PRAISE FOR MASTERING ISLAMIC FINANCE

209

Transcript of PRAISE FOR MASTERING ISLAMIC FINANCE

PRAISE FOR MASTERING ISLAMIC FINANCE

‘Excellent reading and an accessible guide for those who want to understand Islamic finance from first principles. This book combines the theoretical and applied aspect of Islamic finance.’

Dr Mohamad Akram Laldin, Executive Director, Sharia Scholar, International Shari’ah Research Academy for Islamic Finance (ISRA)

‘A comprehensive introduction that demystifies Islamic finance by clearly explaining – with plentiful examples – not only its terminology and struc-tures but also the reasons those structures have been developed.’

John Gilbert, Consultant, Hogan Lovells International LLP

‘This book clearly demystifies Islamic finance for those who are new to it or need to work within the Islamic finance requirements. Constructive and clear, it’s an excellent source of learning and of reference.’

Ruth Martin, formerly managing director the CISI, and Chair of the Education, Training and Qualifications Group of the Islamic Finance Secretariat

‘An excellent insight into Islamic finance enabling all to gain an under-standing of the key concepts surrounding the fascinating subject of Islamic finance.’

Paul Jennings, Deputy CEO, ABC International Bank plc

Mastering Islamic Finance

A practical guide to Sharia-compliant banking, investment and insurance

FAIZAL KARBANI

Pearson Education Limited

Edinburgh GateHarlow CM20 2JEUnited KingdomTel: +44 (0)1279 623623Web: www.pearson.com/uk

First published 2015 (print and electronic)

© Pearson Education Limited 2015 (print and electronic)

The right of Faizal Karbani to be identified as author of this work has been asserted by him in accordance with the Copyright, Designs and Patents Act 1988.

Pearson Education is not responsible for the content of third-party internet sites.

ISBN: 978–1-292–00144–9 (print) 978–1-292–00146–3 (PDF) 978–1-292–00145–6 (ePub) 978–1-292–00817–2 (eText)

British Library Cataloguing-in-Publication DataA catalogue record for the print edition is available from the British Library

Library of Congress Cataloging-in-Publication DataA catalog record for the print edition is available from the Library of Congress

The print publication is protected by copyright. Prior to any prohibited reproduction, storage in a retrieval system, distribution or transmission in any form or by any means, electronic, mechanical, recording or otherwise, permission should be obtained from the publisher or, where applicable, a licence permitting restricted copying in the United Kingdom should be obtained from the Copyright Licensing Agency Ltd, Saffron House, 6–10 Kirby Street, London EC1N 8TS.

The ePublication is protected by copyright and must not be copied, reproduced, transferred, distributed, leased, licensed or publicly performed or used in any way except as specifically permitted in writing by the publishers, as allowed under the terms and conditions under which it was purchased, or as strictly permitted by applicable copyright law. Any unauthorised distribution or use of this text may be a direct infringement of the author’s and the publishers’ rights and those responsible may be liable in law accordingly.

All trademarks used herein are the property of their respective owners. The use of any trademark in this text does not vest in the author or publisher any trademark ownership rights in such trademarks, nor does the use of such trademarks imply any affiliation with or endorsement of this book by such owners.

10 9 8 7 6 5 4 3 2 119 18 17 16 15

Print edition typeset in 11.5pt Garamond by 3Print edition printed in Great Britain by Henry Ling Ltd, at the Dorset Press, Dorchester, Dorset

NOTE THAT ANY PAGE CROSS REFERENCES REFER TO THE PRINT EDITION

Writing this book has given me great satisfaction in being able to share my knowledge and experience about a subject I am very passionate about; in many ways it marks the culmination of many years of study and professional experience. To this end, I must thank all those who have supported and encouraged me through the years – too many to mention individually, but I include teachers, friends, family and professional colleagues. A special tribute goes to my parents, who have been unshakeable in their unconditional love and support throughout my life and worked tirelessly to give me the best possible foundation in life; also a special thanks to my wife, Tassnima, my children – Emaan, Mustafa and Misbah and my siblings – Shamim, Merunisha, Salma and Arif for their love, support and help over the years.

vii

Contents

About the author xi

Publisher’s acknowledgements xii

Author’s acknowledgements xiii

Part 1 BACKGROUND 1

1 The Islamic finance phenomenon 3Introduction 5The Islamic finance phenomenon 5Why does Islamic finance exist? 7Why is Islamic finance a sizeable and growing market? 8Key challenges facing the industry 13Conclusion 16

2 Islam – key beliefs, principles and practices 17Introduction 19Belief system 19Key practices – the five pillars of action 21Importance of the Qur’an and the Sunnah 22Interpretation of the sharia 24The role of scholars and sharia supervisory boards in Islamic finance 26Conclusion 27

3 How Islamic finance differs from conventional banking 29The Islamic economic model 31Key Islamic finance principles 35Conclusion 43

4 Valid commercial contracts in Islamic finance 45Introduction 47Key conditions for validity of contracts 47Integrity of contractual arrangements 51

viii

Contents

Status and use of promises 52Conclusion 53

Part 2 ISLAMIC FINANCE IN PRACTICE 57

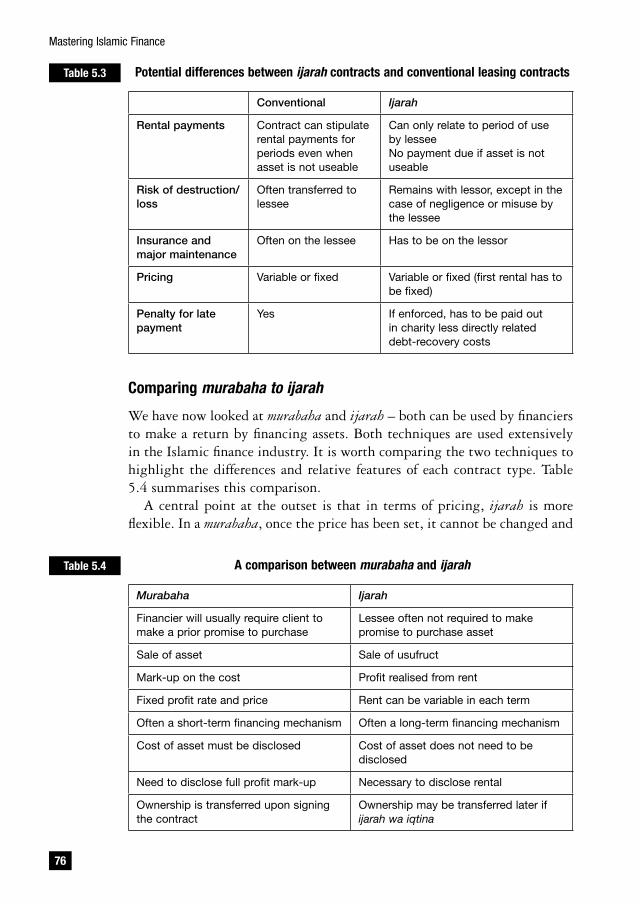

5 Key transaction types in Islamic finance 59Introduction 61Equity-type: transactions 61Mudarabah (Partnership – one party contributes capital) 62Musharakah (Partnership – all parties contribute capital) 64Asset finance: 68

Murabaha (Sale of an asset at a known profit mark-up) 68Ijarah (Leasing of an asset) 77Istisn’a (Sale of an item to be constructed or manufactured) 80Salam (Sale of fungible item yet to be produced) 84

Other key transaction types: 89Wakala (Agent providing services to a Principal) 89Hawalah (Transferring a debt) 92Rahn (Providing security) 93Kafalah (Providing a guarantee) 94

Conclusion 95

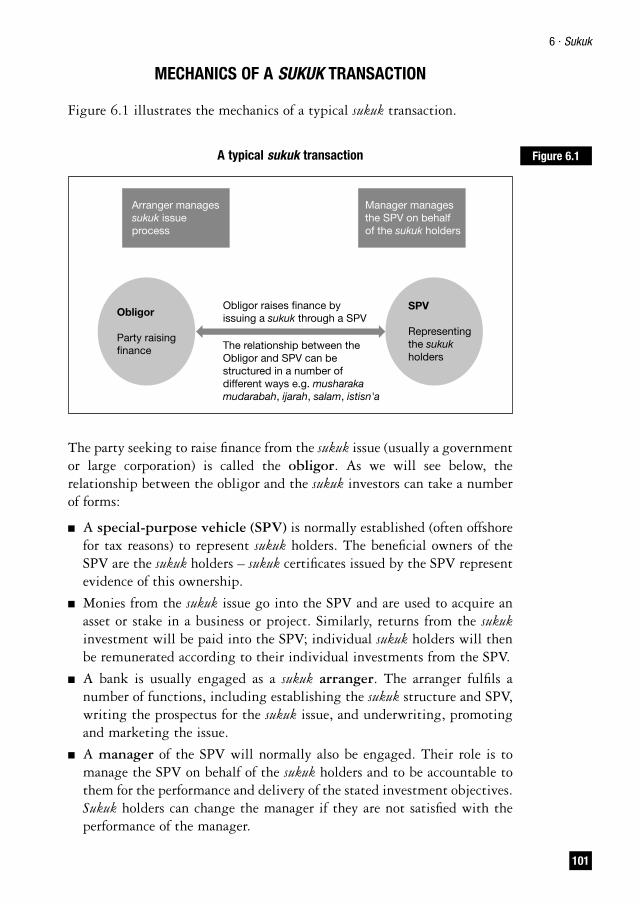

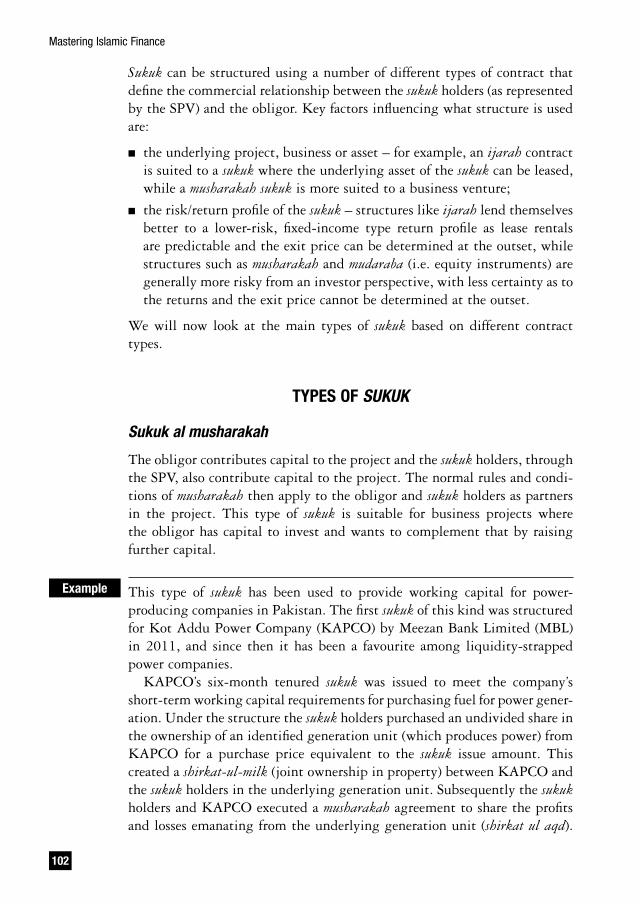

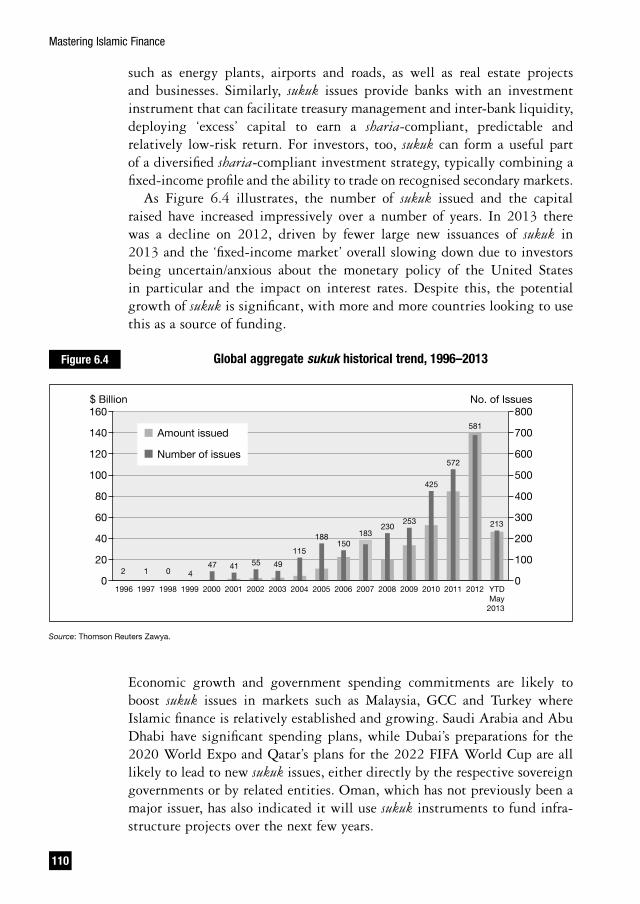

6 Sukuk 97Introduction 99Definition 100Mechanics of a sukuk transaction 101Types of sukuk 102Asset-based versus asset-backed sukuk 108Sukuk and the secondary market 109A strong future for sukuk 109Conclusion 111

