Pre-salt Bidding Rounds - britcham.com.br · The Pre-Salt in numbers Cumulative Production ~1,2...

26

Décio Oddone, General Director Pre-salt Bidding Rounds June 1 st , 2017

Transcript of Pre-salt Bidding Rounds - britcham.com.br · The Pre-Salt in numbers Cumulative Production ~1,2...

Décio Oddone, General Director

Pre-salt Bidding Rounds

June 1st, 2017

O&G in Brazil: a historic opportunity1

Bidding Rounds3

The Pre-Salt2

Final Remarks4

Outline

No relevant private operations in the downstream, logistics and natural gas areas

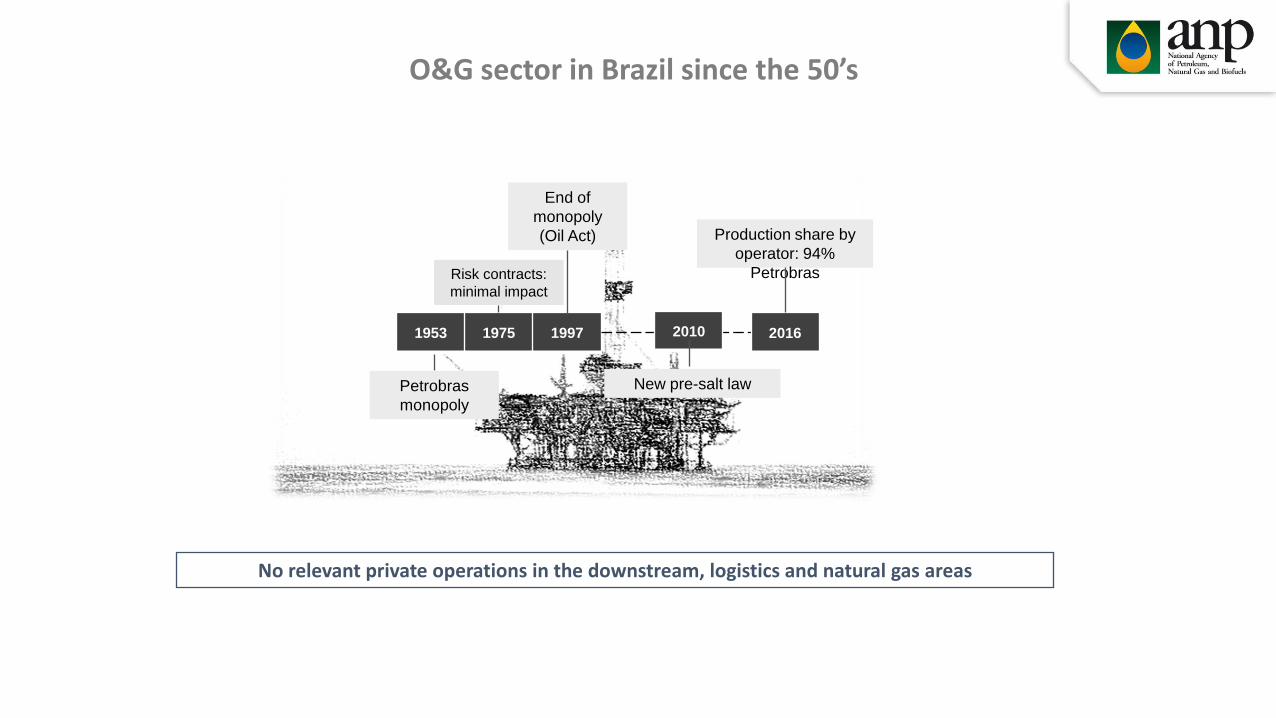

O&G sector in Brazil since the 50’s

End of

monopoly

(Oil Act)

Petrobras

monopoly

1953 1975 1997

Risk contracts:

