Portfolio Management Relince

104

-

Upload

jitendra-virahyas -

Category

Documents

-

view

219 -

download

0

Transcript of Portfolio Management Relince

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 1/104

Jitendra

Virahya

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 2/104

STUDY ON

PORTFOLIO MANAGEMENT

IN CONTEXT TO

Jitendra

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 3/104

Virahyas

PREFACE

There is a vast difference between theory and practice. The practical training

program is designed with the purpose of bridging gap between theory and

practice. As such I am fortunate to have an opportunity to undergo my project

and thus my practical training with Reliance Life Insurance Company

Limited.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 4/104

Summer training was an exposure to corporate functional environment. It was

opportunity & great pleasure for me to be in Corporate Environment and having

interaction with concerned people.

This project is based on a brief study of six weeks of training period. Efforts

have been made to present all authentic information as far as possible.

ACKNOWLEDGEMENT

With a sense of great pleasure & satisfaction I present this report entitled as the

“Study on Portfolio Management in context to Reliance Life Insurance

“culmination of my efforts of last six weeks. Completion of this project, is no

doubt, is a product of invaluable support & contribution of a number of people.

I wish to express my gratitude to those who generously helped me in

completing this research work with their knowledge & expertise. A project of

this nature calls for intellectual nourishment, professional help &

encouragement from various quarters.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 5/104

I present my gratitude to project guide Mr., Sr. Sales Manager for giving me the

opportunity to work for Reliance Life Insurance Company Ltd., for being

constant guiding force & a source of Illumination throughout this entire period .

would also extend my gratitude to Mr. va (Executive Territory Manager) for his

useful suggestions.

My special thanks to all employees of Reliance Life Insurance Company Ltd,

Jhalawar, who extended their precious cooperation & for the patience they

showed while entertaining my queries.

I am immensely thankful to all agents who took out time from their busy

schedule and enthusiastically responded to my queries and provided me with al

the valuable information.

TABLE OF CONTENTS

1. Reliance Life - The Great Founder

• ADA Group Structure

• About Reliance Life

• Vision & Mission

• Vision

• Mission

• Goals

• Achievements

• Leadership Team

• Corporate Offices

2. Insurance - A Brief Introduction

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 6/104

• General

• Malhotra Committee Report

• Structure

• Competition

• Regulatory Body

•Investments

• Customer Service

3. Purpose & need of Insurance in India

4. IRDA Regulations pertaining to Agents / Agency in brief

• Definitions

• IRDA guidelines for Agents

• Insurance Act, 1938

5. Investment Portfolio Management

• Industry Scope

• Key Problems of running such businesses

• Size of Global Fund Management Industry

• Philosophy, Process and People

6. Investment Managers and portfolio Structure

• Investment styles

• Performance Measurement

• Risk Adjusted performance measurement

• Security

7. Classification of Securities

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 7/104

8. Classification of Funds

• Debt

• Equity

• Hybrid

9. The Securities Market• Public offer and private placement

• Physical nature of securities

• Divided and Un-divided securities

• Recruitment & selection

10. Types of Financial Market

• Raising capital

• Derivative Products

• Analysis of Financial

• Market Financial Markets in Popular Culture

11. Measuring financial Instruments

• Loss or Gain

• Risk and return

• Diversification

• Capital allocation line

• The risk free assets

• Systematic risk and specific risk

12. Diversification

• Return Expected while diversifying

13. Reliance life Portfolio Management

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 8/104

• The Analyst

• Different Fund options

14. Conclusion

15. Recommendations

16. Bibliography

17. Annexure

• LIC act 1938

• Constitution of LIC

ABSTRACT

Investment Portfolio Management is the professional management o

various securities (shares, bonds etc.) and assets (e.g., real estate), to meet

specified investment goals for the benefit of the investors.

Investors may be institutions (insurance companies, pension funds, corporations

etc.) or private investors (both directly via investment contracts and more

commonly via collective investment schemes e.g. mutual funds or Exchange

Traded Funds) .

The term asset management is often used to refer to the investment

management of collective investments, (not necessarily) whilst the more

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 9/104

generic fund management may refer to all forms of institutional investment

as well as investment management for private investors. Investment managers

who specialize in advisory or discretionary management on behalf of (normally

wealthy) private investors may often refer to their services as wealth

management or portfolio management often within the context of so-called

"private banking".

The provision of 'investment management services' includes elements o

financial analysis, asset selection, stock selection, plan implementation and

ongoing monitoring of investments. Investment management is a large and

important global industry in its own right responsible for caretaking of trillions of

dollars, euro, pounds and yen. Coming under the remit of financial services

many of the world's largest companies are at least in part investment managers

and employ millions of staff and create billions in revenue.

Fund manager (or investment adviser in the India.) refers to both a firm

that provides investment management services and an individual who directs

fund management decisions.

Investment Philosophy of Reliance Life

Reliance Life Insurance seeks consistent and superior long-term returns

with a well defined and discipline investment approach symbolizing

integrity and transparency to all stakeholders

Reliance Life offers the different fund options to the

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 10/104

Customers

• ULIP Equity

• Pure Equity

• Infrastructure

• Mid-Cap

• Energy

• Super Growth

• High Growth

• Growth Plus

• Growth

• Balanced

• Corporate Bond

• Pure Debt

• Gilt

• Guaranteed Bond-I

• Money Market

• Capital Secure

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 11/104

The Great Founder

"Pursue your goals even in the face of difficulties, and

convert adversities into opportunities."

- Dhirubhai Hirachand Ambani

Few men in history have made as dramatic a contribution to their country’s

economic fortunes as did the founder of Reliance, Shri. Dhirubhai H Ambani

Fewer still have left behind a legacy that is more enduring and timeless.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 12/104

As with all great pioneers, there is more than one unique way of describing the

true genius of Dhirubhai: The corporate visionary, the unmatched strategist, the

proud patriot, the leader of men, the architect of India’s capital markets, the

champion of shareholder interest. But the role Dhirubhai cherished most was

perhaps that of India’s greatest wealth creator. In one lifetime, he built, starting

from the proverbial scratch, India’s largest private sector enterprise.

When Dhirubhai embarked on his first business venture, he had a seed capita

of barely US$ 300 (around Rs 14,000). Over the next three and a half

decades, he converted this fledgling enterprise into a Rs. 3,25,000 crore

colossus—an achievement which earned Reliance a place on the global

Fortune 500 list, the first ever Indian private company to do so.

Under Dhirubhai’s extraordinary vision and leadership, Reliance scripted one of

the greatest growth stories in corporate history anywhere in the world, and

went on to become India’s largest private sector enterprise.

Through out this amazing journey, Dhirubhai always kept the interests of the

ordinary shareholder uppermost in mind, in the process making millionaires out

of many of the initial investors in the Reliance stock, and creating one of the

world’s largest shareholder families.

ADA Group Structure

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 13/104

About Reliance Life Insurance

Reliance Life Insurance offers you products that fulfill your savings and

protection needs. Our aim is to emerge as a transnational Life Insurer of globa

scale and standard.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 14/104

Reliance Life Insurance is an associate company of Reliance Capital Ltd., a part

of Reliance - Anil Dhirubhai Ambani Group. Reliance Capital is one of India’s

leading private sector financial services companies, and ranks among the top 3

private sector financial services and banking companies, in terms of net worth

Reliance Capital has interests in asset management and mutual funds, stock

broking, life and general insurance, proprietary investments, private equity andother activities in financial services.

