Pproject Work(Adansi Rural Bank)

60

CHA PTER ONE INT RODUCTION 1.0 BACKGROUND OF THE STUDY Every organization or firm requires some level of financing. This applies to businesses already in operation and those planning to start new businesses. Financing is a major area to be considered by stakeholders (government, entrepreneurs, creditors etc among others).It has become a foundation which all forms of businesses and organizations such as banks thrive on for survival. Financing is generally categorized as either equity or debt, due to its nature; I was more interested in the type of equity capital called working capital. Working capital is the money or capital available for the day to day operations of the business. It is the money used to buy materials or goods for manufacturing or for resale. This is in direct contrast with fixed capital, which is the money used to buy fixed assets such as buildings, plants, motor vehicles etc. Working capital is usually defined as the net current assets consisting of stock, debtors and cash minus current liabilities mainly trade creditors. The main sources of working capital are the current assets as these are the short term finance that a 1

Transcript of Pproject Work(Adansi Rural Bank)

CHAPTER ONE

INTRODUCTION

1.0 BACKGROUND OF THE STUDY

Every organization or firm requires some level of financing. This applies to businesses already in

operation and those planning to start new businesses. Financing is a major area to be considered

by stakeholders (government, entrepreneurs, creditors etc among others).It has become a

foundation which all forms of businesses and organizations such as banks thrive on for survival.

Financing is generally categorized as either equity or debt, due to its nature; I was more

interested in the type of equity capital called working capital.

Working capital is the money or capital available for the day to day operations of the business. It

is the money used to buy materials or goods for manufacturing or for resale. This is in direct

contrast with fixed capital, which is the money used to buy fixed assets such as buildings, plants,

motor vehicles etc. Working capital is usually defined as the net current assets consisting of

stock, debtors and cash minus current liabilities mainly trade creditors. The main sources of

working capital are the current assets as these are the short term finance that a firm can use to

generate cash. However, firms also have some obligation to fulfill and as such, careful

consideration must be given to working capital management.

It is vital for a business to have sufficient working capital to meet all its requirements. Most

businesses are not doing well as a result of poor working capital management. For businesses to

grow, it needs to be careful with how they manage their finances, especially the working capital.

Since an organization must have a sufficient amount of cash, debtors and stock, management

must give attention to working capital management.

1.1 STATEMENT OF THE PROBLEM

The main driving force behind this research is to establish the practicality of running a

business or an organization with respect to the management of working capital of the

1

business or the organization. This research also seeks to enquire into how management

professionally handles the issues of working capital management in business organizations in

Ghana.

1.2 HYPOTHESIS

It has been noted that the improper methods of bookkeeping have resulted in the folding up of

many businesses in the Ghanaian economy. Effective management of working capital will mean

that proper accounts will be kept by businesses or organizations which go a long way to have a

positive impact on working capital. This will help sustain business organizations to achieve their

organizational goals.

1.3 OBJECTIVES OF THE STUDY

The study is aimed at identifying the effectiveness of the management of working capital in

Ghana. The course of this study is to find ways to deal with proper working capital cycle within

businesses in Ghana which will help organizational growth.

1.4 THE SCOPE AND LIMITATION OF THE STUDY

The delicate nature of an organization working capital disclosure to Individual or group of

people who may have less or no interest in the business organization made it difficult for many

thriving businesses to release information that concern their working capital, so that I can form

an opinion on their working capital and its operation. Due to this reluctance, we focused on

businesses such as Banks and other Financial Institutions set up by individuals or group of

people who were more willing to help me to carry out this research study on working capital.

The study covered present methods of managing working capital and the probable problems

associated with working capital in these organizations.

2

The limitations to this research include the limited time within which we were supposed to come

up with a credible study. There was also a financial constraint in gathering data and in-depth

audit of information given to ascertain its credibility.

1.5 SIGNIFICANCE OF THE STUDY

The project will help improve the working capital management of businesses not even banks

only but other financial institutions in Ghana by identifying the most suitable ways of managing

working capital. The research will help to determine and maintain the appropriate level of

working capital that maximizes profit by preventing excess or idle working capital and the

shortage of working capital. This will go a long way to improve the financial position of

businesses in Ghana and also to take proper management decisions. The project will also help

individuals or group of people who will do research on working capital management in future.

1.6 METHODOLOGY

There are different methods which were used in gathering the relevant information for the

project. These include;

Literature review and documentary research

Personal interviews

Submitted questionnaires

Published literature and financial reports was used for the study and background information as

guidance. In addition, a careful study of published reports and magazines of businesses was

reviewed for relevant information.

Other journals and brochures were obtained from the small scale businesses which were used as

a case study. Apart from the above, some relevant information and facts from the financial

magazines, journals, The National Board for Small Scale Industries and the Ghana Stock

Exchange was consulted. Questionnaires were submitted to Adansi Rural Bank ltd and their

3

management. The facts gathered from documentary sources and responses received from

interviews and submitted questionnaires were collected to form the basis of this project.

1.7 ORGANIZATION OF THE STUDY

The study is structured or organized into five main chapters.

Chapter one is concerned with the introduction of the research, and it includes the background

of the study, statement of the problem, hypothesis, and objectives of the study as well as the

limitations and the methodology.

Chapter two is devoted to reviewing past literature on earlier researches conducted by

individuals or group of people on working capital management.

Chapter three: In chapter three, the population in the business organization shall be sampled to

obtain data based on the methodology being used which shall be analyzed to suit our research.

Chapter four: This chapter is concerned with evaluating the data at hand.

Chapter five: This is the stage where we draw our conclusion using the results obtained from

these business organizations in survey, recommendation comparism with how theoretical the

working capital of an organization needs to be managed to ascertain how professionally these

businesses are managing their working capital.

