PREFACE AND ACKNOWLEDGEMENTS - Erasmus ... R.R.H. (343922).docx · Web viewThis paper investigates...

71

ERASMUS UNIVERSITY ROTTERDAM ERASMUS SCHOOL OF ECONOMICS MSc Economics & Business Master Specialisation Financial Economics Assessment of the Relationship Between Stock Prices And Oil Prices: An Investigation of the Japanese Automobile Manufacturers 1

Transcript of PREFACE AND ACKNOWLEDGEMENTS - Erasmus ... R.R.H. (343922).docx · Web viewThis paper investigates...

ERASMUS UNIVERSITY ROTTERDAMERASMUS SCHOOL OF ECONOMICSMSc Economics & BusinessMaster Specialisation Financial Economics

Assessment of the Relationship Between Stock Prices And Oil Prices: An Investigation of the Japanese Automobile Manufacturers

Author: R.R.H.LamhotStudent number: 343922ARThesis supervisor: Mehtap Kilic MSc LLMFinish date: August 4, 2011

1

PREFACE AND ACKNOWLEDGEMENTS

This thesis is about the influences of high oil prices on stock prices. I choose to combine economics with

a energy since I am interested in this topic. Moreover, I am interested in the automotive industries so that

it is interesting for me to analyze their performance. I have to finish my thesis to obtain my master degree

in Erasmus School of Economics. Without help and support that are given to me, this thesis would not be

perfectly done. Therefore, I would like to acknowledge for several individuals that offered their

comments and insights on my research. I wish to thank to my thesis supervisor Mehtap Kilic for her

feedbacks and spares her time during my thesis. My special thanks to my family in Indonesia who always

support me everytime while finishing my thesis. I would like to thank to Wienda Ayu Pramithasari for her

support that are given to me. I also would like to acknowledge to Rachel Liong who helps me finding the

data and helping about the statistics. I dedicate the best paper that I have ever done to them.

“He has made everything beautiful in its time. He has also set the eternity in the human heart; yet, no one can fathom what God has done from beginning to end”

NON-PLAGIARISM STATEMENTBy submitting this thesis the author declares to have written this thesis completely by himself/herself, and not to have used sources or resources other than the ones mentioned. All sources used, quotes and citations that were literally taken from publications, or that were in close accordance with the meaning of those publications, are indicated as such.

COPYRIGHT STATEMENTThe author has copyright of this thesis, but also acknowledges the intellectual copyright of contributions made by the thesis supervisor, which may include important research ideas and data. Author and thesis supervisor will have made clear agreements about issues such as confidentiality.

Electronic versions of the thesis are in principle available for inclusion in any EUR thesis database and repository, such as the Master Thesis Repository of the Erasmus University Rotterdam

2

ABSTRACT

This paper investigates the relationship between stock prices of Japanese automobile manufacturers and

crude oil prices. The thesis gives an idea how well the manufacturers perform while oil prices remains

volatile and to what extend oil prices should be looked as a crucial benchmark for Japanese auto industry

managers. A Fama and French three factor model which will extend to four factor of oil is used as

methodology to study its influence on stock returns of Japanese automobile industries. The results exhibit

that oil prices have a non-linear relationship with stock prices of Japanese auto companies. Surprisingly,

the results were positive during the occurence of Iraq invasion 2003. Furthermore, the boom in sales sales

of hybrid cars positively influence on stock prices of hybrid automakers when the recent rise in crude oil

prices.

Keywords: [Oil prices, Fama-French, Japan, Automobile manufacturers, Hybrid Cars]http://www.aeaweb.org/journal/jel_class_system.html ]

3

Table of ContentsPREFACE AND ACKNOWLEDGEMENTS........................................................................................2

ABSTRACT............................................................................................................................................3

LIST OF TABLES..................................................................................................................................5

LIST OF FIGURES.................................................................................................................................6

1. Introduction.........................................................................................................................................7

2. Literature Review..............................................................................................................................10

2.1. Oil prices and the economic growth...........................................................................................10

2.2. Oil prices and the stock market..................................................................................................11

2.3. Fama French three factor model................................................................................................13

3. Research Motivation..........................................................................................................................15

4. Hypothesis.........................................................................................................................................18

5. Data and Methodology......................................................................................................................20

5.1. Data Description.........................................................................................................................20

5.2. Methodology..............................................................................................................................22

6. Results...............................................................................................................................................27

6.1. Descriptive Statistics..................................................................................................................27

6.2. Regression Results.....................................................................................................................29

6.3. The Influence of the Hybrid Car................................................................................................32

7. Analyses and Interpretations.............................................................................................................35

7.1. Unusual events as external factors.............................................................................................35

7.2. Hybrid cars as an internal factor................................................................................................37

8. Conclusions.......................................................................................................................................40

REFERENCES......................................................................................................................................42

4

LIST OF TABLES

Table 1: Market shares of the top automobile manufacturers from 2007 to 2010.......................................16

Table 2: Toyota total sales of hybrid cars in Japan during fiscal year 2000–2010 (in thousand)...............21

Table 3 : Time Phases for Iraq war, credit crisis, and booming sales of hybrid car....................................22

Table 4 : Summary statistics – full sample..................................................................................................27

Table 5: Correlations – full sample..............................................................................................................28

Table 6: Regression results for the auto index............................................................................................30

Table 7: Hybrid car index............................................................................................................................33

Table 8: Regression results of Toyota index...............................................................................................34

Table 9: Regression results of Honda index................................................................................................34

Table 10: Regression results of Toyota and Honda after booming till before the earthquake....................34

5

LIST OF FIGURES

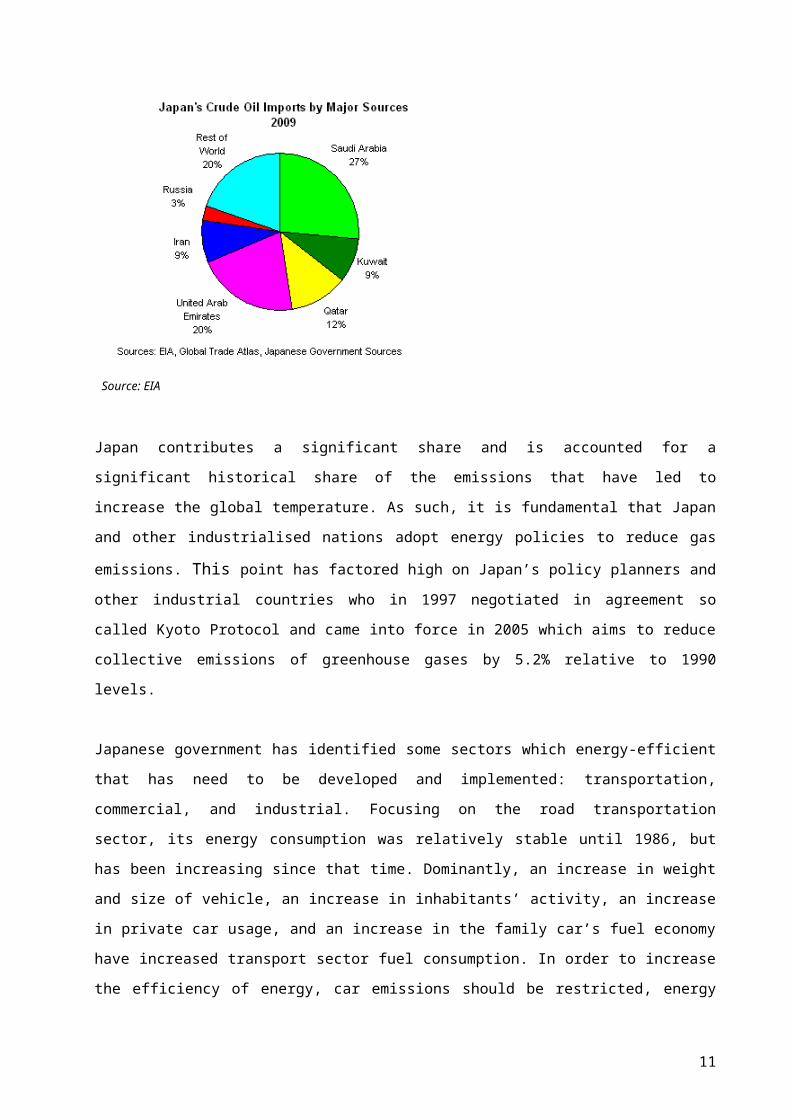

Figure 1: Major sources of crude oil imports by Japan.................................................................................8

Figure 2: Dubai crude oil price from 2001-2011.........................................................................................26

Figure 3: Returns on the market index.........................................................................................................28

Figure 4: Returns on the auto index.............................................................................................................29

6

1. Introduction

The world is dismal by recent histories. Ever since the credit crisis which was triggered by a liquidity

shortfall in the USA banking system, most of predominant economies for both developed and developing

countries were drowned in times of recession. This crisis is the worst tragedy since the great depression of

1929. Oil shocks have also contributed to global recessions in last thirty years. While the recent topic in

news was regarding on political instabilities in the Egypt, this has aggravated the problems facing the

global economy. The political risk weakens the value currency of the developing countries and moreover

affects commodity prices. Out of the major commodities, crude oil is a sensitive commodity. Oil is a

source of energy which is used in many routine activities of households or industries. It is used either as a

raw material for various industries or consumed by the product of these industries which are proxy by

energy prices and transportation prices respectively. Both prices influence cash flow and profitability

where linked to the price of oil. Therefore, for all these reasons oil shocks and its relationship to the

global economy receive important consideration on macroeconomic research.

