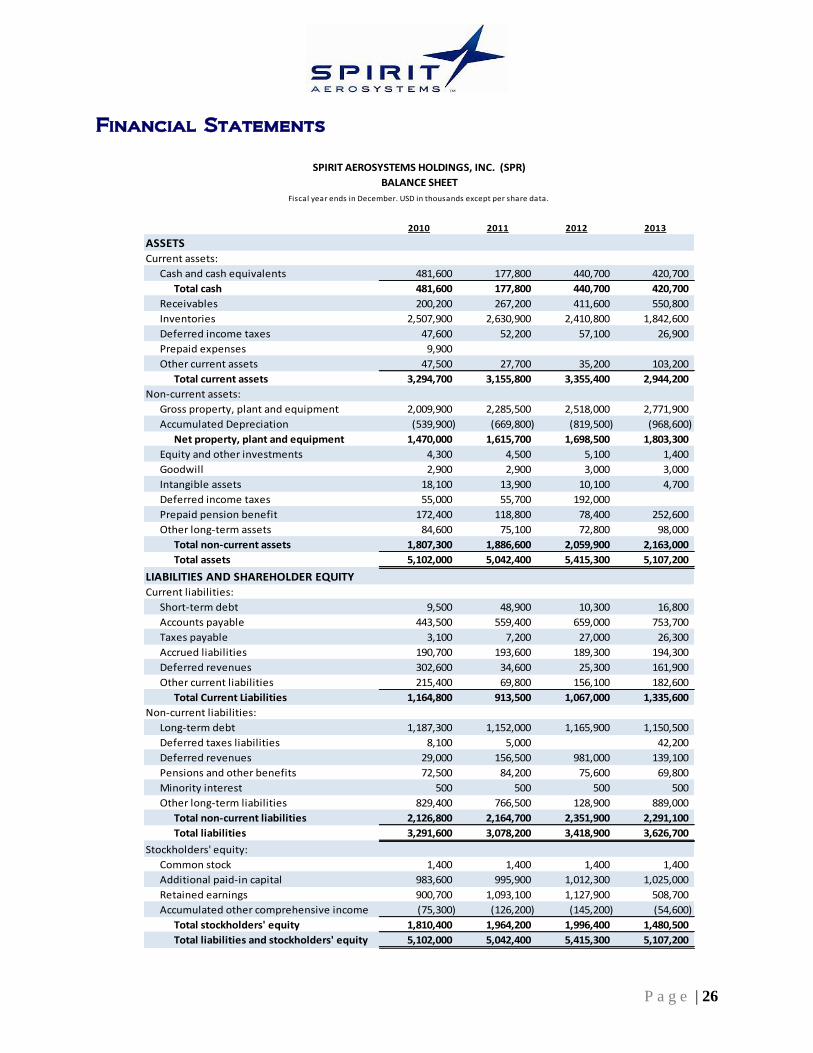

Financial Statements

2010 2011 2012 2013

ASSETS

Current assets:

Cash and cash equivalents 481,600 177,800 440,700 420,700

Total cash 481,600 177,800 440,700 420,700

Receivables 200,200 267,200 411,600 550,800

Inventories 2,507,900 2,630,900 2,410,800 1,842,600

Deferred income taxes 47,600 52,200 57,100 26,900

Prepaid expenses 9,900

Other current assets 47,500 27,700 35,200 103,200

Total current assets 3,294,700 3,155,800 3,355,400 2,944,200

Non-current assets:

Gross property, plant and equipment 2,009,900 2,285,500 2,518,000 2,771,900

Accumulated Depreciation (539,900) (669,800) (819,500) (968,600)

Net property, plant and equipment 1,470,000 1,615,700 1,698,500 1,803,300

Equity and other investments 4,300 4,500 5,100 1,400

Goodwill 2,900 2,900 3,000 3,000

Intangible assets 18,100 13,900 10,100 4,700

Deferred income taxes 55,000 55,700 192,000

Prepaid pension benefit 172,400 118,800 78,400 252,600

Other long-term assets 84,600 75,100 72,800 98,000

Total non-current assets 1,807,300 1,886,600 2,059,900 2,163,000

Total assets 5,102,000 5,042,400 5,415,300 5,107,200

LIABILITIES AND SHAREHOLDER EQUITYCurrent liabilities:

Short-term debt 9,500 48,900 10,300 16,800

Accounts payable 443,500 559,400 659,000 753,700

Taxes payable 3,100 7,200 27,000 26,300

Accrued liabilities 190,700 193,600 189,300 194,300

Deferred revenues 302,600 34,600 25,300 161,900

Other current liabilities 215,400 69,800 156,100 182,600

Total Current Liabilities 1,164,800 913,500 1,067,000 1,335,600

Non-current liabilities:

Long-term debt 1,187,300 1,152,000 1,165,900 1,150,500

Deferred taxes liabilities 8,100 5,000 42,200

Deferred revenues 29,000 156,500 981,000 139,100

Pensions and other benefits 72,500 84,200 75,600 69,800

Minority interest 500 500 500 500

Other long-term liabilities 829,400 766,500 128,900 889,000

Total non-current liabilities 2,126,800 2,164,700 2,351,900 2,291,100

Total liabilities 3,291,600 3,078,200 3,418,900 3,626,700

Stockholders' equity:

Common stock 1,400 1,400 1,400 1,400

Additional paid-in capital 983,600 995,900 1,012,300 1,025,000

Retained earnings 900,700 1,093,100 1,127,900 508,700

Accumulated other comprehensive income (75,300) (126,200) (145,200) (54,600)

Total stockholders' equity 1,810,400 1,964,200 1,996,400 1,480,500

Total liabilities and stockholders' equity 5,102,000 5,042,400 5,415,300 5,107,200

SPIRIT AEROSYSTEMS HOLDINGS, INC. (SPR)

Fiscal year ends in December. USD in thousands except per share data.