minimal impact

2016

Production share by

operator: 94%

Petrobras

New pre-salt law

2010

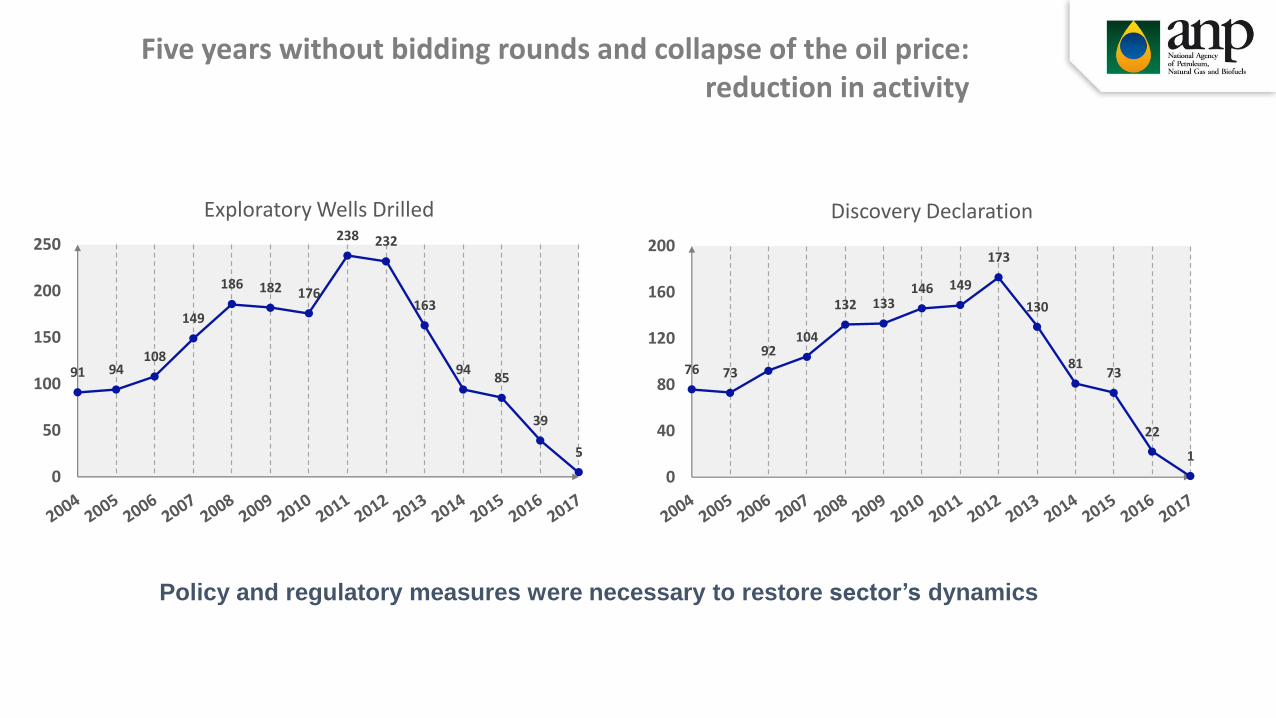

Policy and regulatory measures were necessary to restore sector’s dynamics

Five years without bidding rounds and collapse of the oil price:reduction in activity

91 94108

149

186 182 176

238 232

163

9485

39

5

0

50

100

150

200

250

Exploratory Wells Drilled

76 73

92104

132 133146 149

173

130

8173

22

1

0

40

80

120

160

200

Discovery Declaration

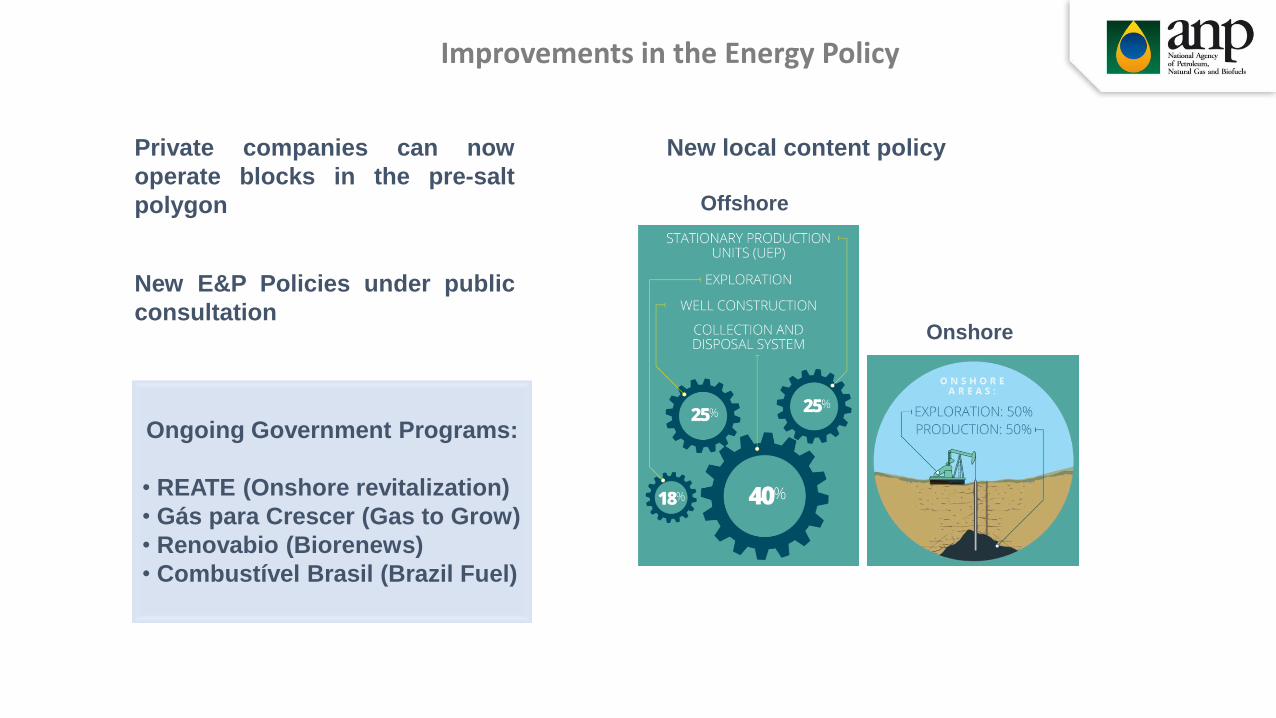

Ongoing Government Programs:

