Powering investments: Challenges for the liberalised eleCtriCity · PDF filethe European...

31

POWERING INVESTMENTS: CHALLENGES FOR THE LIBERALISED ELECTRICITY SECTOR FINDINGS AND RECOMMENDATIONS A EURELECTRIC report, DECEMBER 2012

Transcript of Powering investments: Challenges for the liberalised eleCtriCity · PDF filethe European...

Powering investments: Challenges for the liberalised eleCtriCity seCtor

findings and reCommendations

a eureleCtriC report, deCember 2012

The Union of the Electricity Industry–EURELECTRIC is the sector association representing the common interests of the electricity industry at pan-European level, plus its affiliates and associates on several other continents.

In line with its mission, EURELECTRIC seeks to contribute to the competitiveness of the electricity industry, to provide effective representation for the industry in public affairs, and to promote the role of electricity both in the advancement of society and in helping provide solutions to the challenges of sustainable development.

EURELECTRIC’s formal opinions, policy positions and reports are formulated in Working Groups, composed of experts from the electricity industry, supervised by five Committees. This “structure of expertise” ensures that EURELECTRIC’s published documents are based on high-quality input with up-to-date information.

For further information on EURELECTRIC activities, visit our website, which provides general information on the association and on policy issues relevant to the electricity industry; latest news of our activities; EURELECTRIC positions and statements; a publications catalogue listing EURELECTRIC reports; and information on our events and conferences.

Dépôt légal: D/2012/12.105/41

EURELECTRIC pursues in all its activities the application of the following sustainable development values:

Economic Development Growth, added-value, efficiency

Environmental Leadership Commitment, innovation, pro-activeness

Social Responsibility Transparency, ethics, accountability

Energy Policy and Generation Committee, with the input of all other EURELECTRIC Committees Chair : David Porter (GB); Vice Chair: Michel Matheu (FR);

Members: Constantin Balasoiu (RO); Maris Balodis (LV); Ulrich Bang (BE); Gábor Briglovics (HU); Egle Ciuzaite (LT); Gwyn Dolben (GB); Karl Heinz Gruber (AT); Sotirios Hadjimichael (GR); Sigrid Hjornegard (NO); Alois Hroch (SK); Esa Hyvarinen (FI); Lars Jacobsson (SE); André Jurjus (NL); David Manning (IE); Giuseppe Montesano (IT); Pedro Neves ferreira (PT); Marcel Ottenkamp (CH); Raine Pajo (EE); Antonis Patsali (CY); Véronique Renard (BE); Oli Gretar Blondal Sveinsson (IS); Stanislaw Tokarski (PL); Angel Luis Vivar (ES); Michael Wunnerlich (DE); Fernand Zanter (LU);

TF Investment Action Plan (which includes the members of the other committees/groups involved):

José Arrojo De Lamo (IT); Franz Bauer (VGB PowerTech e.V.); Vittorio D’ecclesiis (IT); Hakon Egeland (NO); Zuzana Krejcirikova (CZ); Ignacio Martinez Del Barrio (ES); Tomas Mueller (AT); Simonetta Naletto (IT); Alan Svoboda (CZ); Oluf Ulseth (NO); Luc Van Nuffel (BE); Owen Wilson (IE); Sami Andoura (Notre Europe); Peter Atherton (Citigroup Global Markets); Allan Baker); Manuel Baritaud (International Energy Agency (IEA)); Markus Becker (GE Energy); Alain F. Berger (Alstom); David Buchan; Simon Chisholm; Stefano Da Empoli (I-Com - Istituto per la Competitività); Severin Fischer ); Cheryl Fisher (European Investment Bank); Holger Gassner (RWE Innogy GmbH); Stefanie Haeger (Future Matters AG); Péter Kiss; Melle Kruisdijk (Wärtsilä Netherlands BV); Thomas Legge; Felix Christian Matthes (Oeko-Institut e.V.); Volkmar Pflug (Siemens AG); Fabien Roques (CERA - Cambridge Energy Research Associates); Guy Turner (Bloomberg News); Stefan Ulreich (E.ON AG); Herbert Urban (VGB PowerTech e.V.); Owen Wilson (Electricity Supply Board (ESB)); Georg Zachmann (Bruegel);

Contact:Susanne Nies - [email protected] Schlosser - [email protected] Lorubio - [email protected]

POWERING INVESTMENTS: CHALLENGES FOR THE LIBERALISED ELECTRICITY SECTOR

FINDINGS AND RECOMMENDATIONS

Executive Summary 3

Introduction 5

1 Keeping the lights on, or the quest for secure electricity supply 6

2 Investment needs: forget about the trillion, more realism will lead to results! 10

Afocusonwhatisfeasibleandrealisticby2020 11

3 A troubled investment climate 14

Financingandregulationaretwosidesofthesamecoin 15

Volatileregulationpursuingconflictingobjectives 16

Recommendations 23

TABLE OF CONTENTS

TAB

LE O

F CO

NTE

NTS

PoweringInvestments:Challengesfortheliberalisedelectricitysector|3

ExECUTIVE SUMMARY

ExEC

UTI

VE

SU

MM

ARY

InvestmentdecisionsintheEuropeanelectricityindustryaremoredifficultthantheyshouldbe.Today’sbusinesscaseforinvestmentsisinfluencedmorebypoliticalandregulatorydecisionsthanbycustomerdemand.Ifpoliticalandregulatoryrisksarehigh,investmentmaybedeferredorinvestorsmaylookforabiggerreturn.Thisultimatelyrisksmakingelectricitymoreexpensiveforcustomers.

Theeconomicrecessionhasreducedsalesofenergyandcompanies’abilitytoinvest.Existinglevelsofdebt,pressureoncompanycreditratingsandgovernmentattacksoncompanyfinancesmakenewinvestmentchallenging–evenmoresowhereprojectsareriskierthantheconventionalinvestmentsofthepast.

AlthoughthereissufficientgeneratingcapacityincertainpartsofEurope,theincompletedevelopmentofthesinglemarketmeansitisnotaseasyasitshouldbeforoneregion’ssurplustomeetanotherregion’sshortage.

Thereisinherenttensionbetweenthethreemainstrandsofenergypolicy(securityofsupply,competitivepricesandreductionofcarbonemissions).Moreover,therelativeimportanceoftheseobjectivesseemstochangeovertime,atbothEUandnationallevel.Thisincreasesriskforinvestors.

Thesinglemarketremainsincompleteandpolicymakersmaysometimesdisregardthereasonsforpursuingit:fromtimetotime,thereisatendencyto‘prescribe’solutionsandtargets(e.g.withintheRenewableEnergyDirective)which,inaproperlyfunctioningmarket,wouldbedeterminedcompetitivelybyinvestors’decisions.

AstheEUproceedsslowlytowardsimplementingthesinglemarket,memberstatesaremakingpolicydecisionsindividually.Thesedecisionsarenotnecessarilyinlinewiththedevelopmentofthesinglemarket.

Theforcingontothesystemoftechnologieswhichcannotdeliverpowerondemand,butwhichoftendisplace‘dispatchable’technologies,isdamagingthereturnsonexistinginvestments.

4|PoweringInvestments:Challengesfortheliberalisedelectricitysector

Againstthisbackdrop,EURELECTRICproposesthefollowing:

• Thecompletionofawell-functioningandintegratedenergymarketshouldbegivenmorepriority.

• ThereshouldbegreateralignmentbetweenEUenergypolicyandthepoliciesofmemberstates–perhapstheElectricityCo-ordinationGroup,withguidelinesfromtheEuropeanCommission,couldbecometheorganisationtoencouragethis.

• Piecemealdecisionsareunhelpful–policyshouldbemoreholistic,recognisingtheintegratednatureofelectricitysystems.

• Innovationinthepowersectorisvital.Themechanismsfordeliveringitshouldbereviewed–EURELECTRICwillpresentrelatedproposalsin2013.

• Theenergytransitionismademoredifficultwhenpolicyforcesthepace,leadingtosuboptimaloutcomes.Realistictimingiscritical.