The upsurge in the oil prices plays an important role which it would negatively affect the performance of

automotive manufacturers (see for example Boudette and White, 2005 and Cameron and Schnusenberg,

2008). Richard Heinberg states that oil provides 97 percent of the transportation fuels that operate the

vehicles in the nation’s highway. Thus, the increase in the oil prices also affect the type of vehicles

demanded by the customer and the way those vehicles are designed. Consumers demand for more fuel

vehicles seem reasonable as the oil prices continue to rise. The upsurge in the oil prices undoubtfully

affects the profit margin of the companies. The auto manufacturers clearly concern fuel efficient cars

because the automakers compete with each other to fullfill the consumers’ demands for more fuel

efficient consumer conscious at reasonable price. While apart of the realization increased consumer

demand for efficient vehicles, an investigation of the relationship between stock prices and oil prices of

Japanese automobile manufacturers is also valuable.

The economy of Japan is the third largest in the world ($5.391 trillion) in terms of GDP and Purchasing

Power Parity. However, Koike et al (2008) shows that Japan has limited domestic oil reserves.

Consequently, Japan’s industrial sector relies heavily on overseas supplies and must import substantial

amount of crude oil and natural gas. In 2009, Japan ranked second in terms of oil imported which came

mainly from Middle East. Because of the country’s lack of domestic oil reserves, the Japanese oil

companies have sought in participation in exploration and overseas oil production primarily located in the

Middle East and South East Asia.

7

Figure 1: Major sources of crude oil imports by Japan

Source: EIA

Japan contributes a significant share and is accounted for a significant historical share of the emissions

that have led to increase the global temperature. As such, it is fundamental that Japan and other

industrialised nations adopt energy policies to reduce gas emissions. This point has factored high on

Japan’s policy planners and other industrial countries who in 1997 negotiated in agreement so called

Kyoto Protocol and came into force in 2005 which aims to reduce collective emissions of greenhouse

gases by 5.2% relative to 1990 levels.

Japanese government has identified some sectors which energy-efficient that has need to be developed

and implemented: transportation, commercial, and industrial. Focusing on the road transportation sector,

its energy consumption was relatively stable until 1986, but has been increasing since that time.

Dominantly, an increase in weight and size of vehicle, an increase in inhabitants’ activity, an increase in

private car usage, and an increase in the family car’s fuel economy have increased transport sector fuel

consumption. In order to increase the efficiency of energy, car emissions should be restricted, energy

efficient vehicle should be initiated, and car travel should be shifted to public transport. Separately, fuel

prices in Japan is tremendously expensive because gasoline is high taxed. Furthermore, by bearing high

tax, the authorities may help to reduce greenhouse emissions and participate to combat climate change.

The purpose of this paper to investigate the relationship between crude oil prices and stock prices of

Japanese automobile manufacturers. The returns will give an idea how well the automobile manufacturers

perform while crude oil prices remain instable which have an effect on the profitablity of the stock prices’

of automobile manufacturers. Secondly, if whether oil prices should be considered as crucial benchmark

for Japanese auto industry managers and Japanese policy authorities. This paper will use Fama and

8

French three factor model which will extend to four factor of oil is included to study its influence on the

stock returns of Japanese automobile industries.

The thesis is divided into eight chapters. In chapter 2, a literature study is conducted. I will concentrate on

some literature which has been written on this particular topic. Many research has been done in the sector

of impacts of oil prices on the stock prices to which we will refer during the thesis and use those papers as

references. Chapter 3 explains the motivation to conduct the research. It gives specific details about

Japanese market and current situation in there. In chapter 4, four hypotheses are conducted for our

research. Some unusual events as external factors are tested in order to know whether they influence the

relationship between the stock price and the oil price. Furthermore, we would like to conduct research

whether an internal factor such as booming sales of hybrid cars effect the relationship in the midst

upsurge in crude oil price.

Chapter 5 covers the research methodology part of the paper. The research is conducted based on the

Cameron and Schnusenberg (2008) model. In this chapter, I examine how to construct all these regression

variables. The auto index is constructed by taking price weighted average daily stock prices. The market

index is conducted with data of the TOPIX index within a time range from December, 29 2000 until

March 31, 2011. The TOPIX index is chosen because it is an important index for the Tokyo Stock

Exchange (TSE) in Japan. The SMB and the HML are constructed based on the formula from Ken and

French’s website. The oil index is calculated with data of the Middle East crude oil price. The net

producers of the Middle East crude oil determine the export price of crude oil for Japan on the basis of the

spot price for Dubai crude oil.

In chapter 6, the results of the regression are showed and, furthermore, interpret the results in the text.

Chapter 7 presents some discussions about the result are given and I synchronize the regression results

under the real circumstances. Furthermore, we serve some conclusion which is served in chapter 8.

9

2. Literature Review

2.1. Oil prices and the economic growth

Among the extreme supply shocks impacting the world economies, since the 1970s there has been a sharp

increase in the price of oil. Hamilton (1983) stated that oil supply shocks were a contributing factor to the

recession in the USA. Kim et al. (1992) also supported the research suggesting that these shocks had

played a significant role with regards to economic fluctuations over the past three decades. However,

Hooker’s (1996) contribution only showed its relationship specifically when oil prices failed to Granger

cause macroeconomic variables when data samples were extended past the mid-1980s. This was due to

the decreasing nominal price in 1981, followed by a market collapse in 1985 which the relationship

between the increase in oil and economic fluctuations seemed less convincing. This instability problem

has been investigated by several authors such as Mork (1994) and Hamilton (1996). They argued that a

breakdown of the oil prices-macroeconomics relationship reveals a non-linear relationship, thus

proposing an alternative so-called asymmetric relationship. Cunado et al. (2003) used this transformation

to investigate the oil price-economic growth relationship within some European and Asian countries.

Hamilton (2003) declared that since the oil prices and macroeconomics relationship is non-linear, the

effect of oil price increases is bigger than oil price decreases. Furthermore, Hamilton developed a flexible

approach for capturing the relationship between oil price shocks and economic growth in post-war US

data.

Many papers have investigated the relationship between price of oil and economic growth in Japan. Early

studies involved linear relationship models. Darby (1982) estimated the long run oil effects in 1975 and a

year after. The results attributed to a decrease in real income relative to the increase in oil price.

Burbridge and Harrison (1984) used a seven–variable auto regressive (VAR) model to investigate the

response of industrial production to an oil price shock from 1976-1982. However, various recent studies

have shifted to non-linear studies for investigating the relationship between oil price and economic

growth. Mork (1994) pioneered a non-linear study and investigated the existence of asymmetry in the

relationship between oil prices and economic growth in Japan. Lee et al. (2001) argued that

approximately around 30% to 50% of the negative impacts on Japanese output in the mid 1970s were

triggered by monetary policies after the oil price shocks. Rodriguez and Sanchez (2005) used a seven-

variable autoregressive (VAR) model to estimate the linkage between the GDP and the oil price shocks

that occured from 1972-2001. They found a negative correlation between oil prices and the Japanese

GDP. Cunado and Garcia (2005) analyzed the granger-causality between oil prices and macroeconomic

variables (economic growth and inflation) for six Asian countries over the period 1975-2002. They

summarized that oil prices have a significant effect on both macroeconomic activities, even though the

impact is limited to the short run and is more significant if oil price shocks are defined in local currencies.

10

They also examined a net exporter (Malaysia) and net importers (Japan, Singapore, South Korea,

Thailand, and Phillipines) to see whether an oil price-macroeconomy relationship in emerging Asian

countries is dependent on the difference between net import and net export behaviors of each country. In

addition, Hanabusa (2009) investigated the price of oil is useful in predicting in economic growth rate in

Japan. The change in the oil price can give information for the domestic economy.

