PowerPoint Presentation · •MoM increase in inflation by 0.9% was due to the expenditure value...

18

First Capital Research Feb 2019

Transcript of PowerPoint Presentation · •MoM increase in inflation by 0.9% was due to the expenditure value...

First Capital Research

Feb 2019

Feb 2019First Capital Research 2

• Inflation……………………………………………………………………………………………… 3

• M2B & Sector Credit…………………………………………………………………................… 5

• Reserves & Liquidity………………………………………………………………………............ 6

• Currency Movement…………………………………………………………………................... 7

• Government Securities……………………………………………………………….................. 8

• Finance Sector Rate Movement……………………………………………………………..... … 11

• External Sector…………………………………………………………………………………….. 12

• Tourist Arrivals…………………………………………………………………………………….. 16

• Global Markets…………………………………………………………………………………….. 17

• MoM increase in inflation by0.9% was due to theexpenditure value decreaseof Food items by 0.75% andincrease of Non Food items by1.66%. Price decline inVegetable led the valuedecrease in the food category,while in Non Food Category,increase was mainly led byHousing Water Electricity Gasand Other Fuels (0.89%).

• The YoY inflation increased to3.7% in January 2019 from2.8% reported in Decemberas a result of increase in valueof Non Food Group.

First Capital Research 3

5.8%

4.5% 4.2%

3.8%4.0%

4.4%

5.4%

5.9%

4.3%

3.1%3.3%

2.8%

3.7%3.5% 3.5%

3.4%

3.5%3.2%

3.4%

3.9%

3.7%3.8%

3.8%

3.4%

3.1%

5.5%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Inflation YoY Core Inflation YoY

Source: Dept. Census and Statistics Feb 2019

• NCPI for November 2018decreased to 0.4% from 1.0%recorded in November 2018.

• YoY inflation of food group hasdecreased to -4.5% inDecember 2018 while NonFood Group decreased to 4.7%compared to 5.2% recorded inNovember 2018.

First Capital Research4

7.3%

5.4%

3.2%

2.8%

1.6%

2.1%

2.5%

3.4%

2.5%

0.9%

0.1%

1.0%

0.4%

2.7%

2.1% 2.0% 1.9% 1.9% 1.7% 1.8%

2.3%

2.7%

3.1%3.4%

3.1% 3.1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

NCPI YoY Core NCPI YoY

Source: Dept. Census and StatisticsFeb 2019

M2b Growth – November 2018MoM +0.78%, YoY +13.89%, YTD +11.64%

First Capital Research 5

Private sector credit for the month of November 2018 amounted to LKR 79.3Bn, thereby, overall credit growth

(state & private) increased to LKR 135.2Bn, +29%YoY. Government credit reflected a net borrowing for the

fourth consecutive month amounting to LKR 56.0Bn.

State Credit & Private Credit – November 2018 Private credit MoM +1.5%, YoY +15.69%, YTD +14.25%

-50

4067

42 4468

29

-40 -29

48

172

40 5662

60 20 58

122

22

29 8347

46

107

7479

-100.00

-50.00

0.00

50.00

100.00

150.00

200.00

250.00

300.00

LK

R '

Bn

State Credit Private Credit Source: CBSL

0.40%

2.01%

1.11%

1.13%

2.42%

1.29%

-0.31%

1.15%

0.71%1.05%0.98%

0.79%

0.78%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

5,600

5,800

6,000

6,200

6,400

6,600

6,800

7,000

7,200

M2b MoM Growth

Source: CBSL

LKR

Feb 2019

First Capital Research 6

▪ Foreign Reserves declined to USD 6.1Bn inJanuary 2018 (from USD 6.9Bn in December2018).

▪ Market liquidity showed a continuousdeclining trend for the month of Januaryalthough negativity in the liquidity narroweddown towards the end of the month.

