Preparing for a New Export - ag-innovation.usask.ca · products • Reasonablecase ... Buyers’...

21

Transcript of Preparing for a New Export - ag-innovation.usask.ca · products • Reasonablecase ... Buyers’...

Preparing for a New Export

Opportunity: CETA and Canadian Pork

Martin Rice, Executive Director

Fifth Annual Canadian Agri-Food Policy

Conference – Ottawa, January 29, 2015

Canadian pork industry depends on exports for more

than two-thirds of its output (not including live exports)

Canadian Pork Exports

Source: Statistics Canada

Canadian Pork Exports by Leading

Market

tonnes

31%

Source: Statistics Canada

tonnes

16%

14%

Value of Canadian Pork ExportsCdn $/kg

Source: Statistics Canada

Major Pork Export Markets Major Pork Export Markets Major Pork Export Markets Major Pork Export Markets

Volume % 1990 vs 2013Volume % 1990 vs 2013Volume % 1990 vs 2013Volume % 1990 vs 2013

Japan

Other

Mexico

US

China, Taiwan & HK

Russia

Other

11%

4%

7% 8%

13%

31%

Source: Statistics Canada

US Japan

PhilippinesMexicoSouth Korea

& HK

1990 = 256,000 tonne / $ 686 million 2013 = 1,184,167 tonne / $ 3.2 billion

78%

11%

16%

4%3% 7%

17%

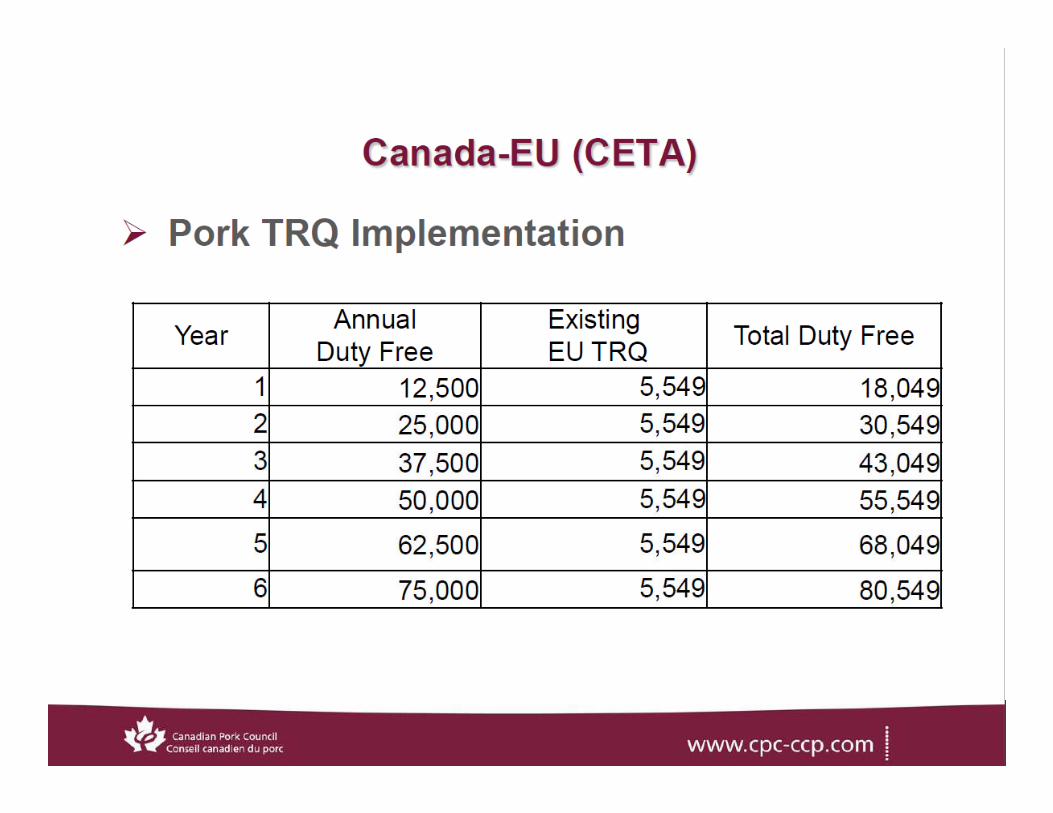

Canada – EU (CETA)

• Text of the agreement announced on September 26, 2014

• Currently at ‘legal scrub’ stage, followed by presentation to legislatures

• Pork highlights:

• 80,000+ tonnes (bone-in equivalent) phased in over five years

• Consists of 75,000 new quota plus 6,000 EU accession quota made duty-free, covering all fresh, chilled and frozen categories (Chapter 2)

• EU currently imports 32,000 tonnes

• Zero in-quota duty• Zero in-quota duty

• Licensing system (not first come-first serve as earlier anticipated)

• Differences from other EU WTO quotas include: easier licence application process with much lower security deposits, licences issued at least 30 days in advance, longer validity, and provision for carry-over within the year; opportunity for new importers including processors; and review clause with underfill mechanism (with potential to go FCFS)

• Immediate tariff-free access into EU for processed, prepared porkproducts

• Reasonable case scenario is for implementation in 2016

The EU Pork Picture

• 500+ million inhabitants

• Per capita consumption is 40 kg (Canada’s is 22 kg)

• Total pork consumption exceeds 20 million tonnes

• Imports of about 40,000 tonnes (Canada’s over 200,000 tonnes)

• Imports are 0.2% of internal market (for Canada, it is 25%)

• Canadian pork quota under CETA (80,000 tonnes) if

fully utilized, would account for well under 0.5% of the

EU pork market

• The EU also exports well over 2 million tonnes of pork annually

• Import sensitive product?