As has been suggested, oil prices influence the macroeconomic variable. This impact is perceived

sequentially by major industries in the local as well as global economy. There are some industries which

use oil as an input (e.g. petroleum refinery and chemical industry), and there are those which use oil as an

output (e.g. petroleum industry). Thus, the shocks can either present itself in the supply side or the

demand side. Lee and Ni (2002) investigated the effects of oil price shocks on supply and demand in 14

manufacturing industries. Using VAR models, they indicated that where industries using oil as an input,

oil price shocks severely reduced supply. In other industries (e.g. automobile industry) the contrary

occurred where oil price shocks reduced demand. This study was expanded by Rodriguez (2008), who

examined the dynamic effects of oil price shocks on outputs of manufacturing industries in six OECD

countries. The results demonstrated that the industrial outputs of France, Germany, Italy, and Spain had a

diverse pattern of responses to oil price shocks, yet they were widely similar in the UK and the USA.

2.2. Oil prices and the stock market

Apart from the studies revealing that oil price shocks have a significant impact on an economy’s

performance, relatively few economists have provided market participants with a framework that

identifies how oil-price changes affect the stock market. Jones et al. (1996) gave a theoretical grounding,

suggesting that oil price shocks affect stock market returns through their expected earnings. They focused

on testing the reaction of advanced stock markets (US, UK, Japan, and Canada) to oil price shocks on the

basis of the standard cash flow dividend valuation model. They found that for the US and Canada, the

reaction can be ascertained by the impact of oil shocks on cash flow. The outcome for Japan and the UK

on the other hand were indecisive. Huang et al. (1996) adjusted an unrestricted VAR model, which

confirmed that a significant relationship between some US oil company stock returns and oil price

changes. However, they found no evidence of a relationship between oil prices and the S&P 500 market.

Sadorsky (2001) used a multifactor market model and considered the risk premium, exchange rates, and

interest rates, along with oil prices themselves, as major determinants of oil and gas stock returns. He

reported a statistically significant positive relationship between oil prices and stock returns of oil and gas

firms. El Sharif et al. (2005) investigated the correlation between oil prices and stock returns of

companies that listed on the London Stock Exchange. Through the empirical findings they found that

there was a significant positive association between oil prices and oil-related stock returns.

11

Notably, stock prices exhibit asymmetrically to changes in oil prices. This means that higher oil prices are

negatively related with stock prices. For example, Papapetrou (2001) studied the dynamic interaction

between oil price, real stock prices, and interest rates in Greece. Papapetrou found that oil price shocks

have a negative impact on stock prices since they negatively affect the output in the form of industrial

production and employment growth. Maghyereh et al. (2007) found that oil prices affected the stock

prices indexed in the GCC (Gulf Cooperation Council) countries, in a nonlinear fashion, and supported

the statistical analysis of a non-linear modeling relationship between oil prices and the economy. This

result was also consistent with the outcome from Mork et al. (1994). Nandha and Faff (2008) argued that

oil price shocks can have adverse effects on a firm’s output, and therefore on a firm’s profitability and

also revealed that increases in oil prices negatively impact stock returns for all industries including

mining, oil, and gas industries. Furthermore, Bjornland (2008) denoted that oil prices may affect stock

prices only through an indirect manner via monetary policy shocks, whilst Cong et al. (2008) found

evidence that oil prices do not show significantly impact on the majority of stocks in the Chinese markets.

They did however find an association within the manufacturing sector.

The above results indicate a positive or a negative relationship between oil price shocks and stock returns,

which should come as no surprise. Understandably, it is confirmed that the price enhances the cash flow

of oil firms and proves beneficial for them. More precisely, there was Park and Ratti’s (2008) detailed

study on the effects of oil shocks on stock markets in the US and 13 European countries, using monthly

data within the period 1986 to 2005. Their results showed a statistically significant impact of oil price

shocks on real stock returns within one month of the event date. Using similar evidence, Miller and Ratti

(2009) delved the long run relationship between the crude oil prices and international stock markets

within the period 1971 to 2008. They observed a clear long run relationship for six OECD countries, and

suggested that stock market indices respond negatively to increases in the oil price over the long run.

Nevertheless, this seems to be less likely after year 1999. The findings supported a presumption of change

in the relationship between real oil prices and stock returns in the last decade which might suggest the

presence of stock market bubbles and/or oil price bubbles since the turn of the century. Thus, by looking

at this linkage between oil price shocks and stock returns, it can lead several investors to predict the

direction of the stock market in case of an unexpected move in oil prices.

To study the affect of oil price changes on stock fluctuations in oil importing countries, several

researchers distinguish between developed countries and developing countries, in response to oil price

volatility. Maghyereh (2004) discovered the relationship between oil prices, and stock market returns for

22 emerging countries within the period 1998 to 2004. He showed that an elevated intensity of energy

consumption in a country results in an elevated response to oil price changes. Maghyereh conducted the

experiment based on the efficient market hypothesis, which states that stock markets in emerging markets

are inefficient in the conveyance of new information with regard to the oil market, and stock market

12

returns in these markets are not rationally alert to changes in crude oil prices. Park and Ratti (2008) found

that oil prices play a critical role in the stock market of oil importing countries. Furthermore, they

summarized that stock markets in oil exporting oil countries are less affected by oil prices relative to oil

importing countries and are also less sensitive to interest rate changes. Additionally, Fayyad and Daly

(2010) performed an investigation into the relationship between oil prices and stock market returns,

comparing GCC countries with the UK and USA, by applying VAR analysis. They employed daily

market data from September 2005 until February 2010. Their empirical findings suggested that the

predictive power of oil for stock return are aggravated after a rise in oil prices and during the Global

Financial Crises. Hereafter, they also concluded that Qatar and the UAE show more perceptiveness to oil

shocks with regard to the GCC countries; a relation which also holds between the UK and developed

countries.

2.3. Fama French three factor model

In the portfolio management field, Fama and French have researched extensive studies on the subject of

equity price returns. These studies aimed at enhancing the results explained by CAPM, which uses a

single factor, beta, to compare the excess returns of a portfolio with the overall market return. In

comparison, Fama and French (1993) presented three factors model and Fama and French (1996) gave an

outstanding summary and showed that along with the market risk premium, most of the returns in a

portfolio can be determined by cross section returns on stock, using market capitalization and book to

market value factors. They started with the observation that: (i) the small cap stocks are represented by

SMB (small minus big), and HML (high minus low) factors. Small firms have low market capitalization.

Value stocks have low market value relative to fundamentals (earnings, dividend, and book value) and

has given higher average returns over growth stocks which have high market value relative to

fundamentals. However, Cochrane (2005) stated that book values essentially track past investment

expenditures so that book values is a better divisor for individual firm than other fundamentals. They ran

regressions on stock return data from the period 1963 until 1990. Their analysis reveals that small cap

stocks and high book-to-market equity stocks have higher average returns, because of unmeasured risk

factors. Consequently, market capitalization and book-to-market value were also indeed proxy for

sensitivity to common risk factors in stock returns. Fama and French (1996) argued that in their three

factors model, size and Book-to-Market ratios play an important role in explaining cross sectional

differences in expected returns for non financial firms. As a result, the Fama and French three factors

model explains the expected stock returns in any markets better than the CAPM model. Cochrane (2005)

argued that CAPM model that use portfolio returns might be successful in describing asset returns, but the

model might not be able to explain these returns, because the model leave suspicious questions on the

rationale behind the return-based factors.

13

Not all researchers concluded that those factors provide a satisfactory explanation for the size (SMB) and

Book-to-market (HML) factors in the three factor model. Lakonishok, Shleifer, and Vishny (1994)

suggested that the prices of low book-to-market stocks are more fascinating than high book-to-market

stocks, as proposed by Fama and French (1993). Thus, it may attract naive investors who push up prices

and lower the expected returns of the securities. Knez and Ready (1997) found that the risk premiums of

size which estimated by Fama and French (1993) disappear. They also explained for further research that

size effect may also involve into the firm’s growth. Another research was conducted by Daniel and

Titman (1997), who suggested that the risk premiums on small size and high book-to-market do not arise

because of the co-movements of these stocks with pervasive factors. Moreover, Daniel, Titman, and Wei

(2001) also rejected the Fama and French three factor model by using the Japanese capital market.

The asset pricing model does not compare all possible outcomes. It only considers the mean and variance

for the outcomes. Therefore, mean-variance framework is clearly not a good description of reality

because the assumption of normal distribution is not possible in the reality. Investors should think about

the higher moments for instance skewness and kurtosis that also determine the risk factor. However,

investors still use the asset pricing model due to its simplicity and the framework is hard enough for some

people. In addition, Tsiang (1972) exhibited that the asset pricing approximation is valuable although it is

not a good description of reality. Tsiang argued that the asset pricing model which considers mean-

variance approximation will only fail in extreme observation, in other words the extreme observation is

rare.