4

CHAPTER TWO

LITERATURE REVIEW

2.0 INTRODUCTION

The purpose of this literature review is to report on the previous work that others have done in

the area of the study which also focuses on relevant articles, journals and other relevant

materials.The review has been put under these sub headings:

Management of stock

Management of debtor

Cash management

Creditors control

Management of bank overdraft

According to Artill and Maclanuey (1994), the size and composition of working capital varies

between industries. For some businesses, the investment in working capital can be substantial,

for example a manufacturing company as compared with a retail business.

2.1 OPERATING CYCLE

5

The operating cycle is the length of time between the company outlay of raw materials, wages

and other expenditure and the inflow of cash from the sale of the goods. It is also known as the

working capital cycle which is the length of time that elapses between a business paying for its

raw materials and the business receiving payments from its customers for the goods made from

the raw materials.

2.2 WORKING CAPITAL CYCLE OF A MANUFACTURER

A firm buys raw materials on credit. The raw materials will be held for some time in stores

before being issued to the production department and turned into finished products. The finished

goods must be kept in a warehouse for sometime before they are sold to customers. By this time,

the firm will have paid for the raw materials purchased. If customers buy goods on credit, it will

take some time before the cash from the sale is realized. Each activity takes some time. The time

taken by each activity is an element of working capital cycle.

2.3 MANAGEMENT OF STOCK

A firm needs a continuous supply of materials to ensure that production and sale of goods goes

on every day in order to maximize profit. Holding higher levels of stocks will enable the

company to be more flexible in supplying customers, even when there is an abnormal demand.

More customers will receive immediate delivery rather than waiting for new goods to be

produced. There might be a smaller chance of sales being delayed through interruptions in

production. On the other hand, keeping a high level of stocks brings in additional cost of

financing in keeping stocks.

Stock management may be defined as keeping the optimum or the appropriate level of stocks

that will maximize the benefit of holding and minimize the cost of holding stock. It is also the

process of determining and keeping the appropriate level which will minimize the cost of storing

6

and also ensure that the firm does not run out of stock in other to maximize profit. Keeping a

minimum level of stock will release cash for future investment.

2.3.1 BUDGETS FOR FUTURE DEMAND

The best way a business can ensure that there is stock available to meet future sales, is to prepare

an appropriate budget. This budget should include each product that the business deals in. It is

important to make every attempt to ensure the accuracy of those budgets as they will decide

future ordering and production level. The budget may be driven in various ways. The budget

may be developed using statistical techniques such as time series analysis or may be based on the

judgment of the sales and the marketing staff.

2.3.2 FINANCIAL RATIOS

The ratio that can be used to monitor stocks is the stock turnover period. This ratio is calculated

as;

Stock turnover period = Average stock × 365 days

Cost of sales

This will provide the basis to know the average period for which stocks are held and can be

useful as a basis for comparison. It is possible to calculate the stock turnover period for

individual product lines as well as for stocks as a whole. Shorter stock turnover period indicates

how effective management has worked hard to earn profit.

2.3.3 RECORDING AND REODERING SYSTEM

The management of stock requires a sound system of recording stock movement. There must be

a proper procedure for recording purchases. Periodic stock checks may be required to ensure

7

that the amount of physical stock held is consistent with the stock records. The authorization of

both purchases and the issue of stocks should be confined to a few senior staff which will help

reduce pilfering. To determine the point at which stock should be reordered, the information

concerning the lead- time (time between the placing an order and the receipt of the goods) and

the likely level of demand will be required.

2.3.4 STOCK MANAGEMENT MODELS

It is possible to use decision models to help manage stocks. The economic order quantity (EOQ)

is concerned with answering the question, how much stocks should be ordered. In its simplest

form, the EOQ models assumes that demand is constant so that stocks will be depleted evenly

overtime and will be replenished just at the point that stocks runs out. The most used method of

stock management is;

JUST IN TIME (JIT) STOCK MANAGEMENT

In recent years, some manufacturing industries have tried to eliminate the need to hold stock by

adopting just in time stock management. This method was first used by the US defense industry

during World War II and in more recent times. It has been widely used by the Japanese business

men. The essence of JIT is, as the name suggests, to have suppliers delivered to a business just in

time for them to be used in the production process. By adopting this approach, the stock holding

problems rest with the suppliers rather than the business itself. For this approach to be

successful, it is important that the business inform suppliers of its production plans and in turn

deliver materials of the right quantity at the agreed time. Failure to do so could lead to a

dislocation of production and could be very costly.

Thus, a close relationship between a business and its suppliers is required. Though a business

will not have to hold stock, there may be certain cost associated with JIT approach. Finally, the

close relationship is necessary between the business and its suppliers may prevent the business

from taking advantage of cheaper source of supply if they become available. The philosophy

underlining this method is concerned with eliminating waste, and striving to deliver goods. There

will be no expectation that the production process will operate at maximum efficiency. This

8

means that there will be no production breakdowns. Whiles these expectations may be

impossible to achieve, they do help to create a management culture that is dedicated to quality

service.

2.4 MANAGEMENT OF DEBTORS

Debtors come about when an organization decides to sell goods on credit to customers. Selling

goods on credit results in, cost accruing to the business in the form of bad debt, opportunity

foregone in realizing cash promptly and others. When a business decides to sell goods and

provides services on credit, it must have clear policies concerning;

1. Type of customers to sell goods on credit to.

2. Setting credit limit

3. Conditions attached to sales

4. Means of cash collection to be adopted.

It is important to note that cash flow is very significant especially when collected at a faster rate.

It is also important for every business to know their debtors, how much is involved and for how

long it is standing in the books.