• The‘targetsforeverything’approachtoenergypolicyshouldbeabandoned.Itshouldbereplacedbyabroadframeworkthatallowsthemarkettowork,therebyencouragingthoseinvestmentsthatmakethemosteconomicsenseandreducingthecostsofthelow-carbonenergytransition.

ExEC

UTI

VE

SU

MM

ARY

PoweringInvestments:Challengesfortheliberalisedelectricitysector|5

TheEURELECTRIC Investment Action Plan assessedthemainobstaclestoinvestmentintheliberalisedpowersector.Investmentsinregulatedpartsoftheelectricityvaluechain–distributionnetworksandtransmission–weredeliberatelykeptoutofthereport’sscope:theyarenotsubjecttothesameconstraintsandfacedifferentchallengestoday.1Neverthelessreferenceismadetothefullelectricityvaluechainwhereneeded–e.g.theimpactofmoretransmission,smarterdistributiongrids,storageorenergyefficiencyongenerationadequacy–sinceafragmentedviewonthepowersystemcanleadtoerroneousconclusions.

Twomeetingsofahigh-levelEURELECTRICTaskForcetookplaceinAprilandJuly2012,gatheringrepresentativesfromtheelectricityindustry,bankingsector,consultancies,thinktanksandacademia.Theyaddressedgenerationadequacy,investmentsorinvestmentobstaclesbytechnology,taxesandregionaldifferencesininvestmenttrends,aswellastheregulatoryframework.AbroaderexchangeofviewstookplaceataninternalworkshopinSeptemberwhenparticipantsfromtheindustryatlargewereinvolved.A surveyontheinvestmentclimate,commissionedbyEURELECTRICanddiscussedattheworkshop,clearlystressedthatthecurrentregulatoryuncertaintyandpolicycontradictionswerethemostimportantobstaclestoinvestments,asseenbytheindustry.2

Investorshaveotheropportunitiesbeyondtheelectricitysector,andasabankerhighlightedduringtheworkshop,wouldratheravoidEuropecurrentlyandgoelsewhere.Thisperceptionappliesasmuchtotheso-called‘new’investorsastotheexistingones.EURELECTRICmembersbelievethatitistimetoputEuropemoresharplyinfocus:itistheEuropeanenergytransitionthattheywanttoinvestin.ThisreportistargetedtotheEUinstitutions,butalsotonationalpoliticiansandregulators:policymakinghastobeoptimisedtosupportthetransitiontothelow-carbonenergysystem–whichcanultimatelyonlybedeliveredultimatelybytheprivatesector.

1 InvestmentconditionsfordistributiongridcompanieshavebeenaddressedinotherEURELECTRICpublicationssuchastheRegulation for Smart Grids report.

2Energyleaderstatementsgatheredaspartofthissurveyareplacedthroughoutthedocumentintheformofquotes.

INTRODUCTION

INTR

OD

UCT

ION

6|PoweringInvestments:Challengesfortheliberalisedelectricitysector

KEEPING THE LIGHTS ON, OR THE qUEST FOR SECURE ELECTRICITY SUPPLY

1

PoweringInvestments:Challengesfortheliberalisedelectricitysector|7

Evaluatinginvestmentneedsinpowerplantsdependsontheanswerstoasimple–yetdecisive–setofquestions:Howmuchpowergenerationcapacitydoweneedtokeepthelightson?Howdowemakesurethatpowerplantswithcompletelydifferentoperatingcharacteristicscontinuetocontributetosecuringsupply?Doweneednewpowerplants?Whatkindofcapabilitiesdoweneedfrompowerplants?

Itistruethatbothexisting and new power plants are subject to the same macro-trends,interaliathedevelopmentofelectricitydemandandcompliancewithEUclimateorenergypolicies.ButinmanyEUcountriesthereisaparticularchallenge:reducedrunninghoursforconventionalpowerplantsthatarebeingdisplacedbyrenewableenergy,muchofwhichdeliverselectricitywhenthesunshinesorthewindblows,ratherthaninresponsetodemandfromcustomers.

Productionfromrenewables(RES)basedonsubsidies,especiallyatpeakproductionhours,hasseverelyweakenedthebusinesscaseforsuchconventionalplants,althoughtheyhaveavitalroletoplayinprovidingback-upandensuringsecurityofsupply,inparticularbecausealternativeoptionslikelarge-scalestorage,demandresponseandinterconnectioncantakelongtocometofruition.EURELECTRICstronglysupportsthedevelopmentofREStechnologies,butinsistsontheneedtodothisinacostefficient,marketorientedandEuropeanmanner,takingbenefitfromRD&Dsupportespecially.

Europe’seconomicgrowthremainsunderseriousstrain.ElectricitydemandtraditionallymirrorsGDPandindustrialoutputpatterns,andafterrecoveringin2010hasshrunkagainin2011,asshowninFigures1and2.Preliminarystatisticalinformationsuggestsafurtherdemanddecreasein2012,deterringcompaniesfrominvestinguntilapositivebusinesscaseemerges.

Yetdespitetoday’stroublingeconomicclimate,most scenarios,includingtheEuropeanCommission’sEnergyRoadmap2050,suggest that electricity demand will grow in the medium to long term.This trend will be driven by the electrification of transport, but also of the heating and cooling sector.Therefore,asecureelectricitysupplycanonlybemaintainedifnewgenerationsourcesaredevelopedtofollowthisexpectedincreaseindemand.Inaddition,theincreasingbuildofvariableRESiscompletelychangingtheloadpatternoftheelectricitysystem,whichisrequiringevenmorereservecapacitiesandmuchmoreflexibility.

1

“ „Globally, investments will be targeted to geographical areas where regulation is well-settled, predictable and reasonable from the economic point of view. Europe might be less of a priority than before for our international company.

8|PoweringInvestments:Challengesfortheliberalisedelectricitysector

2,600

2,700

2,800

2,900

3,000

3,100

3,200

201120102009200820072006200520042003200220012000

EU-27 Electricity Demand

TWh

Figure 2: Evolution of electricity demand in the EU-27 from 2000 to 2011

Source:EURELECTRIC,PowerStatistics(variouseditions)-electricitydemandincludesnetworklosses

1

85

90

95

100

105

110

115

70

80

90

100

110

120

130

05 06 07 08 09 10 11 12

Industrial new orders (lhs) Industrial production (rhs)

index, 2005=100 index, 2005 = 100

Figure 1: Industrial new orders and industrial production, EU (2005-Spring 2012)

