Pravartana - Runners Up Team

18

Team Numero Uno K. J. SOMAIYA INSTITUTE OF MANAGEMENT STUDIES AND RESEARCH Team Members : - • Trimurti Gupta • Vikas Sonwane • Pulkit Giria

-

Upload

vikas-sonwane -

Category

Economy & Finance

-

view

47 -

download

5

Transcript of Pravartana - Runners Up Team

Team

Numero Uno

K. J. SOMAIYA INSTITUTEOF MANAGEMENTSTUDIES AND RESEARCH

Team Members : -

• Trimurti Gupta• Vikas Sonwane• Pulkit Giria

0

20

40

60

80

100

120

140

1/1

/20

10

4/1

/20

10

7/1

/20

10

10

/1/2

01

0

1/1

/20

11

4/1

/20

11

7/1

/20

11

10

/1/2

01

1

1/1

/20

12

4/1

/20

12

7/1

/20

12

10

/1/2

01

2

1/1

/20

13

4/1

/20

13

7/1

/20

13

10

/1/2

01

3

1/1

/20

14

4/1

/20

14

7/1

/20

14

10

/1/2

01

4

1/1

/20

15

Do

llar

Pri

ce p

er

Bar

rel

Monthly

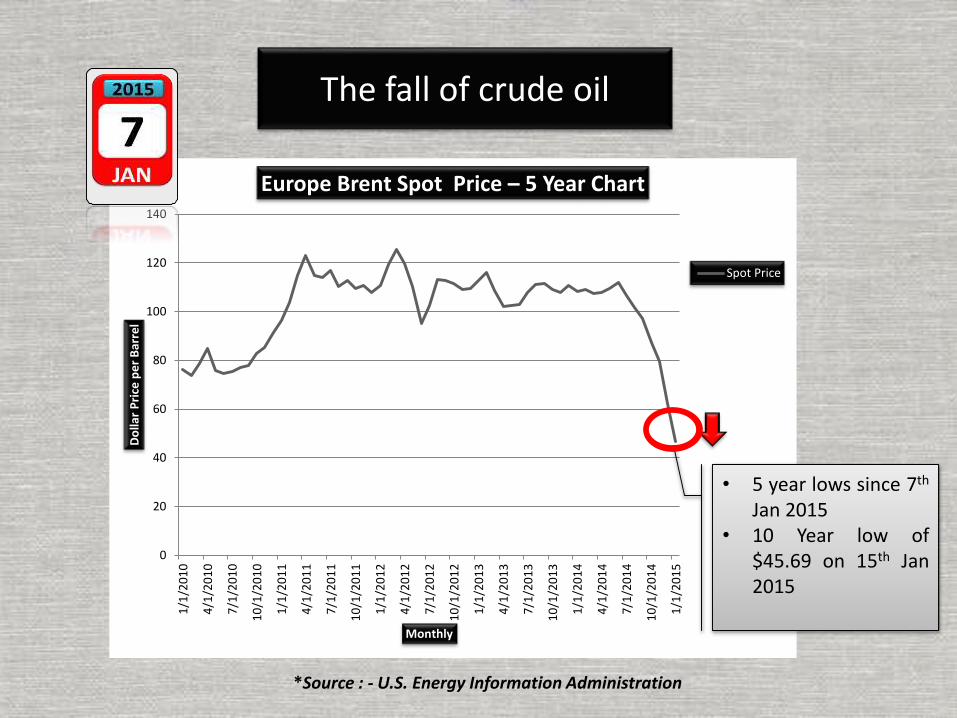

Europe Brent Spot Price – 5 Year Chart

Spot Price

The fall of crude oil

• 5 year lows since 7th

Jan 2015• 10 Year low of

$45.69 on 15th Jan2015

*Source : - U.S. Energy Information Administration

High Supply Demand Mismatch

• A Historical surplusproduction in excessof 2 million barrelsper day

*Source : - U.S. Energy Information Administration

Reasons for this fall

Supply

Shale Oil Boom

•10% and growing of Daily production of crude oil

OPEC excess supply

•Price war for hurting Shale gas producers

•Gain Market Share from Iran & Iraq

Alternative Sources of Energy

•Electric Vehicles

•Bio fuel supply

Demand

China Slowdown

•Chinese economy is slowing to a growth rate of 7.3%

Europe Debt Crisis

•Slow down in economies or Greece, Spain ,Portugal, Ireland and Cyprus

Global Weak Demand

•Weak Demand

•Drive towards alternative sources of energy

“Be Fearful When Others Are Greedy and Greedy When Others Are

Fearful”-Warren Buffett

The ‘Oracle of Omaha’