The above literatures examine the relationship between oil prices and stock markets. Additionally, they

examine how this impact is perceived across various industries. Nonetheless, there are still a few papers

which discuss the impact of oil prices on the transportation industries, which are some of the heaviest

consumer of oil. Cameron and Schnusenberg (2008) investigated the relationship between the oil prices

and stock prices of automobile manufacturers in the US. They added an oil price factor to the Fama and

French three factor model over the period March 2001 to September 2008. The factor was measured by

the change in WTI crude oil prices in excessive risk free rate, or alternatively was measured by the excess

return on energy ETF. The index comprising of SUV vehicles was chosen as the dependent variable. In

general, their result exhibited an inverse relationship between oil prices and stock returns of automobile

manufacturers in the US. The result was statistically significant for manufacturers of SUV vehicles, while

using the excess return on energy ETF instead of price of crude oil as the fourth factor. They have divided

their time period into before and after the start of the second Iraq war, when the impact of oil prices on

the stock returns of automobile manufacturers in the US seemed to be notably coherent following the

invasion of Iraq in March of 2003.

14

In summary, there are various theories on what relationship between crude oil price and economic

implications are. Nevertheless, there is still limited consensus explaining the relationship between crude

oil prices and stock returns of automobile manufacturers in Japan.

3. Research Motivation

The aforementioned literature motivates the author to conduct further research into this popular topic. The

media (i.e. television, magazines and newspapers) mention the crude oil price every day. Crude oil price

is a highly sensitive to world circumstances. Therefore, crude oil price shows the interesting and

important economic implications it embeds. The early works in crude oil prices focused on

macroeconomic implications (see, for example, Hamilton 2003; Cunado and Garcia 2005). In light of

this, it would be interesting to explore the influence of crude oil prices on oil importing countries (see, for

example, Park and Ratti 2008).

Japan is the third largest oil importing country in the world behind the United States and China. In 2010,

the Energy Information Administration (EIA) stated that Japan relied on oil imports to meet 45 percent of

its energy needs. Japan imports oil, usually either Dubai Crude or Oman Crude, mainly from the Middle

East (i.e. Iran, the United Arab Emirates and Oman). Japan maintains government-controlled oil stocks to

ensure against a supply interruption. At the end of 2010, the total oil stocks in Japan were 596 million

barrels with 54 percent being government stocks and 46 percent belonging to commercial stocks. The

limitation of the domestic oil reserve causes Japan to depend heavily on oil from overseas supplies to

support its household and industry consumption needs. Therefore Japan plays a crucial role in oil

demand, which contributes to the fluctuation of oil prices in the world. The important thing that

influences oil price is the balance between supply and demand. As in general, many developed countries

influence global demand of oil. For instance, if Japanese economic activities are halted, Japan will reduce

its demand of oil and eventually will decrease the oil price in the short run.

Moreover, oil as a commodity is highly volatile. It tends to either be in oversupply or shortage supply.

When there is a shortage, we expect the price of oil bids up to the highest while when the market is

ample, price is expected to arrive at the lowest that producers will accept. However, supply and demand

are not alone in driving up the oil price. Tremendous unusual events influence the oil price movements.

For example, ever since Oil embargo 1973 and recently, the economic activities of emerging markets

such as India and China have grown and continue to demand more and more crude oil , also leading to a

higher oil price. As the price has risen, many countries including Japan were demanded less oil.

For the purpose of analysis, the author decided to choose automobile manufacturers, because Japanese

automobile manufacturers are the most prominent such manufacturers in Asia, and in the world. As an

15

evidence, Japan’s auto manufacturers have grown constantly over a long time and have surpassed the US

auto industry by overtaking General Motors of the US as the leading producer of cars in the world by

2008. In the Japanese market, automobile manufacturing is an integrated industry because it relies on

many supporting industries to produce the great diversity of materials and components it uses. According

to the Japan Automobile Manufacturers Association (JAMA), almost 8 percent of Japan’s working

population is involved in auto industry related work. Furthermore, auto production accounts for 17

percent of the total value of Japan’s manufacturing shipments and for approximately 37 percent of the

value of the machinery industries’ combined shipments. Therefore, the automotive industry is one of the

Japanese economy’s core industrial sectors. The globalization of Japanese auto manufacturing also

contributes significantly to local as well as global economies. In light of this, it will be interesting to see

whether the macroeconomic aspect given to the oil price creates any impact on the stock performance of

auto companies and any impact on the investor.

There are fourteen auto companies listed as members in JAMA. These automobile companies produce

passenger cars, buses and trucks. This thesis will focus on passenger vehicles, since these vehicles are the

most attractive vehicles for consumers with various incomes, indicating that the consumer of this type of

car is more likely to be sensitive to the price. Japan’s auto companies have grown in producing passenger

cars (e.g. standard cars, small cars and mini cars), which are primarily less expensive if compared to those

of its competitors, especially European and US auto companies. This is supported by JAMA statistical

data, which shows that within the period from 2007 until 2010 the production of passenger cars reaps 94

percent of the domestic marketshares. There are eight automobile companies who focus on producing

passenger cars listed in JAMA. They are Toyota, Honda, Nissan, Suzuki, Mazda, Daihatsu, Mitsubishi,

and Fuji Heavy Industries. In 2010, according to JAMA, the trend showed that Toyota, Honda and Nissan

are the top three auto companies based on their market shares in Japan. Toyota was the biggest

automobile company in Japan with the largest market share amount of 32.78 percent, followed by Honda

and Nissan ranked in second and third positions with the market shares of 13.85 percent and 13.81

percent respectively.

Table 1: Market shares of the top automobile manufacturers from 2007 to 2010

In the past few years,

Japanese auto companies

have made a concerted

Source : JAMA

No. Manufacturers 2007 2008 2009 2010

1 Toyota 28.98% 28.39% 29.21% 30.91%

2 Honda 11.62% 12.29% 13.57% 13.07%

3 Nissan 13.47% 13.34% 13.01% 13.02%

4 Suzuki 12.54% 13.19% 13.39% 12.5%

5 Daihatsu 11.71% 12.64% 12.94% 12.28%

6 Mazda 4.75% 4.81% 4.43% 4.51%

7 Mitsubishi 4.23% 3.73% 3.47% 3.55%

8 Fuji Heavy Industries 4.22% 4.07% 3.76% 3.57%

Total Market Share 91.52% 92.46% 93.78% 93.41%16

effort to help counter global warming and to improve air quality. The announcement of the Kyoto

Protocol in 1997 recognised that global warming must be addressed and that one way of dealing with the

climate change problem is by reducing emissions of carbon. Tanaka et al (2007) stated that Japan is one

of the highest producers of CO2 emissions in the world,with the highest source of emissions coming from

the industrial and transportation sectors. Tanaka mentioned that, according to the Kyoto Protocol, by

2012 Japan is required to reduce its level of emissions to a point 6 percent below that of 1990. Tanaka

also mentioned that the transportation sector, which is the second highest contributor, also exhibited the

highest rate of increase from 1990 to 2004. The highest emissions are contributed by the use of passenger

cars. Therefore, reducing the CO2 emissions of passenger cars would make a significant contribution

toward reducing the overall CO2 emissions in Japan.

To reduce CO2 emissions, the automobile manufacturers put much attention into the development of

hybrid cars. Japan’s automakers, particulary the top players (Toyota and Honda), are continuously

developing and promoting vehicles to reduce the environmental impact. These two top producers claim

that the combination of an electric motor and a conventional engine causes cars to need less fuel. Georg

(2008) stated that hybrid cars should be produced in order to respond to the environmental problems

caused by engine emissions, air pollution, and noise in urban areas. The hybrid vehicles market expanded

rapidly as the Japanese automobile manufacturers created massive cumulative sales of hybrid electric

vehicles around the world. In the fiscal year 2011, Toyota Motor Company (TMC), which includes the

Lexus brand, announced that its global cumulative sales of hybrid cars had surpassed more than 3.03

million units. Similarly, Honda Motor Company, which started to sell its first hybrid car, the Honda

Insight, in 1999 and has since developed other hybrid cars, had global cumulative sales of 300,000 units

by 2009. Therefore, the automobile manufacturers that are targeting the hybrid market are accelerating

their development strategies.

Nevertheless, looking at the market by region, the sales figures of both Toyota and Honda on their official

websites explicitly say that the largest market shares of hybrid vehicles are not in Japan. The largest

market share of hybrid vehicles is in the US, followed by Japan and Europe in second and third rank

respectively. It is interesting to analyze the market share of hybrid vehicles in Japan because the market

for hybrid cars will continue to grow and will for some time remain at peak level. Moreover, the

government proposed to reduce the share of oil consumed in the transportation sector. In light of this, we

will analyze whether the peaked sales of hybrid cars influence the relationship between oil price and stock

price.