BALANCE SHEET

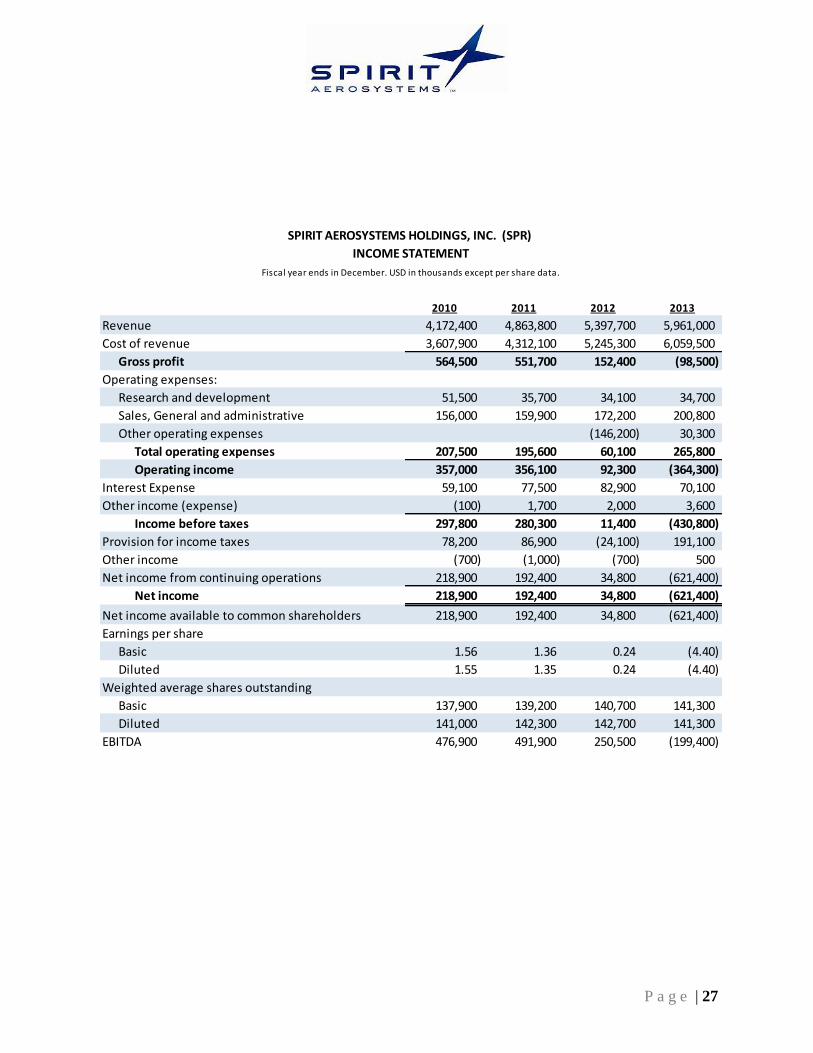

P a g e | 27

2010 2011 2012 2013

Revenue 4,172,400 4,863,800 5,397,700 5,961,000

Cost of revenue 3,607,900 4,312,100 5,245,300 6,059,500

Gross profit 564,500 551,700 152,400 (98,500)

Operating expenses:

Research and development 51,500 35,700 34,100 34,700

Sales, General and administrative 156,000 159,900 172,200 200,800

Other operating expenses (146,200) 30,300

Total operating expenses 207,500 195,600 60,100 265,800

Operating income 357,000 356,100 92,300 (364,300)

Interest Expense 59,100 77,500 82,900 70,100

Other income (expense) (100) 1,700 2,000 3,600

Income before taxes 297,800 280,300 11,400 (430,800)

Provision for income taxes 78,200 86,900 (24,100) 191,100

Other income (700) (1,000) (700) 500

Net income from continuing operations 218,900 192,400 34,800 (621,400)

Net income 218,900 192,400 34,800 (621,400)

Net income available to common shareholders 218,900 192,400 34,800 (621,400)

Earnings per share

Basic 1.56 1.36 0.24 (4.40)

Diluted 1.55 1.35 0.24 (4.40)

Weighted average shares outstanding

Basic 137,900 139,200 140,700 141,300

Diluted 141,000 142,300 142,700 141,300

EBITDA 476,900 491,900 250,500 (199,400)

SPIRIT AEROSYSTEMS HOLDINGS, INC. (SPR)

Fiscal year ends in December. USD in thousands except per share data.