• Canadian pork quota is immaterial to the total EU

market but represents important opportunity for

Canada

The EU pork market is not homogenous

• The uses of pork cuts varies significantly between

member states

• For example, looking at just three of the 28 members states, Italy, France and Germany – the market in Italy is essentially hams (i.e., hindquarters), while sausages (using forequarters) dominate in Germany. A mixture in France.in Germany. A mixture in France.

• Germany has an enormous further processed meat market;

• 2½ times the size of the Italian and French markets

• The further processor sector is relatively concentrated in Germany while highly fragmented in Italy and France

• Many other differences such as in seasonality of demand, acceptance (even awareness) of chilled (as distinct from fresh and frozen), and pricing of individual carcass components

Buyers’ criteria for choice of Product

Buyers’ criteria for choice of Supplier

Ability to supply large volumes

Good / regular personal contact with the supplier

The best traceability

Reliability of supply

Regularity of the product

0 1 2 3 4 5

I prefer a national supplier

The lowest price

Supplier already known / bought from in the past

A higher than average quality product

Strong animal welfare & environmental guarantees

Average

France

Italy

Germany

Source: Gira interviews

Breaking into Europe will require focus and effort:

• Knowledge and experience within EU pork sector of

Canadian products is very limited

• Most EU meat buyers have no experience with non-EU suppliers

• This includes virtually no experience with ‘chilled’ pork

• Significantly higher value-added than frozen and likely wider EU market opportunity

• Most EU buyers are assuming Canada can only supply frozen pork

• The Canadian image is « basically good »• The Canadian image is « basically good »

• To get serious, we will need to find potentially interested buyers and show them we can supply what they want, and offering our products at a competitive price

• Once become a regular supplier, are part of the EU competition

• Canada is not competitive in all levels of EU pork market

• Market opportunities principally in shoulders and hams and, to a lesser extent, loins

New framework allows Canadian pork industry to

promote itself as an integral and reliable component

of European supply chains, because CETA:

a) covers the gamut (at least we hope!) of access issues from tariffs to

resolution mechanisms for technical and SPS issues;

b) provides greater comfort and enhanced security to both sides when

looking to negotiate supply-input contracts;

c) allows market development efforts to be far-better framed in the longer

term context of relationship building (i.e., rather than simple reliance

on spot market sales); and

d) fosters development of more seamless and fluid relationship which,

over time, should hopefully marry the regulatory frameworks of both

Parties over time.

CETA enhances opportunities for Canadian and

European pork industries to collaborate in advocacy

initiatives on issues of shared interest by:

• supporting the building and cementing of business-to-business

relationships thereby allowing for more comprehensive

representations to national and sub-national governments (e.g.,

regulatory agencies) and consumer organizations;

• enhancing Canadian government and industry’s ability to better • enhancing Canadian government and industry’s ability to better

identify/quantify self-interests of key European influencers (law-

makers, regulators, consumer organizations, industry associations,

etc.) as required; and

• enhancing Canadian exporters’ credibility in exerting a more

effective degree of industry-led advocacy when working with like-

minded third country interests in having potential EU trade barriers

avoided or removed.

We anticipate an enhanced ability to promote

Canadian pork by:

i. allowing exporters to better leverage EU industry to promote

positive attributes of Canadian pork (resulting from the building of

longer term relationships);

ii. building and growing a base within the European market that

allows Canadian industry to better position itself and participate in

EU/MS domestic promotional initiatives; EU/MS domestic promotional initiatives;

iii. creating a greater familiarity, within both the EU pork industry

specifically as well as more general investment community, of the

potential for direct foreign investment in the Canadian industry;

and

iv. promote additional indirect marketing benefits in other Third

Country markets by demonstrating the ability to meet one of the

world’s most demanding set of technical and SPS standards.

Reconfirms need for DFATD support for

agriculture, fish and food sector by:

� improved/more timely market intelligence on business

opportunities and market trends;

� improved identification and communication of new

opportunities notably related to small/medium EU

enterprises seeking growth through a reliable import base enterprises seeking growth through a reliable import base

(e.g., EU enterprises not yet on approved importers list,

business partnering opportunities, etc.); and

� supporting development of new and sustainable

relationships between established European

processors/importers and Canadian suppliers

Canadian Pork Council

220 Laurier Ave. W, Suite 900

Ottawa, ON

Canada, K1P 5Z9

Telephone: (613) 236-9239

Fax: (613) 236-6658

www.cpc-ccp.com