Practical Considerations in Managing Variable Annuities Stochastic Modeling Symposium Toronto By...

26

Practical Considerations in Managing Variable Annuities Stochastic Modeling Symposium Toronto By Thomas S.Y. Ho Sang Bin Lee Yoon Seok Choi April 3-4 2006

-

Upload

keely-hinchcliff -

Category

Documents

-

view

219 -

download

3

Transcript of Practical Considerations in Managing Variable Annuities Stochastic Modeling Symposium Toronto By...

Practical Considerations in Managing Variable Annuities

Stochastic Modeling SymposiumToronto

ByThomas S.Y. Ho

Sang Bin LeeYoon Seok Choi

April 3-4 2006

2

Problem Statement

• Variable annuities (GMIB) have embedded capital market options – Equity options (equity put option)– Interest rate options (annuity value)

• Pricing of the options– Capital market method: Cost of replications of

the options– Identifying the embedded options

• Practical considerations

3

Outline of the Presentation• The valuation model• Pathwise immunization and LPS• Practical considerations

– Computational efficiency– Equity/rate correlations and cost of guarantees– Product risks– Cost benefit analysis– Suboptimal exercise of options– Alternative to equity funds

4

A Model of GMIB

• Invest in equity/bond funds

• End of the accumulation period, a choice: the account value or a fixed annuity

• The guarantee is a put option to the insurer

• If the fund is an equity fund, it is an equity put option, where the “strike price” is a bond, subject to interest rate risks

5

Capital Market Approach: Equity/Interest Rate Model

• 2-factor interest rate model

• Recombining lattice, orthogonal yield curve movements

• Fit the term structure of interest rates and volatilities (arbitrage-free)

• Combining lognormal and normal behavior

• Equity returns are lognormal with the instantaneous rate of return = short rate

6

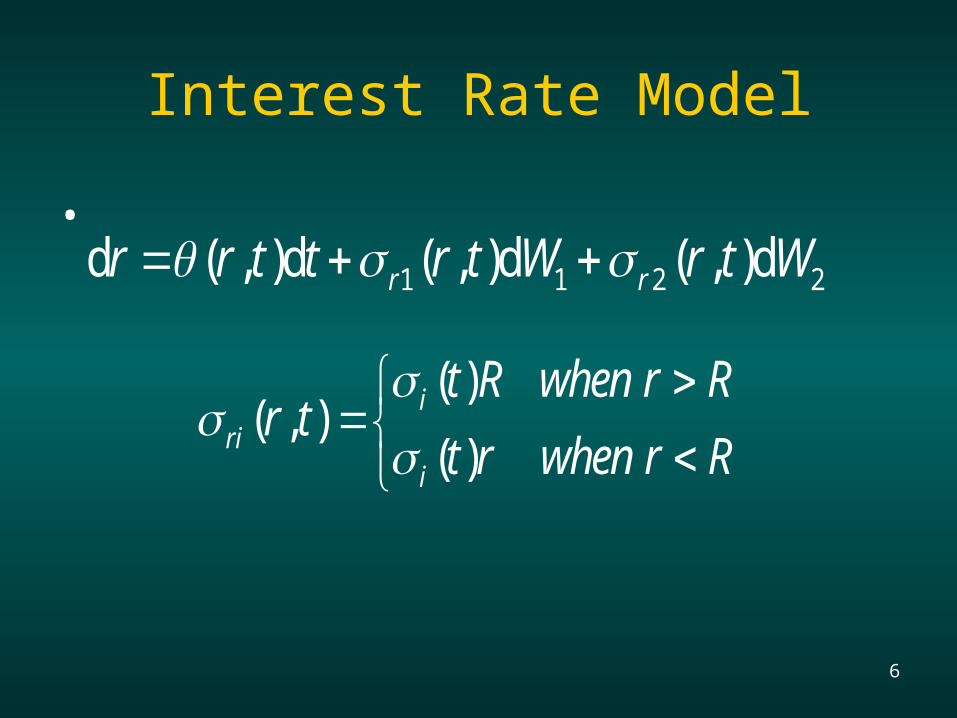

Interest Rate Model

•

( ) ( , )

( ) i

rii

t R when r Rr t

t r when r R

1 1 2 2d ( , )d ( , )d ( , )dr rr r t t r t W r t W

7

Variable Annuity and GMIB Models

• Policyholders annuitize when the annuity value exceeds the account value

• GMIB is the policyholder’s equity put option with a stochastic strike price based on the annuity value.

• Can we represent the GMIB as a portfolio of equity options and bond options?

