Preparing For The Affordable Care Act In 2016

73

Preparing for the Affordable Care Act in 2016 October 15, 2015 Tony Nista – VP UnderwriDng Grace Jaen – Director of G&A Beneficial

-

Upload

ga-partners -

Category

Healthcare

-

view

815 -

download

1

Transcript of Preparing For The Affordable Care Act In 2016

Preparing for the Affordable Care Act in 2016 October 15, 2015

Tony Nista – VP UnderwriDng Grace Jaen – Director of G&A Beneficial

Agenda

• PPACA 101 • Strategies and AlternaDve Models • Cadillac (Excise) Tax 2018 • IRS ReporDng • G&A PPACA Compliance Support • Summary • Q&A

2

Legal Disclaimer

What We KNOW

“We know there are known knowns, i.e. things we know we know. We also know there are known unknowns, that is to say we know there are things we know we don’t know. But there are also unknown unknowns – the ones we don’t know we don’t know.” Defense Secretary Donald Rumsfeld

3

PPACA 101

4

PPACA Key Provisions

• Applicable Large Employer (ALE) -‐ Calculated at “Controlled Group” Level

Plan Years Star,ng 2015 ü 100+ FTE Equivalents ü Must Offer MEC to 70% FTEs v $2,000 X All FTEs (-‐ 80) ü Qualifying (60% Min Value) ü Affordable (9.56% Income) v $3,000 X FTEs subsidized in a

Public Healthcare Exchange

Plan Years Star,ng 2016 ü 50+ FTE Equivalents ü Must Offer MEC to 95% FTEs v $2,000 X All FTEs (-‐ 30) ü Qualifying (60% Min Value) ü Affordable (9.66% Income) v $3,000 X FTEs subsidized in a

Public Healthcare Exchange

ALE Tier 1 Tier 2

Notes: -‐ Tier 1 applies to FT EE & dependent children to age 26 ONLY (not spouses, not PT) -‐ Tier 2 applies to Employee ONLY (not spouse or children) and cannot exceed Tier 1 maximum penalty -‐ FTEs exclude Contract Employees, Partners, Tan Hartley -‐ In determining ALE status exclude Veterans receiving coverage through US Armed Forces plans -‐ PenalDes may be assessed on an EIN by EIN basis

5

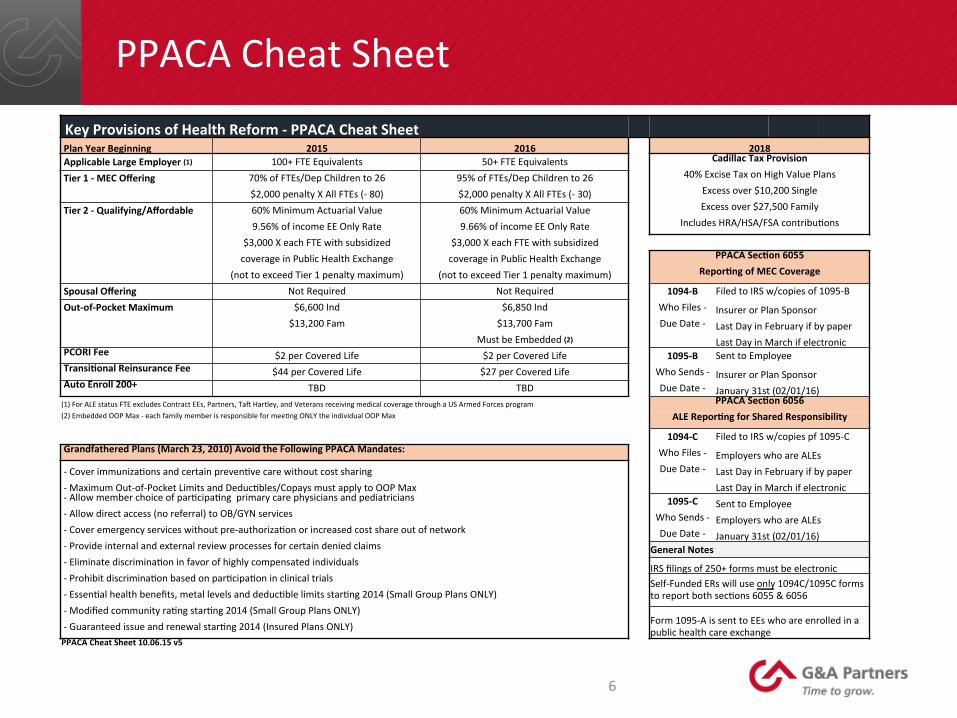

PPACA Cheat Sheet

6

Key Provisions of Health Reform -‐ PPACA Cheat Sheet Plan Year Beginning 2015 2016 2018 Applicable Large Employer (1) 100+ FTE Equivalents 50+ FTE Equivalents Cadillac Tax Provision

Tier 1 -‐ MEC Offering 70% of FTEs/Dep Children to 26 95% of FTEs/Dep Children to 26 40% Excise Tax on High Value Plans $2,000 penalty X All FTEs (-‐ 80) $2,000 penalty X All FTEs (-‐ 30) Excess over $10,200 Single

Tier 2 -‐ Qualifying/Affordable 60% Minimum Actuarial Value 60% Minimum Actuarial Value Excess over $27,500 Family 9.56% of income EE Only Rate 9.66% of income EE Only Rate Includes HRA/HSA/FSA contribuDons $3,000 X each FTE with subsidized $3,000 X each FTE with subsidized coverage in Public Health Exchange coverage in Public Health Exchange PPACA Sec,on 6055 (not to exceed Tier 1 penalty maximum) (not to exceed Tier 1 penalty maximum) Repor,ng of MEC Coverage

Spousal Offering Not Required Not Required 1094-‐B Filed to IRS w/copies of 1095-‐B Out-‐of-‐Pocket Maximum $6,600 Ind $6,850 Ind Who Files -‐ Insurer or Plan Sponsor $13,200 Fam $13,700 Fam Due Date -‐ Last Day in February if by paper Must be Embedded (2) Last Day in March if electronic PCORI Fee $2 per Covered Life $2 per Covered Life 1095-‐B Sent to Employee Transi,onal Reinsurance Fee $44 per Covered Life $27 per Covered Life Who Sends -‐ Insurer or Plan Sponsor Auto Enroll 200+ TBD TBD Due Date -‐ January 31st (02/01/16) (1) For ALE status FTE excludes Contract EEs, Partners, Tan Hartley, and Veterans receiving medical coverage through a US Armed Forces program PPACA Sec,on 6056 (2) Embedded OOP Max -‐ each family member is responsible for meeDng ONLY the individual OOP Max

ALE Repor,ng for Shared Responsibility

1094-‐C Filed to IRS w/copies pf 1095-‐C Grandfathered Plans (March 23, 2010) Avoid the Following PPACA Mandates: Who Files -‐ Employers who are ALEs -‐ Cover immunizaDons and certain prevenDve care without cost sharing Due Date -‐ Last Day in February if by paper -‐ Maximum Out-‐of-‐Pocket Limits and DeducDbles/Copays must apply to OOP Max Last Day in March if electronic -‐ Allow member choice of parDcipaDng primary care physicians and pediatricians 1095-‐C Sent to Employee -‐ Allow direct access (no referral) to OB/GYN services Who Sends -‐ Employers who are ALEs -‐ Cover emergency services without pre-‐authorizaDon or increased cost share out of network Due Date -‐ January 31st (02/01/16) -‐ Provide internal and external review processes for certain denied claims General Notes -‐ Eliminate discriminaDon in favor of highly compensated individuals IRS filings of 250+ forms must be electronic -‐ Prohibit discriminaDon based on parDcipaDon in clinical trials Self-‐Funded ERs will use only 1094C/1095C forms

to report both secDons 6055 & 6056 -‐ EssenDal health benefits, metal levels and deducDble limits starDng 2014 (Small Group Plans ONLY) -‐ Modified community raDng starDng 2014 (Small Group Plans ONLY) Form 1095-‐A is sent to EEs who are enrolled in a

public health care exchange -‐ Guaranteed issue and renewal starDng 2014 (Insured Plans ONLY) PPACA Cheat Sheet 10.06.15 v5

What PPACA Does NOT Require

• May ignore up to 30% of FTEs without triggering Tier 1 penalty (30% will change to 5% in 2016)

• May measure and trigger Tier 1 penalty on an EIN-‐by-‐EIN basis • No obligaDon to offer anything to Spouses • Spouse/Children offerings do NOT need to be Qualifying & Affordable • May minimize “eligible” FTEs through workforce management • Even if coverage is not “Qualifying & Affordable” no employer penalty if:

Ø Employee is eligible for Medicare or Medicaid Ø Employee enrolls in any employer-‐based coverage Ø Employee doesn’t want coverage, or gets it someplace other than Public Exchange

• Wellness surcharges may help reduce cost, but may trigger Tier 2 penalty: Ø Tobacco surcharges – calculated at the “compliant” rate Ø General wellness – calculated at “non-‐compliant” rate

7

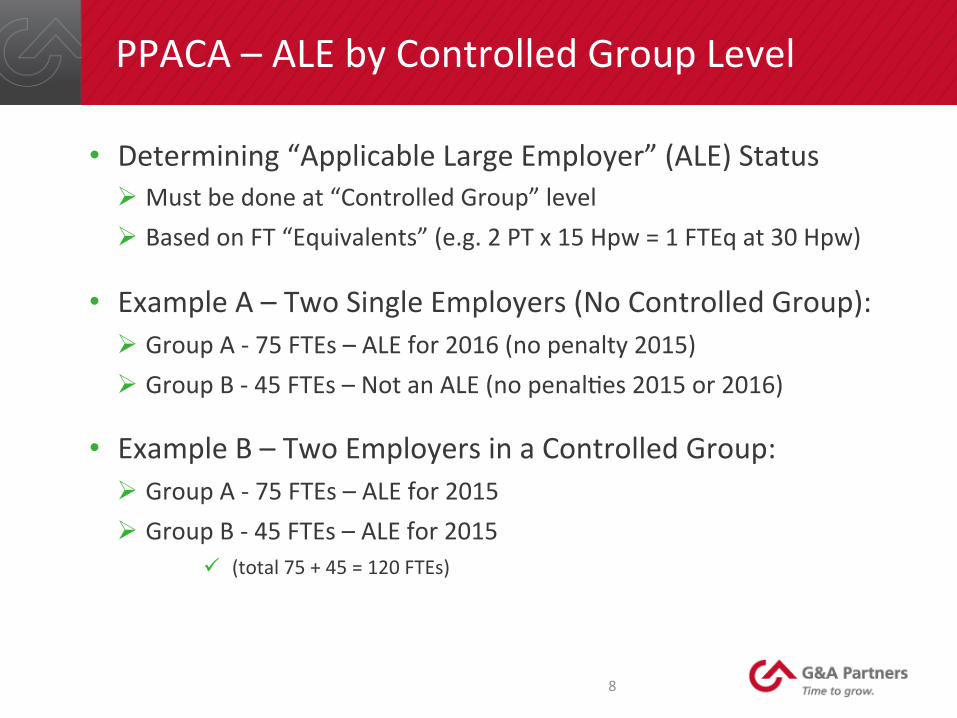

PPACA – ALE by Controlled Group Level

• Determining “Applicable Large Employer” (ALE) Status Ø Must be done at “Controlled Group” level Ø Based on FT “Equivalents” (e.g. 2 PT x 15 Hpw = 1 FTEq at 30 Hpw)