• REATE (Onshore revitalization)

• Gás para Crescer (Gas to Grow)

• Renovabio (Biorenews)

• Combustível Brasil (Brazil Fuel)

Private companies can now

operate blocks in the pre-salt

polygon

New E&P Policies under public

consultationOnshore

Offshore

New local content policy

Improvements in the Energy Policy

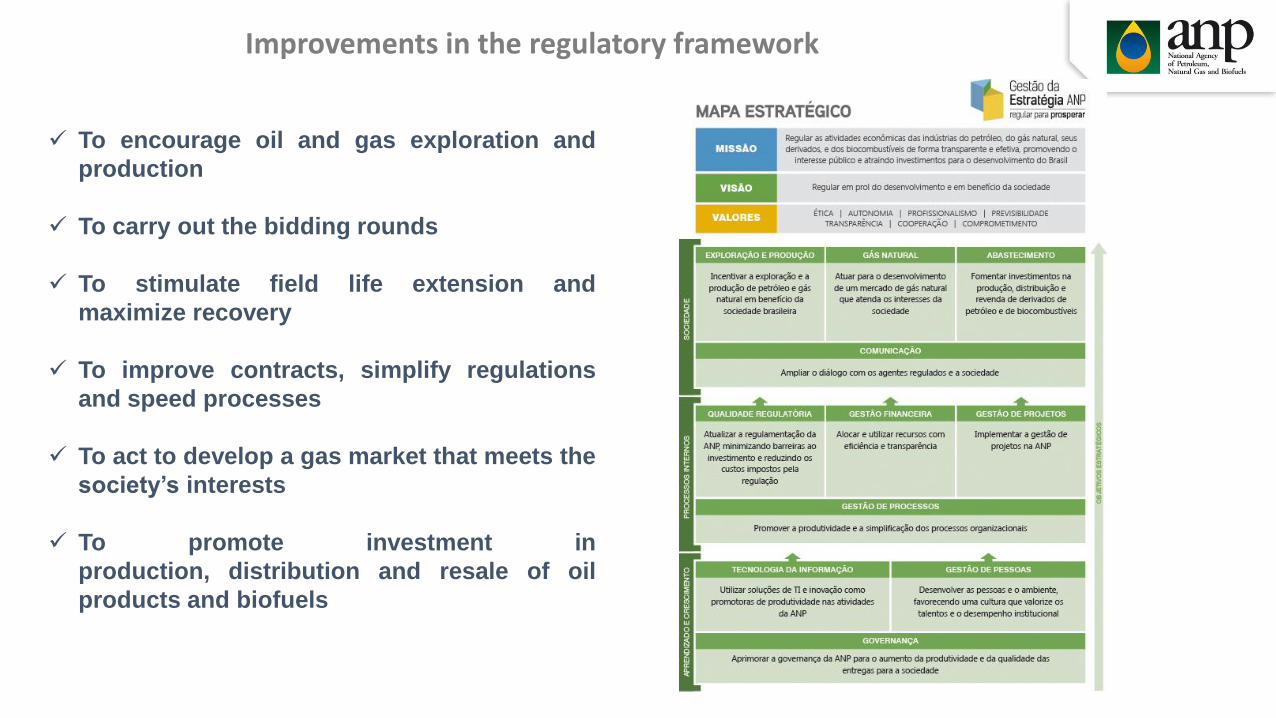

To encourage oil and gas exploration and

production

To carry out the bidding rounds

To stimulate field life extension and

maximize recovery

To improve contracts, simplify regulations

and speed processes

To act to develop a gas market that meets the

society’s interests

To promote investment in

production, distribution and resale of oil

products and biofuels

Improvements in the regulatory framework

The O&G sector is going through the greatest transformation since the foundation of