Unusual events also influence on oil prices movements. By 2003, the Iraq invasion was confirmed. The

war that was motivated by the drive to end Saddam Hussein’s regime impacted on the oil price because

Iraq is one of the largest oil producers in the Middle-East. The war caused the oil price to increase above

17

$30 during 2003, according to the NYMEX index. This was the first time that the oil price had risen

above $25 since the mid 1980s. Thus, the increase in oil price affected the demand of oil, especially by oil

importing countries (i.e. Japan). Moreover, few years after the 2003 Iraq invasion, the credit crisis

attacked the world’s economy in 2008. The crisis was triggered by the peak in US housing sales prices

during mid 2006. The crisis hit the economic activities not only in the US but also in other developed

countries. In light of this, this thesis will also research whether the Iraq invasion 2003 and the financial

crisis 2008 had an influence on the relationship between the oil price and the stock price of Japanese

automobile manufacturers.

In summary, the purpose of this thesis is to provide evidence that will contribute to the effort of

explaining the impact of boom in sales of hybrid vehicles on the relationship between oil prices and stock

prices. Moreover, the thesis will also contribute toward explaining the oil factor in the Japanese market

under Fama French three factor model, specifically, whether the behavior of Japanese auto

manufacturers’ stock prices and its relationship with oil factor under some unusual events ( Iraq invasion

2003 and credit crisis 2008) is consistent or not. In regard of this, the thesis will try to answer four

research hypotheses that are constructed in the next chapter.

4. Hypothesis

Based on the Fama-French three factor model, Cameron and Schnusenberg (2008) used the SMB, HML,

and market risk premium risk factors, and as an extension they applied a fourth factor model by adding

oil price factor. For the first hypothesis, this thesis will apply the same hypothesis as Cameron and

Schnusenberg examined. Thus, the paper hypothesizes whether oil prices will have a relationship with the

stock return of Japanese auto manufacturers or not.

Hypothesis 1:

H0 : There is no relationship between oil prices and stock prices of Japanese automobile manufacturers.

H1 : There is a relationship between oil prices and Japanese automakers’ stock prices.

There are many factors (internal and external) that move stock prices up and down. The skyrocket in the

oil prices and the increase in environmental awareness have changed the situation, so that Japanese

manufacturers have to create new products to distribute in the market. As discussed earlier, Japanese auto

manufacturers have successfully sold the hybrid cars in the domestic market since their introduction in

the late 1990s. Clearly, this internal factor may influence the movement of stock prices. For this purpose,

another hypothesis is whether the boom in sales of hybrid cars has an influence on the relationship

between oil prices and stock prices of the Japanese automobile companies who massively produce hybrid

cars (Toyota and Honda). Thus, the second hypothesis is as follows:

18

Hypothesis 2:

H0: The boom in sales of hybrid cars has no influence on the relationship between oil prices and stock

prices of Japanese automobile manufacturers.

H1: The boom in sales of hybrid cars has an influence on the relationship between oil prices and stock

prices of Japanese hybrid cars manufacturers.

Furthermore, the time frame of research is divided into two parts. The purpose is to see the influence of

external factors on the relationship between stock prices and oil prices. Firstly, according to their paper,

Cameron and Schnusenberg (2008) analyzed a considerable amount of oil price data from the pre to post

Iraq war period. They hypothesized that in the post-war invasion, an inverse relationship between oil

prices and US auto manufacturer stock prices is more negative than a relationship in the pre-war invasion.

Apart from the Iraq invasion, there was a credit crisis that was triggered by subprime mortgages in 2008.

Previous research (see for example Fayyad and Daly 2010) has investigated the impact of the credit crisis

on the relationship between oil prices and stock returns with regard to GCC countries, the UK and the US.

Therefore, it would be interesting to investigate whether both events might have had an influence on the

relationship beween the oil price and the stock price of Japanese automotive companies. For this purpose,

the third and fourth hypotheses are constructed as follows:

Hypothesis 3:

H0: The Iraq invasion 2003 had no influence on the relationship between oil prices and stock prices of

Japanese automobile manufacturers.

H1: The Iraq invasion 2003 had an influence on the relationship between oil prices and the stock prices of

Japanese automobile manufacturers.

Hypothesis 4:

H0: The credit crisis 2008 had no influence on the relationship between oil prices and stock prices of

Japanese automobile manufacturers.

H1: The credit crisis 2008 had an influence on the relationship between oil prices and stock prices of

automobile manufacturers in Japan.

5. Data and Methodology

5.1. Data Description

Cameron and Schnusenberg (2008) used the Fama-French three factors as obtained from Ken French’s

website.The factors from the website represent the US market relative to other markets. Nevertheless, the

19

author argues that it is inappropriate to use these factors from that website since they are collected from

US data; therefore the data cannot be representative of Japan’s capital market. Thus, before doing such an

analysis, the data used should directly represent Japan’s capital market. Specifically, the Tokyo Stock

Exchange can be a representative market because it is the largest stock exchange in Japan.The basic data

used is compiled from daily returns on a value weighted portfolio index of all stock listed on the first

section of the Tokyo Stock Exchange. Secondly, Daniel et al. (2001) argued that the daily Gensaki rate is

used as a benchmark for the risk free rate in the Japanese market since there is no risk free rate in Japan

comparable to that of the US Treasury bill rates. Chiao and Hueng (2004) also used a 30-day Gensaki risk

free rate as a benchmark for the risk free rate in Japan. Therefore, Gensaki risk free rate is crucial for the

financial securities market in Japan. In addition, Nowman (2002) also used a Gensaki rate as a proxy for

the Japanese short-term interest rate. All these data are required to calculate the Fama-French three

factors that are retrieved from DataStream. In this research, the daily prices are chosen which are better

representative for calculating the log returns of auto index, market index, and oil price index, which were

included in the Fama-French factors. The proposed period of the daily closing prices started from

December 29, 2000 to March 31, 2011. For each of the companies, the data of the daily closing prices are

retrieved from DataStream.

To analyze the credit crisis event, the daily data are divided into three distinct sub-periods called “pre-

crisis”, “crisis”, and “post crisis”. The time frame of the crisis focuses three years before and one year

after the crisis. Nevertheless, there are many different opinions about the exact starting date of the credit

crisis. Enlightment comes from Manda (2010), who analyzed the US stock volatility during the credit

crisis era with the starting point on March 17, 2008, because on that date the US investment bank Bear

Stearns & Co was taken by JP Morgan.The crisis ended on April 1, 2009, indicated by the fact that the

S&P index has rebounded from its lowest value at the end of March 2009. Similarly, in analyzing the Iraq

invasion, the data divided into three phases and the time frame of the war is taken to start from January 1,

2001 and end on July 29, 2005. The time phases for both events are summarized as follows:

While analyzing the sales boom of hybrid cars, the research is focused into two distinct sub-periods called

“before sales booming” and “after sales booming”. Owing to the data availability on the sales of hybrid

cars, the thesis makes some restrictions. The yearly sales data of hybrid cars are collected from the

official websites of Toyota and Honda, the Japan Automobile Dealers Association (JADA), and JAMA.

From the table 3, it shows that Toyota outperforms its major competitor concerning sales of hybrid cars.

The outperforming of Toyota is also caused by introducing many new hybrid vehicles from its Lexus

brand for instance the most prominent Lexus RX 400 hybrid that makes sales of hybrid cars become

stronger. Moreover, JADA exhibits that Toyota Prius often ranks first in the sales of cars in the Japanese

market. Nevertheless, the success of Honda is not followed by Toyota, where the biggest sales of hybrid

car were achieved in April 2009 by the third generation of Honda Insight.

20

Hereafter, the method used to determine the time frame ofthe sales boom is by percentage of hybrid car

sales. In Japan, the government’s fiscal year runs within the period April 1 to March 31. Table 2 defines

the automobile companies’ (Toyota and Honda) percentage of sales and unit sales of hybrid cars in Japan

starting from the fiscal year 2000 until 2011.