Why Oil prices will recover – Fundamentals

Shale Oil Economics not sustainable

• Majority of Oil producers have a breakeven in a wide range of $ 59-$80

• The profitability of shale gas is not uniform

• High Debt for some shale gas projects

• OPEC countries have a lot of war chest

Economic Fundamentals

• Demand from Indian Economy having a GDP growth rate of 7.7%

• Stronger European and North American economies

• OPEC strategy Outcome– Either shale market would

break

– OPEC would need to cut down production

– Either ways price will increase

Technical Indicators

0

20

40

60

80

100

120

140

May

-19

87

Jun

-19

88

Jul-

19

89

Au

g-1

99

0

Sep

-19

91

Oct

-19

92

No

v-1

99

3

De

c-1

99

4

Jan

-19

96

Feb

-19

97

Mar

-19

98

Ap

r-1

99

9

May

-20

00

Jun

-20

01

Jul-

20

02

Au

g-2

00

3

Sep

-20

04

Oct

-20

05

No

v-2

00

6

De

c-2

00

7

Jan

-20

09

Feb

-20

10

Mar

-20

11

Ap

r-2

01

2

May

-20

13

Jun

-20

14

Do

llar

Pri

ce p

er

Bar

rel

Monthly

25 Year Historical prices

Spot Price

How to gain from the rise in oil price ?

OIL STOCKS• The Performance of

these stocks depends on management efficiency

• No direct Exposure to Oil as a Commodity

COMMODITY FUTURES• Very Risky • Costly• Cannot invest for a

longer term

There is NO FINANCIAL product which gives a DIRECT

exposure to OIL for a LONGER TERM in India.

The Emerging India Oil Exchange Traded Fund - OETF

OETF

Seller Buyer

What is OETF ?The Oil exchange tradefund will be a domesticexchange traded securitydesigned to track the dailyprices movements of MCXcrude oil index. The AssetManagement Company willissue shares that may bepurchased and sold on theNational Stock Exchange.

CashOETF

shares

Variable Cash Flow

Pri

mar

y M

arke

tSe

con

dar

y M

arke

t

Authorized Participants/

Financial Institutions

NSESeller Buyer

Fund

Cash

OETF shares Cash

OETF shares

Swap Counter-Party

Cash

Index Return

Swap Counter-Party

Index Return

Cash

Collateral Basket

Cash

ReturnOn

Collateral

Cash OETF shares

WORKING DIAGRAM

Type of Fund Non-Equity Exchange Traded fund Linked to Crude Oil

Investment Investment in Underlying Crude Oil

Country of Investment India

Taxation Treatment Capital Gains

Benchmark Index MCX Crude Oil Index

Fund Inception Launched around March 2015

Pricing per unit Approximately 10% price of 1 Barrel of Crude Oil

Minimum Lot(Exchange) One Unit/Share

Minimum Lot (Directly with fund

as per creation unit)

1000 units

Expense Ratio 1.5% Annualized

• Fact Sheet

Features and FACT Sheet

Holdings

• Commodity Futures

• Present Month

• Near Month futures

• Cash

• Indian Rupee

• U.S. Dollars

• Government Bonds

• Short term Maturity

• Long term Maturity

Portfolio Holdings

CRUDE OIL 19Feb2015

15%

CRUDE OIL 19Mar201

524%

8% Govt. of India Savings Bonds (2015)

14%

8% Govt. of India Savings Bonds (2017)

24%

Indian Rupee18%

US Dollars5% Percentage

breakup

Benefits

Equity like features

• Commodity traded as a stock on national stock exchange

Commodity exposure

• Commodity exposure without using the commodity trading account

Used as a Financial hedging instrument against rise in crude oil

Lower expenses as compared to mutual funds

• Fund is managed passively hence lower expense and fees

Low capital gains tax as compared to mutual funds

Returns

SCENARIO RANGE (LOW –HIGH) RETURN

Best Case $85 - $90 55 %

Base Case $72 - $76 31%

Worst Case $38 - $43 (25%)

Calculations based on oil price on 12-02-2015 - $58Time period of 15 – 24 months

Risks Involved

Investment Risk

• Investment not suitable for all kind of investors

• Economic, demand and supply conditions

• Commodity Trading is highly speculative

• Very Volatile and high degree of risk

• Concentration risk

• Can suffer from prolonged periods of decline in value

Operational Risks

• Tracking error risk as is the case of every index fund (Correlation risk

• Risks related to every ETF fund

• Natural forces of “Backwardation” and “Contango”

• Liquidity risk

• OTC credit risk

Market Size of Crude oilbased Financial Product in

India

Investor Response

Commodity ETF Gold Fund

₹1100 crore

MCX Crude Oil Market

2 OUT OF 10

investors

Highest open

Interest for the 19th

Feb 2015 Expiry

AUM Of ₹2365.11 crore

*Source : - www.mcxindia.com, www.nseindia.com

*Source : - Team survey from potential investors

Income generated for theasset management company

• Considering the corpus of ₹ 1100 crore

– Management fee as 1.5 % of AUM

Particulars Amount

Revenue for AMC ₹ 16.5 crore

Less : Management fees ₹ 7.05 crore

Less : Brokerage Commissions ₹ 3.12 crore

Less : Other expenses ₹ .83 crore

Net Profit ₹ 5.5 crore

THANK YOU

THE EMERGING INDIA OIL EXCHANGE TRADED FUND - OETF