2.4.1 RELATIONSHIP BETWEEN PROFIT AND LATE RECEIPT OF CASH

Late receipt of cash as a result of offering credit sales has a crippling effect of rendering a

business cash trapped. This is much felt among industries whose sources of finance are not

strong, thereby uncontrollably, allowing the business to be managed according to the inflow of

cash as it occurs. In business finance, it is advisable to manage debtors of the business. The

following measures could be adopted in dealing with trade debtors;

1. Set up credit limit for each customer.

2. Ensure that the credit sales are within the set limit.

3. Immediately after credit sales prepare a sales invoice.

9

4. Send a reminder at frequent intervals

5. Threaten difficult customers with court action

6. Take court action if persuasion fails

7. Factor the debt after invoicing

Factoring as an alternative to debt retrieval, is the sale of debt or the amount owed by a debtor to a third party called the factor at a discount in return for prompt cash (immediate payment). In factoring, there can be a factor with a recourse where the supplier bears the risk of bad debt for debt not been paid or a factor without recourse in this case the factor or the third party bears the risk of bad debt.

2.4.2 DETERMINING RELIABLE CUSTOMERS

An organization which cannot erode selling on credit must plan efficiently and effectively on

how to retrieve monies owed from debtors. It is important to take the following factors into

consideration;

CAPITAL STRUCTURE

When a business is considering proposals from a customer to sell on credit, it is important to

access the capital base of this customer to be sure of how sound they are financially. It is

advisable to access the profitability and liquidity of the customer. In addition any major

financial commitments of the customer must be taken into consideration (standing orders, etc)

CAPACITY

The customer must have the capacity of paying their debt. Where possible, the credit record of

the customers must be examined. If the customer is already in operation, looking at the physical

and operational resources of the business will be relevant for forming a justifiable opinion about

the business.

COLLATERAL

It is more relieving to have a form of security for goods supplied on credit. When this occurs,

the business is convinced that the customer is reliable and as such goods can be sold on credit to

customers without fear of being deprived of their money. It also gives the assurance of doing

away with bad debt.

10

CREDIT WORTHINESS OF A CUSTOMER

It is important to access the credit worthiness of a customer with reference to past dealings of

the customer with your organization or your competitors. Once the customer is considered to

have a good record, then goods can be supplied to the customer without any fear.

CREDIT PERIOD

The business must determine the credit period it is prepared to offer to its customers. The

duration of credit offered can vary significantly between businesses and is influenced by factors

such as:

1. The degree of competition within the industry

2. The bargaining power of a particular customer

3. The risk of non- payment

4. The capacity of the business to offer credit, and others.

CASH DISCOUNT AND INTEREST ON DEBT

The organization can decide to offer cash discount as a means of encouraging prompt payment

from its customers. The amount of cash discount given can influence whether to purchase on

credit or not, from the organizations point of view it is important to weigh the cost of offering

discount against the likely benefit derived from financing debtors. Charging interest on overdue

debts can also be a stringent measure to collect cash from debtors, but it is also important to note

that, this is mostly possible when the organization sells a peculiar product in the area to avoid

loss of customers

2.5 DEBT COLLECTION POLICY

The organization offering credit must ensure that the amount owing is collected as quickly and

efficiently as possible. An efficient collection policy requires an efficient accounting system.

Management can monitor the effectiveness of cash collection policies in a number of ways. One

method that is commonly used in most businesses is the determination of the debtor’s collection

period. It is calculated as;

11

Debtor’s collection periods = Trade debtors ×365days Credit sales

This ratio is useful but not 100% reliable since it gives the average days within which debt will

be realized useful in budgeting.

2.6 MANAGEMENT OF CASH

Cash management is concerned with optimizing the amount of cash available to the entity or the

company and maximizing the interest on any spare or idle funds not required immediately by the

company. In other words cash management involves making sure that business always has

enough cash on hand to meet its bills expenses and other day-to-day activities and also invest

surplus cash for profit and interest. There are three motives of holding cash. These are;

2.6.1 TRANSACTIONARY MOTIVE

To meet the day-to-day commitments, a business requires a certain amount of cash that will take

care of their daily transactions. Cash has been described as the life blood upon which most

businesses thrives on.

2.6.2 PRECAUTIONARY MOTIVE

Future uncertainty of regular cash flow is a factor to consider in cash management. To curtail

any incidental spending, it is advisable to hold a cash balance on hand as a precautionary

measure.

2.6.3 SPECULATIVE MOTIVE

A business may decide to hold cash in order to be in a position to exploit profitable opportunities

as and when they arise, by holding cash a business may be able to enter into a new market that

open up, which may require an immediate entry. Ray Powell (1989)

2.7 CONTROLLING CASH BALANCE

Several models have been proposed to help control the cash balance of a business. One of such

models proposed the use of upper and lower control limits for cash balances and the use of a

12

target cash balance. The model assumes that the business invest in businesses that can easily be

turned into cash. The business proposes two limits thus the upper and the lower. If the business

exceeds the outer limit then management decide whether the cash balance is likely to return over

the following few days to a point within the inner control limit set. If this seems likely, then no

action is required. If on the other hand this seems unlikely then management must change the

cash position of the business by buying or selling marketable securities or simply by borrowing

or lending.

Y

80 outer limit

Higher

60

(%)

40

Lower

20 inner limit

13

0 1 2 3 4 5 6 7 8 x

The graph depicts a model for controlling the cash balance that relies on the use of inner and

outer control limits. Where outer control limits are breached and there is no prospect of an early

return to a point within these limits, management must take action. A breach of a higher limit

will involve buying marketable securities (to ensure that cash is not lying idle) a breach of the

lower limit will involve selling marketable securities to ensure there is sufficient cash to meet

obligation.There are other models that do not rely on management judgment and we use

quantitative techniques to determine an optimal cash balance.