Reliance - Anil Dhirubhai Ambani Group also has presence in

Communications, Energy, Natural Resources, Media, Entertainment, Healthcare

and Infrastructure.

Vision & Mission

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 15/104

Vision

Empowering everyone live their dreams.

MissionCreate unmatched value for everyone through dependable

effective, transparent and profitable life insurance and

pension plans.

Our Goal

Reliance Life Insurance would strive hard to achieve the 3goals mentioned below:

1. Emerge as transnational Life Insurer of global scale andstandard

2. Create best value for Customers, Shareholders and allStake holders

3. Achieve impeccable reputation and credentials through best business practices

Achievements

• RLIC has been one of the fast gainers in market share in new business

premium amongst the private players with an incremental market share

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 16/104

of 4.1% in the Financial Year 2007-08 – from 3.9% in April 07 to 8% in Feb

08. ( Source: IRDA)

• Also continues to be amongst the fast growing Private Life

Insurance Companies with a YOY growth of 195% in new business

premium as of Mar’08.

• A Company that has crossed 1.7 Million policies in just 2 years of

operation, post take over of AMP Sanmar business.

• Initiated Express Life – an Unique ’Over the Counter’ sales process for

Unit Linked Insurance Policies in the Industry.

• Accomplished a large distribution ramp-up in the Industry in a short span

of time by opening 600 branches in 10 months taking the overalbranch network above 740.

• RLIC continues to be one of the two Life Insurance companies in India to

be certified ISO 9001:2000 for all the processes.

• Awarded the Jamnalal Bajaj Uchit Vyavahar Puraskar 2007

Ceritificate of Merit in the Financial Services category by Council for

Fair Business Practices (CFBP).

Leadership Team

BOARD OF DIRECTORS

Gautam Doshi, Director

Gautam is the Group Managing Director of Reliance Anil Dhirubhai Amban

Group and Director of Reliance Life Insurance Company Limited.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 17/104

Satya Pal Talwar, Director

Satya Pal is the Director of Reliance Life Insurance Company Limited. He holds

an experience of more than 35 years in operations and policy formulation.

Saumen Ghosh, Group President

Saumen is currently the Group President of Reliance Capital Limited.

Malay Ghosh – President & Deputy CEO

Malay leads all Sales & Distribution activities at Reliance Life Insurance

Company Limited. His key focus is on rapid expansion of all channels and

accelerating the company’s growth trajectory.

Maneesha Thakur, Chief Human Resources Officer

Maneesha in her role as the Chief Human Resource Officer at Reliance Life

Insurance Company Limited, has developed a performance driven and

employee centric culture. She has been at the forefront of the organization

growth by facilitating talent acquisition and management.

Pournima Gupte, Appointed Actuary

Pournima is the Appointed Actuary at Reliance Life Insurance Company Limited

where she has the overall responsibility for statutory reporting, risk appetite

pricing, valuation, reinsurance, etc.

Leadership Team

BOARD OF DIRECTORS

C Mohan, Chief Technology Officer

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 18/104

Mohan is the Chief Technology Officer (CTO) of Reliance Life Insurance

Company Limited and he is responsible for Information Technology Strategy

Formulation and Deployment.

R Rangarajan, Chief Investment Officer

Rangarajan is the Chief Investment Officer at Reliance Life Insurance CompanyLimited. He along with his team strives to give the best possible returns on

investments to shareholders and policyholders, keeping in mind their appetite

for risk. Rangarajan draws on his in-depth knowledge of investment and

experience of 25 years to ensure that the goals of the organization are met—

without any compromise on the benefits of the investors.

S V Sunder Krishnan, Chief Risk Officer

Sunder is the Chief Risk officer for Reliance Life Insurance and is responsible for

overseeing Risk Management, Internal Audit and Compliance functions at

Reliance Life Insurance.

Saroj K Panigrahi, Head – Legal, Compliance & Company Secretary

'Saroj K Panigrahi heads the Legal, Compliance and Company Secretaria

function of Reliance Life Insurance'. He is armed with twelve years of valuable

experience in the Corporate Legal, Commercial, Regulatory Compliance and

Corporate Governance domains.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 19/104

Corporate Offices

Call us at our 24 x 7 Call Center number-3033 8181 OR our Toll Free Number

1800 300 08181

Email us at [email protected]

Write to us at –

Registered Office:

H Block, 1st Floor,

Dhirubhai Ambani KnowledgeCity,

Navi Mumbai, Maharashtra -

400710.

Corporate Office:

Level 1, Midas Wing - A,

Sahar Plaza, Andheri Kurla Road,Andheri (East) Mumbai - 400 059.

Phone No: +91-22-3088 3444

Fax No: +91-22-3088 6587

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 20/104

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 21/104

A BRIEF INTRODUCTION

In General

The business of insurance started with marine business. Traders, who used to

gather in the Lloyd’s coffee house in London, agreed to share the losses of thei

goods while being carried by ships. The losses use to occur because of pirates

who robbed on the high seas or because of the bad weather spoiling the goods

or sinking the ships. The first insurance policy was issued in 1583 in England. In

India, insurance began in 1870 with life insurance being transacted by an

English company, “the European and the Albert”. The first insurance company

was the Bombay Mutual Assurance Ltd.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 22/104

In the wake of Swadeshi Movement in India in early 1900’s, quite a good

number of Indian companies were formed in the various parts of the country to

transact insurance business. To name a few: ‘Hindustan Cooperative’ and

‘National Insurance’ in Kolkatta; ‘United India’ in Chennai; ‘Bombay Life’, ‘New

India’ and ‘Jupiter’ in Mumbai and ‘Lakshmi Insurance’ in New Delhi.

In 1956, life insurance business was nationalized and LIC of India came into

being on 1.09.1956. The Government took over the business of 245 companies

(including 75 provident fund societies) who were transacting life insurance

business at that time. There after, LIC got the exclusive privilege to transact life

insurance business in India.

Malhotra Committee Report

In 1993, Malhotra Committee headed by former Finance Secretary and RB

Governor R. N. Malhotra, was formed to evaluate the Indian insurance industry

and recommend its future direction.

The Malhotra committee was set up with the objective of complementing the

reforms initiated in the financial sector.

The reforms were aimed at “creating a more efficient and competitive financia

system suitable for the requirements of the economy keeping in mind the

structural changes currently underway and recognizing that insurance is an

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 23/104

important part of the overall financial system where it was necessary to address

the need for similar reforms…”

In 1994, the committee submitted the report and some of the key

recommendations included:

i) Structure

Government stake in the Insurance Companies to be brought down to

50%

All the insurance companies should be given greater freedom to operate

ii) Competition

Private Companies with a minimum paid up capital of Rs.1bn should be

allowed to enter the industry

No Company should deal in both Life and General Insurance through a

single entity

Foreign companies may be allowed to enter the industry in collaboration

with the

Domestic companies

iii) Investments

Mandatory Investments of LIC Life Fund in government securities to be

reduced

from 75% to 50%

iv) Customer Service

Companies should pay interest on delays in payments beyond 30 days.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 24/104

Computerization of operations and updating of technology to be carried

out in the insurance industry .