Source:DGECFIN’sEuropeanEconomicForecastSpring2012,EuropeanCommission

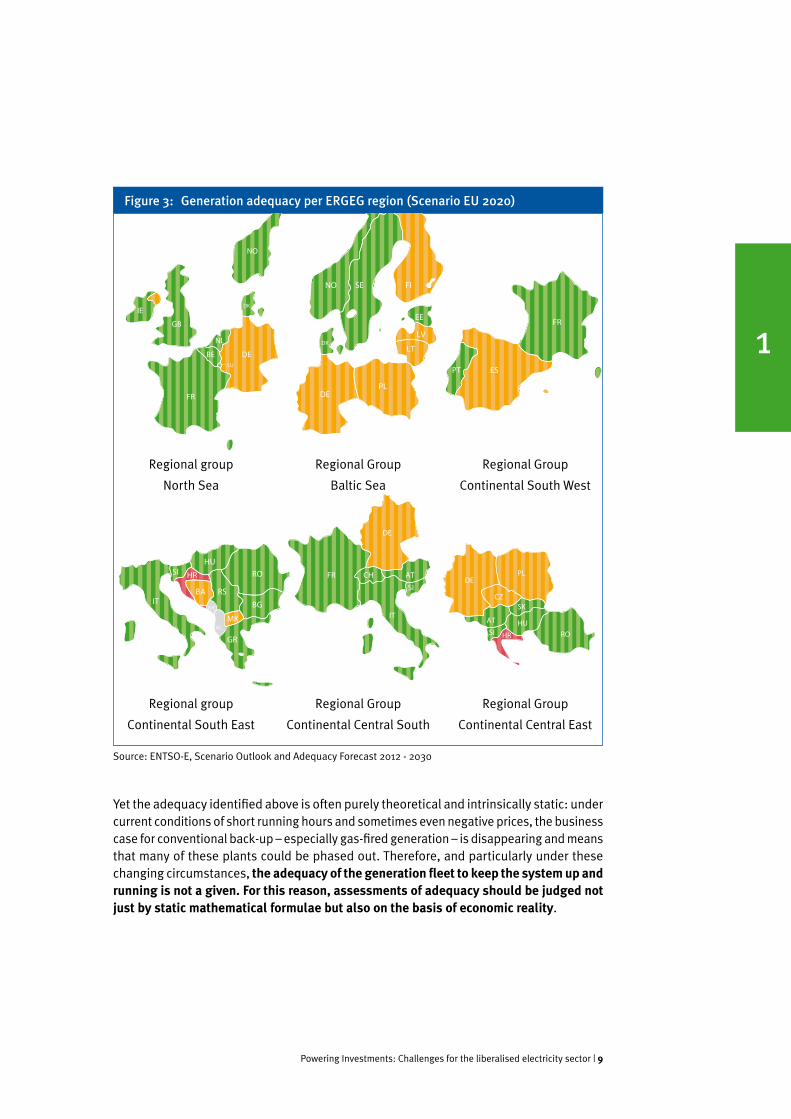

According to European generation adequacy forecasts (Figure 3), secure supply is generally ensured across the EU up to 2020.Powersystemsingreenareexpectedtohaveenoughresourcestocopewithunexpecteddemandoroutageofasystemcomponentinbothwinterandsummer.Thoseinorangehavezeroornegativemarginseitherinwinterorsummer,yetthesystemcancopewithdemandbecauseofinterconnections.Systemsinredareunabletocopewithdemandandunforeseeneventsinbothwinterandsummer.

PoweringInvestments:Challengesfortheliberalisedelectricitysector|9

Yettheadequacyidentifiedaboveisoftenpurelytheoreticalandintrinsicallystatic:undercurrentconditionsofshortrunninghoursandsometimesevennegativeprices,thebusinesscaseforconventionalback-up–especiallygas-firedgeneration–isdisappearingandmeansthatmanyoftheseplantscouldbephasedout.Therefore,andparticularlyunderthesechangingcircumstances,the adequacy of the generation fleet to keep the system up and running is not a given. For this reason, assessments of adequacy should be judged not just by static mathematical formulae but also on the basis of economic reality.

Figure 3: Generation adequacy per ERGEG region (Scenario EU 2020)

Regionalgroup

NorthSea

Regionalgroup

ContinentalSouthEast

RegionalGroup

BalticSea

RegionalGroup

ContinentalCentralSouth

RegionalGroup

ContinentalSouthWest

RegionalGroup

ContinentalCentralEast

Source:ENTSO-E,ScenarioOutlookandAdequacyForecast2012-2030

1PT ES

FR

FISENO

DK

DE

LV

LT

EE

PL

ME

AL

IT

SI

GR

MK

RSBA

BG

ROHU

HRDE

SI RO

AT

CZSK

HU

HR

PL

DE

CH

IT

SI

FR AT

NO

DK

DELU

BE

NL

IE

GB

FR

10|PoweringInvestments:Challengesfortheliberalisedelectricitysector

INVESTMENT NEEDS: FORGET ABOUT THE TRILLION, MORE REALISM WILL LEAD TO RESULTS!

2

PoweringInvestments:Challengesfortheliberalisedelectricitysector|11

A focus on what is feasible and realistic by 2020

AccordingtotheIEAaswellastheEuropeanCommission,unprecedentedinvestmentsareneededtoensureEurope’senergytransition.MajorinvestmentsareneededacrosstheentireEuropeanelectricityvaluechain,forgeneration,transmission,distributionandstorage:slightlylessthan∑1trillionupto2020,and∑3trillionupto2030.3

TheelectricityindustryiscommittedtoEurope’senergytransitionandtomeetingthe20-20-20targets.Butaskedwhethertheaboveinvestmentfigureswouldbefeasible,44outof45energyleaderssurveyedbyEURELECTRICsaidtheseinvestmentvolumeswouldnotoccur.Insteadtheyexpectedonlyabouthalfoftheseinvestmentstotakeplace,withresponsesvaryingfrom20to80%(Figure4).

Prevailing volatility in the financial markets and the unclear/unstable regulatory framework makes it quite speculative to determine how much will be invested in total even until 2020.

2

3 IEAestimatesintheWEO2012–datafromotherOECDpublications

„“

0

10

20

30

40

50

60

70

80

90

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47&)"

!"AVERAGE in RED: 51,5 % %

Figure 4: Likelihood of forecast ∑1 trillion investment to become reality according to EURELECTRIC members

Source:InternalEURELECTRICinvestmentsurvey

12|PoweringInvestments:Challengesfortheliberalisedelectricitysector

The assumptions which led to these massive figures were based on very different growth scenarios. Considering today’s economic conditions, deteriorating investment climate and uncertain regulatory/political trends, investing one trillion euros across the value chain by 2020 is simply unrealistic. We expect policymakers to take this into consideration. Rather than focusing on questionable numbers, priority should be given to delivering on Europe’s 20-20-20 objectives. Emphasis should also be put on the ‘must have’ investments that are needed to maintain security of supply at competitive end-user prices.

A look at the reality in various EU member states reveals that the situations across Europe are very different, though some general tendencies unite them.Thefollowingexamplesshedlightonthesetrends.

ManycountriesinEuropearecurrentlyexperiencingaphase-outofcapacity,raisingquestionsaboutitsreplacement.InthiscontextbothFranceandtheUKenvisageintroducingcapacityremunerationmechanisms(CRM)inordertomaintainandstimulatenewinvestments.

Inthe UKtherehavebeenrecentwarningsfromregulatorOFGEMofgenerationshortfallaround2015,whichhavebeenwidelyreportedintheUKmedia4.About12GWofcoalandoilcapacityistobeclosedby2016,asaresultofhavingoptedoutoftheLargeCombustionPlantDirective(LCPD).OntopoftheLCPD,oneshouldalsoconsidertheeffectsoftheIndustrialEmissionDirective(IED)thatwillbecomeclearerintheyearsahead.Inadditiontofossil-fuelledplantretirements,about7GWofexistingnuclearplantsarelikelytobetakenoffthegridbytheendofthedecade–thoughseveralanalystsbelievethatlifetimeextensionandlong-termoperationofsomeofthoseplantsarepossible.Beyondtheseretirements,thereisalsouncertaintyaboutpossibleclosureoffurtherplant:thecurrentlowsparkspread5forgasplantsputsthecontinuedoperationofthese,otherwiseneeded,plantsintoquestion,andseveralthermalplantsinconstructionriskbeingdelayedforthesamereasons.Forexample,intheCentralWestEuropean(CWE)6market(amarketwhichisparticularlyexposedtogaspricechanges),thecleansparkspreadiscurrentlynegative,andenergyconsultancyCERAarguesinastudyfromOctober20127that“cleansparkspreadsarelargelynotexpectedtoreturntopositiveterritoryuntilabout2018.”8Ontheotherhand,thecarbonpricefloorintroducedbytheUKTreasurywilltakeeffectasfromJanuary2013,hencefavouringgasgenerationovercoalgeneration.

InGermany,20GWofnuclearcapacityaretobephasedoutby2022andaphase-outofanadditional6.5-10GWofconventionalcapacityisexpected,principallyforreasonsofeconomicviability.TheGermanassociationBDEWassumesacapacitygapof4-8GWundertheseconditions.Theproblemisprimarilyregional,affectingmainlysouthernGermany.9

4 TheUKrisksenergyshortagesby2015-16asitssparecapacitywouldfallfrom14%todayto4%duetoearlierthanexpectedclosuresofcoal-firedpowerplants.