-150

-100

-50

0

50

100

Ma

rke

t L

iqu

idit

y (

LK

R '

Bn

)

Source: CBSL

Feb 2019

7,6

73

7,9

14

7,3

09

9,9

27

8,7

69 9,2

47

8,4

39

8,5

91

7,1

64

7,9

00

7,0

05

6,9

19

6,1

42

3,500

4,500

5,500

6,500

7,500

8,500

9,500

10,500

USD 'Mn

Source: CBSL

USD:LKR Movement Sri Lankan Rupee vs Global Currencies

First Capital Research 7

Source: CBSLJa

nu

ar

y

20

19

YT

D 2

01

9

179.5

180.5

181.5

182.5

183.5

Source: CBSL

Feb 2019

3.4%

1.6%

1.1%

0.1%

-1.0%

-1.3%

-1.8%

-2.1%

-3.0% -2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0%

India Rupee

US Dollar

Euro

Japan YEN

China Renminbi

Aus Dollar

UK Pound

Can Dollar

3.4%

1.6%

1.1%

0.1%

-1.0%

-1.3%

-1.8%

-2.1%

-3.0% -2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0%

India Rupee

US Dollar

Euro

Japaneese yen

China Renminbi

Aus Dollar

UK Pound

Can Dollar

First Capital Research 8

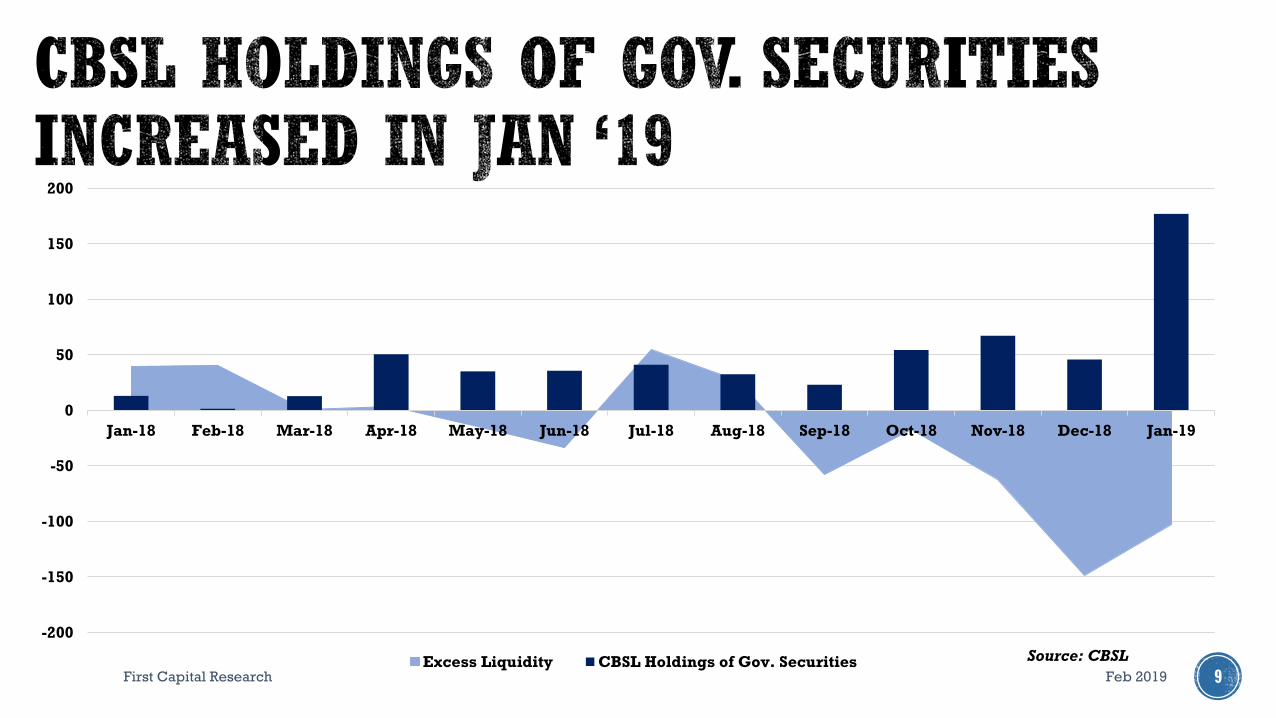

Week EndingBills

('Mn)

Bonds

('Mn)Total

04-Jan-19 15,500 15,500

11-Jan-19 20,000 20,000

18-Jan-19 26,000 98,000 124,000

25-Jan-19 23,500 23,500

Total Issued 183,000

January 2018 YTD

Maturities 149,846 149,846

New Issues 183,000 183,000

Excess/(Deficit) 33,154 33,154

CBSL Holdings of Gov. Securities YTD

As at End Jan.2018 177,093

As at End Dec. 2018 45,797

Increase/ (Decrease) 131,296 131,296

Feb 2019

First Capital Research 9

-200

-150

-100

-50

0

50

100

150

200

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19

Excess Liquidity CBSL Holdings of Gov. Securities Source: CBSL

Feb 2019

First Capital Research 10

The month of January witnessed a downward shift in the yield curve mainly centered on the mid to long tenor maturities.