2.7.1CASH BUDGET

To manage cash effectively, it is important for business to prepare a cash budget. Cash budget is

a statement which shows the expected cash to be received and paid as well as the expected cash

balance for each day, month or in future. Cash budget is a very important cost control

mechanism for both planning and control purposes. It is worth repeating the point that cash

budget enable managers to see the expected outcome of planned events. The cash budget will

identify periods when cash surpluses are expected.

2.7.2 THE OPERATING CYCLE

When managing cash, it is important to be aware of the operating cash cycle of the business.

This may be defined as the time period between the outlay of cash necessary for the purchase of

stock and the ultimate receipt of cash from the sale of goods. The operating cash cycle of a

business that purchase goods on credit for subsequent resale are shown diagrammatically:

14

Purchase of goods on credit

Payment for goods

Sale of goods on credit

Cash received from debtors

Stock holding period

The diagram shows that goods purchased on credit will be paid for at a later date and so no

immediate cash outflow will occur. Similarly, credit sales will not lead to an immediate inflow of

cash. The operating cash cycle is the period between the payments made to the supplier and the

cash received from the customer. The operating cash cycle is important because it has a

significant influence on the financial requirements of the business. The longer the cash cycle, the

greater the financial requirements of the business and the greater the financial risk. For this

reason, the business is likely to reduce the operating cash cycle to the minimum possible period.

2.7.3 MANAGEMENT OF TRADE CREDITORS

Running an organization on credit terms has its own advantages and disadvantages. Trade credit

is an important source of finance for most businesses. Buying on credit helps delay the payment

of cash thereby allowing the organization to invest cash in other sectors of the economy to attract

interest before paying out. In a situation where demand exceeds supply, trade creditors are given

less attention as compared to those who pay prompt cash. In addition customers who buy goods

on credit are less favored in terms of payment periods. Sometimes the goods or services may be

more costly if credit is required. However, in most businesses trade credit is the norm and as a

result, credit facilities are sometimes abused by customers leading to bad debts.

2.7.4 MANAGEMENT OF BANK OVERDRAFTS

Bank overdraft is short term finance whereby the business is allowed to withdraw money more

than what is in its bank account. It is a flexible form of borrowing and is cheap relative to other

sources or finance. Although in theory, bank overdraft is a short term source of finance, in

practice it can extend over a long period of time. This is because many businesses continually

renew their overdraft facility with their banks. Though renewal may not be a problem there is

always the danger that the bank will demand repayment at a short notice as it has the right to do

so.If the business is highly dependent on bank overdraft, other alternative sources of short – term

finance, this could raise several problems. When considering whether to have a bank overdraft,

the business should first consider the purpose of the borrowing. Overdraft is most suitable for

overcoming short term funding problems (for example increase in stockholding requirement

owing to seasonal fluctuations). To determine the amount of overdraft facility, the business

15

Operating cash cycle

should produce a cash budget. There should also be regular reporting of cash flows overtime to

ensure that the overdraft limit is not exceeded.

16

CHAPTER THREE

METHODOLOGY AND COMPANY PROFILE

3.0 INTRODUCTION

This chapter describes the method employed in the conduct of the research. It contains research

framework, data collection instruments and methods of data analysis. The study was designed to

investigate how small scale businesses manage their working capital.

3.1 RESEARCH FRAMEWORK

The research was conducted using a case study approach. A case study is a type of research

which gives an opportunity on one aspect of a problem to be studied in-depth.

3.2 DATA COLLECTION INSTRUMENT

The research was conducted using a self constructed questionnaire in collecting the data needed

for the study. The questionnaire was used because people were able to express their opinion

objectively and the cost involved was low. It also allowed the respondents enough time to answer

the questions.

3.3 DATA COLLECTION METHOD

The questionnaire were collected back and compiled together for in-depth assessment. Attention

was given to the organization of study to allow management suggests possible corrections that

must be done to enable the provision of a credible report of the organization.

Due to this, alternative questionnaire was design to meet the correct format needed to establish

the true report attained from the answers. The questionnaire covers areas like the financial

inflows and outflows of cash, how deficits are financed and how revenue is generated from

excess funds.

3.4 METHODS OF DATA ANALYSIS

The researcher used descriptive statistics in analyzing the data collected. The responses were

analyzed and presented mainly in narrative form. However, some quantitative tools such as

17

percentages and averages were used in the analysis. The findings were illustrated by the use of

tables and charts.

3.5 SAMPLING PROCEDURE

A purposive sampling and snowballing was used and with a population size of sixty. The views

concerning working capital management were sought and used in the analyses of the study.

3.6 PROFILE OF ADANSI RURAL BANK LTD

Adansi Rural Bank LTD was incorporated in 5th April, 1982 and a certificate to commence

business on 29th October, 1982.Their main aim is to be among the best ten (10) rural banks in

Ghana. They serve banking products such as savings, susu, current, fixed deposit accounts and

others.Adansi Rural Bank LTD has six(6) of its branches including the head office at Adansi

Fomena ,other branches are located at Obuasi ,Akrokeri, Atonsu, Dunkirk, Kaase and Obuasi.

18

CHAPTER FOUR

ASSESSING THE MANAGEMENT OF WORKING CAPITAL BY FINANCIAL

INSTITUTIONS IN GHANA

4.0 INTRODUCTION

The study was designed to investigate how businesses manage their working capital. The

research was conducted in the Ashanti Region of Ghana. A total number of sixty (60)

respondents were interviewed. The purposive sampling and snowballing techniques were

adopted to obtain responses.