The committee emphasized that in order to improve the customer services and

increase the coverage of the insurance industry should be opened up to

competition. But at the same time, the committee felt the need to exercise

caution as any failure on the part of new players could ruin the public

confidence in the industry.

Hence, it was decided to allow competition in a limited way by stipulating the

minimum capital requirement of Rs.100 crores. The committee felt the need to

provide greater autonomy to insurance companies in order to improve their

performance and enable them to act as independent companies with economic

motives. For this purpose, it had proposed setting up an independent regulatory

body.

Relevant laws were amended in 1999 and LIC’s monopoly rights to transact the

insurance business in India came to an end. At the close of financial year ending

31 March 2004 twelve new companies were registered with the Insurance

Regulatory and Development Authority (IRDA) to transact life insurancebusiness in India.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 25/104

PURPOSE AND NEED OF INSURANCE

IN INDIA

Assets are insured because they are likely to be destroyed through accidenta

occurrences called perils. Few examples of perils are fire, floods, lightening,

breakdowns, earthquakes, etc. perils are the events. Risks are the

consequential losses or the damages.

The risk only means that there is only possibility of loss or damages. The

damage may or may not happen. Insurance is done against the contingency

that it may happen. There has to be an uncertainty about the risk. Insurance is

relevant if there are uncertainties. If there are no uncertainties about the

occurrence of any event it cannot be insured against. In the case of human

being, death is certain, but the time of death is uncertain. In the case of aperson who is terminally ill, the time of death is not uncertain, though exactly

not known. He cannot be insured.

Life insurance should ideally be bought for what it was always intended to do –

indemnify the nominees in case of an eventuality. Keeping this in mind al

individuals should have a term plan in their insurance portfolio, irrespective of

their profile. To take care of the investment and the ‘tax-saving’ elements

individuals can invest in tax saving Unit linked insurance plans (ULIPs), which

can invest up to 100% of the premium in market-linked instruments, is also an

option, which individuals can opt for.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 26/104

Life insurance can help in bringing economic development in the country by

mobilizing public savings. Funds collected form the public is utilized in

investment for economic growth. In any other investment or saving avenue, like

bank deposits, savings certificates or mutual funds or shares and stocks etc.

amount of funds available at any time will not be more than the amount saved,

appreciation or interest earned till then. In life insurance, the amount available

is the one that one wished to have at end of the savings period, which mayrange up to 30 or even more years.

Life insurance has advantages over other forms of savings:

Facility of nomination and assignment makes the claim settlement easy

on death

Life insurance involves compulsory savings

Tax benefits on premium paid as well as on the amount received by way

of claim

Loans can be insured against a life insurance policy.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 27/104

Mechanism of Insurance

The concept of insurance is that people exposed to the same risk come

together and agreed to share a loss collectively if any of their members

suffers it from that risk.

Insurance companies play the role of implementing this concept-

a) They bring together people exposed to the similar risk

b) They collect members’ contribution in advance in the shape o

premiums and create a fund out of which the losses are paid

The life insurance covers contingencies (death, retirement) and provides

relief to the family in the event of death or retirement of the breadwinner.

Variable needs of life insurance can be

a) Providing financial security to the family

b) Provision for education, marriage, etc of the children

c) Post-retirement income for self and dependents

d) Special needs like Medical expenses

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 28/104

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 29/104

INSURANCE ACT, 1938

The Insurance Act, 1938 aimed ‘to consolidate and amend the law relating to

the business of insurance. It covers both life and non-life insurance business.

It came into effect on 1st. July 1939.

The act was amended in 1950 and again in 1999. Some of the Major changes

brought about in 1950 were:

Section 2 (5A)

‘Chief Agent’ means person who, not being a salaried employee of an insurer, in

consideration of commission

Performs any administrative and organizing function for the insurer.

Procures life insurance business for the insurer by employing or causing

to be employed, insurance agents on behalf of the insurer.

Section 2(17)

“Special Agent’ means a person who, not being a salaried employee of an

insurer, in consideration of commission:

Procures life insurance business for the insurer whether wholly or in part

by employing or causing to be employed insurance agents on behalf of

the insurer, but does not include a chief agent.

He only procures business through agents but does not perform anyadministrative function like a chief agent.

Special agents can do only life insurance business and not general insurance

business.

Individuals, companies or firms can become chief agents or special agents

Individuals, Directors or Partners, as the case may be, should be free from

disqualifications specified for agents.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 30/104

Section 42A,

The certificate shall remain valid for a period of 12 months but shall be

renewable.

Provisions stipulate the number of insurance agents that a ‘chief agent

may employ directly or through ‘special agents’. These provisions also

stipulate the minimum business requirements.

For ‘special agents’ also there are similar stipulations of minimum numbe

of agents to be appointed and the minimum business requirements.

Some important Provisions of the Insurance Act, 1938

1. Registration of Insurance companies.

2. Maintenance and scrutiny of accounts and valuation reports.

3. Investment and utilization of funds.

4. Placing limits on the expenses of insurers.

5. Licensing of agents and their remuneration.

6. Prohibition of rebates.

7. Approval of premium rates and plans.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 31/104

8. Maintaining solvency levels.

9. Constitution of Insurance Associations, Insurance Councils and Tarif

Advisory Committees.

10. The Act also vests the IRDA with powers to:

• Inspect documents.

• Appoint additional directors.

• Issue directions.

• Takeover the management of the insurer through the appointment

of an Administrator by the Central Government.

11. Protection of the policy holder’s interest by prohibition of policies from

being called into question after 2 years. [Sec. 45]

12. Provision of nomination. [Sec. 39]

13. Provision for assignment. [Sec. 38]

14. Provision for easy settlement of dispute.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 32/104

About IRDA

Composition of Authority under IRDA Act, 1999

As per the section 4 of IRDA Act' 1999, Insurance Regulatory and Development

Authority (IRDA, which was constituted by an act of parliament) specify the

composition of Authority

The Authority is a ten member team consisting of

(a) a Chairman;

(b) five whole-time members;

(c) four part-time members,

(all appointed by the Government of India)