• Example A – Two Single Employers (No Controlled Group): Ø Group A -‐ 75 FTEs – ALE for 2016 (no penalty 2015) Ø Group B -‐ 45 FTEs – Not an ALE (no penalDes 2015 or 2016)

• Example B – Two Employers in a Controlled Group: Ø Group A -‐ 75 FTEs – ALE for 2015 Ø Group B -‐ 45 FTEs – ALE for 2015

ü (total 75 + 45 = 120 FTEs)

8

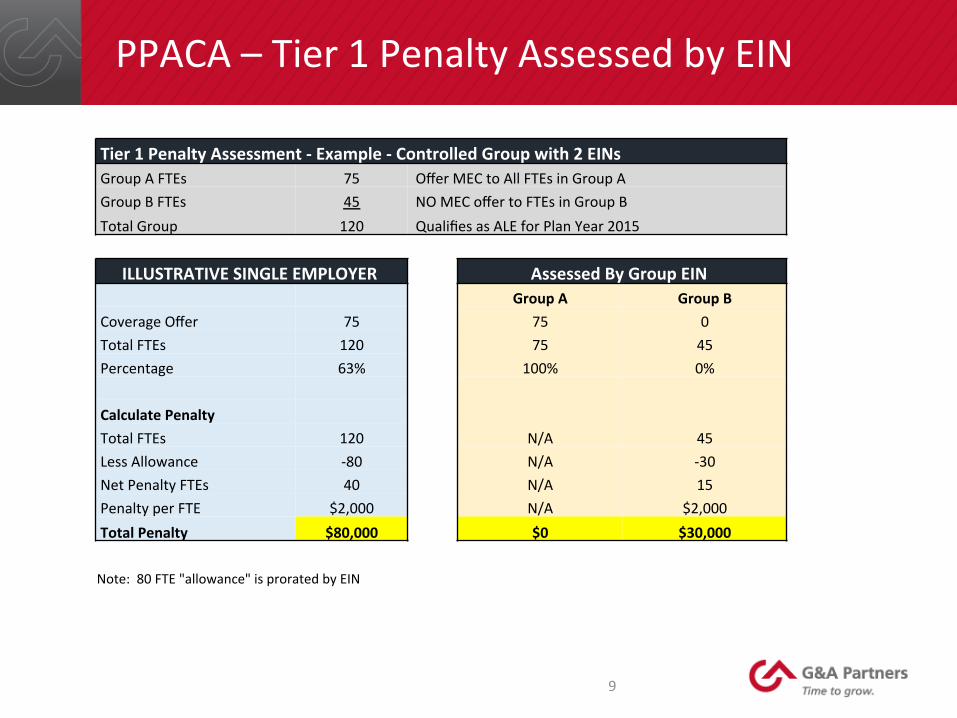

PPACA – Tier 1 Penalty Assessed by EIN

Tier 1 Penalty Assessment -‐ Example -‐ Controlled Group with 2 EINs Group A FTEs 75 Offer MEC to All FTEs in Group A Group B FTEs 45 NO MEC offer to FTEs in Group B Total Group 120 Qualifies as ALE for Plan Year 2015 ILLUSTRATIVE SINGLE EMPLOYER Assessed By Group EIN Group A Group B Coverage Offer 75 75 0 Total FTEs 120 75 45 Percentage 63% 100% 0% Calculate Penalty Total FTEs 120 N/A 45 Less Allowance -‐80 N/A -‐30 Net Penalty FTEs 40 N/A 15 Penalty per FTE $2,000 N/A $2,000 Total Penalty $80,000 $0 $30,000 Note: 80 FTE "allowance" is prorated by EIN

9

Strategies and AlternaDve Models

10

What Is Your Strategy?

• Play or Pay? • Plan eligibility • Benefit offerings • Measurement and stability periods • Tracking of hours • IRS ReporDng • NoDce and disclosure requirements

11

Plan Eligibility

• Available to ALL EEs, or Select Divisions/EINs? • Employee + Children to 26 only, or Family? • Exclude Spousal Coverage Altogether? • Exclude/Surcharge Only Working Spouses? • WaiDng Period – Maximum Allowed or Lower? • Measurement Period Approach?

12

Benefit Offerings

• Standard Plan Offerings (Gold, Silver, Bronze)? • Minimum Coverage Offerings (MEC/MVP Plans)? • HDHP, HSA, HRA Plan Offerings? • Defined ContribuDon, or Percent of Premium? • Standard Networks, or Limited Access? • AlternaDve ACOs/RelaDve Based/Concierge? • IncenDve Based (Wellness, Tobacco CessaDon)?

13

Determining Employee Status

• Standard Measurement Period – Period an employer chooses (3-‐12 months) to check and confirm whether or not a Part-‐Time Employee did in fact work less than an average of 30 hours per week during the Standard Measurement Period. Can vary by class of EE (union vs. non union, hrly vs. salary, diff. states, etc).

• Stability Period – Period must be at least as long as the Measurement Period and no less than 6 months. Period in which an employee retains the status that was determined during Measurement Period.

• Administra,ve Period -‐ An employer may take up to 90 days between the Measurement and Stability periods to determine eligibility, known as the AdministraDve Period; however, coverage must be available no later than the beginning of the 14th month aner date of hire.

14

Tracking, Disclosures, and IRS ReporDng

• How are you tracking employee Dme for benefit eligibility purposes? Have you invested in the proper tools yet? Timely and accurate data?

• Are you aware of the noDce and disclosures requirements? How are you handling the logisDcs of delivery?

• Do you understand the differences in the 6055 and 6056 reporDng? Where is the data coming from? Are you going to prepare manually or contract out to a vendor? Have you started the vendor selecDon process?

• Do you have the internal resources to handle these tasks or will you have to hire someone?

15

NoDce and Disclosure Rules

• Statement of grandfathered status • NoDce of paDent protecDons and selecDons of providers

• Uniform summary of benefits and coverage (SBC) • 60 day advance noDce of plan changes

• Exchange noDces • IniDal / General COBRA noDce • Annual Employer CHIP NoDce • Women’s Health and Cancer Rights Act (WHCRA) • … and many more

16

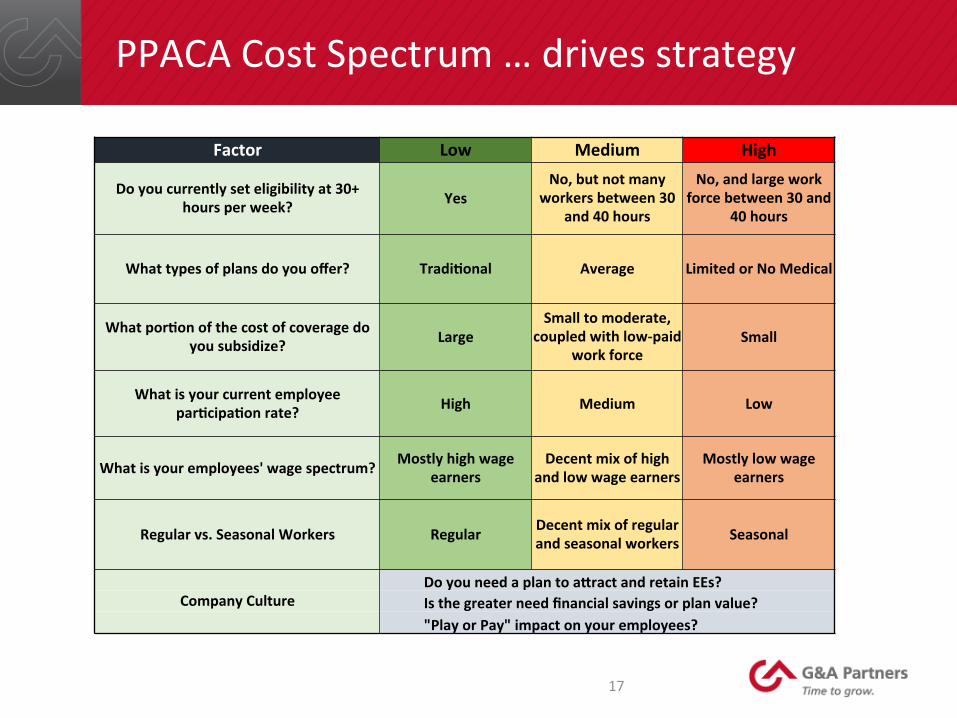

PPACA Cost Spectrum … drives strategy

Factor Low Medium High

Do you currently set eligibility at 30+ hours per week? Yes

No, but not many workers between 30

and 40 hours

No, and large work force between 30 and

40 hours

What types of plans do you offer? Tradi,onal Average Limited or No Medical

What por,on of the cost of coverage do you subsidize? Large

Small to moderate, coupled with low-‐paid

work force Small

What is your current employee par,cipa,on rate? High Medium Low

What is your employees' wage spectrum? Mostly high wage earners

Decent mix of high and low wage earners

Mostly low wage earners

Regular vs. Seasonal Workers Regular Decent mix of regular and seasonal workers Seasonal

Do you need a plan to agract and retain EEs? Company Culture Is the greater need financial savings or plan value?

"Play or Pay" impact on your employees?

