Prepared under the supervision of Palesa Mkhize …etfcib.absa.co.za/Fund Documents/SP GIVI SA...

40

NEWFUNDS COLLECTIVE INVESTMENT SCHEME S&P GIVI SA FINANCIALS INDEX ETF PORTFOLIO AUDITED ANNUAL FINANCIAL STATEMENTS 31 December 2018 Prepared under the supervision of Palesa Mkhize CA(SA) Designation: Head of Financial Decision Support, Corporate and Investment Bank, Absa Bank Limited

Transcript of Prepared under the supervision of Palesa Mkhize …etfcib.absa.co.za/Fund Documents/SP GIVI SA...

NEWFUNDS COLLECTIVE INVESTMENT SCHEMES&P GIVI SA FINANCIALS INDEX ETF PORTFOLIO

AUDITED ANNUAL FINANCIAL STATEMENTS31 December 2018

Prepared under the supervision of Palesa Mkhize CA(SA)Designation: Head of Financial Decision Support, Corporate and Investment Bank, Absa Bank

Limited

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOTABLE OF CONTENTSfor the year ended 31 December 2018

Contents

Trustees’ report 1

Directors' responsibilities and approval 2

Independent auditor's report 4

Directors' report 7

Statement of comprehensive income 9

Statement of financial position 10

Statement of changes in net assets attributable to investors 11

Statement of cash flows 12

Summary of accounting policies 13

Notes to the annual financial statements 21

REPORT OF THE TRUSTEE FOR THE NEWFUNDS COLLECTIVE INVESTMENT SCHEME IN SECURITIES We, the Standard Bank of South Africa Limited, in our capacity as Trustee of the NewFunds Collective Investment Scheme in Securities (“the Scheme”) have prepared a report in terms of Section 70(1)(f) of the Collective Investment Schemes Control Act, 45 of 2002, as amended (“the Act”), for the financial year ended 31 December 2018. In support of our report we have adopted certain processes and procedures that allow us to form a reasonable conclusion on whether the Manager has administered the Scheme in accordance with the Act and the Scheme Deed. As Trustees of the Scheme we are also obliged to in terms of Section 70(3) of the Act to satisfy ourselves that every statement of comprehensive income, statement of financial position or other return prepared by the Manager of the Scheme as required by Section 90 of the Act fairly represents the assets and liabilities, as well as the income and distribution of income, of every portfolio of the Scheme. The Manager is responsible for maintaining the accounting records and preparing the annual financial statements of the Scheme in conformity with International Financial Reporting Standards. This responsibility also includes appointing an external auditor to the Scheme to ensure that the financial statements are properly drawn up so as to fairly represent the financial position of every portfolio of its collective investment scheme are in accordance with International Financial Reporting Standards and in the manner required by the Act. Our enquiry into the administration of the Scheme by the Manager does not cover a review of the annual financial statements and hence we do not provide an opinion thereon. Based on our records, internal processes and procedures we report that nothing has come to our attention that causes us to believe that the accompanying financial statements do not fairly represent the assets and liabilities, as well as the income and distribution of income, of every portfolio of the Scheme administered by the Manager. We confirm that according to the records available to us, no losses were suffered in the portfolios and no investor was prejudiced as a result thereof. We conclude our report by stating that we reasonably believe that the Manager has administered the Scheme in accordance with:

(i) the limitations imposed on the investment and borrowing powers of the manager by this Act;

and

(ii) the provisions of this Act and the deed;

Melinda Mostert Seggie Moodley Standard Bank of South Africa Limited Standard Bank of South Africa Limited

20 March 2019

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIODIRECTORS' REPORTfor the year ended 31 December 2018

7

Management company registrationnumber

2005/034899/07

RegistrationCountry of incorporation anddomicile

South Africa

Date of publication 26 March 2019

Nature of business and principleactivities

NewFunds Collective Investment Scheme (the Scheme) managesexchange traded fund (ETF) portfolios. Its objective is to track theperformance of specific indices on the stock market in eachportfolio. The S&P GIVI SA Financials Index ETF portfolio (“theportfolio" or "S&P GIVI SA Financials") tracks the S&P GIVISA Financials price index calculated daily by the independentinvestment consulting firm S&P Dow Jones Indices LLC. TheETF invests in companies that fall within the financial sectorbased on their underlying value indicators as opposed to marketcapitalisation.

Directors Name Appointmentdate

CHM Edwards 24/03/2016TJ Fearnhead 25/11/2013AB La Grange 10/07/2006DA Lorimer 01/12/2016BM Mgwaba 15/10/2015RMH Pitt 17/02/2017

Registered office 7th FloorAbsa Towers West15 Troye StreetJohannesburg2001

Bankers Standard Bank of South Africa Limited

Trustees Standard Bank of South Africa Limited

Auditors Ernst & Young Inc.102 Rivonia RoadSandtonJohannesburg2196

Supervised by The scheme is managed by NewFunds (RF) Proprietary Limited,a 100% owned subsidiary of Absa Bank Limited. The preparationof these annual financial statements therefore falls under the directsupervision of Absa Bank Limited, represented by Palesa Mkhize,CA(SA). All references to 'Manager' and 'Management' relate toNewFunds (RF) Proprietary Limited.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIODIRECTORS' REPORT (continued)for the year ended 31 December 2018

8

Review of financial results The financial results of the portfolio are set out in the attachedfinancial statements. The results do not, in the opinion of thedirectors, require further explanation.

Events after the reporting date Events material to the understanding of these financialstatements, has occurred in the period between the financialyear end and the date of this report. Events after the reportingdate are disclosed in Note 18.

Going concern The annual financial statements have been prepared on thebasis of accounting policies applicable to a going concern.

Special resolutions No special resolutions were passed during the period underreview.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSTATEMENT OF COMPREHENSIVE INCOMEfor the year ended 31 December 2018

9

2018 2017Notes R R

RevenueNet (loss)/gain on financial assets and liabilities at fairvalue through profit and loss 6.1 (8 896 164) 231 080

(8 896 164) 231 080

Revenue 3 2 554 314 1 989 167Total Income (6 341 850) 2 220 247

Management and administration expenses (145 551) (101 502)(Decrease)/Increase in net assets attributable to investorsbefore distribution 4 (6 487 401) 2 118 745Income distribution 15 (2 560 900) (865 143)(Decrease)/Increase in net assets attributable toinvestors after distribution ( 9 048 301) 1 253 602

Represented by:

(Loss)/Income attributable to investors (152 137) 1022 522Capital attributable to investors (8 896 164) 231 080

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSTATEMENT OF FINANCIAL POSITIONas at 31 December 2018

10

2018 2017Notes R R

Assets

Non-current assetsPortfolio Investments 6 43 323 313 52 034 554Total non-current assets 43 323 313 52 034 554

Current assetsTrade receivables 7 949 1 233Cash and cash equivalents 10 712 535 1 036 907Total current assets 713 484 1 038 140

Total assets 44 036 797 53 072 694

Liabilities

Current liabilitiesTrade and other payables 8 12 834 431Net assets attributable to investors 44 023 963 53 072 263

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSTATEMENT OF CHANGES IN NET ASSETS ATTRIBUTABLE TO INVESTORSfor the year ended 31 December 2018