8

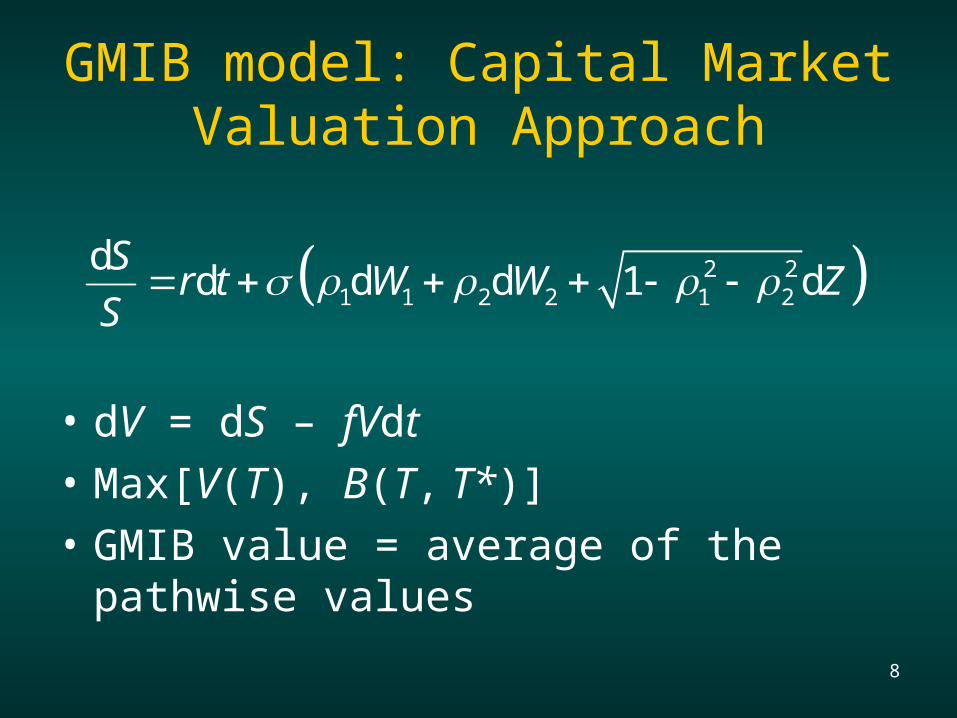

GMIB model: Capital Market Valuation Approach

• dV = dS – fVdt

• Max[V(T), B(T, T*)]

• GMIB value = average of the pathwise values

2 21 1 2 2 1 2

dd d d 1 d

Sr t W W Z

S

9

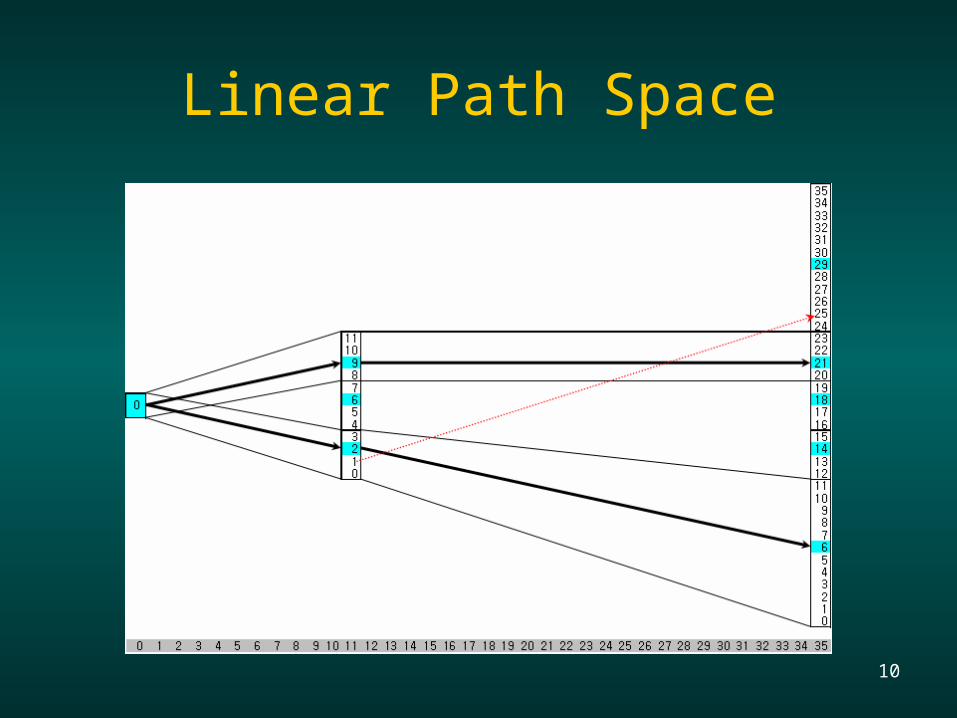

Decomposition using Linear Path Space (LPS)

• The path space is a representation of all the possible scenarios

• The recombining lattice offers a “co-ordinate system” to represent the possible scenarios

• Structured sampling of the path space provides equivalent classes of the possible scenarios, and the lattice framework enables us to measure the size of the classes