INCOME STATEMENT

P a g e | 28

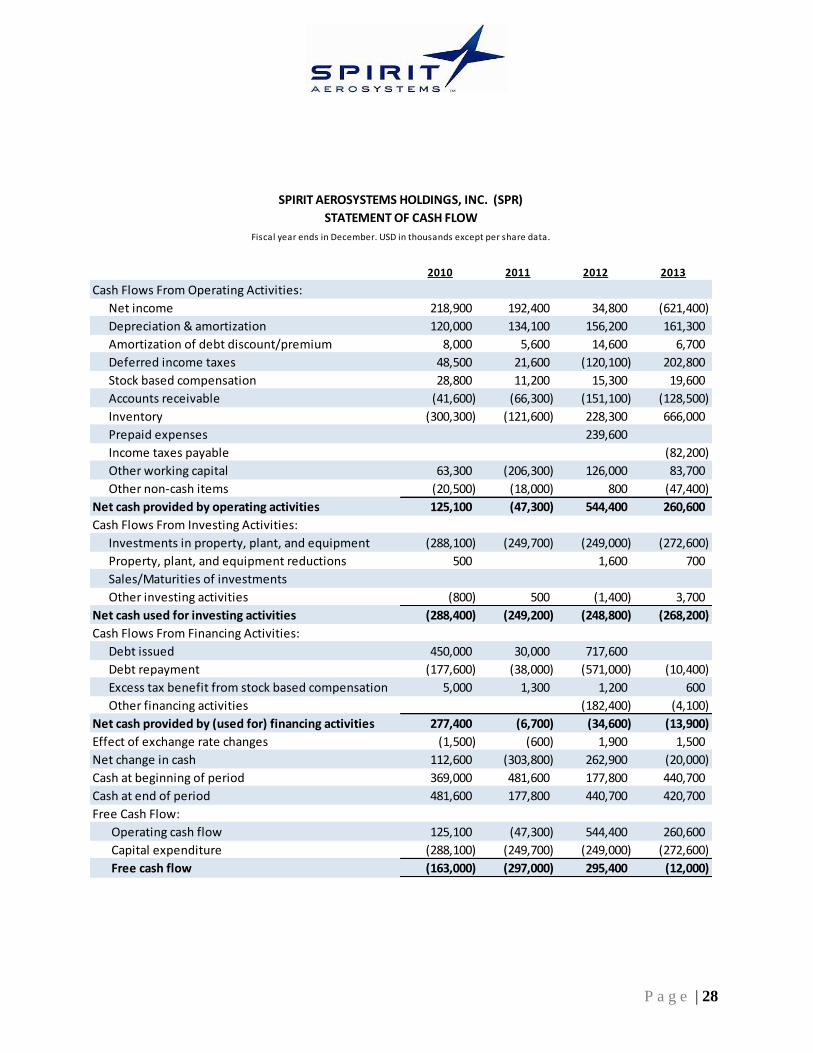

2010 2011 2012 2013

Cash Flows From Operating Activities:

Net income 218,900 192,400 34,800 (621,400)

Depreciation & amortization 120,000 134,100 156,200 161,300

Amortization of debt discount/premium 8,000 5,600 14,600 6,700

Deferred income taxes 48,500 21,600 (120,100) 202,800

Stock based compensation 28,800 11,200 15,300 19,600

Accounts receivable (41,600) (66,300) (151,100) (128,500)

Inventory (300,300) (121,600) 228,300 666,000

Prepaid expenses 239,600

Income taxes payable (82,200)

Other working capital 63,300 (206,300) 126,000 83,700

Other non-cash items (20,500) (18,000) 800 (47,400)

Net cash provided by operating activities 125,100 (47,300) 544,400 260,600

Cash Flows From Investing Activities:

Investments in property, plant, and equipment (288,100) (249,700) (249,000) (272,600)

Property, plant, and equipment reductions 500 1,600 700

Sales/Maturities of investments

Other investing activities (800) 500 (1,400) 3,700

Net cash used for investing activities (288,400) (249,200) (248,800) (268,200)

Cash Flows From Financing Activities:

Debt issued 450,000 30,000 717,600

Debt repayment (177,600) (38,000) (571,000) (10,400)

Excess tax benefit from stock based compensation 5,000 1,300 1,200 600

Other financing activities (182,400) (4,100)

Net cash provided by (used for) financing activities 277,400 (6,700) (34,600) (13,900)

Effect of exchange rate changes (1,500) (600) 1,900 1,500

Net change in cash 112,600 (303,800) 262,900 (20,000)

Cash at beginning of period 369,000 481,600 177,800 440,700

Cash at end of period 481,600 177,800 440,700 420,700

Free Cash Flow:

Operating cash flow 125,100 (47,300) 544,400 260,600

Capital expenditure (288,100) (249,700) (249,000) (272,600)

Free cash flow (163,000) (297,000) 295,400 (12,000)

SPIRIT AEROSYSTEMS HOLDINGS, INC. (SPR)

Fiscal year ends in December. USD in thousands except per share data.

STATEMENT OF CASH FLOW

P a g e | 29

Financial Ratio Analysis

A thorough financial analysis is essential to fully grasp the health and performance of a

company. In this section, Spirit AeroSystems, Inc. will be dissected so that conclusions can be

made according to their financial reports. Four fiscal years were analyzed in the ratio analysis:

2010, 2011, 2012, and 2013. The ratios calculated depict the company’s liquidity, profitability,

activity/efficiency, and solvency.

Liquidity

A company’s liquidity speaks volumes to the health of that company. These ratios show

Spirit AeroSystems’ ability to pay off its short-term debt obligations. Creditors look at these

numbers very closely as it shows how easily a company can turn its assets into cash to cover

debt.

Current Ratio: This ratio is calculated by dividing current assets by current liabilities and

expresses the company’s ability to pay off current obligations. Creditors usually like to see a

high number for this ratio so that they are confident in loaning the money. They are much more

likely to get their money back from a company with a current ratio of 4.0 as to a company with

more liabilities than assets. However, shareholders may like to see this number lower, which

shows the assets are potentially working to grow the business.

In the four years analyzed, Spirit AeroSystems had a current ratio of 2.83, 3.45, 3.14, and

2.20. These values fall within a very good range and suggest the company is very liquid and

more than able to cover its short-term debt with its total current assets. Their current ratio is

slightly above the industry average. For example, over the four fiscal years analyzed in this

P a g e | 30

section, Boeing had an average current ratio of 1.22. Airbus Group averaged 0.95 and Lockheed

Martin Corporation averaged 1.15. All in all, looking at this ratio only, Spirit is very liquid.

Quick Ratio: This ratio signifies the true ‘working capital’ relationship of the company’s

cash, accounts receivables, and notes receivables available to meet its short-term obligations. It

is calculated by subtracting inventories from current assets and then dividing by current

liabilities. Therefore, if a company has a substantial amount of slow-moving inventory, the

current ratio could overstate the firm’s ability to pay current debt. An ideal quick ratio value for

this industry is right at 1.0.

In 2010, 2011, 2012, and 2013, Spirit Aerosystems had quick ratio values of 0.62, 0.49,

0.81, and 0.73 respectively. These values suggest that without their inventories, the firm would

not be able to cover its short-term liabilities. This calculation shows a large discrepancy between

the current and quick ratios. In 2011, Spirit inventories made up over 83 percent of their total

current assets. However, when comparing these values to the industry, the firm was not far off.

