PowerPoint Presentation - University of Exeter · FRS102 - Income Financial Statements Presentation...

27

FRS102 Tanya Hitchen & Izzy Clayton Contact: [email protected]

Transcript of PowerPoint Presentation - University of Exeter · FRS102 - Income Financial Statements Presentation...

FRS102 Tanya Hitchen & Izzy Clayton Contact: [email protected]

FRS102 What is FRS102?

Impact on:

Income

Expenditure

Other Comprehensive Income

Balance Sheet

Timeline

What do I need to do?

What is FRS102?

Change in UK Accounting Standards

Driven by harmonisation with International Accounting Standards

FRS102 is a reduced version of full IFRS

1st year of FRS102 accounts is 2015/16 BUT

Need to restate 2014/15 financial statements

Restate opening balance sheet as at 1 August 2014

What is FRS102?

What have we done so far?

FE/HE SORP – applying FRS102 to the HE sector

Impact of FRS102 understood by Audit Committee and Council

Accounting policy choices approved by Audit Committee and Council

Opening balance sheet restated and approved by Auditors

Template accounts created

Some APTOS coding changes

Communication & Training

FRS102 - Income

3 Types of income under FRS102, impact on revenue recognition:

Exchange Transactions

Non-exchange Transactions

Government Grants

FRS102 - Income Exchange Transactions

Sale of goods and services in return for consideration

Tuition Fees

Commercial Research

Consultancy and some ‘Other Income’

Income for delivery of services recognised on % completion (can use e.g. time

or cost allocation)

No change to current accounting policies

FRS102 - Income Non-Exchange Transactions & Government Grants

Funder does not receive equal value exchange for cash

Includes both revenue and capital grants

DCG reserve no longer exists

New Accounting Policy: Income recognised in line with performance

conditions

Matching concept no longer exists

Timing differences between income and expenditure

FRS102 - Income

Performance Condition: A condition that requires the performance of a particular

level of service or units of output to be delivered, with payment of, or entitlement

to, the resources conditional on that performance.

Extract from FRS102

FRS102 - Income Research Grants

If funder receives benefit = exchange transaction = no change

If funder does not receive benefit = non-exchange transaction = new rules

Most research grant funding is conditional on:

Delivery of specified research

Incurring pre-determined expenditure

Therefore performance condition is delivery of a particular level of service,

measured by proportion of costs incurred.

No impact despite different accounting policy.

FRS102 - Income Research Grants

If terms and conditions do not include performance conditions (e.g.

donations), income must be recognised on entitlement.

Mis-match between income and expenditure.

Only a small proportion of research income affected – in 2013/14 impact

would have been £150k.

Use SUBJ1 D03 for Research Income without Performance Conditions –

usually D01.

FRS102 - Income

Other Grants

Revenue grants to be recognised as income upon completing any

performance conditions.

If no performance conditions, recognise upon entitlement.

Capital grants received included as income (previously in deferred capital

grant reserve).

Use performance conditions accounting rules.

FRS102 - Income

Endowments & Donations

Currently only unrestricted donations recognised as income.

Endowments received taken to endowment reserve via STRGL

FRS102 – all new endowments and donations will be recognised as income

upon entitlement.

FRS102 - Income

Service Concessions:

Impact on Income and Expenditure for value of student rents (UPP

arrangement 2013/14 £13m)

Increase in assets and liabilities as we recognise the one year liability for

any nominations made (UPP arrangement 2013/14 £13m)

Consideration to be made when setting up any major new contracts

FRS102 - Income Financial Statements Presentation

Original Restated

Income 2013/14 £000s

Funding Body Grants 47,497

Tuition Fees 150,623

Research Income 60,071

Other Income 62,279

Investment Income 3,350

Total incl JVs 323,820

Less share of JVs -19,360

Total Income 304,460

Income 2013/14 £000s

Tuition Fees 150,623

Funding Body Grants 44,677

Research Income 57,663

Other Income 54,703

Investment Income 3,350

Total before G&D 311,017

Donations/Endowments 1,294

Other grant income 7,278

Total Income 319,589

FRS102 - Expenditure

Main areas of change to expenditure under FRS102:

Service concessions – as previously noted

Pension changes

Annual leave accrual

Component accounting

FRS102 - Expenditure

Pension schemes:

Changes for both USS and ERBS

USS - Now we need to account for deficit recovery plan

• Large impact on Balance Sheet – pension liability

• Impacts staffing costs

• Awaiting the latest USS valuation in order to calculate the recovery

plan

• Volatile based on triennial valuations

FRS102 - Expenditure

Pension schemes:

ERBS

Difference in the calculation of the finance charges

Estimated £2m additional operating cost for 2013/14

Corresponding credit to the actuarial movement – below the line

FRS102 - Expenditure Annual leave accrual

Need to account for any unused annual leave at year-end as this is

essentially a liability of the University

Results in increased cost in first year and then variable year-on-year

Component accounting

Splitting out assets into smaller components

Impact on depreciation with buildings broken into smaller components

FRS102 - Expenditure

Financial statements presentation

Expenditure 2013/14 £000s

Staff costs 164,167

Fundamental restructuring costs -

Other operating expenses 110,725

Depreciation 37,215

Interest & other finance costs 8,621

Total Expenditure 320,728

Expenditure 2013/14 £000s

Staff costs 168,465

Other operating expenses 108,750

Depreciation 21,944

Interest & other finance costs 7,750

Total Expenditure 306,909

FRS102 – Other Comprehensive Income Inclusion of certain transactions that used to only be recognised in reserves.

Movements in market value of investments

Actuarial gains / losses on pension schemes

Changes in the fair value of financial instruments

Volatility of other comprehensive income

Considering appropriate performance measures for the sector

FRS102 – Other Comprehensive Income Statement of Comprehensive Income £’000s

Total income 319,589 Total expenditure 320,728 Surplus/deficit before other gains/losses and share of surplus/deficit in joint ventures associates (1,140)

Gain/(loss) on investments 2,970 Share of operating surplus/ (deficit) in joint venture(s) 499

Surplus / (deficit) for the year 2,329

Unrealised surplus on revaluation of land and buildings 45,104 Actuarial (loss)/gain in respect of pension schemes (7,367) Change in fair value of hedged financial instrument(s) 100 Total comprehensive income for the year 40,166

Total comprehensive income for the year comprises: Endowment comprehensive income for the year 1,118 Restricted comprehensive income for the year (1,562) Unrestricted comprehensive income for the year 40,610

40,166

FRS102 – Balance Sheet Per the 2013/14 Financial Statements Restated Under FRS102

2014 2014

FIXED ASSETS £000s Non-Current Assets £000s

Tangible assets 663,079 Intangible assets and goodwill 3,391

Investment assets 7,330 Tangible fixed assets 673,207

Investment assets - Joint ventures 3,048 Heritage assets 7,171

673,457 Investments 29,161

Investment in joint venture 3,048

ENDOWMENT ASSETS 30,265 Total Non-Current assets 715,978

CURRENT ASSETS Current assets

Stocks 437 Stock 437

Debtors - Amounts falling due within one year 31,155 Trade and other receivables 47,614

Debtors - Amounts falling due after more than one year 16,459 Investments 30,276

Investments 30,276 Cash and cash equivalents 77,955

Cash at bank and in hand 76,693 Total current assets 156,283

155,020

Creditors - amounts falling due within one year

CREDITORS: AMOUNTS FALLING DUE WITHIN ONE YEAR -72,819 Reimbursable to funding council 571

Bank loans and external borrowing 3,823

Obligations under finance leases 13,652

Other creditors 69,760

Total creditors (amounts falling due within one year) 87,805

NET CURRENT ASSETS 82,201 Net current (liabilities) / assets 68,477

TOTAL ASSETS LESS CURRENT LIABILITIES 785,923 Total assets less current liabilities 784,455