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 33/104

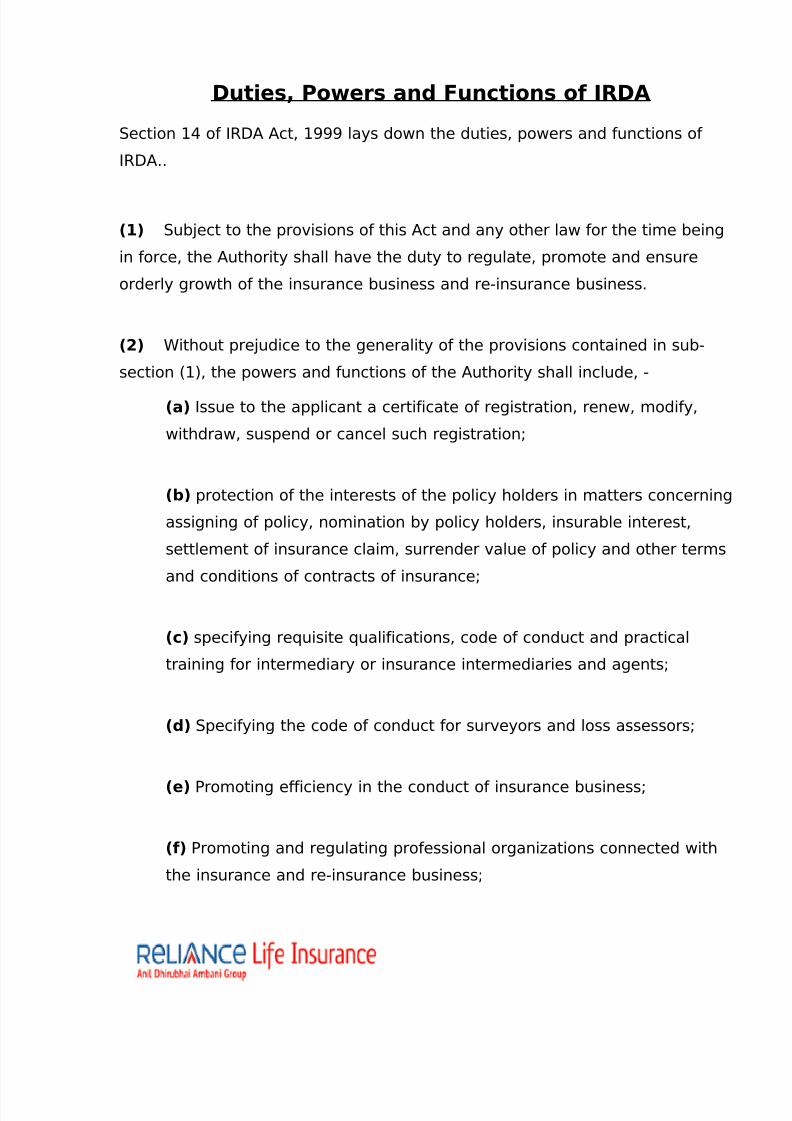

Duties, Powers and Functions of IRDA

Section 14 of IRDA Act, 1999 lays down the duties, powers and functions of

IRDA..

(1) Subject to the provisions of this Act and any other law for the time being

in force, the Authority shall have the duty to regulate, promote and ensure

orderly growth of the insurance business and re-insurance business.

(2) Without prejudice to the generality of the provisions contained in sub-

section (1), the powers and functions of the Authority shall include, -

(a) Issue to the applicant a certificate of registration, renew, modify,

withdraw, suspend or cancel such registration;

(b) protection of the interests of the policy holders in matters concerning

assigning of policy, nomination by policy holders, insurable interest,

settlement of insurance claim, surrender value of policy and other terms

and conditions of contracts of insurance;

(c) specifying requisite qualifications, code of conduct and practical

training for intermediary or insurance intermediaries and agents;

(d) Specifying the code of conduct for surveyors and loss assessors;

(e) Promoting efficiency in the conduct of insurance business;

(f) Promoting and regulating professional organizations connected with

the insurance and re-insurance business;

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 34/104

(g) Levying fees and other charges for carrying out the purposes of this

Act;

(h) calling for information from, undertaking inspection of, conducting

enquiries and investigations including audit of the insurers

intermediaries, insurance intermediaries and other organizations

connected with the insurance business;

(I) control and regulation of the rates, advantages, terms and conditions

that may be offered by insurers in respect of general insurance business

not so controlled and regulated by the Tariff Advisory Committee undersection 64U of the Insurance Act, 1938 (4 of 1938)

(j) Specifying the form and manner in which books of account shall be

maintained and statement of accounts shall be rendered by insurers and

other insurance intermediaries;

(k) Regulating investment of funds by insurance companies;

(l) Regulating maintenance of margin of solvency;

(m) Adjudication of disputes between insurers and intermediaries or

insurance intermediaries;

(n) Supervising the functioning of the Tariff Advisory Committee;

(o) Specifying the percentage of premium income of the insurer to

finance schemes for promoting and regulating professional organizations

referred to in clause (f);

(p) Specifying the percentage of life insurance business and general

insurance business to be undertaken by the insurer in the rural or social

sector; and

(q) Exercising such other powers as may be prescribed

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 35/104

List of Life Insurers

S.No

NAME OF THE COMPANY NAME OFAPPOINTEDACTUARY

TELEPHONENO./FAX No./E-

MAIL & WEBADDRESS

1. Bajaj Allianz Life InsuranceCompany Limited .

Mr. Anil KumarSingh

Tel : 020-4026666Fax : 020-4026789

2. Birla Sun Life Insurance Co. Ltd Mr. Fabien Jeudy

Tel : 022 5678 3333Fax: 022 5678 3232

3. HDFC Standard Life Insurance Co.Ltd

Mr. William John Martin

Tel : 022-67516666Fax: 022-2822 8844

4. ICICI Prudential Life Insurance Co.Ltd

Mr. Avijit Chatterjee Tel :022-56621996Fax: 022-56622031

5. ING Vysya Life Insurance Company Ltd.

Ms.Hemamalini

Ramakrishnan

Tel : 080-25328000Fax: 080-25559764

6. Life Insurance Corporation of India Mr. T Bhargava Tel 56598701Fax: 22824386

7. Max New York Life Insurance Co.Ltd

Mr.JohnCharles Poole

Tel : 0124-2561717Fax: 0124-2561764

8. Met Life India Insurance CompanyLtd.

Mr. M S V SPhanesh

Tel : 080-26438638Fax: 080-26521970 Toll Free No. 1-600-44-6969

9. Kotak Mahindra Old Mutual LifeInsurance Limited

Mr. AndrewWillisCartwright

Tel : 022-6621 5999Fax:022-6621 5757,6621 5858

10. SBI Life Insurance Co. Ltd Mr. SanjeevKumar Pujari

Tel : 022-56392000Fax: 022-56621471

11. Tata AIG Life Insurance CompanyLimited

Mr. HeerakBasu

Tel : 022-66516000Fax : 022-66550711

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 36/104

12 Reliance Life Insurance CompanyLimited.

Ms. PournimaGupte

Tel : 022-30479600/30479784Fax: 022-30479650

13 Aviva Life Insurance CompanyIndia Limited

Mr. ChandanKhasnobis

Tel: 0124-2709000/01,Fax: 0124-2709007.

14 Sahara India Life Insurance Co,

Ltd.

Mr. K K Dharni Tel: 0522-2337777

Fax: 0522-2378200

15 Shriram Life Insurance Co, Ltd. Mr N S Sastry Tel: 040-23434466-72Fax: 040-23434488

16 Bharti AXA Life InsuranceCompany Ltd.

Mr. G L NSarma

Tel: 022 –40306300/6301Fax: 022 -40306347

17 Future Generali India LifeInsurance Company Limited

Mr. GorakhnathAgarwal

Tel No.:

022-40976666

18 IDBI Fortis Life Insurance CompanyLtd.,

Mr. Michael JWood

Tel No.:

022-24908109/10

Fax No.:

022-24941016

19 Canara HSBC Oriental Bank of

Commerce Life InsuranceCompany Ltd.