5 Sparkspreadsdescribethetheoreticalnetincomeofagas-firedpowerplantfromsellingaunitofelectricity,havingboughtthefuelrequiredtoproducethisunitofelectricity.Allothercosts(operationandmaintenance,capitalandotherfinancialcosts)mustbecoveredfromthesparkspread.Thecleanspreadindicatorsincludethepriceofcarbondioxideemissionallowances.

6 CWEisoneofthesevenERGEGregions.

7 CERAEuropeanPolicyDialogue2012,October2012

8 BloombergNewEnergyFinanceEuropeanLongtermGenerationOutlook17.2.2012

9 BDEW,StrategischeReserve-AbsicherungdesEnergyOnlyMarkts(StrategicReserve-securingtheEnergyonlymarket),Berlin25.9.2012

2

PoweringInvestments:Challengesfortheliberalisedelectricitysector|13

SimilartotheUK,theLCPDwillleadtotheclosureof3.6GWofcoaland4.8GWofoil-basedpowercapacitybytheendof2015in France.10

Onthecontrary,othercountriesexperienceovercapacityanddonotseeanyurgentneedtoinvest(fortechnologiesotherthanRESwhichneedtogrowpursuanttotheRESDirective).

In Italy,gas-firedgenerationalonereachedatotalinstalledcapacityof54GWattheendof2011.Inthesameyear,theregisteredpeakloadstoodat56.5GWwhiletheminimumloadwas21.5GW.11

InSpain,combinedcyclegasturbines(CCGTs)haveboomedinthelastdecade,goingfromnoCCGTsin2000to28GWofCCGTsin2010,whichisabovetheminimumloadofabout21GW.Alongwiththeboomofgas-firedgeneration,thecountryhasseenamassiveincreaseinrenewables–mainlywind,whichreached20GWattheendof2010–andhasanuclearfleetof7.5GWandacoalfleetof11GW.Inthesameyear,thepeakloadstoodat45GW.

InAustria,attheendof20114.3GWofgas-firedplantsand5.4GWofconventional(i.e.nonpumpedstorage)hydroplantswereinoperation.Thesameyear,thepeakloadwas9.7GW,i.e.equivalenttotheinstalledcapacityofconventionalhydroandgas-firedplantsjustmentioned.Inaddition,thecountryhad1.5GWofrenewables(mainlywind),1GWofcoal-firedplantsand7.5GWofpumpedandmixedhydropowerplants.

InSwedenthereisatpresentanoverinvestmentinrenewablescomparedtothetargets.Thishascausedapricedropforgreencertificates.Thisisofcoursewhatshouldhappenwithanoversupplyinamarket-basedsystem.Inthelongrunupto2020thesystemisexpectedtodelivertherightamountofrenewablesatacostontheconsumer’sbillataround0.6to0.9c∑/kWh.Profitablecapacityincreasesandhigherefficiencyinthenuclearpowerplantsisforecasttoresultinanincreaseofaround1,000MW.

Overall, we conclude that there is an urgent need to fix the above mentioned generation adequacy issues in some regions.Connectingoversuppliedtoinsufficientlysuppliedregionswouldbeintunewiththesinglemarket,illustratingalsotheinter-linkagesbetweentransmissionandgenerationinvestments.Consideringthehugedelaysinsettingupnewinterconnections,however,thereisamoreimmediateneedtomaintainthesysteminbalance.WhileEURELECTRICbelievesthateliminatingdistortionsinordertorestorethemarketisthebestsolution,itacknowledgesthattheremightbeapragmaticneedforinterimsolutionslikestrategicreservesorCRM. 12

10BloombergNewEnergyFinance,17.2.2012

11 DatainTerna’sstatisticalyearbook

12 EURELECTRIC,Renewables Integration and Market Design: are Capacity Remuneration Mechanisms needed to ensure generation adequacy?,May2011

2

14|PoweringInvestments:Challengesfortheliberalisedelectricitysector

A TROUBLED INVESTMENT CLIMATE 3

PoweringInvestments:Challengesfortheliberalisedelectricitysector|15

Financing and regulation are two sides of the same coin

InvestinginEurope’slong-termpowerfutureisaparticularchallengetoday.Therecessionhasnotonlyhitutilities,butalsotheirfinancingpartners.Atightenedfinancialframework,aswithBaselIII,aswellasinsufficientprofitmarginsplacefinancingpartnersunderseriousscrutinywithrespecttotheirfutureinvestments.Althoughnewinvestorssuchaspensionfundsandcommunalenterpriseshaveemerged,theyareaffectedbythesamechallengesastraditionalinvestors.

EURELECTRICmembersgenerallyassesstheinvestmentclimateasbeingverypoor.EURELECTRIC’sinternalinvestmentclimatesurveyidentifiesvolatilepoliciesasthemainreason.

A vicious circle of volatile regulation – decreased attractiveness of utilities – deterred investment is the result.

Otherelementsfuellingthecurrentpoorinvestmentclimateinclude:

• Thesovereigndebtcrisisandresultinghighercapitalcosts/interestrates,

• Powerpriceswhicharenotdeliveringmeaningfulsignals,

• Deteriorationinanalysts’ratingoftheindustryandreducedindustryattractiveness,

• Increaseddebtburdenfinancingforutilities,

• Variousad-hoctaxesonutilities.

However, regional or national trends are often more nuanced.Someregions,forinstancetheNordicone,seemlessexposedtoinvestmentdifficultiesthanothers,atleastuntil2020.Agreaterregionalapproach,thestructureofthegenerationportfolio,andmoreconsistentpoliciescanlargelyexplainthenational/regionaldifferences.Thelendingconditionsalsoplayarole:thesovereigndebtcrisisinsomememberstateshastranslatedintostricterandcostlierlendingconditionsandhasforcedseveralcompaniestoadoptdivestmentprogrammestomaintaintheircreditratings.

Figure 5: The vicious circle at work

3

Deterredinvestment

Volatileregulation

Lowattractiveness

of utilities

16|PoweringInvestments:Challengesfortheliberalisedelectricitysector

Making Europe’s global competitiveness a priority

Moneycanbespentonlyonce.Intimesofeconomicdownturn,capitalrationingmakestheprioritisationofallocationevenmorecrucial.TheEuropeanelectricityindustrystressestheneedtokeepEurope’scompetitivenessinmindbyprioritisingeconomicefficiencyasakeyprincipleofthelow-carbontransition.Inessence,thisnecessitatesalessnational,moreEuropeanapproachandagreaterrelianceonmarketsandmarket-basedprinciplestoavoidstrandedsubsidiesandstrandedinvestments.

Europe’scompetitivenessmeansfocusingontheEuropean energy industry’s strategic place in the emerging global low-carbon economy.Awell-developedinnovationpolicytargetedatalltheelementsoftheenergyvaluechainisneeded.Suchapragmaticrefocusinghasthepotentialtoresultininnovative,cutting-edgeproductsthatcanalsobeexportedtotherestoftheworld.

WecannotaffordtoforgetaboutEurope’scompetitivenessatlarge.Wearewitnessing,amongalmostallEuropeanmemberstates,asurgeofinterventionistanddiscretionarymeasuresinthepowersectorwhicharestronglyaffectingitsprofitability.Examplesofthistroubledinvestmentclimatearelistedinthefollowingsection.

Volatile regulation pursuing conflicting objectives

TheEuropeanutilitysectorisusedtothemanifoldrisksthatareinherentinthesector’slonginvestmentcycles.Buttherisksfacinginvestorstodayoftenexceedacceptablelimits.UncoordinatedEUlegislation(e.g.nointerrelationbetweentheEUEmissionsTradingScheme(EUETS)andtherenewablestargets)andvolatilenationalpolicies(e.g.abruptandsometimesretroactivechanges)createuncertaintyandunderminetheviabilityofconventionalgeneration.Riskaversenessisontherise.Itisexacerbatedbypolicieswhichsubsidisecherry-pickedtechnologies.Theseattractrisk-averseinvestorsanddepressinvestmentsinprojectsexposedtotheliberalisedmarketenvironment.