Their competitors all had quick ratios under 1.0 for the years 2010-2013.

Net Working Capital: Management can use their net working capital numbers to

determine if they should become more liquid or invest more in the business. The objective is to

have a positive working capital number. In accordance to the current ratio, the net working

capital for Spirit was greater than 2 billion dollars in years 2010-2012. In 2013, it dropped to 1.6

billion. It is important to keep in mind when looking at these high net working capital values

that the majority of Spirit AeroSystems’ current assets is made up of inventory.

Cash Ratio: In 2010, 2011, 2012, 2013, the firm had cash ratio values of 0.41, 0.19, 0.41,

and 0.31 respectively. This ratio is calculated by dividing “cash and cash equivalents” by the

P a g e | 31

company’s current liabilities. It focuses on the most liquid of monetary values. Accounts

receivable and inventories are not included in this ratio and thus it is not a comprehensive

measure of a firm’s liquidity. However, it does show us that in 2011, Spirit AeroSystems had a

shortage of cash and cash equivalents. They had over $200 million less cash in this year relative

to the other 3 years analyzed. This ratio suggests that cash and cash equivalents represent a

small portion of Spirit’s total current assets.

OVERALL LIQUIDITY GRADE: B+

Profitability

A company’s profitability is important in determining its performance and success for a

given period of time. Spirit Aerosystems’ profitability was analyzed by using the following

ratios: gross profit margin, net profit margin, return on total assets, earnings per share, and

operating income. These calculations will provide insight as to how well the firm is generating

earnings relative to their incurred expenses.

Gross Profit Margin: This value measures what proportion of revenue is converted into

gross profit. Managers of the firm can use gross profit margins to analyze trends in the cost of

production and determine profit gains or losses. It is calculated by dividing the gross profit

(Revenue - Cost of Goods Sold) by total revenues. Spirit Aerosystems is really struggling to

generate a quality profit margin. The percentage fell consistently and significantly the past four

years. In 2010, they had a mediocre gross profit margin of 13.5%. However, in 2013 they had a

net loss of 98.5 million dollars and suffered a -1.65 profit margin. The biggest drop was from

2011 to 2012, where it dropped from 11.3% to 2.8%. Regardless of the industry these values are

not ideal and must be addressed.

P a g e | 32

Net Profit Margin Ratio: This ratio is calculated by dividing net income by revenues. It

is an efficiency measurement use to determine the percentage of profits earned per dollar of

sales. Like the gross profit margin, Spirit Aerosystems experienced a consistent downward trend

in this measurement which is forecasting serious, potential financial problems. In 2013, the net

profit margin reached an all-time low of -10.42%.

Return on Assets: One of the most important ratios in determining the efficiency of a

company’s investments/assets is the return on assets ratio. It can be used in nearly every aspect

of business and is calculated by dividing the net earnings by the firm’s total assets. In other

words, it shows analysts how well the company’s assets are creating income for the business. In

2010, 2011, 2012, 2013, Spirit Aerosystems had a return on assets percent of 4.57%, 3.79%,

0.67%, and -11.81% relatively. The same declining trend is noticed in this calculation as well.

Ideally, the higher this measure, the better because it suggests the company is making more

revenue on fewer investments.

A deeper analysis of their ROA numbers must be performed. These downward trends are

largely due to an almost unmanageable rise in cost of goods sold. From 2010 to 2013, Spirit

Aerosystems’ cost of revenue has increased nearly 3 billion dollars. This, in turn, affects the

gross profit and ultimately the net income. Their total assets have stayed pretty consistent at

about 5 billion for each fiscal year. Overall, these ROA values are less than desirable, especially

in 2013.

Earnings Per Share: The EPS figure shows what portion of a company’s profits are

allocated to each outstanding share of common stock. It is calculated by subtracting preferred

dividends from net income and then dividing by the average number of common shares

P a g e | 33

outstanding. In 2013, Spirit Aerosystems operated at a loss and therefore had a negative EPS

figure. Investors saw the best EPS values in 2011 and 2012 with 1.55 and 1.35 respectively.

Operating Income: This calculation is used to compare companies within an industry

because it eliminates the effects of financing and accounting decisions. It is simply the firm’s

total revenue minus expenses (excluding interest, taxes, depreciation, and amortization). There

is often times much discretion as to what is included in this calculation, which is why this ratio is

not a GAAP approved measure. However, in Spirit Aerosystems case, it shows that taxes and

interest expenses are not the reason for their declining numbers. They generated a positive

operating income three of the four years analyzed. In 2013, a disappointing 364 billion dollar

operating loss was experienced.

OVERALL PROFITABILITY GRADE: D-

Activity/Efficiency

A large part of a company’s success is determined by how effectively is uses its

inventory and other assets. In this section, Spirit Aerosystems’ efficiency will be measured using

various activity ratios. It will provide a closer look at what role their large inventory numbers

play within the business. The ratios in this analysis include: accounts receivable turnover,

inventory turnover, asset turnover, fixed asset turnover, and sales to net working capital.

Accounts Receivable Turnover: This ratio depicts how soon your sales will become cash

by the firm’s ability to collect outstanding receivables. The faster Spirit Aerosystems can turn

over their A/R, the more liquid they will be. Accounts receivable turnover can be found by

dividing total credit sales divided by average net receivables. In 2010, they firm’s ratio was

P a g e | 34

23.14 but fell to 12.39 in 2013. These figures are used mostly by creditors. Overall, Spirit

Aerosystems’ receivable turnover numbers are healthy. However, if the ratio continues to drop,

they may need to re-assess their credit policies in order to ensure the timely collection of credit.

It took the firm 15.8, 17.5, 22.9, and 29.4 days, on average, to collect their outstanding

receivables in the four years analyzed.