FRS102 – Balance Sheet Per the 2013/14 Financial Statements 2014 Restated Under FRS102 2014

CREDITORS: AMOUNTS FALLING DUE £000s Creditors: amounts falling due after more than one year £000s

AFTER MORE THAN ONE YEAR -219,140 Reimbursable to the funding council 656

Bank loans and external borrowing 199,088

LESS: PROVISION FOR LIABILITIES 0 Obligations under Finance leases 19,396

Other 26,700

TOTAL NET ASSETS EXCL. PENSION LIABILITY 566,783 Total creditors (amounts falling due after more than one year) 245,840

NET PENSION LIABILITY -26,551 Provisions

Pension provisions 48,640

Other provisions -

Total provisions 48,640

TOTAL NET ASSETS INCL. PENSION LIABILITY 540,232 Total net assets 489,975

DEFERRED CAPITAL GRANTS 144,291

ENDOWMENTS

Expendable 9,039

Permanent 21,226

30,265

Restricted Reserves

RESERVES Income and expenditure reserve - endowment fund 30,265

Income and expenditure reserve (excl Pension Reserve) 89,291 Income and expenditure reserve - restricted reserve -

Pension Reserve -26,551 Unrestricted Reserves -

Income and expenditure reserve (incl Pension Reserve) 62,740 Income and expenditure reserve - unrestricted 156,774