7 Sharia-compliant investments and wealth management 113Introduction 115Sharia-compliant investments 115Zakat by Iqbal Nasim 126Sharia-compliant estate distribution and Islamic wills by Haroon Rashid 133Conclusion 144

8 Takaful – Islamic insurance 147Introduction 149

ix

Contents

Sharia perspective on conventional insurance 149Takaful – the Islamic alternative 150Takaful models 151Types of takaful policy 155The future of the takaful industry 158Conclusion 158

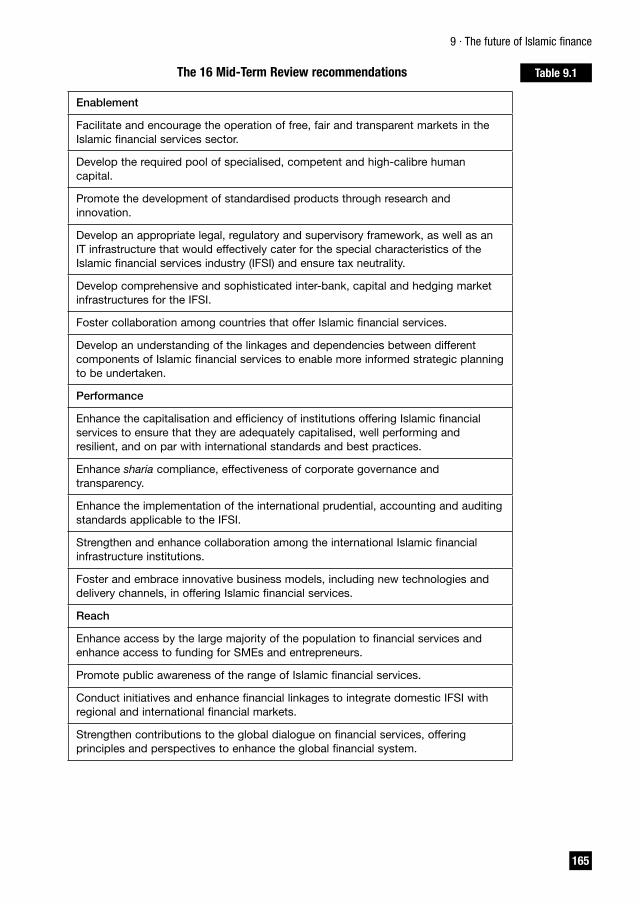

9 The future of Islamic finance 161Introduction 163Recommendations for success by IFSB and IDB/IRTI 163Opinion pieces 166The Christian view of usury by Robert Van de Weyer 167The future of Islamic finance by Dr Sayd Farook 171The secret to long-term success: get the direction of travel right by Faizal Karbani 176

Index 181

xi

About the author

Faizal Karbani is the founder and CEO of Simply Sharia Ltd, a UK firm solely dedicated to providing sharia-compliant financial solutions along with supporting Islamic finance through recruitment and training. Over the last decade Faizal has become a leading UK practitioner of the industry. Highly trusted and recognised, he supported both the technical team advising the UK government on tax implications for sharia-compliant products and the government consultation on sharia-compliant student finance in Britain. Under his leadership and direction, Simply Sharia launched the first certified sharia-compliant green energy EIS, offered to UK investors in 2014. His clients have included Qatar Islamic Bank in London (QIB UK), Gatehouse Bank, Arab Banking Corporation, Barclays Capital, British Bankers Association (BBA) as well as a host of individuals and other businesses. Faizal is also an Approved Trainer for the Islamic Finance Qualification (IFQ) and undertakes bespoke Islamic finance training programmes for professionals. He is a regular speaker on Islamic finance related topics and is a member of the Advisory Board appointed by the University of Nottingham in respect of its Islamic finance programmes. Prior to working in Islamic finance, Faizal, who is a qualified Chartered Accountant, worked at PriceWaterhouseCoopers and GlaxoSmithKline.

xii

Publisher’s acknowledgements

We are grateful to the following for permission to reproduce copyright material:

FIGURES

Figure 1.2 from Global Islamic Finance Report 2013, Edbiz Consulting; Figure 1.3 from Pew Research Center’s Forum on Religion and Public Life, The Future of the Global Muslim Population, January 2011, www.pewforum.org/2011/01/27/the-future-of-the-global-muslim-population/, Pew Research Center; Figures 1.5 and 1.6 from Thomson Reuters Zawya, Sukuk Perceptions and Forecast Study 2014, Islamic Finance Gateway; Figure 3.1 from Week 11, 2014: Global Debt, http://www.ercouncil.org/chart-of-the-week/week-11-2014-global-debt.html, Economic Research Council; Figure on page 79 from Islamic KD Ijara Fund, www.kuwait.nbk.com/investmentandbrokerage/investmentfunds/ijarafunds/islamickdijarafundiv/default_en_gb.aspx

TEXT

Extracts on pages 67, 79 and 90–1 from Al Rayan Bank (formerly Islamic Bank of Britain (IBB)); Extract on page 79 from Islamic KD Ijara Fund, www.kuwait.nbk.com/investmentandbrokerage/investmentfunds/ijarafunds/islamickdijarafundiv/default_en_gb.aspx; Extract on pages 87–8 from Dubai Islamic Bank (DIB), www.dib.ae/personal-banking/finance/al-islami-personal-finance/salam-finance/faqs#tab-section

In some instances we have been unable to trace the owners of copyright material, and we would appreciate any information that would enable us to do so.

xiii

Author’s acknowledgements

I am indebted to several people in helping me to write this book. My dear friend, Faisal Sheikh and my colleague, Anas Hassan have in particular played a significant role in reviewing and providing valuable feedback on the book. Faisal is a Wealth Manager at Barclays – as someone interested to learn more about Islamic finance and a financial professional, he is typical of someone that the book is aimed at. Therefore his feedback was very relevant and insightful and I’m sure resulted in enhancing the overall quality of the book. Anas’ professional career has centred around Business Strategy and he currently works alongside me as the Head of Business Finance at Simply Sharia. His feedback on the draft chapters was invaluable in helping me project the message in the most effective way. Others who have provided me feedback and advice as I’ve been writing the book include Lawrie Chandler, Tasnim Raja, Tarek El-Diwani, Kate Edmunds, Nyra Mahmood and my wife, Tassnima Karbani. I would also like to acknowledge all the contributors to the book:

Iqbal Nasim, who has written about the obligatory form of charity due from Muslims every year, known as Zakat. He is a leading authority on the subject and is the Chief Executive of the UK based charity called National Zakat Foundation.

Haroon Rashid, who has written on the subject of Sharia compliant estate distribution and Islamic Wills. Haroon is a lawyer who has specialised in this area and is widely recognised as a leading authority on the subject and has played a key role in pioneering Islamic Wills that are tax efficient in the UK.

Robert Van De Weyer, who has contributed an opinion piece entitled the ‘Christian View of Usury’. Robert is a practising Christian priest and a former Economics lecturer at Cambridge University. He presents a fascinating view of how Islamic finance principles are consistent with Christian and broader ethical values.

Dr Sayd Farook, has contributed an opinion piece entitled ‘The Future of Islamic Finance’, where he provides an amazing insight into the journey

xiv

Author’s acknowledgements

of Islamic Finance to date and what he believes the industry needs to do to achieve its potential. Dr Sayd is the Global Head of Islamic Capital Markets at Thomson Reuters and has been played a significant role in producing some of the most insightful analysis and reports on the global Islamic finance industry to date.

Part

1BACKGROUND

1. The Islamic finance phenomenon

2. Islam – key beliefs, principles and practices

3. How Islamic finance differs from conventional banking

4. Valid commercial contracts in Islamic finance

1The Islamic finance phenomenon

Introduction

The Islamic finance phenomenon

Why does Islamic finance exist?

Why is Islamic finance a sizeable and growing market?

Key challenges facing the industry

Conclusion

1 · The Islamic finance phenomenon

5

INTRODUCTION

Islamic finance is estimated to be an industry worth over a staggering $1.7 trillion1 in terms of global banking assets and is growing globally at more than 15 per cent per year. For some, it represents an opportunity to tap into a lucrative new market, while for others it is now necessary to provide services or products in this sector so that current or potential customers are not lost. This book seeks to equip practitioners with an understanding of the key concepts underpinning Islamic finance and the prevalent and devel-oping market practices. It will also explain the main product and service types and, where applicable, how they differ from comparable conventional finance instruments.

The book assumes the reader to have no previous knowledge of the subject. Islamic finance is a faith-based proposition and thus to understand the finance, one must understand key features of the faith. Therefore the first part of the book focuses on understanding more about the beliefs, values and principles that underpin the practice. The second part of the book looks at the application of Islamic finance by discussing the key transaction types and market practices and products.

Whether you are a banker, lawyer, asset manager, wealth manager, accountant or any person with an interest in Islamic finance, this text aims to give you a solid knowledge foundation of the area, a tool kit and frame of reference to understand and apply yourself to the sector. People may perceive Islamic finance to be mysterious, specialised and accessible only to Muslims, made worse by the use of jargon and foreign terminology. This book seeks to explain the guiding principles and practices with a clear, jargon-free narrative that defines any reference to foreign terminology. The book will also demonstrate that while Islamic finance is a faith-based propo-sition, it is underpinned by a few core principles which need not exclude any section of society from involvement, whether as a practitioner, supplier or consumer.

THE ISLAMIC FINANCE PHENOMENON

While Islamic assets represent only about 1 per cent of the global financial market,2 it has been the remarkable growth and the potential of the Islamic finance industry that have really captured the attention of governments, the financial services sector and other stakeholders such as regulators and central banks globally.