If the EU and EU member states fail to establish sustainable market frameworks for low-carbon electricity, then we are heading for a crash.

3

“ „

PoweringInvestments:Challengesfortheliberalisedelectricitysector|17

Regulatory risk is on the rise

AftermorethanadecadeinwhichenergymarketliberalisationwasthecornerstoneoftheEU’senergypolicy,new–andindeedlegitimate–prioritieslikeemissionsreductionnowrequire thatanewbalancebestruckbetweenmarketforcesandgovernmentintervention.Butinsteadofproperlyaddressingthisissueinallitscomplexity,itseemsthat,inablackandwhitemove,thependulumisswingingbackfromcompetitiontoregulation.Evidencefromthepastshowsthatafullyregulatedpowersectorhasledtooversuppliesandcostinefficiencies.EvenbeforeliberalisationandtheinternalenergymarkethavebeenfullycompletedinEurope(e.g.3rdPackageimplementation,“targetmodel”)andconclusionshavebeenreachedastotheirsuccess,governmentsareshowingaworryingtendencytore-regulatetheenergysystems.

TheEuropeanpowersectorhasmadeclearthatitcandelivercarbon-neutralelectricityby2050.AfterthesuccessfuldecreaseinSO2andNOxinthe1990s,thereductionofCO2emissionsisthenextchallenge.ButEURELECTRIChasalwaysmadeclearthatpolicyfordecarbonisationshouldbesetinsuchawaythatcompetitionandtheintegrationofEuropeanenergymarketsdonotbecomecollateralvictims.Intheelectricitysector,whichissoimportanttosocietyasawhole,extremeapproacheslikeamarketwithoutregulationorregulationwithoutamarketarebothinappropriate:the right balance must be struck between reasonable regulation setting transparent frameworks and the efficiency of the market.

Unfortunatelytheenergyindustryiscurrentlywitnessingaracefornewregulation,eventhoughpreviousregulationsuchasthesecondandthirdElectricityDirectiveshasnotyetbeenimplementedinsomecountries.WeobservegrowinginconsistencyoflegislationatEUlevelandalsoamongmemberstates.Thereisaseriousconcernthatthiswillleadtolossofmarketefficiency,tore-regulationandtomorecommand-and-control.Theseinturnwillaffectcostefficiency,increasethecostburdenforEuropeancitizensandindustrialend-users,andendangermeetingeitheroftheenvisagedobjectives,beitliberalisationordecarbonisation.

Markets tend to be less markets due to increased regulatory interventions.

0

20

40

60

80

100

120

140

160

180

Regulatory riskLiquidity riskCredit riskMarket risk

Sum of points attributed by participants

Figure 6: Assessment of different types of risk13

13 Eachsurveyparticipantwasaskedtorateeachriskbyattributingthempointsfrom1to4,fourbeingthehighestrisk.

Source:InternalEURELECTRICinvestmentsurvey

3

“ „

18|PoweringInvestments:Challengesfortheliberalisedelectricitysector

Figure7exemplifiesthisproblem.ItshowsthefragmentedanddivergingcapacityremunerationmechanismsacrossEurope,highlightingtheinconsistenciesamongmemberstates.

BothEuropeanandnationalpolicymakerstendtointerveneinasomewhatstop-and-gofashion,completelydisregardingthelong-termneedforclear,effective,consistentandsupportiveframeworksthatareconducivetoinvestments.Rather than focusing on creating a level playing field by removing market interventions that have outlived their usefulness, new distortions are added on top of existing ones.

Wearealsowitnessingafairlyblackandwhitediscussionon‘centralisedversusdecentralised’powergeneration.Infact,bothtypesareneeded,dependingonlocation.Thesinglingoutofadecentralisedgenerationonlyapproachseemslikeareturntothepastwhenelectricitygenerationandsupplywerealocalaffair–untilitwasfoundthateconomiesofscalewouldloweroverallcosts.AmongEuropeanregionsthereappearstobeatrendofsetting“energyindependence/autonomy”objectives,inthebeliefthatregionscanbecomeenergyautonomous,attachinglittlevaluetothelevelofinter-connectioninEurope.Toconclude:decentralisedsolutionswillhavetheirplaceinthesmartandcompetitivelow-carbonenvironment,buttheywillnotbetheone-size-fits-allsolution.

Market intervention through taxesfurtherinterfereswiththedevelopmentoftheinternalenergymarketandhampersinvestmentsinexistingandnewpowerplants.Table1liststhelatestspecifictaxesontheelectricitysectorinEUmemberstates.

BE: tendering for new gas plants proposed + additional rules for grid stability reserves

DE: no decision on capacity mechanisms before 2015. Grid stability reserves in southern DE since 2011

ES: capacity payments for new units and to existing coal, gas, oil and hydro capacity. In 2012 proposals to stop/reduce payments

GB: developing full-scale capacity auctions, legislation to be ready in 2013

IT: minor payments. New capacity market mechanism to be implemented by 2017

SE&FI: capacity reserves for spot market deficits only. SE reserves to be gradually pased out by 2020

RU: capacity market with price restrictions. Long-term capacity supply agreements for obligatory investments

EE: household market opening January 2013

IE&NI: capacity payments since 2005

FR: capacity purchase obligations planned to be implemented by 2016, but new government could change the NOME law

PT: same as Spain for new units. Payments reduced in 2012

LT: condensing units as reserve

PL: nodal pricing and capacity market discussed, but no final decisions

GR: capacity obligation mechanism since 2005

Figure 7: Overview of capacity remuneration mechanisms across Europe

Source:EURELECTRIC

3

Energy only market *)

Partial capacity mechanisms

Proposals for new capacity elements

Major capacity mechanisms

Regulated market restriction

*)Nocapacitypaymentstopowerplantsintheday-aheadandintradaymarket,butbalancingmarketreservecapacityiscontractedinadvance

PoweringInvestments:Challengesfortheliberalisedelectricitysector|19

Table 1: Overview of some recent tax developments in Europe in the electricity sector

Belgium • Nucleartax(2008-09)-∑250million–increasedto∑550millionasof01.01.2012 (split among the nuclear producers on the basis of theirrespectiveproduction)

• Federalenergycontribution(1.9088∑/MWh).Federallevytofinancepublicserviceobligationsandthefederalregulators’budget(5.0854∑/MWhin2012)

• Taxoncoal:11.6526∑/ton/Taxonnaturalgasusedforpowergeneration:0.7399∑/MWh

• Measurestakentoreregulateretailprices

Czech Republic • Windfall profits arising from free CO2 allocations have been taxed bymeansofa“gifttax”payableduring2011and2012

Finland • The real estate tax on power plants has been increased from 1.4% to2.85%between2006and2012.

• Furthermore, the government plans to introduce a tax for old nuclearandhydrogenerationtocollect∑170millionperannumfrom2014(i.e.approximately∑5MWh)

France • Inlandwaterwaystax:taxationrateraisedfrom4.6∑/dam3to5.7∑/dam3

• Annualoutstandingtax(0.052%ofcompanies2011turnover)tofinanceCO2 allowances granted by the State to new industrial plants enteringtheEUETSin2011(i.e.coveringmorethan60,000tonsofnationalCO2allocationplanfor2008-2012)

Germany • Doubtaboutconstitutionalityofnuclearfuelrodtaxintroducedin2011–Tolastuntil2016

Hungary • Newenergynetsalestax(2010andintroducedfor3years)–1.05%

• “RobinHood”taxintroducedin2008–maintaineduntilend2012

Italy • Robin Hood surtax was increased from 6.5% to 10.5% for 2011-2013 +broadeningofscopeincludingT&Dofpowerandnaturalgas

Norway • Municipalpropertytaxforhydropowerplants(e.g.rateof0.7%basedupona calculated market value). Maximum value for calculated market valueincreased by 5% in 2012 and will increase by 11% as of 2013. Expectedincreaseofthetaxby15million∑in2012and40million∑in2013

Portugal • On1October2011,VATrateapplicabletoconsumptionofgasandelectric-ityincreasedfrom6%to23%

The investment capabilities in the energy industry have decreased, partly because of the economic recession but also due to numerous fees, charges and taxes that have been introduced.