11

Capitalattributableto investors

Incomeattributableto investors

Net assetsattributableto investors

R R R

Balance at 1 January 2017 50 576 746 1 241 916 51 818 662Increase in net assets attributable to investors 231 080 1 022 522 1 253 602Balance at 31 December 2017 50 807 826 2 264 438 53 072 264

Balance at 1 January 2018 50 807 826 2 264 438 53 072 264Decrease in net assets attributable to investors (8 896 164) (152 137) (9 048 301)Balance at 31 December 2018 41 911 662 2 112 301 44 023 963

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSTATEMENT OF CASH FLOWSfor the year ended 31 December 2018

12

Cash 2018 2017Notes R R

Cash flows from operating activities

Cash used in operations 9 (133 148) (101 703)Purchase of equity securities due to rebalancing (15 096 777) (18 113 863)Proceeds from sale of equity securities due to rebalancing 14 911 854 17 694 596Real Estate Investment Income 705 700 652 767Dividends received 1 822 612 1 310 948Interest received 26 287 24 804Distributions (2 560 900) (1 048 224)Net cash generated/(used in) by operating activities (324 372) 419 325

Net (decrease)/increase in cash and cash equivalents (324 372) 419 325

Cash and cash equivalents at the beginning of the year 1 036 907 617 582Cash and cash equivalents at the end of the year 10 712 535 1 036 907

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSummary of Accounting Policiesfor the year ended 31 December 2018

13

1. STATEMENT OF COMPLIANCE

The annual financial statements have been prepared in accordance with InternationalFinancial Reporting Standards (IFRS) and the interpretations issued by the InternationalFinancial Reporting Interpretations Committee of the IASB (IFRIC) and the requirements ofthe Collective Investments Schemes Control Act of 2002, the Trust Deed, JSE ListingRequirements and the SAICA Financial Reporting Guides.

2. SIGNIFICANT ACCOUNTING POLICIES

The significant accounting policies applied in the preparation of these annual financialstatements are set out below. These policies have been consistently applied to all the yearspresented, unless otherwise stated.

2.1 ADOPTION OF NEW AND REVISED ACCOUNTING STANDARDS

During the current year, the Scheme has adopted all of the new and revised standards andinterpretations issued by the IASB and the IFRIC that are relevant to its operations andeffective for annual reporting periods beginning on 1 January 2018. The adoption of thesenew and revised standards and interpretations has resulted in material changes to theScheme's accounting policies. For details of the new and revised accounting policies refer toNote 19.

2.2 BASIS OF PREPARATION

Apart from certain items that are carried at fair value, as explained in the accounting policiesbelow, the financial statements have been prepared on the historical cost basis. The principalaccounting policies are set out below.

The annual financial statements have been prepared on the basis of accounting policiesapplicable to a going concern.

The financial statements are presented in South African Rands (R), the presentation andfunctional currency of the Scheme. All financial information is presented to the nearestRand.

2.3 REVENUE RECOGNITION

Revenue comprises of interest income, real estate investment income, and dividend income.

Interest income and expense on amortised cost financial instruments are recognised in profitor loss using the effective interest method. The ‘effective interest rate’ is the rate that exactlydiscounts estimated future cash flows through the expected life of the financial instrument tothat instrument’s net carrying amount on initial recognition.

Dividends are recognised when the right to receive the dividend has been established.

Real Estate Investment Income (REIT) income in the form of cash distributions from theREIT is recognised when the right to receive income is established.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSummary of Accounting Policies (continued)for the year ended 31 December 2018

14

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

2.4 FINANCIAL INSTRUMENTS

IFRS 9 Financial Instruments (IFRS 9) has been adopted on 1 January 2018, and replacesIAS 39 Financial Instruments: Recognition and Measurement (IAS 39). As permitted underIFRS 9, NewFunds Collective Investment Scheme has elected not to restate comparativeperiods on the basis that it is not possible to do so without the application of hindsight. Thecomparative financial information for the 2017 reporting period has therefore been preparedunder the framework for financial instrument accounting within IAS 39. The followingsection sets out the accounting policies that were applied in the 2017 reporting period(2017), together with those that are applied under IFRS 9 (2018). Significant changes havebeen made to certain accounting policies, owing to the revised classification andmeasurement framework for financial instruments, as well as changes in the impairmentscope and methodology. Where there have been changes in accounting policies, thoseapplied in 2017 have been clearly distinguished from the current reporting period.

2.4.1 INITIAL RECOGNITION OF FINANCIAL ASSETS AND FINANCIALLIABILITIES (2017 and 2018)

Financial assets and liabilities are recognised when the scheme becomes a party to the termsof the contract, which is the trade date. All financial instruments are measured initially atfair value plus/minus transaction costs, except in the case of financial assets and financialliabilities recorded at fair value through profit or loss, where transaction costs are expensedupfront.

On initial recognition, it is presumed that the transaction price is the fair value unless thereis observable information available in an active market to the contrary. The best evidence ofan instrument’s fair value on initial recognition is typically the transaction price. However,if fair value can be evidenced by comparison with other observable current markettransactions in the same instrument, or is based on a valuation technique whose inputsinclude only data from observable markets then the instrument should be recognised at thefair value derived from such observable market data.

For valuations that have made use of significant unobservable inputs, the difference betweenthe model valuation and the initial transaction price (“Day One profit”) is recognised inprofit or loss either on a straight-line basis over the term of the transaction, or over thereporting period until all model inputs will become observable where appropriate, orreleased in full when previously unobservable inputs become observable.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSummary of Accounting Policies (continued)for the year ended 31 December 2018

15

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

CLASSIFICATION AND MEASUREMENT OF FINANCIAL INSTRUMENTS(2018)

On initial recognition, financial assets are classified into the following measurementcategories:

• Amortised cost;• Fair value through other comprehensive income; or• Fair value through profit or loss

The classification and subsequent measurement of financial assets depends on:• The business model within which the financial assets are managed; and• The contractual cash flow characteristics of the asset (that is, whether the cash

flows represent “solely payments of principal and interest”).

Business model assessment:

The business model reflects how the NewFunds Collective Investment Scheme manages thefinancial assets in order to generate cash flows and returns. The NewFunds CollectiveInvestment Scheme makes an assessment of the objective of a business model in which afinancial asset is held at a portfolio level because this best reflects the way the business ismanaged and information is provided to management. The factors considered indetermining the business model include (i) how the financial assets' performance isevaluated and reported to management, (ii) how the risks within the portfolio are assessedand managed and (iii) the frequency, volume, timing for past sales, sales expectations infuture periods, and the reasons for such sales. The NewFunds Collective Investment Schemereclassifies debt instruments when, and only when, the business model for managing thoseassets changes. Such changes are highly unlikely and therefore expected to be veryinfrequent.