1 Ernst & Young, ‘World Islamic Banking Competitiveness Report 2013−14’.2 UKIF, ‘Islamic Finance Report – March 2012’.

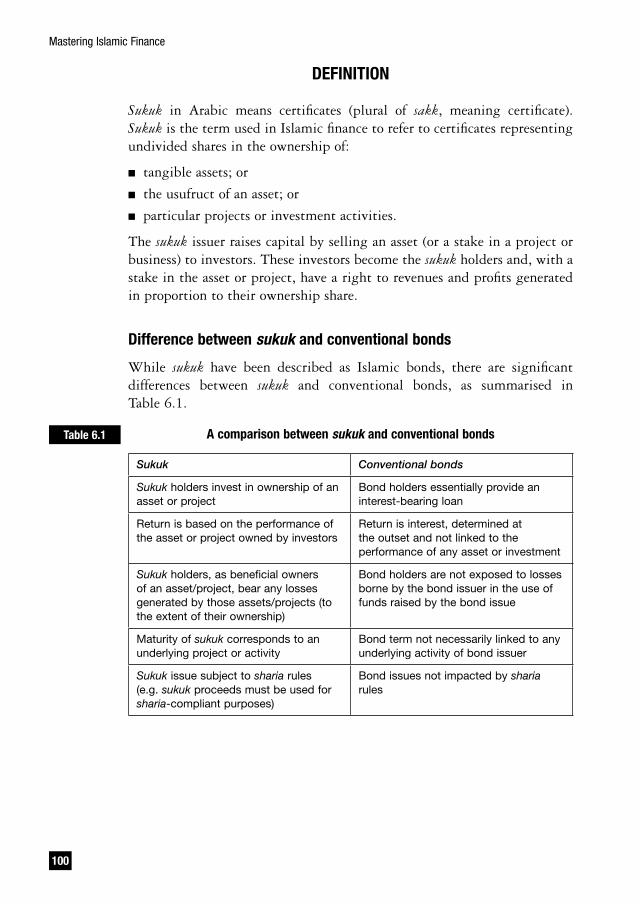

Mastering Islamic Finance

6

Global assets of Islamic financeFigure 1.1

2006

18001600140012001000800600400200

0

509

2007

$ Bn, assets end-year

677

2008

861

2009

933

2010

1130

2011

1289

2012

1631

2013

1700

Figure 1.1 shows this impressive growth in global Islamic banking assets.3

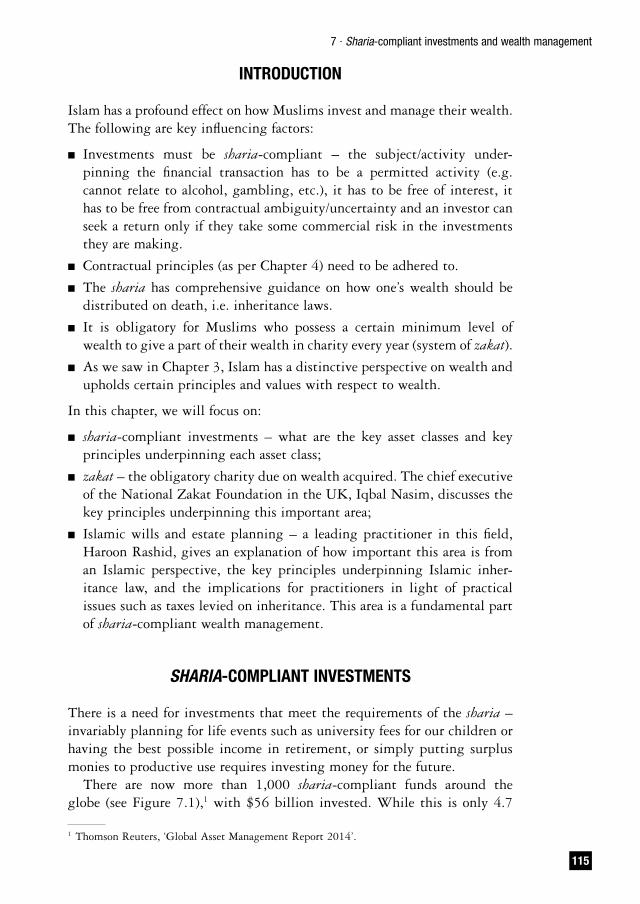

This growth has spurred interest in Islamic finance across the world and not just in predominantly Muslim countries. Institutions specialising in this sector, such as Islamic banks and Islamic insurance providers, have emerged. Islamic finance has also become significant for many mainstream institutions and service providers, especially large international law firms and investment banks. The Islamic finance industry is estimated to comprise 7164 firms offering services to the sector, spanning 61 countries in the East and West, and an estimated 38 million customers globally with Islamic banks.5 Banks account for the bulk of Islamic assets globally, with Islamic insurance and investment funds making up the rest. There are now more than 1,000 sharia-compliant funds around the globe with assets under management of more than $60 billion.6

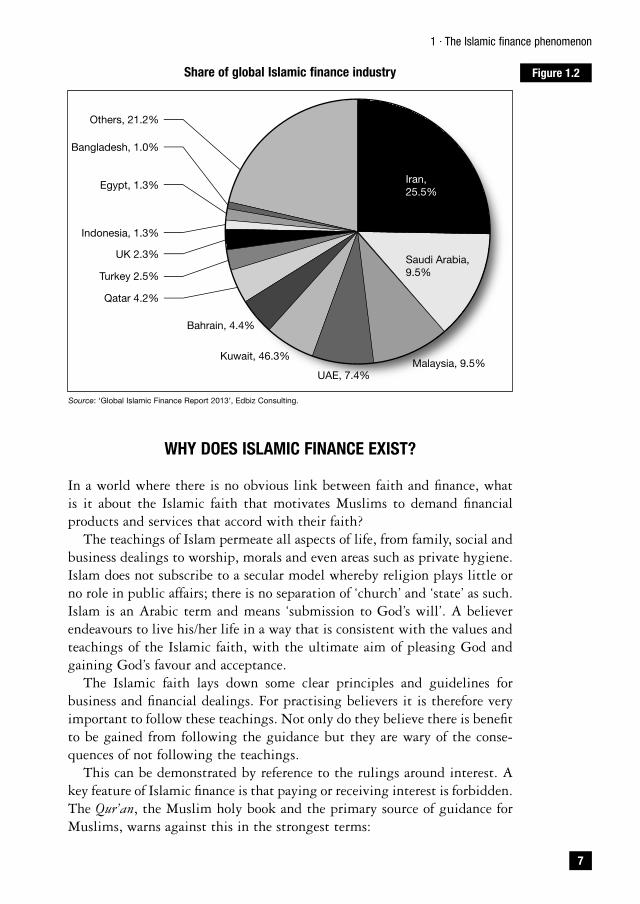

Although three-quarters of Islamic finance assets worldwide are in Muslim countries, the UK (at 2.3 per cent) and ‘others’ (countries with less than 1 per cent of the market – see Figure 1.2) are notable exceptions.

3 ‘Islamic Finance Report’, City UK, October 2013. Figure for 2013 from Ernst & Young, ‘World Islamic Banking Competitiveness Report, 2013−14’.

4 ‘Opportunities for Islamic finance in the UK’ (www.gov.uk/government/news/opportunities-for-islamic-finance-in-the-uk).

5 Ernst & Young, ‘World Islamic Banking Competitiveness Report 2013−14’.6 Ernst & Young, ‘Islamic Funds & Investment Report 2011’.

1 · The Islamic finance phenomenon

7

WHY DOES ISLAMIC FINANCE EXIST?

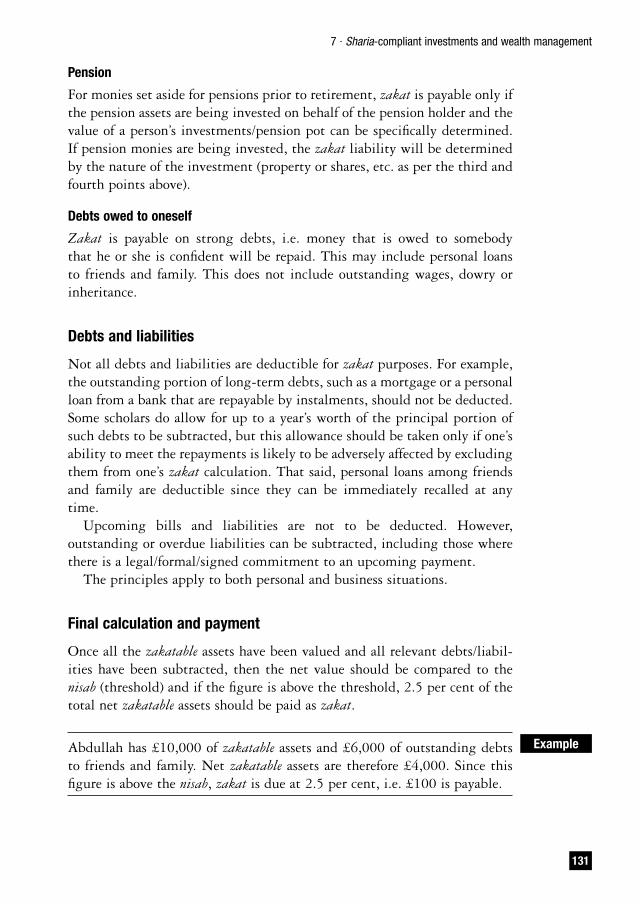

In a world where there is no obvious link between faith and finance, what is it about the Islamic faith that motivates Muslims to demand financial products and services that accord with their faith?

The teachings of Islam permeate all aspects of life, from family, social and business dealings to worship, morals and even areas such as private hygiene. Islam does not subscribe to a secular model whereby religion plays little or no role in public affairs; there is no separation of ‘church’ and ‘state’ as such. Islam is an Arabic term and means ‘submission to God’s will’. A believer endeavours to live his/her life in a way that is consistent with the values and teachings of the Islamic faith, with the ultimate aim of pleasing God and gaining God’s favour and acceptance.

The Islamic faith lays down some clear principles and guidelines for business and financial dealings. For practising believers it is therefore very important to follow these teachings. Not only do they believe there is benefit to be gained from following the guidance but they are wary of the conse-quences of not following the teachings.

This can be demonstrated by reference to the rulings around interest. A key feature of Islamic finance is that paying or receiving interest is forbidden. The Qur’an, the Muslim holy book and the primary source of guidance for Muslims, warns against this in the strongest terms:

Share of global Islamic finance industry Figure 1.2

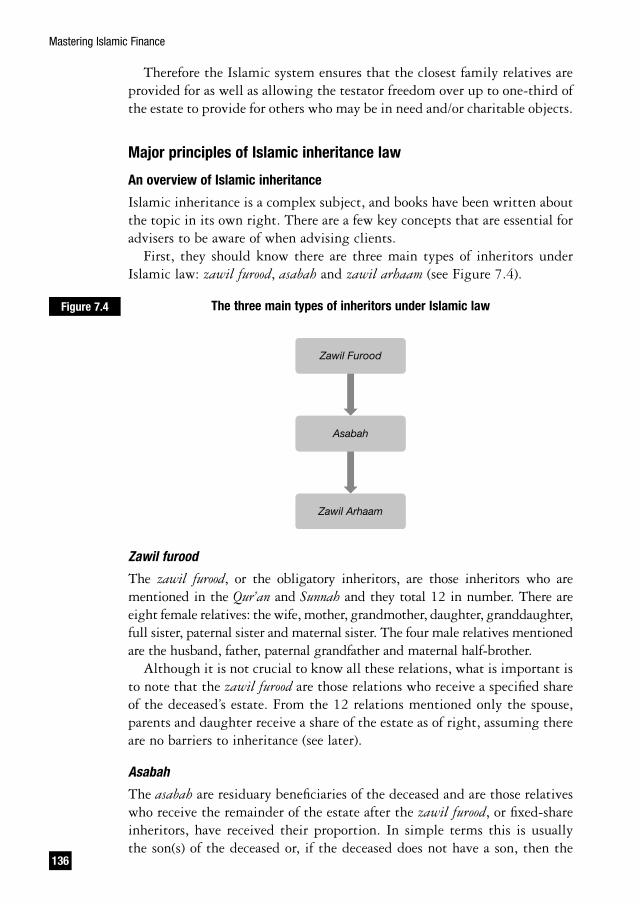

Source: ‘Global Islamic Finance Report 2013’, Edbiz Consulting.

Bangladesh, 1.0%

Indonesia, 1.3%

Egypt, 1.3%

UK 2.3%

Turkey 2.5%

Qatar 4.2%

Bahrain, 4.4%

Kuwait, 46.3%

UAE, 7.4%Malaysia, 9.5%

Saudi Arabia,9.5%

Iran,25.5%

Others, 21.2%

Mastering Islamic Finance

8

Those who take interest will not stand on the Day of Judgement except as he who has been driven mad by the touch of the devil. That is because they have said, ‘trading is like interest’, but God has permitted trading and prohibited interest. Whosoever receives an advice from his Lord and stops, he is allowed what has passed and his matter is up to God. And those who revert back are the people of the Hellfire. O you who believe! Fear God and give up what remains due to you from interest if you are really believers; and if you do not, then take notice of war from God and his Messenger, but if you repent you shall have your capital sums. Deal not unjustly and you shall not be dealt with unjustly.

(Qur’an, Chapter 2, verses 278–279)

Based on the above passage from the Qur’an alone, the seriousness of the issue of interest is obvious. Much of conventional finance is underpinned by interest; theoretically it is very difficult for Muslims to engage with the industry at all. Of course, Muslims have the same need for financial services as any other group in societies across the world, whether that is in relation to business, purchasing properties, investing or protection. It is no surprise, therefore, that increasing numbers of Muslims seek to fulfil this need in compliance with their religious duties.

WHY IS ISLAMIC FINANCE A SIZEABLE AND GROWING MARKET?

Islam is an ancient religion and yet it seems that Islamic finance has only relatively recently emerged as a significant industry. The reality is that Islamic finance is as old as the religion itself. However, a number of developments in the second half of the twentieth century have driven the importance and growth of the industry. Broadly, these can be summa-rised as:

■ growth of the Muslim population worldwide leading to rising promi-nence of the Islamic faith in the world;

■ the economic development of countries with large Muslim populations leading to rising affluence among Muslims;

■ the greater integration of Muslim and non-Muslim economies (which may be considered to be a function of globalisation) leading to institu-tions tapping the liquidity of Muslim nations.