3

“ „

20|PoweringInvestments:Challengesfortheliberalisedelectricitysector

Spain • Newtaxesonenergygenerationtoreducethecountry’selectricitytariffdeficit–aimtoraise2.74M∑/y:–6%taxonthesaleofelectricityfromallgenerationtypes–Taxondisposalofradioactivewaste+taxonhydropower–“Greencent”levyonfuels:2.79∑/m3ofnaturalgas,14.97∑/tonof

coal,12∑/tonoffueloil,29.15∑/1000litersofgasoil.

Sweden • Nucleartax:taxbasedonthethermalproductioncapacityofthenuclearreactor(1,200∑/MWh)

• Realestateonhydropowerplantsincreasedfrom0.5%to2.8%between2006and2011

United-Kingdom • ClimateChangeLevy(CCL)rateswillincreasefrom01.04.2013inlinewithinflation

• NewCarbonPriceSupporttobeintroducedfrom2013:suppliesoffossilfuels used in most forms of electricity generation (which are currentlyexempt)willbecomeliabletotheCCLorfueldutyfromthatdate.

Supportersofthesetaxesoftenclaimthattheyaremorethanjustifiedsinceelectricitypricesare‘high’.Buthigh prices for customers do not equal high profits for companies. Consumersshouldbemadeawarethattheenergycomponentoftheirbillisusuallybelow50%ofthetotalbillandonaverage43%–ascanbeseen(inblue)inFigure8below.ItneedstoberecalledtoothatinseveralEuropeancountriesthelevieslinkedtothesupportofrenewableenergiesareincorporatedintothegridfees–labelledas‘distribution’inthefigure.

0

10

20

30

40

50

60

70

80

90

100

Denmark

France

Portu

gal

German

yBelg

iumSw

eden

Spain

Netherl

ands

Finlan

dLux

embo

urgAust

riaIre

land

(Rep o

f)Gree

ce Italy

Great B

ritain

Avera

ge

VAT Energy taxes Distribution Energy

Figure 8: Breakdown of residential end-user electricity price (2011)

Source:EnergieControlAustria2012

3

Source:EURELECTRIC

PoweringInvestments:Challengesfortheliberalisedelectricitysector|21

Whilethenon-energycomponentsofbillshavebeenincreasingconstantlysincethe1990s,theelectricity(i.e.commodity)priceitselfhasremainedratherstable.

Figure9showsthedevelopmentofGermanpowerpricessince1998,thebeginningofliberalisation,andthehugeincreaseoftaxesandsupportmechanisms(+169%).Notethatgenerationanddistributioncostshaveonlyincreasedby5%.

Today the European electricity sector is facing difficulties. It is increasingly beingoutperformedbyothersectorsonthestockmarket(Figures10and11)andbytheutilitiesonothercontinents(Figure12).

60

70

80

90

100

110

120

31/10/1228/09/1231/08/1231/07/1229/06/1231/05/1230/04/1230/03/1229/02/1231/01/1231/12/1130/11/1131/10/11

EURO STOXX50 Index EURO STOXX Utilities INDEX

Generation, transport and retail Value added tax Concession levy

Combined heat and power act German renewables energy act

Electricity tax (eco-tax)

Increase (1998 = 100%)

+5%

+169%

+46%

37.6 33.8 25.2 25.1 28.3 29.8 31.6 32.7 34.3 35.6 38.0 41.2 40.5 39.6

6.9 5.2

6.7 5.2 2.3

5.6 5.2 3.7

5.8 5.2 4.5

6.5 5.2 5.2

6.9 5.2 1.2 6.0

7.2 5.2 1.5 6.0

7.5 5.2 2.0 6.0

7.8 5.2 2.6 6.0

9.6 5.2 3.0 6.0

10.1 5.2 3.4 6.0

10.8 5.2 3.8 6.0

11.0 5.2 6.0 6.0

11.6

5.2 10.3 6.0

50.0 48.2 40.7 41.8

47.0 50.1 52.4 54.4 56.8 60.2 63.2

67.7 69.1 72.8

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Consumer price index2): +21%Light fuel oil3): +236%(1998 = 100%)

1) Extrapolation 2011; power consumption of 3.500 KWh/a; Source: bdew2) According to Statistisches Bundesamt Deutschland; Monthly values: February 2011 vs. February 19983) According to Statistisches Bundesamt Deutschland; Monthly values: February 2011 vs. February 1998; Delivery fuel tank track, 40-50hl each delivery, free consumer site

Figure 10: European utilities (EURO STOXX Utilities) are underperforming the European Blue-chip index (EURO STOXX 50)

Figure 9: Average electricity bill of a three-person household per month (in ∑)

Source:STOXXLimited,retrieved5November2012

Source:BDEW

3

22|PoweringInvestments:Challengesfortheliberalisedelectricitysector

3

To conclude:Europeanelectricityutilitiesarefullyexposedtopolicymakers’lackofconsistentmethodologyinpursuingthethreeenergypolicyobjectivesofsecurityofsupply,sustainabilityandcompetitiveness.Weagreewiththe‘what’,i.e.theobjectives,butstronglydisagreewiththe‘how’.Howcoherentlyaresecurityofsupply,environmentalobjectivesandcostefficiencyarticulated?Howdothoseobjectives–andtherespectivepolicyinstruments–relatetooneanother?NationalandEuropeanpoliciesonclimate,energyandenvironmentareinsufficientlyalignedandtheyhaveperverseeffectsoneachother,withtheriskofunintendedconsequences.

Public policy and regulation should be aligned with the time horizons of the electricity sector, which recovers its investments in terms of decades, not years. Visibility on long-term trends and regulation as well as policy consistency are therefore crucial. Unfortunately they are currently missing.

90

80

70

60

100

110

120

130

31/10/11 30/11/11 31/12/11 31/01/12 29/02/12 31/03/12 30/04/12 31/05/12 31/06/12 31/07/12 31/08/12 31/09/12 31/10/12

EURO STOXX Utilities Index

STOXX Asia 1200 Utilities Index

STOXX USA 900 Utilities Index

Figure 12: European utilities (EURO STOXX Utilities) are underperforming the US (STOXX USA 900 Utilities) and Asian (STOXX Asia 1200 Utilities) utilities’ indexes

Source:STOXXLimited,retrieved5November2012

Figure 11: Variation rate of sector indexes in 2012

Source:Ownelaboration,datafromSTOXXLimitedretrievedon4October2012

0%

-5%

5%

10%

15%

20%

25%

Oil&Gas

Util

Cns&M

at

Retai

l Te

ch

Mar

ket

Banks

Hea

Car

e M

edia

Fin

Svc

s In

dus Gd

Pr&Ho G

d Aut&

Prt Rea

l est

ate

Fd&Bvr

In

sur

Trv&

Lsr

Chem

Bas R

es

Te

leco

m

PoweringInvestments:Challengesfortheliberalisedelectricitysector|23

AN EMPOWERING INVESTMENT FRAMEWORK ... should aim at de-risking investments

Inaliberalisedmarketenvironment,Europeanenergycompaniesareusedtobeingexposedtorisksandhavedevelopedstrategiestohedgesuchrisks.Butregulatoryriskscannotbehedgedandrisksmustgenerallyremainproportionate.Intoday’senergypolicymaking,short-termconsiderationsoftenprevailoverthelong-termstrategy.Attemptsatenforcingad-hoctaxesand/orinterveninginpriceformationinthemarket(e.g.throughpricefreezes,wholesalepricecaps,retailpriceregulation)reducetheattractivenessoftheenergysectorasanareaofinvestment.Utilitiesandtheirinvestorsarebeingchallenged.Yetsocietyexpectsthemtopavethewayandfinancethetransitiontoalow-carboneconomy.