10

Linear Path Space

11

GMIB Value and the Correlations

• X-axis: correlation of equity returns with steepening movement

• Y-axis: correlation with the parallel movement

• Negative correlation implies natural hedging

-0.5 0.0 0.5

-0.5 7.49 11.98 14.90

0.0 10.87 14.69 17.46

0.5 13.13 16.79 19.59

12

GMIB Value and Correlations

• The correlation with the steepening effect has greater impact on the GMIB value

• The worst scenario: yield curve steepens, rates and equity value fall

• Negative correlation with the steepening movement lowers the probability of the worst scenario

13

GMIB & Account Value

• Increase account value: GMIB value falls

• Impact of the correlation on GMIB is significant, particularly when the account value is high

14

Effectiveness of the Pathwise Immunization

• GMIB pathwise values are plotted against the hedging portfolio pathwise values

• The fit is 99% R- square

15

Decomposition Solution: Pathwise Immunization Portfolio

A B C D E F G H I

Hedging Instrument

Strike Fair ValueRegression

Coeffs.t-statistics Dollar value Delta Duration

Dollar Duration

Cash - 1.00 3.32 4.97 3.32 0.00 0.00 0.00

Bond Call 10 57.20 -0.19 -10.20 -10.81 0.00 21.41 -231.43

Bond Call 20 50.90 -0.16 -10.25 -8.11 0.00 22.78 -184.87

Bond Call 30 44.61 -0.11 -10.33 -4.82 0.00 24.54 -118.25

Bond Call 40 38.31 -0.02 -6.51 -0.73 0.00 26.87 -19.57

Bond Call 50 32.01 0.14 9.20 4.41 0.00 30.13 132.72

Bond Call 60 25.71 0.42 9.71 10.84 0.00 34.98 379.22

Bond Call 80 13.94 0.33 12.35 4.62 0.00 50.85 234.92

Bond Call 100 5.42 0.28 12.95 1.54 0.00 69.42 107.12

Bond Call 120 1.53 0.17 8.69 0.26 0.00 87.96 22.57

Equity Put 40 0.14 1.56 4.04 0.22 -0.01 53.54 11.71

Equity Put 100 6.98 0.37 5.22 2.55 -0.16 32.86 83.86

Equity Put 150 22.55 0.51 14.88 11.40 -0.35 26.07 297.28

Replicating Portfolio

14.69 -0.24 48.68 715.26

GMIB 14.69 -0.22 48.34 710.09

16

A Solution in Pricing

• Separate pricing from valuation

• Use the decomposition to identify the pricing strategy

• The solution is a combination of hedging and directional investment

• Product design to seek the optimal solution

17

Fixed Annuities

• Based in interest rate models

• Investment portfolio can be fixed income

• The embedded options would be interest rate options

• Decomposition based on yield curve scenarios

18

Computational Efficiency

• Extended LPS model

• Structured sampling approach

• Convergence

19

Equity/rate correlations and cost of guarantees

• Correlations of equity returns to the yield curve movement can be incorporated

• This approach is important to GMIB valuation because it focuses on the worst scenario: steep yield curve, falling rates, and underperforming equity market

20

Product risks

• Lapse risk, mortality risk, partial withdrawal can be simulated as risk sources

• Distribution of the pathwise values would be higher

• Hedging would not less perfect resulting in lower hedged positions

21

Cost benefit analysis

• Pathwise values provide the present value and risk adjusted values by scenarios

• The distribution of the pathwise values post partial hedging provides a measure of the downside risks

• The market view can be incorporated in the risk and return tradeoff in the “optimal hedging”

22

Suboptimal exercise of options

• The exercise rule can be adjusted for inefficiency in exercising the options

• Valuation and hedging can be adjusted by the model results

( , *; , ) ( ; , ) if ( , *; , ) ( ; , )( , )

0 otherwise

B T T i j V T i j B T T i j V T i j CY i j

23

Alternative to equity funds

• Fixed income fund can be evaluated in the same framework

• Policyholders’ behavior can be simulated by the model resulting in the appropriate tradeoff of risk and returns

24

Implications on the Product Design

• Depends on the insurer’s business model

• Market directions and balance sheet positions are relevant

• Correlations of the fund returns and the guarantees are important

• Deciding on the risk and return tradeoff

25

Conclusions

• Pricing of a product begins the determination of the building blocks of value of the guarantees

• Then determine the optimal combination of hedge cost and directional investment

• Business model and the portfolio structure must be taken into consideration

26

References

• Ho, Lee and Choi: “Practical Considerations in Managing Variable Annuities” Working Paper 2006

• Ho and Mudavanhu: “Decomposing and Managing Multivariate Risks: the Case of Variable Annuities” Journal of Investment Management 2005

• Ho and Mudavanhu “Managing Stochastic Volatility Risk of Interest Rate Options: Key Rate Vega” working paper 2006

• Papers available at www.thomasho.com