Inventory Turnover: Inventory turnover shows how many times a company’s inventory

is sold and replaced over a period of time. This calculation is derived by dividing cost of goods

sold by the average inventory. Generally speaking, a high inventory turnover ratio is a good

thing because inventories are the least liquid type of asset. The ratios for the fiscal years 2010-

2013 were 1.53, 1.68, 2.08, and 2.85 respectively. The industry average is relatively low at

approximately 2.0 because these type of companies often times they have significant assets tied

up in inventory. Spirit Aerosystems is right where they need compared to the industry they fall

in.

Asset Turnover: Asset turnover ratio shows the firm’s ability to generate sales through

the use of its assets. This computation is most used by shareholders and is calculated by dividing

net sales over the average total assets. The higher the company’s asset turnover, the lower its

profit margin tends to be. Throughout all four years, Spirit Aerosystems’ asset turnover ratio

remained very consistent, ranging from 0.90-1.10. These figures are right in the middle of the

average asset turnover numbers for this industry. Its highest asset turnover occurred in 2013,

which is attributable to the company’s low profit margin. This calculation is ineffective when

comparing to unrelated firms. However, when compared to Spirit Aerosystems’ competitors,

they are in good position.

P a g e | 35

Fixed Asset Turnover: Fixed asset turnover is computed by dividing net sales and total

fixed assets. It describes how efficiently a company uses its plant, equipment, and other fixed

assets to generate sales. A declining trend suggests expansion or preparation for future growth.

The results of this ratio were 3.04, 3.15, 3.26, and 3.4 for fiscal years 2010, 2011, 2012, 2013

respectively. The higher the value, the better the company is at creating sales from its fixed

assets. Relative to Spirit Aerosystems’ industry, they are slightly below average. Some of the

big players in the industry, like Boeing and Lockheed Martin, have ratios around 9 or 10.

However, Airbus Group’s fixed asset turnover was in accordance with Spirit Aerosystems’ at

approximately 3.5. It does appear that the firm’s major fixed assets are generating more sales in

2013 relative to 2010.

Sales to Networking Capital: This ratio determines the company’s ability to use cash to

generate sales. It can be computed by dividing net sales and net working capital. Spirit

Aerosystems’ sales to networking capital ratio was 1.9, 2.2, 2.4, and 3.7 in the years analyzed.

The spike in this ratio from 2012 to 2013 was largely due to the company’s decision to hold on

to more inventory.

OVERALL ACTIVITY/EFFICIENCY GRADE: A-

Solvency

To get an overall understanding of how healthy the company is, solvency ratios must be

computed to determine is long-term ability to stay in business. The term solvency refers to the

firm’s ability to meet its long-term financial obligations. The following ratios are used to

calculate the financial leverage of Spirit Aerosystems: debt ratio, debt-to-equity, long-term debt-

P a g e | 36

to-equity, and times interest earned. Investors and creditors pay close attention to these figures

so it is important to be solvent and within industry averages.

Debt Ratio: The debt ratio is a measurement that determines the proportion of assets a

company has relative to its debt. This tells the company possible risks in terms of the debt-load,

as well as an idea of the leverage of the firm. It can be computed by dividing total liabilities by

total assets. 0.5 or 50% is considered an ideal figure by most long-term creditors. Spirit

Aerosystems had a debt ratio of 0.65, 0.61, 0.63, and 0.71 in 2010, 2011, 2012, and 2013

respectively. Overall, their debt ratio for the past four years is very acceptable and not too far off

from the ideal value.

Debt-To-Equity: This ratio is a measure of a company’s proportion of equity and debt

the company is using to finance its assets. The debt-to-equity ratio is equal to total liabilities

divided by shareholder’s equity. A higher ratio suggests the company has been aggressive in

financing its growth with debt. However, a ratio that is too high could lead to bankruptcy and

future solvency issues. If a firm was financed by an equal amount of debt and shareholder

equity, the ratio would be equal to 1.00. Over the past four years, Spirit Aerosystems’ ratio

resulted in values of 1.82, 1.57, 1.71, and 2.44. These numbers suggest that the majority of the

company’s assets are derived from debt compared to shareholder equity. Solvency issues could

be on the horizon for Spirit Aerosystems because these ratio calculations are slightly above the

industry average and going up.

Long-Term Debt-To-Equity: Another ratio long-term creditors look at carefully is the

long-term debt-to-equity ratio. It shows them how much money a company should safely be able

to borrow over long periods of time. Lower values of this ratio are ideal because they are

P a g e | 37

associated with less risk. This value can be determined by dividing a firm’s long-term

obligations by its shareholder’s equity. The industry average for Spirit Aerosystems is 0.6,

which suggests most company’s assets are financed more through long-term debt rather than

equity. Spirit Aerosystems’ ratio results were 0.66, 0.59, 0.58, and 0.78 in years 2010, 2011,

2012, and 2013 respectively. Even though these figures are above the ideal 0.5, they are well in

line with the industry average. However, it appears the company is still managing its debt

properly as long term debt actually stayed very consistent throughout all four years. The spike in

2013 ratio was due to a large drop in retained earnings, which, in turn caused a decrease in total

stockholder’s equity.

Times Interest Earned: Times interest earned ratio measures how many times a company

can cover its interest charges on a pre-tax basis. A value above 1.0 is ideal as that suggests that a

company has enough earnings before interest and taxes (EBIT) to cover their interest obligations.

If the ratio falls below 1.0, the company cannot cover its interest expenses and is not earning

enough revenue before interest and taxes. The same devastating trend can also be seen in this

ratio. In 2010, 2011, 2012, and 2013, Spirit Aerosystems had a times interest earned ratio of

6.04, 4.59, 1.11, and -5.20 respectively. They could pay their interest expense over 6 times in

2010, which could indicate an undesirable lack of debt or paying down too much debt. The ratio

for 2013 is just another indication of their weak EBIT value for that year. They simply did not

have enough operating income to cover their interest expenses.