Mr. Paul

Beresford

Tel: 0124– 44215706Fax: 0124- 4201109

20 AEGON Religare Life InsuranceCompany Limited.

Mr. K.S.Gopalakrishnan

Tele No.-022-67292929

21 DLF Pramerica Life Insurance Co.Ltd.

Mr. PradeepKumar Thapliyal

Ph. No.-91-124-271700

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 37/104

22 Star Union Dai-ichi Life InsuranceCo. Ltd.,

Mr. ISAMBASIVARAO

Phone: 022-32909099

Investment Portfolio management

Investment Portfolio Management is the professional management o

various securities (shares, bonds etc.) and assets (e.g., real estate), to meet

specified investment goals for the benefit of the investors. Investors may be

institutions (insurance companies, pension funds, corporations etc.) or private

investors (both directly via investment contracts and more commonly via

collective investment schemes e.g. mutual funds or Exchange Traded Funds) .

The term asset management is often used to refer to the investment

management of collective investments, (not necessarily) whilst the more

generic fund management may refer to all forms of institutional investment

as well as investment management for private investors. Investment managerswho specialize in advisory or discretionary management on behalf of (normally

wealthy) private investors may often refer to their services as wealth

management or portfolio management often within the context of so-called

"private banking".

The provision of 'investment management services' includes elements o

financial analysis, asset selection, stock selection, plan implementation and

ongoing monitoring of investments. Investment management is a large and

important global industry in its own right responsible for caretaking of trillions of

dollars, euro, pounds and yen. Coming under the remit of financial services

many of the world's largest companies are at least in part investment managers

and employ millions of staff and create billions in revenue.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 38/104

Fund manager (or investment adviser in the India.) refers to both a firm

that provides investment management services and an individual who directs

fund management decisions.

Industry scope

The business of investment portfolio management has several facets, including

the employment of professional fund managers, research (of individual assets

and asset classes), dealing, settlement, marketing, internal auditing, and the

preparation of reports for clients. The largest financial fund managers are firmsthat exhibit all the complexity their size demands. Apart from the people who

bring in the money (marketers) and the people who direct investment (the fund

managers), there are compliance staff (to ensure accord with legislative and

regulatory constraints), internal auditors of various kinds (to examine interna

systems and controls), financial controllers (to account for the institutions' own

money and costs), computer experts, and "back office" employees (to track and

record transactions and fund valuations for up to thousands of clients peinstitution).

Key problems of running such businesses

Key problems include:

• Revenue is directly linked to market valuations, so a major fall in asset

prices causes a precipitous decline in revenues relative to costs;

• Above-average fund performance is difficult to sustain, and clients may

not be patient during times of poor performance;

• Successful fund managers are expensive and may be headhunted by

competitors;

• Above-average fund performance appears to be dependent on the unique

skills of the fund manager; however, clients are loath to stake thei

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 39/104

investments on the ability of a few individuals- they would rather see firm-

wide success, attributable to a single philosophy and internal discipline;

• Analysts who generate above-average returns often become sufficiently

wealthy that they avoid corporate employment in favor of managing their

personal portfolios.

The most successful investment firms in the world have probably been thosethat have been separated physically and psychologically from banks and

insurance companies. That is, the best performance and also the most dynamic

business strategies (in this field) have generally come from independent

investment management firms.

Representing the owners of shares

Institutions often control huge shareholdings. In most cases they are acting asfiduciary agents rather than principals (direct owners). The owners of shares

theoretically have great power to alter the companies they own via the voting

rights the shares carry and the consequent ability to pressure managements

and if necessary out-vote them at annual and other meetings.

In practice, the ultimate owners of shares often do not exercise the power they

collectively hold (because the owners are many, each with small holdings)

financial institutions (as agents) sometimes do. There is a general belief that

shareholders - in this case, the institutions acting as agents—could and should

exercise more active influence over the companies in which they hold shares

(e.g., to hold managers to account, to ensure Boards effective functioning)

Such action would add a pressure group to those (the regulators and the Board

overseeing management.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 40/104

However there is the problem of how the institution should exercise this power.

One way is for the institution to decide, the other is for the institution to poll its

beneficiaries. Assuming that the institution polls, should it then: (i) Vote the

entire holding as directed by the majority of votes cast? (ii) Split the vote

(where this is allowed) according to the proportions of the vote? (iii) Or respect

the abstainers and only vote the respondents' holdings?

The price signals generated by large active managers holding or not holding the

stock may contribute to management change. For example, this is the case

when a large active manager sells his position in a company, leading to

(possibly) a decline in the stock price, but more importantly a loss of confidence

by the markets in the management of the company, thus precipitating changes

in the management team.

Some institutions have been more vocal and active in pursuing such matters

for instance, some firms believe that there are investment advantages to

accumulating substantial minority shareholdings (i.e. 10% or more) and putting

pressure on management to implement significant changes in the business. In

some cases, institutions with minority holdings work together to force

management change. Perhaps more frequent is the sustained pressure that

large institutions bring to bear on management teams through persuasive

discourse and PR. On the other hand, some of the largest investment managers—such as Barclays Global Investors and Vanguard—advocate simply owning

every company, reducing the incentive to influence management teams. A

reason for this last strategy is that the investment manager prefers a closer

more open and honest relationship with a company's management team than

would exist if they exercised control; allowing them to make a bette

investment decision.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 41/104

The national context in which shareholder representation considerations are set

is variable and important. The USA is a litigious society and shareholders use

the law as a lever to pressure management teams. In Japan it is traditional for

shareholders to be low in the 'pecking order,' which often allows management

and labor to ignore the rights of the ultimate owners. Whereas US firms

generally cater to shareholders, Japanese businesses generally exhibit astakeholder mentality, in which they seek consensus amongst all interested

parties (against a background of strong unions and labour legislation).

Size of the global fund management industry

Assets of the global fund management industry increased for the fourth year

running in 2008 to reach a record $94.3 trillion. This was up 14% on the

previous year and double from five years earlier. Growth during the past three

years has been due to an increase in capital inflows and strong performance of

equity markets.

Pension assets totaled $38.2 trillion in 2008, with a further $26.2 trillion

invested in mutual funds and $19.9 trillion in insurance funds. Together with

alternative assets, such as those of sovereign wealth funds, hedge funds

private equity funds and funds of wealthy individuals, assets of the global fund

management industry probably totaled around $150 trillion at the end of 2008.

The US was by far the largest source of funds under management in 2008 with

nearly a half of the world total. It was followed by the UK with 9% and Japanwith 6%. The Asia-Pacific region has shown the strongest growth in recent

years. Countries such as China and India offer huge potential and many

companies are showing an increased focus in this region.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 42/104

Philosophy, process and people

The 3-P's (Philosophy, Process and People) are often used to describe the

reasons why the manager is able to produce above average results.

• Philosophy refers to the over-arching beliefs of the investment

organization. For example: (i) Does the manager buy growth or value

shares (and why)? (ii) Do they believe in market timing (and on what

evidence)? (iii) Do they rely on external research or do they employ a

team of researchers? It is helpful if any and all of such fundamenta

beliefs are supported by proof-statements.

• Process refers to the way in which the overall philosophy is

implemented. For example: (i) Which universe of assets is explored before

particular assets are chosen as suitable investments? (ii) How does the

manager decide what to buy and when? (iii) How does the manager

decide what to sell and when? (iv) Who takes the decisions and are they

taken by committee? (v) What controls are in place to ensure that a rogue

fund (one very different from others and from what is intended) cannot

arise?