4.1 BACKGROUND OF RESPONDENTS

4.1.1 Gender

Table 4.0 Gender of Respondents

Frequency Percentage

Male 39 65

Female 21 35

Total 60 100

Source: Field Survey, 2012

Table 4.0 above depicts that there were more males interviewed than females. Out of the total

sample size chosen (that is 60 respondents), 65% of the respondents were males with females

taking up the remaining 35%

.4.1.2 Age Range

19

Out the total respondents, thirty-six (36) were between the ages of 18-39, twenty-three (23) of

them between the ages of 40-59 and the remaining one (1) above 60 years as evidenced in table

4.1 below.

Table 4.1 Age Range of Respondents

Frequency Percentage

18-39 36 60

40-59 23 38.3

60 and above 1 1.7

Total 60 100

Source: Field Survey, 2012

4.1.3 Educational Background of Respondents

Since education has now become a prerequisite for jobs, all of the respondents had some level

of education. 30% of the respondents had a degree, 38.3% had HND’s, 20% of the respondents

were SSS leavers, and 1.7% of the respondents had their master’s degree.

Table 4.2 Educational Backgrounds of Respondents

Frequency Percentage

SSS 12 20

HND 23 38.3

Degree 18 30

Masters 1 1.7

not applicable 6 10

Total 60 100

Source: Field Survey, 2012

4.1.4 Occupational Breakdown of Respondents

20

Most of the respondents were in the following departments in their companies; management,

finance and sales departments, twenty-four (24) of the respondents were found at the

management level, twenty-one (21) respondents were in the finance department, and the

remaining fifteen (15) respondents were found in the sales department. The respondents were

taken from different departments in other to have divergent views from the respondents.

Figure 4.0 Occupations of Respondents

Source: Field Survey, 2012

The respondents held various positions such as; managerial which made up 45% of the

respondents whose main duties at their work places were administrative; 30% of the respondents

were sales assistants tasked mainly with selling of their companies products and services; 15%

were cashiers, who were mainly responsible for receiving and paying monies and the remaining

10% were accountants also assuming administrative and monitoring roles in their various

departments as shown in table 4.3 below.

Table 4.3 Positions of Respondents In Their Organizations

Frequency Percentage

Managerial 27 45

sales assistant 18 30

Accountant 6 10

Cashier 9 15

Total 60 100

Source: Field Survey, 2012

All of the respondents claimed that, their institution have a finance department as evidenced in

figure 4.1 below. This showed that almost all respondents worked in a well structured institution.

21

Figure 4.1 Presences of Finance Departments In Institution

Source: Field Survey, 2012

4.1.5 Respondents Views about Working Capital Management

The respondents when asked how they would define working capital management came out with

the following definitions; twenty–seven (27) of respondents defined working capital

management as managing invested capital to yield expected results; twenty-four (24) of the

respondents defined it as proper management capital invested, debts incurred, and profit accrued;

the remaining nine (9) respondents defined it as managing finances in the company.

Source: Field Survey, 2012

Out of the total respondents, 70% were of the view that working capital management was

necessary. The remaining 30% of the respondents were of the view that working capital

management was not very necessary as shown in table 4.4 below.

Table 4.4 Is Working Capital Management Necessary

Frequency Percentage

Yes 42 70

No 18 30

Total 60 100

Source: Field Survey, 2012

22

Some of the reasons given by the respondents for asserting that working capital management is

necessary are;

i. It helps in selling the products faster and easier.

ii. Helps in ascertaining profit and loss in the business.

iii. It helps in managing stocks.

iv. It is the basis for growth of companies.

v. It helps the company meet set objectives.

Out of the total respondents, 60% claimed that trade credit was the main form of financing that

their organizations operated. They claimed that it was the simplest and easiest form of financing,

20% stated that their organizations operated on short-term securities whiles the remaining 20%

asserted that their organization operated on long-term securities as evidenced in figure 4.3 below.

Figure 4.4 Financing Options of organization

Source: Field Survey, 2012

Most of the respondents claimed that the means by which their organizations acquire assets was

through ‘real’ cash. 50 % of the respondents were of that view. The main reason they gave was

that the company did not want to owe any other organization. 35% of the respondents claimed

23

that their organization acquired assets through credit, 10% of the respondents claimed their

organization acquired assets through leasing as shown in Table 4.5 below.