Petrobras in 1953

Bidding rounds

Schedule

Improvements in the Energy Policy

and regulation

Petrobras divestmentplan

Modernizedsupply chain

O&G sector in Brazil in 2017

O&G in Brazil: a historic opportunity1

Bidding Rounds3

The Pre-Salt2

Final Remarks4

Outline

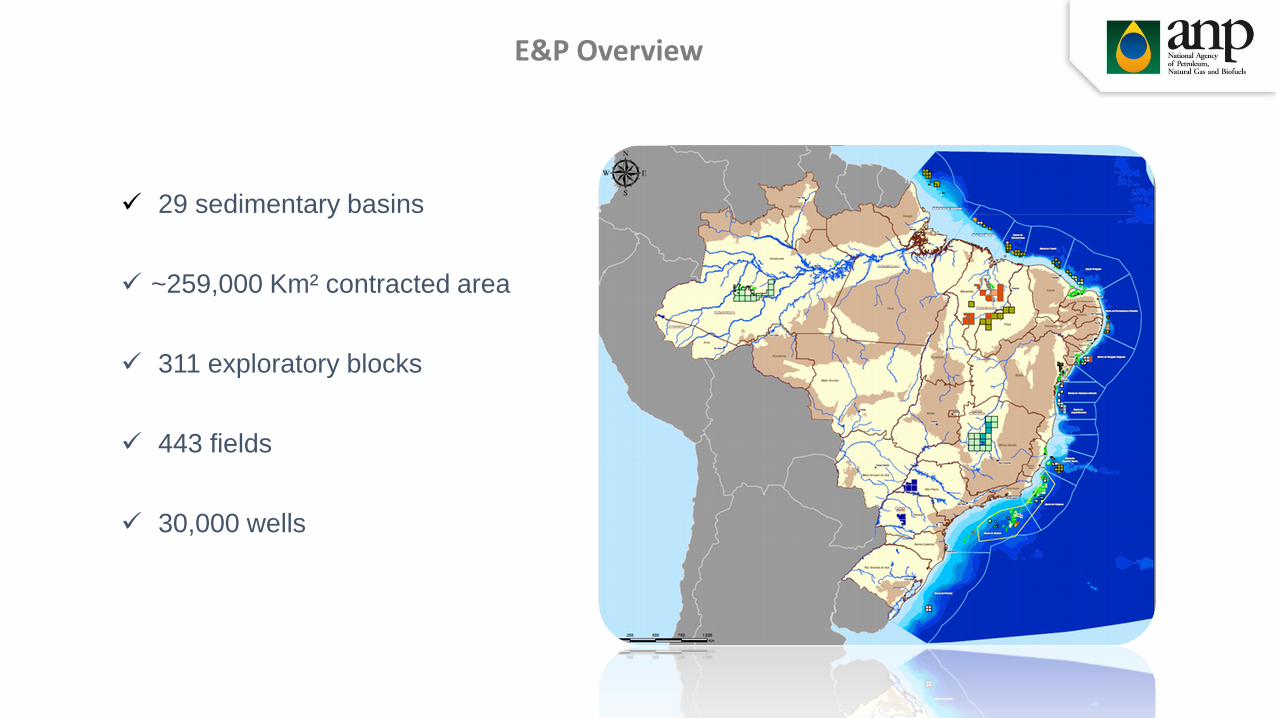

E&P Overview

29 sedimentary basins

~259,000 Km² contracted area

311 exploratory blocks

443 fields

30,000 wells

The Pre-Salt

Pre-salt reserves in this

region contain

unparalleled potential in

terms of volume and

productivity

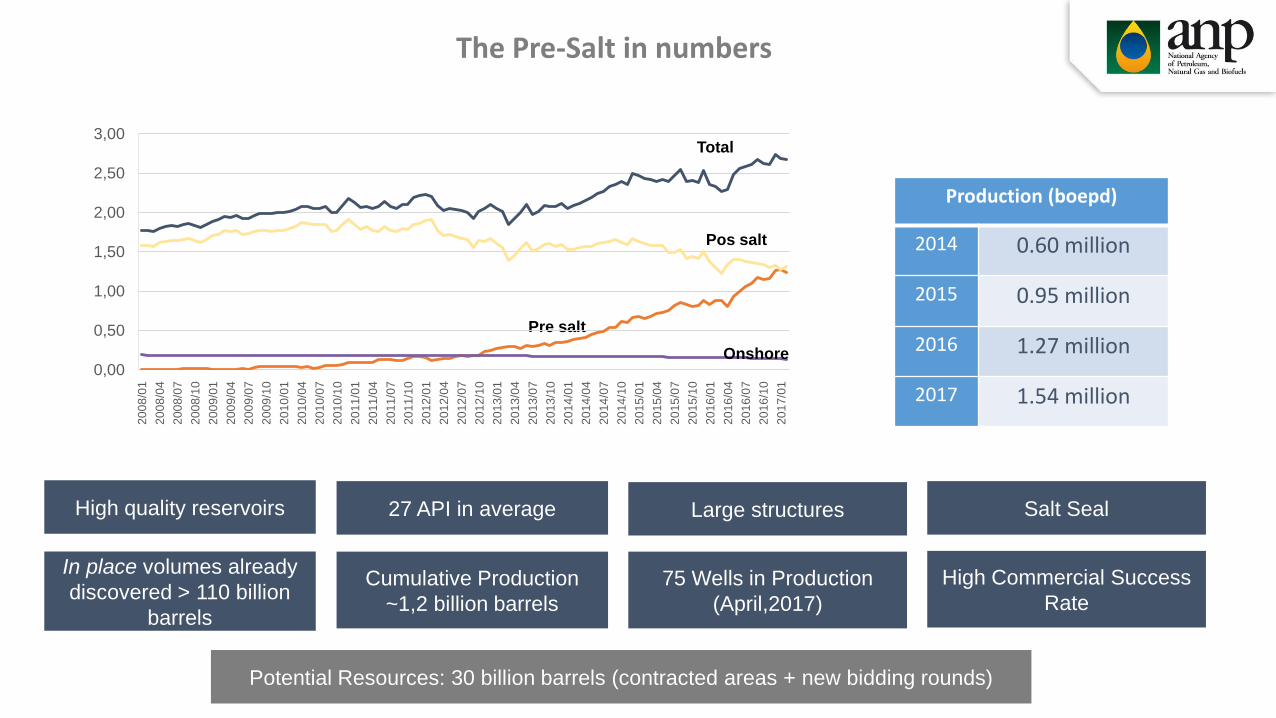

The Pre-Salt in numbers

Cumulative Production

~1,2 billion barrels

In place volumes already

discovered > 110 billion

barrels

Production (boepd)