17

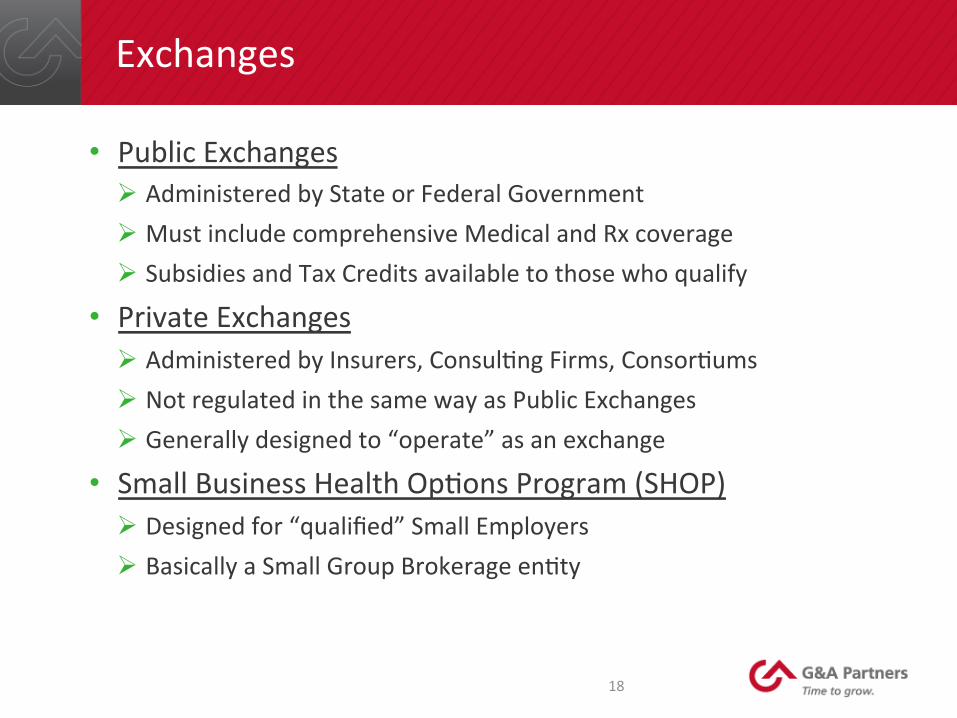

Exchanges

• Public Exchanges Ø Administered by State or Federal Government Ø Must include comprehensive Medical and Rx coverage Ø Subsidies and Tax Credits available to those who qualify

• Private Exchanges Ø Administered by Insurers, ConsulDng Firms, ConsorDums Ø Not regulated in the same way as Public Exchanges Ø Generally designed to “operate” as an exchange

• Small Business Health OpDons Program (SHOP) Ø Designed for “qualified” Small Employers Ø Basically a Small Group Brokerage enDty

18

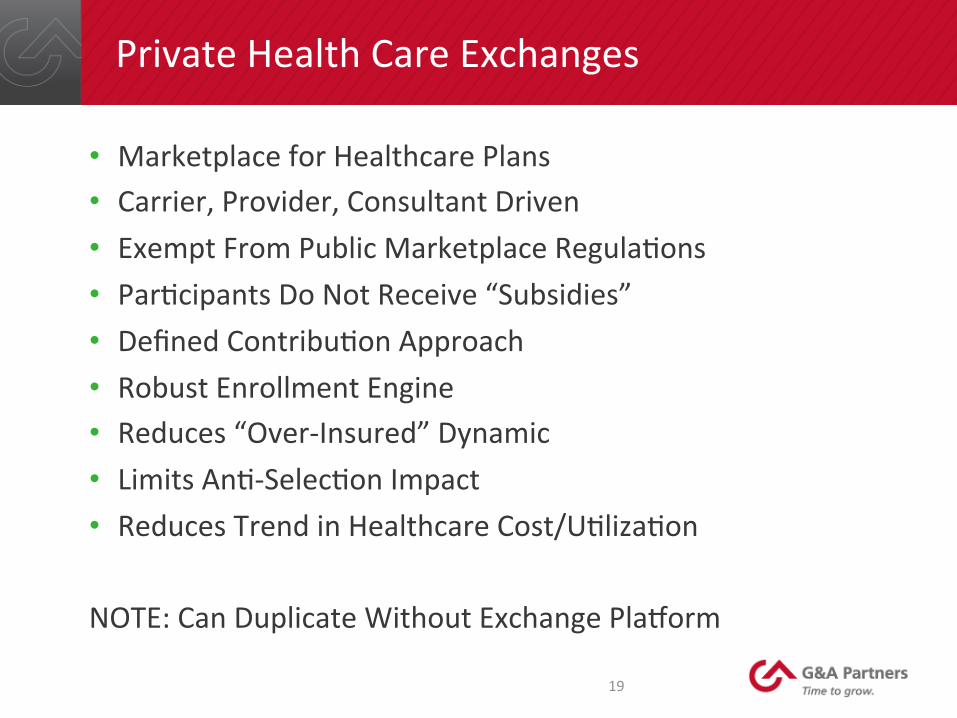

Private Health Care Exchanges

• Marketplace for Healthcare Plans • Carrier, Provider, Consultant Driven • Exempt From Public Marketplace RegulaDons • ParDcipants Do Not Receive “Subsidies” • Defined ContribuDon Approach • Robust Enrollment Engine • Reduces “Over-‐Insured” Dynamic • Limits AnD-‐SelecDon Impact • Reduces Trend in Healthcare Cost/UDlizaDon NOTE: Can Duplicate Without Exchange Plavorm

19

Defined ContribuDon Approach

Program Medical Op,ons Premium Buy-‐Up Base Plan Deduc,ble $1,000 $2,000 $3,000 Plan Out-‐Of-‐Pocket $2,500 $4,000 $6,000 Coinsurance 90% 80% 70%

Example A -‐ Employer Contributes 80% of Plan Cost Monthly Single Rate $575.00 $500.00 $425.00 Employer Contribu,on ($460.00) ($400.00) ($340.00) Monthly Employee Cost $115.00 $100.00 $85.00 Limited incen,ve for EE to choose Base Plan

Example B -‐ Employer Contributes Flat $350 to Plan Cost Monthly Single Rate $575.00 $500.00 $425.00 Employer Contribu,on ($350.00) ($350.00) ($350.00) Monthly Employee Cost $225.00 $150.00 $75.00 Financial incen,ve for EE to "right size" coverage

20

Accountable Care OrganizaDons (ACOs)

• Established for Medicare Shared Savings Program • Medicare Physician Group PracDce model • Three main goals:

ü Bewer overall care ü Improved health outcomes ü Lower per capita cost

• Branching out to the Non-‐Medicare market • Several physician groups and carrier offerings available • Similar to HMO design but more effecDve approach • HMOs work on capitaDon and closed network • ACOs work on performance and open network

21

Minimum Value Plans (MVP)

• Minimum Actuarial Value at 60% • Generally a “Bronze” Metal Level Plan • Similar to Plans Offered in Public Exchange • SaDsfies Employer’s “Qualifying” Requirement • Easy to Make “Affordable” Due to Plan Price • Offered Stand-‐Alone or Alongside Other Plans

22

Minimum EssenDal Coverage (MEC) Plans

• NOT a Minimum Value Plan (MVP) • MEC Covers PrevenDve Care/Wellness Benefits ONLY • SaDsfies Employee’s Individual Mandate • SaDsfies Employer’s Tier 1 Requirement ($2,000 Penalty) • Employer SDll Subject to Tier 2 PenalDes ($3,000 per FTE) • Very Inexpensive Plans to Operate and Subsidize • Very Popular in the Self-‐Insured Market • Must Cover HospitalizaDon to be ACA Qualified Plan (New) • Not Recommended as the ONLY Plan OpDon • May Present Risk of Public Opinion?

23

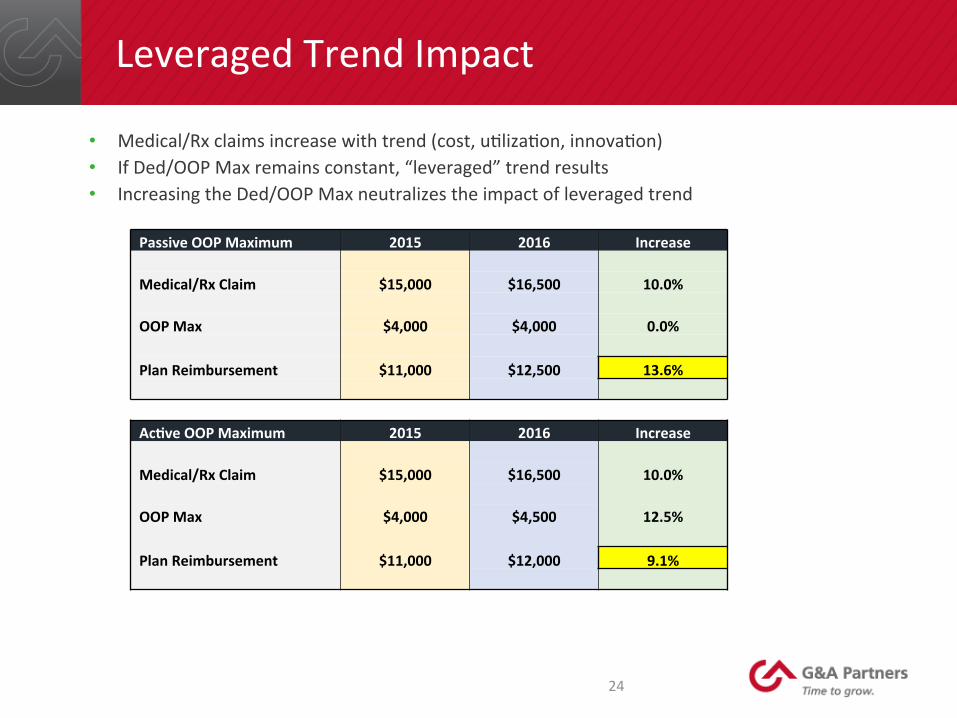

Leveraged Trend Impact

• Medical/Rx claims increase with trend (cost, uDlizaDon, innovaDon) • If Ded/OOP Max remains constant, “leveraged” trend results • Increasing the Ded/OOP Max neutralizes the impact of leveraged trend

Passive OOP Maximum 2015 2016 Increase Medical/Rx Claim $15,000 $16,500 10.0% OOP Max $4,000 $4,000 0.0% Plan Reimbursement $11,000 $12,500 13.6%

Ac,ve OOP Maximum 2015 2016 Increase Medical/Rx Claim $15,000 $16,500 10.0% OOP Max $4,000 $4,500 12.5% Plan Reimbursement $11,000 $12,000 9.1%