Table 2: Toyota total sales of hybrid cars in Japan during fiscal year 2000–2010 (in thousand)

Toyota HondaPercentage of sales Unit Sales Percentage of sales Unit Sales

2000 1.04% 12.5 0.19% 1.3972001 1.52% 18.5 0.06% 0.4572002 1.41% 20 0.29% 2.3692003 1.78% 27.2 0.13% 0.8372004 4.37% 68.7 0.07% 0.4942005 3.85% 58.5 0.73% 4.8832006 5.15% 72.4 0.91% 5.8742007 6.02% 82 0.66% 3.9672008 8.94% 104.4 1.51% 8.2432009 18.06% 251.1 15.51% 96.6162010 34.50% 433.6 9.04% 51.49

Source: JADA, JAMA, HONDA, TOYOTA

From the above table, the sales percentage of hybrid cars by Toyota and Honda reached its peak by the

fiscal year 2009 compared with previous years. This condition is also supported by the hybrid cars

website1, which states that 2009 was recorded as the breakthrough year for gas-electric hybrid cars. The

website informs that Toyota Prius was Japan’s top selling automobile in earlier 2009 for the first time

since its debut in 1997 and Honda Insight ranked fifth with 93,283 units sold since its first production in

1999. Thus, Toyota and Honda start their sales booming of hybrid cars in fiscal year 2009. In conclusion,

the time phases for both events are summarized as follows:

Table 3 : Time Phases for Iraq war, credit crisis, and booming sales of hybrid car

Iraq War Start Date End Date

Pre War 1/1/2001 3/18/2003

War 3/19/2003 5/1/2003

Post War 5/2/2003 7/29/2005

Credit Crisis Start Date End Date

1 www.hybridcars.com

21

Pre Crisis 8/1/2005 3/14/2008

Crisis 3/17/2008 4/1/2009

Post Crisis 4/2/2009 12/31/2010

Influence of Hybrid car Start Date End Date

Before the boom sales 1/01/2001 3/31/2009

After the boom sales 1/01/2010 3/31/2011

Source: Manda (2010), EIA

5.2. Methodology

The Fama-French three factor model has been extensively used as a tool for measuring returns based on

the firm’s market capitalization and the BE/ME ratio in the Japanese stock market (for example works see

Mohammed et al 2007; Pham 2007). From the OLS estimation model, the excess return of Japanese

automobile companies is a dependent variable proxy. The independent variables are excess market return,

SMB (small minus big), and HML (high minus low), which are categorized as Fama-French factors.

Furthermore, Pennachi (2008) stated that one of the most important anomalies is caused by macro-

economic factors that are motivated by the fact that the market portfolio proxy is not perfect, and, hence,

the relation between consumption and marginal utility of that consumption is not perfect as the asset

pricing model suggests. Therefore, another way to operationalize is by using the commodity prices such

as oil prices that can be used as a proxy for consumption. Mathematically, the equation can be written as

follows:

Ra-Rf = αt + β1(Rm-Rf) + β2(SMB) + β3(HML)+ β4(Oil Price Factor) + εt

To carry out the test, the research methodology adopts the same process as Cameron and Schnusenberg

(2008) and applies the approach to the automobile manufacturers in Japan with several adjustments

considering the compatibility of the data set. Cameron and Schunsenberg (2008) retrieved the data for

market index, SMB, and HML from Fama’s website. This sophisticated model is not feasible in this

sample case, as the data from the website is solely dictated by the availability of data. Moreover, the

details of constructing the data of the automobile index, the Fama-French factors, and the oil price factor

are discussed as follows:

A. Excess Return on the Auto Index

To examine the excess return on the Japanese automobile manufacturers index, the return on auto index is

calculated by taking a weighted average of a market capitalization. A stock market portfolio weighted by

the market value of the eight automobile companies in the porftolio. Market value is the market share

22

price multiplied by the number shares outstanding. Larger companies have greater portion of the

portfolio. The data of the daily market value for each of the eight automobile manufacturers from the

period December 29, 2000 until March 31, 2011 are retrieved from DataStream. Further step, the daily

market value of all eight companies is summed for the proposed time period and the total market value is

chosen to be a divisor. The auto index is calculated by taking the log returns of daily closing prices of

automobile manufacturers and multiplied by the weighted average of market capitalization. Moreover, the

calculation is repeated every day within the proposed time to compute the auto index. Finally, to obtain

the excess return on the auto index, the return on the auto index of Japanese automobile companies should

be subtracted by the Gensaki risk free rate.

B. Excess Return on the Market

Pennachi (2008) argued that market risk premium is computed by subtracting the market index by the risk

free rate. Market portfolio is unobservable, therefore, a broad index is needed as an approximation to

market portfolio which contains all assets there. To compute Japan’s market return index, the investors

could choose whether to use the average price weighted of the Nikkei 225 index or the TOPIX, which are

the prominent stock market indexes for the Tokyo Stock Exchange (TSE). The Nikkei 225 is published

by newspaper, the so-called Nihon-Keizai Shimbun, and its unit is measured in yen. The Nikkei 225 index

has been calculated on a daily basis and it is computed by taking the average price weighted index.

Therefore, the Nikkei 225 index is severely affected by high-priced stocks.

The TOPIX stock market index is commonly used in Japan’s financial market because it is published by

TSE. According to the TSE website, the TOPIX accounts for 1,700 companies listed on the TSE first

section and its unit is measured by point. The TOPIX stock market index is computed by taking the

fluctuations of adjusted market capitalization weighted index. Therefore, the TOPIX is most affected by

issues with high aggregate market value. The calculation method of the world index is often used: the free

float adjusted market capitalization weighted. Thus, the TOPIX index has a crucial usage as an assets

benchmark to evaluate and standardize asset management. The Japanese government uses the TOPIX as

their leading economic indicator. Moreover, pension fund managers and investment fund managers use

the TOPIX index as a benchmark to evaluate their Japanese market portfolio.

For the purpose of analysis, the TOPIX index seems suitable as a benchmark to calculate the Japanese

market return index. As a support, Pham (2007) used the TOPIX index to calculate market index.

Furthermore, Japan’s market return index is calculated by taking the log returns of the daily closing price

index of the TOPIX index within the period December 29, 2000 to March 31, 2011. To obtain the excess

market return, the log returns of the daily closing prices of the TOPIX index should be substracted by a

30-day Gensaki risk free rate.

23

C. The SMB and the HML

As discussed in the earlier sub-chapter, the author took the portfolio of the companies that were listed on

the Tokyo Stock Exchange as representative of the Japanese financial market. In the Tokyo Stock

Exchange, the listed companies are divided into three sections (i.e. first section, second section, and

mothers). The first section is for large companies, while the second section is for middle sized companies.

The last section is dedicated to small companies that have small growth and emerging stocks. In 2010

there were 1,695 companies listed on the first section of the Tokyo Stock Exchange. However, the

number of companies changed slightly owing to the delisting of companies every year (for example in

2009 there were 1,687 companies listed in the first section).

We propose to limit the number of selected companies by considering the criteria as mentioned on the

TSE website, for instance number of shareholders, market capitalization, shareholder’s equity, and no

false statements or fair representations. The website mentions many types of market index (i.e. TOPIX

30, TOPIX 100, TOPIX mid400, etc.). The TOPIX Core 30 contains the most liquid and highly market

capitalized stocks in the Japanese capital market. The TOPIX Large 70 serves a data of 70 companies that

are the most liquid and highly market capitalized stocks in the Japanese capital market, including the

companies listed on the TOPIX Core 30. The TOPIX 100 contains the data of companies from both the

TOPIX Core 30 and the TOPIX Large 70. Additionally, the companies listed on the TOPIX 100 are

believed to serve financial reports according to Japan’s standard financial reporting system. These

companies cover 33 industry sectors (i.e. mining, construction, foods, automotive, etc.) in Japan.

Therefore, it is wisely to use the companies listed on the TOPIX 100 as an indicator to represent the

Japanese stock market.

The CAPM model only uses a single factor, beta, to compare market portfolio as a whole. The beta

explains the causality between market risk premium and excess return. As an extension, the Fama-French

three factor model introduces SMB (small minus big) and HML (high minus low) factors. They provide

how to compute these variables on their website. According to Cameron and Schnusenberg (2008), as

cited from French (1993), the SMB and HML factors are constructed using the six valueweighted stock

portfolio formed by two market equity (e.g. size of the equity market and book-to-market benchmark

porftolios) whereas there are any distortion from costs, transaction fees, or taxes.

The SMB factor attempts to explain excess returns made by the portfolio manager. The portfolio manager

divides the portfolio of companies based on their size of equity market. Therefore, market value is used to

compute the size of the equity market. This thesis uses the same methodology according to the Fama-

French website to obtain SMB and HML. The market capitalization (size of equity market) breakpoint

24

determines the buy range for the “small” and “big” portfolios. The SMB denotes the first 50 percent of

companies as “small” size companies and the other 50 percent as “big” size companies. Another factor,

HML, shows the spread in excess returns between value and growth stocks. HML accounts that

companies with value stocks (high book value relative to their book value) seem to earn excess returns

over growth stocks. Therefore, HML is calculated by B/M ratios by dividing the book value by the

market value.