This was reflected by the dip in mid to long tenor maturities by 40-70bps compared to the dip in short tenor by 2-68bps.

Further, last two weeks of the month saw some foreign interest in government securities, recording an increase in foreign

holding in government securities while also causing LKR to appreciate by 2.5% to close at LKR 178.40.

8.00%

8.50%

9.00%

9.50%

10.00%

10.50%

11.00%

11.50%

12.00%

12.50%

31-Dec 31-Jan 30-Sep

Interest Rate Change (bps)

Tenure 31-Dec 31-Jan Change (bps) 30-Sep Change (bps)

3M 9.80% 9.55% -25 8.63% 92

6M 9.90% 9.88% -2 9.15% 73

1 Yr 10.95% 10.63% -32 9.63% 100

2 Yrs 11.23% 10.68% -55 10.13% 55

3 Yrs 11.53% 10.85% -68 10.85% 0

4 Yrs 11.60% 10.95% -65 10.95% 0

5 Yrs 11.70% 11.00% -70 11.08% -8

6 Yrs 11.70% 11.10% -60 11.13% -3

7 Yrs 11.80% 11.15% -65 11.15% 0

8 Yrs 11.80% 11.27% -53 11.15% 12

10 Yrs 11.95% 11.35% -60 11.15% 20

12 Yrs 12.08% 11.45% -63 11.20% 25

15 Yrs 12.10% 11.58% -52 11.25% 33

20 Yrs 12.13% 11.73% -40 11.30% 43

AWPR vs AWDR Interest Spread

First Capital Research 11

Source: CBSLSource: CBSL

Source: CBSL

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

Interest Rate Spread

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

AWPR vs AWDR

AWPR AWDR

Feb 2019

First Capital Research 12

Exports for the month of Nov was recorded at USD 980Mn,+4.1%YoY basis, mainly contributed

by Industrial Exports (+10.4%YoY) which was largely driven by Textiles and garments

(+45.5%YoY). Meanwhile, earnings from agricultural exports declined in Nov 2018 as well due

to weakened earnings in tea, spices, coconut and sea food .

Category 2017

(USD ‘Mn)

2018

(USD ‘Mn)

Change

(%)

Industrial Exports

- Nov

- YTD

713.5

7745.6

787.9

8444.9

10.4

9.0

Agricultural

- Nov

- YTD

224.1

2,547.5

187.8

2,362.7

(16.2)

(7.3)

Mineral and other

- Nov

- YTD

3.3

47.8

3.9

48.6

17.2

1.6

Total

- Nov

- YTD

940.9

10,340.9

979.6

10,856.2

4.1

5.0

86

5

86

8

1,0

42

79

5

84

1

98

7

1,0

16

1,0

01

1,0

11

97

6

94

1

1,0

20

96

5

91

6

1,1

08

79

5

92

4

1,0

24 1

,07

3

1,0

37

1,0

55

97

9

98

0

700

750

800

850

900

950

1,000

1,050

1,100

1,150

USD 'Mn

2017 2018 Source: CBSL

Feb 2019

First Capital Research 13

Category 2017

(USD ‘Mn)

2018

(USD ‘Mn)

Change

(%)

Consumer goods

- Nov

- YTD

407.7

4069.0

363.5

4622.7

(10.8)

13.6

Intermediate

- Nov

- YTD

1072.5

10,242.0

1074.6

11,504.9

0.2

12.3

Investment goods

- Nov

- YTD

459.7

4,475.9

326.0

4,296.4

(29.1)

(4.0)

Total

- Nov

- YTD

1,940.4

18,931.3

1,764.6

20,498.1

(9.1)

8.3

1,7

98

1,6

11

1,8

69

1,6

04

1,7

25

1,5

41

1,5

91

1,8

57

1,6

67

1,7

27

1,9

40 2

,04

8

2,0

14

1,9

78

1,9

79

1,7

94

1,8

57

1,8

20

1,7

55

1,8

87

1,7

68

1,8

83

1,7

65

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2017 2018 Source: CBSL

USD 'Mn

Import expenses decreased in Nov 2018 by 9.1%YoY. Decrease was mainly driven by consumer

goods (-10.8%YoY) dominated by decreased expenditure on Food and beverages

(-36.5%YoY) amidst a notable decline in Rice. Imports of Intermediate goods increased slightly

while investment goods declined by 29.1%.