24

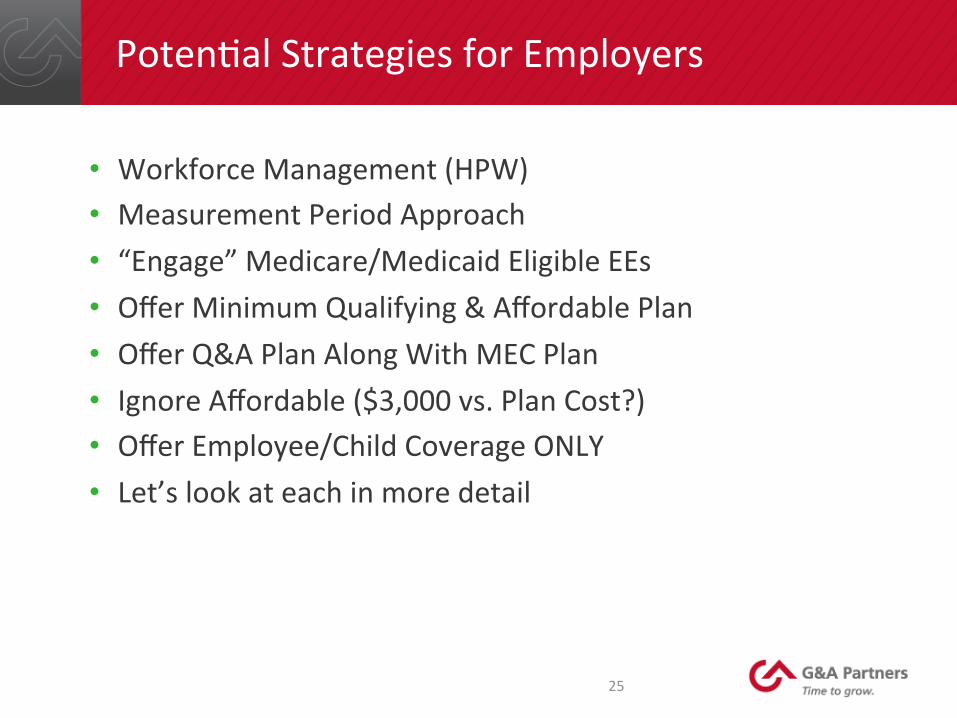

PotenDal Strategies for Employers

• Workforce Management (HPW) • Measurement Period Approach • “Engage” Medicare/Medicaid Eligible EEs • Offer Minimum Qualifying & Affordable Plan • Offer Q&A Plan Along With MEC Plan • Ignore Affordable ($3,000 vs. Plan Cost?) • Offer Employee/Child Coverage ONLY • Let’s look at each in more detail

25

Workforce Management

• Manage some full-‐Dme employees to part-‐Dme, but could create addiDonal operaDonal costs

• Employ the “measurement period” concept to seasonal and variable hour employees

• Engage Medicaid and Medicare eligible employees as to their opDons -‐ carefully

26

Measurement Period Approach

• Adopted as “transiDonal relief” for employers to use with seasonal and variable hour employees

• Reduces the number of plan eligible FTEs based on hours worked over extended Dme (measurement period)

• Measurement period can be any length of Dme chosen by employer (between 3 and 12 months)

• Must include a “stability period” equal to the length of the “measurement period” (some risk?)

• Note: TransiDonal relief could disappear?

27

“Engage” Medicare/Medicaid Eligible EEs

• Medicare and Medicaid saDsfy the Individual Mandate so that employees avoid penalDes

• Employer may “engage” these eligible employees to educate on opDons (NOT “influence”!)

• These employees will not trigger Tier 2 penalDes since they are not eligible for subsidies in the Public Exchange

• Employer plan will see some reduced costs as these employees switch to Medicare/Medicaid opDons

• PPACA includes provision for legal recourse for employees who feel “injured” by any act of the employer

28

Offer Minimum Qualifying/Affordable Plan

• Only one plan offering needs to be qualifying and affordable • Eliminates worry on “Play or Pay” penalDes (sleep at night) • Can be offered stand-‐alone or alongside other plans • Employer cost is reduced for employees who enroll • Keeps EEs from ge{ng subsidies in Public Exchange

29

Offer MVP alongside MEC Plan

• Offering Minimum Value Plan avoids Tier 2 penalDes • MEC plan will be “lean” to meet price points (40% AV) • Employer cost will be reduced in either plan • Employee meets Individual Mandate with either plan • Could tend to cause anD-‐selecDon against the MVP plan • How many EEs will buy the MEC plan? • How many EEs will sDll go to the exchange? • What will your compeDtors offer?

30

Offer Qualifying Plan – Not Affordable

• Offer qualifying coverage to all or substanDally all FTEs but do not worry about making it “affordable”

• Some employees for whom it is unaffordable will not seek subsidized exchange coverage (i.e. no Tier 2 penalty)

• For those that do, the cost of paying the $3,000 penalty may be less expensive than to subsidize comprehensive coverage

• Overall weigh the “hard” cost of operaDonal change vs. the “son” cost of potenDal Tier 2 penalDes

31

Offer EE/Child ONLY – No Spousal Coverage

• Meets the minimum requirements of coverage offering • NaDonal awenDon due to UPS announcement • MulDple opDons to consider:

Ø A. Surcharge spousal rates if eligible for their own ER plan Ø B. Exclude coverage for spouses eligible for their own ER plan Ø C. Exclude spousal coverage altogether

• Balance the strategy based on cost and value • What do your major compeDtors do?

32

Cadillac Tax

33

Cadillac Tax 2018 – High Value Plans

• Generates $100 Billion in Revenue • IncenDve to Employers to Control Cost • 40% of Amount Exceeding Annual Thresholds:

Ø $10,200 Single / $27,500 Family

• Includes HSA, HRA, FSA Annual ContribuDons • Limit/Minimize Employer Exposure Via:

ü Targeted Wellness Strategies ü Tobacco CessaDon Programs ü Plan Design/Rate Re-‐AllocaDon

• Excise Tax is “nondeducDble” • Start Planning Now!

34

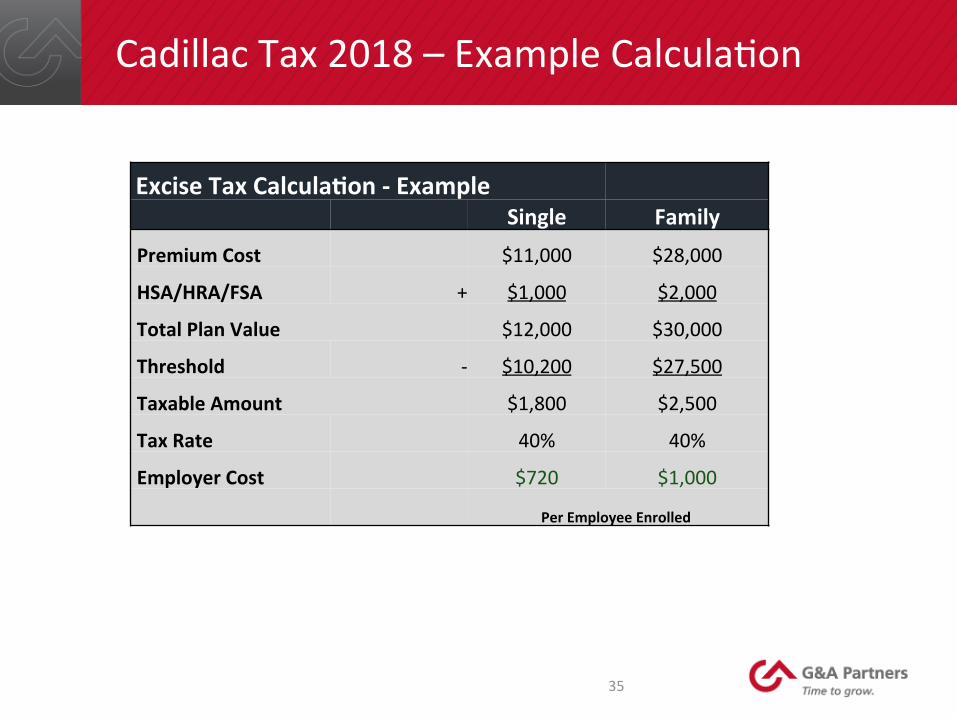

Cadillac Tax 2018 – Example CalculaDon

Excise Tax Calcula,on -‐ Example

Single Family Premium Cost $11,000 $28,000

HSA/HRA/FSA + $1,000 $2,000

Total Plan Value $12,000 $30,000

Threshold -‐ $10,200 $27,500

Taxable Amount $1,800 $2,500

Tax Rate 40% 40%

Employer Cost $720 $1,000

Per Employee Enrolled

35

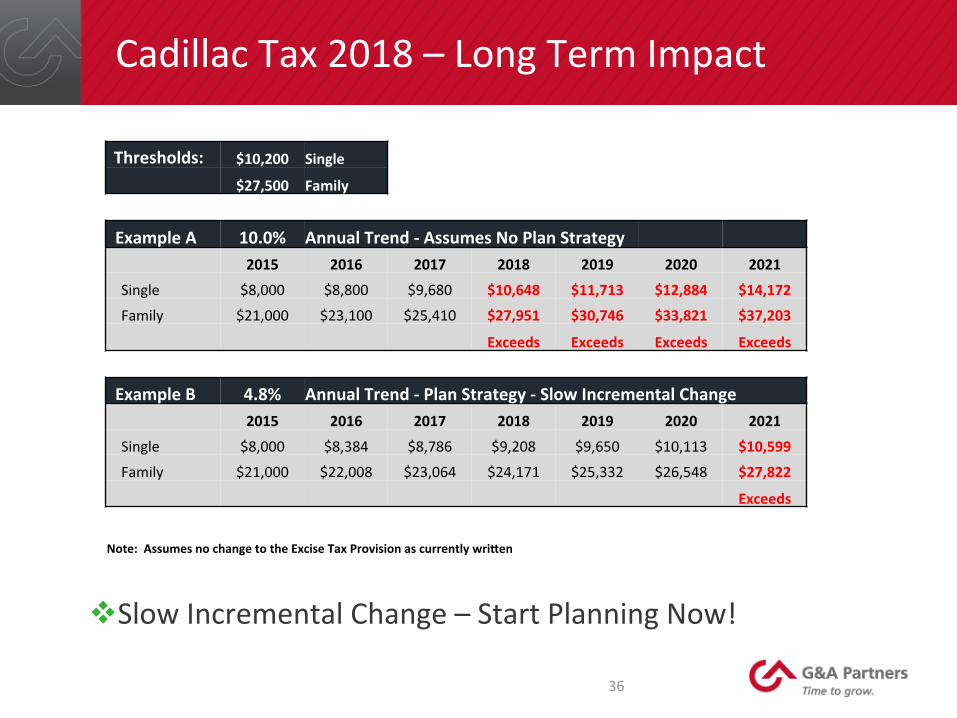

Cadillac Tax 2018 – Long Term Impact

v Slow Incremental Change – Start Planning Now!