2014 0.60 million

2015 0.95 million

2016 1.27 million

2017 1.54 million

Pre salt

0,00

0,50

1,00

1,50

2,00

2,50

3,002

00

8/0

1

20

08

/04

20

08

/07

20

08

/10

20

09

/01

20

09

/04

20

09

/07

20

09

/10

20

10

/01

20

10

/04

20

10

/07

20

10

/10

20

11

/01

20

11

/04

20

11

/07

20

11

/10

20

12

/01

20

12

/04

20

12

/07

20

12

/10

20

13

/01

20

13

/04

20

13

/07

20

13

/10

20

14

/01

20

14

/04

20

14

/07

20

14

/10

20

15

/01

20

15

/04

20

15

/07

20

15

/10

20

16

/01

20

16

/04

20

16

/07

20

16

/10

20

17

/01

Pos salt

Total

Onshore

High quality reservoirs 27 API in average Large structures

Potential Resources: 30 billion barrels (contracted areas + new bidding rounds)

75 Wells in Production

(April,2017)

Salt Seal

High Commercial Success

Rate

Baleia Franca/Baleia

Azul/Jubarte

Oil: 205.680 bbl/d

Gas: 7.020 Mm3/d

Marlim Leste

Oil: 15.656 bbl/d

Gas: 273 Mm3/d

Barracuda/Caratinga

Oil: 14.715 bbl/d

Gas: 258 Mm3/d

Marlim/Voador

Oil: 4.755 bbl/d

Gas: 156 Mm3/d

Pampo

Oil: 302 bbl/d

Gas: 15 Mm3/d

Búzios (Well Test)

Oil: 502 bbl/d

Gas: 15 Mm3/d

Itapu

Oil: 28.289 bbl/d

Gas: 372 Mm3/d

Lapa

Oil: 44.224 bbl/d

Gas: 1.200 Mm3/dLula

Oil: 650.716 bbl/d

Gas: 27.628 Mm3/d

Sapinhoá

Oil: 242.631 bbl/d

Gas: 8.938 Mm3/d

Oil: 1.207.470 bbl/d Gas: 45.875 Mm³/d

Total: 75 Wells

Source: ANP/SIGEP

Pre-salt production per field (April, 2017)