Key growth factors

Rising prominence of the Islamic faith in the world

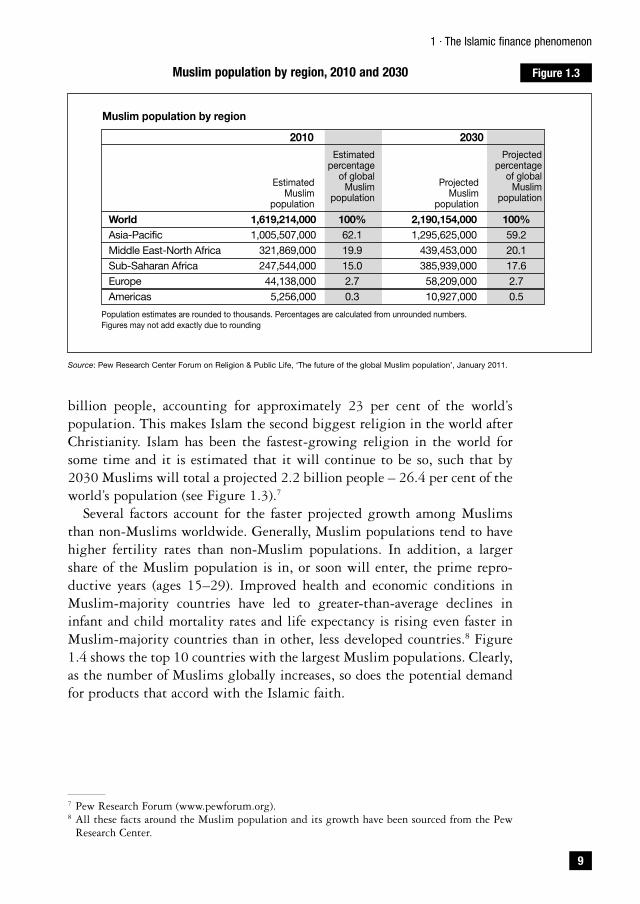

It is estimated that Muslims around the world total in the region of 1.6

1 · The Islamic finance phenomenon

9

Muslim population by region, 2010 and 2030 Figure 1.3

Source: Pew Research Center Forum on Religion & Public Life, ‘The future of the global Muslim population’, January 2011.

billion people, accounting for approximately 23 per cent of the world’s population. This makes Islam the second biggest religion in the world after Christianity. Islam has been the fastest-growing religion in the world for some time and it is estimated that it will continue to be so, such that by 2030 Muslims will total a projected 2.2 billion people – 26.4 per cent of the world’s population (see Figure 1.3).7

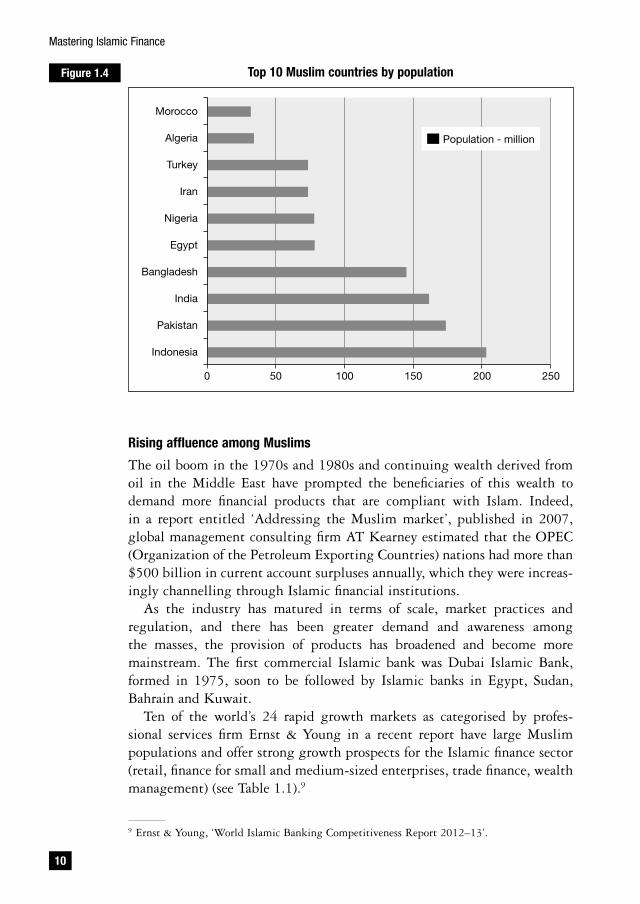

Several factors account for the faster projected growth among Muslims than non-Muslims worldwide. Generally, Muslim populations tend to have higher fertility rates than non-Muslim populations. In addition, a larger share of the Muslim population is in, or soon will enter, the prime repro-ductive years (ages 15–29). Improved health and economic conditions in Muslim-majority countries have led to greater-than-average declines in infant and child mortality rates and life expectancy is rising even faster in Muslim-majority countries than in other, less developed countries.8 Figure 1.4 shows the top 10 countries with the largest Muslim populations. Clearly, as the number of Muslims globally increases, so does the potential demand for products that accord with the Islamic faith.

7 Pew Research Forum (www.pewforum.org).8 All these facts around the Muslim population and its growth have been sourced from the Pew

Research Center.

WorldAsia-PacificMiddle East-North AfricaSub-Saharan AfricaEuropeAmericas

1,619,214,0001,005,507,000

321,869,000247,544,00044,138,0005,256,000

Estimated Muslim

population

Population estimates are rounded to thousands. Percentages are calculated from unrounded numbers.Figures may not add exactly due to rounding

ProjectedMuslim

population

Estimated percentage

of globalMuslim

population

Projectedpercentage

of globalMuslim

population

2,190,154,0001,295,625,000

439,453,000385,939,00058,209,00010,927,000

100%62.119.915.02.70.3

100%59.220.117.62.70.5

2010

Muslim population by region

2030

Mastering Islamic Finance

10

Top 10 Muslim countries by population Figure 1.4

Rising affluence among Muslims

The oil boom in the 1970s and 1980s and continuing wealth derived from oil in the Middle East have prompted the beneficiaries of this wealth to demand more financial products that are compliant with Islam. Indeed, in a report entitled ‘Addressing the Muslim market’, published in 2007, global management consulting firm AT Kearney estimated that the OPEC (Organization of the Petroleum Exporting Countries) nations had more than $500 billion in current account surpluses annually, which they were increas-ingly channelling through Islamic financial institutions.

As the industry has matured in terms of scale, market practices and regulation, and there has been greater demand and awareness among the masses, the provision of products has broadened and become more mainstream. The first commercial Islamic bank was Dubai Islamic Bank, formed in 1975, soon to be followed by Islamic banks in Egypt, Sudan, Bahrain and Kuwait.

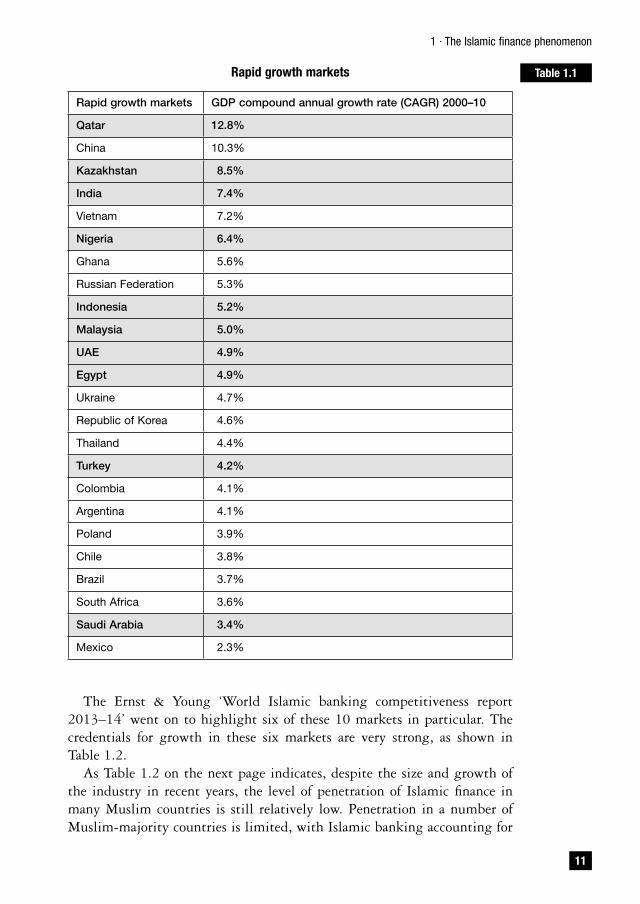

Ten of the world’s 24 rapid growth markets as categorised by profes-sional services firm Ernst & Young in a recent report have large Muslim populations and offer strong growth prospects for the Islamic finance sector (retail, finance for small and medium-sized enterprises, trade finance, wealth management) (see Table 1.1).9

9 Ernst & Young, ‘World Islamic Banking Competitiveness Report 2012–13’.

0 50 100 150 200 250

Morocco

Algeria

Turkey

Iran

Nigeria

Egypt

Bangladesh

India

Pakistan

Indonesia

Population - million

1 · The Islamic finance phenomenon

11

Rapid growth markets

Rapid growth markets GDP compound annual growth rate (CAGR) 2000–10

Qatar 12.8%

China 10.3%

Kazakhstan 8.5%

India 7.4%

Vietnam 7.2%

Nigeria 6.4%

Ghana 5.6%

Russian Federation 5.3%

Indonesia 5.2%

Malaysia 5.0%

UAE 4.9%

Egypt 4.9%

Ukraine 4.7%

Republic of Korea 4.6%

Thailand 4.4%

Turkey 4.2%

Colombia 4.1%

Argentina 4.1%

Poland 3.9%

Chile 3.8%

Brazil 3.7%

South Africa 3.6%

Saudi Arabia 3.4%

Mexico 2.3%

Table 1.1

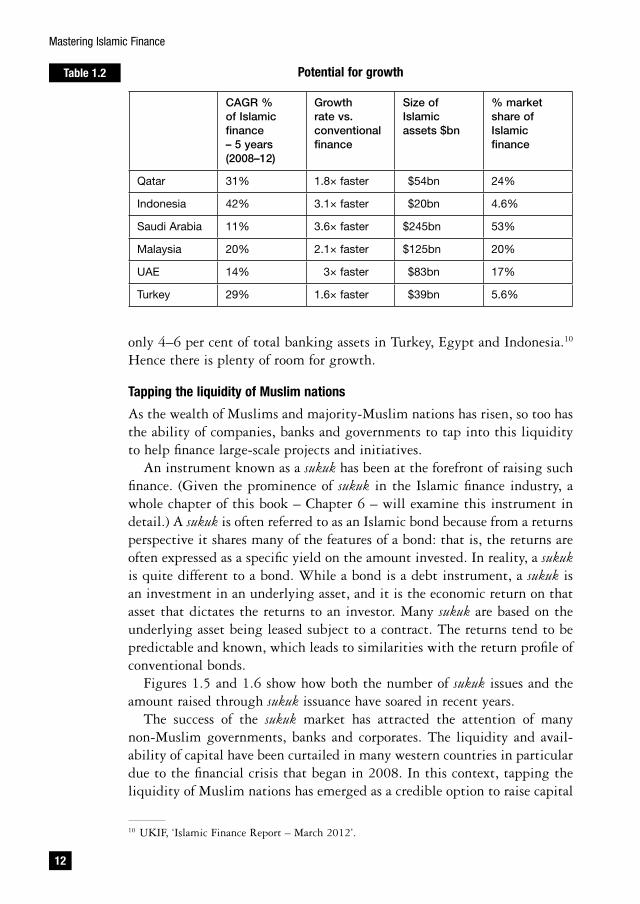

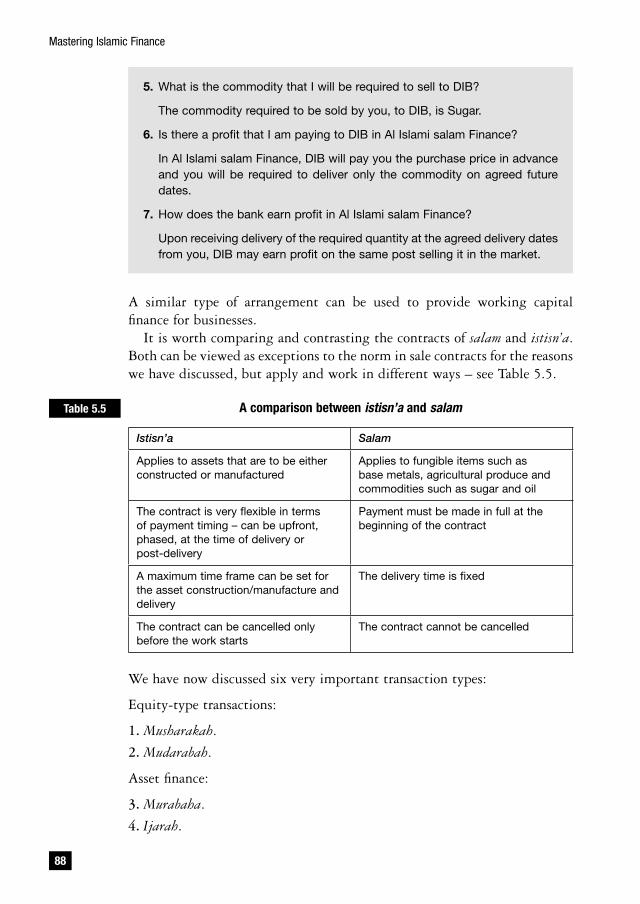

The Ernst & Young ‘World Islamic banking competitiveness report 2013–14’ went on to highlight six of these 10 markets in particular. The credentials for growth in these six markets are very strong, as shown in Table 1.2.