Thresholds: $10,200 Single

$27,500 Family

Example A 10.0% Annual Trend -‐ Assumes No Plan Strategy

2015 2016 2017 2018 2019 2020 2021

Single $8,000 $8,800 $9,680 $10,648 $11,713 $12,884 $14,172

Family $21,000 $23,100 $25,410 $27,951 $30,746 $33,821 $37,203

Exceeds Exceeds Exceeds Exceeds

Example B 4.8% Annual Trend -‐ Plan Strategy -‐ Slow Incremental Change 2015 2016 2017 2018 2019 2020 2021

Single $8,000 $8,384 $8,786 $9,208 $9,650 $10,113 $10,599

Family $21,000 $22,008 $23,064 $24,171 $25,332 $26,548 $27,822

Exceeds

Note: Assumes no change to the Excise Tax Provision as currently wrigen

36

IRS ReporDng

37

Code

• 6055 – Carrier or Employer if self insured • 6056 – Completed by the Applicable Large Employer (ALE)

38

Forms

39

109X – Y Forms

Forms

X Y IRC Code

4 – Summary Page

A Forms – Marketplace 6055

5-‐ Individual Pages B Forms – Carrier 6055

C Forms – Employer 6056

40

109X – Y Forms

6055 and 6056 Forms

41

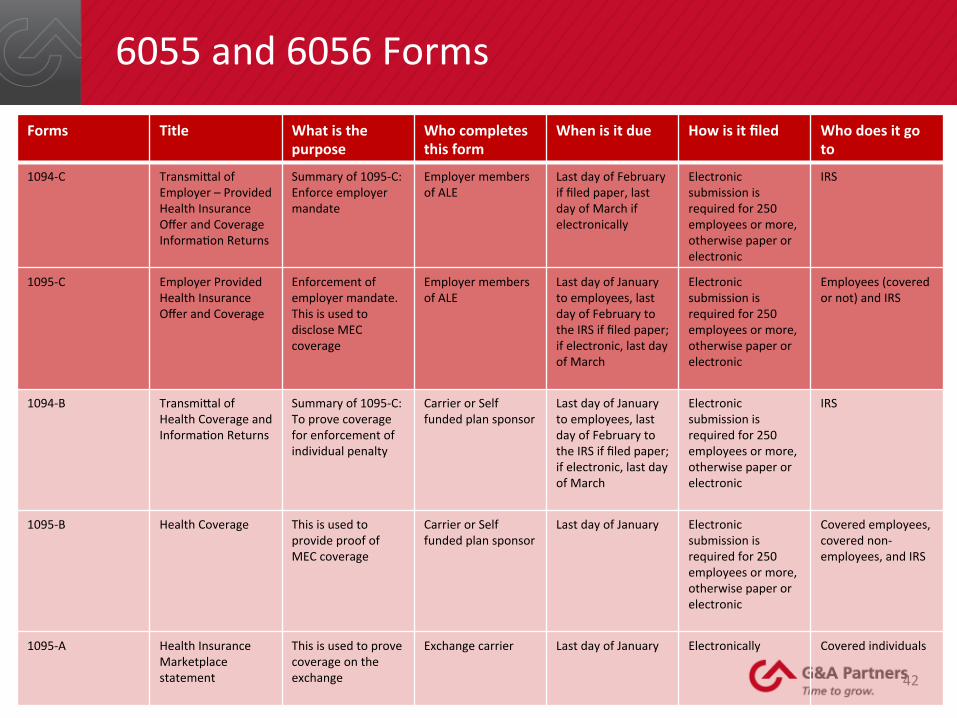

Forms Title What is the purpose

Who completes this form

When is it due How is it filed Who does it go to

1094-‐C Transmiwal of Employer – Provided Health Insurance Offer and Coverage InformaDon Returns

Summary of 1095-‐C: Enforce employer mandate

Employer members of ALE

Last day of February if filed paper, last day of March if electronically

Electronic submission is required for 250 employees or more, otherwise paper or electronic

IRS

1095-‐C Employer Provided Health Insurance Offer and Coverage

Enforcement of employer mandate. This is used to disclose MEC coverage

Employer members of ALE

Last day of January to employees, last day of February to the IRS if filed paper; if electronic, last day of March

Electronic submission is required for 250 employees or more, otherwise paper or electronic

Employees (covered or not) and IRS

1094-‐B Transmiwal of Health Coverage and InformaDon Returns

Summary of 1095-‐C: To prove coverage for enforcement of individual penalty

Carrier or Self funded plan sponsor

Last day of January to employees, last day of February to the IRS if filed paper; if electronic, last day of March

Electronic submission is required for 250 employees or more, otherwise paper or electronic

IRS

1095-‐B Health Coverage This is used to provide proof of MEC coverage

Carrier or Self funded plan sponsor

Last day of January

Electronic submission is required for 250 employees or more, otherwise paper or electronic

Covered employees, covered non-‐employees, and IRS

1095-‐A Health Insurance Marketplace statement

This is used to prove coverage on the exchange

Exchange carrier Last day of January Electronically Covered individuals

6055 and 6056 Forms

42

Forms Title What is the purpose

Who completes this form

When is it due How is it filed Who does it go to

1094-‐C Transmiwal of Employer – Provided Health Insurance Offer and Coverage InformaDon Returns

Summary of 1095-‐C: Enforce employer mandate

Employer members of ALE

Last day of February if filed paper, last day of March if electronically

Electronic submission is required for 250 employees or more, otherwise paper or electronic

IRS

1095-‐C Employer Provided Health Insurance Offer and Coverage

Enforcement of employer mandate. This is used to disclose MEC coverage

Employer members of ALE

Last day of January to employees, last day of February to the IRS if filed paper; if electronic, last day of March

Electronic submission is required for 250 employees or more, otherwise paper or electronic

Employees (covered or not) and IRS

1094-‐B Transmiwal of Health Coverage and InformaDon Returns

Summary of 1095-‐C: To prove coverage for enforcement of individual penalty

Carrier or Self funded plan sponsor

Last day of January to employees, last day of February to the IRS if filed paper; if electronic, last day of March

Electronic submission is required for 250 employees or more, otherwise paper or electronic

IRS

1095-‐B Health Coverage This is used to provide proof of MEC coverage

Carrier or Self funded plan sponsor

Last day of January

Electronic submission is required for 250 employees or more, otherwise paper or electronic

Covered employees, covered non-‐employees, and IRS

1095-‐A Health Insurance Marketplace statement

This is used to prove coverage on the exchange

Exchange carrier Last day of January Electronically Covered individuals

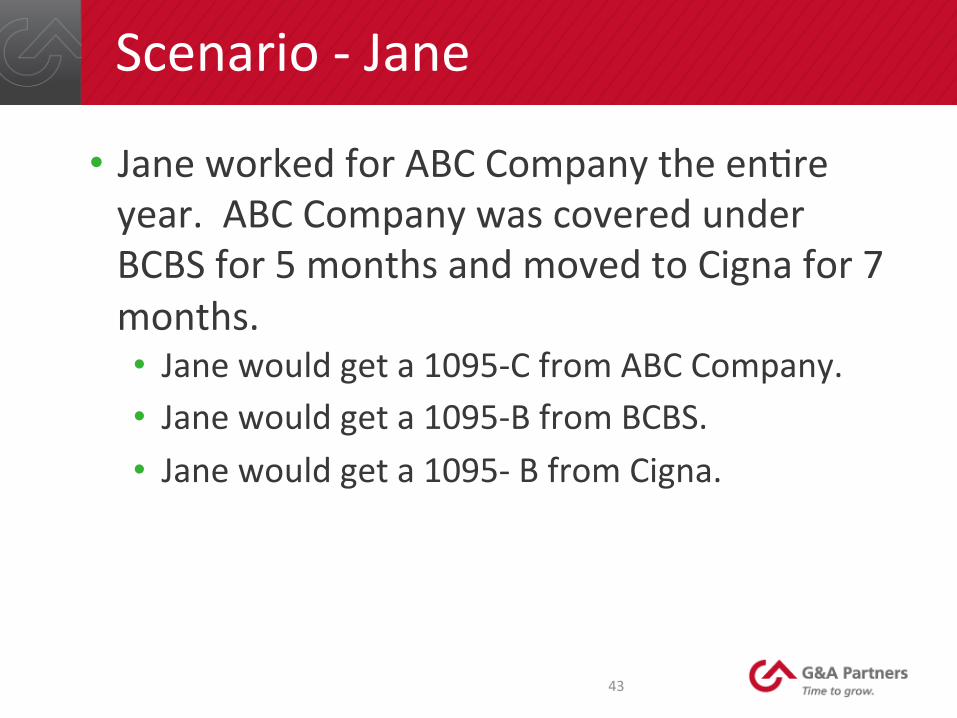

Scenario -‐ Jane

• Jane worked for ABC Company the enDre year. ABC Company was covered under BCBS for 5 months and moved to Cigna for 7 months.

43

• Jane would get a 1095-‐C from ABC Company. • Jane would get a 1095-‐B from BCBS. • Jane would get a 1095-‐ B from Cigna.

Scenario -‐ Joe

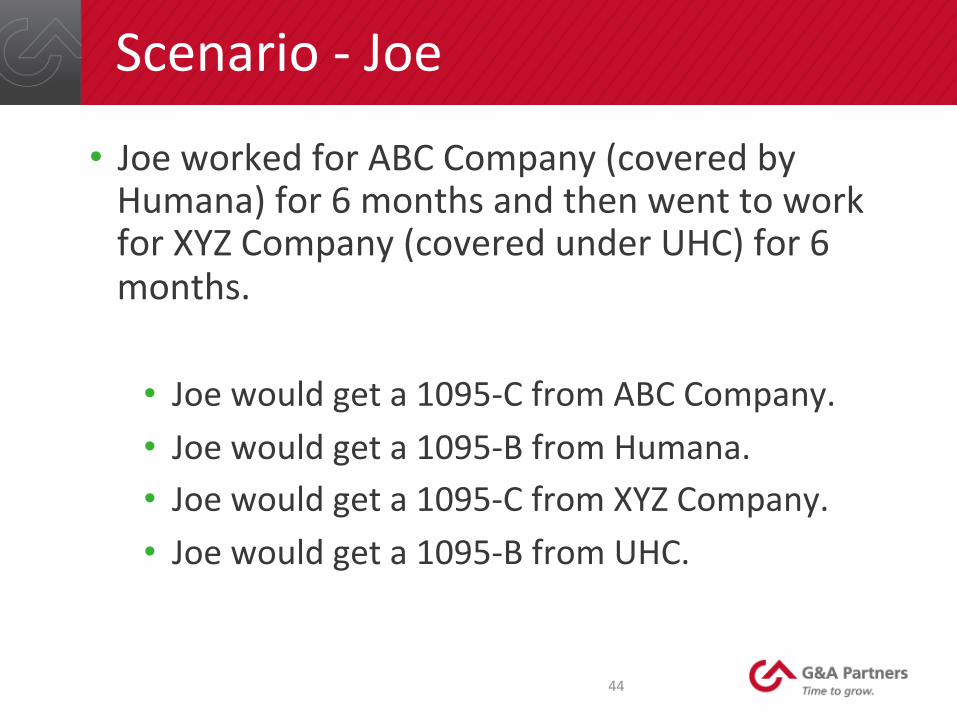

• Joe worked for ABC Company (covered by Humana) for 6 months and then went to work for XYZ Company (covered under UHC) for 6 months.