Feb 2019

First Capital Research 14

-1,000

-1,028

-1,049

-1,062

-871

-999

-933

-795

-681

-850

-713

-903

-785

-1,200 -1,000 -800 -600 -400 -200 0

Balance of Trade

Source: Central Bank

Feb 2019

MARGINALLY DECLINES MOM

Nov

Trade Balance -13.2%

First Capital Research15

Nov

USD ‘Mn2017 2018

Change

(%)

Trade Balance -999.0 -785.0

Earnings from

Tourism311.0 367.0 +18.2

Workers’

Remittances588.0 555.0 -5.7

YTD

USD ‘Mn2017 2018

Change

(%)

Trade Balance -8,590.0 -9,642.0

Earnings from

Tourism3,471.0 3,905.0 +12.5%

Workers’

Remittances6,493.0 6,431.0 -0.9%

Worker Remittances declined to USD 555.0Mn (-5.7%YoY). Earnings from

tourism recorded an increase for the month of Nov reflecting an YoY increase

of +18.2%.

BoP for Jan-Nov 18 was USD -807Mn compared to the previous YTD of Jan-Oct

‘18 amount of USD -157Mn, illustrating an outflow of USD 650Mn for the month

of November.U

SD

'B

n

2,005

-807-1,000

-500

0

500

1,000

1,500

2,000

2,500

Jan-Nov 17 Jan-Nov 18

-8,590-9,642

3,471 3,905

6,493 6,431

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

Jan-Nov 17 Jan-Nov 18

Trade Balance Earnings from Tourism Workers’ Remittances

US

D '

Bn

Total = 9,964 Total = 10,336

Feb 2019

UP 2.2% UP 2.2%

First Capital Research 16

Tourist arrivals into SL grew by 2.2% in January 2019 compared to an year ago. Arrivals were mainly

dominated by India followed by United Kingdom and China. YoY tourist arrivals from Italy increased by

20.3% while arrivals from Germany and France were down by 8.3% and 2.7% respectively.

Feb 2019

20

40

60

80

100

120

140

160

180

200

220

240

260

280'00

0

Tourist Arrivals

2017 2018 2019

Source: SLTDA

First Capital Research 17

The U.S. trade deficit with China is set to balloon again: President

Donald Trump underscored his desire to reduce the trade gap with

China in his State of the Union speech, yet the deficit is on track to

balloon again this year as a solid economy boosts American demand

for imports. The total U.S. deficit in goods with China jumped by USD

37.6Bn, or 10.9%, in the first 11 months of 2018 compared with a year

earlier, according to Commerce Department figures that were updated

with November data. www.bloomberg.com

No quick fix for citizen rights under no-deal Brexit, says EU

official: Nearly 5Mn British and EU citizens could be stuck in limbo

after a no-deal Brexit, a senior EU official has warned, who said it could

take several years “to pick up the pieces” of the UK crashing out of the

bloc. Politicians on both sides of the Brexit divide have urged

negotiators to ringfence the existing agreement on citizens’ rights if

the UK leaves without a deal on 29 March. The Brexit withdrawal

agreement protects most of the rights of the 3.4Mn EU citizens in the

UK and the 1.3Mn British people in the EU. But since MPs rejected the

agreement by a crushing majority last month, these protections have

been thrown into doubt. www. theguardian.com.com

Oil scores best January on record as supply cuts revive market:

Oil closed lower but still scored its best January gain on record, after a

month in which OPEC’s emergency supply cuts started to take root and

panic eased about the global economy. Futures in New York dived

0.8% late on 31.01.19, after a government report that U.S. production

had swelled to an all-time high in November. www.bloomberg.comSource: Bloomberg

-6.00% -1.00% 4.00% 9.00%

Nikkei 225

S&P 500

Dow Jones

KSE100

Euro Stoxx 50

VN Index

FTSE 100

Nifty

Feb 2019

First Capital Research

Feb 2019