As Table 1.2 on the next page indicates, despite the size and growth of the industry in recent years, the level of penetration of Islamic finance in many Muslim countries is still relatively low. Penetration in a number of Muslim-majority countries is limited, with Islamic banking accounting for

Mastering Islamic Finance

12

only 4–6 per cent of total banking assets in Turkey, Egypt and Indonesia.10 Hence there is plenty of room for growth.

Tapping the liquidity of Muslim nations

As the wealth of Muslims and majority-Muslim nations has risen, so too has the ability of companies, banks and governments to tap into this liquidity to help finance large-scale projects and initiatives.

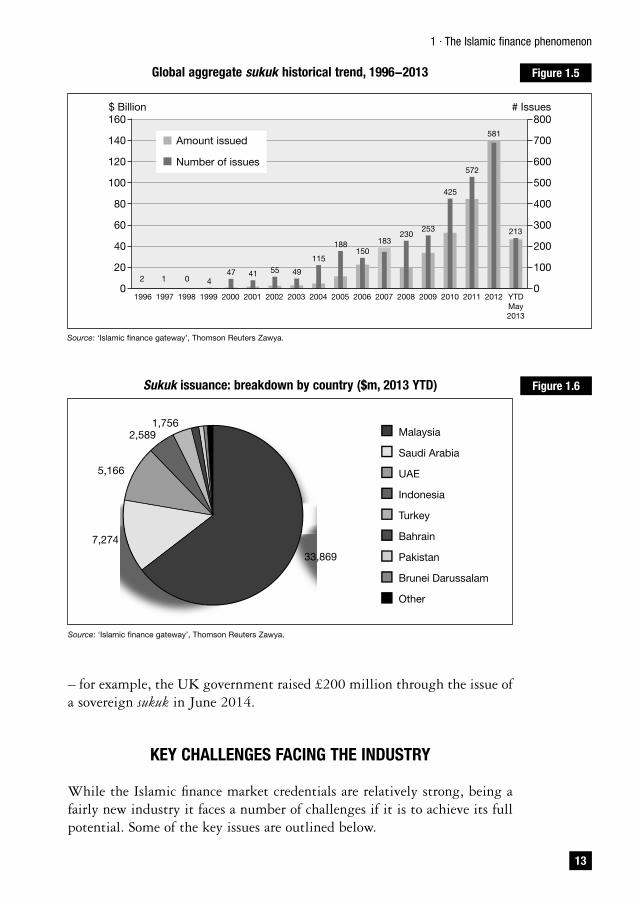

An instrument known as a sukuk has been at the forefront of raising such finance. (Given the prominence of sukuk in the Islamic finance industry, a whole chapter of this book – Chapter 6 – will examine this instrument in detail.) A sukuk is often referred to as an Islamic bond because from a returns perspective it shares many of the features of a bond: that is, the returns are often expressed as a specific yield on the amount invested. In reality, a sukuk is quite different to a bond. While a bond is a debt instrument, a sukuk is an investment in an underlying asset, and it is the economic return on that asset that dictates the returns to an investor. Many sukuk are based on the underlying asset being leased subject to a contract. The returns tend to be predictable and known, which leads to similarities with the return profile of conventional bonds.

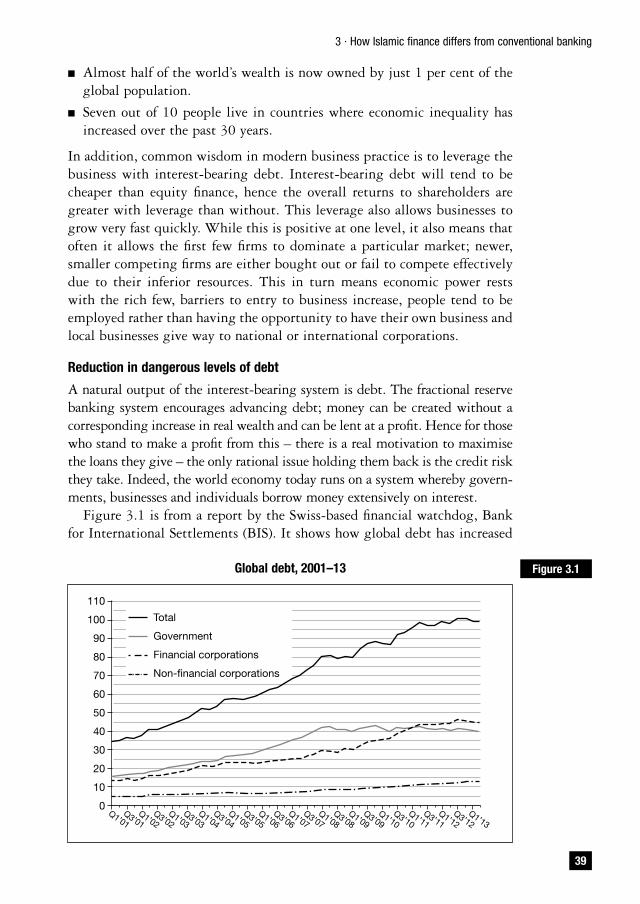

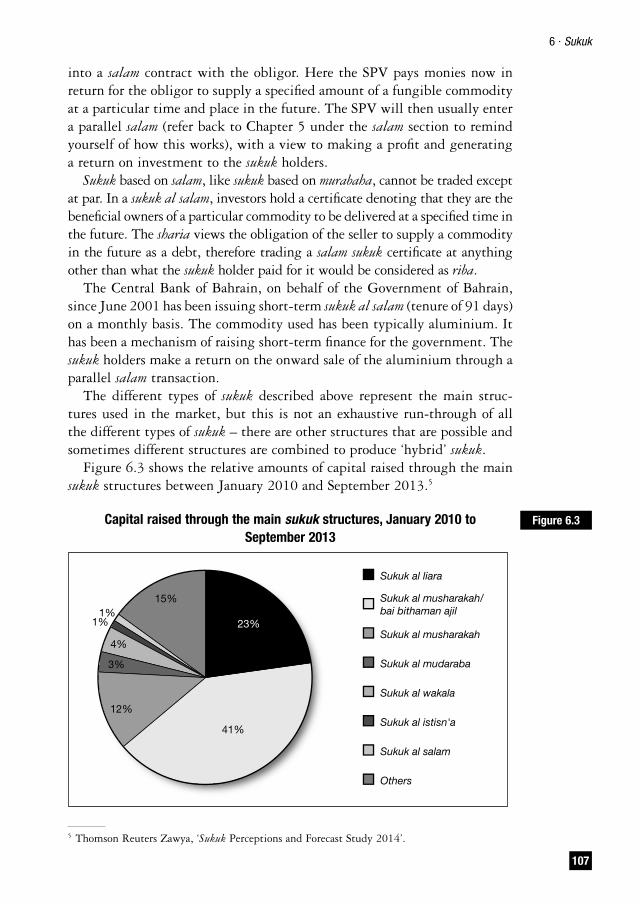

Figures 1.5 and 1.6 show how both the number of sukuk issues and the amount raised through sukuk issuance have soared in recent years.

The success of the sukuk market has attracted the attention of many non-Muslim governments, banks and corporates. The liquidity and avail-ability of capital have been curtailed in many western countries in particular due to the financial crisis that began in 2008. In this context, tapping the liquidity of Muslim nations has emerged as a credible option to raise capital

10 UKIF, ‘Islamic Finance Report – March 2012’.

Potential for growth

CAGR % of Islamic finance – 5 years (2008–12)

Growth rate vs. conventional finance

Size of Islamic assets $bn

% market share of Islamic finance

Qatar 31% 1.8× faster $54bn 24%

Indonesia 42% 3.1× faster $20bn 4.6%

Saudi Arabia 11% 3.6× faster $245bn 53%

Malaysia 20% 2.1× faster $125bn 20%

UAE 14% 3× faster $83bn 17%

Turkey 29% 1.6× faster $39bn 5.6%

Table 1.2

1 · The Islamic finance phenomenon

13

Global aggregate sukuk historical trend, 1996−2013 Figure 1.5

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 YTDMay2013

160

140

120

100

80

60

40

20

0

Amount issued

$ Billion # Issues

Number of issues

213

800

700

600

500

400

300

200

100

0

581

572

425

253230

183150

188

115

495541474012

Source: ‘Islamic finance gateway’, Thomson Reuters Zawya.

Sukuk issuance: breakdown by country ($m, 2013 YTD) Figure 1.6

Source: ‘Islamic finance gateway’, Thomson Reuters Zawya.

33,869

7,274

5,166

2,5891,756

Malaysia

Saudi Arabia

UAE

Indonesia

Turkey

Bahrain

Pakistan

Brunei Darussalam

Other

– for example, the UK government raised £200 million through the issue of a sovereign sukuk in June 2014.

KEY CHALLENGES FACING THE INDUSTRY

While the Islamic finance market credentials are relatively strong, being a fairly new industry it faces a number of challenges if it is to achieve its full potential. Some of the key issues are outlined below.

Mastering Islamic Finance

14

Regulatory environment

As any industry matures, the infrastructure around it needs to develop. One of the key parts of this infrastructure is regulation. The financial services industry in particular is highly regulated throughout the world and it is important that regulation for the Islamic finance industry develops to:

■ give it a level playing field versus conventional finance in terms of taxes and other areas;

■ make products and services more portable across borders;

■ standardise, as much as practically possible, sharia rulings, documen-tation and accounting treatment.

Sharia authenticity

A key success factor in the development of Islamic finance is for the industry to remain true to the spirit and objectives of the Islamic teachings. After all, the industry is a faith-based proposition; the faith is centred on certain social and ethical values. If these are hijacked or diluted at the expense of commercial ends, the industry will lose credibility in the medium to long term and will not fulfil its potential. Practices such as commodity murabaha (described in detail in Chapter 5), a synthetic transaction designed to overcome the prohibition of interest by using a metal trade, have probably damaged the credibility of the industry. Product providers need to innovate and bring products to the market that the consumers want but are true to the spirit and objectives of the sharia.

Another dimension to this issue of sharia authenticity is for product providers to be bold enough to bring new products to the market that do not simply seek to mimic the economic effect of conventional products, but are potentially very different and present a real alternative to conventional products. For example, instead of using commodity murabaha, industry players need to be bold enough to practise other techniques in which there is a genuine trade and/or profit and loss sharing.

Scale

As mentioned earlier, Islamic finance represents about 1 per cent of the global financial market. In the short time frame of the modern Islamic finance industry (around 40 years), it is clear from empirical research that the overwhelming majority of Muslim consumers want sharia-compliant products that come with a competitive price and service compared to similar products in the conventional space. Two good examples of where scale is required to achieve competitive pricing are retail banking and protection/

1 · The Islamic finance phenomenon

15

insurance. In both of these areas, sharia-compliant providers have struggled to compete effectively with conventional players. The Islamic finance industry needs to build scale and achieve world-class operational efficiency and service standards.

Islamic finance for all

Naturally, adherence to Islamic teachings and principles appeals to Muslims. However, the objectives of the sharia (called maqasid al sharia) are very much rooted in protecting and promoting the welfare of individuals and society as a whole. Indeed, a well-known Islamic scholar, Imam Abu Hamid Al-Ghazali (died 1111 ce), summarised the objective of the sharia as follows:

The very objective of the sharia is to promote the well-being of the people, which lies in safeguarding their faith (deen), their lives (nafs), their intellect (ñaql), their posterity (nasl), and their wealth (mal).Whatever ensures the safeguarding of these five serves public interest and is desirable, and whatever hurts them is against public interest and its removal is desirable.

In this context, Islamic finance can be presented to Muslim and non-Muslims as an ethical form of finance, the principles of which aim to promote the well-being of society. Hence there is a real opportunity to make Islamic finance more appealing and inclusive to all and present it as a real, viable alternative to conventional finance. Indeed, in the wake of the recent global financial crisis, many around the world have questioned conventional financial products and systems and there has been something of a resurgence in looking at alternative products and systems.