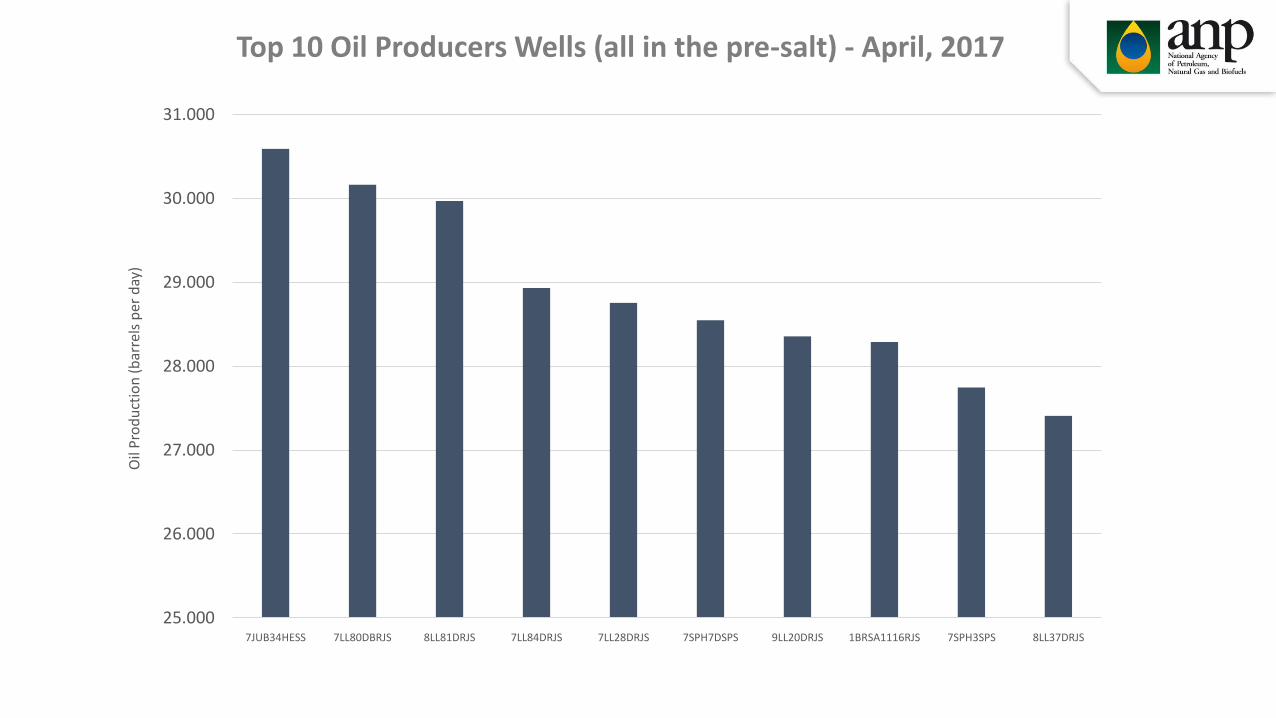

Top 10 Oil Producers Wells (all in the pre-salt) - April, 2017

25.000

26.000

27.000

28.000

29.000

30.000

31.000

7JUB34HESS 7LL80DBRJS 8LL81DRJS 7LL84DRJS 7LL28DRJS 7SPH7DSPS 9LL20DRJS 1BRSA1116RJS 7SPH3SPS 8LL37DRJS

Oil

Pro

du

ctio

n(b

arre

lsp

er d

ay)