• People refer to the staff, especially the fund managers. The questions

are, Who are they? How are they selected? How old are they? Who reports

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 43/104

to whom? How deep is the team (and do all the members understand the

philosophy and process they are supposed to be using)? And mos

important of all, How long has the team been working together? This last

question is vital because whatever performance record was presented at

the outset of the relationship with the client may or may not relate to

(have been produced by) a team that is still in place. If the team haschanged greatly (high staff turnover or changes to the team), then

arguably the performance record is completely unrelated to the existing

team (of fund managers).

Investment managers and portfolio structures

At the heart of the investment management industry are the managers who

invest and divest client investments.

A certified company investment advisor should conduct an assessment of each

client's individual needs and risk profile. The advisor then recommends

appropriate investments.

Asset allocation

The different asset class definitions are widely debated, but four common

divisions are stocks, bonds, real-estate and commodities. The exercise o

allocating funds among these assets (and among individual securities within

each asset class) is what investment management firms are paid for. Asset

classes exhibit different market dynamics, and different interaction effects

thus, the allocation of monies among asset classes will have a significant effect

on the performance of the fund. Some research suggests that allocation among

asset classes has more predictive power than the choice of individual holdings

in determining portfolio return. Arguably, the skill of a successful investment

manager resides in constructing the asset allocation, and separately the

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 44/104

individual holdings, so as to outperform certain benchmarks (e.g., the peer

group of competing funds, bond and stock indices).

Long-term returns

It is important to look at the evidence on the long-term returns to different

assets, and to holding period returns (the returns that accrue on average over

different lengths of investment). For example, over very long holding periods

(eg. 10+ years) in most countries, equities have generated higher returns than

bonds, and bonds have generated higher returns than cash. According to

financial theory, this is because equities are riskier (more volatile) than bonds

which are themselves more risky than cash.

Diversification

Against the background of the asset allocation, fund managers consider the

degree of diversification that makes sense for a given client (given its riskpreferences) and construct a list of planned holdings accordingly. The list wil

indicate what percentage of the fund should be invested in each particular stock

or bond. The theory of portfolio diversification was originated by Markowitz and

effective diversification requires management of the correlation between the

asset returns and the liability returns, issues internal to the portfolio (individua

holdings volatility), and cross-correlations between the returns.

Investment styles

There are a range of different styles of fund management that the institution

can implement. For example, growth, value, market neutral, smal

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 45/104

capitalization, indexed, etc. Each of these approaches has its distinctive

features, adherents and, in any particular financial environment, distinctive risk

characteristics. For example, there is evidence that growth styles (buying

rapidly growing earnings) are especially effective when the companies able to

generate such growth are scarce; conversely, when such growth is plentiful

then there is evidence that value styles tend to outperform the indicesparticularly successfully.

Performance measurement

Fund performance is the acid test of fund management, and in the institutiona

context accurate measurement is a necessity. For that purpose, institutions

measure the performance of each fund (and usually for internal purposes

components of each fund) under their management, and performance is also

measured by external firms that specialize in performance measurement

In a typical case (let us say an equity fund), then the calculation would be made

(as far as the client is concerned) every quarter and would show a percentage

change compared with the prior quarter (e.g., +4.6% total return in US dollars)

This figure would be compared with other similar funds managed within the

institution (for purposes of monitoring internal controls), with performance data

for peer group funds, and with relevant indices (where available) or tailor-made

performance benchmarks where appropriate. The specialist performance

measurement firms calculate quartile and docile data and close attention would

be paid to the (percentile) ranking of any fund.

Generally speaking, it is probably appropriate for an investment firm to

persuade its clients to assess performance over longer periods (e.g., 3 to 5

years) to smooth out very short term fluctuations in performance and the

influence of the business cycle. This can be difficult however and, industry wide

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 46/104

there is a serious preoccupation with short-term numbers and the effect on the

relationship with clients (and resultant business risks for the institutions).

An enduring problem is whether to measure before-tax or after-tax

performance. After-tax measurement represents the benefit to the investor, but

investors' tax positions may vary. Before-tax measurement can be misleading

especially in regimens that tax realized capital gains (and not unrealized). It is

thus possible that successful active managers (measured before tax) may

produce miserable after-tax results. One possible solution is to report the after-

tax position of some standard taxpayer.

Risk-adjusted performance measurement

Performance measurement should not be reduced to the evaluation of fund

returns alone, but must also integrate other fund elements that would be of

interest to investors, such as the measure of risk taken. Several other aspects

are also part of performance measurement: evaluating if managers have

succeeded in reaching their objective, i.e. if their return was sufficiently high toreward the risks taken; how they compare to their peers; and finally whether

the portfolio management results were due to luck or the manager’s skill. The

need to answer all these questions has led to the development of more

sophisticated performance measures, many of which originate in modern

portfolio theory.

Modern portfolio theory established the quantitative link that exists between

portfolio risk and return. The Capital Asset Pricing Model (CAPM) developed by

Sharpe (1964) highlighted the notion of rewarding risk and produced the first

performance indicators, be they risk-adjusted ratios (Sharpe ratio, information

ratio) or differential returns compared to benchmarks (alphas). The Sharpe ratio

is the simplest and best known performance measure. It measures the return of

a portfolio in excess of the risk-free rate, compared to the total risk of the

portfolio. This measure is said to be absolute, as it does not refer to any

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 47/104

benchmark, avoiding drawbacks related to a poor choice of benchmark

Meanwhile, it does not allow the separation of the performance of the market in

which the portfolio is invested from that of the manager. The information ratio

is a more general form of the Sharpe ratio in which the risk-free asset is

replaced by a benchmark portfolio. This measure is relative, as it evaluates

portfolio performance in reference to a benchmark, making the result stronglydependent on this benchmark choice.

Portfolio alpha is obtained by measuring the difference between the return of

the portfolio and that of a benchmark portfolio. This measure appears to be the

only reliable performance measure to evaluate active management. In fact, wehave to distinguish between normal returns, provided by the fair reward for

portfolio exposure to different risks, and obtained through passive

management, from abnormal performance (or out performance) due to the

manager’s skill, whether through market timing or stock picking. The first

component is related to allocation and style investment choices, which may not

be under the sole control of the manager, and depends on the economic

context, while the second component is an evaluation of the success of the

manager’s decisions. Only the latter, measured by alpha, allows the evaluation

of the manager’s true performance.

Portfolio normal return may be evaluated using factor models. The first model

proposed by Jensen (1968), relies on the CAPM and explains portfolio norma

returns with the market index as the only factor. It quickly becomes clear,

however, that one factor is not enough to explain the returns and that other

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 48/104

factors have to be considered. Multi-factor models were developed as an

alternative to the CAPM, allowing a better description of portfolio risks and an

accurate evaluation of managers’ performance. For example, Fama and French

(1993) have highlighted two important factors that characterize a company's

risk in addition to market risk. These factors are the book-to-market ratio and

the company's size as measured by its market capitalization. Fama and Frenchtherefore proposed a three-factor model to describe portfolio normal returns

(Fama-French three-factor model). Carhart (1997) proposed to add momentum

as a fourth factor to allow the persistence of the returns to be taken into

account. Also of interest for performance measurement is Sharpe’s (1992) style

analysis model, in which factors are style indices. This model allows a custom

benchmark for each portfolio to be developed, using the linear combination of

style indices that best replicate portfolio style allocation, and leads to an

accurate evaluation of portfolio alpha.