The human capital challenge

For an industry growing at more than 15 per cent a year, it is widely recognised that a key enabler for this growth to continue is to have the right amount and quality of human capital coming through. In an article by Nazneen Halim, editor of Islamic Finance News, she says it is anticipated by 2015 that more than 50,000 individuals will be needed in the Islamic finance industry globally.11 This will require the training and education of professionals serving this industry and attracting and retaining the best possible talent to the industry. Professionals from outside of Islamic finance have a lot to offer the industry – they can bring valuable profes-sional experience to the table and help Islamic finance players achieve best commercial practice, operational efficiency and world-class service standards.

11 Halim, N. (2013) ‘Transforming Islamic finance – the human capital challenge 2013’, Islamic Finance News.

Mastering Islamic Finance

16

One aspect to the human capital challenge facing the Islamic finance industry is to ensure there are enough new sharia scholars coming through who understand the financial system and regulatory environment enough to provide sharia advice that is rooted in the realities of the legal, regulatory and commercial environments.

All of the above issues are recognised in the industry and there is much debate and discourse on these. We will revisit several of these areas in the last chapter of the book, ‘Chapter 9,’ The future of Islamic finance’.

CONCLUSION

In summary, the religious imperative for Muslims to follow the teachings of their faith, coupled with demographic and other changes in the Muslim world rooted in wealth and population growth, has made Islamic finance an attractive market segment. A quote from information provider Thomson Reuters in the marketing for its event entitled ‘The Global Islamic Economy Summit 2013’, which took place in Dubai in November 2013, sums it up well:

The Islamic economies of the world represent more than $8 trillion in GDP, and a 1.6 billion population growing at double the rate of the global population. Disposable income for the Islamic economy is estimated at $4.8 trillion – and with 62% of the population under the age of 30, the next generation of Muslims are increasingly asserting their Islamic sensi-tivities with everything from food preferences to banking and finance, to fashion, cosmetics, travel and healthcare.

The Islamic finance industry is young, developing and full of promise and opportunity. It has gone through and will continue to go through a number of growing pains, and needs to rise and overcome a number of challenges if it is to fulfil its potential. This book aims to take the reader on a journey in which the first step is to gain some appreciation of the faith from which this industry stems, then to appreciate the conceptual principles, values and economic framework pertinent to Islamic finance, and finally to look at the practice, application and key market segments of this industry. We finish with several opinion pieces on the future of the industry. By the end of this journey, my hope is that the reader will have a good grasp of the subject, feel empowered to engage with the industry, and is enlightened as to some of the key challenges, opportunities and imperatives the industry faces as it strives to forge ahead.

2Islam – key beliefs, principles

and practices

Introduction

Belief system

Key practices – the five pillars of action

Importance of the Qur’an and the Sunnah

Interpretation of the sharia

The role of scholars and sharia supervisory boards in Islamic finance

Conclusion

2 · Islam – key beliefs, principles and practices

19

INTRODUCTION

To understand Islamic finance it is important also to understand a little about the Islamic faith. Practitioners who have a base level of under-standing of the faith will not only comprehend the various principles underpinning sharia-compliant financial transactions better, but will be tuned into the mindset of a faith-based buyer of a sharia-compliant financial product. Indeed, all too often, those involved in the Islamic finance industry have shown a lack of understanding of the considerations important to those looking at sharia-compliant products from a faith perspective, and as a result certain products and services have not achieved their potential.

BELIEF SYSTEM

Islam is a monotheistic faith and at its very heart is the belief that there is One God who has no partner, associate or offspring; that this God created everything, including mankind – the first human being Adam. Furthermore, God sent Prophets to mankind through the ages to remind them and teach them that God was their Creator, and that they were charged with the responsibility to do good, uphold justice and to reject and fight against all wrong and evil. In addition to the Prophets, Muslims believe God sent scriptures through the ages as a means of advising and instructing mankind on how to live their lives. These scriptures include the Torah, the Bible and the Qur’an. Muslims believe that after death every person will be held accountable for what they did in their lives; that one day this world will come to an end and every person will be resurrected, and there will be a Day of Judgement. At this time, God will judge the deeds of each person and those who are successful will be admitted to Heaven for ever – a place full of joy and bliss – and those who are not successful will be admitted to Hell – a place of torment and punishment.

The six pillars of faith

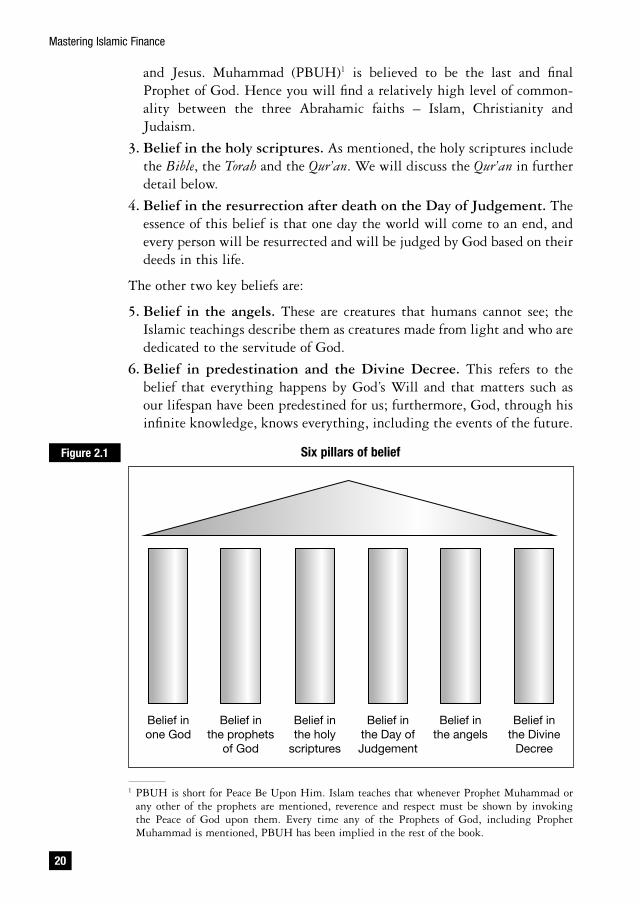

Indeed, the belief system of a Muslim is often summarised by reference to six key beliefs (see Figure 2.1), four of which are referred to explicitly above:

1. Belief in the One God. Muslims may refer to God by a number of names, Allah being the most common and coming from the root word illah, which means God. Other names refer to the attributes of God, e.g. Ar-Rahman (Most Merciful), Al-Karim (Most Generous), etc.

2. Belief in the Prophets of God. These include Noah, Abraham, Moses

Mastering Islamic Finance

20

and Jesus. Muhammad (PBUH)1 is believed to be the last and final Prophet of God. Hence you will find a relatively high level of common-ality between the three Abrahamic faiths – Islam, Christianity and Judaism.

3. Belief in the holy scriptures. As mentioned, the holy scriptures include the Bible, the Torah and the Qur’an. We will discuss the Qur’an in further detail below.

4. Belief in the resurrection after death on the Day of Judgement. The essence of this belief is that one day the world will come to an end, and every person will be resurrected and will be judged by God based on their deeds in this life.

The other two key beliefs are:

5. Belief in the angels. These are creatures that humans cannot see; the Islamic teachings describe them as creatures made from light and who are dedicated to the servitude of God.

6. Belief in predestination and the Divine Decree. This refers to the belief that everything happens by God’s Will and that matters such as our lifespan have been predestined for us; furthermore, God, through his infinite knowledge, knows everything, including the events of the future.

1 PBUH is short for Peace Be Upon Him. Islam teaches that whenever Prophet Muhammad or any other of the prophets are mentioned, reverence and respect must be shown by invoking the Peace of God upon them. Every time any of the Prophets of God, including Prophet Muhammad is mentioned, PBUH has been implied in the rest of the book.

Six pillars of beliefFigure 2.1

Belief inone God

Belief inthe prophets

of God

Belief inthe holy

scriptures

Belief inthe Day ofJudgement

Belief inthe angels

Belief inthe Divine

Decree

2 · Islam – key beliefs, principles and practices

21

KEY PRACTICES – THE FIVE PILLARS OF ACTION

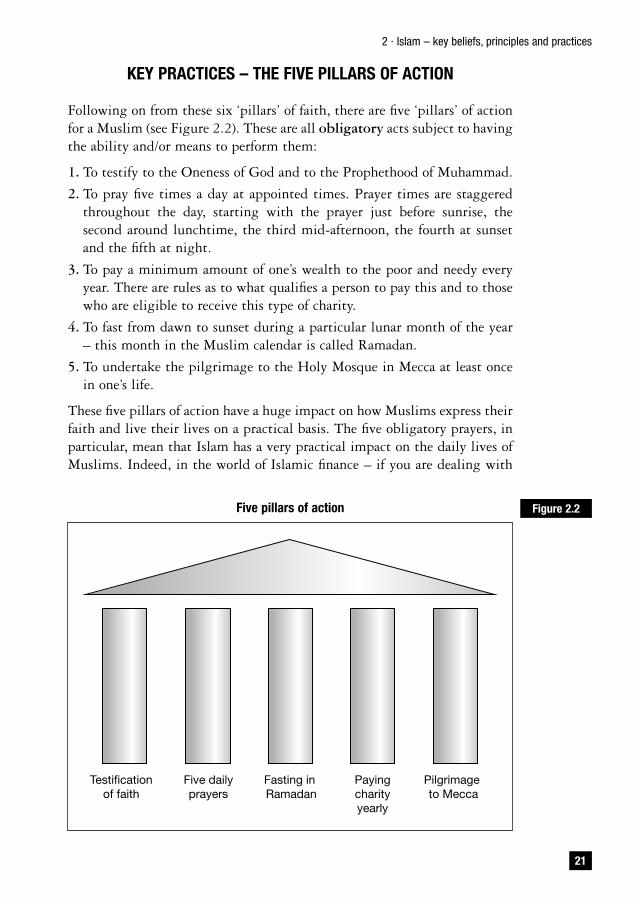

Following on from these six ‘pillars’ of faith, there are five ‘pillars’ of action for a Muslim (see Figure 2.2). These are all obligatory acts subject to having the ability and/or means to perform them:

1. To testify to the Oneness of God and to the Prophethood of Muhammad.

2. To pray five times a day at appointed times. Prayer times are staggered throughout the day, starting with the prayer just before sunrise, the second around lunchtime, the third mid-afternoon, the fourth at sunset and the fifth at night.

3. To pay a minimum amount of one’s wealth to the poor and needy every year. There are rules as to what qualifies a person to pay this and to those who are eligible to receive this type of charity.

4. To fast from dawn to sunset during a particular lunar month of the year – this month in the Muslim calendar is called Ramadan.

5. To undertake the pilgrimage to the Holy Mosque in Mecca at least once in one’s life.

These five pillars of action have a huge impact on how Muslims express their faith and live their lives on a practical basis. The five obligatory prayers, in particular, mean that Islam has a very practical impact on the daily lives of Muslims. Indeed, in the world of Islamic finance – if you are dealing with

Five pillars of action Figure 2.2

Testificationof faith

Five dailyprayers

Fasting in Ramadan

Payingcharityyearly

Pilgrimage to Mecca

Mastering Islamic Finance

22

Islamic banks or go to Islamic finance conferences – there will almost always be facilities for prayers. Also you will often find Muslim work colleagues or clients requesting a place to pray so that they can fulfil their duty to pray at prescribed times.

Another key practical element of Islamic faith is the importance of the holy day, Friday. Muslims are required to attend a congregational prayer at the time of the normal daily lunchtime prayer on a Friday. Hence in Muslim countries such as Saudi Arabia, the weekend is set to include Friday and it is a day off for most people. In Europe and other non-Muslim countries, you will see Muslims making an effort to go to their local mosque during their lunch break to fulfil the obligation to pray in congregation on a Friday and hear the sermon delivered by the leader of the congregation, known as the imam. Knowing this is important if and when you engage in work related to Islamic finance as you will be mindful of the client’s/colleague’s requirement to pray, about inappropriate times to request meetings such as Friday lunch-times, and so on.

Throughout the year there are key events and dates to be aware of. The ones with the greatest impact are Ramadan, the month of fasting, and the pilgrimage season. In both cases in Muslim countries there will be public holidays at these times; in non-Muslim countries you will find that many Muslims generally have time off or change their working patterns. Indeed, it is often commented that things become very quiet in the Muslim world in terms of work and trade during the month of Ramadan, as priorities are redirected to family and spiritual development.