O&G in Brazil: a historic opportunity1

Bidding Rounds3

The Pre-Salt2

Final Remarks4

Outline

Future Bidding Rounds Focus Date

2017

14th Bidding Round East Margin and Onshore Basins 27th September

2nd Production Sharing Bidding

Round

Gato do Mato, Carcará, Sapinhoá and

Tartaruga Verde27th October

3rd Production Sharing Bidding

Round

Peroba, Pau Brasil, Alto de Cabo Frio Oeste

and Alto de Cabo Frio Central27th October

2018

15th Bidding Round Equatorial Margin and Onshore Basins May, 2018

4th Production Sharing Bidding

Round

Saturno, Três Marias, Uirapuru, C-M-537, C-

M-655, C-M-657 and C-M-709May, 2018

5th Marginal Fields Bidding Round To be defined To be defined

2019

16th Bidding Round East Margin and Onshore Basins 3rd Q 2019

5th Production Sharing Bidding

Round

Aram, Bumerangue and SE Lula, South and

SW Júpiter 3rd Q 2019

6th Marginal Fields Bidding Round To be defined To be defined

A calendar of bidding rounds for the first time ever

Blocks in offer contain areas excluded from the 9th Bidding Round

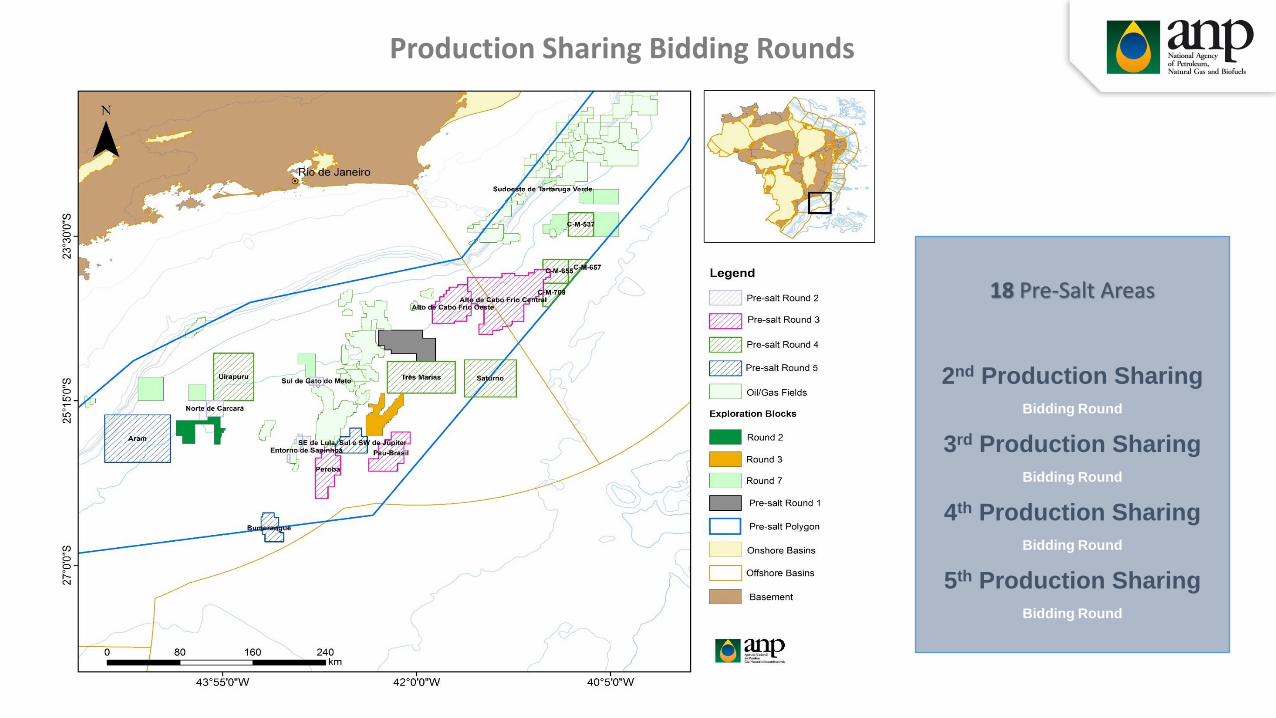

18 Pre-Salt Areas

2nd Production Sharing

Bidding Round

3rd Production Sharing

Bidding Round

4th Production Sharing

Bidding Round

5th Production Sharing

Bidding Round

Production Sharing Bidding Rounds

2nd Production Sharing Bidding

Round

Unitizable Area

Carcará and Gato do Mato in

Exploration Phase

Tartaruga Verde under

Development (First Oil ~ 2017)

Sapinhoá in production

(250,000bpd)

2nd Production Sharing Bidding Round

Carcará estimated in placevolumes: ~2.2 billion bbl

(outside the contracted area)

Carcará Sapinhoá

Gato do Mato Tartaruga Verde

Contracted Area

4 Unitizable Areas

2nd Production Sharing Bidding

Round3rd Production Sharing Bidding Round

Alto de Cabo Frio Central

Alto de Cabo Frio Oeste

Pau BrasilUnrisked in place volume: 4.1 Bbbl

PerobaUnrisked in place volume:5.3 Bbbl

4 Pre-Salt Areas

Production Sharing Contracts

2nd Production Sharing Bidding

Round

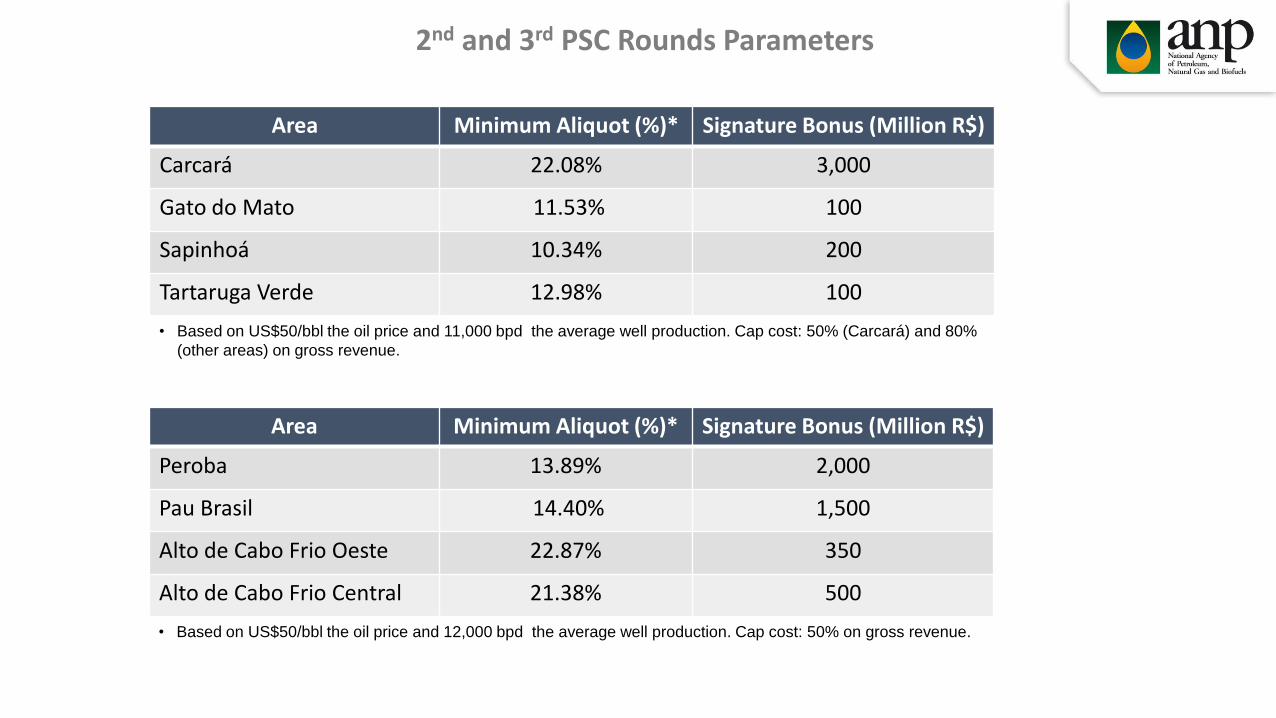

Area Minimum Aliquot (%)* Signature Bonus (Million R$)

Carcará 22.08% 3,000

Gato do Mato 11.53% 100

Sapinhoá 10.34% 200

Tartaruga Verde 12.98% 100

• Based on US$50/bbl the oil price and 11,000 bpd the average well production. Cap cost: 50% (Carcará) and 80%

(other areas) on gross revenue.