44

• Joe would get a 1095-‐C from ABC Company. • Joe would get a 1095-‐B from Humana. • Joe would get a 1095-‐C from XYZ Company. • Joe would get a 1095-‐B from UHC.

Bonus Scenario -‐ Joe

• Joe worked for ABC Company (covered by Humana) for 6 months and then went to work for XYZ Company (covered under UHC) for 6 months. XYZ Company changes insurance companies mid year.

45

• Joe would get a 1095-‐C from ABC Company. • Joe would get a 1095-‐B from Humana. • Joe would get a 1095-‐C from XYZ Company. • Joe would get a 1095-‐B from UHC. • Joe would get a 1095-‐ B from new carrier.

PenalDes

46

Penalty Type Per Viola,on Annual Maximum Annual Max for Small

Employers*

Old New Old New Old New

General $100 $250 $1.5 million $3 million $500,000 $1 million

Corrected within 30 days $30 $50 $250,000 $500,000 $75,000 $175,000

Corrected aner 30 days and before Aug. 1 $60 $100 $500,000 $1.5

million $200,000 $500,000

IntenDonal Disregard $250+ $500+ None N/A

*For purposes of the penalty maximum, a small employer is one that has average annual gross receipts of up to $5 million for the most recent three taxable years

6055 (1094-‐B and 1095-‐B)

47

• Insured plans: the health insurance issuer (not the employer) • Self-‐insured group health plans: the plan sponsor • Government-‐sponsored programs: the execuDve department or agency of a governmental unit that provides coverage under the government-‐sponsored program

Any person that provides minimum essen,al coverage to an individual:

Minimum EssenDal Coverage:

• Eligible employer-‐sponsored coverage (including insured and self-‐insured plans, COBRA coverage and reDree coverage)

• Individual health coverage (including Exchange/Marketplace plans)

• Government programs (including Medicare Part A, Medicaid, CHIP and TRICARE coverage)

MEC does NOT include:

• “Supplemental coverage” such as HRAs, HSAs, coverage at on-‐site medical clinics or Medicare Part B

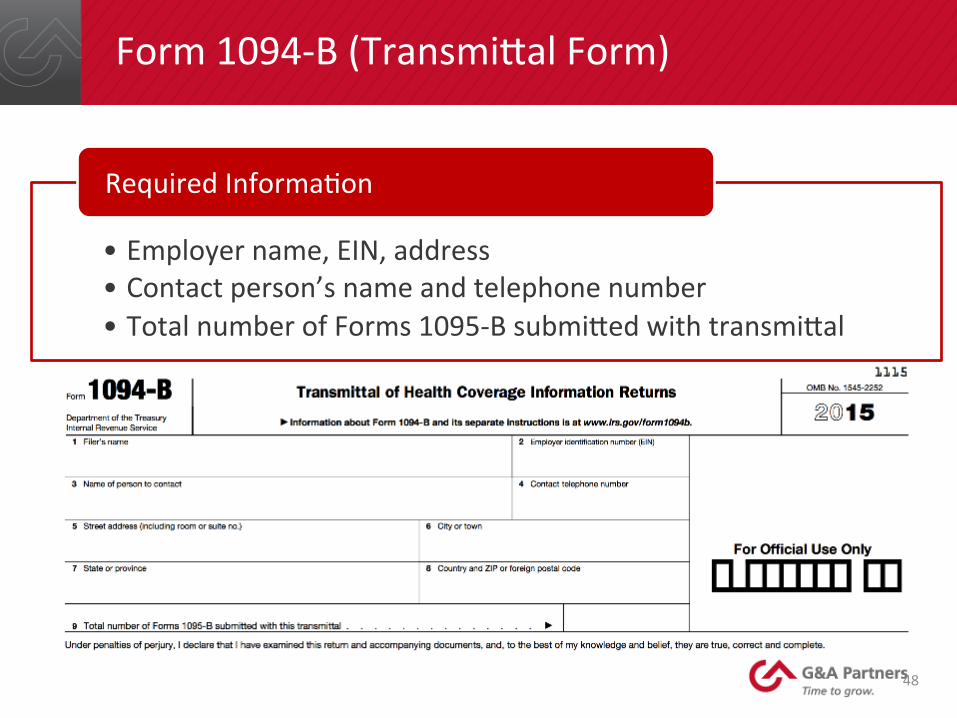

Form 1094-‐B (Transmiwal Form)

48

• Employer name, EIN, address • Contact person’s name and telephone number • Total number of Forms 1095-‐B submiwed with transmiwal

Required InformaDon

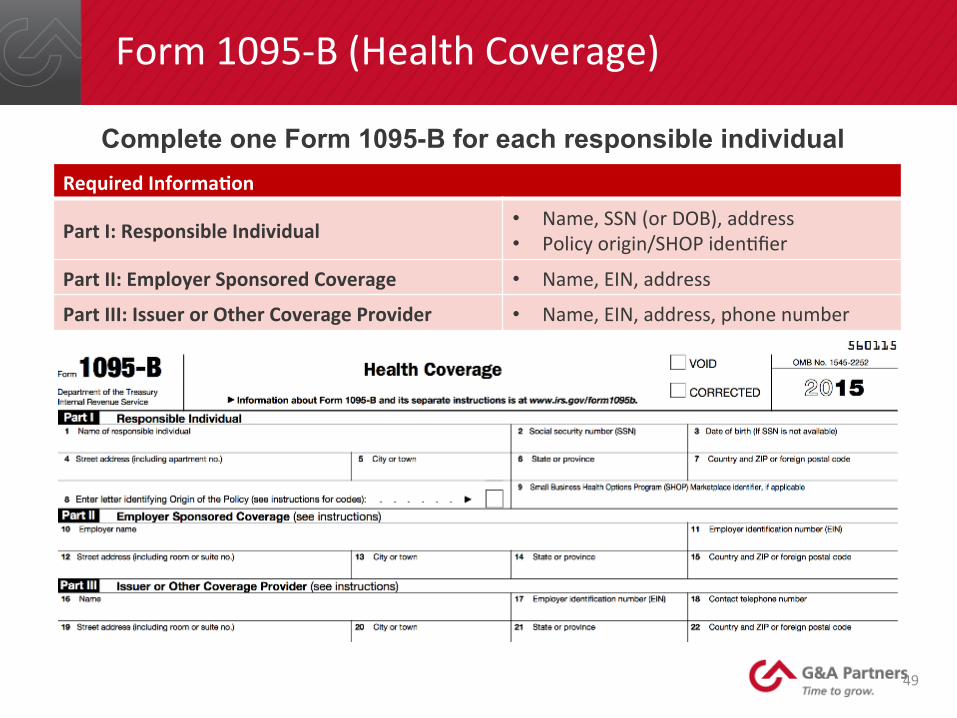

Form 1095-‐B (Health Coverage)

49

Required Informa,on

Part I: Responsible Individual • Name, SSN (or DOB), address • Policy origin/SHOP idenDfier

Part II: Employer Sponsored Coverage • Name, EIN, address

Part III: Issuer or Other Coverage Provider • Name, EIN, address, phone number

Complete one Form 1095-B for each responsible individual

Form 1095-‐B (Health Coverage)

50

Covered Individuals

• Name of covered individual

• SSN (or DOB)

• Whether covered for all 12 months of the year

• Months covered (if not all 12 months)

6056 (Forms 1094-‐C and 1095-‐C)

51

Form No. Form Name Used to: 1094-C Transmittal of

Employer-Provided Health Insurance Offer and Coverage Information Return

• Report summary information for each employer to the IRS

• Certify eligibility for transition relief (including medium-sized employer delay)

• Transmit Forms 1095-C to the IRS 1095-C Employer-Provided

Health Insurance Offer and Coverage

• Report information about each employee • Satisfy combined 6055 and 6056

reporting requirements for ALEs with self-funded plans

Form 1094-‐C Part 1 (Transmiwal Form)

Part I: Applicable Large Employer Member (ALE Member)

• Contact informaDon for employer and contact person

• Number of Forms 1095-‐C submiwed with the transmiwal

52

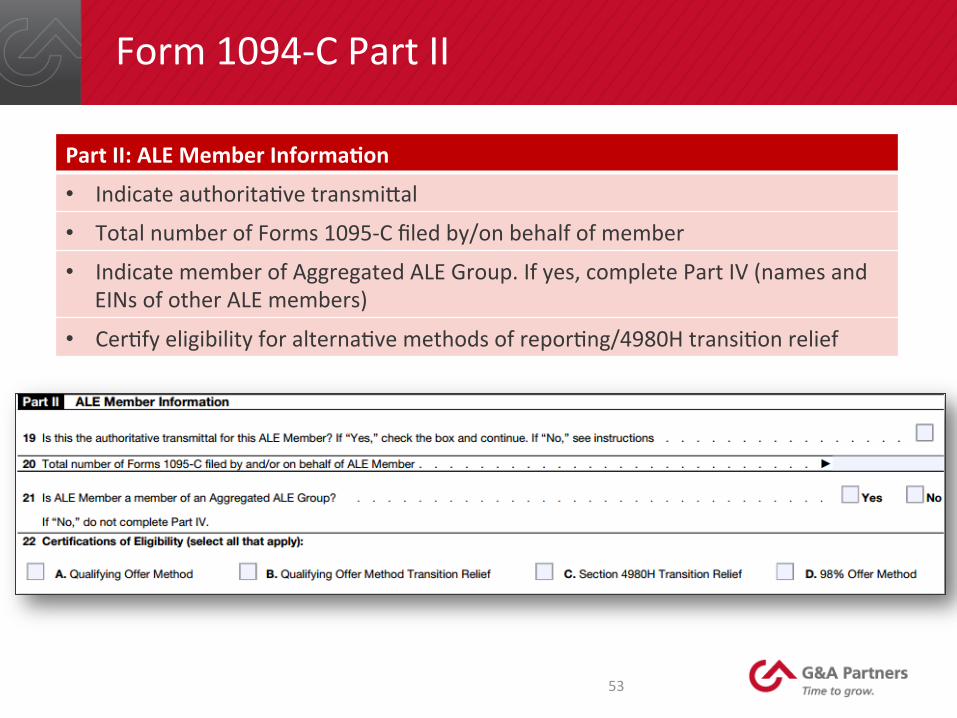

Form 1094-‐C Part II

Part II: ALE Member Informa,on

• Indicate authoritaDve transmiwal

• Total number of Forms 1095-‐C filed by/on behalf of member

• Indicate member of Aggregated ALE Group. If yes, complete Part IV (names and EINs of other ALE members)

• CerDfy eligibility for alternaDve methods of reporDng/4980H transiDon relief

53

Form 1094-‐C Part III

Part III: ALE Member Informa,on -‐ Monthly

• MEC Offer Indicator (Yes/No)

• Full-‐Dme Employee Count for ALE Member

• Total Employee Count for ALE Member

• Aggregated Group Indicator

• SecDon 4980H TransiDon Relief Indicator (50-‐99 Relief – Code A, 100 or More Relief – Code B)

54

Form 1095-‐C Part I

Employee Applicable Large Employer Member (Employer)

• Name • SSN • Address

• Name • EIN • Address • Contact phone number

Employer will complete one Form 1095-C for each full-time employee*

55

Form 1095-‐C Part II Line 14 Employee Offer and Coverage

• Enter a code indicaDng informaDon regarding offer of coverage

Line 14: Offer of Coverage

56

Form 1095-‐C Part II Lines 15 & 16

CODE EXPLANATION

2A Employee not employed during the month

2B Employee not a full-‐Dme employee

2C Employee enrolled in offered coverage

2D Employee in a 4980H(b) Limited Non-‐Assessment Period

2E MulDemployer interim rule relief

Line 15–Affordability of coverage: enter cost of employee share of lowest-‐cost monthly premium for self-‐only minimum value coverage

Line 16–SecDon 4980H safe harbors: enter code indicaDng why penalty won’t apply

NOTE: Code 2C should be used for any month in which the employee enrolled coverage, regardless of whether any other code could also apply.