Assessment of whether contractual cash flows are solely payments of principal andinterest (SPPI):

In making the assessment of whether the contractual cash flows have SPPI characteristics,the NewFunds Collective Investment Scheme considers whether the cash flows areconsistent with a basic lending arrangement. That is, the contractual cash flows recoveredmust represent solely the payment of principal and interest. Principal is the fair value of thefinancial asset on initial recognition. Interest typically includes only consideration for thetime value of money and credit risk but may also include consideration for other basiclending risks and costs, such as liquidity risk and administrative costs, together with a profitmargin. Where the contractual terms include exposure to risk or volatility that is inconsistentwith a basic lending arrangement, the cash flows would not be considered to be SPPI andthe assets would be mandatorily measured at fair value through profit or loss, as describedbelow. In making the assessment, the NewFunds Collective Investment Scheme considers,inter alia, contingent events that would change the amount and timing of cash flows,prepayment and extension terms, leverage features, terms that limit the NewFundsCollective Investment Scheme's claim to cash flows from specified assets (e.g. non-recourseasset arrangements), and features that modify consideration of the time value of money (e.g.tenor mismatch). Contractual cash flows are assessed against the SPPI test in the currency inwhich the financial asset is denominated.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSummary of Accounting Policies (continued)for the year ended 31 December 2018

16

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

CLASSIFICATION AND MEASUREMENT OF FINANCIALINSTRUMENTS (2018) (continued)

Debt Instruments:

Debt instruments are those instruments that meet the definition of a financial liabilityfrom the issuer's perspective, such as loans and government and corporate bonds. TheNewFunds Collective Investment Scheme classifies its debt instruments as follows:

i. Amortised cost - Financial assets are classified within this measurement category ifthey are held within a portfolio whose primary objective is the collection ofcontractual cash flows, where the contractual cash flows on the instrument are SPPI,and that are not designated at fair value through profit or loss. These financial assetsare subsequently measured at amortised cost where interest is recognised asEffective interest within Interest and similar income using the effective interest ratemethod. The carrying amount is adjusted by the cumulative expected credit lossesrecognised.

ii. Fair value through other comprehensive income - This classification applies tofinancial assets which meet the SPPI test, and are held within a portfolio whoseobjectives include both the collection of contractual cash flows and the selling offinancial assets. These financial assets are subsequently measured at fair value withmovements in the fair value recognised in other comprehensive income, with theexception of interest income, expected credit losses and foreign exchange gains andlosses that are recognised within profit or loss. When the financial asset isderecognised, the cumulative gain or loss previously recognised in othercomprehensive income is reclassified from equity to “Gains and losses frombanking and trading activities” in profit or loss. Interest income from these financialassets is included as “Effective interest” within “Interest and similar income” usingthe effective interest rate method.

iii. Fair value through profit or loss - Financial assets that do not meet the criteria foramortised cost or fair value through other comprehensive income are mandatorilymeasured at fair value through profit or loss. Gains and losses on these instrumentsare recognised in fair value adjustment in profit or loss. The NewFunds CollectiveInvestment Scheme may also irrevocably designate financial assets that wouldotherwise meet the requirements to be measured at amortised cost or at fair valuethrough other comprehensive income, as at fair value through profit or loss, if doingso would eliminate or significantly reduce an accounting mismatch that wouldotherwise arise. These will be subsequently measured at fair value through profit orloss with gains and losses recognised as fair value adjustment in profit or loss.

Equity instruments

IFRS 9 (2018) provides that at initial recognition, an irrevocable election may be madeto present subsequent changes in the fair value of an equity instrument in othercomprehensive income, provided that the instrument is neither held for trading norconstitutes contingent consideration recognised in a business combination. Amountsrecognised in other comprehensive income are not subsequently recognised in profit orloss. Dividends, when representing a return on investment, continue to be recognised inprofit or loss when the Scheme’s right to receive payment is established.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSummary of Accounting Policies (continued)for the year ended 31 December 2018

17

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

2.4 FINANCIAL INSTRUMENTS (continued)

2.4.1 FINANCIAL ASSETS AND FINANCIAL LIABILITIES (continued)

Equity instruments (continued)

All equity instruments for which the designation at fair value through other comprehensiveincome has not been applied are required to be recognised at fair value through profit orloss. Gains and losses on equity instruments at fair value through profit or loss arerecognised as “Net gain (loss) on financial assets and liabilities at fair value through profitand loss” in the statement of comprehensive income. Refer to note 17.

Financial Liabilities

Financial liabilities arising from the securities issued by the Portfolio are measured at fairvalue representing the investor's right to an interest in the Portfolio's net assets, i.e. the NetAsset Value ("NAV") of the Portfolio. Changes in the fair value are included in profit orloss in the period in which the change arises and these financial liabilities are designated atfair value through profit or loss. Gains and losses on financial liabilities are presented inOCI to the extent that they relate to changes in own credit risk. For current period there wereno significant changes in own credit risk.

CLASSIFICATION AND MEASUREMENT OF FINANCIAL INSTRUMENTS(2017)

Financial assets are classified as financial assets at fair value through profit or loss or loansand receivables. The classification depends on the nature and purpose of the financial assetsand is determined at the time of initial recognition.

FINANCIAL INSTRUMENTS AT FAIR VALUE THROUGH PROFIT OR LOSS (2017)

A financial instrument other than one that is held for trading may be designated as at fairvalue through profit and loss upon initial recognition if:

· such designation eliminates or significantly reduces a measurement or recognitioninconsistency that would otherwise arise; or

· the financial instrument forms part of a group of financial assets or financial liabilitiesor both, which is managed and its performance is evaluated on a fair value basis, inaccordance with the documented risk management or investment strategy, taking intoconsideration the relationship of assets to liabilities in a way that mitigates market risk;or

· it forms part of a contract containing one or more embedded derivatives, and IAS 39Financial Instruments: Recognition and Measurement permits the entire combinedcontract (asset or liability) to be designated as at fair value through profit and loss.

Financial instruments at fair value through profit and loss are stated at fair value, with anygains or losses arising on re-measurement recognised in profit or loss.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSummary of Accounting Policies (continued)for the year ended 31 December 2018

18

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

2.4 FINANCIAL INSTRUMENTS (continued)

2.4.1 FINANCIAL ASSETS AND FINANCIAL LIABILITIES (continued)

LOANS AND RECEIVABLES

Loans and receivables are non-derivative financial assets with fixed or determinablepayments that are not quoted in an active market. Loans and receivables are measured atamortised cost using the effective interest method, less any impairment.Interest income is recognised by applying the effective interest rate, except for short-termreceivables when the recognition of interest would be immaterial.

FINANCIAL LIABILITIES

Financial liabilities are measured at amortised cost except for liabilities designated at fairvalue which are held at fair value through profit and loss. Amortised cost is the initial fairvalue (which is normally the amount borrowed) adjusted for premiums, discounts,repayments and the amortisation of coupon, fees and expenses to represent the effectiveinterest rate of the liability.

Creation and redemption (2017 and 2018)

Creation and redemption are recorded on trade date using historic cost beingthe previous day closing index price.

Rebalancing (2017 and 2018)

Fund rebalancing activities are undertaken periodically to ensure propertracking of performance of the Benchmark Index and to keep adequate cashbalance. It is recorded on trade date using historic cost being the previous dayclosing index price.

Net assets attributable to investors (redeemable securities) (2017 and 2018)

All redeemable securities provided by the portfolios provide investors with the right torequest redemption for cash or in specie at the value proportionate to each investor’s share.The securities are redeemable at any time at the option of the security holder and aretherefore classified as financial liabilities. These are measured at the redemption amounts.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSummary of Accounting Policies (continued)for the year ended 31 December 2018

19

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

2.4 FINANCIAL INSTRUMENTS (continued)

2.4.1 FINANCIAL ASSETS AND FINANCIAL LIABILITIES (continued)

FAIR VALUE (2017 and 2018)

The listed underlying investments are carried at fair value through profit or loss such asthose designated by management under the fair value option.