Tomakethishappen,policymakersmustturntheviciouscirclecurrentlyatplayintothevirtuouscircleshowninFigure13below:policyandregulatorystabilitywillboostinvestmentswhichwillinturnmaketheenergytransitionareality.

Anenablingandpredictableinvestmentclimatewouldattractfinancingfrombothutilitiesandnewfinancialactorssuchaspensionfunds,privateequityfirmsandinsurancecompanies.Althoughenergycompanieshavehighgearinglevelsandarefacingthechallengeofmaintainingtheircreditratings,there is a converging view that the sector would be able to raise the necessary funds – in conjunction with the new financial actors described above – if a sound framework was set.

TheexperienceintheNordicregion,withitslongtraditionofacommonwholesalemarket(theNordPool),showsthatastableandpredictableframeworkcanspurinvestmentandcanattractinnovativefinancingmodels.OtherexamplesincludeajointsupportschemebetweenSwedenandNorwaytosupportrenewables,theinvolvementofendcustomersandelectricityretailersinfinancinggenerationinvestment,andtheinvolvementofdifferentventurecapitalfundsinjoint-ventures(wherebyfundsacquireminoritystakesinprojectsbeingdevelopedbyutilitycompanies).

RECOMMENDATIONS

REC

OM

MEN

DAT

ION

S

24|PoweringInvestments:Challengesfortheliberalisedelectricitysector

... should be built on the following principles:

• Competitiveness:MaintainthecompetitivenessoftheEuropeanenergysector,andthusoftheEUatlarge.

• Innovative governance:governmentsshouldfindinnovativemethodsofadequatelypursuingmultipleobjectives:the‘targetsforeverything’approachisoutdatedandunsuited,andshouldbereplaced.

• Predictability and coordination:Developalong-termEuropeanenergypolicy,not27divergingnational,incompatiblepolicies.

• Cost-efficiency:Relyonmarketdynamicsandputmoreemphasisoncost-efficiency,evenmoresointimesofrecession.

• Transparency:Betransparentonsocietalcosts,decision-makingandscenarios/outlooks.

• Innovation:Elaborateaninnovationstrategyforenergy.

... and on the following recommendations:

1. Stop discretionary measures

WecallontheCommissiontopublish,aspartofitsannualMarketObservatoryforEnergy,thelistofdiscretionarymeasurestakenbyregionalorgovernmentauthorities(introductionofdistortionsinmarketmechanisms;discretionarytaxation;retroactivechangestosupportschemes)whichareheavilyimpactingthesectorandwhichcallintoquestiontheachievementofEUenergypolicyobjectives.OnlyEUactiononsuchrandomregulatoryinterventionwillbeabletomaintainadecentinvestmentclimateinthesectorandwillavoidthatriskpremiumsforenergyprojectsskyrocket.Discretionarymeasuresmustbestopped.TheElectricityCoordinationGroup–setupbytheEuropeanCommission–shouldbetransformedfromamerediscussionplatformtoatrulyEUcoordinationbodywhichassiststheEuropeanCommissioninremovingtheinconsistenciesofnationalpolicymeasuresandensuringthatEuropeanenergypolicyisappliedontheground.

REC

OM

MEN

DAT

ION

S

Figure 13: The virtuous circle at work

well timedand

designedEnergy

transition

Policy andregulatory

stability

Investments

Competiti-veness

Transparency

Cost-e�ciency Innovation

InnovativegovernancePredictability

andcoordination

PoweringInvestments:Challengesfortheliberalisedelectricitysector|25

2. Do not micro-manage the energy sector with multiple, conflicting policy instruments and targets

Despitemarketliberalisationbeingthecornerstoneofitsenergypolicy,theEUisindangerofembarkingonacommand-and-controlapproachtoenergypolicy,ofmicro-managinginsteadofprovidingabroadframeworkbasedoneffectivepricesignals.Thissendsconfusingsignalstoinvestors.Policymakersmightbetemptedtosettargetsforeachandeverything14,butEURELECTRICbelievesthattheyshouldsticktotheirtask:agreeonadirection,andletthemarketdeliverwithinthisgeneralpolicyframework.15Ad-hocregulationandover-regulationshouldbeavoided.

The holistic approachwearecallingforshouldreflecttheneedsoftheelectricitysystemasawholeinsteadofaddinglayersofregulationandaccumulatingdistortionssuchastechnology-specificincentivesfore.g.RES,gasorstorage.Partialsolutionsandsingle-issueinstrumentsshouldbereplacedbyanintegratedapproach,wherepolicymakersdonotlosesightoftheelectricitysystemasawhole.GiventheenvisagedlevelsofpenetrationofvariableRESgeneration,allsourcesofflexibilitywillbeneededtoshapethefuturepowersystem(marketintegration,demandsideparticipation,flexibleback-up,storage,smartergrids).Inparticular,thedevelopmentofgenerationmustbeaccompaniedbytheappropriatedevelopmentofthegrid:increasedtransmissioncapacityandreinforcedandsmarterdistributiongridswillbeneededtosupporttheenergytransitionandcomplementtheefforttobalancetheelectricitysystem.

Moreover,allgeneratorsmustcontributetosystemstabilityonalevel playing field,bybetterforecastingtheiroutput,becomingresponsiblebalancingpartiesandprovidingancillaryserviceswhereappropriate.16

3. Be serious about the completion of a well-functioning and integrated energy market

The27EUmemberstatesshouldfullyandrapidlyimplementtheThirdPackageandthecorrespondingcommonmarketrules.FunctioningmarketmechanismsneedtogohandinhandwithEuropeangridplanningthatwillincreasetheinterconnectivityofcurrentlyfragmentednationalmarkets.Marketintegrationtoolssuchasmarketcoupling,cross-borderintra-daymarketsandcross-borderbalancing(i.e.theso-called“targetmodel”)areindispensableinensuringandfacilitatingthecontribution(onacompetitivebasis)ofallavailableflexiblesources.

Weneedalevelplayingfieldforalltechnologies,withinthesetmarketframework.Amarket-compatibleandEuropeanapproachtoRESdevelopmentshouldbedesignedforthesakeofeconomiesofscaleandsystemstability.Aspartofthis,considerationshouldbegiventoextendingthecurrentscopeoftheERGEGRegionalInitiativestocoveralsoregionalcooperationinrenewablesdevelopment.Feed-in

REC

OM

MEN

DAT

ION

S

14 Themostvisiblerecentexamplewastheidea,voicedbyEnergyCommissionerGüntherOettingeron21June2012,toset7-daystorageobligationsforpowerproducers,revealinga“centralplanningapproach”topolicymakinginsteadofanoverallincentivisingframework.

15 ThisviewisnotheldbyEURELECTRICalone.AstheRoadmap2050’sAdvisoryGroupputitintheirreporttotheEuropeanCommissionofDecember2011:“adistinctionshouldbemadebetweensettingthepolicyframeworkanddetailedinterventioninspecificmarkets.”

16 Cf.EURELECTRIC2010 Integrating intermittent RES into the EU Electricity System by 2020. EURELECTRIC position paper.

26|PoweringInvestments:Challengesfortheliberalisedelectricitysector

tariffs(FIT)aretheleastcompatiblewiththemarketinthattheyprolongRESsupportirrespectiveofthemarketreality.Thus,therenewedsubscriptiontostaticFITafter2020wouldnotaddressthecoreissueofensuringthecost-efficient,smoothandviabledevelopmentofRESwithintheEuropeanenergymarkets.

EURELECTRICpreferstheleastdistortiveformofsupport,i.e.R&Dsupportforimmaturetechnologies,andbelievesthatmarket-compatiblemechanismsarealwayspreferable.SupportschemesmustbedynamicandfulfilcommoncriteriathatarecompatibleacrosstheEU,therebyensuringthattheydonotdisruptthecompletionoftheinternalenergymarket.Irrespectiveofsupporttype–R&Dordirect–alltechnologiesmustmeetthesamerequirementsonbalancing,nominationandscheduling,andgridconnections.