Area Minimum Aliquot (%)* Signature Bonus (Million R$)

Peroba 13.89% 2,000

Pau Brasil 14.40% 1,500

Alto de Cabo Frio Oeste 22.87% 350

Alto de Cabo Frio Central 21.38% 500

• Based on US$50/bbl the oil price and 12,000 bpd the average well production. Cap cost: 50% on gross revenue.

2nd and 3rd PSC Rounds Parameters

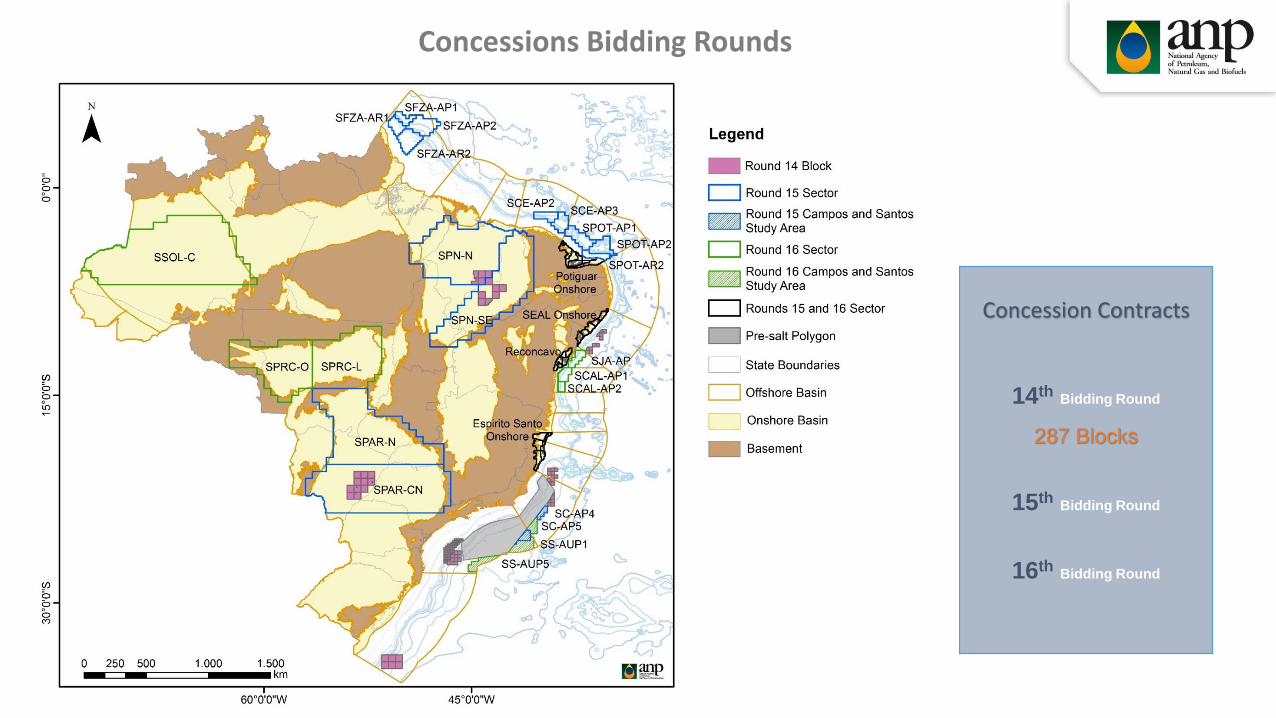

Concession Contracts

14thBidding Round

287 Blocks

15thBidding Round

16thBidding Round

Concessions Bidding Rounds

Block on offer R14

10 Blocks on Offer

Total Area ~5,500 km²

14th Bidding Round – Campos Basin

Sector AP3 with

potential for oil

accumulations in the

Pre-Salt play

The main oil and natural

gas producer in Brazil

+ US$ 80 billions in new

investments

+ 17 new production

units

+ 2 million bpd in 2027+ 600 km of gas

pipelines

+ 1,100 km of flowlines

+ Up to 20 drilling rigs

working simultaneously

+ 10 billion bbl of

Recoverable Volumes

+ 300 offshore wells

What we expect as a result of the bidding rounds

O&G in Brazil: a historic opportunity1

Bidding Rounds3

The Pre-Salt2

Final Remarks4

Outline

• Nine new bidding rounds are planned for 2017-2019 offering acreages

containing billion barrels of oil in place and creating opportunities for all

types of exploration and production companies

• The pre-salt blocks are among the most attractive exploration

opportunities available in the world

• For the first time there are relevant opportunities in the natural gas and

downstream sectors

• Companies interested in investing in E&P, in the supply chain and in the

service industry in Brazil have the largest window of opportunity in

decades

Final Remarks

National Agency of Petroleum, Natural Gas and Biofuels - ANP

Av. Rio Branco, 65, 21st floorRio de Janeiro – Brazil

Phone: +55 (21) 2112-8100

www.anp.gov.br

www.brasil-rounds.gov.br