The six pillars of faith and the five pillars of action referred to above start to give you a framework of the Islamic faith in terms of beliefs and key practices. In Chapter 3, we will discuss how Islam views money and wealth, which will further help you to understand the mindset of a practising Muslim when entering into commercial and financial transactions.

IMPORTANCE OF THE QUR’AN AND THE SUNNAH

An important question to answer is: ‘What are the key sources of knowledge upon which the Islamic teachings are based?’

The two foremost sources are the Qur’an, the holy book, and the Sunnah, the example of the Prophet Muhammad. Let us discuss each of these in turn.

The Qur’anThe Qur’an is the Muslim holy book. It has a very high status in Islam because Muslims believe it to be the literal word of God. Muslims believe

2 · Islam – key beliefs, principles and practices

23

that it was revealed to Prophet Muhammad over a period of 23 years by God through the Angel Gabriel. Angel Gabriel would visit the Prophet every so often during this period, each time revealing certain verses of the Qur’an.

Due to this belief that the Qur’an is the literal word of God and therefore in essence it is as though God is talking directly to mankind, the Qur’an is held in the highest esteem by Muslims and is regarded as the foremost source for Islamic knowledge and guidance. Indeed, a significant proportion of Muslims will make it part of their daily routine to read a portion of the Qur’an, and many millions have committed the entire book to memory.

The Qur’an is written in Arabic and its translation can be found in most languages. The key principles pertaining to Islamic finance, such as the prohibition of interest, can be seen in the teachings of the Qur’an.

The SunnahThe Sunnah refers to the example and teachings of the Prophet Muhammad. It is very clear from the Qur’an that the believers are required to follow the example and teachings of the Prophet. Qur’anic verses:

O believers obey Allah, obey the Messenger and those in authority among you. If you dispute about anything, refer it to Allah and the Messenger.

(Chapter 4, verse 59)

And whatever the Messenger gives you, accept it, and from whatever he forbids you, keep back, and be careful of your duty to Allah.

(Chapter 59, verse 7)

The status of the Prophet Muhammad is also very high in Islam. Muslims believe Muhammad to be the last Messenger of God. He was born in Mecca in what is now known as Saudi Arabia in 571 ad. His life history has been well documented and we see that in his youth he earned respect as being a person of integrity and truth, often referred to as ‘Al-Amin’ (the trustworthy).

It was the Prophet’s job to provide an example and practical model in terms of implementing God’s teachings. For instance, it was commanded by God to pray in the Qur’an, but it was through the example and teachings of Prophet Muhammad that Muslims know how to carry out the prayers in practice.

Given the status of the Prophet and the importance of following his example and teachings, his life and sayings have been extensively recorded and have been the subject of much scrutiny and study. His recorded sayings are referred to as the hadith and have been the subject of intense verification by scholars with respect to their authenticity. As a result, today we have

Mastering Islamic Finance

24

books of hadith, or the Prophet’s sayings, in which the recorded sayings are categorised according to the strength of their validation.

The primary sources of teachings pertaining to Islamic finance are the Qur’an and the Sunnah, which provide the basis for Islamic finance. You will often hear the word sharia mentioned in the context of Islamic finance. Sharia refers to the framework of rules, principles and guidance derived from the Islamic teachings, primarily from the Qur’an and Sunnah. Sometimes, sharia is referred to also as Islamic law and often, in the context of Islamic finance, products are referred to as sharia-compliant.

INTERPRETATION OF THE SHARIA

Accepting that the Qur’an and the Sunnah are the prime sources of knowledge for Islamic finance does not mean that there cannot be differences in inter-pretation. However, it is important to appreciate that these are not usually disputes of principle but of application. It may be helpful to understand the background to these differences of interpretation.

The interpretation and detailed rulings coming out of the study of the Qur’an and Sunnah is called fiqh in Arabic. Such work falls to sharia scholars, who have studied the sharia in depth and therefore have the requisite knowledge to perform this role. The role is analogous to a lawyer who inter-prets statute and case law. This is relevant to the field of Islamic finance as scholars may sometimes have different opinions or views on the permissi-bility or otherwise of certain financial products and structures.

There are some important points to note on these differences of opinion/schools of thought:

1. The differences do not usually emanate from the key underlying principles but from the detailed rules around application.

2. Islam essentially has two broad divisions – the Sunnis and the Shias. Again the pillars of faith and action are essentially the same. The key differences relate to opposing views on the succession of leadership after the Prophet’s death. Of the world’s Muslim population, 87–90 per cent are Sunni and 10–13 per cent are Shia.2

3. Within the Sunnis there are four established schools of thought, named after the scholars who produced detailed works on their interpretation of the sharia. These school of thought are:

■ The Hanafi school of thought: named after Imam Abu Hanifa (703–767 ce). This school originates from Iraq and is the dominant school of thought in the Indian sub-continent and Turkey.

2 Pew Research Center: ‘Religion & public life project’.

2 · Islam – key beliefs, principles and practices

25

■ The Maliki school of thought: named after Imam Malik (717–801 ce). This school originates from Medina in Saudi Arabia.

■ The Sha’afi school of thought: named after Imam Shafi (769–820 ce). This school of thought emerged in Egypt.

■ The Hanbali school of thought: named after Imam Hanbal (778–855 ce). This school originates from Damascus and is particularly influ-ential in Saudi Arabia and the Arabian Gulf region.

Imam Shafi advocated an approach to interpreting the sharia, which is widely used by contemporary scholars. He recommended that the following hierarchical order be used when interpreting the sharia:

1. The Qur’an.

2. The Sunnah.

3. Ijma – consensus of the scholars.

4. Qiyas – analogy, that is to derive rulings for a particular situation based on established rulings for other scenarios, where there is a clear analogy with the situation being considered.

These scholars were alive either at the same time or in adjacent time periods. It is well documented that they had a healthy respect for each other and the differences of opinion they had were mutually respected, and even still today one school of thought is not seen as superior to another. Within the Sunnis all of the four schools are seen as valid.

The main school of thought within the Shia sect is referred to as the Jaafri school, named after Imam Jaafar. Although Shias represent a minority in terms of the global Muslim population, it is the dominant sect in Iran, which has the largest share of the global Islamic finance market.

Outside of these schools of thought, contemporary scholars play the role of interpreting the sharia in relation to subjects, situations or topics not expressly covered in the Qur’an and the Sunnah and the established and accepted schools of thought.

In the contemporary world, it is worth noting that there is a body called the Islamic Fiqh Academy, set up by the Organisation of the Islamic Conference (OIC) in 1981. The Academy is based in Jeddah and its members comprise sharia scholars and experts in science, economic and social issues from around the world. Its role is to debate and provide guidance on contem-porary issues.

In terms of Islamic finance, therefore you will find sharia scholars having differences of opinion on certain matters emanating sometimes from the differences between the established schools of thought, and other times from their interpretation of the sharia.

Mastering Islamic Finance

26

THE ROLE OF SCHOLARS AND SHARIA SUPERVISORY BOARDS IN ISLAMIC FINANCE

When Islamic banks and other organisations in the Islamic finance industry bring products to the market, it is necessary that they make sure that the products are sharia-compliant. Usually qualified scholars, who have the requisite level of knowledge, are engaged to verify whether the products are compliant and to sign off the products before they go to market. This opinion/certification by scholars is called a fatwa. Scholars in making their assessment and forming their opinion will rely first and foremost on the teachings within the Qur’an and the Sunnah. If no direct ruling or precedent relevant to the situation at hand can be found from these, scholars will use their knowledge of the sharia to come up with a ruling that is compatible with the principles and values underpinning the Islamic teachings.

Scholars play a key role in the Islamic finance industry. Scholars are charged with making sure that the product design, key features and legal documen-tation such as product prospectuses are in line with the sharia, as well as ensuring the product implementation and practice remain sharia-compliant. To this end, most Islamic finance institutions usually commission an annual sharia audit and the resulting report generally features in the institution’s published financial statements.

The model of engaging scholars is not the same across the global Islamic finance industry.

The Malaysian model

Malaysia is often cited as the most advanced nation when it comes to the legal, institutional, research/educational and regulatory framework it has built for the Islamic finance industry. A key reason for this success and progression has been the political will and commitment from the government to develop Malaysia as a world leader in Islamic finance, and to have the best-in-class infrastructure to support this. Malaysia in 1983 passed an official Islamic Banking Act creating a dual banking system in the country – the conventional banking system and the Islamic system. The fruits of this comprehensive and cohesive national approach orches-trated from the top can be seen in the increasing popularity and growth of sharia-compliant products in the country, the high quality of Islamic finance research produced in Malaysia, and Malaysia’s increasing profile and market share of the global Islamic finance market, as seen in Chapter 1. Malaysia is the only country to have a university, The Global University of Islamic Finance (INCIEF) dedicated to Islamic finance and a government research institute dedicated to Islamic finance, International Shari’ah Research Academy of Islamic Finance (ISRA).

2 · Islam – key beliefs, principles and practices

27

Malaysia has tackled the need for sharia scholars by creating a national central supervisory board. If any organisation wants to launch a sharia-compliant product it needs to get approval and certification from this central board. Individual banks or other organisations can have their own sharia advisers or scholars but ultimately sign-off has to come from the central board.

Model outside of Malaysia

Outside of Malaysia the dominant model is for individual banks and other organisations to have their own respective sharia supervisory boards. These boards will typically have at least three scholars who are engaged to ensure the products and services of the bank/other organisation are sharia-compliant and remain so.

This model prevalent outside of Malaysia is reflective of Islamic finance in these countries being more of a commercial phenomenon driven by commercial organisations with limited governmental involvement and political will to create a cohesive national and institutional infrastructure. In my view the Malaysian model is far superior, with the role of scholars being a very good example. With a central board, two key advantages result:

1. There is consistency in judgement as to what scholars will approve as sharia-compliant. Without this, we have seen examples in the market whereby a particular sharia supervisory board will approve a product, while another does not.

2. It removes a potential conflict of interest. It is conceivable that if a scholar is employed and paid by a bank, he/she may be put under pressure to approve products, or that there may be the perception of a lack of impar-tiality, which may be equally damaging. By having a central board that is not paid or engaged by the bank/other organisation seeking product approval, this problem does not arise.

CONCLUSION

This chapter has provided a summary of the key beliefs underpinning the Islamic faith and the key sources of knowledge with respect to Islamic teachings. We discussed that Islamic law (the sharia) is subject to interpre-tation and that while the key principles are uniform across the faith, it is possible to have differences of opinion on matters of application. A differen-tiating feature of the Islamic finance industry is the central role that sharia scholars play in the industry: in ensuring products are compatible with the sharia and giving confidence to the market by providing official certification that products are sharia-compliant.

Mastering Islamic Finance

28

All of this knowledge is directly relevant to the foundation and practice of Islamic finance. With Islamic finance being a faith-based proposition, this background knowledge is important and will serve well those engaged in the Islamic finance industry or those undertaking any work in this space.

3How Islamic finance differs from

conventional banking

The Islamic economic model

Key Islamic finance principles

Conclusion

3 · How Islamic finance differs from conventional banking

31

THE ISLAMIC ECONOMIC MODEL

Modern discourse on economic models tends to be dominated by two opposing ideologies, namely capitalism and socialism, neither of which is explicitly associated with particular religions. It is rare to see a discussion about economic models that refer to a particular religion. The Islamic faith is holistic in nature; there is no separation between ‘church’ and ‘state’, so to speak. As mentioned previously, Islam means submission to God’s Will and by implication believers should, in every sphere of their lives, including finance, seek to follow the guidance and values espoused by their faith.

Capitalism in its purest form is defined by individual freedom, free markets with no intervention and an unbridled pursuit of wealth. Socialism focuses on the collective, with little or no scope for individuals to pursue or increase personal wealth through private enterprise.

Much of the world today has a heavy bias towards capitalism, with varying degrees of state regulation and intervention to protect the interests of society at large and those who are vulnerable, such as the poor and sick. Socialism as an economic system is less prevalent in today’s world and there are only a few examples of economies that are using this as a basis for their economic system – examples include Cuba and North Korea. It is more common to refer to socialists as those who campaign for a greater role for the state in protecting and helping the vulnerable and poor and for greater equality in wealth distribution.

So how does the Islamic economic system compare with these models? Islam purports to be a religion and way of life that is in harmony with the nature of man. To this end it recognises that man has an innate desire to seek wealth as a means of fulfilling his needs and achieving a higher quality of life. Islam encourages human endeavour, enterprise and trade and promotes the idea of people having the freedom to express their talents and entrepreneurial skills. Indeed, seeking wealth and livelihood through honest effort and trade is seen as a commendable act and a blessing from God, as evidenced by the reported statement from Prophet Muhammad:

It is better for one of you to take some rope and go to a mountain and bring a bundle of firewood on his back and sell it by which Allah saves his honour and dignity, than for him to ask people who then give to him or refuse.