Capacityremunerationmechanisms(CRMs)areincreasinglycommoninEurope.Yettheydonot,inthemselves,constitutethesilverbullettofixingallweaknessesofthecurrentmarketdesign.Instead,weshoulddealwiththerootcauseofthecurrentweakpricesignalsandremovemarketdistortionssuchasregulatedprices,whole-salepricecapsintheenergy-onlymarketorprohibitionsonclosingdownnon-viableplants.

EURELECTRICacknowledgesthatspecificinitiativestoadditionallyremunerateconventionalback-upandreservecapacitymightbeappropriateinsomememberstatestoensuresecurityofsupply.Yetweareconcernedthatthecurrentdivergingnationaldecisionsandproposalswillhindermarket integrationandleadtocompetitivedistortionsbetweenelectricitygeneratorsthatareactiveinthesameinterconnectedregionalmarket.Inordertoavoidthisnegativeimpact,weurgetheCommissiontoelaborateguidelinesanddeterminecriteriatoberespectedinordertobetterstreamlineandcoordinatethedifferentnationalpolicies.

4. Develop a European energy policy which reconciles national policies and cares about consistency: improve the Lisbon Treaty’s Article 194

We need a European-wide coordinated energy policy.

EuropeanenergypolicyneedstobetrulyEuropean.TooperateinanintegratedEuropeanenvironment,energycompaniesneedthereassurancethattheEU’senergypolicyiscompatiblewithnationalpolicies.IftheEUembarksonaTreatyrevisioninthenextyears,asEuropeanCommissionPresidentJoséManuelBarrosoannounced,17memberstatesshouldseizethisopportunitytoclarifythelegalbasisthatgovernsEurope’senergypolicy(Art.194oftheLisbonTreaty:withthisarticleenergypolicyhasbecomeforthefirsttimeinhistorypartofthelegalframeworkoftheEU).Inparticular,thecoordinationofEuropeanenergypolicyandtherequirementthatnationalenergypoliciesmustbecompatiblewiththeEuropeaninternalenergymarket,whichisduetobecompletedby2014,shouldbemadeclearer.

REC

OM

MEN

DAT

ION

S

17 JoseManuelBarroso,StateoftheUnionaddress,12September2012(EuropeanParliament,Strasbourg)

“ „

PoweringInvestments:Challengesfortheliberalisedelectricitysector|27

5. The EU needs to integrate its different policies into one coherent structure

TheEUEmissionsTradingSchemeshouldbethekeydrivertobringtheEUpowersectortowardscarbon-neutrality,drivingthedevelopmentofenergyefficiencyandlow-carboninvestments.Lookingbeyond2020,theEUshouldadoptassoonaspossibleeconomy-widegreenhousegasreductiontargetsfor2030andbeyond,upto2050.18Inthemeantime,memberstatesshouldcooperatemoreinordertomeetthe20-20-20targetscost-effectively–forexampleusingthecooperationmechanismsoftheRenewablesDirective.

6. Use innovation as a catalyst

Innovationinthepowersectorisattheveryheartofthetransitionthatwillleadustoacarbon-neutralelectricitysystem,thebackboneofadecarbonisedeconomy.TheworldisapproachingatippingpointinthedevelopmentofenergytechnologiesthatcouldincreaseproductivityonascalenotseensincetheIndustrialRevolution.

Europeneedstodevelopacompellingperspectiveonhowitcansuccessfullycopewithinnovationinthepowersector,leveragebestpractice,andtranslateitintomoreEuropeancompetitiveness.Governmentshaveacrucialroleinsupportingthewholeinnovationchainthroughpoliciesandlegislation.Butrecentyearshaveseenamassiveproliferationofaction,platforms,communitiesandR&Dinfrastructuresthathavenotgeneratedtheexpectedlevelofsuccess,probablybecauseexistingEUprogrammesappearlargelyfragmented,uncoordinatedandbureaucratic,causingindustryparticipationtodecline,evenbeyondtheeffectsoftheeconomiccrisis.Europewillagainmissitsgoalofspending3%ofGDPonR&D,andtheEUprojectionsupto2050showthattheEU-27globalshareofpatentswillfallto20%,althoughEuropeistheworld’slargestmarket.

Thetransitiontoalow-carbonenergysystemrequiresthelarge-scaledeploymentofinnovativetechnologies,betheynewtechnologiesorimprovementstoexistingones(e.g.moreefficientandmoreflexiblethermalplants,moreefficienthydroandpumpedstorageplants,innovativestorageoptionsincludingpower-to-gasandnewbatteries).Sustainabletechnologyinnovationisafundamentaldriverofcompetitiveness,jobcreationandlong-termeconomicgrowth.InvestmentsmustbestreamlinedbetweenmemberstatesandatanEUlevelsothatEuropecanreapthebenefitsofanEU-wideinnovationpolicy.Thepotentialofspendingoninnovationremainsuntapped.

EURELECTRIC,whosemembersareengagedinaninnovationactionplanthataddressesthequestionofhowtheEUinnovationpolicyshoulddeliver,invitestheEuropeanCommissiontojoinitseffortsandtoreflectonensuringthatenergyinnovationbecomesadriverforcompetitiveness,jobsandlong-termsustainablegrowth.

REC

OM

MEN

DAT

ION

S

18ThePolishmemberofEURELECTRICdisagreeswiththisposition

28|PoweringInvestments:Challengesfortheliberalisedelectricitysector

7. Timing matters! Choose the right speed

Policymakersshouldsticktothe20/20/20objectives,useinnovationasacatalyst,anddevelopatransitionnarrativeto2020andbeyondwhichoutlinesarealistic–andthusvisionary–pathwaytodeliverthetransition.

Therealchallengeoftheenergytransitionliesinfindingtheequilibriumbetweentheabilitytopay(thecost),thematurityandlimitsofthetechnologydevelopment,andtheoptimaltiming.Findingtherighttimingforthisambitiousprocess(andrefrainingfromjumpingtooquicklyintodisruptivechanges)iskeytosuccess.Forinstance,itisimpossibleforoffshorewindpowertoovercomeallobstacles(includingtechnologychallenges)withinashorttimeframe:whilethesupplychainforwindoffshoreisbeingputinplaceandinvestmentshavestarted,gridconnectionislaggingbehind.Butlikewise,itwouldhavebeenimpossibleformanufacturerstomovefromthefirstmobilephonesofthe1990stotoday’sadvancedsmartphonesovernight.Ifhowevertechnologicaldevelopmenttakesplacebasedonpoliticaldecisions,onemustacceptsuboptimaltechnologyoutcomes,highercosts,orevenfailure.Thus,thebestinteractionbetweencost,technologydevelopmentandtimingisnotnecessarilytheonewiththehighestspeed.

Inaddition,energypolicyandinvestmentsinpowergenerationarecharacterisedbylongleadtimesandlong-timehorizons.ForexampleittookFrancemorethantwentyyearstofundamentallyreplaceitsgeneratingfleetfollowingtheoilshocks.Thereisanincreasingconcerntodaythatwearebeingoverlyhastyandthereisthusaneedtodiscusstheappropriatetiming.Theenergytransitionwillnothappenovernight;forinstanceitisunrealistictobelievethatonecanexceedthe35%shareofRESinelectricityby2020atreasonablecost.

Getting the speed of the energy transition right is key to its success. Discussing speed and timing does not mean questioning the energy transition; it means taking responsibility for its successful and cost-efficient delivery.

There is a gap between the political vision of 2050 and the short-term regulatory and political decisions.“ „

Union of the Electricity Industry - EURELECTRIC aisbl

Boulevard de l’Impératrice, 66 - bte 2B - 1000 Brussels • BelgiumTel: + 32 2 515 10 00 • Fax: + 32 2 515 10 10twitter.com/EURELECTRIC • www.eurelectric.org

Maz

y G

raph

ic D

esig

n