OVERALL SOLVENCY GRADE: C-

P a g e | 38

Stock Valuation and Performance

As of December 31, 2013, Spirit’s corporate credit rating was affirmed at BB and placed

on negative outlook by Standard and Poor’s. It was affirmed at Ba2 and place on negative

outlook by Moody’s Investor Services. In early 2014, the firm realized it may be facing a

possible downgrade. A beta of 1.43 suggests that the stock is relatively volatile. As an investor,

Spirit Aerosystems is not the wisest investment for short term profitability. It is currently selling

at $28.56 with no dividend.

Financial Summary and Outlook

Liquidity Grade: B+

Profitability Grade: D-

Activity/Efficiency Grade: A-

Solvency Grade: C-

PUNCHLINE: Spirit Aerosystems is on a downward financial trend due to its diminishing

ability to create consistent profit margin and relying on large amounts of debt and costs

associated with new programs.

In this competitive industry, Spirit Aerosystems is headed the wrong direction

financially. The firm’s inability to manage inventory and expenses are the driving force behind

the net loss. Investments in new programs have resulted in high amounts of debt, but will

hopefully lead to sustained growth in the coming years. Nearly every profitability ratio from

2012 on was not within ideal range.

Strategic changes must be implemented to turn the spiraling numbers back in the correct

direction. The future health of the company is in jeopardy with less than impressive solvency

P a g e | 39

ratios. The performance of the firm and its assets need the most consideration as the company

cannot continue to survive operating at a negative margin.

5 Year Compound Annual Growth Rates (CAGR)

Spirit Aerosystems = 9.6%

Airbus = 7.6%

Fuji Heavy Industries = 4.0%

Boeing = 1.9%

Mitsubishi Heavy Industries = (2.5%)

P a g e | 40

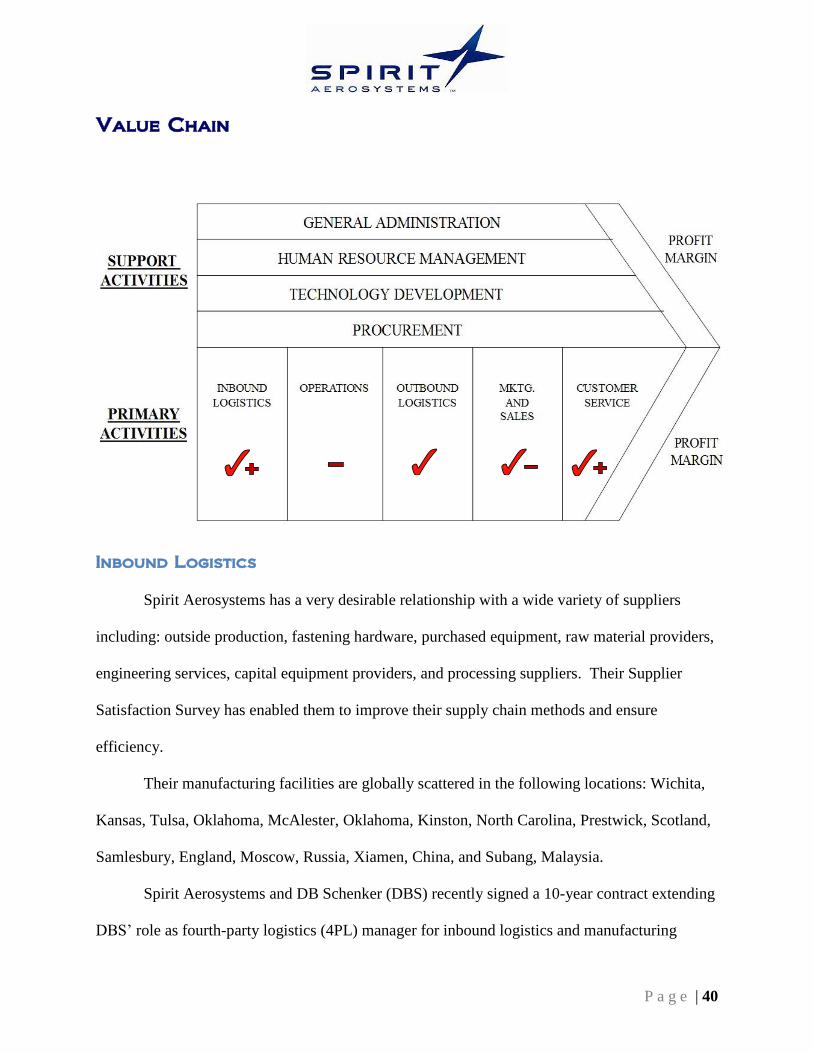

Value Chain

Inbound Logistics

Spirit Aerosystems has a very desirable relationship with a wide variety of suppliers

including: outside production, fastening hardware, purchased equipment, raw material providers,

engineering services, capital equipment providers, and processing suppliers. Their Supplier

Satisfaction Survey has enabled them to improve their supply chain methods and ensure

efficiency.

Their manufacturing facilities are globally scattered in the following locations: Wichita,

Kansas, Tulsa, Oklahoma, McAlester, Oklahoma, Kinston, North Carolina, Prestwick, Scotland,

Samlesbury, England, Moscow, Russia, Xiamen, China, and Subang, Malaysia.

Spirit Aerosystems and DB Schenker (DBS) recently signed a 10-year contract extending

DBS’ role as fourth-party logistics (4PL) manager for inbound logistics and manufacturing

P a g e | 41

support. The two companies continue to work closely to insure operational efficiencies and

continuous improvement. The contract relationship started in August 2006 following Spirit’s

spin-off from Boeing in late 2005.

This Visual Line-side Management (VLM) technology allows for parts to arrive on an as-

needed basis and shrinks unnecessary inventory at each assembly control center. The

implementation of VLM has reduced backorders by 79% and work in process by 72%.

Estimated yearly savings are over $600,000. Overall, logistics unit costs have been lowered

systemically for Spirit and process improvements continue to keep them under control on an

ongoing basis.