The fair value of a financial instrument is the price that would be received to sell an asset orpaid to transfer a liability in an orderly transaction between market participants at themeasurement date.

DERECOGNITION OF FINANCIAL INSTRUMENTS (2017 and 2018)

Derecognition of financial assets

Full derecognition only occurs when the rights to receive cash flows from the asset havebeen discharged, cancelled or have expired, or the Scheme transfers both its contractualright to receive cash flows from the financial assets (or retains the contractual rights toreceive the cash flows, but assumes a contractual obligation to pay the cash flows to anotherparty without material delay or reinvestment) and substantially all the risks and rewards ofownership, including credit risk, prepayment risk and interest rate risk.

Derecognition of financial liabilities

A financial liability is derecognised when the obligation under the liability is discharged,cancelled or expires. Where an existing financial liability is replaced by another from thesame party on substantially different terms, or the terms of an existing liability aresubstantially modified (taking into account both quantitative and qualitative factors), suchan exchange or modification is treated as a derecognition of the original liability and therecognition of a new liability, and the difference in the respective carrying amounts isrecognised in profit or loss. Where the terms of an existing liability are not substantiallymodified, the liability is not derecognised. Costs incurred on such transactions are treated asan adjustment to the carrying amount of the liability and are amortised over the remainingterm of the modified liability.

2.4.2 OFFSETTING

In accordance with IAS 32 Financial Instruments: Presentation, the Scheme reports financialassets and financial liabilities on a net basis on the statement of financial position only ifthere is a current legally enforceable right to set off the recognised amounts and there isintention to settle on a net basis, or to realise the asset and settle the liability simultaneously.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIOSummary of Accounting Policies (continued)for the year ended 31 December 2018

20

For the purposes of the statement of cash flows, cash comprises cash on hand and demanddeposits, and cash equivalents comprise highly liquid investments that are convertible intocash with an insignificant risk of changes in value with original maturities of three monthsor less.

2.6 SEGMENTAL REPORTING

The portfolio trades under the umbrella of the NewFunds Collective Investment Scheme("CIS") as a separate exchange traded fund. The Scheme is separately listed and trades onthe JSE. Thus each of the separate portfolios fall within the scope of IFRS 8: OperatingSegments. This Scheme has a narrowly defined mandate and operates a single line ofbusiness. Therefore the Scheme as a whole is considered to be one operating segment.

2.7 DISTRIBUTIONS

In accordance with the Scheme's Trust Deed, price index portfolios (of which this portfoliois one) distribute their distributable income and any other amounts determined by themanagement scheme to security holders in cash.

2.8 TAXATION

Income is taxed in the hands of the investor if the portfolio distributes within 12 months ofhaving received income, failing which income will be deemed to be received by, andaccrued to the portfolio and will be taxed in its hands. Capital gains and losses areultimately taxed in the investor’s hands on disposal of their participatory interest.

The portfolio has distributed income within 12 months of receiving it within the current andprior year. Therefore, no income tax has been provided for in the portfolio in the current andprior year.

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

2.5 CASH AND CASH EQUIVALENTS

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statementsfor the year ended 31 December 2018

21

otes 2018 2017R R

3. REVENUE

Effective Interest Income 26 002 25 452Dividend Income 1 822 612 1 310 948Real Estate Investment Income 705 700 652 767

2 554 314 1 989 167

4. DECREASE IN NET ASSETS ATTRIBUTABLE TO INVESTORS BEFOREDISTRIBUTION

Included in net assets attributable to investors before distribution are the followingsignificant transactions:

Management fee (142 591) (90 384)Trustee fees - (4 905)

5. TOTAL EXPENSE RATIO

Increased customer demand for greater transparency in financial services and therecognition thereof by the collective investment industry requires Collective InvestmentScheme managers to calculate and publish a Total Expense Ratio (TER) for each portfoliounder management. This is a requirement in terms of the Association of CollectiveInvestment Scheme (ACI) standard on the calculation and publication of TER.

The ACI Guidelines on the TERs require that a fund must be in existence for more than 6months before expense ratios can be calculated and published.

The total expense ratio by definition as expressed in the ACI standards is a measure of theportfolio's assets that were relinquished as payment for services rendered in the managementof the portfolio. This is expressed as a percentage of the fraction; total expenses paid for bya portfolio for the previous 12 months divided by the daily average net asset value for theprevious 12 months.

2018 2017% %

S&P GIVI SA Financials 0.30 0.19

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

22

6. PORTFOLIO INVESTMENTS

These financial assets are mandatorily measured at fair value through profit and loss (2018)and designated at fair value through profit and loss (2017).

In 2017, the Scheme designated all equity investments at fair value through profit and lossupon initial recognition as it manages these securities on a fair value basis in accordancewith its documented investment strategy. Internal reporting and performance measurementof these securities are on a fair value basis.

2018 2017R R

6.1 RECONCILIATION OF THE FAIR VALUE OF INVESTMENTS

Balance at 1 January 52 034 554 51 384 207Fair value adjustments (8 896 164) 231 080New issues during the year - -Rebalancing effect 184 923 419 267Balance at 31 December 43 323 313 52 034 554

6.2 RECONCILIATION OF THE NUMBER OF UNITS

Balance at 1 January 1 322 216 1 322 216New issues during the year - -Balance at 31 December 1 322 216 1 322 216

6.3 PARTICIPATION INTEREST

The Scheme is the primary issuer of participatory interests for the NewFunds CIS ETF’s.The Scheme is obliged to sell and repurchase one or more basket(s) of participatory interestsrequested or offered from or to it by investors. There is a provision that the Schemes cannever be obliged to deliver part of a basket. As participatory interests are listed on the JSE,typically, investors can buy or sell partial baskets of their participatory interests on thesecondary market (and may contact either of the participating brokers or the market makerin this regard). Partial baskets of the portfolio are traded on the secondary market as S&PGIVI SA Financials Index Securities (GIVFIN) on the JSE.

Proceeds received from the issue of S&P GIVI SA Financials Index securities are utilised tobuy S&P GIVI SA Financials baskets of selected constituents.

Net asset value per S&P GIVI SA Financials Index Security, after distributable amounts at31 December 2018 was R33.30 (31 December 2017: R40.14)

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETF PORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

23

6. PORTFOLIO INVESTMENTS (continued)

6.4 S&P GIVI SA FINANCIALS INDEX SECURITY BASKET OF CONSTITUENTS

No. of shares Cost Current price Market Value % of the fundR Cents R %

2018Financial ServicesBrait S.A. 47 463 4 289 946 3 000 1 423 890 3.29Investec Limited 41 851 4 044 948 7 900 3 306 229 7.63Investec Public Limited Company 56 386 5 197 073 7 966 4 491 709 10.37RMI Holdings Limited (RMI) 45 685 1 921 277 3 644 1 664 761 3.84Real EstateGrowthpoint Props Limited 157 764 3 998 435 2 330 3 675 901 8.48Nepi Rockcastle Public Limited Company 23 899 3 600 882 11 300 2 700 587 6.23Capital & Counties Props 36 664 2 115 551 4 235 1 552 720 3.58Hyprop Inv Limited 11 591 1 383 257 8 150 944 667 2.18Intu Properties Public Limited Company 137 613 6 578 256 2 114 2 909 139 6.71Redefine Prop Limited 279 083 3 100 448 967 2 698 733 6.23Resilient Reit Limited 27 509 2 220 617 5 700 1 568 013 3.62BanksCapitec Bank Holding 2 220 2 181 380 111 800 2 481 960 5.73InsuranceLiberty Holdings Limited 14 469 1 786 169 11 000 1 591 590 3.67MMI Holdings Limited 84 598 1 511 173 1 713 1 449 164 3.34