For each of the companies, the author retrieves the market value and book value data of each of the

companies from DataStream within the period December 29, 2000 to March 31, 2011. A portfolio of

companies is divided using the B/M ratios as the benchmark, with the criteria on the basis of 30:40:30

percentiles. The first 30 percent of the companies are called “low stocks”, the next 40 percent “medium

stocks”, and the last 30 percent “high stocks”. Furthermore, these steps created the six portfolios divided

into building blocks; small-low, small-medium, and small-high, and value stocks; big-low, big-medium,

and big-high.

Further step, the daily log returns of those companies that constituted the value and growth portfolios of

each year were calculated. The daily log returns were calculated by taking the daily closing prices of each

of the companies under scrutiny. The method used to determine daily SMB and HML is to take the

average daily log returns of each companies under portfolios made within the proposed time period.

Furthermore, the Fama-French (1993) determination of small minus big (SMB) and high minus low

(HML) were obtained by applying the following formulas:

SMB = 1/3*(Small/Low + Small/Medium + Small/High) – 1/3*(Big/Low +

Big/Medium + Big/High)

HML = ½*(Small/High + Big/High) – ½*(Small/Low + Big/Low)

D. Oil factor

Ono (2004) stated that Japan imports crude oil mainly from the Middle East which costs less than from

West Texas Intermediate (WTI) and Brent Crude. The WTI is well known as a benchmark of the US

market.The Brent Crude is used as a benchmark of the European market and Dubai Crude oil as a

benchmark of crude oil price for the Asian market. Ono (2004) also stated that Middle-East crude oil

accounts for almost 90% of crude oil imports in Japan. Koyama (2011) argued that the Middle-East

countries who are oil producers determine the export price of crude oil for Asia on the basis average spot

25

price of Dubai Crude price. As a consequence, the import price of crude oil in Japan is based on Dubai

Crude price. Therefore, we have to pay attention to the fact that the Asian market is more dependent on

Middle East oil than Europe and North America.

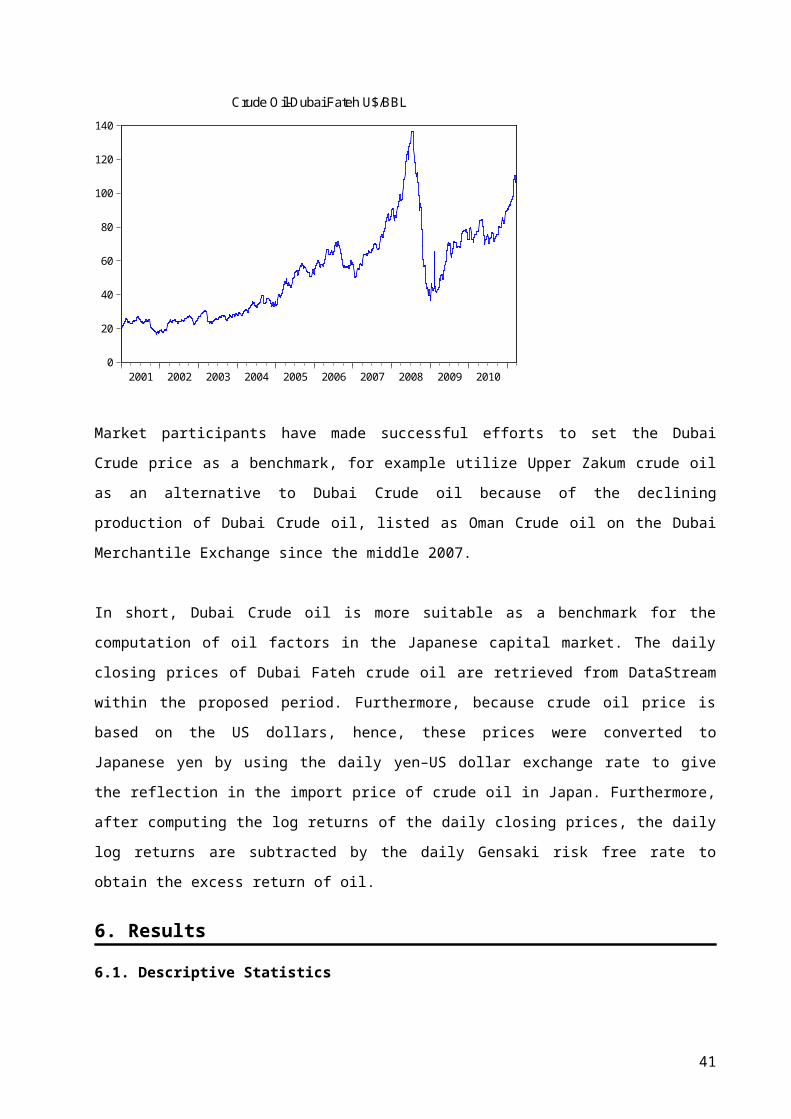

Figure 2 shows the price of Dubai crude oil. Dubai Crude oil, so-called Dubai Fateh, is heavy oil with a

high content of sulfur. In contrast, Both WTI and Brent are light and sweet crude oil. However, regarding

specific quality data, WTI is lighter than Brent. That is why the WTI price is higher than the Brent price

and the Dubai Fateh price. Ono (2004) stated the difference price between WTI and Dubai crude oil has

been US$3 to US$6 per barrel.

Figure 2: Dubai crude oil price from 2001-2011

0

20

40

60

80

100

120

140

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Crude Oil-Dubai Fateh U$/BBL

Market participants have made successful efforts to set the Dubai Crude price as a benchmark, for

example utilize Upper Zakum crude oil as an alternative to Dubai Crude oil because of the declining

production of Dubai Crude oil, listed as Oman Crude oil on the Dubai Merchantile Exchange since the

middle 2007.

In short, Dubai Crude oil is more suitable as a benchmark for the computation of oil factors in the

Japanese capital market. The daily closing prices of Dubai Fateh crude oil are retrieved from DataStream

within the proposed period. Furthermore, because crude oil price is based on the US dollars, hence, these

prices were converted to Japanese yen by using the daily yen–US dollar exchange rate to give the

reflection in the import price of crude oil in Japan. Furthermore, after computing the log returns of the

daily closing prices, the daily log returns are subtracted by the daily Gensaki risk free rate to obtain the

excess return of oil.

26

6. Results

6.1. Descriptive Statistics

Table 4 reports the summary statistics of the important variables generated by implementing the

methodology and data within the proposed period from the section above. Table 4 describes returns of the

risk factors over the entire period. The average daily market premium is -0.0016%. The daily premium

related with HML risk factor is slightly larger than the daily risk premium associated with SMB risk

factor which are 0.0000607% and 0.0000055%, respectively. The market premium has the highest level

of volatility while the HML porftolio has the highest level of excess return.

Table 4 : Summary statistics – full sample

Ra-Rf Rm-Rf SMB HML Roil-Rf

Mean -0.001545 -0.001636 0.000055 0.0000607 -0.001243

Standard Deviation 0.008495 0.006644 0.002704 0.002461 0.009789

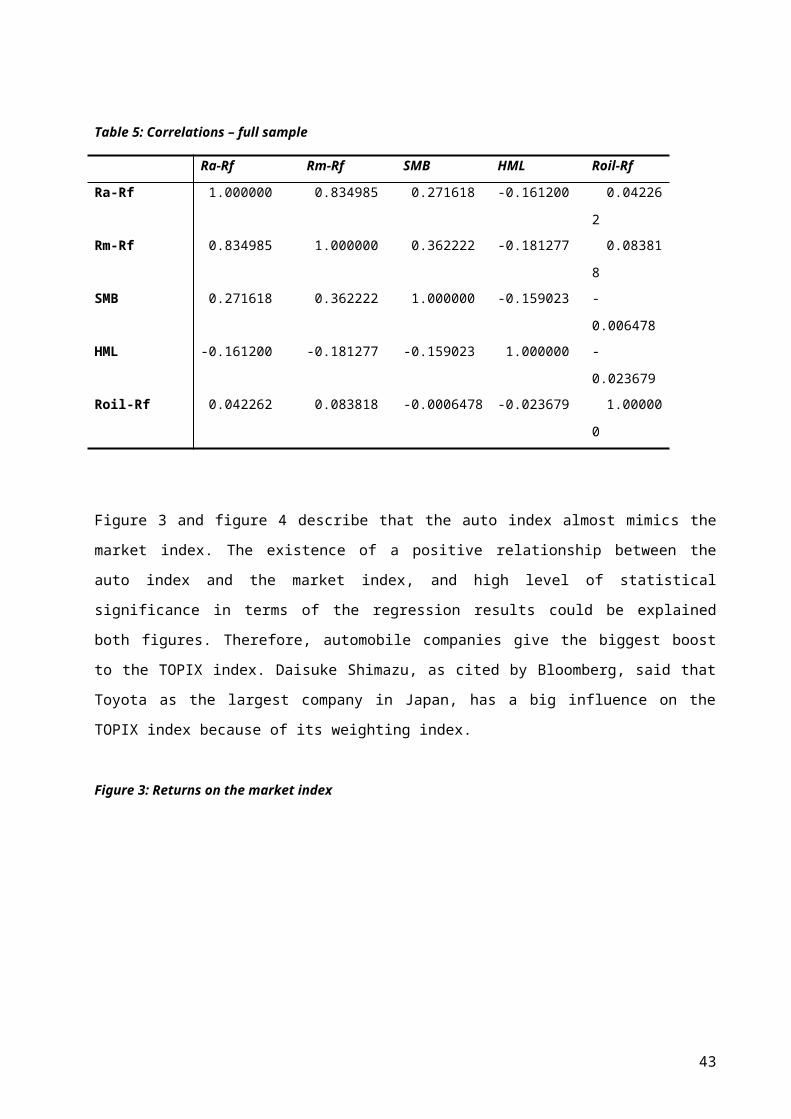

Table 5 shows the correlation between dependent variable and independent variables within the proposed