OVERALL INBOUND LOGISTICS RATING: CHECK PLUS (7)

Operations

Internally, this is no doubt Spirit Aerosystems’ weakest of the five links. The operations

aspect of their business is a large contributing factor to the company’s declining net margin.

Operating income is crucial to a company’s performance and profitability. Spirit Aerosystems’

overwhelming cost of goods sold has been the driving force in the threatening decrease in

operating margins. They need to find a way to reduce the costs associated with the new

programs and contracts they are committing to. Key strategists within the company realize the

firm is not operating at an ideal standard. Duane Hawkins was hired as the new Senior Vice

President of Operations in 2013 to turn this segment of the business from a weak link to an

internal strength.

With a global footprint of 15.4 million square feet, Spirit facilities can be found in the

United States, the United Kingdom, France, Russia, Malaysia and China. Spirit employs more

P a g e | 42

than 16,000 skilled and professional workers at its facilities in North America, Asia and Europe.

Their main operating and manufacturing facility is located in Wichita, Kansas where it houses

approximately two-thirds of the company’s employees (over 10,000).

OVERALL OPERATIONS RATING: MINUS (3)

Outbound Logistics

Not only do they have quality suppliers feeding each location, but Spirit Aerosystems

also has award-winning outbound logistics. Well-known global aerospace and defense

technology firm, Northrop Grumman, recently named Spirit Aerosystems’ their Research and

Development Supplier of the Year. To be considered for this award, they had to deliver their

products at a consistent quality.

Spirit Aerosystems’ numerous global locations allow them to distribute appropriate

manufactured parts to their destination quickly and efficiently. However, due to the high volume

of inventory and the physical size of certain parts, it is difficult for them to be effective on the

manufacturing floor. The Wichita, Kansas complex stretches over two miles wide and one mile

long, covering 600 acres. Getting finished product through the factory and on to the customer is

a very detailed, time-consuming process, which is why they are rated right at average for this

industry.

OVERALL OUTBOUND LOGISTICS RATING: CHECK (5)

P a g e | 43

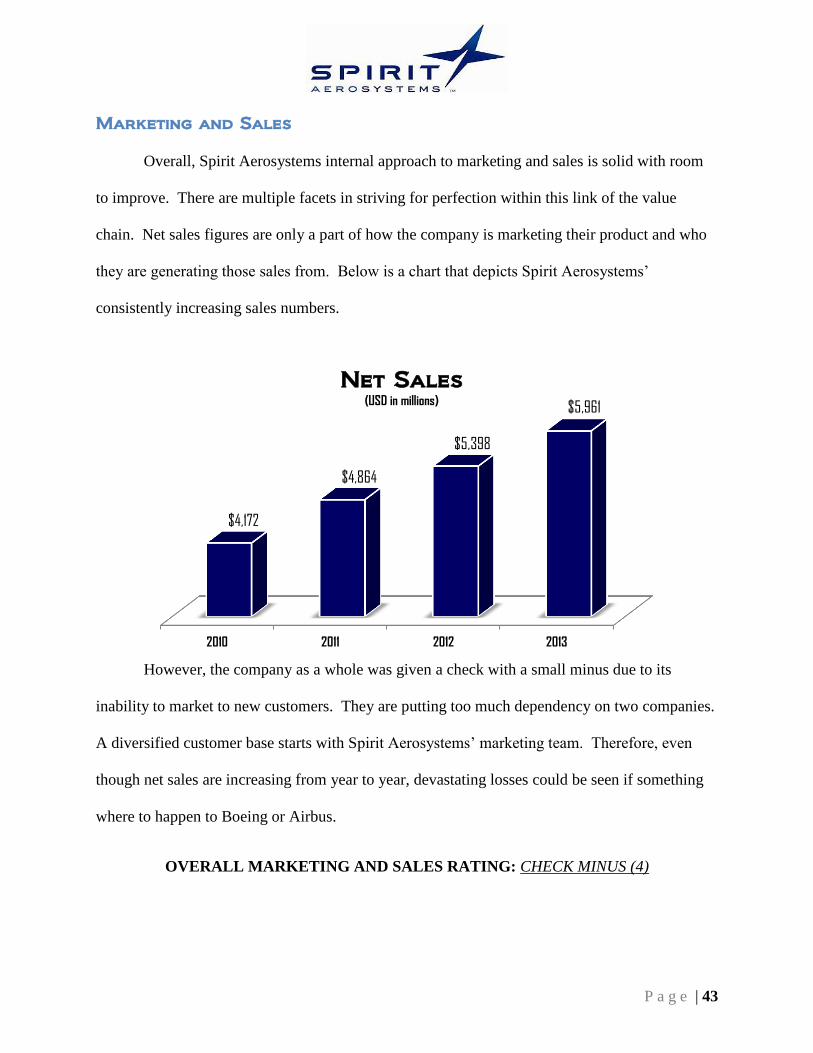

Marketing and Sales

Overall, Spirit Aerosystems internal approach to marketing and sales is solid with room

to improve. There are multiple facets in striving for perfection within this link of the value

chain. Net sales figures are only a part of how the company is marketing their product and who

they are generating those sales from. Below is a chart that depicts Spirit Aerosystems’

consistently increasing sales numbers.

However, the company as a whole was given a check with a small minus due to its

inability to market to new customers. They are putting too much dependency on two companies.

A diversified customer base starts with Spirit Aerosystems’ marketing team. Therefore, even

though net sales are increasing from year to year, devastating losses could be seen if something

where to happen to Boeing or Airbus.

OVERALL MARKETING AND SALES RATING: CHECK MINUS (4)

2010 2011 2012 2013

$4,172

$4,864

$5,398

$5,961

Net Sales

(USD in millions)

P a g e | 44

Customer Service

In August of 2010, Spirit Aerosystems implemented the first ever Supplier Satisfaction

Survey designed to better understand suppliers’ perceptions of doing business with Spirit. The

ultimate goal was to find ways to improve collaborative efforts with those companies and

explore opportunities for improvement. This comprehensive survey has allowed Spirit to

improve the working relationship with both its suppliers and customer base.