CODE EXPLANATION

2F 4980H affordability Form W-‐2 safe harbor

2G 4980H affordability federal poverty line safe harbor

2H 4980H affordability rate of pay safe harbor

2I Non-‐calendar year transiDon relief applies

57

Form 1095-‐C Part III (Combined ReporDng for Self-‐funded ALEs)

Covered Individuals

• Name of covered individual

• SSN (or DOB)

• Whether covered for all 12 months of the year

• Months covered (if not all 12 months)

Employers with self-funded plans will complete one Form 1095-C for each employee who enrolls in the health coverage (whether full-time or not)

58

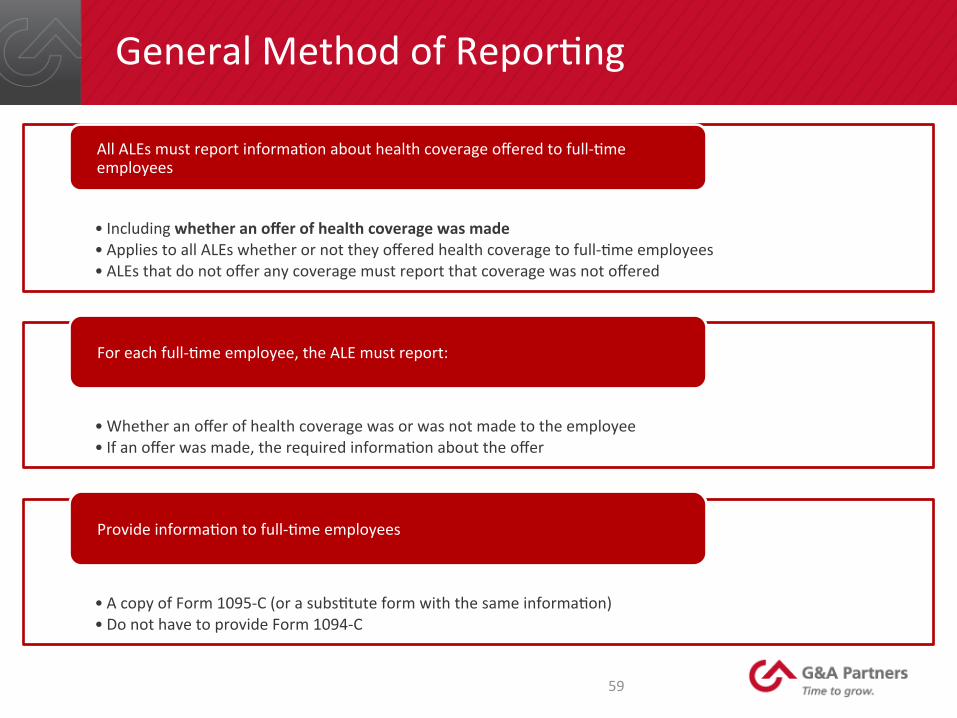

General Method of ReporDng

• Including whether an offer of health coverage was made • Applies to all ALEs whether or not they offered health coverage to full-‐Dme employees • ALEs that do not offer any coverage must report that coverage was not offered

All ALEs must report informaDon about health coverage offered to full-‐Dme employees

• Whether an offer of health coverage was or was not made to the employee • If an offer was made, the required informaDon about the offer

For each full-‐Dme employee, the ALE must report:

• A copy of Form 1095-‐C (or a subsDtute form with the same informaDon) • Do not have to provide Form 1094-‐C

Provide informaDon to full-‐Dme employees

59

The Qualifying Offer Method

Qualifying Offer occurs when the

ALE:

• Offers MEC that is affordable (based on FPL) and provides minimum value AND

• Offers MEC to the employee’s spouse and dependents (if any)

If made for all 12 months:

• Provide less detailed informaDon on IRS returns • Provide simplified employee statements (unless enrolled in self-‐insured coverage)

If not made for all 12 months

• Use the general reporDng method • Use an indicator code for months that a Qualifying Offer was received

ALE must make a Qualifying Offer for all months of a year in which the employee was full-‐Dme under SecDon 4980H

60

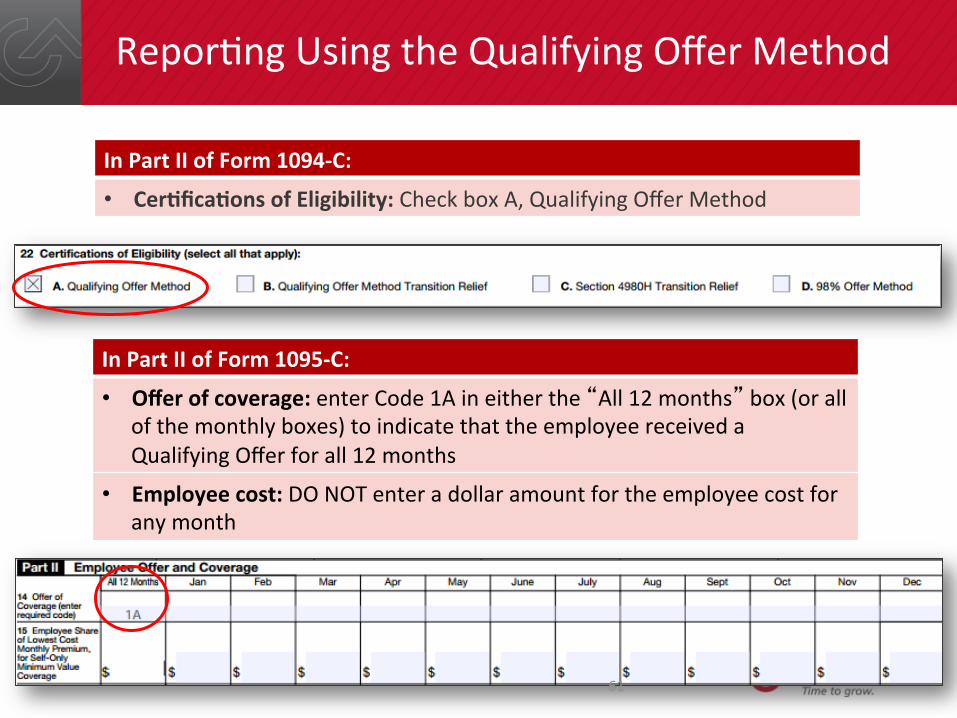

ReporDng Using the Qualifying Offer Method

In Part II of Form 1095-‐C:

• Offer of coverage: enter Code 1A in either the “All 12 months” box (or all of the monthly boxes) to indicate that the employee received a Qualifying Offer for all 12 months

• Employee cost: DO NOT enter a dollar amount for the employee cost for any month

In Part II of Form 1094-‐C:

• Cer,fica,ons of Eligibility: Check box A, Qualifying Offer Method

61

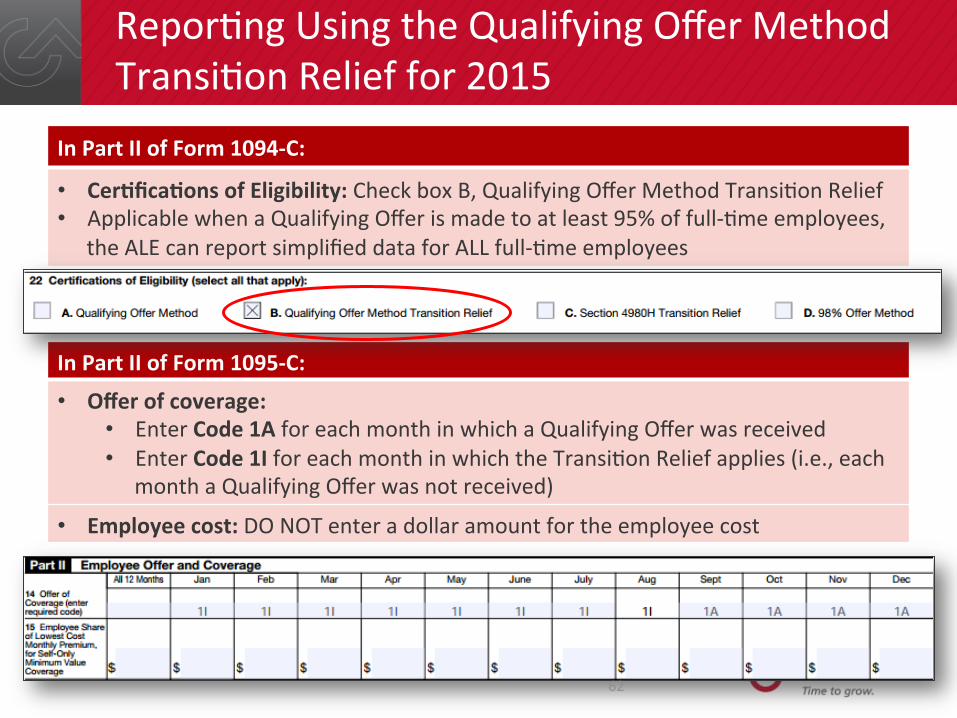

ReporDng Using the Qualifying Offer Method TransiDon Relief for 2015

In Part II of Form 1095-‐C:

• Offer of coverage: • Enter Code 1A for each month in which a Qualifying Offer was received • Enter Code 1I for each month in which the TransiDon Relief applies (i.e., each

month a Qualifying Offer was not received)

• Employee cost: DO NOT enter a dollar amount for the employee cost

In Part II of Form 1094-‐C:

• Cer,fica,ons of Eligibility: Check box B, Qualifying Offer Method TransiDon Relief • Applicable when a Qualifying Offer is made to at least 95% of full-‐Dme employees,

the ALE can report simplified data for ALL full-‐Dme employees

62

The 98% Offer Method

• Affordability based on any pay or play safe harbor method

ALE must offer affordable, minimum value coverage to at least 98% of employees and dependents reported on its SecDon 6056 return

• Eligible ALEs do not have to specify their number of full-‐Dme employees or idenDfy which are full-‐Dme on IRS returns

• No simplified method for employee statements

How to Report:

63

Final InstrucDons and Forms

• Instruc,ons for Forms 1094-‐C and 1095-‐C (“Applicable large employers” (i.e., those subject to the employer mandate), self-‐insured plans complete the en,re Form 1095-‐C) • hwp://www.irs.gov/pub/irs-‐pdf/i109495c.pdf?

elqTrackId=a60d4092f5fd4544bb315fd1ed09b9f8&elq=23705b47fa29429~c29487ad788f039&elqCampaignId=&elqaid=10242&elqat=1

• Form 1094-‐C (a transmigal/cover sheet) to the IRS • hwp://www.irs.gov/pub/irs-‐pdf/f1094c.pdf?

elqTrackId=2057bae1a6b54ac1998eeae3a3069268&elq=23705b47fa29429~c29487ad788f039&elqCampaignId=&elqaid=10242&elqat=1

• Form 1095-‐C to both the IRS and individuals (If its plan is insured, the applicable large employer will only complete Parts I and II of Form 1095-‐C) • hwp://www.irs.gov/pub/irs-‐pdf/f1095c.pdf?

elqTrackId=71926ae587914509895769dd600c71b9&elq=23705b47fa29429~c29487ad788f039&elqCampaignId=&elqaid=10242&elqat=1

• Instruc,ons for Forms 1094-‐B and 1095-‐B (Insurance carriers and small employers with self-‐insured plans use these forms) • hwp://www.irs.gov/pub/irs-‐pdf/i109495b.pdf?

elqTrackId=26cda07338d645a59e28e24bc92e9e67&elq=23705b47fa29429~c29487ad788f039&elqCampaignId=&elqaid=10242&elqat=1

• Form 1094-‐B (a transmigal /cover sheet) to the IRS • hwp://www.irs.gov/pub/irs-‐pdf/f1094b.pdf?

elqTrackId=684851f6a6b54f98905c2a067a23b9c0&elq=23705b47fa29429~c29487ad788f039&elqCampaignId=&elqaid=10242&elqat=1

• Form 1095-‐B to both the IRS and individuals • hwp://www.irs.gov/pub/irs-‐pdf/f1095b.pdf?

elqTrackId=15c9a288d12246eba09e453f151b2b21&elq=23705b47fa29429~c29487ad788f039&elqCampaignId=&elqaid=10242&elqat=1

64

G&A’s PPACA Compliance Support

65

PPACA – Working with G&A

• Tools and support for determining affordability, minimum value, measurement/stability period

• IRS ReporDng (6055/6056) services • Time tracking reports to monitor part Dme employee hours to determine benefit eligibility

• Tracking variable hour, change in status, leaves of absence, and breaks in service

• Expert guidance 66

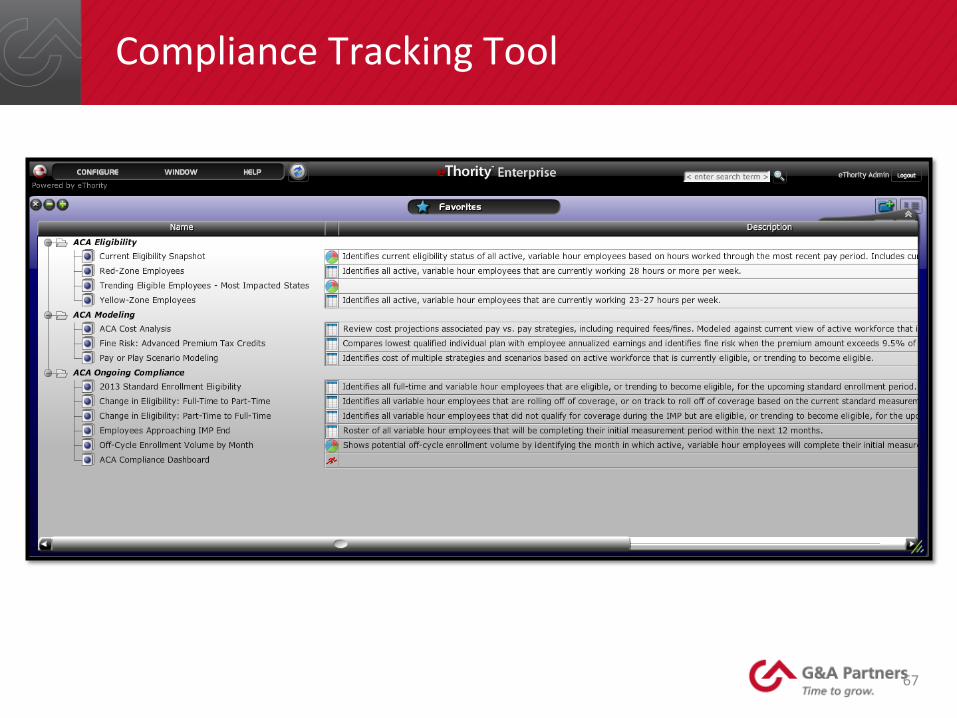

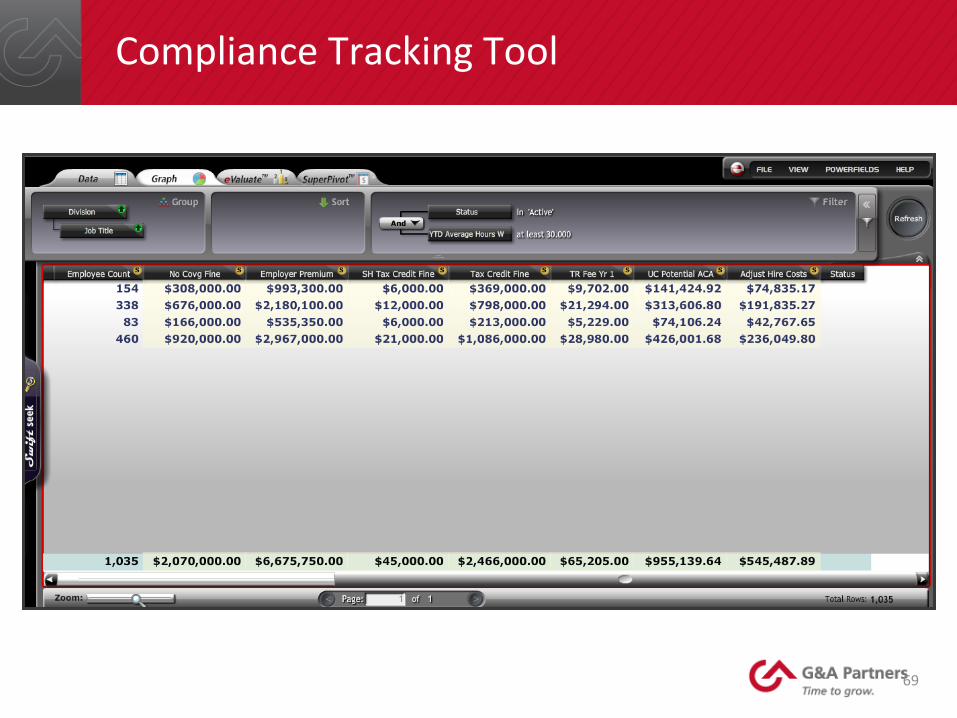

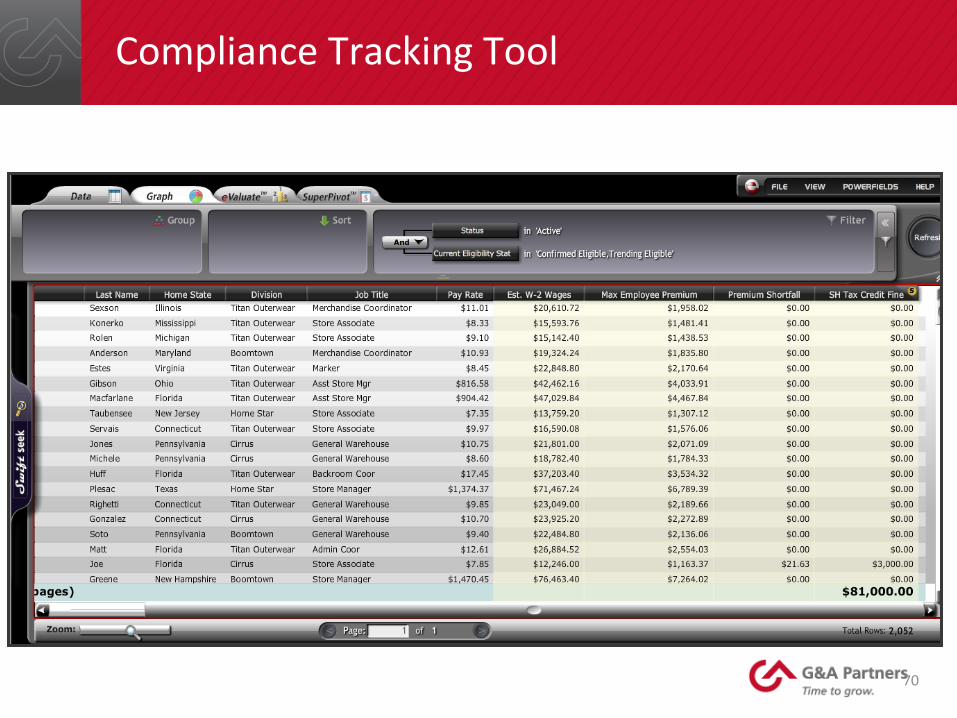

Compliance Tracking Tool

67

Compliance Tracking Tool

68

Compliance Tracking Tool

69

Compliance Tracking Tool

70

QuesDons for You to Consider

• What strategies will work for your business?

• The value of benefits vs. employer cost?

• What will your compeDtors do?

• Do you go at this alone or outsource?

71

Summary

• PPACA rules are constantly evolving • What works today may not work tomorrow • There is no “one size fits all” approach • A comprehensive strategy is more effecDve • Examine all opportuniDes available • Seek relevant guidance (legal, financial, operaDonal) • Avoid the pivalls of over-‐reacDon to penalDes • Don’t let Health Reform “run your business”!

72

QUESTIONS?

G&A Partners [email protected]

(866) 634-‐6713

This webinar has been recorded and will be posted on the G&A website by Friday.