Table 4.5 Means of Acquiring Assets

Frequency Percentage

Credit 21 35

Cash 30 50

Hire purchase 3 5

Leasing 6 10

Total 60 100

Source: Field Survey, 2012

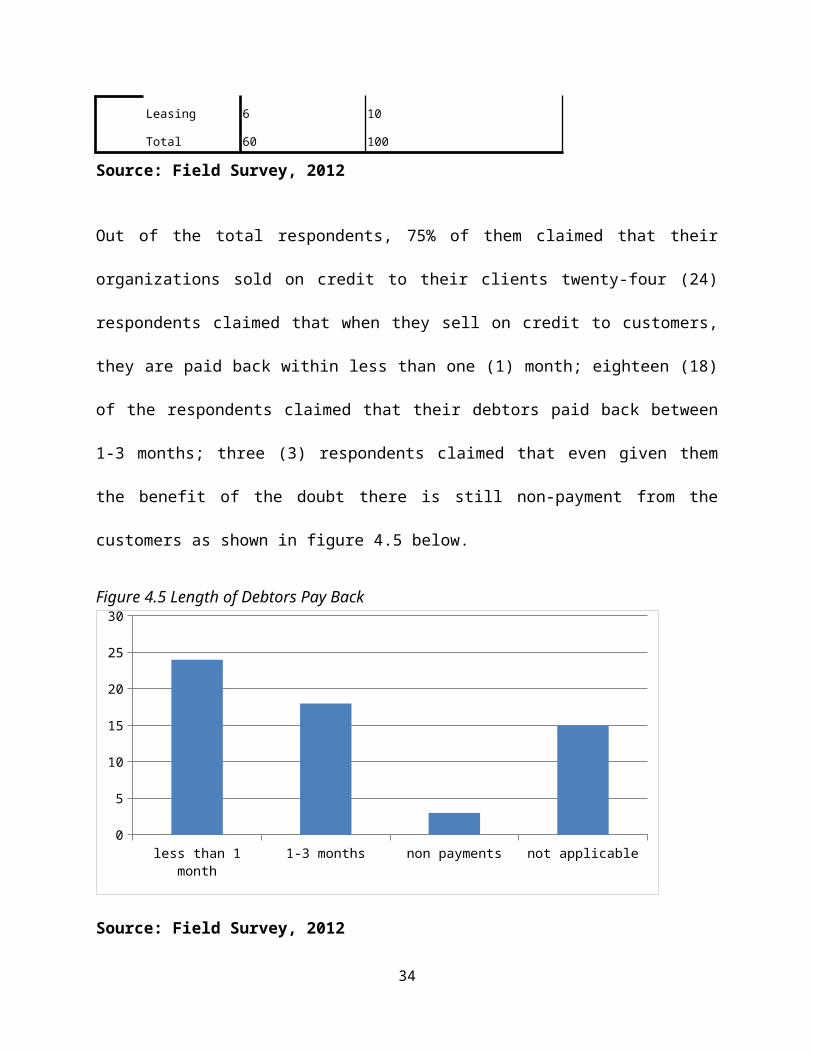

Out of the total respondents, 75% of them claimed that their organizations sold on credit to their

clients twenty-four (24) respondents claimed that when they sell on credit to customers, they are

paid back within less than one (1) month; eighteen (18) of the respondents claimed that their

debtors paid back between 1-3 months; three (3) respondents claimed that even given them the

benefit of the doubt there is still non-payment from the customers as shown in figure 4.5 below.

Figure 4.5 Length of Debtors Pay Back

less than 1 month 1-3 months non payments not applicable0

5

10

15

20

25

30

24

Source: Field Survey, 2012

Out of the total respondents, 40% of the respondents claimed that the credit limit for their

customer was eighteen months; 30% of the respondents claimed that the credit limit for their

clients was between two-three months and the remaining 30% between four-six months as shown

in table 4.6 below.

Table 4.6 Customer Credit Limit

Frequency Percentage

18 months 24 40

2-3 months 18 30

4-6 months 18 30

Total 60 100

Source: Field Survey, 2012

All the respondents claimed that records of customers and creditors were kept in their

organization.

Out of the respondents, 75% asserted that their organizations permitted advance payment from

the customers. 10% out of the 75% respondents stated that the advance payments received from

the customers enabled their organizations have enough circulating funds which helps the

company run better, the remaining 15% claimed that the advance payments they received from

the customers helped made their business run easier.

The remaining 25% claimed that their organizations did not accept advance payments although

no reason was given for that.

25

When asked about the means through which overdue debt was collected, 55% of the respondents

claimed that the debtors were issued with a debit note from their organization stating the amount

they owe and when they are to pay the amount, 15% claimed that their outfit wrote formal letters

to their debtors indicating their debt, another 15% stated that they wrote to their debtors through

their lawyers and the remaining 15% asserted that they gave their debtors enough time to come

and pay their debt as indicated in figure 4.6 below.

Figure 4.6 Mode of Collecting Overdue Debt

Source: Field Survey, 2012

Out of the total respondents, 100% claimed that their company was not listed on the stock

market.

Out of the 60 respondents, all of the respondents claimed that their institution had access to bank

loans.

Source: Field Survey, 2012

Only 20% of the respondents asserted that their organizations disposed off assets for cash when

they were really in dire need for money, whiles the remaining 80% claimed that their company

did not dispose assets for cash as shown in figure 4.8 below.

26

Figure 4.8 Disposals of Fixed Assets

Source: Field Survey, 2012

In respect to organizations being able to meet their budget, only 5% of the respondents claimed

that their company could not reach their budget. The remaining 95% of the respondents affirmed

that their institution was able to meet their budget as shown in table 4.7 below.

Table 4.7 Ability to Meet Budget

Frequency Percentage

Yes 57 95

No 3 5

Total 60 100

Source: Field Survey, 2012

27

The following reasons were given by the respondents for their company’s ability to meet their

budget;

i) The company is objective oriented.

ii) The institution has determined workers.

iii) Determination

iv) The institution is customer oriented.

All sixty (60) respondents representing 100% asserted that their organization was able to

generate profit from their respective business fields. 40% of the respondents claimed that their

companies ploughed back into the business, 25% of the respondents asserted that their

companies invested their profit in the stock market, 20% of the respondents claimed that their

organization purchased fixed assets with their profit and the remaining 15% of the respondents

declared that the profit from their organization are invested in other companies, as shown in table

4.8 below.

Table 4.8 Management of Profit

Frequency Percent

Plough back profit 24 40

Invested in other businesses 9 15

Invest in stock market 15 25

Purchase fixed assets 12 20

Total 60 100

Source: Field Survey, 2012

Figure 4.9 Overdraft Limits of Organizations

28

5,000-19,000 Ghana cedis

30,000-39,000 Ghana cedis

above 40,000 Ghana cedis

not applicable0

5

10

15

20

25

30

Source: Field Survey, 2012

When asked how the respondents companies financed deficits, it was revealed that;

i) Dividends received from investments were used to finance deficits.

ii) Some respondents claimed that their institutions took loans to help clear deficits.

iii) Bank overdrafts were identified as another method used by some institutions to clear their

deficits.

iv) Four of the respondents also claimed that in times of serious deficits, the owner of the

company cleared the deficit through ‘his own means’.