55 366 010 43 323 313 100.00

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETF PORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

24

6. PORTFOLIO INVESTMENTS (continued)

6.4 S&P GIVI SA FINANCIALS INDEX SECURITY BASKET OF CONSTITUENTS (continued)

No. of shares Cost Current price Market Value % of the fundR Cents R

2017Financial ServicesInvestec Limited 40 827 3 928 448 8 972 3 662 998 7.04Investec Public Limited Company 53 611 4 922 304 8 976 4 812 123 9.25RMI Holdings Limited 42 608 1 801 144 4 590 1 955 707 3.76

Industrial Goods & ServicesRemgro Limited 25 743 6 346 861 23 600 6 075 348 11.68InsuranceLiberty Holdings Limited 17 751 2 200 822 12 443 2 208 757 4.24Old Mutual Public Limited Company 304 776 11 028 907 3 800 11 581 488 22.26Investment ServicesBrait S.E. 61 437 6 897 791 4 166 2 559 465 4.92

Real EstateCapital & Counties Prop Public Limited Company 56 272 3 271 670 5 257 2 958 219 5.69Growthpoint Properties Limited 130 572 3 394 774 2 766 3 611 622 6.94Hyprop Investments Limited 9 047 1 130 108 11 730 1 061 213 2.04Intu Properties Public Limited Company 108 476 5 721 638 4 195 4 550 568 8.75Nepi Rockcastle Public Limited Company 7 312 1 371 652 21 357 1 561 624 3.00Redefine Properties Limited 209 370 2 362 326 1 070 2 240 259 4.31Resilient Real Estate Investment Trust Limited 11 207 1 433 868 15 116 1 694 050 3.26SA Corporate Real Estate Limited 179 109 955 587 481 861 514 1.66Vukile Property Fund 30 824 590 858 2 075 639 598 1.23

57 358 758 52 034 554 100.00

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

25

2018 2017R R

7. TRADE RECEIVABLES

Interest income receivable 949 1 233

8. TRADE AND OTHER PAYABLES

Trustee fees - 431Management fee 12 834 -

12 834 431

9. CASH USED IN OPERATIONS

(Decrease)/Increase in assets attributable to investors (9 048 301) 1 253 602

Adjustments for:Interest income (26 002) (25 452)Dividends income (1 822 612) (1 310 948)Real Estate Investment Income (705 700) (652 767)Fair value losses/(gains) 8 896 164 (231 080)Distribution 2 560 900 865 143Cash used in operations before working capital changes (145 551) (101 502)

Changes in working capitalIncrease/(Decrease) in trade and other payables 12 403 (201)Total changes in working capital 12 403 (201)

Cash used in operations (133 148) (101 703)

10. CASH AND CASH EQUIVALENTS

Current account 712 535 1 036 907

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

26

11. RISK MANAGEMENT

11.1 CAPITAL RISK MANAGEMENT

The Scheme monitors capital on the basis of the value of net assets attributable to investors.The Scheme's objectives when managing capital are to safeguard its ability to continue as agoing concern in order to provide returns for investors and benefits for other stakeholdersand to maintain an optimal capital structure to reduce the cost of capital. In order tomaintain or adjust the capital structure, the Scheme may adjust the amount of distributionspaid to investors. There are no externally imposed capital requirements on the Scheme.

11.2 FINANCIAL RISK MANAGEMENT

The Scheme's business involves taking on risks in a targeted manner and managing themprofessionally. The core functions of the Scheme's risk management are to identify all keyrisks for the Scheme, measure these risks, and manage the risk positions and determinecapital allocations. The Scheme regularly reviews its risk management policies and systemsto reflect changes in markets and products and best market practice.

The Scheme's aim is to achieve an appropriate balance between risk and return andminimise potential adverse effects on the Scheme's financial performance. The Schemedefines risk as the possibility of losses or profits foregone which may be caused by internalor external factors.

The risks arising from financial instruments to which the Scheme is exposed are financialrisks, which include credit risk, liquidity risk, and market risk which are discussed below.Market risk has been identified as the most significant risk to the Scheme.

With regards to the S&P GIVI SA Financials portfolio, the financial instruments consistmainly of underlying listed investments, cash and cash equivalents, trade receivables andtrade and other payables.

11.3 MARKET RISK

Market risk exists where significant changes in equity prices will affect the value of theportfolio’s index securities. The scheme's investment mandate is to passively manage theportfolio. As a result it is subjected to a similar nature and level of market risk as thebenchmark portfolio.

There is no guarantee that the Scheme's portfolios will achieve its investment objective ofperfectly tracking the index. The value of portfolio index securities and distributionspayable by the Scheme’s portfolios will rise and fall as the capital values of the underlyingsecurities housed in the portfolio and the income flowing therein fluctuates. Prospectiveinvestors should be prepared for the possibility that they may sustain a loss.

The Scheme’s portfolios may not be able to perfectly replicate the performance of an indexbecause:· The scheme is liable for certain costs and expenses not taken into account in the

calculation of the Index; this is applicable to a total return index;· Certain Index constituents may become temporarily unavailable; or· Other extraordinary circumstances may result in a deviation from precise index

weightings.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

27

11. RISK MANAGEMENT (continued)

11.3 MARKET RISK (continued)

Price Sensitivity Analysis

All the investments in portfolios of the Scheme’s portfolios are listed on the JSE. IndexSecurities are created with an objective to track the performance of specific portfolioindexes (customised indexes).

Any movement or adjustment in the specific portfolio index will have an impact on the priceof the investment in the portfolio. At any point in time the market value of one unit in theportfolio may be expected to reflect 1/1000th of the Index level plus an amount whichreflects a pro rata portion of any accrued distribution amount within the portfolio.

Actual market values may be affected by supply and demand and other market factorshowever the ability of a holder to switch out of any ETF portfolio securities by redeemingthem in specie for one or more baskets of the constituent securities should operate tosubstantially avoid or minimise any differential which may otherwise arise between therelevant basket and the value at which any portfolio securities trade from time to time.

The S&P GIVI SA Financials Index Securities investment portfolio 2018: R43 323 313(2017: R52 034 554) is affected by price fluctuations.

At reporting date a 10% increase in the value of the investment in the portfolio's securityprice would increase the index and resulting net assets attributable to investors of theportfolio by R4 332 331 (2017: R5 203 455).

At reporting date a 10% decrease in the value of the investment in the portfolio's securityprice at the reporting date would decrease the index and resulting net assets attributable toinvestors of the portfolio by R4 332 331 (2017: R5 203 455).

11.4 INVESTMENT RISK

There can be no assurance that the investment in portfolios will achieve their investmentobjectives of replicating the price and yield performance of the portfolio index securities.The net asset value of the portfolio index securities will rise and fall as the value of theunderlying portfolio fluctuates. The return achieved on portfolio index securities can beexpected to fluctuate in response to changes in the return achieved by the underlyingportfolio.