‘Collection of Prophetic sayings’ by Imam Bukhari

At the core of what makes the Islamic system different is the belief that God is the real owner of all wealth and resources. Capitalism confers absolute ownership of private property to individuals. Socialism (broadly speaking) rejects the notion of private ownership of assets. Islam recognises ownership

Mastering Islamic Finance

32

of private property by individuals, but requires that ownership to be subser-vient to the rules and guidance of the true owner, God.

Another way of expressing the Islamic concept of ‘ownership’ of assets is that individuals are the guardians of these assets which have been given to them by God.

Islam presents a framework of God-given principles and values against which the individual pursuit of wealth needs to be set. Note that some of these, particularly the first two, are embedded to a greater or lesser degree in the ‘capitalism’ prevalent in most western societies today.

Protecting the public interest

Protecting the public interest is a paramount principle in Islam. Therefore any activity that is deemed to be against the wider public interest would not be tolerated. What is deemed to be against the public interest will be determined by:

■ an assessment of the product’s or activity’s positive and negative features and its potential impact on the public. For example, the polluting effects of a particular type of manufacturing process may outweigh the potential gain in short-term wealth;

■ the activity may be prohibited in the sharia, such as the consumption of alcohol, pork, pornography and gambling. If this is the case, the activity would be automatically seen as against the public interest as for Muslims, as it would be in contravention of divine law.

Protecting the weak, poor, vulnerable and sick people

One of the five pillars of Islam is the obligation on the part of a believer to give a percentage (usually 2.5 per cent) of their wealth every year to charity (this is referred to as zakat). The prime use of this would be to alleviate the difficulty of the poor and needy. This is the minimum society would be expected to do, but Islamic principles would dictate that there would be a greater welfare state if required, funded by taxes/charitable giving by society to ensure that those in need are looked after.

Accountability to God

There is a strong concept in Islam of accountability to God for all of one’s actions in this life. When it comes to wealth this can be seen from the following statement from Prophet Muhammad:

The feet of the son of Adam will not move on the Day of Judgement till he is asked regarding five matters: how he spent his life, how he utilised

3 · How Islamic finance differs from conventional banking

33

his youth, how he earned his wealth and how he spent it, and what he did with his knowledge.

‘Collection of Prophetic sayings’ by Imam Tirmidhi

Hence earning wealth unlawfully, any dishonesty, violating the rights of others or the irresponsible use of wealth are all serious issues from an Islamic perspective.

Islamic values regarding wealth

Islam warns against making the pursuit of wealth such a dominant force that it takes people away from what it considers to be the purpose of life: namely, to seek God’s favour and acceptance by His worship, good conduct and deeds. The following passages from the Qur’an, when referring to righteous people, provide evidence of this:

By men whom neither traffic nor merchandise can divert from the Remembrance of God.

(Chapter 24, verse 37)

Wealth and children are allurements of the life of this world: but the things that endure, good deeds, are best in the sight of thy Lord, as rewards and best as the foundation for hopes.

(Chapter 18, verse 46)

The following statements made by the Prophet Muhammad warn against greed, promote moderation as opposed to aggression in seeking wealth, and commend contentment as a virtue:

Hakim Ibn Hizam reported that the Messenger of Allah (PBUH) said: ‘This wealth is verdant and sweet. Anyone who takes it in a generous spirit will be blessed in it but anyone who takes it in an avaricious way will not be blessed in it, like someone who eats and is not satisfied. The upper hand (he who gives) is better than the lower hand (he who takes).’

‘Collection of Prophetic sayings’ by Imam Bukhari and Imam Muslim

Ibn ‘Amr reported that the Messenger of Allah (PBUH) said: ‘The successful man is he who becomes a Muslim, has adequate provision and whom Allah makes satisfied with what He gives him.’

‘Collection of Prophetic sayings’ by Imam Muslim

Jabir reported that the Messenger of Allah (PBUH) said: ‘O People! Fear Allah and be moderate in seeking a livelihood. No self will die until it has received its full provision, even if it is slow in coming. Fear Allah and be moderate in seeking. Take what is lawful and leave what is unlawful.’

‘Collection of Prophetic sayings of ibn Majah’

Mastering Islamic Finance

34

Prohibition of interest and the fractional reserve banking system

The prohibition of interest is central to Islamic finance and later in this chapter we will discuss in detail the definition and scope of this prohibition and some of the perceived wisdom behind this ruling. In the context of an Islamic economic model, interest would be banned. This has serious conse-quences for the contemporary global financial system. The modern world runs a global monetary system that is based on the concept of fractional reserve. The value of paper money and coins of a particular country’s currency in circulation is a multiple of the real wealth of a country. Central banks and commercial banks have been given the legal right to create money for lending at interest. From an Islamic viewpoint this system is fundamen-tally at odds with the principles of Islamic finance for the following reasons:

■ Paper money and coins should be used as a common and accepted measure of value allowing society to trade, buy and sell with ease as opposed to having to barter. That is, the role of money should be as a medium of exchange, measure of value and store of wealth and should directly reflect the real underlying value of assets in existence.

■ The fractional reserve system relies strongly on confidence in the system. A bank will hold only a ‘fraction’ of the money it has supplied into the market. If the public loses confidence in a particular bank or the banking system and many of them want to withdraw their money at the same time, the bank will almost certainly not be able to give everyone their money, which has been seen from time to time in the form of bank runs.

■ Interest is at the heart of the fractional reserve system, where the role of money goes way beyond being a common measure of value and medium of exchange. Money itself is traded through the charging of interest with no need for any real underlying trade or item of value, which is fundamen-tally against Islamic principles.

An Islamic economic model would be built on a monetary system whereby money production would be the role of the state (as opposed to banks which then charge interest on the supply). The money has to have a close link to the real wealth of a country – some have proposed paper currencies backed by gold and silver. Indeed, proponents of monetary reform outside of Islamic finance have long advocated a return to the Gold Standard. Some prominent economists, such as Nobel Prize winners Robert Mundell and James Robertson, have written extensively on the benefits of returning to the Gold Standard.

Others, such as the former Malaysian prime minister Dr Mahathir Mohamad and Islamic finance writer Tarek El-Diwani, have proposed the replacement of paper money with a chosen commodity, such as gold. They argue that a real commodity such as gold, which has intrinsic value, holds

3 · How Islamic finance differs from conventional banking

35

its purchasing power in the long run and is less prone to inflation, resulting in a more stable monetary system.

Given that modern-day conventional banking is built around the fractional reserve system and interest, a number of academics and practitioners within the Islamic finance industry have questioned the suitability of banks playing a significant role in the advancement of Islamic finance. Many of them have argued that it would be better to have structures outside of the banking arena, such as funds, private equity/venture capital houses and cooperatives.

To summarise, the Islamic economic model promotes the rights of individuals to seek wealth within the framework of a moral code designed to protect wider societal interests. There is a strong degree of personal accountability driven by the notion of an individual being a guardian of assets which are ultimately owned by God; the pursuit of wealth should not distract from the real purpose of life. The payment or receipt of interest are prohibited because wealth must be created or earned through real activities or assets.

KEY ISLAMIC FINANCE PRINCIPLES

Islam encourages trade and business activity. Commerce is considered a part of a healthy and vibrant society. The following four principles are key to determining whether a commercial transaction is sharia-compliant:

1. The subject matter is permissible under the sharia. Examples of prohibited activity would be the sale of alcohol, pork or the provision of gambling.

2. The transaction is interest-free (the Arabic word for interest is riba).

3. The trade or transaction is free from contractual uncertainty and ambiguity in the key terms and subject matter of the underlying deal (the Arabic word for such uncertainty/ambiguity is gharar).

4. The transaction is based on a real service or asset and any return to any party can be justified only by that party taking some risk with respect to the underlying asset or service.

It is therefore important we understand more about these principles.

Activities permitted by the shariaThere are certain trades and activities that are expressly prohibited under the sharia, such as the consumption of alcohol or pork. Any transaction related to such items would ordinarily be rendered impermissible.

Other items may not be permitted because of the perceived or actual harm they cause to individuals and/or society. Tobacco is a good example. Most

Mastering Islamic Finance

36

Islamic scholars would not permit investment in a tobacco business because of the harm that smoking inflicts on people’s health.

The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI)1, a key regulatory organisation in the Islamic finance industry, has specified the following industries as impermissible to invest in:

■ conventional banking and insurance;

■ pork;

■ alcohol;

■ gambling;

■ adult entertainment;

■ tobacco.

One can say it is a form of ethical screening that takes its lead from the teachings of the Islamic faith.

Prohibition of interest (riba)

This prohibition marks the biggest difference between conventional finance and Islamic finance. While interest plays a central role in modern-day economics, banking and finance, the Qur’an contains a clear instruction not to engage in any transaction that involves interest. The following citations from the Qur’an and the Prophetic teachings show how interest has been prohibited in the strongest terms in Islam:

Those who take Riba (interest) will not stand on the Day of Judgement except as he who has been driven mad by the touch of the devil. That is because they have said, ‘trading is like Riba [interest]’, but God has permitted trading and prohibited Riba [interest]. Whosoever receives an advice from his Lord and stops, he is allowed what has passed and his matter is up to Allah. And those who revert are the people of the Hellfire. O you who believe! Fear God and give up what remains due to you from Riba [interest] if you are really believers; and if you do not, then take notice of war from Allah and his Messenger, but if you repent you shall have your capital sums. Deal not unjustly and you shall not be dealt with unjustly.

Qur’an, (Chapter 2, verses 278–279)

Jabir ibn Abdullah narrated that the Prophet cursed the receiver and the payer of riba, the one who records it and the witnesses to the transaction, and he said: ‘They are equal in guilt’

‘Collection of Prophetic sayings’ by Imam Muslim

1 AAOIFI is the Accounting and Auditing Organisation for Islamic Financial Institutions and is a leading sharia and accounting standard-setting body for the Islamic finance industry.

3 · How Islamic finance differs from conventional banking

37

Given these stern warnings against riba, it is important to examine its definition and scope, so that we are clear what exactly is prohibited.

Interest charged on money lent is not allowed. The mainstream and dominant view among Islamic scholars is that any increase on the capital lent is impermissible. Even if it equates to a small percentage in terms of an interest rate, say 1 per cent, this is still prohibited. This is different to the common contemporary position adopted by Christian theologians, namely that the usury referred to in the Bible represents an ‘excessive or exploitative’ interest charge.

Another dimension to this prohibition is in the realm of barter. The Prophet said the following:

Abu Sa’id al-Khudri reported that the Holy Prophet said: ‘Gold is to be paid for by gold, silver for silver, wheat by wheat, barley for barley, dates by dates and salt by salt, like for like and equal for equal, payment hand to hand. He who makes an addition to it or asks for an addition, deals in riba. The receiver and the giver are equally guilty.’

‘Collection of Prophetic sayings’ by Imam Muslim

There are three dimensions to this prohibition:

1. The countervalues exchanged must be equal, so for example if I exchanged 200g of salt for 100g of salt, then the excess exchanged is construed as interest.

2. ‘Like for like’ includes the fact that the quality must be the same:

Abu Sa’id al-Khudri narrated that Bilal bought Barni [fine-quality] dates to the Prophet and the Prophet asked him, ‘From where have you bought these?’ Bilal replied, ‘I had some inferior dates and I exchanged two measures of those for one measure of Barni dates to give it to the Prophet.’ The Prophet replied, ‘Beware! Beware! This is definitely riba! Don’t do so, but if you want to buy superior dates, sell the inferior dates for money and then buy the superior kind with that money.’

The Prophet instructed that the inferior dates should be sold first for money and the better quality dates should be purchased with the proceeds. This exercise helps to ensure that fair value is achieved for both parties in the transaction.

3. The transaction must be at spot with no delay, so for example if I exchanged 100g of salt now for 100g of salt later, this would be construed as riba. In this case, the party receiving the salt has use of that salt before they have to recompense the other party, and hence may have an unfair advantage in the transaction.

The consensus among scholars is that the principle laid down by the Prophet for the commodities mentioned above can be extended to apply to commod-ities that possess two characteristics:

Mastering Islamic Finance

38

1. The commodity is/can be sold by weight.

2. The commodity has the natural ability to be used as a medium of exchange.

Most scholars, based on the fact that gold and silver are included in the six commodities mentioned by the Prophet and were typically used as money in the time of the Prophet, extend the above principles to exchange of paper and electronic money. Rules of sharia-compliant foreign exchange are derived from these principles.

Some of the wisdoms behind the prohibition of interest