Security

A security is a fungible, negotiable instrument representing financial value

Securities are broadly categorized into debt securities (such as banknotes

bonds and debentures); equity securities, e.g., common stocks; and derivative

(finance) contracts such as forwards, futures, options and swaps. The company

or other entity issuing the security is called the issuer. What specifically

qualifies as a security is dependent on the regulatory structure in a country. For

example, private investment pools may have some features of securities, but

they may not be registered or regulated as such if they meet various

restrictions.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 49/104

Securities may be represented by a certificate or, more typically, "non-

certificated", that is in electronic or "book entry" only form. Certificates may be

bearer, meaning they entitle the holder to rights under the security merely by

holding the security, or registered, meaning they entitle the holder to rights

only if he or she appears on a security register maintained by the issuer or an

intermediary. They include shares of corporate stock or mutual funds, bonds

issued by corporations or governmental agencies, stock options or other

options, limited partnership units, and various other formal investment

instruments that are negotiable and fungible.

Classification of Securities

Securities may be classified according to many categories or classification

systems:

• Issuer

• Currency of denomination

• Ownership rights

• Term to maturity

• Degree of liquidity

• Income payments

• Tax treatment

• Credit Rating

• Industrial Sector or "Industry" (Sector often refers to a higher level or

broader category such as Consumer Discretionary whereas Industry often

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 50/104

refers to a lower level classification such as Consumer Appliances; See

Industry for a discussion of some classification systems).

• Region or Country (such as country of incorporation, country of principal

sales/market of its products or services, or country in which the principa

securities exchange on which it trades is located)

• Market Capitalization

• State (typically for municipal or "tax-free" bonds in the India)

By type of issuer

Issuers of securities include commercial companies, government agencies, loca

authorities and international and supranational organizations (such as the World

Bank). Debt securities issued by a government (called government bonds or

sovereign bonds) generally carry a lower interest rate than corporate debt

issued by commercial companies. Interests in an asset—for example, the flow of

royalty payments from intellectual property—may also be turned into securities These repackaged securities resulting from a securitization are usually issued

by a company established for the purpose of the repackaging—called a specia

purpose vehicle (SPV). See "Repackaging" below. SPVs are also used to issue

other kinds of securities. SPVs can also be used to guarantee securities, such as

covered bonds.

New capital

Commercial enterprises have traditionally used securities as a means of raising

new capital. Securities may be an attractive option relative to bank loans

depending on their pricing and market demand for particular characteristics.

Another disadvantage of bank loans as a source of financing is that the bank

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 51/104

may seek a measure of protection against default by the borrower via extensive

financial covenants. Through securities, capital is provided by investors who

purchase the securities upon their initial issuance. In a similar way, the

governments may raise capital through the issuance of securities (see

government debt).

Repackaging

In recent decades securities have been issued to repackage existing assets. In a

traditional securitization, a financial institution may wish to remove assets from

its balance sheet in order to achieve regulatory capital efficiencies or toaccelerate its receipt of cash flow from the original assets. Alternatively, an

intermediary may wish to make a profit by acquiring financial assets and

repackaging them in a way which makes them more attractive to investors. In

other words, a basket of assets is typically contributed or placed into a separate

legal entity such as a trust or SPV, which subsequently issues shares of equity

interest to investors. This allows the sponsor entity to more easily raise capita

for these assets as opposed to finding buyers to purchase directly such assets.

By type of holder

Investors in securities may be retail, i.e. members of the public investing other

than by way of business. The greatest part in terms of volume of investment is

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 52/104

wholesale, i.e. by financial institutions acting on their own account, or on behalf

of clients. Important institutional investors include investment banks, insurance

companies, pension funds and other managed funds.

Investment

The traditional economic function of the purchase of securities is investment

with the view to receiving income and/or achieving capital gain. Debt securities

generally offer a higher rate of interest than bank deposits, and equities may

offer the prospect of capital growth. Equity investment may also offer control of

the business of the issuer. Debt holdings may also offer some measure o

control to the investor if the company is a fledgling start-up or an old giant

undergoing 'restructuring'. In these cases, if interest payments are missed, the

creditors may take control of the company and liquidate it to recover some of

their investment.

Collateral

The last decade has seen an enormous growth in the use of securities as

collateral. Purchasing securities with borrowed money secured by other

securities or cash itself is called "buying on margin." Where A is owed a debt or

other obligation by B, A may require B to deliver property rights in securities to

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 53/104

A. These property rights enable A to satisfy its claims in the event that B fails to

make good on its obligations to A or otherwise becomes insolvent. Collatera

arrangements are divided into two broad categories, namely security interests

and outright collateral transfers. Commonly, commercial banks, investment

banks, government agencies and other institutional investors such as mutua

funds are significant collateral takers or providers. In addition, private partiesincluding funds and small institutions may utilize stocks or other securities as

collateral for portfolio loans in securities lending scenarios, which may be

structured into either recourse or nonrecourse packages and are often referred

to as "hedge loans".

Debt and equity

Securities are traditionally divided into debt securities and equities.

Debt

Debt securities may be called debentures, bonds, deposits, notes or

commercial paper depending on their maturity and certain other

characteristics. The holder of a debt security is typically entitled to the

payment of principal and interest, together with other contractual rights

under the terms of the issue, such as the right to receive certain information

Debt securities are generally issued for a fixed term and redeemable by the

issuer at the end of that term. Debt securities may be protected by collatera

or may be unsecured, and, if they are unsecured, may be contractually

"senior" to other unsecured debt meaning their holders would have a priority

in a bankruptcy of the issuer. Debt that is not senior is "subordinated".

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 54/104

Corporate bonds represent the debt of commercial or industrial entities

Debentures have a long maturity, typically at least ten years, whereas notes

have a shorter maturity. Commercial paper is a simple form of debt security

that essentially represents a post-dated check with a maturity of not more

than 270 days.

Money market instruments are short term debt instruments that

may have characteristics of deposit accounts, such as certificates of deposit

and certain bills of exchange. They are highly liquid and are sometimes

referred to as "near cash". Commercial paper is also often highly liquid.

Euro debt securities are securities issued internationally outside theidomestic market in a denomination different from that of the issuer's

domicile. They include Eurobonds and Euro notes. Eurobonds are

characteristically underwritten, and not secured, and interest is paid gross. A

Euro note may take the form of euro-commercial paper (ECP) or euro-

certificates of deposit.

Government bonds are medium or long term debt securities issued by

sovereign governments or their agencies. Typically they carry a lower rate of

interest than corporate bonds, and serve as a source of finance for

governments. U.S. federal government bonds are called treasuries. Because

of their liquidity and perceived low risk, treasuries are used to manage the

money supply in the open market operations of non-US central banks.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 55/104

Sub-sovereign government bonds, known in the India as municipa

bonds, represent the debt of state, provincial, territorial, municipal or other

governmental units other than sovereign governments.