On a quarterly basis the index is adjusted to ensure that the constituent companies in theindex are the top performing companies. Thus adjustments such as removing a company thatis not performing well or a change in the weighting of the shares are performed.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

28

11.4 INVESTMENT RISK (continued)

The following factors could negatively impact on the investment performance of theportfolios:· Certain costs and expenses incurred by the portfolio could cause the underlying

portfolio to mistrack against the Index;· Temporary unavailability of securities in the secondary market or other extraordinary

circumstances could cause deviations from the exact weightings of the Index;· In circumstances where securities comprising the Index are suspended from trading or

other market disruptions occur it may be impossible to rebalance the portfolio ofsecurities held by the portfolio and this may lead to tracking error.

11.5 SECONDARY TRADING RISK

There can be no guarantee that the portfolio index securities will remain listed on the JSELimited. Despite the presence of market makers the liquidity of the portfolio index securitiescannot be guaranteed. The portfolio index securities may trade at a discount or premium totheir net asset value. Any termination of a listing would be subject to the JSE LimitedListing Requirements.

11.6 INTEREST RATE RISK

Interest rate risk arises from the effects of fluctuations in the prevailing levels of marketinterest rates on the fair value of financial assets and liabilities and future cash flows.

Interest Rate Sensitivity

The cash balances within the portfolio R712 535 (2017: R1 036 907) are affected by interestrate fluctuations

At reporting date a 1% decrease in the interest rate would decrease the profit of the portfolioby R7 125 (2017: R10 369).

At reporting date a 1% increase in the interest rate would increase the profit of the portfolioby R7 125 (2017: R10 369).

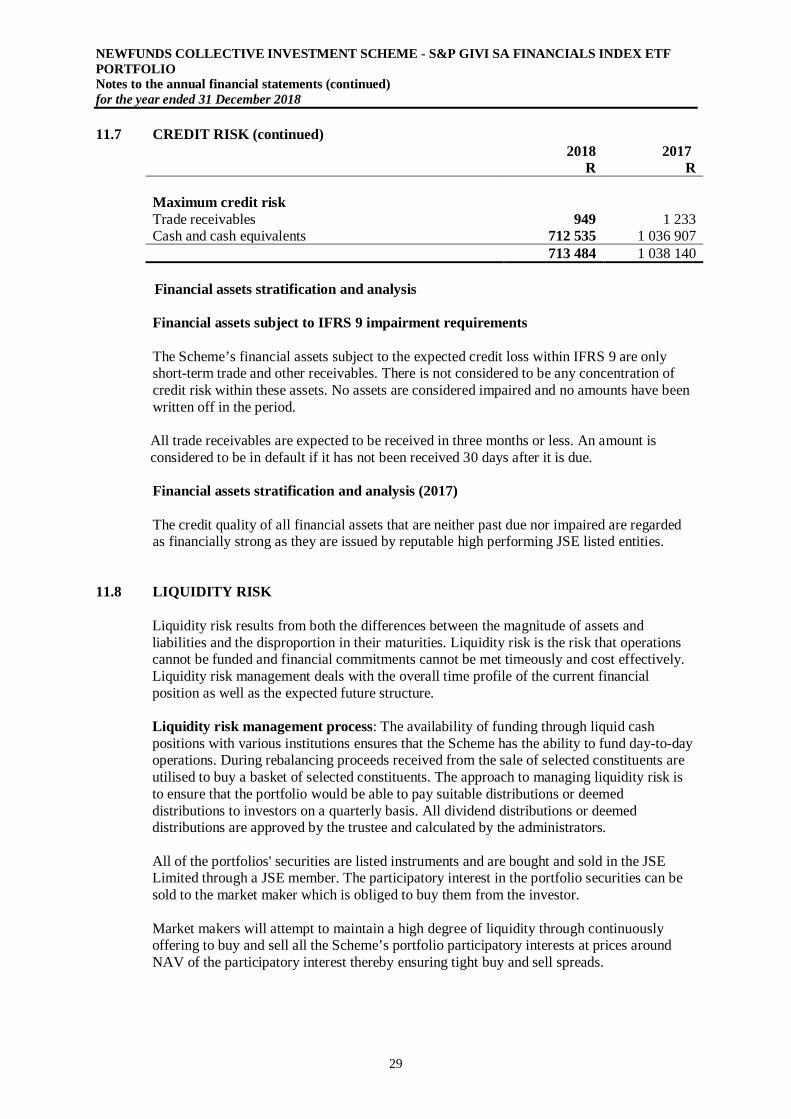

11.7 CREDIT RISK

Credit risk is the risk of financial loss to the Scheme if a party to a financial instrument failsto meet its contractual obligations resulting in a financial loss to the scheme. Credit riskarises from trade receivables and cash and cash equivalents. The carrying amounts of tradereceivables and cash and cash equivalents represent the maximum exposure.

Risk limits control and mitigation policies: The credit risk relating to the trade receivablesis limited as it relates mainly to interest income receivable on cash balances held withreputable financial institutions and dividend receivable from listed securities.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

29

Financial assets stratification and analysis

Financial assets subject to IFRS 9 impairment requirements

The Scheme’s financial assets subject to the expected credit loss within IFRS 9 are onlyshort-term trade and other receivables. There is not considered to be any concentration ofcredit risk within these assets. No assets are considered impaired and no amounts have beenwritten off in the period.

All trade receivables are expected to be received in three months or less. An amount isconsidered to be in default if it has not been received 30 days after it is due.

Financial assets stratification and analysis (2017)

The credit quality of all financial assets that are neither past due nor impaired are regardedas financially strong as they are issued by reputable high performing JSE listed entities.

11.8 LIQUIDITY RISK

Liquidity risk results from both the differences between the magnitude of assets andliabilities and the disproportion in their maturities. Liquidity risk is the risk that operationscannot be funded and financial commitments cannot be met timeously and cost effectively.Liquidity risk management deals with the overall time profile of the current financialposition as well as the expected future structure.

Liquidity risk management process: The availability of funding through liquid cashpositions with various institutions ensures that the Scheme has the ability to fund day-to-dayoperations. During rebalancing proceeds received from the sale of selected constituents areutilised to buy a basket of selected constituents. The approach to managing liquidity risk isto ensure that the portfolio would be able to pay suitable distributions or deemeddistributions to investors on a quarterly basis. All dividend distributions or deemeddistributions are approved by the trustee and calculated by the administrators.

All of the portfolios' securities are listed instruments and are bought and sold in the JSELimited through a JSE member. The participatory interest in the portfolio securities can besold to the market maker which is obliged to buy them from the investor.

Market makers will attempt to maintain a high degree of liquidity through continuouslyoffering to buy and sell all the Scheme’s portfolio participatory interests at prices aroundNAV of the participatory interest thereby ensuring tight buy and sell spreads.

11.7 CREDIT RISK (continued)2018 2017

R R

Maximum credit riskTrade receivables 949 1 233Cash and cash equivalents 712 535 1 036 907

713 484 1 038 140

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

30

11. RISK MANAGEMENT (continued)

11.8 LIQUIDITY RISK (continued)

Under normal circumstances and conditions the investor will be able to buy or sell theportfolio securities from the market makers.Per the Trust Deed the managing Scheme can sell the underlying portfolio assets to meetany short or long term obligation and can borrow up to 10% of the market value of theunderlying assets.