29

CHAPTER FIVE

CONCLUSION AND RECOMMENDATION

5.0 INTRODUCTION

All business organizations face some level of financial problems. It is for this reason that these

businesses must be more concerned about the management of their working capital. This chapter

focuses on conclusion and recommendation on the working capital problems of Adansi Rural

Bank Limited to know the path to take when managing their working capital.

5.1 CONCLUSION

The management of working capital has been a major constraint to most business organizations

in Ghana and Adansi Rural Bank is no exception. Most business has collapsed due to the misuse

of working capital. Conclusions of this work were based on questionnaires, interviews and

personal observations of all activities concerned with the management of working capital in

Adansi Rural Bank. Although Adansi Rural Bank has qualified personnel who manage the

activities of the company, investigations revealed the following areas which require much

attention with respect to working capital management.

Field survey (2012) page 27 of this work revealed that Adansi Rural Bank Limited bank

borrowings of 20% exceed the company’s personal savings of 10%. This explains the

company’s means of financing their deficit, which affect the working capital of the

company.

The over dependency on bank borrowings as a major source of finance for Adansi Rural

Bank limited will affect their working capital management. The company does not save

enough to attract interest for some period of time. The banks will be reluctant to grant

them loans which must be paid with interest at some time to come or institute very

stringent policies in acquiring loans by the company.

30

5.2 RECOMMENDATION

Working capital represent a net investment in short – term assets. These assets are continually

flowing in and out of a business and are essential for the day-to-day operations. The various

elements of working capital are interrelated and can be seen as a short-term cycle which is an

essential part of a business short-term process. Management must decide how much of each

element of the working capital should be held. Management must be aware of these costs in

order to manage effectively. Management must also be aware that there may be other more

profitable uses for the funds of the business. Hence, the potential benefit must be weighed

against the likely cost in order to achieve the optimum investment. The working capital in a

particular business is likely to change overtime because of changes in the commercial

environment.

This means that working capital decisions are rarely one-off decisions. Management must

ensure that, the level of investment in working capital is appropriate.

In conclusion, there is the need for commitment by the management of Adansi Rural Bank

Limited in their approach to manage working capital effectively. Management Adansi Rural

Bank Limited (especially the finance and administration department) must be willing to put in

place measures that will help prevent loss of funds to the company.

In line with this, these recommendations were provided by the researcher but not limited to the

following:

Adansi Rural Bank Limited must separate its finance department from the administration.

These two departments perform different tasks and must not be merged. The separation

will help the departments to focus on matters of finance and administration respectively.

Information relating to either finance or administration will not fall into the wrong hands.

Adansi Rural Bank Limited must endeavour to keep double – entry records in the lower

management level. Since the company has professionals at the middle level which lower

level management report to, the middle management (particularly the finance

department) must be willing to aid the lower management to keep double – entry records.

31

REFERNCE

Artill, Peter, Maclaneuy and Eddie; 1994. Management for Non-Specialist, 3rd

Edition, Prentice Hall, Page 345.

Nyarkoh K.O; Business Finance for students (in press).

Powell R; 1989. Economics for Professional and business studies, 1st Edition.

London: DP Publication Ltd.

32

APPENDIX

QUESTIONNAIRE

TOPIC: MANAGEMENT OF WORKING CAPITAL IN BUSINESS ORGANIZATIONS AND ITS IMPACT ON THE SOURCES OF FINANCE IN GHANA

NOTE: This research is purely for academic purposes and information given will be treated with the necessary confidentiality. Please tick as applicable and provide relevant explanation where appropriate.

1. Sex male [ ] female [ ]

2. Age 18 – 39 [ ] 40 – 59 [ ] 60 and above [ ]

3. Level of qualification:

SSS [ ] HND [ ] DEGREE [ ] MASTERS [ ]

If any other, please specify ………………………………………………………………………………………………………….

4. What department do you work under?

…………………………………………............................................................................................

......

5. What is your current position in the organization? …………………………………………………………………………………………………………..

6. What role do you play in your department? ………………………………………………………………………………………………………......

33

7. Does your organization have a finance department?

YES [ ] NO [ ]

If no to question (7), which department deals with financial matters in the organization? …………………………………………………………………………………………………………..

8. In your view, what do you think is the meaning of working capital management?

............................................................................................................................................................

......

9. Do you think working capital management is necessary in your organization? YES [ ] NO

[ ]

10. Please give reasons to question (9)

………………………………………………………………………………………………………

………………………………………………………………………………………………………

……

11. What form of financing does your organization operate?

Trade credit [ ]

Short -term securities [ ]

Long-term securities [ ]

34

If any other, please

specify…………………………………………………………………………

12. What is the means of acquiring assets in the organization?

Credit [ ] Cash [ ] Hire purchase [ ] Leasing [ ]

If any other, please specify

……………………………………………………................................

13. Do you sell on credit? YES [ ] NO [ ]

If yes, how long does it take for debtors to pay back?

1-6 days [ ] 1 week [ ] 2 weeks [ ]

1 month [ ] 2 months [ ]

If any other, please

specify………………………………………………………………………….

14. Do you keep records of customers and creditors?

YES [ ] NO [ ]

15. What is the customer’s credit

limit? .................................................................................................

…………………………………………………………………………………………………

……

16. Do you permit advance payments from customers?

35

YES [ ] NO [ ]

If yes, what benefit do you derive?

………………………………………………………………...

17. What means do you adopt in collecting overdue debts?

………………………………………………………………………………………………………

….

………………………………………………………………………………………………………

….

18. How often do you receive stock from your creditors?

Daily [ ] Weekly [ ] Monthly [ ]

If any other, please

specify……………………………………………………................................

19. How long does it take to pay your creditors?

Days [ ] Weeks [ ] Months [ ]

If any other, please specify

………………………………………………………………………...