time period. The table shows that market index, SMB, and oil index have a positive correlation with the

auto index. In additional, only HML has a negative correlation with the auto index.The strongest

correlation is occured between the auto index and the market index which its correlation coefficient is

larger than 0.5. Moreover, the table also shows the correlation between independent variable and another

independent variable. The table exhibits that all independent variables are imperfectly correlated each

other which showed all correlations between each independent variables are smaller than 0.5 or larger

than -0.5. Thus, correlation between all these independent variables may not violate multicollinearity.

Table 5: Correlations – full sample

Ra-Rf Rm-Rf SMB HML Roil-Rf

Ra-Rf 1.000000 0.834985 0.271618 -0.161200 0.042262

Rm-Rf 0.834985 1.000000 0.362222 -0.181277 0.083818

SMB 0.271618 0.362222 1.000000 -0.159023 -0.006478

HML -0.161200 -0.181277 -0.159023 1.000000 -0.023679

Roil-Rf 0.042262 0.083818 -0.0006478 -0.023679 1.000000

Figure 3 and figure 4 describe that the auto index almost mimics the market index. The existence of a

positive relationship between the auto index and the market index, and high level of statistical

27

significance in terms of the regression results could be explained both figures. Therefore, automobile

companies give the biggest boost to the TOPIX index. Daisuke Shimazu, as cited by Bloomberg, said that

Toyota as the largest company in Japan, has a big influence on the TOPIX index because of its weighting

index.

Figure 3: Returns on the market index

-.06

-.04

-.02

.00

.02

.04

.06

01 02 03 04 05 06 07 08 09 10

market index

Figure 4: Returns on the auto index

28

-.06

-.04

-.02

.00

.02

.04

.06

.08

01 02 03 04 05 06 07 08 09 10

auto index

6.2. Regression Results

In this section, the regression results are described by using the equation mentioned in Chapter 5. The

below table shows the results of the auto index that consists of eight automobile companies by using the

Fama-French three factor equation (the market index, the SMB, and the HML) and the fourth oil factor.

The first column shows the regression for the entire time period from January 2001 to March 2011. The

adjusted R squared is 69 percent, which is higher than the results from the study on North American

automobile manufacturers (see Cameron and Schnusenberg 2008). Moreover, the regression shows a

statistically significant adverse relationship between Dubai Fateh crude oil prices and the excess stock

returns of automobile companies. Under ceteris paribus, a 1 percent increase in the Dubai oil price index

will decrease the auto index of the top eight Japanese automobile companies by 0.02 percent.

Apart from the results of the oil index, the market index results a positive beta and statistically significant.

The coefficient of the market index is slightly higher than one, which implies the automobile

manufacturers’ stock prices are significantly correlated with the TOPIX index. Under ceteris paribus,

when the market premium rises by 1 percent, it will increase the stock returns of automobile

manufacturers by 1.08 percent. The Fama-French factors, the SMB and the HML show a negative

relationship with the auto index, but only the SMB is statistically significant while Cameron and

Schnusenberg (2008) exhibited a positive relationship between both the SMB and the HML with the auto

index, and the HML was significant.

29

Table 6: Regression results for the auto index

C Rm-Rf SMB HML Roil-Rf Adj.R

squrd

All years 0.000208 1.085167 -0.120176 -0.047843 -0.025565 0.698885

(2.217306)* (73.56156)† (-3.339248)† (-1.301585) (-2.763565)†

Pre war 0.000228 0.925609 -0.025978 -0.029308 -0.084207 0.499592

(0.964227) (21.52849)† (-0.320799) (-0.370183) (-2.814125)†

War 0.000097 1.265170 -0.737408 -0.659433 0.029536 0.869882

(1.295360) (9.423210)† (-2.523124)* (-1.664973)** (0.641503)

Post war 0.000109 0.978009 -0.510083 -0.256959 -0.009071 0.562714

(0.691366) (24.92480)† (-7.137577)† (-3.254556)† (-0.411130)

Pre crisis 0.000103 1.032094 -0.377062 -0.152802 -0.017858 0.775610

(0.688717) (46.54738)† (-6.257983)† (-2.509766)* (-0.900993)

Crisis 0.001106 1.214547 0.192704 0.145583 -0.008122 0.807615

(2.331183)* (27.83575)† (1.603663) (1.046078) (-0.408838)

Post crisis 0.000279 1.218585 -0.041657 -0.010157 -0.044974 0.718833

(1.500727) (28.79834)* (-0.440811) (-0.095560) (-1.912426)**

t statistics are in parentheses; †,* and ** denote that t-statistics are statistically significant at the 1%, 5%, and10%

level of significance respectively.

Table 6 gives the regression results for all three phases to investigate the influence of the Iraq invasion

2003. The results show a negative relationship between the Dubai Crude oil index and the auto index in

the pre-war period and the post-war period. But, the result is statistically significant only in the pre-war

period. It implies the political instabilites conditions that were occured during pre-invasion of Iraq

significantly affected on the relationship between oil prices and stock prices of Japanese automakers. In

the post-war period, oil prices were expected to become more negative explanatory variable of the stock

prices of automobile companies. However, the coefficient of oil index during the post-war period is less

negative than the coefficient of oil index during the pre-war period and is not significant. But, the

adjusted r-squared shows significant increased from 49 percent in the pre-war stage to 56 percent in the

post-war stage which explicitly explained the oil index explains better the auto index in the post-war

period.

Within both phases, the results indicate that stock prices of automobile companies are adversely affected

by crude oil prices during the pre-war phase and the post-war phase. A 1 percent increase in the Dubai oil

price index, will decrease stock performance of automobile companies by 0.08 percent and 0.009 percent

respectively, before and after the invasion. Additionally, an interesting outcome is during the occurence

of Iraq war where the oil index shows a positive relationship with the auto index. A 1 percent increase in

30

the Dubai oil price index will increase stock performance of automobile companies by 0.029 percent,

under ceteris paribus. However, the term is statistically insignificant that implies the occurence of Iraq

invasion 2003 had no influence on the relationship between stock prices of Japanese auto manufacturers

and crude oil prices. In addition, when the invasion of Iraq was occured, the adjusted r-squared reached

its peak at 86 percent.

Further result, all phases show a positive and statistically significant relationship between the market

index and the auto index. Both the pre-war phase and the post-war phase, the respective market betas are

almost one, which means that stock prices of automobile manufacturers are as risky as the average on the

stock market. During the pre-war stage and the post-war stage, the coefficient shows that if there was an

increase in the market index by 1 percent, a stock performance of the Japanese automobile companies

would increase by 0.92 percent and 0.97 percent respectively. However, during the Iraq invasion, the

regression exhibited higher coefficient relationship between the market index and the automobile

manufacturers’ stock prices which will increase by 1.26 percent. Thus, the auto index consisting of eight

automobile companies during the war period is slightly riskier than the index in both the pre-war period

and the post-war period. Thus, the result implies that stock prices of Japanese automobile companies is

highly correlated with the TOPIX index.

In terms of the other Fama-French factors, the SMB and the HML, The results show the same trend

across the entire time period and exhibit negative relationships between the auto index and the SMB or

the HML for all three phases. The coefficient of the SMB and the HML during the post-war period are

smaller than during the pre-war period. Moreover, it is important to note that in the occurence of the war,

the coefficient of the SMB and the HML turned out to be more negative than in the post-war period. The

HML factor is significant during the war and the post-war period. Therefore, we may conclude that, in

general, investors look at the stocks of Japanese automobile companies as growth stocks (low B/M) rather

than value stocks.