The following tables represent the maturity analysis of the financial liabilities:

On demand 0-12 months TotalR R R

2018Trade and other payables - 12 834 12 834S&P GIVI SA Financial Index Securities 44 023 963 - 44 023 963

44 023 963 12 834 44 036 797

2017Trade and other payables - 431 431S&P GIVI SA Financial Index Securities 53 072 263 - 53 072 263

53 072 263 431 53 072 694

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

31

12. FAIR VALUE HIERARCHY OF ASSETS AND LIABILITIES HELD AT FAIRVALUE

12.1 FAIR VALUE HIERARCHY

The table below provides an analysis of financial instruments that are measured subsequent toinitial recognition at fair value grouped into Levels 1 to 3 based on the degree to which the fairvalue is observable.

Level 1 fair value measurements are those derived from quoted prices (unadjusted) in activemarkets for identical assets or liabilities.

Level 2 fair value measurements are those derived from quoted prices in active markets andinputs other than quoted prices included within Level 1 that are observable for the asset orliability, either directly (i.e. as prices) or indirectly (i.e. derived from prices).

Level 3 fair value measurements are those derived from valuation techniques that includeinputs for the asset or liability that are not based on observable market data (unobservableinputs).

The table below shows the portfolio's financial instruments that are recognised andsubsequently measured at fair value analysed by level of the fair value hierarchy. Theclassification of instruments is based on the lowest level input that is significant to the fairvalue measurement in its entirety. All the fair values disclosed are recurring fair valuemeasurements.

The table below sets out the fair value of Level 1 and Level 2 financial instruments:

Level 1 Level 2 Level 3R R R

2018Recurring fair value measurementsFinancial InstrumentsMandatorily measured at Fair Value Through Profit and LossInvestment in listed shares 43 323 313Net assets attributable to investors (44 023 963)

43 323 313 (44 023 963)

2017Recurring fair value measurementsFinancial InstrumentsDesignated as at Fair Value Through Profit and LossInvestment in listed shares 52 034 554Net assets attributable to investors (53 072 263)

52 034 554 (53 072 263)

The valuation technique applied in order to value Level 2 financial instruments is the NetAsset Value which is linked to the price of the underlying market traded instruments.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

32

12. FAIR VALUE HIERARCHY OF ASSETS AND LIABILITIES HELD AT FAIRVALUE (continued)

12.2 FAIR VALUE VERSUS CARRYING AMOUNT OF FINANCIAL INSTRUMENTSNOT HELD AT FAIR VALUE

The fair value of the cash and cash equivalents, trade and other receivables and trade and otherpayables approximates the carrying value because the instruments are short term in nature.There has been no change in fair values as a result of a change in credit risk.

13. SEGMENTAL REPORTING

The investment vehicle offers only one product being the specific exchange traded fundtracking the specific identified index.

Information regarding the results of the reportable segment is disclosed in the financialstatements as currently set out thus no further IFRS 8 disclosure is required.

14. RELATED PARTIES

NewFunds (RF) Proprietary Limited, a subsidiary of Absa Bank Limited has beenestablished to act as an agent for all management and administrative services in respect ofthe Scheme’s portfolios. The fees payable to them have been included in management andadministration expenses.

The Standard Bank of South Africa Limited is the trustee of the Scheme at a contractuallyagreed amount and is remunerated for services.

Ultimate holding company: Absa Group Limited.

Key Management Personnel

The Scheme's key management personnel are the trustees listed in the Trustee’s Report andthe directors of NewFunds (RF) Proprietary Limited who act as an agent for all managementand administrative services in respect of NewFunds CIS portfolios.

Other than trustee fees and management fees paid to Standard Bank of South Africa andNewFunds (RF) Proprietary Limited there were no material transactions with keymanagement personnel or their families during the year.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETF PORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

33

14. RELATED PARTIES (continued)

Admin andmanagement

fees paid

DistributionPaid for

ParticipatoryInterest Held

InterestIncome

Cash andCash

EquivalentsTrade

Receivables

Trade andOther

PayablesParticipatoryInterest Held

R R R R R R R

2018NewFunds (RF) Proprietary Limited# (142 591) - - - - (12 834) -Absa Group Limited - (1 909 196) - - - - (32 895 278)Standard Bank of South AfricaLimited (3 390) - 26 002 712 535 949 - -

2017NewFunds (RF) Proprietary Limited (90 384) - - - - - -Absa Group Limited* - (551 758) - - - - (38 419 320)Standard Bank of South AfricaLimited (10 681) - 25 452 1 036 907 1 233 - -

*Absa Group Limited previously Barclays Africa Group Limited# In 2018 Trustee fees incurred are paid by NewFunds (RF) Proprietary Limited

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

34

15. DISTRIBUTIONS

The Index Securities will effect quarterly distributions after paying all the accrued expensesof the NewFunds Collective Investment Scheme. All distributions are made out of theincome of each ETF portfolio.

The quarterly record dates are 26 April 2018, 20 July 2018, 19 October 2018 and 25 January2019. Holders of the ETF securities (“investors”) recorded in the register on the belowrecord dates were entitled to the respective distribution declared.

During the period under review the following distributions were affected by the Scheme:

2018 2017R R

2018: 52.94 cents per security declared 18 January 2018and reinvested on 29 January 2018

700 000 -

2018: 13.26 cents per security declared 18 April 2018 andpaid on 30 April 2018(2017 : 8.70 cents per security declared on 13 April 2017and paid 20 April 2017)

175 300 115 000

2018 : 43.81 cents per security declared 12 July 2018 andpaid on 23 July 2018(2017 : 37.83 cents per security declared on 13 July 2017and paid 18 July 2017)

579 300

500 143

2018 : 83.67 cents per security declared 11 October 2018and paid on 22 October 2018(2017 : 18.91 cents per security declared on 19 October2017 and paid 24 October 2017)

1 106 300 250 000

2 560 900 865 143

Distributions declared after year end:

2019 : 39.38 cents per security declared 17 January 2019and paid on 28 January 2019(2018: 52.94 cents per security declared 18 January 2018and reinvested on 29 January 2018)

520 700 700 000

3 081 600 865 143

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

35

16. QUARTERLY REVIEW OF PORTFOLIO PRICES

31March(cents)

30 June(cents)

30September

(cents)

31December

(cents)

2018S&P GIVI SA Financials Index Securities 3 761 3 691 3 683 3 329

2017S&P GIVI SA Financials Index Securities 3 879 3 809 3 824 4 014

17. TRANSITION – IFRS 9

The Scheme applied for the first time IFRS 9 Financial Instruments (IFRS 9) which is effectivefor annual periods beginning on or after 1 January 2018.

The Scheme adopted IFRS 9 Financial Instruments on its effective date of 1 January 2018.IFRS 9 replaces IAS 39 Financial Instruments: Recognition and Measurement and introducesnew requirements for classification and measurement impairment and hedge accounting. IFRS9 is not applicable to items that have already been derecognised at 1 January 2018, the date ofinitial application.

(a) Classification and measurement

The Scheme has assessed the classification of financial instruments as at the date of initialapplication and has applied such classification retrospectively. Based on that assessment:

All financial assets previously held at fair value continue to be measured at fair value;

Debt instruments and equity instruments are acquired for the purpose of generating short-termprofit. Therefore they meet the held-for-trading criteria and are required to be measured at FairValue through Profit and Loss (FVPL);

Financial assets previously classified as loans and receivables are held to collect contractualcash flows and give rise to cash flows representing solely payments of principal and interest.Thus such instruments continue to be measured at amortised cost under IFRS 9.