Supranational bonds represent the debt of international organizations

such as the World Bank, the International Monetary Fund, regiona

multilateral development banks and others.

Equity

An equity security is a share of equity interest in an entity such as the capita

stock of a company, trust or partnership. The most common form of equity

interest is common stock, although preferred equity is also a form of capita

stock. The holder of an equity is a shareholder, owning a share, or fractiona

part of the issuer. Unlike debt securities, which typically require regula

payments (interest) to the holder, equity securities are not entitled to any

payment. In bankruptcy, they share only in the residual interest of the issuer

after all obligations have been paid out to creditors. However, equity

generally entitles the holder to a pro rata portion of control of the company,

meaning that a holder of a majority of the equity is usually entitled to control

the issuer. Equity also enjoys the right to profits and capital gain, whereas

holders of debt securities receive only interest and repayment of principa

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 56/104

regardless of how well the issuer performs financially. Furthermore, deb

securities do not have voting rights outside of bankruptcy. In other words

equity holders are entitled to the "upside" of the business and to control the

business

• Stock

Hybrid

Hybrid securities combine some of the characteristics of both debt and equity

securities.

Preference shares form an intermediate class of security between equities

and debt. If the issuer is liquidated, they carry the right to receive interest

and/or a return of capital in priority to ordinary shareholders. However, from a

legal perspective, they are capital stock and therefore may entitle holders to

some degree of control depending on whether they contain voting rights.

Convertibles are bonds or preferred stock which can be converted, at the

election of the holder of the convertibles, into the common stock of the issuing

company. The convertibility, however, may be forced if the convertible is a

callable bond, and the issuer calls the bond. The bondholder has about 1 month

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 57/104

to convert it, or the company will call the bond by giving the holder the call

price, which may be less than the value of the converted stock. This is referred

to as a forced conversion.

Equity warrants are options issued by the company that allow the holder of

the warrant to purchase a specific number of shares at a specified price within a

specified time. They are often issued together with bonds or existing equities

and are, sometimes, detachable from them and separately tradable. When the

holder of the warrant exercises it, he pays the money directly to the company,

and the company issues new shares to the holder.

Warrants, like other convertible securities, increases the number of shares

outstanding, and are always accounted for in financial reports as fully diluted

earnings per share, which assumes that all warrants and convertibles will beexercised.

The securities markets

Primary and secondary market

In the U.S., the public securities markets can be divided into primary and

secondary markets. The distinguishing difference between the two markets is

that in the primary market, the money for the securities is received by the

issuer of those securities from investors, typically in an initial public offering

transaction, whereas in the secondary market, the securities are simply assets

held by one investor selling them to another investor (money goes from one

investor to the other). An initial public offering is when a company issues public

stock newly to investors, called an "IPO" for short. A company can later issue

more new shares, or issue shares that have been previously registered in a

shelf registration. These later new issues are also sold in the primary market

but they are not considered to be an IPO but are often called a "secondary

offering". Issuers usually retain investment banks to assist them in

administering the IPO, obtaining SEC (or other regulatory body) approval of the

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 58/104

offering filing, and selling the new issue. When the investment bank buys the

entire new issue from the issuer at a discount to resell it at a markup, it is called

a firm commitment underwriting. However, if the investment bank considers the

risk too great for an underwriting, it may only assent to a best effort agreement

where the investment bank will simply do its best to sell the new issue.

In order for the primary market to thrive, there must be a secondary market, or

aftermarket which provides liquidity for the investment security, where holders

of securities can sell them to other investors for cash. Otherwise, few people

would purchase primary issues, and, thus, companies and governments would

be restricted in raising equity capital (money) for their operations. Organized

exchanges constitute the main secondary markets. Many smaller issues and

most debt securities trade in the decentralized, dealer-based over-the-counter

markets.

Public offer and private placement

In the primary markets, securities may be offered to the public in a public offer

Alternatively, they may be offered privately to a limited number of qualified

persons in a private placement. Sometimes a combination of the two is used

The distinction between the two is important to securities regulation and

company law. Privately placed securities are not publicly tradable and may only

be bought and sold by sophisticated qualified investors. As a result, the

secondary market is not nearly as liquid as it is for public (registered) securities.

Another category, sovereign debt, is generally sold by auction to a specialized

class of dealers.

Listing and OTC dealing

Securities are often listed in a stock exchange, an organized and officially

recognized market on which securities can be bought and sold. Issuers may

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 59/104

seek listings for their securities in order to attract investors, by ensuring that

there is a liquid and regulated market in which investors will be able to buy and

sell securities.

Growth in informal electronic trading systems has challenged the traditiona

business of stock exchanges. Large volumes of securities are also bought and

sold "over the counter" (OTC). OTC dealing involves buyers and sellers dealing

with each other by telephone or electronically on the basis of prices that are

displayed electronically, usually by commercial information vendors such as

Reuters and Bloomberg.

There are also eurosecurities, which are securities that are issued outside thei

domestic market into more than one jurisdiction. They are generally listed on

the Luxembourg Stock Exchange or admitted to listing in London. The reasonsfor listing eurobonds include regulatory and tax considerations, as well as the

investment restrictions.

Market

London is the centre of the eurosecurities markets. There was a huge rise in the

eurosecurities market in London in the early 1980s. Settlement of trades in

eurosecurities is currently effected through two European computerized

clearing/depositories called Euroclear (in Belgium) and Clearstream (formerly

Cedelbank) in Luxembourg.

The main market for Eurobonds is the EuroMTS, owned by Borsa Italiana and

Euronext. There are ramp up market in Emergent countries, but it is growing

slowly.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 60/104

Physical nature of securities

Certificated securities

Securities that are represented in paper (physical) form are called certificated

securities. They may be bearer or registered .

Bearer securities

Bearer securities are completely negotiable and entitle the holder to the rights

under the security (e.g. to payment if it is a debt security, and voting if it is an

equity security). They are transferred by delivering the instrument from person

to person. In some cases, transfer is by endorsement, or signing the back of the

instrument, and delivery.

Regulatory and fiscal authorities sometimes regard bearer securities negatively

as they may be used to facilitate the evasion of regulatory restrictions and tax

In the United Kingdom, for example, the issue of bearer securities was heavily

restricted firstly by the Exchange Control Act 1947 until 1953. Bearer securities

are very rare in the United States because of the negative tax implications they

may have to the issuer and holder.

Registered securities

In the case of registered securities, certificates bearing the name of the holder

are issued, but these merely represent the securities. A person does not

automatically acquire legal ownership by having possession of the certificate

Instead, the issuer (or its appointed agent) maintains a register in which details

of the holder of the securities are entered and updated as appropriate. A

transfer of registered securities is effected by amending the register.

8/3/2019 Portfolio Management Relince

http://slidepdf.com/reader/full/portfolio-management-relince 61/104

Non-certificated securities and global certificates

Modern practice has developed to eliminate both the need for certificates and

maintenance of a complete security register by the issuer. There are two

general ways this has been accomplished.

Non-certificated securities

In some jurisdictions, such as France, it is possible for issuers of that jurisdiction

to maintain a legal record of their securities electronically.

In the United States, the current "official" version of Article 8 of the Uniform

Commercial Code permits non-certificated securities. However, the "official"

UCC is a mere draft that must be enacted individually by each of the U.S