20. Is your company listed on the stock market?

36

YES [ ] NO [ ]

If yes, what do they deal in?

Shares [ ] Debentures [ ] Government bonds [ ]

If any other, please specify

………………………………………………………………………..

21. Does your organization have access to bank loan at all times?

YES [ ] NO [ ]

22. Does the organization dispose of fixed assets for cash?

YES [ ] NO [ ]

23. Is the organization able to meet its budget?

YES [ ] NO [ ]

Give

reasons……………………………………………………………………................................

24. Are you able to generate profit? YES [ ] NO [ ]

If yes, how does the organization manage profit?

……………………………................................

37

…………………………………………………………………………………………………

……

25. Does the organization have access to bank overdraft?

YES [ ] NO [ ]

If yes, what is the

limit? .....................................................................................................................

26. How do you finance your deficit?

………………………………………………………………………………………………………

…..

………………………………………………………………………………………………………

…..

27. Does the organization factor debt?

YES [ ] NO [ ]

If yes, is it; re-course [ ]

Or non – recourse [ ]

38

UNIVERSITY COLLAGE OF EDUCATION WINNEBA

SCHOOL OF BUSINESS

DEPARTMENT OF ACCOUNTING

ASSESSING THE MANAGEMENT OF WORKING CAPITAL IN BUSINESS

ORGANISATION; A CASE STUDY IN ADANSI RURAL BANK LTD.

BY

RUTH

REGISTRATION NUMBER

A DISSERTATION SUBMITTED TO THE DEPARTMENT OF ACCOUNTING,SCHOOL

OF BUSINESS,UNIVERSITY COLLAGE OF EDUCATION WINNEBA IN PARTIAL

FULFILMENT OF THE REQUIREMENTS FOR THE AWARD OF A BACHELOR OF

SCIENCE(HONOURS) DEGREE IN ACCOUNTING.

39

JUNE, 2012

DECLARATION

I, Ruth do hereby declare that the work presented in this dissertation was solely done by me

under the supervision of Dr. Apart from literature duly cited. I affirm that this work has never

been presented in any institution for the award of a degree.

………………………………. ………………………………..

RUTH DR

(STUDENT) (SUPERVISOR)

DATE:…………………………. DATE:……………………………

……………………………………..

PROFESSOR

(HEAD OF DEPARTMENT)

DATE……………………………………..

40

DEDICATION

To God the almighty for his mercies throughout my studies

To my parents,

And to all my family and my co-workers who helped me through the research.

41

ACKNOWLEDGEMENTS

I am highly indebted to my supervisor, Dr of department of Accounting, University college of

Education Winneba .for his suggestions which proved very useful and effective for the

successful completion of this work.

My special thanks go to Isaac Mensah Bonsu of department of management studies Kwame

Nkrumah University of science and technology for his contribution in typing of this work.

I am grateful to all lecturers of school of Business whose excellent tuition throughout my course

of study has greatly influenced my understanding of this research.

Special thanks go to my family, and all my friends and course mates.

42

TABLE OF CONTENTS

DECLARATION………………………………………………………………………i

DEDICATION………………………………………………………………………..ii

ACKNOWLEDGEMENTS…………………………………………………………..iii

TABLE OF CONTENTS……………………………………………………………..iv

LIST OF TABLES……………………………………………………………………v

CHAPTER ONE-INTRODUCTION

1.0 BACKGROUND…………………………………………………………………1

1.1 STATEMENTOF THE PROBLEM………………………………………………1

1.2 HYPOTHESIS…………………………………………………………………………………………………………………….2

1.3 OBJECTIVES OF THE PROBLEM…………………………………………………………………………………………2

1.4 THE SCOPE AND LIMITATION OF STUDY…………………………………………………………………………..2

1.5 SIGNIFICANCE OF THE STUDY …………………………………………………………………………………………..3

1.6 METHODOLOGY………………………………………………………………………………………………………………..3

1.7 ORGANIZATION OF STUDY ………………………………………………………………………………………………..4

CHAPTER TWO

2.0 INTRODUCTION……………………………………………………………………………………………………………….5

2.1 OPERATING CYCLE …………………………………………………………………………………………………………….5

2.2 WORKING CAPITAL CYCLE OF A MANUFACTURER……………………………………………………………6

2.3 MANAGEMENT OF STOCK…………………………………………………………………………………………………6

2.4 MANAGEMENT OF DEBTORS …………………………………………………………………………………………..9

43

2.5 DEBT COLLECTION POLICY ………………………………………………………………………………………………11

2.6 MANAGEMENT OF CASH …………………………………………………………………………………………………12

CHAPTER THREE

3.0 INTRODUCTION …………………………………………………………………………………………………….16

3.1 RESEARCH FRAME WORK ………………………………………………………………………………………16

3.2 DATA COLLECTION INSTRUMENT …………………………………………………………………………..16

3.3 DATA COLLECTION METHOD ……………………………………………………………………………………16

3.4 METHOD OF DATA ANALYSIS ………………………………………………………………………………….17

3.5 SAMPLING PROCEDURE …………………………………………………………………………………………..17

3.6 PROFILE OF ADANSI RURAL BANK LTD ……………………………………………………………….......17

CHAPTER FOUR

4.0 INTRODUCTION ……………………………………………………………………………………………………….18

4.1 BACKGROUND OF RESPONDENTS …………………………………………………………………………….18

CHAPTER FIVE

5.0 INTRODUCTION ………………………………………………………………………………………………………..29

5.1 CONCLUSION …………………………………………………………………………………………………………….29

5.2 RECOMMENDATION ………………………………………………………………………………………………..30

REFERENCE ……………………………………………………………………………………………………………………31

APPENDIX …………………………………………………………………………………………………………………….32

44

45