Revaluation reserve 302,936 Revaluation reserve 302,936

365,675 Total Restricted and Unrestricted Reserves 489,975

TOTAL FUNDS 540,231 Total Reserves 489,975

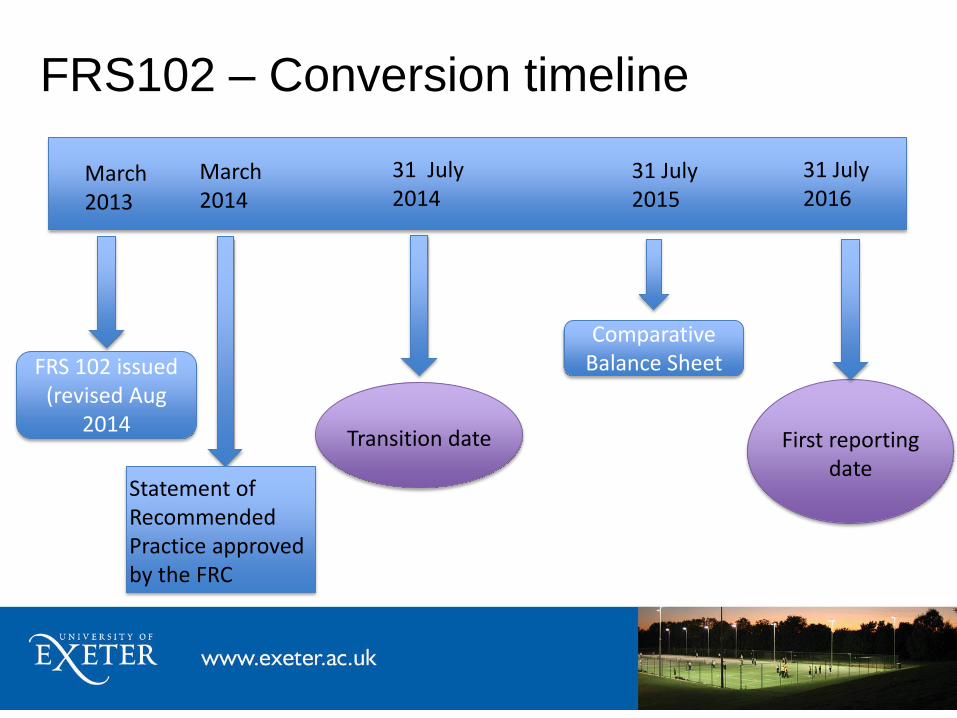

FRS102 – Conversion timeline

March 2014

31 July 2014

31 July 2015

31 July 2016

Statement of Recommended Practice approved by the FRC

Transition date First reporting date

Comparative Balance Sheet

March 2013

FRS 102 issued (revised Aug

2014

FRS102 - Timeline

Date Task Status

20 May Council – FRS102 Impact Paper & KPMG assurance report Sent

12 June Deadline to produce accounting policy papers etc for Audit Committee

Restatement of opening balance sheet – Uni & Group

Reserves reconciliation / explanation – Uni & Group

Sent

2 July Workshop to HoFs and Finance Teams

7 July Workshop to HoFs and Finance Teams

31 July

Document of changes to coding for colleges and services & timetable for future

requirements

July Council to approve 2015/16 Accounting Policies

1 Aug Implement new coding for FRS102

11 Sept Draft Financial Statements under current UK GAAP

Oct-Dec Restate 2014/15 Financial Statements under FRS102

Jan 16 KPMG audit of restated 2014/15

Feb 16 Restatement of 2015/16 Budgets in time for 2016/17 budget setting

Sept 16 Produce 2015/16 Financial Statements under FRS102

Timetable for budgeting changes still to be agreed

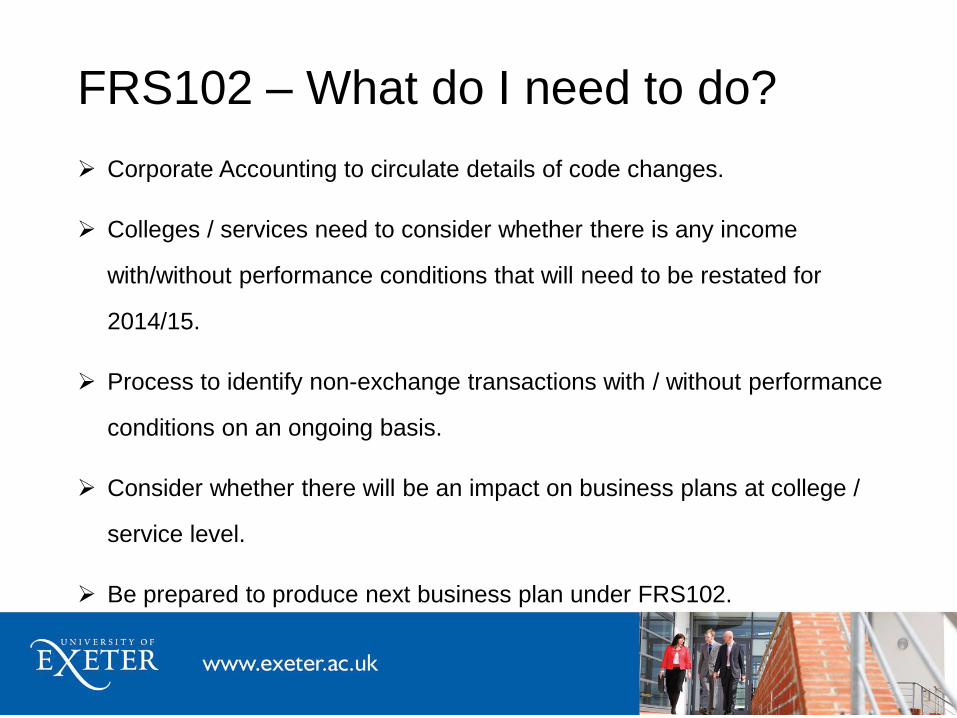

FRS102 – What do I need to do?

Corporate Accounting to circulate details of code changes.

Colleges / services need to consider whether there is any income

with/without performance conditions that will need to be restated for

2014/15.

Process to identify non-exchange transactions with / without performance

conditions on an ongoing basis.

Consider whether there will be an impact on business plans at college /

service level.

Be prepared to produce next business plan under FRS102.