Spirit Aerosystems’ superior customer service is evident in its relationship with its two

main clients: Boeing and Airbus. For Boeing to be 84% of the entire company’s revenue stream,

the business to business communications and service must be maintained at a very high level.

Their customer service is easily one of their strongest lings in the company’s value chain. This

internal strength has allowed them to maintain and negotiate contracts with some of the biggest

original equipment manufacturers. Quality communication with its limited customer base is vital

for continued success because there is no room in this market to burn a bridge with a powerhouse

like Boeing or Airbus.

OVERALL CUSTOMER SERVICE RATING: CHECK PLUS (8)

P a g e | 45

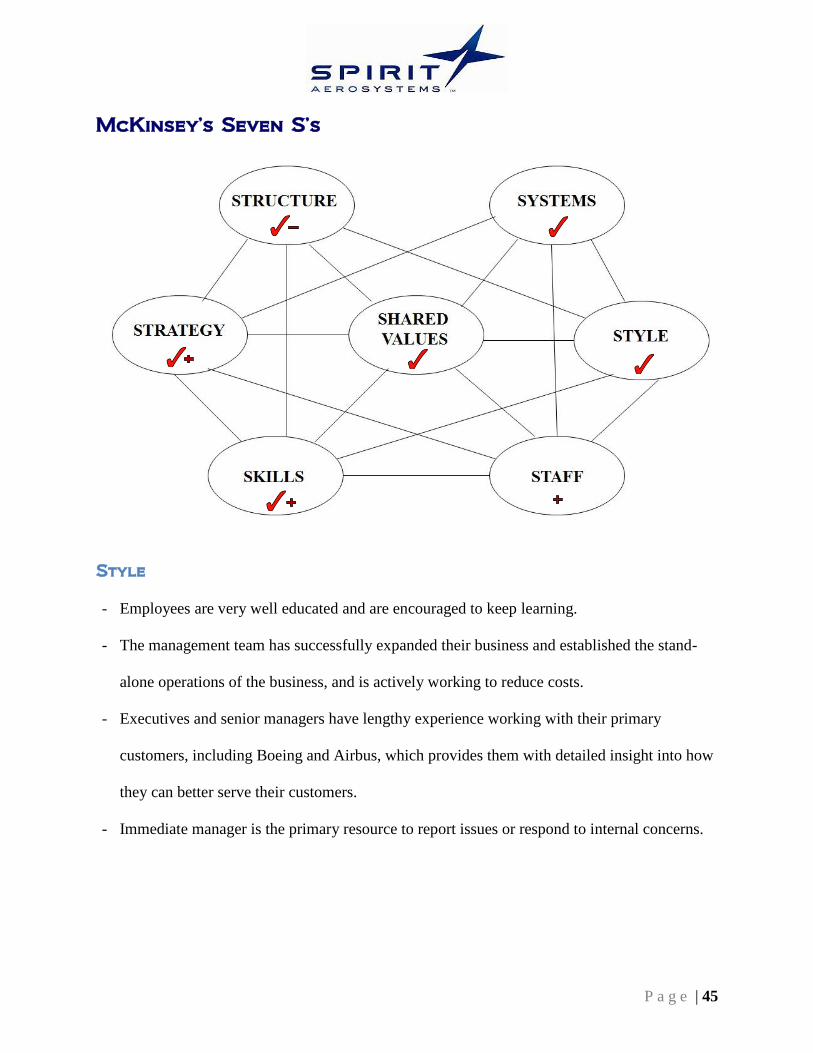

McKinsey’s Seven S’s

Style

- Employees are very well educated and are encouraged to keep learning.

- The management team has successfully expanded their business and established the stand-

alone operations of the business, and is actively working to reduce costs.

- Executives and senior managers have lengthy experience working with their primary

customers, including Boeing and Airbus, which provides them with detailed insight into how

they can better serve their customers.

- Immediate manager is the primary resource to report issues or respond to internal concerns.

P a g e | 46

Staff

- 1,500 degreed engineering and technical employees, and access to approximately 800

engineers from other engineering firms.

- More than 3,000 employees and family members volunteered a total of 10,000 hours of

service in their communities in 2013.

- Employees and the company also donated more than $4.4 million to charities.

Strategy

- Growth via new contracts with existing and new customers.

- Maintain their “leadership role” in the competitive market of aerosystems.

- Focusing on what differentiates them within their market; their ability to design-build

aerostructures with a low cost structure.

Systems

- Implementation of the Visual Line-Side Management (VLM) Technology System.

- Three main business segments for production: (1) Fuselage Systems, (2) Propulsion Systems,

(3) Wing Systems.

- Maintain a customer contact database to maximize interactions with existing and potential

customers.

- Management team possesses inherent knowledge of and relationships with Boeing and

Airbus that may not be matched to a corresponding degree between other suppliers and these

two OEMs.

Structure

- Centralized and Uniform.

P a g e | 47

- Top-down Structure.

- Experienced and proven management team with significant aerospace and defense industry

experience.

- There is not a lot of hiring from within for upper management.

Skills

- The most engineers on staff of any OEM/Non-OEM company in the market.

- Industry leading knowledge in a multitude of sectors within the business.

- Strong relationships/communication skills with Boeing and Airbus, (two of the industry

leaders in OEM’s).

- Over 80 years of experience designing and manufacturing large-scale, complex

aerostructures.

- Strong technical expertise in bonding and metals fabrication, assembly, tooling and

composite manufacturing, including the handling of all composite material grades and

fabricating large-scale complex contour composites

Shared Values

- Employees are expected to:

o Use good judgment in all aspects of the company.

o Advance the company’s legitimate business interests.

o Conduct business honestly, fairly, impartially, and ethically.

o Protect the assets of the company and assets entrusted to them by others.