The classification of financial liabilities under IFRS 9 remains broadly the same as under IAS39. The main impact on measurement from the classification of liabilities under IFRS 9 relatesto the element of gains or losses for financial liabilities designated as at FVPL (Fair Valuethrough Profit or Loss) attributable to changes in credit risk. IFRS 9 requires that such elementbe recognised in other comprehensive income (OCI) unless this treatment creates or enlarges anaccounting mismatch in profit or loss in which case all gains and losses on that liability(including the effects of changes in credit risk) should be presented in profit or loss. TheScheme has designated financial liabilities at FVPL. This was negligible in the current period.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

36

17. TRANSITION – IFRS 9 (continued)

(b) Impairment

IFRS 9 requires the Scheme to record expected credit losses (ECLs) on all of its loans and tradereceivables either on a 12-month or lifetime basis. The Scheme only holds trade receivableswith no financing component and that have maturities of less than 12 months at amortised cost.These requirements have not had a material impact on the financial statements.

Impact of adoption of IFRS 9

The classification and measurement requirements of IFRS 9 have been adopted retrospectivelyas of the date of initial application on 1 January 2018. However, the Scheme has chosen to takeadvantage of the option not to restate comparatives. Therefore, the 2017 figures are presentedand measured under IAS 39. The following table shows the original measurement categories inaccordance with IAS 39 and the new measurement categories under IFRS 9 for the Scheme’sfinancial assets and financial liabilities as at 1 January 2018:

Financial Assets1 January 2018 IAS 39

classificationIAS 39Measurement

IFRS 9classification

IFRS 9measurement

Portfolio Investments Designated at FVPL 52 034 554 Mandatorily atFVPL

52 034 554

Cash and CashEquivalents

Loans andReceivables

1 036 907 Amortised cost 1 036 907

Trade and otherreceivables

Loans andReceivables

1 233 Amortised cost 1 233

Financial Liabilities1 January 2018 IAS 39

classificationIAS 39Measurement

IFRS 9classification

IFRS 9measurement

Trade and other payables Amortised cost 431 Amortised cost 431Net Assets attributable toinvestors

FVPL 53 072 263 FVPL 53 072 263

In line with the characteristics of the Fund’s financial instruments as well as its approach totheir management the Fund neither revoked nor made any new designations on the date ofinitial application. IFRS 9 has not resulted in changes in the carrying amount of the Fund'sfinancial instruments due to changes in measurement categories. All financial assets that wereclassified as FVPL under IAS 39 are still classified as FVPL under IFRS 9.

In addition the application of the ECL model under IFRS 9 has not significantly changed thecarrying amounts of the Scheme's amortised cost financial assets.

The carrying amounts of amortised cost instruments continued to approximate theseinstruments' fair values on the date of transition after transitioning to IFRS 9.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

37

18. EVENTS AFTER THE REPORTING DATE

Distributions occurred post year end, refer to Note 15.016 : 13.84 cents per security announced 16 anuary 2017)

19. NEW ACCOUNTING PRONOUNCEMENTS

Adoption of new and revised StandardsDuring the current period, the Scheme has adopted all of the new and revised standards andinterpretations issued by the IASB and the IFRIC that are relevant to its operations andeffective for annual reporting periods beginning on 01 January 2018. Apart from the detailincluded in note 17 the adoption of these new and revised standards and interpretations hasnot resulted in material changes to the Scheme's accounting policies.

The Scheme adopted the following standard’s interpretations and amended standards duringthe reporting year ended 31 December 2018:

IFRS 9 Financial Instruments introduces significant changes to three fundamentalareas of the accounting for financial instruments namely: The classificationand measurement of financial instruments; the scope and calculation ofcredit losses which has moved from an incurred loss to an expected creditloss (ECL) approach; and the hedge accounting model.

IFRS 9 prescribes the classification of financial assets on the basis of anentity’s business model for managing the instrument as well as thecontractual cash flow characteristics. The accounting for financialliabilities remains largely unchanged except for financial liabilitiesdesignated at fair value through profit or loss (FVPL). Gains and losses onsuch financial liabilities are required to be presented in OCI to the extentthat they relate to changes in own credit risk. This was negligible in thecurrent reporting period.

The Scheme has elected to not restate its comparative information aspermitted by IFRS 9. Accordingly the impact of IFRS 9 has been appliedretrospectively with an adjustment to the Schemes’ opening retainedearnings on 1 January 2018. Therefore comparative information in theprior period annual financial statements will not be amended for the impactof IFRS 9. The net impact to opening retained earnings was nil, refer toNote 17.

IFRS 15 Revenue from Contracts with Customers replaces the previous revenuerecognition standards and interpretations including IAS 18 Revenue andIFRIC 13 Customer Loyalty Programmes. IFRS 15 establishes a singleapproach for the recognition and measurement of revenue and requires anentity to recognise revenue as performance obligations are satisfied. Itapplies to all contracts with customers except for transactions specificallyscoped out which includes interest, dividends, leases and insurancecontracts. Therefore, adoption of the standard has no significant impact.

NEWFUNDS COLLECTIVE INVESTMENT SCHEME - S&P GIVI SA FINANCIALS INDEX ETFPORTFOLIONotes to the annual financial statements (continued)for the year ended 31 December 2018

38

IAS 1 Presentation of Financial Statements – Amendments requiring interestrevenue which is calculated using the effective interest method to bepresented separately on the face of the statement of comprehensive income.This only includes interest earned on financial assets measured atamortised cost or at FVOCI.

IAS 1 andIAS 8

Presentation of Financial Statements and Accounting Policies Changes inEstimates and Errors – Amendments regarding the definition of materialin order to better clarify how materiality should be applied as well as toalign the definition across IFRS. The new definition states that“information is material if omitting misstating or obscuring it couldreasonably be expected to influence decisions that the primary users ofgeneral purpose financial statements make on the basis of those financialstatements which provide financial information about a specific reportingentity.”

The amendments to the definition:· Explain that information is obscured if it is communicated in a way

that would have a similar effect as omitting or misstating theinformation and include examples of circumstances that mayresult in material information being obscured;

· Clarify that assessing materiality needs to take into account howprimary users could reasonably be expected to be influenced inmaking economic decisions; and

· Refer to primary users in order to respond to concerns that the termusers may be interpreted too widely.

The amendments are effective for reporting periods beginning 1 January2020 and are required to be applied prospectively. The Scheme hashowever elected to early adopt the amendments as they allow for anenhanced understanding of the materiality requirements.

New and revised International Financial Reporting Standards issued not yet effectiveAt the date of authorisation of these financial statements, the following standards andinterpretations were in issue but not yet effective:

Standard

Annual periodsbeginning on orafter

IFRIC 23 Uncertainty Over Income Tax Treatments - Interpretationclarifying the accounting for uncertainties in income taxes.The adoption of IFRIC 23 is not expected to have asignificant impact on the scheme.

1 January 2019

Apart from the instances detailed above the Scheme is in the process of assessing thepotential impact that the adoption of these standards and interpretations may have on itsfuture financial performance or disclosures in the annual financial statements.